pwc ifrs internal audit considerations312

TRANSCRIPT

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 1/42

IFRS - Internal Audit Considerations

Presenters:

Duaine Smith/Saad Bounjoua – PricewaterhouseCoopers

!IIA"s #$th Annual Audit Seminar

%arch &'( &'')

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 2/42

Slide & PricewaterhouseCoopers

*his session"s o+jecti,es

i.h le,el o,er,iew o the ollowin.0

12 3hat is IFRS4

&2 Conte5t and mar6et trends

#2 7e8 dierences +etween IFRS and 9S AAP;2 *he case or con,ersion

<2 Potential role or Internal Audit

$2 IFRS implementation – Challen.es and =essons =earned

>2 7e8 %essa.es

?2 @ A

+jecti,es

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 3/42

3hat is IFRS4

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 4/42

Slide ; PricewaterhouseCoopers

3here is all o this .oin.4

*he ultimate .oal( we +elie,e( is a common( hi.h-Eualit8 .lo+al inancial

reportin. s8stem that can +e used or decision-ma6in. purposes across the

capital mar6ets o the world2

*hus( we +elie,e that plannin. or a transition o 92S2 pu+lic companies to an

impro,ed ,ersion o IFRS would +e a lo.ical wa8 orward to achie,in. the .oal

o a set o common .lo+al standards2

3h8 is IFRS .oin. on4

-Ro+ert erG( Chairman o the Financial Accountin. Standards Board

cto+er &;( &''>( Senate earin. on lo+al Reportin. Standards

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 5/42

Slide < PricewaterhouseCoopers

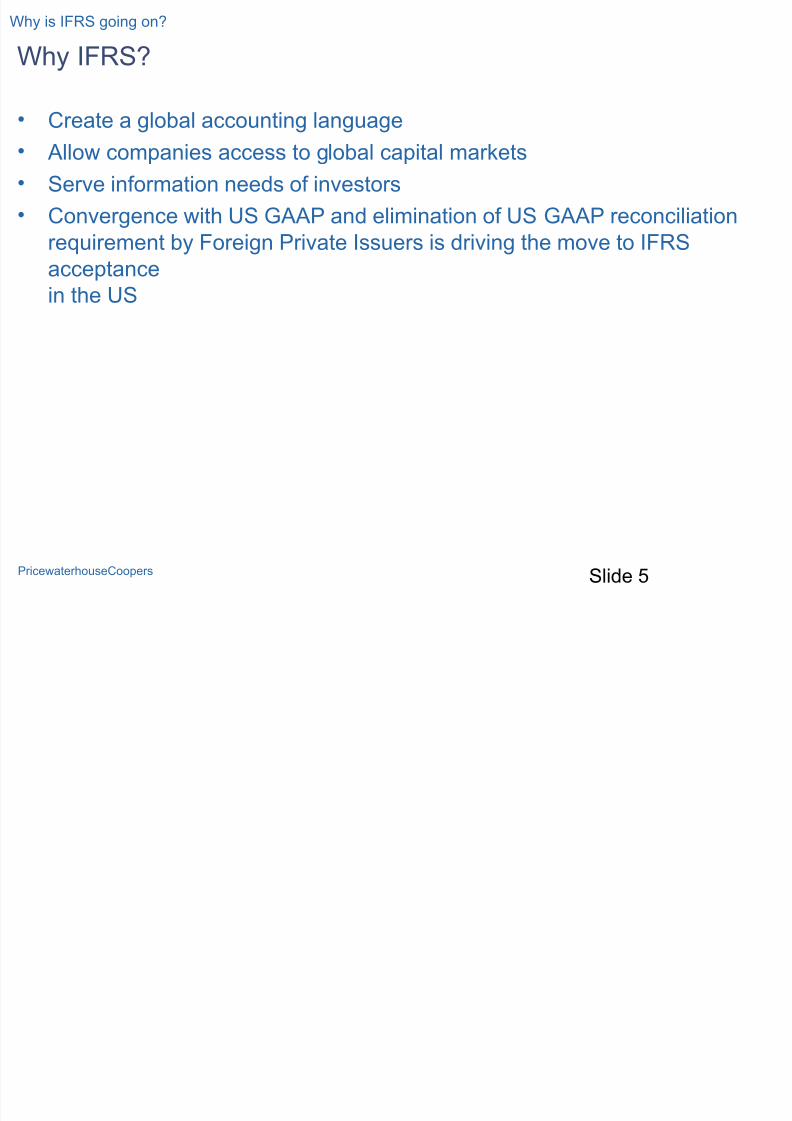

3h8 IFRS4

H Create a .lo+al accountin. lan.ua.e

H Allow companies access to .lo+al capital mar6ets

H Ser,e inormation needs o in,estors

H Con,er.ence with 9S AAP and elimination o 9S AAP reconciliation

reEuirement +8 Forei.n Pri,ate Issuers is dri,in. the mo,e to IFRS

acceptancein the 9S

3h8 is IFRS .oin. on4

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 6/42

Conte5t and mar6et trends

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 7/42Slide > PricewaterhouseCoopers

*he world has chosen IFRS

%ore than 1'' countries reEuire or permit the use o IFRS( or are con,ertin.

*op 1' lo+al Capital %ar6ets

9S 9S AAP

apan Con,er.in. to IFRS

97 IFRS

France IFRS

Canada Con,ertin. to IFRS

erman8 IFRS

on. 7on. IFRS

Spain IFRS

SwitGerland IFRS or 9S AAP

Australia IFRS

Conte5t and mar6et trends

Countries see6in. con,er.ence with the IASB or pursuin. adoption o IFRSs

Countries that reEuire or permit IFRSs

Countries with no current plans to con,ert to IFRS

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 8/42Slide ? PricewaterhouseCoopers

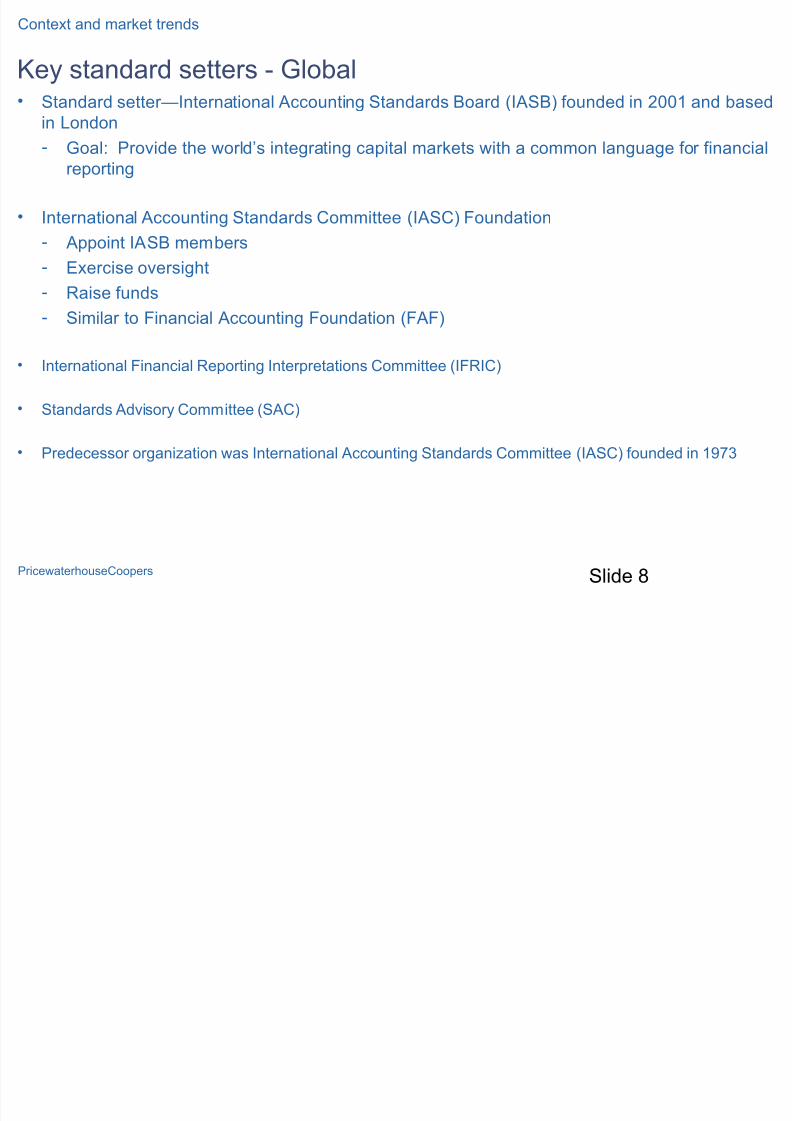

7e8 standard setters - lo+alH Standard setterJInternational Accountin. Standards Board KIASBL ounded in &''1 and +ased

in =ondon

- oal: Pro,ide the world"s inte.ratin. capital mar6ets with a common lan.ua.e or inancial

reportin.

H International Accountin. Standards Committee KIASCL Foundation

- Appoint IASB mem+ers

-M5ercise o,ersi.ht

- Raise unds

- Similar to Financial Accountin. Foundation KFAFL

H International Financial Reportin. Interpretations Committee KIFRICL

H Standards Ad,isor8 Committee KSACL

H Predecessor or.aniGation was International Accountin. Standards Committee KIASCL ounded in 1)>#

Conte5t and mar6et trends

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 9/42Slide ) PricewaterhouseCoopers

7e8 standard setters - ational

SMC – Securities and M5chan.e CommissionH Protect in,estors( maintain air( orderl8( and eicient mar6ets( and acilitate

capital ormation

FASB – Financial Accountin. Standards Board

H Desi.nated or.aniGation in the pri,ate sector or esta+lishin. standards oinancial reports

H iciall8 reco.niGed as authoritati,e +8 the Securities and M5chan.e

Commission and the American Institute o Certiied Pu+lic Accountants

MC – Muropean Commission

Conte5t and mar6et trends

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 10/42Slide 1' PricewaterhouseCoopers

Catal8sts o the 9S transormation

H Creation o IASB in &''1

H cto+er &''& orwal6 A.reement

H Con,er.ence was the pathwa8 to create one .lo+al set o hi.h-Eualit8 standards which are

ro+ust and transparent

H April &''< SMC roadmap – .oal to eliminate reconciliation

H Reports on competiti,eness o the 9S capital mar6ets

H SMC roundta+le discussions in %arch and Decem+er &''>

H Focus on simplicit8 in 9S inancial reportin.

H %arch &''? SMC accepts IFRS rom Forei.n Pri,ate Issuers without reconciliation

H Au.ust &''? SMC proposed roadmap o mandator8 adoption o IFRS +e.innin. in &'1; +8

issuers in the 9S

H Au.ust &''? SMC proposed to allow the optional use o IFRS +8 certain Euali8in. domestic

issuers

H o,em+er &''? SMC pu+lished or pu+lic comment a proposal( titled Roadmap or the Potential

9se o Financial Statements Prepared in accordance with International Financial Reportin.

Standards +8 9S Issuers

Conte5t and mar6et trends

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 11/42Slide 11 PricewaterhouseCoopers

M5pected timeline or 9S transition

Conte5t and mar6et trends

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 12/42Slide 1& PricewaterhouseCoopers

Is there a case or IFRS in the 9S4

Hlo+aliGation will dri,e a chan.e to IFRS in the 9S

H Domestic re.istrants should ha,e the same option as FPIs

H 9ltimatel8 the 9S mar6ets should ha,e onl8 one AAP

H *ransitionin. to IFRS will +e at a cost( +ut it will +e worthwhile

- Mnhance eicienc8 o capital allocation

- Cost sa,in.s or harmoniGed .lo+al reportin. s8stems

- Competiti,eness o the 9S capital mar6ets

- Simplicit8 in inancial reportin.

- Mlimination o the 9S AAP reconciliation or non-9S re.istrants

- Return to a more purel8( principles-+ased ramewor6 in the 9S

Conte5t and mar6et trends

The earlier a company plans strategically for this transition, the better

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 13/42Slide 1# PricewaterhouseCoopers

Beneits and irst-mo,er ad,anta.es

*he case or con,ersion

IFRS:

9niorm

lo+al

Accountin.

=an.ua.e

Reduced cost o

inancial reportin. or

.lo+al companies

Industr8 perception

o mar6et leadership

Suicient time to

adeEuatel8 de+ate

strate.ic irst time

adoption – in

particular with loo6

+ac6 pro,ision

Streamlined

%A acti,it8

%ore eecti,e

procurement with

,endors and

customers reportin.

under IFRS

Impro,ed

transparenc8 and

compara+ilit8

or in,estors and

ratin. a.encies

%ore eicient

access to capital or

.lo+al corporations

A+ilit8 to anal8Geimpact on

ta5-related issues

A+ilit8 to understand

interaction with

strate.ic initiati,es

to .enerate ,alue

rom s8ner.ies

A+ilit8 to secure

scarce IFRS

6nowled.e resources

and optimiGe human

capital deplo8ment

decisions

%ore room or

mana.ement"s

jud.ment and truer

relection o

economic realit8 with

principles-+asedAAP

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 14/42

7e8 dierences +etween IFRS and 9S AAP

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 15/42Slide 1< PricewaterhouseCoopers

%ajor dierences +etween IFRS and 9S AAP

Principles ,s2 rules

H Both ramewor6s +uilt under principles-+ased methodolo.8

H owe,er( 9S AAP is more prescripti,e and rules-+ased addressin.

speciic industries and t8pes o transactions in man8 areas

H &(<'' pa.es ,s2 &<(''' pa.es

H Simple ,s2 comple5

Fair ,alue accountin.

H reater use o FN under IFRS than 9S AAP Ke2.2( re,aluations o PPM(In,estment Propert8 and Intan.i+lesL

7e8 dierences +etween IFRS and 9S AAP

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 16/42Slide 1$

PricewaterhouseCoopers

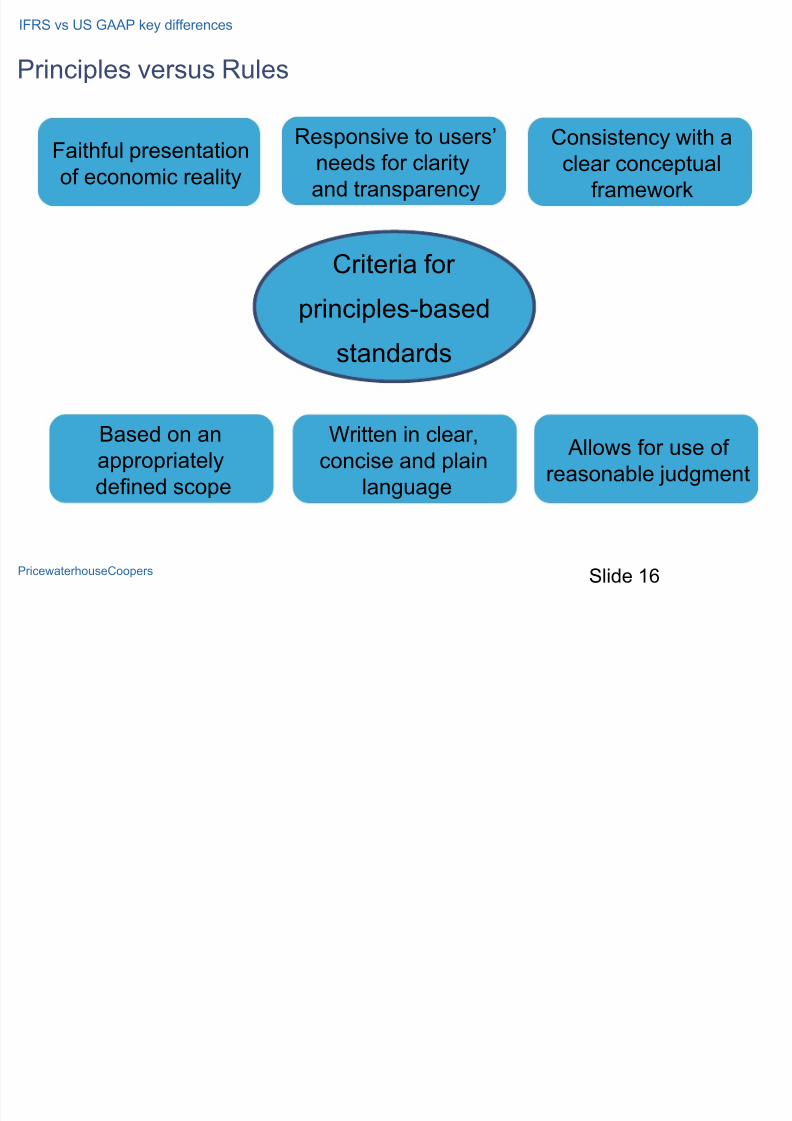

Principles ,ersus Rules

Criteria or principles-+ased

standards

Faithul presentation

o economic realit8

Responsi,e to users"needs or clarit8

and transparenc8

Consistenc8 with aclear conceptual

ramewor6

Based on an

appropriatel8

deined scope

3ritten in clear(

concise and plain

lan.ua.e

Allows or use o

reasona+le jud.ment

IFRS ,s 9S AAP 6e8 dierences

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 17/42Slide 1>

PricewaterhouseCoopers

7e8 dierences +etween IFRS and 9S AAP

7e8 dierences +etween IFRS and 9S AAP

Business

Com+inations*a5 accountin.

Reco.nition andmeasurement o

pro,isions

Deri,ati,es and

hed.e accountin.

Consolidation o

entities

Impairment testin.

methods

CapitaliGation o

RD

Asset retirement

o+li.ations

SecuritiGations /

Dereco.nition

Re,enue

reco.nition

%easurement o

in,entories

Classiication and

measurement o

inancial

instruments

AccrualsDe+t and eEuit8

classiication

Mmplo8ee stoc6

compensation=IF

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 18/42Slide 1?

PricewaterhouseCoopers

*his inormation is deri,ed rom Form &'-F

IFRS ,s2 9S AAP um+er o

Mntit8 et

income MEuit8reconcilin.

items 7e8 dierences

BASF -;O &O $ Pensions AcEuisitions Deerred ta5es

A6Go o+el -1#O >#O 1$ Income ta5es Deri,ati,es Pensions and PMB

S8n.enta -&1O -11O 1# Purchase accountin. rant o put option Pensions and PMB

Rhodia ->$O 1)O ? PensionsCumulati,e translationadjustment

CapitaliGed de,elopmentcosts

Sinopec 1On/a &Depreciation on re,aluedPPM CapitaliGed interest n/a

Sanoi-A,entis 1O 1O ? Application o IFRS1 Business com+ination Restructurin.

Mni )O -;O 1'Successul eortsaccountin. In,entor8 ,aluation ain o sale o +usiness

Ro8al Dutch Shell -#O -$O ? Retirement +eneitsCurrenc8 translationdierences Re,ersals o impairments

*otal SA -#O >?O 1' AcEuisition Financial instruments

*a5 eect o intercompan8

transers

IFRS ,s2 9S AAP dierences +enchmar6in. inormation

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 19/42

*he case or con,ersion

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 20/42Slide &'

PricewaterhouseCoopers

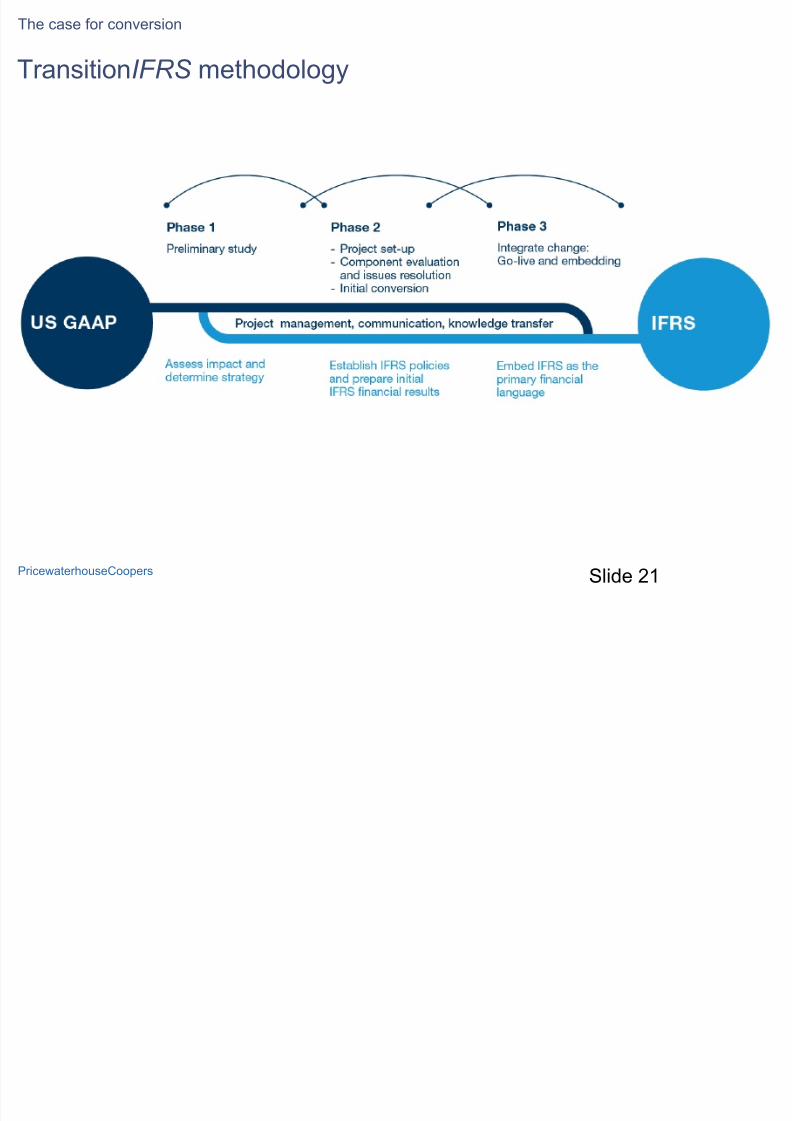

Transition IFRS con,ersion methodolo.8

H De,eloped and reined o,er 1' 8ears o successul con,ersions in Murope(

Asia and the 9S

H Implemented +8 a +road networ6 o e5perienced con,ersion specialists2

H Considers the +roader impact on the +usiness - accountin. policies( people(

inancial reportin.( ta5 and other +usiness processes and s8stems(sta6eholder mana.ement( statutor8 reportin. and communications

H 9sed +8 more than 1(#'' companies

H Scala+le and responsi,e to the uniEue comple5ities o each client"s +usiness

H Msta+lishes clear o+jecti,es with the client in the plannin. sta.e

H Applies a phased approach to IFRS con,ersions

H Is a ramewor6 that is supplemented +8 deep +usiness process and

technical accountin. and s8stems s6ills2

*he case or con,ersion

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 21/42Slide &1

PricewaterhouseCoopers

*ransitionIFRS methodolo.8

*he case or con,ersion

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 22/42

Slide && PricewaterhouseCoopers

3hat does a con,ersion impact

Chan.in. People

Ka new +usiness lan.ua.eL

H Communication

- Internal

- M5ternal

H *rainin.:

- At dierent le,els

- ot onl8 Finance people

Chan.in. um+ers

Addition o another AAP and/or chan.e in primar8 AAP - Accountin. policies determination0 Chart o Accounts re,iew( penin.

Balance Sheet(2

Chan.in. Processes

H M5istin. processes to +e enhanced:

- ot adeEuate with ,olume

- As alternati,e to s8stem chan.e

H ew processes created

H Bud.etin. orecastin.

H Internal controls re,isited

Chan.in. S8stems

H Data a,aila+ilit8 and s8stem

reEuirements

H ew s8stems components: data

warehouse( calculation en.ine

H Re-ali.nment o mana.ementinormation s8stems

H %ulti-AAP solutions

H Primar8 AAP chan.eo,er

Chan.in. Business

H Perormance mana.ement to +e em+edded across :

- Perormance measure/7PIs

- %ana.ement accounts

- Remunerations/+onuses

- Bud.etin./orecastin.

- Financial and Business impact anal8sis: de+t co,enants

- Dierent ,aluations

*he case or con,ersion

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 23/42

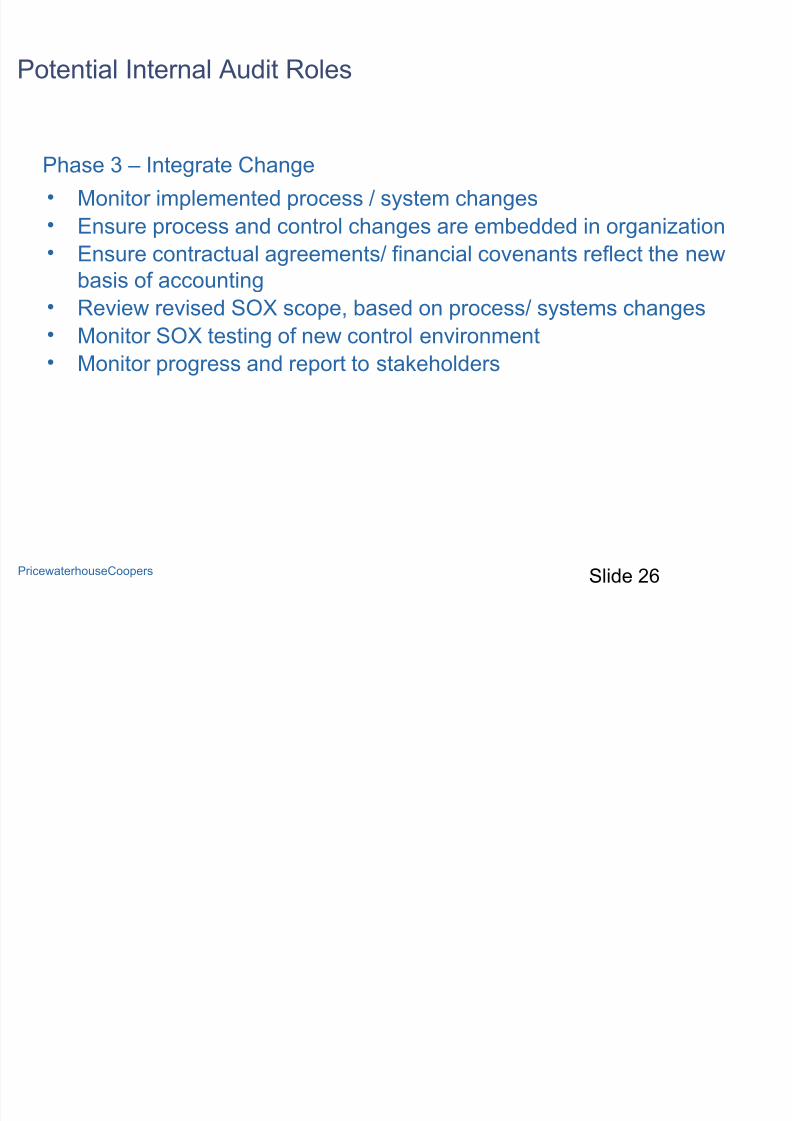

Potential Internal Audit Roles

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 24/42

Slide &; PricewaterhouseCoopers

Potential Internal Audit Roles

ow – Beore the process +e.ins( ser,e as a resource or

H Board / Audit CommitteeH Finance Sta

H Business 9nit Personnel

Phase 1 – Preliminar8 Stud8

H Assist in plannin. / Scopin. the projectH Mnsure all aspects Kpeople( processes( s8stems( operationsL are

addressed

H Re,iew dia.nostic Euestionnaires / summaries prepared

H Mnsure all si.niicant constituencies participate in the process

H %onitor pro.ressH Participate in report to the Board / Audit Committee /

Sta6eholders

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 25/42

Slide &< PricewaterhouseCoopers

Potential Internal Audit Roles

Phase & – Project Set 9p0 Component M,aluations and Issue Resolution0Initial Con,ersion

H Re,iew project .o,ernance structure / related responsi+ilities

H %onitor completion o detailed component e,aluation

H Re,iew mana.ement assessment o alternati,e policies / issue

e,aluation processH %onitor plan or trainin./ 6nowled.e transer

H Re,iew prioritiGed plan or process / s8stem chan.es

H %onitor plan or dual reportin. periods

H Re,iew controls o,er initial IFRS con,ersion

H %onitor pro.ress and report to sta6eholders

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 26/42

Slide &$ PricewaterhouseCoopers

Potential Internal Audit Roles

Phase # – Inte.rate Chan.e

H %onitor implemented process / s8stem chan.es

H Mnsure process and control chan.es are em+edded in or.aniGation

H Mnsure contractual a.reements/ inancial co,enants relect the new

+asis o accountin.H Re,iew re,ised S scope( +ased on process/ s8stems chan.es

H %onitor S testin. o new control en,ironment

H %onitor pro.ress and report to sta6eholders

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 27/42

IFRS Implementation – Challen.es and =essons =earned

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 28/42

Slide &? PricewaterhouseCoopers

7e8 Challen.es in an IFRS Implementation

H 9nderestimation o time reEuired

- Project mana.ement essential

H ot enou.h ocus on correlati,e eects

- In,estor relations and mar6et communications

- Contracts and a.reements

- *a5 related issues

- Bonus and compensation plans

- Mects on I* s8stems

H =ost opportunities

- *oo man8 wor6arounds- I* not used as eecti,el8 as it could ha,e +een

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 29/42

Slide &) PricewaterhouseCoopers

7e8 Challen.es in an IFRS Implementation

H Ineiciencies

- ot enou.h coordination +etween the parent and su+sidiaries

- =ac6 o 6nowled.e transer

H Increased ris6 o,er inancial reportin.

- eed or topside entries

- Mnsurin. process and controls relect the chan.ed accountin.

standards and lan.ua.e

H Focus on reco.nition and measurement

- 3hat will the accounts actuall8 loo6 li6e- Mducation around depth and e5tent o new disclosures

*h i

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 30/42

PricewaterhouseCoopers

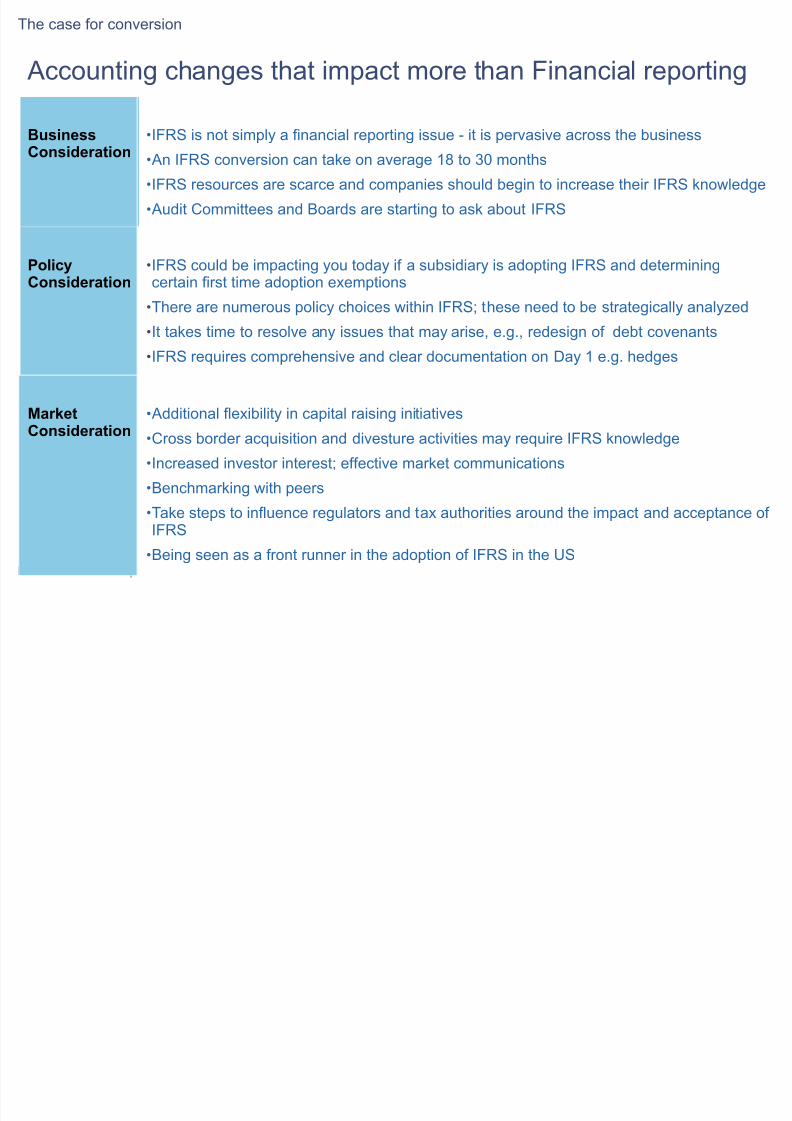

Accountin. chan.es that impact more than Financial reportin.

• Suppliers

• HR

• IT

• AcquisitionIntegration

*he case or con,ersion

BusinessConsiderationHIFRS is not simpl8 a inancial reportin. issue - it is per,asi,e across the +usiness

H An IFRS con,ersion can ta6e on a,era.e 1? to #' months

HIFRS resources are scarce and companies should +e.in to increase their IFRS 6nowled.e

H Audit Committees and Boards are startin. to as6 a+out IFRS

Policy

Consideration

HIFRS could +e impactin. 8ou toda8 i a su+sidiar8 is adoptin. IFRS and determinin.

certain irst time adoption e5emptions

H*here are numerous polic8 choices within IFRS0 these need to +e strate.icall8 anal8Ged

HIt ta6es time to resol,e an8 issues that ma8 arise( e2.2( redesi.n o de+t co,enants

HIFRS reEuires comprehensi,e and clear documentation on Da8 1 e2.2 hed.es

MarketConsideration H Additional le5i+ilit8 in capital raisin. initiati,esHCross +order acEuisition and di,esture acti,ities ma8 reEuire IFRS 6nowled.e

HIncreased in,estor interest0 eecti,e mar6et communications

HBenchmar6in. with peers

H*a6e steps to inluence re.ulators and ta5 authorities around the impact and acceptance oIFRS

HBein. seen as a ront runner in the adoption o IFRS in the 9S

*he case or con,ersion

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 31/42

Slide #1 PricewaterhouseCoopers

Financial reportin. process considerations

H pportune time to address an8 issues or enhance inancial reportin. processes

H Potential or reduced cost o compliance- CentraliGed IFRS policies and shared ser,ices department can +e de,eloped

and used +8 all in the roup

- Potential to reduce the num+er o reported AAPs and costl8 con,ersion eorts

Kcon,er.e the statutor8 reportin.L

H 3hat is the most eicient method to incorporate multiple AAPs in the inancial

reportin. processes and s8stems

H S8ner.ies with other +usiness initiati,es and the opportunit8 to +uild IFRS reportin.

capa+ilit8

H Consistent policies amon. the .roup can help impro,e Eualit80 one ,ersion o the

truth

H Mnsure that the IFRS policies ha,e adeEuate processes and controls KSar+o5L

*he case or con,ersion

*he case or con,ersion

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 32/42

Slide #& PricewaterhouseCoopers

Financial reportin. challen.es

H Companies enhancin. standardiGation Kchallen.e and +eneitL

H Application o jud.ment within a principles-+ased AAP IFRS ,ersus rules-+ased 9S AAP

H Polic8 settin. diicult +ecause IFRS pro,ides options

H Findin. man8 more dierences than initiall8 e5pected

H 9S AAP reportin. oten done usin. .lo+al materialit8

H =ocal IFRS reportin. done usin. local materialit8

H Data .aps resultin. rom si.niicantl8 increased disclosures

*he case or con,ersion

*he case or con,ersion

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 33/42

Slide ## PricewaterhouseCoopers

Financial reportin. challen.es KcontinuedL

H %ulti-AAP reportin. Ks8stems capa+ilit8( man8 dierent reportin. s8stems and

processes within the reportin. unitsL

H %an8 hand-os are reEuired to prepare consolidated inancial results KA lac6 o

automation in the transer o inancial inormationL

H Dierent sets o data and process lows are used to support statutor8( re.ulator8

and mana.ement reportin. reEuirements

- A lac6 o standard processes and s8stems in the recordin. and consolidation oinancial inormation across the roup

- Nar8in. le,els o ownership o the consolidation processes at peratin.

Compan8 le,el

*he case or con,ersion

*he case or con,ersion

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 34/42

Slide #; PricewaterhouseCoopers

ther or.aniGational aspects

H Si.niicant eort to inte.rate a new accountin.

lan.ua.e throu.hout an or.aniGation

H umerous tactical wor6arounds ,ersus

strate.ic i5es

H It ta6es time or companies to .et comorta+le

with the new principles

- %aintain pre,ious AAP or a period o time- on-IFRS measures still widel8 used to

communicate perormance

- =e,el o transparenc8 ,aried

- ew perormance standards Ke2.2 jo+

descriptions( hirin. practicesL

- Communication needs across or.aniGation

- =ocal re.ulator8 reportin. reEuirements

As several multinational Fortune

5 companies have already

discovered, transition!related

changes have the potential to

deliver future dividends, such asstreamlined operations and

reduced costs" #ith this outlook,

companies can approach their

conversion efforts strategically

$e"g", overhaul an infle%ible

information technology system or

rethink accounting choices&, not 'ust treat them as a compliance

e%ercise

Two birds, one stone

*he case or con,ersion

Dri,in. ,alue throu.h an IFRS con,ersion

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 35/42

Slide #< PricewaterhouseCoopers

IFRS – =essons learned rom 1'' countries

H Msta+lish a clear ,ision and plan at the start

H Msta+lish the tone at the top and set up the ri.ht .o,ernance structure and clear

decision-ma6in. powers2

H Plan and e5ecute appropriatel8 considerin. impacts across the +usiness2

H Don"t outsource the con,ersion process – .row 8our own resources2

H De,elop a con,ersion plan that ta6es into account pea6s and ,alle8s o acti,it8

Ke2.2 Euarterl8 reportin.L2

H Consider how IFRS will impact 7PIs and 8our internal and e5ternal

communication strate.82

H *a6e steps earl8 to communicate with and inluence re.ulators( ta5 authorities and other sta6eholders around the

impact and acceptance o IFRS2

H Become 6nowled.ea+le with the standard-settin. process( as IFRS will continue to e,ol,e durin.

implementation2

H %a6e the most o opportunities or other project eiciencies Ke2.2 aster close processL2

H Consider opportunities or reportin. rationaliGation/streamlinin. Ke2.2 multi-AAP reportin.( ta5 +alancesL2H Implement at the +usiness unit le,el usin. a top-down and +ottom-up approach( with +usiness units in,ol,ed

earlier rather than later( as the impact can +e proound2

Dri,in. ,alue throu.h an IFRS con,ersion

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 36/42

7e8 %essa.es

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 37/42

Slide #> PricewaterhouseCoopers

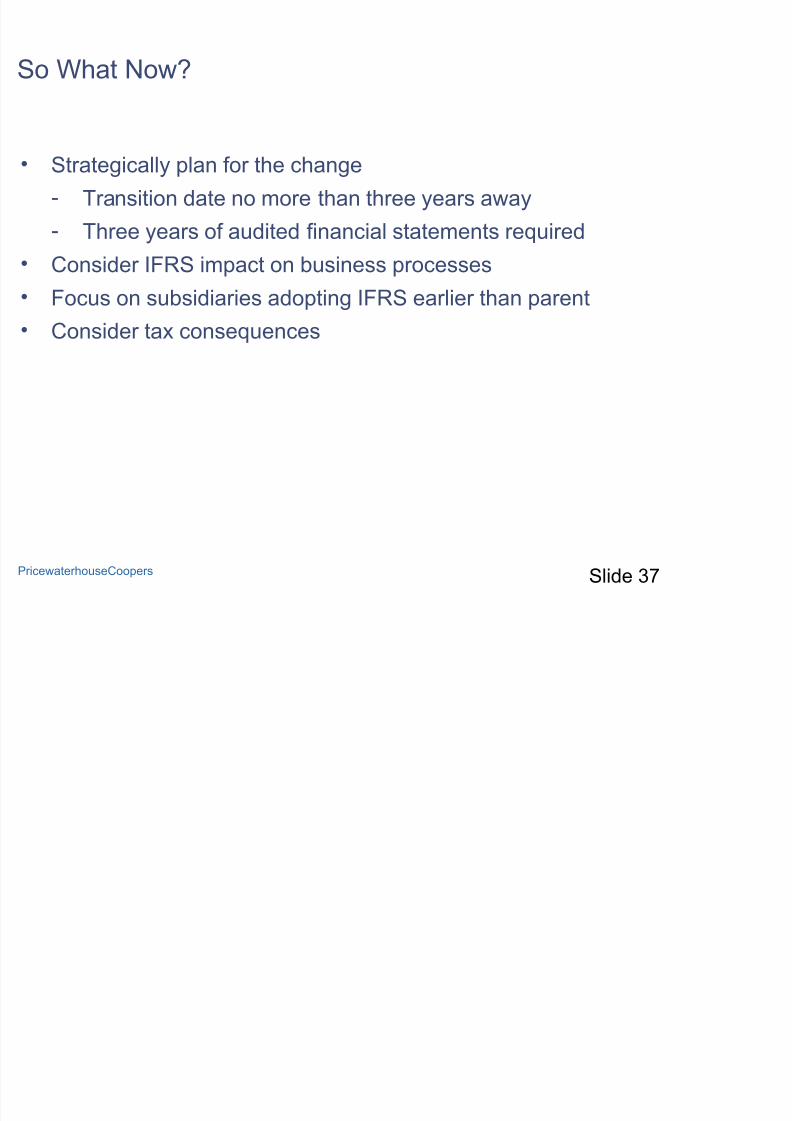

So 3hat ow4

H Strate.icall8 plan or the chan.e

- *ransition date no more than three 8ears awa8

- *hree 8ears o audited inancial statements reEuired

H Consider IFRS impact on +usiness processes

H Focus on su+sidiaries adoptin. IFRS earlier than parent

H Consider ta5 conseEuences

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 38/42

Slide #? PricewaterhouseCoopers

*ime to act is now

H *he SMC outlined its roadmap to con,er.ence in Au.ust &''?

H Sta6eholders will +e as6in. Euestions

H *here are si.niicant dierences +etween 9S AAP and IFRS

H Beneit o a realistic timeline( without the pressure o mandator8 adoptiondeadlines

H IFRS resources are scarce

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 39/42

Slide #) PricewaterhouseCoopers

Remem+er the 6e8 messa.es

H IFRS – *he world"s AAP

H *here are si.niicant dierences +etween 9S AAP and IFRS

H A +usiness transormation( not just de+its/credits

H *here are si.niicant dierences +etween 9S AAP and IFRS

H 7e8 challen.es in an IFRS Implementation

H *he potential Roles or Internal Audit in an IFRS Implementation

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 40/42

Slide ;' PricewaterhouseCoopers

Final message( #hen you )ake up tomorro)*""

H 7eep a+reast o the SMC"s actions concernin. IFRS0

H Mn.a.e in the de+ate on the IASB"s Kand FASB"sL a.enda0

H Add IFRS talent to 8our or.aniGation0

H Do 8our own anal8sis o the costs and +eneits o

transition2

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 41/42

Slide ;1 PricewaterhouseCoopers

Contact +nformation

Duaine Smith 1 $;$ ;>1 ;;;'

duaine2smithQus2pwc2com

Saad Bounjoua 1 $;$ ;>1 1'??saad2+ounjouaQus2pwc2com

8/9/2019 Pwc Ifrs Internal Audit Considerations312

http://slidepdf.com/reader/full/pwc-ifrs-internal-audit-considerations312 42/42

&''? PricewaterhouseCoopers2 All ri.hts reser,ed2 PricewaterhouseCoopers reers to PricewaterhouseCoopers