q1 2014 ir presentation

DESCRIPTION

ÂTRANSCRIPT

May 2014

Q1 2014 Investors Presentation

FINANCIAL & BUSINESS RESULTS

This document does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire securities of AFI Development Plc (the "Company") or any of its subsidiaries in any jurisdiction or an inducement to enter into investment activity. No part of this document, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions contained herein. None of the Company or any of its affiliates, advisors or representatives shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with the document.

This communication is only being distributed to and is only directed at (1) qualified institutional buyers (within the meaning of Rule 144A of the United States Securities Act of 1933, as amended (the "Securities Act") or (2) accredited investors (as defined in Rule 501(a) of Regulation D adopted pursuant to the Securities Act). Any person who is not a "qualified institutional buyer" or "accredited investor" should not act or rely on this document or any of its contents.

This document contains "forward-looking statements", which include all statements other than statements of historical facts, including, without limitation, any statements preceded by, followed by or that include the words "targets", "believes", "expects", "aims", "intends", "will", "may", "anticipates", "would", "could" or similar expressions or the negative thereof. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond the Company's control that could cause the actual results, performance or achievements of the Company to be materially different from future results, performance or achievements expressed or implied by such forward-looking, including, among others, the achievement of anticipated levels of profitability, growth, cost and synergy of recent acquisitions, the impact of competitive pricing, the ability to obtain necessary regulatory approvals and licenses, the impact of developments in the Russian economic, political and legal environment, volatility in stock markets or in the price of our shares or GDRs, financial risk management and the impact of general business and global economic conditions.

Such forward-looking statements are based on numerous assumptions regarding the Company's present and future business strategies and the environment in which the Company will operate in the future. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. These forward-looking statements speak only as at the date as of which they are made, and the Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company's expectations with regard thereto or any change in events, conditions or circumstances on which any such statements are based.

Neither the Company, nor any of its agents, employees or advisors intends or has any duty or obligation to supplement, amend, update or revise any of the forward-looking statements contained in this document.

The information contained in this document is provided as at the date of this document and is subject to change without notice.

Disclaimer

2

SECTION 1

Company Overview

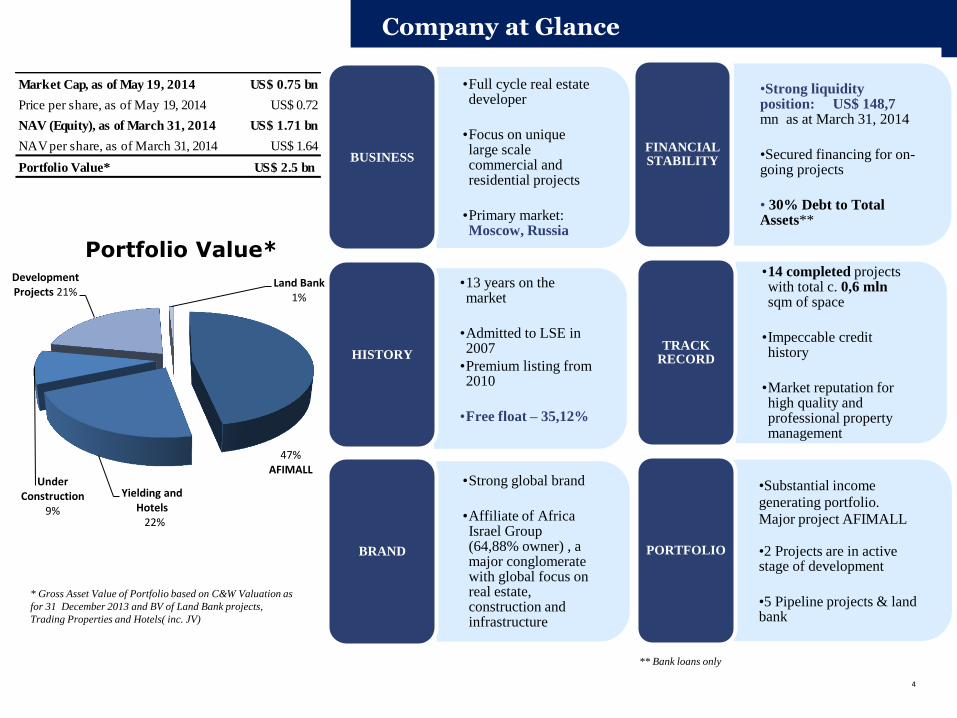

Company at Glance

4

•Full cycle real estate developer

•Focus on unique large scale commercial and residential projects

•Primary market: Moscow, Russia

BUSINESS

•13 years on the market

•Admitted to LSE in 2007

•Premium listing from 2010

•Free float – 35,12%

HISTORY

•Strong global brand

•Affiliate of Africa Israel Group (64,88% owner) , a major conglomerate with global focus on real estate, construction and infrastructure

BRAND

•Strong liquidity position: US$ 148,7 mn as at March 31, 2014

•Secured financing for on-going projects

• 30% Debt to Total Assets**

FINANCIAL STABILITY

•14 completed projects with total c. 0,6 mln sqm of space

•Impeccable credit history

•Market reputation for high quality and professional property management

TRACK RECORD

•Substantial income

generating portfolio.

Major project AFIMALL

•2 Projects are in active stage of development

•5 Pipeline projects & land bank

PORTFOLIO

47% AFIMALL

Yielding and Hotels 22%

Under Construction

9%

Development Projects 21%

Land Bank 1%

Portfolio Value*

* Gross Asset Value of Portfolio based on C&W Valuation as

for 31 December 2013 and BV of Land Bank projects,

Trading Properties and Hotels( inc. JV)

** Bank loans only

Market Cap, as of May 19, 2014 US$ 0.75 bn

Price per share, as of May 19, 2014 US$ 0.72

NAV (Equity), as of March 31, 2014 US$ 1.71 bn

NAV per share, as of March 31, 2014 US$ 1.64

Portfolio Value* US$ 2.5 bn

Note: the NOI projections are “forward looking statements” based on C&W valuation assumptions and Company estimations and they can be realized or not realized due to factors beyond the Company's control including, among others, the impact of competitive

pricing, the ability to obtain necessary regulatory approvals and licenses, the impact of developments in the Russian economic, political and legal environment, volatility in stock markets or in the price of our shares or GDRs, financial risk management and the

impact of general business and global economic conditions

Key Projects in Moscow

Yielding Assets (retail, offices and hotels)

Ownership:50%

Other

** Odinburg presented with cost value

* Outside of Moscow

Value** ( C&W, Dec, 31 2013):

US$ 1.7 bn

GLA(excl. hotels),sqm: 195K sqm

NOI stab. ( excl. hotels):

US$ 204 mn

Value (BV): US$ 16 mn

5

Projects Under Development

Value** (afid share, C&W):

US$ 760 mn

GLA,sqm: 217,6K sqm

GSA,sqm: c. 588,4K sqm

Land Bank

Active phase of construction

Yielding Assets

Projects under

Development

Completed Assets

Tverskaya IB Riversede Station AFIMALL

PLAZA SPA Kisl* PLAZA SPA ZHEL* Aquamarine III

Aquamarine Hotel Paveletskaya,1 H2O

* * Hotels presented with cost value

Odinburg** Paveletskaya II

Plaza IC Pochtovaya

Plaza iia

Expolon

Plaza IV

SECTION 1

Project Update

Yielding Projects

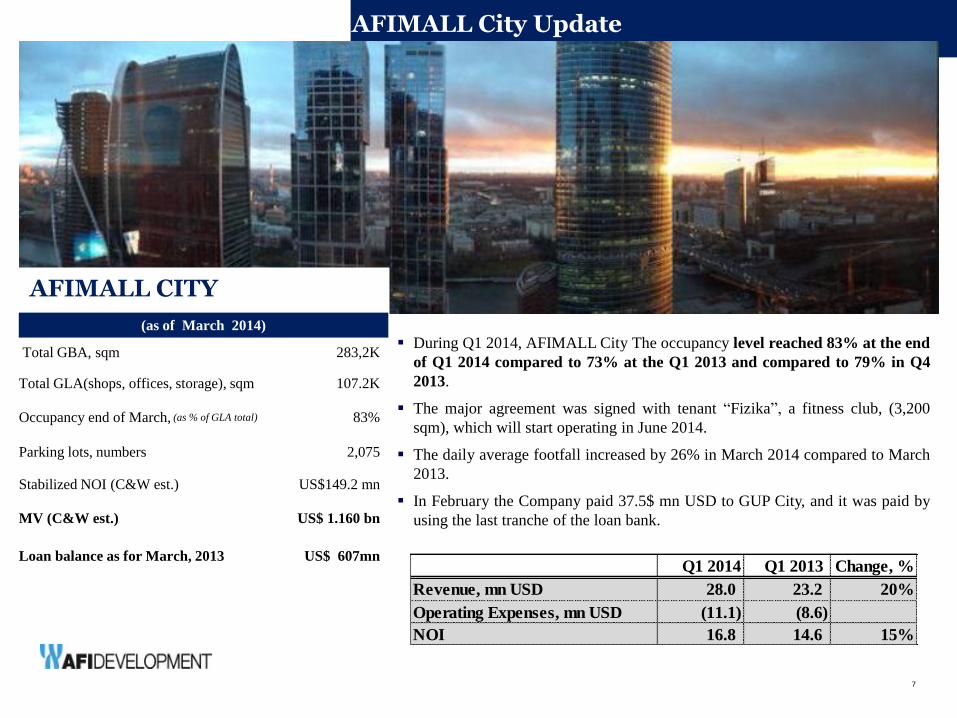

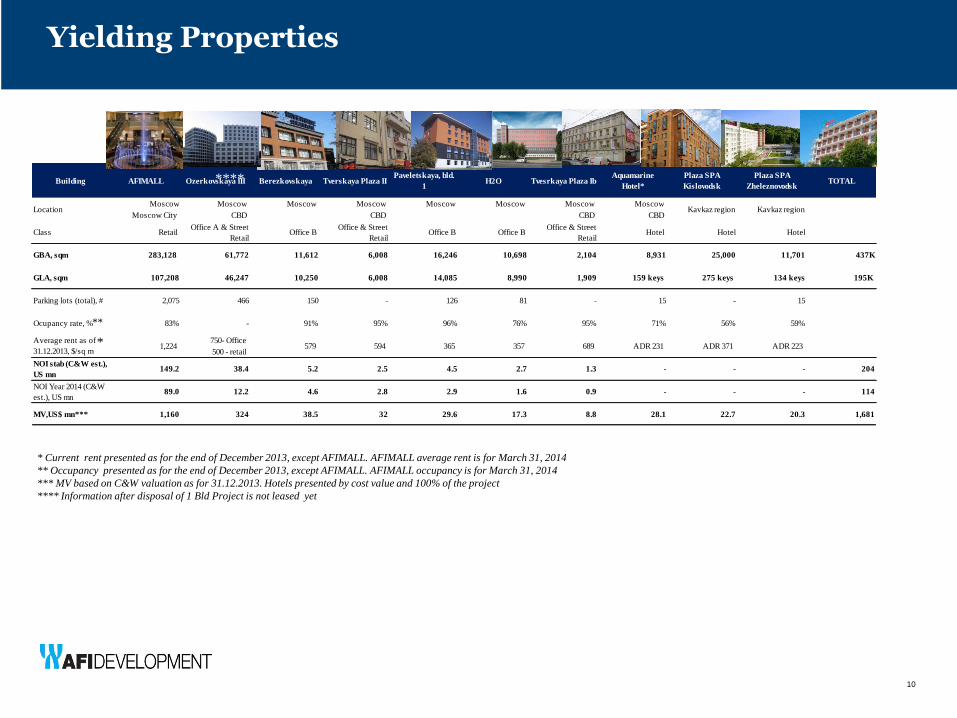

(as of March 2014)

Total GBA, sqm 283,2K

Total GLA(shops, offices, storage), sqm 107.2K

Occupancy end of March, (as % of GLA total) 83%

Parking lots, numbers 2,075

Stabilized NOI (C&W est.) US$149.2 mn

MV (C&W est.) US$ 1.160 bn

Loan balance as for March, 2013 US$ 607mn

AFIMALL CITY

During Q1 2014, AFIMALL City The occupancy level reached 83% at the end

of Q1 2014 compared to 73% at the Q1 2013 and compared to 79% in Q4

2013.

The major agreement was signed with tenant “Fizika”, a fitness club, (3,200

sqm), which will start operating in June 2014.

The daily average footfall increased by 26% in March 2014 compared to March

2013.

In February the Company paid 37.5$ mn USD to GUP City, and it was paid by

using the last tranche of the loan bank.

AFIMALL City Update

7

Q1 2014 Q1 2013 Change, %

Revenue, mn USD 28.0 23.2 20%

Operating Expenses, mn USD (11.1) (8.6)

NOI 16.8 14.6 15%

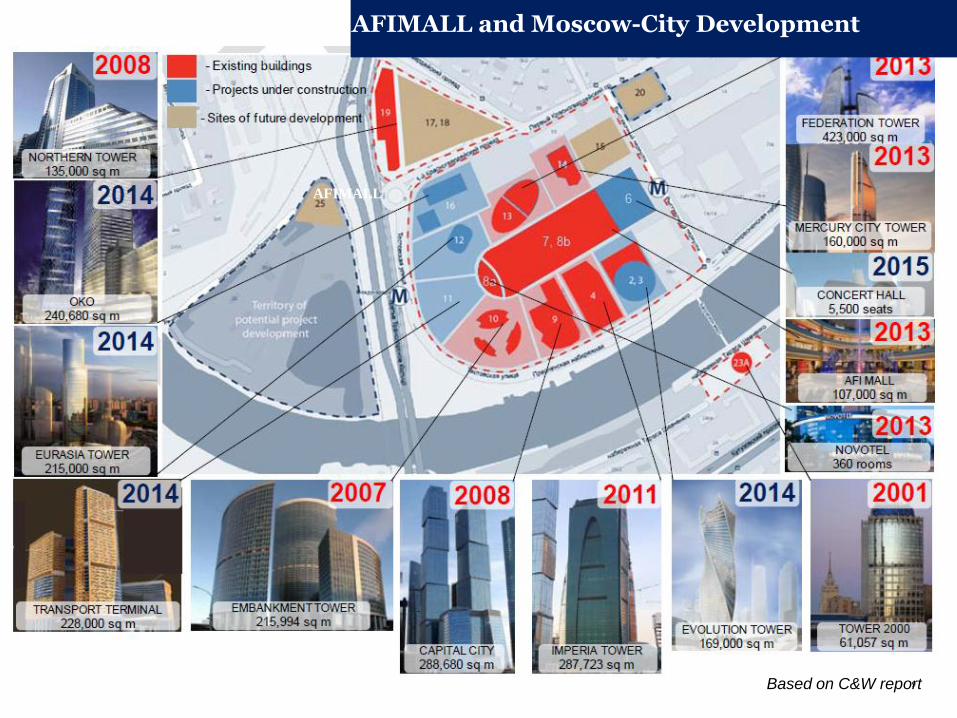

AFIMALL and Moscow-City Development

AFIMALL

MOSCOW CITY DEVELOPMENT

Existing Office Complex 0 – Tower 2000

4 – Imperia Tower

8 – CityPoint

9 – Capital City

10 – Naberezhnaya Tower

12 – Eurasia Tower

13a – Federation Tower (West)

19 – Northern Tower

6, 7 – Central Core (AFIMALL City)

Under Construction 2, 3 – Evolution Tower

11 – IQ-quarter

13b – Federation Tower (East)

14 – Mercury City Tower

16a – OKO

16b – Parking

Planned 15 – Moscow City Government

Building

20 – Exposition and Business Center

By 2015 total office stock expected to reach 1.0 m sq m

Following the delivery of Eurasia Tower in Q1 2014 (90K sqm) , the total

stock in Moscow-City reached 676K sqm. By the end of 2014, market expects

it to growth further with the commissioning of OKO MFC, while in 2015 the

delivery of Evolution Tower (78K sqm), IQ-quarter (107K sqm) and possibly

part of Federation Tower East (101K sqm) will bring the total stock of Moscow-

City to 1m sq m.

About 120K workforce are expected to work in the Moscow City area by the

time all planned office has been constructed

The Moscow City vacancy rate increased to c. 37% due to the recent launching

of the new building Eurazia Tower.

2 additional metro lines: Prolongation of Tretyakovskaya till Ramenki,

construction of Hordovaya with 4 different lines connections (Vystovochnaya,

Polezhaevskaya, Hodinskoye Pole, Dinamo, Savelovskaya) by 2015 – 2016.

One of the major deals that was singed in Q1 2014 in MCC were the agreement

to lease the 2,336 sqm in Naberezhnaya Tower.

The new metro station Delovoy Center, which has a direct access to the mall,

has started its operations. 8

AFIMALL and Moscow-City Development

AFIMALL

Based on C&W report 9

Building AFIMALL Ozerkovskaya III Berezkovskaya Tverskaya Plaza IIPaveletskaya, bld.

1H2O Tvesrkaya Plaza Ib

Aquamarine

Hotel*

Plaza SPA

Kislovodsk

Plaza SPA

ZheleznovodskTOTAL

Moscow Moscow Moscow Moscow Moscow Moscow Moscow Moscow

Moscow City CBD CBD CBD CBD

Class Retail Office A & Street

Retail Office B

Office & Street

Retail Office B Office B

Office & Street

Retail Hotel Hotel Hotel

GBA, sqm 283,128 61,772 11,612 6,008 16,246 10,698 2,104 8,931 25,000 11,701 437K

GLA, sqm 107,208 46,247 10,250 6,008 14,085 8,990 1,909 159 keys 275 keys 134 keys 195K

Parking lots (total), # 2,075 466 150 - 126 81 - 15 - 15

Ocupancy rate, % 83% - 91% 95% 96% 76% 95% 71% 56% 59%

750- Office

500 - retail

NOI stab (C&W est.),

US mn149.2 38.4 5.2 2.5 4.5 2.7 1.3 - - - 204

NOI Year 2014 (C&W

est.), US mn 89.0 12.2 4.6 2.8 2.9 1.6 0.9 - - - 114

MV,US$ mn*** 1,160 324 38.5 32 29.6 17.3 8.8 28.1 22.7 20.3 1,681

Location Kavkaz region Kavkaz region

1,224 Average rent as of

31.12.2013, $/sq m357 579 365 689 594 ADR 231 ADR 371 ADR 223

Yielding Properties

10

* Current rent presented as for the end of December 2013, except AFIMALL. AFIMALL average rent is for March 31, 2014

** Occupancy presented as for the end of December 2013, except AFIMALL. AFIMALL occupancy is for March 31, 2014

*** MV based on C&W valuation as for 31.12.2013. Hotels presented by cost value and 100% of the project

**** Information after disposal of 1 Bld Project is not leased yet

10

*

**

****

SECTION 2 Project Update

Development Projects

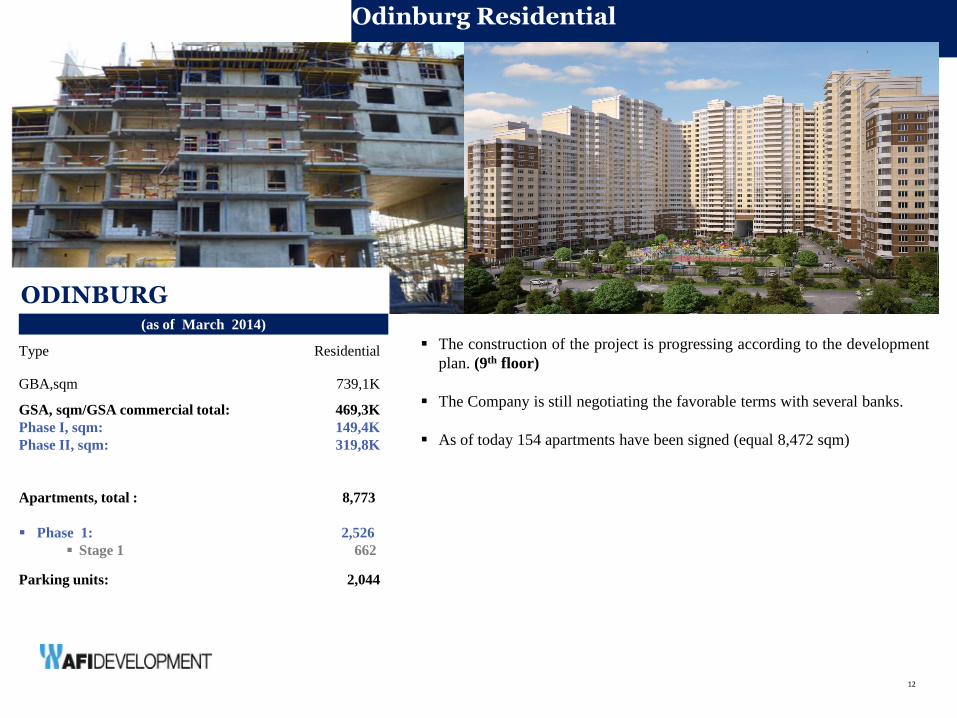

ODINBURG

The construction of the project is progressing according to the development

plan. (9th floor)

The Company is still negotiating the favorable terms with several banks.

As of today 154 apartments have been signed (equal 8,472 sqm)

Odinburg Residential

12

(as of March 2014)

Type Residential

GBA,sqm 739,1K

GSA, sqm/GSA commercial total:

Phase I, sqm:

Phase II, sqm:

469,3K

149,4K

319,8K

Apartments, total : 8,773

Phase 1: 2,526

Stage 1 662

Parking units: 2,044

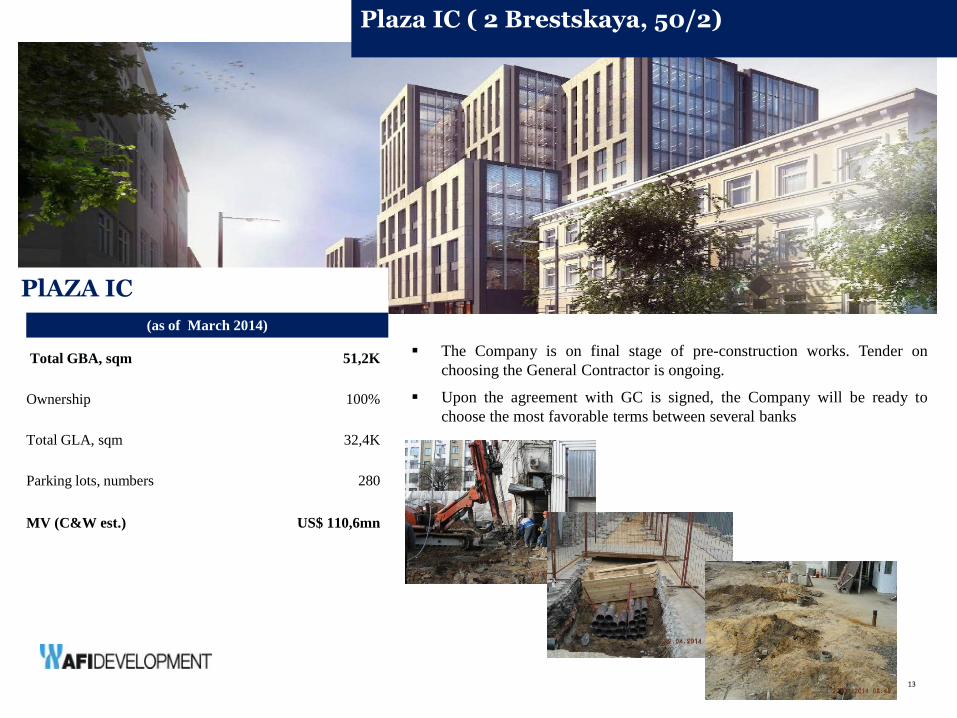

PlAZA IC

(as of March 2014)

Total GBA, sqm 51,2K

Ownership 100%

Total GLA, sqm 32,4K

Parking lots, numbers 280

MV (C&W est.) US$ 110,6mn

13

Plaza IC ( 2 Brestskaya, 50/2)

The Company is on final stage of pre-construction works. Tender on

choosing the General Contractor is ongoing.

Upon the agreement with GC is signed, the Company will be ready to

choose the most favorable terms between several banks

PARAMETERS:

Type: Mix

GBA, sqm: 111,7K

GLA, sqm: 90,3K

MV(C&W),mn: S$ 103,5

(as of March 2014)

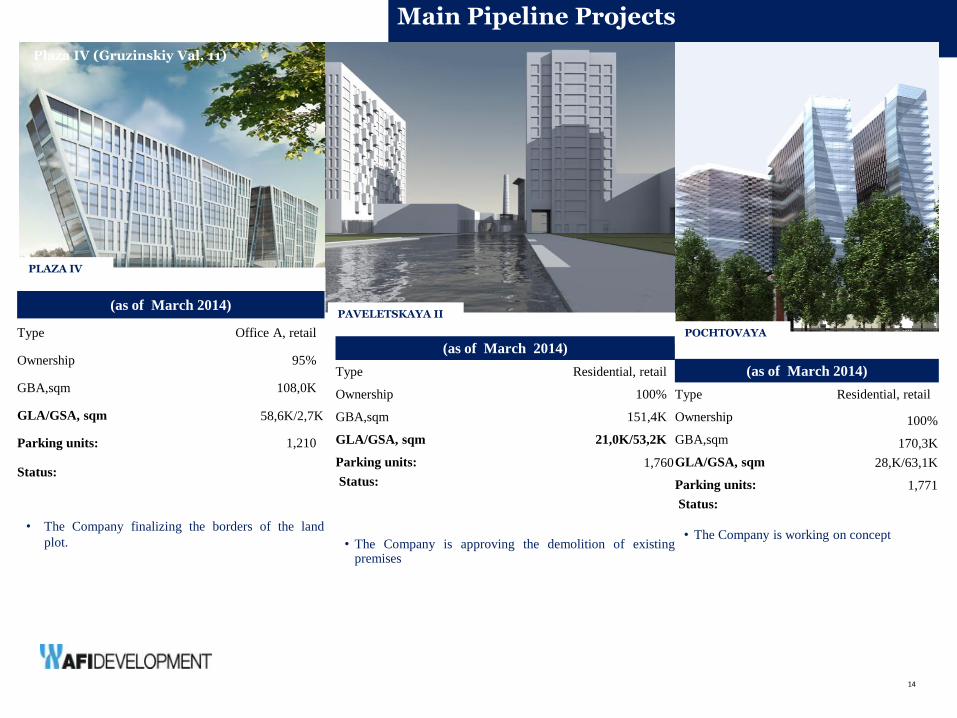

Type Office A, retail

Ownership 95%

GBA,sqm 108,0K

GLA/GSA, sqm 58,6K/2,7K

Parking units: 1,210

Status:

• The Company finalizing the borders of the land

plot.

(as of March 2014)

Type Residential, retail

Ownership 100%

GBA,sqm 151,4K

GLA/GSA, sqm 21,0K/53,2K

Parking units: 1,760

Status:

• The Company is approving the demolition of existing premises

(as of March 2014)

Type Residential, retail

Ownership 100%

GBA,sqm 170,3K

GLA/GSA, sqm 28,K/63,1K

Parking units: 1,771

Status:

• The Company is working on concept

PLAZA IV

PAVELETSKAYA II

POCHTOVAYA

14

Plaza IV (Gruzinskiy Val, 11)

Main Pipeline Projects

SECTION 3 Financial Update

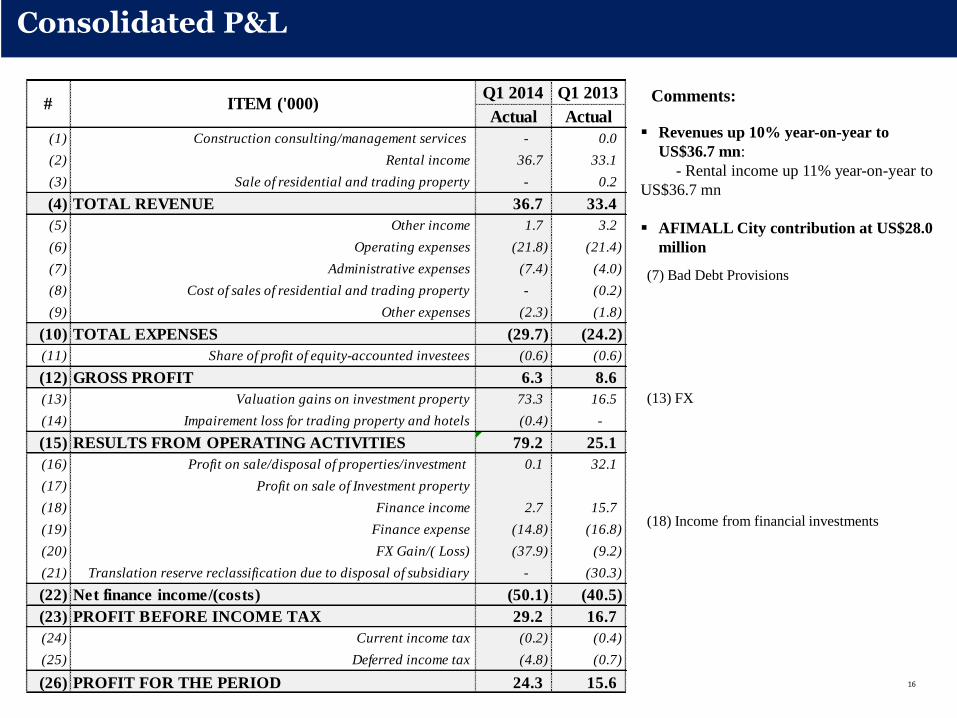

Q1 2014 Q1 2013

Actual Actual

(1) Construction consulting/management services - 0.0

(2) Rental income 36.7 33.1

(3) Sale of residential and trading property - 0.2

(4) TOTAL REVENUE 36.7 33.4

(5) Other income 1.7 3.2

(6) Operating expenses (21.8) (21.4)

(7) Administrative expenses (7.4) (4.0)

(8) Cost of sales of residential and trading property - (0.2)

(9) Other expenses (2.3) (1.8)

(10) TOTAL EXPENSES (29.7) (24.2)

(11) Share of profit of equity-accounted investees (0.6) (0.6)

(12) GROSS PROFIT 6.3 8.6

(13) Valuation gains on investment property 73.3 16.5

(14) Impairement loss for trading property and hotels (0.4) -

(15) RESULTS FROM OPERATING ACTIVITIES 79.2 25.1

(16) Profit on sale/disposal of properties/investment 0.1 32.1

(17) Profit on sale of Investment property

(18) Finance income 2.7 15.7

(19) Finance expense (14.8) (16.8)

(20) FX Gain/( Loss) (37.9) (9.2)

(21) Translation reserve reclassification due to disposal of subsidiary - (30.3)

(22) Net finance income/(costs) (50.1) (40.5)

(23) PROFIT BEFORE INCOME TAX 29.2 16.7

(24) Current income tax (0.2) (0.4)

(25) Deferred income tax (4.8) (0.7)

(26) PROFIT FOR THE PERIOD 24.3 15.6

# ITEM ('000)

Consolidated P&L

16

Revenues up 10% year-on-year to

US$36.7 mn:

- Rental income up 11% year-on-year to

US$36.7 mn

AFIMALL City contribution at US$28.0

million

16

(7) Bad Debt Provisions

(13) FX

(18) Income from financial investments

Comments:

17

Statement of Financial Position

Comments:

(2) Disposition of Saint-Petersburg project

(32) Execution of last payment referred to GUP City and VAT from

Ozerkovskaya 1st building deal.

17

Strong cash position with US 148,7 million in cash ,cash equivalents and

marketable securities as at 31 March 2014

Debt to equity ratio ( 47%)

Investment property is significant part of total asset portfolio

31.03.2014 31.12.2013

US$ mn US$ mn US$ mn %

(1) Investment property 1,609.8 1,609.8 0.0 0%

(2) Investment property under development 633.9 635.3 (1.4) 0%

(3) Investment in Joint Ventures 4.5 5.6 (1.1)

(4) Property, plant and equipment 62.3 69.7 (7.4)

(5) Long-term loans receivable 21.4 21.7 (0.2)

(6) VAT recoverable 0.1 0.4 (0.4)

(7) Goodwill 0.0 0.0 0.0

(8) Non-current assets 2,331.9 2,342.4 (10.5) 0%

(9) Trading property 5.9 6.4 (0.5) (8%)

(10) Trading properties under construction 129.4 127.2 2.2

(11) Inventory 0.5 0.6 (0.1)

(12) Short-term loans receivable 0.7 0.8 (0.0)

(13) Trade and other receivables 107.2 106.4 0.8 1%

(14) Current tax assets 0.2 0.0 0.2

(15) Cash and cash equivalents 137.9 193.3 (55.4) (29%)

(16) Other investments 10.8 10.0 0.8

(17) Current assets 392.6 444.7 (52.1) -12%

(18) TOTAL ASSETS 2,724.6 2,787.1 (62.6) -2%

(19) Equity

(20) Share capital 1.0 1.0 0.0

(21) Share premium 1763.4 1763.4 0.0 -

(22) Translation reserve (191.3) (150.5) (40.9) 27%

(23) Retaining earnings 142.9 117.7 25.2

(24) Non-controlling interest (2.0) (2.2) 0.2

(25) TOTAL EQUITY 1,714.0 1,729.5 (15.4) -1%

(26) Trade and other payables 0.0 0.0 0.0

(27) Long-term loans and borrowings 580.7 778.9 (198.2) (25%)

(28) Deferred tax liabilities 131.0 125.3 5.7 5%

(29) Deferred income 20.6 22.0 (1.5) (7%)

(30) Non-current liabilities 732.3 926.2 (193.9) -21%

(31) Short-term loans and borrowings 232.0 27.0 204.9 758%

(32) Trade and other payables 46.3 100.4 (54.1)

(33) Income tax payable - 4.1

(33) Current liabilities 278.3 131.4 146.8

(34) TOTAL LIABILITIES 1010.5 1057.7 (47.1) (4%)

(35) TOTAL EQUITY AND LIABILITIES 2,724.6 2,787.1 (62.6) (2%)

# NARRATIVE Changing

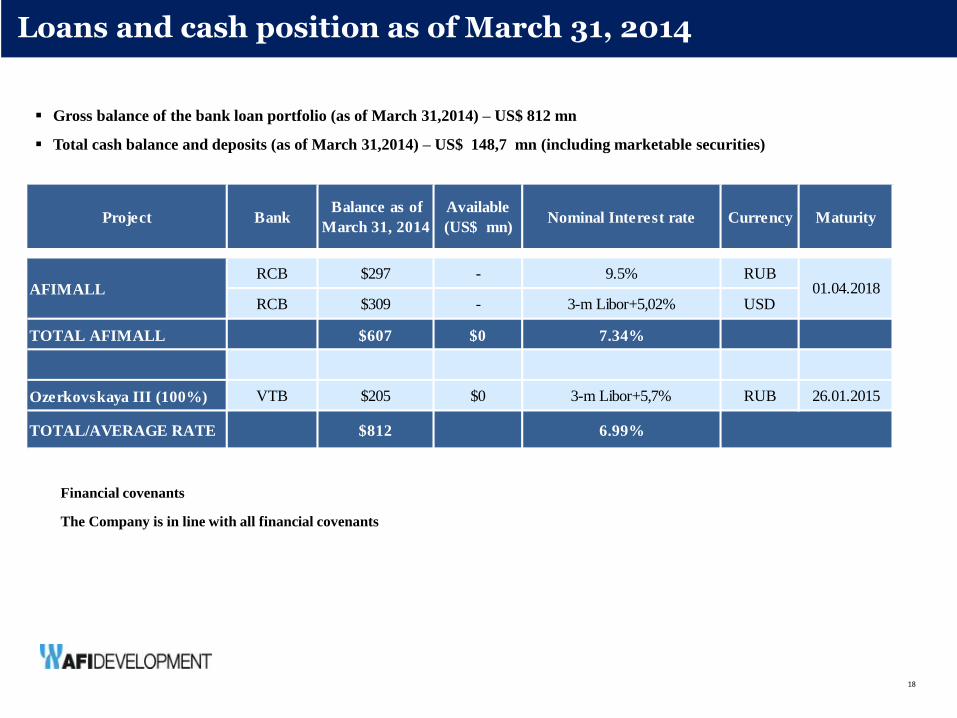

Loans and cash position as of March 31, 2014

The Company is in line with all financial covenants

*

18

Gross balance of the bank loan portfolio (as of March 31,2014) – US$ 812 mn

Total cash balance and deposits (as of March 31,2014) – US$ 148,7 mn (including marketable securities)

Financial covenants

Project BankBalance as of

March 31, 2014

Available

(US$ mn)Nominal Interest rate Currency Maturity

RCB $297 - 9.5% RUB

RCB $309 - 3-m Libor+5,02% USD

TOTAL AFIMALL $607 $0 7.34%

Ozerkovskaya III (100%) VTB $205 $0 3-m Libor+5,7% RUB 26.01.2015

TOTAL/AVERAGE RATE $812 6.99%

AFIMALL 01.04.2018

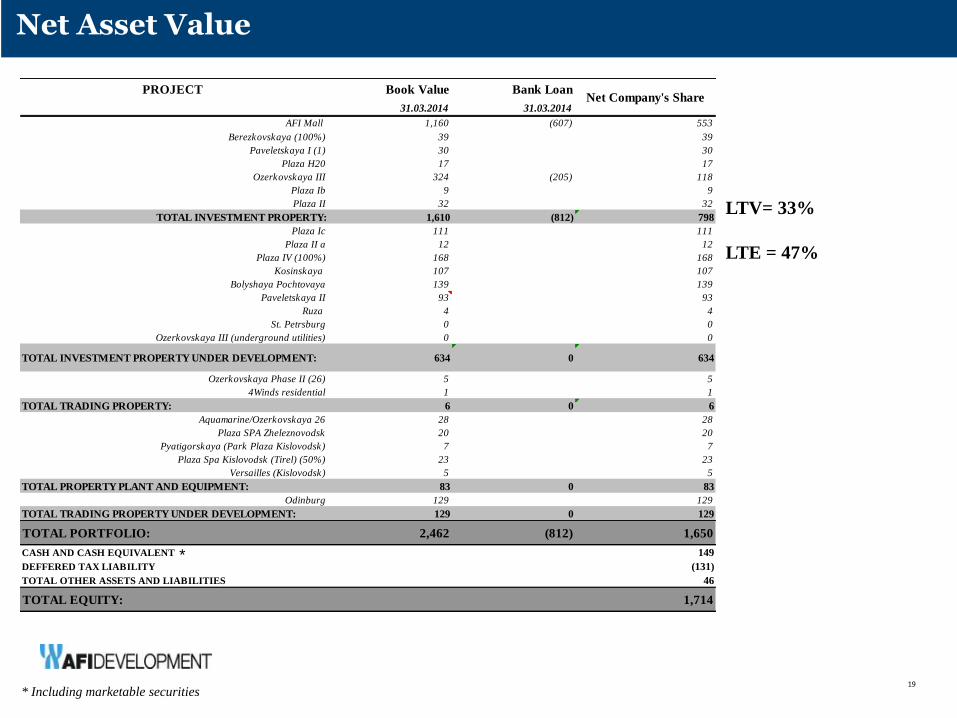

PROJECT Book Value Bank Loan

31.03.2014 31.03.2014

AFI Mall 1,160 (607) 553

Berezkovskaya (100%) 39 39

Paveletskaya I (1) 30 30

Plaza H20 17 17

Ozerkovskaya III 324 (205) 118

Plaza Ib 9 9

Plaza II 32 32

TOTAL INVESTMENT PROPERTY: 1,610 (812) 798

Plaza Ic 111 111

Plaza II a 12 12

Plaza IV (100%) 168 168

Kosinskaya 107 107

Bolyshaya Pochtovaya 139 139

Paveletskaya II 93 93

Ruza 4 4

St. Petrsburg 0 0

Ozerkovskaya III (underground utilities) 0 0

TOTAL INVESTMENT PROPERTY UNDER DEVELOPMENT: 634 0 634

Ozerkovskaya Phase II (26) 5 5

4Winds residential 1 1

TOTAL TRADING PROPERTY: 6 0 6

Aquamarine/Ozerkovskaya 26 28 28

Plaza SPA Zheleznovodsk 20 20

Pyatigorskaya (Park Plaza Kislovodsk) 7 7

Plaza Spa Kislovodsk (Tirel) (50%) 23 23

Versailles (Kislovodsk) 5 5

TOTAL PROPERTY PLANT AND EQUIPMENT: 83 0 83

Odinburg 129 129

TOTAL TRADING PROPERTY UNDER DEVELOPMENT: 129 0 129

TOTAL PORTFOLIO: 2,462 (812) 1,650

CASH AND CASH EQUIVALENT 149

DEFFERED TAX LIABILITY (131)

TOTAL OTHER ASSETS AND LIABILITIES 46

TOTAL EQUITY: 1,714

Net Company's Share

19

Net Asset Value

LTV= 33%

LTE = 47%

19

*

* Including marketable securities

Annex

Market Update

Market Overview and Capital Markets

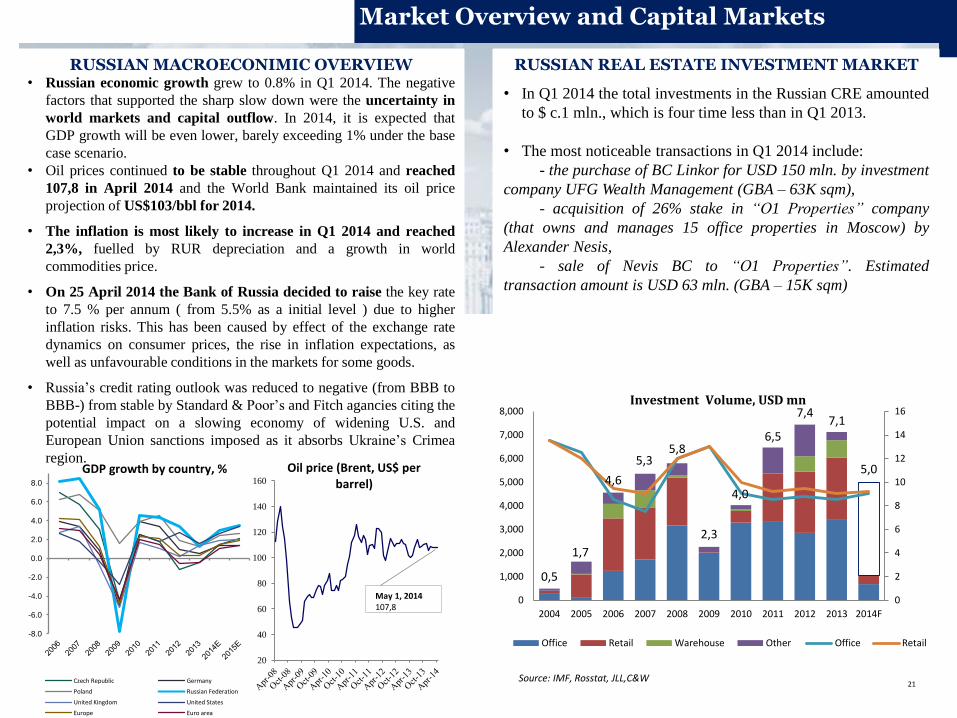

RUSSIAN MACROECONIMIC OVERVIEW RUSSIAN REAL ESTATE INVESTMENT MARKET • Russian economic growth grew to 0.8% in Q1 2014. The negative

factors that supported the sharp slow down were the uncertainty in

world markets and capital outflow. In 2014, it is expected that

GDP growth will be even lower, barely exceeding 1% under the base

case scenario.

• Oil prices continued to be stable throughout Q1 2014 and reached

107,8 in April 2014 and the World Bank maintained its oil price

projection of US$103/bbl for 2014.

• The inflation is most likely to increase in Q1 2014 and reached

2,3%, fuelled by RUR depreciation and a growth in world

commodities price.

• On 25 April 2014 the Bank of Russia decided to raise the key rate

to 7.5 % per annum ( from 5.5% as a initial level ) due to higher

inflation risks. This has been caused by effect of the exchange rate

dynamics on consumer prices, the rise in inflation expectations, as

well as unfavourable conditions in the markets for some goods.

• Russia’s credit rating outlook was reduced to negative (from BBB to

BBB-) from stable by Standard & Poor’s and Fitch agancies citing the

potential impact on a slowing economy of widening U.S. and

European Union sanctions imposed as it absorbs Ukraine’s Crimea

region.

• In Q1 2014 the total investments in the Russian CRE amounted

to $ c.1 mln., which is four time less than in Q1 2013.

• The most noticeable transactions in Q1 2014 include:

- the purchase of BC Linkor for USD 150 mln. by investment

company UFG Wealth Management (GBA – 63K sqm),

- acquisition of 26% stake in “O1 Properties” company

(that owns and manages 15 office properties in Moscow) by

Alexander Nesis,

- sale of Nevis BC to “O1 Properties”. Estimated

transaction amount is USD 63 mln. (GBA – 15K sqm)

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

GDP growth by country, %

Czech Republic Germany

Poland Russian Federation

United Kingdom United States

Europe Euro area

21

20

40

60

80

100

120

140

160

Oil price (Brent, US$ per barrel)

May 1, 2014 107,8

Source: IMF, Rosstat, JLL,C&W

0,5

1,7

4,6

5,3 5,8

2,3

4,0

6,5

7,4 7,1

5,0

0

2

4

6

8

10

12

14

16

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F

Investment Volume, USD mn

Office Retail Warehouse Other Office Retail

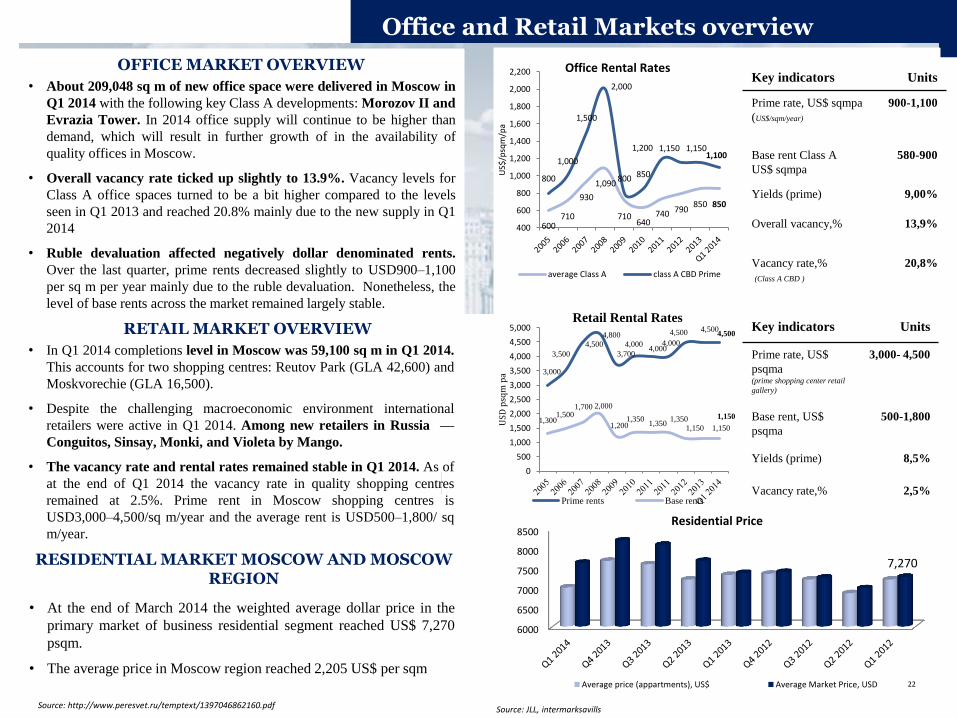

Office and Retail Markets overview

OFFICE MARKET OVERVIEW

RETAIL MARKET OVERVIEW

Key indicators Units

Prime rate, US$ sqmpa

(US$/sqm/year)

900-1,100

Base rent Class A

US$ sqmpa

580-900

Yields (prime) 9,00%

Overall vacancy,% 13,9%

Vacancy rate,%

(Class A CBD )

20,8%

Key indicators Units

Prime rate, US$

psqma (prime shopping center retail

gallery)

3,000- 4,500

Base rent, US$

psqma

500-1,800

Yields (prime) 8,5%

Vacancy rate,% 2,5%

• About 209,048 sq m of new office space were delivered in Moscow in

Q1 2014 with the following key Class A developments: Morozov II and

Evrazia Tower. In 2014 office supply will continue to be higher than

demand, which will result in further growth of in the availability of

quality offices in Moscow.

• Overall vacancy rate ticked up slightly to 13.9%. Vacancy levels for

Class A office spaces turned to be a bit higher compared to the levels

seen in Q1 2013 and reached 20.8% mainly due to the new supply in Q1

2014

• Ruble devaluation affected negatively dollar denominated rents.

Over the last quarter, prime rents decreased slightly to USD900–1,100

per sq m per year mainly due to the ruble devaluation. Nonetheless, the

level of base rents across the market remained largely stable.

• In Q1 2014 completions level in Moscow was 59,100 sq m in Q1 2014.

This accounts for two shopping centres: Reutov Park (GLA 42,600) and

Moskvorechie (GLA 16,500).

• Despite the challenging macroeconomic environment international

retailers were active in Q1 2014. Among new retailers in Russia —

Conguitos, Sinsay, Monki, and Violeta by Mango.

• The vacancy rate and rental rates remained stable in Q1 2014. As of

at the end of Q1 2014 the vacancy rate in quality shopping centres

remained at 2.5%. Prime rent in Moscow shopping centres is

USD3,000–4,500/sq m/year and the average rent is USD500–1,800/ sq

m/year.

22

RESIDENTIAL MARKET MOSCOW AND MOSCOW REGION

• At the end of March 2014 the weighted average dollar price in the

primary market of business residential segment reached US$ 7,270

psqm.

• The average price in Moscow region reached 2,205 US$ per sqm

600 710

930

1,090

710 640

740 790 850 850

800

1,000

1,500

2,000

800 850

1,200 1,150 1,150 1,100

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

US$

/psq

m/p

a

Office Rental Rates

average Class A class A CBD Prime

3,000

3,500

4,500

4,800

3,700

4,000 4,000

4,000

4,500 4,500 4,500

1,300 1,500

1,700 2,000

1,200 1,350

1,350 1,350

1,150 1,150

1,150

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

USD

psq

m p

a

Retail Rental Rates

Prime rents Base rents

6000

6500

7000

7500

8000

8500

7,270

Residential Price

Average price (appartments), US$ Average Market Price, USD

Source: JLL, intermarksavills Source: http://www.peresvet.ru/temptext/1397046862160.pdf