quality growth; growing returns

TRANSCRIPT

Alison CooperChief Executive

Deutsche Bank Global Consumer Conference June 2016

Quality Growth; Growing Returns

2 |

Disclaimer

Certain statements in this presentationconstitute or may constitute forward-lookingstatements. Any statement in thispresentation that is not a statement ofhistorical fact including, without limitation,those regarding the Company’s futureexpectations, operations, financialperformance, financial condition andbusiness is or may be a forward-lookingstatement. Such forward-looking statementsare subject to risks and uncertainties thatmay cause actual results to differ materiallyfrom those projected or implied in anyforward-looking statement. These risks anduncertainties include, among other factors,changing economic, financial, business orother market conditions. These and otherfactors could adversely affect the outcome

and financial effects of the plans and eventsdescribed in this presentation. As a result,you are cautioned not to place any relianceon such forward-looking statements. Theforward-looking statements reflect knowledgeand information available at the date of thispresentation and the Company undertakes noobligation to update its view of such risks anduncertainties or to update the forward-lookingstatements contained herein. Nothing in thispresentation should be construed as a profitforecast or profit estimate and no statementin this presentation should be interpreted tomean that the future earnings per share ofthe Company for current or future financialyears will necessarily match or exceed thehistorical or published earnings per share ofthe Company. This presentation has been

prepared for, and only for the members of theCompany, as a body, and no other persons.The Company, its directors, employees,agents or advisers do not accept or assumeresponsibility to any other person to whomthis presentation is shown or into whosehands it may come and any suchresponsibility or liability is expresslydisclaimed. The material in this presentationis not provided for tobacco productadvertising or promotional purposes. Thismaterial does not constitute and should notbe construed as constituting an offer to sell,or a solicitation of an offer to buy, anytobacco products. The Company’s productsare sold only in compliance with the laws ofthe particular jurisdictions in which they aresold.

Deutsche Bank Consumer Conference | June 2016

3 |

Introducing Imperial Brands

160 markets

36,400 employees

Top 5 marketsUS

GermanyUK

AustraliaSpain

5 year TSR+125%Dividend

+10% pa

Adjusted operating

profit

£3.1bn

3 | Deutsche Bank Consumer Conference | June 2016

4 |

AGILITY

Maximise sustainable shareholder returns

Develop Footprint

• Opportunities in Growth Markets

• Balanced approach in Returns Markets

Drive CostOptimisation

• Operating model

• Lean manufacturing

• Overhead control

Embed CapitalDiscipline

• Cash conversion

• Capital allocation: investment, dividend and debt repayment

Strengthen Portfolio

• Further simplification

• Investment in Growth & Specialist Brands

• E-vapour development

A Clear Strategy

QUALITY DISCIPLINE

Deutsche Bank Consumer Conference | June 2016

5 |

Quality GrowthBrand and market choices

Fewer, bigger, stronger

Returns&

Growth

Markets that matter

Rigorous evaluation

Balanced approach

Focus on profitable growth

Optimise portfolio

Strengthen brands

Build equity

Growth Brands

Portfolio Brands

Brands Footprint

Deutsche Bank Consumer Conference | June 2016

6 |

Sep 13 Sep 15 TargetBrands

249

200

12520%

50%

Targeting 50% reduction

Strengthening the portfolio

Start

*Brand count excludes Premium cigar and Fontem Ventures brands

Sep 13 Sep 15 TargetBrand Market Units

1076

911

53515%

50%

Focus on Fewer, Bigger, Stronger

Deutsche Bank Consumer Conference | June 2016

7 |

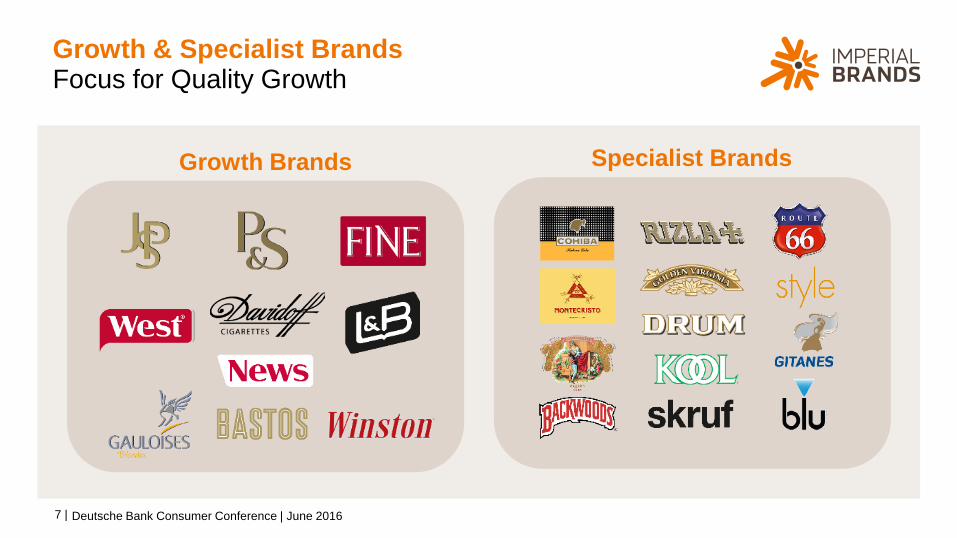

Growth & Specialist BrandsFocus for Quality Growth

Growth Brands Specialist Brands

Deutsche Bank Consumer Conference | June 2016

8 |

Simplifying the PortfolioPrioritising to removing complexity

Simplification Options

Delist

Brands and SKUs with low commercial and

strategic value

c.20% tail SKUs delisted (limited commercial impact)

Migrate

Brands overlapping with Growth Brands (where transition commercially

viable)

38 migration cases completed(+25% Growth Brand volume by

end of FY16)

Divest

Segments which are small, declining and

non-strategic

Pipe, chewing tobacco, snuff sold in FY15

Deutsche Bank Consumer Conference | June 2016

9 |

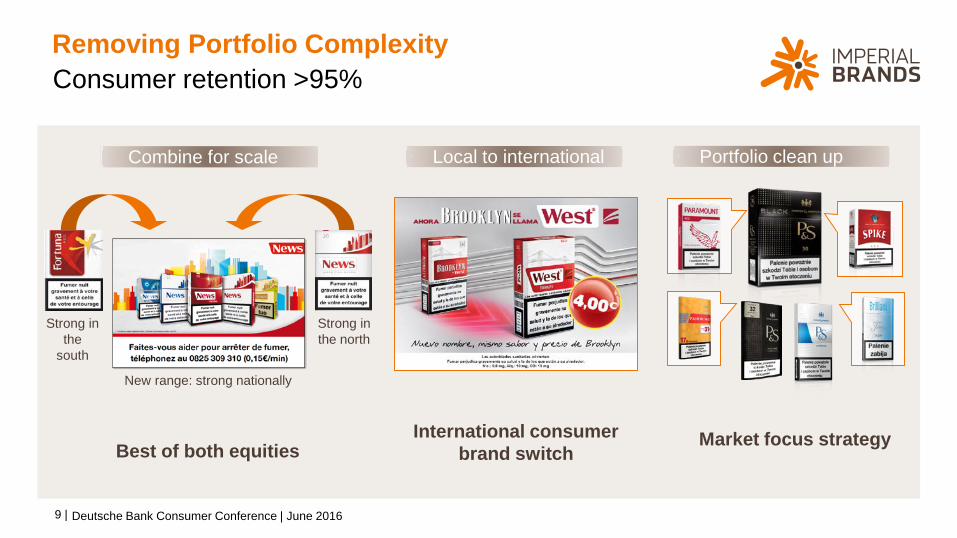

Removing Portfolio Complexity

Best of both equities

Consumer retention >95%

Strong in the

south

Strong in the north

New range: strong nationally

International consumer brand switch

Market focus strategy

Combine for scale Local to international Portfolio clean up

Deutsche Bank Consumer Conference | June 2016

10 |

81% 91%today after

Reality: Insufficient shelf space for full portfolio

Need: Drive distribution behind top SKUs

Knock On: Increased rate of sales (‘halo effect’)

Average weighted distribution of strongest SKUs

Average shelfspace

SKUs today

Rat

e of

sal

es

Weighted distribution and on-shelf availability, advocacy

46

84Market example

Taking Portfolio Transformation FurtherGrowth & cost saving opportunities

Deutsche Bank Consumer Conference | June 2016

11 |

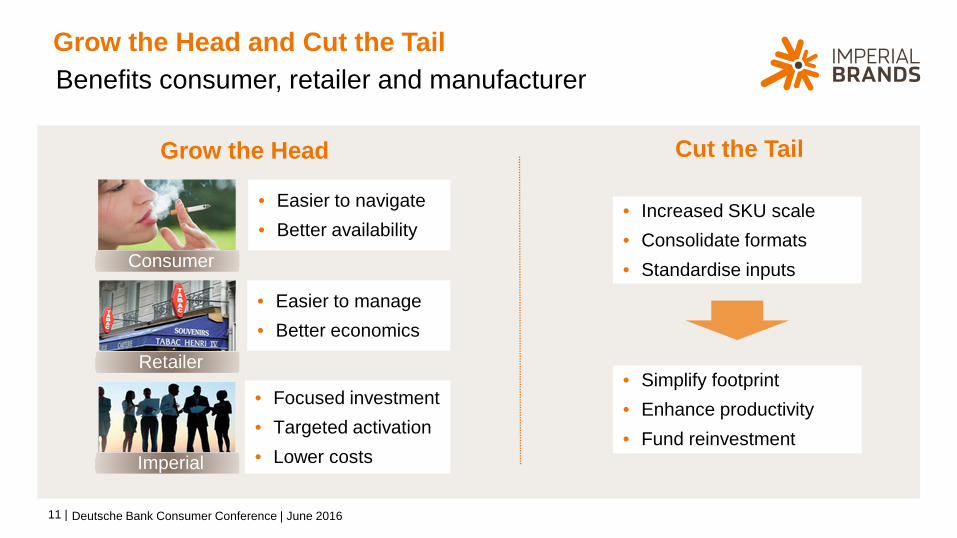

• Easier to navigate• Better availability

• Easier to manage • Better economics

• Focused investment• Targeted activation• Lower costs

Grow the Head and Cut the TailBenefits consumer, retailer and manufacturer

Deutsche Bank Consumer Conference | June 2016

Consumer

Retailer

Imperial

Grow the Head Cut the Tail

• Increased SKU scale• Consolidate formats• Standardise inputs

• Simplify footprint• Enhance productivity• Fund reinvestment

12 |

Further Simplification: RussiaBrand reduction from fourteen to five

Primary Secondary

Top Cities

Maintain(4 Brands) / Launch (P&S)

Maintain(4 brands) /

Launch (P&S)

Delist (5 Brands)Delist(5 brands)

Migrate (4 Brands)Migrate(4 brands)

Deutsche Bank Consumer Conference | June 2016

13 |

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jun-15 Sep-15 Dec-15 Mar-16

Russia: Focused Choices Paying Off

Source: Nielsen

Improved market share of Growth and Specialist Brands

Balkan Star migration & portfolio simplification

• “Grow the head” pilot market

• Better portfolio quality

• Reduced complexity

• Positive feedback from tradeM

arke

tsha

re (%

)

Deutsche Bank Consumer Conference | June 2016

14 |

51 54 57 5975

49 46 43 4125

FY13 FY14 FY15 HY16 Target

More revenue from strongest brands

Growth & Specialist BrandsPortfolio Brands

20

40

110

80

FY13 FY14 FY15 HY16

Growing share of Growth Brands

Providing Platform for Sustainable Quality GrowthImproving quality of growth

Deutsche Bank Consumer Conference | June 2016

15 |

Investing in Markets that MatterClear priorities

Based on industry profit pool potential and our ability to win

Leverage sales growth drivers across our footprint

New operating model improving efficiencies and effectiveness

Agile

Effective

Disciplined

Portfolio optimisation strategy driving simplicity

Growth Brands

Portfolio Brands

Disciplined and agile approach to market investment choices

Returns&

Growth

Deutsche Bank Consumer Conference | June 2016

16 |

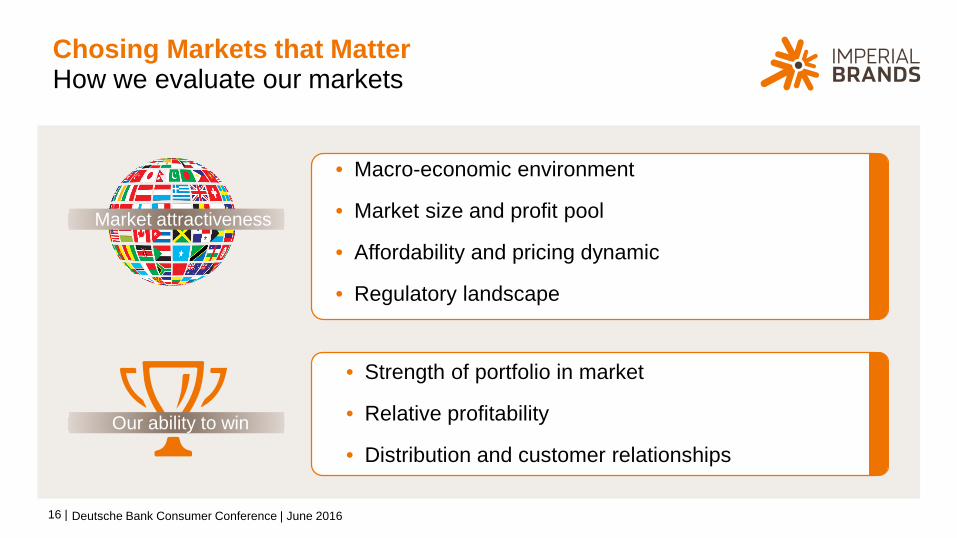

Chosing Markets that MatterHow we evaluate our markets

Market attractiveness

Our ability to win

• Macro-economic environment

• Market size and profit pool

• Affordability and pricing dynamic

• Regulatory landscape

• Strength of portfolio in market

• Relative profitability

• Distribution and customer relationships

Deutsche Bank Consumer Conference | June 2016

17 |

0

30

60

90

120

150

180

210

240

Venezuela

India

Morocco

Bulgaria

Rom

ania

Indonesia

Thailand

Egypt

Ukraine

Vietnam

Ireland

Malaysia

Poland

UK

Turkey

Portugal

Czech R

ep.

Brazil

Norw

ay

Slovakia

Greece

Netherlands

France

Australia

Spain

Italy

Belgium

Sweden

Saudi Arabia

Russia

Germ

any

Argentina

Austria

Japan

Taiwan

US

A

South Korea

No presence or revenue < 0.5%

Affordability

Data Source: Euromonitor

Majority of revenue from most affordable markets

Growth Markets

330

c.75% revenue in markets with better than average affordability

average

Min

uets

of l

abou

r at a

vg. w

age

per 2

0 ci

gare

ttes

Returns MarketsMarkets representing > 0.5% of IMB net revenue:

≈

Deutsche Bank Consumer Conference | June 2016

18 |

Market Investment Criteria in Action

Macro Market size Growth of profit pool Affordability Regulation Ability

to winInvest today

Germany

Ukraine

Saudi

India

=

Deutsche Bank Consumer Conference | June 2016

19 |

Investment in New Consumer Experiences

Global• blu• Product range

Invest • Brand• Innovation • Digital

Global • blu• product range

Build• Lean scalable

operating model

Profitability• 4 markets• IP licensing

blu the consumer preferred e-vapour brand

20 |

• Stable economy

• Growing consumer confidence

• World’s largest profit pool1

• High affordability – long term growth potential

• Stable regulatory environment

A great start for ITG Brands

Market Attractiveness Ability to Win

• Highly experienced team

• New distributor contracts

• Strong cigarette, cigar and E-vapour portfolio

Investing in the US

Deutsche Bank Consumer Conference | June 2016

Premium Discount Cigar E-vapour

21 |

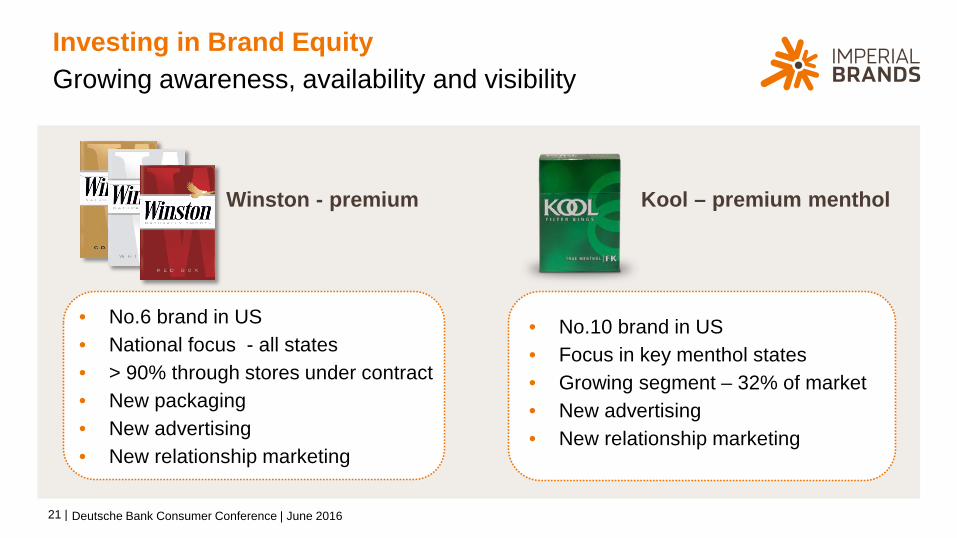

• No.6 brand in US• National focus - all states• > 90% through stores under contract• New packaging• New advertising• New relationship marketing

Growing awareness, availability and visibility

Winston - premium

Investing in Brand Equity

Deutsche Bank Consumer Conference | June 2016

Kool – premium menthol

• No.10 brand in US• Focus in key menthol states • Growing segment – 32% of market• New advertising• New relationship marketing

22 |

1.60

1.70

1.80

1.90

2.00

2.10

2.20

2.30

2.40

2.502.37

2.002.00

Merger

*Share based on 4 week rolling average volume

Strengthening Share of Focus Brands

2012 2013 2014 2015 2016

Building momentum M

arke

t sha

re*

1.73 1.71

1.88

Start of increased

promo 2.17

Deutsche Bank Consumer Conference | June 2016

23 |

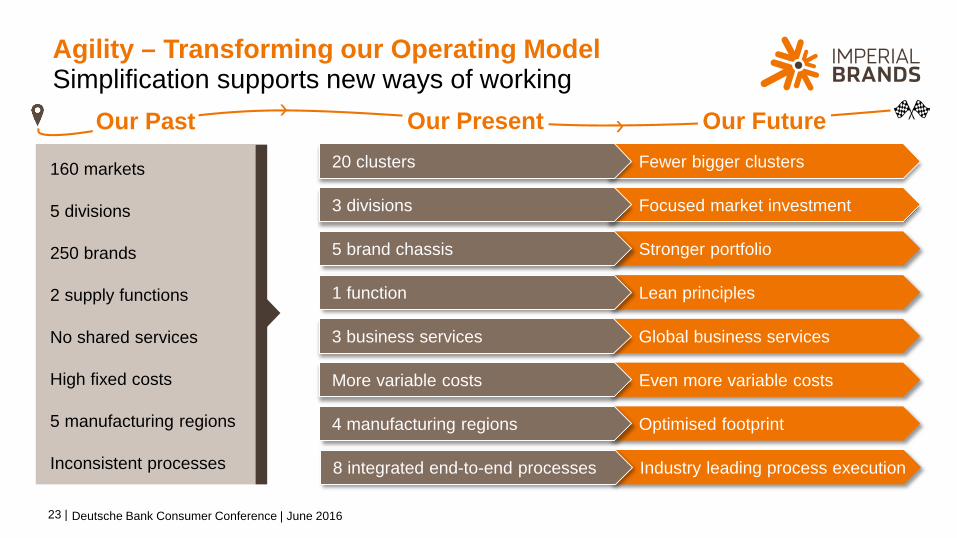

Agility – Transforming our Operating ModelSimplification supports new ways of working

160 markets

5 divisions

250 brands

2 supply functions

No shared services

High fixed costs

5 manufacturing regions

Inconsistent processes

Fewer bigger clusters

Focused market investment

Lean principles

Even more variable costs

Stronger portfolio

Optimised footprint

Global business services

Industry leading process execution

Our Past Our Present Our Future

8 integrated end-to-end processes

20 clusters

3 divisions

1 function

More variable costs

5 brand chassis

4 manufacturing regions

3 business services

Deutsche Bank Consumer Conference | June 2016

24 |

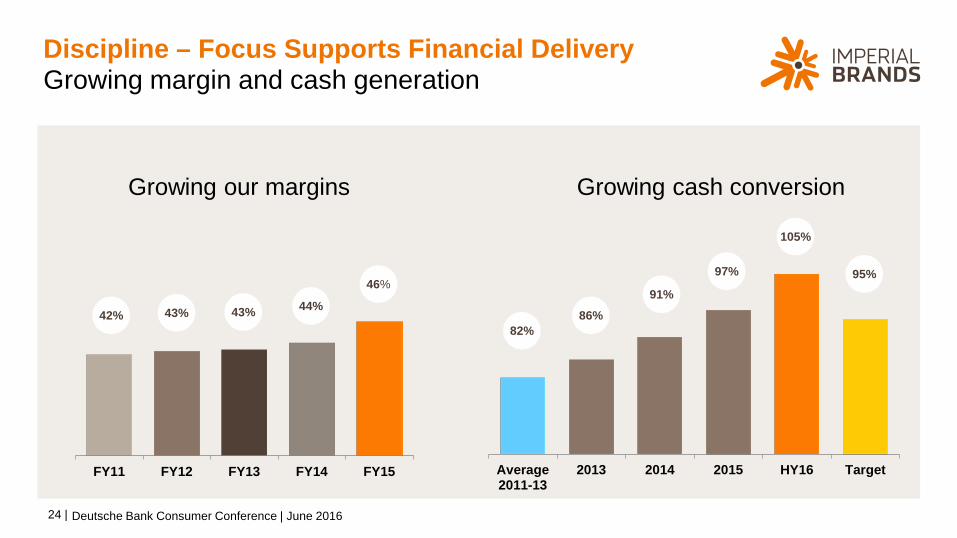

FY11 FY12 FY13 FY14 FY15

42% 43%

46%

Discipline – Focus Supports Financial Delivery

Growing our margins

Growing margin and cash generation

43% 44%

Average2011-13

2013 2014 2015 HY16 Target

82%

95%

105%

97%

91%

86%

Growing cash conversion

Deutsche Bank Consumer Conference | June 2016

25 |

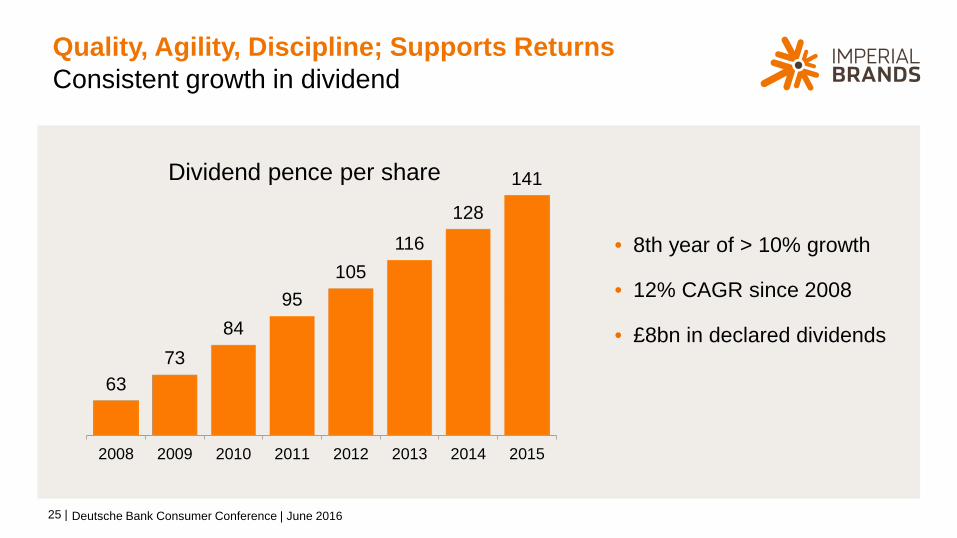

6373

8495

105116

128

141

2008 2009 2010 2011 2012 2013 2014 2015

Dividend pence per share

Quality, Agility, Discipline; Supports Returns

• 8th year of > 10% growth

• 12% CAGR since 2008

• £8bn in declared dividends

Consistent growth in dividend

Deutsche Bank Consumer Conference | June 2016

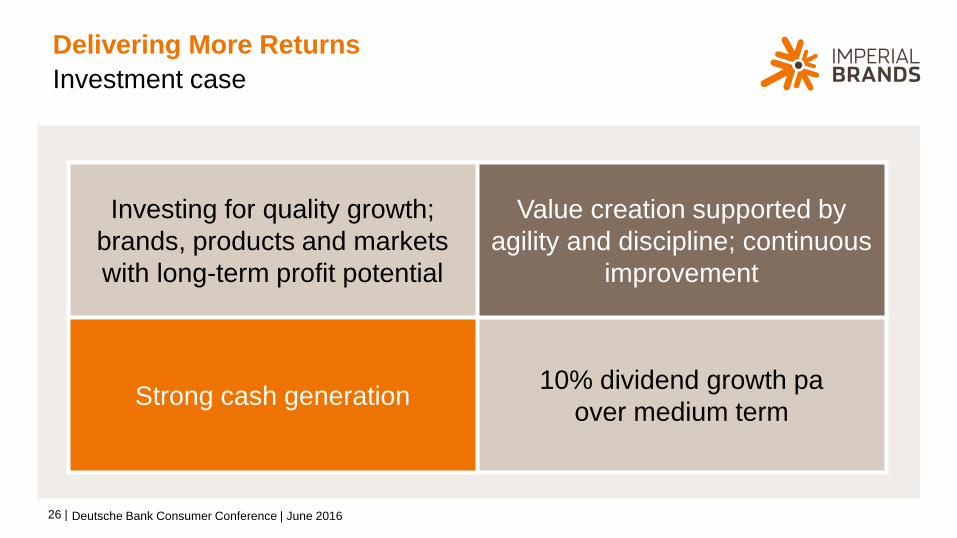

26 |

Delivering More ReturnsInvestment case

Investing for quality growth; brands, products and markets with long-term profit potential

Value creation supported by agility and discipline; continuous

improvement

Strong cash generation 10% dividend growth pa over medium term

Deutsche Bank Consumer Conference | June 2016

Alison CooperChief Executive

Deutsche Bank Global Consumer Conference June 2016

Quality Growth; Growing Returns