quant trader algorithms

TRANSCRIPT

Quant Trader

Presented by Quant Trade Technologies, Inc.

Market Forecasting Algorithms

Premium selection of algorithms

Self-optimizing ARIMA expert Finite Impulse Response Neural Network Finite State Markov Automation Stepwise Best Regression Square Root Regression Square Regression Logistic Regression

2

ARIMA for time series forecasting ARIMA models are, in theory, the most general class of models for forecasting a time series which can be made to be “stationary” by differencing.

3

An ARIMA model can be viewed as a “filter” that tries to separate the signal from the noise, and the signal is then extrapolated into the future to obtain forecasts.

Example of ARIMA forecast

4

Self-optimizing ARIMA expert

Full ARIMA(p,d,q) implementation Unlimited order of mixed modeling Conditional error estimates Chi-square statistics on residuals Expert inference for optimal parameters Automatic trend adjustments Prediction on multiple future horizons

5

FIR Neural Network Finite-Impulse-Response (FIR) Optimal selection of filter parameters Adaptive neural network training Temporal back-propagation algorithm

6

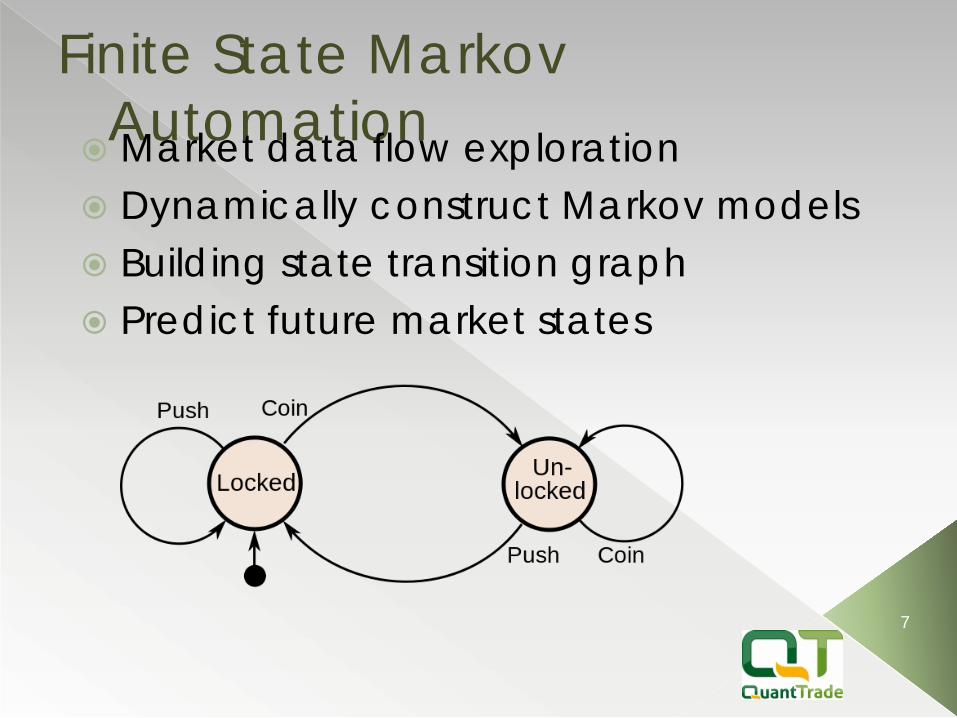

Finite State Markov Automation

Market data flow exploration Dynamically construct Markov models Building state transition graph Predict future market states

7

Stepwise Best Regression

8

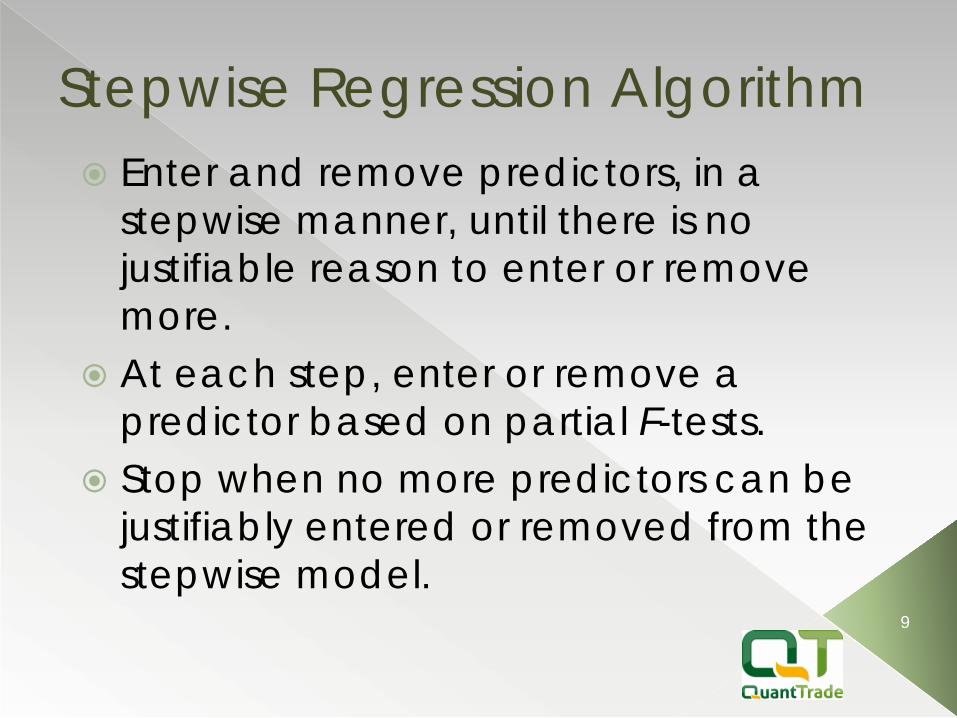

Stepwise Regression Algorithm Enter and remove predictors, in a

stepwise manner, until there is no justifiable reason to enter or remove more.

At each step, enter or remove a predictor based on partial F-tests.

Stop when no more predictors can be justifiably entered or removed from the stepwise model.

9

Linear Regression

10

Linear Regression Model Simple linear regression Least squares estimator Single explanatory variable

11

iii εβXαY ++=

• Classics of technical analysis • Useful as a reference for comparison

with nonlinear estimates

Linear versus Nonlinear Fit

12

Linear fit does not give random residuals

Nonlinear fit gives random residuals

X

resi

dual

s

X

Y

X

resi

dual

s

Y

X

Square Root Regression The square-root transformation

13

iii εXββY ++= 110

• Used to • overcome violations of the

homoscedasticity assumption • fit a non-linear relationship

Square Root Transformation

14

Shape of original relationship

X

b1 > 0

b1 < 0

X

Y

Y

Y

Y

X

X

Relationship when transformed i1i10i εXββY ++=i1i10i εXββY ++=

Quadratic Regression Model

15

where: β0 = Y intercept β1 = regression coefficient for linear effect of X on Y β2 = regression coefficient for quadratic effect on Y εi = random error in Y for observation i

Model form:

iiii εXβXββY +++= 212110

Logistic Regression

16

Log Transformation

17

Original multiplicative model Transformed multiplicative model

iβ1i0i εXβY 1= i1i10i ε logX log ββ log Ylog ++=

The Multiplicative Model:

Original multiplicative model Transformed exponential model

i2i21i10i ε ln XβXββ Yln +++=

The Exponential Model:

iXβXββ

i εeY 2i21i10 ++=

Forecast with average value

Simple moving average predictor Predicted value equal to moving

average over previous values Useful as a reference for comparison

with more complex algorithms

18

nppp

SMA nMMM )1(1 −−− +++=

History Prophet

Dummy predictor for strategy testing Predicts every point with its future value Imitates a “prophet” knowing the future Delivers 100% of profitable trades Explicitly uses forward info Not suitable for practical trading Analog of “Maximum Profit System”

19

Maximum Profit Simulation

20

Extensible algorithmic API

Modular algorithmic server Extendable calculation engine Real-time C++ core framework Open standard development API Universal DLL interface Compatibility with development tools Multiple sample models

21

22

Pioneers in the fractal exploration of financial markets

Trading futures and options involves the risk of loss. You should consider carefully whether futures or options are appropriate to your financial situation. You must review the customer account agreement and risk disclosure prior to establishing an account. Only risk capital should be used when trading futures or options. Investors could lose more than their initial investment. Past results are not necessarily indicative of futures results. The risk of loss in trading futures or options can be substantial, carefully consider the inherent risks of such an investment in light of your financial condition. Information contained, viewed, sent or attached is considered a solicitation for business.

Quant Trade, LLC has been a Commodity Futures Trading Commission (CFTC) registered Commodity Trading Advisor (CTA) since September 4, 2007 and a member of the National Futures Association (NFA).

Copyright @ 2012 Quant Trade, LLC. All rights reserved. No part of the materials including graphics or logos, available in this Web site may be copied, reproduced, translated or reduced to any electronic medium or machine-readable form, in whole or in part without written permission.

2 N Riverside Plaza Suite 2325 Chicago, Illinois 60606 Quant Trade LLC (872) 225-2110