quarterly article on emerging islamic capital market …

TRANSCRIPT

BUSINESS AND ECONOMIC NEWSFLASH

URDU GLOSSARY

MARKETS IN REVIEW

QUOTES AND JOKES

TERMS OF THE MONTH

QUARTERLY

Jan-Mar 2021

Your Gateway to Careers in Financial Markets

Institute of Financial Markets of Pakistan

Address: Building 9-A, 2nd Floor,

P.E.C.H.S Block No. 6, Shahrah-e-Faisal Karachi.

Tel: +92 (21) 34540843-44

MESSAGE FROM THE CEO

INTRODUCTION TO THE INSTITUTE

IFMP ACTIVITIES

INDUSTRY PROFESSIONALS’ INTERVIEW

FEATURED ARTICLE

ARTICLE BY IFMP MEMBER

TERMS OF THE MONTH

BUSINESS AND ECONOMIC NEWSFLASH

URDU GLOSSARY

FEEDBACKS

MARKETS IN REVIEW

ARTICLE ON

EMERGING ISLAMIC CAPITAL

MARKET IN PAKISTAN

00 CONTENT

Message from the CEO

Introduction to the Institute

IFMP Activities

Article by IFMP Member

Urdu Glossary

Feedbacks

Business and Economic Newsflash (Local & International)

Page: 1

Page: 2

Page: 27

www.ifmp.org.pk 92 (21) 34540843-44 [email protected]

Terms of the Quarter

Markets in Review

Featured Article

Page: 3

Regulatory Updates

Investment Quotes

Industry Professionals’ Interview Page: 5

Page: 7

Page: 19

Page: 22

Page: 23

Page: 31

Page: 35

Page: 36

Page: 38

Page: 37

IFMP Upcoming Activities Page: 4

01

Message from the Chief Executive Officer

◊ FIRST QUARTERLY 2021

he last few years have seen a rapid growth in size, quality and sophistication of finan-

cial markets, because of changes in the policy and regulatory environment, the entre-

preneurial initiatives of individuals and institutions, and the availability of trained man-

power. The continuing growth of financial markets is further adding to the demand for

well-trained professionals.

Institute of Financial Markets of Pakistan is dedicated to the professional development of

financial markets and research on financial markets as well as the well being of financial

markets by educating the professionals about the norms and ethics being practiced in the

markets. IFMP has had a pioneering role in meeting the demand for educated manpower.

It is Pakistan's first specialized institution devoted to the education and updating of

knowledge of manpower for financial markets. It will provide high-quality educational

standards for all types of financial market participants; investors, brokers, mutual funds,

investment banks and policy makers.

The Institute's main activities are (1) Licensing the professionals working in the financial

markets by certifications. The institute’s key responsibility is to educate the professionals

working in different financial markets of Pakistan through examining their knowledge in

their relevant field of work; (2) Studying the latest developments in the financial markets

in order to discover whether there is such a thing as an ideal market economy; and (3)

Contributing to the development of financial markets in Pakistan. By means of these three

activities the Institute seeks to communicate its ideas to the audience both at home and

overseas. The Institute's research is intended, first and foremost, to be neutral, profes-

sional and practical. Rooted in practice, it aims to contribute to the healthy development

of Pakistani financial markets as well as to related policies by conducting neutral and pro-

fessional studies of how these markets and the financial system are regulated and orga-

nized and how they perform.

The economy is changing all the time. The Institute hopes that, by responding to these

changes positively, it can contribute to the dynamic development of the country's finan-

cial markets as well as of the economy itself.

T

02

Introduction to the Institute

◊ FIRST QUARTERLY 2021

The Institute of Financial Markets of Pakistan (IFMP), Pakistan’s first

securities market institute, has been established as a permanent platform to de-velop quality human capital, meet the emerging professional knowledge needs of

financial markets and create standards among market professionals. The Insti-tute has been envisioned to conduct various licensing examinations leading to

certifications for different segments of the financial markets. IFMP develops a pool of trained and certified professionals, skilled not only to deal in convention-

al instruments but also to trade in new and complex financial market products.

◊ FEE STRUCTURE ◊

Candidate Registration Fee Rs.10,000

Examination Registration Fee Rs.7,000

Membership Fee (Annual) Rs.5,000

Study Guide (Hard Copy) Rs.800

◊ EXAMINATION SCHEDULE ◊

Sunday, May 30, 2021

Sunday, July 25, 2021

Sunday, September 26, 2021

PROGRAMMES

LICENSING CERTIFICATIONS INSURANCE CERTIFICATIONS SPECIALIZED CERTIFICATIONS

Fundamentals of Capital Markets Certifi-

cation

Pakistan’s Market Regulations Certifica-

tion

Stock Brokers Certification

Mutual Funds Distributors Certification

Commodity Brokers Certification

Financial Analysts Certification

Mutual Funds Basic Certification

Securities and Futures Advisors’ Certifica-

tion Programme (Basic and Core Modules)

General Takaful Agents Certifi-

cation

Family Takaful Agents

Certification

Life Insurance Agents

Certification

Non-Life Insurance Agents Certi-

fication

Bancassurance Certification

Bancatakaful Certification

Authorized Surveying Officers

Certification

Financial Derivative Traders Certification

Compliance Officers Certification

Clearing and Settlement Operations Certification

Risk Management Certification

Capital Budgeting and Corporate Finance

Certification

Investment Banking and Analysis Certification

Islamic Finance Certification

Fixed Income Certification

AML/CFT Certification

◊ FIRST QUARTERLY 2021 IFMP

IFMP Activities 03

Date Program Trainer Dura-

tion

January, 2021 Virtual Accounting & Bookkeeping Mr. Riaz Ahmed & Mr. Muhammad Has-

san

1 Month

23rd January, 2021 AML/CFT Certification Training (4th batch) Sumera Baloch - Additional Director

FMU, Govt. of Pakistan

6 Hours

February, 2021 Virtual Accounting & Bookkeeping Mr. Muhammad Hassan 1 Month

9th February, 2021 Microsoft Power BI Mr. Imran Bukhari 3 Hours

March, 2021 Virtual Accounting & Bookkeeping Mr. Amin Ahsan & Mr. Muhammad Has-

san

1 Month

February & March,

2021

CHRP Diploma Multiple 2 Months

4th March 2021 Leading Effective Virtual Meetings M. Asim Ali 1 Hour

9th March 2021 Role of Women in Pakistan's Financial Markets Mobashar Sadik, Mashmooma Majeed -

MUFAP, Sarwat Ahson - CFA Society,

Sadaf Shabbir - Awwal Modaraba, Zun-

aira Saqib - Merafuture.pk

1 Hour

10th March 2021 Equity Valuation using Fundamental Analysis Ap-

proach

Jabran Ata - CFA 1 Hour

12th March, 2021 Detecting and metigating the risk of TBML Salim Thobani - Head of Trade Compli-

ance Meezan Bank

3 Hours

20th March, 2021 AML/CFT Certification Training (5th batch) Sumera Baloch - Additional Director

FMU, Govt. of Pakistan

4 Hours

25th March, 2021 SECP AML/CFT Regulations 2020 M USMAN - ACA 3 Hours

27th March 2021 Taxation of Salaried Individuals Mudassar Farooq 1 Hour

◊ FIRST QUARTERLY 2021 IFMP

IFMP Upcoming Activities 04

Date Program Duration Type of Event

6th May, 2021 Building the savings and pension culture for Mutual Funds 1 Hour CPD

5th June, 2021 Understanding the requirements of fair dealing as an equity sales person (Stock Bro-kers)

1 Hour CPD

7th July, 2021 Understanding the risks associated with insider trading (Stock Brokers) 1 Hour CPD

15th July, 2021 Accounting for non Accounting Professionals 3 Hours Paid Train-ing

29th July, 20201 Mutual Fund Basic Certification Training 2 Hours Paid Train-ing

7th Aug, 2021 Capital Market Regulatory Developments 1 Hour CPD

14th August 2021 IFRS 9 & 16 3 Hours Paid Train-ing

26th August, 2021 Managing Sanctions Risk 3 Hours Paid Train-ing

8th Sep, 2021 The role of Behavioral Finance in wealth management (Mutual Funds) 1 Hour CPD

16th September, 2020

SECP Revised Regulations 2020 2 Hours Paid Train-ing

30th September, 2021

Power BI Analytics & Visualization 10 Hours Paid Train-ing

9th Oct, 2021 Complying with brokers code of conduct; ensuring client’s assets and confidentiality of information (Stock Brokers)

1 Hour CPD

14th October 2021 Detecting and metigating the risk of TBML 3 Hours Paid Train-ing

28th October 2021 Taxation of Salaried Individuals 2 Hours Paid Train-ing

13th Nov, 2021 NBFC Regulatory Developments 1 Hour CPD

18th November 2021

Financial Risk Management 3 Hours Paid Train-ing

25th November, 2021

Microsoft Excel 10 Hours Paid Train-ing

15th Dec, 2021 Leadership & Team management Skills for Financial Services Professionals (All Indus-try Professionals)

1 Hour CPD

16th December, 2021

Budgeting and Control 3 Hours Paid Train-ing

05

◊ FIRST QUARTERLY 2021 IFMP

Dr. Amjad Waheed holds a Doctorate in Business Administration with a major in Investments

and Finance from Southern Illinois University, USA and is also a Chartered Financial Analyst

(CFA). Since inception of the company (fifteen years ago), Dr. Amjad Waheed is the CEO of NBP

Fund Management Limited (NBP Funds). Dr. Amjad has served on the Board of various compa-

nies including Bank Islami Pakistan, Siemens (Pakistan) Engineering Co.Ltd., Nishat Mills Ltd.,

PICIC, Askari Bank Ltd., Millat Tractors Ltd., Fauji Fertilizer Company Ltd., Pakistan Tobacco

Company Ltd., Parke-Davis & Company Ltd., Treet Corporation Ltd., Atlas Investment Bank Ltd., Gul Ahmed Textile

Mills Ltd., Bata Pakistan Ltd. and Mehran Sugar Mills Ltd. among others. He has also served as Chairman, Mutual

Funds Association of Pakistan (MUFAP).

Tell us about your journey of becoming a CEO.

Initially, I wanted to become a Doctor but then I didn’t have enough marks so I decided to do B.Com from Hailey

College of Commerce Lahore. After completing my B.Com I went to the US to do my MBA and afterwards I decided

to do my Doctorate in Finance and Investments. After completing my PhD, I was an Assistant professor in finance at

Tennessee State University, USA for three years. I came back to Pakistan where I first worked in Lahore with ABN

Amro Equities then moved to NIT in Karachi. I was head of Investments of NIT for about three years. Then I went to

Saudi Arabia Riyadh Bank, where I worked for five years managing the equities mutual fund business which was

about $8 billion. And after that, I came back to Pakistan about 15 years ago and started this company NBP Funds

and today we are Ma’shaa’Allah the largest AMC in Pakistan. We are managing about 80 billion rupees and we have

an AM1 rating which is the highest rating offered to any asset management company. So basically it has been a good

journey where there have been challenges, one of the key challenges was the Macroeconomic environment in Paki-

stan which is pretty volatile and because of that stock market you know goes up and it goes down more than you

know it should, and since we managed stock funds in addition to income funds and Islamic funds and pension

funds. And if the market goes down it impacts on investors’ returns for those who are holding stock funds.

What coaching tips will you give to other CEOs to stay skilful at the top of the heap?

I think the biggest tip of all is ownership. I think a lot of professionals even whether there are CEOs or senior man-

agement they do not take ownership of the company. When you are working for a company you are getting a salary,

you are getting bonuses, you need to start thinking that this is my company and when you start thinking like that

then you obviously start being more responsible. Next thing which is more important is Entrepreneurship, you

need to have a mind of an entrepreneur, how to grow the business, how to reward your people and how to hire

good people, so a lot of entrepreneurship skills are required which are generally missing in high salaried profes-

sionals. And the third thing is to keep yourself updated of recent developments and fourth thing is I think for the

CEO to hire the right people is the very important job, it makes the life easy if you have the right people around you.

What do you think is an effective way to measure the success of a CEO?

Well I think ultimately it has to be output and the reputation of a company. The most important thing for a CEO is to

ensure reputational risk is mitigated with extent possible. Obviously growing business is always the dream of the

CEO and also working in the interest of all the stakeholders is important. In our case we have shareholders obvious-

ly, but we also have investors (about a hundred thousand of them), they are also stakeholders so basically it is a

work in the interest of all the stakeholders and government is one of the stakeholders.

Interview of dr. amjad waheed, CEO - NBP Funds

What was the moment that shaped your career as a CEO?

One moment that shaped my career as CEO is when I was in Saudi Arabia and I was getting a good salary, I had a

good job and I was the head of equity mutual funds, I get a call from NBP Funds which was just starting its opera-

tions and I had to make the decision whether I took up the big salary cut to come back to Pakistan, and I decided to

come back and it proved to be the right decision maybe not in the monetary terms but as overall satisfaction.

What skills/traits do you think to raise the bar as a CEO?

I think professional skills obviously are the requirement no questions about it whether you are a chartered account-

ant, a finance major or sales person and these skills are required from a CEO but I think biggest skill for a CEO is the

entrepreneurship and you need to think like a businessman because it is you running a business and you must own

it, think long term, reward your people based on their performance, make decisions based on market forces, antici-

pate things, you think of future products, statutory developments, grow your business, future expansion and im-

provement of products and services for your clients. In all these skills entrepreneurship is the most important skill

for raising the bar as CEOs.

How would you describe the importance of systems for gathering feedback from lower level employees?

Obviously employees are the key ingredient you know for especially for the service sector business and so it is very

important to know how your employees think, we carry out employee engagement survey every year to find out

what all the employees think about the company. We found the gaps, for example one of the key gaps they identified

was work and family balance, because of the late hours and they did not get much time to spend with the family so

we tried to improve that. We are trying to ensure that people leave the office at a reasonable time and are not stuck

here for late hours. I think it is important to get feedback from employees so you can get to know their problems

and if they are happy they will perform.

How would you describe the importance of staying humble with employees as a CEO?

I think being humble are the basic characteristics of the CEO if you are not humble if you are arrogant you will any

way mess up, some way your business will suffer, so I think all good CEOs should be humble.

How would you describe the importance of sharing your vision with the lower level employees as a CEO?

Very important, we use to have more physical meeting before Covid and especially with the large sales force about

800-900 hundred people. I used to travel to different cities but now things have changed and we are doing most of

the meetings online as obviously it is important to engage with all the employees and share your thoughts with

them and get feedback from them.

How would you describe the importance of Building a Continuous Learning Culture in an organization?

Very important, we ensure at it all levels, our HR department ensures that employees are getting the proper training

and in addition to the professional skills they also need to learn the managerial skills as eventually they will go to

the managerial positions. So we keep on sending people to different seminars and workshops to upgrade their skills.

06

◊ FIRST QUARTERLY 2021 IFMP

interview

07

◊ FIRST QUARTERLY 2021 IFMP

Introduction: The Islamic capital market is growing as the Islamic banking industry has become more sophisticated and assets are being trans-

ferred from the banking industry to the capital markets. This came about when in 1980s and 1990s, Islamic banks were successfully

able to mobilize dormant savings into investments through their Shariah compliant financial instruments. The development of shari-

ah compliant tradable securities formed the basis for the Securities markets.

Capital Market A capital market is a financial market in which long-term debt (over a year) or equity-backed securities are bought and sold, in con-

trast to a money market where short-term debt is bought and sold.

Are the Capital Market and the Money Market are same?

No, there is the difference between capital Market and Money Market. The money markets are used for the raising of short-term fi-

nance, sometimes for loans that are expected to be paid back as early as overnight. In contrast, the "capital markets" are used for the

raising of long-term finance, such as the purchase of shares/equities, or for loans that are not expected to be fully paid back for at

least a year.

Do we classify regular bank lending as a capital market transaction?

Regular bank lending is not usually classed as a capital market transaction, even when loans are extended for a period longer than a

year due to the following reasons,

First, regular bank loans are not securitized (i.e. they do not take the form of a resalable security like a share or bond that can be

traded on the markets).

Second, lending from banks is more heavily regulated than capital market lending.

Third, bank depositors tend to be more risk-averse than capital market investors.

Capital markets recognize and drive capital to the best ideas and enterprises. Coupled with the free flow of capital, innovation is an

integral component to a country for supporting job creation, economic development and prosperity. Markets facilitate the transfer of

funds from those who seek a return on their assets to those who need capital and credit to expand.

Islamic Capital Market Islamic capital market is a market where all financial activities are shariah compliant. The concept can also refer to the investments

that are permissible under Sharia.

The Islamic Capital Market is an integral part of Islamic Financial System where Shariah compliant financial assets are transacted. It

plays a pivotal role in the growth of Islamic Financial Institutions.

The backbone of Islamic Capital Market are the following Shariah principles. Prohibits Paying or charging an interest

Do not Invest in businesses involved in prohibited activities

Prohibits Speculation (maisir)

Prohibits Gambling and Ambiguity (gharar)

Ensure Material finality of the transaction

FEATURED ARTICLE: EMERGING ISLAMIC

CAPITAL MARKET IN PAKISTAN

08

◊ FIRST QUARTERLY 2021 IFMP

Profit/loss sharing

The Islamic Capital Market functions as a parallel market to the conventional capital market for capital seekers and providers. The

Islamic Capital Market attracts funds from domestic as well as international sources.

Today, various capital market products are available such as Shariah-compliant securities, sukuk, Islamic unit trusts, Islamic Real

Estate Investment Trusts etc.

Reasons for the growth of Islamic capital market There are several reasons for the faster growth of the Islamic capital Markets. Islamic financial and insurance institutions had sur-

plus funds after providing for statutory reserves and financing for clients. The unavailability of efficient Shariah compliant financial

products on a liquid Islamic capital market was making Islamic financial and insurance institutions operations less efficient.

In addition to this, prohibition of interest based loans, absence of money market and greater emphasis on equity investment also

meant that there had to be a greater reliance upon securities markets to mobilize funds. Shariah compliant financial instruments and

products is at various stages in different countries. It offers many different types of products, which include:

Shariah compliant stocks,

Islamic bonds, Islamic funds,

Islamic derivatives,

Structured products and

Islamic risk management products

Thus Shariah compliant products have increased the ownership base in the society and are regarded as a new asset class by the con-

ventional investors. They have also grown to represent an alternative investment philosophy and are progressing parallel to the con-

ventional ethical Stocks and shares. They are open to non-Muslims investors who wish to invest in socially responsible investment.

Indices of Islamic finance market There are also a number of indices that track the performances of Islamic finance markets such as

Dow Jones Islamic Market Indices (DJIMI)

Standard and Poor’s Shariah Compliant Indices

Morgan Stanley Capital Index (MSCI)

FTSE global Islamic Index Series etc.

Prominent rating agencies have also entered the markets creating their own rating methodologies for shariah compliant products.

The DJIMI tracks performance for diverse regions such as Asia, BRIC, GCC, and globally emerging markets. It also has an “index on

Islamic Market sustainability. This index outperformed the conventional market during 2007-2008 by a small margin. On the other

hand, indices such as MSCI have also shown clear superiority of the performance of Islamic funds during the above period.

Regulatory Organization in Islamic capital Market The rise of Shariah compliant stock exchanges necessitates a supportive infrastructure for efficient operation. There are some Super-

visory and self-regulatory organizations established such as

Islamic Financial Services Board

Accounting Auditing Organization for Islamic Institutions

FEATURED ARTICLE: EMERGING ISLAMIC

CAPITAL MARKET IN PAKISTAN

09

◊ FIRST QUARTERLY 2021 IFMP

International Islamic Financial Market and

Islamic International Rating Agency

The establishment of key supervisory and self-regulatory organizations has facilitated the formulation of legal and regulatory stand-

ards. It has also galvanized the efforts to standardize the global Islamic finance market.

The International Organization of Securities Commissions (IOSCO) has also acknowledged the growing importance of Shariah com-

pliant securities markets in the global financial market. IOSCO established an Islamic Capital Market task force to assess the extent of

development and identify the gaps in the legal and regulatory framework. Similarly, international Islamic institutions such as the Is-

lamic Research and Training Institution have also undertaken significant research projects to track new developments and incorpo-

rate IOSCO standards in formulating policies. Shariah is set of ethical principles and prohibitions which are applied in the context of

Islamic banking, securities markets, financial institutions and financial products.

Global Market Perspective The Shariah compliant securities market is at an important juncture of becoming a vibrant market place after the last financial crisis.

The growth indicates that capital seekers and providers are becoming increasingly comfortable with Shariah compliant instruments

for financing and investment tools. It also provides an excellent opportunity to tap into liquidity rich Islamic countries. The amount

of funds mobilized by the Shariah compliant instruments and the current demand for the Shariah compliant financial products in

Middle East, South East Asia, North Africa and Western world has reached a critical threshold to support a well-functioning capital

market. This is also evident from the estimates of total market capitalization of Dow Jones Islamic Market World index which has

reached to 5,527.28 USD as of March 30, 2021.

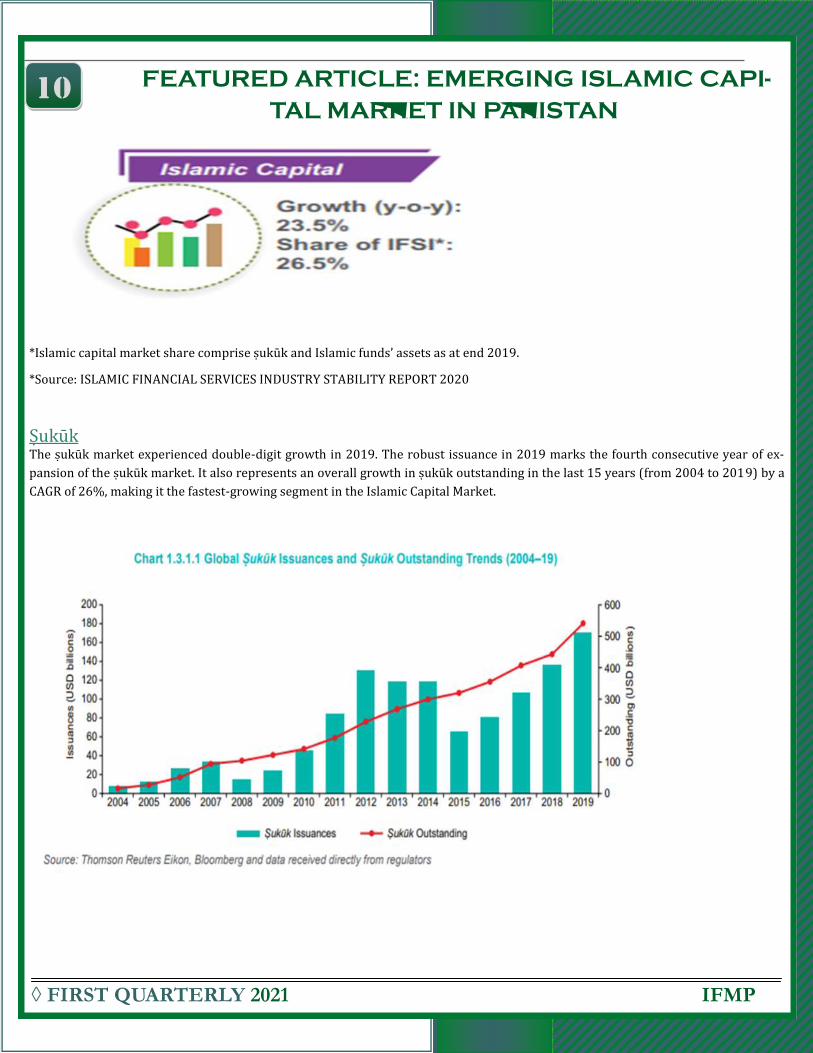

A glimpse of global Islamic finance shown in the chart below:

The Islamic capital markets marked a record high in 2019 in terms of volume of annual s uku k issuances. Both sukuk and Islamic

funds entered a renewed and stronger growth phase in 2019 after a more subdued, albeit consistent, growth rate in recent years.

Several new trends are emerging across the sector. The Islamic capital markets continue to be the most rapidly growing segment in

the IFSI, posting double-digit growth across all three sub-segments .

FEATURED ARTICLE: EMERGING ISLAMIC

CAPITAL MARKET IN PAKISTAN

10

◊ FIRST QUARTERLY 2021 IFMP

*Islamic capital market share comprise s uku k and Islamic funds’ assets as at end 2019.

*Source: ISLAMIC FINANCIAL SERVICES INDUSTRY STABILITY REPORT 2020

S uku k The s uku k market experienced double-digit growth in 2019. The robust issuance in 2019 marks the fourth consecutive year of ex-

pansion of the s uku k market. It also represents an overall growth in s uku k outstanding in the last 15 years (from 2004 to 2019) by a

CAGR of 26%, making it the fastest-growing segment in the Islamic Capital Market.

FEATURED ARTICLE: EMERGING ISLAMIC CAPI-

TAL MARKET IN PAKISTAN

11

◊ FIRST QUARTERLY 2021 IFMP

Islamic Funds Islamic funds demonstrated positive growth in terms of the total value of assets under management, recovering from the slower

growth observed in recent years. The growth in total value of AuM may have been supported by the strong growth in equity markets,

as well as by an increase in average size of funds, while the total number of Islamic funds increased from 1,489 in 2018 to 1,545 in

2019.

Islamic Equities Islamic equity markets rebounded in 2019, posting the strongest performance since the GFC in 2009. Following weak returns in

2018 due to a steep sell-off in December, equity markets recovered in 2019, with the S&P Global 1200 Shariah Index gaining 32.6%,

while its conventional comparator, the S&P Global 1200 Index, gained 28.2%. Despite transient market volatility during the year due

to fears of a global economic slowdown, a disruptive trade war or a hard Brexit, and the volatility of oil prices, global equity markets

ended 2019 at a record high, helped by rate cuts by central banks which alleviated recession fears along with easing of trade tensions

towards the end of the year.

FEATURED ARTICLE: EMERGING ISLAMIC CAPI-

TAL MARKET IN PAKISTAN

12

◊ FIRST QUARTERLY 2021 IFMP

Growth Drivers in the Islamic Capital Market Following are the growth drivers in the Islamic Capital Market

Regulatory capital issuances that will continue to be a significant driver of sukuk issuances.

Utilization of financial technologies for issuance of sukuk, as well as growth in other FinTech-based models to provide Islamic

Capital Market products and services.

Sukuk market growth propelled by sovereign issuers for fiscal deficit financing needs and the issuance of short-term sukuk for

liquidity management.

Downside risks to the positive growth outlook include the unknown magnitude and duration of the COVID-19 outbreak, a global

economic downturn, re-escalation of trade tensions, or materialization of other lingering global risks.

Pakistani Capital Markets The Securities and Exchange Commission of Pakistan (SECP, or the Commission) accomplished great jobs, overdue for many years,

during 2017.

Firstly, keeping in view the changes in the corporate business environment, impact of globalization and technology, and evolution of

Islamic financial markets, it revised the Companies Ordinance, 1984 and promulgated the Companies Act, 2017 (the Act) on May 30,

2017. For the first time ever, the concept of Shariah-compliant companies and securities has been given in the Act. In addition to sha-

riah-compliant companies and securities, the Companies Act 2017 has provisions for Shariah compliance, shariah advisory, and Sha-

riah audit.

Secondly, the Commission notified the Shariah Advisors Regulations, 2017 (SAR, The Regulations) on 15th November, 2017. This

notification is recognition of Shariah Advisory function as a respectable profession, and Shariah Advisors (SA) as formal profession-

als by the leading Regulator of corporate sector and capital markets. SECP has set the Content from this work is copyrighted by Jour-

nal of Islamic Business and Management, which permits restricted commercial use, distribution and reproduction in any medium

under a written permission. Users may print articles for educational and research uses only, provided the original author and source

are credited in the form of a proper scientific referencing. 150 Strengthening the Islamic capital market: - Editorial 2017 stage for the

Shariah Advisors who would now be easily approachable within and outside Pakistan by having their name on the website of the

SECP. The Shariah Professionals of Pakistan have been provided with this unique opportunity to highlight themselves across the

globe through the platform provided by the capital market Regulator.

Financial Instruments in Islamic Capital Markets Islamic capital markets only recognize financial products that are compliant with Islamic rules and regulations.

Shariah regulates financial instruments as part of its overall philosophy of investor protection. It regards financial instruments as

tools to facilitate exchange through its contractual structure leading to natural equilibrium and economic development. Shariah re-

gards the fulfillment of these basic purposes of contract an integral and mandatory part of its ethics.

FEATURED ARTICLE: EMERGING ISLAMIC CAPI-

TAL MARKET IN PAKISTAN

13

◊ FIRST QUARTERLY 2021 IFMP

Equity Based Shariah Compliant Structures The strict prohibition of interest dictates that individual and institutional investors are reliant upon equity as opposed to debt financ-

ing. Equity financing products in Islamic finance are based upon partnership and profit and loss sharing (PLS) modes similar to ven-

ture capitalism. The cost of financing through the contractual modes directly links returns to the performance of the investment, pro-

portionate to the risk undertaken.

It is argued that profit and loss sharing and risk undertaking features promote fairness. This is in contrast to a fixed rate of interest

accrued on debt which does not have any link with the return on the real investment and is viewed as oppressive.

By employing equity financing based on the PLS structure and shirkah, Shariah promotes balance of power, mutual dependence

among the financiers and entrepreneurs. In conventional banking terminology, these instruments are referred to as a trustee project

and joint venture project finance.

The main modes of Shariah compliant equity financing are as follows:

Mudhrabah

Musharakah

Mudhrabah (Profit-Sharing Dormant Partnership) Mudhrabah is one of the most important principles of the Shariah investment. There could be two or more parties involved. One of

the parties involved is the capital owner (Rab-al-Mal) and the other one act as an investment manager or entrepreneur (Mudarib).

The capital owner invests the money without becoming involved in the actual day to day running of the project. In the case of any

losses, its liability is limited to the capital invested.

On the other hand, the entrepreneur solely controls the entire project and provides professional, technical, managerial expertise in

making the project a success. His liability is limited to the loss of opportunity, time and effort unless loss is incurred deliberately or

negligently. The role of investment manager is fiduciary and honesty and diligence is expected of him.

The profit from the project is distributed in accordance with the pre-arranged ratio agreed in advance between the investor and the

entrepreneur. The ratio may depend on the risks assumed by the capital and the endeavors and contributions made by the entrepre-

neurs. It may be 50:50 or 70:30 ratio. One of the distinguishing features of the Mudhrabah contract is that the lender is not guaran-

teed any pre-arranged fixed amount on its investment. The profit is distributed once the success of the project is proven ex-post.

Musharakah (Risk/Profit-sharing Partnership) Musharakah is Arabic word which means sharing. In the business context, it represents Islamic financial instruments that are based

on profit and loss sharing and risk sharing partnership techniques with comprehensive effects on production and distribution. It is a

partnership contract (also referred to as shirkah) between two parties: the investor and the entrepreneur. It resembles a western

style joint venture, partnership financing or private equity financing. Both parties contribute equity capital and assets, technical and

managerial expertise to an agreed proportion. They jointly have the right to manage the day to day affairs of the business except

when one party voluntarily waives its rights to manage. This is in contrast to Mudhrabah where one party provides the funds and the

other contributes through their special business skills.

Entitlement to profit depends upon the risk assumed and the commercial worth of the contributions by each party but not in propor-

tion to the capital invested. The entrepreneur or investment manager may be able to negotiate a higher share of profit depending on

greater contributions or efforts as compared to the investor. This may also be possible if the bank decides to waive its rights of man-

agement and entrust supervision solely to the entrepreneur.

On the other hand, if the business accrues losses, both the parties share liability for the losses in proportion to the contribution of

financial capital. This distinguishes the Musharakah from Mudhrabah where the investor is liable for all loses with his entire contri-

bution and entrepreneur may only loose his efforts for the business venture.

FEATURED ARTICLE: EMERGING ISLAMIC CAPI-

TAL MARKET IN PAKISTAN

14

◊ FIRST QUARTERLY 2021 IFMP

Debt Based Shariah Compliant Financing Islamic finance acknowledges the importance of debt for investment, corporate and government borrowing. It can facilitate creation

of employment and prosperity leading to economic growth if utilized in a productive way. Islamic finance does not prohibit the debt

financing instruments as long as it complies with Shariah requirements and pre-conditions. Debt instruments follow different types

of Shariah compliant mode, which are as follows.

• Murabaha

• Deferred Payment (Bai Bithaman-Ajil)

• Sukuk

Murabaha The Murabaha structure is analogous to the concept of purchase finance. Islamic Financial Institutions (IFI) uses this model to pur-

chase goods, commodities and assets for their (individual and corporate) clients and sell them at a mark-up price. Individuals may

use Murabaha to finance real estate and automobile purchases whereas corporate clients may use this model to obtain financing for

raw materials or their fixed assets such as machinery and equipment. It is also referred to as mark-up sale, cost plus profit or de-

ferred payment sale.

Deferred Payment (Bai Bithaman-Ajil) Bai Bithamin Ajil has features similar to Murabaha. It is a sale transaction. The Islamic Financial Institution (IFI) purchases the assets

for resale to the buyer at an increased price as agreed in advance by the both the parties involved. The difference with the Murabaha

lies with the fact that the seller is not obligated to disclose the mark up included in the selling price and this mode of financing can be

used for long term financing. The payment by the purchaser is made sometimes after the delivery of the assets or commodity.

Sukuk Saak is singular of Sukuk, which means investment title or certificates. The modern concept of sukuk originated from the need to de-

vise riba free instruments in the Islamic capital market.

A sukuk is a sharia-compliant bond-like instruments used in Islamic finance. Sukuk involves a direct asset ownership interest, while

bonds are indirect interest-bearing debt obligations.

The implication of the principle of prohibition of riba and the prohibition on trading of debt meant that conventional fixed interest

securities such as conventional bills, bonds and notes were not an acceptable form of investment instruments in the Islamic Capital

Market. The innovation of Shariah-compliant debt securities that linked the return with the performance of underlying real assets

revolutionized the Islamic capital market.

Shariah-Compliant Securities Shariah-compliant securities are listed which have been classified as Shariah permissible for investment, based on the company’s

compliance with Shariah principles in terms of its primary business and investment activities.

Islamic Unit Trust Funds Islamic unit trust funds are a collective investment scheme that offers investors the opportunity to invest in a diversified portfolio of

Shariah-compliant securities, fixed income securities and money market instruments.

Islamic Real Estate Investment Trusts Islamic real estate investment trusts or I-REITs are collective investment vehicles (typically in the form of trust funds) that pool mon-

ey from investors and use the pooled capital to buy, manage and sell real estate. I-REITs provide an investment opportunity for those

who wish to invest in real estate through Shariah-compliant capital market instruments.

FEATURED ARTICLE: EMERGING ISLAMIC CAPI-

TAL MARKET IN PAKISTAN

15

◊ FIRST QUARTERLY 2021 IFMP

Hedging and Risk Management Instruments in Islamic Capital Market Risk management refers to the practice of identifying potential risks in advance, analyzing them and taking precautionary steps to

reduce/curb the risk.

Traders, producers, investors and conventional financial institutions are generally faced with market and financial risks in their day-

to-day operation. Market risk originates from price increase risk, regulatory risk, operational risk, commodity price risk, human re-

sources risk, legal and product risks. Financial risk refers to credit risk, liquidity risk, currency risk, and settlement risk. Western fi-

nanciers innovates financial instruments to transfer and diversify the risk to various participants of the financial exchange in the field

of science and enterprise

The tools commonly used to hedge against the above mentioned risks are referred to as derivative instruments

Islamic concept of risk management and products should effectively comply with the following three conditions.

The nature of risk to be mitigated should originate from Shariah compliant transactions as opposed to non- Shariah compliant

transactions.

Hedging instruments should also comply with the Shariah compliant risk management principles, modes, structure and con-

tracts. Invariably, it means that noble means be employed to achieve the noble ends.

The products should only minimize or diversify the risk as opposed to commoditize it into a market of its own. This would be

promoting speculation and gambling as a source of earning money.

The Islamic concept of hedging should also promote the overall objective of promoting an equitable system of distributive justice and

the common good. In the context of the allocation of risk, distributive justice refers to the willingness and capability of the various

parties to assume risk in promoting general welfare and avoiding adverse effects on the financial system. It promotes generation of

utility and avoidance of economic waste and financial losses. Avoidance from financial loss is assigned a higher priority than the ex-

pectations of large profit in Shariah.

The achievements of the above objectives are heavily dependent upon the creative design of Islamic derivative instruments and the

mechanics of the market.

Some products may be rejected in different countries because of difference in school of thought

Derivatives Derivatives refer to financial instruments whose value depends upon the underlying asset, equity, currency and commodities. Some

of the common derivatives are futures, swaps, options etc. The popular view is that derivative instruments are not permitted in Sha-

riah. However, financial engineering has made it possible to devise Shariah compliant derivatives such as arboun, wa’ad and forward

contracts based on Salam Risk diversification by derivatives has improved prudential regulation, liquidity management and en-

hanced financial stability. Similarly, in the evolution of Islamic finance, risk has to be managed to ensure stable growth. Thus risk

hedging instruments in derivative market give investor a wider choice between the risks they want to take.

The non-Shariah elements in the contractual structures of most conventional derivative products are set out as follows,

Derivative products defer payment and delivery of goods

Parties lack ownership or possession of underlying items in derivative transactions

Futures, options, swaps facilitate excessive and abusive speculation (maisir)

The Shariah compliant contractual structures and modes used on its own or in combination as the building blocks are as follows:

Bay-Salam

Istisna

FEATURED ARTICLE: EMERGING ISLAMIC CAPI-

TAL MARKET IN PAKISTAN

16

◊ FIRST QUARTERLY 2021 IFMP

Bay-Salam (Advanced Purchase) The instrument has been used to avoid riba-based transactions as an alternative form of contracting. Although the general principle

of Shariah prohibited sales of any commodity which was not in physical or constructive possession of the seller, as it amounted to

gharar, the Salam was permitted as an exception.

Salam was practiced in Medina to purchase fruit, wheat, barley etc. with delivery in one, two or three years by making full advance

payments. Upon the Prophet’s arrival in Medina in 622 CE,

He added new features to the sale transaction by making it obligatory to specify the quality and quantity of the commodity (weight

and measure), the date and time of the delivery and definitive terms in order to avoid future dispute.

The rationale to allow this sale structure was to mitigate against the hardship for small farmers who struggled to obtain the liquidity

required to pay for the expense incurred during the growing of the crop season.

Salam transaction can only take place in commodities where it is possible to define the quantity and quality precisely. It is not possi-

ble to particularize the product of specific tree, orchard, farm or field for Salam transaction.

The structure based on Salam transaction can be used as a mode of Shariah compliant debt financing for farmers and traders in agri-

cultural sector. The price is agreed in advance and is generally lower than the spot rate and this may amount to a profit for the mod-

ern IFI. However, IFI may want to insist on a guarantee or security in order to ensure that the seller complies with the Salam contract

and delivers on time.

Having purchased the commodity once, IFI can resell the commodity by entering into another contract completely independent of the

first. This is referred to as parallel Salam. In the first contract, IFI is purchasing and in the second contract, IFI is selling the same

commodity. It is mandatory that both contracts should be independent and must not be reliant upon the specific performance of each

other.

Forward contract Vs. Bay Salam The similarity of Salam with forward contracts from conventional finance is unmistakable. However, in reality there are many differ-

ences in the structure of both transactions.

A conventional forward contract allows the payment of price and delivery of the object at a specified future date. The net profit or

loss by the parties over the life of the contract is also settled on the delivery date. These are non-standardized contracts traded on

OTC market.

In contrast to this, Salam requires full payment of price in advance. Classical Shariah jurists take the view that deferring the payment

of price and delivery of goods bring in an element of gharar and parties may exploit each other. Similarly, partial payment is also not

permissible as it amount to reliance of credit and is prohibited.

Moreover, the resale of the goods without receipt of the goods curbs speculative tendencies. In this context, forward contracts are

very much similar to futures contracts, which are standardized exchange traded contracts.

It is observed from the foregoing discussion that the permissibility of the deferment of both price and delivery of objects may create

an opportunity for finance professionals to synthesize forbidden forward contracts.

The recent development in the form of fatwas also seems a step in that direction. It permits IFIs to engage in parallel Salam with the

similar net results as conventional forward contracts. It allows Salam-long (seller) to open another position as a salaam-short with a

third party after the inception of the first contract. Salam-long can engage in this contract on conditions similar to the first contract

before the delivery of the goods take place.

Contemporary scholars acknowledge the need for flexibility bearing in mind the tough competition Salam contracts face in the west-

ern markets with highly developed derivative products and the organized legal and institutional framework.

FEATURED ARTICLE: EMERGING ISLAMIC CAPI-

TAL MARKET IN PAKISTAN

17

◊ FIRST QUARTERLY 2021 IFMP

The Salam contract is an effective tool suitable to seek entry and access these highly competitive markets in providing a credit facility

in compliance with the Shariah principles. The Scholars has shown willingness in their fatwas to allow this as a form of systematic

trade and debt financing if the existing injustice and consideration of wider benefit to public and economic circumstances so dictates.

Istisna The general principles of Shariah prohibits the sale or purchase of the any object which is not in possession of the seller or which has

not come into existence as yet and regard it as form of gharar.

Istisna is regarded as a second exception to this principle. Classical jurists have legalized this exception on the basis of rationale of

Istihsan or falah, which means creating lenience in the wider public interests.

The contract of Istisna involves buyer paying the price in flexible mode of either lump sum or multiple installments in consideration

for the seller to manufacture a commodity with specific requirements to be delivered at some future date.

The essential features of Istisna are the specific requirements of the commodity and the price which have to be settled at the time of

the contract. Istisna deals in products, which are made to order. Historically, these types of contracts were used in leather products,

shoes and carpentry etc.

Although Istisna shares the financing of the non-existent commodity with Salam and structure of transaction appear to be similar,

however, both have several differences.

Firstly, in Istisna, the object of sale transaction is manufactured or constructed however; in Salam contract the object of sale

transaction need not be manufactured.

Secondly, Istisna stipulate a unique manufacturing process whereas Salam contracts do not prescribe to any particular produc-

tion process such as the crops of any particular field.

Thirdly, the price in Istisna may be paid on flexible terms at any agreed time whereas Salam requires the payment to be made in

advance to ensure validity.

Fourthly, the object of Istisna sale is usually non-fungibles whereas the object of sale in Salam is usually fungible.

In addition to this, an Istisna contract can be revoked before the manufacturer starts the work however a Salam contract cannot

be rescinded unilaterally.

Finally, the time of delivery is flexible in Istisna whereas in Salam contracts it is fixed.

Istisna can also be used as mode of financing by IFI in the real estate sector for the construction of residential dwellings, hospitals,

schools and universities etc. Similarly, government departments can also use Istisna for the construction of bridges, dams, highways,

aircrafts, ships and airplanes etc. Istisna is flexible enough to allow the manufacturer to subcontract the project to a third party. This

arrangement is called a parallel Istisna. A typical transaction entails IFIs signing an Istisna contract with the client and another one

with the manufacturer to deliver at certain date. The difference of price amounts to profit for IFI.

Future Prospects Under the National Financial Inclusion Strategy, a quarter of banking assets in the Islamic Republic are expected to comply with Sha-

riah principles by 2023, while 20% of the country’s banking branch network is expected to be those of Islamic banks or branches.

With about US$1 trillion of assets lodged in Islamic financial institutions and capital markets, the swift post-crisis recovery of de-

mand for shariah-compliant structured transactions, such as sukuk, points to a real and inescapable demand for religiously accepta-

ble risk management solutions.

Islamic finance comes into its own, and more companies turn to capital market-based sources of finance, shari’ah-compliant deriva-

tives will become ever more essential to enhance liquidity management, supplement cash markets at lower funding cost, and ensure

FEATURED ARTICLE: EMERGING ISLAMIC CAPI-

TAL MARKET IN PAKISTAN

18

◊ FIRST QUARTERLY 2021 IFMP

an efficient transmission of funds from savers to investors.

Islamic Capital Markets have potential of extraordinary growth but in order to achieve that, certain steps need to be taken:

Customer acceptability, both Muslims and Non-Muslims needs to be increased

Public IPO’s trend needs to go up

Cross Border trading within OIC Countries needs to be promoted to diversify and minimize risk and volatility

Building on Information Technology

Improvement in Transparency to attract international investors

Guidelines on Day trading to be established

Adequate infrastructure to enable the system to operate and function efficiently and effectively

Industry to be built on ethical grounds

Improving regulatory infrastructure

References https://corporatefinanceinstitute.com/resources/knowledge/finance/islamic-finance/

https://slideplayer.com/slide/4274306/

https://www.slideshare.net/IntazarAliShah/islamic-capital-markets-53048826

https://www.slideshare.net/mandalina/islamic-capital-market?next_slideshow=1

"Source: ISLAMIC FINANCIAL SERVICES INDUSTRY STABILITY REPORT 2020"

https://aims.education/7-basic-islamic-capital-market-instruments-products/

https://courses.edx.org/asset-v1:IRTIx+IFCM101x+1T2016+type@asset+block/

Islamic_Financial_and_Capital_Markets_Chapter_1-4.pdf

https://www.investsmartsc.my/what-is-islamic-capital-markets/

https://www.elibrary.imf.org/view/IMF001/12664-9781463938406/12664-9781463938406/12664-

9781463938406_A001.xml?rskey=vGtN7I&result=9&highlight=true

IFN PAKISTAN Report 2019

Shariah Principles for Islamic Capital Markets and the Regulation of Market Abuse in UK and the US: Common Grounds, Di-

vergences and Proposal for Reform

https://www.investopedia.com/terms/s/sukuk.asp#:~:text=A%20sukuk%20is%20a%20sharia,indirect%20interest%

2Dbearing%20debt%20obligations.

https://economictimes.indiatimes.com/definition/risk-management

**********

FEATURED ARTICLE: EMERGING ISLAMIC CAPI-

TAL MARKET IN PAKISTAN

19

◊ FIRST QUARTERLY 2021 IFMP

Fund management industry comprising of both conventional and Islamic funds is growing rapidly in Pakistan but have

some challenges as well as opportunities which are as follows:-

Challenges:

Increased Competitive:

There is a great competition in the Fund Management industry. Switching cost is easy for investors if a fund is underper-

forming relative to its benchmark or peer.

Investment Constraints:

In order to fully comply, the Fund Manager may not be able to capitalize on the opportunities available in the market due

to the investment constraints which resulting in Active return to be less than that of un-constrained fund e.g. a money

market fund is bound to invest maximum 80% of the total portfolio in Government Treasury bills as per its offering doc-

ument; cannot invest more than the said limit even if it have more profitable opportunities.

Taxes on Part of Investors:

Two types of taxes are applicable at investor level i.e. Dividend and capital Gain Tax (CGT) which are at higher levels and

they also depend on the tax status of the Investor (i.e. Filer/ Non-Filer) and varied based on number of years from the

date of investment till the date of redemption. If the taxes are lower, then it will increase after tax investment return and

may appeal local and foreign investors. However, tax credits under section 62 and 63 of Income Tax Ordinance, 2001 for

investment in shares and insurance (including open end mutual funds) and Contribution to an approved Pension Fund

respectively reduce tax liability of Individuals upon meeting the certain conditions which increases with higher effective

tax rate and higher investment. This results in attraction to individuals to invest in collective investment schemes and

insurance.

Expense Ratio:

In a competitive Fund Management, an investor may analyze and compare the expense ratio with other Fund Managers

offering similar Funds before making investment decision. Higher expense ratio of the Fund reduces the return before

taxes.

Regulatory Oversight:

Investors’ protection is a big concern now a days and is increasing Regulatory attention, strict compliance on Fund Man-

ager may be a hectic exercise but it’s necessary for sustainable development of Capital Markets and also to protect inves-

tors’ fund.

Generating Positive Alpha:

Alpha is the excess return after deducting all expenses of the Fund as compare to its benchmark return (e.g. a Fund Man-

ager achieve the return of 12% in a year compared with 10% return of KSE-100 index (the benchmark); the active return

or alpha in this case shall be 2%. Generating positive alpha return is good for the Fund Manager.

ARTICLE BY IFMP MEMBER: Fund Management -

Challenges and Opportunities

by MUDASSAR FAROOQ (Punjab Pension Fund)

20

◊ FIRST QUARTERLY 2021 IFMP

Know Your Customer:

Globally, for Fund Management Industry it is important to know your customer (KYC) to ensure that money invested is

not from the illegal sources and shall not be used in illegal activities manner. The regulators all over the world are mak-

ing strict compliance in order to avoid money laundering or terrorism financing.

Slow Economic Growth

Like any other Industries slow economic growth also impacts Fund Management industry. When the growth of any econ-

omy is slow then it effects investments in the sectors like banking and non-banking (e.g. Fund Management).

Performance Measurement:

Fair and standardized performance measurement is a big challenge for the Industry. This makes comparison easy for in-

vestor among different Fund Managers. Globally, Fund Manager may voluntarily adopt the Global Investment Perfor-

mance Standards (GIPS) standards and claim compliance with the standards however they are not mandatory but are

preferred.

Adherence to Ethical & Professional Standards:

Due to the various ethical issues and fraudulent activities in the financial sector globally, the need for ethical and profes-

sional standards both on individual level (firms employing Fund Managers) and Firm level is seeking more attention. The

Fund Manager and employees may adopt them or may have strict standards at their own in order to stay professional

and ethical.

Opportunities:

Parent Branches for Fund Distribution

Although some Fund Managers/ Asset Manager Companies (AMCs) are using branch network of their banks (parent

companies) to distribute or sell their funds reducing a lot of cost and mobilizing the funds. But still there are few AMC

not using the branch network of their banks to boost their business.

Wide Range of Asset Classes:

The avenues to offer other non-traditional asset classes like Real Estate Funds, Hedge Funds, PE Funds, and Commodity

Funds are also popular in the rest of the world but not in Pakistan so there is huge potential in this area to capitalize on

opportunities.

Fin-Tech:

Technology is playing a key role in increasing efficiency and reducing cost. Robo-advisors that provides Fund Manage-

ment services with moderate to minimal human intervention based on mathematical rules or algorithms is also reshap-

ing the Future of investment industry by providing the cost effective and efficient advisory services. However, it may not

provide customize products to clients.

Digital (Account Opening, Account Maintenance, Fund Conversion, Investment and Redemption) is also helping in terms

of ease of investing and managing funds.

ARTICLE BY IFMP MEMBER

21

◊ FIRST QUARTERLY 2021 IFMP

Sustainable Investing:

Economic, Social and Governance (ESG) consideration is attracting investors and has positive impact on Asset return.

Studies shows that the Fund Manager invest in companies considering ESG factors have more sustainable business.

Sharia Compliant Fund Potential:

Fund Management industry offering Sharia Compliant products has a lot of potential. But currently it has very low asset

base in Pakistan.

Value Added Services:

Value added services (VAS) may be a reason to attract new clients or retain existing clients to differentiate a Fund Man-

ager with regard to varied services it offers, this may include swift redemption, ATM withdrawal facility, free insurance

coverage, smart phone mobile applications and online fund transfer/ electronic statement facility etc.

Public Sector Funds:

The public sector funds in Pakistan are either passively managed or a very small proportion are actively managed

through professional Fund Manager or do not have independent board (good Corporate Governance) to oversight Fund

Management function at Public Sector companies. The private sector Fund Manager may target this huge potential mar-

ket which has a lot of Funds to be managed actively.

Exchange Traded Funds:

Exchange Traded Funds globally is an attractive investment avenue due to its unique features and advantages. Hence,

there is a huge potential for Fund Management industry to be launch in Pakistan.

Conclusion:

Apart from the challenges the Fund Management industry is facing, it also has huge potential for growth including but

not limited to Islamic Funds avenues, Exchange Traded Funds (ETFs), Private Equity Fund, Commodity Funds etc. The

financial technology, Capital Market stringent regulations, uniform investment performance measurement in the indus-

try, reduced taxes to attract local and foreign investors, value added services, well designed investor education plan and

promotion of savings culture among others will be the determining factors in the growth of Fund Management industry

in Pakistan. To achieve such objectives; all the stakeholders need to work in synergy and collaboration.

**********

ARTICLE BY IFMP MEMBER

22

Terms of the quarter

◊ FIRST QUARTERLY 2021 IFMP

Get Yourself Registered!!

Last Date of Registration for 30th May, 2021

Examination

3rd May, 2021

Commodity Commodity in relation to a futures contract, means—

(a) agricultural, livestock, fishery, forestry, mining or ener-

gy goods and any product that is manufactured or pro-

cessed from any such goods; and

(b) Any other goods or products which as such may be no-

tified by the Commission in the official Gazette;

Financial instrument Financial instrument includes any currency, currency in-

dex, interest rate, interest rate instrument, interest rate

index, commodity index bond index and such other finan-

cial instruments as may be notified by the Commission in

the official Gazette;

Futures broker “Futures broker” means a person who, by way of business,

whether as principal or agent,—

(a) makes or offers to make with any person, or induces or

attempts to induce any person to enter into or to offer to

enter into any agreement for or with a view to purchase or

sale of a futures contract; or

(b) Solicits or accepts any order for, or otherwise dealing

in, or effects transactions in a futures contract for its cus-

tomer or on its own account;

Majority shareholder Majority shareholder means shareholder who holds, owns

or control, directly or indirectly, more than fifty per cent of

the shares having voting rights in a company or who, for

other reasons, has domination or control of the company

and includes group of shareholders who collectively own

more than fifty per cent of shares or otherwise have that

domination or control;

Book-entry security Book-entry security", in relation to a central depository,

means a security which is transferable by book-entry in

the central depository register pursuant to a declaration

made by the central depository under sub-section (6) of

section 4 and which is —

(a) in the case of a security transferable by registration,

registered in the name of the central depository or issued

to the central depository pursuant to section 14 ; or

(b) in the case of a security transferable by delivery or en-

dorsement, deposited with or transferred by endorsement

to the central depository ;

Qualifying creditors Qualifying creditors means one or more creditors holding

unpaid and overdue claims for an

aggregate amount of not less than

two-third of the value of assets of

the debtor as per its latest balance

sheet.

23

Business and Economic Newsflash (local)

◊ FIRST QUARTERLY 2021 IFMP

Rupee rises as world’s best performer this year KARACHI: Terming rupee’s becoming world’s best performer in the first quarter of this year as tremendous, analysts on Wednesday

however warned against sharp currency movements. The rupee benefited in a big way from robust foreign exchange inflows from

Pakistani diaspora in the form of remittances, Roshan Digital Account, resumption of International Monetary Fund’s (IMF) loan pro-

gram, issuance of Eurobonds, and anticipated inflows from multilateral institutions.

“PKR has been the world’s best currency against USD from January 1st to March 31st,” said Muzammil Aslam, CEO at Tangent Capital

in a Tweet, citing Bloomberg data.

“It’s good to celebrate but it’s equally [a matter of] concern to maintain competitiveness. I’m for gradual changes than abrupt,” Aslam

added.

“The sudden fluctuations in the currency don’t give a good signal to the markets and businesses,” he said.

The rupee has strengthened 4.09 percent against the dollar in January to March (trading at 153.55) this year, outperforming its re-

gional peers and various global currencies. It is also one of the four world currencies that have posted gains versus the greenback

together with the Canadian dollar, British Pound, Saudi Riyal, and the Norwegian Krone.

The local unit appreciated 3 percent in March.

The Canadian dollar rose 1.09 percent against the dollar in the first quarter of 2021, with the sterling, appreciating 0.64 percent, Nor-

wegian currency 0.23 percent and Saudi currency 0.03 percent, respectively.

The rupee gained 0.22 percent to close at 152.76 per dollar in the interbank market on Wednesday. It had ended at 153.09 to the dol-

lar in the previous session.

The local unit breached the 153 mark after the government received around $500 million ($498.7 million) from the IMF as a dis-

bursement under the Extended Fund Facility for budget support.

The launch of a three-tranche Eurobond deal to raise $2.5 billion, comprising tranches of five, 10 and 30 years also helped aid senti-

ment, supporting the local unit. The government received $5.3 billion in combined orders for the bonds.

Traders suspected the SBP’s intervention through dollar buying from the market to prevent the sharp rally in the rupee and to sup-

port exporters, but it didn’t confirm.

In the open market, the rupee closed at 153.20 versus the greenback, compared with 153.70 on Tuesday.

“The rupee has been appreciating versus dollar due to the lack of dollar demand led by reduced smuggling,” Aslam said.

The speculative elements had been removed from the foreign exchange markets owing to the vigilant and the supervisory role of the

central bank, the analyst said.

The limited outflows due to subdued international traveling amid Covid-19 restrictions and remittances coming through official

channels also supported the remittances as well as currency.

“In the market based exchange rate system, the currency is influenced by the demand and supply conditions, so, the rupee is ex-

pected to be stable in the times to come subject to repayments requirements,” Aslam said.

“Pakistan’s foreign exchange reserves are all set to make new all-time high of $23.5 billion,” he said, referring to the launch of $2.5

billion Eurobonds in the international capital market.

The reserves last time saw $23 billion was in 2015-16. When PTI took over the reserves were at $16.4 billion, Aslam added. The

country’s forex reserves increased 1.36 percent to $20.434 billion in the week ended March 19.

Traders expect the rupee to hover around 150 to 152 levels against the dollar in the near term.

24

Business and Economic Newsflash (local)

◊ FIRST QUARTERLY 2021 IFMP

Exports hit decade high of $2.3 billion in March ISLAMABAD: Pakistan’s exports in March reached a decade-high of $2.3 billion with monthly figures showing growth year-on-year

and over the previous month, commerce adviser said on Thursday.

“Ministry of commerce is glad to share that according to provisional figures, in March 2021 our exports increased to $2.345 billion.

This is an increase of 13.4 percent over February 2021. It is the monthly highest in last 10 years,” Adviser to Prime Minister for Com-

merce and Investment Razak Dawood wrote on Twitter.

“This is also the first time since 2011 that exports have crossed the $2 billion mark for six consecutive months.”

However, commerce adviser termed the annual growth as misleading because the last year’s lockdown kept the industrial wheel ex-

tremely slow.

“The export growth of 29.3 percent over March 2020 should not be considered as it is misleading since there was a lockdown last

year,” Dawood said.

For the 9-month period of July-March of the current fiscal year, exports increased 7 percent to $18.6 billion as compared to $17.4

billion in the corresponding period last year, according to the ministry of commerce’s data.

Exports are expected to get an upset due to shortage of cotton, the main industrial input of textile industry that accounts for more

than 60 percent of total exports.

The government is uncertain about giving a go-ahead to cotton and yarn import from India, the world’s largest cotton producer. Ana-

lysts said textile industry’s growth is tied with cotton import from India to keep up momentum of textile exports from the country.

“It’s extremely important as there is significant shortfall in cotton production this year. Lack of cotton will result in reduced textile

output and hence exports,” Saad Hashemy, an executive of Karachi-based BMA Capital said.

Although some analysts said banning Indian cotton would not deprive Pakistan’s textile industry of the raw material, they still be-

lieve cross-border trade is more cost-effective.

“Eventually we will be importing from China and Europe as we are doing it right now,” said Tahir Abbas, head of Research at Arif

Habib Limited.

However, there are two differences when it comes to cost-effectiveness of Chinese and European cotton, Abbas said. One is transpor-

tation time and cost involved in importing cotton from neighbouring India vis-a -vis international import. Secondly, there is four to

five percent difference in cotton prices.

In July-March period, imports grew 12 percent to $39.2 billion compared to $34.8 billion during the corresponding period last year.

The growth has come from increase in import of raw material as well as import of wheat, sugar and cotton, commerce adviser said.

Forex reserves rise to $20.836bln KARACHI: Pakistan’s foreign exchange reserves increased $402 million, or 1.96 percent, in the week ended March 26, the central

bank said on Thursday.

The total liquid foreign exchange reserves held by the country stood at $20.836 billion, compared with $20.434 billion in the previ-

ous week.

“During the week ended March 26, 2021, the [State Bank of Pakistan] SBP) received $498.7 million from the IMF [International Mon-

etary Fund] under EFF [Extended Fund Facility] program; after accounting for external debt repayments, the SBP reserves increased

by $378 million to $13,673.0 million,” the central bank said in a statement.

The forex reserves held by commercial banks also rose to $7.163 billion from $7.139 billion.

25

Business and Economic Newsflash (local)

◊ FIRST QUARTERLY 2021 IFMP

SECP may allow direct listing of companies on stock exchange

The Securities and Exchange Commission of Pakistan (SECP) is considering a proposal to allow direct listing of local companies on

the stock exchange – a route that’s easier than meeting rules required for initial public offerings (IPOs).

SECP Chairman Aamir Khan who proposed the idea said that the regulator is discussing the plan.

If the proposal is approved, it will help companies, especially state-owned ones, looking to sell existing shares as they will not even

need approvals from the regulator for the transaction in most instances, he said.

“Direct listing is a concept which is there in developed markets already,” said Khan. “It’s something on our internal drawing board

right now.”

The SECP is now working on making real estate investment trust launches easier. The need for a mandatory building completion cer-

tificate, seen by many investors as a hurdle, has been removed, Khan said.

Pakistan has not seen any REITs after its debut in 2015. An increase in taxes stymied plans of about eight REITs.

Just like in most other global markets, companies in Pakistan are rushing to tap capital markets for funds, riding on strong investor

sentiment. —TLTP

SBP injects Rs.1975b in open market The State Bank of Pakistan (SBP) has injected Rs.1975.05 billion in market for seven days through Open Market Operation.

According to a report issued by the central bank’s Domestic Markets and Monetary Management Department on Friday,25 quotes

were offered for reverse repo purchase at the rate ranging from 7.04 to 7.10 percent. —APP

Baqir announces 3 important measures for Capital Markets

Pakistan Stock Exchange (PSX) hosted Governor State Bank of Pakistan (SBP), Dr Reza Baqir at its Gong Ceremony to mark the begin-

ning of a new chapter of cooperation between SBP and PSX on multiple initiatives.

SBP and PSX have recently been working closely to improve and widen the access of capital market participants to government debt

securities; facilitate investments by non-residents in the stock exchange; remove bottlenecks hindering companies from leveraging

against shares of their group companies and developing information sharing arrangements between banks and capital markets.

Speaking on the occasion, Governor SBP, Dr. Reza Baqir said he was pleased to visit PSX for this Gong Ceremony as it marked the

commitment of SBP and PSX to work together for the deepening of debt and capital markets in Pakistan and improving financial in-

termediation.

He made three important announcements in this regard. First, he said that SBP has revised the Rules governing appointment of pri-

mary dealers for the Government’s debt securities.

This will expand the list of institutions eligible to work as primary dealers, including Security Depositories and Clearing institutions.

This measure is aimed at widening the investor base of government securities, improving liquidity, enhancing transparency and pro-

moting market development.

In addition, SBP has relaxed the selection and performance criteria for development finance institutions (DFIs), investment banks

and brokerage houses to encourage them to become part of the primary dealer system, which is currently dominated by banks.

Hence, among other privileges offered to primary dealers, a larger and more diverse group of institutions will now have direct access

to primary auctions.

He said that while the government debt market in Pakistan is well developed and liquid, participation of capital market clients has

26

Business and Economic Newsflash (local)

◊ FIRST QUARTERLY 2021 IFMP

historically been limited and SBP wants to encourage wider ownership of Government securities among retail investors.

SECP enables startups to offer Employee Stock Options Plan

Employee Stock Option Plan (ESOP) is a popular method of attracting, motivating, and retaining employees.

Stock Option Plans permit employees to share in the company’s success without requiring a startup business to spend precious cash.

Previously, only public companies were allowed to issue employee stock options. As a step forward to facilitate corporate sector, the

SECP hereby clarifies that private limited companies especially startups can also now offer ownership rights to their employees as a

non-monetary compensation for their intellectual services and promotion of their business.

A private company may offer shares to its existing shareholders in accordance with section 83(1)(a) of the Companies Act, 2017, and

if the whole or any part of the shares offered is declined or is not subscribed, such shares can be offered to its employees under pre-

determined contractual arrangements.

Option for employees to own a company they work for proves to be a highly motivating factor to increase productivity and efficacy

which startups immensely require at their initial stages of business commencement.

PSX introduces compliance calendar for listed companies

Pakistan Stock Exchange (PSX) being the premier Exchange of the country and a frontline regulator ensures and monitors the timely

fiscal disclosures, announcements of material and price-sensitive information for the benefit of shareholders and other stakeholders

of the capital market.

To automate and simplify the process of regulatory and financial disclosures, PSX has in place PUCARS (Pakistan Unified Corporate

Action Reporting System) which facilitates listed companies in submission of required information and ensuring timely disclosure

directly on PSX website.

Going a step further, PSX has now introduced a Compliance Calendar which consolidates applicable requirements of PSX Regulations,

including requirements of financial disclosures, and serves as a guide for listed companies to meet their requirements in accordance

with their deadlines.

The Compliance Calendar also consists of forms to be used from the Correspondence Manual for dissemination/ submission of par-

ticular information.

The Compliance Calendar consists of both periodic as well as situational requirements.