quarterly conversations - federal reserve bank of st. louis · 1 quarterly conversations: live from...

TRANSCRIPT

1

Quarterly Conversations: Live from First State Bank and Trust

Caruthersville, Missouri

August 19, 2015

2

Options to Join the Conversation

Webinar and audio

• Click on the link: https://www.webcaster4.com/Webcast/Page/584/8667

• Choose to listen with your PC speakers

Webinar and phone

• Click on the link: https://www.webcaster4.com/Webcast/Page/584/8667

• Choose to listen with your phone

• Call in number: 888-625-5230

• Enter the participant code: 71833541

Phone only

• Call in number: 888-625-5230

• Enter the participant code: 71833541

3

• Julie Stackhouse, Senior Vice President, Federal Reserve Bank of St. Louis

• Leslie Hurst, Examiner, Federal Reserve Bank of St. Louis

• Rob Ryan, Senior Examiner, Federal Reserve Bank of St. Louis

Today’s Presenters

4

Agenda

1. New integrated Truth in Lending Act (TILA)/Real Estate Settlement Procedures Act (RESPA) disclosure form – Changes in coverage

– Definitions

– Timing requirements

– Tolerances

– Disclosure formatting

2. The U.S. Supreme Court ruling on disparate impact: implications for banking – The ruling and possible implications for the supervisory process.

– The ways in which banks can use monitoring and reviews to effectively control any increased fair lending risk.

5

Part 1: TILA-RESPA Integrated Disclosure (TRID)

6

TILA-RESPA Integrated Disclosure (TRID)

• Effective: October 3, 2015

• Introduces two new forms that combine old disclosures

– Loan estimate (LE) – new disclosure

• Early truth in lending disclosure (Regulation Z)

• Good faith estimate (Regulation X)

– Closing disclosure (CD) – new disclosure

• Final TIL disclosure (Regulation Z)

• Housing and urban development (HUD) 1/1A settlement statement (Regulation X)

• Introduces two servicing-related disclosures

– Escrow closing notice

– Partial payment disclosure

7

TILA-RESPA Integrated Disclosure (TRID)

• Applies to most closed-end consumer loans secured by real estate, including:

– Loans secured by more than 25 acres

– Loans secured by vacant land

– Construction-only loans

• Exemptions:

– Home equity lines of credit

– Reverse mortgages

– Mobile home loans without real estate

8

TILA-RESPA Integrated Disclosure (TRID)

• “Application” definition involves the receipt of the consumer’s:

– Name

– Income

– Social security number

– Address of property

– Estimate of value of property

– Requested mortgage loan amount

• These items do not have to be verified to be considered a completed application according to the new rule.

9

TILA-RESPA Integrated Disclosure (TRID)

• Loan estimate:

10

TILA-RESPA Integrated Disclosure (TRID)

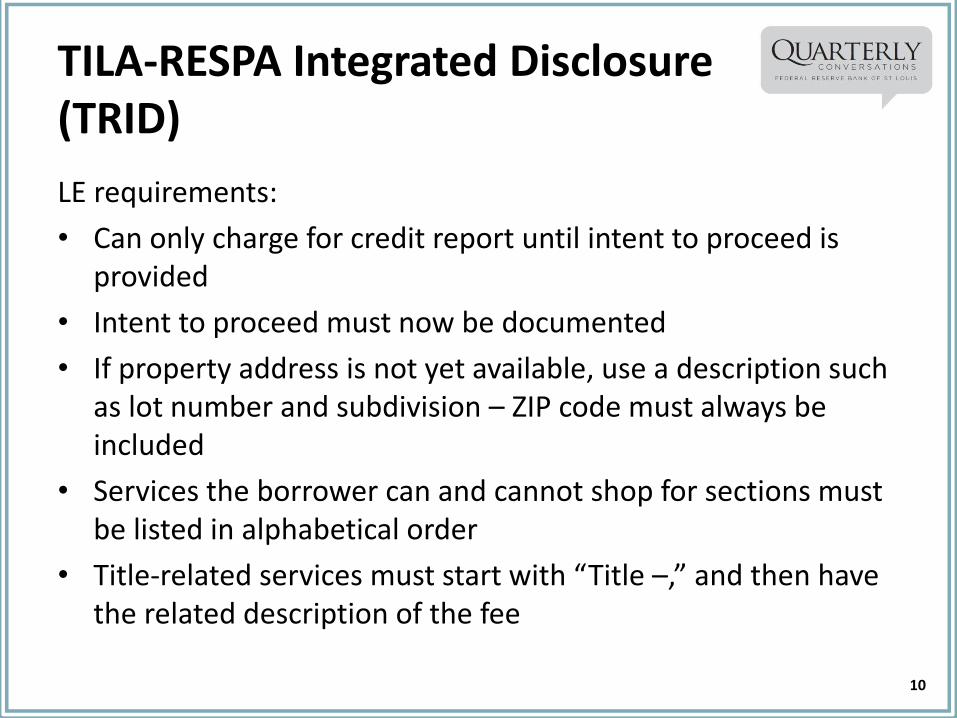

LE requirements:

• Can only charge for credit report until intent to proceed is provided

• Intent to proceed must now be documented

• If property address is not yet available, use a description such as lot number and subdivision – ZIP code must always be included

• Services the borrower can and cannot shop for sections must be listed in alphabetical order

• Title-related services must start with “Title –,” and then have the related description of the fee

11

TILA-RESPA Integrated Disclosure (TRID)

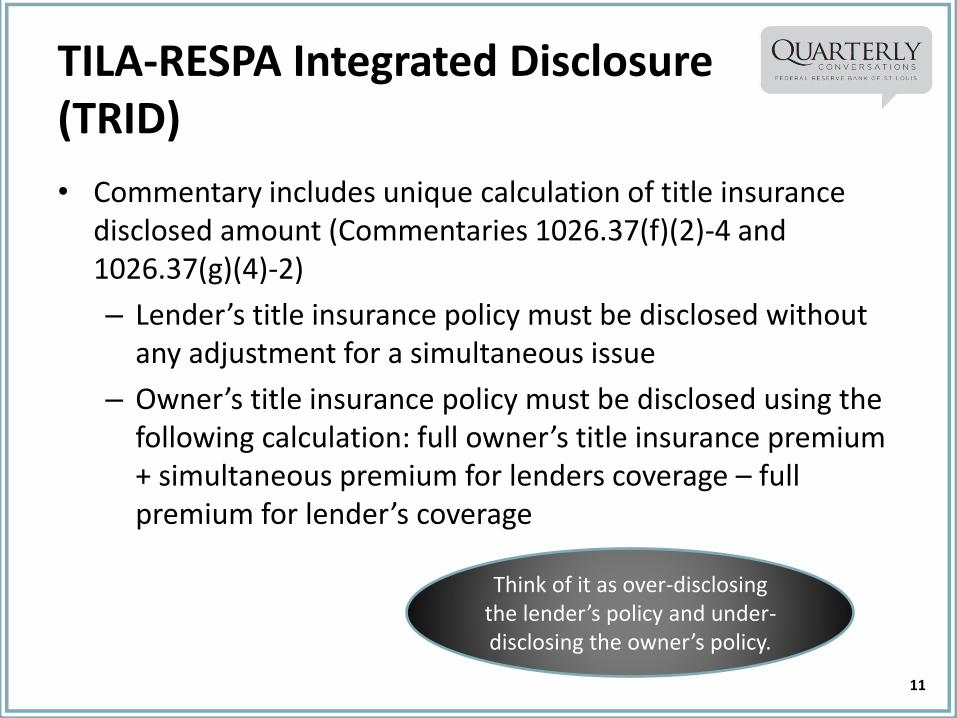

• Commentary includes unique calculation of title insurance disclosed amount (Commentaries 1026.37(f)(2)-4 and 1026.37(g)(4)-2)

– Lender’s title insurance policy must be disclosed without any adjustment for a simultaneous issue

– Owner’s title insurance policy must be disclosed using the following calculation: full owner’s title insurance premium + simultaneous premium for lenders coverage – full premium for lender’s coverage

Think of it as over-disclosing

the lender’s policy and under-disclosing the owner’s policy.

12

TILA-RESPA Integrated Disclosure (TRID)

LE – Payment Tables

• General guidelines:

– May have up to four payment columns

– Balloon payment, scheduled as a final payment, must have its own column

– “1–5 years” on the payment table reflects payments 1–59 • The schedule is reflecting up to the fifth year

• Payment 60 would be disclosed as year six

13

TILA-RESPA Integrated Disclosure (TRID)

• Adjustable rate mortgage (ARM) payment schedule:

– Minimum payments: calculate assuming interest rate will decrease as rapidly as possible

– Maximum payments: calculate assuming interest rate will rise as rapidly as possible

– No longer limited to: initial, maximum in 5 years, and maximum ever

14

TILA-RESPA Integrated Disclosure (TRID)

• Balloon LE payment schedule example: — 62 month balloon — 61 payments at $1,007.68 — Balloon on 62nd month of $191,134.68

15

TILA-RESPA Integrated Disclosure (TRID)

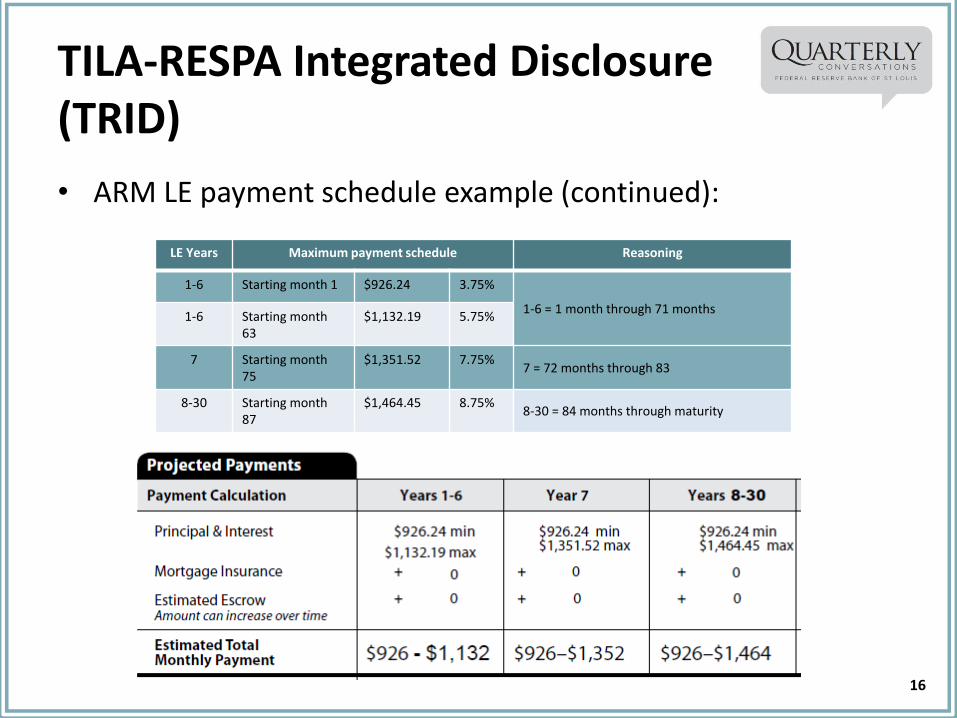

• ARM LE payment schedule example:

— $200,000 loan amount

— 30-year loan

— Initial rate of 3.75 percent

— Floor of 3.75 percent

— 2/6 caps

— Fully indexed rate of 8.75 percent

— Initial fixed period of 62 months, adjust yearly thereafter

16

TILA-RESPA Integrated Disclosure (TRID)

LE Years Maximum payment schedule Reasoning

1-6 Starting month 1 $926.24 3.75%

1-6 = 1 month through 71 months 1-6 Starting month

63 $1,132.19 5.75%

7 Starting month 75

$1,351.52 7.75% 7 = 72 months through 83

8-30 Starting month 87

$1,464.45 8.75% 8-30 = 84 months through maturity

• ARM LE payment schedule example (continued):

17

TILA-RESPA Integrated Disclosure (TRID)

• LE timing requirements:

– Timing • LE: Must be delivered or placed in the mail within 3 business days

after application and 7 business days before consummation.

• Revised LE: Must be received 4 business days before consummation.

– LE business day • A day on which creditor’s offices are open for carrying out

substantially all of its business functions.

– The LE business day definition differs from the CD business day.

18

TILA-RESPA Integrated Disclosure (TRID)

• LE timing requirements (continued):

KEY: RED is bank/borrower actions

BLUE is regulatory requirements

19

• Fee tolerance changes

– Zero tolerance category: • Fees paid to creditor, mortgage broker, or affiliate of either

• Transfer taxes

• Third party charges the borrower was NOT allowed to shop for

– 10 percent tolerance category: • Third party charges (not paid to creditor or affiliate) where consumer

is permitted to shop and selects from written list of providers

• Recording fees

– No tolerance category: • Prepaid interest, property insurance, escrow

• Third party charges (not paid to creditor or affiliate) where consumer selects servicer NOT on written list of providers

TILA-RESPA Integrated Disclosure (TRID)

20

TILA-RESPA Integrated Disclosure (TRID)

• LE changed circumstances:

– Event beyond control of any interested party or other event specific to consumer or transaction (cost related)

– Information specific to transaction or consumer that creditor relied upon to provide LE is found to be inaccurate or changed (cost related)

– New information specific to transaction or consumer that creditor did not rely on when providing LE (cost related)

– Information received that affects eligibility for a loan program (loan program and related costs)

– Borrower requested changes that affect charges or loan terms

– Rate lock, where rate was not locked when initial LE was provided

21

TILA-RESPA Integrated Disclosure (TRID)

• LE changed circumstances (continued):

– A missed fee or inaccurate calculation by the bank is NOT a changed circumstance. A revised LE is not allowed.

– Only provide a revised LE when the changed circumstance causes charges to exceed the allowed tolerances. • Commentary states that the CD will only be compared to revised

LEs that are issued when a changed circumstance causes charges to exceed tolerance.

• The Zero Tolerance category has the rule changes to watch

• 10% Tolerance and No Tolerance categories generally remained the same

22

LOAN ESTIMATE CHANGED CIRCUMSTANCES

KEY: RED is bank/borrower actions

BLUE is regulatory requirements

TILA-RESPA Integrated Disclosure (TRID)

23

TILA-RESPA Integrated Disclosure (TRID)

• Closing Disclosure:

24

TILA-RESPA Integrated Disclosure (TRID)

• CD timing requirements: – Timing

• A CD received at least 3 business days prior to consummation:

– A CD that is mailed is considered received 3 business days after it is mailed.

• Consider delivery confirmation to speed up the process.

– A CD that is emailed is also considered received 3 business days after it is emailed.

• Consider read receipts to speed up the process.

• Must obtain consent from the borrower to send a CD electronically. This is required by the E-sign Act. If consent is not documented, delivery of the CD via email is not allowed.

• A CD business day is all calendar days except Sundays and legal holidays.

– This definition differs from the LE business day.

25

TILA-RESPA Integrated Disclosure (TRID)

• Everybody is saying, “Oh no! Closings will be delayed.”

– It will be okay. • Three types of changes that will require a new 3-business day

waiting period:

– Disclosed annual percentage rate becomes inaccurate.

• 1/8 percent for regular loans and 1/4 percent for irregular loans

– The loan product changes.

• Fixed rate to ARM; principal and interest to interest only; Conventional to Federal Housing Administration (FHA)

– Prepayment penalty is added.

– It will be important to watch the lender required services that borrower cannot shop for such as appraisal, credit reports.

26

TILA-RESPA Integrated Disclosure (TRID)

• Record retention: (Record retention does not only apply to disclosures, it now applies to documents related to disclosures such as estimates and changed circumstance events.)

– LE: 3 years after consummation

– CD: 5 years after consummation

– Escrow closing notice and partial payment disclosure: 2 years

• Remember:

– If servicing is sold, both the new servicer and original servicer must retain the CD for the remainder of the 5 years.

27

TILA-RESPA Integrated Disclosure (TRID)

• Suggestions for success: – Training, policies, and procedures – Test the process and system using a “dummy loan” scenario – Have a dialog with parties involved to ensure all understand the

importance of timely communication – Collaboration with title companies will need to be reviewed

• Fee estimates • CD • Timing

– Broker relationships? Review the process and ensure all parties understand who will do what.

– Online applications? Think about the order in which information is collected.

– Listen to regulatory discussions and hot topics – Contact us!

28

Questions?

• You have three ways to ask a question

By webinar: Type your question into the chat box

By phone: Press *1 to ask a live question

By email: [email protected]

29

Part 2: The U.S. Supreme Court Ruling on Disparate Impact:

Implications for Banking

30

Ruling on Disparate Impact: Implications for Banking

• Key take-aways from the Supreme Court’s decision

• Anti-discrimination legislation/regulation overview

• Disparate impact versus disparate treatment

• Summary of Texas Department of Housing and Community Affairs v. The Inclusive Communities Project, Inc.

• Components of valid disparate-impact claims

• Examples of recent settlements involving lenders

• Implications for the Equal Credit Opportunity Act (ECOA)

• Implications for the supervisory process

• Components of effective disparate-impact risk management

31

• Texas Department of Housing and Community Affairs v. Inclusive Communities Project, Inc. (June 25, 2015)

• “Held: Disparate-impact claims are cognizable under the Fair Housing Act”

• Applying the determination throughout lower courts:

– “A disparate-impact claim relying on a statistical disparity must fail if the plaintiff cannot point to a defendant’s policy or policies causing that disparity.”

– “A robust causality requirement is important . . .”

– “. . . prompt resolution of these cases is important.”

– “Policies . . . are not contrary to the disparate-impact requirement unless they are artificial, arbitrary, and unnecessary barriers.”

– “These limitations are also necessary to protect defendants against abusive disparate-impact claims.”

Ruling on Disparate Impact: Implications for Banking

32

Two pieces of legislation outlawing discrimination on a “prohibited basis” are enforced through Regulation B

The FHA prohibits discrimination in all aspects of "residential real estate-related transactions” on the basis of:

Race or color

National origin

Religion

Sex

Familial status (defined as children under the age of 18 living with a parent or legal custodian, pregnant women, and people securing custody of children under 18)

Handicap

The ECOA prohibits discrimination in any aspect of a credit transaction on the basis of:

Race or color

Religion

National origin

Sex

Marital status

Age (provided the applicant has the capacity to contract)

The applicant’s receipt of income derived from any public assistance program

The applicant’s exercise, in good faith, of any right under the Consumer Credit Protection Act

Ruling on Disparate Impact: Implications for Banking

33

• Both the FHA and ECOA establish two standards for determining whether discrimination has taken place:

– Disparate Treatment: When overtly or comparatively different policies or practices are applied to credit applicants on a prohibited basis (intentional discrimination.)

– Disparate Impact: When a lender applies a neutral policy or practice equally to all credit applicants, but the policy or practice disproportionately excludes or burdens certain persons on a prohibited basis (unintentional discrimination).

Ruling on Disparate Impact: Implications for Banking

34

• Summary of Texas Department of Housing and Community Affairs (Department) v. The Inclusive Communities Project, Inc. (ICP)

– The Department distributes low-income housing tax credits on behalf of the federal government.

– The ICP, a Texas-based nonprofit corporation that assists low-income families in obtaining affordable housing, alleged that the Department caused continued segregated housing patterns by allocating too many tax credits to housing in predominantly black inner-city areas and too few in predominantly white suburban neighborhoods.

Ruling on Disparate Impact: Implications for Banking

35

• Summary of Department v. ICP (continued) – In the original suit filed in 2009, the District Court decided:

• ICP showed disparate impact • And the Department failed to meet its burden to show that there

were no less discriminatory alternatives for allocating the tax credits

• While the Department’s appeal was pending, in 2012 HUD issued a regulation asserting: – The FHA encompasses disparate-impact liability – Three-step burden-shifting framework for deciding whether a

violation has occurred: • Plaintiff proves discriminatory effect of a specific policy or practice • Defendant has the burden of proving legitimate business necessity of

that policy or practice • Plaintiff may prevail upon proving that the same legitimate interest

could be served by another practice with a less discriminatory effect

Ruling on Disparate Impact: Implications for Banking

36

• In deciding the appeal in 2014, the Fifth Circuit Court wrote

– Disparate-impact claims are cognizable under the FHA

– The District Court improperly required the Department to prove that there are no less discriminatory alternatives (in light of HUD’s regulation)

• Supreme Court “affirmed and remanded” the Fifth Circuit’s decision

Ruling on Disparate Impact: Implications for Banking

37

• Components of a valid disparate-impact claim:

– Proof of a specific policy’s discriminatory effect • Burden of proof is on the plaintiff.

• If the claim is based upon statistical evidence, it must be tied to a specific policy.

– Proof that the legitimate business need behind the policy can be achieved through some other policy with less discriminatory effects • Supreme Court ruled that the plaintiff must demonstrate the less-

discriminatory alternative policy, affirming HUD’s 2012 rule.

• Previously, lower courts burdened the defendant with proving that no less-discriminatory alternative policy existed.

Ruling on Disparate Impact: Implications for Banking

38

• Recent disparate-impact settlements involving lenders

Consent Order Act Policy Impact Alternative Policy

USA v. Luther Burbank Savings, 9/12/12

FHA and ECOA

$400,000 minimum mortgage loan amount

Black and Hispanic residents of the Los Angeles area were denied access to mortgage loans

$20,000 minimum loan amount

Ally Financial Inc. and Ally Bank, 12/20/13

ECOA

Through indirect lending relationships, permitting automobile/motorcycle dealers to charge higher interest rates to consumers on the basis of race and national origin

Minority borrowers were charged significantly higher dealer markups than similarly-situated non minority borrowers

Allow dealers to charge markups, but implement controls to prevent dealers' illegally discriminatory actions

USA v. Evergreen Bank Group, 5/17/15

American Honda Motor Co., 7/14/15

Ruling on Disparate Impact: Implications for Banking

39

• Implications for the ECOA • Expect examiners to continue evaluating evidence of disparate-

impact under ECOA for the foreseeable future. – HUD, the Consumer Financial Protection Bureau (CFPB), and

other regulators have reiterated their position that they will pursue disparate-impact claims under ECOA.

– Even as disparate impact cases were approaching the Supreme Court, the CFPB stated that it would pursue disparate impact under ECOA even if it was struck down under FHA.

• Further down the line – Some speculate that the Supreme Court’s ruling will affirm the

legitimacy of disparate-impact claims under ECOA. – Others suspect that the Supreme Court’s opinion on the FHA

may actually call that legitimacy into question.

Ruling on Disparate Impact: Implications for Banking

40

• Implications for the supervisory process

– For now, routine mandated examinations should not look much different.

– Expect continued pressure on indirect lending and redlining • Neither issue would have been immediately affected if the Supreme

Court had overturned disparate impact anyway.

– We may see an increase in complaints, which could alter the normal course of examinations and applications. • Some say the ruling may embolden community groups to file more

complaints, Community Reinvestment Act public comment letters, and application protests.

• If true, this would likely cause extended examination and application processing times.

• Home Mortgage Disclosure Act reporters in diverse markets would be especially vulnerable to such complaints.

Ruling on Disparate Impact: Implications for Banking

41

• Implications for the supervisory process (continued)

In the future, two things that may change are:

– Interagency Fair Lending Examination Procedures (IFLEP) could be updated to put more emphasis on disparate impact. • Currently, the IFLEP tells examiners how to “recognize fair lending

issues that may have a potential disparate impact,” but they “do not call for examiners to plan examinations to identify or focus on [them].”

• The Federal Financial Institutions Examination Council may update or amend IFLEP, or individual regulators may issue their own supplementary guidance.

Ruling on Disparate Impact: Implications for Banking

42

• Implications for the supervisory process (continued)

– A legal challenge to ECOA could affirm or invalidate disparate-impact claims for lending unrelated to residential real estate. • Very unlikely that it would reach the Supreme Court within the

next 5 years

• Given the regulators’ stance on the applicability of disparate impact before June 25, 2015, it seems unlikely that lower court rulings would change anything.

Ruling on Disparate Impact: Implications for Banking

43

• Components of effective disparate-impact risk management:

– Identification of policies or practices with the potential for disparate impact • Things like minimum loan amounts and indirect lending

relationships automatically deserve attention.

• For all loan products and residential real estate-related activities, use management information systems to look for disparities in denial rates, pricing, application volume, etc. on a prohibited basis, and trace them back to a specific policy or practice.

Ruling on Disparate Impact: Implications for Banking

44

• Components of effective disparate-impact risk management (continued):

— Adjust policies with disparate-impact risk to include fair lending controls.

— Document justifications for legitimate business needs, where appropriate.

— Conduct ongoing monitoring of lending data to evaluate effectiveness of controls, and make adjustments as necessary.

Ruling on Disparate Impact: Implications for Banking

45

• Components of effective disparate-impact risk management (continued):

– Example: CFPB/Department of Justice Consent Order’s “Option One” for Honda American Finance, Inc.

– Limit dealer discretion to 125 basis points (bps) for loans with terms of 60 months or less, 100 bps for loans with terms over 60 months, etc.

– Send regular notices to all dealers stating expectations of ECOA compliance and the dealer’s obligation to price loans in a non discriminatory manner.

– Monitor lending data to ensure that dealers are in compliance with discretion limits.

Ruling on Disparate Impact: Implications for Banking

46

• In conclusion . . .

– Disparate-impact claims under the FHA are here to stay.

– Evidence of disparate impact under the ECOA will be pursued by bank regulators unless the Supreme Court stops them.

– Banks should continue to identify and control fair lending risk associated with disparate-impact liability in all residential real estate-related activity and all lending.

– Expect to hear more questions about the legality of disparate-impact claims under ECOA, but don’t expect answers anytime soon.

Ruling on Disparate Impact: Implications for Banking

47

Questions?

• You have three ways to ask a question

By webinar: Type your question into the chat box

By phone: Press *1 to ask a live question

By email: [email protected]

48

Contacts

• Leslie Hurst [email protected] (314) 444-8743

• Rob Ryan [email protected] (314) 444-8419

49

Acronyms and Abbreviations

• TILA – Truth In Lending Act

• RESPA – Real Estate Settlement Procedures Act

• TRID – TILA/RESPA Integrated Disclosure

• LE – Loan Estimate

• CD – Closing Disclosure

• HUD – Housing and Urban Development

• ARM – Adjustable Rate Mortgage

• FHA – Fair Housing Act

• ECOA – Equal Credit Opportunity Act

• Department – Texas Department of Housing and Consumer Affairs

• ICP – Inclusive Communities Project

• CFPB – Consumer Financial Protection Bureau

• IFLEP – Interagency Fair Lending Examination Procedures

50

Thank you!