quarterly economic review of the food and … economic review of the food and beverages industry in...

TRANSCRIPT

agriculture,forestry & fisheries

Quarterly Economic Review of the Food

and Beverages Industry in South Africa

October to December

2016

Volume 3, number 2

DIRECTORATE: AGRO-PROCESSING SUPPORT

i

PREFACE

This Quarterly Economic Review of the Food and Beverage Industry in South Africa: October

to December, 2016 publication is the second quarterly review by the Directorate: Agro-

processing Support to provide an overview of the economic performance of the food and

beverage industry in South Africa. The Food and beverages industry in South Africa is one of

the sub-sectors of agro-processing that plays a dominant role in terms of output and

employment in the agro-processing sector. By adding value to the primary agriculture and

fisheries production, the food and beverages industry stimulates output and job creation in

the primary sector and contributes directly to the food security of the country. In addition, it

played a pivotal role in supplying inputs to the food and beverage service industry,

wholesale and retail sectors.

One of the core businesses of the Directorate: Agro-processing Support is to provide timely

and updated economic information regarding the food and beverages industry to monitor

its performance and provide insight into the effects of economic policies and exogenous

factors on the industry. The main economic indicators reviewed are the changes in prices,

production, capacity utilisation, value of sales, formal employment and trade. An outlook of

the industry for the next quarter is also presented. In addition, some indicators of the food

and beverages service industry, wholesale and retail sectors are reviewed to evaluate the

forward linkages of the food and beverages industry.

Any comments and suggestions on the content of the publication are most welcome.

Victor Thindisa

Director: Agro-processing Support

Pretoria

Disclaimer: The Department of Agriculture, Forestry and Fisheries did everything to ensure the

accuracy of the information reported in this publication. The department will, however, not

be liable for the results of action based on this publication.

ii

CONTENTS

PREFACE ................................................................................................................................................ i

1. INTRODUCTION ........................................................................................................................... 1

2. FOOD PRODUCTS ....................................................................................................................... 1

2.1 PRICE ..................................................................................................................................... 2

2.2 PRODUCTION ...................................................................................................................... 4

2.3 VALUE OF SALES .................................................................................................................. 5

2.4 INCOME FROM FOOD SALES IN THE SERVICE INDUSTRY .......................................... 7

2.5 TRADE .................................................................................................................................... 9

2.6 EMPLOYMENT .................................................................................................................... 19

2.7 OUTLOOK ............................................................................................................................ 20

3. BEVERAGES ................................................................................................................................ 21

3.1 PRICE ................................................................................................................................... 21

3.2 PRODUCTION .................................................................................................................... 22

3.3 VALUE OF SALES ................................................................................................................ 23

3.4 INCOME FROM BAR SALES IN THE SERVICE INDUSTRY ............................................ 24

3.5 TRADE .................................................................................................................................. 25

3.6 EMPLOYMENT .................................................................................................................... 34

3.7 OUTLOOK ............................................................................................................................ 34

4. CONCLUSION ............................................................................................................................ 35

5. REFERENCES ............................................................................................................................... 37

Compiled by: Directorate: Agro-processing Support

Department of Agriculture, Forestry and Fisheries

Sefala Building

503 Belvedere Street, Arcadia, South Africa

All correspondence can be addressed to:

Director: Agro-processing Support

Private Bag X416, Pretoria 0001, South Africa

Tel.: +27 (12) 319 8457

Fax: +27 (12) 319 8093

E-mail: [email protected]

This publication is also available on the internet at: http://www.daff.gov.za

1

1. INTRODUCTION

The global economic activity improved in 2016: Q4, with growth improvement observed in

developed economies. The economic performance, with respect to emerging markets and

developing economies, has remained mixed. China’s growth remained strong, reflecting

continued policy support, while economic activity has slowed in India as a result of the

impact of the currency exchange initiative. Brazil continued with a negative growth

trajectory, leading to a deep recession (IMF, 2017).

During 2016: Q4, the South African economy contracted at an annualised rate of 0,3%,

following a marginal growth of 0,4% in the preceding quarter. The disappointing

performance, amongst other reasons, is attributed to weak consumer demand, acceleration

in consumer price inflation, stagnant formal sector employment, persistent subdued business

and consumer confidence levels that suppressed fixed investment and the adverse effects

of the prolonged drought conditions experienced in many parts of the country (Reserve

Bank, 2017).

During 2016: Q4, the seasonally adjusted physical volume of production of the food and

beverages industry stagnated by 1,4% quarter-to-quarter, however, it decelerated by 0,3%

following a 0,3% contraction previously. Sales for food and beverages moderated by 0,5%

from a 3,0% growth in the last quarter, representing a nominal value increase of R30 826 697

in the current period from R30 658 186 million in 2016: Q3.

The trade deficit of food and beverages expanded by R933,4 million in the current period of

review from a R525,2 million registered in the last quarter.

The employment in the food and beverages and tobacco divisions of the agro-processing

sector rebounded by 3,4% quarter-to-quarter, however, moderated by 7,1% year-on-year.

This represents 244 448 jobs created in the current period as compared to 240 278 jobs

created previously.

This quarterly review assesses the economic performance of the food and beverages

industry, given a moderate global economic growth and a contraction of domestic

economic activities recorded during 2016: Q4.

2. FOOD PRODUCTS

According to the Standard Industrial Classification, the food industry incorporates groups of

products which are categorised into the following four codes:

Code 301 refers to manufacturing, processing and preservation of meat, fish,

vegetables, fruits, oils, and fats

Code 302 refers to manufacturing, processing and preservation of dairy products

Code 303 refers to manufacture of grain mill products, starch products and prepared

animal feeds

Code 304 refers to manufacture of other food products like bread, sugar, chocolate,

pasta, coffee, nuts and spices.

Hence, food products will refer to those primary agricultural and fisheries products that have

undergone some form of change through manufacturing and processing or performed some

value addition activities such as preservation.

2

2.1 PRICE

Consumer Price Index (CPI)1

Table 2.1 below shows the consumer price index of food products during 2016: Q4. The year-

on-year total CPI index of food grew by 6,9% during the period. Similarly, the quarter-to-

quarter CPI increased by 0,9%. During the quarter, most of the items recorded a positive

growth except for oils and fats which declined by 0,3%. On the other hand, the year-on-year

growth of most CPI agro-processed products increased during the current period.

Table 2:1 Consumer price Index of food products

Source: (Stats SA, 2016a)

1 Stats SA defines CPI as a current social and economic indicator that is constructed to measure changes over time

in the general level of prices of consumer goods and services that households acquire, use, or pay for.

Food products

Indices % change between

Weight 2015: Q4 2016: Q3 2016: Q4 2015: Q4

and

2016: Q4

2016: Q3

and

2016: Q4

All items (CPI

Headline)

100 116,4 123,3 124,4 6,9 0,9

Food and non-

alcoholic beverages

15,4 117,5 130,1 132,4 12,7 1,8

Food

14,2 117,7 130,7 133,0 13,0 1,8

Processed

6,8 118,9 131,2 133,4 12,2 1,7

Unprocessed

7,4 116,6 130,3 132,6 13,7 1,8

Bread and cereals 3,5 118,0 138,1 139,9 18,6 1,3

Meat

4,6 115,6 120,4 123,3 6,7 2,4

Fish

0,4 122,5 133,1 135,0 10,2 1,4

Milk, eggs and

cheese

1,7 123,3 134,7 135,7 10,1 0,7

Oils and fats

0,5 112,8 127,0 126,6 12,2 -0,3

Fruit 0,2 104,4 123,6 129,2 23,8 4,5

Vegetables

1,6 116,3 129,5 131,5 13,1 1,5

Sugar, sweets and

deserts

0,6 124,5 148,2 153,2 23,1 3,4

Other food 0,9 88,6 97,6 99,8 12,6 2,3

3

Producer price index (PPI)2

The consumer price index for food products grew by 6% year-on-year and by 1,7% quarter-

to-quarter. The producer price index for meat and meat products, fish and fish products, fruit

and vegetables, food products, (Starch and starch products, animal feeds), bakery and

sugar grew by 6,0%, 4,9%, 2,8%, 1,7%, 1,4%, 0,5% and 0,1%, respectively during the period

under review, while the grain mill products and fats and oils producer price index contracted

by 4,3% and 0,1%, respectively during the period under review. The year-on-year producer

price of the most of agro-processing products grew during the current quarter.

Table 2.2: Producer price index of food products

Source: Stats SA (2016b)

2 OECD defines the producer price index (PPI) as a measure of the change in the prices of goods either as they

leave their place of production or as they enter the production process. The PPI can be used as an economic

indicator of inflation, as an escalator in contracts and as a deflator in the calculation of the national accounts.

Food products

Indices % change between

Weight 2015: Q4 2016:

Q3

2016:

Q4

2015: Q4

and

2016: Q4

2016: Q3

and

2016: Q4

Final manufactured

goods (Headline PPI)

100 120,4 127,3 128,6 6,8 1,0

Food products

26,3 125,3 138,4 140,8 12,4 1,7

Meat and meat

products

4,5 127,2 129,2 136,9 7,6 6,0

Fish and fish products

1,6 135,4 148,9 156,2 15,4 4,9

Fruit and vegetables

2,4 117,6 129,0 132,6 12,8 2,8

Oils and fats

0,5 121,1 134,4 134,2 10,8 -0,1

Dairy products

3,3 122,6 139,0 139,0 13,4 0,0

Grain mill products

1,8 121,0 144,2 138,0 14,0 -4,3

Starch and starch

products, animal feeds

1,6 127,4 140,3 142,3 11,7 1,4

Other food products

0,9 125,7 142,5 143,2 13,9 0,5

Bakery products

6,9 131,8 146,7 147,4 11,8 0,5

Sugar 1,9 114,1 140 ,8 141,0 23,6 0,1

4

Table 2.3 shows import unit values of selected food products. During the current period, the

imported unit values for total food product and grain mill products registered a negative

growth of 5,7% and 14,0%, respectively, while fats and oils grew by 1,2%

Table 2.3: Import unit value index of food products

Source: Stats SA (2016c)

2.2 PRODUCTION

Source: Statistics SA (2016d)

Figure 2.1 presents a physical volume of production for food products division items from

2011: Q4 to 2016: Q4. The quarter-to-quarter physical volume of production of dairy products

decelerated by 2,% from a 1,3% contraction in 2016: Q4, ‘’other food products’’ contracted

by 0,2% as compared to a 1,1% growth previously, grain mill products rebounded by 1,2%

from 1,9% in the last quarter and meat and meat products registered an improved negative

growth of 1,2% from a 2,4% contraction registered in 2016: Q4.

50

60

70

80

90

100

110

120

130

2011: Q

4

2012: Q

1

20

12

: Q

2

2012: Q

3

2012: Q

4

2013: Q

1

2013: Q

2

2013: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

2016: Q

4 In

de

x (

2010 =

100)

Figure 2.1: Seasonally adjusted physical volume of production:

food products

Meat, fish, fruit etc Dairy products

Grain mill products Other food products

Food products

Indices % change between

2015: Q4 2016: Q3 2016: Q4 2016: Q4

and

2016: Q4

2016: Q3

and

2016: Q4

Food (total) 100,8 110,7 104,4 3,6 -5,7

Fats and oils 94,7 100,7 101,9 7,6 1,2

Grain mill products 110,4 125,6 108,0 -2,2 -14,0

5

Production capacity

Table 2.4: Utilisation and reasons for underutilisation of production capacity by large

enterprises: Food products (percentage)

Period Utilisation Reasons for underutilisation

Total

under-

utilisation

Shortage of Insufficient

demand

Other

Raw

materials

Labour

Skilled Semi and

unskilled

2015: Q4 81,7 18,3 1,9 1,1 10,8 10,8 4,5

2016: Q3 83,2 16,8 2,2 1,0 9,7 9,7 3,7

2016: Q4 82,4 17,6 1,8 1,5 9,7 9,7 4,3

Source: Statistics SA (2016e)

The utilisation of production capacity by large enterprises of food products showed a

marginal increase year-on-year and marginal decrease quarter-to-quarter (see Table 2.4).

Insufficient demand and a shortage of semi and unskilled labour were the main reasons for

underutilisation during the current period.

2.3 VALUE OF SALES

Source: Statistics SA (2016d)

Figure 2.2 above shows the seasonally adjusted value of sales for the food products division.

During 2016: Q4, the value of sales for food products moderated by 0,5% as compared to the

3,0% growth registered in the previous quarter. Similarly, the year-on-year value of sales

moderated by 10,7% following a 13,2% previously. The graph illustrates a pattern of sales

performance over a period of five years. It can be seen that value of sales for food products

over the years has been increasing steadily. Figure 2.3 shows the performance of food items

20 000

5 020 000

10 020 000

15 020 000

20 020 000

25 020 000

20

11

: Q

4

2012: Q

1

2012: Q

2

2012: Q

3

2012: Q

4

2013: Q

1

2013: Q

2

2013: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

R'm

illio

n

Figure 2.2: Seasonally adjusted value of sales (current prices):

food products

6

under the food products division during the current period. The dairy and ‘’other food

products’’ division moderated by 0,6% and 0,4% as compared to growth of 1,5% and 6,2%,

respectively in the last quarter. However, dairy products moderated by 0,6%, while grain mill

products increased by 1,6% during the period.

Source: Statistics SA (2016d)

Wholesale and retail sales3

The current value of wholesale and retail sales of food, beverages and tobacco are given in

Figure 2.4. During 2016: Q4, the quarter-to-quarter wholesale of food, beverages and

tobacco grew by 11,9% following a growth of 7,0% in the last quarter, however, it moderated

by 6,0% year-on-year. Similarly, the quarter-to-quarter retail sales of food, beverages and

tobacco grew by 24,9%, as compared to a 7,4% growth previously and moderated by 13,8%

year-on-year. As a result, the quarter-to-quarter value of income of wholesale and retail sales

of food, beverages and tobacco increased from R25 754,3 million and R5 765,6 million in the

last quarter to R28 831,0 million and R7 198, 6 million, respectively during the period.

3 Statistics South Africa (Stats SA) conducts a monthly survey covering enterprises in the wholesale and retail trade industry.

The results of the monthly wholesale and retail trade sales survey are used to compile estimates of the gross domestic product (GDP) and its components, which are used in monitoring the state of the economy and formulation of economic policy. These statistics are also used in the analysis of comparative business and industry performance.

50

2 000 050

4 000 050

6 000 050

8 000 050

10 000 050

12 000 050

14 000 050

2011: Q

4

2012: Q

1

2012: Q

2

2012: Q

3

2012: Q

4

2013: Q

1

2013: Q

2

2013: Q

3

20

13

: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

Ind

ex (

2010 =

100)

Figure 2.3: Seasonally adjusted value of sales (current prices):

food products

Meat , fish, fruit etc Dairy products

Grain mill products Other food products

7

Source: Statistics SA (2016f, 2016g)

2.4 INCOME FROM FOOD SALES IN THE SERVICE INDUSTRY6

Figure 2.5 and Figure 2.6 below shows the income from food sales4 in the service industry

which includes food sales in restaurants and coffee shops5, take-away and fast food outlets6

and catering services7. Figure 2.5 indicates that during 2016: Q4, the income from food sales

in the service industry accelerated by 11,7% following 5,6% growth registered in the previous

quarter, however, it moderated by 8,8% year-on-year as compared to 9,0% growth

previously. As a result, the total income increased from R3 892,0 million in the last quarter to

R4 346,8 million in the current period. Figure 2.6 below illustrates the breakdown in total

income growth for service industries, i.e., restaurants and coffee shops8, take-away and fast

food outlets9 and catering services. During the period under review, the restaurants and

coffee shops10, take-away and fast food outlets grew by 16,4% and 12,3% as compared to

the 5,5% and 5,4% respective growth recorded previously. However, catering services

contracted by 1,7% from a 6,4% growth in the last quarter. On the other hand, the year-on-

4 Income from food sales in the service industry refers to income from the sale of meals and non-alcoholic drinks.

5 Restaurants and coffee shops refers to enterprises involved in the sale and provision of meals and drinks, ordered from a

menu, prepared on the premises for immediate consumption and with provided seating. 6 Take-away and fast food outlet refers to enterprises involved in the sale and provision of meals and drinks, ordered from a

menu, prepared on the premises for takeaway purposes in a packaged format, at a stand or in a location, with or without provided seating. 7 Catering services refers to enterprises involved in the sale and supply of meals and drinks prepared on the premises on a

contract basis and brought to other premises chosen by the person ordering them, to be served for immediate consumption to guests or customers. Catering services also include bars, taverns, other drinking places, ice-cream parlours, etc. 8 Restaurants and coffee shops refers to enterprises involved in the sale and provision of meals and drinks, ordered from a

menu, prepared on the premises for immediate consumption and with provided seating. 9 Take-away and fast food outlet refers to enterprises involved in the sale and provision of meals and drinks, ordered from a

menu, prepared on the premises for takeaway purposes in a packaged format, at a stand or in a location, with or without provided seating. 10

Restaurants and coffee shops refers to enterprises involved in the sale and provision of meals and drinks, ordered from a menu, prepared on the premises for immediate consumption and with provided seating.

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

2011: Q

4

2012: Q

1

2012: Q

2

2012: Q

3

2012: Q

4

2013: Q

1

20

13

: Q

2

2013: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

20

15

: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

R m

illio

n

Figure 2.4: Wholesale and retail trade sales of food, beverages

and tobacco (current prices)

Wholesale Retail

8

year restaurants and coffee shops grew by 11,6%, take-away and fast food outlets

moderated by 9,6% and catering services contracted by 1,2%.

Source: Statistics SA (2016h)

Source: Statistics SA (2016h)

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

20

11

: Q

4

2012: Q

1

2012: Q

2

2012: Q

3

2012: Q

4

2013: Q

1

2013: Q

2

2013: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

20

16

: Q

2

2016: Q

3

2016: Q

4

R m

illio

n

Figure 2.5: Income from food sales in the service industry

500

1 000

1 500

2 000

2 500

2011: Q

4

2012: Q

1

2012: Q

2

2012: Q

3

2012: Q

4

2013: Q

1

20

13

: Q

2

2013: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

20

16

: Q

3

2016: Q

4

R m

illio

n

Figure 2.6: Income from food sales in the service industry

Restaurants and coffee shops Take-away/fast food outlets

Catering services

9

2.5 TRADE

Main food export destinations and products

Figure 2.7 below shows food export destination share of the continents. During 2016: Q4,

Africa constituted the main export destination of food by 58%, followed by Asia and Europe

by 20% and 16%, respectively. The Americas and Oceania altogether accounted for 6% of

the total food export. The trend during the past five years shows that Africa still remains the

biggest share of the continent when it comes to food export, while the Americas and Asia’s

share still remains marginal over the period (see Figure 2.8).

Source: Quantec EasyData (2016)

Source: Quantec EasyData (2016)

Africa

58%

Americas

4%

Asia

20%

Europe

16%

Oceania

2%

Figure 2.7: The food export destinations' share of continents in

2016: Q4

0

10

20

30

40

50

60

70

80

Figure 2.8: The food export destination's share of the

continents

(2011: Q4 – 2016: Q4)

Africa Europe Asia Americas

10

Figure 2.9 shows the food export destinations’ share of the main regions11 in 2016: Q4.

Among the main regions, SACU (Excluding, RSA) (32%), accounted for the highest share of

food export, followed by SADC (Excluding SACU) by 27%. NAFTA, Eastern Asia, South Eastern

Asia, Western Asia and (Australia and New Zealand) accounted for 25% combined of the

total share, while the European Union accounted for 16% of the share during the period.

Source: Quantec EasyData (2016)

Source: Quantec EasyData (2016)

Figure 2.10 above shows the top four countries for food export destinations during 2016: Q4.

During the period under review four African countries, Namibia, Botswana, Mozambique,

11

The main regions which are included in the analysis are the top eight regions: SADC, Western Africa, EU; NAFTA

(North Atlantic Free Trade Area consisting of the USA, Canada and Mexico); Eastern Asia (includes China, Japan,

North Korea, South Korea); Western Asia (mostly Middle East countries); South Central Asia (include India, Pakistan

and Bangladesh) and Australia and New Zealand.

SADC

(excluding

SACU)

27%

SACU

(Excluding

RSA)

32%

NAFTA

3%

Eastern Asia

11%

South-

eastern

Asia

3%

Western

Asia

6%

European

Union

16%

Australia and

New Zealand

2%

Figure 2.9: The food export destinations' share of main regions in

2016: Q4

0

2

4

6

8

10

12

Na

mib

ia

Bo

tsw

an

a

Mo

zam

biq

ue

Zim

ba

bw

e

Leso

tho

Za

mb

ia

Sw

azi

lan

d

Ch

ina

Ho

ng

Ko

ng

Ge

rma

ny

%

Figure 2.10: The share of top ten food export destination

countries in 2016: Q4

11

Zimbabwe, Zambia and Lesotho had the highest share of food export, while from Asia it was

China and Hong Kong, while from Europe, it was Germany. Table 2.5 presents the major

exported food products during 2016: Q4 and Table 2.6 show the year-on-year high and low

export performers of food products during the current quarter of review by comparing the

export values of the present quarter to the same quarter of the previous year (year-on-year).

Table 2.5: Major exported food products in 2016: Q4

HS Code Food product Total amount (R

Million)

HST100630 Semi-milled or wholly milled rice, whether or not polished

or glazed

206,9

HST210410 Soups and broths and preparations 184,6

HST040690 Other cheese 91,71

HST210500 Ice cream and other edible ice, whether or not

containing cocoa

90,9

HST110220 Maize (corn) flour 86,9

HST100640 Broken rice 84,6

HST210320 Tomato ketchup and other tomato sauces 76,8

HST190110 Preparations for infant use, put up for retail sale 52,5

HST190120 Mixes and doughs for the preparation of bakers' wares

of heading

47,6

HST190230 Other pasta 47,1

HST151800 Animal or vegetable fats and oils and their fractions,

boiled, oxidised, dehydrated, sulphurised, blown,

polymerised by heat in vacuum or in inert gas

31,1

HST210330 Mustard flour and meal and prepared mustard 15,0

HST210130 Roasted chicory and other roasted coffee substitutes

and extracts, essences and concentrates thereof

14,2

HST100890 Other cereals 13,6

HST230110 Flours, meals and pellets, of meat or meat offal; greaves 11,5

HST040510 Butter 6,3

12

HST190532: Waffles and wafers 4,6

HST100620 Husked (brown) rice 3,9

HST190220 Stuffed pasta, whether or not cooked or otherwise

prepared

3,6

HST110510 Flour, meal and powder 2,9

HST110520 Flakes, granules and pellets 2,0

HST190300 Tapioca and substitutes therefor prepared from starch,

in the form of flakes, grains, pearls, siftings or in similar

forms.

1,1

HST110814 Manioc (cassava) starch 1,0

HST150410 Fish-liver oils and their fractions 0,7

HST151550 Sesame oil and its fractions 0,6

HST170250 Chemically pure fructose 0,5

HST151530 Castor oil and its fractions 0,2

Source: Quantec EasyData (2016)

Table 2.6: Export performance of food products

HS Code Food product Changes

compared to a

year ago

(R million)

High performers

HST150420

Fats and oils and their fractions of fish, other than liver oils

210 340,3

HST180400

Cocoa butter, fat and oil

3 228,5

HST190300 Tapioca and substitutes therefor prepared from starch, in

the form of flakes, grains, pearls, siftings or in similar forms

88,5

HST151620

Vegetable fats and oils and their fractions

44,9

HST180500 Cocoa powder, not containing added sugar or other

sweetening matter

34,9

13

HST190420 Prepared foods obtained from unroasted cereal flakes or

from mixtures of unroasted cereal flakes and roasted

cereal flakes or swelled cereals

26,9

HST190410 Prepared foods obtained by the swelling or roasting of

cereals or cereal products

25,8

HST210230

Prepared baking powders

20,8

HST151710

Margarine, excluding liquid margarine

19,6

HST180610 Cocoa powder, containing added sugar or other

sweetening matter

16,2

HST210500 Ice cream and other edible ice, whether or not

containing cocoa

13,5

HST190220

Stuffed pasta, whether or not cooked or otherwise

prepared

12,0

HST210410

Soups and broths and preparations therefor

11,5

HST210320

Tomato ketchup and other tomato sauces

9,4

HST110510

Flour, meal and powder

9,4

HST190531

Sweet biscuits

4,9

HST190120 Mixes and doughs for the preparation of bakers' wares of

heading

2,5

HST210310

Soya sauce

2,1

Low performers

HST151800 Animal or vegetable fats and oils and their fractions,

boiled, oxidised, dehydrated, sulphurised, blown,

polymerised by heat in vacuum or in inert gas or otherwise

chemically modified, excluding those of heading inedible

mixtures

-0,4

HST230110

Flours, meals and pellets, of meat or meat offal; greaves

-4,5

HST190532

Waffles and wafers

-6,0

HST210330

Mustard flour and meal and prepared mustard

-18,5

HST170410

Chewing gum, whether or not sugar-coated

-18,7

14

HST190110

Preparations for infant use, put up for retail sale

-22,6

HST151530

Castor oil and its fractions

-50,3

HST151550

Sesame oil and its fractions

-69,2

HST152110

Vegetable waxes

-94,3

HST230320 Beet-pulp, bagasse and other waste of sugar

manufacture

-96,2

Source: Quantec EasyData (2016)

Main source of food imports and imported food products

South Africa’s main source of food import during 2016:Q4 is presented in Figure 2.11. South

Africa imported 38% of its food from Europe, followed by Asia (32%). The share of the

Americas (24%) is also substantial as a source of imports then followed by Africa with a share

of 5%. Oceania’s contribution is very marginal at 1%. Figure 2.12 indicates that during the

past five years, Europe and Asia has become the major source of food imports while Africa is

still below 15%.

Source: Quantec EasyData (2016)

Africa

5%

Americas

24%

Asia

32%

Europe

38%

Oceania

1%

Figure 2.11: The share of continents as a source of food import

in 2016: Q4

15

Source: Quantec EasyData (2016)

As the main trading region, the EU accounts approximately 38% of the total food imports,

followed by South Eastern Asia (23%), South America (21%), Eastern Asia (8%) and NAFTA (3%)

during the period. SACU (Excluding RSA) accounted 4% share during 2016: Q4 (see Figure

2.13).

Source: Quantec EasyData (2016)

0

5

10

15

20

25

30

35

40

45 2011: Q

4

2012: Q

1

2012: Q

2

2012: Q

3

20

12

: Q

4

2013: Q

1

2013: Q

2

2013: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

20

14

: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

20

16

: Q

4

Figure 2.12: The share of continents as a source of food import

(2011: Q4 – 2016: Q4)

Africa Americas Asia Europe

SACU

(Excluding

RSA)

4%

South America

21% NAFTA

3%

Eastern Asia

8%

Southeast Asia

22%

European

Union

38%

Others

4%

Figure 2.13: The share of regions as sources of food imports in

2016: Q4

16

Source: Quantec EasyData (2016)

The significant share of food imports were sourced from Argentina (14,8%), Indonesia (8,7%),

Spain (10,5%), China (8,7%), Malaysia (8,2%), Brazil (5,4%), Thailand (2,8%), the United

Kingdom (2,8%), Germany (2,4%) and the United States (2,4%)(see Figure 2.14). Table 2.6

presents the major imported food products during 2016: Q4.

Table 2.6: Top 30 imported food products in 2016: Q4

HS Code Food product Total amount (R

million)

HST230400

Oil-cake and other solid residues, whether or not

ground or in the form of pellets, resulting from the

extraction of soya bean oil

672,6

HST230910 Dog or cat food, put up for retail sale

191,3

HST170290

Other, including invert sugar and other sugar and

sugar syrup blends containing in the dry state 50% by

weight of fructose

140,2

HST040630 Processed cheese, not grated or powdered

83,9

HST170410 Chewing gum, whether or not sugar-coated

78,5

HST180400 Cocoa butter, fat and oil

68,1

HST040690 Other cheese

66,4

HST190531 Sweet biscuits

66,4

0

2

4

6

8

10

12

14

16

Arg

en

tin

a

Ind

on

esi

a

Sp

ain

Ch

ina

Ma

laysi

a

Bra

zil

Tha

ilan

d

Un

ite

d K

ing

do

m

Ge

rma

ny

Un

ite

d S

tate

s

%

Figure 2.14: The share of top ten countries as sources of food

import in 2016: Q4

17

HST110100 Wheat or meslin flour

55,3

HST180500 Cocoa powder, not containing added sugar or other

sweetening matte

53,9

HST040410

Whey and modified whey, whether or not

concentrated or containing added sugar or other

sweetening matter

36,4

HST100640 Broken rice

35,5

HST190532 Waffles and wafers

21,2

HST210500 Ice cream and other edible ice, whether or not

containing cocoa

16,0

HST040610 Fresh (unripened or uncured) cheese, including whey

cheese and curd

13,6

HST110812 Maize (corn) starch

10,4

HST210310 Soya sauce

10,3

HST040620 Grated or powdered cheese, of all kinds

9,8

HST210330 Mustard flour and meal and prepared mustard

6,5

HST200990 Mixtures of juices

5,3

HST110520 Flakes, granules and pellets

5,2

HST190540 Rusks, toasted bread and similar toasted products

4,9

HST040640 Blue-veined cheese and other cheese containing

veins produced by Penicillium roqueforti

4,6

HST040310 Yogurt

4,2

HST151000

Other oils and their fractions, obtained solely from

olives, whether or not refined, but not chemically

modified, including blends of these oils or fractions with

oils or fractions of heading.

3,9

HST190510 Crispbread

2,4

HST190300

Tapioca and substitutes, therefor prepared from

starch, in the form of flakes, grains, pearls, siftings or in

similar forms

1,8

18

HST110510 Flour, meal and powder

0,5

HST040510 Butter

0,3

Source: Quantec EasyData (2016)

Source: Quantec EasyData (2016)

During 2016: Q4, quarter-to-quarter exports of food products decelerated by 0,9% following a

contraction of 0,3% previously. However, it moderated by 4,1% year-on-year. On the other

hand, the quarter-to-quarter and year-on-year imports for food products moderated by 5,0%

and 7,9% following an 11,5% and 17,7% growth registered in the last quarter. As a result, the

quarter-to-quarter trade deficit for food products expanded from R2 533,6 million in 2016: Q3

to R3 411,4 million in the current quarter. (see Figure 2.16).

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

2012: Q

4

2013: Q

1

2013: Q

2

2013: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

R m

illio

n

Figure 2.15: Quarterly trade balance of food products

Export Import

19

2.6 EMPLOYMENT

Source: Statistics SA (2016i)

Source: Statistics SA (2016i)

Figure 2.17 shows the number of formal employment of the food products division. The year-

on-year, formal employment of meat, fish, fruit, vegetables, oils and fats, grain mill products

and ‘’other food products’ moderated by 4,3%, 3,6% and 7,4% as compared to the growth

of 4,9%, 4,2% and 12,6%, respectively as recorded in the previous quarter. Whereas the year-

on-year for dairy products grew by 0,7% following a 0,2% growth in the last quarter. On the

150 000

160 000

170 000

180 000

190 000

200 000

210 000

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

Figure 2.16: Total number of formal employment: food

products

0 10 000 20 000 30 000 40 000 50 000 60 000 70 000 80 000 90 000

100 000

20

15

: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

Figure 2.17: Number of formal employment: food products

Production, processing and preservation of meat, fish, fruit,

vegetables, oils and fats Dairy products

Grain mill products, starches and starch products and prepared

animal fat Other food products

20

other hand, the quarter-to-quarter, formal employment of food products division rebounded

by 10,6% for meat, fish, fruit, vegetables, oils and fats, grew by 4,1% for dairy products,

moderated by 1,1% for grain mill products and decelerated by 0,1% for other food products.

As a result in the rebound of total food products by 3,7% as compared to a contraction of

0,9% previously, it represented a total number of 7 361 jobs created in the food division under

the period from 1 758 jobs shed in the last quarter.

2.7 OUTLOOK

Table 2.7: Net balance12 of BER manufacturing survey: food products

2016: Q2 2016: Q3 2016: Q4 2017: Q1*

Domestic sales volumes 51 34 24 -6

Export sales volumes 22 37 24 33

Production volumes 30 28 19 -25

Domestic order volumes received 56 35 11 -9

Export order volumes received 14 25 7 21

General business conditions -31 10 -28 -16

Number of factory workers -12 -19 2 -24

Fixed investment -34 -5 -30 -51

Business confidence13 35 62 40

Expected volume of goods imported in

12 months’ time 13 -5 -13

Expected volume of goods exported in

12 months’ time 15 38 28

Expected real investment in machinery

and equipment in 12 months’ time -19 10 -41

12 BER calculates the net balance statistics by subtracting the percentage of the respondents replying “down” from

the percentage replying “up” to a particular question. Respondents are asked to compare the current quarter’s

experience to that of a year ago. A positive net balance implies an improvement (i.e., positive year-on-year growth)

and vice versa. Therefore, the net balance varies from -100 to 100 where -100 is the most negative response; 0 is a

situation of no change and 100 is the most positive response.

13

BER calculates the business confidence index by asking respondents to rate current business conditions as “satisfactory” or “unsatisfactory.” Then the index is derived as a gross percentage of the respondents replying “satisfactory.” A value of 50 is indicative of neutrality, 100 indicative of extreme confidence and 0 of extreme lack of confidence. An index greater than 50 shows the majority of respondents are satisfied with the prevailing economic conditions.

21

2016: Q2 2016: Q3 2016: Q4 2017: Q1*

Expected business conditions in 12

months’ time -16 24 -28

*Expected Source: BER (2016)

A survey by the Bureau for Economic Research (BER) on food manufacturing is presented in

Table 4.5. The survey shows that the year-on-year outlook for 2017: Q1 is negative for most

variables except sales volumes.

3. BEVERAGES

According to SIC classification, beverages are coded 305 and it comprises the following

beverage products:

Distilling, rectifying and blending of spirits; ethyl alcohol production from fermented

materials; manufacture of wine

Manufacture of beer and other malt liquors and malt

Breweries, except sorghum beer breweries

Sorghum beer breweries

Manufacture of malt

Manufacture of soft drinks; production of mineral waters.

3.1 PRICE

Table 3.1 shows the consumer price indices and export unit value of beverages. The year-on-

year and quarter-to-quarter consumer price inflation for alcoholic beverages grew by 6,9%

and 0,9%, respectively in the period under review. The consumer price indices for alcoholic

beverages grew by 0,5% during the quarter. Items that increased under the alcoholic

beverages are spirits and wine, amongst others, which grew by 0,6% and 1,0%, respectively.

Similarly, the non-alcoholic beverages grew by 1,5% during the period. Amongst the items

under the category was hot beverages and cold beverages that grew by 1,5% and 1,3%,

respectively. The table below also depicts the producer price index of beverages which

grew by 2,5% in the current quarter. However, the export unit value of beverages registered

a negative growth of 2,1% in the same period.

22

Table 3.1: Price indices of beverages

Source: Stats SA (2016a, 2016b, 2016

3.2 PRODUCTION

Source: Statistics SA (2016d)

50

60

70

80

90

100

110

120

2010: Q

4

2011: Q

1

2011: Q

2

2011: Q

3

2011: Q

4

2012: Q

1

2012: Q

2

2012: Q

3

2012: Q

4

2013: Q

1

2013: Q

2

2013: Q

3

2013: Q

4

20

14

: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

Ind

ex (

2010 =

100)

Figure 3.1: Seasonally adjusted physical volume of production:

beverages

Beverages products

Indices % change between

Weight 2015: Q4 2016: Q3 2016:

Q4

2015: Q4

and

2016: Q4

2016: Q3

and

2016: Q4

Consumer price indices

All items (CPI

headline)

100 116,4 123,3 124,4 6,9 0,9

Alcoholic

beverages

3,9 124,2 130,4 131,0 5,4 0,5

Spirits

0,8 117,0 122,5 123,2 5,3 0,6

Wine

0,7 125,9 132,1 132,2 5,0 0,1

Beer

2,5 119,8 125,7 125,8 5,0 0,1

Non-alcoholic

beverages

1,2 114,0 123,2 124,9 9,5 1,4

Hot beverages

0,3 123,2 141,9 144,1 17,0 1,5

Cold beverages

0,9 110,7 116,3 117,8 6,5 1,3

Producer price index

Beverages

8,5 119,4 125,8 128,9 8,0 2,5

Export unit value

Beverages

135,2 104,9 102,8 100,6 -4,2 -2,1

23

Figure 3.1 presents the seasonally adjusted physical volume of production for beverages.

During 2015: Q4, the volume of production for beverages contracted year-on-year and

quarter-to-quarter by 0,8% and 0,5% in the current quarter, following growths of 0,1% and

1,1%, respectively as recorded in the previous quarter.

Production capacity

Table 3.2: Utilisation and reasons for underutilisation of production capacity by large

enterprises: Beverages division (percentage)

Period Utilisation Reasons for underutilisation

Total

under-

utilisation

Shortage of Insufficient

demand

Other

Raw

materials

Labour

Skilled Semi and

unskilled

2015: Q4 88,3 11,7 1,0 0,8 10,8 7,2 2,6

2016: Q3 85,1 14,9 2,4 1,4 9,7 6,6 4,3

2016: Q4 88,1 11,9 2,1 1,0 9,7 6,3 2,1

Source: Statistics SA (2016e)

Table 3.2 shows that the year-on-year and quarter-to-quarter utilisation capacity grew during

2016: Q4. Insufficient demand and shortage of semi and unskilled labour remained the main

reasons for underutilisation in the period under review.

3.3 VALUE OF SALES

Source: Statistics SA (2016d)

10 000

2 010 000

4 010 000

6 010 000

8 010 000

10 010 000

12 010 000

2011: Q

4

2012: Q

1

20

12

: Q

2

20

12

: Q

3

2012: Q

4

2013: Q

1

2013: Q

2

2013: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

R m

illio

n

Figure 3.2: Seasonally adjusted value of sales (current

prices): beverages

24

During 2016: Q4, the seasonal adjusted value of sales of beverages rebounded by 0,6%

quarter-to-quarter following a 0,4% contraction registered in the last quarter. However, it

moderated by 5,5% year-on-year as compared to a 5,6% growth previously. (see Figure 4.6).

Due to the strong linkages between agro-processing and primary agriculture, the growth of

the beverages division during the period can be attributed to the bountiful harvest

experienced by farmers in the current season.

3.4 INCOME FROM BAR SALES IN THE SERVICE INDUSTRY14

Figure 3.3 shows the income from bar sales in the food and beverages service industry in

2016: Q4. During this period, the quarter-to-quarter income from bar sales in the services

industry grew modestly by 11,7% as compared to a 5,6% growth registered previously.

However, it moderated by 8,8% following a 9,0% growth in the last quarter. That resulted in

the total income growth of R 4 346,8 million in the current quarter from R3 892,0 million

registered in 2016: Q3.

Source: Statistics SA (2016h)

14 Income from bar sales refers to income from liquor sales.

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

2011: Q

4

2012: Q

1

2012: Q

2

2012: Q

3

2012: Q

4

2013: Q

1

20

13

: Q

2

2013: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

20

16

: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

R m

illio

n

Figure 3.3: Income from food sales in the service industry

25

Source: Statistics SA (2016h)

Figure 3.4 shows the services performance of the food sales in the services industry. The

services are restaurants and coffee shops, take aways/fast food outlets and catering

services. During the current review period, the restaurants and coffee shops, take aways/fast

food outlets accelerated by 16,4% and 12,3% following growths of 3,5% and 5,4%,

respectively. However, the catering services contracted by 1,7% as compared to a 6,4%

registered in the last quarter. The year-on-year restaurants and coffee shops increased

substantially by 11,6%, take aways/fast food outlets moderated by 9,6% and catering

services contracted by 1,2%.

3.5 TRADE

Main export destinations and food products

Figure 3.5 shows during the quarter under review; Africa is by far the largest export

destination for South African beverages. It accounted for 58% of the total export followed by

Asia (20%), Europe (16%), the Americas (4%) and Oceania (2%). The trend of the export

destination’s share during the past five years shows that Africa was the biggest, followed by

Europe and Asia. The Americas and Oceania share were marginal. (see Figure 3.6).

500

1 000

1 500

2 000

2 500

2011: Q

4

2012: Q

1

2012: Q

2

2012: Q

3

2012: Q

4

2013: Q

1

20

13

: Q

2

2013: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

20

15

: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

R m

illio

n

Figure 3.4: Income from food sales in the service industry

Restaurants and coffee shops Take-away/fast food outlets

Catering services

26

Source: Quantec EasyData (2016)

Source: Quantec EasyData (2016)

Among the main trading regions, the European Union (36%) accounted for most of the total

beverages export share, followed by SADC (Excluding SACU), which accounted for 19%,

followed by NAFTA (9%), Eastern Asia (8%), Southeast Asia (3%) and Eastern Europe (2%). (see

Figure 3.7).

Africa

58%

Americas

4%

Asia

20%

Europe

16%

Oceania

2%

Figure 3.5: The beverages export destination's share of

continents in 2016: Q4

0

10

20

30

40

50

60

%

Figure 3.6: The beverages export destination's share of the

continents in 2016: Q4

(2011-2016)

Europe Africa Americas Asia

27

Source: Quantec EasyData (2016)

Source: Quantec EasyData (2016)

Figure 3.8 above shows the top ten countries that South Africa exported beverages to during

2016: Q4. The following are the main countries that constituted a huge share of beverages

export during the quarter: Namibia (9,6%), the United Kingdom (9,1%), Germany (6,9%),

Botswana (5,5%), Mozambique (5,4%), China (4,8%), the United States (4,7%), the Netherlands

(4,4%), Zambia (3,5%) and Canada (3,5%). Figure 3.4 shows high and low export performers

of beverages during 2016: Q4 by comparing the export values of the present quarter to the

same quarter of the previous year (year-on-year).

SADC

(Excluding

SACU)

19%

SACU

(Excluding

RSA)

23%

NAFTA

9%

Eastern Asia

8%

Southeast Asia

3%

Eastern

Europe

2%

European

Union

36%

Figure 3.7: The share of top beverages export destination

regions in 2016: Q4

0

2

4

6

8

10

12

Na

mib

ia

Un

ite

d K

ing

do

m

Ge

rma

ny

Bo

tsw

an

a

Mo

zam

biq

ue

Ch

ina

Un

ite

d S

tate

s

Ne

the

rla

nd

s

Za

mb

ia

Ca

na

da

%

Figure 3.8: The share of top ten beverages export destination

countries in 2016: Q4

28

Table 3.3: Major exported beverages products in 2016: Q4

HS Code Food product Total amount (R

million)

HST220710 Undenatured ethyl alcohol of an alcoholic

strength by volume of 80% vol. or higher

329,3

HST220600 Other fermented beverages (for example,

cider, perry, mead); mixtures of fermented

beverages and mixtures of fermented

beverages and non-alcoholic beverages, not

elsewhere specified or included

248,7

HST220300 Beer made from malt 246,4

HST220410 Sparkling wine 104,1

HST220720 Ethyl alcohol and other spirits, denatured, of

any strength

102,0

HST220830 Whiskies 100,3

HST220820 Spirits obtained by distilling grape wine or

grape marc

88,5

HST220860

Vodka

80,3

HST220850 Gin and Geneva 36,2

HST220110 Mineral waters and aerated waters 28,3

HST220840 Rum and other spirits obtained by distilling

fermented sugar cane products

27,3

HST220900 Vinegar and substitutes for vinegar obtained

from acetic acid

10,5

Source: Quantec EasyData (2016)

3.4: Export performance of beverages in 2016: Q4

HS Code Beverages Changes compared

to a year ago

(R million)

High performers

HST090230 Black tea (fermented) and partly fermented

tea, in immediate packings of a content not

exceeding 3 kg

113,9

HST220850

Gin and Geneva

75,1

29

HST220860

Vodka

74,1

HST220840 Rum and other spirits obtained by distilling

fermented sugar cane products

46,2

HST220210 Waters, including mineral waters and aerated

waters, containing added sugar or other

sweetening matter or flavoured

26,1

HST220900 Vinegar and substitutes for vinegar obtained

from acetic acid.

4,9

HST220870

Liqueurs and cordials

1,5

Low performers

HST220710 Undenatured ethyl alcohol of an alcoholic

strength by volume of 80% vol. or higher

-0,3

HST220720 Ethyl alcohol and other spirits, denatured, of

any strength

-0,3

HST090210 Green tea (not fermented) in immediate

packings of a content not exceeding 3 kg

-1,5

HST220820 Spirits obtained by distilling grape wine or

grape marc

-5,9

HST220300 Beer made from malt -6,6

HST220110

Mineral waters and aerated waters

-8,9

HST220830 Whiskies -11,8

HST220600 Other fermented beverages (for example,

cider, perry, mead); mixtures of fermented

beverages and mixtures of fermented

beverages and non-alcoholic beverages, not

elsewhere specified or included

-17,9

HST220410

Sparkling wine

-21,6

HST090240 Other black tea (fermented) and other partly

fermented tea

-44,9

HST090220

Other green tea (not fermented)

-48,9

HST090300

Maté

-88,6

Source: Quantec EasyData (2016)

30

Main imported beverage products and the source

Figure 3.9 illustrates the share of continents as a source of beverage import in 2016: Q4.

Europe, which accounted 69% import share, was the largest source of beverage import

during 2014: Q4, followed by Africa (15%), while the Americas, Asia and Oceania altogether

accounted for 16% of the total beverages import during the period. Figure 3.10 shows that

during the past five years, Europe, followed by Africa, is the key source of beverages imports.

Both continents contributed to an average of 74% of the total beverages imports from 2011-

2016.

Source: Quantec EasyData (2016)

Source: Quantec EasyData (2016)

Africa

15%

Americas

11%

Asia

4% Europe

69%

Oceania

1%

Figure 3.9: The share of continent's as a source of beverages

import in 2016: Q4

0

10

20

30

40

50

60

70

80

90

2011: Q

4

2012: Q

1

20

12

: Q

2

2012: Q

3

2012: Q

4

2013: Q

1

2013: Q

2

20

13

: Q

3

2013: Q

4

2014: Q

1

2014: Q

2

2014: Q

3

2014: Q

4

2015: Q

1

2015: Q

2

2015: Q

3

2015: Q

4

2016: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

Figure 3.10: The beverages import destination's share of the

continents

(2011 – 2016)

Africa Americas Asia Europe

31

Among the top trading regions, the EU (70%) still accounts as the largest share of beverages

import followed by SACU (Excluding SADC) (15%) and NAFTA (6%). Western Asia and SADC

(Excluding SACU) played a minor role as a source of import for beverages; they accounted

for 2% contribution each (see Figure 3.11).

Source: Quantec EasyData (2016)

Source: Quantec EasyData (2016)

SACU

(Excluding

RSA)

15% South America

5%

NAFTA

6%

Western Asia

2%

Western

Europe Rest

2% European

Union

70%

Figure 3.11: The share of top regions as a source of beverages

import in 2016: Q4

0

5

10

15

20

25

30

Un

ite

d K

ing

do

m

Fra

nc

e

Na

mib

ia

Au

stria

Ne

the

rla

nd

s

Ire

lan

d

Arg

en

tin

a

Be

lgiu

m

Me

xic

o

Ge

rma

ny

%

Figure 3.12: The share of top ten countries as a source of

beverages import in 2016: Q4

32

Figure 3.12 shows the share of the top ten countries as a source of beverages import in 2016:

Q4. Five of the top ten countries that contributed to the share of import beverages in the

world are from the European countries: United kingdom (25,%), France (19,1%) the

Netherlands (4,1%), Belgium (3,0%) and Germany (2,8%), while two are from Latin America,

another two from Oceania, Ireland (4,0%) and Austria (4,2%) and Namibia from Africa

(14,0%).

Table 3.5: Main imported beverages in 2016: Q4

HS Code Food product Total amount (R

million)

HST220830

Whiskies

601,1

HST220300

Beer made from malt

349,0

HST220210 Waters, including mineral waters and aerated

waters, containing added sugar or other

sweetening matter or flavoured

231,4

HST220820 Spirits obtained by distilling grape wine or

grape marc 122,1

HST220410

Sparkling wine

106,5

HST090240 Other black tea (fermented) and other partly

fermented tea

99,0

HST220870

Liqueurs and cordials

62,6

HST220860

Vodka

35,0

HST220710 Undenatured ethyl alcohol of an alcoholic

strength by volume of 80% vol. or higher

27,6

HST220600 Other fermented beverages (for example,

cider, perry, mead); mixtures of fermented

beverages and mixtures of fermented

beverages and non-alcoholic beverages, not

elsewhere specified or included.

26,5

HST220850

Gin and Geneva

21,3

HST220840 Rum and other spirits obtained by distilling

fermented sugar cane products

14,8

HST220900 Vinegar and substitutes for vinegar obtained

from acetic acid

9,5

HST220110

Mineral waters and aerated waters

7,9

HST090230 Black tea (fermented) and partly fermented 5,9

33

tea, in immediate packings of a content not

exceeding 3 kg

HST090210 Green tea (not fermented) in immediate

packings of a content not exceeding 3 kg

4,1

HST090220

Other green tea (not fermented)

2,8

Source: Quantec EasyData (2016)

Source: Quantec EasyData (2016)

During 2016: Q4, the quarter-to-quarter exports of beverages rebounded by 7,4% as

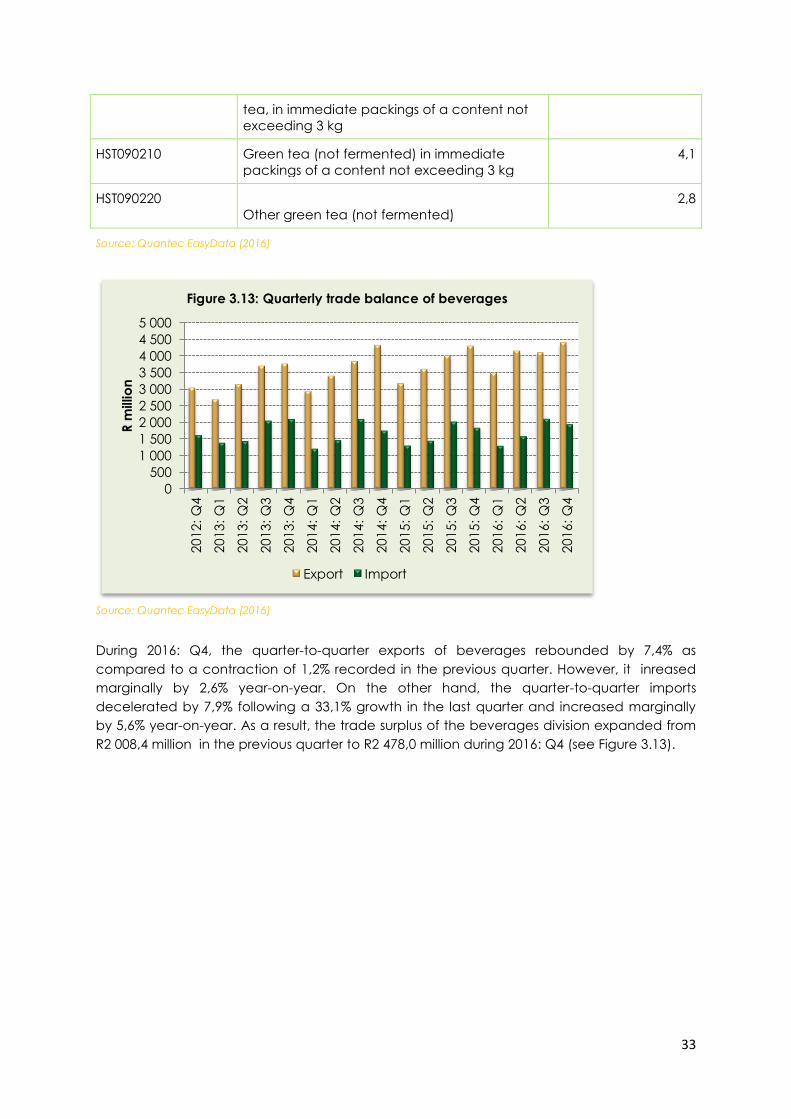

compared to a contraction of 1,2% recorded in the previous quarter. However, it inreased

marginally by 2,6% year-on-year. On the other hand, the quarter-to-quarter imports

decelerated by 7,9% following a 33,1% growth in the last quarter and increased marginally

by 5,6% year-on-year. As a result, the trade surplus of the beverages division expanded from

R2 008,4 million in the previous quarter to R2 478,0 million during 2016: Q4 (see Figure 3.13).

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

20

12

: Q

4

20

13

: Q

1

20

13

: Q

2

20

13

: Q

3

20

13

: Q

4

20

14

: Q

1

20

14

: Q

2

20

14

: Q

3

20

14

: Q

4

20

15

: Q

1

20

15

: Q

2

20

15

: Q

3

20

15

: Q

4

20

16

: Q

1

20

16

: Q

2

20

16

: Q

3

20

16

: Q

4

R m

illio

n

Figure 3.13: Quarterly trade balance of beverages

Export Import

34

3.6 EMPLOYMENT

Source: Quantec EasyData (2016i)

Figure 3.14 shows the number of formal employment of beverages and tobacco products

industry. The quarter-to-quarter of formal employment of beverages and tobacco products

divisions increased marginally by 1,9% following a growth of 1,5% in the previous quarter.

However, the year-on-year and formal employment of beverage and tobacco products

moderated by 2,6% as compared to a 5,6% growth registered in the preceding quarter. As a

result, the total number of formal employment in beverages and tobacco products industries

increased from 42 783 in the previous quarter to 43 592 in 2016: Q4.

3.7 OUTLOOK

Table 3.6: Net balance of BER manufacturing survey: Beverages

2016: Q2 2016: Q3 2016: Q4 2017: Q1*

Domestic sales volumes 36 91 49 30

Export sales volumes 92 80 -57 -3

Production volumes 83 86 16 31

Domestic order volumes received 35 90 40 57

Export order volumes received 92 67 -42 2

37 000

38 000

39 000

40 000

41 000

42 000

43 000

44 000

45 000

2015: Q

2

2015: Q

3

2015: Q

4

20

16

: Q

1

2016: Q

2

2016: Q

3

2016: Q

4

Figure 3.14: Number of formal employment: beverage and

tobacco products

35

2016: Q2 2016: Q3 2016: Q4 2017: Q1*

General business conditions 9 5 -43 -52

Number of factory workers 7 2 15 19

Fixed investment 2 89 40 16

Business confidence 64 88 44

Expected volume of goods imported in

12 months’ time 40 -68 31

Expected volume of goods exported in

12 months’ time 97 91 48

Expected real investment in machinery

and equipment in 12 months’ time 63 2 30

Expected business conditions in 12

months’ time -26 56 -69

*Expected Source: BER (2016)

The survey of the beverages division by BER shows that the year-on-year outlook for 2017: Q1

is positive for all variables except export volumes and general business conditions.

4. CONCLUSION

The global economic activity has witnessed improvement in 2016: Q4, which was observed in

developed economies. The economic performance with respect to emerging market and

developing economies has remained mixed. However, during 2016: Q4, the South African

economy contracted at an annualised rate of 0,3%, following a marginal growth of 0,4% in

the preceding quarter.

During the period, the share of continents as a source of food exports was largely constituted

by Africa, then Asia and Europe. On the other hand, Europe, followed by Asia and the

Americas, constituted a huge share of continents share of food imports whereas Oceania

and Africa constituted a minimal share.

In terms of beverages, Africa, Asia and Europe contributed a large share of beverages

exports during the period, whereas Europe, followed by Africa then the Americas constituted

a huge share of beverages imported during the period to a total of 95% combined.

During 2016: Q4, the seasonally adjusted physical volume of production of the food and

beverages industry stagnated by 1,4% quarter-to-quarter, however, it decelerated by 2,9%

following a 0,3% contraction previously. Sales for food and beverages moderated by 0,5%

from a 3,0% growth recorded in the last quarter, representing a nominal value increase of

R30 826 697 in the current period from R30 658 186 million in 2016: Q3. Despite the stagnant

growth in physical volume of production, the trade deficit of food and beverages widened

by R933,4 million in the current period of review from a R525,2 million registered in the last

quarter.

36

The employment in the food and beverages and tobacco industry rebounded by 3,4%

quarter-to quarter and moderated by 7,1% year-on-year. This represents 244 448 jobs created

in the current period as compared to 240 278 jobs created previously. This quarterly review

assesses the economic performance of the food and beverages industry, given a moderate

global economic growth and a contraction of domestic economic activities recorded

during 2016: Q4.

37

5. REFERENCES

BER (2016), Manufacturing Survey. Bureau for Economic Research, University of Stellenbosch.

Quantec EasyData (2015), RSA International Trade. Accessed in December 2016.

IMF (2017), Global prospects and policies, April 2017. International Monetary Fund.

Reserve Bank (2017), Quarterly Bulletin, March 2017, South African Reserve Bank.

Statistics SA (2016a), Consumer Price Index, various issues. Statistics South Africa.

Statistics SA (2016b), Producer Price Index, various issues. Statistics South Africa.

Statistics SA (2016c), Export and Import Unit Value Indices, various issues. Statistics South

Africa.

Statistics SA (2016d), Manufacturing: Production and Sales, various issues. Statistics South

Africa.

Statistics SA (2016e), Manufacturing: Utilisation of Production Capacity by Large Enterprises.

Statistics South Africa.

Statistics SA (2016f), Wholesale Trade Sales, various issues, Statistics South Africa.

Statistics SA (2016g), Retail Trade Sales, various issues, Statistics South Africa.

Statistics SA (2016h), Food and Beverages, various issues, Statistics South Africa.

Statistics SA (2016i), Quarterly Employment Statistics, various issues. Statistics South Africa.

38

NOTES

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------

--------------------------------------------------------------------------------------------------------------------------------------