quarterly presentation q3 2016 dof subsea group sub/ir/2016/dof subsea... · group of energy and...

TRANSCRIPT

Quarterly Presentation Q3 2016

DOF Subsea Group

DOF Subsea Group

DOF Subsea Group in Brief

3

2005Established

21 256NOK million

total assets(according to management reporting)

Modernhigh-end fleet

and equipment

21owned subsea

vessels

4vessels

on order

2vessels

on charter

63 ROVs,

4 ROVs

on order

First Reserve

Corporation (49%)

1 372employees

DOF Subsea

DOF Subsea Holding(100%)

DOF ASA(51%)

DOF Subsea Group in Brief

• Fleet

• One of the largest subsea vessel owners in the world

• Owns and operates a fleet of 21 vessels, plus 4 newbuilds on order

• In addition, 2 chartered-in vessels as at 30th September 2016

• The market value of owned vessels in operation is about NOK 15.5 billion, with a value

adjusted age of 6.2 years

• Operates 63 ROVs and 4 ROVs on order

• Global organization

• Head office in Bergen

• Regional offices in Australia, Singapore, Norway, UK, Angola, US, Canada and

Brazil

• Total of 1 372 employees

• Onshore: 622

• Offshore: 750

4

Asia Pacific Atlantic Brazil North America

345 467 326 234

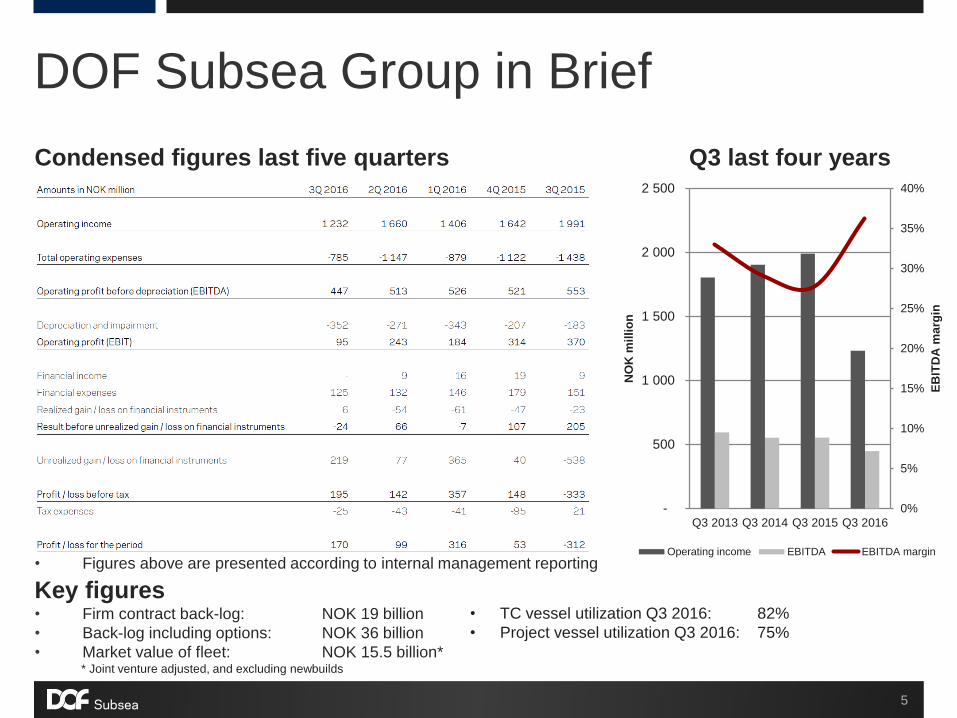

DOF Subsea Group in Brief

Condensed figures last five quarters Q3 last four years

• Figures above are presented according to internal management reporting

Key figures• Firm contract back-log: NOK 19 billion

• Back-log including options: NOK 36 billion

• Market value of fleet: NOK 15.5 billion*

5

0%

5%

10%

15%

20%

25%

30%

35%

40%

-

500

1 000

1 500

2 000

2 500

Q3 2013 Q3 2014 Q3 2015 Q3 2016

EB

ITD

A m

arg

in

NO

K m

illi

on

Operating income EBITDA EBITDA margin

• TC vessel utilization Q3 2016: 82%

• Project vessel utilization Q3 2016: 75%

* Joint venture adjusted, and excluding newbuilds

Recent Events

• Fleet

• First of four PLSVs, Skandi Açu, on-hire with Petrobras from 13th of August

• Delivery of second PLSV, Skandi Buzios, from yard. Vessel in Holland for topside

installation

• On-hire with Petrobras from Q2 2017

• Agreement regarding sale of Skandi Santos to AKASTOR ASA

• Contracts

• Shell Australia awarded DOF Subsea an IMR contract in Asia Pacific for 5 years firm

plus 2 x 2 years options

• Petrobras awarded Skandi Salvador 1 year IMR contract plus 1 year option

• Finance

• Drawdown of 1st tranche on Skandi Buzios at delivery from yard in September 2016

• Refinancing Skandi Singapore

6

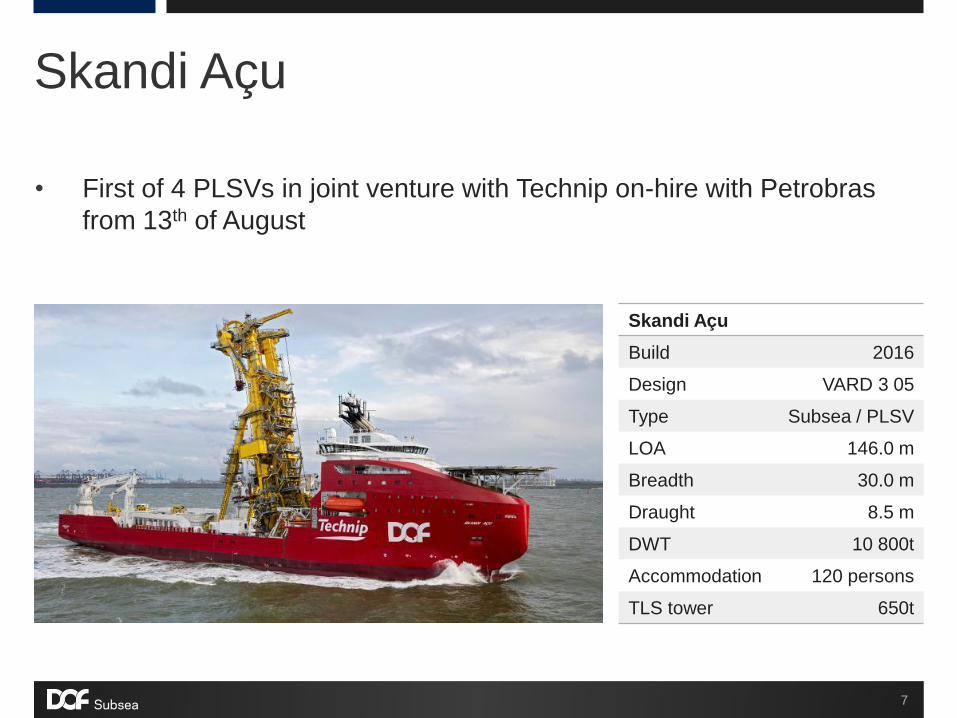

Skandi Açu

• First of 4 PLSVs in joint venture with Technip on-hire with Petrobras

from 13th of August

7

Skandi Açu

Build 2016

Design VARD 3 05

Type Subsea / PLSV

LOA 146.0 m

Breadth 30.0 m

Draught 8.5 m

DWT 10 800t

Accommodation 120 persons

TLS tower 650t

Shell Prelude 5-year IMR Contract

• Shell Australia awarded DOF Subsea a 5 year + 2 x 2 year options for fulltime

Underwater Services and Multi-Purpose Supply Vessel (MPSV) Services to the

Prelude FLNG facility, offshore Australia

• Combination of vessel expertise, subsea operations track-record and shared safety,

environmental and local-content objectives made DOF Subsea competitive

• Established local presence and organizational expertise – combination of Australian

and Norwegian teams

• Client opted for an integrated solution with one supplier

• Differentiated offering from DOF resulted in contract award

8

Integrated work scope:

• Vessel charter

• Project Management and Engineering

• IMR program services

• Subsea inspection/intervention services

• Survey Services

• Data Management / Reporting services

• ROV and tooling services

• Asset management

• Platform Supply services

• Non-planned maintenance

• Emergency response

Client and location:

Shell Australia is part of The Shell Group, a global

group of energy and petrochemical companies. Shell’s

world-leading FLNG technology is to be deployed at the

Prelude FLNG facility – it is the largest floating facility

ever built, it will produce, liquefy, store and transfer

LNG at sea. The facility will be located 475 kilometres

north-north east of Broome, in Western Australia.

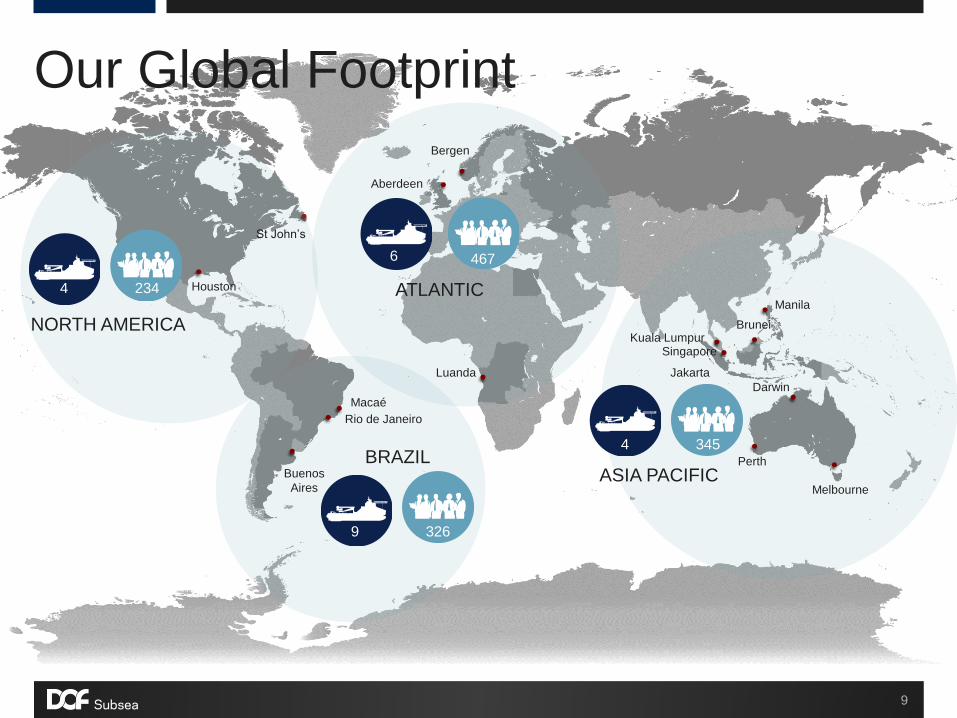

Our Global Footprint

9

ATLANTIC

NORTH AMERICA

BRAZILASIA PACIFIC

Macaé

Rio de Janeiro

Buenos

Aires

Houston

St John’s

Aberdeen

Bergen

Luanda

Singapore

Manila

Melbourne

Jakarta

BruneiKuala Lumpur

Darwin

Perth

3269

4676

2344

3454

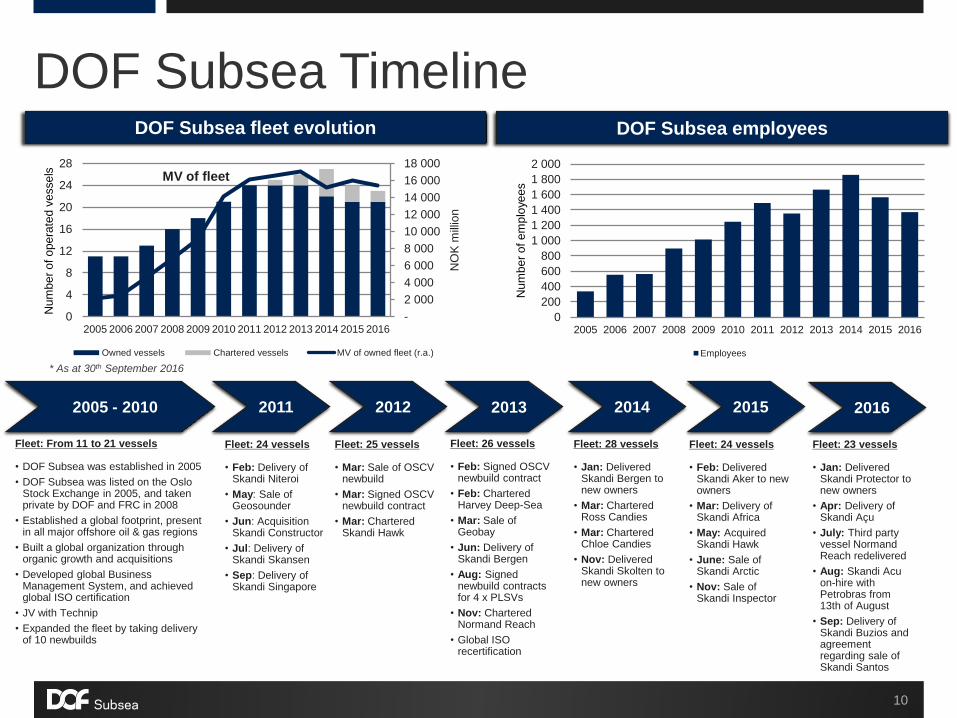

DOF Subsea Timeline

10

DOF Subsea fleet evolution

-

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

0

4

8

12

16

20

24

28

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

NO

K m

illio

n

Nu

mb

er

of o

pe

rate

d v

essels

Owned vessels Chartered vessels MV of owned fleet (r.a.)

MV of fleet

2005 - 2010

Fleet: From 11 to 21 vessels

• DOF Subsea was established in 2005

• DOF Subsea was listed on the Oslo Stock Exchange in 2005, and taken private by DOF and FRC in 2008

• Established a global footprint, present in all major offshore oil & gas regions

• Built a global organization through organic growth and acquisitions

• Developed global Business Management System, and achieved global ISO certification

• JV with Technip

• Expanded the fleet by taking delivery of 10 newbuilds

2011

Fleet: 24 vessels

• Feb: Delivery of Skandi Niteroi

• May: Sale of Geosounder

• Jun: Acquisition Skandi Constructor

• Jul: Delivery of Skandi Skansen

• Sep: Delivery of Skandi Singapore

2012

Fleet: 25 vessels

• Mar: Sale of OSCV newbuild

• Mar: Signed OSCV newbuild contract

• Mar: CharteredSkandi Hawk

2013

Fleet: 26 vessels

• Feb: Signed OSCV newbuild contract

• Feb: Chartered Harvey Deep-Sea

• Mar: Sale ofGeobay

• Jun: Delivery of Skandi Bergen

• Aug: Signed newbuild contracts for 4 x PLSVs

• Nov: Chartered Normand Reach

• Global ISO recertification

2014

Fleet: 28 vessels

• Jan: Delivered Skandi Bergen to new owners

• Mar: CharteredRoss Candies

• Mar: CharteredChloe Candies

• Nov: Delivered Skandi Skolten to new owners

DOF Subsea employees

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Nu

mb

er

of e

mp

loye

es

Employees

2015

Fleet: 24 vessels

• Feb: Delivered Skandi Aker to new owners

• Mar: Delivery of Skandi Africa

• May: Acquired Skandi Hawk

• June: Sale of Skandi Arctic

• Nov: Sale of Skandi Inspector

* As at 30th September 2016

2016

Fleet: 23 vessels

• Jan: Delivered Skandi Protector to new owners

• Apr: Delivery of Skandi Açu

• July: Third party vessel Normand Reach redelivered

• Aug: Skandi Acuon-hire with Petrobras from 13th of August

• Sep: Delivery ofSkandi Buzios and agreementregarding sale ofSkandi Santos

Modern High-end Fleet

11

• Majority of the fleet delivered from 2007 and onwards

• Modern fleet with a value adjusted average fleet age of approx. 6 years

• High-end vessels, capable of a wide scope of worldwide operations

Skandi Africa, Ship of the Year 2015

Skandi Acu, PLSV built 2016

Newbuild16 %

2007 - 201560 %

2000 - 200624 %

Year of delivery DOF Subsea fleet

-

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

Average fleet age

Value adjusted

Business Management

12

• Global business management system accredited by DNV to:

• Business Management System ISO 9001:2015

• Health and Safety System OHSAS 18001:2007

• Environmental Management System ISO 14001:2015

• Sustainability reporting according to Global Reporting Initiative G4 implemented

• Achieved Carbon Disclosure Project reporting result of B (report for 2015)

• IMCA International Contractor membership

• ISO recertification by DNV GL achieved during Q2 2016

2009

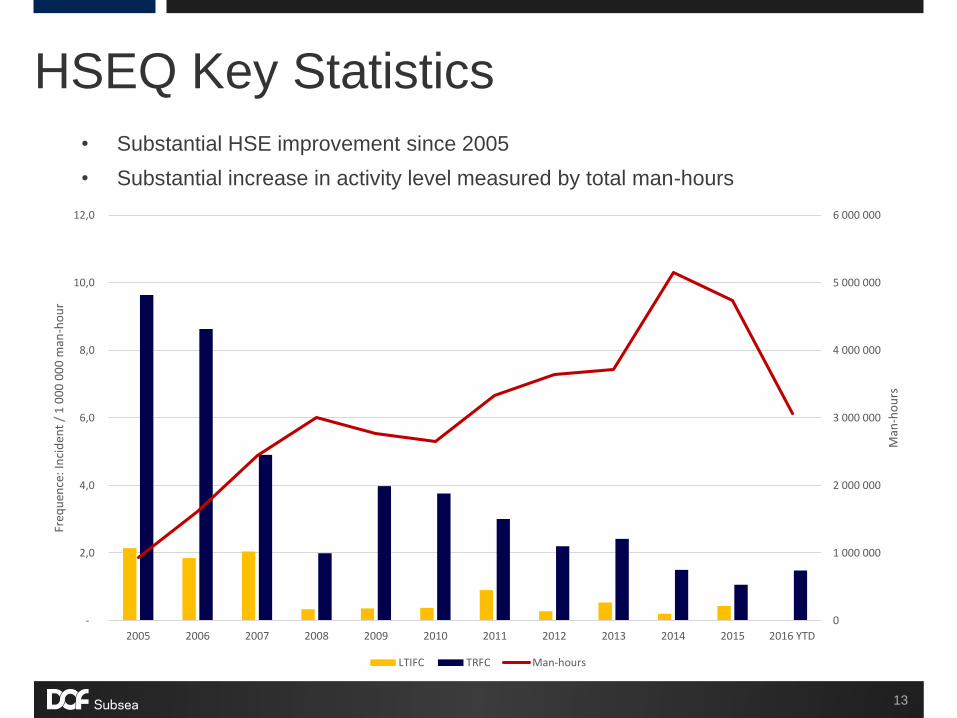

HSEQ Key Statistics

13

• Substantial HSE improvement since 2005

• Substantial increase in activity level measured by total man-hours

0

1 000 000

2 000 000

3 000 000

4 000 000

5 000 000

6 000 000

-

2,0

4,0

6,0

8,0

10,0

12,0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 YTD

Man

-ho

urs

Freq

uen

ce:

Inci

den

t /

1 0

00

00

0 m

an-h

ou

r

LTIFC TRFC Man-hours

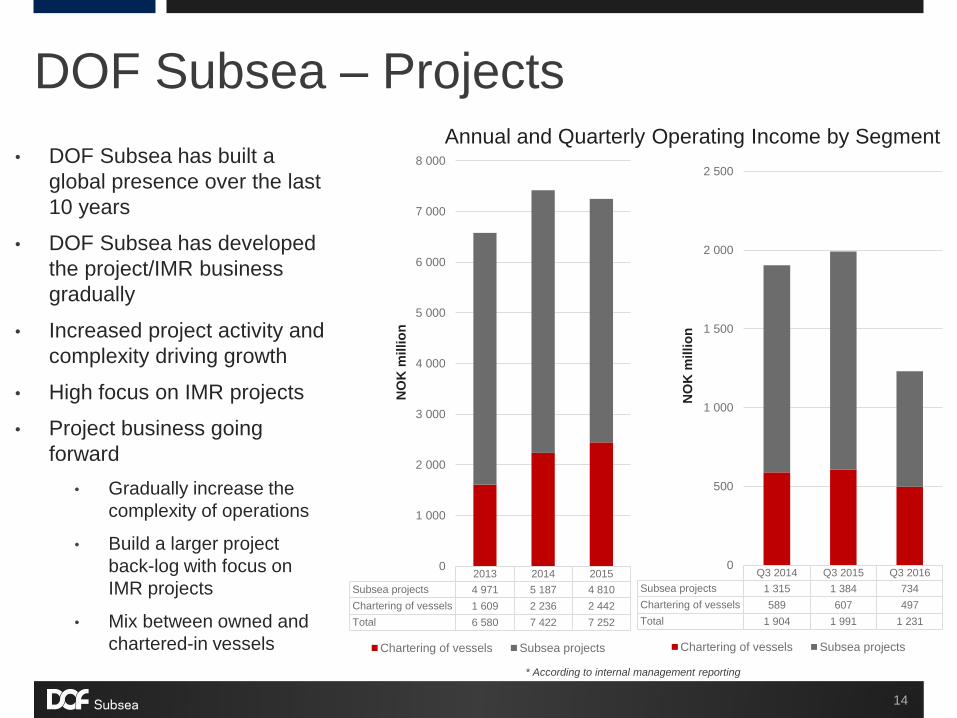

DOF Subsea – Projects

• DOF Subsea has built a

global presence over the last

10 years

• DOF Subsea has developed

the project/IMR business

gradually

• Increased project activity and

complexity driving growth

• High focus on IMR projects

• Project business going

forward

• Gradually increase the

complexity of operations

• Build a larger project

back-log with focus on

IMR projects

• Mix between owned and

chartered-in vessels

14

* According to internal management reporting

Annual and Quarterly Operating Income by Segment

2013 2014 2015

Subsea projects 4 971 5 187 4 810

Chartering of vessels 1 609 2 236 2 442

Total 6 580 7 422 7 252

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

NO

K m

illio

n

Chartering of vessels Subsea projects

Q3 2014 Q3 2015 Q3 2016

Subsea projects 1 315 1 384 734

Chartering of vessels 589 607 497

Total 1 904 1 991 1 231

0

500

1 000

1 500

2 000

2 500

NO

K m

illio

n

Chartering of vessels Subsea projects

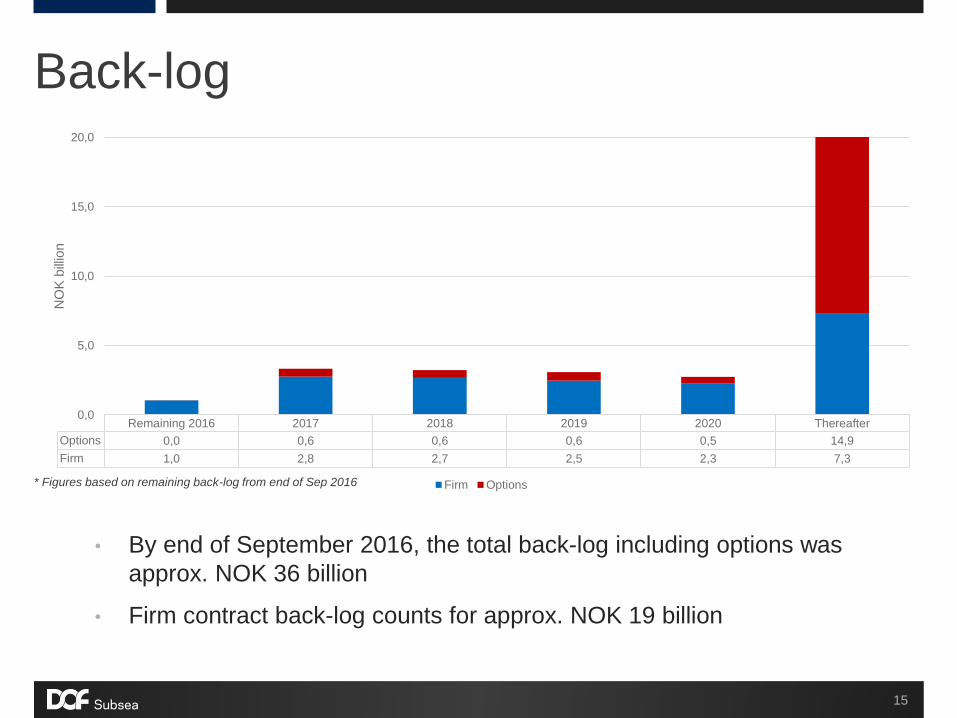

Back-log

15

• By end of September 2016, the total back-log including options was

approx. NOK 36 billion

• Firm contract back-log counts for approx. NOK 19 billion

* Figures based on remaining back-log from end of Sep 2016

Remaining 2016 2017 2018 2019 2020 Thereafter

Options 0,0 0,6 0,6 0,6 0,5 14,9

Firm 1,0 2,8 2,7 2,5 2,3 7,3

0,0

5,0

10,0

15,0

20,0

NO

K b

illio

n

Firm Options

Financials

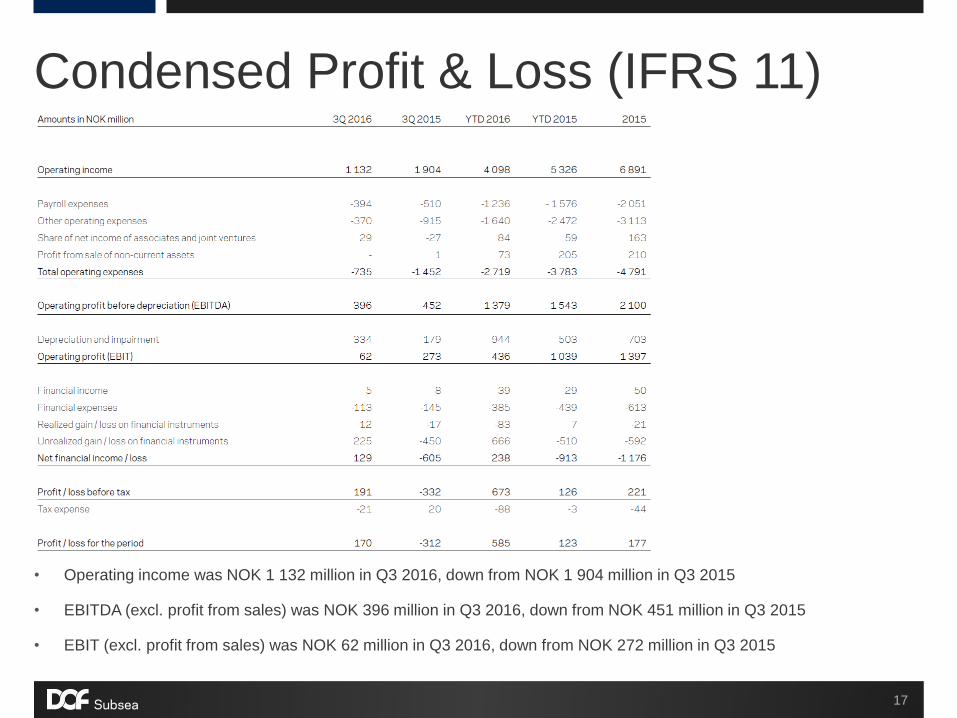

Condensed Profit & Loss (IFRS 11)

• Operating income was NOK 1 132 million in Q3 2016, down from NOK 1 904 million in Q3 2015

• EBITDA (excl. profit from sales) was NOK 396 million in Q3 2016, down from NOK 451 million in Q3 2015

• EBIT (excl. profit from sales) was NOK 62 million in Q3 2016, down from NOK 272 million in Q3 2015

17

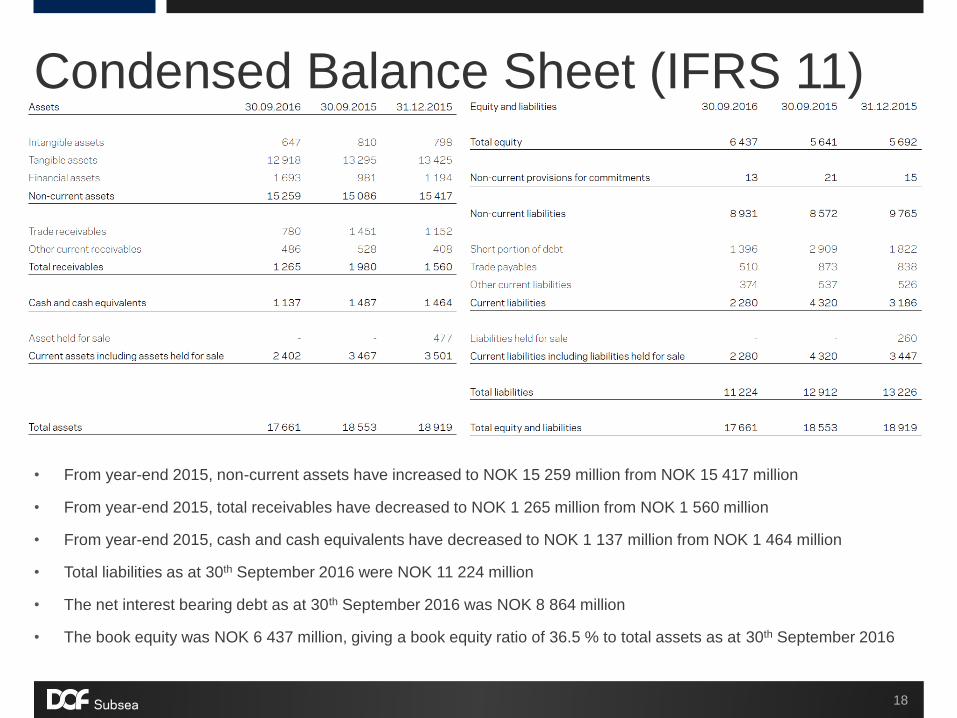

Condensed Balance Sheet (IFRS 11)

• From year-end 2015, non-current assets have increased to NOK 15 259 million from NOK 15 417 million

• From year-end 2015, total receivables have decreased to NOK 1 265 million from NOK 1 560 million

• From year-end 2015, cash and cash equivalents have decreased to NOK 1 137 million from NOK 1 464 million

• Total liabilities as at 30th September 2016 were NOK 11 224 million

• The net interest bearing debt as at 30th September 2016 was NOK 8 864 million

• The book equity was NOK 6 437 million, giving a book equity ratio of 36.5 % to total assets as at 30th September 2016

18

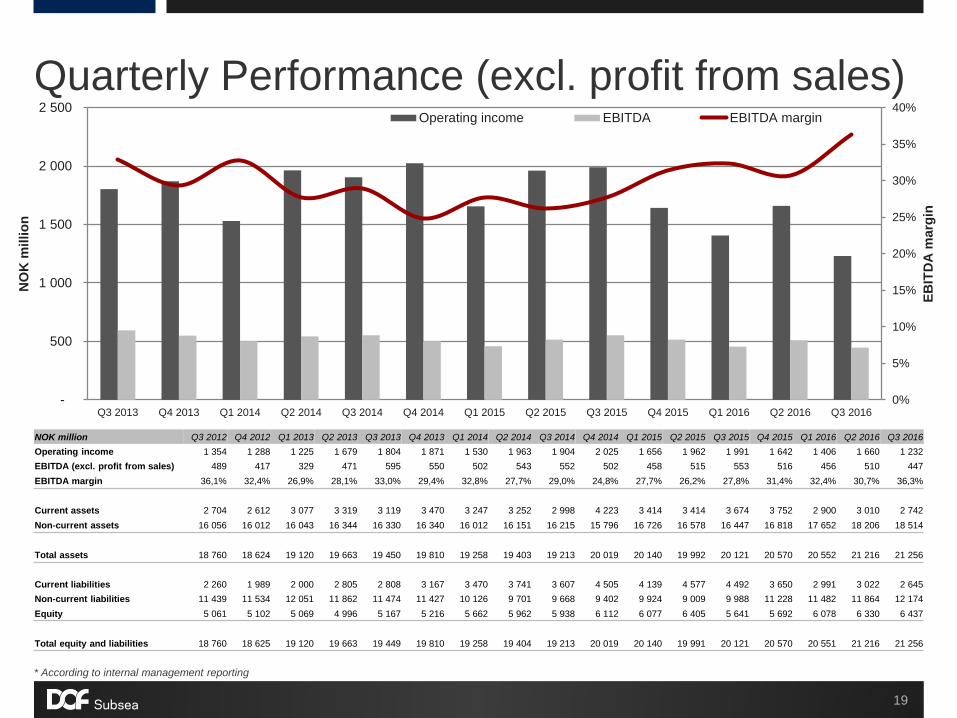

Quarterly Performance (excl. profit from sales)

19

* According to internal management reporting

0%

5%

10%

15%

20%

25%

30%

35%

40%

-

500

1 000

1 500

2 000

2 500

Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016

EB

ITD

A m

arg

in

NO

K m

illio

n

Operating income EBITDA EBITDA margin

NOK million Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016

Operating income 1 354 1 288 1 225 1 679 1 804 1 871 1 530 1 963 1 904 2 025 1 656 1 962 1 991 1 642 1 406 1 660 1 232

EBITDA (excl. profit from sales) 489 417 329 471 595 550 502 543 552 502 458 515 553 516 456 510 447

EBITDA margin 36,1% 32,4% 26,9% 28,1% 33,0% 29,4% 32,8% 27,7% 29,0% 24,8% 27,7% 26,2% 27,8% 31,4% 32,4% 30,7% 36,3%

Current assets 2 704 2 612 3 077 3 319 3 119 3 470 3 247 3 252 2 998 4 223 3 414 3 414 3 674 3 752 2 900 3 010 2 742

Non-current assets 16 056 16 012 16 043 16 344 16 330 16 340 16 012 16 151 16 215 15 796 16 726 16 578 16 447 16 818 17 652 18 206 18 514

Total assets 18 760 18 624 19 120 19 663 19 450 19 810 19 258 19 403 19 213 20 019 20 140 19 992 20 121 20 570 20 552 21 216 21 256

Current liabilities 2 260 1 989 2 000 2 805 2 808 3 167 3 470 3 741 3 607 4 505 4 139 4 577 4 492 3 650 2 991 3 022 2 645

Non-current liabilities 11 439 11 534 12 051 11 862 11 474 11 427 10 126 9 701 9 668 9 402 9 924 9 009 9 988 11 228 11 482 11 864 12 174

Equity 5 061 5 102 5 069 4 996 5 167 5 216 5 662 5 962 5 938 6 112 6 077 6 405 5 641 5 692 6 078 6 330 6 437

Total equity and liabilities 18 760 18 625 19 120 19 663 19 449 19 810 19 258 19 404 19 213 20 019 20 140 19 991 20 121 20 570 20 551 21 216 21 256

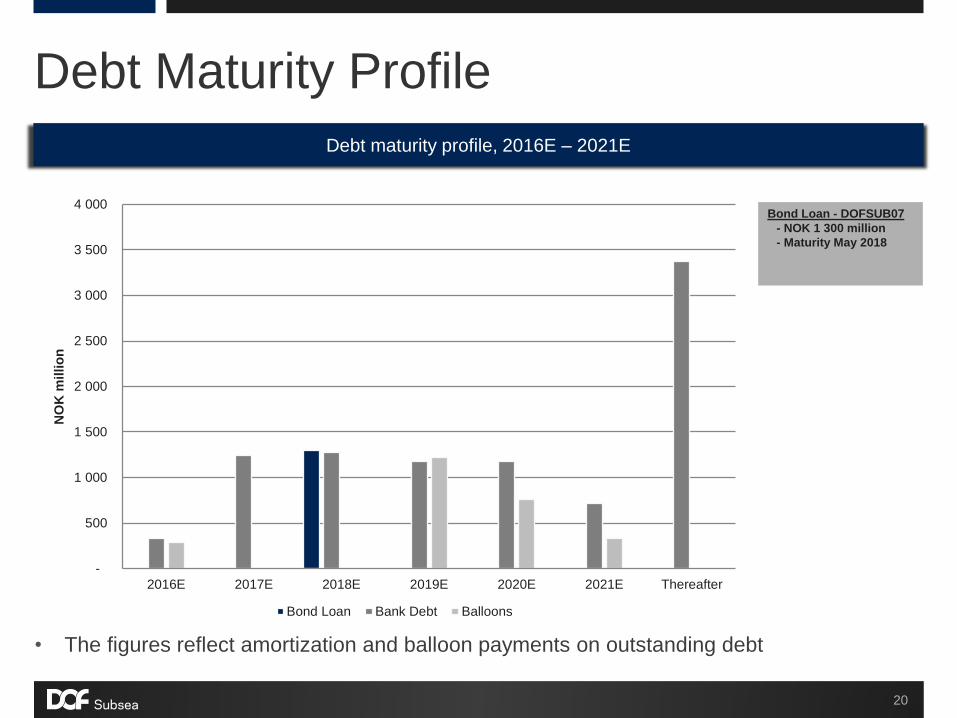

Debt Maturity Profile

20

Bond Loan - DOFSUB07

- NOK 1 300 million

- Maturity May 2018

• The figures reflect amortization and balloon payments on outstanding debt

Debt maturity profile, 2016E – 2021E

-

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2016E 2017E 2018E 2019E 2020E 2021E Thereafter

NO

K m

illio

n

Bond Loan Bank Debt Balloons

Risk Mitigating Factors

21

Risk mitigating

factors

Global presence provides access to more market opportunities

Strong back-log provides stable

earnings

Diversified blue-chip customers

reduce counterpart risk

Value added services provide

increased earnings potential

Modern, high-end fleet

provides safe collateral

Strong bank-and investor relationships

provide access to credit

Sale of vessels confirms values

Weaker subsea market

Outlook

Challenging Fundamentals for Subsea Activity

23

• Demand

• Volatile oil price

• Continued cost focus by oil companies

• Reduced offshore E&P spending

• Uncertain project timing

• Counterpart risk

• Increased focus on price, technologically

advanced and flexible vessels and

engineering capabilities

• DOF Subsea owns the world’s most

sophisticated fleet, and has a global

organization

Challenging Fundamentals for Subsea Activity

24

• Supply

• Over-supply of vessels

• Several vessels in lay-up

• Number of subsea contractors to be reduced

Weaker market

conditions

Reduced demand

Over-

supply

Challenging Fundamentals for Subsea Activity

25

Weak subsea

market and pressure

on margins

Lower IMR activity, globally

Lower rig activity and

delayed field developments

Reduced E&P spending

Volatile oil price

Number of niche subsea

players

Improved access to qualified

personnel

Over-supply of subsea vessels

DOF Subsea has mitigated the weaker fundamentals through a global footprint and a

diversified portfolio of clients

Thank you!