radio frequency identification (rfid) industry white paper

DESCRIPTION

TRANSCRIPT

Radio Frequency Identification (RFID) Industry White Paper

May, 2006

Table of Contents

TABLE OF CONTENTS ...................................................................................................2

TABLE OF FIGURES .......................................................................................................2

1. BACKGROUND........................................................................................................3

1.1. TECHNOLOGY .....................................................................................................3 1.2. POLICY ...............................................................................................................4 1.3. STANDARDS........................................................................................................4 1.4. MATRIX COMPARING TAGS, READERS AND MIDDLEWARE .......................................6 1.5. STATE OF THE INDUSTRY .....................................................................................9

2. STATUS OF IMPLEMENTATIONS ........................................................................10

2.1. WAL-MART .......................................................................................................11 2.2. OTHER U.S. GOVERNMENT AGENCIES ...............................................................11 2.3. UNITED STATES DEPARTMENT OF DEFENSE.......................................................14 2.4. COSTS AND RETURN ON INVESTMENT (ROI) ......................................................15

3. MAP DOD SYSTEM ...............................................................................................16

4. DOD’S IN-TRANSIT VISIBILITY (ITV) NETWORK................................................16

5. OPERATIONAL CONCEPT....................................................................................17

5.1. ACTIVE RFID IMPLEMENTATION ..............................................................................17

6. WAY AHEAD ..........................................................................................................18

6.1. CONSIDERATIONS .............................................................................................18 6.2. ACTIONS FOR THE FUTURE ................................................................................19 6.3. OBJECTIVE SYSTEM ..........................................................................................21 6.4. RFID CHRONOLOGY..........................................................................................22

Table of Figures FIGURE 1 WORLDWIDE REGULATIONS VARY FOR UHF ........................................................................ 5 FIGURE 2 ENTERPRISE LEVEL SOFTWARE PLATFORM INTEGRATES DATA ............................................. 8 FIGURE 3 PESSIMISTIC ROI IN THE DEPARTMENT OF DEFENSE .......................................................... 15 FIGURE 4 OPTIMISTIC ROI IN THE DEPARTMENT OF DEFENSE ............................................................ 15 FIGURE 5 “FACTORY TO FOXHOLE” CURRENT PROCESS IN THE DEPARTMENT OF DEFENSE................. 16 FIGURE 6 DEPARTMENT OF DEFENSE’S ITV NETWORK ...................................................................... 17 FIGURE 7 AN OPERATIONAL VIEW OF THE RF-ITV ARCHITECTURE..................................................... 18 FIGURE 8 A THEORETICAL OBJECTIVE SYSTEM ................................................................................. 21 FIGURE 9 TIMELINE OF RFID MILESTONES........................................................................................ 22

RFID Industry White Paper Page 2 of 23

1. Background This white paper will address five issues regarding the background of RFID technology and DoD: 1) the history of the technology within DoD logistics operations, 2) policy background, 3) technology standards, 4) a comparison of tags, readers, and middleware, and 5) the current state of technology available in the market place.

1.1. Technology During Operation Desert Shield/Desert Storm in the early 1990s, DoD moved over 40,000 containers of supplies. Nearly two-thirds of these containers had to be opened and examined to determine what was inside. This lack of asset visibility led to significant operational inefficiencies. To address this problem, the DoD began investigating and deploying Automatic Identification Technologies (AIT). In one of the earliest deployments of AIT in DoD, the Army installed RFID Reader technology at selected sites around the world and integrated them with active, data rich tags to track containers through the logistics pipeline and to provide stand-off visibility of container contents. This network of Active RFID has evolved into a fixed-reader In-Transit Visibility (ITV) network that today stretches across more than 45 countries, 2,000 sites and tracks an average of 35,000 shipments daily. Fixed interrogators installed at key nodes read RFID tags attached to pallets, containers and large mobile equipment, providing near real-time data to a regional server and then passing the data to the DoD’s global asset visibility systems. With the approach of Operation Iraqi Freedom (OIF) a decade later, the need for increased asset visibility became even more critical. Since OIF, NATO allies such as the defense forces in the United Kingdom, Denmark, and Spain, and Australia and Israel are implementing similar ITV networks. These networks can track national consignments and are designed to be interoperable with each other’s networks for joint-force, multi-national deployments. Other active RFID solutions have been used by DoD services for parts and materials tracking in remanufacturing processes, stockpile management of ammunitions inventory, and other applications. Commercial industry has shared this need for improved asset visibility and began investigating technologies that could provide a greater level and detail than had previously been possible with bar code technology. Unlike bar code technology, both active and passive RFID tags allow for the automatic capture and retention of data relevant to the shipment(s) to which the tag is affixed. Bar codes are a unique sequence of numbers that correlate to a database, which reconciles the bar code to shipment information. Passive RFID tags contain additional data to identify the shipper and the shipment type (case or pallet), while active RFID tags have the capacity to document the entire contents, or manifest, of a container.

RFID Industry White Paper Page 3 of 23

Table 1 RFID tags have many advantages over the barcode.

Barcode / UPC RFID Tag Efficiency Ability to read one tag

at a time (line of Sight required)

Ability to read multiple tags simultaneously (no line of sight required)

Dependability Labels easily damaged

Tags less susceptible to damage

Data Capacity Limited amount of data can be assigned

Significantly higher data capacity to capture detailed information about product

Flexibility Static information Potential for read / write capability, making tags reusable.

1.2. Policy In response to the need for improved asset visibility, the DoD issued an RFID Policy memorandum in October 2003. This policy, which was updated and finalized on July 30, 2004, states that DoD must take advantage of the inherent capabilities of RFID technology to improve business functions and facilitate all aspects of the DoD supply chain. Specifically, it directs the use of high data capacity (active) RFID tags to be used in the DoD operational environment and requires that suppliers put passive RFID tags on the lowest possible piece part/case/pallet packaging by January 2005.

1.3. Standards Frequencies standards As this technology has been developing, it has become critical to deploy standards-based frequencies when using RFID to obtain visibility within and between different military services or countries. Ensuring interoperability provides maximum performance in different environments. Currently active RFID that is deployed is based on ISO 18000-7 operating at 433.92 MHz. The US is currently using 915MHz for passive RFID and other countries are using 850-960. Detail regarding other nation utilization of frequencies for RFID is provided in Figure 1 below:

RFID Industry White Paper Page 4 of 23

Figure 1 Worldwide Regulations Vary for UHF Frequency, performance and application standards also enable both passive and active RFID devices to interoperate with each other, and enable NATO and allied networks to communicate with each other. Data standards As passive RFID technology was being used, efforts were concurrently underway to make it possible for computers to track and identify any object anywhere in the world instantly using passive RFID technology. The key was to create a universal, open standard for identifying products and sharing information. Part of that work was to develop the Electronic Product Code (EPC) - a unique number that identifies a specific item in the supply chain. EPC global Inc., formed on November 1, 2003, administers the electronic product codes and will develop EPC standards for RFID technology going forward. The EPC Network was developed by the Auto ID Center, an academic research project headquartered at the Massachusetts Institute of Technology (M.I.T.) with 5 leading research universities around the globe. Again, the purpose of standardization is to achieve interoperability between devices used to perform the same function but from different manufacturers. The standards DoD are mandating for passive technology are the same as those being used by major commercial players such as Best Buy and Wal-Mart. In addition, DoD has created its own data construct, which allows for compatibility with EPC global specifications.

RFID Industry White Paper Page 5 of 23

1.4. Matrix comparing tags, readers and middleware In considering the topic of RFID hardware, there are two areas worth reviewing: 1) the types of tags, readers and middleware available and 2) the process for matching the right technology with the user/shipper application. Hardware/Software and Middleware The RFID network begins with a tag, which carries an Electronic Product code (EPC) or a purely serialized number. It may also carry other data, especially in the case of active RFID tags. The tag interacts with a reader/antenna, which is responsible for interrogating tags and reporting results to Site Managers, middleware or other application/backend systems (see Figure 5, page 16). The site manager connects to a Regional Server, which is connected to the National Server (Database). A list of commercially available tags, readers, printers, etc. is provided in Table 2 below. Table 2 List of RFID hardware providers

Company Name Ticker

Semi-Conductors Inlays/Tags Readers

Printers / Encoders Networking Software

Integration/ Services

AbeTech Private X Accenture ACN X Acsis Private X Alien Private X X X Applied Wireless Private X

Atmel ATML X Avery Dennison AVY X Axcess AXSI X X X BearningPoint, Inc. BE X

Brady Corp BRC X X BT Auto-ID BT X X Capgemini CGEMY.PK X Checkpoint Systems Inc. CKP X X X

CIM Bar Code Private X Cisco CSCO X Danaher (Accu-Sort) DHR X

Datalogic DAL X X Digital Angel DOC X X Dynasys Private X X EM Microelectronic Marin

UHR.DE X

Feig Electronic Private X X Globe Ranger Private X Hana Microelectronics Private X

Hewlett-Packard HPQ X

HID Corporation Private X X

HK Systems Private X IBM IBM x X X ID Micro Private X X X X ID Systems IDSY X X X Identec Solutions Private X X X X

Impinj Inc. Private X X X X Infineon IFX X Kennedy Group Private X X X X Manhattan Associates MANH X X

Miles Technologies Private X

Source: Robert W. Baird & Co.

RFID Industry White Paper Page 6 of 23

Company Name Ticker

Semi-Conductors Inlays/Tags Readers

Printers / Encoders Networking Software

Integration/ Services

Moore Wallace RRD X NCR Corporation NCR X X X OATSystems, Inc. Private X Omron Corporation OMRNF.PK X X

Parlex Corporation PRLX X Paxar Corporation PXR X Philips PHG X PLITEK Private X Printronix PTNX X Precision Dynamics Private X X

Provia Software Inc. Private X

R4 Global Services Private X

RFTechnologies Private X X X UPM Rafsec UPM X Red Prairie Private X X Reva Systems Private X RF Code Private X X X Rfid, Inc. Private X X RF Technologies Private X X Rush Tracking Systems Private X

SAP SAP X X Sato Japan X X Savi Technology Private X X X X X Sirit SI.TSX X X SkyeTek Private X SmartCode Private X X Sovereign Tracking Sys. Private X X X X

STMicroelectronics STM X Sun Microsystems SUNW X X Symbol Technologies SBL X X X

Tagsys USA Private X X X Texas Instruments TXN X X ThingMagic Private X TrenStar Inc. Private X X Unisys Corporation UIS X UNOVA Inc. UNA X X X X WJ Communications WJCI X

Xterprise Private X Yantra Corporation Private X Zebra Technologies ZBRA X X

Source: Robert W. Baird & Co. Matching Technology with Application Use of Automatic Identification Technology (AIT) first began in 1966. Since that time, the development of both standards and the proper utilization of the technology have become the focus of today’s logistics professionals. AIT technologies – from sensors to satellites – must be matched with the right application (as shown in Figure 2 below) to provide the maximum benefit from this form of data capture and transfer.

RFID Industry White Paper Page 7 of 23

Transport unit

Movementvehicle Item Packaging Unit Load Container

Barcode

Passive RFID Gen 2 ISO 18000-6

Active RFID

GPS

Figure 2 Enterprise Level Software Platform Integrates Data These capabilities will find broad application cutting across multiple business processes, as shown in Table 3 below. Table 3 RFID Business Process Applications Process Area RFID Will Enable Potential Applications Metrics

Supply Chain Management

Real time Visibility into the location and movement of inventory, stock levels, and consumer demand.

Inventory visibility and movements across trading relationships, product pedigree/lifecycle history tracking, process exception triggers

• Reduced inventory & logistics costs

• Enhance service levels and sales

• Enhance consumer responsiveness

Work In Process Manufacturing

Visibility and control of Work In Process (WIP) manufacturing operations and production line and transaction recording efficiencies, and JIT manufacturing triggers

Automation of assembly, WIP inventory management, component production

• Reduced manufacturing defects

• Reduced inventory costs • More efficient production

planning

Asset Management

Visibility to the location, movement and maintenance history of physical assets -- trailers, dollies, fixtures, parts

Vehicle management and maintenance, fleet management, financial asset reporting

• Increased capital asset utilization

• Enhanced transportation management

Security & Access Control

Authentication and tracking of products at risk of counterfeiting, as well as valuable assets and potential personnel resources

Counterfeiting and fraud prevention, animal tracking, protein tracking, baggage tracking and handling

• Reduction of costs related to counterfeiting and fraud

• Enhanced food safety

Consumer Applications

Improved consumer shopping experienced through dynamic and interactive sales floor applications and more accurate insight into consumer preferences.

Real time merchandising and shelf replenishment, automated payment, returns management, personal identification and authentication, personal security and safety, patient identification and security

• Improved consumer satisfaction & loyalty

• Improved service levels and sales

• Reduced labor costs • Enhanced client/patient

privacy

RFID Industry White Paper Page 8 of 23

1.5. State of the industry RFID Spending Worldwide RFID spending is expected to total $504 million this year, up 39% from 2004. By the end of 2006, new license revenue is expected to total $751 million. By 2010, Gsur

loyments across emerging sectors, not just consumer goods nd retail, will become evident in 2006 and 2007.”

arket adoption

stions regarding hardware stallations and the percentage of companies automated with RFID. However,

varying answers when questioned about their reasons for

ID to provide business process improvements and therefore are aking the capital investment necessary to achieve this improvement.

logy while 3% of the respondents planned to evaluate, pilot or implement RFID in 2005. In

artner Research predicts worldwide RFID spending will pass $3 billion.

“Businesses are beginning to discover business value in places where they cannot use bar coding, which will be the force that moves RFID forward,” said Gartner analyst Jeff Woods in the study.1 “As the innovators' trials become public, broader depa According to AMR research, “RFID budgets will average just over $500K in 2005, with 16% growth in the next year and 20% growth in 2007; market accelerations for mainstream adoption will not happen until 2008.” 2 MThere is a variety of market research available on the topic of RFID adoption. A review by this white paper team found that the results of the surveys contained some consistencies, based on responses to queincompanies gave implementing RFID (see below). In one study, the findings suggest that implementation is based on customer mandates. In another study, survey results indicate that RFID was implemented to create and exploit supply chain labor efficiencies. For example, a survey of 510 companies conducted by Frost and Sullivan found that the number one reason for planned deployment of RFID is “improved process efficiency” – not mandates.3 This study states that companies are expecting RFm Conversely, an AMR Research study indicates that for the process-manufacturing segment of the market – including consumer goods – 53% of companies implementing RFID are doing so to remain customer compliant. In that same study, only 23% of companies have installed RFID techno6the commercial marketplace, budget growth for RFID remains modest through 2008. Additionally, rather than RFID expenses being included as part of the Research & Development budget, RFID appears as a separate line item.

1 TMCnet December 13, 2005 2 AMR Market Research Market Research Analysis Report, 2005. AMR Research. 3 O’Connor, M.C. “Efficiencies Drive RFID Adoption.” RFID Journal August 25, 2005

RFID Industry White Paper Page 9 of 23

Survey Conclusions A synopsis of the major findings from the AMR study of RFID implementations follows. Reasons for implementing RFID:

• Comply with retail mandates and public sector policies (DoD, FDA) • Reduce out of stocks (OOS) (Wal-Mart study showed RFID reduced

stock-outs by 16%)

• Improve security, authenticity and integrity of product, and create an audit

al-time, event- or exception-driven data from end to improve management and optimization of assets and

Ano eCargo similar$1,150 in efficiencies per container, not to mention improved security and faster ross-border clearances. This study was based on lengthy interviews with senior

as Wal-Mart, Target, Metro AG)

RFID for electronic proof of delivery

2. Status of Implementations RF a early 1990s. Fol rget are among a umber of retail stores that have issued their own RFID policy requirements (see

rnationally, several countries are vying to RFID arena. This white paper will discuss

• Reduce labor costs

trail. • Enhance supply chain visibility, efficiency and security – by providing and

having access to reend. This data can inventory.

th r study, conducted by A.T. Kearney in conjunction with the International Security Council, determined that a commercial active RFID network

to the DoD’s ITV network could provide major shippers with an average of

cexecutives at one-third of the largest 100-shipping/manufacturing companies. What retailers are not doing:

• Not embracing universal item tagging – the value of the items is driving the adoption at this point. The higher the value, the greater the likelihood that a retailer would apply item level tagging (exceptions exist such

• Not considering passive• Not delivering edicts for passive RFID implementations

ID doption and implementation has progressed rapidly since thelowing closely on the heels of Wal-Mart, Best Buy and Ta

nTable 4 below for further detail). Inteestablish themselves as leaders in thethe status of implementation in 4 areas: 1) Wal-Mart, 2) U.S. government agencies excepting the DoD, 3) International adoption, and 4) the U.S. DoD.

RFID Industry White Paper Page 10 of 23

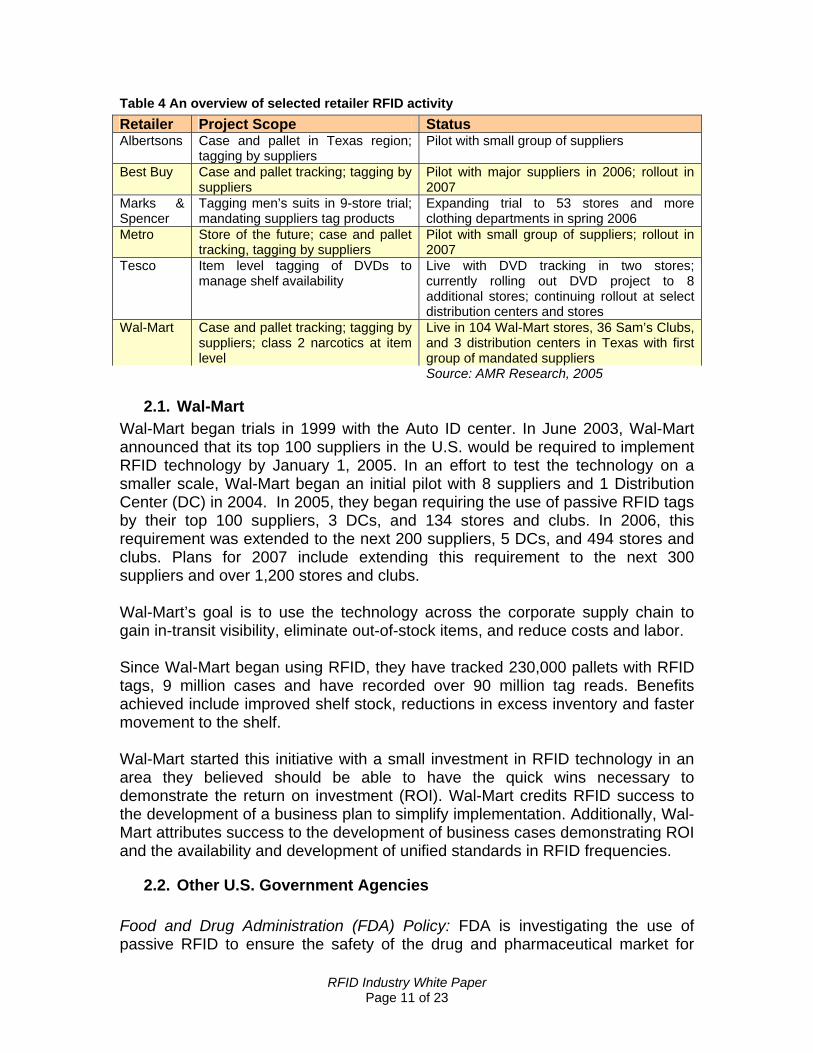

Table 4 An overview of selected retailer RFID activity Retailer Project Scope Status Albertsons Case and pallet in Texas region;

tagging by suppliers Pilot with small group of suppliers

Best Buy Case and pallet tracking; tagging by suppliers

Pilot with major suppliers in 2006; rollout in 2007

Marks & Spencer

Tagging men’s suits in 9-store trial; mandating suppliers tag products

Expanding trial to 53 stores and more clothing departments in spring 2006

Metro Store of the future; case and pallet tracking, tagging by suppliers

Pilot with small group of suppliers; rollout in 2007

Tesco Item level tagging of DVDs to manage shelf availability

Live with DVD tracking in two stores; currently rolling out DVD project to 8 additional stores; continuing rollout at select distribution centers and stores

Wal-Mart Case and pallet tracking; tagging by suppliers; class 2 narcotics at item level

Live in 104 Wal-Mart stores, 36 Sam’s Clubs, and 3 distribution centers in Texas with first group of mandated suppliers

Source: AMR Research, 2005

2.1. Wal-Mart Wal-Mart began trials in 1999 with the Auto ID center. In June 2003, Wal-Mart announced that its top 100 suppliers in the U.S. would be required to implement RFID technology by January 1, 2005. In an effort to test the technology on a smaller scale, Wal-Mart began an initial pilot with 8 suppliers and 1 Distribution Center (DC) in 2004. In 2005, they began requiring the use of passive RFID tags by their top 100 suppliers, 3 DCs, and 134 stores and clubs. In 2006, this requirement was extended to the next 200 suppliers, 5 DCs, and 494 stores and clubs. Plans for 2007 include extending this requirement to the next 300 suppliers and over 1,200 stores and clubs. Wal-Mart’s goal is to use the technology across the corporate supply chain to gain in-transit visibility, eliminate out-of-stock items, and reduce costs and labor. Since Wal-Mart began using RFID, they have tracked 230,000 pallets with RFID tags, 9 million cases and have recorded over 90 million tag reads. Benefits achieved include improved shelf stock, reductions in excess inventory and faster movement to the shelf. Wal-Mart started this initiative with a small investment in RFID technology in an area they believed should be able to have the quick wins necessary to demonstrate the return on investment (ROI). Wal-Mart credits RFID success to the development of a business plan to simplify implementation. Additionally, Wal-Mart attributes success to the development of business cases demonstrating ROI and the availability and development of unified standards in RFID frequencies.

2.2. Other U.S. Government Agencies Food and Drug Administration (FDA) Policy: FDA is investigating the use of passive RFID to ensure the safety of the drug and pharmaceutical market for

RFID Industry White Paper Page 11 of 23

U.S. consumers. FDA held a public hearing to discuss this matter on February 8- A recommendation g developed by FDA staff, n esenting

to

2

Homeland afe C rce, which was approved by s a

“green lane status” of trusted partner shippextra layer of protection. These active RFI

eslocation.

he U.S. T ade and Development Agenc n with Asia Pac Cooperation (APEC), funded projects to deploy E-Seals on

to leverage the investment of £5.5m

test technology available to us if we are to catch them”

d bar codes, active RFID and GPS systems into a single supply chain visibility oft

9, 2006. report and is beinsummarizi g the industry and public comments, as well as prrecommendations for possible use of RFID by FDA. Additionally, FDA isexpected

ut the Prescription Drug Marketing Act release an announcement abo

(PDMA) peimplementi

digree rule later this year. Drung pilots using passive RFID in

g manufacturers and distributors are 006.

Security: Operation S omme

Custom nd Border Protection, has laid early plans to improve commerce via ers using RFID-based E-Seals for an

D tags are envisioned with a variety of capabiliti to transmit information about seal status, temperature, moisture, and

T r y (USTDA), in conjunctio

ific Economic ocean shipments between Asia and the United States. USTDA and the European Union also funded similar projects tracking shipments between South Africa and the United Kingdom. Non-U.S. Government RFID Initiatives/Funding4

Outside of the United States, other national and territorial governments are taking an even more direct role in the promotion of RFID technology. For instance: United Kingdom: In March 2000, the UK’s Home Office launched the Chipping of

oods Initiative. The goal of the project wasG(or approximately U.S. $8.8 million at the time) in public funding, in order to demonstrate how theft could be reduced in the retail supply chain through the se of RFID technologies. The project sought to demonstrate how RFID couldu

reduce property crime and, in the process, reduces the strain on police resources in combating such crime and attempting to reunite items with their proper owners (U.K. Home Office, 2003). John Denham, the UK’s crime reduction minister, commented that, “as criminals are using increasingly sophisticated methods, so

e must harness the law(quoted in Clark, 2002, n.p.). Matching funds from the private sector partners selected for the project almost tripled the UK government’s funding for the project, bringing the total investment in the Chipping of Goods Initiative to £15m (AIM Global, 2003). The eight demonstration projects of the initiative were in the areas outlined below in Table 5. In one of the more innovative examples, the Woolworth’s UK project integrate

s ware solution to address product shrinkage – or theft – within its own supply

4 IBM “RFID the Right Frequency for Government” October 2005

RFID Industry White Paper Page 12 of 23

chain. Improved visibility, reduced shrinkage and better audit trails led to numerous benefits, including better goods distribution and lower supply chain and transportation costs. Mark Roberti’s (publisher and editor of RFID Journal) “The U.K. Chips In” (2002) analysis of the initiative was that beyond its stated goals, the real aim of the UK government was to “seed the market” for RFID and encourage British firms to be

t the forefront of adopting and capitalizing on the technology. In 2002, Roberti

5).

apredicted that this would be a wise investment of public dollars, rather than a simple subsidy of large firms’ technology projects. His prediction has proven correct, as a recent analysis of the European market for RFID points to the Chipping of Goods Initiative as the catalyst that helped propel the UK to the forefront of the European market (Collins,“EU RFID Spending to Near $1.9 Billion,” 200 Table 5 Eight demonstration projects of the Chipping of Goods initiative Project Private Sector Partners URL for Case Study Boats • HPI

• British Marine Federation

http://www.chippingofgoods.org.uk/download/ casestudies/boats.pdf

Wines and spirits • Allied Domecq http://www.chippingofgoods.org.uk/download/ casestudi• De La Rue

• CHEP es/winesandspirits.pdf

Jewelry • Argos http://www.chippingofgoods.org.uk/download/ casestudies/jewelry.pdf

Personal care • Unilever http://www.chippingofgoods.org.uk/download/ products • Tibbett & Britten

• Safeway casestudies/personalcare.pdf

Fast-moving consumer goods

• Woolworth’s http://www.chippingofgoods.org.uk/download/ casestudies/consumerproducts.pdf

Laptop computers • Dell • BT

http://www.chippingofgoods.org.uk/download/ casestudies/laptopcomputers.pdf

Compact discs • e.centre • EMI • Handleman • Asda

http://www.chippingofgoods.org.uk/download/ casestudies/compactdiscs.pdf

Mobile phones • TRI-MEX International • DHL • Nokia

http://www.chippingofgoods.org.uk/download/ casestudies/mobilephones.pdf

Source: U.K. Home Office (2003). “Chipping of Goods Case Studies.” Retrieved from the web on October 19, 2004. Available at http://www.chippingofgoods.org.uk/casestudies.htm South Korea: In June 2005, the government of South Korea announced its intent

invest approximately $800 million between 2005 and 2010 in RFID research

recently talked about the strategic importance of his government’s taking a leading role in RFID technology. Minister Chin stated, “This [RFID] will be very

toand development efforts. Among other projects, the Korean government is financing the construction and operation of an RFID center in the northern city of Songdo. South Korean Minister of Information and Communication Daeje Chin

RFID Industry White Paper Page 13 of 23

important for us in the next 10 years. The handset business is very big, but RFID will be as important. We are trying to procure a number of goals with RFID, and the application of new technology brings benefits in all social systems including

e individual family” (quoted in Ilett, 2005, n.p.).

to showcase the state’s RFID capabilities. According to Marsha homson, Victoria’s minister for information and communication technology, the

ctoria Eager to RFID Ho

Scotland: The g Scotland mic development authority, Scottish Enterprise, opened the Wireless Innovation Demonstration

gto n CentreDownie, who directs the lab, the goals for ely

Scottish government, are to ed and to enable them to devel

firms, suchtems, an contributed hardware and software to the

operation and have begun working with Scottish firms on RFID applications. The ati ion Lab has already enabled a Scotland-based Sp Solutions, to partla vides RFID Suppo

tment of DefThe United States of Defense (DoD) has been working with Active RFID since the early 1990s.) The success of this implementation in one region of

d to ecworldwide. The use of passive RFID ome early

raceability and Control Transportation System. DoD implementation continues

th Victoria, Australia: The Australian state of Victoria is seeking to establish the region as a leader in RFID technology. The state established the VicRFID cluster in August 2004 as a public/private effort to foster research, development, and deployment of RFID technology. In July 2005, the state government announced the broadening of the VicRFID cluster to become the RFID Association of Australia, a move to enlarge the group’s reach while retaining its focus on economic and technological development in its home region. At the same time, Victoria also announced that it would establish a permanent exhibition center in Port MelbourneTaim is to “cement Victoria as an RFID hotspot” (cited in “ViBecome tspot,” 2005, n.p.).

overnment of ’s principal econo

Lab at the Hillin n Park Innovatio in Glasgow in 2005. According to Ian the operation, which is funded entir

by the technology

ucate Scottish enterprises on RFID op business relationships with RFID

vendors. AlreadyMicrosys

, leading as Symbol Technologies, Sun d IBM, have

Wireless Innov on Demonstratsoftware firm, (O’Connor, “Sco

artan o

tner with Sun on an RFID project rt,” 2005). nd Pr

2.3. United States Depar ense Department

the world lea the expansion of this t hnology use to all military commands began in 2003 with s

implementations and testing of the technology. These included testing at Norfolk Ocean Terminal, a test on the USS Nassau, and a pilot within the Advance Twith the publication of the Defense Federal Acquisition Regulation (DFAR) for 2005 effective November 14, 2005. The DFAR for 2006 commodities is in the process of being reviewed by the Office of Management and Budget. Full implementation of RFID within the DoD system will begin with the 2007 DFAR. The funding of RFID within the services is in process and will be realized starting in FY08 and beyond.

RFID Industry White Paper Page 14 of 23

2.4. Costs and Return on Investment (ROI) Full case study details regarding the return on investment (ROI) for implementation of RFID are just emerging. In 2005, the DoD conducted a theoretical business case analysis on the use of passive RFID, since actual

plementation of passive RFID had not yet begun. The DoD business case imexamined a best case and a worst-case scenario. In the pessimistic view, DoD breaks even in about three years, as shown in Figure 3 below.

Figure 3 Pessimistic ROI in the Department of Defense By contrast, in the optimistic view below, DoD breaks even almost immediately.

Figure 4 Optimistic ROI in the Department of Defense

RFID Industry White Paper Page 15 of 23

ystem

In the case of the military supply chain, emphasis is on support to the war fighter over immediate cost efficiencies. For this reason, adoption by DoD was considered even if the pessimistic view was assumed at start up.

3. Map DoD s

Figure 5 “Factory to Foxhole” Current Processes in the Department of Defense 4. DoD’s In-Transit Visibility (ITV) Network • 45+ Countries • 2,000+ read/write locations - airports, seaports, rail terminals • 35,000+ Conveyances/Day

RFID Industry White Paper Page 16 of 23

Foxholeodal tracking of international shipments for all of DoD, including retrograde, and

formation about the location of his upplies. In addition, it allows for medical supply chain, and munitions tracking,

ib nt during deployments, tracking of war reserve equipment d depiction of

d Fig

Figure 6 Department of Defense’s ITV Network 5. Operational concept

5.1. Active RFID implementation As the owner of the world’s largest Active RFID infrastructure, the Army has led the way in RFID implementation for the DoD. The Army infrastructure includes four regional servers that replicate data continuously and over 2,000 locations that read or write RFID tags worldwide. It employs data rich active RFID tags with up to 128Kb memory and a guaranteed read range of up to 300 feet. Over 1.1 million tags have been put into service, and the tags may be integrated with

satellite GPS on vehicles. This extensive network enables Factory tonprovides the war fighter with accurate, timely insvis ility of equipmeand supplies, and depot repair work in process tracking. A detaile

nsit Visibility (RF-ITV) Architecture is providethe Army Radio Frequency In-Tra ure 7 below. in

RFID Industry White Paper Page 17 of 23

BCS3IDE-AVGTN

BCS3MMC / JBFSA

ABA

IRRISILAPGTN

DAVSBCS3

Operational ViewRadio Frequency In-Transit Visibility (RF-ITV) Architecture

RF-ITV Server

Interrogator

Read/Write Station

Satellite

Radio Frequency (RF) TagField Data Unit

Military User

RF Tag Interface (FOUO)

Electronic Data

LEGEND

Satellite Tracking System (STS)

Depot/Vendor/DLA/POESatellite FeedTag Point of Origin

DTRACS

VistarMTS

LogisticsNode

AxTracker

UniTrac

PWC

To PACIFIC NATIONAL To NATIONALEUROPE

SWA

PACIFIC

WPSRandNLACLIDB

IDE-AV

STS Tag Interface (FOUO)STS Interface(Classified)

S-ITV

CMST

RF Tag and STS Interface (Classified) Note: STSs are interfaces, not part of RF-ITV System.

itecture

via servers in Europe, US, and Southwest Asia. This data is transferred via satellite from current military movements in progress. Act and download applicable

rporating greater use of sensors and GPS satellite location acking systems.

Figure 7 An Operational View of the RF-ITV Arch Active RFID data is managed

ive RFID users access the data via the servers detail to their local operations.

6. Way Ahead 6.1. Considerations

This White paper team reviewed a series of ideas for consideration. These ideas presented are not meant to be limiting but are offered as concepts for consideration. An enduring theme mentioned by all industry participants is the need to continue to develop and follow commercial open standards for RFID and all AIT technologies. Utilization of open standards allows for interoperability among users, manufactures, commercial entities and the U.S. Government. An open technology platform, with RFID as the backbone, can provide supply-level and in-transit visibility incotr

RFID Industry White Paper Page 18 of 23

RFID provides benefits to DoD beyond asset visibility. RFID presents an opportunity to know the condition of the asset (temperature, damage) as well as offers data regarding the security of the assets. Suggestions for consideration:

• Continue to evaluate further development and deployment of RFID solutions for all U.S. Government agencies, including U.S. Department of Homeland Security (FEMA, Customs and Border Protection), DOE, etc.

• Continue to evaluate further development and deployment of RFID

for weapons systems to monitor onboard health of the systems. Sensor data on the health of the weapons system can be monitored, stored and transmitted automatically via RFID for improved performance.

• Continue the development of mobile reader infrastructure to track

supplies in remote and harsh environments where fixed infrastructure does not exist.

• Implement process and policy for the recovery, return, and reuse of

tags

6.2. Actions for the future • Continue to push for implementation of RFID technology within the

services. Currently OSD issued a policy requiring RFID implementation and the services have each developed plans for implementation. Some plans call for an extended implementation between 2008 and 2011 based on the funding process. Additional emphasis for more rapid deployment is

Automatic Identification Technologies, including bar codes, sensors, passive and active RFID, biometrics, OCR, satellite communications, etc. An open technology platform can get the best use for the right technology applied to the right asset.

suggested. • Conduct a review and analysis of all current DoD distribution centers,

and DoD managed ocean and air terminals/ports that have implemented either active RFID or passive RFID to determine “as is state”.

• Expand remainder of ITV within DoD and with allies to fill existing

visibility gaps identified by the above actions, and supports all Combatant Commanders (All Stakeholders), as well as to make the network more robust to ensure a highly reliable performance.

• Create graduated visibility capability – This capability would allow for

interoperable fixed and mobile networks to capture gradations of data from all kinds of

RFID Industry White Paper Page 19 of 23

• First and Last Mile Tactical Logistics. Combination of passive and

active RFID, when integrated with satellite, can improve box- or carton-level visibility when the primary conveyance, such as a container, is aggregated and on the other end when it is de-aggregated. This

de the ability to track all levels of assets from

•

and passive. Assign one entity responsibility for oversight of outsourced

•

t vehicles and their cargo while in-transit and “on the move.” Move toward

• nalysis and move toward implementation of best of

breed COTS Supply Chain and Event or Exception Management Web

y to the foxhole.

• Operationalize RF-ITV system integration efforts with the Common luding more training prior to deployment and

•

EPC Class 1 RFID systems to meet DoD mandates, but should also provide those enhancements that are required for demanding

s employed to ensure long battery life demanded by DoD requirement but in a flexible and cost

ese capabilities. If you

graduated visibility will provi“factory to foxhole”.

Outsource implementation and management of RFID network – active

operation (third party logistics concept for RFID)

Promote the aggressive integration of RFID with GPS and satellite communications where warranted to continuously monitor both transpor

elimination of the requirement for a fixed reader infrastructure.

Conduct an a

based applications for greater flexibility and ITV-wide visibility from the factor

Operational Picture, incregular refresher training.

Increase the capability of RFID systems to add robust performance, enhanced range, and superior security to RFID deployments within the DoD. The hardware developed should maintain compatibility with commercial

military applications. Such intelligent sensing and adaptive RFID technologies can be achieved by targeting the following technology developments:

• Battery assisted passive RFID tag systems designed to be compatible with EPC class I generation II for maximum compatibility commercial and DoD deployed infrastructure. Advanced power management technique

effective form factor.

• Single chip RFID transceivers using NanoBlock IC technology that allow for significant reductions in tag size, power and costs. Readers already deployed by the DoD will only need firmware to be developed to take unique advantage of th

RFID Industry White Paper Page 20 of 23

move to a satellite type system the infrastructure is no longer

purposes of sharing data, including the development of sensor fusion capabilities to both tags and readers.

6.3 O

required. • RFID with anti-tamper and tripwire systems to enable the use of

RFID to secure critical assets. This includes ad hoc networking between RFID transceivers to coordinate and orchestrate data capture for the

bjective System

Theoretical Objective System Figure 8 A

RFID Industry White Paper Page 21 of 23

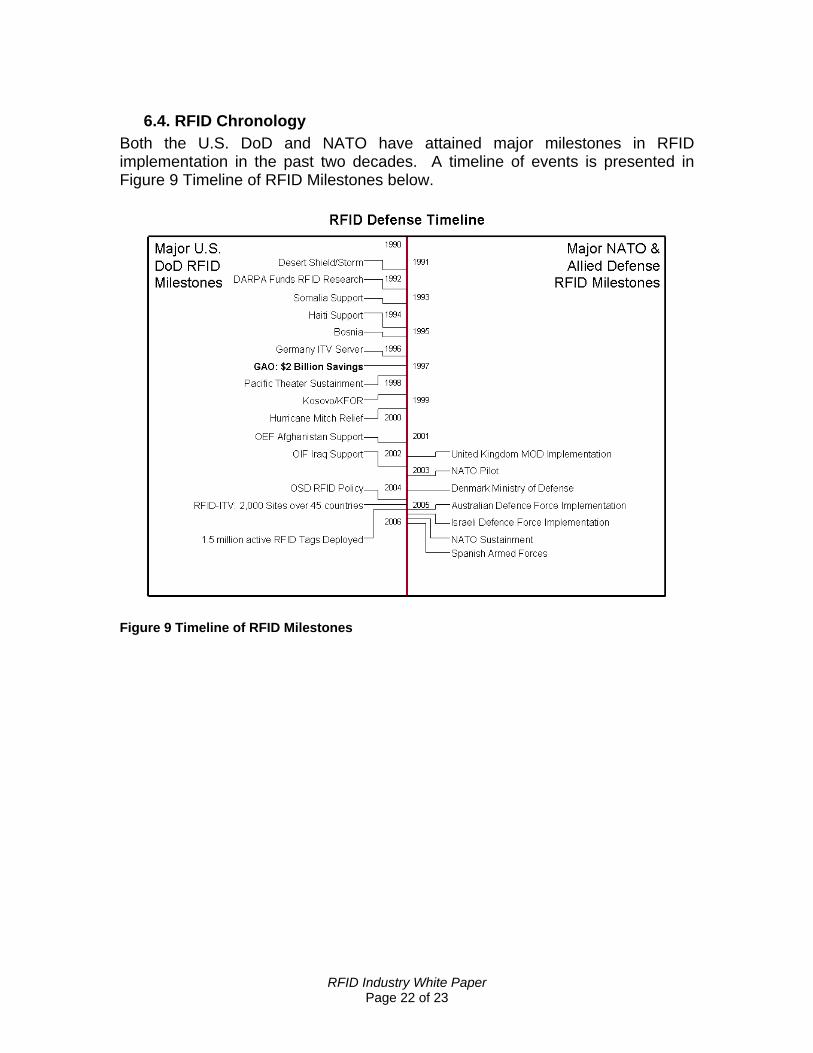

6.4. RFID Chronology Both the U.S. DoD and NATO have attained major milestones in RFID implementFigure 9 Time

ation in the past two decades. A timeline of events is presented in line of RFID Milestones below.

Figure 9 Timeline of RFID Milestones

RFID Industry White Paper Page 22 of 23

In compliance with the Department of Defense’s RFID policy, the military services are implementing the technology in the near future. Table 6 (below) details the strategies and timetables for implementation within each military service. Table 6 U.S. Military Services Strategies for RFID Implementation

Service Passive RFID Strategy Active RFID Strategy Roll-out USA

FY06-11: Rollout to National Level Depots, then IMA maintenance activities, then tactical SSAs

FY06-11: Integrating with SARSS, MTS; CONUS shipments

Plan includes rollout schedule and milestones. Featured implementation: Fort Eustis

USN

FY08-13: Outfit ashore commands, then afloat commands; implement by AIS/ship platform

FY06-11: Outfit Fleets/ Component Commands, Non-self deploying units, strategic Navy nodes, prepo force

Plan includes rollout schedule, budget information, and milestones. Featured implementation: TRF Bangor

USAF FY06-12: Outfit Hill AFB, pallet aggregation, base receiving, stowage, issue and delivery

FY06-11: High Value containers, prepo and ammo; RTLS for maintenance

Plan includes rollout schedule, budget information, and milestones. Featured implementation: Hill AFB

USMC FY08-13: Pilot then roll-out: MARCOROGCOM pilot (FY08), SMU pilot (FY09), TMO pilot (FY10), deployed pilot (FY11)

FY06-11: Outfitting operating forces in US and Okinawa; EEDSKs to I, II, and III MEFs

Plan includes rollout schedule, budget information, and milestones. Featured implementation: MARCORLOGCOM

USTC FY06-11: Travis AFB (FY06); Norfolk, Charleston, McGuire, Dover (FY07); 13 aerial ports (FY08)

FY06-09: Initiated capability where AMC opens the port; will develop capability to write and read

Plan includes rollout schedule for passive at aerial ports and milestones. Featured implementation: Travis AFB

DLA FY04-11: Retrofit SDPs, install CCP and remaining depots (FY06) for receiving; MSL level, MRO level for shipping; internal processing

DLA has already implemented Active RFID

Plan includes rollout schedule, budget information, and milestones. Featured implementations: DDSP and DDJC

For more information, please contact:

ary Ann Wagner mail: [email protected]

ME

RFID Industry White Paper Page 23 of 23