rapid appraisal of business development … philippines bds...rapid appraisal of business...

TRANSCRIPT

RAPID APPRAISAL OF BUSINESS DEVELOPMENT SERVICES I. Background and Summary of Key Outputs A. Background The objective of the rapid appraisal of business development services

(BDS) in the Visayas is to determine if the necessary conditions for developing and sustaining a BDS market development program are present.

The rapid appraisal of BDS markets will establish information and validate

certain conditions on the private sector, demand and supply for business services, opportunities or problems for expansion and possible interventions.

The areas of study are Region 6 - Western Visayas (Metro Iloilo) and

Region 7 (Central Visayas (Metro Cebu). A few inputs on Region 8 (Eastern Visayas) are also provided.

Integrated research covering secondary data and primary data gathering

was conducted from March 18 to April 10, 2002. Secondary data gathering included information from the Philippine Statistical Yearbook, NSO website and yellow pages in the areas analyzed.

Primary data efforts involved a survey of forty eight (48) key informants

classified as twenty two (22) enterprise business development service users; thirteen (13) private sector BDS providers; five (5) public sector BDS providers; five (5) business membership organization and three (3) external support agencies.

Face to face interviews were conducted using structured questionnaires

with liberal use of open-ended questions. (See Appendix 1.) B. Summary of Key Outputs The two regions analyzed, as with all areas nationwide show that majority

of enterprises are micro-enterprises. There are 46,346 establishments in Region 6; 49,759 establishments in

region 7 and 21,399 establishments in Region 8 Growth sectors are in manufacturing and services.

BDS are being bought and sold through the private sector in the two

regions analyzed.

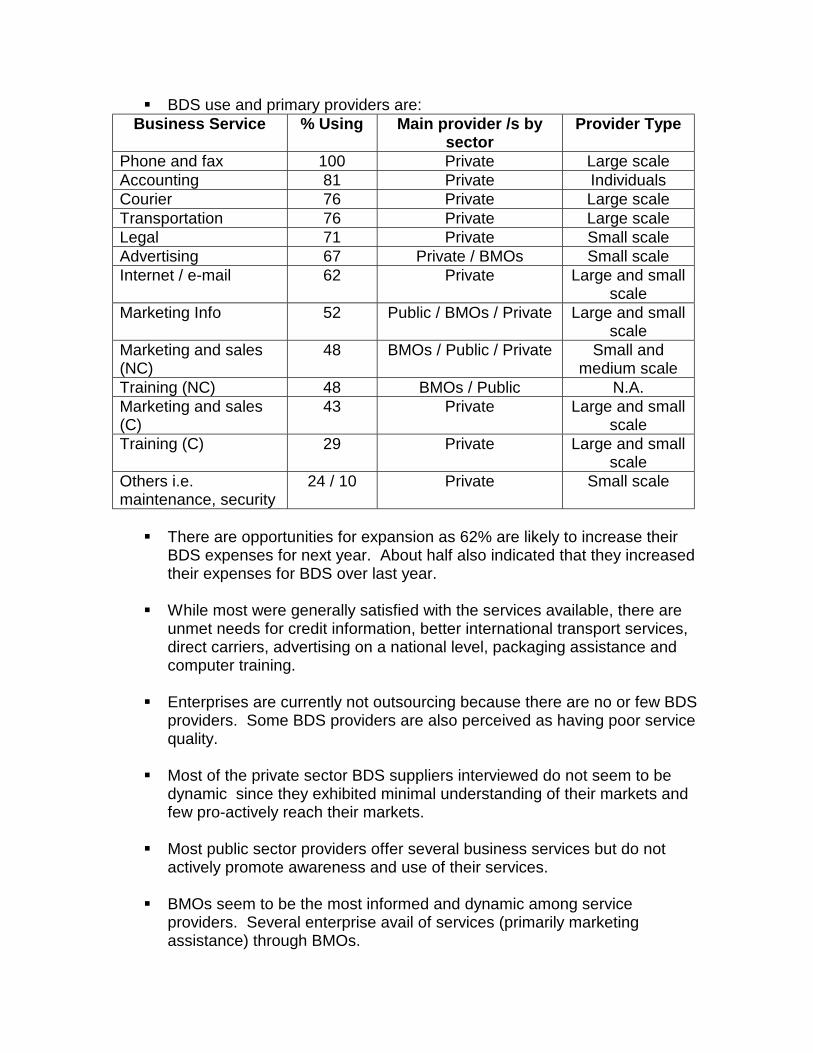

BDS use and primary providers are: Business Service % Using Main provider /s by

sector Provider Type

Phone and fax 100 Private Large scale Accounting 81 Private Individuals Courier 76 Private Large scale Transportation 76 Private Large scale Legal 71 Private Small scale Advertising 67 Private / BMOs Small scale Internet / e-mail 62 Private Large and small

scale Marketing Info 52 Public / BMOs / Private Large and small

scale Marketing and sales (NC)

48 BMOs / Public / Private Small and medium scale

Training (NC) 48 BMOs / Public N.A. Marketing and sales (C)

43 Private Large and small scale

Training (C) 29 Private Large and small scale

Others i.e. maintenance, security

24 / 10 Private Small scale

There are opportunities for expansion as 62% are likely to increase their

BDS expenses for next year. About half also indicated that they increased their expenses for BDS over last year.

While most were generally satisfied with the services available, there are

unmet needs for credit information, better international transport services, direct carriers, advertising on a national level, packaging assistance and computer training.

Enterprises are currently not outsourcing because there are no or few BDS

providers. Some BDS providers are also perceived as having poor service quality.

Most of the private sector BDS suppliers interviewed do not seem to be

dynamic since they exhibited minimal understanding of their markets and few pro-actively reach their markets.

Most public sector providers offer several business services but do not

actively promote awareness and use of their services. BMOs seem to be the most informed and dynamic among service

providers. Several enterprise avail of services (primarily marketing assistance) through BMOs.

There is an apparent awareness gap (need for the service and on specific

providers) between users and providers of business services. Several enterprise users rely on friends, relatives and associates for

service provider referrals. BMOs offering business services tend to exclude non-member SMEs from

their target market. The level of service quality provided by business service enterprises meets

the expectations of enterprise users because most users are limited to one or two choices of providers.

Possible program interventions are:

BDS Market Issues Possible Interventions SMEs are not aware of the need for some business services for their enterprises.

Appropriate assistance for service providers involved in training to help SMEs on the effective and efficient use of business services.

SMEs are not aware of the presence of some business services.

Develop communication vehicles for SMEs i.e. use of internet for information aside from communication

Some SMEs demand higher level of quality among their service providers.

Appropriate training to improve service quality level of business service providers.

Some business services are not available.

Assist start-up suppliers and help existing suppliers expand or diversify.

Some business services are not accessible.

Improve system for delivery of business services through ICT i.e. market matching and information, training

Most entrepreneurs rely on personal forms of communication for business services.

Enhance this preference through ICT based "membership" groups via the net

BMOs tend to exclude SMEs in their market

Provide appropriate assistance for BMOs to offer services to non-member SMEs

SME expectations and experience with business service providers are low or limited

Provide information on high service level quality providers i.e. case studies, user - provider encounters, etc.

Business service providers see the need to link up with related service providers.

Provide vehicle for service providers in area to link up.

Service quality level of business service providers needs improvement

Provide quality improvement venues for business service providers i.e. training, exposure visits, consulting, etc.

Considering the results of the study, the business services with the

greatest potential for market expansion are: (1) Advertising, (2) Non-computer based marketing sales and services, (3) Computer based business and market information and intelligence and (4) non-computer based training and counseling.

II. Background on Private Sector Enterprises in the Visayas The Visayas has three (3) main regions classified as Region 6 - Western

Visayas, Region 7 - Central Visayas and Region 8 - Eastern Visayas. Region 6 or Western Visayas includes the provinces of Aklan, Capiz,

Guimaras, Negros Occidental, Antique and Iloilo. The primary area of business activity is in Iloilo City where most government and private regional offices are located.

Region 7 or Central Visayas cover the provinces of Bohol, Negros Oriental,

Siquijor and Cebu. For this area, Metro Cebu is a major business activity center.

Region 8 or Eastern Visayas includes the provinces of Biliran, Eastern

Samar, Leyte, Northern Samar, Southern Leyte and Western Samar. Tacloban City is the main hub of commercial activity.

For the Rapid Appraisal of BDS Markets, Regions 6 and 7 were the main

areas covered in the interviews and observation; specifically Iloilo and Cebu.

A. VISAYAS MACRO ECONOMIC SITUATIONER

The Visayas contributed 16% of Gross National Domestic Product

nationwide. Regions 6 and 7 contributed 43% and 42% respectively to the Visayas GNDP. (See Exhibit 1.)

Gross National Domestic Product for Regions 6 and 7 has experienced

growth for the past five years. Relative to other regions in Luzon, these regions have experienced higher growth but Regions 9, 10 and 11 in Mindanao exhibited faster growth.

Gross value added in the manufacturing and service sector in Regions

6 and 7 has continued to grow over the past 5 years. (See Exhibits 2 and 3.)

Gross value added in construction, mining and quarrying has declined

in the past years for Central and Western Visayas. (See Exhibits 4 and 5.)

Agricultural, fishery and forestry gross value added declined from 1999

to 2000 in Central Visayas but slightly increased in Western Visayas. (See Exhibit 6.)

Personal consumption expenditure has continued to grow in both

regions. (See Exhibit 7.)

B. SMALL AND MEDIUM ENTERPRISE SITUATIONER Of the total 70,236 SMEs in the Philippines, 9,480 or 13.5% are located

in the Visayas region. 1

The 8,206 SMEs in Regions 6 and 7 comprise a large 87% of SMEs in the region. Western Visayas with 3,353 SMEs has a share of 41% while Central Visayas with 4,853 SMEs has a share of 59%.

SMEs generate employment of 1,938,913 people or 34% of the total

employment nationwide. The Visayas SMEs absorbs 14% of this or about 263,137 people.

SMEs in Western Visayas has generated employment for 91,424 while

Central Visayas SMEs provided employment for 139,295. This represents 35% and 53% shares respectively.

C. BUSINESS SERVICES SITUATIONER Information obtained from the Cebu and Iloilo yellow pages indicate

very few available business service providers. (See Annexes 1 and 2.)

Considering advertising, legal, computer equipment and rentals, courier, internet services, shopping centers and telecommunications, there were 171 listed companies in Iloilo and 216 in Cebu.

The 171 service providers were available for the 46,346 SMEs in Iloilo

while the 216 companies were available for 49,759 Cebu SMEs.

Some specific indicators are: one (1) advertising agency for 46,346 SMEs in Iloilo and nine (9) advertising agencies for 49,759 SMEs in Cebu and six (6) internet service providers in Iloilo and nine (9) in Cebu.

1 http://www.census.gov.ph/data/sectoraldat/2000/establishment00/html

III. Profile of Enterprise BDS Users (Demand) A. Awareness Levels of Business Development Services A maximum of 5 of the 21 or 24% of the enterprise users was able to

spontaneously identify services that assisted in their business. More spontaneous answers for advertising, accounting, transportation and e-mail / internet services were gathered than other services. (See Annex 3 - Table 1.)

One hundred percent (100%) awareness on the availability of business

services were obtained for phone and fax services, courier, transportation and internet / e-mail services.

Lowest awareness levels were encountered for training (computer and

non-computer based), marketing information and computer based selling and marketing.

For legal and accounting services, friends, relatives and referrals were

primary sources of information. (See Annex 4.) For advertising and some marketing related services, referrals and

advertisements in the yellow pages were sources of awareness. For most often used services i.e. courier, transportation, communication,

etc., the pervasive presence of large corporations and long-term patronage were mentioned for sources of awareness.

Information on marketing and marketing related services and training were

also likely to be obtained from associations or membership organizations. B. Usage / Patronage of BDS Usage and patronage of business development services range from a low

of 29% for computer based training to a high 100% for phone and fax services. (See Annex 3 - Table 2.)

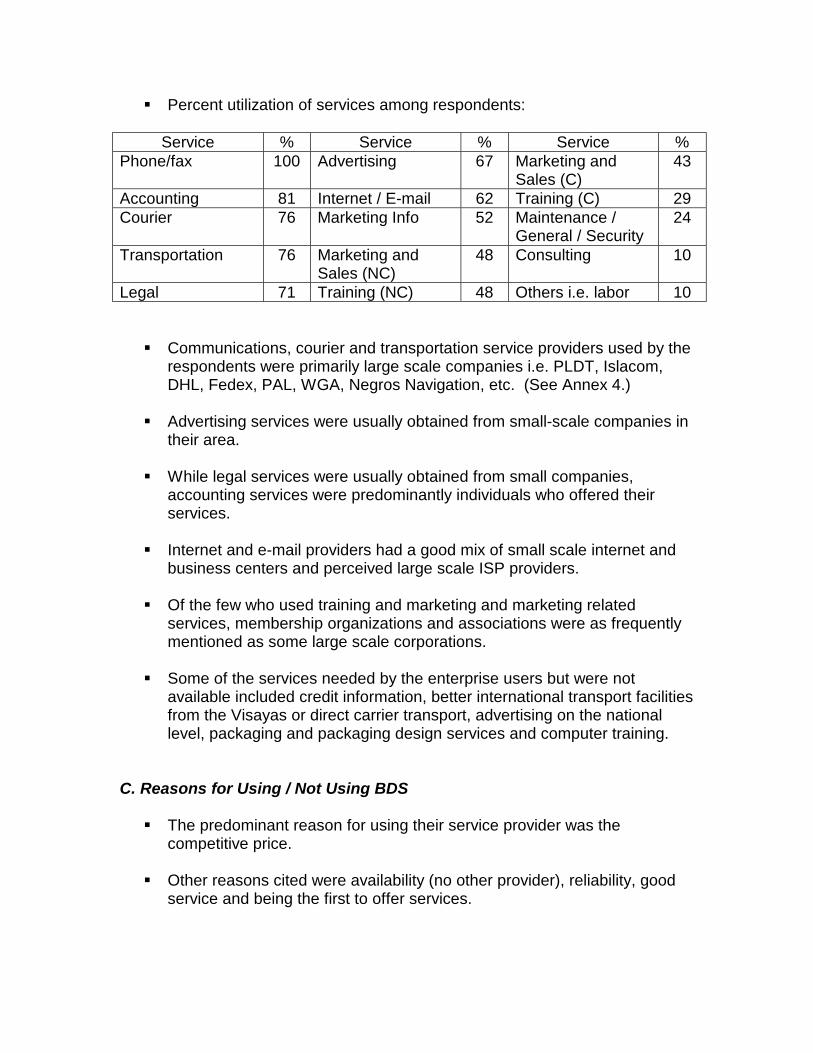

Percent utilization of services among respondents:

Service % Service % Service % Phone/fax 100 Advertising 67 Marketing and

Sales (C) 43

Accounting 81 Internet / E-mail 62 Training (C) 29 Courier 76 Marketing Info 52 Maintenance /

General / Security 24

Transportation 76 Marketing and Sales (NC)

48 Consulting 10

Legal 71 Training (NC) 48 Others i.e. labor 10 Communications, courier and transportation service providers used by the

respondents were primarily large scale companies i.e. PLDT, Islacom, DHL, Fedex, PAL, WGA, Negros Navigation, etc. (See Annex 4.)

Advertising services were usually obtained from small-scale companies in

their area. While legal services were usually obtained from small companies,

accounting services were predominantly individuals who offered their services.

Internet and e-mail providers had a good mix of small scale internet and

business centers and perceived large scale ISP providers. Of the few who used training and marketing and marketing related

services, membership organizations and associations were as frequently mentioned as some large scale corporations.

Some of the services needed by the enterprise users but were not

available included credit information, better international transport facilities from the Visayas or direct carrier transport, advertising on the national level, packaging and packaging design services and computer training.

C. Reasons for Using / Not Using BDS The predominant reason for using their service provider was the

competitive price. Other reasons cited were availability (no other provider), reliability, good

service and being the first to offer services.

Aside from a particular service provider not being available, the most often mentioned reason for not using a provider was the capability to do it in-house.

In-house capability was most often mentioned for accounting services,

advertising and promotions and marketing information. Other reasons for not using services i.e. advertising, training, marketing

information, etc. were the expensive price, poor quality service and the perception that the service was not needed i.e. advertising

D. Image of BDS providers Generally, the public agencies with which enterprise users had linkages

with obtained favorable images as they were cited as providers of free services.

Most respondents were satisfied with their private sector providers but

shared that they would appreciate better quality service. Essentially, users seem satisfied with the current level of service they get. ("We learn how to make do with what is available.") (See Annex 4.)

Among enterprises using the service, satisfaction was highest for phone

and fax providers and accounting providers. They were least satisfied with non computer based marketing and sales services. (See Annex 3 - Table 4.)

Most networking or market contacts and market information were

apparently indirectly obtained from membership organizations. E. Likelihood of patronizing / using BDS Majority of enterprise users indicated that phone and fax services and

transportation services were very important. (See Annex 3 - Table 4.) Aside from phone and fax services and transport, accounting, courier and

internet / e-mail services were considered as important. Despite the perceived importance, however, few instances of actively

seeking and availing of a free service were mentioned. Respondents were willing to "buy" services they needed and were

particularly willing to pay for services that they needed but were not available.

Services which were not available or which they perceived as too

expensive were obtained from informal sources. To illustrate, the absence of reputable marketing research groups is substituted by utilizing students to do data gathering as supervised by in-house marketing personnel.

Half (52%) of the respondents said they spent more for business services

this year than the previous year and sixty two percent (62%) were likely to spend even more for business services next year. (See Annex 3 - Tables 5 and 6.)

F. SME Respondent Profiles Eleven (11) respondent companies are based in Cebu, eight (8) in Iloilo

and two (2) in Aklan. Considering their primary product line, seven (7) manufacturing

companies, nine(9) service firms and five (5) retail organizations were interviewed.

Product lines of the manufacturer respondents included furniture,

processed fruits, bakery products, handicrafts, abaca and fiber blends and processed food.

Retail companies offered wine and liquor, hardware supplies, architectural

materials and household furnishings, residential real estate, commercial real estate, computer hardware and bakery products.

Service firms offered heavy equipment rentals, cargo forwarding, computer

services, accounting and financial services, management consulting, lodging and recreation, training, music and advertising and car rentals

The SME Respondents were in operation for an average of nineteen (19)

years. The "youngest" company had been in operation for three (3) years and the "oldest" company had been in operation for forty four (44) years

Annual expenditures for business services ranged from a low of twenty

thousand pesos (P20,000) to a high of twelve million pesos (P12M). Employee size ranged from a low of three (3) to a high of two hundred

thirty (230) Most of these respondents had in-house business services and outsourced

some business services.

Eighty percent (80%) of the enterprise respondents were members in various organizations and associations and / or had linkages with organizations.

Membership organizations included professional groups i.e. PICPA

(accounting), IBP (law), IATA (transport); industry associations i.e. Chambers of Commerce, Business Clubs and activity or membership specific groups i.e. AIM alumni, Philexport, etc.

IV. Profile of BDS Providers in the Visayas A. Private Sector Providers A total of thirteen (13) private sector business development service

providers were interviewed with an almost equal mix from Cebu and Iloilo cities. (See Annex 5 - Summary Information on Private Sector Providers)

Business services covered were advertising, legal, financial, business

development, distribution, transport, computer services, consulting and training.

All providers are registered and 7 out of the 12 are corporations; the

remaining providers are single proprietors. While service providers do not proactively search for SMEs, majority

service small to medium scale companies and a few also manage to reach large or micro-enterprises.

Advertising services seem to be more aggressive in sourcing clients by

going directly to client offices. Most providers rely on walk-in clients in their offices, inquiries on the phone

or referrals of existing clients. Majority (9 of the 12) are members of various organizations or link with

other organizations and companies. The primary reasons for linking with organizations are finding new markets

("networking") and getting market information. Most organization memberships are specific to their industry i.e. Philippine

Marketing Association, Hotel Restaurant Association of the Philippines, Integrated Bar of the Philippines, etc.

Most linkages with government agencies are related to their industry i.e.

Department of Energy and Natural Resources, Department of Science and Technology, etc.

Business planning and evaluation seems limited as most respondents were

not spontaneously familiar with their market segments. Cebu providers are conscious of the need to deliver better quality service

considering increasing competition.

Iloilo providers seem to be more concerned with operational efficiency and the lack of more "sophisticated" markets needing their services

Providers would like to see more government support for professionalizing

and / or legalizing some services i.e. ensuring "fly-by-night" individuals or corporations are identified.

Several realize a need for training and education to improve all aspects of

their business. A few would like assistance in financing to address expansion plans and

provision of quality services. Industry cooperation as well as more congenial relations within industry

associations were recommended to enhance provision on quality service. A group emphasized the need for values formation and education i.e.

ethical practices among businesses. Majority of those interviewed feel the quality and availability of business

services in the country is competitive or at par with those offered by other countries in the region.

Despite comparable quality, desire of providers to use emerging

technologies in further improving their products and services was mentioned.

B. Public Sector BDS Providers Five (5) public sector providers were interviewed: Department of Trade and

Industry for Cebu City and Iloilo City, National Statistics Office and National Economic and Development Authority in Cebu and the University of the Philippines in the Visayas (Iloilo City) (See Annex 6 - Summary Information on Public Sector Providers.)

The Business Information Center (BIC) of the DTI office in Iloilo City

provides business information and consulting i.e. industry studies, business books, technical assistance and to a limited extent also provides training.

The regional office of DTI in Cebu City provides information and assistance

on trade development and investment promotions, countryside development and trade regulations.

UPV in Iloilo City offers training and consulting, preparation of feasibility studies, accounting services and advertising to a limited extent as offered by their faculty and students.

The NSO provides statistics and information on the Philippines and also

offers books on Philippine statistics. NEDA in Cebu provides economic information and data.

Public sector companies provide services for free or at subsidized prices to

cover direct costs i.e. reproduction expenses for information obtained. Majority (90%) of those seeking business information from the BIC in Iloilo

and NEDA in Cebu are students or researchers. Those availing of the DTI services (investment promotions trade development, etc.) in Cebu City are primarily private SMEs in retail and service industries.

DTI Cebu and NSO are able to deliver services on-line through their web

pages aside from traditional outelts such as their offices, by phone, fax and mail. The services offered by the BIC in DTI Iloilo is physically located in their office. Most training and consulting of UPV are provided at client offices or in the school premises.

Respondents feel that most of the services they offer are also available

from the private sector and from business membership organizations but hesitate to judge quality level of these providers.

The DTI offices noted that private sector providers focus in cities only and

may be limited in servicing larger size companies. DTI seeks out SMEs outside of the cities through their provincial and regional offices.

Countrywide development activities, in particular is usually not offered by

the private sector because it is not profitable. All public sector agencies are linked to relevant agencies in the

government that they have to deal with. Aside from public corporations, they also have active linkages with BMOs, external agencies and NGOs.

NSO annually plans for offering new statistical information or new forms of

information. Other respondents usually develop new services or products in response to market needs.

Consistently, public sector providers voice a need to reach out to their

markets by improving awareness through promotions. They cite increases in government funding and more government support as crucial for this improvement. The lack of funds and manpower are common complaints.

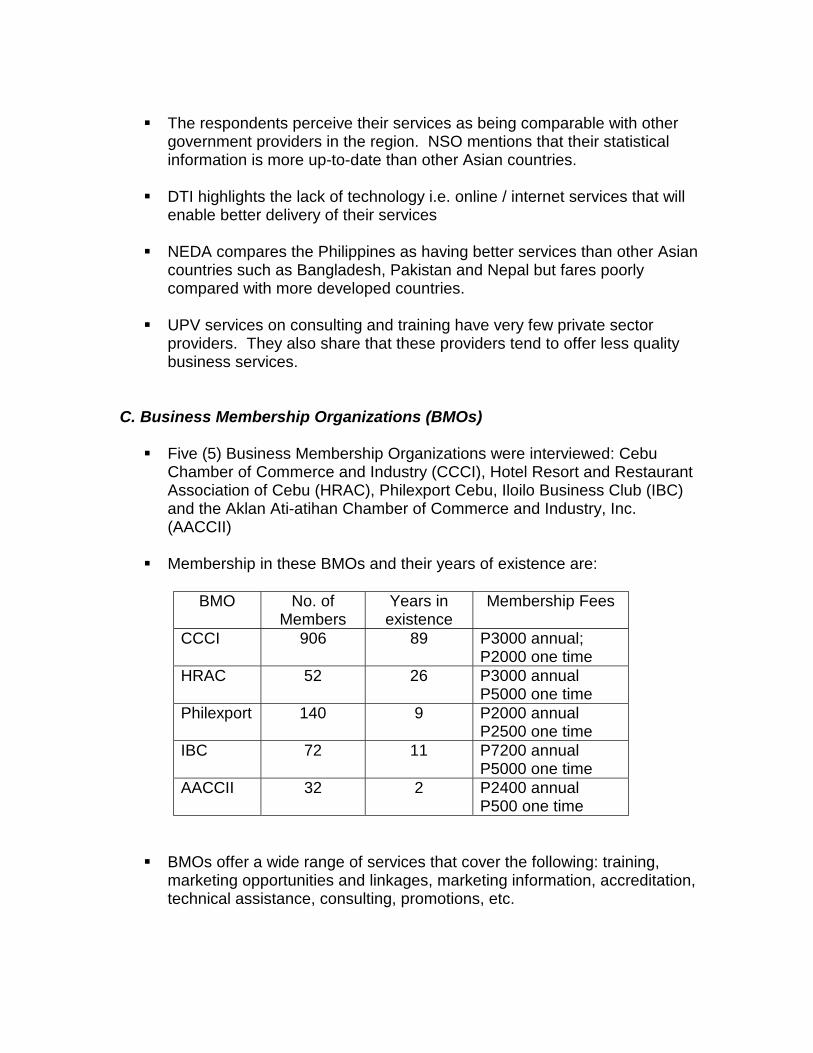

The respondents perceive their services as being comparable with other

government providers in the region. NSO mentions that their statistical information is more up-to-date than other Asian countries.

DTI highlights the lack of technology i.e. online / internet services that will

enable better delivery of their services NEDA compares the Philippines as having better services than other Asian

countries such as Bangladesh, Pakistan and Nepal but fares poorly compared with more developed countries.

UPV services on consulting and training have very few private sector

providers. They also share that these providers tend to offer less quality business services.

C. Business Membership Organizations (BMOs) Five (5) Business Membership Organizations were interviewed: Cebu

Chamber of Commerce and Industry (CCCI), Hotel Resort and Restaurant Association of Cebu (HRAC), Philexport Cebu, Iloilo Business Club (IBC) and the Aklan Ati-atihan Chamber of Commerce and Industry, Inc. (AACCII)

Membership in these BMOs and their years of existence are:

BMO No. of

Members Years in

existence Membership Fees

CCCI 906 89 P3000 annual; P2000 one time

HRAC 52 26 P3000 annual P5000 one time

Philexport 140 9 P2000 annual P2500 one time

IBC 72 11 P7200 annual P5000 one time

AACCII 32 2 P2400 annual P500 one time

BMOs offer a wide range of services that cover the following: training,

marketing opportunities and linkages, marketing information, accreditation, technical assistance, consulting, promotions, etc.

Expectedly, BMOs have linkages with several private and public organizations including foreign organizations.

Developing new services or products is limited to the needs of their market

and is not actively pursued. Except for IBC, the BMOs are generally optimistic in their ability to expand

and get new members. Government support, membership support, internal training, continuous

market information are seen as requirements to grow. CCCI highlights the lack of training and willingness of SMEs to pay for quality service and is considering external support from donors and the government.

BMOs perceive government and private sector service providers as

delivering poor quality of services. Aside from funding support, the attitude and mentality of government and

private sector providers are cited as needing improvement. Four of the five BMOs offer training mostly for their members. These

training seminars are usually specific to their area i.e. hotel management, export documentation although they also offer special management courses.

The training programs provided by BMOs are also offered by private sector

providers. The programs are not offered by government agencies. Private sector providers of training are usually hampered by the lack of qualified local trainors.

Other services offered by BMOs are conferences, exhibits, market info,

seminars, publications, policy advocacy and processing of documents. Payment is usually required from participants availing of BMO services. In

some cases, training is a benefit from paying membership dues or is usually charged at partial cost.

Promotional activities i.e. exhibits and publications are offered by the

private sector. Policy advocacy and other activity specific services are not suited for private service providers. Government, on the other hand, may offer some activities but usually targets micro enterprises.

D. External Support Agencies The External Support Agencies and specific programs covered in the study

generally targetted the local government units (LGUs). JICA's Cebu SEED provides assistance to the LGUs in Cebu for the

"socio-economic development and empowerment of the province" through livelihood generation.

The Canadian Urban Institute of CIDA in Iloilo City supports LGUs directly

with the goal of eventually assisting the private sector indirectly. ESAs recognize the availability of several business services from the

government such as technical assistance, project consultations, market development and information, financing, skills training, product development and design and other enterprise support programs.

They mentioned that the private sector offers more specific services such

as banking and financial services, marketing, advertising and promotions, courier and transport, telecommunications, manpower, training and consultancy.

Business services from the private sector is generally of good quality

except that some may not be available to all companies or potential users i.e. financial services.

Advertising, sales and marketing services and training form the private

sector are usually not available or not maximized because of low market demand and limited resources to reach wider areas of coverage.

ESAs had varying ratings on service quality level for private sector

business service providers. Ratings were good, fair and poor. For the industry to grow, ESAs cited the need to have more investors,

increase competition for better quality levels, improve the quality of infrastructure, promote trade and tourism and increase affordability among SMEs,

To make the most of opportunities, it also seems necessary to reduce

bureacracy, improve infrastructure, improve business networks and work ethics, enhance policies and tax incentives and increase awareness.

Perceived constraints for private sector involvement are the unstable

political situation, unstable currency and security, absence of a critical mass to demand the services and competition from government that provides free services.

Major barriers to providing good quality service are lack of funding and

credit, lack of good infrastructure, red tape and bureaucracy, lack of manpower and willingness of the market to pay for quality service.

Possible solutions for constraints and barriers are good governance,

improving the business atmosphere and work ethics, improving peace and order, improving business systems and networking, private sector exposure, training, non-competitive stance from government.

To increase service quality, streamlining and standardizing business

operations for quality improvement can be supported by government. Business service providers may also be exposed to quality service.

V. Analysis of BDS Markets in the Visayas

A. Gaps analysis of SME expectations and BDS providers

COMMUNICATION OR AWARENESS GAP

There seems to be an apparent awareness gap between users and providers of business services.

Most enterprise users limit their regular patronage to business services

directly affecting production or delivery of their goods or services i.e. communication, transportation and delivery and accounting.

Market information, searching for new markets, increasing sales and

training are not sought after services among the enterprise users.

There seems to be relatively high awareness and patronage of internet and e-mail services but usage seems to be limited to mere communication rather than marketing, information and training.

This awareness gap is observed among Iloilo and Cebu users for

advertising services. Cebu enterprises are more likely to use advertising since the advertising agencies and marketing service providers seem to be more aggressive in looking for clients. (Note: The sole marketing services company listed in the Iloilo yellow pages could not be found.)

Awareness gaps for "non-traditional business services" i.e. marketing

information and training are likely to remain since most SMEs have not yet realized operational efficiency from their other business services i.e. transportation.

Communication gaps are also likely to remain since most enterprise

users rely on friends, relatives and associates in membership organizations for service provider referrals.

Non-personal means of communicating product or service offers can be

more effective once an awareness of such business services is present.

Training services seem to be the primary "beneficiary" of the awareness and communication gap. While there seems to be a number of training service providers, few enterprise users mention training as a regular business service they use or are aware of.

Awareness and communication gaps seem to be prevalent between

users and the government service providers. Most SMEs see government as regulatory or licensing agencies and not as sources of free business services such as information and training.

DELIVERY, INACCESSIBILITY OR UNAVAILABILITY

As discussed, enterprise users "make do with what is available". In

some cases, they individually find solutions to their problems by sourcing outside their immediate location i.e. the case of international transport - Cebu directly to Europe

Service providers involved in sales and marketing activities i.e. selling,

information, research, etc. seems to be unavailable to most SMEs. Non-use, however, is sometimes a decision of the entrepreneur who is not willing to pay for market info and promotions.

BMOs that offer business services also tend to exclude SMEs from their

market reach.

KNOWLEDGE OR INFORMATION GAP

Several service providers, particularly BMOs, mention the need for educating the market in the use of "non-traditional" business services.

Enterprise users also tend to personalize their business service need

("in-house accounting is best because we understand our business best") and do not bother to look for qualified service providers.

Interestingly, some small business service providers are also not sure

of how their products and services are able to help SMEs. A number of these companies are reactive to market forces and are satisfied with their existing client base.

Enhancing strategic marketing capability of business service providers

seems essential to improving the BDS market.

STANDARDS OR EXPECTATIONS / EXPERIENCE GAP

The level of quality service provided by business service enterprises meets the expectations of enterprise users because most enterprise users are limited to one or two choices of service providers i.e. communications.

Aside from having limited choices of service providers, experience with service providers seems to be limited to very few encounters with non-traditional services i.e. market linkages, training etc. Expectations are necessarily relatively low.

B. Stakeholder Analysis

INTER-RELATIONSHIPS OF STAKEHOLDERS

Cebu, Iloilo and to a certain extent Aklan BDS markets are in various stages of growth. The Aklan respondents sought out Iloilo service providers while a number of Iloilo enterprise users had to go to Cebu for reliable business service providers.

This varying level of activity in each area was observed across all

respondent groups from government, service provider, enterprise user and BMOs.

The BMOs seem to be the most influential group in BDS markets.

Government service providers realize the relative ease of BMOs to offer

various products and services. Service providers see the need to become part of these BMOs to reach their markets and the more progressive enterprise users are likely to be members of several BMOs.

Most BMOs, however, tend to be "exclusive" groups that limit their

services for members. This was observed in Iloilo were the 3 BMOs (IBC, Iloilo Chamber of Commerce and Filipino Chinese Chamber of Commerce) apparently had some relationship problems.

The BMOs in Cebu, particularly the 89-year old CCCI, seems to be very

effective in generating support from its members in undertaking activities that benefit a relatively large number of SMEs.

Business service providers see a need to associate with other service

providers to a limited extent in order to be more effective and efficient in delivering their services and to expand their markets.

External support agencies have a good grasp of the constraints and

barriers to the development of business services and the delivery of quality service.

Assistance from external support groups usually target the government

sector.

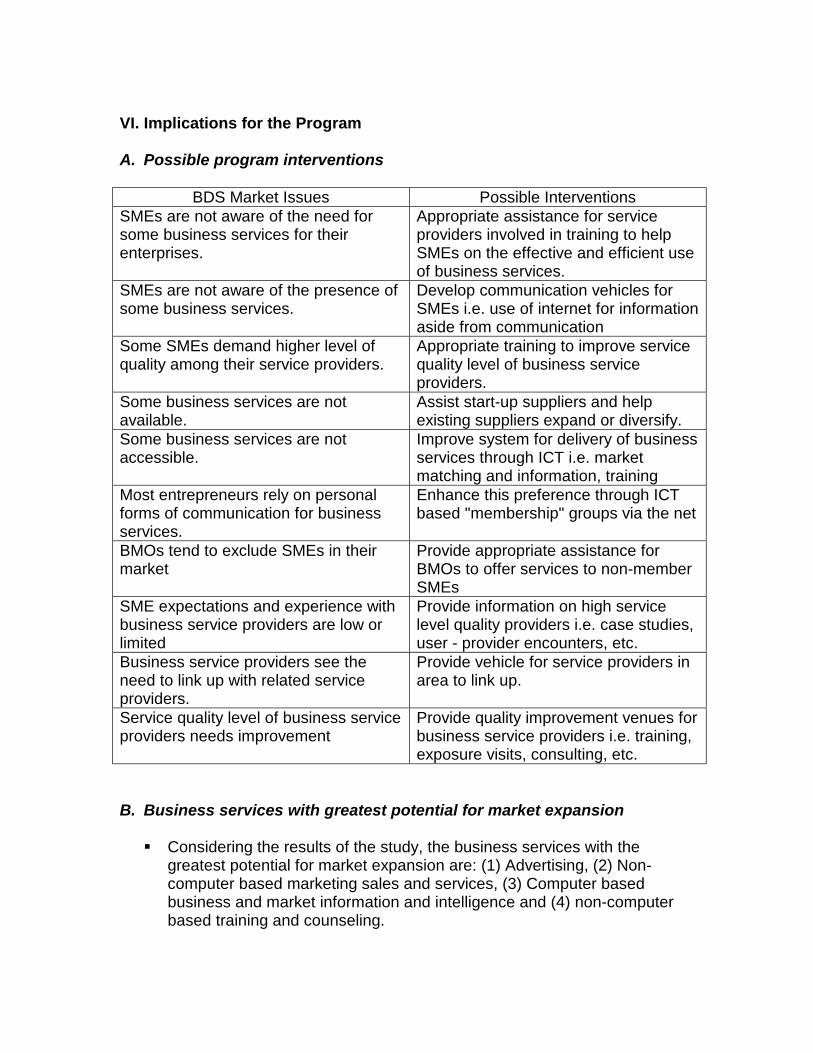

VI. Implications for the Program A. Possible program interventions

BDS Market Issues Possible Interventions SMEs are not aware of the need for some business services for their enterprises.

Appropriate assistance for service providers involved in training to help SMEs on the effective and efficient use of business services.

SMEs are not aware of the presence of some business services.

Develop communication vehicles for SMEs i.e. use of internet for information aside from communication

Some SMEs demand higher level of quality among their service providers.

Appropriate training to improve service quality level of business service providers.

Some business services are not available.

Assist start-up suppliers and help existing suppliers expand or diversify.

Some business services are not accessible.

Improve system for delivery of business services through ICT i.e. market matching and information, training

Most entrepreneurs rely on personal forms of communication for business services.

Enhance this preference through ICT based "membership" groups via the net

BMOs tend to exclude SMEs in their market

Provide appropriate assistance for BMOs to offer services to non-member SMEs

SME expectations and experience with business service providers are low or limited

Provide information on high service level quality providers i.e. case studies, user - provider encounters, etc.

Business service providers see the need to link up with related service providers.

Provide vehicle for service providers in area to link up.

Service quality level of business service providers needs improvement

Provide quality improvement venues for business service providers i.e. training, exposure visits, consulting, etc.

B. Business services with greatest potential for market expansion Considering the results of the study, the business services with the

greatest potential for market expansion are: (1) Advertising, (2) Non-computer based marketing sales and services, (3) Computer based business and market information and intelligence and (4) non-computer based training and counseling.

VII. Further Studies and Market Analysis

To add precision to the BDS market analysis, any or all of the market research programs can be conducted:

1) A larger enterprise user survey using more structured sampling i.e. quota and cluster sampling and wider areas of coverage may be conducted to assess specific industry sectors requiring BDS support and to specify available service providers. Profiles of heavy BDS users can also be analyzed better.

2) A focused group discussion among enterprise heavy user groups and

minimal or non-user groups to determine differentiating SME characteristics for use or non use of BDS as well as to enhance strategies and programs to increase usage.

3) Case studies of marketing programs or operations of BMOs may be

conducted to determine applications for new organizations specifically targeting smaller scale enterprises.

4) A specialized survey on quality standards between enterprise users and

private sector providers may be done to enhance this issue on BDS markets.

5) A more-in-depth analysis of specific business services particularly

advertising and marketing, professional services i.e. accounting and legal, training and computer based business assistance may be done through surveys. This can be incorporated with the consumer survey mentioned previously.

In the course of the study, more information can be obtained from BMOs

and public sector agencies and educational institutions not covered in the study. This includes the following:

1) More Chambers of Commerce and Industry 2) Specific divisions and units of DTI with front-line business services

3) Schools and universities in the regions and in Manila i.e. AIM and

UA&P with programs and projects assisting SMEs in the area

4) Industry specific BMOs

The national, regional and provincial offices of NEDA, NSO and DTI would also have more secondary data on the Visayas region.