rating company buy hengrui medicineimg3.gelonghui.com/pdf201611/pdf20161118140416186.pdf · buy...

TRANSCRIPT

Deutsche Bank Markets Research

Rating

Buy Asia

China

Health Care

Pharmaceuticals / Biotechnology

Company

Hengrui Medicine

Date

16 November 2016

Company Update

Revising estimates due to pipeline prioritization

Reuters Bloomberg Exchange Ticker 600276.SS 600276 CH SHH 600276

Forecasts And Ratios

Year End Dec 31 2014A 2015A 2016E 2017E 2018E

Sales (CNYm) 7,452.3 9,316.0 11,273.5 13,375.8 16,141.5

DB EPS FD(CNY) 0.64 0.92 1.13 1.36 1.66

Source: Deutsche Bank estimates, company data 1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses

the year end close

Key changes to our estimates for the late-stage pipeline

________________________________________________________________________________________________________________

Deutsche Bank AG/Hong Kong

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016.

Price at 15 Nov 2016 (CNY) 45.30

Price target - 12mth (CNY) 55.00

52-week range (CNY) 51.70 - 38.90

Shanghai Composite 3,207

Jack Hu, Ph.D

Research Analyst

(+852 ) 2203 6208

Linc Yiu

Research Associate

(+852 ) 2203 6248

Bo Yu

Research Associate

(+852 ) 2203 5928

Price/price relative

20

30

40

50

60

70

11/14 5/15 11/15 5/16

Hengrui Medicine

Shanghai Composite (Rebased)

Performance (%) 1m 3m 12m

Absolute -1.3 -0.2 -10.2

Shanghai Composite 4.7 2.6 -10.5

Source: Deutsche Bank

We make the following changes to our model on expecting Hengrui to re-prioritize its pipeline: 1) we now expect the launch of SHR1210, its anti PD-1 mAb, in 2H19 with a combo strategy with its own apatinib or Abraxane generic; 2) we anticipate SHR6390 (CDK4/6 inhibitor) and SHR3680 (AR antagonist) to be launched in 2H19 for breast cancer and prostate cancer respectively; 3) we estimate the refiling of 19K and retagliptin by YE16 and 2Q17 respectively, 4) we remove famitinib from our model for now; 5) we expect the launch of Abraxane generic in 1H18. As such, we model RMB7.3 per share for NPV of these late-stage compounds, vs. RMB6.8 previously.

Innovative drugs: pyrotinib, SHR1210, SHR3680, and SHR6390 the priority Hengrui recently started a P2/3 study on its PD-1 mAb in 2L/3L liver cancer, while the P1/2 study on SHR1210/apatinib in gastric cancer is ongoing. We believe the combo strategy will effectively differentiate its first anti-PD-1 drug amid intensive competition. While Hengrui could be the first domestic company to launch an IO drug, we model only RMB1.2-1.8bn peak sales but keep apatinib peak sales estimates intact to reflect Hengrui's realistic decision-making. For SHR3680, we expect a launch in 2H19 while the company may target an earlier PC setting with a premium pricing strategy, although the ongoing P1/2 study is on 3L. For SHR3680, we see a chance of clinical activity in breast cancer, similar to palbociclib. For pyrotinib, we believe the P3 study in 3L breast cancer is on track and we expect the completion in 2018. We highlight that the P2 study on henaglifozin (SGLT-2 inhibitor) has been completed and the P3 study should start in the near term.

Generics: expect Abraxane launch in 1H18; slightly adjust POS for Advair We continue to believe the Abraxane generic could reach RMB1-1.2bn peak sales, while the launch is expected in 1H18 with a priority review from CFDA. We also highlight that Hengrui is likely to be first-to-market (FTM) and the drug is likely to replace Lipusu in the long run. For Advair generic, we lower our probability of success to 55-65% from 60-70% as the technical barrier for the inhaler could be difficult to overcome. However, Hengrui is slightly ahead of SBP for this drug in the formulation of a blister strip.

Maintaining our price target of RMB55; risks Our price target is based on 40.5x 2017E EPS. We believe 40.5x is justified as A-share peers are trading at 29x with 19% EPS growth in 2017E (vs. 20% for Hengrui). The premium is justified by the superior value of its products and its strong pipeline. Key risks include product launch delays and price cuts.

Distributed on: 16/11/2016 04:51:42 GMT

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Page 2 Deutsche Bank AG/Hong Kong

Model updated:15 November 2016

Running the numbers

Asia

China

Pharmaceuticals / Biotechnology

Hengrui Medicine Reuters: 600276.SS Bloomberg: 600276 CH

Buy Price (15 Nov 16) CNY 45.30

Target Price CNY 55.00

52 Week range CNY 38.90 - 51.70

Market Cap (m) CNYm 106,344

USDm 15,510

Company Profile

Jiangsu Hengrui Medicine Co. Ltd. was established in 1970 and its headquarters is in Lianyungang, Jiangsu province. The company is primarily involved in the manufacture and R&D of drugs, including those for oncology, muscle relaxation and anesthetics, contrast agents, electrolytes, and anti-infective drugs. Apart from its domestic business, Hengrui exports drugs to the US, Europe, and other countries.

Price Performance

20

30

40

50

60

70

Nov 14Feb 15May 15Aug 15Nov 15Feb 16May 16Aug 16

Hengrui MedicineShanghai Composite (Rebased)

Margin Trends

23

24

26

27

29

30

13 14 15 16E 17E 18E

EBITDA Margin EBIT Margin

Growth & Profitability

19

20

21

22

23

24

25

0

5

10

15

20

25

30

13 14 15 16E 17E 18E

Sales growth (LHS) ROE (RHS)

Solvency

-70-60-50-40-30-20-10

0

13 14 15 16E 17E 18E

Net debt/equity (LHS) Net interest cover (RHS)

Jack Hu, Ph.D

+852 2203 6208 [email protected]

Fiscal year end 31-Dec 2013 2014 2015 2016E 2017E 2018E

Financial Summary

DB EPS (CNY) 0.52 0.64 0.92 1.13 1.36 1.66

Reported EPS (CNY) 0.53 0.65 0.92 1.13 1.36 1.66

DPS (CNY) 0.04 0.05 0.06 0.08 0.09 0.12

BVPS (CNY) 2.7 3.3 4.2 5.3 6.5 8.1

Weighted average shares (m) 2,350 2,338 2,348 2,348 2,348 2,348

Average market cap (CNYm) 50,845 61,188 100,841 106,344 106,344 106,344

Enterprise value (CNYm) 48,993 58,103 96,055 99,888 97,886 95,494

Valuation Metrics P/E (DB) (x) 41.7 40.9 46.5 40.0 33.4 27.3

P/E (Reported) (x) 41.1 40.4 46.4 40.1 33.4 27.3

P/BV (x) 9.78 8.63 11.58 8.58 6.92 5.60

FCF Yield (%) 1.8 2.1 1.9 1.8 2.1 2.6

Dividend Yield (%) 0.2 0.2 0.1 0.2 0.2 0.3

EV/Sales (x) 7.9 7.8 10.3 8.9 7.3 5.9

EV/EBITDA (x) 30.6 30.4 36.3 31.5 25.9 20.7

EV/EBIT (x) 34.3 34.2 39.7 33.9 28.0 22.4

Income Statement (CNYm)

Sales revenue 6,203 7,452 9,316 11,274 13,376 16,142

Gross profit 5,045 6,139 7,944 9,673 11,503 13,962

EBITDA 1,599 1,912 2,643 3,175 3,778 4,612

Depreciation 168 209 218 228 281 343

Amortisation 3 4 4 5 6 7

EBIT 1,428 1,699 2,420 2,942 3,491 4,261

Net interest income(expense) 25 81 148 175 226 258

Associates/affiliates 0 0 0 0 0 0

Exceptionals/extraordinaries -3 -7 -7 0 0 0

Other pre-tax income/(expense) 28 27 1 0 13 32

Profit before tax 1,479 1,800 2,562 3,117 3,731 4,552

Income tax expense 186 227 338 411 492 601

Minorities 54 57 52 52 52 52

Other post-tax income/(expense) 0 0 0 0 0 0

Net profit 1,238 1,516 2,172 2,653 3,186 3,899

DB adjustments (including dilution) -19 -19 -1 8 0 0

DB Net profit 1,219 1,497 2,171 2,661 3,186 3,899

Cash Flow (CNYm)

Cash flow from operations 1,365 1,574 2,277 2,472 2,947 3,524

Net Capex -453 -298 -394 -564 -669 -807

Free cash flow 912 1,276 1,883 1,909 2,278 2,717

Equity raised/(bought back) 16 136 19 0 0 0

Dividends paid -99 -122 -150 -186 -223 -273

Net inc/(dec) in borrowings 10 -10 0 0 0 0

Other investing/financing cash flows 0 1 -67 0 0 0

Net cash flow 840 1,280 1,684 1,723 2,055 2,444

Change in working capital -104 -198 -169 -466 -579 -777

Balance Sheet (CNYm)

Cash and other liquid assets 2,169 3,449 5,133 6,856 8,911 11,355

Tangible fixed assets 1,564 1,624 1,770 2,106 2,494 2,958

Goodwill/intangible assets 203 200 196 191 185 178

Associates/investments 1 1 79 79 79 79

Other assets 3,283 3,812 4,319 4,989 5,739 6,782

Total assets 7,220 9,087 11,497 14,221 17,407 21,351

Interest bearing debt 20 10 0 0 0 0

Other liabilities 544 923 1,139 1,343 1,514 1,779

Total liabilities 564 933 1,139 1,343 1,514 1,779

Shareholders' equity 6,357 7,798 9,931 12,399 15,362 18,988

Minorities 299 355 426 479 531 584

Total shareholders' equity 6,656 8,154 10,358 12,878 15,893 19,572

Net debt -2,149 -3,439 -5,133 -6,856 -8,911 -11,355

Key Company Metrics

Sales growth (%) 14.1 20.1 25.0 21.0 18.6 20.7

DB EPS growth (%) 16.9 23.4 44.5 22.6 19.7 22.4

EBITDA Margin (%) 25.8 25.7 28.4 28.2 28.2 28.6

EBIT Margin (%) 23.0 22.8 26.0 26.1 26.1 26.4

Payout ratio (%) 8.0 8.1 6.9 7.0 7.0 7.0

ROE (%) 21.4 21.4 24.5 23.8 23.0 22.7

Capex/sales (%) 7.3 4.0 4.2 5.0 5.0 5.0

Capex/depreciation (x) 2.7 1.4 1.8 2.4 2.3 2.3

Net debt/equity (%) -32.3 -42.2 -49.6 -53.2 -56.1 -58.0

Net interest cover (x) nm nm nm nm nm nm

Source: Company data, Deutsche Bank estimates

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Deutsche Bank AG/Hong Kong Page 3

Late-stage pipeline

Summary of innovative pipeline

We highlight the innovative drugs developed by Hengrui in the following

exhibit. With ongoing regulatory overhaul, the cost of clinical studies is going

up rapidly. As such, we expect every company to re-prioritize its pipeline to

focus on mid/late stage compounds with reasonable product differentiation,

which could lead to appropriate ROI.

Figure 1: Pipeline summary for Hengrui

Phase 1 Phase 2 Phase 3 NDA

SHR1314 (Il-17 mAb) Henagliflozin (SGLT2 inhibitor) Apatinib (VEGFR-2 inhibitor) 19K (long acting GCSF)

Psoriasis Diabetes NSCLC/Liver cancer Oncology

HR1539 (Hedgehog inhibitor) # GLP-1 agonist Retagliptin/metformin Retagliptin (DPP-4 inhibitor) *

Solid tumors Diabetes Diabetes Diabetes

SHR3162 (PARP inhibitor) # Hetrombopag Olamine (TPOR) * Pyrotinib (EGFR/Her2 inhibitor) *

Solid tumors ITP HER2+ breast cancer

SHR6390 (CDK4/6 inhibitor) Remimazolam (GABA receptor agonist)

Solid tumors Analgesics

SHR7390 (MEK inhibitor) Pyrotinib (EGFR/Her2 inhibitor) *

Solid tumors NSCLC

GPR40 agonist * SHR3680 (AR antagonist) #

Diabetes Prostate cancer

SHR0302 (JAK1 inhibitor) SHR1210 (PD-1 mAb) #

Rheumatoid arthritis/Psoriasis Liver cancer/Gastric cancer

SHR4640 (URATI inhibitor) # Chemical drug

Gout Biological drug

* US phase 1 ongoing

# Australia phase 1 ongoing Source: Deutsche Bank, Company data

We summarize our revised expectations in each of the major compounds as

follows:

PD1 and its combo strategy: we now expect the launch of SHR1210,

its anti PD-1 mAb, in 2H19 with a combo strategy with its own

apatinib or Abraxane generic. We believe a combo strategy could

effectively differentiate its first IO drug from intensive competition. We

also anticipate that Hengrui will avoid popular indications such as

melanoma, but will focus instead on large solid tumor indications with

large prevalence in the Chinese population, such as liver, gastric and

lung cancers. As SHR1210 is moved into the P2/3 study officially, we

now expect Hengrui to be the first to launch an IO drug in China. We

modestly model RMB1.2-1.8bn peak sales to reflect future competition

in IO, although we kept our peak sales for apatinib and Abraxane

generic intact to demonstrate our confidence in Hengrui's combo

strategy. We believe it is more reasonable to forecast these three

compounds together.

SHR3680 could target early stage of prostate cancer: This AR

antagonist is in P1/2 for 3L prostate cancer. We see a chance of

premium pricing in earlier settings to maximize its commercial value.

We now model the product launch in 2H19.

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Page 4 Deutsche Bank AG/Hong Kong

SHR6390 (CDK4/6 inhibitor) remains a wild card: we see a chance for

this compound to demonstrate clinical activity in ER+/Her2- breast

cancer patients, just like palbociclib. Additionally, we believe it is

possible for this compound to reach the market before palbociclib. We

anticipate the product launch in 2H19.

Henagliflozin could reach the market sooner than expected: we now

model the product launch in 2H19 vs. 2020 previously, as we believe

the phase 2 study has been completed while the phase 3 study is

likely to start soon. We also increase our POS to 75-85% from 70-80%.

We remove famitinib from our model.

We estimate the refiling of 19K and retagliptin by YE16 and 2Q17

respectively. We believe consensus might be too bullish on the

retagliptin timeline and peak sales opportunity.

On generics, we expect the launch of Abraxane generic in 1H18. We

also reduce POS for Advair to 55-65% from 60-70%.

On mAb opportunities, Hengrui is likely to focus on biosimilars of

Avastin, TD-M1, pertuzumab, while clinical studies are likely to start in

2017 after regulatory approvals.

Valuation of the late-stage pipeline

We now model NPV of RMB7.3 from these mid/late stage compounds, vs. 6.8

previously. We summarize our estimates in the following exhibit.

Figure 2: Valuation of late-stage pipeline candidates

Drug Ind ication

Launch

date

Peak sa les

(RMBm)

Probab il ity o f

success

Va lue per share

(Prob. Ad justed)

Innovative drugs

19K Oncology 2H17 1,200-1,500 85-95% 0.73

Retagliptin Diabetes 2H18 1,600-2,200 83-93% 0.94

Pyrotinib Breast cancer, NSCLC 1H19 1,200-1,600 80-90% 0.62

SHR1210 (anti-PD-1 mAb) Liver cancer, gastric cancer 2H19 1,200-1,800 60-70% 0.47

SHR3680 (AR antagonist) Prostate cancer 2H19 800-1,200 50-60% 0.28

SHR6390 (CDK4/6 inhibitor) Breast cancer 2H19 1,500-2,000 35-45% 0.79

Henagliflozin Diabetes 2H19 1,000-1,400 75-85% 0.51

Remimazolam Anesthetics 2020 800-1,200 75-85% 0.39

Hetrombopag Olamine Idiopathic thrombocytopenic purpura 2020 800-1,200 70-80% 0.36

Subtota l 5.1

Generic d rugs

Cialis Erectile dysfunction 2H17 1,000-1,400 85-95% 0.37

Celebrex Autoimmune disease 2H17 1,000-1,500 85-95% 0.39

Exforge CCV 2H17 800-1,000 85-95% 0.28

Abraxane Oncology 1H18 1,000-1,200 85-95% 0.35

Advair Respiratory 2H18 2,000-2,500 55-65% 0.43

Lyrica CNS 2020 1,200-1,800 85-95% 0.39

Subtota l 2.2

Tota l 7.3 Source: Deutsche Bank, Company data

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Deutsche Bank AG/Hong Kong Page 5

SHR1210: anti-PD-1 monoclonal antibody

Hengrui: two trials started recently in China

We believe Hengrui could be the first player to launch in China for its anti-PD-1

mAb. Hengrui recently filed two clinical trials for its anti-PD-1 mAb. The first

study, filed on 20 Oct, was a phase 1/2, single-arm, open-label study in liver

cancer or gastric cancer in combination with apatinib. The enrollment is

estimated to be 30, while the primary endpoint is an overall survival rate.

The second trial, filed on 14 Nov, was a phase 2/3 and open-label study on liver

cancer in second line or below. 60 patients will be enrolled in phase 2 and will

be divided into two groups to receive SHR1210 every two or three weeks. The

primary endpoint is an overall survival rate after six months and an overall

response rate. We summarize all ongoing trials for SHR1210 by Hengrui

below.

We model RMB1.2-1.8bn peak sales for SHR1210 and expect the product

launch in 2H19.

Figure 3: Ongoing trials on SHR1210 by Hengrui

Indications Line of therapy

Stage Study design Primary endpoint Enrollment Study arm Start Date

Estimated end date

Advanced hepatocellular carcinoma

2L or below

Phase 2/3 Open-label, parallel assignment, multi-center

Overall survival rate, overall response rate

60 SHR1210 (once/two week) vs. SHR1210 (once/three weeks)

Nov-16 Dec-18

Advanced hepatocellular carcinoma or gastric cancer

3L Phase 1/2 Open-label, single group, single center

Overall survival rate 30 SHR1210 + apatinib Oct-16 Oct-18

Advanced solid tumors 3L Phase 1 Open-label, single group, single center

Dose limited toxicity 36 SHR1210 Apr-16 Dec-16

Advanced melanoma 3L Phase 1 Open-label, single group, single center

Dose limited toxicity 36 SHR1210 Apr-16 Dec-16

Lung cancer 3L Phase 1 Open-label, single group, single center

Dose limited toxicity 45 SHR1210 Apr-16 Dec-16

Advanced solid tumors 3L Phase 1 (Australia)

Open-label, single group, multi center

Adverse events 24 INCSHR01210 Sep-15 Dec-17

Source: Deutsche Bank, clinicaltrial.gov

Competitive landscape for anti-PD-1/PD-L1 mAb by Chinese players

We highlight that there are four Chinese players developing PD-1/PD-L1

compounds, including JS001 from Shanghai Junshi, SHR1210 from Hengrui,

BGB-A317 from BeiGene and IBI308 from another Chinese player. There are

also four domestic players with its anti-PD-1/PD-L1 compounds pending

clinical trial approvals from the CFDA.

For Shanghai Junshi, we highlight it is the first domestic player to receive

clinical trial approval for its anti-PD-1 compound. We summarize the ongoing

trials for JS001 in the following table. We also highlight that there is an anti-

PD-L1 compound in preclinical stage.

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Page 6 Deutsche Bank AG/Hong Kong

Figure 4: Ongoing trials for JS001 by Shanghai Junshi

Indications Line of therapy

Stage Study design Primary endpoint Enrollment Study arm Start Date

Gastric cancer, head-and-neck cancer, esophageal cancer, nasopharyngeal carcinoma

2L or below Phase 1b/2

Open-label, single group, multi center Overall response rate 326 JS001 Sep-16

Triple-negative breast cancer 3L Phase 1 Open-label, single group, single center Adverse events 27 JS001 Aug-16

Advanced solid tumors 3L Phase 1 Open-label, single group, single center Adverse events 24 JS001 May-16

Melanoma, urological cancer 3L Phase 1 Open-label, single group, single center Adverse events 27 JS001 Apr-16

Lymphoma, lung cancer 3L Phase 1 Open-label, single group, single center Adverse events 54 JS001 Aug-16 Source: Deutsche Bank, clinicaltrial.gov

For BeiGene, its BGB-A317 received a clinical trial approval in China in Sep

2016. However no clinical trial has yet started. For ex-China, we highlight that

there are three trials in Australia/US. The company also published data from an

ongoing phase 1 study on 14 Nov. We summarize the ongoing trials below.

Figure 5: Ongoing trials for BGB-A317 by BeiGene

Indications Line of therapy

Stage Study design Primary endpoint Enrollment Study arm Start Date

Advanced tumors 3L Phase 1 (US and

Australia)

Open-label, single group, multi center Adverse events 300 BGB-A317 Jun-16

B-cell lymphoid malignancies 3L Phase 1 (Australia)

Open-label, single group, single center Adverse events 25 BGB-A317 + BGB-3111

Feb-16

Advanced solid tumors 3L Phase 1 (Australia)

Open-label, single group, multi center Adverse events and ORR

124 BGB-A317 + BGB-290

Jan-16

Source: Deutsche Bank, clinicaltrial.gov

Another Chinese company received clinical trial approval for IBI308 in China in

Sep 2016. A phase 1 study has started in China on advanced solid tumors. For

this drug, the global right has been licensed to Eli Lilly. We summarize the

ongoing study in China below.

Figure 6: Ongoing trials for IBI308

Indications Line of therapy

Stage Study design Primary endpoint Enrollment Study arm Start Date

Advanced solid tumors 3L Phase 1 Open-label, single group, multi center Adverse events 104 IBI308 Sep-16 Source: Deutsche Bank, clinicaltrial.gov

There are also four domestic players with its anti-PD-1/PD-L1 compounds

pending clinical trial approval from CFDA.

Figure 7: Domestic players with anti-PD-1/PD-L1 mAb pending for approval

Company Drug name (CN) Drug name (EN) Status start date

Registration number

Genor Bio (嘉和生物) 杰诺单抗注射液 NA Apr-16 CXSL1600016

Alphamab (康宁杰瑞) 重组人源化 PDL1 单域抗体 Fc 融

合蛋白注射液

KN035 May-16 CXSL1600033

Gloria Pharma (哈尔滨

誉衡)

抗 PD-1 单抗产品 GLS-010 注射

液

GLS-010 Jun-16 CXSL1600045

CStone Pharma (基石药业)

抗 PD-L1 全人单克隆抗体注射液 WBP3155 Oct-16 CXSL1600075

Source: Deutsche Bank, CFDA

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Deutsche Bank AG/Hong Kong Page 7

SHR3680 and SHR6390

SHR3680: androgen receptor (AR) antagonist

We highlight that Hengrui is making good progress in its phase 1/2 study for

this drug in 3L castration-resistant prostate cancer. As an AR antagonist, this

drug is similar to Xtandi (enzalutamide) from Medivation and Astellas. Xtandi

was approved by the US FDA in Aug 2012 to treat castration-resistant prostate

cancer. As of 2015, global sales reached USD1.9bn with USD1.1/0.8bn from

the US/ex-US. We model RMB0.8-1.2bn peak sales potential for this drug and

expect the product launch in 2H19.

Figure 8: Ongoing trials for SHR3680 by Hengrui in China

Indications Line of therapy

Stage Study design Primary endpoint Enrollment Study arm Start Date

Castration-resistant prostate cancer

3L Phase 1/2 Open-label, single group, multi center Maximum tolerated dose for phase 1; PFS for phase 2

140 SHR3680 Apr-16

Neoplasm, prostate cancer 3L Phase 1 Open-label, single group, single center Maximum tolerated dose 42 SHR3680 Sep-16

Source: Deutsche Bank, clinicaltrial.gov

SHR6390: CDK4/6 inhibitor

This drug is undergoing a phase 1 trial in China. As a CDK4/6 inhibitor, we see

a chance for this compound to demonstrate clinical activity in ER+/Her2-

breast cancer patients, just like palbociclib. We also believe that this

compound could be launched in China before palbociclib. Palbociclib is a

CDK4/6 inhibitor developed by Pfizer. The product was approved by the US

FDA in Feb 2015 for the treatment of ER-positive and HER2-negative breast

cancer in 1L. US sales of this drug reached USD723m in 2015 and USD1.5bn

in 9m16. We summarize the ongoing trials on SHR6390 by Hengrui in China in

the following exhibit.

Figure 9: Ongoing trials for SHR6390 by Hengrui in China

Indications Line of therapy

Stage Study design Primary endpoint Enrollment Study arm Start Date

Neoplasm 3L Phase 1 Open-label, single group, single center Maximum tolerated dose 40 SHR6390 Feb-16

Melanoma 3L Phase 1 Open-label, single group, single center Maximum tolerated dose 30 SHR3680 Jan-16 Source: Deutsche Bank, clinicaltrial.gov

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Page 8 Deutsche Bank AG/Hong Kong

Figure 10: Income statement

Income Statement (RMB m) 2012 2013 2014 2015 2016E 2017E 2018E 2019E

Revenue 5,435 6,203 7,452 9,316 11,274 13,376 16,142 19,747

Cost of sales (870) (1,158) (1,313) (1,372) (1,601) (1,873) (2,179) (2,567)

Gross profit 4,565 5,045 6,139 7,944 9,673 11,503 13,962 17,180

Revenue tax and others (95) (106) (133) (156) (192) (227) (274) (336)

Research and development costs (535) (563) (652) (892) (1,094) (1,311) (1,598) (1,975)

Administrative expenses (892) (1,156) (1,464) (1,843) (2,266) (2,702) (3,277) (4,028)

Distribution costs (2,340) (2,355) (2,844) (3,525) (4,273) (5,083) (6,150) (7,544)

EBIT - core 1,238 1,428 1,699 2,420 2,942 3,491 4,261 5,273

EBITDA - core 1,370 1,599 1,912 2,643 3,175 3,778 4,612 5,697

Other non-recurring items 35 19 19 1 (8) - - -

Other income 47 34 41 28 34 40 48 59

Other expense (1) (7) (14) (25) (34) (27) (16) (10)

Impairment loss of assets 45 (3) (7) (7) - - - -

Investment income 0 0 0 (3) - - - -

Gain/loss on fair value changes

Finance costs - net 16 25 81 148 175 226 258 329

Interest income 18 26 81 126 175 226 258 329

Interest expense and others (1) (1) (1) 22 - - - -

Profit before taxation - reported 1,346 1,479 1,800 2,562 3,117 3,731 4,552 5,651

Taxation (195) (186) (227) (338) (411) (492) (601) (746)

Tax rate 14% 13% 13% 13% 13% 13% 13% 13%

Net profit - reported 1,151 1,292 1,573 2,224 2,706 3,239 3,951 4,906

Non-controlling interests (74) (54) (57) (52) (52) (52) (52) (52)

Net income attributable to Equity holders - reported 1,077 1,238 1,516 2,172 2,653 3,186 3,899 4,853

Net income attributable to Equity holders - core 1,043 1,219 1,497 2,171 2,661 3,186 3,899 4,853

Common shares

EPS: Basic (RMB) - Reported 0.458 0.527 0.648 0.925 1.130 1.357 1.661 2.067

EPS: Diluted (RMB) - Reported 0.458 0.527 0.648 0.925 1.130 1.357 1.661 2.067

EPS: Basic (RMB) - core 0.444 0.519 0.640 0.925 1.133 1.357 1.661 2.067

EPS: Diluted (RMB) - core 0.444 0.519 0.640 0.925 1.133 1.357 1.661 2.067 Source: Deutsche Bank estimates, company data

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Deutsche Bank AG/Hong Kong Page 9

Appendix 1

Important Disclosures

*Other information available upon request

Disclosure checklist

Company Ticker Recent price* Disclosure

Hengrui Medicine 600276.SS 45.30 (CNY) 15 Nov 16 NA *Prices are current as of the end of the previous trading session unless otherwise indicated and are sourced from local exchanges via Reuters, Bloomberg and other vendors . Other information is sourced from Deutsche Bank, subject companies, and other sources. For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr. For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com/ger/disclosure/Disclosure.eqsr?ricCode=600276.SS

Analyst Certification

The views expressed in this report accurately reflect the personal views of the undersigned lead analyst(s) about the subject issuer and the securities of the issuer. In addition, the undersigned lead analyst(s) has not and will not receive any compensation for providing a specific recommendation or view in this report. Jack Hu

Historical recommendations and target price: Hengrui Medicine (600276.SS) (as of 11/15/2016)

1

2

3 45

6

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

Nov 14 Feb 15 May 15 Aug 15 Nov 15 Feb 16 May 16 Aug 16

Secu

rity

Pri

ce

Date

Previous Recommendations

Strong Buy Buy Market Perform Underperform Not Rated Suspended Rating

Current Recommendations

Buy Hold Sell Not Rated Suspended Rating

*New Recommendation Structure as of September 9,2002

**Analyst is no longer at Deutsche Bank

1. 06/10/2015: Upgrade to Buy, Target Price Change CNY55.00 Jack Hu, Ph.D

4. 16/06/2016: Buy, Target Price Change CNY49.50 Jack Hu, Ph.D

2. 30/10/2015: Buy, Target Price Change CNY60.00 Jack Hu, Ph.D 5. 31/08/2016: Buy, Target Price Change CNY50.00 Jack Hu, Ph.D

3. 14/04/2016: Buy, Target Price Change CNY59.50 Jack Hu, Ph.D 6. 01/11/2016: Buy, Target Price Change CNY55.00 Jack Hu, Ph.D

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Page 10 Deutsche Bank AG/Hong Kong

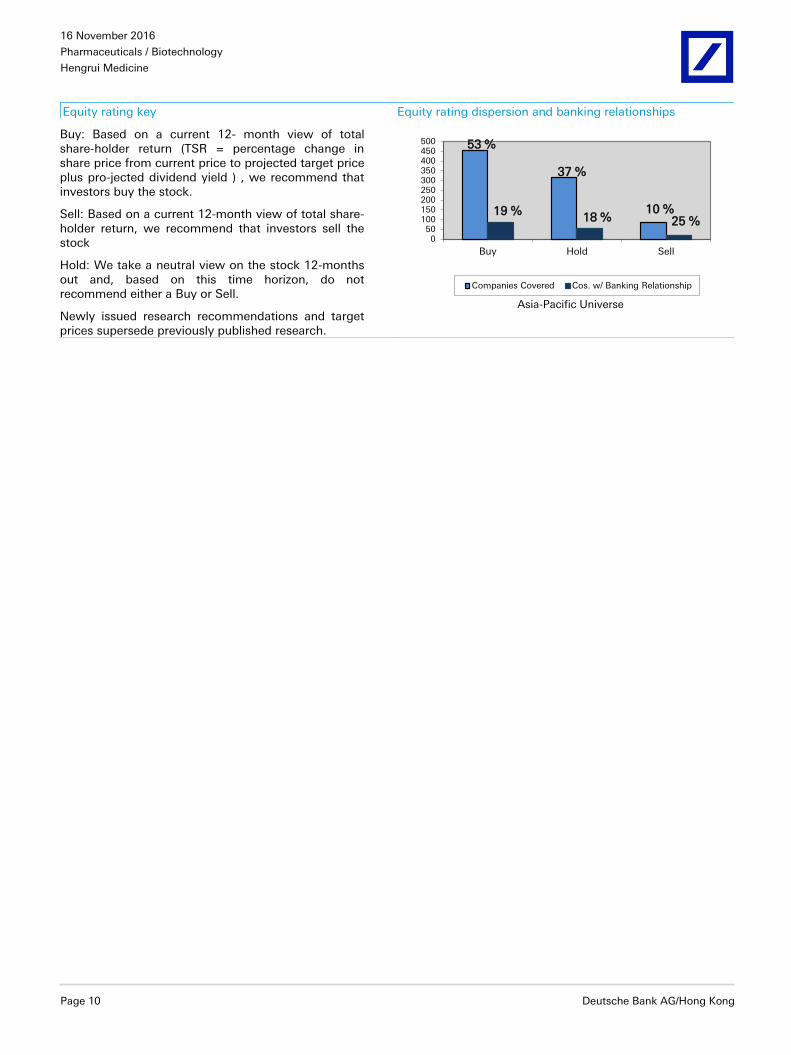

Equity rating key Equity rating dispersion and banking relationships

Buy: Based on a current 12- month view of total share-holder return (TSR = percentage change in share price from current price to projected target price plus pro-jected dividend yield ) , we recommend that investors buy the stock.

Sell: Based on a current 12-month view of total share-holder return, we recommend that investors sell the stock

Hold: We take a neutral view on the stock 12-months out and, based on this time horizon, do not recommend either a Buy or Sell.

Newly issued research recommendations and target prices supersede previously published research.

53 %

37 %

10 %19 %18 % 25 %

050

100150200250300350400450500

Buy Hold Sell

Asia-Pacific Universe

Companies Covered Cos. w/ Banking Relationship

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Deutsche Bank AG/Hong Kong Page 11

Additional Information

The information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively

"Deutsche Bank"). Though the information herein is believed to be reliable and has been obtained from public sources

believed to be reliable, Deutsche Bank makes no representation as to its accuracy or completeness.

If you use the services of Deutsche Bank in connection with a purchase or sale of a security that is discussed in this

report, or is included or discussed in another communication (oral or written) from a Deutsche Bank analyst, Deutsche

Bank may act as principal for its own account or as agent for another person.

Deutsche Bank may consider this report in deciding to trade as principal. It may also engage in transactions, for its own

account or with customers, in a manner inconsistent with the views taken in this research report. Others within

Deutsche Bank, including strategists, sales staff and other analysts, may take views that are inconsistent with those

taken in this research report. Deutsche Bank issues a variety of research products, including fundamental analysis,

equity-linked analysis, quantitative analysis and trade ideas. Recommendations contained in one type of communication

may differ from recommendations contained in others, whether as a result of differing time horizons, methodologies or

otherwise. Deutsche Bank and/or its affiliates may also be holding debt or equity securities of the issuers it writes on.

Analysts are paid in part based on the profitability of Deutsche Bank AG and its affiliates, which includes investment

banking, trading and principal trading revenues.

Opinions, estimates and projections constitute the current judgment of the author as of the date of this report. They do

not necessarily reflect the opinions of Deutsche Bank and are subject to change without notice. Deutsche Bank provides

liquidity for buyers and sellers of securities issued by the companies it covers. Deutsche Bank research analysts

sometimes have shorter-term trade ideas that are consistent or inconsistent with Deutsche Bank's existing longer term

ratings. Trade ideas for equities can be found at the SOLAR link at http://gm.db.com. A SOLAR idea represents a high

conviction belief by an analyst that a stock will outperform or underperform the market and/or sector delineated over a

time frame of no less than two weeks. In addition to SOLAR ideas, the analysts named in this report may from time to

time discuss with our clients, Deutsche Bank salespersons and Deutsche Bank traders, trading strategies or ideas that

reference catalysts or events that may have a near-term or medium-term impact on the market price of the securities

discussed in this report, which impact may be directionally counter to the analysts' current 12-month view of total return

or investment return as described herein. Deutsche Bank has no obligation to update, modify or amend this report or to

otherwise notify a recipient thereof if any opinion, forecast or estimate contained herein changes or subsequently

becomes inaccurate. Coverage and the frequency of changes in market conditions and in both general and company

specific economic prospects make it difficult to update research at defined intervals. Updates are at the sole discretion

of the coverage analyst concerned or of the Research Department Management and as such the majority of reports are

published at irregular intervals. This report is provided for informational purposes only and does not take into account

the particular investment objectives, financial situations, or needs of individual clients. It is not an offer or a solicitation

of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Target prices are

inherently imprecise and a product of the analyst’s judgment. The financial instruments discussed in this report may not

be suitable for all investors and investors must make their own informed investment decisions. Prices and availability of

financial instruments are subject to change without notice and investment transactions can lead to losses as a result of

price fluctuations and other factors. If a financial instrument is denominated in a currency other than an investor's

currency, a change in exchange rates may adversely affect the investment. Past performance is not necessarily

indicative of future results. Unless otherwise indicated, prices are current as of the end of the previous trading session,

and are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank,

subject companies, and in some cases, other parties.

The Deutsche Bank Research Department is independent of other business areas divisions of the Bank. Details regarding

our organizational arrangements and information barriers we have to prevent and avoid conflicts of interest with respect

to our research is available on our website under Disclaimer found on the Legal tab.

Macroeconomic fluctuations often account for most of the risks associated with exposures to instruments that promise

to pay fixed or variable interest rates. For an investor who is long fixed rate instruments (thus receiving these cash

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Page 12 Deutsche Bank AG/Hong Kong

flows), increases in interest rates naturally lift the discount factors applied to the expected cash flows and thus cause a

loss. The longer the maturity of a certain cash flow and the higher the move in the discount factor, the higher will be the

loss. Upside surprises in inflation, fiscal funding needs, and FX depreciation rates are among the most common adverse

macroeconomic shocks to receivers. But counterparty exposure, issuer creditworthiness, client segmentation, regulation

(including changes in assets holding limits for different types of investors), changes in tax policies, currency

convertibility (which may constrain currency conversion, repatriation of profits and/or the liquidation of positions), and

settlement issues related to local clearing houses are also important risk factors to be considered. The sensitivity of fixed

income instruments to macroeconomic shocks may be mitigated by indexing the contracted cash flows to inflation, to

FX depreciation, or to specified interest rates – these are common in emerging markets. It is important to note that the

index fixings may -- by construction -- lag or mis-measure the actual move in the underlying variables they are intended

to track. The choice of the proper fixing (or metric) is particularly important in swaps markets, where floating coupon

rates (i.e., coupons indexed to a typically short-dated interest rate reference index) are exchanged for fixed coupons. It is

also important to acknowledge that funding in a currency that differs from the currency in which coupons are

denominated carries FX risk. Naturally, options on swaps (swaptions) also bear the risks typical to options in addition to

the risks related to rates movements.

Derivative transactions involve numerous risks including, among others, market, counterparty default and illiquidity risk.

The appropriateness or otherwise of these products for use by investors is dependent on the investors' own

circumstances including their tax position, their regulatory environment and the nature of their other assets and

liabilities, and as such, investors should take expert legal and financial advice before entering into any transaction similar

to or inspired by the contents of this publication. The risk of loss in futures trading and options, foreign or domestic, can

be substantial. As a result of the high degree of leverage obtainable in futures and options trading, losses may be

incurred that are greater than the amount of funds initially deposited. Trading in options involves risk and is not suitable

for all investors. Prior to buying or selling an option investors must review the "Characteristics and Risks of Standardized

Options”, at http://www.optionsclearing.com/about/publications/character-risks.jsp. If you are unable to access the

website please contact your Deutsche Bank representative for a copy of this important document.

Participants in foreign exchange transactions may incur risks arising from several factors, including the following: ( i)

exchange rates can be volatile and are subject to large fluctuations; ( ii) the value of currencies may be affected by

numerous market factors, including world and national economic, political and regulatory events, events in equity and

debt markets and changes in interest rates; and (iii) currencies may be subject to devaluation or government imposed

exchange controls which could affect the value of the currency. Investors in securities such as ADRs, whose values are

affected by the currency of an underlying security, effectively assume currency risk.

Unless governing law provides otherwise, all transactions should be executed through the Deutsche Bank entity in the

investor's home jurisdiction. Aside from within this report, important conflict disclosures can also be found at

https://gm.db.com/equities under the "Disclosures Lookup" and "Legal" tabs. Investors are strongly encouraged to

review this information before investing.

United States: Approved and/or distributed by Deutsche Bank Securities Incorporated, a member of FINRA, NFA and

SIPC. Analysts located outside of the United States are employed by non-US affiliates that are not subject to FINRA

regulations.

Germany: Approved and/or distributed by Deutsche Bank AG, a joint stock corporation with limited liability incorporated

in the Federal Republic of Germany with its principal office in Frankfurt am Main. Deutsche Bank AG is authorized under

German Banking Law and is subject to supervision by the European Central Bank and by BaFin, Germany’s Federal

Financial Supervisory Authority.

United Kingdom: Approved and/or distributed by Deutsche Bank AG acting through its London Branch at Winchester

House, 1 Great Winchester Street, London EC2N 2DB. Deutsche Bank AG in the United Kingdom is authorised by the

Prudential Regulation Authority and is subject to limited regulation by the Prudential Regulation Authority and Financial

Conduct Authority. Details about the extent of our authorisation and regulation are available on request.

Hong Kong: Distributed by Deutsche Bank AG, Hong Kong Branch.

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Deutsche Bank AG/Hong Kong Page 13

India: Prepared by Deutsche Equities India Pvt Ltd, which is registered by the Securities and Exchange Board of India

(SEBI) as a stock broker. Research Analyst SEBI Registration Number is INH000001741. DEIPL may have received

administrative warnings from the SEBI for breaches of Indian regulations.

Japan: Approved and/or distributed by Deutsche Securities Inc.(DSI). Registration number - Registered as a financial

instruments dealer by the Head of the Kanto Local Finance Bureau (Kinsho) No. 117. Member of associations: JSDA,

Type II Financial Instruments Firms Association and The Financial Futures Association of Japan. Commissions and risks

involved in stock transactions - for stock transactions, we charge stock commissions and consumption tax by

multiplying the transaction amount by the commission rate agreed with each customer. Stock transactions can lead to

losses as a result of share price fluctuations and other factors. Transactions in foreign stocks can lead to additional

losses stemming from foreign exchange fluctuations. We may also charge commissions and fees for certain categories

of investment advice, products and services. Recommended investment strategies, products and services carry the risk

of losses to principal and other losses as a result of changes in market and/or economic trends, and/or fluctuations in

market value. Before deciding on the purchase of financial products and/or services, customers should carefully read the

relevant disclosures, prospectuses and other documentation. "Moody's", "Standard & Poor's", and "Fitch" mentioned in

this report are not registered credit rating agencies in Japan unless Japan or "Nippon" is specifically designated in the

name of the entity. Reports on Japanese listed companies not written by analysts of DSI are written by Deutsche Bank

Group's analysts with the coverage companies specified by DSI. Some of the foreign securities stated on this report are

not disclosed according to the Financial Instruments and Exchange Law of Japan. Target prices set by Deutsche Bank's

equity analysts are based on a 12-month forecast period.

Korea: Distributed by Deutsche Securities Korea Co.

South Africa: Deutsche Bank AG Johannesburg is incorporated in the Federal Republic of Germany (Branch Register

Number in South Africa: 1998/003298/10).

Singapore: by Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch (One Raffles

Quay #18-00 South Tower Singapore 048583, +65 6423 8001), which may be contacted in respect of any matters

arising from, or in connection with, this report. Where this report is issued or promulgated in Singapore to a person who

is not an accredited investor, expert investor or institutional investor (as defined in the applicable Singapore laws and

regulations), they accept legal responsibility to such person for its contents.

Taiwan: Information on securities/investments that trade in Taiwan is for your reference only. Readers should

independently evaluate investment risks and are solely responsible for their investment decisions. Deutsche Bank

research may not be distributed to the Taiwan public media or quoted or used by the Taiwan public media without

written consent. Information on securities/instruments that do not trade in Taiwan is for informational purposes only and

is not to be construed as a recommendation to trade in such securities/instruments. Deutsche Securities Asia Limited,

Taipei Branch may not execute transactions for clients in these securities/instruments.

Qatar: Deutsche Bank AG in the Qatar Financial Centre (registered no. 00032) is regulated by the Qatar Financial Centre

Regulatory Authority. Deutsche Bank AG - QFC Branch may only undertake the financial services activities that fall

within the scope of its existing QFCRA license. Principal place of business in the QFC: Qatar Financial Centre, Tower,

West Bay, Level 5, PO Box 14928, Doha, Qatar. This information has been distributed by Deutsche Bank AG. Related

financial products or services are only available to Business Customers, as defined by the Qatar Financial Centre

Regulatory Authority.

Russia: This information, interpretation and opinions submitted herein are not in the context of, and do not constitute,

any appraisal or evaluation activity requiring a license in the Russian Federation.

Kingdom of Saudi Arabia: Deutsche Securities Saudi Arabia LLC Company, (registered no. 07073-37) is regulated by the

Capital Market Authority. Deutsche Securities Saudi Arabia may only undertake the financial services activities that fall

within the scope of its existing CMA license. Principal place of business in Saudi Arabia: King Fahad Road, Al Olaya

District, P.O. Box 301809, Faisaliah Tower - 17th Floor, 11372 Riyadh, Saudi Arabia.

United Arab Emirates: Deutsche Bank AG in the Dubai International Financial Centre (registered no. 00045) is regulated

16 November 2016

Pharmaceuticals / Biotechnology

Hengrui Medicine

Page 14 Deutsche Bank AG/Hong Kong

by the Dubai Financial Services Authority. Deutsche Bank AG - DIFC Branch may only undertake the financial services

activities that fall within the scope of its existing DFSA license. Principal place of business in the DIFC: Dubai

International Financial Centre, The Gate Village, Building 5, PO Box 504902, Dubai, U.A.E. This information has been

distributed by Deutsche Bank AG. Related financial products or services are only available to Professional Clients, as

defined by the Dubai Financial Services Authority.

Australia: Retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product

referred to in this report and consider the PDS before making any decision about whether to acquire the product. Please

refer to Australian specific research disclosures and related information at

https://australia.db.com/australia/content/research-information.html

Australia and New Zealand: This research is intended only for "wholesale clients" within the meaning of the Australian

Corporations Act and New Zealand Financial Advisors Act respectively.

Additional information relative to securities, other financial products or issuers discussed in this report is available upon

request. This report may not be reproduced, distributed or published without Deutsche Bank's prior written consent.

Copyright © 2016 Deutsche Bank AG

David Folkerts-Landau Group Chief Economist and Global Head of Research

Raj Hindocha Global Chief Operating Officer

Research

Michael Spencer Head of APAC Research

Global Head of Economics

Steve Pollard Head of Americas Research

Global Head of Equity Research

Anthony Klarman Global Head of Debt Research

Paul Reynolds Head of EMEA

Equity Research

Dave Clark Head of APAC

Equity Research

Pam Finelli Global Head of

Equity Derivatives Research

Andreas Neubauer Head of Research - Germany

Stuart Kirk Head of Thematic Research

International locations

Deutsche Bank AG

Deutsche Bank Place

Level 16

Corner of Hunter & Phillip Streets

Sydney, NSW 2000

Australia

Tel: (61) 2 8258 1234

Deutsche Bank AG

Große Gallusstraße 10-14

60272 Frankfurt am Main

Germany

Tel: (49) 69 910 00

Deutsche Bank AG

Filiale Hongkong

International Commerce Centre,

1 Austin Road West,Kowloon,

Hong Kong

Tel: (852) 2203 8888

Deutsche Securities Inc.

2-11-1 Nagatacho

Sanno Park Tower

Chiyoda-ku, Tokyo 100-6171

Japan

Tel: (81) 3 5156 6770

Deutsche Bank AG London

1 Great Winchester Street

London EC2N 2EQ

United Kingdom

Tel: (44) 20 7545 8000

Deutsche Bank Securities Inc.

60 Wall Street

New York, NY 10005

United States of America

Tel: (1) 212 250 2500