ratio analysis syntax

TRANSCRIPT

1

CONTENT

Chapter 1:

Introduction

Conceptual Framework.

Chapter 2:

Review of Literature,

Rationale

Objectives

Chapter 3:

Research Methodology

o Universe

o Sample

o Hypothesis

Research Design (if any),

Tools for Data Collection and Analysis

Chapter 4:

Results

Discussion & Interpretation

Chapter 5:

Conclusions

Implications,

Limitations

Scope for future work

2

Chapter-1

Introduction

Conceptual Framework.

3

INTRODUCTION-

Sintex leads in meaningful innovations and solutions. With their multifarious capabilities in the

field of plastics, metals, concrete etc. They have created many path breaking products They have an

excellent design, engineering, marketing and manufacturing set up to offer many standard and

custom products and solutions for satisfying needs anywhere in the world

• Sintex Industries Limited (Earlier known as The Bharat Vijay Mills Ltd) has two divisions –

textiles and plastics.

• Global spanning 9 countries

• Established in India in 1931

• Plastics Division started in the year 1975

Products

Sintex have pioneered development of number of products in such as Water Tanks, Doors,

Windows, Frames, Partitions, False Ceiling, Wall Paneling, Prefabs etc. for Buildings and Interiors.

they also brought for the first time in India Pallets, Intermediate Bulk Containers, Insulated Boxes,

Milk Cans, Multibins, Waste Bins etc. that are delivering better utility and value to the customers.

Recently they have created number of innovative products for the Electrical, Telecom and

Infrastructure Sectors such as Tamper Proof Meter Boxes, Shock Proof Chequered Plates, FRP

Cable Trays, BTS Shelters, Prefab Schoolrooms, Prefab Anganwadis, Prefab Police Chowkies etc.

There are six different types of Products range

1. Building & Construction

2. Prefabs

3. Interiors

4. Industrial

5. Electrical Engineering

6. Consumer

Sintex has an effective network of 10 manufacturing plants, 12 branch offices, over 500 distributors

and around 10,000 retailers spread across India.

4

ACHIEVEMENT

Major landmarks Along the Journey

1975 Moulded Polyethylene Industrial Containers and Tanks of sizes up to

10,000 litre

1977 Material Handling Containers for Industries and Institutions

1978 Water Tank

1985 Plastic Sections for Conversion into Partitions, False Ceilings, Wall

Panellings, Cabins, Cabinets, Furniture etc.

1988 Plastic Doors, Windows and Frames

1989 Insulated Containers, Sandwich Panels, Agri Containers and Biogas

Holders

1990 SMC and SMC Moulded Products, Pultruded Products, Resin Transfer

Moulded (RTM) Products, Blow Moulded Products, Injection Moulded

Products etc.

1995 Water Filters cum Purifiers

2000 Solar Water Heaters

2001 Prefabs

2002 Turnkey Blow Moulding & Profile Extrusion Plants

2004 FRP Underground Storage Tanks

2005 ISO 9001 Certification

Monolithic Concrete Construction Technology

2006 UL Listed for FRP Underground Petroleum Tanks

2008 Sandwich Panels

2010 Package Sewage Treatment Plants (PSTP) & Manholes

2011 Prefab Homes, Gloria Siding Panels

5

Finance performance definition:-

A subjective measure of how well a firm can use assets from its primary mode of business and

generate revenues. This term is also used as a general measure of a firm's overall financial health

over a given period of time, and can be used to compare similar firms across the same industry or to

compare industries or sectors in aggregation.

By financial analysis we come to know about the financial position of the company. Following are

the few terms which we have to understand

RATIO ANALYSIS

Meaning of Ratio: - A ratio is simple arithmetical expression of the relationship of one number to

another. It may be defined as the indicated quotient of two mathematical expressions.

According to Accountant‟s Handbook by Wixon, Kell and Bedford, “a ratio is an expression o f the

quantitative relationship between two numbers”.

Ratio Analysis: - Ratio analysis is the process of determining and presenting the relationship of

items and group of items in the statements. According to Batty J. Management Accounting “Ratio

can assist management in its basic functions of forecasting, planning coordination, control and

communication”.

It is helpful to know about the liquidity, solvency, capital structure and profitability of an

organization. It is helpful tool to aid in applying judgement, otherwise complex situations.

Ratio analysis can represent following three methods.

Ratio may be expressed in the following three ways:

1. Pure Ratio or Simple Ratio: - It is expressed by the simple division of one number by

another. For example, if the current assets of a business are Rs. 200000 and its current

liabilities are Rs. 100000, the ratio of „Current assets to current liabilities‟ will be 2:1.

2. ‘Rate’ or ‘so Many Times: - In this type, it is calculated how many times a figure is, in

comparison to another figure. For example , if a firm‟s credit sales during the year are Rs.

200000 and its debtors at the end of the year are Rs. 40000 , its Debtors Turnover Ratio is

200000/40000 = 5 times. It shows that the credit sales are 5 times in comparison to debtors.

3. Percentage: - In this type, the relation between two figures is expressed in hundredth. For

example, if a firm‟s capital is Rs.1000000 and its profit is Rs.200000 the ratio of profit capital, in

term of percentage, is 200000/1000000*100 = 20%

ADVANTAGE OF RATIO ANALYSIS 1. Helpful in analysis of Financial Statements.

2. Helpful in comparative Study.

3. Helpful in locating the weak spots of the business.

4. Helpful in Forecasting.

5. Estimate about the trend of the business.

6. Fixation of ideal Standards.

6

7. Effective Control.

8. Study of Financial Soundness.

LIMITATIONS OF RATIO ANALYSIS 1. Comparison not possible if different firms adopt different accounting policies.

2. Ratio analysis becomes less effective due to price level changes.

3. Ratio may be misleading in the absence of absolute data.

4. Limited use of a single data.

5. Lack of proper standards.

6. False accounting data gives false ratio.

7. Ratios alone are not adequate for proper conclusions.

8. Effect of personal ability and bias of the analyst.

CLASSIFICATION OF RATIO Ratio may be classified into the four categories as follows:

A. Liquidity Ratio

a. Current Ratio

b. Quick Ratio or Acid Test Ratio

B. Leverage or Capital Structure Ratio

a. Debt Equity Ratio

b. Debt to Total Fund Ratio

c. Proprietary Ratio

d. Fixed Assets to Proprietor‟s Fund Ratio

e. Capital Gearing Ratio

f. Interest Coverage Ratio

C. Activity Ratio or Turnover Ratio

a. Stock Turnover Ratio

b. Debtors or Receivables Turnover Ratio

c. Average Collection Period

d. Creditors or Payables Turnover Ratio

e. Average Payment Period

f. Fixed Assets Turnover Ratio

g. Working Capital Turnover Ratio

D. Profitability Ratio or Income Ratio

(A) Profitability Ratio based on Sales: a. Gross Profit Ratio

b. Net Profit Ratio

c. Operating Ratio

d. Expenses Ratio

(B) Profitability Ratio Based on Investment:

I. Return on Capital Employed

II. Return on Shareholder’s Funds:

a. Return on Total Shareholder‟s Funds

b. Return on Equity Shareholder‟s Funds

7

c. Earning Per Share

d. Dividend per Share

e. Dividend Payout Ratio

f. Earning and Dividend Yield

g. Price Earning Ratio

8

Chapter-2

Review of Literature,

Rationale

Objectives

Variables

9

LITERATURE REVIEW

Pinc research Suman Memani +91-22-6618 6479

Abhishek Kumar +91-22-6618 6398

Structurally a strong growth story: We initiate coverage on Sintex with a BUY rating (upside of

38%). We like Sintex primarily for: (1) A diversified business model marked bylow volatility in

sales, profit and cash flows; (2) Market leadership in the prime Monolithic and Prefab segments

which are expected to show CAGR of 25% and 27% during FY11-FY13E respectively; (3)

Acquired overseas and domestic subsidiaries likely to show operational improvement with

300bps increase in margin in FY13e v FY10; (4) Emerging cash flow positive in FY12-FY13e

through better management. At our TP of Rs220, the stock looks attractive

and discounts 12x & 10.6x FY12e & FY13e EPS of Rs18.5 & Rs20.7 respectively.

On behalf of the Board,

Date : April 30, 2011

Dinesh B. Patel

Chairman

Place : Ahmedabad

Your Directors have pleasure in presenting the 80th Annual Report of the Company, together with

audited accounts for the year, which ended on March 31, 2011.

Your Company reported another strong performance this year as it extended its presence into value-

added business verticals and strengthened its market position in existing businesses – delivering

superior value to its stakeholders.

Gross turnover grew 29% from `2,103.56 crore in 2009-10 to `2,718.74 crore in 2010-11, due to a

significant increase in existing business volumes. While all business segments contributed to your

Company‟s growth, the key growth drivers were monolithic construction and civil infrastructure.

24th September 2010

Ms. Revati Kasture

+91-22-6754 3465

CARE Equity Research assigns 4/5 on fundamental grade to Sintex Industries Limited

CARE Equity Research assigns fundamental grade of 4/5 to Sintex Industries Limited (Sintex).

This indicates „Very Good Fundamentals‟. The grade draws strength from Sintex‟s leadership

position in plastic water tanks, prefabricated building systems and monolithic construction coupled

with experienced management. While strong order book of monolithic construction gives revenue

visibility for next 20-22 months, increased Government focus on social spending provide huge

10

growth opportunities for Sintex. Furthermore, CARE Equity Research believes that risks associated

with acquired subsidiaries are behind us and Sintex is likely to start realizing synergy benefits

going forward.

Sintex‟s textile business had witnessed dip in FY10. Though CARE Equity Research is skeptical,

the management is positive about the future of this business. Additionally Sintex‟s increased focus

on monolithic business may elongate the working capital cycle of the company and any gap in

securing funding may affect the company‟s prospects adversely.

11

RATIONALE

The purpose of the research is to increase the knowledge and experience about the financial

position of the company and to learn about the financial aspect and financial position of the

company.

This study is related to the financial performance of the sintex industries. The finding will be

helpful for the sintex industries to improve their financial performance in future. Ratio analysis is a

very important to know about the financial performance and position (strengths and weaknesses) of

companies. To understand about the overall performance and efficiency of the company. For

investor to invest money in sintex industries it is very important that to know about ability of this

company. Before knowing about the financial position of the company, we can‟t say anything

about that company.

Financial (ratio) analysis reflects the inside mirror image of company. After doing study of

financial analysis you can easily identify ability (strength and weaknesses) of the company.

Financial analysis is just like weather forecast. Today there is more chance for rain then before to

go out from your house you prepare for rain. Same way financial analysis gives that guide about

company, for trading or long term investment.

12

OBJECTIVE

Primary objective –

An analytical Study of financial performance of Sintex Industries Ltd. with reference to last

three years

Secondary objective -

To analyse profit and loss account.

To analyse the balance sheet of the company.

To analyse the cash flow and fund flow statement of the company.

13

VARIABLES

The variables which affect the financial performance of the company are as follows:

1. Economic growth:-

Slowdown in the growth of Indian economy or future volatility in global financial market,

could adversely affect the business, including the future financial performance,

2. Significant change in the Government‟s policies

Any significant change in the Government‟s policies or any political instability in India

could adversely affect the business and economic conditions in India and could also adversely

affect the business, future financial performance.

3. Sensitivity to the economy and extraneous factors:-

The Company‟s performance is highly correlated to the performance of the economy and

the financial markets. The health of the economy and the financial markets in turn depends on

the domestic economic growth.

4. Legal and Compliance Risk:

The market regulators in India. New laws / rules and changes in any law and application of

current laws / rules could affect our manner of operations and profitability.

14

Chapter-3

Research Methodology

Research Design (if any),

Tools for Data Collection and Analysis

15

RESEARCH METHODOLOGY

Tools for data collection Secondary data will be taken from last 3 years

annual report

Tools for data analysis Percentage, Pie chart, Bar graph.

Performance analysis

Credit analysis

Security analysis

Competitive analysis

16

Chapter -4

Results

Discussion & Interpretation

17

RATIO ANALYSIS

1. LIQUIDITY RATIOS:

1. Current Ratio

Formula 2008-2009 2009-2010 2010-2011

Current Assets

Current Liabilities

3.82 4.68 4.00

Significance: - This ratio is calculated for knowing short term solvency of the organization. This ratio indicates

the solvency of the business. Certain authorities have suggested that in order to ensure solvency of

a concern current assets should be twice the current liabilities and therefore this ratio is known as

2:1 ratio . Here the Current Ratio of Sintex industries Ltd indicates that it has got sufficient assets to

pay off short term liabilities as. The company has maintained its short term solvency

throughout the years and it is improving its short term solvency status which is appreciable.

3.82

4.68

4

0

1

2

3

4

5

2008-09 2009-10 2010-11

Financial years

Current Ratio

18

2. Acid Test

Formula 2008-2009 2009-2010 2010-2011

Liquid Assets Liquid Liabilities

3.02 2.85 3.36

Significance: -

It gives a better picture of the firms ability to meet its short term debts out of its short term

assets. An Acid Test Ratio of 1:1 is considered to be ideal and standard. Here the Acid Ratios throughout the years considered indicates that it has adequate assets which

can be converted in the form of cash almost immediately to pay off those liabilities which are to be

paid off immediately. It must be remembered that the company has improved its Acid Test Ratio

in year 2010-11 as compared to previous year which is appreciable as such higher the liquid ratio

better the situation

3.02

2.85

3.36

2.4

2.6

2.8

3

3.2

3.4

2008-09 2009-10 2010-11

Financial Year

Acid Test Ratio

19

2. TURNOVER RATIO:

1. Fixed Assets Turnover Ratio

Formula 2008-2009 2009-2010 2010-2011

Net sales Fixed assets

1.32 1.36 1.36

Significance:- This ratio indicates whether the fixed assets are being fully utilized. It is an important measure of the

efficient and profit earning capacity of the business. The financial year 2008-09 had low ratio out of these three years. In the financial year

2009-10 and 2010-2011 has same ratio. This shows better asset management policy of these years.

1.32

1.36 1.36

1.3

1.31

1.32

1.33

1.34

1.35

1.36

1.37

2008-09 2009-10 2010-11

Financial Years

Fixed Assets Turnover Ratio

20

2. Current Assets Turnover Ratio

Significance: -

This ratio indicates capability of the organization in efficient use of current assets. It indicates the

sales generated per rupee of investment in current assets. The financial year 2008-09 and 2009-10 the ratio decreased i.e. the sale in the coming year slightly

decreased. In the 2010-11 the ratio increase means sales increase compared to the last years.

0.84 0.82

1.07

0

0.2

0.4

0.6

0.8

1

1.2

2008-09 2009-10 2010-11

Financial Years

Current Assets Turnover Ratio

Formula 2008-2009 2009-2010 2010-2011

Net sales Current assets

0.84 0.82 1.07

21

3. Inventory Turnover Ratio

Formula 2008-2009 2009-2010 2010-2011

Net sales

Avg. inventory

14.37 15.00 20.96

Significance: This is a test of inventory to discover possible trouble in the form of overstocking or

overvaluation. A low inventory turnover may reflect dull business, over investment in inventory.

A high inventory turnover indicates relatively lower amount of working capital locked in

inventories. In the financial year 2008-09 the inventory is very low and the 2009-10 and 2010-11 the

inventory turnover ratio is increasing. In year 2010-11 excellent inventory turnover ratio has

been seen.

14.37 15

20.96

0

5

10

15

20

25

2008-09 2009-10 2010-11

Financial Years

Inventory Turnover Ratio

22

4. Debtor Turnover Ratio

Formula 2008-2009 2009-2010 2010-2011

Net Credit Sales

Closing Sundry Debtors

4.81 3.88 3.43

Significance: -

This ratio indicates the speed at which the sundry debtors are converted in the form of cash.

In the 2008-09 the debtor turnover ratio is very high it means in that is good for the business but in

the financial year 2010-11 the debtor turnover ratio is less that is not good indicator for the company.

4.81

3.88 3.43

0

1

2

3

4

5

6

2008-09 2009-10 2010-11

Financial Years

Debtor Turnover Ratio

23

3. SOLVENCY RATIO

1. Debt-Equity Ratio

Formula 2008-2009 2009-2010 2010-2011

External liabilities

Shareholders fund

0.54 0.41 0.28

Significance: -

A high debt-equity ratio may indicate that financial status of the creditors is more than

that of the owners. A very low debt equity rate may mean that the borrowing capacity of the

organization is being underutilized. It is a measure of financial strength of a concern. Lower the

ratio greater the security available to the creditors. Generally 1:2 ratio is acceptable, but the ratio

of at least 1:1 is desirable as banks even do accept this.

In the financial year 2008-09 the debt-equity ratio is more than the other years it means it

is not good sign for the company. In the 2010-11 the debt-equity ratio is very less means in that

year the borrowing capacity of the organization is being underutilized.

0.54

0.41

0.28

0

0.1

0.2

0.3

0.4

0.5

0.6

2008-09 2009-10 2010-11

Financial Years

Debt-Equity Ratio

24

2. Capital Employed Ratio

Formula 2008-2009 2009-2010 2010-2011

Fixed assets *100

Capital employed

38.37 35.00 39.28

Significance: -

Normally a proprietor should provide all the funds required to purchase fixed assets. If the

capital employed ratio exceeds 100%, it indicates that the company has used short-term funds for

acquiring fixed assets, which policy is not desirable. when the percentage is less that 100, a part of

the net working capital is supplied by the shareholders, provided that there are no other non-current

assets. The ratio should generally be 65%.

In the financial year 2010-11 the ratio is 38.28 that is very less improvement from the last

year because the fixed assets of company is having minor improvement in the 2010-11 so that

ratio is approximately same for the past years.

38.37

35

39.28

32

33

34

35

36

37

38

39

40

2008-09 2009-10 2010-11

Financial Years

Capital Employed Ratio

25

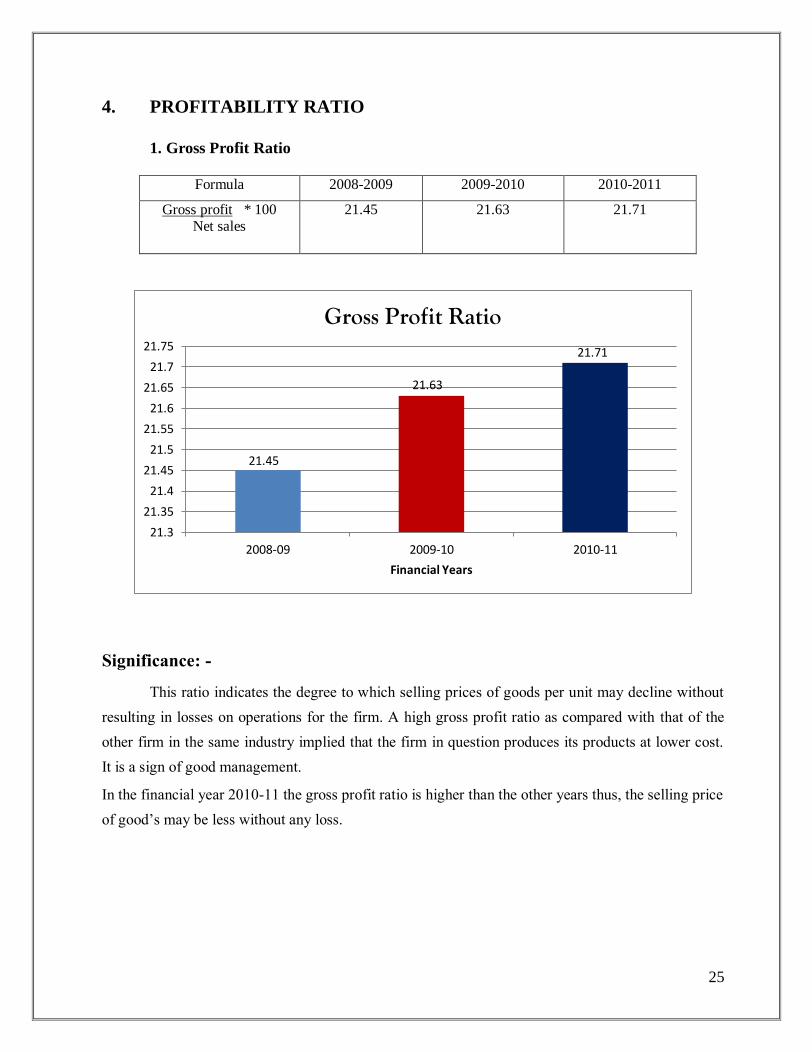

4. PROFITABILITY RATIO

1. Gross Profit Ratio

Formula 2008-2009 2009-2010 2010-2011

Gross profit * 100 Net sales

21.45 21.63 21.71

Significance: -

This ratio indicates the degree to which selling prices of goods per unit may decline without

resulting in losses on operations for the firm. A high gross profit ratio as compared with that of the

other firm in the same industry implied that the firm in question produces its products at lower cost.

It is a sign of good management. In the financial year 2010-11 the gross profit ratio is higher than the other years thus, the selling price

of good’s may be less without any loss.

21.45

21.63

21.71

21.3

21.35

21.4

21.45

21.5

21.55

21.6

21.65

21.7

21.75

2008-09 2009-10 2010-11

Financial Years

Gross Profit Ratio

26

2. Net Profit Ratio

Formula 2008-2009 2009-2010 2010-2011

Net profit(after tax)*100 Net sales

17.26 13.61 17.58

Significance: -

This ratio is widely used as a measure of over-all profitability and is very useful to the

proprietors. it gives an idea of the efficiency as well as profitability of the business to a limited

extent. The company has improved its net profits in the financial year 2010-11 the net profit ratio is

17.58.It means in that year the profit is more than the other years. The sale of the company has

been improved.

17.26

13.61

17.58

0

2

4

6

8

10

12

14

16

18

20

2008-09 2009-10 2010-11

Financial Years

Net Profit Ratio

27

3. Return On Assets

Formula 2008-2009 2009-2010 2010-2011

Net Profit * 100

Total Assets

6.69 6.13 7.42

Significance:-

The ratio is a measure of the return on the total resources of the business enterprise. It

shows how efficiently management has used the funds provided be the creditors and the owners. It can be referred that the financial year 2009-10 had not so good ratio because of high operating

expenses. However the company has improved in year 2010-11. The financial year 2010-11 had

7.42% as returns on its various resources which is appreciable.

6.69 6.13

7.42

0

1

2

3

4

5

6

7

8

2008-09 2009-10 2010-11

Financial Years

Return On Assets

28

5. Return On Shareholders’ Fund

Formula 2008-2009 2009-2010 2010-2011

PAT * 100

Total shareholders fund

19.06 14.05 21.17

Significance:-

This ratio is a measure of the profitableness of an enterprise. The realization of a

satisfactory net income is the major objective is being achieved. The financial year 2009-10 had low returns on shareholders fund as compared to next financial

years. In the 2010-11 the return on share holder‟s fund is high for compare than the past years. It

is good sign for the Company.

19.06

14.05

21.17

0

5

10

15

20

25

2008-09 2009-10 2010-11

Financial Years

Return On Shareholders’ Fund

29

5. Earnings Per Share

Significance:-

The earning per share ratio help to determining the market price of equity share of the

company. In the financial year 2010-11 the EPS has decreased as compare to previous year

and it is 13.19% thus, that is not sign for the company.

19.68 20.2

13.19

0

5

10

15

20

25

2008-09 2009-10 2010-11

FInancial years

Earnings Per Share

Formula 2008-2009 2009-2010 2010-2011

NPATD No. of eq. Shareholders

19.68 20.20 13.19

30

6. Dividend Pay Out Ratio

Formula 2008-2009 2009-2010 2010-2011

Dividend per share* 100

EPS

5.58 5.94 4.67

Significance:-

It indicates the policy of management to pay cash dividend. A high dividend pay out

ratio is better position of the company in the 2010-11 the ratio is 4.67 but in the 2010-11 the

dividend payout ratio is 5.94% it means the company has good position in paying dividend.

5.58 5.94

4.67

0

1

2

3

4

5

6

7

2008-09 2009-10 2010-11

Financial Years

Dividend Pay Out Ratio

31

FINAL DISCUSSION

The conclusion about Sintex industries ltd, it is growing and increasing year by year.

By the comparison of the Ratio analysis this conclusion can be drawn.

Net Profit & Gross profit ratio of company is favourable and has increased.

Return on equity capital of company is favourable and has increased.

EPS of the company is unfavourable

Liquidity ratio is favourable more than the standard.

Stock turnover ratio is increasing.

Debtor‟s turnover ratio is negative.

Fixed And Current assets turnover ratio of company has increasing.

Current ratio of company is increasing year by year.

On the basis of these findings I would say that SINTEX INDUSTRIES LTD has

improved financial position and continually increasing its financial position year by year.

32

Chapter-5

Conclusions

Implications

Limitations

Scope for future work

33

Conclusion

The term ratio refers to the numerical or quantities relationship between two items or

variables. Ratio analysis is a widely used tool of financial analysis. It is defined as the

systematic use of ratio, to interpret the financial statements, so that the strengths & weakness

of the firm as well as its history, performance and current financial position can be

determined. Ratio analysis is the most simplified method of appraisal of business

performance.

By going through the different variables We arrived at this conclusion that the |SINTEX

INDUSTRIES LTD. is growing every years. The company do the business of plastic and it is

one of the leading company in India.The product are of international standards.

On The ratios basis of the ratios analysing I can conclude the financial position of the

company and conclude the ratios.

Liquidity Ratio

In liquidity ratio the current ratio in the financial year 2010-

11 is 4.00 it is improved by 14.5% for compare to the past year. And acid test ratio in

financial year 2010-11 is 3.36 it is improved by17.89% for compare to the past year. Thus I

conclude on the basis of liquidity ratios that it is sign of improvement.

Turnover Ratio In the turnover ratio the fixed assets turnover ratio in the

financial year 2010-11 is 1.36 it has not improved as compare to the last year and the

current assets turnover ratio in the financial year 2010-11 is 1.07 and other inventory turnover

ratios are also improved in 2010-11 for compared to the last year but and debtor turnover has

decreased as compare to previous year.

Solvency Ratio In the solvency ratio the debt equity ratio in the financial

year 2010-11 is 0.28 and the capital employed ratio is 39.28, on the basis of these ratio I can

say that company financial position is positive.

34

Profitability Ratio In the profitability ratios the gross profit ratio in the 2010-

11 is 21.71 and the net profit ratio is 17.58 it means the profit of the company is increasing

every year.

35

Suggestions

After the detailed study of financial analysis of Sintex industries ltd. there are some

suggestions to offer for improving their performance, profitability, liquidity & sales. The

main suggestions are given below: -

1) GROSS PROFIT RATIO: The company is doing well and has potential to earn

more profit by exploring those market segments which are yet to explore to increase

their sales. Gross profit will increase with the help of reducing their cost of production

and direct expenses.

2) NET PROFIT RATIO: The company can improve its net profit ratio by reducing

operating expenses.

3) RETURN ON INVESTMENT: Return on investment is improving every year and

they should try improving operational efficiency and borrowing policy of enterprise.

4) FIXED ASSETS TURNOVER RATIO: They should use fixed assets efficiently so

that the fixed assets turnover ratio improves.

5) INVENTORY TURNOVER RATIO: For better performance of business and to

make inventory turnover ratio higher they should increase the sale.

36

Limitations

The annual report may be not exact so the result interpreted may vary from actual

situation

This research is stick to only quantitative analysis of the company.

37

Scope For Future Work

After analyzing the annual reports, profit and loss and balance sheet of Sintex industries ltd. I

found that company is growing and it has good potential to do best in coming years.

With the help of analysis the ratio of Sintex industries ltd the researchers can forecast the

position of that company in future and if we think from investors point of view on the basis of

these ratio they can invest in Sintex industries ltd.

So we can say that there are scope and opportunity for Sintex industries ltd. in the

future.

38

Reference

39

REFERENCE

Webliography

http://www.sintex-plastics.com

http://www.sintex-india.com

http://www.moneycontrol.com/india/stockpricequote/diversified/sintexindustries/SI27

Bibliography

Sharma & Gupta „Fianacial Management‟ Kalyani Publication 2010

Pandey I M „Fianacial Management‟ Tata Mchill Pubilcation 2010

Research paper & report

Pinc research (2011) Suman memani, abhishek kumar pp 1

Annual report sintex industries ltd (2010-2011)

Care equigrade (2010) Ms. Revati Kasture

40

Annexure

41

Data analysis

Data 2008-09(in crore) 2009-10(in crore) 2010-11(in crore)

Current asset 2221.15 2450.06 2437.14

Current liability 581.10 522.70 609.16

Liquid asset 2154.45 2377.57 1536.17

Net sales 1883.41 2010.55 2615.97

Fixed asset 1418.67 1473.34 1909.61

Avg. Inventory 140.95+121.03

2

126.98+140.95

2

126.98 + 121.62

2

Net credit sales 1,982.04 2,103.56 2,718.74

Closing debtors 495.80 677.06 838.12

Ext. Liabilities 934.76 801.45 609.16

Share holders fund 1,704.92 1,946.88 2172.42

Gross profit 404.06 425.51 567.94

Net profit after tax 325.12 273.70 460.01

Net profit 341.66 341.48 478.69

Total assets 5104.38 5566.94 6445.46

PAT 325.12 273.70 460.01

Total share holders

fund

1,704.92 1,946.88 2172.42

NPATD same

No of eq. Share

holders

37,374 37,210 56586

Dividend per share Rs. 1.1 Per Share ` 1.20 ` 0.65 Per Share

EPS 19.68 20.20 13.19