rationale of property tax collection and methodology to ... of property tax...6.bommanahalli 7.raja...

TRANSCRIPT

Rationale of Property Tax

Collection and methodology to increase revenue

UA Vasanth Rao General Manager (Finance)

Bangalore Metro Rail Corporation, Bangalore

The Rational for the tax: • For the urban bodies to function as independent entities and to take independent decisions they need a discretionary source of revenue.

• Local Governments across the world derive power to tax property from the constitution.

• In India the Municipalities draw their powers to levy Property tax from Entry 49 List 11 of the Constitution. This entry contemplates a levy of tax on lands and

buildings or both as units.

• Local government being the lowest hierarchy under the Constitution, is yet closest to the citizens

• When local people pay local taxes to the local government they become concerned how the amounts are spent. , thereby fostering accountability for local officials.

• Property tax gives an opportunity for the taxpayers’ participation with the local government.

2

Property Tax-An old tax and a good tax for local body

• Local government must have a tax base that is easily administered, easily identified and on which the tax rate is set by the local government.

• Property tax stands out as the ideal base for taxing as properties are within their respective jurisdictions.

• It is a different matter that this ‘good old tax’ is not, at administered effectively

• Ironically, this ineffective administration has paved way for reform to make local bodies financially independent of the State government.

• State governments has commitments for other priority sectors like agriculture, social, education, industry and health etc. and cannot can continue to generously fund local governments especially ULBs.

• This inevitably requires reform and restructuring of property tax systems in

line with the 74th Constitutional amendments which has empowered the local bodies to function as independent entities.

3

First Step • The first step is to develop a long-term strategy for property taxation. Basically four

issues need to be addressed: • The long run revenue elasticity of the new system • The transparency of the system • The administrative costs and convenience of the system • Horizontal equity.

1. Elasticity:

Municipal budgets will grow over time, and revenue from property tax should also grows proportionately.

• Property tax revenues can grow because of: • (a) adding new properties (Coverage ratio), • (b) increasing the values of those on the existing roll(Valuation ratio) • (c) increasing the collection rate, or (Collection ratio) • (d) raising the tax rate (Tax ratio)

• An inherent difficulty with the property tax is that none of these four sources of

revenue increase are automatic. These requires political will and government to take some administrative or legal action.

4

First step (cont)

2. Transparency:

• The general perception is that the tax assessment process of taxation is cumbersome and complicated.

• If the taxpayers understand how they are taxed, they are more likely to comply with the system.

• The self-assessment scheme does provide some transparency as the tax payer himself can calculate the tax based on the criteria provided to him.

• But some aspects like value indexes and how they are derived are not easy to understand.

• Ultimately, the taxpayers must be convinced that the index values reflect the rental value of the property.

5

First Step (cont) 3. Administrative Costs:

•The costs of collection should result in proportionate gains.

•Mass appraisal can significantly lower the costs of administering the property tax system.

•A shift to a self-reporting system, reduces the number of inspectors and collectors.

•But it is also necessary to invest in areas like survey, coverage, developing a good data system and training to improve the over all efficiency of the system.

4. Horizontal Equity: • To maintain fairness, the property tax should be horizontally equal i.e., it should treat similar properties in the same way.

6

Choice of Tax Design-method of assessment

• With these benchmarks a suitable tax design will have to be chosen from the following options:

1. A tax based on the annual or rental value of the property. 2. A tax based on the capital value of the property 3. A tax based on the site value. 4. A combination of the above two or three methods.

• ARV System: • The oldest and the easiest for taxpayers to understand yet difficult to administer.

• For the ARV system to remain tax productive, it is essential that the rental values for

computerizing of tax should represent the current market value.

• The problems of rent control - the solution seems to lie in either abolishing rent control or delink property tax from rent control regulations.

• Abolishing rent control would mean a major change in housing policy and has political

implications.

7

ARV cont..

• Amend the Rent Control Act as Karnataka and redefine the Standard Rent as the rent calculated on the basis of a certain percentage of the cost of construction and the market price of the land on the date of commencement of construction. Some enhancement linked to inflation for periodic revision.

• Judicial pronouncement has further complicated the ARV system: not the actual rent or rent receivable from hypothetical tenant which has to form the base for determining Annual Rental Value (ARV) but the standard or fair rent which has to form the basis for determining the Annual Rental Value.

myriad interpretations benefiting neither the taxpayer nor the local governments.

absence of a organized property and real estate market in rental and sale transactions valuation

administrative problems of laxity and collusion in tax administration.

8

Capital Value System

• The System that has an inbuilt mechanism for being tax productive. Prevalent is most developed countries.

• To succeed in Indian it is essential to create credible data base to derive the value of land

and building. • Depends on a well developed property market with multiple sources of information

instead of placing reliance solely on sale statistics with Sub-Registrars which generally reflect undervaluation.

• Secondly, the tax rate should be carefully prescribed after analyzing the revenue implication in comparison with the previous system.

• Thirdly, there may be problems from tenanted properties as the owner may find it legally difficult to pass the burden to the existing tenant.

• Finally, any shift to the capital value system needs to be proceeded by lot of preparations

by way of training the staff and educating the public. Again going by the Karnataka experience, lack of adequate preparation can cause confusion and lead to negative results.

9

Site Value System • Under this system tax is levied only on the capital value of the land, the structures are not

taxed. • Its chief merit is its potential in improving the efficiency of urban land use.

• Secondly, the administrative task is simplified, as valuation of structures is not involved.

• The main disadvantage of the system is that it narrows the tax base and requires a higher

tax rate to produce the same revenue.

• it imposes a tax burden for unimproved land to the same extent on site where improvements are made. two properties will be paying the same extent of tax, though one has build far in excess of the permitted limits, yet getting away by paying tax only to the extent of the land value.

• be regressive on poor people who are allotted site by allotment from government and

other housing societies but can build only when they have the money. • in smaller cities the cost of improvements is more than the value of land, • require frequent adjustment in the tax rate to keep the revenue buoyant.

10

Area Based System • Pragmatic approach to reform for the urban local bodies was to adopt the area-based

property tax system.

• The Area-based system which combines the features of the above three models has shown encouraging results in cities like Ahmedabad, Bangalore, Hyderabad and Patna.

• There is an attempt to make the process transparent and objective by basing the valuation on certain parameters like location, usage and building characteristics.

• But the system needs to be further simplified. The classification of structures and classification of zones.

• Interface with other agencies help: Many State Central Valuation Board have prepared and notified guidance value for

land and buildings to determine the minimum registration value in a given area. valuation of buildings, the public works department publishes

A training program could further refine their skill and prepare them to switch over to

the value-based taxation when it happens

11

Area Based System

• Will these reform survive?

• Revenue has increased • Outdated valuation rolls addressed • Taxpayer acceptance of reform measure • Helped in training ground towards capital valuation • Successful in short run

• The long-term buoyancy potential is yet to be tested.

• If there is no revision, the growth will stagnate.

• Subject to the resolution for revision by the city council

12

Why Area based system will succeed: Under the area based system, property is classified into 5-6 zones and prefixed a (rental) rate for properties falling the respective zones depending on the following factors: •(a) Location (city grouped into 4-6 value zones) scaling from posh areas to poorly developed •areas.

•(b) Type of construction: Roof type-(RCC) (Tiled/sheeted) hutment

•(c) Usage-Commercial or residential - tax rates differed

•(d) Occupancy - Own or tenanted-rebate for own use

•(e) Age of the building –for deprecation Equation with rental rates was easy to convince taxpayers to pay according to the location & the type of construction This method revalued properties with ARV as the base but the approach resembled an

assessment under capital value system. 13

SIMPLE FORMULA

Simple formula to calculate tax payable:

BA X R X10 months.=T-1 T1 - D = T2 T2 X 20 % = PT (BA-Built up Area) R- (Rate) T (Total) D- Depreciation)

The new system imparted considerable realism to valuation.

BBMP Zones

4 8 1

2 5

6 7 3

1.West

2.East

3.South

4.Yelahanka

5.Mahadevapura

6.Bommanahalli

7.Raja Rajeshwari Nagara

8.Dasarahalli

Objectives of GIS project for Property tax system

To identify all properties in the BBMP area.

To Assign Unique Property Identification Number (PID) to every property with their details in the BBMP Jurisdiction.

Properties that are in the Tax net are corrected to have an accurate information (on its Site Dimensions, Built up area, Land Use and classification whether Owner occupied or Tenanted) to maximise the tax base.

Prepare GIS framework for integrated and interconnected platform for all other services such as with Trade licenses, Grievances Redressal , Automated building Plan approval , Project Mgmt etc..

Process followed Use satellite digital map of BBMP area Generate vector map Plot the vector maps on to A0 paper along with list of

property & identifications Use the physical map to identify the properties Physically verify all the properties, and update/

Correct the base map Mark the individual property on to the map along

with legend sheet.

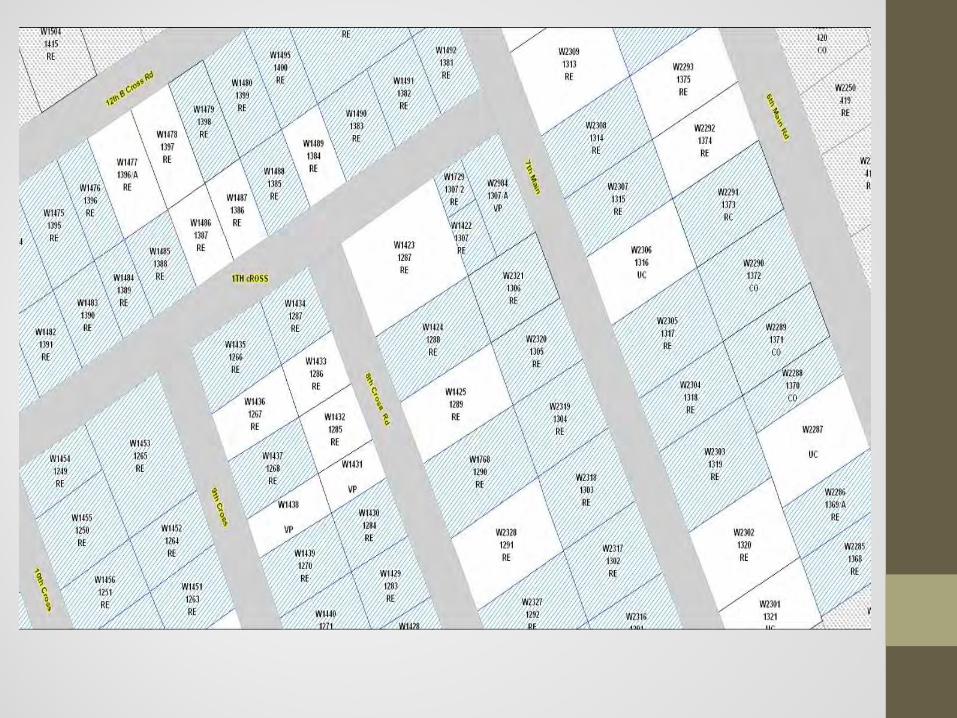

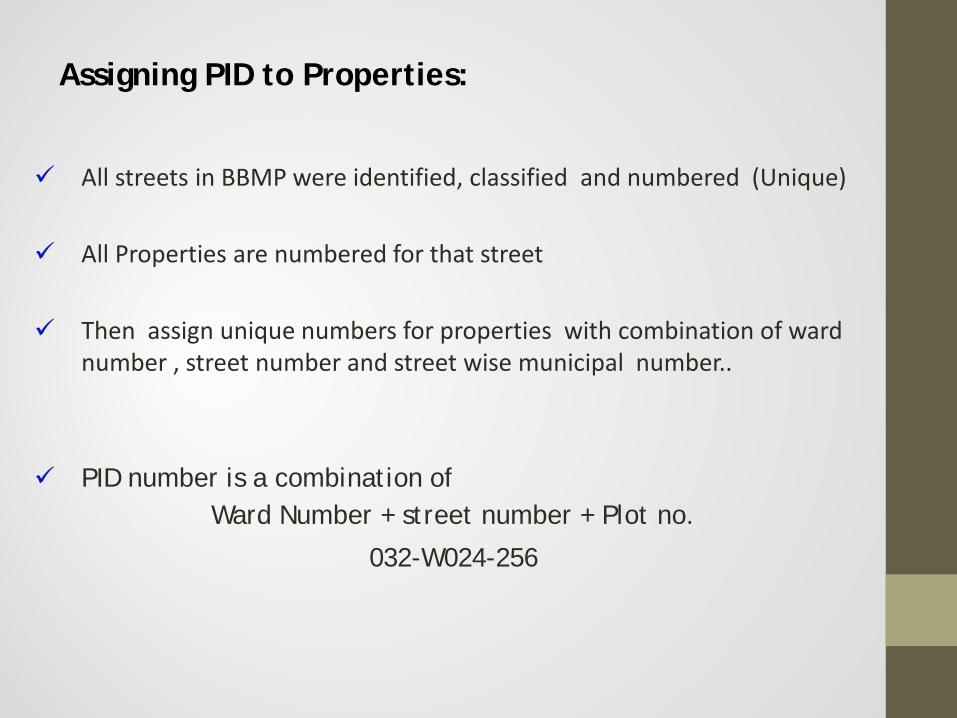

PROPERTY MAPPING AND INFORMATION SYSTEM VECTOR LAYER

All streets in BBMP were identified, classified and numbered (Unique)

All Properties are numbered for that street

Then assign unique numbers for properties with combination of ward

number , street number and street wise municipal number..

PID number is a combination of Ward Number + street number + Plot no.

032-W024-256

Assigning PID to Properties:

The impact

21

Impact of these process resulted in ………..

• In 2007-08, number of properties in tax net was 7.40 lakhs and collection was Rs. 448 Crs

• In 2011-12, with completion of GIS activity total number of properties • identified are now 16.2 lakhs and the property tax collection has increased to Rs. 1210 Crs

• For 2012-13, the property tax collected was Rs. 1300 crs Million

• For 2013-14 collection is Rs.900 crs up to October and is expected to reach Rs.1400-1450 • BBMP has the potential to collect Rs.3000 crores of revenue in the next 3-4 years • BBMP in now using the GIS for road work monitoring and also for the issue of trade license and plan sanctioning, which automatically updates the property information.

MEDIA & PUBLICITY- BRANDING OF BANGALORE REFORM MEASURE

23

CHANGE EFFECTIVE IMPLEMENTATION

CHANGE WONDERFUL INNINGS

CHANGE SURE WINNER

What is a Suitable Model for India?

Initial Phase: •Take steps to delink property tax from the rental value system. In the meantime introduce the Area-based system, retaining the principle of ARV but where the value is derived not on the basis of actual or hypothetical rent but on a combination of factors such as location, usage and quality of building. Transition Phase: •Develop a good database of market value of land from different sources –Registration Department, Real Estate Agents, Developers etc., and formulate index value. After the Area-based system has worked for some years and the necessary database is in place, prepare for shifting towards capital value system. •During this phase, officials should be well trained in valuation methods, information must be computerized and people educated about the changes in tax system.

Final Phase: •Introduce capital value system or site value system depending on the experience gained and the suitability of the system for the particular City/State.

27

IN CONCLUSION: No reform can come without people supporting it. Property tax had gained the attributes of ‘ benefit Tax’ Taxpayers more likely to pay tax if they are involved in the decision making process. A quid pro quo approach can help effectuate capital value assessment-after all it was this approach that helped introduce the area-based valuation. Bangalore has shown that periodic revision of valuation is possible and that it can be replicated.

28

THANK YOU