rayovac corporation 2003 annual report proud past … · rayovac corporation 2003 annual report p...

TRANSCRIPT

Proud PastPowerful Future

R a y o v a c C o r p o r a t i o n

2003 Annual Report

R a y o v a c C o r p o r a t i o n

2003 Annual Report

P R O U D

P A S T

P O W E R F U L

F U T U R E

Rayovac Corporation is a global consumer products

company with a diverse portfolio of world-class brands, including Rayovac,

Varta and Remington. With operations on six continents and more than

5,000 employees, Rayovac is one of the largest battery, lighting and personal

grooming products companies in the world.

The Company holds many leading market positions including: world leader in

hearing aid batteries; top selling rechargeable battery brand in North America

and Europe; and number one selling brand of men’s and women’s foil electric

razors in North America. Rayovac markets its products in more than 100

countries and counts nine of the world’s top 10 retailers as its customers.

Rayovac trades on the New York Stock Exchange under symbol ROV.

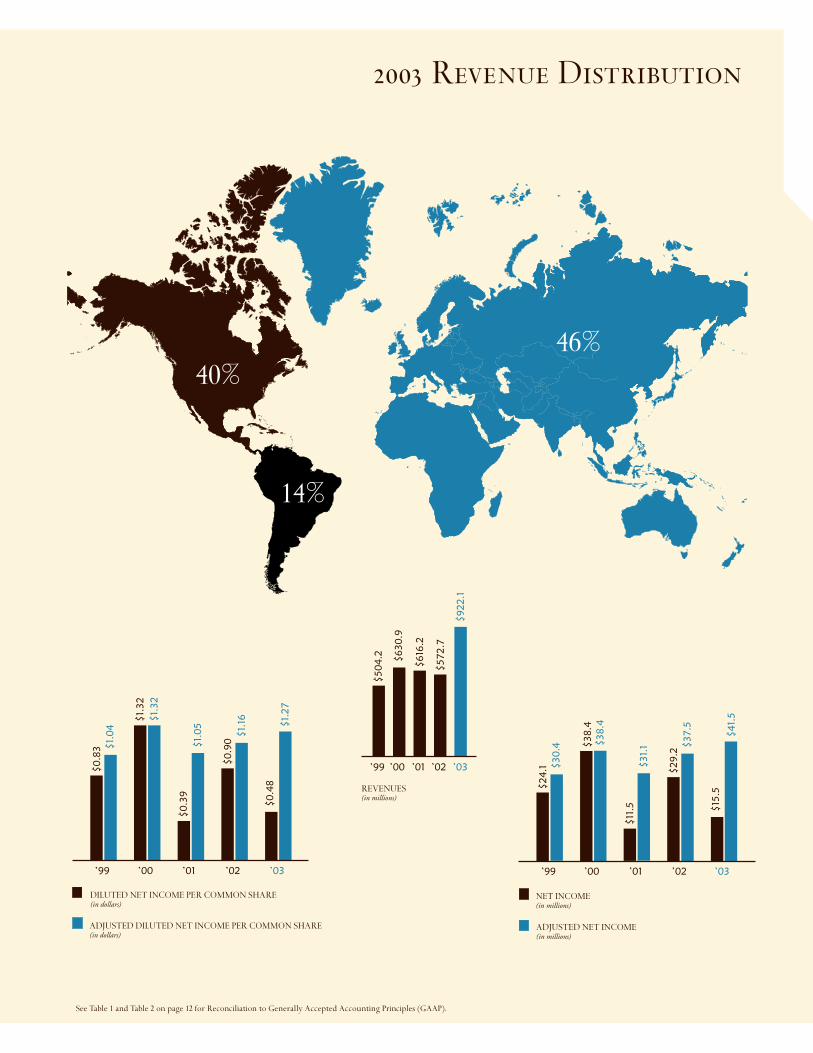

2003 Revenue Distribution

’02

$41.

5

$37.5

$31.

1$38.4

$30

.4

$15

.5

$29.2

$11

.5

$38.4

$24.1

’03’01’00

ADJUSTED NET INCOME(in millions)

’99

NET INCOME (in millions)

’02

$1.

27

$1.

16

$1.

05

$1.

32

$1.

04

$0

.48

$0

.90

$0

.39

$1.

32

$0

.83

’03’01’00

ADJUSTED DILUTED NET INCOME PER COMMON SHARE(in dollars)

DILUTED NET INCOME PER COMMON SHARE(in dollars)

’99

’02

$616

.2

$630

.9

$50

4.2

REVENUES (in millions)

’03’01’00’99

$922.1

$572.7

40%

14%

46%

See Table 1 and Table 2 on page 12 for Reconciliation to Generally Accepted Accounting Principles (GAAP).

Page 2/3

R a y o v a c C o r p o r a t i o n

2003 Annual Report

RAYOVAC’S GROWING

ARRAY OF WORLD-CLASS

CONSUMER PRODUCTS

ENSURES THAT RAYOVAC

WILL CONTINUE TO MEET

THE NEEDS OF TODAY’S

CONSUMERS.

Diverse Product Line

To Our Shareholders Over the last several years, Rayovac Corporation has aggressively

pursued its goal to become a technology-focused, market-driven, global battery company.

In fiscal 2003, our efforts paid off abundantly. We not only achieved our long-held objective,

but we set our sights on a bold new mission: to become a leading global consumer products

enterprise. During the past year, we engaged in a number of strategic measures geared to

help us realize our ambitious new vision. We:

• Completed the integration of the consumer battery business of Varta AG, which

we acquired in October 2002, by restructuring our global business and creating new

organizational efficiencies.

• Developed and launched a successful new U.S. alkaline battery retail strategy to

differentiate Rayovac from our competitors, while underscoring our traditional

value position with retailers and consumers.

• Reinforced our reputation for innovation by introducing a revolutionary new

round-cell rechargeable battery system that secures our position as the industry’s

technology leader.

• Acquired Remington Products Company, a leading designer and distributor of

battery-powered electric shavers and accessories, grooming products, and personal

care appliances. This acquisition diversified our product line and enhanced our

status with our customers as a global supplier. We financed the transaction through

an attractive and successful high-yield bond offering, an indication that investors

recognize the strength of our growing enterprise and our ability to generate cash.

These collective efforts provided us with a broader product portfolio, solidified our position

with global retail customers, enhanced our worldwide supply capabilities, fortified our

reputation for innovation and provided us with an expanded portfolio of powerful global

brands. They also positioned us to assume an exciting new place among some of the leading

consumer products companies in the world.

Transforming to a Global Consumer Products Company Rayovac’s largest retail

customers are expanding around the world and are seeking to partner with suppliers who

can serve their global needs. To respond to these demands, Rayovac has moved strategically

to make acquisitions, including Varta’s consumer battery business. Our October 2002

acquisition of Varta immediately positioned us as one of the largest consumer battery

and lighting companies in the world and the number two battery company in Europe.

Page 4/5

It also broadened our product portfolio and provided us with a European manufacturing

and distribution infrastructure, thereby increasing our ability to serve our global

retail customers.

Our next step was to capitalize on our newly expanded global presence by diversifying

our product line. Rayovac’s history is as a manufacturer and marketer of battery and

lighting products. By acquiring Remington Products Company at the close of fiscal 2003,

we significantly broadened our product mix. The addition of Remington electric shavers,

grooming and other personal care products was an important first move toward meeting

our product diversification goals.

Remington, a highly respected global brand, is an ideal complement to the Rayovac and

Varta brands. Remington also shares with Rayovac and Varta an outstanding record of

growth and a commitment to innovation, quality and value. Through this acquisition, we

have enhanced our ability to leverage our global distribution system and customer base.

We have decreased our reliance on a single product and industry. Moreover, we have

propelled Rayovac into new channels and new markets with new competitors, thereby

providing access to a range of growth opportunities.

Meeting the Challenges of Integration Rayovac has repeatedly demonstrated its

success in integrating acquisitions. In 1999, we expanded our global presence through

the integration of ROV Ltd., a Latin American battery company. In fiscal 2003, we

demonstrated our expertise once again with the highly successful integration of the

Varta consumer battery business, a move that has generated significant cost synergies

at lower costs than originally anticipated.

During the year, we also implemented a series of restructuring initiatives that maximized

operating efficiencies and merged the Rayovac and Varta businesses around the world

into three fully integrated regional business units: North America, Latin America and

Europe/Rest of World. By combining each company’s strengths, we streamlined our

business, reduced our combined operating costs by more than $40 million, and offered

our customers enhanced service. We also continued to invest in our implementation of

the SAP enterprise system in order to support the operation of our global business. This

involved upgrading to the current production release of the software and installing the

package in some remaining countries where it was not yet operating.

Our acquisition of Varta and the accompanying restructuring had a dramatic impact on

our year-over-year financial results. Fiscal 2003 sales increased to $922.1 million, compared

R a y o v a c C o r p o r a t i o n

2003 Annual Report

REMINGTON’S NEW

PRODUCT PIPELINE WILL

ALLOW RAYOVAC TO

SERVE THE NEEDS OF A

GROWING SHAVING

AND GROOMING MARKET

FOR YEARS TO COME.

New Product Pipeline

®MD

North America Latin America Europe/Rest of World

2004 Projection

Rayovac/Varta/Remington

2003 Remington2003 Rayovac/Varta

70%

30%

50%

40%

10%

46%

14%

40%

Revenue Distribution by Region

Page 6/7

R a y o v a c C o r p o r a t i o n

2003 Annual Report

A Global Industry Player

RAYOVAC’S ACQUISITION

OF VARTA’S CONSUMER

BATTERY BUSINESS HAS

TRANSFORMED THE

COMPANY INTO A

GLOBAL PLAYER IN THE

RAPIDLY EXPANDING

BATTERY INDUSTRY.

with $572.7 million in fiscal 2002. Diluted earnings per share was $0.48. However, adjusted

diluted earnings per share, excluding certain charges as detailed in Table 1 on page 12,

rose to $1.27.

We are currently applying the same proven management disciplines and principles that

we used in integrating Varta to our newest acquisition, Remington. We are driving sales

through our global distribution network and customer base, and we are creating new

efficiencies by integrating our supply chain, back-office operations, product development

and information systems functions. We expect these efforts to generate significant savings by

fiscal 2005, creating a more efficient and capable organization that will compete effectively

on a global scale.

Executing an Aggressive New Retail Strategy During the past year, we also focused

on addressing the challenges in our North American battery business. We responded

to increased promotional and pricing competition in the alkaline battery category by

launching an exciting new retail strategy aimed at reestablishing our value positioning

in the market.

This strategy, unique to the battery industry, offers “50% More” batteries in AA and AAA

sizes, at roughly the same retail price points as the smaller package sizes offered by major

competitors. Rayovac’s value proposition of “More Power for Your Money!” was well

received by North American retailers, who welcomed the new package configuration on

their shelves. To support the strategy, we launched a comprehensive marketing effort,

including a new targeted television campaign. Consumer reaction has been positive, and

we expect sales growth in our North American alkaline business in fiscal 2004.

Reaffirming Our Reputation for Innovation Rayovac has developed a reputation

as a technology leader by continually providing consumers with new or improved,

technologically advanced products to meet their portable power needs. In 1994, we

introduced rechargeable alkaline batteries to the U.S. market. In 2001, we launched the first

portable charger that charged high-capacity Nickel Metal Hydride (NiMH) batteries in one

hour or less. In the summer of 2003, we took speed charging to a higher level with the

introduction of the revolutionary new In-Cell Charge Control (I-C3) rechargeable NiMH

battery system of batteries and chargers. This breakthrough in NiMH technology offers

performance and convenience advantages over existing rechargeable and disposable battery

systems. An I-C3 battery will charge in an unprecedented 15 minutes or less and up to 1,000

times. The battery also lasts up to four times longer than alkaline batteries in digital cameras.

Page 8/9

Since its introduction, the new I-C3 rechargeable system has generated favorable press

coverage from several leading trade and consumer technology publications. The system

was chosen by the editors of Popular Science to receive their “Best of What’s New in 2003”

award, one of only 100 products that are chosen for this honor. American Photo named

the system “Editor’s Choice for Fastest Charger” and positive stories about the system

have appeared in PC World, U.S. News and World Report, Popular Photography, The New York Times

and others. More importantly, retailers and consumers have embraced the system for its

compelling convenience, power and value.

Building Our Business with World-Class Brands As a result of our acquisitions,

Rayovac has assembled a portfolio of powerful brands that are well recognized and highly

regarded by consumers around the world. Together Rayovac, Varta and Remington

represent more than 350 years of branding—giving us a considerable advantage in the

consumer products marketplace where brand recognition and trust is crucial to success.

We intend to continue to grow our business and leverage our global distribution and

customer base by adding more leading brands to our product mix. We will continue to

seek appropriate acquisition candidates like Varta and Remington—market-share

leaders with innovative products, excellent growth, attractive profit margins and proven

capabilities in product development and marketing. We are confident that we will be able

to continue to identify and acquire the best opportunities and integrate them in a way that

yields maximum value for our shareholders.

Implementing Our Proven Strategy for Future Growth We set and met a high

operating standard in 2003, and we expect to reap the benefits of our efforts in 2004 and

beyond. As always, we will concentrate on executing our proven business strategy to

globalize and diversify our organization; leverage and strengthen our brand portfolio;

expand our worldwide distribution capabilities; generate growth through innovative

product technology, product design and marketing; drive efficiencies and reduce costs;

and pursue strategic acquisitions. Execution of this strategy will allow us to grow both

revenue and earnings over the long term, creating increased shareholder value.

Proud Past, Powerful Future At Rayovac, we are firmly committed to building on our

past investments as a solid foundation for our Company’s future growth. What’s more, we

believe that we have the fundamental strengths that will enable us to do so in a highly

effective way. We are a market leader in several product areas, including batteries, lighting

products and electric shavers. Our distribution network is global, and our relationships

R a y o v a c C o r p o r a t i o n

2003 Annual Report

Power and Value

RAYOVAC’S BATTERY AND

LIGHTING PRODUCTS

DELIVER OUTSTANDING

PERFORMANCE FOR

CONSUMERS AT

ATTRACTIVE VALUE PRICES.

Page 10/11

Left–David A. Jones

Right–Kent J. Hussey

RAYOVAC’S POWERFUL

BRANDS PROVIDE NEW

OPPORTUNITIES TO DRIVE

INCREASED SALES AND

EARNINGS, AS WELL AS THE

ABILITY TO MARKET AND

DISTRIBUTE MORE PRODUCTS

TO MORE CUSTOMERS IN

MORE PLACES IN THE WORLD

THAN EVER BEFORE.

A Powerful Team

“Our greatest strength is our growing portfolio of world-class

brands that pave the way for our further expansion as a

technology-focused, market-driven, global consumer

products company.”

R a y o v a c C o r p o r a t i o n

2003 Annual Report

with global retailers are expanding. We have a proven history of successful acquisitions, as

well as the ability to generate cost savings and significant cash flow. Our management team

brings years of experience from leading companies around the world. And we have the best

and the brightest people—creative and dedicated employees who bring their individual

skills and talents to every function at Rayovac, from product innovation to customer

service to marketing to manufacturing.

Our greatest strength, however, is in our growing portfolio of world-class brands that pave

the way for our further expansion as a technology-focused, market-driven, global consumer

products company. Rayovac’s powerful brands, combined with our other strengths, provide

us with brighter growth prospects, new opportunities to drive increased sales and earnings,

and a substantial new ability to market and distribute more products to more customers

in more places in the world than ever before.

We’re proud of our long and successful history. We pledge to continue to build on that

solid foundation by making the sound business decisions that will propel our Company

forward. We believe we are poised for even greater success well beyond the global consumer

battery marketplace. By staying focused on the keys to our past success—technological

innovation, top-quality products and people, strategic acquisitions, product diversification

and customer service—we are confident that we will have a rewarding future. As

shareholders in Rayovac, we will settle for nothing less.

David A. JonesChairman and Chief Executive Officer

Kent J. HusseyPresident and Chief Operating Officer

1.

4.

7. 8.

5.

2. 3.

6.

9.

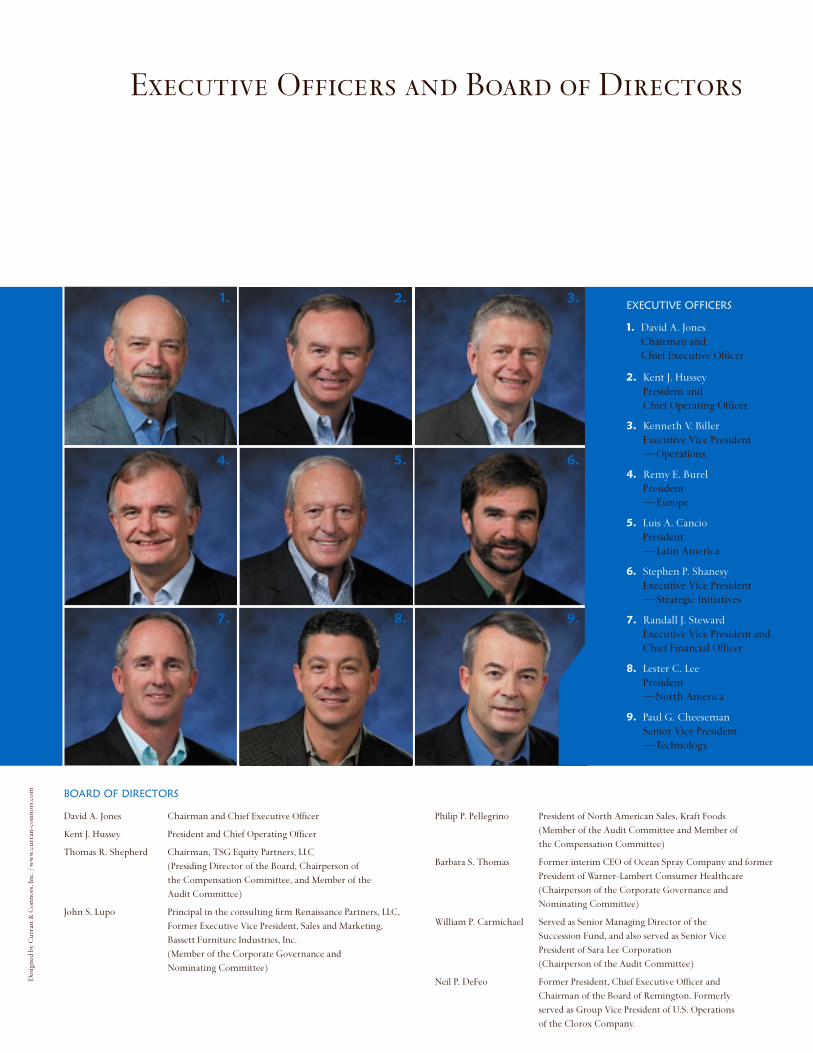

Executive Officers and Board of Directors

EXECUTIVE OFFICERS

1. David A. Jones Chairman and Chief Executive Officer

2. Kent J. Hussey President and Chief Operating Officer

3. Kenneth V. Biller Executive Vice President— Operations

4. Remy E. Burel President— Europe

5. Luis A. Cancio President— Latin America

6. Stephen P. Shanesy Executive Vice President— Strategic Initiatives

7. Randall J. Steward Executive Vice President and Chief Financial Officer

8. Lester C. Lee President —North America

9. Paul G. Cheeseman Senior Vice President—Technology

BOARD OF DIRECTORS

David A. Jones Chairman and Chief Executive Officer

Kent J. Hussey President and Chief Operating Officer

Thomas R. Shepherd Chairman, TSG Equity Partners, LLC (Presiding Director of the Board, Chairperson of the Compensation Committee, and Member of the Audit Committee)

John S. Lupo Principal in the consulting firm Renaissance Partners, LLC,Former Executive Vice President, Sales and Marketing, Bassett Furniture Industries, Inc. (Member of the Corporate Governance and Nominating Committee)

Philip P. Pellegrino President of North American Sales, Kraft Foods (Member of the Audit Committee and Member of the Compensation Committee)

Barbara S. Thomas Former interim CEO of Ocean Spray Company and formerPresident of Warner-Lambert Consumer Healthcare (Chairperson of the Corporate Governance and Nominating Committee)

William P. Carmichael Served as Senior Managing Director of the Succession Fund, and also served as Senior Vice President of Sara Lee Corporation (Chairperson of the Audit Committee)

Neil P. DeFeo Former President, Chief Executive Officer and Chairman of the Board of Remington. Formerly served as Group Vice President of U.S. Operations of the Clorox Company.

Des

igne

d by

Cur

ran

& C

onno

rs, I

nc. /

ww

w.c

urra

n-co

nnor

s.com

Page 12/13

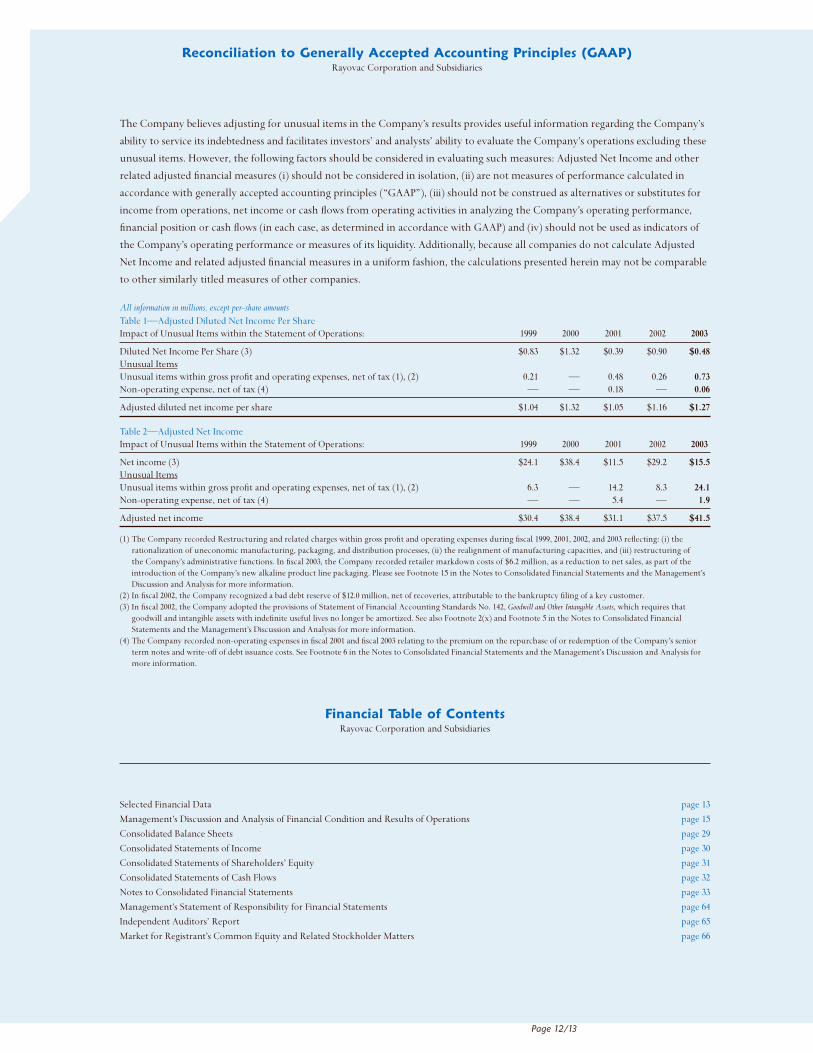

The Company believes adjusting for unusual items in the Company’s results provides useful information regarding the Company’s

ability to service its indebtedness and facilitates investors’ and analysts’ ability to evaluate the Company’s operations excluding these

unusual items. However, the following factors should be considered in evaluating such measures: Adjusted Net Income and other

related adjusted financial measures (i) should not be considered in isolation, (ii) are not measures of performance calculated in

accordance with generally accepted accounting principles (“GAAP”), (iii) should not be construed as alternatives or substitutes for

income from operations, net income or cash flows from operating activities in analyzing the Company’s operating performance,

financial position or cash flows (in each case, as determined in accordance with GAAP) and (iv) should not be used as indicators of

the Company’s operating performance or measures of its liquidity. Additionally, because all companies do not calculate Adjusted

Net Income and related adjusted financial measures in a uniform fashion, the calculations presented herein may not be comparable

to other similarly titled measures of other companies.

All information in millions, except per-share amountsTable 1—Adjusted Diluted Net Income Per ShareImpact of Unusual Items within the Statement of Operations: 1999 2000 2001 2002 2003

Diluted Net Income Per Share (3) $0.83 $1.32 $0.39 $0.90 $0.48Unusual ItemsUnusual items within gross profit and operating expenses, net of tax (1), (2) 0.21 — 0.48 0.26 0.73Non-operating expense, net of tax (4) — — 0.18 — 0.06

Adjusted diluted net income per share $1.04 $1.32 $1.05 $1.16 $1.27

Table 2—Adjusted Net IncomeImpact of Unusual Items within the Statement of Operations: 1999 2000 2001 2002 2003

Net income (3) $24.1 $38.4 $11.5 $29.2 $15.5Unusual ItemsUnusual items within gross profit and operating expenses, net of tax (1), (2) 6.3 — 14.2 8.3 24.1Non-operating expense, net of tax (4) — — 5.4 — 1.9

Adjusted net income $30.4 $38.4 $31.1 $37.5 $41.5

(1) The Company recorded Restructuring and related charges within gross profit and operating expenses during fiscal 1999, 2001, 2002, and 2003 reflecting: (i) the rationalization of uneconomic manufacturing, packaging, and distribution processes, (ii) the realignment of manufacturing capacities, and (iii) restructuring of the Company’s administrative functions. In fiscal 2003, the Company recorded retailer markdown costs of $6.2 million, as a reduction to net sales, as part of the introduction of the Company’s new alkaline product line packaging. Please see Footnote 15 in the Notes to Consolidated Financial Statements and the Management’sDiscussion and Analysis for more information.

(2) In fiscal 2002, the Company recognized a bad debt reserve of $12.0 million, net of recoveries, attributable to the bankruptcy filing of a key customer.(3) In fiscal 2002, the Company adopted the provisions of Statement of Financial Accounting Standards No. 142, Goodwill and Other Intangible Assets, which requires that

goodwill and intangible assets with indefinite useful lives no longer be amortized. See also Footnote 2(x) and Footnote 5 in the Notes to Consolidated FinancialStatements and the Management’s Discussion and Analysis for more information.

(4) The Company recorded non-operating expenses in fiscal 2001 and fiscal 2003 relating to the premium on the repurchase of or redemption of the Company’s seniorterm notes and write-off of debt issuance costs. See Footnote 6 in the Notes to Consolidated Financial Statements and the Management’s Discussion and Analysis formore information.

Financial Table of ContentsRayovac Corporation and Subsidiaries

Selected Financial Data page 13

Management’s Discussion and Analysis of Financial Condition and Results of Operations page 15

Consolidated Balance Sheets page 29

Consolidated Statements of Income page 30

Consolidated Statements of Shareholders’ Equity page 31

Consolidated Statements of Cash Flows page 32

Notes to Consolidated Financial Statements page 33

Management’s Statement of Responsibility for Financial Statements page 64

Independent Auditors’ Report page 65

Market for Registrant’s Common Equity and Related Stockholder Matters page 66

Reconciliation to Generally Accepted Accounting Principles (GAAP)Rayovac Corporation and Subsidiaries

The following selected historical financial data is derived from our audited consolidated financial statements. Only the most recent

three fiscal years’ audited statements are included elsewhere in this Annual Report. The following selected financial data should be

read in conjunction with our consolidated financial statements and notes thereto and the information contained in “Management’s

Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere herein.

Fiscal Year Ended September 30,

(In millions, except per share data) 1999 (4) 2000 2001 (5) 2002 (6) 2003 (7) (8)

Statement of Operations Data:

Net sales (1) $504.2 $630.9 $616.2 $572.7 $ 922.1

Gross profit (1) 198.2 259.4 232.9 237.4 351.5

Income from operations (2) 53.6 89.3 54.4 63.0 59.6

Income before income taxes (3) 37.6 58.0 17.5 45.7 23.0

Net income 24.1 38.4 11.5 29.2 15.5

Restructuring and related charges—cost of goods sold $ 1.3 $ — $ 22.1 $ 1.2 $ 21.1

Restructuring and related charges—operating expenses 8.1 — 0.2 — 11.5

Non-operating expense (3) — — 8.6 — 3.1

Interest expense $ 16.3 $ 30.6 $ 27.2 $ 16.0 $ 37.2

Per Share Data:

Net income per common share:

Basic $ 0.88 $ 1.39 $ 0.40 $ 0.92 $ 0.49

Diluted 0.83 1.32 0.39 0.90 0.48

Average shares outstanding:

Basic 27.5 27.5 28.7 31.8 31.8

Diluted 29.2 29.1 29.7 32.4 32.6

Cash Flow and Related Data:

Net cash provided by operating activities $ 13.3 $ 32.8 $ 18.0 $ 66.8 $ 76.2

Capital expenditures 24.1 19.0 19.7 15.6 26.1

Depreciation and amortization (excluding amortization of

debt issuance costs) (2) 13.5 20.0 21.1 19.0 31.6

Balance Sheet Data (at period end):

Cash and cash equivalents $ 11.1 $ 9.8 $ 11.4 $ 9.9 $ 107.8

Working capital (9) 104.4 104.7 158.5 140.5 269.8

Total assets (1) 513.1 549.6 566.5 533.2 1,576.5

Total long-term debt, net of current maturities 307.4 272.8 233.5 188.5 870.5

Total debt 330.3 317.6 258.0 201.9 943.4

Total shareholders’ equity 46.5 80.7 157.6 174.8 202.0

Selected Financial DataRayovac Corporation and Subsidiaries

(1) Certain reclassifications have been made to reflect the adoption of EITF 01-09 (which codified certain provisions of EITF 00-14, 00-22 and 00-25) for periods prior to adoption in fiscal 2002. EITF 01-09 addresses the recognition, measurement and income statement classification of various types of sales incentives, either as a reductionto revenue or as an expense. Concurrent with the adoption of EITF 00-25, we reclassified certain accrued trade incentives as a contra receivable versus our previous presentation as a component of accounts payable.

(2) Pursuant to FASB Statement No. 142, Goodwill and Other Intangible Assets, we ceased amortizing goodwill on October 1, 2001. Upon initial application of Statement No. 142,we reassessed the useful lives of its intangible assets and deemed only the trade name to have an indefinite useful life because it is expected to generate cash flowsindefinitely. Based on this, we ceased amortizing the trade name on October 1, 2001. Goodwill and tradename amortization expense for 1999, 2000 and 2001 included in depreciation and amortization in income from operations are as follows:

(In millions) 1999 2000 2001

Goodwill amortization $0.8 $1.2 $1.1Trade name amortization 0.4 2.3 2.3

$1.2 $3.5 $3.4

(3) The FASB issued Statement No. 145, which addresses, among other things, the income statement presentation of gains and losses related to debt extinguishments,requiring such expenses to no longer be treated as extraordinary items, unless the items meet the definition of extraordinary per APB Opinion No. 30. We adopted this statement on October 1, 2002. As a result, we recorded non-operating expenses within income before income taxes as follows during the fiscal years endedSeptember 30, 2001 and 2003:

In fiscal 2001, a non-operating expense of $8.6 million was recorded for the premium on the repurchase of $65.0 million of our senior subordinated notes and relatedwrite-off of unamortized debt issuance costs in connection with a primary offering of our common stock in June 2001.

In fiscal 2003, a non-operating expense of $3.1 million was recorded for the write-off of unamortized debt issuance costs associated with the replacement of our previouscredit facility in October 2002.

(4) Fiscal 1999 includes restructuring and related charges—cost of goods sold of $1.3 million, and restructuring and related charges—operating expenses of $8.1 million.

(5) Fiscal 2001 includes restructuring and related charges—cost of goods sold of $22.1 million, and restructuring and related charges—operating expenses of $0.2 million.Fiscal 2001 also includes a non-operating expense of $8.6 million discussed in (3) above. See Notes 15 and 2(x), respectively, in the Notes to Consolidated FinancialStatements included in this Annual Report for further discussion.

(6) Fiscal 2002 includes restructuring and related charges—cost of goods sold of $1.2 million. See Note 15 in the Notes to Consolidated Financial Statements included inthis Annual Report for further discussion.

(7) Fiscal 2003 includes a net sales reduction of $6.2 million related to North American retailer inventory repricing programs associated with the launch of our compre-hensive new alkaline pricing program announced in 2003. These programs were launched in response to Duracell’s price reduction in the U.S. market on certain AAand AAA batteries.

Fiscal 2003 includes restructuring and related charges—cost of goods sold of $21.1 million, and restructuring and related charges—operating expenses of $11.5 million.Fiscal 2003 also includes a non-operating expense of $3.1 million discussed in (3) above. See Notes 15 and 2(x), respectively, in the Notes to Consolidated FinancialStatements included in this Annual Report for further discussion.

(8) Fiscal 2003 selected financial data is impacted by two acquisitions completed during the fiscal year. The VARTA acquisition was completed on October 1, 2002 and theRemington acquisition was completed on September 30, 2003.

(9) Working capital is defined as current assets less current liabilities.

Selected Financial DataRayovac Corporation and Subsidiaries

Page 14/15

The following is management’s discussion of the financial results, liquidity, and other key items related to our performance. This

section should be read in conjunction with the “Selected Financial Data” and our Consolidated Financial Statements and related

notes in the “Financial Statements” section of this Annual Report. Certain prior year amounts have been reclassified to conform

to current year presentation. All references to 2001, 2002, and 2003 refer to fiscal year periods ended September 30, 2001, 2002, and

2003, respectively.

INTRODUCTIONOn October 1, 2002, we acquired substantially all of the consumer battery business of VARTA AG. The acquisition consisted of the

purchase of all of VARTA AG’s consumer battery subsidiaries and business outside of Germany, excluding Brazil, and a controlling

ownership and management interest in a new joint venture entity that will operate the VARTA AG consumer battery business in

Germany. The residual interest in the joint venture is held by VARTA AG. With the acquisition of VARTA, we became a truly global

battery manufacturer and marketer and acquired additional low-cost manufacturing capacity and battery technology.

In addition, on September 30, 2003, we acquired all of the equity interests of Remington Products Company, L.L.C. Remington is a

leading consumer products company focusing on the development and marketing of personal care products. Remington designs and

distributes electric shavers and accessories, grooming products, hair care appliances and other small electrical consumer products.

The acquisition of Remington allowed us to become a diversified consumer products company no longer solely focused on the

battery and lighting product markets. Remington was attractive due to its position as a strong branded company, its new product

pipeline and its use of distribution channels similar to those employed by Rayovac in the United States.

Following the acquisitions of VARTA and Remington, we are a global branded consumer products company with leading market

positions in our two major product categories: consumer batteries and electric personal care products. We are a leading worldwide

manufacturer and marketer of alkaline and zinc carbon batteries. We are also the leading worldwide manufacturer and marketer of

hearing aid batteries, a leading worldwide designer and marketer of rechargeable batteries and a leading marketer of battery-powered

lighting products. With the acquisition of Remington, we are also a leading designer and marketer of electric shavers and accessories,

electric grooming products and hair care appliances. Our products are sold on a global basis in over 100 countries through a variety

of channels, including mass merchandisers, home centers and hardware stores, consumer electronics stores, warehouse clubs, food,

drug and convenience stores, department stores, hearing aid professionals, industrial distributors and original equipment manufac-

turers (“OEMs”). We enjoy strong name recognition in our markets under the Rayovac, VARTA and Remington brands, each of

which has been in existence for more than 80 years.

Our financial performance is influenced by a number of factors including: general economic conditions and trends in consumer

markets; our overall product line mix, including sales prices and gross margins which vary by product line; and our general com-

petitive position, especially as impacted by our competitors’ promotional activities and pricing strategies. These influencing factors

played significant roles in our financial results during fiscal 2001, 2002 and 2003.

We manage our business based upon three geographic regions. The regions are as follows: North America, which includes the United

States and Canada; Latin America, which includes Mexico, Central America, South America and the Caribbean; and Europe/Rest of

World (“Europe/ROW”), which includes continental Europe, the United Kingdom, and all other countries in which we do business.

Our Consolidated Results of Operations for the twelve months ended September 30, 2003 do not include the impacts of the

Remington acquisition, as the transaction occurred on the close of business on September 30, 2003. Our Consolidated Balance

Sheet, as of September 30, 2003, and Consolidated Statement of Cash Flows for the year then ended do incorporate the impacts

of the Remington transaction.

Cost Reduction Initiatives We continually seek to improve our operational efficiencies, match our manufacturing capacity

and product costs to market demand and better utilize our manufacturing resources. Since the beginning of fiscal 2001, we have

undertaken various initiatives to reduce manufacturing, operating and other costs. We believe that we can continue to drive down

our cost of goods manufactured with continued focus on cost reduction initiatives.

Fiscal 2001. In fiscal 2001, we closed our Wonewoc, Wisconsin plant and now source lighting products previously made at this plant

from third party suppliers. With this closure, we now outsource all of our lighting products. In addition, we outsourced certain

manufacturing operations at our Fennimore, Wisconsin plant to accommodate the installation of a new high speed AA-size alkaline

battery line and discontinued inefficient packaging operations.

Management’s Discussion and Analysis of Financial Condition and Results of OperationsRayovac Corporation and Subsidiaries

Also in fiscal 2001, we closed our zinc carbon battery plants in Tegucigalpa, Honduras and rationalized our manufacturing and

distribution processes in our Mexico City, Mexico manufacturing facilities and in our European operations by discontinuing or

outsourcing uneconomic product lines or production processes, including the outsourcing of zinc carbon rod manufacturing, and

by changing uneconomical modes of distribution.

Finally, in fiscal 2001, we engaged in an organizational restructuring in North America and Latin America. As part of this initiative,

sales and marketing functions were eliminated and/or consolidated. These cost reduction initiatives reduced our global workforce

by approximately 570 employees.

Fiscal 2002. In fiscal 2002, we closed our Santo Domingo, Dominican Republic manufacturing facility and transferred production

of zinc carbon batteries to our Guatemala City, Guatemala manufacturing facility. We also outsourced a portion of our zinc carbon

battery production previously manufactured at our Mexico City, Mexico facility.

The impact of the fiscal 2001 and fiscal 2002 cost reduction initiatives on our operations is described below under the heading “Fiscal

Year Ended September 30, 2002 Compared to Fiscal Year Ended September 30, 2001—Restructuring and Related Charges.”

Fiscal 2003. In October 2002, in conjunction with the acquisition of the VARTA consumer battery business described above, we

announced a series of initiatives designed to position our consumer battery business for future growth opportunities and to opti-

mize the combined global resources of Rayovac and VARTA. These initiatives, which are expected to provide significant benefits to

the combined organization, include the renegotiation of certain sourcing arrangements, the elimination of duplicate costs in our

consumer battery business and the consolidation of sales and marketing functions.

In October 2002, we closed our Mexico City, Mexico manufacturing facility. With the closure of the Mexico City, Mexico plant,

the plants in Guatemala City, Guatemala, Breitenbach, France, and Manizales, Colombia became our remaining zinc carbon manu-

facturing plants. The consolidation of our zinc carbon capacity within Latin America is consistent with the global market trend

away from zinc carbon toward alkaline batteries, and is intended to allow us to more closely match our manufacturing capacity

to anticipated market demands.

We also announced the closure of operations at our Madison, Wisconsin packaging center and Middleton, Wisconsin distribution

center in October 2002. These facilities were closed during fiscal 2003 and their operations were combined into a new leased complex

in Dixon, Illinois. Transition to the new facility was completed in June 2003. We anticipate that the relocation to the new leased

packaging and distribution center will result in operational changes that are intended to reduce freight and inventory handling costs.

We expect that all geographies will benefit from decreased costs and expenses resulting from the VARTA initiatives. These initiatives

are anticipated to create long-term opportunities for procurement savings resulting from renegotiated raw material and finished

good sourcing arrangements and lower operating costs as duplicative administrative support and sales and marketing functions are

consolidated and overlapping functions are eliminated.

The benefits of the VARTA initiatives are expected to positively impact future gross profit and operating margins, but were partially

offset during fiscal 2003 and in the near-term by exit and integration costs, including employee termination benefits and asset impair-

ments associated with the elimination of duplicative functions, an increase in interest expense associated with the acquisition, and

increased exposure to foreign currency movements reflecting our expanded global presence. In addition, the acquisition of the

VARTA consumer battery business is expected to negatively impact our effective tax rate, as we estimate a larger percentage of our

income will be generated in higher tax jurisdictions.

Annual savings associated with the VARTA initiatives are projected to be in the range of $40–45 million when fully realized by

the end of fiscal 2005. Costs associated with certain cost reduction initiatives are discussed in Note 15, Restructuring and Related

Charges, to our Notes to Consolidated Financial Statements.

The impact of the fiscal 2003 cost reduction initiatives on our operations is described below under the heading “Fiscal Year Ended

September 30, 2003 Compared to Fiscal Year Ended September 30, 2002—Restructuring and Related Charges.”

Management’s Discussion and Analysis of Financial Condition and Results of OperationsRayovac Corporation and Subsidiaries

Page 16/17

In conjunction with the acquisition of the Remington business, we identified annual savings opportunities of approximately $23.5

million when fully realized, which we currently expect by 2006. These savings are primarily related to purchasing, supply chain

management, manufacturing and back office functions. We estimate we will incur total costs (cash and non-cash) of approximately

$35.0 million over the next two years to achieve these savings. Integration activities are currently underway and savings and cost

estimates will be further refined during fiscal 2004. We expect the North America and Europe/ROW geographies to benefit from

decreased costs and expenses resulting from these Remington initiatives to optimize the combined resources of Rayovac and

Remington.

Meeting Consumer Needs through Technology and Development We continue to focus our efforts on meeting con-

sumer needs for portable power, personal care, and lighting products through new product development and technology innovations.

Prior to the Remington acquisition, we announced improvements and new developments in our rechargeable, alkaline, hearing

aid, and lighting products product lines.

During fiscal 2001, we introduced a one-hour charger for nickel metal hydride (NiMH) batteries, and began selling higher perform-

ing NiMH batteries. In fiscal 2002, we announced the development of a revolutionary rechargeable NiMH battery system capable

of recharging batteries in as little as 15 minutes which was introduced in the retail market during fiscal 2003. These technological

advancements provide consumers with portable, rechargeable power as the use of digital cameras and other high drain devices

continues to grow.

In fiscal 2002, we launched our new, more powerful Rayovac Maximum Plus alkaline batteries, with bold new graphics. Also during

fiscal 2001 and fiscal 2002, we increased the performance of our hearing aid batteries, and launched innovative packaging allowing

consumers to more easily dispense the hearing aid batteries. In Europe during fiscal 2003, we launched our High Energy� alkaline

batteries and upgraded our graphic designs for our MaxiTech� and LongLife� batteries, all marketed under the VARTA brand name.

Finally, we rejuvenated our lighting products product line through a series of new product launches designed to reach unique

markets within the mass and retail channels.

During fiscal 2003, we introduced to the United States marketplace a comprehensive pricing strategy for our alkaline battery product

portfolio. We simplified the battery buying decision process for consumers by offering fifty percent more of our AA and AAA batter-

ies for the same price as the competition. We believe this “fifty percent more” strategy will help redefine the value position of our

Maximum Plus� alkaline products. This strategy will also match up with the consumer trend of buying larger pack size of batteries.

Research and development efforts at Remington allow us to maintain our unique manufacturing process in cutting systems for

shavers. Remington is continuously pursuing new innovations for its line of shavers including foil improvements and new cutting

and trimmer configurations. Remington also devotes resources to the development of new technologies for its other products.

During fiscal 2003 and prior to the acquisition, Remington introduced the Remington Titanium� line of men’s MicroScreen� and

MicroFlex� shavers, a line of personal grooming products that utilize titanium-coated blades and trimmers.

We believe that our products are well poised to meet the portable power, lighting and electric personal care needs of consumers.

We will continue to focus on identifying new technologies necessary to meet consumer and retailer needs within the marketplace.

Competitive Landscape The alkaline battery business is highly competitive on a global scale. Within North America, Europe

and Latin America, there are four primary branded providers of alkaline batteries and a few local manufacturers within each geo-

graphic region. The alkaline marketplace has seen changes in recent years related to product line segmentation, with attempts to

segment the category into high-performance, regular and value positions, combined with the introduction of private label batteries

at certain retailers. In addition, market participants continue to engage in high levels of promotional and pricing activities to gain

market share. In the United States in 2003, Duracell, one of our competitors, announced they were lowering the prices of their

alkaline batteries. This action, in conjunction with our and Energizer’s responses, is expected to have a short-term impact on the

overall United States battery category growth.

Within Latin America, poor economic conditions have dramatically impacted battery sales especially within the zinc carbon product

line. Zinc carbon batteries continue to be the largest share of the battery market in Latin America in unit terms. In North America

and Europe, the majority of consumers purchase alkaline batteries.

Management’s Discussion and Analysis of Financial Condition and Results of OperationsRayovac Corporation and Subsidiaries

Within North America and Europe, the rechargeable battery business has experienced dramatic changes over the past three years.

Primary rechargeable alkaline sales have declined over this period with a shift towards rechargeable batteries, such as NiMH, which

are higher performing in high drain devices. Our development of a one-hour charger and an innovative 15-minute rechargeable

battery technology help us maintain the number one market position within the rechargeable category in the United States, as

estimated by management.

Within the hearing aid battery category, we continue to hold the number one global market position based on management estimates.

We believe that our close relationship with hearing aid manufacturers and other customers, as well as our product performance

improvements and packaging innovations, position us for continued success in this category.

Seasonal Product Sales Our quarterly results are impacted by our seasonal sales. Sales during the first and fourth fiscal quarters

of the year are generally higher than other quarters due to the impact of the December holiday season. The seasonality of our sales

during the last three fiscal years is as follows:Percentage of Annual Sales

Fiscal Year Ended September 30,

Fiscal Quarter Ended 2001 2002 2003

December 27% 28% 28%

March 22% 21% 22%

June 24% 24% 23%

September 27% 27% 27%

Remington also experiences seasonal sales. During calendar 2002, Remington’s sales for the quarters ended March 31, June 30,

September 30, and December 31 were 15%, 19%, 22%, and 44%, respectively. We anticipate our sales for the fiscal quarter ending

in December will be a larger portion of our annual sales going forward.

Fiscal Year Ended September 30, 2003 Compared to Fiscal Year Ended September 30, 2002

Highlights of consolidated operating results

Year over year historical comparisons are influenced by our October 1, 2002 acquisition of substantially all of the consumer battery

business of VARTA AG, which is included in our current year but not prior year results. See Note 16, Acquisitions and Divestitures,

of Notes to the Consolidated Financial Statements for additional information regarding the VARTA acquisition. The acquisition

of Remington, had no effect on fiscal 2003 operating results, as the transaction was completed after the close of business on

September 30, 2003.

Net Sales. Our net sales increased $349.4 million to $922.1 million in fiscal 2003 from $572.7 million the previous year. The sales

increase is attributable to the VARTA acquisition partially offset by sales decreases in the North America segment.

Operating Income. Our income from operations decreased $3.4 million to $59.6 million in fiscal 2003 from $63.0 million the

previous year. The decrease was primarily attributable to $32.6 million in restructuring charges reflecting a series of restructuring

initiatives announced and implemented during fiscal 2003 and a $20.7 million decrease in North America segment profitability dis-

cussed below. These decreases were mostly offset by the profitability associated with the VARTA acquisition. For further discussion of

restructuring and related charges see Note 15, Restructuring and Related Charges, of Notes to the Consolidated Financial Statements.

Net Income. Our net income in fiscal 2003 decreased $13.7 million to $15.5 million from $29.2 million the previous year. The

decrease was due to restructuring and related charges of $20.2 million, after tax, an increase in interest expense of $13.1 million,

after tax, North America retailer markdown programs of $3.8 million, after tax, non-operating expense of $1.9 million, after tax,

reflecting the write-off of unamortized debt issuance costs associated with the replacement of our previous credit facility, and the

decline in North America profitability, partially offset by the profitability of the VARTA acquisition. Fiscal 2002 includes a $7.5 mil-

lion, after tax, net bad debt expense related to the bankruptcy filing of a North America segment customer.

Management’s Discussion and Analysis of Financial Condition and Results of OperationsRayovac Corporation and Subsidiaries

Page 18/19

Segment Results. We evaluate segment profitability based on income from operations before corporate expense and restructuring

and related charges. Corporate expense includes corporate purchasing expense, general and administrative expense, and certain

research and development expenses.

Europe/ROW 2002 2003

Net sales from external customers $ 52.5 $421.1

Segment profit 5.1 49.7

Segment profit as a % of net sales 9.7% 11.8%

Assets $ 31.4 $537.4

The Europe/ROW segment was the segment most dramatically impacted by the VARTA acquisition. Increases in sales, segment prof-

itability and assets all reflect the significance of VARTA within the region and the favorable impact of foreign currency movements.

Intense sales, marketing, operational and administrative integration activities were implemented and substantially completed within

the region making identification of factors causing year-over-year variation difficult.

Profitability as a percent of net sales increased to 11.8% in fiscal 2003 from 9.7% in the previous year primarily reflecting the impact of

the VARTA acquisition and improved gross profit margins.

Intangible assets of $240.6 million, primarily related to the VARTA acquisition, now make up a substantial portion of the asset base

within the segment. The segment’s asset base as of September 30, 2003, includes the international operations of Remington.

North America 2002 2003

Net sales from external customers $435.6 $376.0

Segment profit 85.5 64.8

Segment profit as a % of net sales 19.6% 17.2%

Assets $256.4 $625.5

Our sales to external customers decreased $59.6 million, or 13.7%, to $376.0 million in fiscal 2003 from $435.6 million the previous

year due primarily to weakness in alkaline, zinc carbon, and rechargeable product line sales. Alkaline sales decreases of $54.3 million

were caused by intense competitive promotional pricing activity in this battery category, a $9.7 million decline in post-bankruptcy

sales to a customer, approximately $6.2 million in retailer markdown programs associated with the Company’s new alkaline pricing

program, and our inability to replace $4.0 million in sales to a discontinued low-margin OEM customer in the prior year. Zinc carbon

sales decreased $9.6 million compared to last year due to reduced distribution and general marketplace trends away from the use of

this type of battery. Rechargeable battery sales also decreased $2.6 million compared to last year due to lower sales in advance of the

I-C3 rechargeable battery system launched in the fourth quarter of fiscal 2003. Hearing aid battery sales increased $3.7 million, or

9.0% due to overall category strength.

Our profitability decreased $20.7 million to $64.8 million from $85.5 million the previous year. The decrease in profitability was

primarily attributable to lower gross profit due to the current year sales decrease partially offset by a $12.0 million net bad debt

expense related to the bankruptcy filing of a key customer recorded in the prior year. Due to the reasons mentioned above, our

profitability margins decreased 240 basis points to 17.2% from 19.6% the previous year.

Our assets increased to $625.5 million from $256.4 million the previous year primarily reflecting the impacts of the Remington

acquisition and intangible assets of approximately $283.0 million attributable to the transaction. The purchase price allocation for

the Remington acquisition is not yet final.

Latin America 2002 2003

Net sales from external customers $ 84.7 $125.0

Segment profit 5.3 17.7

Segment profit as a % of net sales 6.3% 14.2%

Assets $191.0 $203.9

Our sales to external customers increased $40.3 million, or 47.6% to $125.0 million in fiscal 2003 from $84.7 million the previous

year. The increase in sales is due to the impact of the VARTA acquisition and sales increases within Central America of $7.6 million

primarily reflecting improvements in our wholesaler and distributor channels. These increases were partially offset by currency

devaluations in the Dominican Republic contributing to a sales decrease of $4.3 million, declines caused by unfavorable economic

conditions and political uncertainties in Venezuela resulting in a sales decline of $2.3 million, and the unfavorable impacts of foreign

currency movements impacting other geographies within the region.

Management’s Discussion and Analysis of Financial Condition and Results of OperationsRayovac Corporation and Subsidiaries

Our profitability increased $12.4 million to $17.7 million and was primarily the result of the VARTA acquisition, improved profit-

ability in Central America partially offset by profit declines in Venezuela and Dominican Republic.

Our assets increased $12.9 million, or 6.8%, to $203.9 million from $191.0 million the previous year. The acquisition of the VARTA

business in Latin America resulted in asset increases across all asset categories, except for a reduction in accounts receivable reflect-

ing improvements in collections, a decrease in property, plant and equipment reflecting the closure of the Mexico manufacturing

facility. The closure and subsequent write-off of the Mexico manufacturing related assets are included in restructuring and related

charges in our Consolidated Statement of Operations (see Note 15, Restructuring and Related Charges, of Notes to the Consolidated

Financial Statements) and are not included in our Latin America segment results. The Remington acquisition had no effect on Latin

America segment assets.

Corporate Expense. Our corporate expenses increased $8.3 million to $40.0 million from $31.7 million in the previous year. As a

percentage of sales, our corporate expense was 4.3% in fiscal 2003, compared with 5.5% in the previous year. Fiscal 2003 corporate

expense includes higher legal expense associated with patent infringement litigation, a $1.5 million net charge associated with the

settlement of such litigation, generally higher costs associated with the integration of the VARTA businesses and other increases

in compensation expense, primarily reflecting an increase in unearned restricted stock compensation of $2.1 million. Fiscal 2002

included a loss of $1.5 million related to the bankruptcy filing of a freight payment service provider.

Restructuring and Related Charges. In fiscal 2003, we recorded restructuring and related charges of $32.6 million associated with

our cost reduction initiatives, as more fully described above under the heading “Cost Reduction Initiatives—Fiscal 2003,” relating

to: (i) approximately $13.0 million of employee termination benefits for approximately 650 notified employees and non cash costs

of approximately $0.7 million associated with the write-off of pension intangible assets reflecting the curtailment of our Madison,

Wisconsin packaging facility pension plan, (ii) approximately $12.8 million of equipment, inventory and other asset write-offs pri-

marily reflecting the abandonment of equipment and inventory associated with the closure of our Mexico City, Mexico plant and

inventory and fixed asset impairments related to the closure of our Wisconsin packaging and distribution locations, (iii) approxi-

mately $6.1 million of other expenses which include, distributor termination costs of approximately $0.9 million, research and

development contract termination costs of approximately $0.5 million, and other legal and facility shutdown expenses of approxi-

mately $4.7 million, net of a $0.3 million change in estimate reducing our anticipated costs to close our Wonewoc, Wisconsin facility.

In fiscal 2003, we recorded restructuring and related charges in cost of goods sold of approximately $21.1 million including amounts

related to: (i) the closure in October 2002 of our Mexico City, Mexico plant and integration of production into our Guatemala

City, Guatemala manufacturing location, resulting in charges of approximately $6.2 million, including termination payments of

approximately $1.4 million, fixed asset and inventory impairments of approximately $4.3 million, and other shutdown related

expenses of approximately $0.5 million, (ii) the closure of operations at our Madison, Wisconsin packaging facility and combination

with the Company’s Middleton, Wisconsin distribution center into a new leased complex in Dixon, Illinois resulting in charges of

approximately $12.4 million, including termination costs of approximately $2.4 million and non cash pension curtailment costs of

approximately $0.7 million, fixed asset and inventory impairments of approximately $6.9 million, and relocation expenses and other

shutdown related expenses of approximately $2.4 million, (iii) a series of restructuring initiatives impacting our manufacturing

functions in Europe, North America, and Latin America resulting in charges of approximately $2.8 million, including termination

benefits of approximately $1.8 million and inventory and asset impairments of approximately $1.0 million, and (iv) a change in

estimate relating to our anticipated costs to close our Wonewoc, Wisconsin facility resulting in a credit of $0.3 million.

In fiscal 2003, we recorded restructuring and related charges in operating expenses of approximately $11.5 million including amounts

related to: (i) the closure of operations at our Middleton, Wisconsin distribution center and combination with our Madison,

Wisconsin packaging facility into a new leased complex in Dixon, Illinois resulting in charges of approximately $1.4 million, includ-

ing termination costs of approximately $0.3 million, fixed asset impairments of approximately $0.3 million, and relocation expenses

and other shutdown related expenses of approximately $0.8 million, and (ii) a series of restructuring initiatives impacting our sales,

marketing, and administrative functions in Europe, North America, and Latin America resulting in charges of approximately $10.1

million, including termination costs of approximately $7.1 million, distributor termination costs of approximately $0.9 million,

research and development contract termination costs of approximately $0.5 million, fixed asset impairments of $0.3 million, and

legal and other expenses of approximately $1.3 million. The carrying value of assets held for sale under restructuring plans is

approximately $8.7 million, and is included in Prepaid expense and other in our Consolidated Balance Sheets.

Management’s Discussion and Analysis of Financial Condition and Results of OperationsRayovac Corporation and Subsidiaries

Page 20/21

In fiscal 2002, we recorded net restructuring and related charges in cost of goods sold of $1.2 million related to: (i) the closure of

our manufacturing facility in Santo Domingo, Dominican Republic and transfer of production to our Guatemala City, Guatemala

manufacturing facility and the outsourcing of a portion of our zinc carbon battery production previously manufactured at our

Mexico City, Mexico manufacturing facility, as more fully described above under the heading “Cost Reduction Initiatives—Fiscal

2002” and (ii) the reversal of $1.3 million of expenses related to the December 2000 restructuring announcement which were not

realized, primarily reflecting a change in estimated termination benefits of $1.0 million, due to lower estimates of outplacement

costs and costs attributable to fringe benefits, and the retention of selected employees.

The closure of the Dominican Republic manufacturing facility and outsourcing of Mexico zinc carbon production, in fiscal 2002,

resulted in $1.2 million of employee termination benefits for approximately 115 manufacturing employees, $0.9 million of charges

from the abandonment of equipment and inventory, net of a change in estimate of $0.4 million, associated with the closing of the

manufacturing facility and $0.3 million of other expenses. The change in estimate reflected our ability to utilize more inventory and

manufacturing equipment at our Guatemala City, Guatemala manufacturing location than originally anticipated.

Interest Expense. Interest expense increased $21.1 million to $37.2 million in fiscal 2003 due to the increase in debt to finance the

VARTA acquisition.

Non-Operating Expense. In fiscal 2003, we recorded non-operating expense of $3.1 million relating to the write-off of unamor-

tized debt fees associated with our previous credit facility, replaced in conjunction with the VARTA acquisition. There was no

non-operating expense in fiscal 2002.

Other (Income) Expense. Other (income) expense, net, improved $4.9 million to income of $3.6 million in fiscal 2003, primarily

attributable to foreign exchange transaction gains.

Income Tax Expense. Our effective tax rate was 32.8% for fiscal 2003, a decrease from 36.0% during the previous year. The decrease

in the effective tax rate from the prior year primarily reflects the net impact of certain tax credits realized during fiscal 2003, favor-

able adjustments to prior year deferred taxes, adjustments to prior year tax reserves reflecting the expiration of certain statute of

limitations, partially offset by non-deductible interest expense associated with our acquisition of VARTA.

Fiscal Year Ended September 30, 2002 Compared to Fiscal Year Ended September 30, 2001

Highlights of consolidated operating results

Net Sales. Our net sales decreased $43.5 million, or 7.1%, to $572.7 million in fiscal 2002 from $616.2 million the previous year.

Increases in hearing aid battery and lighting product sales were unable to offset declines in zinc carbon and alkaline sales.

Income from Operations. Our income from operations increased $8.6 million, or 15.8%, to $63.0 million in fiscal 2002 from $54.4

million the previous year. This increase was primarily due to reduction in restructuring charges of $21.1 million offset by a $12.0

million bad debt reserve, net of recoveries, resulting from the bankruptcy filing of a key customer.

Net Income. Our net income for fiscal 2002 increased $17.7 million, or 153.9%, to $29.2 million from $11.5 million the previous year.

The increase reflects a reduction in interest expense attributable to the retirement of $65.0 million of senior subordinated notes

following our June 2001 common stock offering, plus a $56.1 million reduction in debt during fiscal 2002 due to strong cash flow

from operations. In addition, fiscal 2001 results reflect a $22.3 million pretax restructuring charge and an $8.6 million pretax non-

operating expense. These improvements were partially offset by a bad debt reserve of $7.5 million, net of tax, recognized in fiscal

2002 related to the bankruptcy filing of a key customer.

North America 2001 2002

Net sales from external customers $448.8 $435.6

Segment profit 80.8 85.5

Segment profit as a % of net sales 18.0% 19.6%

Management’s Discussion and Analysis of Financial Condition and Results of OperationsRayovac Corporation and Subsidiaries

Our revenue from external customers decreased $13.2 million, or 2.9%, to $435.6 million in fiscal 2002 from $448.8 million the pre-

vious year. Zinc carbon sales decreases of $12.3 million reflect the trend in the industry toward alkaline and the discontinuation of

certain products at selected stores of a major retailer. Alkaline sales decreases of $4.8 million were attributable to the decline in sales

to a key customer in bankruptcy, a cautious retail inventory environment and continued promotional activity, and our inability to

replace sales to an OEM customer in the previous year. Increases in lighting products of $4.3 million resulted from new product

launches and distribution gains.

Our profitability increased $4.7 million to $85.5 million in fiscal 2002 from $80.8 million the previous year. This increase was prima-

rily attributable to the benefits of the 2001 plant closures and organizational restructurings as more fully described under the head-

ing “Cost Reduction Initiatives,” that lowered operating expenses and improved gross profit margins. This was partially offset by a

$12.0 million bad debt reserve, net of recoveries, resulting from the bankruptcy filing of a North America segment customer.

Latin America 2001 2002

Net sales from external customers $118.7 $84.7

Segment profit 16.9 5.3

Segment profit as a % of net sales 14.2% 6.3%

Our revenue from external customers decreased $34.0 million, or 28.6%, to $84.7 million in fiscal 2002 from $118.7 million the pre-

vious year due primarily to decreased sales of zinc carbon batteries. Net sales were impacted by unfavorable economic conditions

in Mexico, Argentina, and Venezuela, primarily due to general weakened market conditions. Also impacting net sales were curtail-

ments of shipments to certain distributors and wholesalers who were delinquent on payments, general political uncertainties and

instability in Argentina and Venezuela, and the unfavorable impacts of currency devaluation which contributed approximately

$9.3 million of the sales decline versus fiscal 2001.

We have a business presence in approximately 100 countries throughout the world, all of which are subject to varying degrees of

political and economic risk. In fiscal 2002, changes in the economic and political environments in Mexico, Argentina and Venezuela

subjected us to varying degrees of political and economic risks. While these markets collectively represent approximately 40.0% and

23.3% of our Latin America segment revenue and total assets, respectively, they collectively represent approximately 6.0% and 8.4%

of our consolidated revenue and total assets, respectively.

In spite of the sales decline, the segment remained profitable, with profit of $5.3 million in fiscal 2002. However, this was a decrease

of $11.6 million from the previous year. This decrease was primarily attributable to the impact of the sales decline, partially offset

by lower advertising expenses and a reduction in other operating expenses in the region. As of October 1, 2001, we adopted FASB

Statement No. 142 and were no longer required to amortize goodwill and certain intangibles with indefinite lives. This resulted in

a reduction of amortization expense of $3.0 million, within the segment, for the year. Segment profit margins decreased primarily

due to an unfavorable customer mix compounded by relatively fixed operating expenses spread over lower sales.

Europe/ROW 2001 2002

Net sales from external customers $48.7 $52.5

Segment profit 4.1 5.1

Segment profit as a % of net sales 8.4% 9.7%

Our revenue from external customers increased $3.8 million, or 7.8%, to $52.5 million in fiscal 2002 from $48.7 million the previous

year, primarily reflecting increased sales of alkaline and hearing aid batteries, and favorable impacts of foreign currency movements.

Our profitability increased $1.0 million, or 24.4%, due primarily to sales gains and a reduction in operating expenses due to the

cost reduction initiatives described above under the heading “Cost Reduction Initiatives—Fiscal 2001” and the adoption of FASB

Statement No. 142, which resulted in lower amortization expense.

Corporate Expenses. Our corporate expenses increased $6.6 million, or 26.3%, to $31.7 million in fiscal 2002 from $25.1 million the

previous year. The increase was primarily due to higher legal expenses, technology spending, and compensation expense.

Management’s Discussion and Analysis of Financial Condition and Results of OperationsRayovac Corporation and Subsidiaries

Page 22/23

Restructuring and Related Charges. In fiscal 2002, we recorded net restructuring and related charges of $1.2 million related to:

(i) the closure of our manufacturing facility in Santo Domingo, Dominican Republic and transfer of production to our Guatemala

City, Guatemala manufacturing facility and the outsourcing of a portion of our zinc carbon battery production previously manu-

factured at our Mexico City, Mexico manufacturing facility, as more fully described above under the heading “Cost Reduction

Initiatives—Fiscal 2002” and (ii) the reversal of $1.3 million of expenses related to the December 2000 restructuring announcement

which were not realized, primarily reflecting a change in estimated termination benefits of $1.0 million, due to lower estimates of

outplacement costs and costs attributable to fringe benefits, and the retention of selected employees.

The closure of the Dominican Republic manufacturing facility and outsourcing of Mexico zinc carbon production resulted in $1.2

million of employee termination benefits for approximately 115 manufacturing employees, $0.9 million of charges from the aban-

donment of equipment and inventory, net of a change in estimate of $0.4 million, associated with the closing of the manufacturing

facility and $0.3 million of other expenses. The change in estimate reflected our ability to utilize more inventory and manufacturing

equipment at our Guatemala City, Guatemala manufacturing location than originally anticipated.

The cost reduction initiatives undertaken in fiscal 2002 and described above are complete as of September 30, 2002. The remaining

accrued termination benefits were paid before December 2002. We believe cost reduction initiatives generated annual savings

approximating the cash costs of the restructuring initiatives.

We recorded restructuring and related charges of $22.3 million in fiscal 2001, reflecting $10.1 million of employee termination bene-

fits for approximately 570 employees, $10.2 million of equipment, inventory, and other asset write-offs and $2.0 million of other

expenses associated with the cost reduction initiatives described above under the heading “Cost Reduction Initiatives—Fiscal 2001,”

including: (i) an organizational restructuring in the U.S., (ii) the closure of the Tegucigalpa, Honduras facility and the rationalization

of our manufacturing and distribution processes in our Tegucigalpa, Honduras and Mexico City, Mexico manufacturing facilities

and in our European operations, (iii) the closure of our Wonewoc, Wisconsin manufacturing facility and (iv) the rationalization of

inefficient manufacturing processes, packaging operations and product lines at our Fennimore, Wisconsin manufacturing facility

and Madison, Wisconsin packaging location. In addition, “Restructuring and Related Charges” also reflected costs associated with

our June 2001 common stock offering.

The cost reduction initiatives undertaken in fiscal 2001 are complete and we do not anticipate any further material charges to result

from such initiatives.

Interest Expense. Interest expense decreased $11.2 million, or 41.2%, to $16.0 million in fiscal 2002 from $27.2 million in the

previous year primarily due to the retirement of $65.0 million of senior subordinated notes in June 2001 using proceeds from

our common stock offering and the repayment of $56.1 million in debt from our strong cash flow from operations.

Non-Operating Expense. In fiscal 2001, we recorded non-operating expense of $8.6 million resulting from the premium on the

repurchase of $65.0 million of Senior Subordinated Notes and the related write-off of unamortized debt issuance costs.

Income Tax Expense. Our effective tax rate for fiscal 2002 was 36.0% compared to 34.1% for fiscal 2001. The higher rate for fiscal

2002 primarily reflects a change in geographic profitability away from lower tax jurisdictions, primarily within Latin America, and

proportionately higher income in the United States.

Liquidity and Capital Resources For fiscal 2003, operating activities provided $76.2 million in net cash, an increase of $9.4

million over the previous year. Within operating cash flow, we recognized lower net income of $13.8 million reflecting the impacts

of the fiscal 2003 restructuring activities partially offset by the impacts of the VARTA acquisition. We also experienced an increase in

other non-cash adjustments primarily reflecting non-cash restructuring charges of $13.6 million, depreciation expense of $12.3 mil-

lion primarily reflecting the impacts of the VARTA acquisition, the write-off of the unamortized debt issuance costs of $3.1 million,

and amortization of unearned restricted stock compensation of $2.1 million partially offset by increases in deferred taxes of $13.8

million. Operating cash flow from changes in working capital was essentially unchanged from the previous year.

Net cash used by investing activities increased to $446.4 million for fiscal 2003, primarily reflecting payments associated with the

VARTA and Remington acquisitions, net of cash acquired, of $420.4 million. Capital expenditures of $26.1 million were primarily

for improvements to alkaline battery manufacturing and leasehold improvements on the Dixon, Illinois leased packaging and dis-

tribution center. Capital expenditures for fiscal 2004 are expected to be approximately $25.0 million, which are expected to include

spending for continued investment in our alkaline and hearing aid manufacturing operations, continued technology investments,

and spending associated with our recent Remington acquisition.

Management’s Discussion and Analysis of Financial Condition and Results of OperationsRayovac Corporation and Subsidiaries

During fiscal 2003 we granted approximately 1.2 million options to purchase shares of common stock to various employees of the

company. All grants have been at an exercise price equal to the market price of the common stock on the date of the grant. We also

granted approximately 0.4 million shares of restricted stock on October 1, 2002, from the 1997 incentive plan, to certain members

of management. The majority of these shares will vest on September 30, 2005, with the remainder vesting on September 30, 2006,

provided the recipient is still employed by us. The total market value of the restricted shares on date of grant totaled approximately

$4.8 million and has been recorded as unearned restricted stock compensation as a separate component of shareholders’ equity.

Unearned compensation is being amortized to expense over the vesting period. During fiscal 2003, restricted shares with a value

of approximately $0.3 million on the grant date were forfeited.

The Third Amended and Restated Credit Agreement (“Third Restated Agreement”), undertaken to acquire substantially all of the

consumer battery business of VARTA AG, and subsequently amended on January 29, 2003 (“First Amendment”), required, among

other provisions, that the recording and incurrence of restructuring charges meet certain definitions and time constraints to qualify

as additions in calculating Adjusted EBITDA, as defined, that we were to transform the German subsidiary acquired from VARTA

AG from a GmbH legal structure to a KGaA legal structure (the “Transformation”) on or before June 30, 2003, and that we obtain

consent of the Required Lenders to effect releases or substitutions of collateral pledges. Effective June 27, 2003, the Third Restated

Agreement was amended (“Second Amendment”): (i) to re-define and permit acceleration, recording, and incurrence of certain

Restructuring Charges, as defined in the Third Restated Agreement, (ii) to extend the deadline for the Transformation to on or

before March 31, 2004, and (iii) to consent to certain organizational restructurings (“Restructurings”), including releases and sub-

stitutions of collateral pledges, and disregarding application of certain basket amounts as necessary to effect the Restructurings.

Effective September 30, 2003, the Third Restated Agreement was amended (“Third Amendment”) to (i) permit the Remington

acquisition (the “Acquisition”) including issuance of $350.0 million of senior subordinated debt, increase the Dollar-denominated