rbi retail loan loss provisioning - wb 2014 - world...

TRANSCRIPT

Loan loss provisioning of a retail portfolio -

an example from RBI AG Deyan IVANOV Retail Risk Methodology and Validation Raiffeisen Bank International AG

Slide no.2

A leading corporate and investment bank for Austria‘s Top 1,000 companies and for Western European commercial customers

A leading universal bank in CEE with the largest network of any Western banking group

Home market Austria and Central and Eastern Europe (CEE) with further focus on Asia

15 markets in CEE

~14.5 milion customers

~ 3000 business outlets

> 57 000 employees

Market capitalization ~ EUR 7.1 bilion

RBI at a glance (data as of 1Q2014)

Listed on the Vienna Stock Exchange

Slide no.3

Agenda

1 Types of Loan Loss Provisions in the Retail Segment of RBI

2 Individual Loan Loss Provisions (ILLP) - Overview

3 ILLP – Treatment of Restructured Accounts

4 ILLP – Calculation steps

5 Portfolio-based Loan Loss Provisions (PLLP) - Overview

6 PLLP – Flow Rates, Loss Factors, Transition Matrix – Definitions and Examples

7 PLLP – Gross Provisions, Recovery Models, Net Provisions - Calculations

8 Risk Costs – Definitions and Examples

9 Experience from the roll-out across the RBI Group

10 Future Plans for Loan Loss Provisioning Methodology in RBI Retail Portfolio

Slide no.4

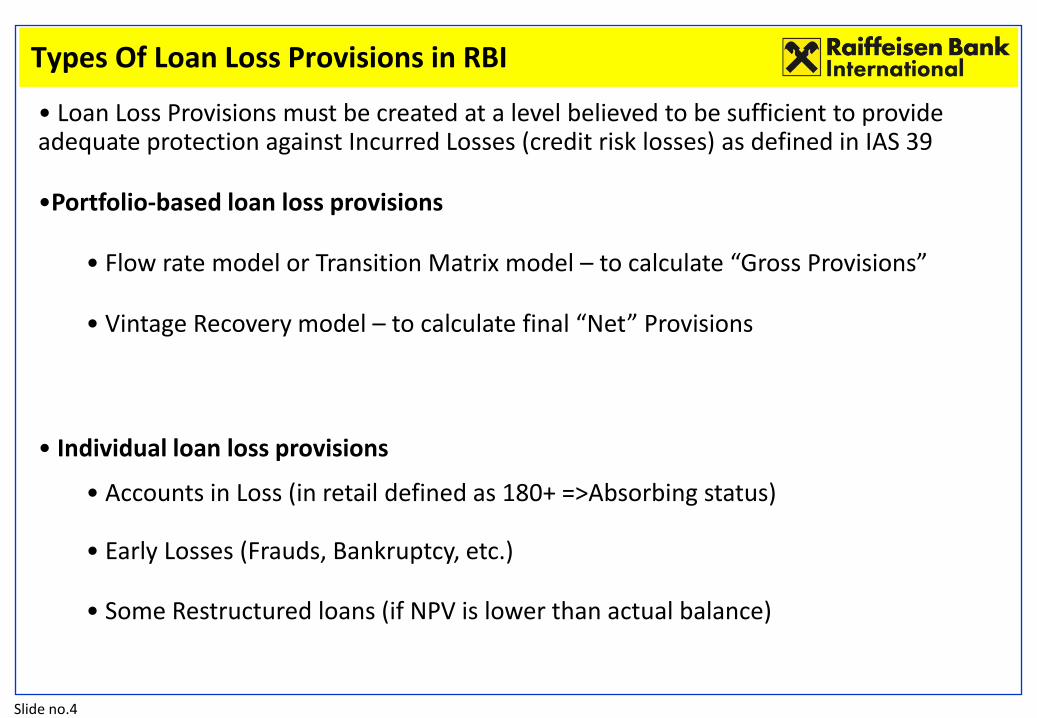

• Loan Loss Provisions must be created at a level believed to be sufficient to provide adequate protection against Incurred Losses (credit risk losses) as defined in IAS 39

•Portfolio-based loan loss provisions

• Flow rate model or Transition Matrix model – to calculate “Gross Provisions”

• Vintage Recovery model – to calculate final “Net” Provisions

• Individual loan loss provisions

• Accounts in Loss (in retail defined as 180+ =>Absorbing status)

• Early Losses (Frauds, Bankruptcy, etc.)

• Some Restructured loans (if NPV is lower than actual balance)

Types Of Loan Loss Provisions in RBI

Slide no.5

180+ accounts

90_180 accounts

Accounts with no

delinquencies

1_90 accounts

360+ accounts

180+ accounts

90_180

accounts

Accounts with

no

delinquencies

1_90 accounts

360+ accounts

Balance Provisions

NPL

PLLP

ILLP

New volume No provisions

Types Of Loan Loss Provisions in RBI (cont’d)

Slide no.6

Agenda

1 Types of Loan Loss Provisions in the Retail Segment of RBI

2 Individual Loan Loss Provisions (ILLP) - Overview

3 ILLP – Treatment of Restructured Accounts

4 ILLP – Calculation steps

5 Portfolio-based Loan Loss Provisions (PLLP) - Overview

6 PLLP – Flow Rates, Loss Factors, Transition Matrix – Definitions and Examples

7 PLLP – Gross Provisions, Recovery Models, Net Provisions - Calculations

8 Risk Costs – Definitions and Examples

9 Experience from the roll-out across the RBI Group

10 Future Plans for Loan Loss Provisioning Methodology in RBI Retail Portfolio

Slide no.7

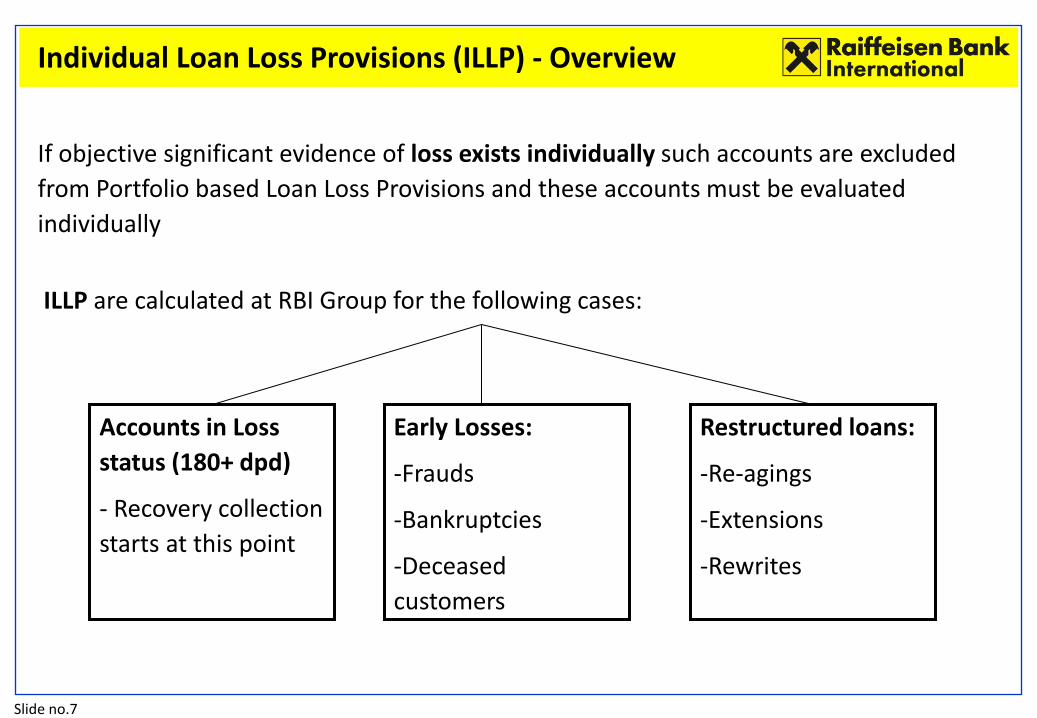

Restructured loans:

-Re-agings

-Extensions

-Rewrites

Early Losses:

-Frauds

-Bankruptcies

-Deceased

customers

Accounts in Loss

status (180+ dpd)

- Recovery collection

starts at this point

Individual Loan Loss Provisions (ILLP) - Overview

If objective significant evidence of loss exists individually such accounts are excluded

from Portfolio based Loan Loss Provisions and these accounts must be evaluated

individually

ILLP are calculated at RBI Group for the following cases:

Slide no.8

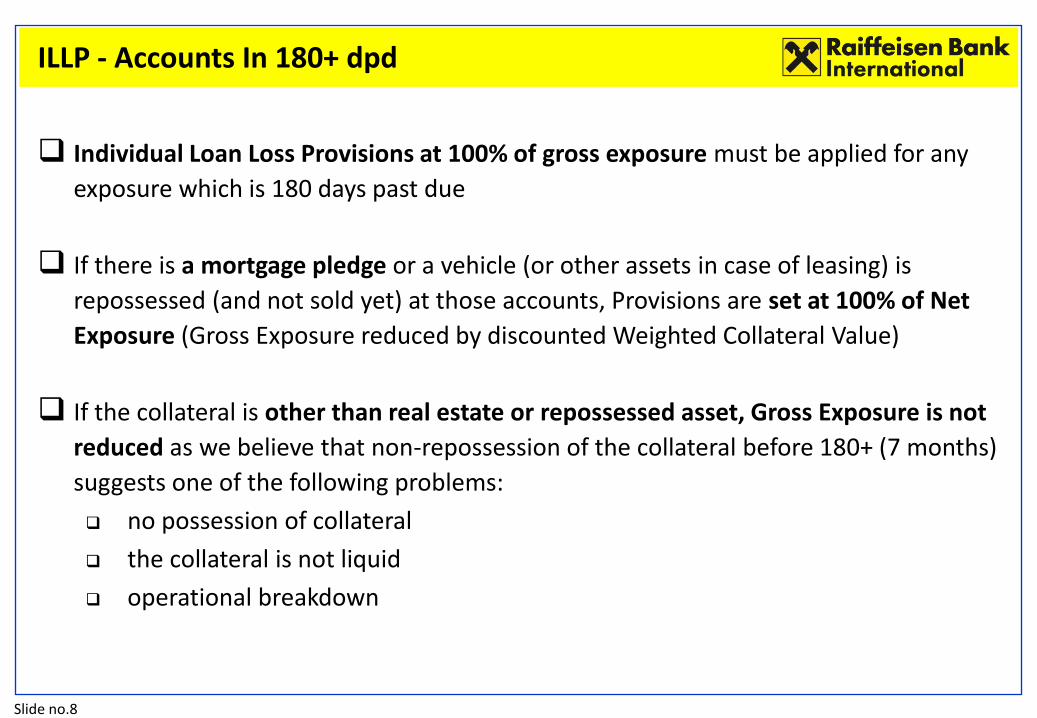

ILLP - Accounts In 180+ dpd

Individual Loan Loss Provisions at 100% of gross exposure must be applied for any

exposure which is 180 days past due

If there is a mortgage pledge or a vehicle (or other assets in case of leasing) is

repossessed (and not sold yet) at those accounts, Provisions are set at 100% of Net

Exposure (Gross Exposure reduced by discounted Weighted Collateral Value)

If the collateral is other than real estate or repossessed asset, Gross Exposure is not

reduced as we believe that non-repossession of the collateral before 180+ (7 months)

suggests one of the following problems:

no possession of collateral

the collateral is not liquid

operational breakdown

Slide no.9

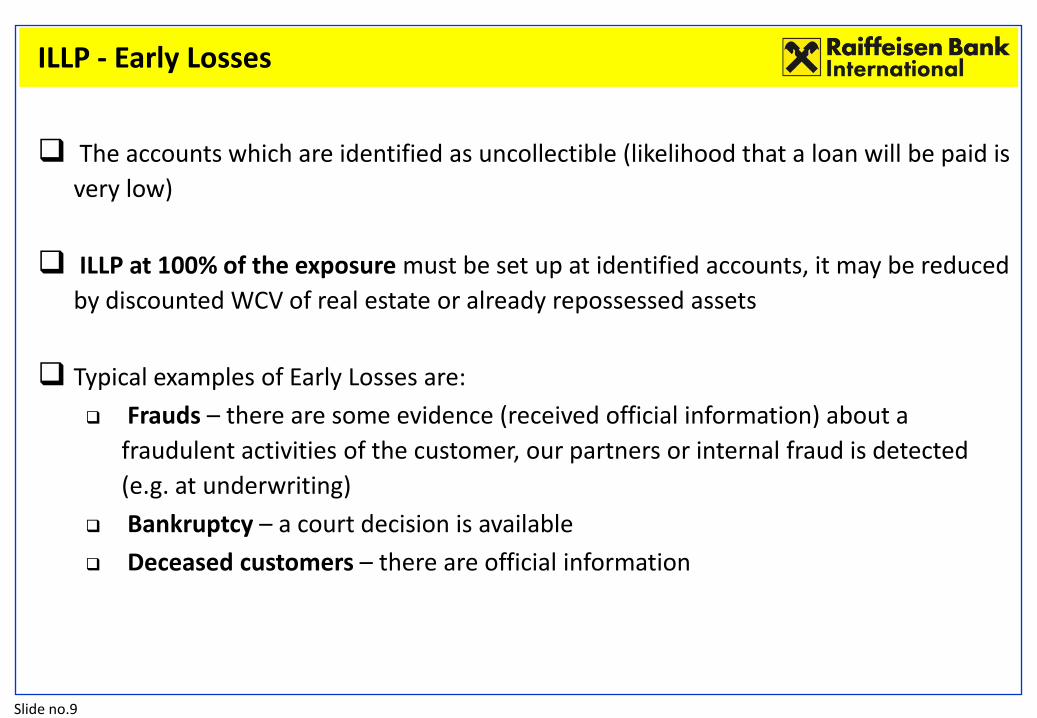

The accounts which are identified as uncollectible (likelihood that a loan will be paid is

very low)

ILLP at 100% of the exposure must be set up at identified accounts, it may be reduced

by discounted WCV of real estate or already repossessed assets

Typical examples of Early Losses are:

Frauds – there are some evidence (received official information) about a

fraudulent activities of the customer, our partners or internal fraud is detected

(e.g. at underwriting)

Bankruptcy – a court decision is available

Deceased customers – there are official information

ILLP - Early Losses

Slide no.10

Agenda

1 Types of Loan Loss Provisions in the Retail Segment of RBI

2 Individual Loan Loss Provisions (ILLP) - Overview

3 ILLP – Treatment of Restructured Accounts

4 ILLP – Calculation steps

5 Portfolio-based Loan Loss Provisions (PLLP) - Overview

6 PLLP – Flow Rates, Loss Factors, Transition Matrix – Definitions and Examples

7 PLLP – Gross Provisions, Recovery Models, Net Provisions - Calculations

8 Risk Costs – Definitions and Examples

9 Experience from the roll-out across the RBI Group

10 Future Plans for Loan Loss Provisioning Methodology in RBI Retail Portfolio

Slide no.11

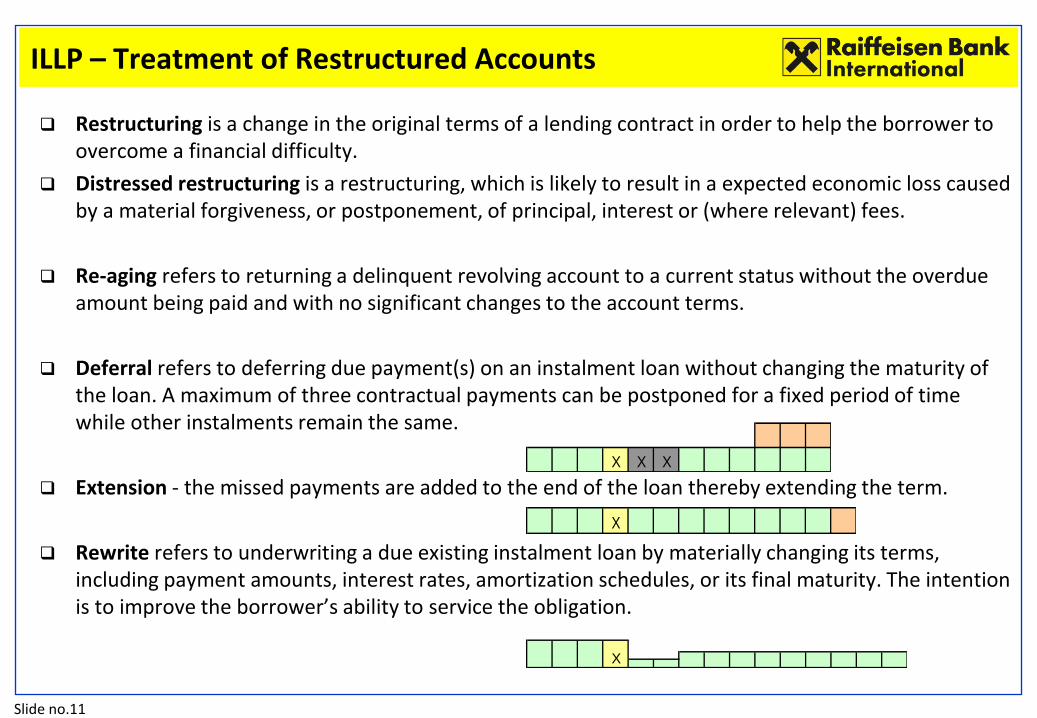

ILLP – Treatment of Restructured Accounts

Restructuring is a change in the original terms of a lending contract in order to help the borrower to overcome a financial difficulty.

Distressed restructuring is a restructuring, which is likely to result in a expected economic loss caused by a material forgiveness, or postponement, of principal, interest or (where relevant) fees.

Re-aging refers to returning a delinquent revolving account to a current status without the overdue amount being paid and with no significant changes to the account terms.

Deferral refers to deferring due payment(s) on an instalment loan without changing the maturity of the loan. A maximum of three contractual payments can be postponed for a fixed period of time while other instalments remain the same.

Extension - the missed payments are added to the end of the loan thereby extending the term.

Rewrite refers to underwriting a due existing instalment loan by materially changing its terms, including payment amounts, interest rates, amortization schedules, or its final maturity. The intention is to improve the borrower’s ability to service the obligation.

X

X X X

X

Slide no.12

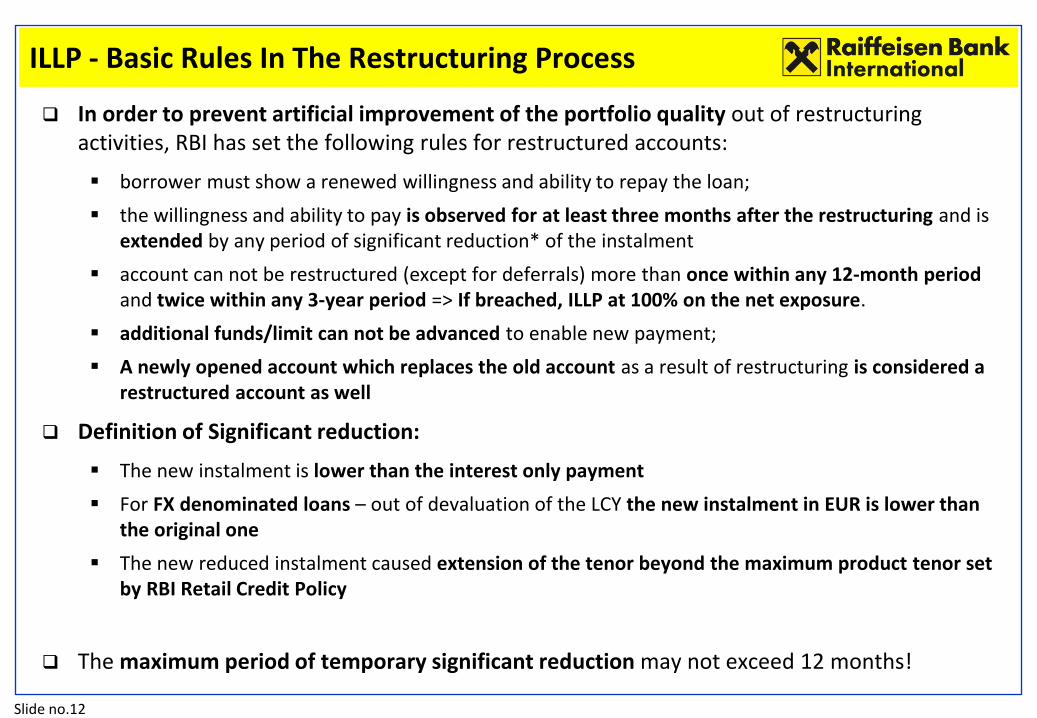

ILLP - Basic Rules In The Restructuring Process

In order to prevent artificial improvement of the portfolio quality out of restructuring activities, RBI has set the following rules for restructured accounts:

borrower must show a renewed willingness and ability to repay the loan;

the willingness and ability to pay is observed for at least three months after the restructuring and is extended by any period of significant reduction* of the instalment

account can not be restructured (except for deferrals) more than once within any 12-month period and twice within any 3-year period => If breached, ILLP at 100% on the net exposure.

additional funds/limit can not be advanced to enable new payment;

A newly opened account which replaces the old account as a result of restructuring is considered a restructured account as well

Definition of Significant reduction:

The new instalment is lower than the interest only payment

For FX denominated loans – out of devaluation of the LCY the new instalment in EUR is lower than the original one

The new reduced instalment caused extension of the tenor beyond the maximum product tenor set by RBI Retail Credit Policy

The maximum period of temporary significant reduction may not exceed 12 months!

Slide no.13

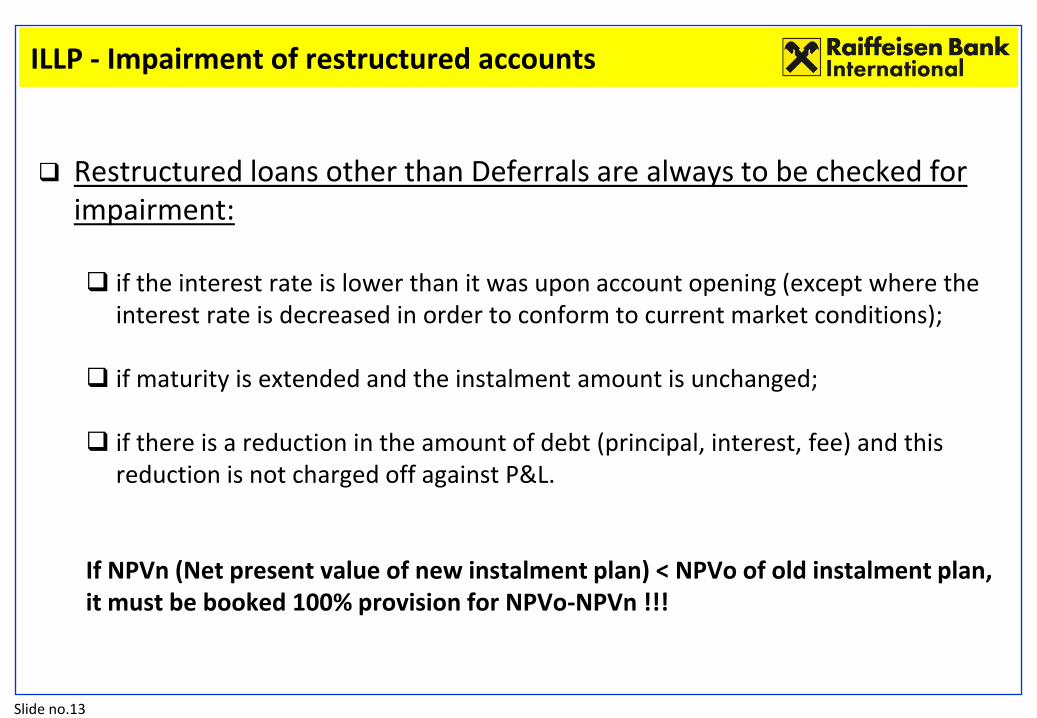

ILLP - Impairment of restructured accounts

Restructured loans other than Deferrals are always to be checked for impairment:

if the interest rate is lower than it was upon account opening (except where the

interest rate is decreased in order to conform to current market conditions);

if maturity is extended and the instalment amount is unchanged;

if there is a reduction in the amount of debt (principal, interest, fee) and this reduction is not charged off against P&L.

If NPVn (Net present value of new instalment plan) < NPVo of old instalment plan, it must be booked 100% provision for NPVo-NPVn !!!

Slide no.14

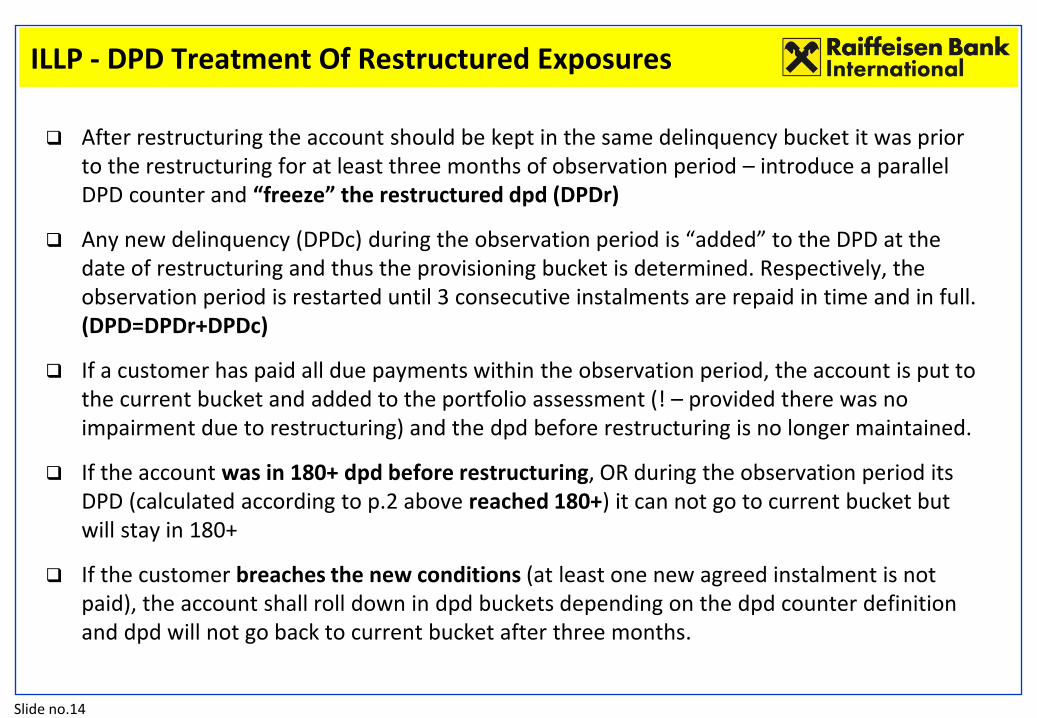

ILLP - DPD Treatment Of Restructured Exposures

After restructuring the account should be kept in the same delinquency bucket it was prior to the restructuring for at least three months of observation period – introduce a parallel DPD counter and “freeze” the restructured dpd (DPDr)

Any new delinquency (DPDc) during the observation period is “added” to the DPD at the date of restructuring and thus the provisioning bucket is determined. Respectively, the observation period is restarted until 3 consecutive instalments are repaid in time and in full. (DPD=DPDr+DPDc)

If a customer has paid all due payments within the observation period, the account is put to the current bucket and added to the portfolio assessment (! – provided there was no impairment due to restructuring) and the dpd before restructuring is no longer maintained.

If the account was in 180+ dpd before restructuring, OR during the observation period its DPD (calculated according to p.2 above reached 180+) it can not go to current bucket but will stay in 180+

If the customer breaches the new conditions (at least one new agreed instalment is not paid), the account shall roll down in dpd buckets depending on the dpd counter definition and dpd will not go back to current bucket after three months.

Slide no.15

Agenda

1 Types of Loan Loss Provisions in the Retail Segment of RBI

2 Individual Loan Loss Provisions (ILLP) - Overview

3 ILLP – Treatment of Restructured Accounts

4 ILLP – Calculation steps

5 Portfolio-based Loan Loss Provisions (PLLP) - Overview

6 PLLP – Flow Rates, Loss Factors, Transition Matrix – Definitions and Examples

7 PLLP – Gross Provisions, Recovery Models, Net Provisions - Calculations

8 Risk Costs – Definitions and Examples

9 Experience from the roll-out across the RBI Group

10 Future Plans for Loan Loss Provisioning Methodology in RBI Retail Portfolio

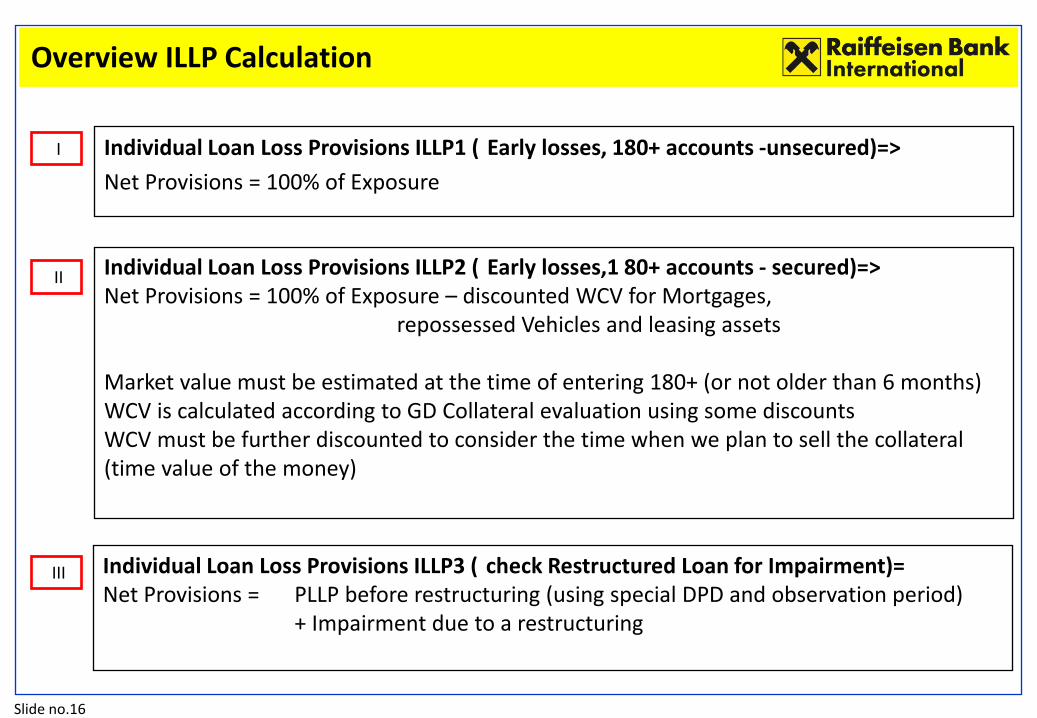

Slide no.16

Individual Loan Loss Provisions ILLP1 ( Early losses, 180+ accounts -unsecured)=>

Net Provisions = 100% of Exposure

I

II Individual Loan Loss Provisions ILLP2 ( Early losses,1 80+ accounts - secured)=> Net Provisions = 100% of Exposure – discounted WCV for Mortgages, repossessed Vehicles and leasing assets Market value must be estimated at the time of entering 180+ (or not older than 6 months) WCV is calculated according to GD Collateral evaluation using some discounts WCV must be further discounted to consider the time when we plan to sell the collateral (time value of the money)

III Individual Loan Loss Provisions ILLP3 ( check Restructured Loan for Impairment)= Net Provisions = PLLP before restructuring (using special DPD and observation period) + Impairment due to a restructuring

Overview ILLP Calculation

Slide no.17

Agenda

1 Types of Loan Loss Provisions in the Retail Segment of RBI

2 Individual Loan Loss Provisions (ILLP) - Overview

3 ILLP – Treatment of Restructured Accounts

4 ILLP – Calculation steps

5 Portfolio-based Loan Loss Provisions (PLLP) - Overview

6 PLLP – Flow Rates, Loss Factors, Transition Matrix – Definitions and Examples

7 PLLP – Gross Provisions, Recovery Models, Net Provisions - Calculations

8 Risk Costs – Definitions and Examples

9 Experience from the roll-out across the RBI Group

10 Future Plans for Loan Loss Provisioning Methodology in RBI Retail Portfolio

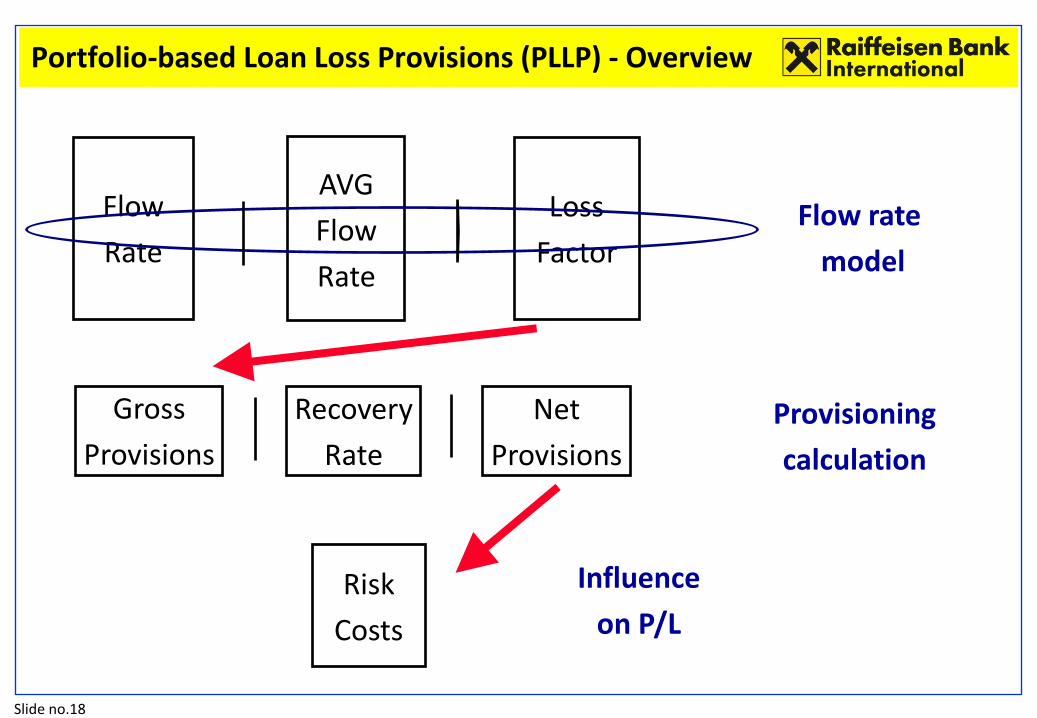

Slide no.18

Flow

Rate

AVG

Flow

Rate

Loss

Factor

Gross

Provisions

Recovery

Rate

Net

Provisions

Flow rate

model

Provisioning

calculation

Risk

Costs

Influence

on P/L

Portfolio-based Loan Loss Provisions (PLLP) - Overview

Slide no.19

Agenda

1 Types of Loan Loss Provisions in the Retail Segment of RBI

2 Individual Loan Loss Provisions (ILLP) - Overview

3 ILLP – Treatment of Restructured Accounts

4 ILLP – Calculation steps

5 Portfolio-based Loan Loss Provisions (PLLP) - Overview

6 PLLP – Flow Rates, Loss Factors, Transition Matrix – Definitions and Examples

7 PLLP – Gross Provisions, Recovery Models, Net Provisions - Calculations

8 Risk Costs – Definitions and Examples

9 Experience from the roll-out across the RBI Group

10 Future Plans for Loan Loss Provisioning Methodology in RBI Retail Portfolio

Slide no.20

Bucket (i) Previous month balance Bi(t-1)

Current month balance Bi(t) Monthly Flow rate (%) FR

Current (1) B10[1] B11 FR1[3] = min(100%; B21/B10)

1-30 dpd (2) B20 B21 [2] FR2 = min(100%; B31/B20)

31-60 dpd (3) B30 B31 FR3 = min(100%; B41/B30)

61-90 dpd (4) B40 B41 FR4 = min(100%; B51/B40)

91-120 dpd (5) B50 B51 FR5 = min(100%; B61/B50)

121-150 dpd (6) B60 B61 FR6 = min(100%; B71/B60)

151 - 180 dpd (7) B70 B71 FR7 = min(100%; B81/B70)

180+ (8) B80 B81 100%

[1] B10 – balance of loans in the category (Current Bucket) in month “t-1” (previous month)

[2] B21 – balance of loans in the category (1_30) in month “t” (current month – for which the reporting is done)

[3] FR1– Flow rate (%) of rolling from Current bucket to 1-30 dpd bucket corresponding to the actual month (t) for which the reporting is done.

It is based on the assumption that an account either flows down or is paid out

Flow rate is calculated as a ratio – the balance in dpd bucket from actual month over the balance in the previous dpd bucket from previous month (maximum 100%)

PLLP - Flow Rate – Definition

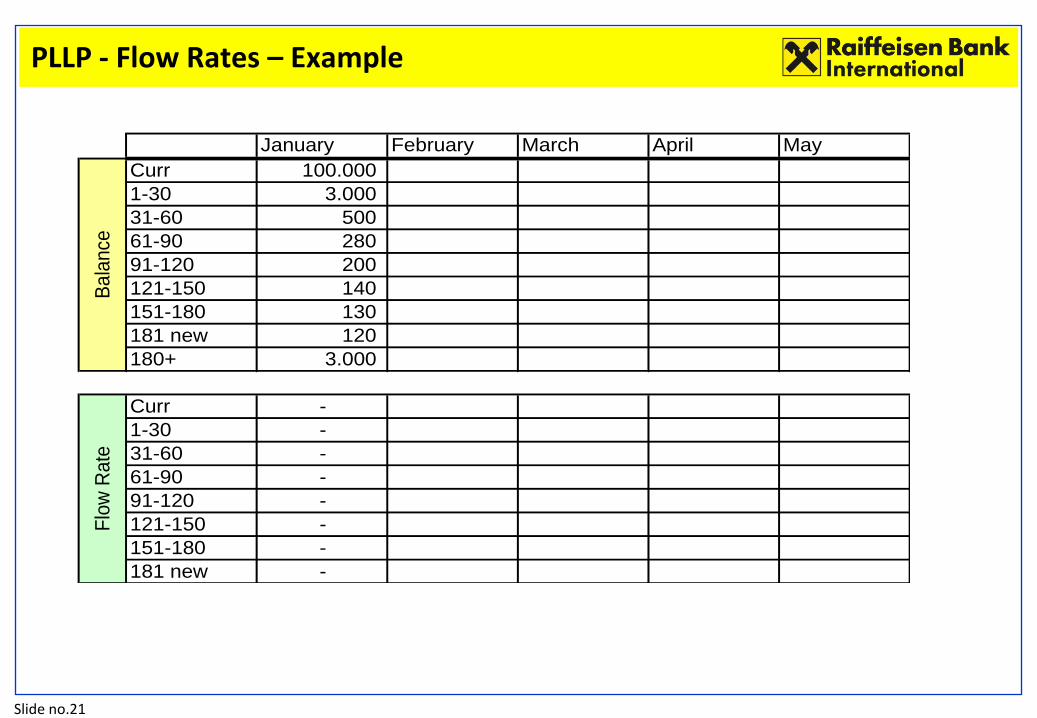

Slide no.21

January February March April May

Curr 100.000

1-30 3.000

31-60 500

61-90 280

91-120 200

121-150 140

151-180 130

181 new 120

180+ 3.000

Curr -

1-30 -

31-60 -

61-90 -

91-120 -

121-150 -

151-180 -

181 new -

Ba

lance

Flo

w R

ate

PLLP - Flow Rates – Example

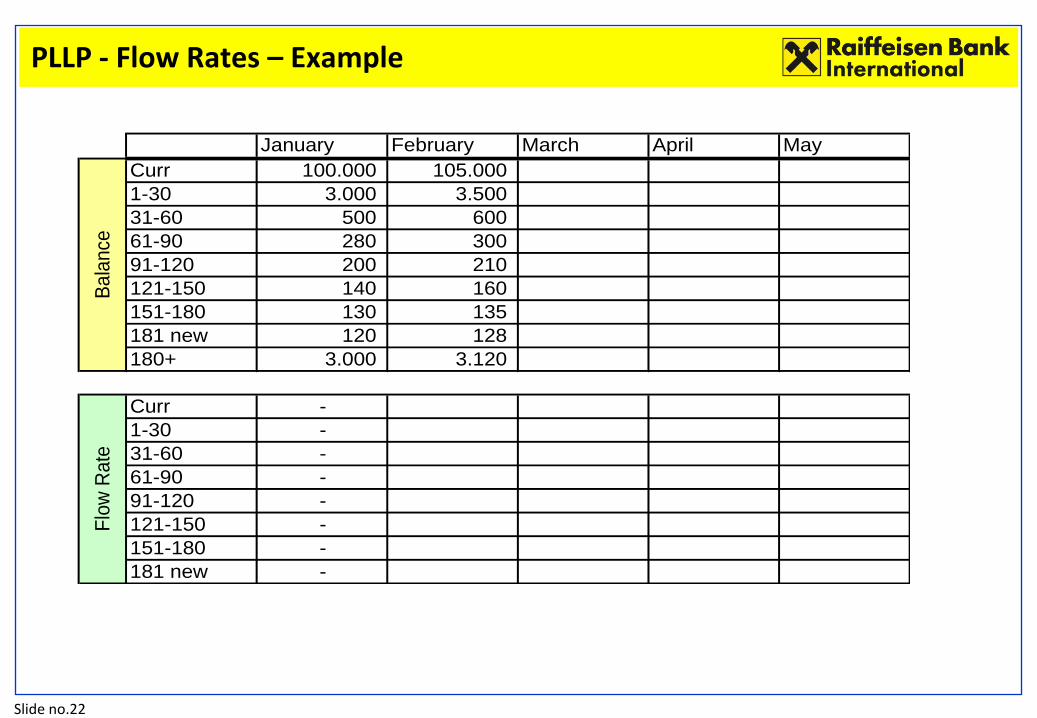

Slide no.22

January February March April May

Curr 100.000 105.000

1-30 3.000 3.500

31-60 500 600

61-90 280 300

91-120 200 210

121-150 140 160

151-180 130 135

181 new 120 128

180+ 3.000 3.120

Curr -

1-30 -

31-60 -

61-90 -

91-120 -

121-150 -

151-180 -

181 new -

Ba

lance

Flo

w R

ate

PLLP - Flow Rates – Example

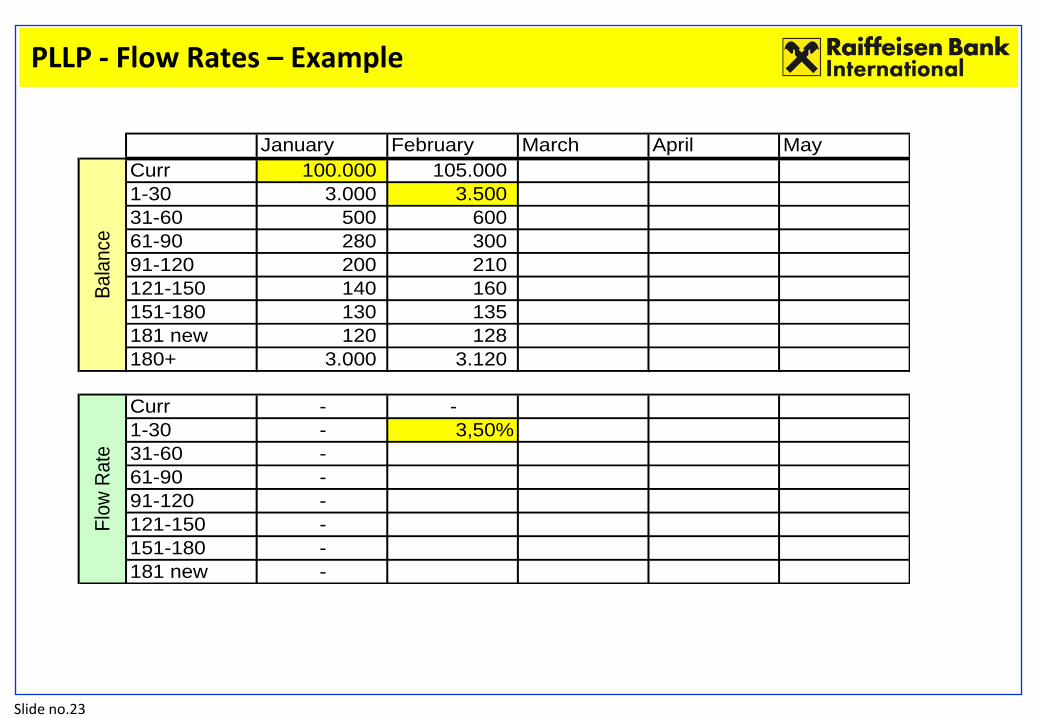

Slide no.23

January February March April May

Curr 100.000 105.000

1-30 3.000 3.500

31-60 500 600

61-90 280 300

91-120 200 210

121-150 140 160

151-180 130 135

181 new 120 128

180+ 3.000 3.120

Curr - -

1-30 - 3,50%

31-60 -

61-90 -

91-120 -

121-150 -

151-180 -

181 new -

Ba

lance

Flo

w R

ate

PLLP - Flow Rates – Example

Slide no.24

January February March April May

Curr 100.000 105.000

1-30 3.000 3.500

31-60 500 600

61-90 280 300

91-120 200 210

121-150 140 160

151-180 130 135

181 new 120 128

180+ 3.000 3.120

Curr - -

1-30 - 3,50%

31-60 - 20,00%

61-90 -

91-120 -

121-150 -

151-180 -

181 new -

Ba

lance

Flo

w R

ate

PLLP - Flow Rates – Example

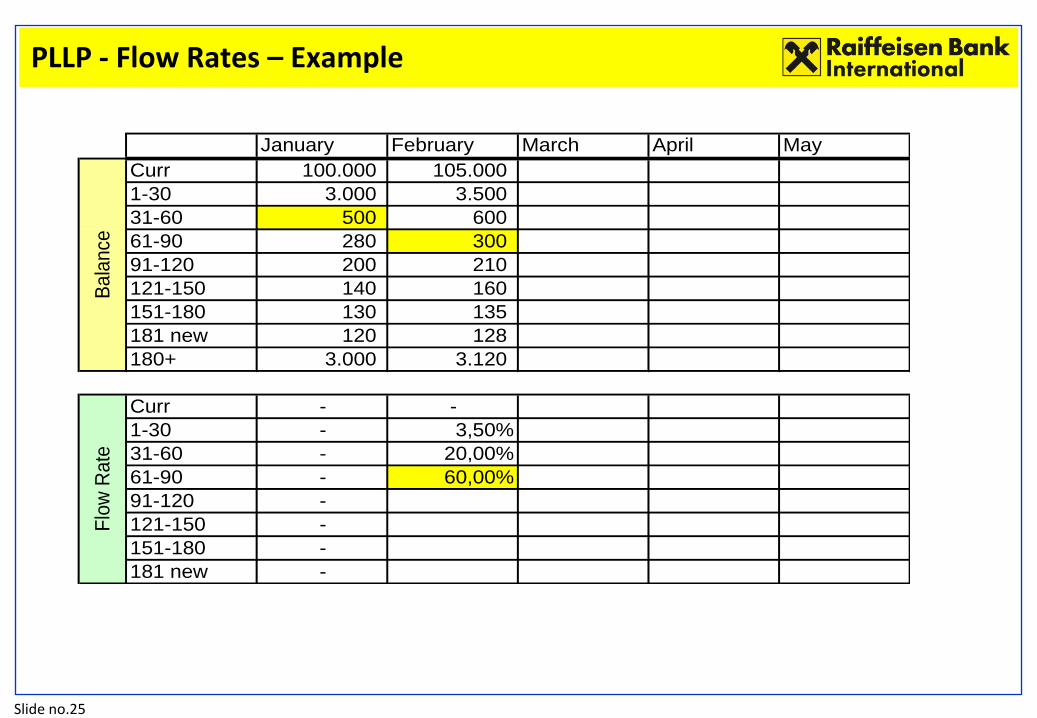

Slide no.25

January February March April May

Curr 100.000 105.000

1-30 3.000 3.500

31-60 500 600

61-90 280 300

91-120 200 210

121-150 140 160

151-180 130 135

181 new 120 128

180+ 3.000 3.120

Curr - -

1-30 - 3,50%

31-60 - 20,00%

61-90 - 60,00%

91-120 -

121-150 -

151-180 -

181 new -

Ba

lance

Flo

w R

ate

PLLP - Flow Rates – Example

Slide no.26

January February March April May

Curr 100.000 105.000

1-30 3.000 3.500

31-60 500 600

61-90 280 300

91-120 200 210

121-150 140 160

151-180 130 135

181 new 120 128

180+ 3.000 3.120

Curr - -

1-30 - 3,50%

31-60 - 20,00%

61-90 - 60,00%

91-120 - 75,00%

121-150 -

151-180 -

181 new -

Ba

lance

Flo

w R

ate

PLLP - Flow Rates – Example

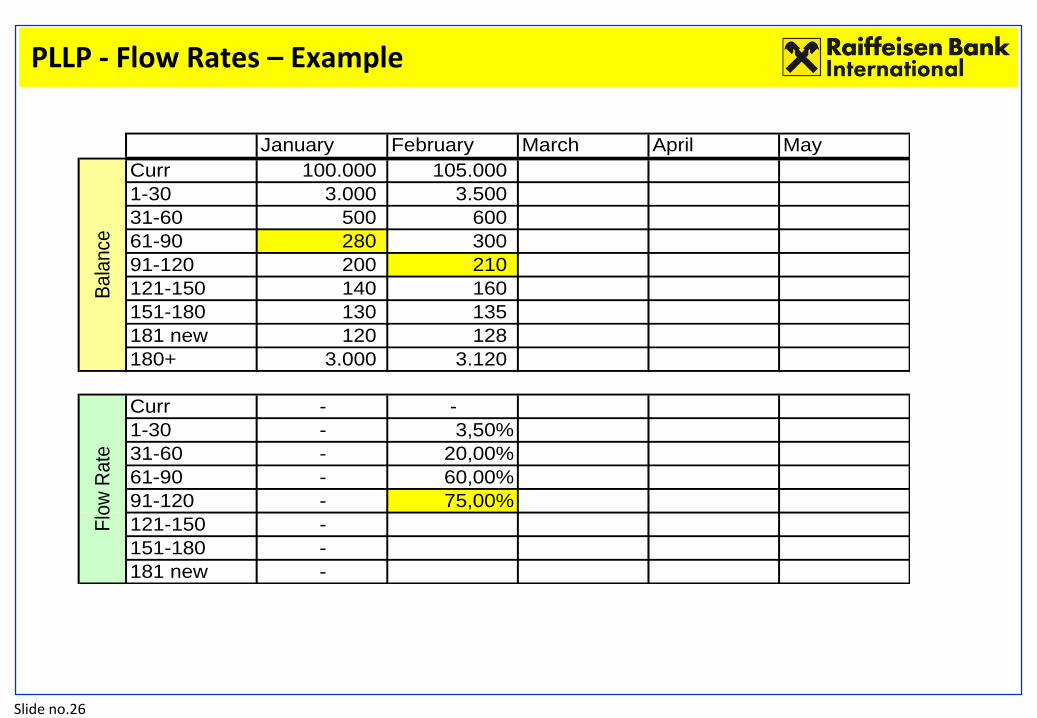

Slide no.27

January February March April May

Curr 100.000 105.000

1-30 3.000 3.500

31-60 500 600

61-90 280 300

91-120 200 210

121-150 140 160

151-180 130 135

181 new 120 128

180+ 3.000 3.120

Curr - -

1-30 - 3,50%

31-60 - 20,00%

61-90 - 60,00%

91-120 - 75,00%

121-150 - 80,00%

151-180 -

181 new -

Ba

lance

Flo

w R

ate

PLLP - Flow Rates – Example

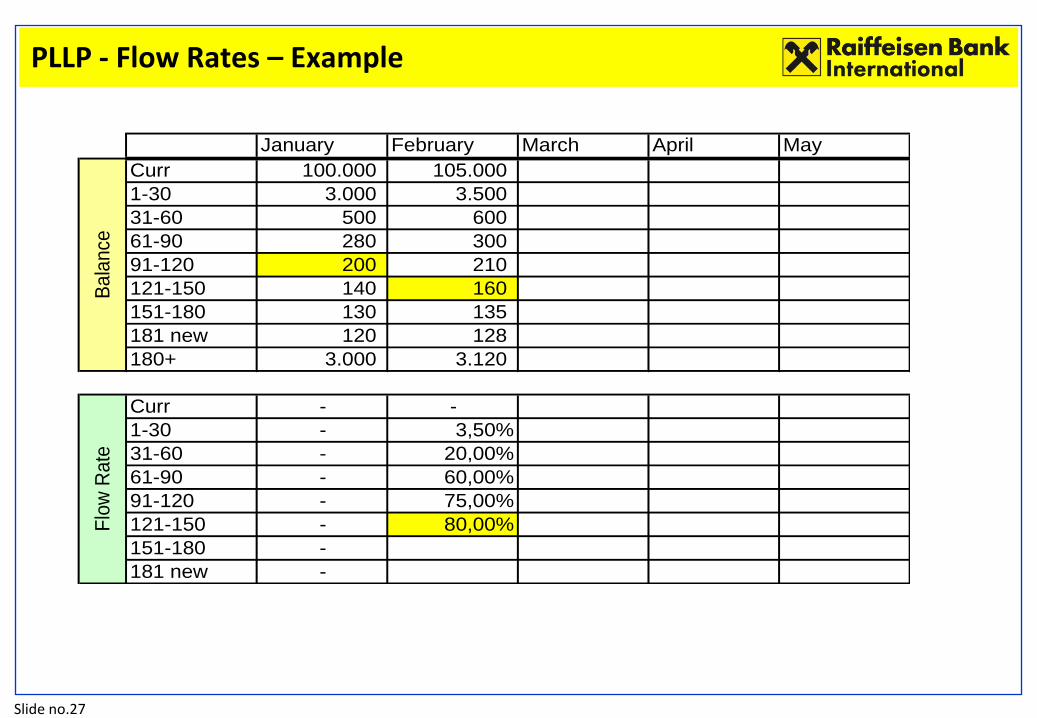

Slide no.28

January February March April May

Curr 100.000 105.000

1-30 3.000 3.500

31-60 500 600

61-90 280 300

91-120 200 210

121-150 140 160

151-180 130 135

181 new 120 128

180+ 3.000 3.120

Curr - -

1-30 - 3,50%

31-60 - 20,00%

61-90 - 60,00%

91-120 - 75,00%

121-150 - 80,00%

151-180 - 96,43%

181 new -

Ba

lance

Flo

w R

ate

PLLP - Flow Rates – Example

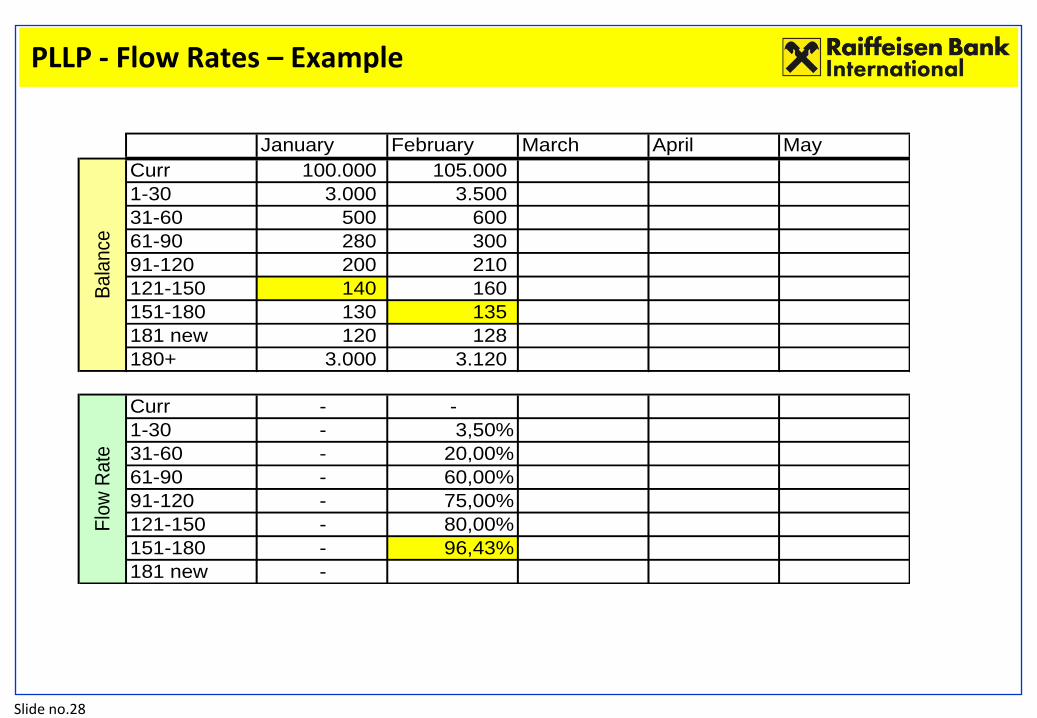

Slide no.29

January February March April May

Curr 100.000 105.000

1-30 3.000 3.500

31-60 500 600

61-90 280 300

91-120 200 210

121-150 140 160

151-180 130 135

181 new 120 128

180+ 3.000 3.120

Curr - -

1-30 - 3,50%

31-60 - 20,00%

61-90 - 60,00%

91-120 - 75,00%

121-150 - 80,00%

151-180 - 96,43%

181 new - 98,46%

Ba

lance

Flo

w R

ate

PLLP - Flow Rates – Example

Slide no.30

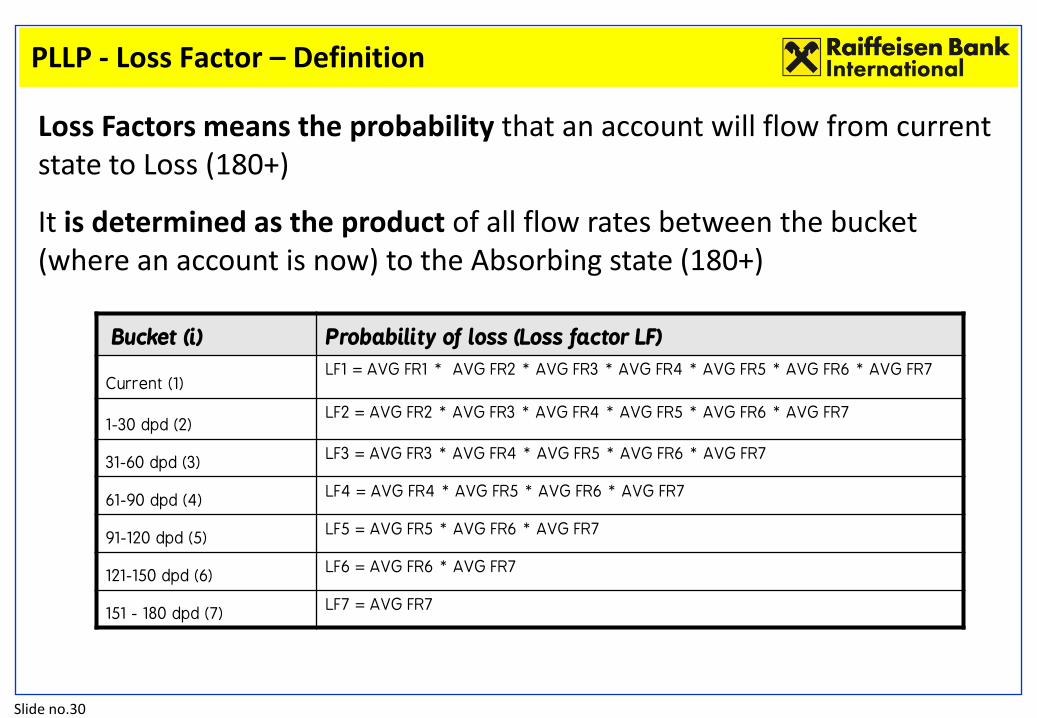

Loss Factors means the probability that an account will flow from current state to Loss (180+)

It is determined as the product of all flow rates between the bucket (where an account is now) to the Absorbing state (180+)

Bucket (i) Probability of loss (Loss factor LF)

Current (1) LF1 = AVG FR1 * AVG FR2 * AVG FR3 * AVG FR4 * AVG FR5 * AVG FR6 * AVG FR7

1-30 dpd (2) LF2 = AVG FR2 * AVG FR3 * AVG FR4 * AVG FR5 * AVG FR6 * AVG FR7

31-60 dpd (3) LF3 = AVG FR3 * AVG FR4 * AVG FR5 * AVG FR6 * AVG FR7

61-90 dpd (4) LF4 = AVG FR4 * AVG FR5 * AVG FR6 * AVG FR7

91-120 dpd (5) LF5 = AVG FR5 * AVG FR6 * AVG FR7

121-150 dpd (6) LF6 = AVG FR6 * AVG FR7

151 - 180 dpd (7) LF7 = AVG FR7

PLLP - Loss Factor – Definition

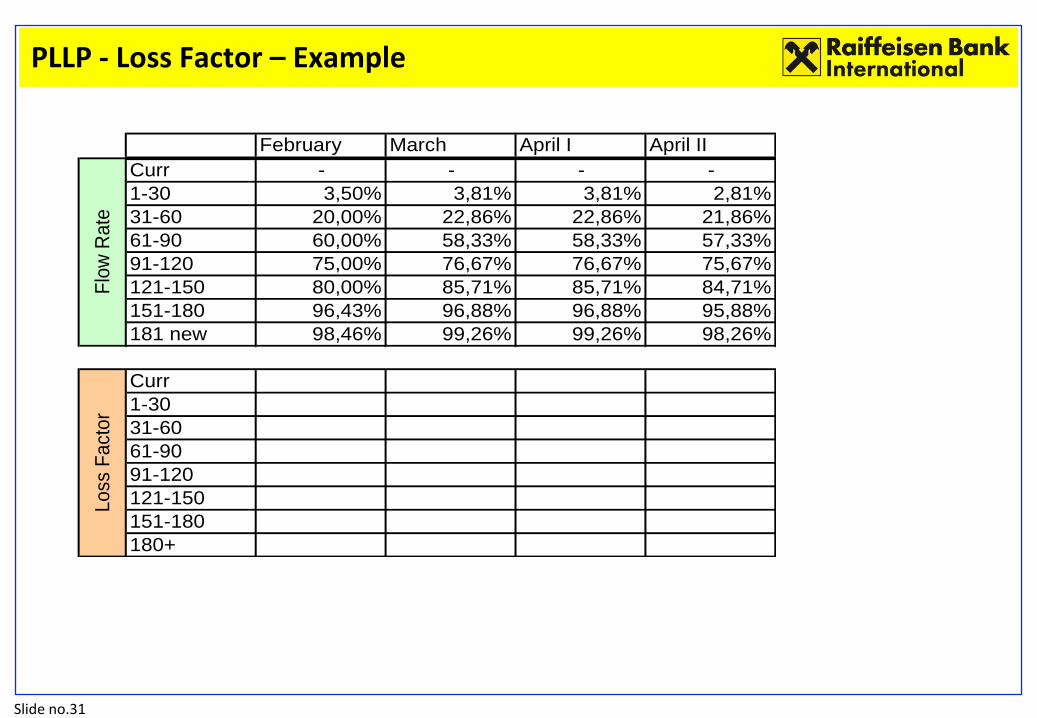

Slide no.31

February March April I April II

Curr - - - -

1-30 3,50% 3,81% 3,81% 2,81%

31-60 20,00% 22,86% 22,86% 21,86%

61-90 60,00% 58,33% 58,33% 57,33%

91-120 75,00% 76,67% 76,67% 75,67%

121-150 80,00% 85,71% 85,71% 84,71%

151-180 96,43% 96,88% 96,88% 95,88%

181 new 98,46% 99,26% 99,26% 98,26%

Curr

1-30

31-60

61-90

91-120

121-150

151-180

180+

Flo

w R

ate

Loss

Fact

or

PLLP - Loss Factor – Example

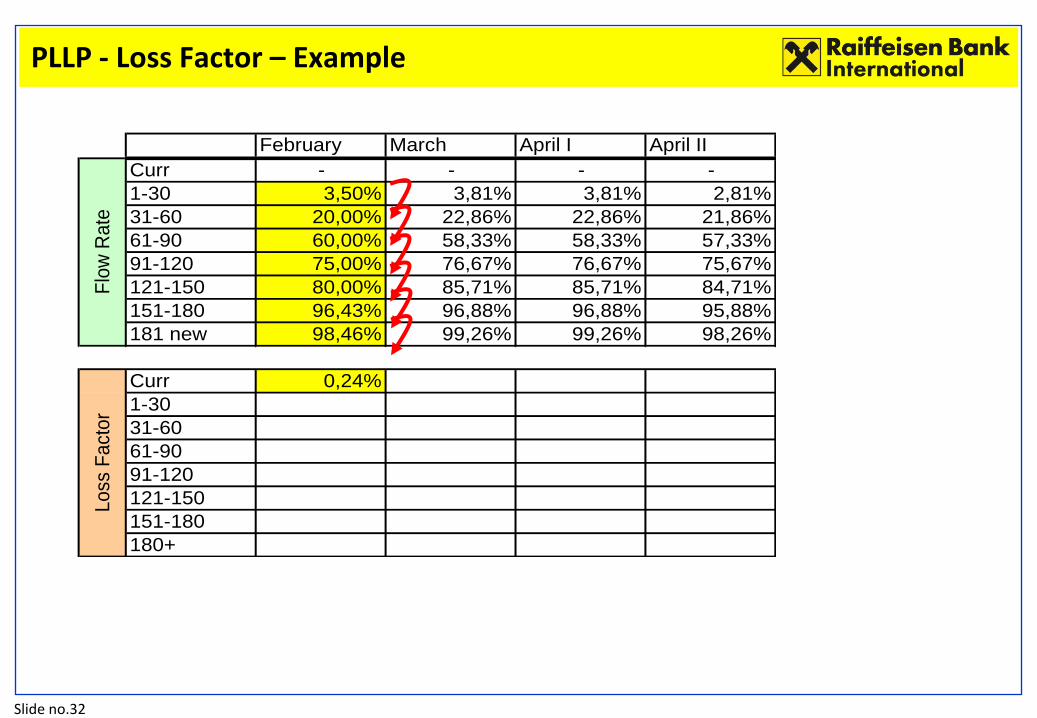

Slide no.32

February March April I April II

Curr - - - -

1-30 3,50% 3,81% 3,81% 2,81%

31-60 20,00% 22,86% 22,86% 21,86%

61-90 60,00% 58,33% 58,33% 57,33%

91-120 75,00% 76,67% 76,67% 75,67%

121-150 80,00% 85,71% 85,71% 84,71%

151-180 96,43% 96,88% 96,88% 95,88%

181 new 98,46% 99,26% 99,26% 98,26%

Curr 0,24%

1-30

31-60

61-90

91-120

121-150

151-180

180+

Flo

w R

ate

Loss

Fact

or

PLLP - Loss Factor – Example

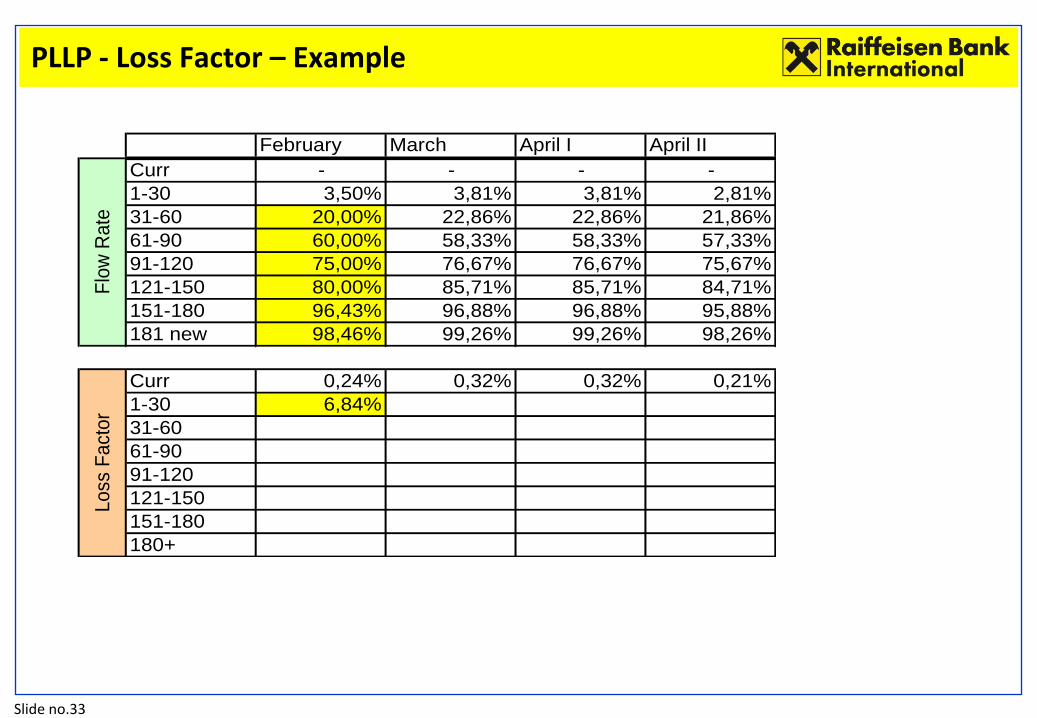

Slide no.33

February March April I April II

Curr - - - -

1-30 3,50% 3,81% 3,81% 2,81%

31-60 20,00% 22,86% 22,86% 21,86%

61-90 60,00% 58,33% 58,33% 57,33%

91-120 75,00% 76,67% 76,67% 75,67%

121-150 80,00% 85,71% 85,71% 84,71%

151-180 96,43% 96,88% 96,88% 95,88%

181 new 98,46% 99,26% 99,26% 98,26%

Curr 0,24% 0,32% 0,32% 0,21%

1-30 6,84%

31-60

61-90

91-120

121-150

151-180

180+

Flo

w R

ate

Loss

Fact

or

PLLP - Loss Factor – Example

Slide no.34

February March April I April II

Curr - - - -

1-30 3,50% 3,81% 3,81% 2,81%

31-60 20,00% 22,86% 22,86% 21,86%

61-90 60,00% 58,33% 58,33% 57,33%

91-120 75,00% 76,67% 76,67% 75,67%

121-150 80,00% 85,71% 85,71% 84,71%

151-180 96,43% 96,88% 96,88% 95,88%

181 new 98,46% 99,26% 99,26% 98,26%

Curr 0,24% 0,32% 0,32% 0,21%

1-30 6,84% 8,43% 8,43% 7,57%

31-60 34,18%

61-90

91-120

121-150

151-180

180+

Flo

w R

ate

Loss

Fact

or

PLLP - Loss Factor – Example

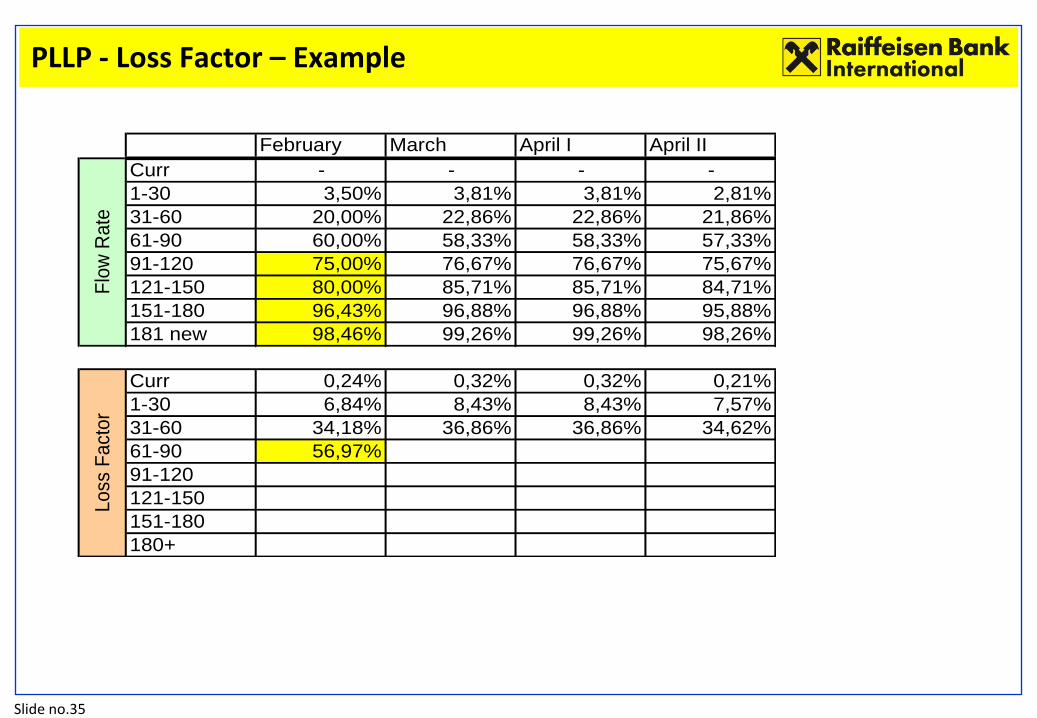

Slide no.35

February March April I April II

Curr - - - -

1-30 3,50% 3,81% 3,81% 2,81%

31-60 20,00% 22,86% 22,86% 21,86%

61-90 60,00% 58,33% 58,33% 57,33%

91-120 75,00% 76,67% 76,67% 75,67%

121-150 80,00% 85,71% 85,71% 84,71%

151-180 96,43% 96,88% 96,88% 95,88%

181 new 98,46% 99,26% 99,26% 98,26%

Curr 0,24% 0,32% 0,32% 0,21%

1-30 6,84% 8,43% 8,43% 7,57%

31-60 34,18% 36,86% 36,86% 34,62%

61-90 56,97%

91-120

121-150

151-180

180+

Flo

w R

ate

Loss

Fact

or

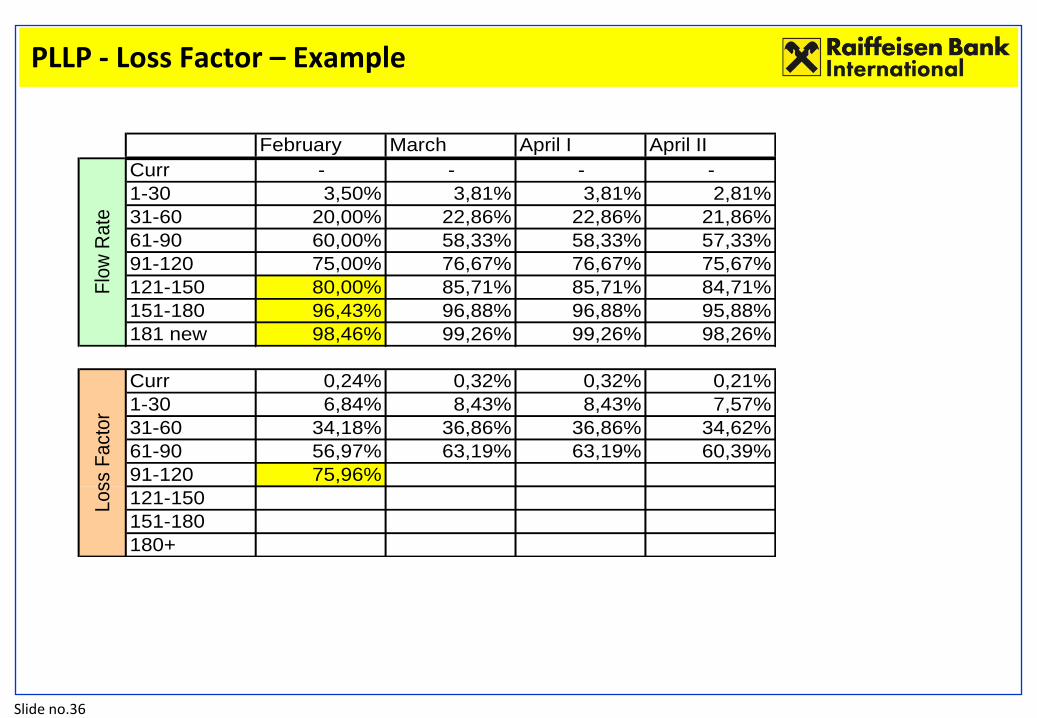

PLLP - Loss Factor – Example

Slide no.36

February March April I April II

Curr - - - -

1-30 3,50% 3,81% 3,81% 2,81%

31-60 20,00% 22,86% 22,86% 21,86%

61-90 60,00% 58,33% 58,33% 57,33%

91-120 75,00% 76,67% 76,67% 75,67%

121-150 80,00% 85,71% 85,71% 84,71%

151-180 96,43% 96,88% 96,88% 95,88%

181 new 98,46% 99,26% 99,26% 98,26%

Curr 0,24% 0,32% 0,32% 0,21%

1-30 6,84% 8,43% 8,43% 7,57%

31-60 34,18% 36,86% 36,86% 34,62%

61-90 56,97% 63,19% 63,19% 60,39%

91-120 75,96%

121-150

151-180

180+

Flo

w R

ate

Loss

Fact

or

PLLP - Loss Factor – Example

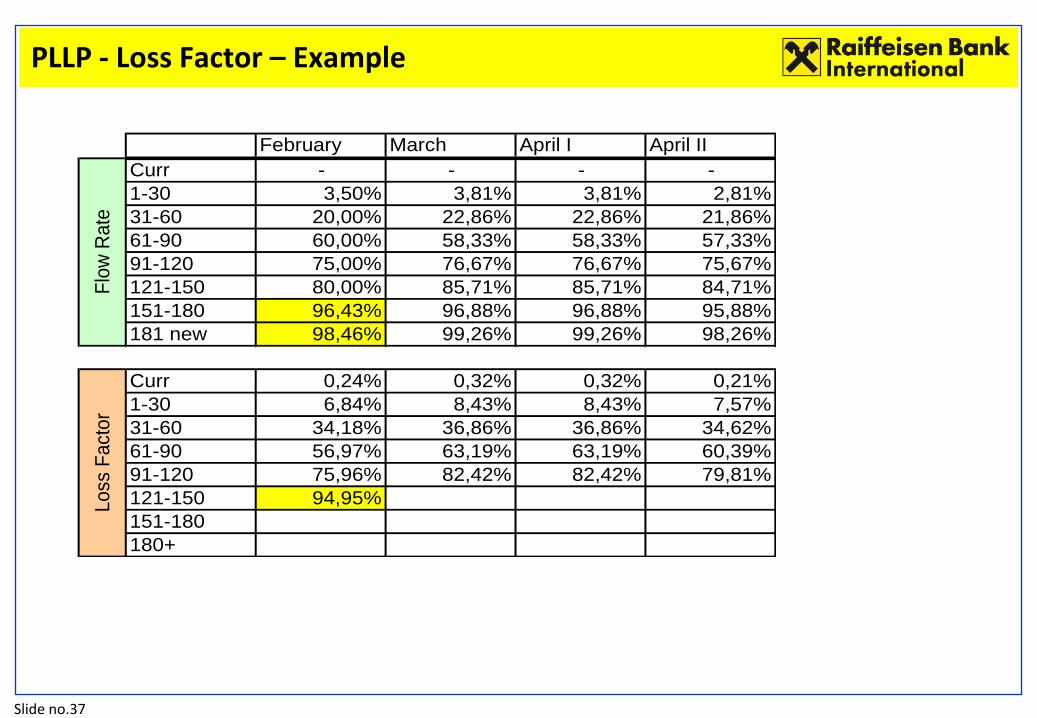

Slide no.37

February March April I April II

Curr - - - -

1-30 3,50% 3,81% 3,81% 2,81%

31-60 20,00% 22,86% 22,86% 21,86%

61-90 60,00% 58,33% 58,33% 57,33%

91-120 75,00% 76,67% 76,67% 75,67%

121-150 80,00% 85,71% 85,71% 84,71%

151-180 96,43% 96,88% 96,88% 95,88%

181 new 98,46% 99,26% 99,26% 98,26%

Curr 0,24% 0,32% 0,32% 0,21%

1-30 6,84% 8,43% 8,43% 7,57%

31-60 34,18% 36,86% 36,86% 34,62%

61-90 56,97% 63,19% 63,19% 60,39%

91-120 75,96% 82,42% 82,42% 79,81%

121-150 94,95%

151-180

180+

Flo

w R

ate

Loss

Fact

or

PLLP - Loss Factor – Example

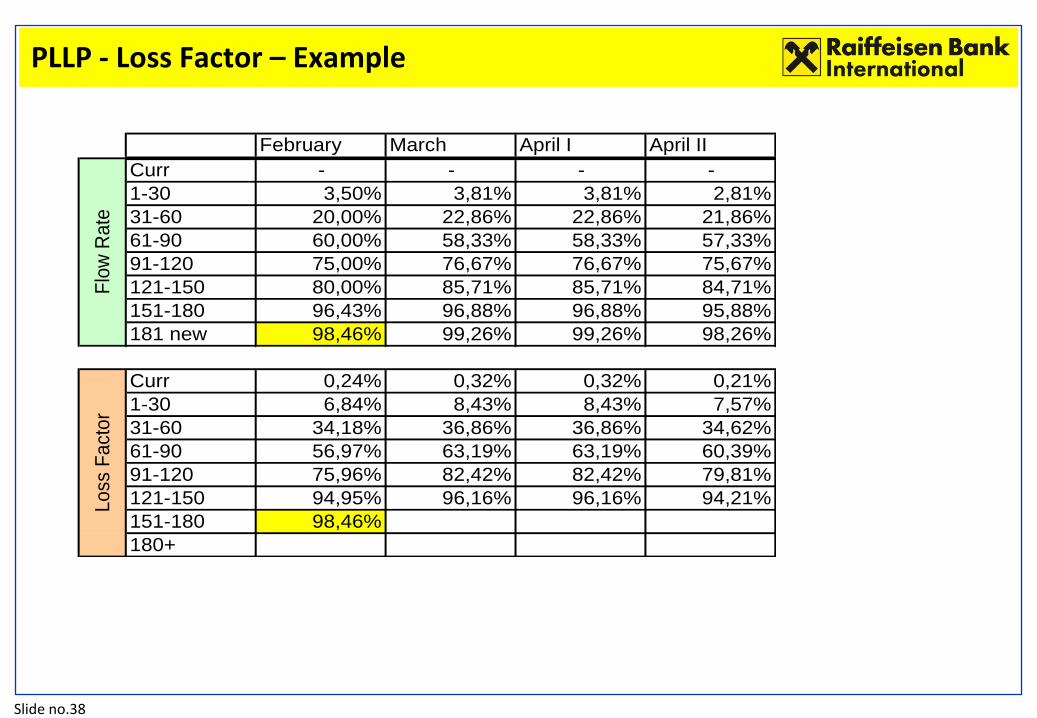

Slide no.38

February March April I April II

Curr - - - -

1-30 3,50% 3,81% 3,81% 2,81%

31-60 20,00% 22,86% 22,86% 21,86%

61-90 60,00% 58,33% 58,33% 57,33%

91-120 75,00% 76,67% 76,67% 75,67%

121-150 80,00% 85,71% 85,71% 84,71%

151-180 96,43% 96,88% 96,88% 95,88%

181 new 98,46% 99,26% 99,26% 98,26%

Curr 0,24% 0,32% 0,32% 0,21%

1-30 6,84% 8,43% 8,43% 7,57%

31-60 34,18% 36,86% 36,86% 34,62%

61-90 56,97% 63,19% 63,19% 60,39%

91-120 75,96% 82,42% 82,42% 79,81%

121-150 94,95% 96,16% 96,16% 94,21%

151-180 98,46%

180+

Flo

w R

ate

Loss

Fact

or

PLLP - Loss Factor – Example

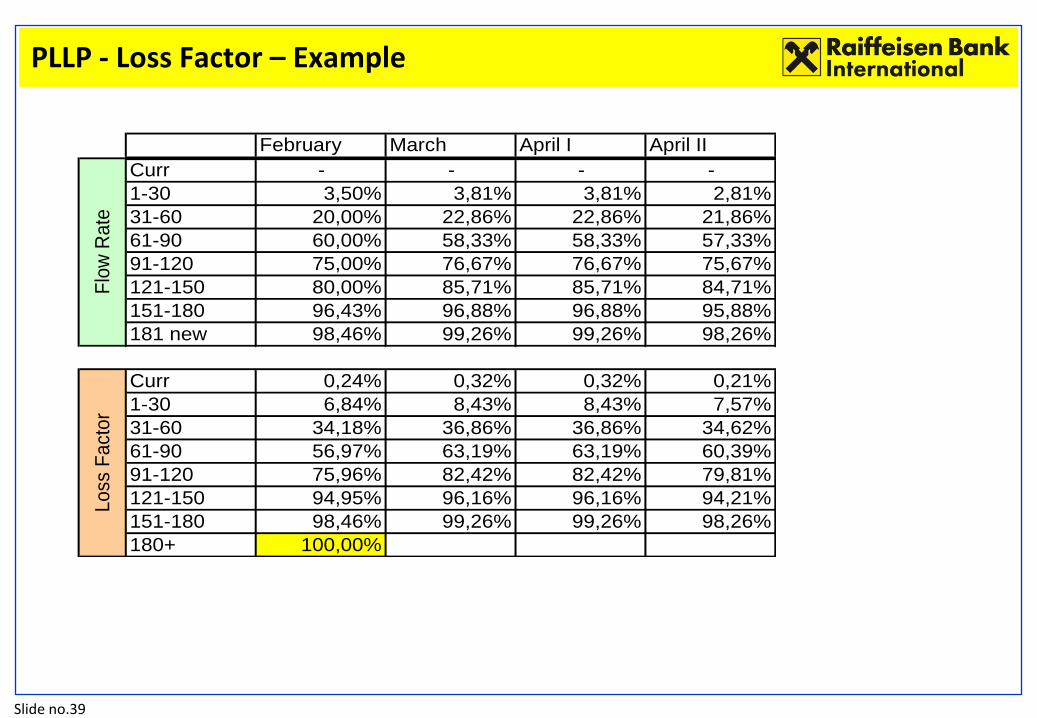

Slide no.39

February March April I April II

Curr - - - -

1-30 3,50% 3,81% 3,81% 2,81%

31-60 20,00% 22,86% 22,86% 21,86%

61-90 60,00% 58,33% 58,33% 57,33%

91-120 75,00% 76,67% 76,67% 75,67%

121-150 80,00% 85,71% 85,71% 84,71%

151-180 96,43% 96,88% 96,88% 95,88%

181 new 98,46% 99,26% 99,26% 98,26%

Curr 0,24% 0,32% 0,32% 0,21%

1-30 6,84% 8,43% 8,43% 7,57%

31-60 34,18% 36,86% 36,86% 34,62%

61-90 56,97% 63,19% 63,19% 60,39%

91-120 75,96% 82,42% 82,42% 79,81%

121-150 94,95% 96,16% 96,16% 94,21%

151-180 98,46% 99,26% 99,26% 98,26%

180+ 100,00%

Flo

w R

ate

Loss

Fact

or

PLLP - Loss Factor – Example

Slide no.40

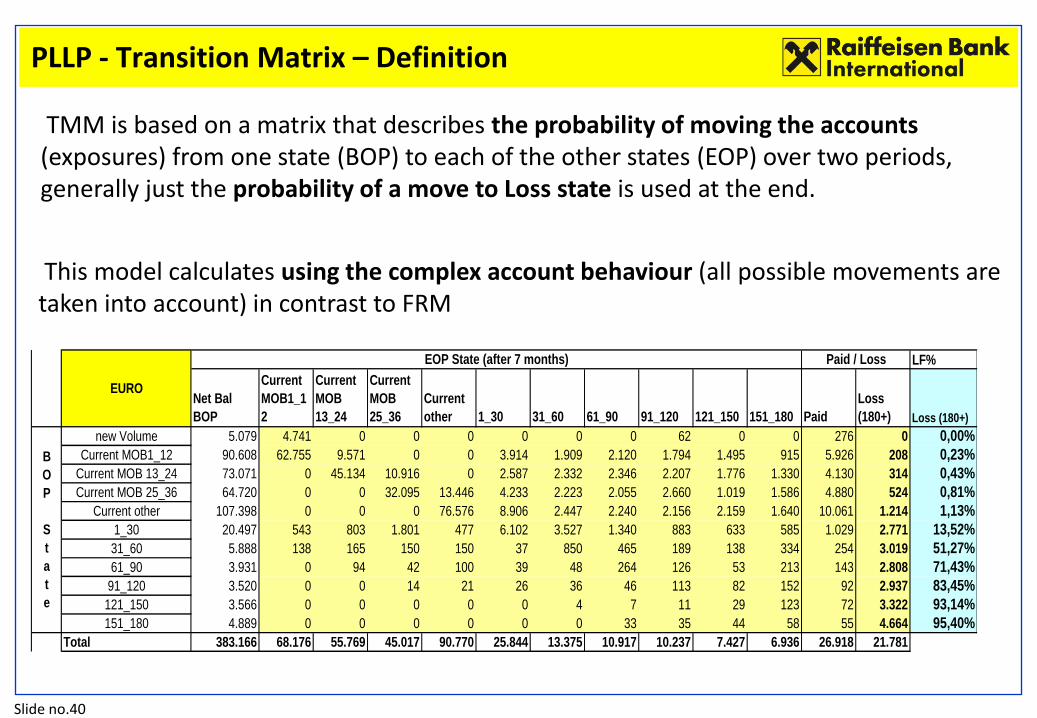

TMM is based on a matrix that describes the probability of moving the accounts (exposures) from one state (BOP) to each of the other states (EOP) over two periods, generally just the probability of a move to Loss state is used at the end.

This model calculates using the complex account behaviour (all possible movements are taken into account) in contrast to FRM

LF%

Net Bal

BOP

Current

MOB1_1

2

Current

MOB

13_24

Current

MOB

25_36

Current

other 1_30 31_60 61_90 91_120 121_150 151_180 Paid

Loss

(180+) Loss (180+)

new Volume 5.079 4.741 0 0 0 0 0 0 62 0 0 276 0 0,00%

Current MOB1_12 90.608 62.755 9.571 0 0 3.914 1.909 2.120 1.794 1.495 915 5.926 208 0,23%

Current MOB 13_24 73.071 0 45.134 10.916 0 2.587 2.332 2.346 2.207 1.776 1.330 4.130 314 0,43%

Current MOB 25_36 64.720 0 0 32.095 13.446 4.233 2.223 2.055 2.660 1.019 1.586 4.880 524 0,81%

Current other 107.398 0 0 0 76.576 8.906 2.447 2.240 2.156 2.159 1.640 10.061 1.214 1,13%

1_30 20.497 543 803 1.801 477 6.102 3.527 1.340 883 633 585 1.029 2.771 13,52%

31_60 5.888 138 165 150 150 37 850 465 189 138 334 254 3.019 51,27%

61_90 3.931 0 94 42 100 39 48 264 126 53 213 143 2.808 71,43%

91_120 3.520 0 0 14 21 26 36 46 113 82 152 92 2.937 83,45%

121_150 3.566 0 0 0 0 0 4 7 11 29 123 72 3.322 93,14%

151_180 4.889 0 0 0 0 0 0 33 35 44 58 55 4.664 95,40%

Total 383.166 68.176 55.769 45.017 90.770 25.844 13.375 10.917 10.237 7.427 6.936 26.918 21.781

Paid / Loss

B

O

P

S

t

a

t

e

EURO

EOP State (after 7 months)

PLLP - Transition Matrix – Definition

Slide no.41

Agenda

1 Types of Loan Loss Provisions in the Retail Segment of RBI

2 Individual Loan Loss Provisions (ILLP) - Overview

3 ILLP – Treatment of Restructured Accounts

4 ILLP – Calculation steps

5 Portfolio-based Loan Loss Provisions (PLLP) - Overview

6 PLLP – Flow Rates, Loss Factors, Transition Matrix – Definitions and Examples

7 PLLP – Gross Provisions, Recovery Models, Net Provisions - Calculations

8 Risk Costs – Definitions and Examples

9 Experience from the roll-out across the RBI Group

10 Future Plans for Loan Loss Provisioning Methodology in RBI Retail Portfolio

Slide no.42

February March

Curr 105.000 110.000

1-30 3.500 4.000

31-60 600 800

61-90 300 350

91-120 210 230

121-150 160 180

151-180 135 155

181 new 128 134

180+ 3.120 3.248

Curr 0,24% 0,32%

1-30 6,84% 8,43%

31-60 34,18% 36,86%

61-90 56,97% 63,19%

91-120 75,96% 82,42%

121-150 94,95% 96,16%

151-180 98,46% 99,26%

180+ 100,00% 100,00%

Bala

nce

Loss

Fact

or

February March

Curr

1-30

31-60

61-90

91-120

121-150

151-180

181 new

180+

Exp

ect

ed L

oss

Pro

visi

on

s

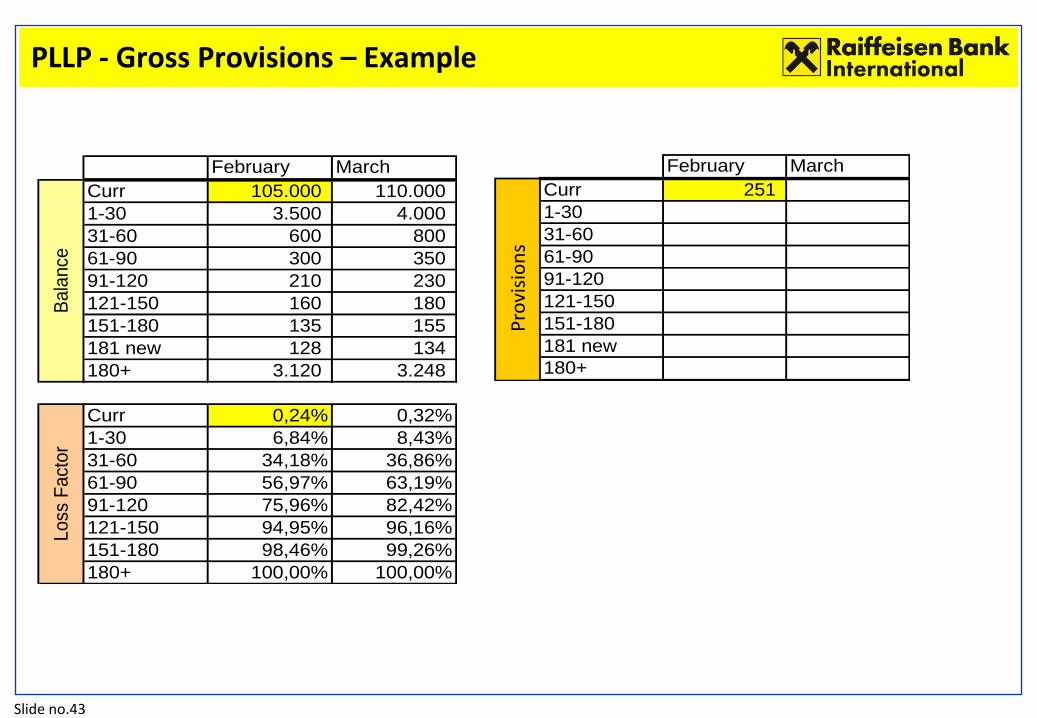

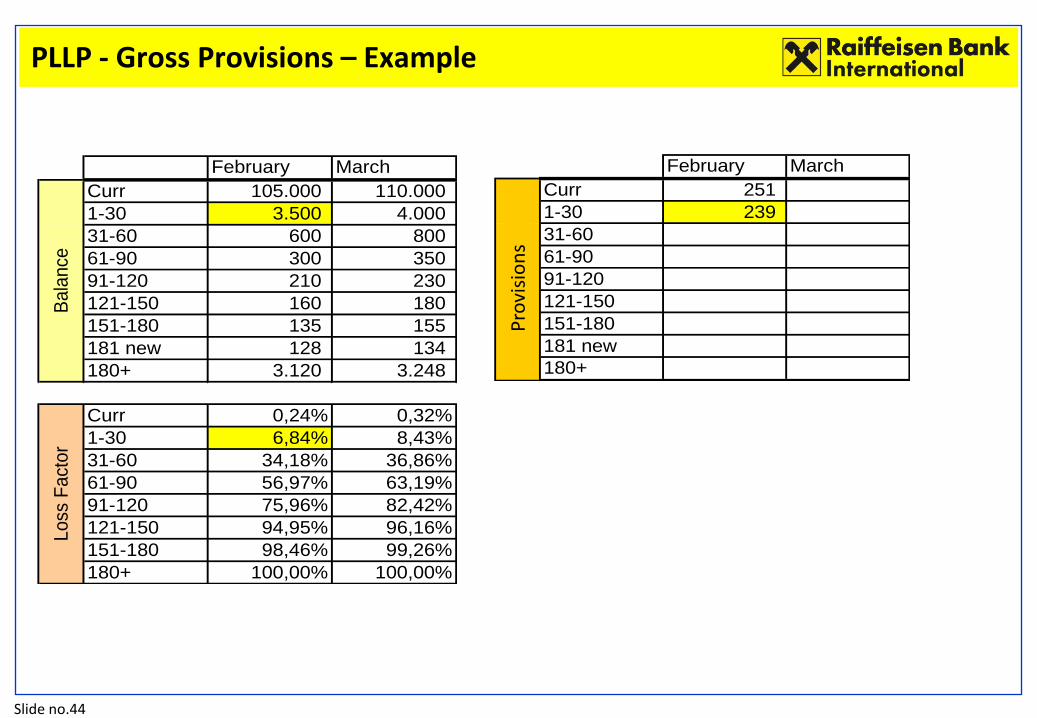

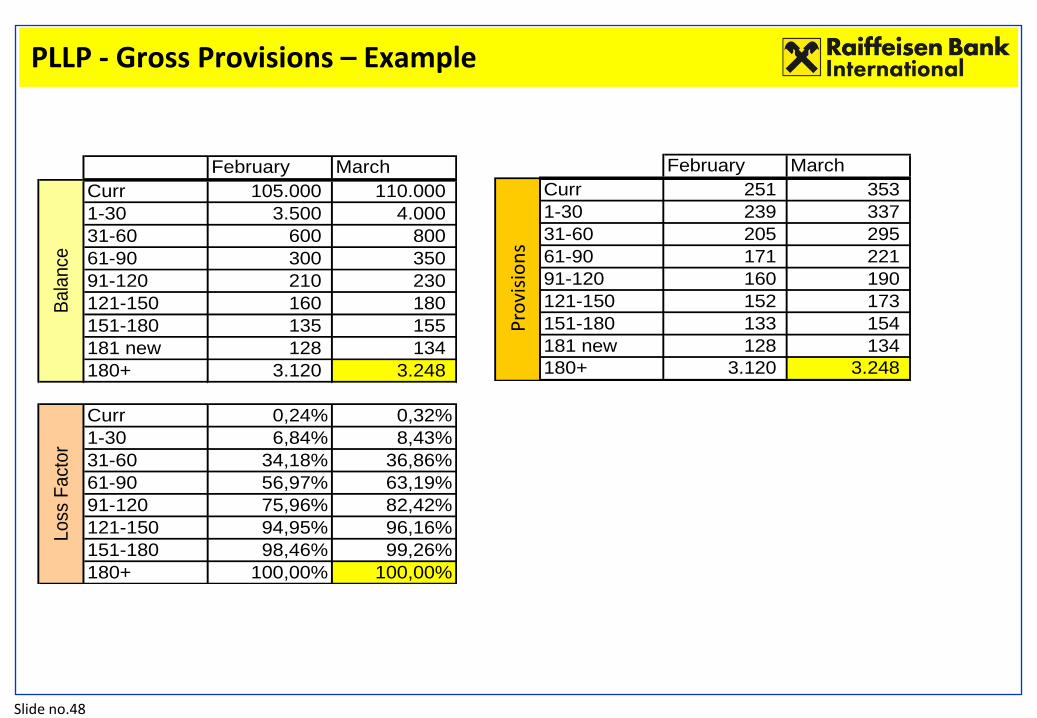

• To calculate the Gross provisions, the probabilities for each state is multiplied with the respective balances, which will give the gross provisions amounts for each state

PLLP - Gross Provisions – Definition

Slide no.43

February March

Curr 105.000 110.000

1-30 3.500 4.000

31-60 600 800

61-90 300 350

91-120 210 230

121-150 160 180

151-180 135 155

181 new 128 134

180+ 3.120 3.248

Curr 0,24% 0,32%

1-30 6,84% 8,43%

31-60 34,18% 36,86%

61-90 56,97% 63,19%

91-120 75,96% 82,42%

121-150 94,95% 96,16%

151-180 98,46% 99,26%

180+ 100,00% 100,00%

Bala

nce

Loss

Fact

or

February March

Curr 251

1-30

31-60

61-90

91-120

121-150

151-180

181 new

180+

Exp

ect

ed L

oss

Pro

visi

on

s

PLLP - Gross Provisions – Example

Slide no.44

February March

Curr 105.000 110.000

1-30 3.500 4.000

31-60 600 800

61-90 300 350

91-120 210 230

121-150 160 180

151-180 135 155

181 new 128 134

180+ 3.120 3.248

Curr 0,24% 0,32%

1-30 6,84% 8,43%

31-60 34,18% 36,86%

61-90 56,97% 63,19%

91-120 75,96% 82,42%

121-150 94,95% 96,16%

151-180 98,46% 99,26%

180+ 100,00% 100,00%

Bala

nce

Loss

Fact

or

February March

Curr 251

1-30 239

31-60

61-90

91-120

121-150

151-180

181 new

180+

Exp

ect

ed L

oss

Pro

visi

on

s

PLLP - Gross Provisions – Example

Slide no.45

February March

Curr 105.000 110.000

1-30 3.500 4.000

31-60 600 800

61-90 300 350

91-120 210 230

121-150 160 180

151-180 135 155

181 new 128 134

180+ 3.120 3.248

Curr 0,24% 0,32%

1-30 6,84% 8,43%

31-60 34,18% 36,86%

61-90 56,97% 63,19%

91-120 75,96% 82,42%

121-150 94,95% 96,16%

151-180 98,46% 99,26%

180+ 100,00% 100,00%

Bala

nce

Loss

Fact

or

February March

Curr 251

1-30 239

31-60 205

61-90

91-120

121-150

151-180

181 new

180+

Exp

ect

ed L

oss

Pro

visi

on

s

PLLP - Gross Provisions – Example

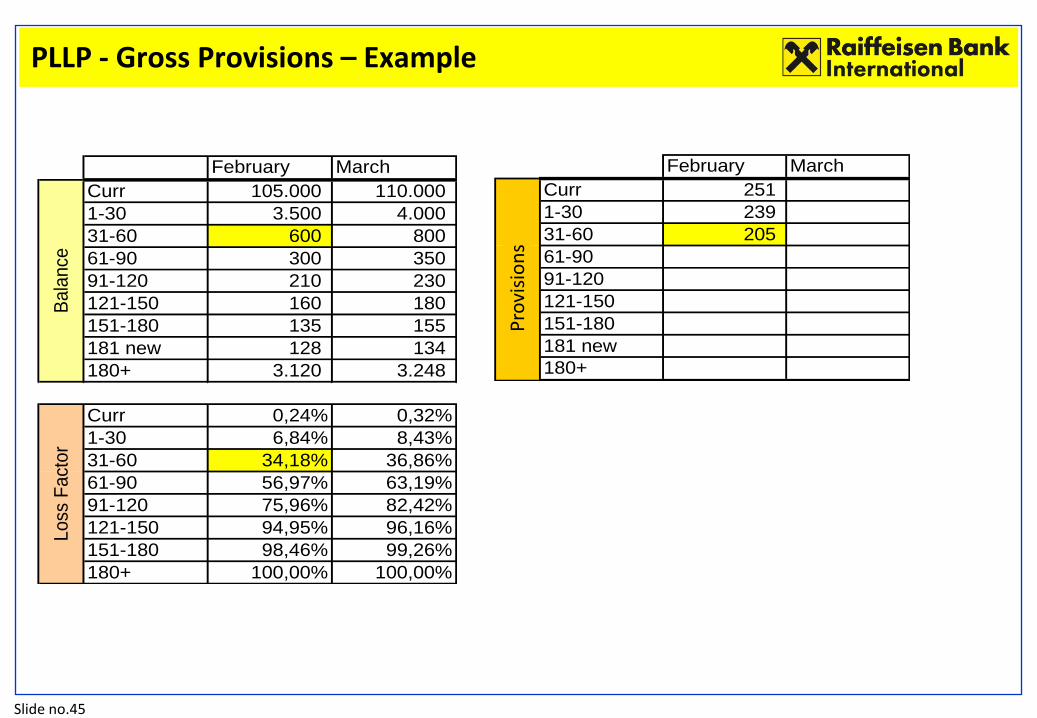

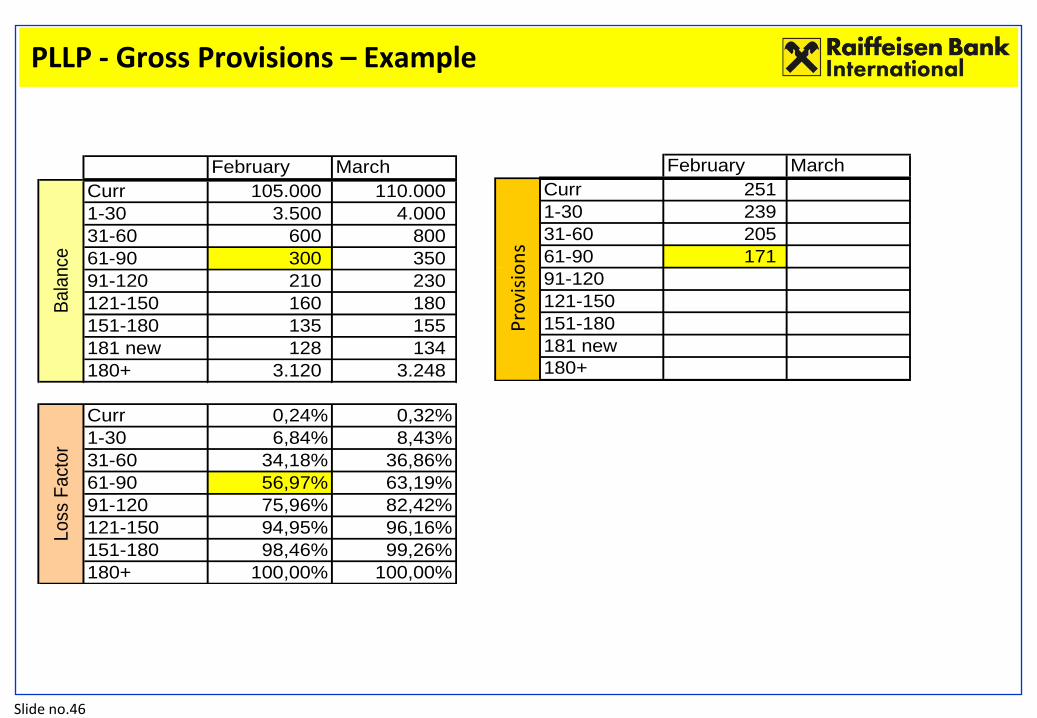

Slide no.46

February March

Curr 105.000 110.000

1-30 3.500 4.000

31-60 600 800

61-90 300 350

91-120 210 230

121-150 160 180

151-180 135 155

181 new 128 134

180+ 3.120 3.248

Curr 0,24% 0,32%

1-30 6,84% 8,43%

31-60 34,18% 36,86%

61-90 56,97% 63,19%

91-120 75,96% 82,42%

121-150 94,95% 96,16%

151-180 98,46% 99,26%

180+ 100,00% 100,00%

Bala

nce

Loss

Fact

or

February March

Curr 251

1-30 239

31-60 205

61-90 171

91-120

121-150

151-180

181 new

180+

Exp

ect

ed L

oss

Pro

visi

on

s

PLLP - Gross Provisions – Example

Slide no.47

February March

Curr 105.000 110.000

1-30 3.500 4.000

31-60 600 800

61-90 300 350

91-120 210 230

121-150 160 180

151-180 135 155

181 new 128 134

180+ 3.120 3.248

Curr 0,24% 0,32%

1-30 6,84% 8,43%

31-60 34,18% 36,86%

61-90 56,97% 63,19%

91-120 75,96% 82,42%

121-150 94,95% 96,16%

151-180 98,46% 99,26%

180+ 100,00% 100,00%

Bala

nce

Loss

Fact

or

February March

Curr 251

1-30 239

31-60 205

61-90 171

91-120 160

121-150

151-180

181 new

180+

Exp

ect

ed L

oss

Pro

visi

on

s

PLLP - Gross Provisions – Example

Slide no.48

February March

Curr 105.000 110.000

1-30 3.500 4.000

31-60 600 800

61-90 300 350

91-120 210 230

121-150 160 180

151-180 135 155

181 new 128 134

180+ 3.120 3.248

Curr 0,24% 0,32%

1-30 6,84% 8,43%

31-60 34,18% 36,86%

61-90 56,97% 63,19%

91-120 75,96% 82,42%

121-150 94,95% 96,16%

151-180 98,46% 99,26%

180+ 100,00% 100,00%

Bala

nce

Loss

Fact

or

February March

Curr 251 353

1-30 239 337

31-60 205 295

61-90 171 221

91-120 160 190

121-150 152 173

151-180 133 154

181 new 128 134

180+ 3.120 3.248

Exp

ect

ed L

oss

Pro

visi

on

s

PLLP - Gross Provisions – Example

Slide no.49

Accounts that went into Loss status (180+ dpd) can be partly (or fully) recovered in the

future as an outcome of internal collections or debt sales

All payments that came after an account reached Loss status are considered recoveries

Recovery rate can be calculated either by using Vintage recovery model (strongly

recommended) or Simple recovery model

Irrespective of the model used the Debt sale accounts must be excluded from the

recovery modeling data (only exception is if it is a forward flow type of deal)

PLLP - Recovery Models - Overview

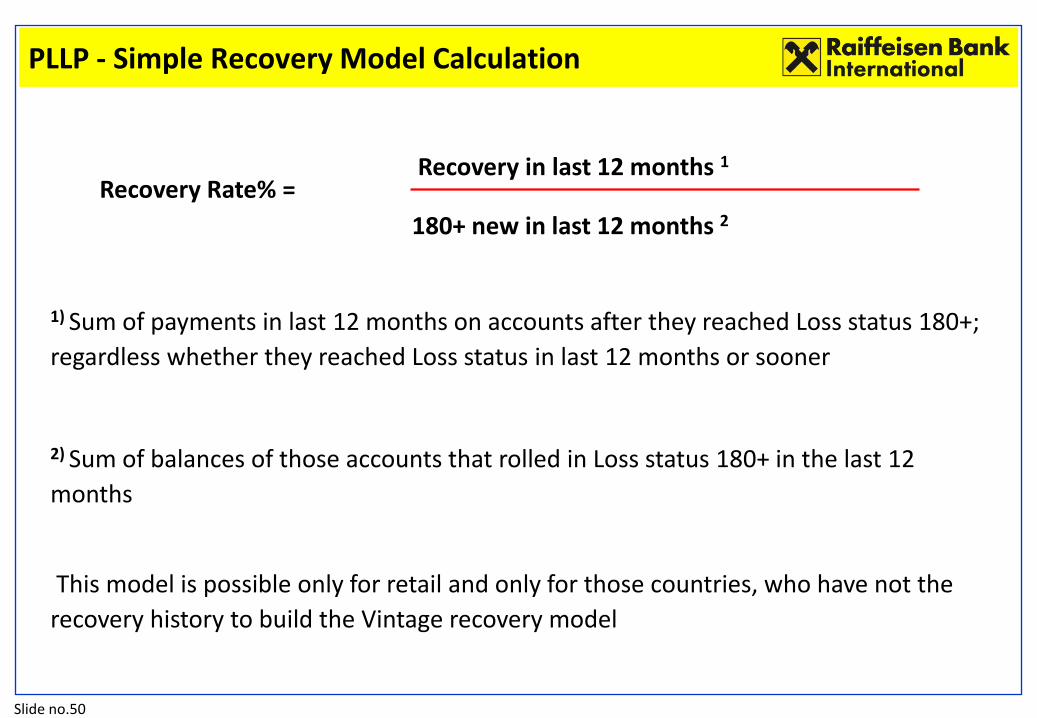

Slide no.50

Recovery in last 12 months 1

180+ new in last 12 months 2

Recovery Rate% =

1) Sum of payments in last 12 months on accounts after they reached Loss status 180+;

regardless whether they reached Loss status in last 12 months or sooner

2) Sum of balances of those accounts that rolled in Loss status 180+ in the last 12

months

This model is possible only for retail and only for those countries, who have not the

recovery history to build the Vintage recovery model

PLLP - Simple Recovery Model Calculation

Slide no.51

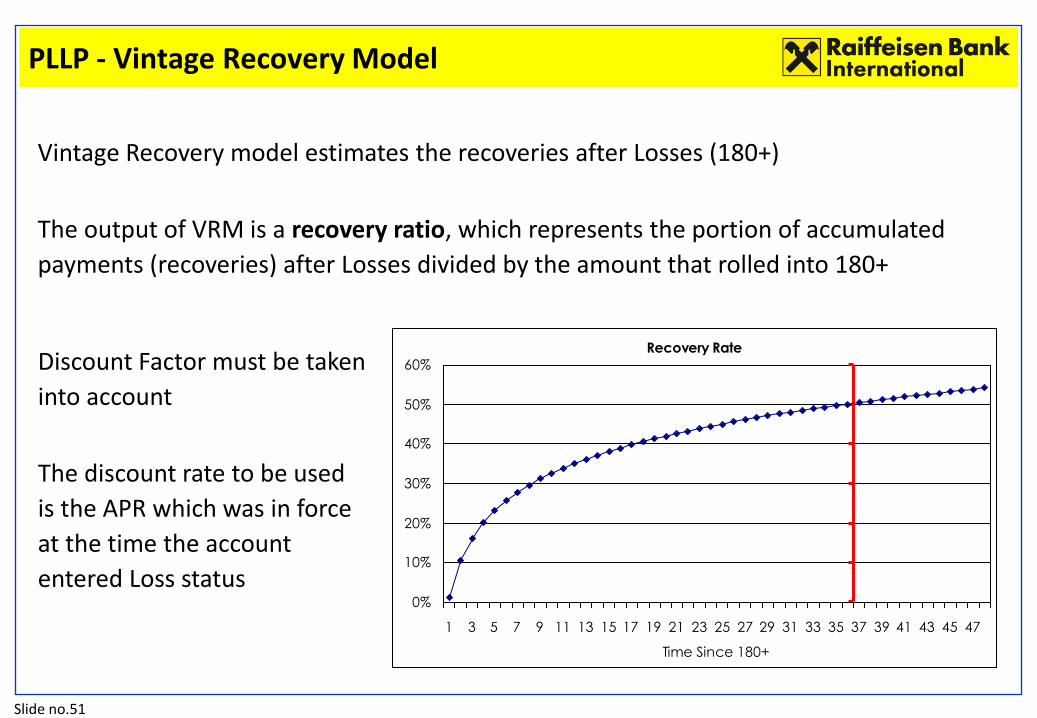

Vintage Recovery model estimates the recoveries after Losses (180+)

The output of VRM is a recovery ratio, which represents the portion of accumulated

payments (recoveries) after Losses divided by the amount that rolled into 180+

PLLP - Vintage Recovery Model

Recovery Rate

0%

10%

20%

30%

40%

50%

60%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47

Time Since 180+

Discount Factor must be taken

into account

The discount rate to be used

is the APR which was in force

at the time the account

entered Loss status

Slide no.52

A1

B

C

A2 A3

D

Months since write-off

Write off

date

Write-off

amount 1 2 3 4 5 6 7 8

Month, when account

rolled into 180+

Account balance at roll to 180+; see also comments to mortgage ptf.

Loss date Amount

at Loss

Months since Loss

PLLP - Vintage Recovery Rate Calculation

Slide no.53

February March

Curr 251 353

1-30 239 337

31-60 205 295

61-90 171 221

91-120 160 190

121-150 152 173

151-180 133 154

181 new 128 134

180+ 3.120 3.248

Provisions BS 4.559 5.105

Exp

ect

ed L

oss

Pro

visi

on

s

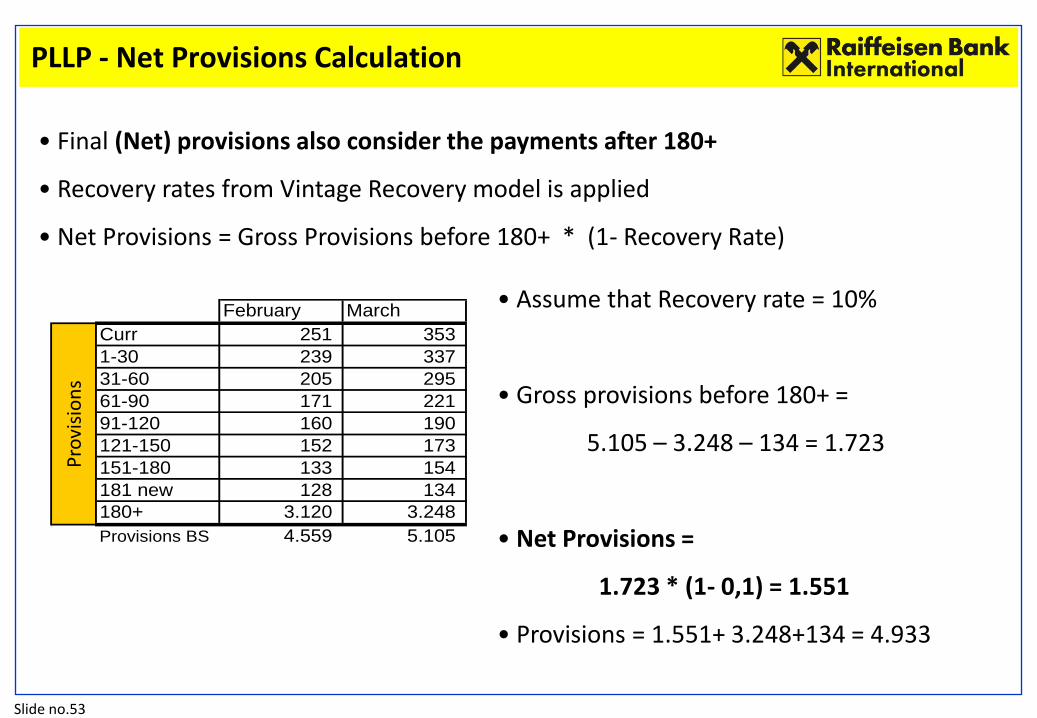

• Final (Net) provisions also consider the payments after 180+

• Recovery rates from Vintage Recovery model is applied

• Net Provisions = Gross Provisions before 180+ * (1- Recovery Rate)

• Assume that Recovery rate = 10%

• Gross provisions before 180+ =

5.105 – 3.248 – 134 = 1.723

• Net Provisions =

1.723 * (1- 0,1) = 1.551

• Provisions = 1.551+ 3.248+134 = 4.933

PLLP - Net Provisions Calculation

Slide no.54

Agenda

1 Types of Loan Loss Provisions in the Retail Segment of RBI

2 Individual Loan Loss Provisions (ILLP) - Overview

3 ILLP – Treatment of Restructured Accounts

4 ILLP – Calculation steps

5 Portfolio-based Loan Loss Provisions (PLLP) - Overview

6 PLLP – Flow Rates, Loss Factors, Transition Matrix – Definitions and Examples

7 PLLP – Gross Provisions, Recovery Models, Net Provisions - Calculations

8 Risk Costs – Definitions and Examples

9 Experience from the roll-out across the RBI Group

10 Future Plans for Loan Loss Provisioning Methodology in RBI Retail Portfolio

Slide no.55

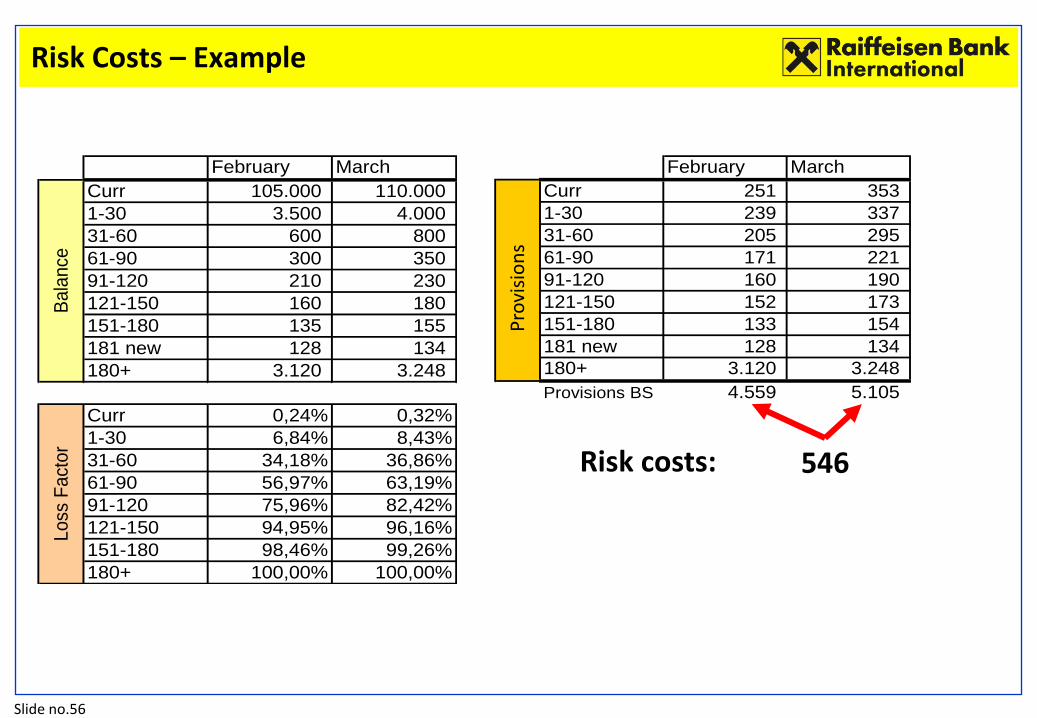

Risk costs =

+ EOP Provisions

– BOP Provisions

+ Usage (Net Write-offs)

BOP – Beginning of Period EOP – End of Period

• has an impact on the Income statement (P&L)

• also called Provisioning for Impairment Losses (P/L) in some financial reports

• shown as the sum of “standard risk costs” and “risk results” (Controlling)

• sum of Allocation, Release, Direct Write downs (Accounting)

• are calculated based on the result of the formula bellow to built new provisions in B/S or to release provisions no longer required

15

40

10

3 3

5

30

0

10

20

30

40

50

60

Provisions

BOP

Allocation* Direct Write

down*

Usage (Net

Write Off)

Release* Provisions

EOP

Risk Costs – Definition

Slide no.56

February March

Curr 105.000 110.000

1-30 3.500 4.000

31-60 600 800

61-90 300 350

91-120 210 230

121-150 160 180

151-180 135 155

181 new 128 134

180+ 3.120 3.248

Curr 0,24% 0,32%

1-30 6,84% 8,43%

31-60 34,18% 36,86%

61-90 56,97% 63,19%

91-120 75,96% 82,42%

121-150 94,95% 96,16%

151-180 98,46% 99,26%

180+ 100,00% 100,00%

Bala

nce

Loss

Fact

or

February March

Curr 251 353

1-30 239 337

31-60 205 295

61-90 171 221

91-120 160 190

121-150 152 173

151-180 133 154

181 new 128 134

180+ 3.120 3.248

Provisions BS 4.559 5.105

Exp

ect

ed L

oss

546 Risk costs:

Pro

visi

on

s

Risk Costs – Example

Slide no.57

Agenda

1 Types of Loan Loss Provisions in the Retail Segment of RBI

2 Individual Loan Loss Provisions (ILLP) - Overview

3 ILLP – Treatment of Restructured Accounts

4 ILLP – Calculation steps

5 Portfolio-based Loan Loss Provisions (PLLP) - Overview

6 PLLP – Flow Rates, Loss Factors, Transition Matrix – Definitions and Examples

7 PLLP – Gross Provisions, Recovery Models, Net Provisions - Calculations

8 Risk Costs – Definitions and Examples

9 Experience from the roll-out across the RBI Group

10 Future Plans for Loan Loss Provisioning Methodology in RBI Retail Portfolio

Slide no.58

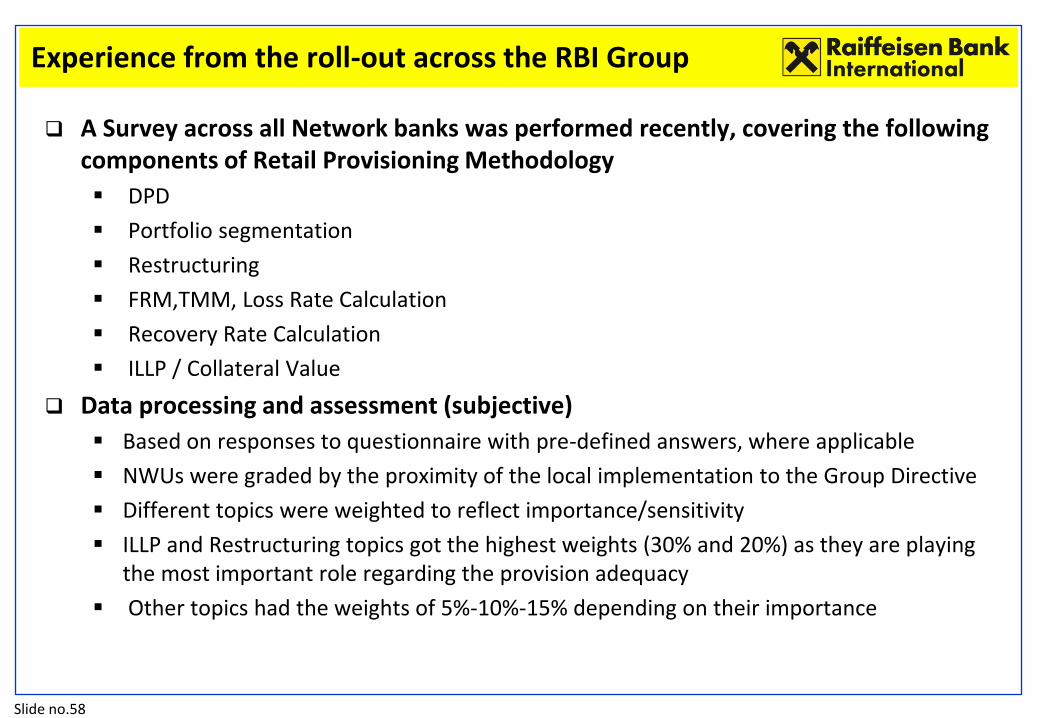

Experience from the roll-out across the RBI Group

A Survey across all Network banks was performed recently, covering the following components of Retail Provisioning Methodology

DPD

Portfolio segmentation

Restructuring

FRM,TMM, Loss Rate Calculation

Recovery Rate Calculation

ILLP / Collateral Value

Data processing and assessment (subjective)

Based on responses to questionnaire with pre-defined answers, where applicable

NWUs were graded by the proximity of the local implementation to the Group Directive

Different topics were weighted to reflect importance/sensitivity

ILLP and Restructuring topics got the highest weights (30% and 20%) as they are playing the most important role regarding the provision adequacy

Other topics had the weights of 5%-10%-15% depending on their importance

Slide no.59

Experience from the roll-out across the RBI Group

Private Individuals

NWBDPD

Portfolio

segmentationRestructuring

Loss rate

calculation

Recovery rate

calculationILLP (WCV) Overall

1 8 9 9 1 0 9 8 8 .9

2 1 0 9 1 0 9 8 1 0 9 .4

3 9 9 7 9 9 5 7 .1

4 8 0 0 3 0 4 3 .3

5 9 1 0 3 6 7 7 6 .4

6 6 8 0 7 6 6 5 .0

7 9 1 0 6 9 6 7 7 .3

8 9 9 3 7 8 8 6 .9

9 1 0 1 0 7 1 0 7 8 7 .8

10 1 0 9 9 8 7 6 7 .5

11 9 9 6 8 8 8 7 .9

12 1 0 9 4 7 0 8 6 .2

13 1 0 1 0 3 4 6 7 6 .1

14 9 9 6 7 8 7 7 .2

15 - - - - - - -

ConservatismNWB PI

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

MicroSME

NWBDPD

Portfolio

segmentationRestructuring

Loss rate

calculation

Recovery rate

calculationILLP (WCV) Overall

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

ConservatismNWB Micro

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Slide no.60

Experience from the roll-out across the RBI Group

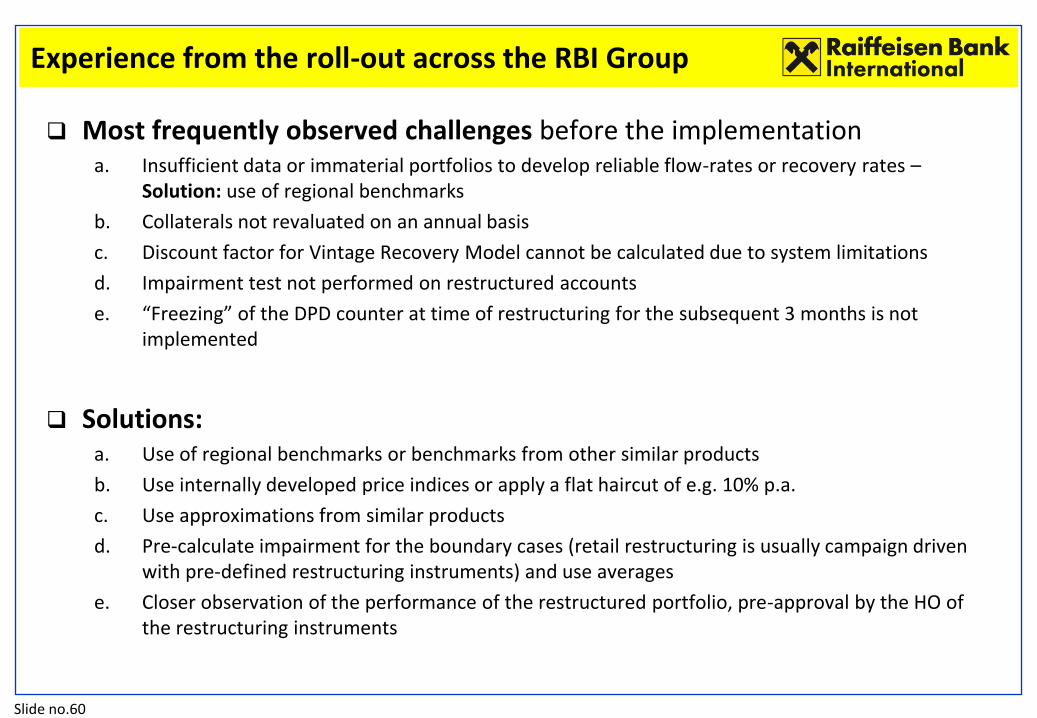

Most frequently observed challenges before the implementation a. Insufficient data or immaterial portfolios to develop reliable flow-rates or recovery rates –

Solution: use of regional benchmarks

b. Collaterals not revaluated on an annual basis

c. Discount factor for Vintage Recovery Model cannot be calculated due to system limitations

d. Impairment test not performed on restructured accounts

e. “Freezing” of the DPD counter at time of restructuring for the subsequent 3 months is not implemented

Solutions: a. Use of regional benchmarks or benchmarks from other similar products

b. Use internally developed price indices or apply a flat haircut of e.g. 10% p.a.

c. Use approximations from similar products

d. Pre-calculate impairment for the boundary cases (retail restructuring is usually campaign driven with pre-defined restructuring instruments) and use averages

e. Closer observation of the performance of the restructured portfolio, pre-approval by the HO of the restructuring instruments

Slide no.61

Agenda

1 Types of Loan Loss Provisions in the Retail Segment of RBI

2 Individual Loan Loss Provisions (ILLP) - Overview

3 ILLP – Treatment of Restructured Accounts

4 ILLP – Calculation steps

5 Portfolio-based Loan Loss Provisions (PLLP) - Overview

6 PLLP – Flow Rates, Loss Factors, Transition Matrix – Definitions and Examples

7 PLLP – Gross Provisions, Recovery Models, Net Provisions - Calculations

8 Risk Costs – Definitions and Examples

9 Experience from the roll-out across the RBI Group

10 Future Plans for Loan Loss Provisioning Methodology in RBI Retail Portfolio

Slide no.62

Possible (Near) Future Approaches

Different approaches for the network units depending on available setup (“hierarchy of provisioning methodologies”): Provisioning based on Basel 2/3 framework (if available):

“Before” loss event: Portfolio-based impairments

PLLP = Exposure * PD * LGD' * LIP

“After” loss event: Individual impairments:

ILLP = Exposure * BEEL

Provisioning based on “days-past-due grid”:

Transition matrix model

Flow rate model

1

2

Important: Reconciliation of approaches by benchmarking and backtesting

LGD’ without down-turn adjustment. BEEL = Best estimate of expected loss

Slide no.63

MIND STRETCHERS

Slide no.64

Mind stretchers

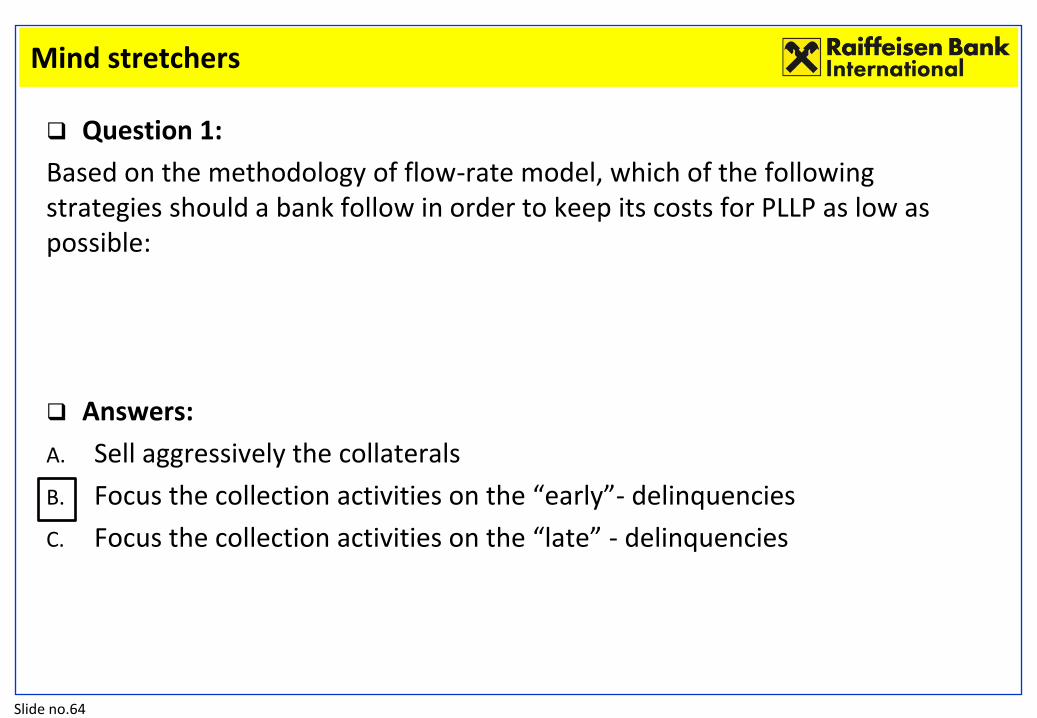

Question 1:

Based on the methodology of flow-rate model, which of the following strategies should a bank follow in order to keep its costs for PLLP as low as possible:

Answers:

A. Sell aggressively the collaterals

B. Focus the collection activities on the “early”- delinquencies

C. Focus the collection activities on the “late” - delinquencies

Slide no.65

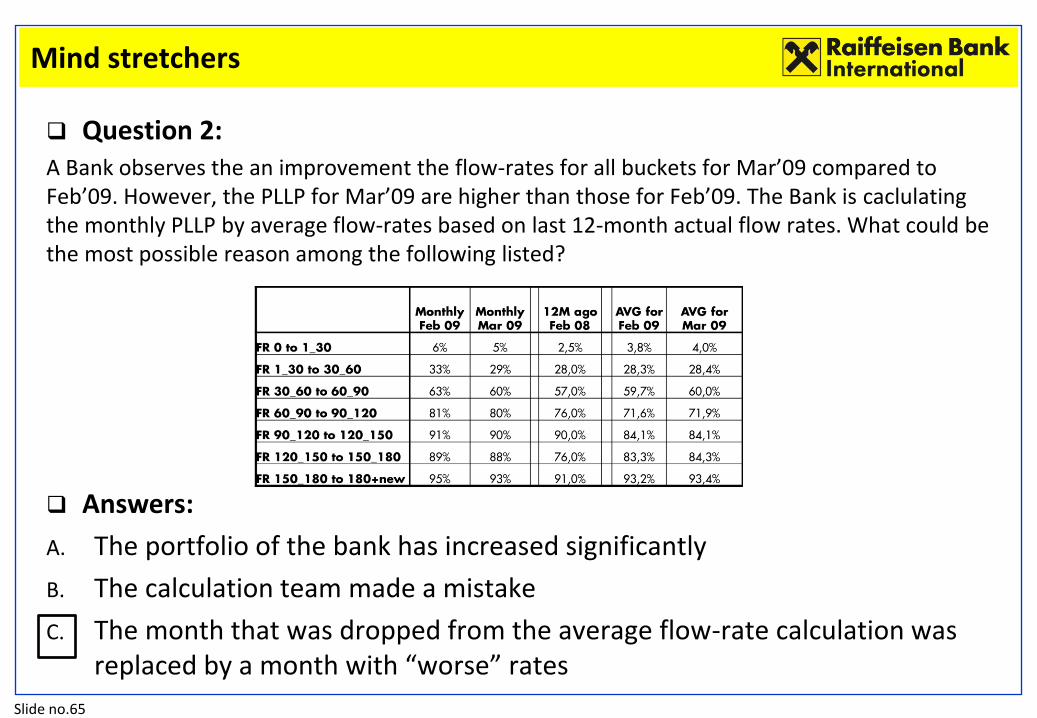

Mind stretchers

Question 2: A Bank observes the an improvement the flow-rates for all buckets for Mar’09 compared to Feb’09. However, the PLLP for Mar’09 are higher than those for Feb’09. The Bank is caclulating the monthly PLLP by average flow-rates based on last 12-month actual flow rates. What could be the most possible reason among the following listed?

Answers:

A. The portfolio of the bank has increased significantly

B. The calculation team made a mistake

C. The month that was dropped from the average flow-rate calculation was replaced by a month with “worse” rates

Slide no.66

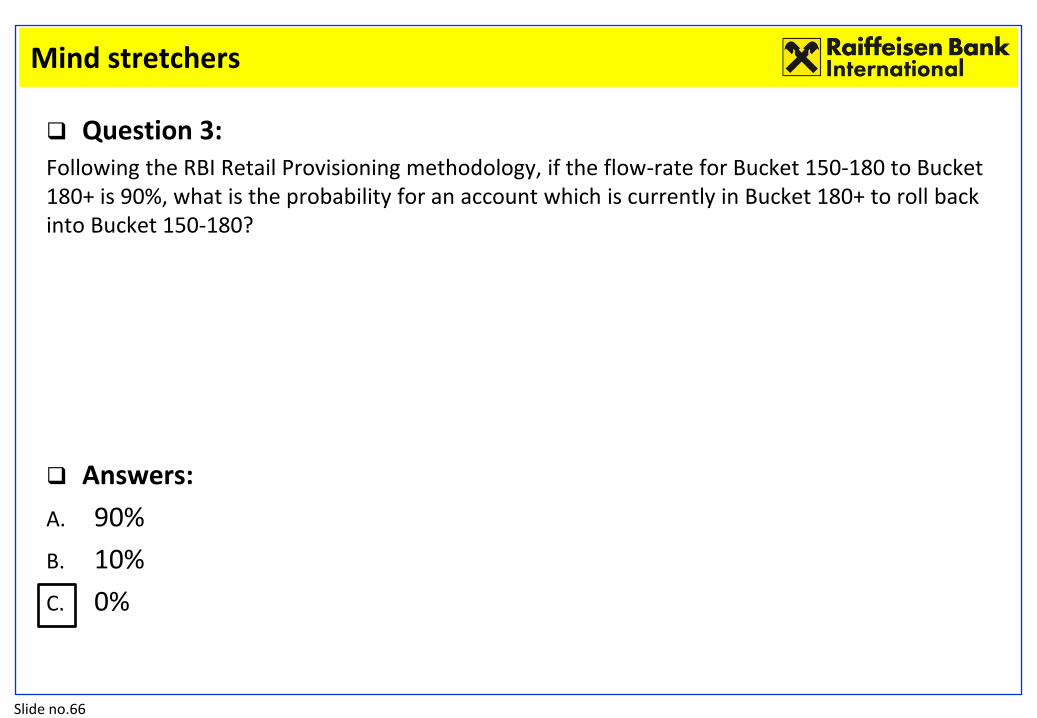

Mind stretchers

Question 3: Following the RBI Retail Provisioning methodology, if the flow-rate for Bucket 150-180 to Bucket 180+ is 90%, what is the probability for an account which is currently in Bucket 180+ to roll back into Bucket 150-180?

Answers:

A. 90%

B. 10%

C. 0%

Slide no.67

Mind stretchers

Question 4: If a Bank applying the RBI’s retail provisioning methodology sells a Residential real estate collateral linked to a mortgage account in Bucket 180+ DPD, which of the following provision pools for the Mortgage portfolio will be affected?

Answers:

A. PLLP

B. ILLP

C. Both PLLP and ILLP

Slide no.68

Mind stretchers

Question 5: On 25.05.2013 an unsecured account with current DPD = 55 has been restructured by the Bank whereby during the impairment test it showed an impairment of 2.5%.

On 25.11.2013 the same had DPD = 85 and the Bank restructured the account for a second time, whereby the impairment test showed loss of 5%. What should be the provisioning rate for this account for the end of November 2013?

Additional information: The loss rate for Bucket 30-60 is 30%, the loss rate for Bucket 60-90 is 70%, the Recovery rate for unsecured accounts is 50%.

Answers:

A. 5%

B. 35%

C. 100%

Slide no.69

Q & A

Slide no.70

THANK YOU

Deyan IVANOV

Retail Risk Management

Methodology & Validation

Raiffeisen Bank International AG

Tel.: +43 1 71707-1962

Email: [email protected]