rbs round up: 21 january 2011

TRANSCRIPT

8/7/2019 RBS Round Up: 21 January 2011

http://slidepdf.com/reader/full/rbs-round-up-21-january-2011 1/10

Equity Structured Products and Warrants

This material has been produced by RBS sales and trading staff and should not be considered independent.

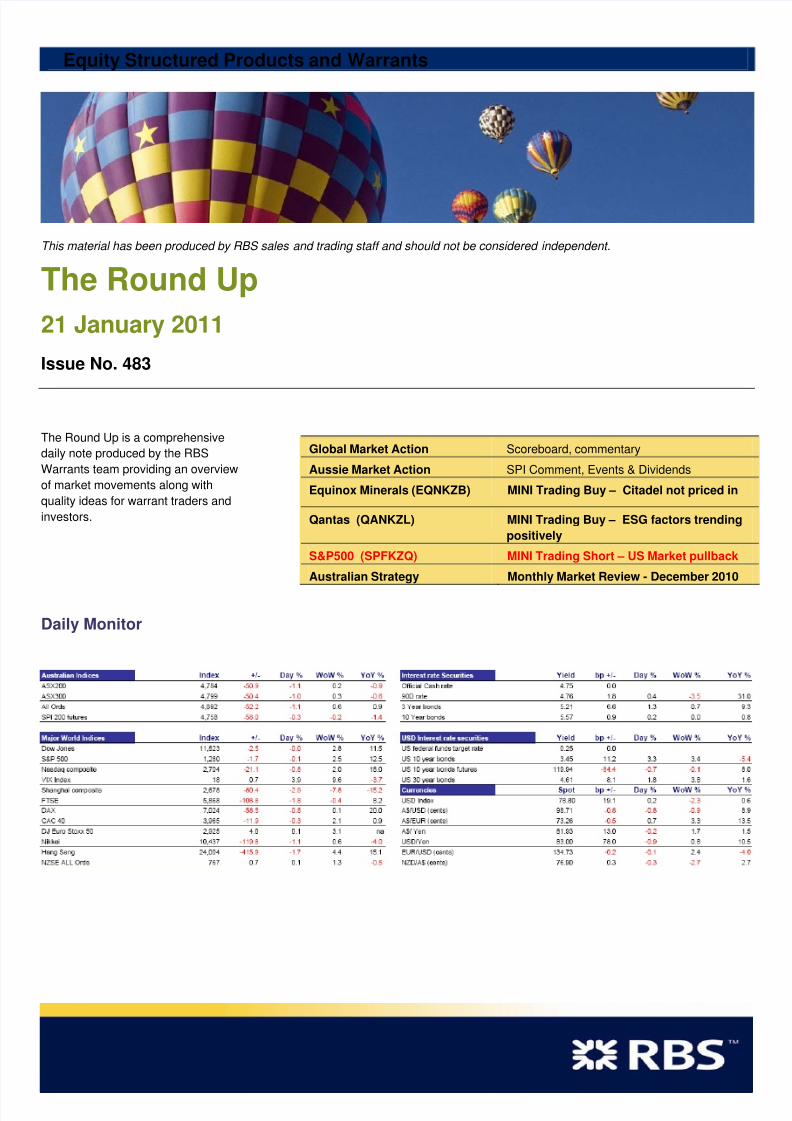

The Round Up

21 January 2011 Issue No. 483

The Round Up is a comprehensive

daily note produced by the RBS

Warrants team providing an overview

of market movements along with

quality ideas for warrant traders and

investors.

Daily Monitor

Global Market Action Scoreboard, commentary

Aussie Market Action SPI Comment, Events & Dividends

Equinox Minerals (EQNKZB) MINI Trading Buy – Citadel not priced in

Qantas (QANKZL) MINI Trading Buy – ESG factors trending

positively

S&P500 (SPFKZQ) MINI Trading Short – US Market pullback

Australian Strategy Monthly Market Review - December 2010

8/7/2019 RBS Round Up: 21 January 2011

http://slidepdf.com/reader/full/rbs-round-up-21-january-2011 2/10

Equity Structured Products and Warrants

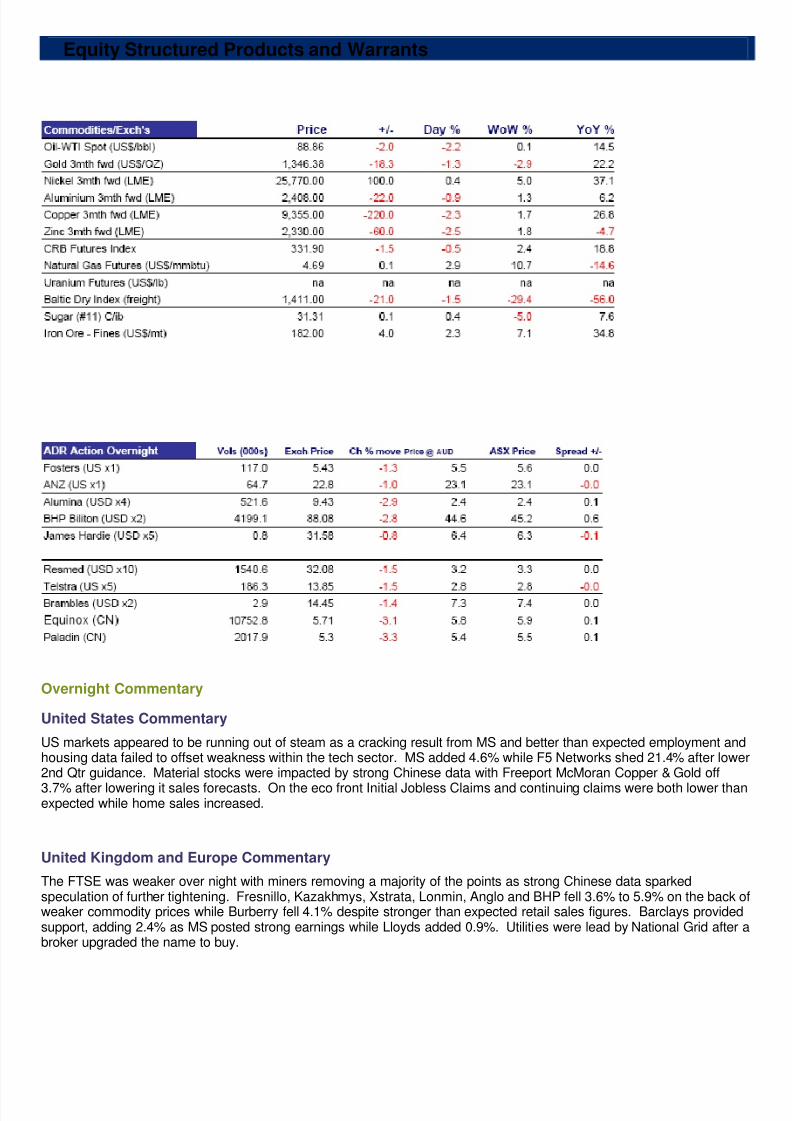

Overnight Commentary United States Commentary

US markets appeared to be running out of steam as a cracking result from MS and better than expected employment andhousing data failed to offset weakness within the tech sector. MS added 4.6% while F5 Networks shed 21.4% after lower2nd Qtr guidance. Material stocks were impacted by strong Chinese data with Freeport McMoran Copper & Gold off

3.7% after lowering it sales forecasts. On the eco front Initial Jobless Claims and continuing claims were both lower thanexpected while home sales increased.

United Kingdom and Europe Commentary

The FTSE was weaker over night with miners removing a majority of the points as strong Chinese data sparkedspeculation of further tightening. Fresnillo, Kazakhmys, Xstrata, Lonmin, Anglo and BHP fell 3.6% to 5.9% on the back ofweaker commodity prices while Burberry fell 4.1% despite stronger than expected retail sales figures. Barclays providedsupport, adding 2.4% as MS posted strong earnings while Lloyds added 0.9%. Utilities were lead by National Grid after abroker upgraded the name to buy.

8/7/2019 RBS Round Up: 21 January 2011

http://slidepdf.com/reader/full/rbs-round-up-21-january-2011 3/10

Equity Structured Products and Warrants

Commodities Commentary

SPI Commentary

The SPI traded down 58pts to 4770. Open at 4828 with a high of 4831 and a low of 4760. Volume 32,410. Overnight the SPI traded

down 12pts to 4758.

SPI Intraday SPI Daily

*SPI report taken from the 9:50am open to the 4:30pm close on the previous trading day. Charts taken from IRESS

Upcoming Economic Events for the Week

Monday AUS New Motor Vehicle Sales (MoM)

US

Tuesday AUS

US NY Empire State Manufacturing Index , NAHB Housing Market Index

Wednesday AUS Westpac Consumer SentimentUS MBA Mortgage Applications , Housing Starts

Thursday AUS

US Initial Jobless Claims , Continuing Jobless Claims , Existing Home Sales , PhiladelphiaFed Manufacturing Index , Crude Oil Inventories

Friday AUS Import Price Index (QoQ)

US

*Dates are indicative only and may change

8/7/2019 RBS Round Up: 21 January 2011

http://slidepdf.com/reader/full/rbs-round-up-21-january-2011 4/10

Equity Structured Products and Warrants

MINI Trading Buy: Equinox Minerals (EQNKZB) - Opportunity: Citadel not priced in

We have factored CGG into our estimates for EQN, which has materially lifted our NPV. In ourview, the market has overlooked the value created by the deal, creating an opportunity for

investors. The stock remains one of our key picks for 2011. Strike $3.52, Stop Loss $4.17.

Source: IRESS

A solid end to the year, 45Mtpa processing rates under review 4Q10 production of 34kt was slightly higher than our estimate of 32kt on the back of a significant jump in ore processingrates. Ore milled of 5.48kt (22Mtpa rate) was another record and comfortably above the 20Mtpa nameplate (EQN plans tobe at a 24Mtpa rate by year end). Copper ore grades fell significantly from 0.87% in 3Q10 to 0.69% (lower grades wereflagged, but slightly disappointing due to the read through to future years). Overall, it was a solid quarter, with full-yearproduction of 147kt ahead of 2010 guidance of 140kt. 2011 production guidance of 145kt was provided, slightly lowerthan we were expecting (at a cash cost of US$1.45/lb). We note 2011 guidance could be conservative, as was the casefor 2010. Further, expansion studies now include a 45Mtpa processing-rate scenario (previously 35Mtpa), which couldprovide further upside to our valuation.

Factoring in CGG has lifted our EPS EQN now holds more than 93% of Citadel Resources (CGG) and is proceeding with the compulsory acquisition of theremaining stock. We believe the deal is a credit to management, which has secured a high-quality asset at a low premiumrelative to recent transactions. RBS Research EPS rises on average 9% over 2013-15 due to the CGG contribution.

EQN one of our top picks for 2011 The overriding factor is the completion of the CGG transaction and NPV accretion. We continue to see upside potential atboth Jabil Sayid, and Lumwana. Further, with copper remaining comfortably above US$4.00/lb, we see upside risk toconsensus earnings as higher commodity prices are factored in, in our view. Our NPV and target price have risen fromA$6.45ps to A$7.03ps after factoring in CGG, the end-of-year cash balance and other operational changes. EQN is oneof our key picks in 2011. Buy.

Security ExPrc Stop Loss CP ConvFac Delta Description

EQNKZA 2.2578 2.71 Long 1 1 Long MINI

EQNKZB 3.472 4.17 Long 1 1 Long MINI

8/7/2019 RBS Round Up: 21 January 2011

http://slidepdf.com/reader/full/rbs-round-up-21-january-2011 5/10

Equity Structured Products and Warrants

MINI Trading Buy: Qantas (QANKZL): ESG factors trending positively

QAN has embraced ESG reporting, which in our view is important in such a challenging

industry. In this note we update QAN's FY10 sustainability performance in detail, noting it wasgenerally positive across most measures. With QAN trading below 1.0x P/B, we maintain ourBuy recommendation. Get long QANKZL

Source: IRESS 2010 ESG data points largely trended well On a majority of the ESG data points we track, QAN trended positively in FY10. Positively, fuel efficiency continued toimprove as new aircraft were brought into the fleet (ASK/bbl increased by a solid 2.7% on the pcp), governance measuresstrengthened, and operational performance (on-time arrivals and load factor) improved. On the negative side, the losttime injury frequency rate (LTIFR) increased marginally (from 4.2 to 4.3), while the workforce is aging, suggesting QANmay be having more difficulty attracting new employees.

Valuation upside potential dominated by fuel efficiencies Our long-term DCF valuation is most influenced by potential fuel efficiency improvements (+54%), offset by carbonpollution reduction scheme imposts (-25%). Operational measures such as passenger yields and load factors are also

influential, and are affected by QAN's performance in relation to customer satisfaction and brand. Risks are ever-presentin the airline industry, but we believe QAN has well defined risk management policies to react to and minimise these risksas much as possible.

QAN compares well on ESG metrics to peers and the broader S&P/ASX 200 The aviation industry generally is focused on ESG issues given impending emission trading schemes globally. In ourview, QAN shows particularly strong engagement on ESG issues, with many initiatives integrated into businessoperations. Not surprisingly, therefore, comparative data shows QAN generally ranking in the top half on ESG metricsagainst peers and strongly against the broader S&P/ASX 200 on ESG related disclosure.

QAN good value at <1.0x P/B, reiterate Buy recommendation We believe that QAN's positive ESG metrics should have a positive influence on its trading multiples. However, QAN iscurrently trading at both a P/E and P/B discount to its global peers due in large part to the recent A380 issues. With the

fleet now returning to normal operations, we expect QAN to rerate and maintain our Buy recommendation.

RBS MINIs over QAN Security ExPrc Stop Loss CP ConvFac Delta Description

QANKZL 1.6607 1.83 Long 1 1 MINI Long

QANKZM 2.02 2.23 Long 1 1 MINI Long

8/7/2019 RBS Round Up: 21 January 2011

http://slidepdf.com/reader/full/rbs-round-up-21-january-2011 6/10

Equity Structured Products and Warrants

MINI Trading Short: S&P 500 – US Market pullback The US S&P 500 has rallied significantly over the festive season on reasonably light volumes. Fromthe end of August 2010 to 17th January 2011 the S&P500 has jumped 24% compared to a relately weak

11% gain in the Australian XJO over the same 4.5 month period. We expect to see a modest pullbackin the S&P500 as the large mutual funds return from holidays and look to take profits in many of theirpositions.

SPFKZQ (Stop Loss at 1,313) is the instrument to play a pullback (Or SPFKZR higher Stop Loss of1,396) and we believe the S&P500 futures could easily fall from 1,262 to 1,220 and even below 1,200before the end of January.

Alternatively, some traders will prefer a pairs trade to take advantage of the US outperformance andtherefore mitigate the market risk of global economic news. Traders wishing to use this strategy cantherefore Buy 1 Long MINI XJOKZL for every 4 SPFKZQ shorts (market exposure of 1 XJOKZL is $47and 1 SPFKZQ is $12.60).

We would look to close out this trade at around 1,220 in the S&P 500 and this would return ~65%purely in the SPFKZQ MINI.

Source: IRESS

Pure S&P500 Short play Security ExPrc Stop Loss CP ConvFac Delta Description

SPFKZQ 1382 1313 Short .01 1 MINI ShortSPFKZR 1469.8 1396 Short .01 1 MINI Short

Pairs tradeBuy 1 Long MINI XJOKZL for every 4 SPFKZQ shorts

Security ExPrc Stop Loss Type ConvFac Delta Description

XJOKZL 4088.4 4293 Long .01 1 MINI LongSPFKZQ 1382 1313 Short .01 1 MINI Short

8/7/2019 RBS Round Up: 21 January 2011

http://slidepdf.com/reader/full/rbs-round-up-21-january-2011 7/10

Equity Structured Products and Warrants

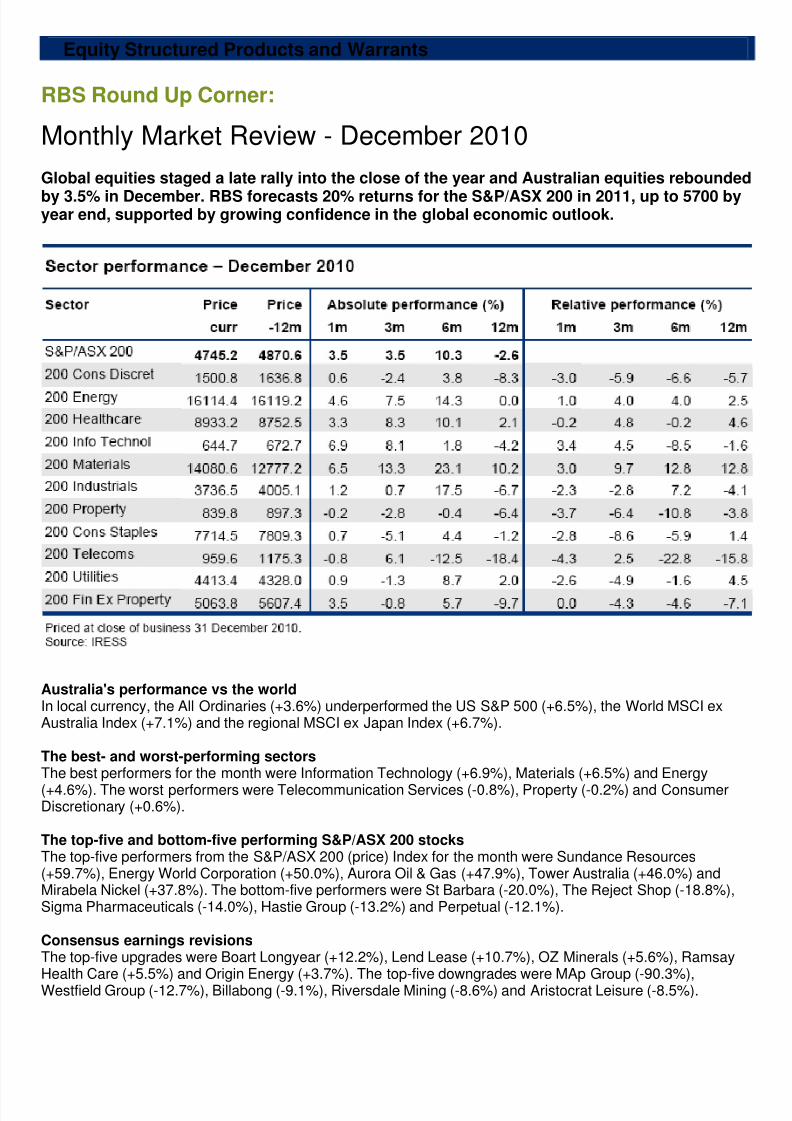

RBS Round Up Corner: Monthly Market Review - December 2010

Global equities staged a late rally into the close of the year and Australian equities rebounded

by 3.5% in December. RBS forecasts 20% returns for the S&P/ASX 200 in 2011, up to 5700 byyear end, supported by growing confidence in the global economic outlook.

Australia's performance vs the world In local currency, the All Ordinaries (+3.6%) underperformed the US S&P 500 (+6.5%), the World MSCI exAustralia Index (+7.1%) and the regional MSCI ex Japan Index (+6.7%).

The best- and worst-performing sectors The best performers for the month were Information Technology (+6.9%), Materials (+6.5%) and Energy

(+4.6%). The worst performers were Telecommunication Services (-0.8%), Property (-0.2%) and ConsumerDiscretionary (+0.6%).

The top-five and bottom-five performing S&P/ASX 200 stocks The top-five performers from the S&P/ASX 200 (price) Index for the month were Sundance Resources(+59.7%), Energy World Corporation (+50.0%), Aurora Oil & Gas (+47.9%), Tower Australia (+46.0%) andMirabela Nickel (+37.8%). The bottom-five performers were St Barbara (-20.0%), The Reject Shop (-18.8%),Sigma Pharmaceuticals (-14.0%), Hastie Group (-13.2%) and Perpetual (-12.1%).

Consensus earnings revisions The top-five upgrades were Boart Longyear (+12.2%), Lend Lease (+10.7%), OZ Minerals (+5.6%), RamsayHealth Care (+5.5%) and Origin Energy (+3.7%). The top-five downgrades were MAp Group (-90.3%),Westfield Group (-12.7%), Billabong (-9.1%), Riversdale Mining (-8.6%) and Aristocrat Leisure (-8.5%).

8/7/2019 RBS Round Up: 21 January 2011

http://slidepdf.com/reader/full/rbs-round-up-21-january-2011 8/10

Equity Structured Products and Warrants

Looking back and looking forwardAs we moved towards the close of the year, equity markets have staged a late rally back towards pre-Lehmanlevels. Equity and currency markets are less concerned about periphery Europe than bond markets, andequities are slowly rerating, a trend we expect to continue in 1H11. In local terms, in December the S&P 500was up 6.5%, the Stoxx 600 was up 5.3% and the S&P/ASX 200 was up 3.5%. We note the rally has beenbroad-based as equities in Spain, Italy, Portugal and Ireland have also participated. The sovereign bond

markets are not so relaxed, and European peripheral bond yields and CDS spreads are close to their highs,highlighting to us that sovereign risk in Europe will be an ongoing concern. The catalysts for this late stagerally are a combination of reduced US recession risk and reduced concerns about European contagion risk.Investors are retreating from bond funds following signs of a US economic recovery and the stock market rallyhas increased speculation that interest rates may rise.

US economic growth gaining momentum – Alongside continued monetary accommodation in the US, theeconomic recovery looks to be picking up momentum, providing a firmer macro backdrop as we move into2011. The December Philly Fed highlighted the trend, with forwardlooking components returning to thestronger March-April levels that were interrupted by the European sovereign crisis from May. In particular, theexpected capex component is at its strongest level since mid-2005, and the prices paid component suggestsinflation should normalise. This is particularly important, given monetary policy must now give way to the

private sector to drive economic growth. We highlight US capex as a significant equity market theme as wemove into 2011. In addition, small to medium-sized enterprises are beginning to rehire and income growth isdriving consumer spending.

European stability – While improving economically, Europe remains vulnerable to pockets of deflation and aresurgence of European sovereign debt woes as this structural issue takes time to repair. From an economicperspective, the manufacturing PMIs in core Europe have remained resilient as demand in foreign marketshas benefitted the region. The latest survey data continue to point to ongoing recovery in the euro areabusiness cycle, albeit at muted levels. It will likelytake time for a sustained domestic demand recovery to emerge in Europe, while real income growth remainsmoderate in an environment of modest employment and wage growth. We expect peripheral sovereign debt toweigh on markets from time to time, but we note investors appear less concerned that this will cause outright

financial markets seizure, as was feared in May this year. Also, at the latest ECB press conference there wasa clear desire to ensure the stability of the Eurozone and a greater willingness to use the bond purchaseprogramme (SMP). Chinese officials have also offered to step up their support of European stabilisationefforts. What form this might take is unclear, but at the very least should be successful in lifting sentiment.

Chinese property – We highlighted Chinese residential construction as a linch-pin for our investment strategygoing forward, as this sector is 33% of steel demand. The IMF’s new report on Chinese property highlightssome interesting conclusions, notably that house prices do not appear to be significantly higher than justifiedby fundamentals. While there may be overvaluation in some coastal cities, developments are still ‘early stage’.Moreover, there are powerful structural drivers underpinning the housing market, namely low real interestrates, strong income growth and a low mortgage-to-GDP ratio. We believe these drivers will result in a widereconomic rebalancing, providing the global economy with an invaluable growth engine for the foreseeablefuture.

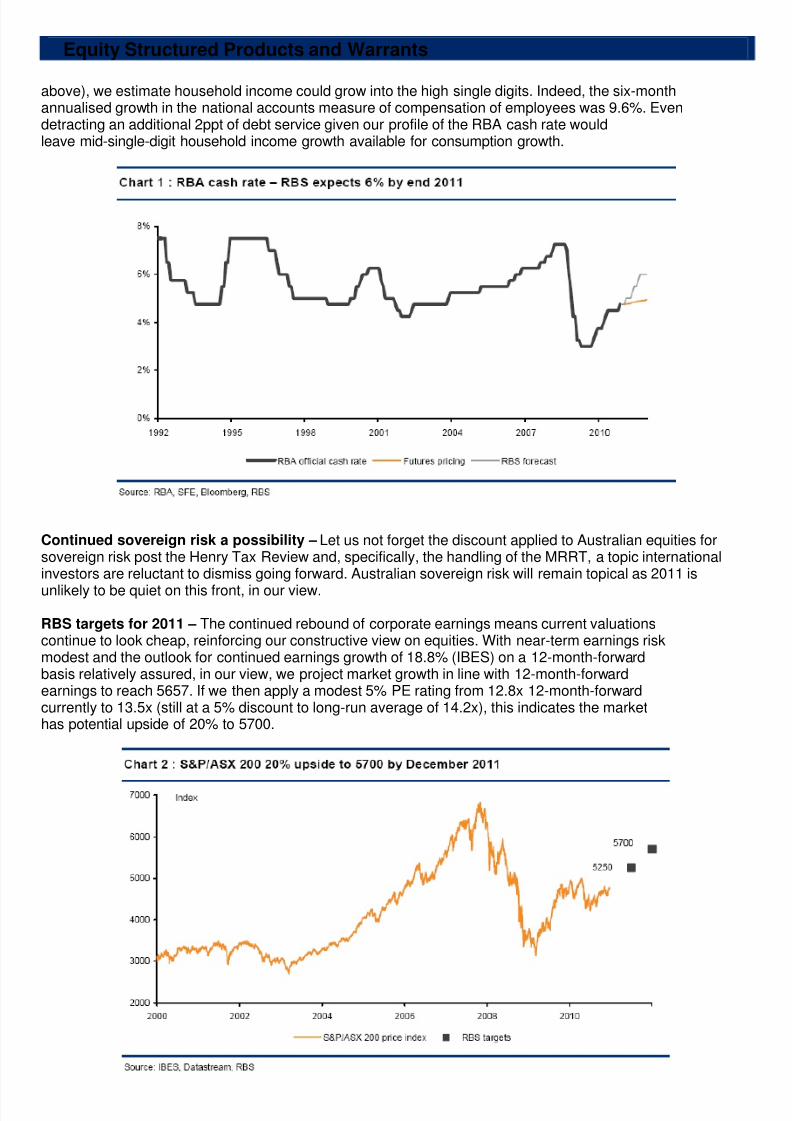

Australian economic growth on a rising trend – RBS economist Kieran Davies expects 3.7% growth yoy for2011, and we expect Australia to remain in the fortunate position of enjoying buoyant terms of trade while alsogenerating significant export volume growth through the expansion of iron ore, coal and LNG operations.Australia’s increasing dependence on China, however, does give rise to risks of greater volatility. RBS expectsthe RBA to take the cash rate to 6% by the end of 2011. The RBA responded recently to the risks to medium-term inflation, given the strong growth outlook and limited spare capacity in the economy. The market iscurrently pricing in 25bp to end 2011 and we expect this to change as the outlook for growth in advancedeconomies firms. On our forecast cash rate of 6% by the end of 2011, we expect rates to take 2ppt off income,as the RBA’s actions would be magnified by higher household debt. However, on the positive side, our banks

team does not forecast further increases in the standard variable rate above the cash rate from here. The tightlabour market (unemployment now at 5.2%) is now feeding through to wages growth; this month we saw thewage price index up 1.1% in the quarter, a sharp increase from 0.8% in 2Q10 and showing the fastest growthsince 4Q08. This gain lifts annual growth in this key measure of wages from 3.0% to 3.5%, although it is stillwell short of the peak of 4.3% reached in 4Q08. Also, given hours worked are rising at a rate of 3.1% yoycombined with wages growing at about 3% (and, given previous experience, that wages could grow at 4% or

8/7/2019 RBS Round Up: 21 January 2011

http://slidepdf.com/reader/full/rbs-round-up-21-january-2011 9/10

Equity Structured Products and Warrants

above), we estimate household income could grow into the high single digits. Indeed, the six-monthannualised growth in the national accounts measure of compensation of employees was 9.6%. Evendetracting an additional 2ppt of debt service given our profile of the RBA cash rate wouldleave mid-single-digit household income growth available for consumption growth.

Continued sovereign risk a possibility – Let us not forget the discount applied to Australian equities forsovereign risk post the Henry Tax Review and, specifically, the handling of the MRRT, a topic internationalinvestors are reluctant to dismiss going forward. Australian sovereign risk will remain topical as 2011 is

unlikely to be quiet on this front, in our view.

RBS targets for 2011 – The continued rebound of corporate earnings means current valuationscontinue to look cheap, reinforcing our constructive view on equities. With near-term earnings riskmodest and the outlook for continued earnings growth of 18.8% (IBES) on a 12-month-forwardbasis relatively assured, in our view, we project market growth in line with 12-month-forwardearnings to reach 5657. If we then apply a modest 5% PE rating from 12.8x 12-month-forwardcurrently to 13.5x (still at a 5% discount to long-run average of 14.2x), this indicates the markethas potential upside of 20% to 5700.

8/7/2019 RBS Round Up: 21 January 2011

http://slidepdf.com/reader/full/rbs-round-up-21-january-2011 10/10