ready to serve 1800 88 4000 - mbsb.com.my fileready to serve 1800 88 4000 annual report 2005...

TRANSCRIPT

READY TO SERVE

1800 88 4000

A N N U A L R E P O RT 2 0 0 5

MA

LAY

SIA B

UILD

ING

SOC

IETY

BER

HA

D

AN

NU

AL R

EPORT 2005

(94

17

-K)

CoverRationale

Ready to Serve

Contemporary and artistic, this

painting portrays MBSB as a

modern and dynamic organisation.

The main subject of the abstract

painting is on property, to

illustrate MBSB’s core business

as a property fi nancier. Designed

with different hues of blue, the

cover effectively utilises MBSB’s

corporate colour blue, a colour

that signifi es trust, confi dence,

wisdom and truth, in line with an

image of reliability and reliance.

Service and how it is delivered in

today’s dynamic market place is

highly competitive. To serve our

customers better, we recognise

that service is more than about

our own performance, but about

providing added value to the

lives of our customers. We have

in our palette a colourful array

of products that cater to our

customers’ needs and desires

ensured by our commitment to

service excellence.

MBSB Annual Report 2005

1

Contents

CORPORATE INFORMATION 2

DIRECTORS’ PROFILE 3 - 7

SHARIAH COUNCIL PROFILE 8 - 9

NOTICE OF ANNUAL GENERAL MEETING 10

NOTICE OF DIVIDEND ENTITLEMENT AND PAYMENT 11

CHAIRMAN’S STATEMENT 12 - 16

CEO’S MISSION 17

SENIOR MANAGEMENT 18 - 19

CALENDAR OF EVENTS 20 - 21

STATEMENT OF CORPORATE GOVERNANCE 22 - 27

STATEMENT ON INTERNAL CONTROL 28 - 30

REPORT OF THE AUDIT & RISK MANAGEMENT COMMITTEE 31 - 33

FINANCIAL HIGHLIGHTS OF THE COMPANY 34 - 35

ANALYSIS OF SHAREHOLDING 36 - 37

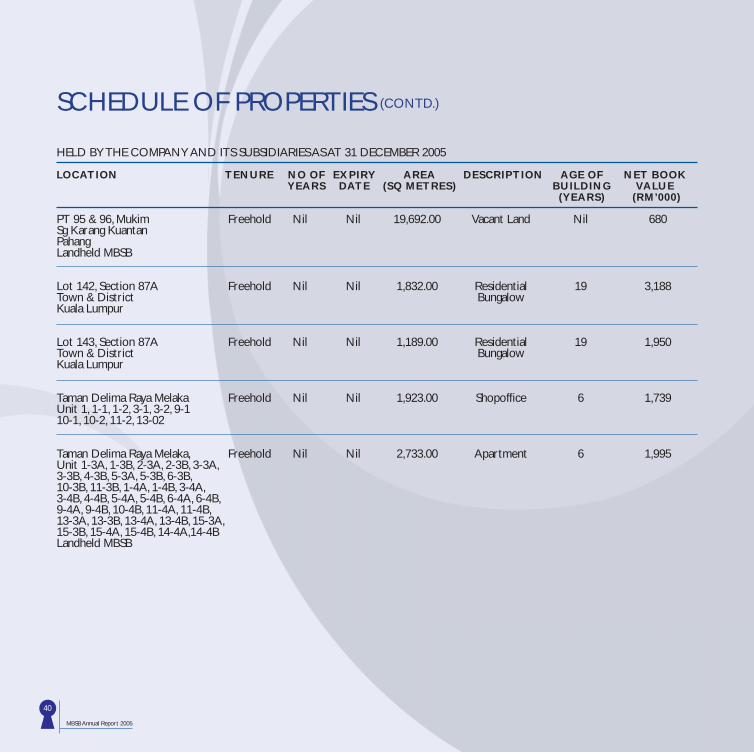

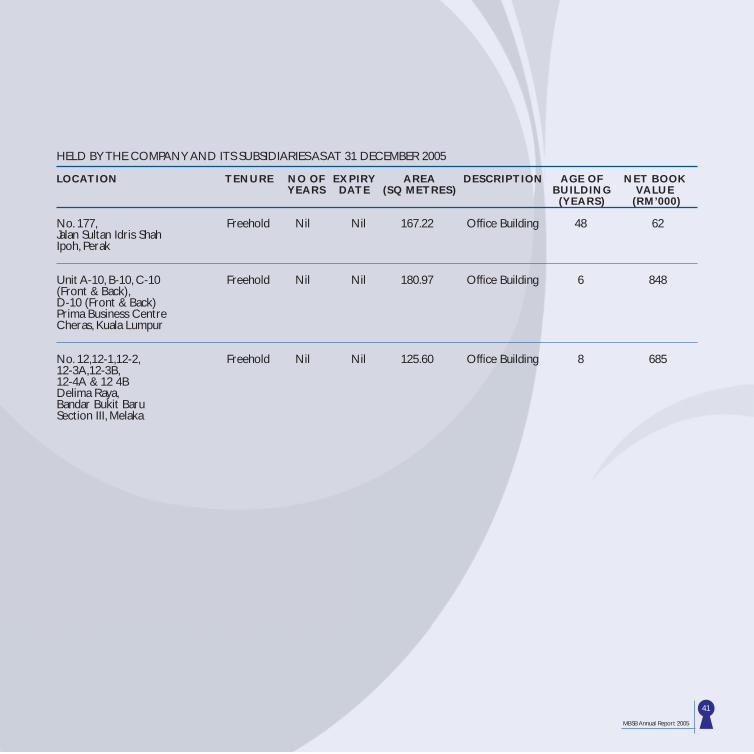

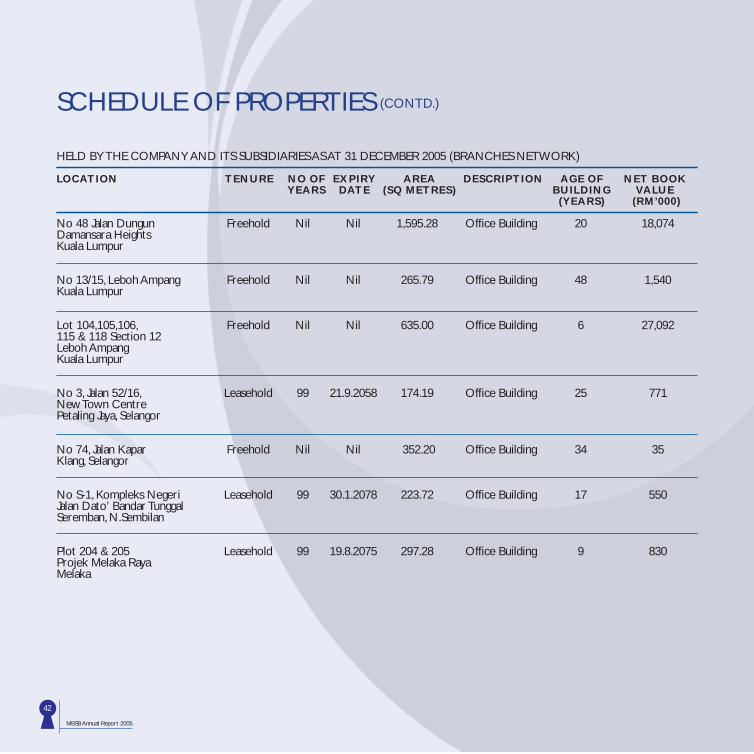

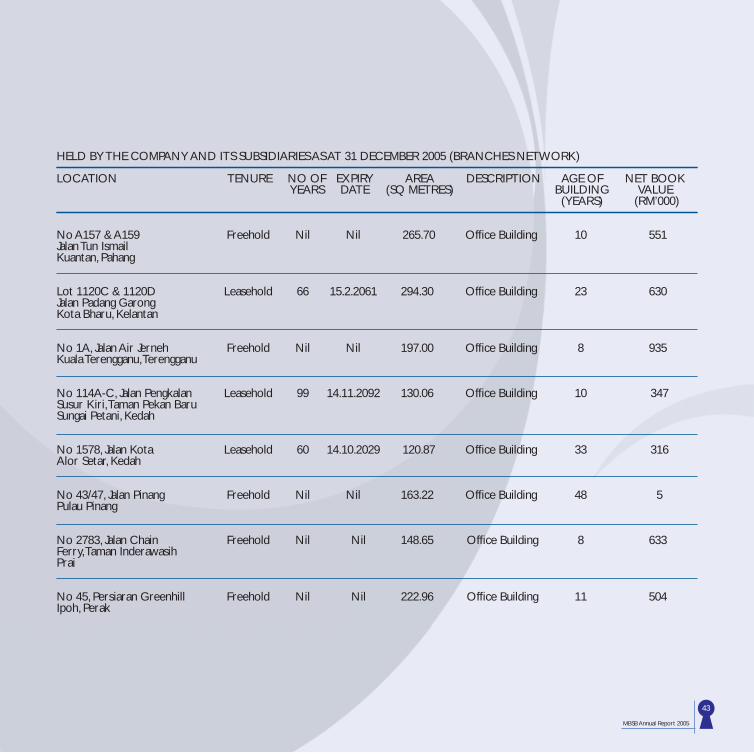

SCHEDULE OF PROPERTIES 38 - 43

BRANCH NETWORK 44

• PROXY FORM

MBSB Annual Report 2005

2

Corporate InformationChairman YBhg Tan Sri Abdul Halim bin Ali

Board of Directors YBhg Datuk Haji A. Rahim bin Abdullah Syed Zaid bin Syed Jaffar Albar Encik Lau Tiang Hua Puan Cindy Tan Ler Chin YBhg Datuk Abdullah bin Haji Kuntom Encik Khalid bin Haji Sufat (appointed with effect from 18 August 2005)

Encik Aw Hong Boo (appointed with effect from 10 November 2005)

YBhg Datuk Azlan bin Mohd. Zainol

Shariah Council Professor Madya Syed Ghazali Wafa Bin Syed Adwam Wafa Professor Dr. Mohd. Ali bin Haji Baharum Ustaz Omar bin Johari

Chief Executive Offi cer Encik Ahmad Farid bin Omar

Company Secretary Encik Fariz bin Abdul Aziz (LS 0007997)

Registrar Symphony Share Registrars Sdn Bhd (378993-D) (Formerly known as Malaysian Share Registration Services Sdn Bhd) Level 26, Menara Multi-Purpose, Capital Square, No. 8, Jalan Munshi Abdullah, 50100 Kuala Lumpur.

Auditors Ernst & Young Public Accountants

Bankers Malayan Banking Berhad RHB Bank Berhad

Registered Offi ce 11th Floor, Wisma MBSB 48, Jalan Dungun Damansara Heights 50490 Kuala Lumpur Tel : 03-2095 4000 Fax : 03-2095 4260

Bumiputra-Commerce Bank Berhad

MBSB Annual Report 2005

2

(resigned with effect from 1 August 2005)

MBSB Annual Report 2005

3

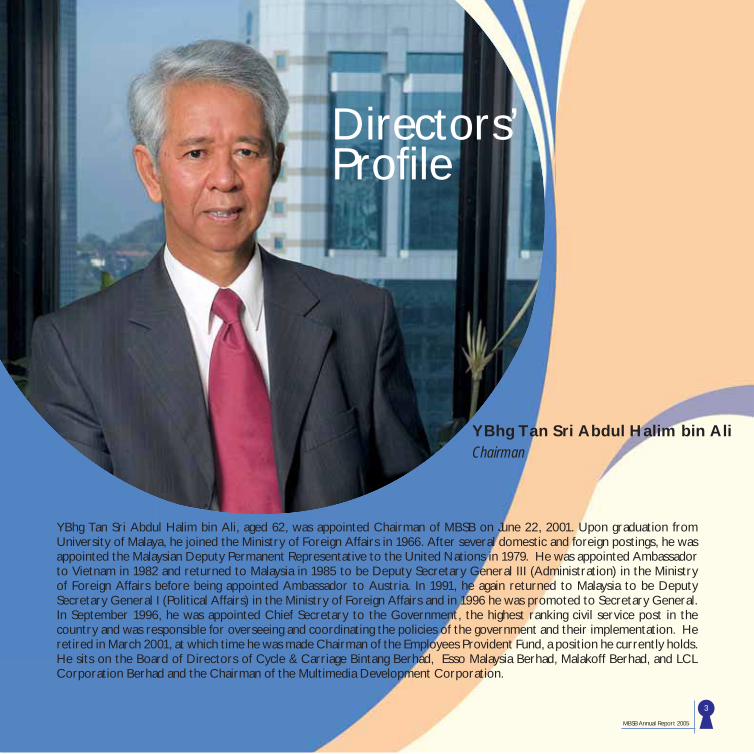

YBhg Tan Sri Abdul Halim bin Ali, aged 62, was appointed Chairman of MBSB on June 22, 2001. Upon graduation from University of Malaya, he joined the Ministry of Foreign Affairs in 1966. After several domestic and foreign postings, he was appointed the Malaysian Deputy Permanent Representative to the United Nations in 1979. He was appointed Ambassador to Vietnam in 1982 and returned to Malaysia in 1985 to be Deputy Secretary General III (Administration) in the Ministry of Foreign Affairs before being appointed Ambassador to Austria. In 1991, he again returned to Malaysia to be Deputy Secretary General I (Political Affairs) in the Ministry of Foreign Affairs and in 1996 he was promoted to Secretary General. In September 1996, he was appointed Chief Secretary to the Government, the highest ranking civil service post in the country and was responsible for overseeing and coordinating the policies of the government and their implementation. He retired in March 2001, at which time he was made Chairman of the Employees Provident Fund, a position he currently holds. He sits on the Board of Directors of Cycle & Carriage Bintang Berhad, Esso Malaysia Berhad, Malakoff Berhad, and LCL Corporation Berhad and the Chairman of the Multimedia Development Corporation.

Directors’ Profi le

YBhg Tan Sri Abdul Halim bin Ali Chairman

MBSB Annual Report 2005

3

MBSB Annual Report 2005

4

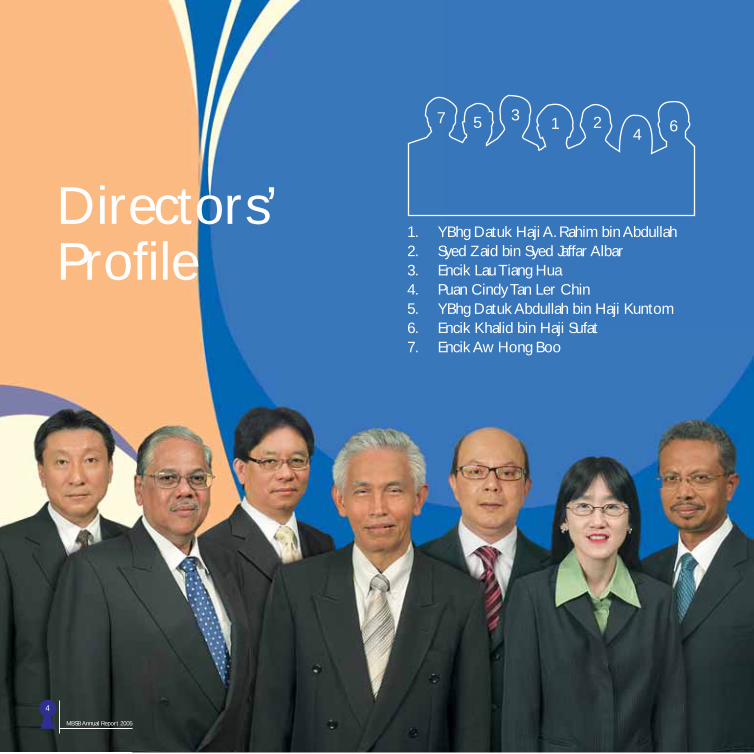

Directors’Profi le

1. YBhg Datuk Haji A. Rahim bin Abdullah2. Syed Zaid bin Syed Jaffar Albar3. Encik Lau Tiang Hua4. Puan Cindy Tan Ler Chin5. YBhg Datuk Abdullah bin Haji Kuntom6. Encik Khalid bin Haji Sufat7. Encik Aw Hong Boo

MBSB Annual Report 2005

4

6421357

MBSB Annual Report 2005

5

YBhg Datuk Haji A. Rahim bin AbdullahIndependent Non-Executive Director

YBhg Datuk Haji A. Rahim bin Abdullah, aged 62, graduated with a Diploma in Building Design from the Technical College, Kuala Lumpur, now Universiti Teknologi Malaysia (UTM) and obtained his Bachelor of Architecture and Master of Architecture from University of Auckland, New Zealand. He is an associate member of the New Zealand Institute of Architects (NZIA) and Malaysian Institute of Architects (PAM) as well as Director of Badan Warisan Malaysia.

He was appointed as an Independent Non-Executive Director of MBSB on 15 July, 2000. Prior to this, he was attached to Jabatan Kerja Raya (JKR) from 1972 until he retired as Deputy Director General in 1998. He was also appointed President of the Board of Architects Malaysia (BAM) from 1989 to 1998.

He currently sits on the Board of Directors of Pelangi Berhad,Plaza Damansara Sdn Bhd and PNB Merdeka Ventures Sdn Bhd. besides serving as Property Development Consultant with Golden Hope Development Berhad.

Syed Zaid bin Syed Jaffar AlbarIndependent Non-Executive Director

Syed Zaid bin Syed Jaafar Albar, aged 51, joined the Board as an Independent Non-Executive Director on 14 August 2002.

He obtained his law degree from the United Kingdom and qualifi ed as a Barrister-at-Law from Lincoln’s Inn. He was called to the Malaysian Bar as an advocate and solicitor of the High Court of Malaya in 1980 and has been active in legal practise ever since.

Presently, Syed Zaid Albar is the managing partner of a law fi rm in Kuala Lumpur. He also sits on the Board and Audit Committees of several other listed companies, namely, Malaysian Pacifi c Industries Berhad, Narra Industries Berhad and Cycle & Carriage Bintang Berhad.

Encik Lau Tiang HuaIndependent Non-Executive Director

Encik Lau Tiang Hua, aged 53, was appointed as an Independent Non-Executive Director on 16 August 2001. He is a member of the Malaysian Institute of Certifi ed Public Accountants (MACPA) and the Malaysian Institute of Accountants.

He began his career with one of the international public accounting fi rms in Malaysia and later rose to the rank of Audit Manager. He was the General Manager of fi nance and administration with a major publishing company in Malaysia before starting his own practice, JB Lau & Associates, Chartered Accountants, in 1985.

He also sits on the Board of Directors of PanGlobal Berhad, Nanyang Press Holdings Berhad and several private limited companies.

MBSB Annual Report 2005

5

MBSB Annual Report 2005

6

Puan Cindy Tan Ler ChinNon-Independent Non-Executive Director

Puan Cindy Tan Ler Chin, aged 45, obtained an Honours Degree in Economics, majoring in Statistics, from University Kebangsaan Malaysia. In 1991, she obtained a Certifi ed Diploma in Accounting and Finance, accorded by the Chartered Association of Certifi ed Accountants.

She began her career with the Employees Provident Fund (EPF), Finance and Investment Department in 1984. She is currently the General Manager of the Corporate Finance - Investment Division of the EPF.

She was appointed as a Non-Independent Non-Executive Director of MBSB on 26 September 2002. She also sits on the Board of Directors of Sunway Holdings Incorporated Berhad.

Directors’ Profi leYBhg Datuk Abdullah bin Haji KuntomNon-Independent Non-Executive Director

YBhg Datuk Abdullah bin Haji Kuntom, aged 62, joined the Board as a Non-Independent Non-Executive Director on 26 September 2003. He obtained a Master’s Degree in Public Policy and Administration from University of Wisconsin, USA in 1979 and also attended a course in Advanced Management Programme at University of Oxford, U.K in 1995.

He began his career with the Johor Civil Servicein 1967 and had served with the Ministry of Home Affairs,Ministry of Finance, Syarikat Kemajuan Perumahan Pegawai Kerajaan Sdn Bhd, Selangor Treasury, Asia Pacifi c Development Centre and National Registration Department. His last post was as Senior Deputy Secretary General in the Prime Minister’s Department until his retirement in April 1999. Thereafter he was reemployed with the Ministry of ForeignAffairs for 4 years until April 2003.

MBSB Annual Report 2005

6

MBSB Annual Report 2005

7

Encik Khalid bin Haji Sufat Independent Non-Executive Director

Encik Khalid bin Haji Sufat, aged 50, joined the Board as an Independent Non-Executive Director on 18 August 2005. An accountant by profession, he is a Fellow of the Chartered Association of Certifi ed Accountants (United Kingdom) and a Member of both The Malaysian Institute of Accountants (MIA) as well as The Malaysian Institute of Certifi ed Public Accountants (MICPA).

He has considerable experience in the banking and fi nance industry having held several senior positions, namely Managing Director of Bank Kerjasama Rakyat Malaysia Berhad from June 1998 to June 2000, as General Manager Consumer Banking of Malayan Banking Berhad in 1994 and as Executive Director of United Merchant Finance Berhad from 1995 to 1998.

He had also managed two listed companies, namely as Executive Director of Tronoh Mines Malaysia Berhad in 2002 and as the Managing Director of Furqan Business Organisation Berhad in 2003.

He presently sits on the Board of Directors of Binapuri Holdings Berhad, Amtek Holdings Berhad, VTI Vintage Berhad and Syarikat Kayu Wangi Berhad.

Encik Aw Hong BooIndependent Non-Executive Director

Encik Aw Hong Boo, aged 55 was appointed as an Independent Non-Executive Director on 10 November 2005. He is a member of The Malaysian Institute of Certifi ed Public Accountants (MICPA), The Malaysian Institute of Accountants (MIA) and a Fellow of the Institute of Chartered Accountants (England & Wales).

He began his career in 1970 as an Audit Senior in London and later with Ernst & Whinney, an international public accounting fi rm in Singapore and London. He served RHB Bank Berhad for 21 years from 1978 to 1999, holding various senior managerial positions in fi nancial management, banking, fi nance and leasing. He was the Senior General Manager of Branch Network and Risk Management before optional retirement in November 1999.

He presently sits on the Board of Directors of KP KeningauBerhad and serves as the Financial Advisor to the Quill Group of Companies.

MBSB Annual Report 2005

7

MBSB Annual Report 2005

8

Professor Madya Syed Ghazali Wafa Bin Syed Adwam Wafa

Associate Professor Syed Ghazali Wafa bin Syed Adwam Wafa was formerly the Deputy Dean of Academics and Student Affairs, Faculty of Business Management, Universiti Kebangsaan Malaysia. He started lecturing in Universiti Kebangsaan Malaysia since 1985. A Diploma holder in Agriculture (UPM), BSc (Finance) and an MBA from U.S., he is currently attached to the School of Accounting, Faculty of Economics and Business, UKM.

Besides conducting courses in Financial Accounting, Management Accounting and Auditing, he also lectures the Business From Islamic Perspective course at both undergraduate and graduate levels.

Through the Pusat Zakat Selangor, he participated in efforts to streamline the method of assessing zakat for businesses. His publications and current research area of interest is in Muamalat, specifi cally relating to contracts and business mechanisms, cooperatives, zakat accounting for businesses,zakat and corporate governance, Baitulmal and Islamic Financial Institutions. He is currently a Shariah Committeemember of several cooperatives and also a Council Member of the Cooperative College of Malaysia.

Shariah Council Profi leProfessor Dr. Mohd. Ali bin Haji Baharum

Professor Dr. Mohd. Ali Hj Baharum, the Deputy President of Angkatan Koperasi Kebangsaan Malaysia Berhad was born in Alor Setar in the year 1951 and received his early education in Maktab Mahmud, Alor Star, Kedah. He graduated with a Degree B.Is (Hons) in Shariah and Law from UKM in 1976. He took his Ph.D (Law) at University of Essex in 1986 and obtained his MBA in 1994. He also obtained a Diplomain Education from UKM and Diploma in Arabic from the International University of Africa, Khartoum, Sudan in 1990. In 1995, he opted for early retirement as a lecturer in the Law Faculty of UKM.

An ardent author and has written authoritative books and seminar papers regarding islamic contract law and zakat.

He is also directly involved in developing the National IslamicFinancial and Banking system. Because of his efforts and contributions, he was appointed the Shariah Advisor of Bank Negara, Bank Muamalat, Bank Pertanian, Hong Leong Bank and several other banks. He was also the Shariah Advisor to Amanah Saham Apex Investment Services Bhd, a member of the Maktab Kerjasama Malaysia (MKM), Board Member of Permodalan Risda Bhd and Deputy Chairman of Belia Islam (M) Bhd.

MBSB Annual Report 2005

8

MBSB Annual Report 2005

9

Ustaz Omar bin Johari

Ustaz Omar Johari, aged 59, is an independent religious scholar and motivator from Muar, Johor. He obtained his degree in Dakwah from the Islamic Call University, Tripoli, Libya.

He has vast experience in the area of management from both the Government and private sector. He was the Offi cer in Religious Affair in the Prime Minister’s Department from 1974 - 1977 and was a lecturer at the Islamic Faculty in UKM from 1981 - 1984.

He was also the Shariah Advisor for Rashid Hussain Securties from 1983 - 1997, DCB/RHB (1997), Oriental Bank and Amanah Raya Berhad and the Advisor for Islamic Religious Affair for Mc Food Industries Sdn Bhd and Mc Donald Malaysia.

MBSB Annual Report 2005

9

MBSB Annual Report 2005

10

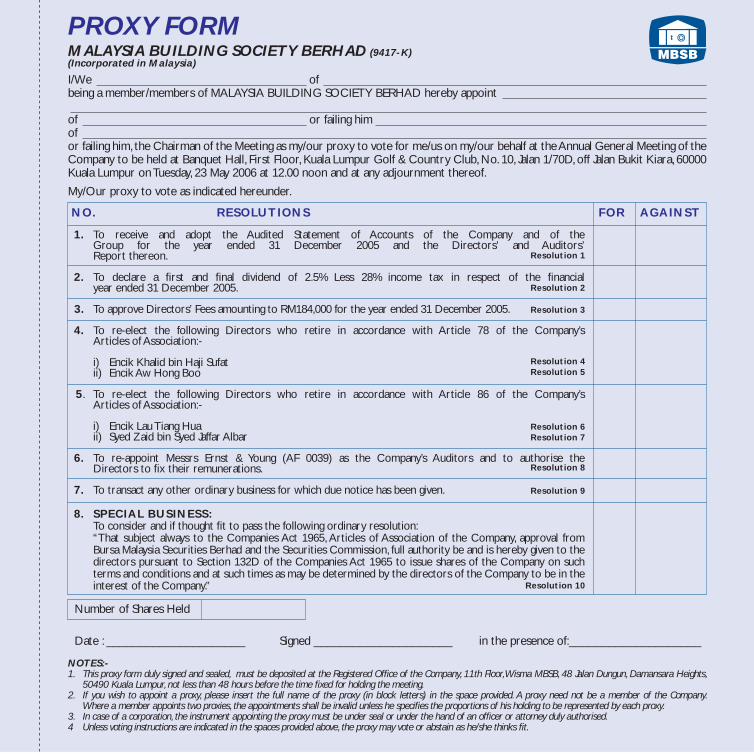

1. To receive and adopt the Audited Financial Statements of the Company and of the Group for the year ended 31 December 2005 and the Directors’ and Auditors’ Report thereon.

2. To declare a fi rst and fi nal dividend of 2.5% less 28% income tax in respect of the fi nancial year ended 31 December 2005.

3. To approve Directors’ Fees amounting to RM184,000 for the fi nancial year ended 31 December 2005

4. To re-elect the following who retired in accordance with Article 78 of the Company’s Articles of Association:-

(i) Encik Khalid bin Haji Sufat (ii) Encik Aw Hong Boo

5. To re-elect the following who retired in accordance with Article 86 of the Company’s Articles of Association:-

(i) Encik Lau Tiang Hua (ii) Syed Zaid bin Syed Jaffar Albar

6. To re-appoint Messrs Ernst & Young (AF 0039) as the Company’s Auditors and to authorise the Directors to fi x their remuneration.

7. To transact any other ordinary business for which due notice has been given.

8. SPECIAL BUSINESS: To consider and if thought fi t, to pass the following ordinary resolution:

“That subject always to the Companies Act 1965, Articles of Association of the Company, approval from Bursa Malaysia Securities Berhad and Securities Commission, full authority be and is hereby given to the Directors pursuant to Section 132D of the Companies Act 1965 to issue shares of the Company on such terms and conditions and at such times as may be determined by the directors of the Company to be in the interest of the Company.

BY ORDER OF THE BOARD

FARIZ ABDUL AZIZ (LS 0007997)COMPANY SECRETARY

Kuala Lumpur2 May 2006

NOTICE OF ANNUAL GENERAL MEETING

NOTICE IS HEREBY GIVEN THAT THE THIRTY SIXTH ANNUAL GENERAL MEETING of the Company will be held at Banquet Hall, First Floor, Kuala Lumpur Golf & Country Club, No.10, Jalan 1/70D, Off Jalan Bukit Kiara, 60000 Kuala Lumpur on Tuesday 23 May 2006 at 12.00 noon for the following purposes:

Resolution 1

Resolution 2

Resolution 3

Resolution 4Resolution 5

Resolution 6Resolution 7

Resolution 8

Resolution 9

Resolution 10

NOTE :A member entitled to attend and vote at the meeting is entitled to appoint a proxy to attend and, on a poll, to vote in his stead. A proxy may but need not be a member of the Company and a member may appoint any person to be his proxy without limitation and the provisions of Section 149(1)(b) of the Companies Act, 1965 shall not apply to the Company. Where a member appoints two proxies, the appointment shall be invalid unless he specifi es the proportions of his holding to be represented by each proxy.

In the case of a Corporate Body, the proxy appointed must be in accordance with its Memorandum and Articles of Association and the instrument appointing a proxy shall be given under the Company’s Common Seal or under the hand of an offi cer or attorney duly authorised.

The form of proxy must be deposited at the Registered Offi ce of the Company at 11th Floor, Wisma MBSB, No.48, Jalan Dungun, Damansara Heights, 50490 Kuala Lumpur not less than 48 hours before the time appointed for holding the Meeting

MBSB Annual Report 2005

10

MBSB Annual Report 2005

11

A Depositor shall qualify for entitlement to the dividend only in respect of:-

a. Shares transferred into the Depositor’s securities account before 4.00 p.m. on 26 May 2006 in respect of transfers;

b. Shares deposited into the Depositor’s securities account before 12.30 p.m. on 24 May 2006 in respect of securities exempted from mandatory deposit; and

c. Shares bought on Bursa Malaysia Securities Berhad (“the Exchange”) on a cum entitlement basis according to the Rules of the Exchange.

BY ORDER OF THE BOARD

FARIZ ABDUL AZIZ (LS 0007997)COMPANY SECRETARY

Kuala Lumpur2 May 2006

NOTICE OF DIVIDEND ENTITLEMENT AND PAYMENT

Notice is hereby given that subject to the approval of Members at the Annual General Meeting to be held on 23 May 2006, a fi rst and fi nal dividend of 2.5% less 28% income tax in respect of the fi nancial year ended 31 December 2005, will be paid on 12 June 2006 to Depositors whose names appear in the record of Depositors on 26 May 2006.

NOTE :A member entitled to attend and vote at the meeting is entitled to appoint a proxy to attend and, on a poll, to vote in his stead. A proxy may but need not be a member of the Company and a member may appoint any person to be his proxy without limitation and the provisions of Section 149(1)(b) of the Companies Act, 1965 shall not apply to the Company. Where a member appoints two proxies, the appointment shall be invalid unless he specifi es the proportions of his holding to be represented by each proxy.

In the case of a Corporate Body, the proxy appointed must be in accordance with its Memorandum and Articles of Association and the instrument appointing a proxy shall be given under the Company’s Common Seal or under the hand of an offi cer or attorney duly authorised.

The form of proxy must be deposited at the Registered Offi ce of the Company at 11th Floor, Wisma MBSB, No.48, Jalan Dungun, Damansara Heights, 50490 Kuala Lumpur not less than 48 hours before the time appointed for holding the Meeting.

MBSB Annual Report 2005

11

MBSB Annual Report 2005

12

Chairman’s Statement

“ Our aim of transforming into a customer - centric organisation has raised the bar of performance to deliver excellence beyond

expectations.

We have re - emerged to deliver value to our shareholders and customers, and have established elements of strategy to continue

our every effort to create added value and thrust for both our shareholders and customers.“

Tan Sri Abdul Halim bin AliChairman

MBSB Annual Report 2005

12

MBSB Annual Report 2005

13

OVERALL BUSINESS ENVIRONMENT 2005

The Malaysian economy continued its growth trend in 2005 albeit at a lower but more sustainable rate. Eventhough the growth momentum was held back in the second half of the year by infl ationary pressures caused by the oil price hike, overall healthy domestic and buoyant external demand pushed Malaysian economy back on track. Once again the manufacturing and services sectors continued its trend as key drivers of growth.

Due to consolidation and restructuring initiatives, Malaysia’s banking system remained strong. It enjoyed better profi ts with improvements in both profi tability and asset quality and reduced non-performing loans (NPLs) as it was supported by improved loan recovery, superior quality of loan infl ows and favourable economic and fi nancial market conditions.

The domestic property demand experienced slight decline overall due to increasing interest rates despite a promising fi rst half. Nonetheless the property market still remained strong. There was an increase in demand for property in prime locations.

REVIEW OF THE GROUP’S FINANCIAL PERFORMANCE

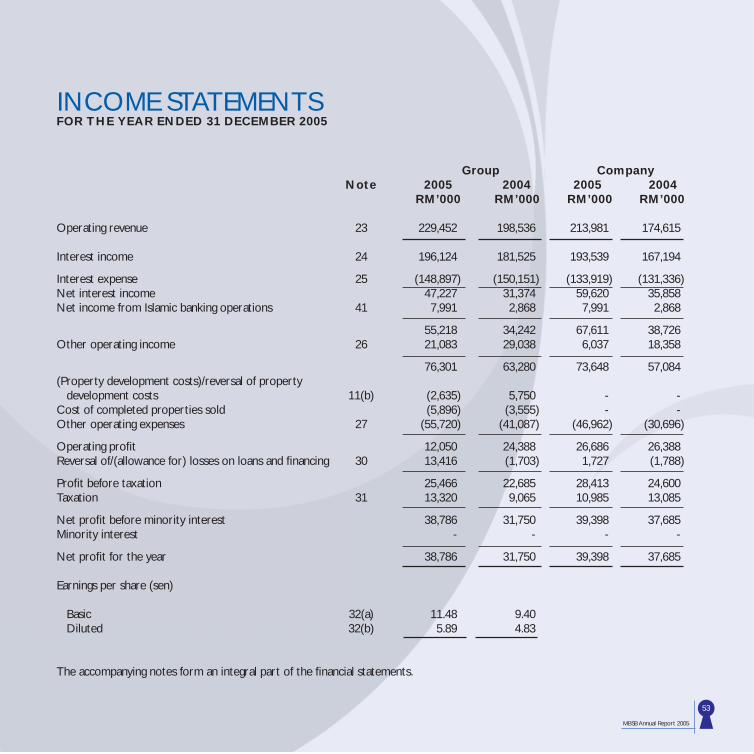

Financial Performance of the Group

For 2005, MBSB Group achieved a consolidated profi t after taxation of RM38.786 million, an increase of 22.2% as compared to the previous year of RM31.750 million. At the Company level, we also achieved a profi t after taxation of RM39.398 million for 2005, an increase of 4.5% as compared to RM37.685 million of the previous year.

CHAIRMAN’S STATEMENT

The increase in profi t was mainly due to higher interest income resulted from increase in the growth of the loan assets base (especially the retail loans) and better funding cost structure due to increase in deposits resulting in lower bank borrowings that carried higher interest cost.

The increase in recovery from losses on loans and fi nancing also contributed to the increase in the profi t. The recoveries were substantially attributed by settlement of corporate loans during the year. The recoveries together with retail collection activities have improved the Company and Group’s NPL ratios from 40% (2004) to 35% (2005) and 41% (2004) to 34% (2005) respectively.

However, the growth in profi t was partially set off by higher operating expenses such as higher staff costs from additional staff recruitment and staff training for the expanding retail loan business, additional provision for doubtful debts made for subsidiaries’ trade receivables and also impairment loss on land and property.

The profi t improvement for 2005 has resulted in a better Group return on equity of 10.3% as compared to previous year 9.3%.

Property Development Subsidiaries

The property development activities of the Company have scaled down substantially over the past few years, which is in line with the Group’s policy to refocus on its core mortgage retail business. In 2005, MBSB had successfully terminated some of the Joint Venture Arrangements (JVA) either through takeovers by JV partners or via settlements by way of foreclosing the properties pledged to MBSB.

To our shareholders,On behalf of the Board of Directors, I am pleased to present the Annual Report and Audited Financial Statements of Malaysia Building Society Berhad (MBSB) and its Group for the fi nancial year ended 31 December 2005.

MBSB Annual Report 2005

13

MBSB Annual Report 2005

14

Lending Activities

Consistent with the primary objective of the Company, retail-lending remained its core business activity. To increase market share and create added value to its services MBSB continued to improve and review its product offerings, enhance its features and extend special packages for the benefi t of its customers.

Despite a challenging year for its core business, the performance of MBSB had been positive with higher contribution mainly from retail business. The Company continued to undertake measures to improve operational effi ciencies and fi nancial performance of its business, and to compete more effectively in the ever-evolving business environment.

As of 31 December 2005, the Company’s retail loan releases had grown by RM0.981 billion or 40% and mortgage assets grew by 17% or RM4.37 billion.

Deposit Mobilisation and Savings

MBSB continued to mobilise fi xed deposits, which form the major source of funds for its operations, with the view to reduce the cost of borrowing. Strategy adopted was to capture potential depositors with long-term placements combined with effort to retain existing customer loyalty. To facilitate this, MBSB introduced innovative deposit packages with attractive returns and improved quality of services.

In addition, following the approval received from the Ministry of Finance to allow Government Agencies and Statutory Bodies to place deposits with MBSB in 2004, an aggressive marketing drive, was undertaken and the result was very encouraging. As at 31 December 2005 deposits grew by RM1.232 billion or 57% to RM3.358 billion. With increase in deposits, the bank borrowings were reduced by RM407.249 million or 33% to RM804.828 million.

Dividends

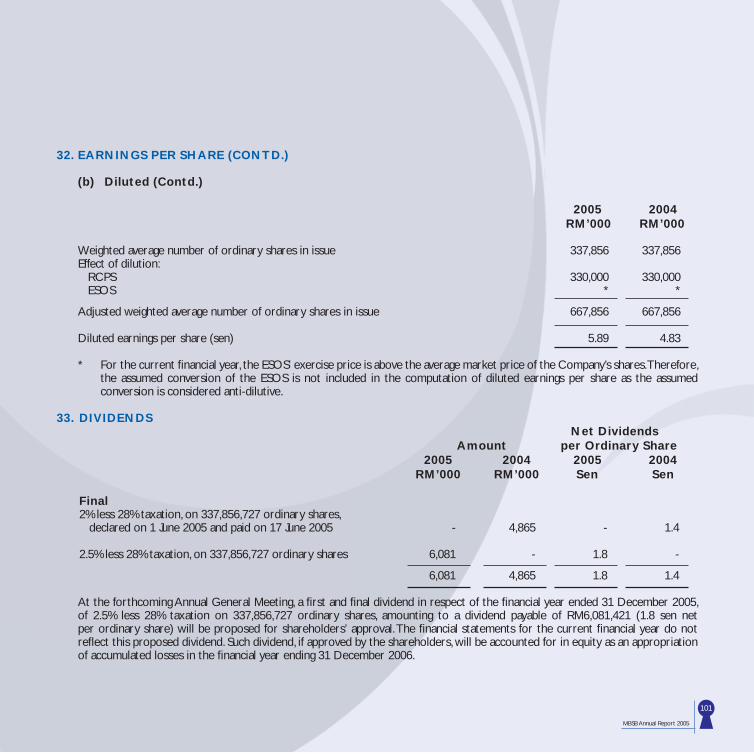

In 2005, MBSB paid fi rst and fi nal dividend of 2% less 28% income tax which amounted to RM4.865 million for the fi nancial year ended 31 December 2004. Based on MBSB’s current performance, the Board has recommended a fi rst and fi nal dividend of 2.5% less 28% income tax amounting to RM6.081 million for the fi nancial year ended 31 December 2005, for the approval of the Company’s shareholders at this Annual General Meeting.

STRATEGIC INITIATIVES

MBSB Branch Transformation

A major initiative that started in 2005 was the roll - out of the Branch Transformation Project tailored to enhance the delivery system and customer service in line with the transformation of MBSB into a customer centric organisation.

A positive and professional work culture is imperative for the success of the Branch Transformation to improve the Branch networks in terms of service level alignment with consumer needs. The process will involve changes such as the opening of new outlets and relocation of some to more strategic locations, enhancing work processes for better service delivery as well as redeployment and re-training of staff.

As part of MBSB’s new business model, it has started transforming some of its branches into hub service centres to emphasise on sales and services while unveiling the new MBSB banking concept.

MBSB continued to expand its high quality service network through the opening of its 23rd branch in Kota Kinabalu, in September 2005. MBSB will continue with its plan to invest selectively in high growth areas and to acquire high potential volume of businesses throughout its networks.

MBSB Annual Report 2005

14

MBSB Annual Report 2005

15

Product Development

MBSB needs to offer more competitive products and services in order to remain in a dominant position. We believe that a concerted push towards higher level of service combined with strong products will help MBSB chart new and more challenging territories that will steer MBSB to capitalise on a larger market.

The second quarter of the year under review saw the launch of the Home Improvement Financing and, its Islamic variant, the Home Improvement Financing-i products. These products are complementary packages to MBSB’s existing Property Financing-i and specially designed for individuals seeking fi nance to renovate, repair or furnish their homes.

In complementing the core business activities, MBSB has diversifi ed its product portfolios by moving into fee-based income products and services such as credit cards and legacy management to improve the performance of MBSB. In this connection, MBSB ventured into strategic partnerships with RHB Bank Berhad (RHB), Bank Islam Malaysia Berhad (BIMB) and Amanah Raya Berhad to promote credit card business and will writing and legacy management with MBSB acting as an agent for these products.

Human Capital Development

Fully aware of the importance of human resource as a vital asset to the organisation, MBSB has invested signifi cantly in various programmes to ensure its employees are profi cient and ready to meet the challenges ahead, towards achieving its mission and vision. MBSB conducted a series of change management programmes to ensure employees understand the change in business conditions and the processes taking place, as well as the key role they play towards the achievement of corporate goals and aspirations.

Information Technology

Tapping into the existing infrastructure of the Information Technology system, the corporate website was launched in the middle of May 2005, to facilitate customers’ quests for information on MBSB’s array of products and services available instantly and conveniently.

MBSB’s Information Technology system will continue to be improved to ensure a customer-friendly system to support the ever-expanding product portfolios.

OTHER INITIATIVES

One of the highlights of the year was the Government’s initiative towards promoting a culture of high performance in Government Linked Corporations (GLCs). This involve the implementation of Key Performance Indicators and the introduction of Performance Linked Compensation where execution and performance will be the prevailing theme moving forward. In tandem with this GLC reform theme, MBSB has embarked on its Corporate Scorecard with both quantitative and qualitative targets set for 2006.

Another major initiative undertaken during the year was the development of the Credit Risk Framework Blueprint with Business Associate Consulting Sdn Bhd. This exercise was undertaken to strengthen the risk management system and ensure MBSB implements best practices across the whole spectrum of its business as part of its commitment to good corporate governance and compliance.

Several other proposals are being developed to establish collaborations with our strategic partners to exchange knowledge on best practices and explore new business opportunities.

MBSB Annual Report 2005

15

MBSB Annual Report 2005

16

CHALLENGES AND OUTLOOK FOR 2006

To cope with a more competitive environment, there will be renewed focus on expanding the core business segments and developing new sources of revenue. Continued efforts will be in place to enhance the asset quality position and to control costs.

The Company had already seen some changes in human assets with the injection of professionals at the management and support levels. The new core values introduced and embraced by all employees focus on 5 key areas in their daily activities involving customers, work integrity, competency, teamwork and innovation of ideas.

We will continue to enhance organisational capability in key areas. Concerted efforts are ongoing in leadership developments to keep pace with the ever changing environment. Performance improvement areas tackled include process effi ciencies and cost take-out.

This year’s achievements offered MBSB and its Group of Companies the ingredients required to scale new heights in the coming years. Building on the foundation of a reliable pool of human assets, strong integrated risk management practices, good compliance and corporate governance, MBSB is poised to ride the wave of economic optimism to achieve better results in the next fi nancial year.

APPRECIATION

A key contributor to our continued strong performance is the dedication and commitment of the team that forms MBSB. Their continued determination as well as unwavering loyalty and contribution has helped MBSB achieve its growth targets.

On behalf of the Board of Directors and shareholders, I wish to express our gratitude to our management team and all our employees for their dedication and diligence, which are vital to our continued success.

My fellow Board members join me in expressing our gratitude and appreciation to YBhg Datuk Azlan Zainol for his invaluable service and contribution to the Board as MBSB’s Director, until his resignation in August 2005. At the same time, we welcome En Khalid Hj Sufat and Mr Aw Hong Boo as new members at the Board in August 2005 and November 2005 respectively. Collectively, they brought with them vast invaluable experience which I am confi dent will greatly benefi t MBSB.

Last but not least, I would like to thank our customers, clients, business associates, depositors and shareholders for their trust, continuous support and confi dence in MBSB.

Thank you.

TAN SRI ABDUL HALIM ALIChairman

Kuala Lumpur12 April 2006

CHAIRMAN’S STATEMENT (CONTD.)

MBSB Annual Report 2005

16

MBSB Annual Report 2005

17

“Poised to fulfi l our corporate strategies to become a customer - centric organisation and enhance shareholders’ value.

Our energies and resources over the past years were channelled towards positioning ourselves for future success and profi tability of MBSB.”

Encik Ahmad Farid OmarChief Executive Offi cer

MBSB Annual Report 2005

17

MBSB Annual Report 2005

18

SENIOR MANAGEMENTManagement StatementEnhancing shareholder confi dence as well as maintaining a stable platform is vital for any public listed company. We understand the responsibility entrusted upon us and we share a passion to see MBSB performing to meet its growth expectations. We pledge to improve our image, services and productivity for 2006. Our focus is to achieve effi ciency in our operations, continue to be a customer-centric organisation and pursue business growth to further enhance our revenue. We will play a signifi cant role to drive the business growth by providing the right infrastructure and culture. In our business progression journey, we consolidated our inherent strengths and determination to continue to deliver excellent returns to our customers and shareholders and we are confi dent of continuing the Company’s vision and mission.

MBSB Annual Report 2005

18

MBSB Annual Report 2005

19

From Left to Right:

Ariffa Ariffi n Assistant General Manager, Corporate Services

Abd. Rahim AmbakGeneral Manager,Credit Management

Ibarahim IshakSenior Manager, JV Special Project & Subsidiaries

Tang Yow SaiGroup Financial Controller, Finance & Information Technology

Huzaifah ZainuddinSenior Manager,Legal & Secretarial

Md Nordin Abdul JalilSenior Manager, Treasury

Shamsudin Hj. Md YusoffGeneral Manager,Branch Management & Retail

Norhayati Mohd DaudSenior Manager,Internal Audit

Zaili IsmailSenior Manager,Corporate Loans

Fatimah Nurhaliza Mohd HattaSenior Manager,Mortgage Sales Marketing & Credit Processing

Steven Lee Chui Chick Senior Manager,Rehabilitation & Recovery

Zainol Rashid NorddinSenior Manager,Credit Processing

Tan Chin KiatAssistant General Manager, Business Development & Marketing

MBSB Annual Report 2005

19

MBSB Annual Report 2005

20

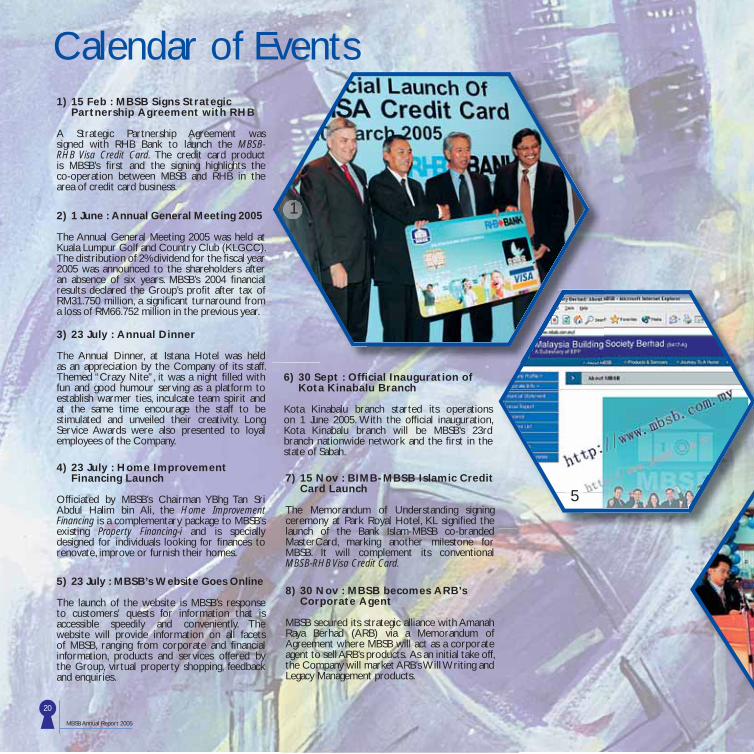

Calendar of Events1) 15 Feb : MBSB Signs Strategic Partnership Agreement with RHB

A Strategic Partnership Agreement was signed with RHB Bank to launch the MBSB-RHB Visa Credit Card. The credit card product is MBSB’s fi rst and the signing highlights the co-operation between MBSB and RHB in the area of credit card business.

2) 1 June : Annual General Meeting 2005

The Annual General Meeting 2005 was held at Kuala Lumpur Golf and Country Club (KLGCC). The distribution of 2% dividend for the fi scal year 2005 was announced to the shareholders after an absence of six years. MBSB’s 2004 fi nancial results declared the Group’s profi t after tax of RM31.750 million, a signifi cant turnaround from a loss of RM66.752 million in the previous year.

3) 23 July : Annual Dinner

The Annual Dinner, at Istana Hotel was held as an appreciation by the Company of its staff. Themed “Crazy Nite”, it was a night fi lled with fun and good humour serving as a platform to establish warmer ties, inculcate team spirit and at the same time encourage the staff to be stimulated and unveiled their creativity. Long Service Awards were also presented to loyal employees of the Company.

6) 30 Sept : Offi cial Inauguration of Kota Kinabalu Branch

Kota Kinabalu branch started its operationson 1 June 2005. With the offi cial inauguration, Kota Kinabalu branch will be MBSB’s 23rd branch nationwide network and the fi rst in the state of Sabah.

5) 23 July : MBSB’s Website Goes Online

The launch of the website is MBSB’s response to customers’ quests for information that is accessible speedily and conveniently. The website will provide information on all facets of MBSB, ranging from corporate and fi nancial information, products and services offered by the Group, virtual property shopping, feedback and enquiries.

4) 23 July : Home Improvement Financing Launch

Offi ciated by MBSB’s Chairman YBhg Tan Sri Abdul Halim bin Ali, the Home Improvement Financing is a complementary package to MBSB’s existing Property Financing-i and is specially designed for individuals looking for fi nances to renovate, improve or furnish their homes.

7) 15 Nov : BIMB-MBSB Islamic Credit Card Launch

The Memorandum of Understanding signing ceremony at Park Royal Hotel, KL signifi ed the launch of the Bank Islam-MBSB co-branded MasterCard, marking another milestone for MBSB. It will complement its conventional MBSB-RHB Visa Credit Card.

8) 30 Nov : MBSB becomes ARB’s Corporate Agent

MBSB secured its strategic alliance with Amanah Raya Berhad (ARB) via a Memorandum of Agreement where MBSB will act as a corporate agent to sell ARB’s products. As an initial take off, the Company will market ARB’s Will Writing and Legacy Management products.

1

5

MBSB Annual Report 2005

21

2

3 4

6

7

8

MBSB Annual Report 2005

22

The Board is committed to ensuring the highest standards of corporate governance and maintaining the highest level of integrityin discharging its responsibilities to protect and enhance shareholders value and the fi nancial performance of Malaysia Building Society Berhad. (the “Company”)

In the area of corporate governance, the year ended 2005 saw the implementation of the GLC Transformation Program affecting all government linked companies (GLC). The GLC Transformation Program, launched during the second half of the year ended 2005, is an initiative of the Government of Malaysia aimed at driving the development of GLCs by the introduction of specifi c guidelines and procedures designed to assist the Board of GLCs to achieve a higher standard of management. As the Company is designated as a GLC, the GLC Transformation Program would necessarily affect the manner in which the Company is managed in tandem with the prevailing laws, rules and guidelines on the management of a listed corporation. Although the said Program has only recently been implemented,the Board believes that the proper implementation of the guidelines and procedures recommended pursuant to the said Program would further enhance the manner in which the Board governs the management of the Company and the Group in the future.

Having said the above and in compliance with the Listing Requirements of Bursa Malaysia Securities Berhad, the Board is pleased to make a disclosure to shareholders the manner in which it has applied the principles of good governance and the extent to which it has complied with the best practices set out in the Malaysian Code on Corporate Governance. These principles and best practices have been applied throughout the year ended 31 December 2005 and are regularly audited and reviewed to ensure transparency and accountability.

A. Board of Directors

Composition of the Board

At the date of this Report, the Board consists of eight (8) Directors, out of which fi ve (5) are Independent Non- Executive Directors whilst the remainder are Non– Independent Non-Executive Directors.

STATEMENT OF CORPORATE GOVERNANCE

Two (2) new additions to the Board were made during the fi nancial year ended 31 December 2005, in the form of Encik Khalid Sufat and Mr Aw Hong Boo who were appointed on 18 August 2005 and 10 November 2005 respectively. Both Encik Khalid and Mr Aw bring with them a wealth of experience and knowledge in the area of banking and fi nance which the Board believes will ultimately enrich the present pool of skills and attributes of the Board. The year ended 2005 also saw the resignation of YBhg Datuk Azlan Zainol as a Director of the Company on 1 August 2005.

With further regard to the above, the number of Independent Directors who represents the majority of the members on the Board not only exceeds the requirement of Bursa Malaysia Securities Berhad but also contributes towards greater impartiality and objectivity in the Board’s decision making process.

The diversity of skills, experiences and knowledge of its members in various disciplines and professions allow the Board to address and/or to resolve the various issues that affects the Company and the Group in an effective and effi cient manner. For a brief description of the background and experience of the Board members, kindly refer to the Directors’ Profi le section of this Report.

The responsibilities of the Board includes the following:-

i) Reviewing and approving the strategic business plan of the Company and the Group as a whole. ii) Overseeing the conduct of the Company and the Group’s business to ascertain its proper management, including setting clear objectives and policies within which senior executives are to operate. iii) Identifying and approving policies pertaining to the management of all risk categories including but not limited to credit, market, liquidity, operational, legal and reputational risks. iv) Succession planning, including appointing, training and fi xing the compensation of and where appropriate, replacing senior management. v) Reviewing the adequacy and the integrity of the Company and the Group’s internal control system and management information system for compliance with applicable laws, regulations, rules, directives and guidelines. vi) Developing and implementing an investor relations programme or shareholders communications policy for the Company.

MBSB Annual Report 2005

22

MBSB Annual Report 2005

23

All Directors have complied with the minimum 50% attendance requirement at Board Meetings during the fi nancial year as stipulated by the Listing Requirements of Bursa Malaysia Securities Berhad.

Supply of Information

The Directors have full and timely access to information concerning the Company and Group. The Directors are provided with the relevant agenda and Board papers, and suffi cient time are given before Board meetings to enable them to obtain further explanation and clarifi cation to facilitate informed decision-making.

In addition, there is a schedule of matters specifi cally reserved for the Board’s decision which includes approval of loans to the Company’s customers, loan recovery strategies and restructuring schemes, approval of corporate plans and budgets, material acquisitions and disposal of assets as well as the Company’s fi nancial results. Minutes of meetings of various committees of the Company are also tabled to the Board for notation and/or endorsement.

The Board has ready and unrestricted access to all informationwithin the Company and Group as well as the advice and servicesof senior management and Company Secretaries in carrying out their duties. The Directors may also seek independent professional advice, at the Company’s expense, if and when required.

Appointment and Re-election to the Board Appointments to the Board are made based on the recommendation of the Nomination and Remuneration Committee. In accordance with the Company’s Articles of Association, one-third of the members of the Board for the time being shall retire by rotation and offer themselves for re-election.

Director’s Training

All Directors are encouraged and have during the year ended 31 December 2005 attended talks, training programs and seminars to update themselves on new developments in the business environment. In addition, seminars and conferences organised by the relevant authorities and professional bodies on, inter-alia, areas relevant to the Finance’s operations, Directors’ responsibilities, and corporate governance issues, as well as on changes to statutory requirements and regulatory guidelines, are informed to the Directors for their participation.

vii) Discussing and where appropriate, resolving all matters referred by Management to the Board that affects the interest of the Company and the Group.

There is a clear division of responsibility between the Chairman and Chief Executive Offi cer to ensure a proper balance of power and authority. Whilst the Chairman leads and guides the Board on all issues presented before them at meetings or at such other forums where the consensus of the Board is required, the Chief Executive Offi cer is in charge of the day to day management of the Company and whenever applicable, ensure that all decisions, directions and/or instructions of the Board are given effect by Management in a timely and effi cient manner.

Board Meetings The Board has at least four (4) regularly scheduled annual meetings with additional meetings being convened as and when necessary. The agenda for every Board Meeting, together with comprehensive Management reports, proposal papers and supporting documents are furnished to all Directors for their perusal well in advance of the Board meeting date, so that the Directors’ have ample time to review matters to be deliberated at the Board meeting and to facilitate informed decision making by the Directors. Minutes of every Board meeting are circulated to all Directors for their perusal prior to confi rmation of the minutes at the following Board meeting. The Board met 7 times during the fi nancial year ended 31 December 2005. The details of each Director’s attendance are given below:-

Name of Directors Total Percentage of Meetings Attendance (%) Attended

YBhg Tan Sri Abdul Halim bin Ali 7/7 100 YBhg Datuk Azlan bin Mohd Zainol 5/5 100 (Resigned w.e.f 01.08.2005) YBhg Datuk Haji A.Rahim bin Abdullah 7/7 100 Encik Lau Tiang Hua 7/7 100 Syed Zaid bin Syed Jaffar Albar 6/7 86 Puan Cindy Tan Ler Chin 5/7 71 YBhg Datuk Abdullah bin Kuntom 7/7 100 Encik Khalid bin Haji Sufat 1/1 100 (Appointed w.e.f. 18.08.2005) Encik Aw Hong Boo – – (Appointed w.e.f 10.11.2005)

MBSB Annual Report 2005

23

MBSB Annual Report 2005

24

STATEMENT OF CORPORATE GOVERNANCE

Board Committee

On 29 April 2005, the Executive Committee of the Board was formed to tackle all matters in relation to the operations of the Company and the Group. The establishment of this Committee led to the dissolution of the Loan Approval Committee as the roles and responsibilities of the said Committee was taken over by the Executive Committee of the Board in its entirety.

Pursuant to the above, the Board has established fi ve (5) committees at the date of this Report. Each committee has detailed terms of reference regarding its objectives, duties and responsibilities, authority, meeting and membership. These committees were established to assist the Board in the execution of their tasks. Notwithstanding the formation of these committees, the fi nal decision on all matters will ultimately rest with the entire Board. The following are details of each committee’s responsibilities and the members of each respective committee.

(a) Audit & Risk Management Committee

The principal functions of this Committee is to assist the Board in the effective discharge of its fi duciary responsibilities in relation to corporate governance, ensure timely and accurate fi nancial reporting, ensure the proper implementation of risk management policies and strategies in relation to the Company’s business strategies as well as the development of sound internal controls. The Committee consists of three (3) Independent Non-Executive Directors.

During the year ended 31 December 2005, seven (7) meetings were held. The members of the Audit & Risk Management Committee during the year and their attendance at the meetings are as follows:

Name of Members No of Meetings Attended

Encik Lau Tiang Hua (Chairman) 7/7 YBhg Datuk A. Rahim bin Abdullah 7/7 Syed Zaid bin Syed Jaffar Albar 6/7

(b) Nomination & Remuneration Committee

The principal functions of this Committee is to make recommendations to the Board of candidates for directorship, reviewing the Board’s composition in terms of the mix of responsibilities, skills and experience, recommendation on the appointment and remuneration of Chief Executive Offi cer and key senior management offi cers, as well as assessing the effectiveness of such individuals and their performances. The Committee consists of three (3) Independent Non-Executive Directors.

During the year ended 31 December 2005, four (4) meetings were held. The members of the Nomination & Remuneration Committee during the year and their attendance at the meeting are as follows:

Name of Members No of Meetings Attended

YBhg Datuk A. Rahim bin Abdullah 4/4 (Chairman) Encik Lau Tiang Hua 4/4 Syed Zaid bin Syed Jaffar Albar 4/4

(c) Arrears Recovery Committee

The principal function of this Committee is to ensure and when required, recommend to the Board, the best strategies to be applied in the recovery of the Company’s Non- Performing Loans (NPLs). The Committee consists of two (2) Independent Non-Executive Directors and one (1) Non-Independent Non-Executive Director.

During the year ended 31 December 2005, nine (9) meetings were held. The members of the Arrears Recovery Committee during the year and their attendance at the meetings are as follows:

Name of Members No of Meetings Attended

Encik Lau Tiang Hua (Chairman) 9/9 Syed Zaid bin Syed Jaffar Albar 9/9 Puan Cindy Tan Ler Chin 9/9

(CONTD.)

MBSB Annual Report 2005

24

MBSB Annual Report 2005

25

(f) The Loan Approval Committee This Committee was dissolved on 29 April 2005.

The function of this Committee was to exercise powers of credit approvals as authorised by the Board.

Three (3) meetings were held by the Committee during the year ended 2005 prior to its dissolution. The members of the Loan Approval Committee during the year and their attendance at the meetings are as follows:

Name of Members No of Meetings Attended

Syed Zaid Bin Syed Jaffar Albar 3/3 (Chairman) YBhg Datuk Abdullah Kuntom 3/3 Encik Lau Tiang Hua 3/3 Puan Cindy Tan Ler Chin 3/3

B. Directors’ Remuneration

Objective of Directors’ Remuneration

The Company’s remuneration policy for Directors is tailored at levels that will enable the Company to attract and retain the Directors with relevant experience and expertise needed to assist in managing the Company effectively.

Remuneration Package

The Remuneration Package are as follows:-

(a) Directors’ Fee

The Directors will each be paid an annual fee, the quantum of which is subject to the approval by the shareholders at a General Meeting. In the event that a Director is appointed or resigns during a fi nancial year, the fee will be pro-rated and apportioned accordingly based on the date of the said Director’s appointment or resignation.

MBSB Annual Report 2005

25

(d) ESOS Committee

The principal function of this Committee is to administer the Company’s Employees’ Share Option Scheme in accordance with the Scheme’s by-laws. The Committee consists of two (2) Independent Non-Executive Directors and one (1) Non-Independent Non-Executive Director.

No Meetings were held by this Committee during the year ended 31 December 2005 as the Committee was not called upon to administer any allocation to eligible employees within the said year.

Name of Members YBhg Datuk A. Rahim bin Abdullah (Chairman) Syed Zaid bin Syed Jaffar Albar Puan Cindy Tan Ler Chin

(e) Executive Committee of the Board This Committee was established on 29 April 2005. The principal functions of this Committee is to allow the Board to deliberate specifi cally on issues and matters relating to the operational requirements of the Company. Prior to his resignation, YBhg Datuk Azlan Zainol was appointed as the Chairman of the Committee. The Chairmanship was then taken over by YBhg Tan Sri Abdul Halim Bin Ali upon the former Director’s resignation from the Board.

During the year ended 31 December 2005, seven (7) meetings were held by the Committee. The members of the Executive Committee during the year and their attendance at the meetings are as follows:

Name of Members No of Meetings attended

YBhg Tan Sri Abdul Halim bin Ali 6/6 (Chairman) Encik Lau Tiang Hua 1/1 (withdrew as member w.e.f 08.06.2005) Syed Zaid bin Syed Jaffar Albar 6/7 YBhg Datuk Azlan bin Mohd Zainol 2/2 (Chairman. Withdrew as member w.e.f 08.06.2005) Puan Cindy Tan Ler Chin 4/7 YBhg Datuk Abdullah bin Haji Kuntom 5/7 Encik Khalid bin Haji Sufat 5/5

MBSB Annual Report 2005

26

(b) Allowance

The Directors will be paid a meeting allowance for their attendance at all Meetings of the Board as well as Board Committees. The quantum of the allowance is recommended by the Nomination & Remuneration Committee for the approval of the Board.

(c) Details

The details of the remuneration of each Director of the Company who served during the fi nancial year ended 31 December 2005 are set out in page 96 of this Annual Report.

C. Shareholders

Relationship with Shareholders and Investors

The Board recognizes the importance of communication and proper dissemination of information to its shareholders and investors. Through extensive disclosures of appropriate and relevant information, the Company and the Group aims to effectively provide shareholders and investors with information to fulfi ll transparency and accountability objectives. In this respect, the Company keeps shareholders informed via announcements and timely release of quarterly fi nancial results, press releases, annual reports and circulars to shareholders.

Annual General Meeting

The Annual General Meeting of the Company represents the principal forum for dialogue and interaction with all shareholders. Shareholders are given ample time to participate in the question and answer sessions. Any queries or concerns relating to the Company may be conveyed to the Company Secretary.

STATEMENT OF CORPORATE GOVERNANCE

D. Accountability and Audit Financial Reporting

The Board is required by the Companies Act 1965 to prepare fi nancial statements for each fi nancial year to give a true and fair view of the state of affairs of the Company.

The Board takes responsibility for presenting a fair assessment of the Company’s operations and fi nancial statements released to shareholders.

The Board is responsible to ensure that the Company keeps proper accounting records, which disclose with reasonable accuracy the fi nancial position of the Company and which enable them to ensure that the fi nancial statements comply with the Companies Act 1965 and other regulatory requirements. The Audit & Risk Management Committee of the Board assists by scrutinising the information to be disclosed, to ensure accuracy and adequacy.

Internal Control

The Board has the overall responsibility of maintaining a system of internal controls that provides reasonable assurance of effective and effi cient operations, and compliance with laws and regulations, as well as with internal procedures and guidelines. The effectiveness of the system of internal controls of the Group is reviewed periodically by the Audit & Risk Management Committee. The review covers the fi nancial, operational and compliance controls as well as risk management.

The Statement of Internal Control as set out in this Annual Report provides an overview of the state of internal controls within the Group.

Relationship with Auditors

The role of the Audit & Risk Management Committee in relation to the internal and external auditors is described in the Audit & Risk Management Committee Report section of the Annual Report. The Board maintains a formal and transparent relationship with its auditors in seeking professional advice and ensuring compliance with the accounting standards in Malaysia.

(CONTD.)

MBSB Annual Report 2005

26

MBSB Annual Report 2005

27

Directors’ Responsibility Statement

The Directors are required by the Companies Act 1965 to prepare fi nancial statements for the fi nancial year which have been made out in accordance with the applicable approved accounting standards and give a true and fair view of the state of affairs of the Company and the Group at the end of the fi nancial year and of the results and cash fl ows of the Company and the Group for the fi nancial year.

In preparing the fi nancial statements, the Directors have used appropriate and relevant accounting policies that are consistently applied and supported by reasonable as well as prudent judgements and estimates, and that all accounting standards which they consider applicable have been followed during the preparation of the fi nancial statements.

The Directors are responsible for ensuring that the Company and the Group keep proper accounting records which disclose with reasonable accuracy the fi nancial position of the Group and Company and which enable them to ensure that the fi nancial statements comply with the Companies Act 1965.

The Directors have the general responsibility for taking such steps as are reasonably open to them to safeguard the assets of the Group, to detect and prevent fraud and other irregularities.

E. Statement on Compliance with the Best Practices of the Malaysian Code on Corporate Governance

Having reviewed the governance structure and practices of the Company, the Board considers that it has complied with the best practices as set out in the Code as well as the items set out in Part A of Appendix 9C of the Listing Requirements of Bursa Malaysia Securities Berhad in relation to the requirement of a separate disclosure in the Annual Report.

This statement is made in accordance with the resolution of the Board of Directors dated 17 March 2006.

MBSB Annual Report 2005

27

RESPONSIBILITY

The Board of Directors (“Board”) acknowledges the responsibility for maintaining a sound system of internal control and ensuring its effectiveness. The Board also places importance for risk management practices and corporate governance in the Company and its Subsidiaries (“the Group”). The system of internal control includes fi nancial controls, operational effi ciency, effectiveness, systems and process improvements, audit and risk management. These ongoing processes have been in place for the fi nancial year under review. The internal control framework only manages rather than eliminate the risk of failure to achieve business goals. It can only provide a reasonable and not an absolute assurance against material misstatement of management and fi nancial information or against fi nancial losses and fraud.

The Board also acknowledges that the system of internal control in place for the year is sound and suffi cient to safeguard shareholders’ investments, customers’ interests and the Group’s assets.

KEY INTERNAL CONTROL PROCESSES

The process governing the effectiveness and integrity of the system of internal control is through the establishment of the following committees:

• Audit & Risk Management Committee (ARMCO)

ARMCO is represented by three (3) Independent Non-Executive Directors and one (1) Non-Independent Non-Executive Director. ARMCO’s principal functions are as follows:

• To oversee the fi nancial reporting and internal control system of the Group.

• To oversee the adequacy of risk management processes and effectiveness.

• To support and maintain the independence of the internal and external audit functions.

• To deliberate and address signifi cant breaches and risks identifi ed.

STATEMENT ON INTERNAL CONTROL (SIC)

• Executive Committee of the Board (EXCO)

On 29 April 2005, the EXCO was established to tackle all matters in relation to the operations of the Company and the Group. The establishment of this Committee led to the dissolution of the Loan Approval Committee as the roles and responsibilities of the said Committee were taken over by the EXCO in its entirety. The EXCO comprises at least three (3) Board members and its principal functions are as follows:-

• To consider and approve capital expenditure of the Company and the Group as referred to it by Management.

• To deliberate, consider and approve new credit proposals for facility up to its authority limit.

• To consider and approve terms for restructuring of non-performing Corporate and Retail loans, etc.

• To notify the Board of such approvals and to make appropriate recommendations to the Board for consideration and approvals of new credit facilities above the EXCO’s authority limit.

• Arrears Recovery Committee (ARC)

ARC comprises three (3) Independent Non-Executive Directors and one (1) Non-Independent Non-Executive Director. ARC’s principal function is to decide on the restructuring of the non-performing loans of the Group and the strategies to be adopted in the recovery process. It also monitors the performance of the restructured loans.

• Key Supervisory Committees

MBSB has two (2) key supervisory management committees, which are chaired by the Chief Executive Offi cer to support and monitor the controls that have been put in place.

MBSB Annual Report 2005

28

MBSB Annual Report 2005

29

• Management Committee (MANCO)

MANCO is the highest authority of reference at Management level where procedural, operational and personnel issues and matters are deliberated and decided upon.

• Asset and Liability Committee (ALCO)

ALCO serves as the primary oversight and decision making body that provides strategic direction for the management of assets and liabilities of the Group which include asset quality, funding portfolio, liquidity and interest rate exposure.

INTERNAL AUDIT

Internal Audit Department, reporting to ARMCO, assists the Board in monitoring and managing business risks and internal controls. The department performs scheduled review of operations and compliance with policies and procedures to assess the effectiveness of internal controls. ARMCO approves the Internal Audit Plan each year.

Regular internal audit visits are systematically arranged over the period to oversee compliance with policies and procedures and to assess the integrity of both fi nancial and non-fi nancial informa-tion provided. The results of each audit are submitted to ARMCO for attention and signifi cant fi ndings are deliberated upon. The minutes of ARMCO meetings are formally tabled to the Board for noting, and for action by the Board, where necessary. Follow-up actions were undertaken periodically to ensure full compli-ance.

The scope of Internal Audit covers the audit of MBSB depart-ments and branches and is prioritized based on audit risk assess-ments. Internal Audit’s responsibilities include the audit of opera-tions, credit, fi nancial controls, management directives, regulatory compliance and information technologies.

OTHER KEY AREAS OF INTERNAL CONTROL

• The Board reviewed and approved business plans within which the business objectives, strategies and targets are articulated. These plans are communicated across the organisation to ensure effective implementation through MANCO and Management meetings.

• Regular and comprehensive management reports to the Board, covering fi nancial performance, which allows for effective monitoring of signifi cant variances against budgets and plans. The budget is reviewed and updated with performance monitored and explanation sought for signifi cant differences.

• Defi nes delegation of responsibilities to committees of the Board and Management, including fi nancial authority limits, organisation structures and appropriate authority levels.

• Regular update of internal policies and procedures to refl ect changing risks or to resolve operational defi ciencies. Documentation of key business processes and policies for standardisation of practices and identifi cation of process improvement opportunities.

• Reports on fi nancial and operating performance are regularly provided to Board to enable them to review the Group’s progress. In addition, reports on monitoring of compliance such as capital adequacy and other regulatory requirements are tabled to ARMCO and the Board at their monthly or periodic meetings. Quarterly fi nancial statements are assessed through ARMCO who then recommends to the Board for adoption.

• Monitoring of regulatory and statutory compliance through Internal Audit and Risk Management Departments to support ARMCO and Board on proper management of effective corporate governance practices and requirements.

• The Group is keeping abreast of developments and changes in legislation, which may affect the Group’s operations and seek to minimise legal and regulatory risk through consultation with internal and external lawyers to ensure compliance with all applicable rules and regulations.

MBSB Annual Report 2005

29

MBSB Annual Report 2005

30

RISK MANAGEMENT

The Board had embarked on an ongoing process to identify, evaluate and manage signifi cant risks that affect the achievement of the Group’s business objectives. The process includes the review on the adequacy of the present internal control system to manage principal risks inherent in all operations of the Group. ARMCO oversees the implementation of the functions of Risk Management through the Risk Management Department. The Department oversees the establishment of Risk ManagementFramework and identify and implement action plans to specifi cally address credit risks affecting the Group.

The Risk Management Framework that is supplemented by a Credit Risk Management Framework, provides for regular review and reporting through ALCO and includes an assessment of risk, an evaluation of the effectiveness of the controls in place and the requirements for further controls.

• Market Risk

ALCO reviews the dynamic cash-fl ow projections and the maturity mismatch analysis on monthly basis to monitor liquidity and mismatch of funds in MBSB. ALCO ensures maximisation of interest margin through effective management of funding and liquidity.

• Credit Risk

For retail credit risk, the application of credit scoring system embedded in the computerised banking system serves as a recommendation guide to assist the Management to screen through credit applications.

EXCO has been established for monitoring credit risk exposure and approval of loans through credit risk analysis to ensure good credit within their approval limit.

Risk parameters such as single customer limit, maximum tenure, acceptable structures and collateral types for accepting credit risk are clearly defi ned and complemented by policies and processes to ensure that MBSB maintains a well diversifi ed and quality credit portfolio.

STATEMENT ON INTERNAL CONTROL (SIC)

• Operational Risk

The primary responsibility for managing operational risks rests with the business and support units to re-engineer and improve the workfl ow processes without compromising on risks and controls. The processes are benchmarked, the roles and responsibilities are clearly defi ned and communicated. The process aims to ensure that the risks associated with new products or services are identifi ed, analysed and managed.

MBSB minimises operational risk by putting in place appropriate policies, internal controls and procedures that are constantly being reviewed by process-owners.

Management has exerted continuous effort to identify company-wide operational risk and undertake measures to mitigate and monitor the identifi ed risks. During the year under review, the following actions were carried out: -

• The continued enhancement of the existing fully integrated core information system with adequate checks and over-riding authorisation to further mitigate the operational risks.

• Completion of the Credit Risk Management Framework and implementation of a new mortgage credit scorecard.

• The assets and properties of MBSB are protected through appropriate insurance coverage.

Legal and regulatory risks of its business are actively being managed by MBSB. Legal risk is minimised through consultation with internal and external legal counsels and the use of industry standard agreements for fi nancial products.

Notwithstanding the above, these internal control measures only manage and do not entirely eliminate the risk of internal control. Continuous efforts are undertaken to ensure standardisation, timeliness and comprehensiveness of key internal control procedures including authorisation, accountability, monitoring and reconciliation processes.

This statement is made in accordance with the resolution of the Board of Directors dated 6 April 2006.

(CONTD.)

MBSB Annual Report 2005

30

MBSB Annual Report 2005

31

The Committee

The Board shall establish an Audit & Risk Management Committee of at least three (3) directors, a majority of whom are independent, with written terms of reference which deal clearly with its authorities and duties. The Chairman of the Committee should be an independent Non-Executive Director.

Meetings

The quorum for a meeting shall be two (2) members whereby at least one of the members present must be an Independent Non-Executive Director. The Committee may, as and when considered necessary, invite other Board members and request the presence of the Chief Executive Offi cer, Management Team and Internal Audit & Risk Management Team to attend meetings to brief the Committee on activities involving their areas of responsibility. The presence of external auditors will be requested when required.

The Head of the Internal Audit Department is the Secretaryto the Committee. The Secretary shall prepare an agenda, which shall be circulated with the relevant papers prior to each meeting, to members of the Committee. The minutes of the meeting shall be circulated to the Board of Directors.

Composition / Attendance

Members of the Committee during the fi nancial year ended 31 December 2005 and attendance record of each member are as follows: -

REPORT OF THE AUDIT & RISK MANAGEMENT COMMITTEE

Terms of References

1. Objectives

The primary objectives of the Committee are to: -

i) Assist the Board of Directors in fulfi lling its fi duciary responsibilities particularly in the areas of accounting and management control and fi nancial reporting;

ii) Reinforce the independence and objectivity of the Internal Audit Department and Risk Management Department;

iii) Acts as a focal point for communication between external auditors, internal auditors, Directors and Management on matters concerning accounting, management reporting and internal controls and to provide a forum for discussion, independent of the Management; and

iv) Undertake additional duties as may be deemed appropriate and necessary to assist the Board of Directors in ensuring transparency and proper internal control.

2. Rights

The Committee shall: -

i) Have authority to investigate any matter within its terms of reference;

ii) Have the resources, which are required to perform its duties;

iii) Have full and unrestricted access to any information pertaining to the Group;

iv) Have direct communication channels with external auditors, internal auditors and risk managers;

v) Be able to obtain independent professional or other advices; and

vi) Be able to convene meetings with external auditors, excluding the attendance of executive members of the Committee, whenever deemed necessary.

Number of Meetings Attended / Held

Encik Lau Tiang Hua 7/7(Chairman / Independent Non-Executive Director)

Y. Bhg Datuk Haji A. Rahim bin Abdullah 7/7(Member / Independent Non-Executive Director)

Syed Zaid bin Syed Jaafar Albar 6/7(Member / Independent Non-Executive Director)

Composition of The Committee

MBSB Annual Report 2005

31

MBSB Annual Report 2005

32

3. Duties and Responsibilities

The following are the main duties and responsibilities of the Committee: -

i) To review with external auditors, their audit plan, scope and nature of the audit;

ii) To review with external auditors, their audit report and audit fi ndings and Management’s response thereto;

iii) To review the Group’s Quarterly fi nancial reports and the Group’s annual audited fi nancial statements before submission to the Board of Directors for approval, focusing on: -

a) Changes in accounting policies and practices,

b) Signifi cant adjustments and issues arising from the audit,

c) Signifi cant and unusual events,

d) Compliance with applicable approved accounting standards, and

e) Compliance with Bursa Malaysia Securities Berhad’s listing requirements.

iv) To review any related party transactions and confl ict of interest situation that may arise within the Group including any transaction, procedures or course of conduct that raise questions on Management’s integrity;

v) To consider the appointment of external auditors, their audit fee and any question of their resignation or dismissal;

vi) To recommend the nomination of a person or persons as external auditors;

vii) To review the adequacy of the scope and resources of the Internal Audit Department and that it has the necessary authority to carry out its functions;

viii) To review the internal audit programmes and processes, and the fi ndings of the internal audit or investigation undertaken and whether appropriate action has been taken on the recommendation of the Internal Audit Department;

ix) To review the signifi cant risks identifi ed by the Group and their impact on the operations;

x) To ensure that the identifi ed risks are monitored and mitigated on an on going basis;

xi) To ensure risk exposures of the Group are within parameters set by the Board;

xii) To review operational policies and processes of the Group and to formulate new ones where appropriate with a view to improve effi ciency, cost effectiveness and control over the resources of the Group; and

xiii) To undertake any other activities as delegated by the Board.

Activities

During the fi nancial year, the Committee had fulfi lled its obligations in accordance with its terms of reference. The following is a summary of the activities that had been carried out by the Committee: -

i) Reviewed the external auditor’s audit planning memorandum for the year ended 31 December 2005.

ii) Reviewed the external auditors’ reports in relation to audit and accounting issues arising from their audit works and updates of new developments on fi nancial reporting standards.

iii) Reviewed the quarterly and annual fi nancial reports prior to recommending to the Board for approval.

iv) Reviewed the Internal Audit Department’s resource requirements, annual Internal Audit Plan and Budget and the annual performance assessment of the Internal Audit Department.

v) Reviewed internal audit reports, which outlined the audit issues, recommendations and Management’s response thereof. Discussed with Management, actions taken to improve the systems of internal controls based on the Internal Auditors’ recommendations as identifi ed in the internal audit reports.

vi) Reviewed the adequacy and effectiveness of the internal control systems and risk management framework.

REPORT OF THE AUDIT & RISK MANAGEMENT COMMITTEE (CONTD.)

MBSB Annual Report 2005

32

MBSB Annual Report 2005

33

Internal Audit Functions

The Internal Audit Department’s principal responsibility is to conduct audits on internal control matters to ensure compliance with the systems and standard operating procedures as laid down by the Group. The main objective of these audits is to provide reasonable assurance to the Board of Directors that the Group operates satisfactorily and effectively. The Internal Audit Department is also responsible for providing comfort that the Group has an adequate and functioning internal control to protect the Group’s investment in information technology and information managed on technology platforms. The audits are carried out based on audit plans, which have been reviewed and approved by the Committee.

Unscheduled audits and investigations were also made at the request of the Committee on areas of concern identifi ed by the Committee.

The Internal Audit Department forms strategic alliance with Risk Management and Organisation & Methods Departments in reviewing the adequacy and effectiveness of the internal control systems and risk management framework to ensure there is systematic methodology in identifying, assessing and mitigating / controlling all types of risks.

The Internal Audit Department maintains a close working relationship with the Committee and this facilitates the fulfi lment of the Committee’s responsibility in ensuring good corporate governance practices are observed and ultimately the well-being of the Group.

MBSB Annual Report 2005

33

MBSB Annual Report 2005

34

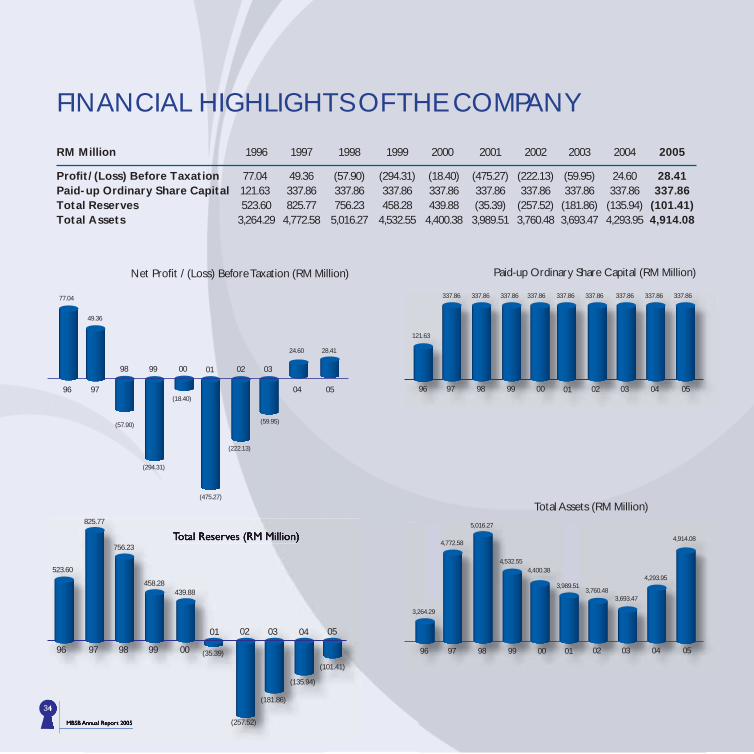

FINANCIAL HIGHLIGHTS OF THE COMPANY

RM Million 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005