real estate 199a aggregation and 469 grouping rules: real

TRANSCRIPT

WHO TO CONTACT DURING THE LIVE EVENT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 ext. 1 (or 404-881-1141 ext. 1).

Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

Real Estate 199A Aggregation and 469 Grouping Rules: Real Estate Professionals and Safe Harbor ElectionTHURSDAY, OCTOBER 17, 2019, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

FOR LIVE PROGRAM ONLY

October 17, 2019

Real Estate 199A Aggregation and 469 Grouping Rules: Real Estate Professionals and Safe Harbor Election

Brian T. Lovett, CPA, JD, Partner

WithumSmith+Brown

Guinevere M. Moore, Partner

Johnson Moore

Kira Wheat, Senior Tax Manager

DHJJ

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Agenda

5

• Final Section 199A regulations• Notice 2019-07• Aggregation under Section 199A• Grouping under Section 469• Deductible expenses• Depreciation• Tax planning for real estate owners after

TCJA

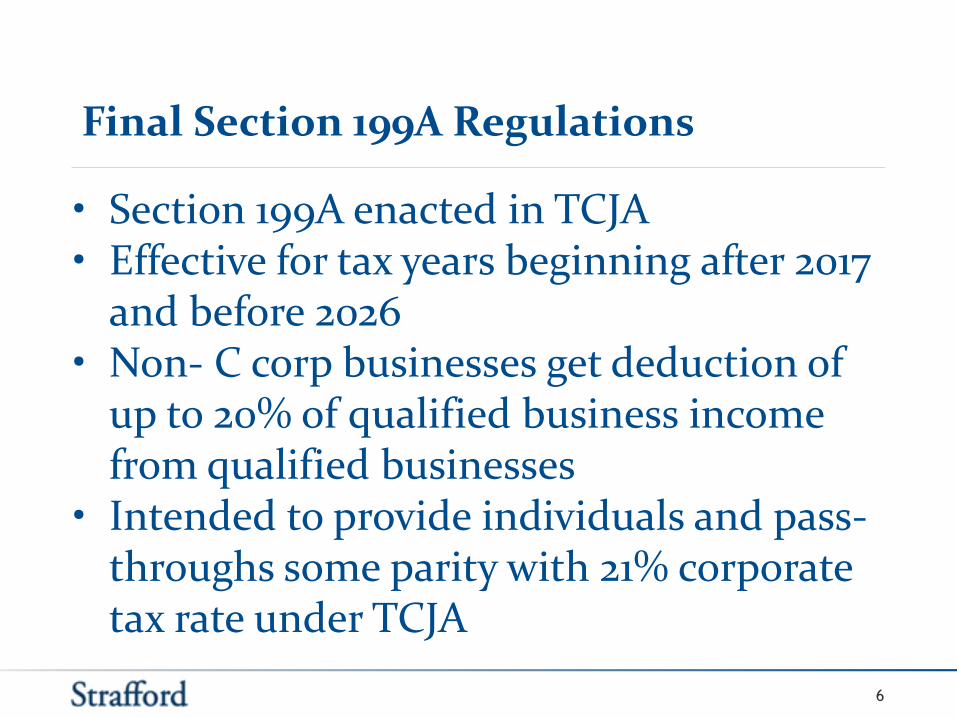

Final Section 199A Regulations

6

• Section 199A enacted in TCJA• Effective for tax years beginning after 2017

and before 2026• Non- C corp businesses get deduction of

up to 20% of qualified business income from qualified businesses

• Intended to provide individuals and pass-throughs some parity with 21% corporate tax rate under TCJA

Final Section 199A Regulations

7

• The deduction results in an effective maximum tax rate of 29.6% (i.e., 37% x (1- 20%)) to individuals.– This compares favorably to C corporations who distribute out

their income as dividends. They end up at a 39.8% effective tax rate.

• The statute gives eligible taxpayers a deduction equal to the lesser of:– 20% of the combined qualified business income (“QBI”)

component of the taxpayer, or– 20% of taxable ordinary income.

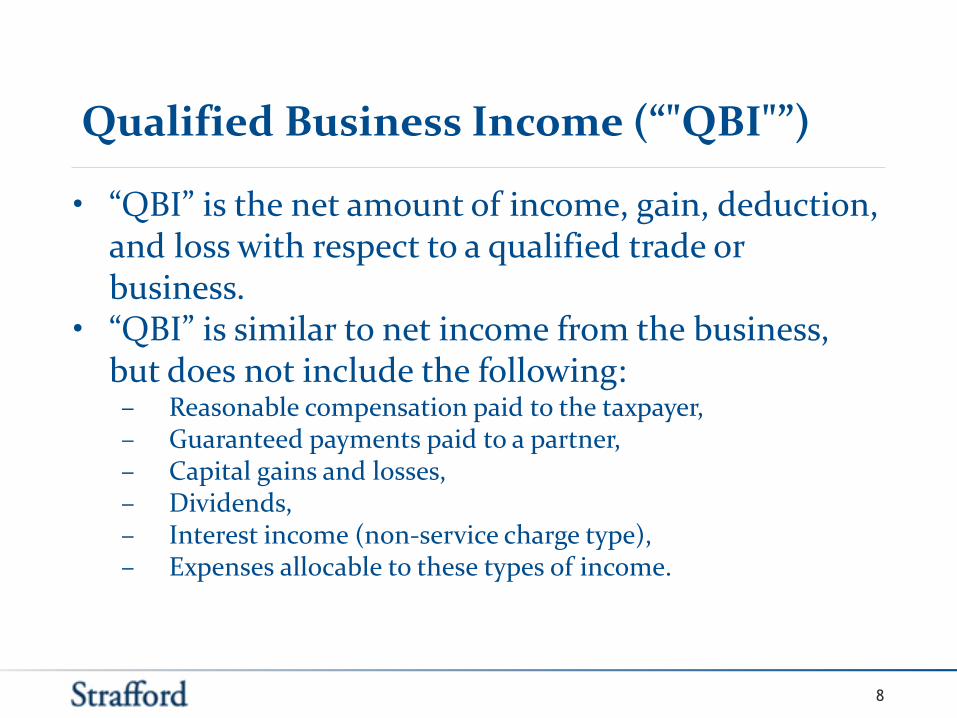

Qualified Business Income (“"QBI"”)

8

• “QBI” is the net amount of income, gain, deduction, and loss with respect to a qualified trade or business.

• “QBI” is similar to net income from the business, but does not include the following:– Reasonable compensation paid to the taxpayer,– Guaranteed payments paid to a partner,– Capital gains and losses,– Dividends,– Interest income (non-service charge type),– Expenses allocable to these types of income.

Qualified Trade or Business (“T/B”)

9

• What is a “Qualified Trade or Business”?– This is a facts and circumstances determination.

Generally to be regarded as a T/B, the individual must be involved in the activity with continuity and regularity for the primary purpose of engaging in the activity for profit.

– Sporadic or hobby type of activities would not be a T/B.

– Managing one’s own investments, even though substantial, is not a T/B.

– Some rental real estate may not be regarded as a T/B.

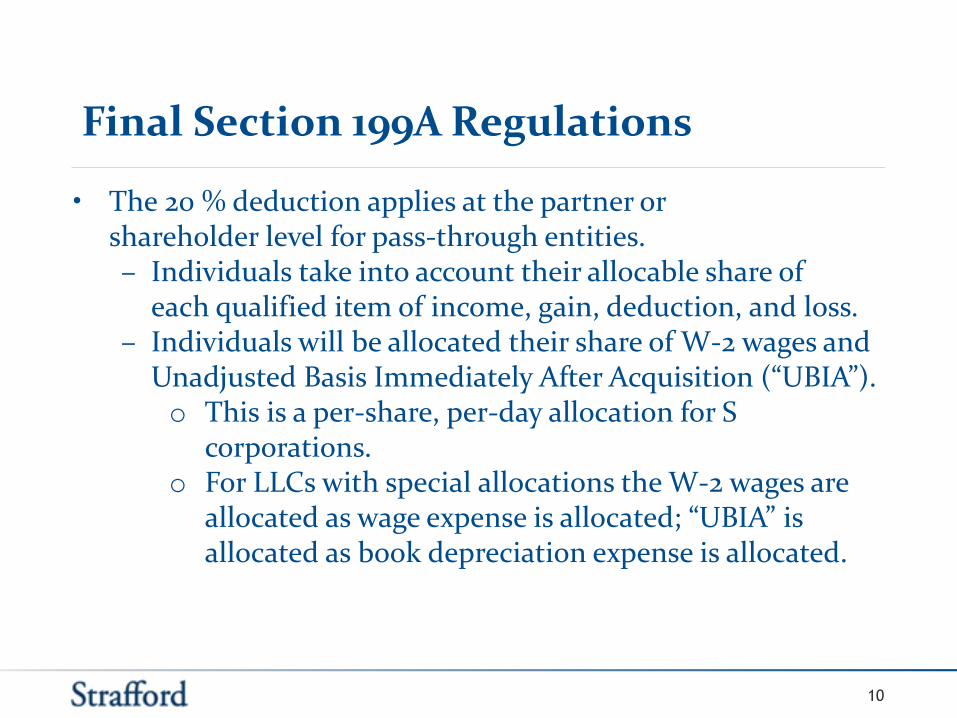

Final Section 199A Regulations

10

• The 20 % deduction applies at the partner or shareholder level for pass-through entities.– Individuals take into account their allocable share of

each qualified item of income, gain, deduction, and loss.– Individuals will be allocated their share of W-2 wages and

Unadjusted Basis Immediately After Acquisition (“UBIA”).o This is a per-share, per-day allocation for S

corporations.o For LLCs with special allocations the W-2 wages are

allocated as wage expense is allocated; “UBIA” is allocated as book depreciation expense is allocated.

Pass-Through Entities

11

• S corporations and partnerships must report each shareholder’s or partner’s share of the following items for each qualified T/B (or aggregated T/B) on Schedule K-1 so that the shareholder or partner may figure their deduction.– §199A “QBI”– §199A W-2 wages– §199A “UBIA”– Disclosure if any T/B is a specified service T/B– Disclosure of information for aggregated trades or

businesses

Pass-Through Entities

12

• The deduction does not affect basis calculations.– If an S corporation distributed out 100% of its

“QBI” but then also have to reduce basis by the§199A deduction. The result would be adistribution in excess of income creating a taxable event.

– The 20% deduction may potentially be limited for Specified Service Trades or Businesses (“SSTB”)

Specified Service Trades/Businesses (“SSTB”)

13

o Health

o Law

o Accounting

o Actuarial science

o Consulting

o Athletics

o Performing arts

o Financial services

o Brokerage services

o Investing and investment management trading or dealing in securities, commodities, etc.

o Principal asset being the reputation/skill of one or more EE’s.

Brokerage SSTB

14

• Includes services in which a person arranges transactions between a buyer and a seller with respect to securities for a commission or fee including services provided by stock brokers and other similar professionals.

• Excludes services provided by real estate agents and brokers, or insurance agents and brokers.

Investment Management SSTB

15

• Includes investing and investment management, in which a fee is received for providing investing, asset management, or investment management services, including providing advice with respect to buying and selling investments.

• Excludes the service of directly managing real property.

Dual T/Bs SSTB & Non-SSTB

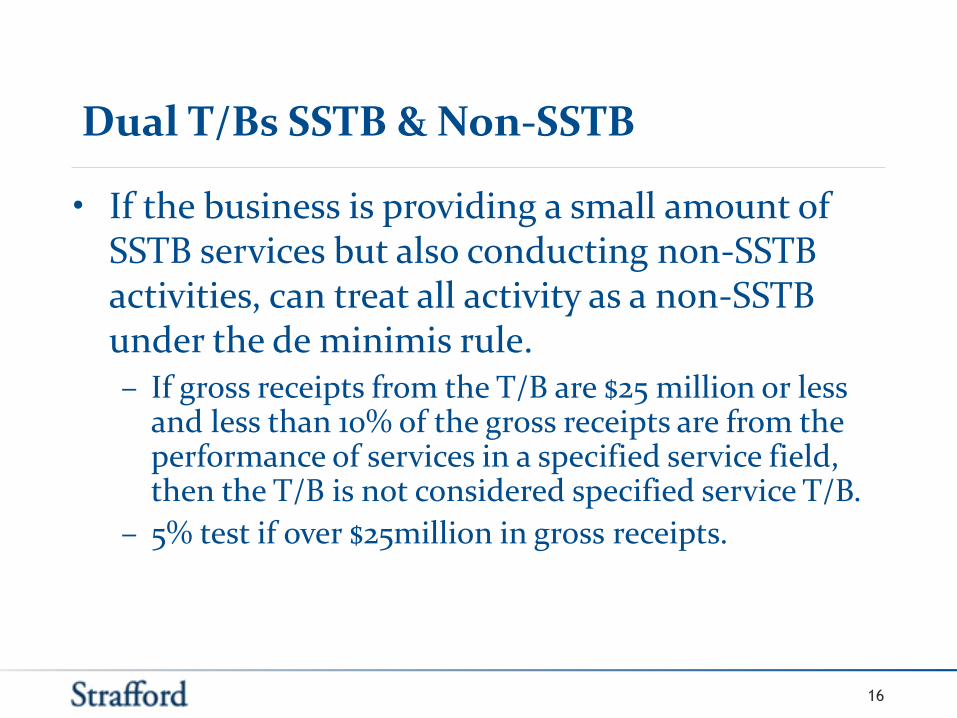

16

• If the business is providing a small amount of SSTB services but also conducting non-SSTB activities, can treat all activity as a non-SSTB under the de minimis rule.– If gross receipts from the T/B are $25 million or less

and less than 10% of the gross receipts are from the performance of services in a specified service field, then the T/B is not considered specified service T/B.

– 5% test if over $25million in gross receipts.

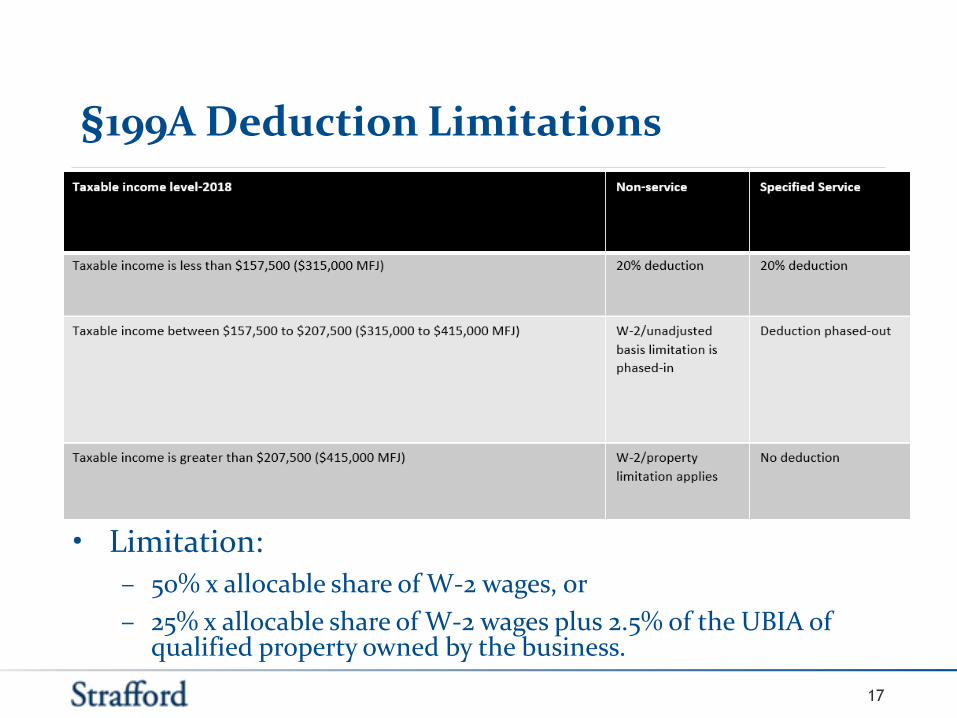

§199A Deduction Limitations

17

• Limitation:

– 50% x allocable share of W-2 wages, or

– 25% x allocable share of W-2 wages plus 2.5% of the UBIA of qualified property owned by the business.

Definitions – W-2 Wages

18

• Qualified wages are amounts paid to an employee including elective deferrals, SEPs, Roth contributions, deferred compensation. Excludes management fees, independent contractor payments, etc.

• §199A(b)(4)(C) provides that an amount is not a W-2 wage unless it is reflected on a payroll taxreport.

Definitions – W-2 Wages

19

• For taxpayers conducting more than one T/B, the W-2 wages must be allocated among the various trades or businesses (or aggregated trades or businesses).

• Only the W-2 wages properly allocable to ""QBI"" are includible.– W-2 wages are properly allocable to ""QBI"" if the

associated wage expense is taken into account incomputing ""QBI"".

Definitions – Qualified Property

20

• Tangible, depreciable property which is held bythe T/B at the end of the year and which is used, at any point in the year, in the production of ""QBI"".

• The “regular depreciable period" of the propertymust not have ended prior to the last day of theyear.

• The depreciable period starts on the date theproperty is placed in service and ends on the later of:

– 10 years, or

– the last day of the last full year in the asset's "regular" (not “ADS”) depreciation period.

Definitions – Qualified Property

21

• Example – Essco, an S corporation, purchases a piece of machinery on November 18, 2014. The machinery is used in the T/B and is depreciated over 5-years. Even though the depreciable life of the asset is only 5-years, the owners of Essco will be able to take the unadjusted basis of $10,000 into consideration for purposes of this second limitation for ten full years, from 2014-2023, because the qualifying period runs for the longer of the regular useful life (5-years) or10 years.

Definitions – Qualified Property

22

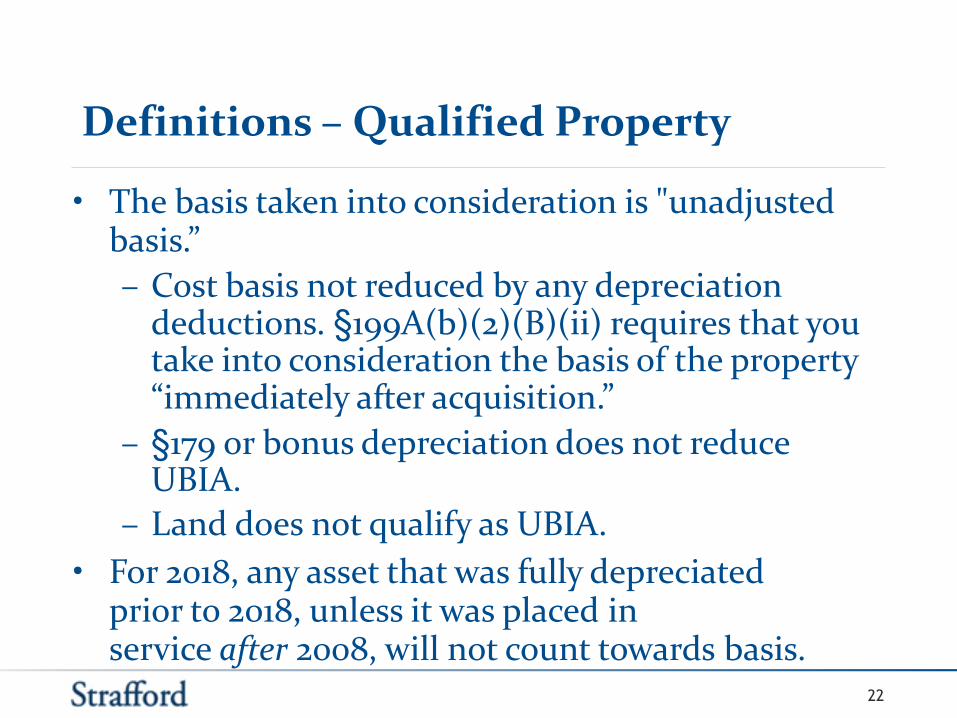

• The basis taken into consideration is "unadjusted basis.”

– Cost basis not reduced by any depreciation deductions. §199A(b)(2)(B)(ii) requires that you take into consideration the basis of the property “immediately after acquisition.”

– §179 or bonus depreciation does not reduce UBIA.

– Land does not qualify as UBIA.

• For 2018, any asset that was fully depreciated prior to 2018, unless it was placed inservice after 2008, will not count towards basis.

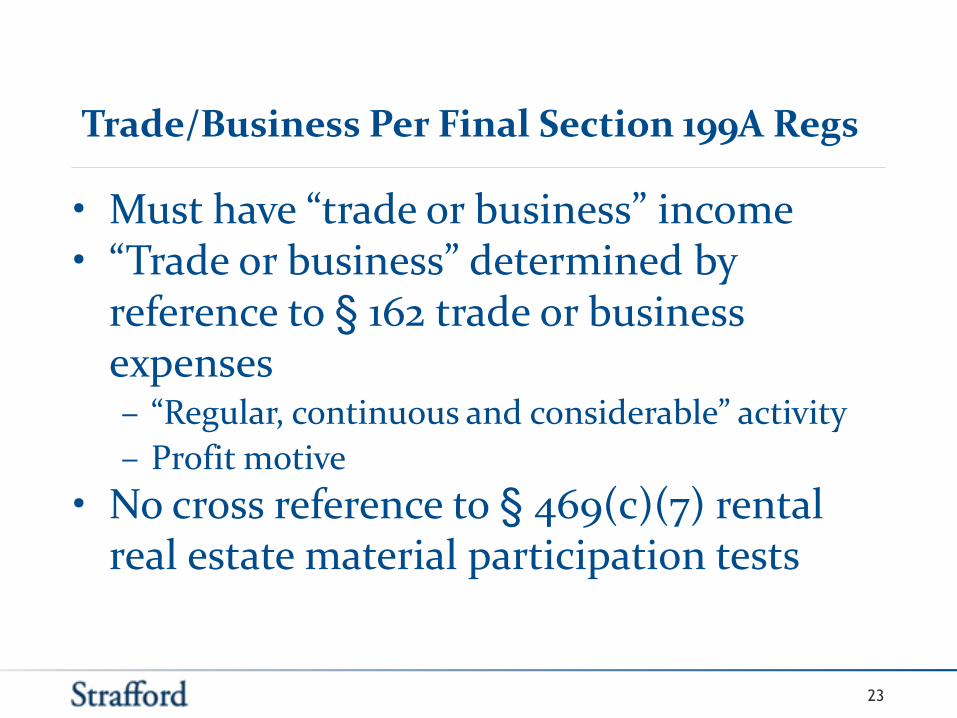

Trade/Business Per Final Section 199A Regs

23

• Must have “trade or business” income• “Trade or business” determined by

reference to § 162 trade or business expenses– “Regular, continuous and considerable” activity

– Profit motive

• No cross reference to § 469(c)(7) rental real estate material participation tests

Rental Real Property

25

• The Tax Court has held that the rental of a single piece of real property can constitute a T/B.

• The IRS has stated that ownership and management of real property does not constitute a T/B as a matter of law.

• Owing rental property qualifies as a T/B if it is engaged in to earn a profit and activity is systematic and continuous. If not, rental ownership would be treated as an investment thus not qualifying for deduction.

Rental Real Property

26

• Need to ask how extensive the taxpayer’s activities are personally or through the use ofagents. Are they so extensive as rising to the level of a T/B?

– How many hours involved with the activity?

– What does the taxpayer do as to the activity?

– Has the taxpayer documented their participation?

Rental Real Property

27

• Factors for rental real estate activity as section 162 trade or business:– Type of property (commercial or residential)

– Number of properties rented

– Owner’s or agent’s day-to-day involvement

– Type and nature of services provided by lessor

– Lease terms (net v. traditional, duration)

• Owner with large number of commercial propertieswhere owner provides significant services day-to-day under traditional long-term lease most likely to be viewed by IRS as a trade or business

Rental Real Estate Self Rentals

28

• The rental or licensing of tangible orintangible property to a commonlycontrolled T/B is a T/B.– For this rule to apply, the same person or group of

persons must own (directly or indirectly) 50% ormore of the rental activity and the T/B.

– The rental of building to operating T/B are both treated as a T/B for §199A.

Rental Real Estate – IRS Pub. 535

29

• “Determining your qualified T/Bs.The ownership and rental of real property may constitute a T/B. Notice 2019-07 provides a safe harbor under which rental real estate enterprise will be treated as a T/B for purposes of the "QBI" deduction. For more information, on the safe harbor see Notice 2019-07. Rental real estate that does not meet the requirements of the safe harbor may still be treated as a T/B for purposes of the "QBI" deduction if it is a section 162 T/B.In addition, the rental or licensing of property to a commonly controlled T/B operated by an individualor a pass-through entity is considered a T/B under section 199A.”

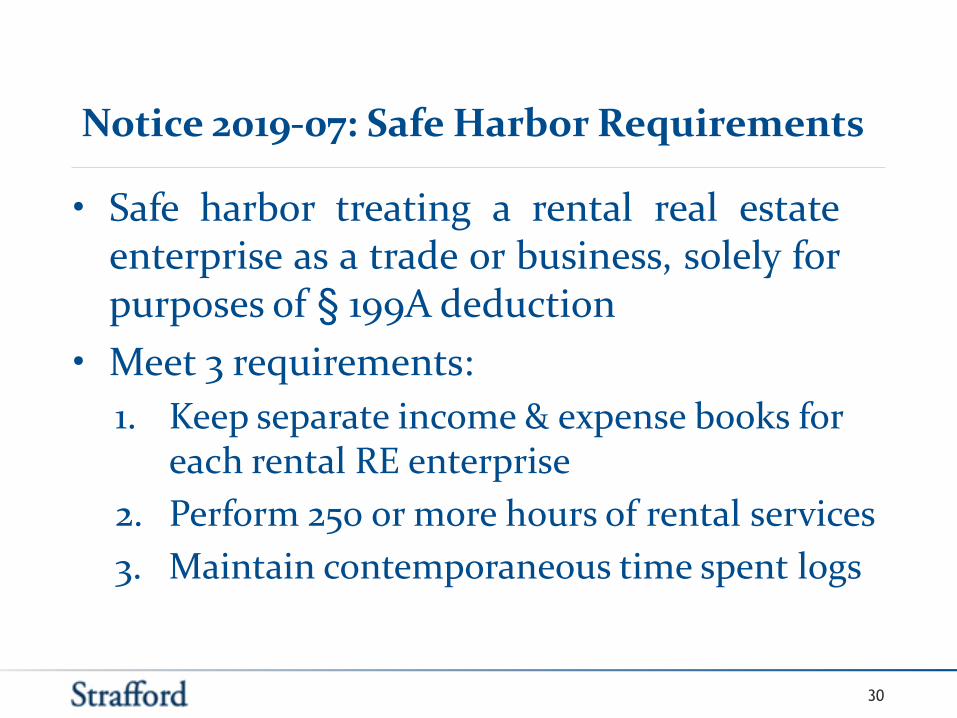

Notice 2019-07: Safe Harbor Requirements

30

• Safe harbor treating a rental real estateenterprise as a trade or business, solely forpurposes of § 199A deduction

• Meet 3 requirements:

1. Keep separate income & expense books for each rental RE enterprise

2. Perform 250 or more hours of rental services

3. Maintain contemporaneous time spent logs

Notice 2019-07: Contemporaneous Records

31

• Contemporaneous records, including time reports, logs, or similar documents, regarding the following:– Hours of all services performed

– Description of all services performed

– Dates on which such services were performed

– Who performed the services.

• The contemporaneous records requirement will

not apply to taxable years beginning prior to January 1, 2019.

Notice 2019-07: 250 Hour Requirement

32

• For 250+ hour requirement, rental servicesinclude:– Advertising to rent the real estate

– Negotiating and executing leases

– Verifying info in tenant applications

– Collecting rent

– Operating, maintaining and repairing property

– Managing the property

– Purchasing materials for the property

– Supervising employees and contractors

• Rental services done by owner, employees, agents and/or independent contractors can count toward the 250 hours

33

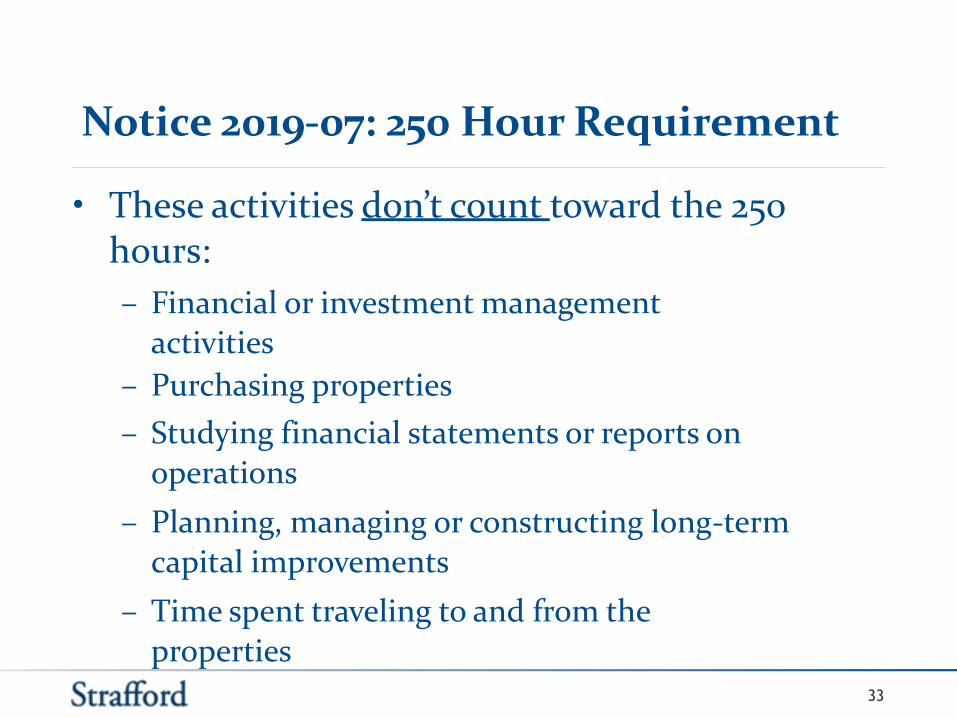

Notice 2019-07: 250 Hour Requirement

• These activities don’t count toward the 250hours:

– Financial or investment management activities

– Purchasing properties

– Studying financial statements or reports on operations

– Planning, managing or constructing long-term capital improvements

– Time spent traveling to and from the properties

34

• Not eligible for the safe harbor:– Real estate used by the taxpayer as a residence

– Real estate rented under a triple net lease (“NNN”)

• Although no safe harbor, NNN leases may still be a trade or business based on all facts andcircumstances

• Consider renegotiating NNN leases so owner can provide 250 hours of services annually(cumulatively on all properties that owner canaggregate)

Notice 2019-07: Ineligible activities

35

Triple Net Lease

• The IRS defines a triple net lease asincluding a lease agreement that requiresthe tenant to pay taxes, fees, andinsurance, and to be responsible formaintenance in addition to rent andutilities, etc.– This includes a lease agreement that requires

the tenant to pay for common areamaintenance expenses.

36

Notice 2019-07: Statement Required

• An affirmative statement must be attached to thereturn if you are using the safe harbor.

• The statement must be signed by the taxpayer, or anauthorized representative of an eligible taxpayer orrelevant pass-through entity (“RPE”)– “Under penalties of perjury, I (we) declare that I

(we) have examined the statement, and, to the best of my (our) knowledge and belief, the statement contains all the relevant facts relating to the revenue procedure, and such facts are true, correct, and complete.”

• The individual or individuals who sign must havepersonal knowledge of the facts and circumstances related to the statement.

37

Aggregation of Commonly Controlled T/Bs

• An individual or pass-through entity may be engaged in more than one T/B. Each T/B is a separate T/B for purposes of applying the W-2 wage limitation or the UBIA limitation.

• Taxpayer may choose to aggregatemultiple trades or businesses into a singleT/B for purposes of applying thelimitations.

38

Aggregation under Section 199A

• 199A final regs allow aggregation of certain trades and businesses

• May increase deduction amount

• Factors for § 199A aggregation:

– Whether businesses provide products or services

typically sold together

– Whether businesses share centralized back- officeservices

– Whether businesses are interdependent

• No cross reference to § 469 grouping rules

39

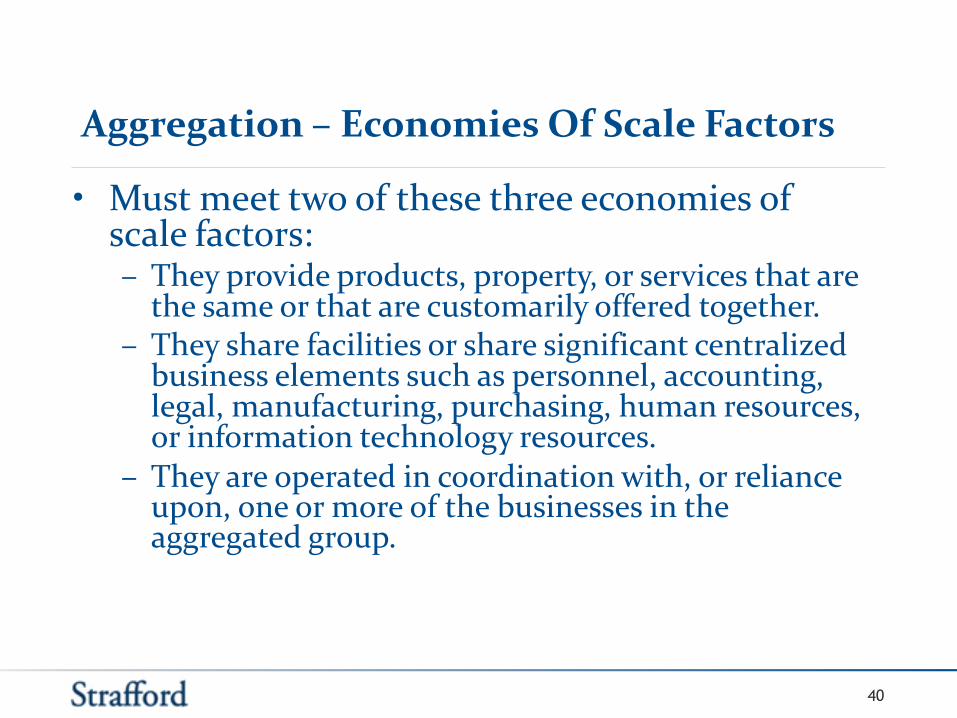

Aggregation under Section 199A

• The following requirements must be metfor a taxpayer or a group of taxpayers toaggregate T/B activities:– Must own, directly or indirectly, 50% or more of

each T/B for a majority of the tax year, including the last day of the tax year, and all trades or businesses use the same tax year end.

– None of the trades or business are a specified service T/B’s.

– The T/B’s meet at least two of economies of scale factors.

40

Aggregation – Economies Of Scale Factors

• Must meet two of these three economies of scale factors:– They provide products, property, or services that are

the same or that are customarily offered together.– They share facilities or share significant centralized

business elements such as personnel, accounting, legal, manufacturing, purchasing, human resources, or information technology resources.

– They are operated in coordination with, or reliance upon, one or more of the businesses in the aggregated group.

41

Final Treasury Regulations

• The final Treasury Regulations are comprised of seven sections as follows:o 1.199A-0 table of contents.o 1.199A-1 covers calculation rules as well as definitional guidance on the

standard of being engaged in a T/B, and loss carry-over rules.o 1.199A-2 covers the rules regarding the determination of W-2 wages and

unadjusted basis immediately after acquisition of Qualified Property.o 1.199A-3 provides guidance surrounding the terms and calculations

regarding ""QBI"", REIT Trust dividends, and qualified PTP income.o 1.199A-4 covers the rules relating to aggregation non-Specified Service

Trades or Businesses and Specified Service Trades or Businesses.o 1.199A-5 covers definitional guidance of Specified Service Trades or

Businesses.o 1.199A-6 covers computational guidance for individuals who own or are

beneficiaries of Relevant Pass-Through Entities, PTP, trusts and estates.o 1.643(f)-1 covers the treatment of multiple trusts, aggregation when the

trusts have significantly the same beneficiaries and the same grantors, namely that the IRS has the power to aggregate them into singular trusts.

42

Grouping under Section 469

• Activity losses deductible only if taxpayer“materially participates” in the activity

• Material participation means beinginvolved in the activity on a regular,continuous and substantial basis

• 7 tests for material participation, including participation for more than 500hours/year

43

Grouping under Section 469

• Activities may be grouped if the activities are an “appropriate economic unit” based on thesefactors:– Similar types of businesses

– Extent of common control

– Extent of common ownership

– Geographical location

– Interdependencies among the businesses

• Example: commercial and residential realestate development businesses were anappropriate economic unit. Lamas v.Commissioner.

44

Grouping under Section 469

• Rental activities can’t be grouped with otheractivities (even if an appropriate economicunit) unless:– The rental activity, or the other business activity, is

insubstantial in relation to the other, or– Each owner of the business activity has the same

proportionate ownership in the rental activity

• Example: husband and wife grocery storebusiness, and rental of building to grocerystore, can be grouped into a single trade orbusiness activity. Treas. Reg. § 1.469-4(d)(1)(ii), Ex. 1

45

Grouping under Section 469

• Rental RE activities are passive unless:– Grouped to meet material participation, or

– Taxpayer is a real estate professional under §469(c)(7) (750 hours AND more than half of taxpayer’s services are in RE)

• Rental RE can’t be grouped with non-REbusinesses to meet material participation forthe rental RE activity, Treas. Reg. § 1.469-9(e)(3)(i), but

• Rental RE can be grouped with other activities to find an appropriate economic unit. Stanley v. US.

46

Depreciation

• Section 199A deduction limited to either thetaxpayer’s proportionate share of a percentage of the W-2 payroll expense of the qualified business or a combination of a proportionate share of a lower percentage of the W-2 payroll expense of the qualified business plus 2.5% of the original cost of depreciable tangible property (not land) used in the qualified business

• RE owners with few W-2 employees will benefitfrom the provision allowing them to calculate the199A deduction cap by reference to 2.5% of theunadjusted cost of the depreciable tangible property

SERVICE. VALUE. RESULTS.

Changes Impacting the Real Estate Industry

Business Interest Expense Limitation

48

Business Interest Limitation

49

2018 Tax Law Changes

• Repeals the old “earnings stripping” rules for interest paid to related

persons who pay no US tax on the corresponding income

• Now applies to all business and limits net interest expense

deductions

• Interest may only be deducted the extent of 30% of “adjusted

taxable income.”

• Doesn’t include investment interest expense.

• Small taxpayer exception - doesn’t apply to businesses with average

receipts of less than $25M (Uses the test in Sec. 448(c), so must

aggregate receipts)

• Excess interest expense is carried forward indefinitely.

Business Interest Limitation

50

2018 Tax Law Changes

• Exceptions to this limitation

– On election, limitation does not apply to electing “real

property trades or businesses.” These businesses then have to

use the ADS depreciation method for nonresidential,

residential, and qualified improvement property.

▪ Includes real property development, redevelopment,

construction, reconstruction, acquisition, conversion,

rental, operation, management, leasing, or brokerage

trade or business

– Doesn’t apply to car dealerships with floor-plan interest.

Business Interest Limitation

51

2018 Tax Law Changes

• Adjusted taxable income is taxable income BEFORE:

– Any income/deduction/gain/loss not properly allocable

to a trade or business,

– Any business interest expense or income

– Any net operating loss deduction (Code Sec. 172)

– Any depreciation, amortization, or depletion

deductions (for tax years beginning before Jan. 1, 2022).

– Any qualified business income deduction (Code Sec.

199A)

Business Interest Limitation

• The deduction allowed to a business subject to this

limitation can not exceed the sum of:

– The taxpayer’s business interest income for the tax year;

– 30% of the taxpayer’s adjusted taxable income for the tea year;

plus

– The taxpayer’s floor plan financing interest (vehicle dealers)

for the tax year

• As mentioned, disallowed interest carries forward and will be

treated as business interest paid or accrued in the following tax

year. May be carried forward indefinitely.

52

2018 Tax Law Changes

Business Interest Limitation

53

2018 Tax Law Changes

• For partnerships, the limitation is first applied at

the partnership level

• Excess interest expense is allocated to the partners

and carried forward at the partner level

• Partner may deduct its share of excess business

interest in any future year, but only against excess

taxable income attributed to the partner by the

partnership whose activities gave rise to the excess

business interest

Business Interest Limitation

54

2018 Tax Law Changes

• Excess taxable income is the amount that bears the

same ratio to the partnership’s adjusted taxable

income as:

– The excess (if any) of 30% of the partnership’s

adjusted taxable income over the amount by

which the partnership’s business interest

exceeds its business interest income, bears to

– 30% of the partnerships adjusted taxable income

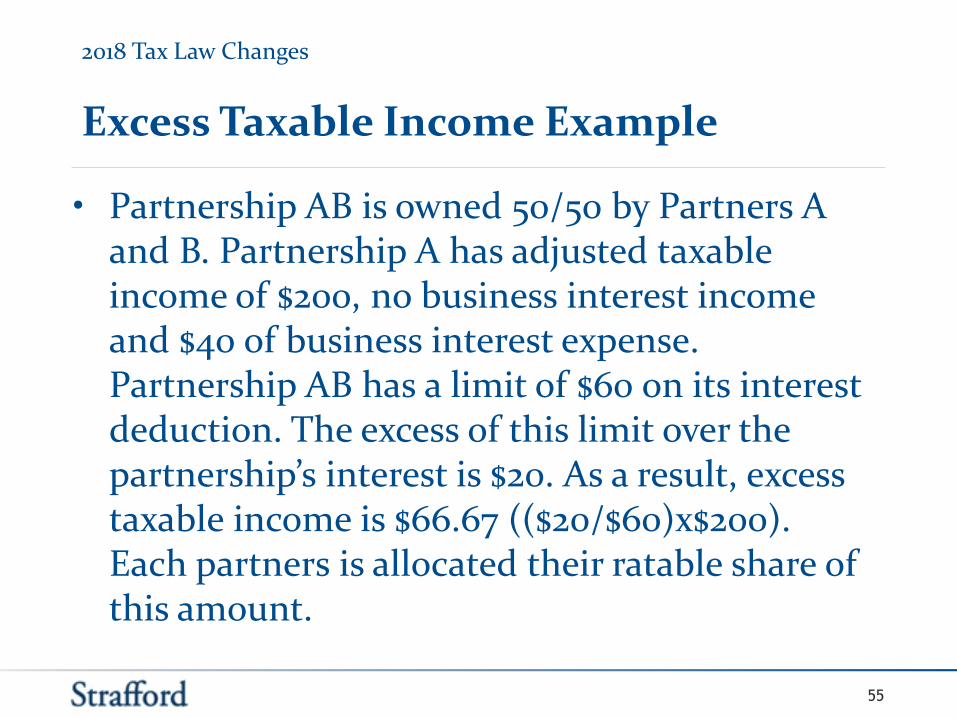

Excess Taxable Income Example

55

2018 Tax Law Changes

• Partnership AB is owned 50/50 by Partners A and B. Partnership A has adjusted taxable income of $200, no business interest income and $40 of business interest expense. Partnership AB has a limit of $60 on its interest deduction. The excess of this limit over the partnership’s interest is $20. As a result, excess taxable income is $66.67 (($20/$60)x$200). Each partners is allocated their ratable share of this amount.

Business Interest Limitation

56

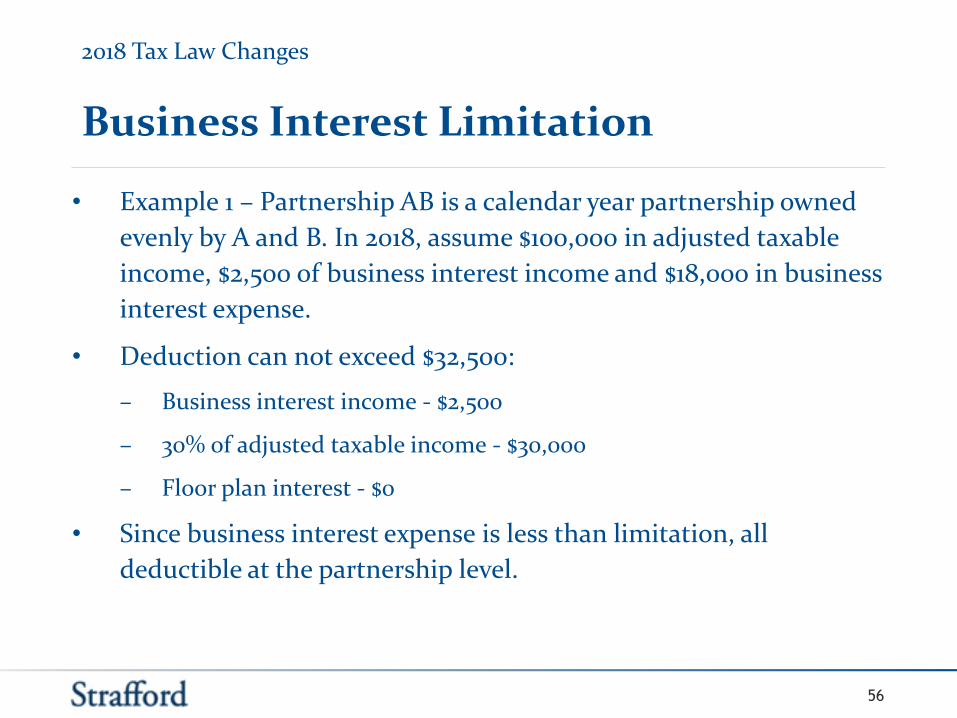

2018 Tax Law Changes

• Example 1 – Partnership AB is a calendar year partnership owned

evenly by A and B. In 2018, assume $100,000 in adjusted taxable

income, $2,500 of business interest income and $18,000 in business

interest expense.

• Deduction can not exceed $32,500:

– Business interest income - $2,500

– 30% of adjusted taxable income - $30,000

– Floor plan interest - $0

• Since business interest expense is less than limitation, all

deductible at the partnership level.

Business Interest Limitation

57

2018 Tax Law Changes

• Example 2 – Partnership AB is a calendar year taxpayer owned

evenly by A and B. In 2018, assume $10,000 in adjusted taxable

income, $2,500 of business interest income and $18,000 in business

interest expense.

• Deduction can not exceed $5,500:

– Business interest income - $2,500

– 30% of adjusted taxable income - $3,000

– Floor plan interest - $0

• Partnership X can deduct $5,500 of it’s business interest expense.

The excess interest of $12,500 would be allocated to Partners A and

B and would carry forward to 2019

Business Interest Limitation

58

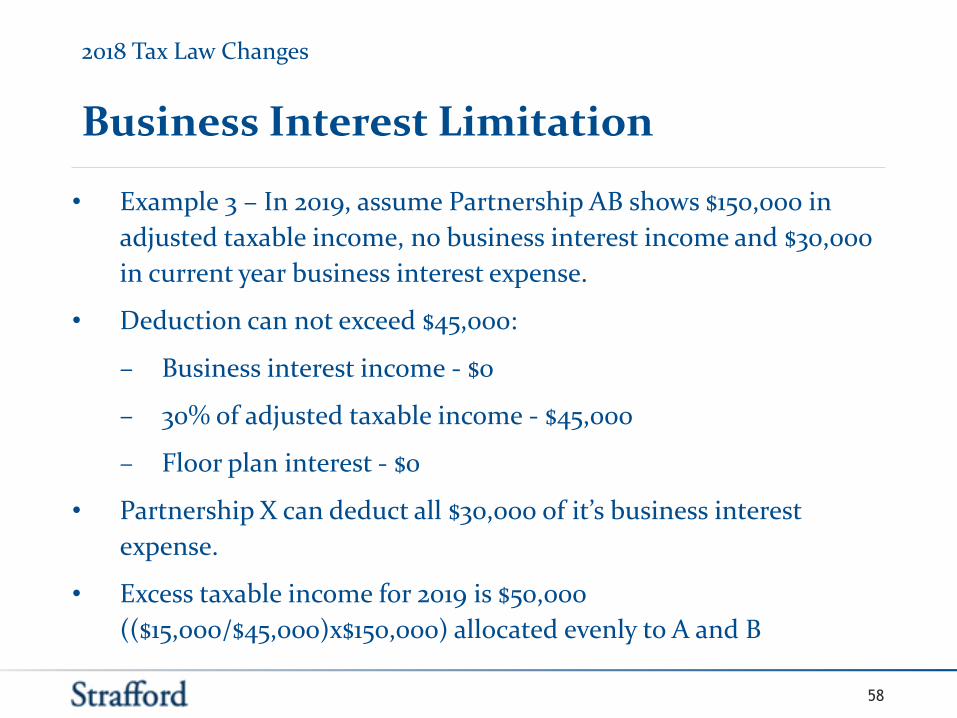

2018 Tax Law Changes

• Example 3 – In 2019, assume Partnership AB shows $150,000 in

adjusted taxable income, no business interest income and $30,000

in current year business interest expense.

• Deduction can not exceed $45,000:

– Business interest income - $0

– 30% of adjusted taxable income - $45,000

– Floor plan interest - $0

• Partnership X can deduct all $30,000 of it’s business interest

expense.

• Excess taxable income for 2019 is $50,000

(($15,000/$45,000)x$150,000) allocated evenly to A and B

59

Election Out of Interest Limitation

• As mentioned, limitation doesn’t apply to electing “real property trades or businesses”

– Includes real property development, redevelopment, construction, reconstruction, acquisition, conversion, rental, operation, management, leasing, or brokerage trade or business

• Must use the ADS depreciation method for nonresidential, residential, and qualified improvement property.

• Not eligible for bonus depreciation

SERVICE. VALUE. RESULTS.

Changes Impacting the Real Estate Industry

Depreciation Changes

60

61

Section 179 Deduction

Old Law: New Law:

Expensing Limitation $500,000 indexed for inflation ($510,000 in 2017)SUVs eligible up to $25,000

$1,000,000 for tax years beginning after 12/31/17, indexed for inflation in tax years beginning in 2019,SUV’s eligible for $25,000 deduction (inflation indexed)

Phase-out Threshold $2,000,000 indexed for inflation ($2,030,000 in 2017), dollar for dollar phase-out as property placed in service exceeds threshold

$2,500,000 for tax years beginning after 12/31/17, indexed for inflation in tax years beginning in 2019, dollar for dollar phase-out as property placed in service exceeds threshold

Effective Date Tax years beginning before 1/1/2018

Tax years beginning on or after 1/1/2018

62

Section 179 Deduction

Old Law: New Law:

EligibleProperty

Tangible personal property that is purchased for use in the active conduct of a trade or business, andincludes off-the-shelf computer software and qualified real property (i.e., qualified leasehold improvement property, qualified restaurant property, and qualified retail improvement property).

Tangible personal property that is purchased for use in the active conduct of a trade or business, and includes off-the-shelf computer software and qualified real property.

179(f) For purposes of this section, the term “qualified real property” means—(1) any qualified improvement property described in section 168(e)(6)*, and(2) any of the following improvements to nonresidential real property placed in service after the date such property was first placed in service:(A) Roofs.(B) Heating, ventilation, and air-conditioning property.(C) Fire protection and alarm systems.(D) Security systems.

*168(e)(6) QIP: improvement to interior portion of nonresidential real property after it was placed in service. Does not include enlargement of building, elevator or escalator, internal structural framework of the building

Implications for Real Estate

Industry

Expanded definition under 179(f)(2) will allow for 179 deduction for items under 179(f)(2) A-D above which do not qualify for bonus under 168(k) due to the “internal portion” and “internal structural framework of building” requirements.

63

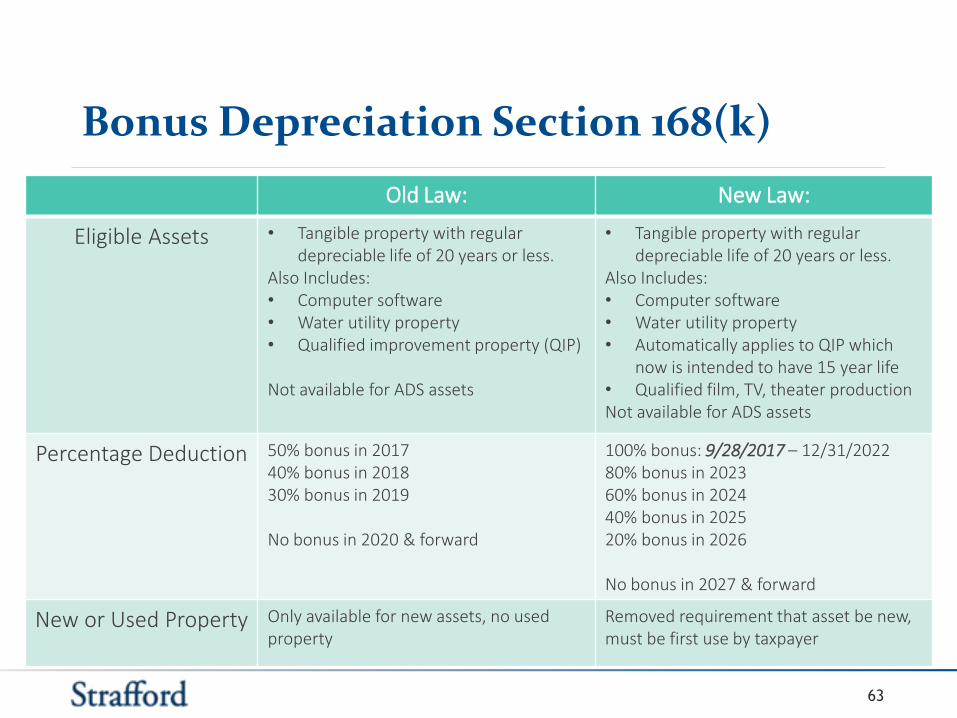

Bonus Depreciation Section 168(k)

Old Law: New Law:

Eligible Assets • Tangible property with regular depreciable life of 20 years or less.

Also Includes:• Computer software• Water utility property• Qualified improvement property (QIP)

Not available for ADS assets

• Tangible property with regular depreciable life of 20 years or less.

Also Includes:• Computer software• Water utility property• Automatically applies to QIP which

now is intended to have 15 year life• Qualified film, TV, theater productionNot available for ADS assets

Percentage Deduction 50% bonus in 201740% bonus in 201830% bonus in 2019

No bonus in 2020 & forward

100% bonus: 9/28/2017 – 12/31/202280% bonus in 202360% bonus in 202440% bonus in 202520% bonus in 2026

No bonus in 2027 & forward

New or Used Property Only available for new assets, no used property

Removed requirement that asset be new, must be first use by taxpayer

64

Bonus Depreciation - Requirements

• In order to qualify for 100% bonus depreciation,

property must be both acquired and placed in service

after Sept. 27, 2017

― Buildings are deemed to be acquired on the date that

there is a binding contract for the sale of the

building (Reg. Sec. 1.168(k)-1(b)(4)(ii))

― Self-constructed buildings are acquired when

physical work of a significant nature begins (Reg.

Sec. 1.168(k)-1(b)(4)(iii)(B))

65

Qualified Improvement Property

• Lease requirement removed

• Related party restrictions removed

• 3 year after placed in service required removed

• 3 categories down to one

• Intended to be 15 year property eligible for bonus

depreciation

― IRS Chief Counsel Branch 7 Chief says IRS cannot fix

― Without congressional action QIP is 39 year S/L

― Taxpayers with election out of interest limitation won’t be

as affected

Section 461(l) Excess Business Loss Limitation

66

Limitation of Excess Business Losses – New Section 461(l)

Passive Activity Rules (IRC Section 469)

At Risk Limitations (IRC Section 465)

Basis Limitations (IRC Section 1366/704)

Excess Business Loss Limitation (461(l))

67

2018 Tax Law Changes

• Applies to non-corporate taxpayers

• “Excess Business Losses” cannot be

deducted

• Amounts disallowed under this section

will be treated as NOL’s carrying over to

the following tax year

“Excess Business Loss” Defined

68

2018 Tax Law Changes

• Excess of aggregate deductions attributable to the taxpayer’s trade or businesses over

• The sum of:

– Aggregate gross income from trades or businesses

– $250k S / $500k MFJ

Excess Business Loss Limitation (461(l))

69

2018 Tax Law Changes

• Applies to tax years beginning after

12/31/17 and before 1/1/2026

• The $250/$500k threshold amounts are

indexed for inflation for tax years

beginning after 12/31/18

• Applied at the partner/shareholder level

70

Deductible Expenses

• Most common ordinary and necessary deductibleexpenses for rental property:– Mortgage interest

– Property tax

– Operating expenses (materials, supplies)

– Depreciation

– Repairs and maintenance

– Utilities and insurance

– Advertising

• Cost of improvements (restoration, adaptation to a new use) are not deductible. The cost of improvements is recovered through depreciation.

71

Deductible Expenses

• TCJA makes adjustments to the fringebenefit rules (for amounts paid or incurred after 12/31/17):– Denies a deduction for employee transportation

fringe benefits. However, the TCJA retains the exclusion from income for such benefits received by an employee.

– Eliminates a deduction for transportation expenses that are the equivalent of commuting for employees, except as provided for the safety of the employee.

72

Non-deductible Parking

• The IRS issued Notice 2018-99 whichprovides interim guidance on determining the amount of parking expenses that are notdeductible.– If a taxpayer pays a third party for employee parking

then the disallowance is the amount paid to thethird party.

– For facilities owned or leased by employers, the notice permits a taxpayer to use any “reasonable method” to compute its disallowed expenses using a safe harbor method.

73

Non-deductible Entertainment - Notice 2018-76

• TCJA disallows deductions for entertainment expenses including expenses for a facility used in connection with entertainment.

• Can continue to deduct 50% of the cost of business meals if the taxpayer or employee is present and the food or beverages are not considered lavish or extravagant.

• If meals are provided during an entertainment activity,

they must be purchased separately from the

entertainment or the meal cost must be stated separately

on the bill.

74

Deductible Entertainment

• The following entertainment expenses remainfully deductible:– Entertainment expenses for goods, services,

and facilities that are treated as compensation or a gift/award to an employee.

– Expenses for recreational, social, or similar activities and related facilities primarily for the benefit of employees who are not highly compensated employees.

– Expenses for entertainment sold to customers.

75

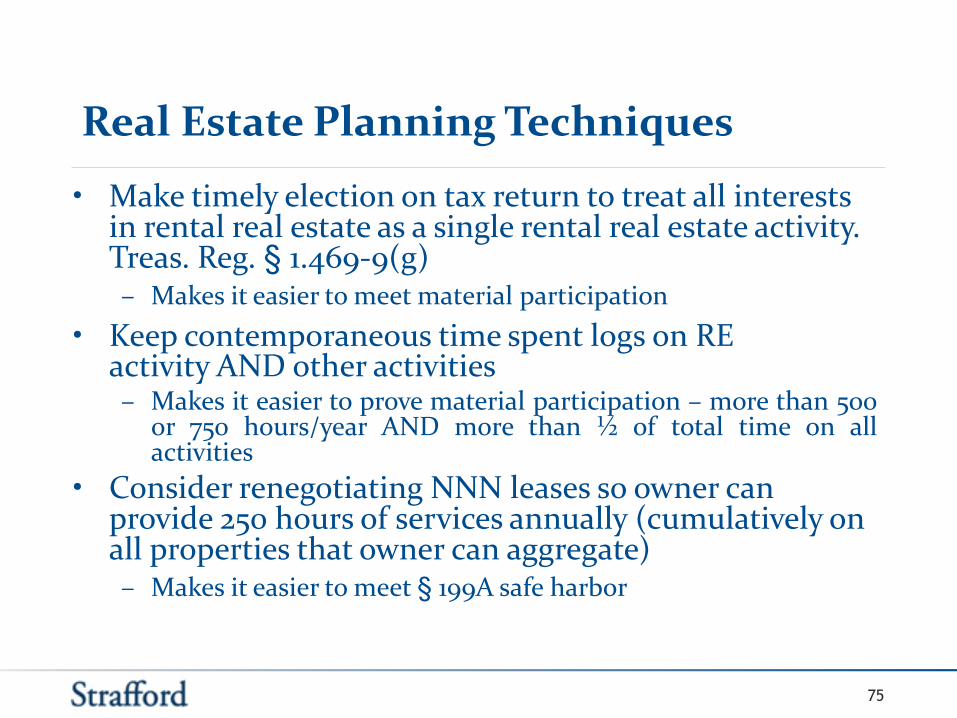

Real Estate Planning Techniques

• Make timely election on tax return to treat all interests in rental real estate as a single rental real estate activity. Treas. Reg. § 1.469-9(g)– Makes it easier to meet material participation

• Keep contemporaneous time spent logs on REactivity AND other activities– Makes it easier to prove material participation – more than 500

or 750 hours/year AND more than ½ of total time on allactivities

• Consider renegotiating NNN leases so owner canprovide 250 hours of services annually (cumulatively on all properties that owner can aggregate)– Makes it easier to meet § 199A safe harbor

76

Brian T. Lovett, CPA, CGMA, JDBrian is a tax partner based in Withum’s East Brunswick office and is a certified public accountant in the states of New Jersey and Pennsylvania.

He has extensive experience serving the tax needs of both public companies and closely-held businesses, including all aspects of tax compliance for partnerships, corporations and individuals.

Brian advises clients with regard to the structure and tax consequences of new business ventures, and assists with restructuring existing businesses for increased tax efficiency. A frequent speaker on various tax topics, Brian has spent the last two years digesting the Tax Cuts and Jobs Act and presenting its various changes throughout the country.

76

Faculty

Guinevere Moore is a partner with the law

firm of Johnson Moore LLC in Chicago and

she is the Executive Director of US

Partnership Representative, Inc. She has

over a decade of experience representing

taxpayers in high stakes disputes with the

IRS. She represents taxpayers before the

IRS and in litigation before the United States

Tax Court, United States District Courts,

Courts of Appeals, and the United States

Supreme Court. She particularly enjoys her

client counseling role and advising clients on

how to navigate a dispute with the IRS.

Telephone: 312-549-9993

Email: [email protected];

Website:

www.uspartnershiprepresentative.com;

www.jmtaxlitigation.com

77

DHJJ.com

Kira Wheat is a Senior Tax Manager at DHJJ with over 14 years of experience serving a diverse client base, including high-net-worth individuals and closely held businesses.

She has expertise in the real estate, family office, service and investment fund industries.

Kira’s skills include a deep knowledge of individual, trust and partnership tax. She works extensively with real estate developers and operators as well as wealthy families. Her clients are often involved in multi-state and international activity. Her standard services include tax compliance as well as tax planning and consulting.

Kira Wheat, CPASenior [email protected] 420 1360

78

Thank You

Brian T. Lovett, CPA, JD, Partner

WithumSmith+Brown

Guinevere M. Moore, Partner

Johnson Moore

Kira Wheat, Senior Tax Manager

DHJJ