real estate office - zacks investment research: stock research

TRANSCRIPT

Skyline broker survey suggests strong leasing activity carrying into 2H13. We expect

that strong Office employment gains over the trailing three-month (+1.9% ann.) and

twelve-month (+1.9%) periods led by technology and business services should continue to

support positive absorption and enhanced net effective rent growth for Office. In particular,

we are incrementally positive on HIW, PKY and CUZ given the positive assessments

regarding tenant size, geography and amenities that are driving the greatest among of

tenant leasing activity.

■ Baird Skyline. Our survey of top Office leasing brokers suggests strong activity in

Secondary U.S. metropolitan areas--driven primarily by smaller footprint tenants--that is

resulting in incrementally better net effective rents. We expect that HIW, PKY and CUZ

should be primary beneficiaries of the trends noted in our detailed write-up that follows.

■ Key Takeaways From Broker Commentary Include:

- Small tenants continue to drive market activity. Tenants seeking 10-25k spaces

are driving market activity higher and reflect greater incremental volume from the

5-10k average lease size 12 months ago. Value-oriented spaces in live, work and play

environments remain most active. Energy, technology and housing remain active

drivers of absorption.

- Net effective rents are improving across most major markets. While face rents

are moving higher in a small number of markets, declining free rent periods (now a

1mo./yr) are driving effective rents higher across most major metro areas.

- Densification active among professional services firms. Despite broader

management commentary regarding a moderation in the trend toward downsizing, it

appears that legal, accounting and financial firms continue to drive "densification" in

renewals and intra-market relocations. Parking, however, is limiting some of the

densification that tenants would like to achieve.

- "For Rent" amenities increasingly attractive to tenants. Building renovations that

include "For Rent" conference facilities (as well as traditional amenities including

on-site food and fitness) are attracting tenants seeking to minimize space utilization.

- Office development limited by Multifamily, Hotel activity. Although most U.S.

metro areas do not yet support speculative Office development, the strongest of

geographies are experiencing heavy competition for land and redevelopment from

Multifamily and Hotel builders/operators.

■ Most intriguing comment: Restroom size is a limiting factor for tenant densification

and is incrementally important in negotiations. [San Diego suburbs]

■ Office employment favors Secondary markets. While few investors are likely to be

surprised that Houston, Austin and Dallas are in the "Top 10" metro areas for 3-month

and 12-month Office employment growth, these cities are joined by Nashville, Denver

and L.A. in both categories as well.

INDUSTRY UPDATE

Prices as of 7/8/13

Ticker PriceMkt Cap

(mil)Rating Risk

DRE $15.74 $5,075 O A

FPO $13.63 $724 N H

FSP $13.50 $1,119 O A

IRET $8.69 $1,027 N A

OFC $26.22 $2,237 O A

PDM $18.29 $3,069 O A

SLG $90.81 $8,563 N A

WRE $27.07 $1,800 O A

Baird covered companies

July 9, 2013 Baird Equity ResearchReal Estate

Real Estate OfficeSkyline: Broker Comments Suggest Office Leasing Fundamentals Improving

David B. Rodgers, CFA

216.737.7341

Jonathan Pong

203.425.2740

Mathew R. Spencer

414.298.5053

[Please refer to Appendix- Important Disclosuresand Analyst Certification]

July 9, 2013 | Real Estate Office

Employment Growth by Market

Total Estimated Change In Office Employment - 3-Month Total Estimated Change In Office Employment - 12-Month

Prof. & Business Services Employment 2.7% Prof. & Business Services Employment 4.2%

Information Employment 2.2% Information Employment 1.9%

Total Office 1.9% Total Office 1.9%

Government Employment 1.9% Financial Employment 1.5%

Other Services Employment 1.3% Other Services Employment 1.4%

Financial Employment 0.5% Government Employment -0.3%

Source: BLS and Baird Research. Source: BLS and Baird Research.

Total Office Employment -- 3-Month Change Total Office Employment -- 12-Month Change

Nashville 3.3% Nashville 5.4%

Denver 3.2% San Francisco 4.3%

Pittsburgh 3.2% Dallas 4.2%

Los Angeles 2.9% Raleigh 3.9%

Charlotte 2.9% Denver 3.8%

Houston 2.6% Houston 3.1%

Austin 2.6% Austin 3.1%

Dallas 2.4% Boston 3.0%

Chicago 2.4% Los Angeles 2.5%

Baltimore 2.3% San Diego 2.5%

Tampa 2.1% Tampa 2.2%

New York City 1.8% Seattle 2.1%

Boston 1.8% Pittsburgh 2.1%

Philadelphia 1.7% Norfolk 1.9%

Raleigh 1.7% Charlotte 1.9%

Triad 1.7% Atlanta 1.9%

Atlanta 1.6% Phoenix 1.8%

Norfolk 1.5% Chicago 1.6%

Phoenix 1.5% Minneapolis 1.6%

Minneapolis 1.4% Memphis 1.3%

San Diego 1.4% Washington, D.C. 1.2%

Washington, D.C. 1.4% Jacksonville 1.0%

Miami 1.2% Baltimore 0.9%

Memphis 1.1% New York City 0.7%

Richmond 1.1% Richmond 0.5%

Jacksonville 1.0% Philadelphia 0.3%

Seattle 0.9% Miami 0.1%

San Francisco 0.7% Triad -0.9%

Total Office Employment 1.9% Total Office Employment 1.9%

Source: BLS and Baird Research. Source: BLS and Baird Research.

Details

2Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Atlanta

Solid leasing activity in ATL, picked up significantly in the past 12 months

Tenant negotiations remain protracted First time in five years tenants are doing expansion leases

Businesses are expanding operations and hiring new workers Current space cannot hold new employee hires

Flight to quality window is over Landlords are holding rents for high-quality space Rental rates in high-quality space have priced out deal seekers

Rental rates are trickling up, Central Perimeter and Buckhead to benefit Bullish commentary on rental rates from brokers

Expectation is for 5% y/y growth in rental rates (forecast) ’14 could see significant increases due to limited blocks of space

Positive environment could help increase future leasing budgets Brokers are trying to get deals done this year

Buckhead and Central Perimeter markets are peaking tenant interests Could see incremental activity in these submarkets Rental rates are set to outpace the overall market Expectation for lower TIs from the current ~$35/SF (10-yr term)

Corporate relocations are occurring in Atlanta State Farm is looking to build 800k SF in the Central Perimeter Coke is moving its IT group downtown; 250k SF AIG is looking at the North Fulton submarket for its 300k SF roll 2016 Pulte Homes is relocating to Buckhead; 100k SF

Barriers are limiting development activity No new major developments currently Developers are no longer able to underwrite spec projects Spec activity in ’07 is now full and is no longer pressuring the market

Densification trend will continue; parking employees could be a challenge SF/employee will continue to go down Parking the employees will be a challenge, focus in negotiations

Key amenities are allowing tenants to use space more efficiently Large conferencing facilities available for rent are in popular demand

The facilities can hold 50-60 people Available for rent on a per-use basis Reduces space needs for tenants Increases space efficiency for tenants

Atlanta

Office SF % of TotalCUZ 4,757,000 40.2%PKY 2,019,122 17.0%GOV 947,759 9.3%FSP 773,870 8.4%PDM 1,062,521 5.0%HIW 1,203,888 3.5%DRE 582,177 0.4%CWH 244,000 0.3%

Source: SNL Financial and Baird research

3Robert W. Baird & Co.

Baird's Skyline

Atlanta Office Market Fundamentals -- Central Business District (CBD)

Class A Class B Total

Size Of Atlanta Office Market (MSF) 48.4 26.8 75.3

% of total market 64.3% 35.7% 100.0%

Office Employment, Estimated ('000) 222.0 136.3 358.2

1-year historical employment growth 1.4%

5-year historical employment growth -0.3%

10-year historical employment growth 0.8%

Vacancy (%) 18.5% 9.7% 15.4%

Direct 17.3% 9.4% 14.4%

Sublet 1.2% 0.3% 0.9%

Effective Rents ($/SF) $23.65 $18.61 $21.85

1-year historical rent growth 0.0% 4.3% 1.5%

5-year historical rent growth 0.6% 0.5% 0.6%

10-year historical rent growth -0.1% -0.7% -0.3%

Vacancy Change Needed For Rent Growth 6.4%

SF of Absorption Needed For Equilibrium (MSF) 4.1

Employment Needed For Equilibrium 23,065

Office Employment Growth Needed For Equilibrium 6.4%

Estimated Time To Reach Market Equilibrium (yrs) 1.7

Current Replacement Cost $283

Acquisition Cost Estimate $209 $149 $187

Discount To Replacement Cost 26.1% 47.4% 33.7%

Current Development Yield 7.0%

Current Acquisition Yield 7.0% 8.0% 7.4%

Public REIT Exposure SF ('000) % of port.

CUZ 4,217 35.7%

PKY 1,263 10.7%

GOV 948 9.3%

HIW 492 1.4%

DRE 436 0.3%

CWH 164 0.2%

Vacancy, Rent & Construction Analysis

Source: Bureau of Labor Statistics, CoStar, and Baird estimates Source: Bureau of Labor Statistics, CoStar, and Baird estimates

Source: CoStar and Baird Research Source: CoStar and Baird Research

Development Yield & Replacement Cost Analysis

Source: CoStar and Baird estimates Source: CBRE, Colliers, Grubb & Ellis, Jones Lang LaSalle, Real Capital Analytics, RSMeans, and

Baird estimates

ATL Employment BreakdownATL Statistics at a Glance -- CBD

ATL Development Yield -- CBD ATL Replacement Cost & Historical Trades -- CBD

ATL Vacancy & Employment ATL Demand Requirement For Equilibrium -- CBD

ATL Vacancy & Effective Rents -- CBD ATL Vacancy & Annualized New Construction -- CBD

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

Rep

lacem

en

t Y

ield

& 1

0-Y

ea

r

Sp

rea

d

New

Co

nstr

ucti

on

, %

Of

Exis

tin

g

Sto

ck, A

nn

ua

lized

Class A Starts Class A Replacement Yield Dev Spread To 10-YR

0%

15%

30%

45%

60%

75%

90%

$0

$50

$100

$150

$200

$250

$300

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Dis

co

un

t T

o R

ep

lacem

en

t C

ost

Asset

Va

lue (

$/S

F)

% discount - Class A % discount - Class B Replacement CostTrading Price Class A Trading Price Class B

0%

3%

6%

9%

12%

15%

18%

21%

24%

27%

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13 Va

ca

nc

y (

Dir

ec

t &

In

dir

ec

t) -

- B

ars

Eff

ec

tive

Re

nts

($

/ S

F)

-- L

ine

s

Vacancy, Total, Class A Vacancy, Total, Class B Effective Rent, Class A Effective Rent, Class B

0%

5%

10%

15%

20%

25%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Va

ca

nc

y (

Dir

ec

t &

In

dir

ec

t)

Vacancy, Direct, Class A Vacancy, Indirect, Class A Class A Starts

-9.0

-6.0

-3.0

0.0

3.0

6.0

9.0

-45,000

-30,000

-15,000

0

15,000

30,000

45,000

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

SF

Of

Ab

so

rpti

on

Ne

ed

ed

Fo

r R

en

t G

row

th -

- B

ars

(In

Millio

ns)

Em

plo

ye

es N

ee

de

d T

o A

bso

rb S

F

To

Va

ca

nc

y E

qu

ilib

riu

m -

- L

ine

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

0%

5%

10%

15%

20%

25%

30%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Em

plo

ym

en

t G

row

th -

- T

railin

g

Fo

ur

Qu

art

er

YO

Y G

row

th

Va

ca

nc

y (

Dir

ec

t &

In

dir

ec

t)

Vacancy, Direct -- Total Vacancy, Indirect -- Total Employment Growth

Trade Transportation and

Utilities 23%

Professional and Business Services

18%

Government 13%

Education and Health Services

12%

Leisure and Hospitality

10%

Manufacturing 6%

Financial Activities 6%

Other Services 4%

Construction 4%

Information 4%

4Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Austin

White-hot market has cooled off a bit from 12 months prior

Activity has fallen off some from the really hot period a year ago Market is still healthy, but has leveled off to a steady pace Southwest submarket is the healthiest in the MSA Average deal size is 5-7k SF

Rental rates continue to climb upward Rental rates are at or close to replacement rents TPGI has controlled the CBD market and is setting rates

Low $30/NNN rental rates for high-quality space Overall CBD market is realizing $25-30/NNN rental rates New lease TIs of $3.5/SF/yr Renewal lease TIs of $2.5/SF/yr Free rent is 1 mo/3 years of lease term

Southwest market is realizing rents in the $23-24/SF range New lease TIs of $3/SF/yr Renewal lease TIs of $2/SF/yr Free rent is around 1 mo/4 years of lease term

Northwest market is achieving $20-22/SF rents TI package is similar to the Southwest Free rent is around 1 mo/2 years of lease term

Tech and Social Media are driving CBD; Financials and Law firms are flat Tech/Social Media firms are driving the growth downtown Financials and Law Firms are steady with no growth

Two Law Firms leased space at CUZ’s CBD development Vacancy and replacement rental rates justify construction

Expectation is for increased development given a relatively tight market Low vacancy percentage

Southwest market will likely see a lot of construction activity Recent deal rates are at replacement rents

Apple bought land near existing campus; building 300k SF Two development projects in the CBD including Colorado Tower

Multifamily and Hotel competition for parking could limit densification MF and Hotels have swallowed a lot of the good sites and parking lots Offsite parking options are limited Densification will likely be limited by parking options

Tenants are hoping employees will live downtown MF rental rates are $3/SF/mo Pricing some of the employees out of the CBD market

Austin

Office SF % of TotalTPGI 2,615,749 24.9%BDN 1,626,811 5.1%PDM 195,230 0.9%CWH 170,052 0.2%

Source: SNL Financial and Baird research

5Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Boston

Boston is starting to become a landlord’s market

Leasing activity has increased quite a bit with more tenants in the market Faster negotiation times shifting towards the landlords’ favor Market is being driven by 10-30k SF tenants

A lot of 5k SF tenants going to 10-15k SF Larger institutional tenants are shrinking floor plates Tenants are moving downtown from neighboring suburbs Class B office space is “hot” along with Class A low-rise space

Class A rents are going up, Sea Port rents have gone up 20-30% Back Bay rents were the first to increase with pricing being very high

Landlords are being patient to achieve desired pricing Sea Port rents have gone up 20-30% and is an “unbelievably hot market” Financial District submarket is starting to see rents creep up

Tenants are looking for value right now Only “value space” available is in the Financial District

Suburbs TIs are ~$40/SF for a 10-year lease Small Tech firms are growing organically, driving the overall market health

5k SF Tech firms are growing rapidly and require more space needs I.e. DataXu Inc. going from 5k SF to ~30k SF

Tech firms are also moving from Cambridge/suburbs to CBD Sea Port and suburbs likely to see build-to-suit developments

Big users are looking at the Sea Port for BTS opportunities PWC is a likely candidate for a BTS or move into the Sea Port

Moving from 125 High St., owned by Tishman Speyer 291k SF in the building, going to potentially 350k SF

Sea Port could begin to see infrastructure issues ~10k employees to move to the area Needs improvements to transportation/parking options

Large blocks of space in the suburbs are “not great” Will likely lead to build-to-suit projects

Work, live, play in full swing for Boston Tenants are looking for proximity of entertainment for employees

Need to be close to the excitement; bars, food, shopping BXP is looking to convert to more ground floor retail at 100 Federal St.

Will be much needed for the area Brown Brothers Harriman & Co. is moving nearby

Access to public transportation is important in making a leasing decision

Boston

Office SF % of TotalBXP 13,055,187 30.9%PDM 1,294,307 6.1%SIR 495,967 2.0%BPO 1,032,000 1.3%CWH 448,723 0.6%

Source: SNL Financial and Baird research

6Robert W. Baird & Co.

Baird's Skyline

Boston Office Market Fundamentals -- Central Business District (CBD)

Class A Class B Total

Size Of Boston Office Market (MSF) 71.2 39.1 110.3

% of total market 64.6% 35.4% 100.0%

Office Employment, Estimated ('000) 274.1 154.4 428.5

1-year historical employment growth 3.4%

5-year historical employment growth 0.5%

10-year historical employment growth 0.4%

Vacancy (%) 10.8% 8.4% 8.8%

Direct 10.1% 8.3% 8.4%

Sublet 0.7% 0.1% 0.4%

Effective Rents ($/SF) $44.01 $28.50 $38.52

1-year historical rent growth 3.2% 9.1% 5.3%

5-year historical rent growth 1.1% 0.7% 0.9%

10-year historical rent growth -0.5% -1.6% -0.9%

Vacancy Change Needed For Rent Growth 0.0%

SF of Absorption Needed For Equilibrium (MSF) 1.0

Employment Needed For Equilibrium 4,442

Office Employment Growth Needed For Equilibrium 1.0%

Estimated Time To Reach Market Equilibrium (yrs) 0.1

Current Replacement Cost $500

Acquisition Cost Estimate $521 $354 $462

Discount To Replacement Cost -4.1% 29.2% 7.7%

Current Development Yield 7.2%

Current Acquisition Yield 4.4% 4.5% 4.4%

Public REIT Exposure SF ('000) % of port.

BXP 6,378 15.1%

BPO 1,032 1.3%

CWH 133 0.2%

Vacancy, Rent & Construction Analysis

Source: Bureau of Labor Statistics, CoStar, and Baird estimates Source: Bureau of Labor Statistics, CoStar, and Baird estimates

Source: CoStar and Baird Research Source: CoStar and Baird Research

Development Yield & Replacement Cost Analysis

Source: CoStar and Baird estimates Source: CBRE, Colliers, Grubb & Ellis, Jones Lang LaSalle, Real Capital Analytics, RSMeans, and Baird estimates

BOS Employment BreakdownBOS Statistics at a Glance -- CBD

BOS Development Yield -- CBD BOS Replacement Cost & Historical Trades -- CBD

BOS Vacancy & Employment BOS Demand Requirement For Equilibrium -- CBD

BOS Vacancy & Effective Rents -- CBD BOS Vacancy & Annualized New Construction -- CBD

Education and Health Services

21%

Professional and Business Services

17%

Trade Transportation and

Utilities 16%

Government 12%

Leisure and Hospitality

9%

Manufacturing 8%

Financial Activities 7%

Other Services 4%

Construction 3%

Information 3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Rep

lacem

en

t Y

ield

& 1

0-Y

ear

S

pre

ad

New

Co

nstr

ucti

on

, %

Of

Exis

tin

g

Sto

ck, A

nn

uali

zed

Class A Starts Class A Replacement Yield Dev Spread To 10-YR

0%

15%

30%

45%

60%

75%

90%

$0

$100

$200

$300

$400

$500

$600

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Dis

co

un

t T

o R

ep

lacem

en

t C

ost

Asset

Valu

e (

$/S

F)

% discount - Class A % discount - Class B Replacement CostTrading Price Class A Trading Price Class B

0%

3%

6%

9%

12%

15%

18%

21%

24%

$0

$5

$10

$15

$20

$25

$30

$35

$40

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13 V

acan

cy (

Dir

ect &

In

dir

ect)

--

Bars

Eff

ecti

ve R

en

ts (

$ / S

F)

-- L

ines

Vacancy, Total, Class A Vacancy, Total, Class B Effective Rent, Class A Effective Rent, Class B

0%

5%

10%

15%

20%

25%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Vacan

cy (

Dir

ect &

In

dir

ect)

Vacancy, Direct, Class A Vacancy, Indirect, Class A Class A Starts

-9.0

-6.0

-3.0

0.0

3.0

6.0

9.0

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13 S

F O

f A

bso

rpti

on

Need

ed

Fo

r R

en

t G

row

th -

- B

ars

(In

Mil

lio

ns)

Em

plo

yees N

eed

ed

To

Ab

so

rb S

F

To

Vacan

cy E

qu

ilib

riu

m -

- L

ine

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

0%

5%

10%

15%

20%

25%

30%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13 Em

plo

ym

en

t G

row

th -

- T

rail

ing

F

ou

r Q

uart

er

YO

Y G

row

th

Vacan

cy (

Dir

ect &

In

dir

ect)

Vacancy, Direct -- Total Vacancy, Indirect -- Total Employment Growth

7Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Charlotte

Activity is really good right now in Charlotte

A lot of companies coming into the market including: MetLife

500k SF requirement bringing 1400 jobs to the city Chiquita Brands United Technologies

Tenants are demanding more space and longer terms Average deal size in the suburbs was 5-10k SF, now 10-12k SF In Uptown was 15-20k SF and that is getting bigger as well

Both the suburbs and CBD are experiencing solid leasing activity Strong rental rates and lower concessions are being realized

Rental rates declined 20-30% in downturn, now back to that level Uptown and SouthPark

TIs were $40/SF 24 months ago, now $30/SF Free rent is 0.5-months/year

The one market where Financial Services firms are growing Demand drivers in the market include Energy and Financial Services Tenants are looking for a mixed-use type environment Employees still want to work close to home

Suburbs/CBD are both doing well due to this trend Definitely getting more dense

Charlotte is experiencing the National market trend of densification Recent lease started at 4 employees/1,000 SF; signed at 7/1,000 SF

Charlotte

Office SF % of TotalPKY 1,693,182 14.3%CUZ 1,065,000 9.0%FSP 171,886 1.9%

Source: SNL Financial and Baird research

8Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Chicago

Leasing activity has slowed after working through pent-up demand

Leasing activity has slowed over the past 6-12 months The pent-up demand is gone and companies are not growing rapidly Not many large deals out in the market today Small- and Mid-size deals are what’s driving the market

5k SF tenants are going to 25k SF Demand is coming from new economy-based companies

Tenants are moving up in building quality; a flight to quality Buildings that have had improvements are performing better

Negotiation times are speeding up slightly Tenants are more comfortable with business environment

Image and location are important in signing leases New developments should perform well despite overall market vacancy

McDermott Will & Emery signed a 225k SF lease at 444 W. Lake William Blair is entering the market soon DLA Piper is a likely candidate for a development

Location and space efficiency is key for tenants Tenants want the image, location and newness at their location

Large floor plates near transportation could be top performers in market 111 North Canal is a loft-type building in a good location

Can accommodate large floor plate users in the 50k SF range Tech companies are looking for this type of space

Merchandise Mart Complex is very attractive for similar reasons

Chicago

Office SF % of TotalPDM 4,972,538 23.5%FSP 746,709 8.1%CWH 3,923,656 5.0%GOV 57,770 0.6%DRE 99,538 0.1%

Source: SNL Financial and Baird research

9Robert W. Baird & Co.

Baird's Skyline

Chicago Office Market Fundamentals -- Central Business District (CBD)

Class A Class B Total

Size Of Chicago Office Market (MSF) 83.0 68.5 151.5

% of total market 54.8% 45.2% 100.0%

Office Employment, Estimated ('000) 433.8 370.4 804.2

1-year historical employment growth 1.5%

5-year historical employment growth -0.6%

10-year historical employment growth 0.1%

Vacancy (%) 15.0% 12.1% 12.9%

Direct 13.8% 11.1% 12.0%

Sublet 1.2% 1.1% 0.8%

Effective Rents ($/SF) $30.34 $27.35 $28.99

1-year historical rent growth -2.3% 5.7% 1.3%

5-year historical rent growth 0.1% 3.8% 1.8%

10-year historical rent growth -0.4% 0.7% 0.1%

Vacancy Change Needed For Rent Growth 2.9%

SF of Absorption Needed For Equilibrium (MSF) 5.6

Employment Needed For Equilibrium 34,724

Office Employment Growth Needed For Equilibrium 4.3%

Estimated Time To Reach Market Equilibrium (yrs) 1.4

Current Replacement Cost $346

Acquisition Cost Estimate $413 $179 $307

Discount To Replacement Cost -19.2% 48.3% 11.4%

Current Development Yield 8.9%

Current Acquisition Yield 4.8% 8.3% 6.4%

Public REIT Exposure SF ('000) % of port.

PDM 3,654 17.2%

CWH 3,591 4.6%

FSP 375 4.1%

Vacancy, Rent & Construction Analysis

Source: Bureau of Labor Statistics, CoStar, and Baird estimates Source: Bureau of Labor Statistics, CoStar, and Baird estimates

Source: CoStar and Baird Research Source: CoStar and Baird Research

Development Yield & Replacement Cost Analysis

Source: CoStar and Baird estimates Source: CBRE, Colliers, Grubb & Ellis, Jones Lang LaSalle, Real Capital Analytics, RSMeans, and Baird estimates

CHI Employment BreakdownCHI Statistics at a Glance -- CBD

CHI Development Yield -- CBD CHI Replacement Cost & Historical Trades -- CBD

CHI Vacancy & Employment CHI Demand Requirement For Equilibrium -- CBD

CHI Vacancy & Effective Rents -- CBD CHI Vacancy & Annualized New Construction -- CBD

Trade Transportation and

Utilities 21%

Professional and Business Services

17%

Education and Health Services

15%

Government 13%

Leisure and Hospitality

9%

Manufacturing 9%

Financial Activities 7%

Other Services 4%

Construction 3%

Information 2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Rep

lacem

en

t Y

ield

& 1

0-Y

ea

r

Sp

rea

d

Ne

w C

on

str

ucti

on

, %

Of

Exis

tin

g

Sto

ck, A

nn

ua

lized

Class A Starts Class A Replacement Yield Dev Spread To 10-YR

0%

15%

30%

45%

60%

75%

90%

$0

$100

$200

$300

$400

$500

$600

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Dis

co

un

t T

o R

ep

lacem

en

t C

ost

Asset

Va

lue (

$/S

F)

% discount - Class A % discount - Class B Replacement CostTrading Price Class A Trading Price Class B

0%

5%

10%

15%

20%

25%

$0

$5

$10

$15

$20

$25

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13 Va

ca

nc

y (

Dir

ec

t &

In

dir

ec

t) -

- B

ars

Eff

ecti

ve R

en

ts (

$ / S

F)

-- L

ines

Vacancy, Total, Class A Vacancy, Total, Class B Effective Rent, Class A Effective Rent, Class B

0%

5%

10%

15%

20%

25%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Va

ca

nc

y (

Dir

ec

t &

In

dir

ec

t)

Vacancy, Direct, Class A Vacancy, Indirect, Class A Class A Starts

-12.0

-8.0

-4.0

0.0

4.0

8.0

12.0

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13 S

F O

f A

bso

rpti

on

Ne

ed

ed

Fo

r R

en

t G

row

th -

- B

ars

(In

Millio

ns)

Em

plo

ye

es N

ee

de

d T

o A

bso

rb S

F

To

Va

ca

nc

y E

qu

ilib

riu

m -

- L

ine

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

0%

5%

10%

15%

20%

25%

30%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Em

plo

ym

en

t G

row

th -

- T

railin

g

Fo

ur

Qu

art

er

YO

Y G

row

th

Va

ca

nc

y (

Dir

ec

t &

In

dir

ec

t)

Vacancy, Direct -- Total Vacancy, Indirect -- Total Employment Growth

10Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Dallas

Things are getting better; leasing activity is improving

Dallas has performed well with some submarkets really taking off Uptown, Far North Dallas, and Las Colinas seeing good activity

Two-fold market with Mid- and Small-sized deal activity Average deal size is 20-50k SF Entrepreneurial businesses are growing around 1-4k SF

Companies are looking to create a presence in Dallas; satellite offices State Farm signed 9k SF as a corporate relocation out of CA

Deal negotiations have been taking a little longer Decreasing free rent is helping the market’s overall net effective rent

Rents are starting to rise for the overall Dallas MSA Tenants are still requesting more and more TIs every year

Class A TIs for a 5-year term is $20-30/SF 10-year deals could get up to $40/SF in TIs Free rent for a 5-year deal is 2-3 months

Underperforming markets could see 7-9 months Las Colinas is 1 month per year of lease term

Mortgage servicing groups and Tech firms are active in the market Mortgage servicing groups are growing and driving the market Tech tenants are active in the market as well

Uptown and Las Colinas, different feels but each meeting tenants’ needs The Uptown and Las Colinas submarkets are both performing well

Uptown: Work, live, play environment Employee retention is a huge focus for tenants Amenity rich submarket; shops, residential, bars A lot of land to do BTS projects Starting to see spec developments take place

Las Colinas: Historically, a regional HQ driven submarket Doing really well since the recovery Access to labor pools and close to the airport

Development activity is well underway including some spec office For the first time since 2007, Dallas is seeing some spec office projects Several proposed sites in the Uptown submarket

One project landed KPMG as its anchor tenant Will begin “putting the shovel in the ground” soon

1.0MSF is under construction, developers targeting 40-50% pre-leasing Buildings will lease fast with demand spilling into other buildings

Densification is occurring in Dallas Cramming more people in the same space Market is realizing 5-6 employees/1,000SF

Dallas

Office SF % of TotalFSP 1,467,714 15.9%CUZ 1,047,000 8.9%PDM 1,279,944 6.0%PSB 715,000 2.5%SIR 607,549 2.5%BDN 150,000 0.5%

Source: SNL Financial and Baird research

11Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Denver

Downtown is where the majority of the leasing activity is occurring

The Denver CBD is outpacing the decent overall MSA activity level Nobody is looking to vacate the Denver market Law firms are the No. 1 occupier of space in the market

Rental rates are definitely increasing, TIs remaining steady Increased leasing activity is driving rents higher TIs for the market are $4-6/SF/year of term

Max is ~$50/SF with landlords trying not to go over $40/SF Free rent is 1 month/year of lease term with max being 5-6 months

Energy sector is driving the incremental demand in the market Energy is the key driver of growth Some Law firms that are expanding their space needs

Construction is occurring in the LoDo area of the CBD 16M is a mixed-use development that will have 130k SF of office space

The project is located just a couple blocks from Union Station The development started spec but is now leased

Law firms and Energy companies are not reducing the space per employee Not seeing the densification among Law firms or Energy companies Realizing some reduction of space by other industries Densification doesn’t seem as prevalent as other markets

Not making a meaningful impact Best-in-class buildings in the CBD

Wells Fargo Center Republic Plaza (BPO owned) 1801 California (BPO owned)

Major renovations attracting tenants from outside the MSA

Denver

Office SF % of TotalFSP 1,358,213 14.7%BPO 3,735,000 4.9%GOV 422,973 4.1%IRET 152,603 1.2%CWH 672,465 0.9%PDM 148,200 0.7%SIR 140,162 0.6%

Source: SNL Financial and Baird research

12Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Houston

Nothing really to say but that it’s a “white hot” market

90% of Energy companies are growing on their renewals Hottest submarket is the Energy Corridor

Woodlands and Westchase to 249 are on fire The Galleria submarket is very stable

So much money in Houston right now Want the best product with the best amenities Absorption is going to new construction

Net new demand could come from foreign companies looking to enter Foreign companies are beginning to move to Houston

Generally speaking, everyone is growing BHP Billiton had 350k SF; now has 1.2MSF of space in 4 Oaks

Building recently purchased by CUZ (Post Oak Central) New construction rents are going up daily for Class A space

Demand for new construction is driving rates up daily Class B+ buildings are having rents go up as well TIs are in the $40-75/SF range for 12-15 year leases

3 months free rent New construction is drawing tenants from Class B space

Class B assets could be pressured given the move to new construction The majority of developments have some pre-leasing in place

Houston

Office SF % of TotalTPGI 2,453,492 23.4%PKY 2,182,012 18.4%FSP 1,191,630 12.9%BPO 9,173,000 11.9%CUZ 1,280,000 10.8%PDM 312,564 1.5%DRE 159,175 0.1%LRY 43,200 0.1%

Source: SNL Financial and Baird research

13Robert W. Baird & Co.

Baird's Skyline

Houston Office Market Fundamentals -- Suburban (SUB)

Class A Class B Total

Size Of Houston Office Market (MSF) 75.8 93.2 169.0

% of total market 44.8% 55.2% 100.0%

Office Employment, Estimated ('000) 525.0 615.7 1,140.7

1-year historical employment growth 3.9%

5-year historical employment growth 1.6%

10-year historical employment growth 1.7%

Vacancy (%) 10.3% 14.5% 12.7%

Direct 9.8% 14.1% 12.1%

Sublet 0.6% 0.5% 0.5%

Effective Rents ($/SF) $29.37 $18.99 $23.64

1-year historical rent growth 3.9% 1.7% 2.7%

5-year historical rent growth 5.3% 1.7% 3.3%

10-year historical rent growth 3.8% 1.4% 2.5%

Vacancy Change Needed For Rent Growth 0.7%

SF of Absorption Needed For Equilibrium (MSF) 1.1

Employment Needed For Equilibrium 8,507

Office Employment Growth Needed For Equilibrium 0.7%

Estimated Time To Reach Market Equilibrium (yrs) 0.2

Current Replacement Cost $213

Acquisition Cost Estimate $222 $124 $168

Discount To Replacement Cost -4.5% 41.7% 21.0%

Current Development Yield 8.2%

Current Acquisition Yield 5.7% 8.3% 7.1%

Public REIT Exposure SF ('000) % of port.

PKY 2,182 18.4%

FSP 1,192 12.9%

CUZ 1,280 10.8%

PDM 313 1.5%

DRE 159 0.1%

LRY 43 0.1%

Vacancy, Rent & Construction Analysis

Source: Bureau of Labor Statistics, CoStar, and Baird estimates Source: Bureau of Labor Statistics, CoStar, and Baird estimates

Source: CoStar and Baird Research Source: CoStar and Baird Research

Development Yield & Replacement Cost Analysis

Source: CoStar and Baird estimates Source: CBRE, Colliers, Grubb & Ellis, Jones Lang LaSalle, Real Capital Analytics, RSMeans, and Baird estimates

HOU Employment BreakdownHOU Statistics at a Glance -- SUB

HOU Development Yield -- SUB HOU Replacement Cost & Historical Trades -- SUB

HOU Vacancy & Employment HOU Demand Requirement For Equilibrium -- SUB

HOU Vacancy & Effective Rents -- SUB HOU Vacancy & Annualized New Construction -- SUB

Trade Transportation and

Utilities 21%

Professional and Business Services

15%

Government 14% Education and

Health Services 12%

Leisure and Hospitality

10%

Manufacturing 9%

Construction 7%

Financial Activities 5%

Other Services 3%

Mining and Logging

4%

0%

2%

4%

6%

8%

10%

12%

0%

5%

10%

15%

20%

25%

30%

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Rep

lacem

en

t Y

ield

& 1

0-Y

ear

S

pre

ad

New

Co

nstr

ucti

on

, %

Of

Exis

tin

g

Sto

ck, A

nn

uali

zed

Class A Starts Class A Replacement Yield Dev Spread To 10-YR

0%

15%

30%

45%

60%

75%

90%

$0

$50

$100

$150

$200

$250

$300

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Dis

co

un

t T

o R

ep

lacem

en

t C

ost

Asset

Valu

e (

$/S

F)

% discount - Class A % discount - Class B Replacement CostTrading Price Class A Trading Price Class B

0%

5%

10%

15%

20%

25%

$0

$5

$10

$15

$20

$25

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13 V

acan

cy (

Dir

ect &

In

dir

ect)

--

Bars

Eff

ecti

ve R

en

ts (

$ / S

F)

-- L

ines

Vacancy, Total, Class A Vacancy, Total, Class B Effective Rent, Class A Effective Rent, Class B

0%

5%

10%

15%

20%

25%

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Vacan

cy (

Dir

ect &

In

dir

ect)

Vacancy, Direct, Class A Vacancy, Indirect, Class A Class A Starts

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

-75,000

-50,000

-25,000

0

25,000

50,000

75,000

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13 S

F O

f A

bso

rpti

on

Need

ed

Fo

r R

en

t G

row

th -

- B

ars

(In

Mil

lio

ns)

Em

plo

yees N

eed

ed

To

Ab

so

rb S

F

To

Vacan

cy E

qu

ilib

riu

m -

- L

ine

-15%

-10%

-5%

0%

5%

10%

15%

0%

5%

10%

15%

20%

25%

30%

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Em

plo

ym

en

t G

row

th -

- T

rail

ing

F

ou

r Q

uart

er

YO

Y G

row

th

Vacan

cy (

Dir

ect &

In

dir

ect)

Vacancy, Direct -- Total Vacancy, Indirect -- Total Employment Growth

14Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Jacksonville

Major tenants could move from the suburbs to downtown and vice versa

Stein Mart and Carolina Casualty are both considering space options Looking for long-term deals and are assessing their options

Excess space in the market with known move-outs downtown Rental rates are soft

Rental rates are in the $20-22/SF range TIs for the market are close to $35/SF

New construction will enter the market Large blocks of space are limited downtown Will likely see BTS options in the suburbs to accommodate tenant needs

Jacksonville

Office SF % of TotalPKY 1,459,678 12.3%LRY 1,041,353 1.3%CWH 318,997 0.4%

Source: SNL Financial and Baird research

15Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Los Angeles

Leasing volume has been slow, Playa Vista seeing increased demand

Playa Vista is the new hot market driven by new retail development Cheaper rents and new amenities are attracting tenants

Red Bull is looking at Playa Vista; 250k SF Riot Games looking at submarket; 300k SF

Adding electric charging stations, a popular demand by tenants Santa Monica has outpaced the overall market the past 18 months

Tech companies are driving demand in the submarket Average deal size was 5-10k SF but is increasing

Financial services firms are all decreasing space needs Advertising, marketing and entertainment are increasing space

Tenants are seeking cheaper rent alternatives Playa Vista is seeing incremental demand from Santa Monica

Playa Vista is realizing rents around $3.00/SF/month Santa Monica is realizing rents of ~$4.50/SF/month

TIs in Santa Monica are lower than the overall MSA West LA TI packages and free rent include:

First-generation space of $40-60/SF Second-generation space of $20-40/SF

~$5-10/SF/year of lease term Free rent is around 1 month/year of lease term

Migration occurring from Bunker Hill to LA Live and the Staples Center Professional services firms are still under pressure There is less demand for the Bunker Hill area of the CBD

Densification is limited given the parking restrictions Most employees drive to work and need access to parking The rail system is currently in place through Culver City

Will likely reach Santa Monica by 2015 Could alleviate some of the parking constraints

Los Angeles

Office SF % of TotalDEI 9,864,043 67.2%MPG 5,154,849 56.1%HPP 1,899,457 35.6%KRC 4,002,310 29.1%TPGI 2,496,084 23.8%BPO 5,184,000 6.8%PDM 998,792 4.7%VNO 355,000 0.5%CWH 212,000 0.3%

Source: SNL Financial and Baird research

16Robert W. Baird & Co.

Baird's Skyline

LA Office Market Fundamentals -- Central Business District (CBD)

Class A Class B Total

Size Of LA Office Market (MSF) 37.9 18.9 56.8

% of total market 66.8% 33.2% 100.0%

Office Employment, Estimated ('000) 287.7 148.1 435.8

1-year historical employment growth 2.9%

5-year historical employment growth -1.4%

10-year historical employment growth -0.3%

Vacancy (%) 15.2% 12.3% 14.3%

Direct 14.7% 12.3% 13.9%

Sublet 0.5% 0.1% 0.3%

Effective Rents ($/SF) $21.46 $14.38 $19.10

1-year historical rent growth -2.1% 2.1% -0.7%

5-year historical rent growth 2.7% 2.4% 2.6%

10-year historical rent growth 3.2% 0.6% 2.4%

Vacancy Change Needed For Rent Growth 3.3%

SF of Absorption Needed For Equilibrium (MSF) 1.9

Employment Needed For Equilibrium 16,572

Office Employment Growth Needed For Equilibrium 3.8%

Estimated Time To Reach Market Equilibrium (yrs) 0.3

Current Replacement Cost $498

Acquisition Cost Estimate $344 $274 $321

Discount To Replacement Cost 30.9% 44.9% 35.5%

Current Development Yield 3.9%

Current Acquisition Yield 5.0% 5.0% 5.0%

Public REIT Exposure SF ('000) % of port.

MPG 4,959 54.0%

TPGI 2,496 23.8%

DEI 2,595 17.7%

KRC 851 6.2%

BPO 3,517 4.6%

HPP 241 4.5%

VNO 243 0.3%

Vacancy, Rent & Construction Analysis

Source: Bureau of Labor Statistics, CoStar, and Baird estimates Source: Bureau of Labor Statistics, CoStar, and Baird estimates

Source: CoStar and Baird Research Source: CoStar and Baird Research

Development Yield & Replacement Cost Analysis

Source: CoStar and Baird estimates Source: CBRE, Colliers, Grubb & Ellis, Jones Lang LaSalle, Real Capital Analytics, RSMeans, and

Baird estimates

LA Employment BreakdownLA Statistics at a Glance -- CBD

LA Development Yield -- CBD LA Replacement Cost & Historical Trades -- CBD

LA Vacancy & Employment LA Demand Requirement For Equilibrium -- CBD

LA Vacancy & Effective Rents -- CBD LA Vacancy & Annualized New Construction -- CBD

Trade Transportation and

Utilities 20%

Professional and Business Services

16%

Education and Health Services

14%

Government 13%

Leisure and Hospitality

11%

Manufacturing 10%

Financial Activities 6%

Information 4%

Other Services 3%

Construction 3%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Rep

lacem

en

t Y

ield

& 1

0-Y

ea

r

Sp

rea

d

New

Co

nstr

ucti

on

, %

Of

Exis

tin

g

Sto

ck, A

nn

ua

lized

Class A Starts Class A Replacement Yield Dev Spread To 10-YR

0%

15%

30%

45%

60%

75%

90%

$0

$100

$200

$300

$400

$500

$600

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011 D

isco

un

t T

o R

ep

lacem

en

t C

ost

Asset

Va

lue (

$/S

F)

% discount - Class A % discount - Class B Replacement CostTrading Price Class A Trading Price Class B

0%

5%

10%

15%

20%

25%

$0

$5

$10

$15

$20

$25

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13 V

ac

an

cy

(D

ire

ct

& In

dir

ec

t) -

- B

ars

Eff

ec

tive

Re

nts

($

/ S

F)

-- L

ine

s

Vacancy, Total, Class A Vacancy, Total, Class B Effective Rent, Class A Effective Rent, Class B

0%

5%

10%

15%

20%

25%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Va

ca

nc

y (

Dir

ec

t &

In

dir

ec

t)

Vacancy, Direct, Class A Vacancy, Indirect, Class A Class A Starts

-9.0

-6.0

-3.0

0.0

3.0

6.0

9.0

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

SF

Of

Ab

so

rpti

on

Need

ed

Fo

r R

en

t G

row

th -

- B

ars

(In

Millio

ns)

Em

plo

yees N

eed

ed

To

Ab

so

rb S

F

To

Va

ca

nc

y E

qu

ilib

riu

m -

- L

ine

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

0%

5%

10%

15%

20%

25%

30%

1Q

98

3Q

98

1Q

99

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Em

plo

ym

en

t G

row

th -

- T

railin

g

Fo

ur

Qu

art

er

YO

Y G

row

th

Va

ca

nc

y (

Dir

ec

t &

In

dir

ec

t)

Vacancy, Direct -- Total Vacancy, Indirect -- Total Employment Growth

17Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

Miami

Market in general has definitely rebounded with fundamentals stabilizing

Market was flooded by spec buildings that hit the market near the peak Those buildings have since filled up alleviating the pressure

Fundamentals have stabilized with incremental demand Definitely still seeing a flight to quality from Class B assets Investment activity has outpaced overall leasing fundamentals

Buying on cap rate compression speculation Average tenant in the CBD is 6k SF on average

Only 10-15 tenants that occupy over 100k SF Downtown is recovering better with Miami Airport only doing “okay” Aventura is a heavily dense area that does not get overbuilt

Should perform well Expectations for gradual increases in rents, TIs remaining level

Landlords are a bit more bullish on the market and starting to push rents Higher rents are generally met with higher concessions

New leases downtown seeing TIs of $5/SF/year TIs for new leases in the suburbs are $4/SF/year Second gen. space is seeing $80/SF for 10-year term Free rent is 1 month/year up to 5-6 months for the term

Market is unlike any other, driven by Sovereign wealth The market is being driven by Latin American wealth purchasing homes

Residential developments are taking the best plots of land Limits the viable options for office developments Reduces new construction in the market

Sovereign wealth trickles in to increase office demand Still an immature market for office space; not institutionally relevant

Starting to change with a lot of institutional activity Northern Trust to move into Brickell World Plaza

Northern Trust is expected to move into 600 Brickell Ave. Taking 75k SF of space and will move in September ‘13

Foram Group owns the building which was developed in ‘11

Miami

Office SF % of TotalFSP 212,619 2.3%PKY 215,812 1.8%LRY 1,128,580 1.4%PDM 148,368 0.7%DRE 946,865 0.7%

Source: SNL Financial and Baird research

18Robert W. Baird & Co.

Baird's Skyline

Miami Office Market Fundamentals -- Central Business District (CBD)

Class A Class B Total

Size Of Miami Office Market (MSF) 7.2 8.4 15.6

% of total market 46.2% 53.8% 100.0%

Office Employment, Estimated ('000) 46.5 57.0 103.5

1-year historical employment growth 0.5%

5-year historical employment growth -1.5%

10-year historical employment growth 0.4%

Vacancy (%) 19.6% 15.4% 16.0%

Direct 19.2% 14.6% 15.7%

Sublet 0.4% 0.8% 0.3%

Effective Rents ($/SF) $37.91 $27.18 $32.13

1-year historical rent growth -2.8% -0.1% -1.3%

5-year historical rent growth 2.1% 1.9% 2.0%

10-year historical rent growth 2.1% 1.8% 1.9%

Vacancy Change Needed For Rent Growth 4.0%

SF of Absorption Needed For Equilibrium (MSF) 0.8

Employment Needed For Equilibrium 6,693

Office Employment Growth Needed For Equilibrium 6.5%

Estimated Time To Reach Market Equilibrium (yrs) 1.4

Current Replacement Cost $356

Acquisition Cost Estimate $415 $289 $347

Discount To Replacement Cost -16.5% 18.9% 2.5%

Current Development Yield 7.4%

Current Acquisition Yield 4.8% 4.9% 4.9%

Public REIT Exposure SF ('000) % of port.

PKY 111 0.9%

Vacancy, Rent & Construction Analysis

Source: Bureau of Labor Statistics, CoStar, and Baird estimates Source: Bureau of Labor Statistics, CoStar, and Baird estimates

Source: CoStar and Baird Research Source: CoStar and Baird Research

Development Yield & Replacement Cost Analysis

Source: CoStar and Baird estimates Source: CBRE, Colliers, Grubb & Ellis, Jones Lang LaSalle, Real Capital Analytics, RSMeans, and Baird estimates

MIA Employment BreakdownMIA Statistics at a Glance -- CBD

MIA Development Yield -- CBD MIA Replacement Cost & Historical Trades -- CBD

MIA Vacancy & Employment MIA Demand Requirement For Equilibrium -- CBD

MIA Vacancy & Effective Rents -- CBD MIA Vacancy & Annualized New Construction -- CBD

0%

3%

6%

9%

12%

15%

18%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Rep

lacem

en

t Y

ield

& 1

0-Y

ear

S

pre

ad

New

Co

nstr

ucti

on

, %

Of

Exis

tin

g

Sto

ck, A

nn

uali

zed

Class A Starts Class A Replacement Yield Dev Spread To 10-YR

0%

15%

30%

45%

60%

75%

90%

$0

$100

$200

$300

$400

$500

$600

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Dis

co

un

t T

o R

ep

lacem

en

t C

ost

Asset

Valu

e (

$/S

F)

% discount - Class A % discount - Class B Replacement Cost

Trading Price Class A Trading Price Class B

0%

5%

10%

15%

20%

25%

30%

$0

$5

$10

$15

$20

$25

$30

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Vacan

cy (

Dir

ect &

In

dir

ect)

--

Bars

Eff

ecti

ve R

en

ts (

$ / S

F)

-- L

ines

Vacancy, Total, Class A Vacancy, Total, Class B Effective Rent, Class A Effective Rent, Class B

0%

10%

20%

30%

40%

50%

60%

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Vacan

cy (

Dir

ect &

In

dir

ect)

Vacancy, Direct, Class A Vacancy, Indirect, Class A Class A Starts

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

SF

Of

Ab

so

rpti

on

Need

ed

Fo

r R

en

t G

row

th -

- B

ars

(In

Mil

lio

ns)

Em

plo

yees N

eed

ed

To

Ab

so

rb S

F

To

Vacan

cy E

qu

ilib

riu

m -

- L

ine

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

0%

5%

10%

15%

20%

25%

30%

3Q

99

1Q

00

3Q

00

1Q

01

3Q

01

1Q

02

3Q

02

1Q

03

3Q

03

1Q

04

3Q

04

1Q

05

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

Em

plo

ym

en

t G

row

th -

- T

rail

ing

F

ou

r Q

uart

er

YO

Y G

row

th

Vacan

cy (

Dir

ect &

In

dir

ect)

Vacancy, Direct -- Total Vacancy, Indirect -- Total Employment Growth

Government 24%

Professional and Business Services

16%

Education and Health Services

16%

Manufacturing 13%

Leisure and Hospitality

11%

Construction 7%

Financial Activities 4%

Information 4%

Other Services 3%

Trade Transportation and

Utilities 2%

19Robert W. Baird & Co.

July 9, 2013 | Real Estate Office

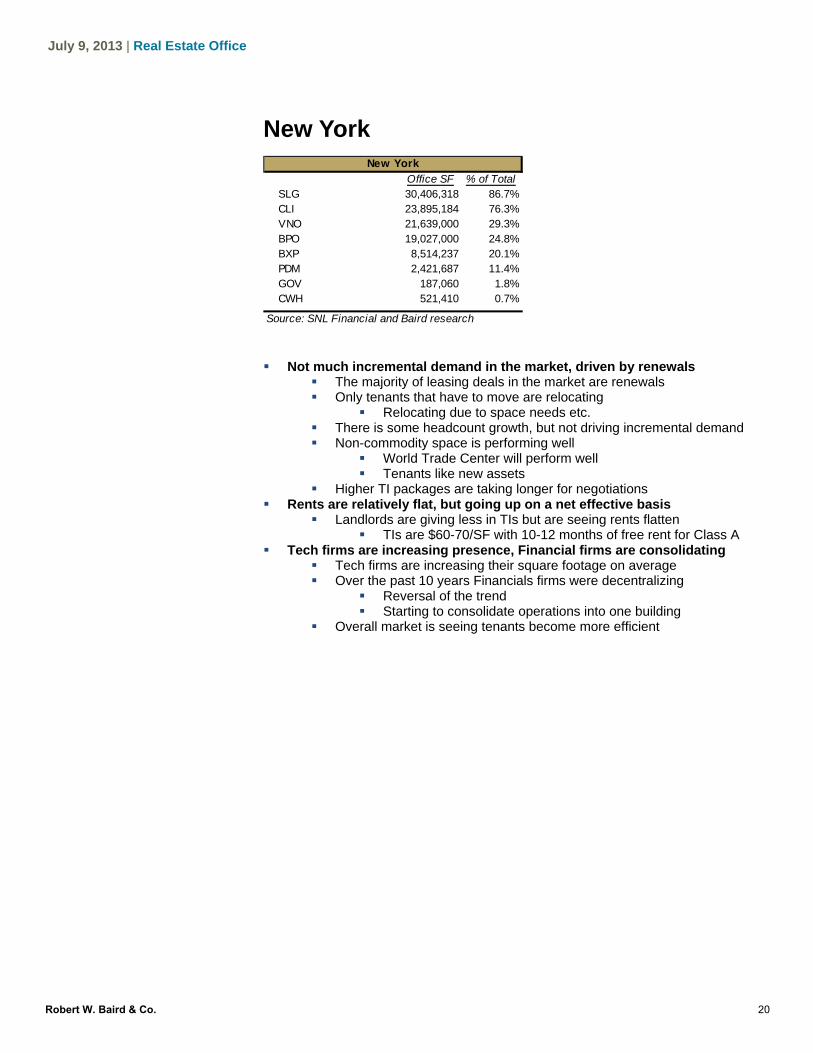

New York

Not much incremental demand in the market, driven by renewals

The majority of leasing deals in the market are renewals Only tenants that have to move are relocating

Relocating due to space needs etc. There is some headcount growth, but not driving incremental demand Non-commodity space is performing well

World Trade Center will perform well Tenants like new assets

Higher TI packages are taking longer for negotiations Rents are relatively flat, but going up on a net effective basis

Landlords are giving less in TIs but are seeing rents flatten TIs are $60-70/SF with 10-12 months of free rent for Class A

Tech firms are increasing presence, Financial firms are consolidating Tech firms are increasing their square footage on average Over the past 10 years Financials firms were decentralizing

Reversal of the trend Starting to consolidate operations into one building

Overall market is seeing tenants become more efficient

New York

Office SF % of TotalSLG 30,406,318 86.7%CLI 23,895,184 76.3%VNO 21,639,000 29.3%BPO 19,027,000 24.8%BXP 8,514,237 20.1%PDM 2,421,687 11.4%GOV 187,060 1.8%CWH 521,410 0.7%

Source: SNL Financial and Baird research

20Robert W. Baird & Co.

Baird's Skyline

Midtown Office Market Fundamentals -- Central Business District (CBD)

Class A Class B Total

Size Of Midtown Office Market (MSF) 228.9 118.1 347.0

% of total market 66.0% 34.0% 100.0%

Office Employment, Estimated ('000) 969.1 514.3 1,483.4

1-year historical employment growth 0.7%

5-year historical employment growth -0.1%

10-year historical employment growth 0.3%

Vacancy (%) 8.4% 5.8% 7.6%