realty cityscape - teja8.kuikr.com · executive summaryforeword prashant kumar thakur head of...

TRANSCRIPT

REALTY CITYSCAPE

Hyderabad September-2016

http://www.quikr.com/homes

Executive SummaryForeword

Prashant Kumar ThakurHead of Research & Data Services| [email protected]

Indian real estate is standing at a crossroad today. The euphoria ofdouble digit return on investment overnight has given way to a morerational expectation. The big bulls of real estate market- Delhi NCRand Mumbai have retreated resulting in softening of prices in thesemarket as well as significant investor’s money being stuck. Moreover,the RERA and development of REITS are also expected to re-define thelandscape of Indian Real Estate.

In the backdrop of weak real estate environment one city that isemerging out from the bruises of long drawn Telangana agitation isHyderabad. The prolonged uncertainty severely impacted the buyer’ssentiments and took the sheen away from brand Hyderabad as one ofthe fastest growing investment destinations. Corporates shelved theirplan of expansion and the buyers shied away from buying.

However, with the formation of Telangana, the period of uncertainty has given way to optimism andthe Hyderabad is slowly but steadily reclaiming the lost ground. It is one of the most affordablemarket with the good quality of ready to move in inventory. In today’s market scenario, buyers arepreferring ready to move in property as they do not take the risk of execution delays. As a result, thesales volume in Hyderabad has gradually picked up, clocking a growth of approximately 60% over aperiod of one year. The prices have appreciated in the range of 4-5% in the year 2016.

The city fares better in terms of infrastructure when it comes to metro and outer ring roadconnectivity as compared to Bangalore and other prominent IT destinations. Post Telanganaformation, Google has initiated its expansion plans in Hyderabad. The search giant is building its own7.2 acres’ campus in the city that is expected to be completed in the year 2019. Overall commercialreal estate has been on upswing- a precursor to residential market revival. In the first half of thecurrent year commercial real estate market has witnessed a robust absorption growth of 80% to 90%.Whereas, new office space supply has gone up by 120% as compared to the previous year.

In this backdrop, Hyderabad is at the cusp of a strong revival, presenting a sweet spot for the buyerswhere they have an opportunity to enter the market at a much more rational price. Hyderabadprovided a buyer with broader choice of ready to move in apartments, new launch, plots as well asvilla projects at a very compelling price. This report will take you through the journey of Hyderabadreal estate market from its emergence to stagnation and its journey towards gradual recovery.

Executive Summary

Hyderabad, the joint capital of Telangana and Andhra Pradesh, has been on the roller coaster ride since 2008. Once famously known as the cynosure for investors and realty developers, the city lost its charm during the global financial crisis. 2008-2013 was the worst-hit period in the history of the Hyderabad real estate market. While other major cities started recovering from the global financial crisis, Hyderabad was stuck in the state of political upheaval leading to prolonged stagnation in capital values and reduced absorption. The unsold inventory touched a all-time high during this period. Buoyed by these factors, Hyderabad witnessed stagnation in capital values till 2014. Investors and developers also took a cautious approach during this period that resulted in reduced new supply.

Post formation of the separate state and new industrial policy initiated by the government, the city gradually started recovering with increase in new launches across the city. The bifurcation of the new state resulted in realty sentiments moving northwards, which in turn reinstated buyers’ confidence in the sector. Primarily being an end-user market, Hyderabad holds strong future growth potential with the state-of-art infrastructure, better connectivity and affordable property values.

Improved infrastructure development, such as Outer Ring Road (ORR), Rajiv Gandhi International Airport, Multi-Model Transport System, Inner Ring Road, under construction Metro Rail and availability of Grade A offices at comparatively lower prices than those in Bangalore and Pune has made Hyderabad one of the most sought after destinations for real estate development. During the first half of 2016, Hyderabad witnessed the abortion in grade A office space by Amazon and IBM in Hi Tech City.

The residential market of Hyderabad witnessed significant increase in unit launches in the first half 2016 compared to its preceding period in 2015. West Hyderabad remained the prominent zone for new launches. Out of the total unit launched, Gachibowli, Hi Tech City, Narsingi and Madinagudawitnessed approximate 85 percent of new supply. Jubilee Hills and Banjara Hills in Central Hyderabad remained the prime residential markets in the city majorly compromising bungalows and independent houses. Interestingly, Gandhinagar and Begumpet emerged as posh residential markets with several luxury apartment projects.

Availability of grade A office space and direct connectivity to major micro-markets of Hyderabad through Outer Ring Road has made Hi Tech City and Gachibowli climb the realty growth ladder. Narsingi, Madinagua , Kukatpally and Madhapur are a few other western markets that have significantly benefited due to their proximity to Hi Tech City and Gachibowli.

INTRODUCTION1.

The foundation of Telangana as the 29th State of the country symbolizes a beginning and an end. Telangana gained its identity as the Telugu-speaking region of the princely state of Hyderabad, ruled by the Nizam of Hyderabad. The Nizam’srule became a princely state during the British Raj, and continued so for 150 years, with the city serving as its capital. On July 2013, the Congress Working Committee with one accord passed a resolution to endorse the establishment of a separate Telangana state. After several stages, the bill was placed in the Parliament and was finally passed in February 2014. The state of Telangana was officially formed on 2nd June 2014.

Hyderabad is the joint capital of Telangana and Andhra Pradesh for the next ten years. Andhra Pradesh has been bifurcated into two successor states - Telangana with ten districts and Andhra Pradesh with thirteen districts. The new state is bordered by the states of Karnataka in the west , Maharashtra in the north and north-west, Chhattisgarh in the north-east and Andhra Pradesh in the south and east. Hyderabad has a population of around 6.7 million and a metropolitan population of around 7.75 million, making it 4th most populous city in the country.

Hyderabad was traditionally a manufacturing, service and tourism based economy. In the early 1990s, the city witnessed a revolution in the Biopharmaceutical industry with establishment of the Genome Valley (Science Park), Indian Institute of Chemical Technology, National Institute of Pharmaceutical Education and Research, along with the state level institutions making Hyderabad the hub of pharmaceutical and biotechnology in the country. Improved infrastructure in bio-technology has attracted regional companies and MNC’s to set up offices, warehouses, research and development centers in the city.

Origin of the City

…Origin of the City

In the late 1990s, IT revolution started and Hyderabad emerged as the prominent IT destination in the country. The IT revolution transformed the development scenario in the city with key infrastructure developments announcement, favored policies and proactive support by the government. The improved infrastructure plan for the city attracted investors and developers from across the globe to participate in the vertical growth of the city. Major sectors, such as pharmaceuticals, Bio-technology, manufacturing and telecommunications, also started growing in the city, leading to the overall development of the city. This development phase impacted employment opportunities in the city, leading to increase in demand for housing, retail and hospitality.

In 2008, like any other city, Hyderabad was also affected badly by the global financial crisis. The realty sentiments took a dip and the development phase halted with sluggish demand and stagnation in capital values and absorption. Investors and developers restricted themselves from the market and took a wait and watch approach.

Post financial crisis, the city was trapped in political turmoil. While other major cities started recovering from the financial crisis, Hyderabad realty market witnessed stagnation in capital values and investor interest. During this period, the sum of unsold inventories reached an all-time high. Thus, developers largely focused on clearing existing stock instead of infusing fresh supply in the market.

On 2nd June 2014, the state of Telangana was officially formed, which led to political stability in the state. With this, realty sentiments improved and capital values also witnessed a significant rise of about 5-10% year-on-year. There were significant increases in new launches and government also initiated new industry policies to make Telangana the most preferred investment destination.

• Set up of pharmaceutical and electronic industries in the city.• Genome Valley announced. (Genome Valley (Science Park) is an Indian high- technology business

district)• Its strategic location in South-Central India gave Hyderabad the epithet of the “Gateway of South-

Central India.”

1970 -1990Beginning of

Pharmaceutical & Bio Technology Era

• The city witnessed development in diversified industries such as IT/ITEs Services, Biotech, Insurance and Financial institutions .

• Cyber Tower (1st Phase of Hi-tech City) was inaugurated in 1998.• The city started attracting investments in IT driven services.• Microsoft India’s Development Center operational in 1990.(largest campus of Microsoft in India).• Residential development happened in and around micro-markets of Commercial Business District, such

as Banjara Hills, Jubilee Hills, Begumpet, Ameerpet, Somajiguda, Himayat Nagar.

1990 – 2000Beginning of IT Era

• The city emerged as one of the prominent IT/ITEs hub of the country.• Outer Ring Road phase 1 construction started, from Gachibowli to Shamshabad. (Dec 2005).• Hi Techh City and Gachibowli emerged as the prominent IT hub of the city , which led to residential

development in peripheral areas such as Madhapur, Miyapur, Gachibowli, Kukatpally and Kondapur.• Developers welcomed unlimited FSI norm, and participated in vertical growth of the city.• FDI up to 100% is permitted on the automatic route in hotel and tourism sector/ construction and

maintenance of roads, highways, vehicular bridges, toll roads, vehicular tunnels, ports and harbors./ Mass Rapid Transport Systems in all metropolitan cities, including associated commercial development of real estate.

• Multi- Modal Transport System phase 1 started its operation in August 2003.• Hyderabad Metro Rail announced.

2000 – 2007 Hyderabad realty on Pinnacle

• Global Subprime mortgage crisis crashed the realty market in the city, with decline in launches and absorption.

• The city witnessed decline in capital values in major markets.• Rajiv Gandhi International Airport commenced operation.• Outer Ring Road commenced operation, phase 1 from Gachibowli to Shamshabad.• Hyderabad's IT exports reached US$ 4.7 billion.• Hyderabad's bio-pharmaceuticals exports reached US$3.1 billion.

2008- 2009Beginning of Global

Financial Crisis

• Realty market remained subdued post global crisis. Capital values remained stagnant.• Due to political instability and weak market sentiments, development activity slowed down in the city. • No new companies started operations in the city.

2010- 2012Political Turmoil in the

State

• Announcement of separate state.• Political instability remains. Slowdown continued in real estate development • Investors remained on back-seat. • Marginal price appreciation recorded due to increase in construction cost. • Central Government gave the official approval for the ITIR project.

2013Contd. Political Turmoil,

Separation of State

• Telangana state formed.• Hyderabad, became the second largest city in India for software exports in FY14.• The New Industrial Policy 2014 introduced, for making Telangana preferred investment destination.• Implementation of Telangana State Industrial Project Approval and Self Certification Systems (TS-iPASS).• Development of the Hyderabad-Warangal Industrial Corridor.• Improvement in realty sentiments due to political stability led to increase in new launches and marginal

price appreciation. Gachibowli and Hi Techh City remained the preferred micro-markets for new launches due to its proximity to commercial hub.

• Absorption remained sluggish, consumers continued with a wait-and-watch policy.• City witnessed a price appreciation of 5.2 per cent (year-on-year) in 2015.

2014 -2015 New State formation/Development on Track

• Realty sentiments improved and poised for correction. Decrease in unsold inventory.• The State GDP has grown at 9.2 % during 2015-2016 as against 8.8 % in during 2014-2015.• Hyderabad Metro Rail to be operational soon.• Outer Ring Road to be fully operational.• Absorption and New launches increased. • West Hyderabad remained the preferred destination for new launches due to its proximity to the

commercial hub of the city.

2016Realty Sentiments

improved

Timeline

Hyderabad is the joint capital of Telangana and Andhra Pradesh, and post 2024 it will be completelytransferred to Telangana. Information technology, pharmaceuticals and biotechnology industries arethe leading sectors which contribute to its economic growth. The city is the largest contributor to thestate's GDP of about $74 billion. It also has the highest number of SEZs (Special Economic Zone)among all cities in India. The main economic sectors of Hyderabad are traditional manufacturing, theknowledge sector and tourism.

Since its establishment in 1591, Hyderabad has been a global trade center in various fields andfamously known as only diamond market in the world. During Nizam’s rule, the city has witnessedfoundation of varied industrial zones leading to industrial growth with traditional manufacturing.During 1950s and 1960s, the city became home to several public enterprises such as BEL, NMDC,BHEL, HAL and DRDO.

In 1970s, the city witnessed the establishment of pharmaceutical and electronic industries due to itsstrategic location in south central India. While in 1990s, the city saw development in diversifiedindustries such as IT/ITeS services, Biotech, Insurance and Financial Institutions.

Industry Overview

Information Technology

The city is among the global centers of IT/ITeS and considered as the second silicon valley after Bangalore. The city’s IT sector includes the Information Technology – enabled services, Business Process Outsourcing, Entertainment Industries and Financial services. Hi Techh City and Gachibowli are the key commercial hubs and are home to several US based companies.Deloitte, GE Capital, KPMG, Ernst & Young, HSBC, Bank of America, Genpact are some of the financial services companies that have their offices in the city.During 2008-09, the city’s IT exports reached US $4.7 billion, and 22 per cent of the NASSCOM’s total membership is from the city.

Retail and Real Estate

Hyderabad is undoubtedly the most affordable residential markets out of the country's top seven cities including Mumbai, National Capital Region, Bangalore, Pune, Chennai and Kolkata. The current infrastructure development in and around the city has made it one of the most sought-after destination. The World Bank ranked the city as the second best city for doing business in 2009. Banjara Hills and Jubilee Hills are the prime residential areas. The Economic Times valued Banjara Hills to be worth of US $20.7 billion.Post the elections and formation of the new state, the city has seen quite positive realty sentiments with increase in new launches and absorption.

Economic Overview

Table 1.1: Economic Industry Overview

Industry Overview

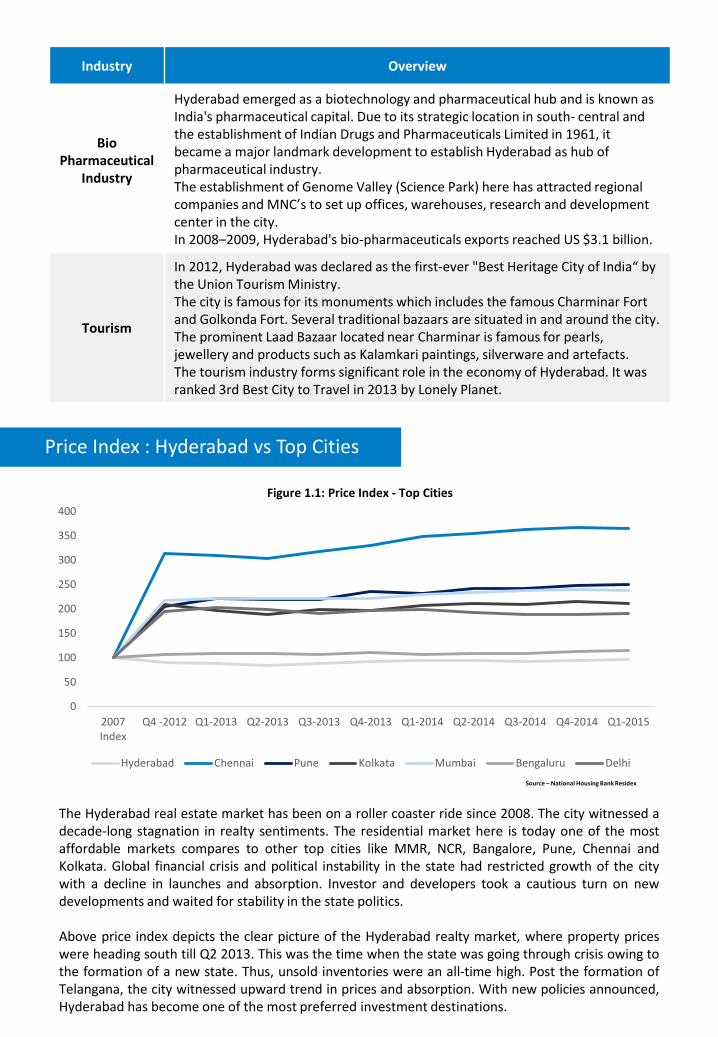

Bio Pharmaceutical

Industry

Hyderabad emerged as a biotechnology and pharmaceutical hub and is known as India's pharmaceutical capital. Due to its strategic location in south- central and the establishment of Indian Drugs and Pharmaceuticals Limited in 1961, itbecame a major landmark development to establish Hyderabad as hub of pharmaceutical industry. The establishment of Genome Valley (Science Park) here has attracted regional companies and MNC’s to set up offices, warehouses, research and development center in the city.In 2008–2009, Hyderabad's bio-pharmaceuticals exports reached US $3.1 billion.

Tourism

In 2012, Hyderabad was declared as the first-ever "Best Heritage City of India“ bythe Union Tourism Ministry.The city is famous for its monuments which includes the famous Charminar Fort and Golkonda Fort. Several traditional bazaars are situated in and around the city. The prominent Laad Bazaar located near Charminar is famous for pearls, jewellery and products such as Kalamkari paintings, silverware and artefacts.The tourism industry forms significant role in the economy of Hyderabad. It was ranked 3rd Best City to Travel in 2013 by Lonely Planet.

0

50

100

150

200

250

300

350

400

2007Index

Q4 -2012 Q1-2013 Q2-2013 Q3-2013 Q4-2013 Q1-2014 Q2-2014 Q3-2014 Q4-2014 Q1-2015

Hyderabad Chennai Pune Kolkata Mumbai Bengaluru Delhi

Source – National Housing Bank Residex

The Hyderabad real estate market has been on a roller coaster ride since 2008. The city witnessed adecade-long stagnation in realty sentiments. The residential market here is today one of the mostaffordable markets compares to other top cities like MMR, NCR, Bangalore, Pune, Chennai andKolkata. Global financial crisis and political instability in the state had restricted growth of the citywith a decline in launches and absorption. Investor and developers took a cautious turn on newdevelopments and waited for stability in the state politics.

Above price index depicts the clear picture of the Hyderabad realty market, where property priceswere heading south till Q2 2013. This was the time when the state was going through crisis owing tothe formation of a new state. Thus, unsold inventories were an all-time high. Post the formation ofTelangana, the city witnessed upward trend in prices and absorption. With new policies announced,Hyderabad has become one of the most preferred investment destinations.

Price Index : Hyderabad vs Top Cities

Figure 1.1: Price Index - Top Cities

CITY

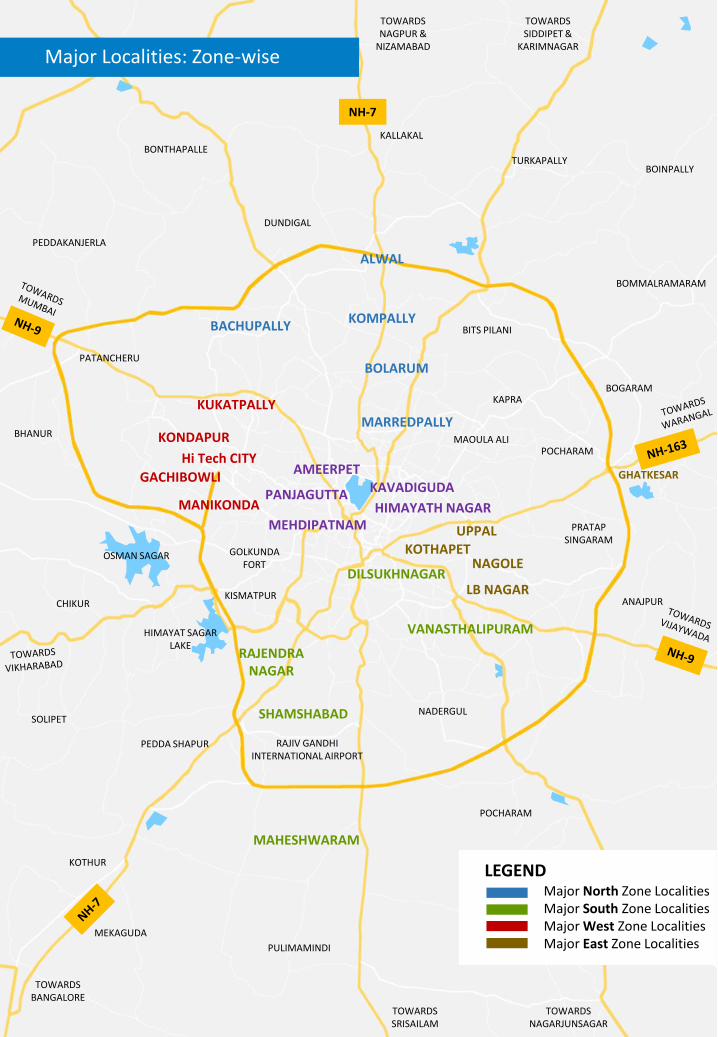

ZONES2.

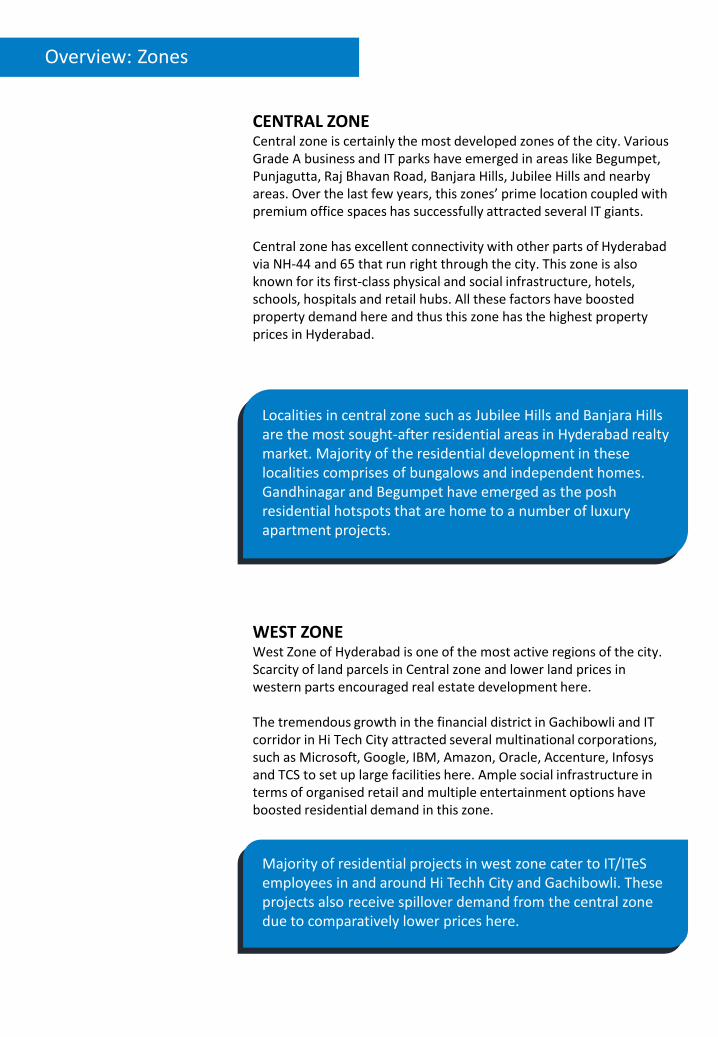

CENTRAL ZONE Central zone is certainly the most developed zones of the city. Various Grade A business and IT parks have emerged in areas like Begumpet, Punjagutta, Raj Bhavan Road, Banjara Hills, Jubilee Hills and nearby areas. Over the last few years, this zones’ prime location coupled with premium office spaces has successfully attracted several IT giants.

Central zone has excellent connectivity with other parts of Hyderabad via NH-44 and 65 that run right through the city. This zone is also known for its first-class physical and social infrastructure, hotels, schools, hospitals and retail hubs. All these factors have boosted property demand here and thus this zone has the highest property prices in Hyderabad.

WEST ZONEWest Zone of Hyderabad is one of the most active regions of the city. Scarcity of land parcels in Central zone and lower land prices in western parts encouraged real estate development here.

The tremendous growth in the financial district in Gachibowli and IT corridor in Hi Tech City attracted several multinational corporations, such as Microsoft, Google, IBM, Amazon, Oracle, Accenture, Infosys and TCS to set up large facilities here. Ample social infrastructure in terms of organised retail and multiple entertainment options have boosted residential demand in this zone.

Overview: Zones

Localities in central zone such as Jubilee Hills and Banjara Hills are the most sought-after residential areas in Hyderabad realty market. Majority of the residential development in these localities comprises of bungalows and independent homes. Gandhinagar and Begumpet have emerged as the posh residential hotspots that are home to a number of luxury apartment projects.

Majority of residential projects in west zone cater to IT/ITeS employees in and around Hi Techh City and Gachibowli. These projects also receive spillover demand from the central zone due to comparatively lower prices here.

Overview: Zones

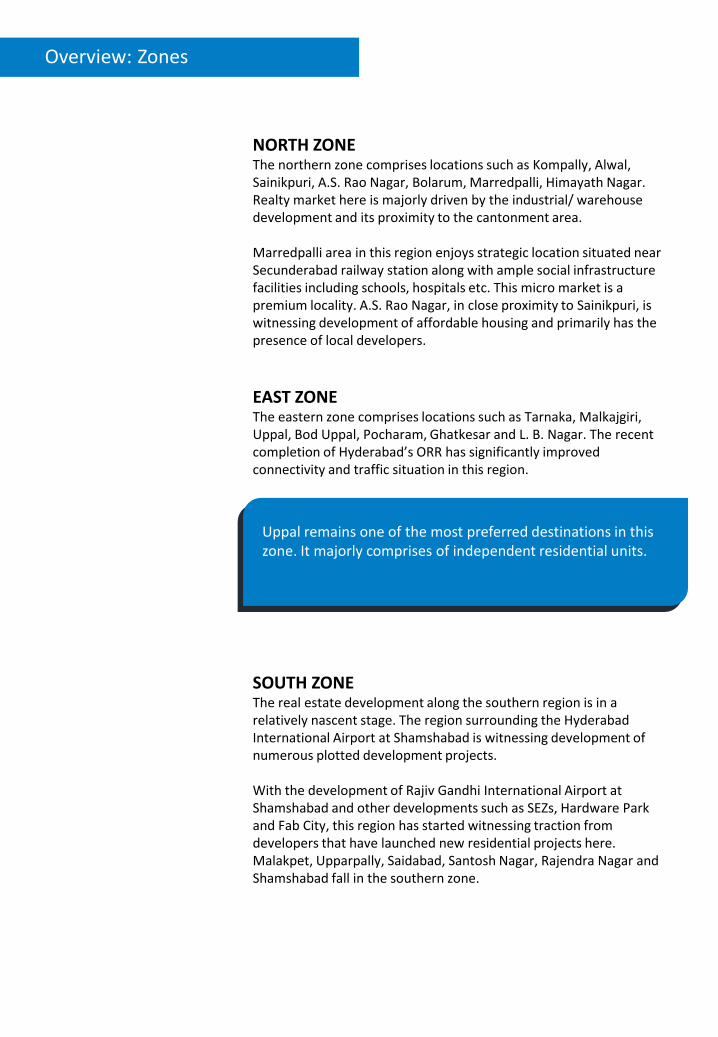

NORTH ZONE The northern zone comprises locations such as Kompally, Alwal, Sainikpuri, A.S. Rao Nagar, Bolarum, Marredpalli, Himayath Nagar. Realty market here is majorly driven by the industrial/ warehouse development and its proximity to the cantonment area.

Marredpalli area in this region enjoys strategic location situated near Secunderabad railway station along with ample social infrastructure facilities including schools, hospitals etc. This micro market is a premium locality. A.S. Rao Nagar, in close proximity to Sainikpuri, is witnessing development of affordable housing and primarily has the presence of local developers.

EAST ZONE The eastern zone comprises locations such as Tarnaka, Malkajgiri, Uppal, Bod Uppal, Pocharam, Ghatkesar and L. B. Nagar. The recent completion of Hyderabad’s ORR has significantly improved connectivity and traffic situation in this region.

Uppal remains one of the most preferred destinations in this zone. It majorly comprises of independent residential units.

SOUTH ZONE The real estate development along the southern region is in a relatively nascent stage. The region surrounding the Hyderabad International Airport at Shamshabad is witnessing development of numerous plotted development projects.

With the development of Rajiv Gandhi International Airport at Shamshabad and other developments such as SEZs, Hardware Park and Fab City, this region has started witnessing traction from developers that have launched new residential projects here. Malakpet, Upparpally, Saidabad, Santosh Nagar, Rajendra Nagar and Shamshabad fall in the southern zone.

PANJAGUTTA KAVADIGUDA

KOMPALLY

MARREDPALLY

BOLARUM

UPPAL

LB NAGAR

GACHIBOWLI

ALWAL

RAJENDRA NAGAR

SHAMSHABAD

KUKATPALLY

Hi Tech CITY

KONDAPUR

HIMAYATH NAGAR

AMEERPET

MEHDIPATNAM

MANIKONDA

BACHUPALLY

DILSUKHNAGAR

MAHESHWARAM

VANASTHALIPURAM

NAGOLE

GHATKESAR

KOTHAPET

KAPRA

MAOULA ALI

BOGARAM

ANAJPUR

NADERGUL

BHANUR

POCHARAM

DUNDIGAL

TURKAPALLY

KALLAKAL

BONTHAPALLE

CHIKUR

PEDDA SHAPUR

SOLIPET

KOTHUR

PULIMAMINDI

MEKAGUDA

OSMAN SAGAR

HIMAYAT SAGAR LAKE

BOINPALLY

BOMMALRAMARAM

PEDDAKANJERLA

KISMATPUR

GOLKUNDA FORT

RAJIV GANDHI INTERNATIONAL AIRPORT

PRATAP SINGARAM

POCHARAM

BITS PILANI

PATANCHERU

Major North Zone LocalitiesMajor South Zone LocalitiesMajor West Zone LocalitiesMajor East Zone Localities

LEGEND

NH-7

TOWARDS SIDDIPET &

KARIMNAGAR

TOWARDS BANGALORE

TOWARDS SRISAILAM

TOWARDS NAGARJUNSAGAR

TOWARDS NAGPUR &

NIZAMABADMajor Localities: Zone-wise

INFRASTRUCTURE

OVERVIEW3.

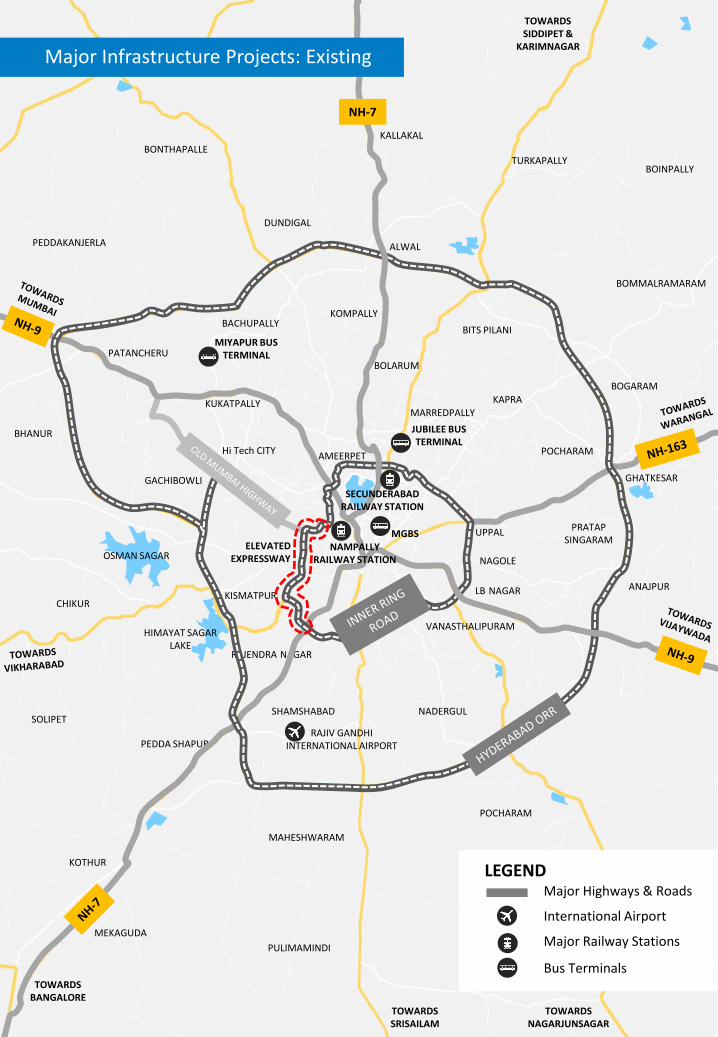

Name Development Connectivity Details

Rajiv Gandhi International Airport

International Airport

Flights to 60+ international and national airports

It is located in Shamshabad, south Hyderabad and was opened in March 2008

MMTSSuburban rail

system

Bhongir, Bolaram, Falaknuma, Jangaon, Kacheguda/Falaknuma, Malkajgiri, Manoharabad, Medchal, Mola ali, Secunderabad, Umdanagar

It connects various areasof the city

MGBSJubilee bus stationMiyapur bus depot

Bus TerminalsMajor cities Bangalore, Chennai, Mumbai, Pune, Vijayawada etc.

Provides intra and inter state transportation

Hyderabad ORRAccess

ControlledExpressway

This is a radial road that provides multiple access and exit points around the city

The Nehru Outer Ring Road encircles the city of Hyderabad and is a 158-km, 8-lane road

Hyderabad Elevated Expressway

ElevatedExpressway

Hyderabad International Airport to Mehdipatnam

This is a 11.6-km long expressway connecting the city centre to the airport

Hyderabad Inner Ring Road (IRR)

Arterial Road

Mehdipatnam, Banjara Hills, Punjagutta, Mettuguda, Begumpet, Tarnaka, Habsiguda, Uppal, NH-202 via Ghatkesar road, Nagole, L. B. Nagar, Santosh Nagar crossroads, ChandrayanGutta, Kurnool highway, Rajendra Nagar Bypass Road, Attapurand Rethibowli

It is a 50-km long arterial ring road encircling the inner perimeter of the city

Mumbai Highway (NH-9)

HighwayKukatpally, Patancheru, Chanda Nagar, Punjagutta, Dilsukhnagar, L. B. Nagar and Hayathnagar

It is an arterial road that connects the northwest and southeast locations to the centre of Hyderabad

NH-7 HighwayMedchal, Quthbullapur, Kompally, Secunderabad, Shivarampally and Gandiguda

It is an arterial road that connects the north and south locations to the centre of Hyderabad

Warangal Highway (NH-163)

HighwayUppal, Pocharam, Ghatkesar and Ramananthapur

It connects the eastern locations to the centre of Hyderabad

Old Mumbai Highway

HighwayMehdipatnam, Raidurgam, Shaikpet, Gachibowli, Serilingampally and Chanda Nagar

It connects the western locations to the centre of Hyderabad

Major Infrastructure Projects: Existing

Table 3.1: Hyderabad Metro Details

KOMPALLY

MARREDPALLY

BOLARUM

UPPAL

LB NAGAR

GACHIBOWLI

ALWAL

RAJENDRA NAGAR

SHAMSHABAD

KUKATPALLY

Hi Tech CITYAMEERPET

BACHUPALLY

MAHESHWARAM

VANASTHALIPURAM

NAGOLE

GHATKESAR

KAPRABOGARAM

ANAJPUR

NADERGUL

BHANUR

POCHARAM

DUNDIGAL

TURKAPALLY

KALLAKAL

BONTHAPALLE

CHIKUR

PEDDA SHAPUR

SOLIPET

KOTHUR

PULIMAMINDI

MEKAGUDA

OSMAN SAGAR

HIMAYAT SAGAR LAKE

BOINPALLY

BOMMALRAMARAM

PEDDAKANJERLA

KISMATPUR

RAJIV GANDHI INTERNATIONAL AIRPORT

PRATAP SINGARAM

POCHARAM

BITS PILANI

PATANCHERU

ELEVATED EXPRESSWAY

TOWARDS SIDDIPET &

KARIMNAGAR

TOWARDS BANGALORE

TOWARDS SRISAILAM

TOWARDS NAGARJUNSAGAR

NH-7

MIYAPUR BUS TERMINAL

JUBILEE BUS TERMINAL

MGBS

SECUNDERABAD RAILWAY STATION

NAMPALLY RAILWAY STATION

Major Infrastructure Projects: Existing

Major Highways & Roads

LEGEND

International Airport

Major Railway Stations

Bus Terminals

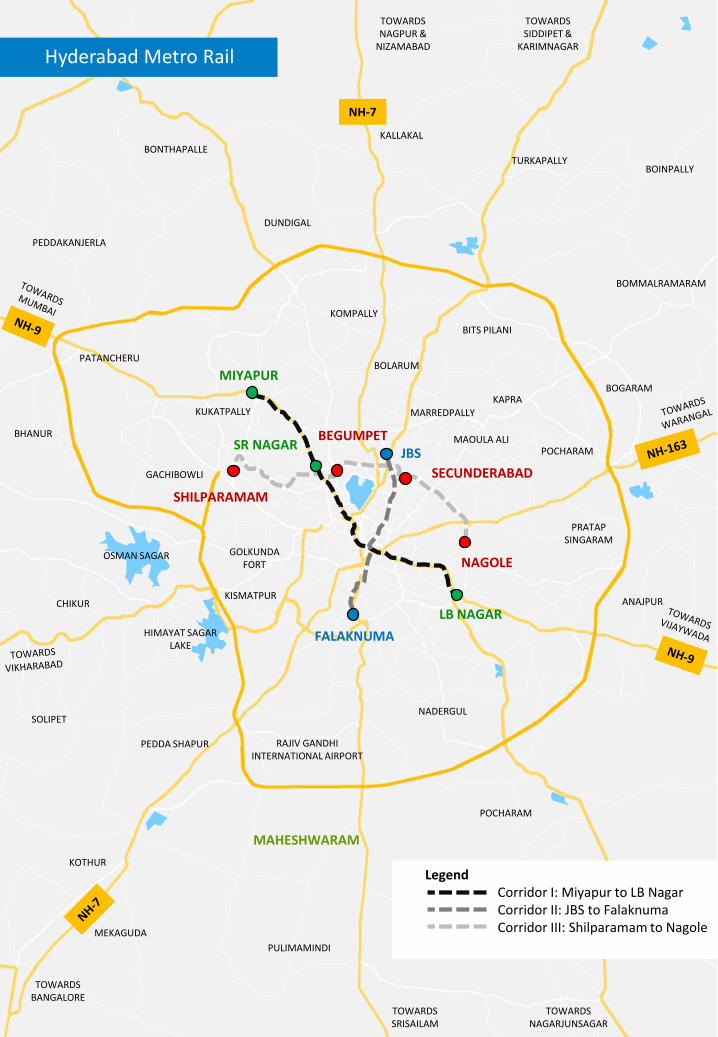

Hyderabad Metro Rail (HMR) is a rapid transit system, currently under construction. It is being implemented entirely on public-private partnership (PPP) basis, with the state government holding a minority equity stake. The construction work is being undertaken in two phases. Further, there are six stages of completion in Phase I.

Hyderabad Metro Rail

Metro Line Connectivity Total Length

Line I Miyapur - LB Nagar 29.9 kms

Line II JBS – Falaknuma 14.8 kms

Line IIIShilparamam -

Nagole26.5 kms

Stage Target Section Distance (in km) Line

Stage 1 Nagole to Secunderabad 9 Line III

Stage 2 Miyapur to S R Nagar 11.9 Line I

Stage 3 Secunderabad to Begumpet 10 Line III

Stage 4 Begumpet to Shilparamam 9.5 Line III

Stage 5 SR Nagar to LB Nagar 17.9 Line I

Stage 6 JBS to Falaknuma 14.8 Line II

Table 3.2: Hyderabad Metro Details

Table 3.3: Hyderabad Metro Rail Construction Stages (Phase-I)

MIYAPUR

SR NAGAR

LB NAGAR

JBSBEGUMPET

SECUNDERABAD

NAGOLE

FALAKNUMA

SHILPARAMAM

LegendCorridor I: Miyapur to LB NagarCorridor II: JBS to FalaknumaCorridor III: Shilparamam to Nagole

MAHESHWARAM

KAPRA

MAOULA ALI

BOGARAM

ANAJPUR

NADERGUL

BHANUR

POCHARAM

DUNDIGAL

TURKAPALLY

KALLAKAL

BONTHAPALLE

CHIKUR

PEDDA SHAPUR

SOLIPET

KOTHUR

PULIMAMINDI

MEKAGUDA

OSMAN SAGAR

HIMAYAT SAGAR LAKE

BOINPALLY

BOMMALRAMARAM

PEDDAKANJERLA

KISMATPUR

GOLKUNDA FORT

RAJIV GANDHI INTERNATIONAL AIRPORT

PRATAP SINGARAM

POCHARAM

BITS PILANI

PATANCHERU

NH-7

TOWARDS SIDDIPET &

KARIMNAGAR

TOWARDS BANGALORE

TOWARDS SRISAILAM

TOWARDS NAGARJUNSAGAR

TOWARDS NAGPUR &

NIZAMABAD

KOMPALLY

MARREDPALLY

BOLARUM

GACHIBOWLI

KUKATPALLY

Hyderabad Metro Rail

OFFICE MARKET

OVERVIEW4.

Hyderabad Office Market

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

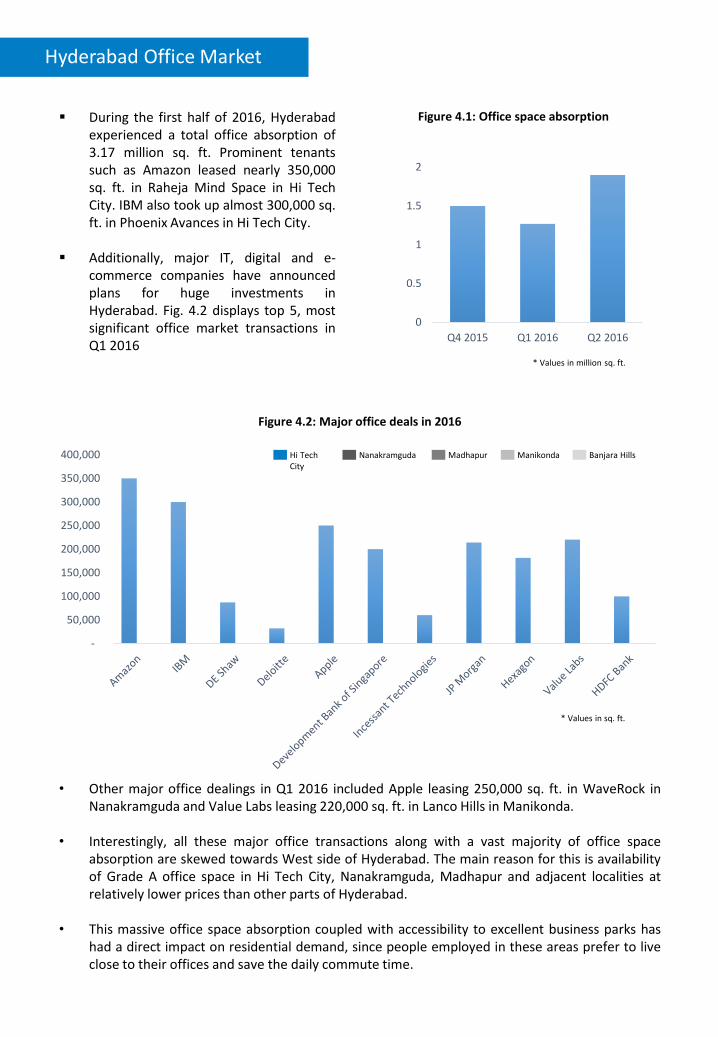

During the first half of 2016, Hyderabadexperienced a total office absorption of3.17 million sq. ft. Prominent tenantssuch as Amazon leased nearly 350,000sq. ft. in Raheja Mind Space in Hi TechCity. IBM also took up almost 300,000 sq.ft. in Phoenix Avances in Hi Tech City.

Additionally, major IT, digital and e-commerce companies have announcedplans for huge investments inHyderabad. Fig. 4.2 displays top 5, mostsignificant office market transactions inQ1 2016

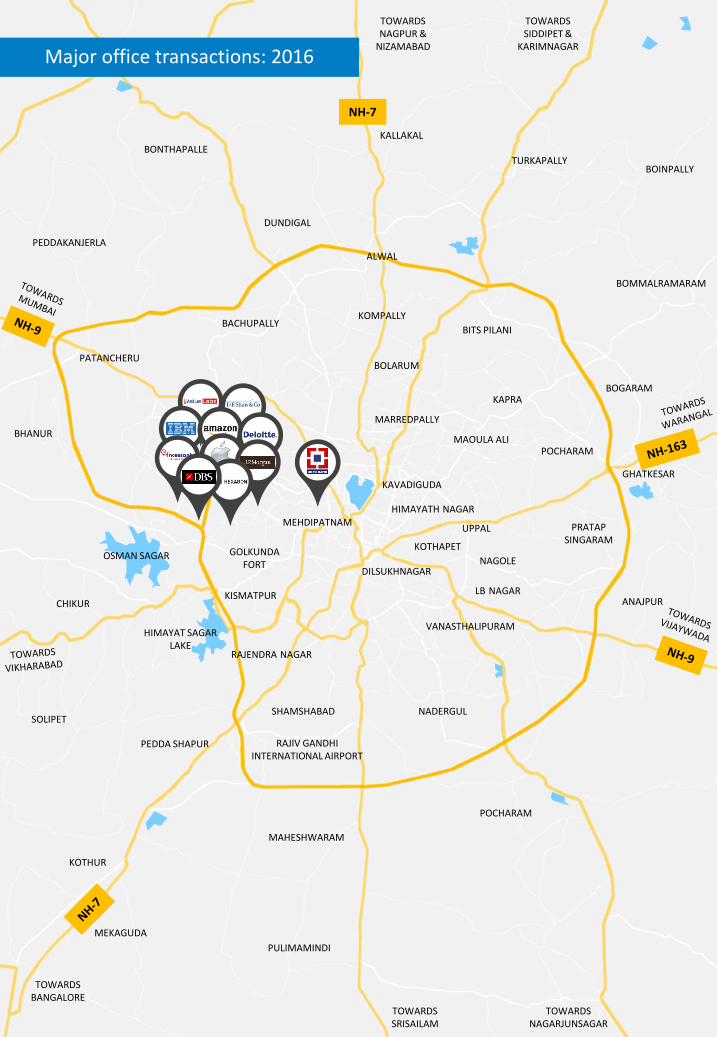

• Other major office dealings in Q1 2016 included Apple leasing 250,000 sq. ft. in WaveRock inNanakramguda and Value Labs leasing 220,000 sq. ft. in Lanco Hills in Manikonda.

• Interestingly, all these major office transactions along with a vast majority of office spaceabsorption are skewed towards West side of Hyderabad. The main reason for this is availabilityof Grade A office space in Hi Tech City, Nanakramguda, Madhapur and adjacent localities atrelatively lower prices than other parts of Hyderabad.

• This massive office space absorption coupled with accessibility to excellent business parks hashad a direct impact on residential demand, since people employed in these areas prefer to liveclose to their offices and save the daily commute time.

Figure 4.2: Major office deals in 2016

Figure 4.1: Office space absorption

Hi Tech City

Nanakramguda Madhapur Manikonda Banjara Hills

0

0.5

1

1.5

2

Q4 2015 Q1 2016 Q2 2016

* Values in million sq. ft.

* Values in sq. ft.

KAVADIGUDA

KOMPALLY

MARREDPALLY

BOLARUM

UPPAL

LB NAGAR

ALWAL

RAJENDRA NAGAR

SHAMSHABAD

Hi Tech CITY

HIMAYATH NAGARMEHDIPATNAM

BACHUPALLY

DILSUKHNAGAR

MAHESHWARAM

VANASTHALIPURAM

NAGOLE

GHATKESAR

KOTHAPET

KAPRA

MAOULA ALI

BOGARAM

ANAJPUR

NADERGUL

BHANUR

POCHARAM

DUNDIGAL

TURKAPALLY

KALLAKAL

BONTHAPALLE

CHIKUR

PEDDA SHAPUR

SOLIPET

KOTHUR

PULIMAMINDI

MEKAGUDA

OSMAN SAGAR

HIMAYAT SAGAR LAKE

BOINPALLY

BOMMALRAMARAM

PEDDAKANJERLA

KISMATPUR

GOLKUNDA FORT

RAJIV GANDHI INTERNATIONAL AIRPORT

PRATAP SINGARAM

POCHARAM

BITS PILANI

PATANCHERU

NH-7

TOWARDS SIDDIPET &

KARIMNAGAR

TOWARDS BANGALORE

TOWARDS SRISAILAM

TOWARDS NAGARJUNSAGAR

TOWARDS NAGPUR &

NIZAMABADMajor office transactions: 2016

Name Area (sq.ft) Location Zone

Knowledge City 1540000 Raidurg West

Meenakshi IT Campus 1300000 Gachibowli West

Amsri Brain Storm 900000 Gachibowli West

aVance – Bldg # H3 560000 Madhapur West

Salarpuria Sattvaa 1500000 Madhapur West

My Home Divija 3,000,000 Raidurg West

Laxmi Cyber Towers 1,000,000 Nanakramguda West

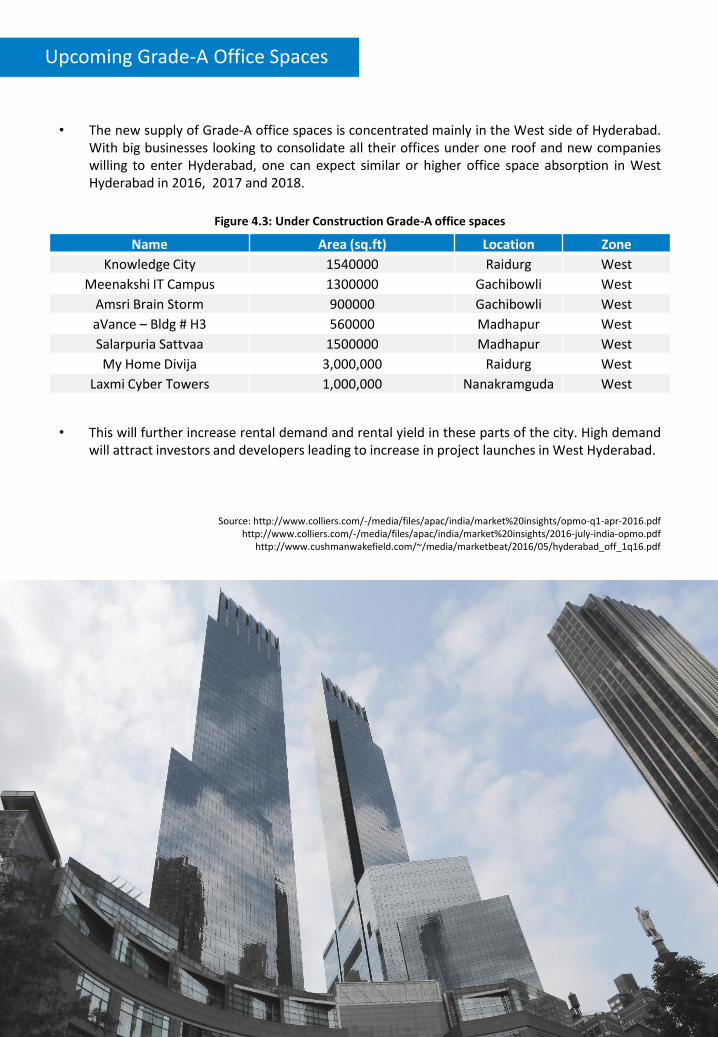

• This will further increase rental demand and rental yield in these parts of the city. High demandwill attract investors and developers leading to increase in project launches in West Hyderabad.

Figure 4.3: Under Construction Grade-A office spaces

Upcoming Grade-A Office Spaces

• The new supply of Grade-A office spaces is concentrated mainly in the West side of Hyderabad.With big businesses looking to consolidate all their offices under one roof and new companieswilling to enter Hyderabad, one can expect similar or higher office space absorption in WestHyderabad in 2016, 2017 and 2018.

Source: http://www.colliers.com/-/media/files/apac/india/market%20insights/opmo-q1-apr-2016.pdfhttp://www.colliers.com/-/media/files/apac/india/market%20insights/2016-july-india-opmo.pdf

http://www.cushmanwakefield.com/~/media/marketbeat/2016/05/hyderabad_off_1q16.pdf

RESIDENTIAL

MARKET TRENDS5.

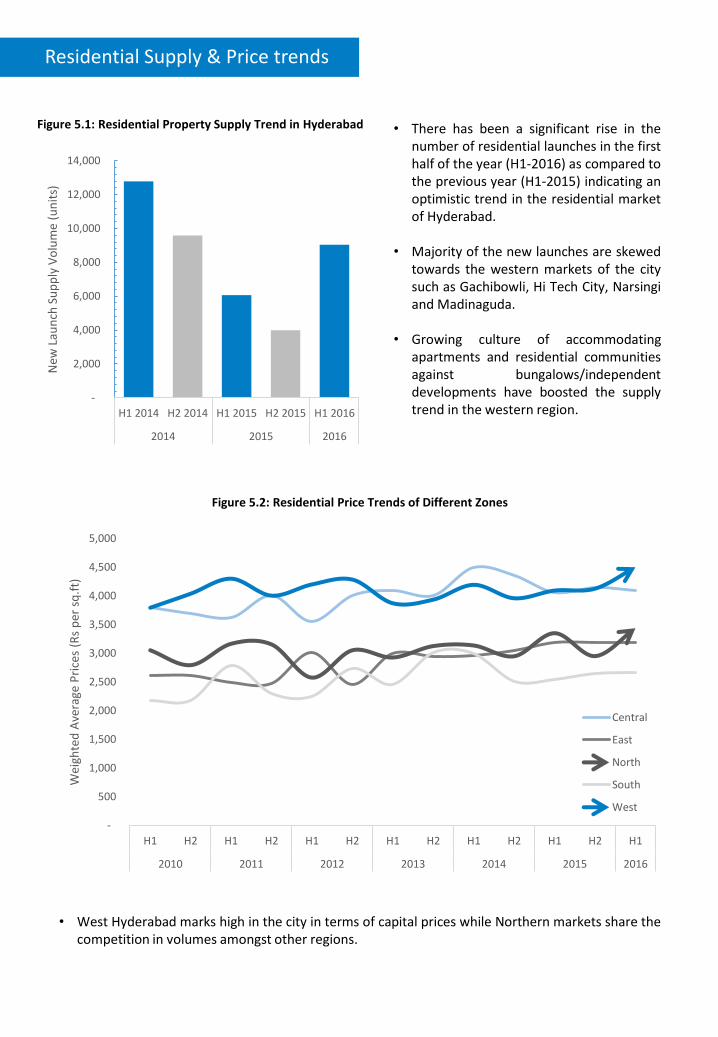

• There has been a significant rise in thenumber of residential launches in the firsthalf of the year (H1-2016) as compared tothe previous year (H1-2015) indicating anoptimistic trend in the residential marketof Hyderabad.

• Majority of the new launches are skewedtowards the western markets of the citysuch as Gachibowli, Hi Tech City, Narsingiand Madinaguda.

• Growing culture of accommodatingapartments and residential communitiesagainst bungalows/independentdevelopments have boosted the supplytrend in the western region.

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

H1 2014 H2 2014 H1 2015 H2 2015 H1 2016

2014 2015 2016

New

Lau

nch

Su

pp

ly V

olu

me

(un

its)

• West Hyderabad marks high in the city in terms of capital prices while Northern markets share thecompetition in volumes amongst other regions.

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1 H2 H1

2010 2011 2012 2013 2014 2015 2016

Wei

ghte

d A

vera

ge P

rice

s (R

s p

er s

q.f

t)

Central

East

North

South

West

Residential Supply & Price trends

Figure 5.1: Residential Property Supply Trend in Hyderabad

Figure 5.2: Residential Price Trends of Different Zones

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

A M L UL A M L UL A M L UL A M L UL A M L UL

H1 2014 H2 2014 H1 2015 H2 2015 H1 2016

2014 2015 2016

Res

iden

tial

Su

pp

ly (

un

its)

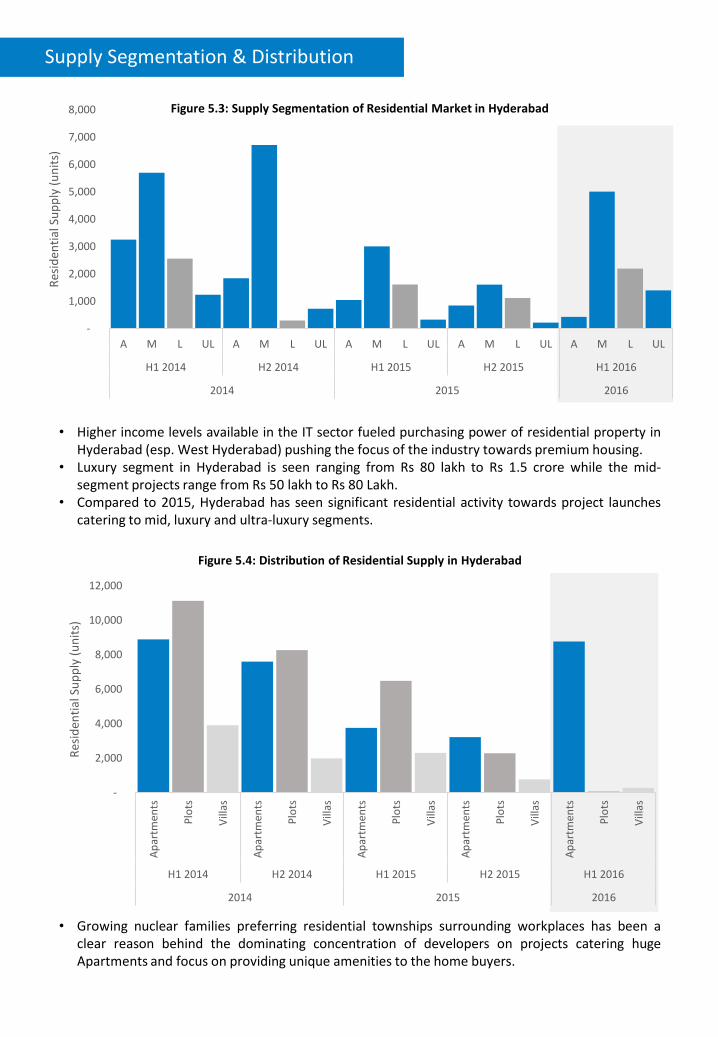

• Higher income levels available in the IT sector fueled purchasing power of residential property inHyderabad (esp. West Hyderabad) pushing the focus of the industry towards premium housing.

• Luxury segment in Hyderabad is seen ranging from Rs 80 lakh to Rs 1.5 crore while the mid-segment projects range from Rs 50 lakh to Rs 80 Lakh.

• Compared to 2015, Hyderabad has seen significant residential activity towards project launchescatering to mid, luxury and ultra-luxury segments.

-

2,000

4,000

6,000

8,000

10,000

12,000

Ap

artm

ents

Plo

ts

Vill

as

Ap

artm

ents

Plo

ts

Vill

as

Ap

artm

ents

Plo

ts

Vill

as

Ap

artm

ents

Plo

ts

Vill

as

Ap

artm

ents

Plo

ts

Vill

as

H1 2014 H2 2014 H1 2015 H2 2015 H1 2016

2014 2015 2016

Res

iden

tial

Su

pp

ly (

un

its)

• Growing nuclear families preferring residential townships surrounding workplaces has been aclear reason behind the dominating concentration of developers on projects catering hugeApartments and focus on providing unique amenities to the home buyers.

Figure 5.4: Distribution of Residential Supply in Hyderabad

Figure 5.3: Supply Segmentation of Residential Market in Hyderabad

Supply Segmentation & Distribution

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000C

entr

al

East

Ou

ter

No

rth

Sou

th

Wes

t

Cen

tral

East

No

rth

Sou

th

Wes

t

Cen

tral

East

Ou

ter

No

rth

Sou

th

Wes

t

No

rth

Wes

t

No

rth

Wes

t

H1 2014 H2 2014 H1 2015 H2 2015 H1 2016

2014 2015 2016

Res

iden

tial

Su

pp

ly (

un

its)

• Fig. 5.5 indicates a clear controlled launch pattern of residential supply in the western andnorthern markets of the city from the past three years.

• Promising returns and fast paced development due to infrastructure and regulatory provisions forenhancing employment centres in the West zone has brought more attention to these markets.

1

5

25

125

625

3,125

15,625

GachibowliMadinaguda

Narsingi

Kondapur

Hi Tech City

Pocharam

Bachupally

Beeramguda

Manikonda

NallagandlaTellapur

Kompally

Madhapur

Nanakramguda

Patancheru

Sanath Nagar

Jubilee Hills

Yapral

Gajularamaram

Nagole

*Measured on logarithmic scale

• Gachibowli clearly marks as the most sought out destination from the past 3-5 years spanning dueto a variety of positive reasons such as IT dominance, sound infrastructure and accessibility.

• Also the neighbouring IT dominant areas and peripheral residential markets have been in thespotlight from the beginning such as Madinaguda, Narsingi, Kondapur and Hi Tech City.

• Apart from the development of IT sector, active emphasis on city-scale infrastructure projects(such as Metro Project, ORR) have proven to bring good demand to the adjacent localities.

Figure 5.5: Distribution of Residential Supply in Hyderabad

Supply Distribution & Markets

Figure 5.6: Since 2014, Residential Developer Interest in Hyderabad (unit supply)

H1 2016

Residential Recap6.

North15%

West85%

Gachibowli39%

Narsingi22%

Hi Tech City15%

Nanakramguda8%

Jubilee Hills7%

Manikonda5%

Others4%

West HyderabadSanath Nagar

43%

Gajularamaram

33%

Yapral21%

Other3%

North Hyderabad

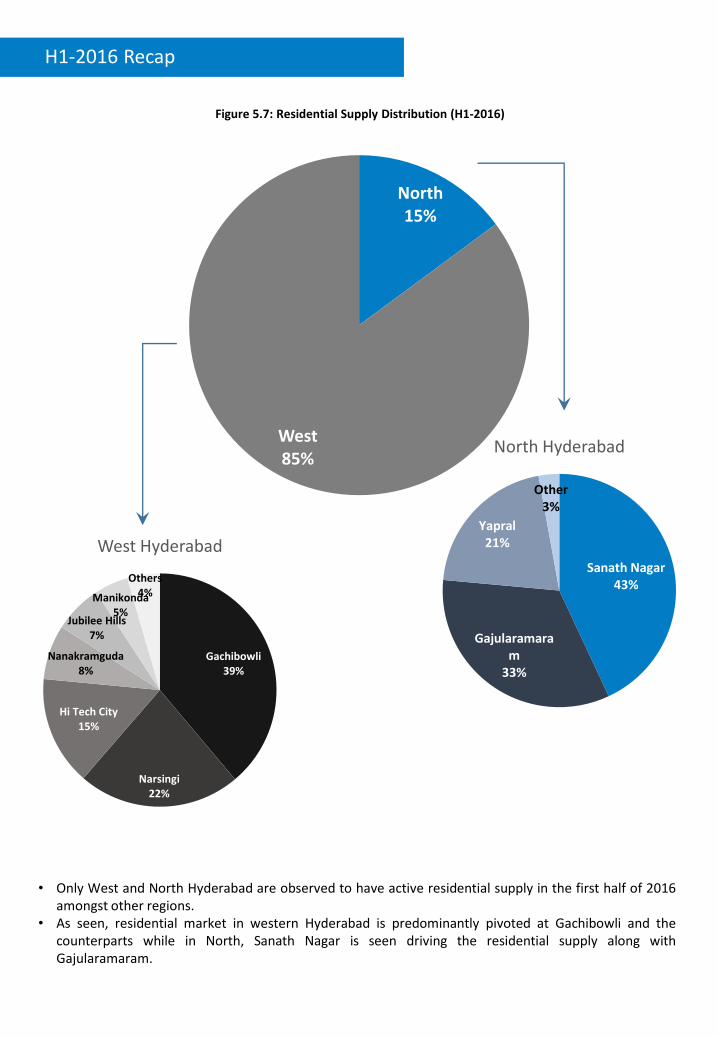

• Only West and North Hyderabad are observed to have active residential supply in the first half of 2016amongst other regions.

• As seen, residential market in western Hyderabad is predominantly pivoted at Gachibowli and thecounterparts while in North, Sanath Nagar is seen driving the residential supply along withGajularamaram.

H1-2016 Recap

Figure 5.7: Residential Supply Distribution (H1-2016)

29%

70%

1%

North Hyderabad

Affordable Mid Luxury Ultra Luxury

1%

53%28%

18%

West Hyderabad

Affordable Mid Luxury Ultra Luxury

• Data indicates that North Hyderabad has seen maximum launches in the affordable segment,followed by mid segment while West Hyderabad saw decent activity in luxury market as well.

• Hi Tech City, one of the established micro markets in West Hyderabad further had ultra-luxuryprojects while the remaining markets have projects in upper mid-segment and luxury segments.

• Jubilee Hills in West and Begumpet in North are the two veteran residential markets filled withluxury supply.

3%

100%

12%

94%

99%

77%

6%

1%

100%

8%

Jubilee Hills

Nanakramguda

Hi Tech City

Narsingi

Gachibowli

West Hyderabad

Affordable Mid Luxury Ultra Luxury

87%

81%

100%

19%

100%

100%

13%

Begumpet

Nizampet

Yapral

Gajularamaram

Sanath Nagar

North Hyderabad

Affordable Mid Luxury Ultra Luxury

• North Hyderabad, being a low dense residential region compared to West Hyderabad, witnessedsupply of new residential projects comprising villa units.

• Besides Jubilee Hills, all major residential areas in the West are tuned in to apartment culture.

100%

99%

100%

100%

100%

100%

1%

0% 20% 40% 60% 80% 100%

Manikonda

Jubilee Hills

Nanakramguda

Hi Tech City

Narsingi

Gachibowli

West Hyderabad

Apartments Plots Villas

Segmentation and Typology Distribution

100%

87%

100%

81%

100%

13%

19%

0% 20% 40% 60% 80% 100%

Begumpet

Nizampet

Yapral

Gajularamaram

Sanath Nagar

North Hyderabad

Apartments Plots Villas

DEEP DIVE

WEST HYDERABAD7.

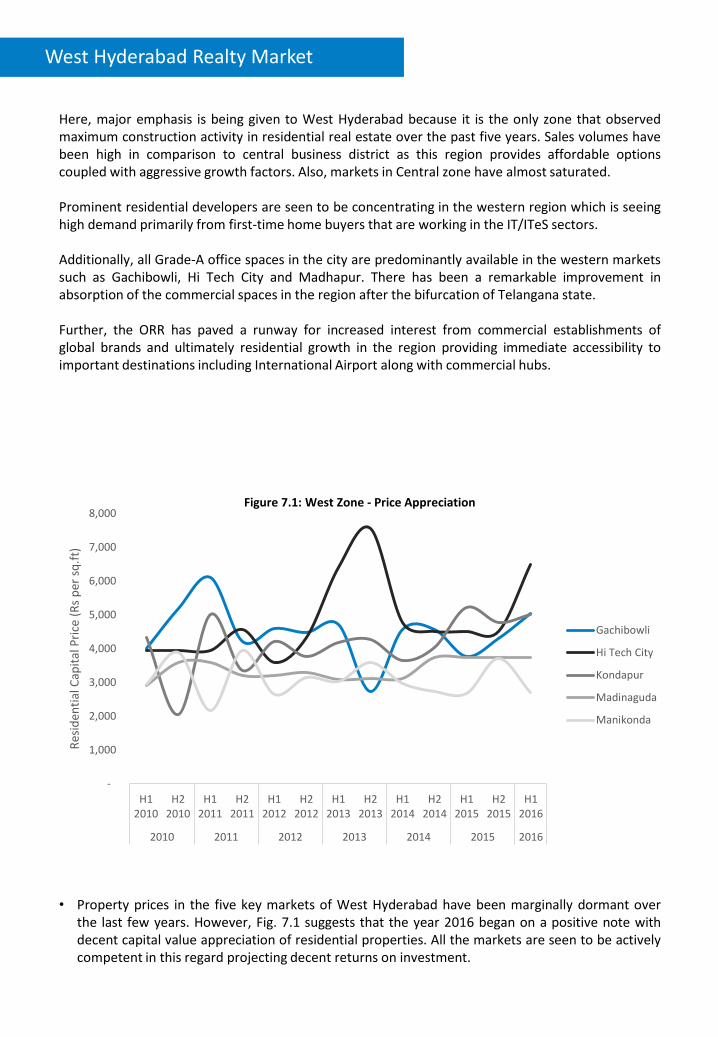

Here, major emphasis is being given to West Hyderabad because it is the only zone that observedmaximum construction activity in residential real estate over the past five years. Sales volumes havebeen high in comparison to central business district as this region provides affordable optionscoupled with aggressive growth factors. Also, markets in Central zone have almost saturated.

Prominent residential developers are seen to be concentrating in the western region which is seeinghigh demand primarily from first-time home buyers that are working in the IT/ITeS sectors.

Additionally, all Grade-A office spaces in the city are predominantly available in the western marketssuch as Gachibowli, Hi Tech City and Madhapur. There has been a remarkable improvement inabsorption of the commercial spaces in the region after the bifurcation of Telangana state.

Further, the ORR has paved a runway for increased interest from commercial establishments ofglobal brands and ultimately residential growth in the region providing immediate accessibility toimportant destinations including International Airport along with commercial hubs.

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

H12010

H22010

H12011

H22011

H12012

H22012

H12013

H22013

H12014

H22014

H12015

H22015

H12016

2010 2011 2012 2013 2014 2015 2016

Res

iden

tial

Cap

ital

Pri

ce (

Rs

per

sq

.ft)

Gachibowli

Hi Tech City

Kondapur

Madinaguda

Manikonda

• Property prices in the five key markets of West Hyderabad have been marginally dormant overthe last few years. However, Fig. 7.1 suggests that the year 2016 began on a positive note withdecent capital value appreciation of residential properties. All the markets are seen to be activelycompetent in this regard projecting decent returns on investment.

West Hyderabad Realty Market

Figure 7.1: West Zone - Price Appreciation

52%

17%

8%

7%

4%3%

2%2%

6%My Home Constructions Pvt Ltd

NCC Urban Infrastructure Limited

Sumadhura Infracon Pvt Ltd

Salarpuria Group

Hallmark Builders

Muppa Projects India Pvt Ltd

Alekhya Homes Pvt Ltd

Jayabheri Group

Other Builders

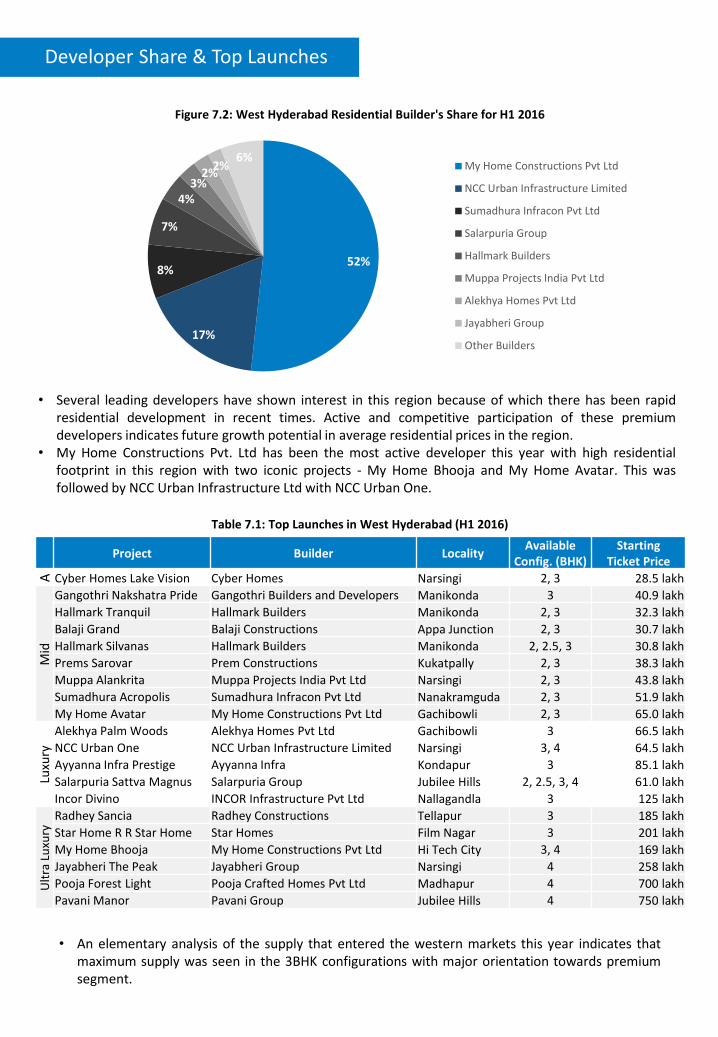

• Several leading developers have shown interest in this region because of which there has been rapidresidential development in recent times. Active and competitive participation of these premiumdevelopers indicates future growth potential in average residential prices in the region.

• My Home Constructions Pvt. Ltd has been the most active developer this year with high residentialfootprint in this region with two iconic projects - My Home Bhooja and My Home Avatar. This wasfollowed by NCC Urban Infrastructure Ltd with NCC Urban One.

Project Builder LocalityAvailable

Config. (BHK)Starting

Ticket Price

A Cyber Homes Lake Vision Cyber Homes Narsingi 2, 3 28.5 lakh

Mid

Gangothri Nakshatra Pride Gangothri Builders and Developers Manikonda 3 40.9 lakh

Hallmark Tranquil Hallmark Builders Manikonda 2, 3 32.3 lakh

Balaji Grand Balaji Constructions Appa Junction 2, 3 30.7 lakh

Hallmark Silvanas Hallmark Builders Manikonda 2, 2.5, 3 30.8 lakh

Prems Sarovar Prem Constructions Kukatpally 2, 3 38.3 lakh

Muppa Alankrita Muppa Projects India Pvt Ltd Narsingi 2, 3 43.8 lakh

Sumadhura Acropolis Sumadhura Infracon Pvt Ltd Nanakramguda 2, 3 51.9 lakh

My Home Avatar My Home Constructions Pvt Ltd Gachibowli 2, 3 65.0 lakh

Luxu

ry

Alekhya Palm Woods Alekhya Homes Pvt Ltd Gachibowli 3 66.5 lakh

NCC Urban One NCC Urban Infrastructure Limited Narsingi 3, 4 64.5 lakh

Ayyanna Infra Prestige Ayyanna Infra Kondapur 3 85.1 lakh

Salarpuria Sattva Magnus Salarpuria Group Jubilee Hills 2, 2.5, 3, 4 61.0 lakh

Incor Divino INCOR Infrastructure Pvt Ltd Nallagandla 3 125 lakh

Ult

ra L

uxu

ry

Radhey Sancia Radhey Constructions Tellapur 3 185 lakh

Star Home R R Star Home Star Homes Film Nagar 3 201 lakh

My Home Bhooja My Home Constructions Pvt Ltd Hi Tech City 3, 4 169 lakh

Jayabheri The Peak Jayabheri Group Narsingi 4 258 lakh

Pooja Forest Light Pooja Crafted Homes Pvt Ltd Madhapur 4 700 lakh

Pavani Manor Pavani Group Jubilee Hills 4 750 lakh

• An elementary analysis of the supply that entered the western markets this year indicates thatmaximum supply was seen in the 3BHK configurations with major orientation towards premiumsegment.

Developer Share & Top Launches

Figure 7.2: West Hyderabad Residential Builder's Share for H1 2016

Table 7.1: Top Launches in West Hyderabad (H1 2016)

4.2%

4.0%4.0%

3.9% 3.9%

4.2%

4.0%4.0%

3.9% 3.9% 3.9% 3.9%3.8% 3.8% 3.8%

3.9%

3.4%

3.1% 3.1%3.0%

3.4%3.2%

3.0% 3.0%

2.8%

East

Mar

red

pal

ly

Mo

osa

pet

Mal

lap

ur

Niz

amp

et R

oad

Mo

ti N

agar

Ko

ti

Am

eer

pet

Gan

dh

i Nag

ar

Him

ayat

h N

agar

Mas

ab T

ank

Ko

nd

apu

r

Pra

gath

i Nag

ar

Gac

hib

ow

li

Man

iko

nd

a

Hi T

ech

Cit

y

Pad

ma

Rao

Nag

ar

Gh

atke

sar

Hab

sigu

da

Up

pal

Ram

anth

apu

r

Sham

shab

ad

Saro

or

Nag

ar

Dils

ukh

nag

ar

Said

abad

Ch

and

raya

nag

utt

a

North Hyderabad Central Hyderabad West Hyderabad East Hyderabad South Hyderabad

• While Hyderabad residential market essentially saw significant number of options in the premiumsegment, data indicates that the Western markets amongst other counterparts will also offerreasonable returns (gross rental yield ranging from 3.8 per cent to 4 per cent). Add to this, thereare myriad property options by premium developers here and the growing importance of ITindustry will provide a good opportunity for residential investment and home-buying experience.

Average Rental Yield

Figure 7.3: Average Rental Yield available in Residential Market of Hyderabad

Outlook

Post the state bifurcation, realty sentiments in Hyderabad residential market seem to have improved. Further, with investment favored industrial policies and improved social infrastructure facilities, Hyderabad is again on the investor’s radar.

Telangana is among the fastest growing states in India by registering 9.2 per cent growth in 2015-16. The state economy is now fundamentally strong backed by a stable government while the IT/ITeS, manufacturing, Bio Technology and Tourism industries are also on a roll. The investor-favored policies initiated by the Government are likely to boost economic growth in the state and the capital city will also benefit from this. IT/ITeS will remain the primary growth driver which in turn will boost employment opportunities here leading to a rise in demand for residential, retail and hospitality sectors.

First Half of 2016 has witnessed quite a healthy residential supply, particularly in West and North Hyderabad. Moreover, consumer sentiments are gradually picking up pace here resulting in increase in new launches and marginal rise in capital values.

West Hyderabad remained the preferred destination for most realty players in their real estate portfolio expansion. Availability of Grade A office spaces in Hi Tech City and Gachibowli have made West Hyderabad one of the prominent and most sought-after zone. The current residential supply trend connotes future capital appreciation in and around micro markets of Hi Tech City and Gachibowli.

With current pace of infrastructure development, government policy, relatively affordable property prices and improving buyer sentiments, the realty market of Hyderabad is likely to gain more momentum in the second half of 2016.

ABOUT QuikrHomes

QuikrHomes is the leading Real Estate Marketing Solutions company in the Indian market. We have the largest

and most comprehensive list of detailed real estate sales and rental options covering all cities and budget

categories.

In the highly volatile and scattered Indian real estate market it is quite challenging to understand the dynamics

and make profitable investments. We help investors to take informed decision backed by real time data.

We capture real estate data across India and also update historical data of supply & absorption in top cities. To

ensure the most up-to-date and detailed data availability, our dedicated team/analysts monitor property activity

from a number of sources, including developers and property brokers, real estate forums and property listings,

as well as our own intensive research.

Our research services give clients the tools to review & analyze markets and realty insights that support

successful investment strategies. The solutions we provide always cater to our clients needs as we ensure that

all captured data and all customized reports undergo thorough due diligence by our in-house audit team.

Our Services :-

Land Potential Assessment Customized Reports Competitive Benchmarking Study Market Assessment Reports Feasibility Reports Quarterly demand Supply Analysis Report Projects Monitoring Services Tier 1 Cities Residential Projects Details with historical price & Absorption Trends.

Quikr India Pvt LtdNext to Manyata Tech Park,Back Gate No 5. Krishnarajapuram Hobli,Bangalore-560045

Copyright © 2007-16 QuikrHomes | CommonFloor. All rights reserved.The information provided herein is based on QuikrHomes & CommonFloor data which is collected from various publicly known sources viz,websites, documents and maps including QuikrHomes & CommonFloor's proprietary data model. Projects mentioned in the report areselected solely on basis of various parameters including number of units, price range and unique selling point, among others. Theselection, omission, or content of items does not imply any endorsement or other position taken by QuikrHomes & CommonFloor.The information is provided on an "as is" and "as available" basis. QuikrHomes & CommonFloor expressly disclaim warranties of any kind,whether express or implied, including, but not limited to, the implied warranties of merchantability, fitness for a particular purpose andnon-infringement.

Authors –

Rahul Panwar Yadunandan Batchu Priyanka Kapoor Asst. Manager | Research Sr. Research Associate | Research Senior Manager | Research & [email protected] [email protected] [email protected]

Abhai Mani ChaturvediSenior Manager | Research & Data Services [email protected]

For Residential Data Services: Please contact -Prashant Kumar ThakurHead of Research & Data Services [email protected]