received by msc 4/17/2018 2:02:22 pm...

TRANSCRIPT

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

STATE OF MICHIGAN

IN THE SUPREME COURT

SONG YU and SANG CHUNG,

Plaintiff-Appellees,

v

FARM BUREAU GENERAL INSURANCE COMPANY OF MICHIGAN, a Michigan Insurance company,

Defendant-Appellant.

Supreme Court No. 155811 Court of Appeals No. 331570 Ingham County Circuit No. 14-1421-CK

PLAINTIFF/APPELLEE SONG YU AND SANG CHUNGS' BRIEF ON APPEAL

ORAL ARGUMENT REQUESTED

Respectfully submitted,

Attorney for Plaintiff/ Appellees Song Yu and Sang Chung

John L. Noud (P18349) Noud & Noud, PLC 155 W . Maple St. P.O. Box 316 Mason, MI 48854 (517) 676-6010 Fax: (517) 676-6035

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

TABLE OF CONTENTS

INDEX OF AUTHORITIES ............................ ... ..... ....................................... ... ... ... ... ... ........ ....... . iii

COUNTER-STATEMENT OF QUESTIONS INVOLVED .................................................. ........ v

INTRODUCTION ................ .............. ........ ..... .. ...... ......................... .... ... .... .. .... ... ......................... . 1

The plain language of the insurance policy did not preclude coverage but rather provided coverage ...................... ..... .... ................................................................................... ............ 1

Circumstances under which the doctrine of equitable estoppel may be applied to require an insurer to expand coverage that is contrary to the express terms of an insurance contract. ............. ......... ............... ..... ...................... ..... ........... ......... ....................... ............ ... 5

Michigan Supreme Court opinions applying the doctrine of equitable estoppel sometimes seem to assume that a party, against whom the doctrine is to be applied, has access to "full knowledge" ofthe relevant facts and circumstances. However, most of those opinions do not specifically discuss "full knowledge." Application of the doctrine does, however, clearly require a showing of justifiable reliance on the part of the party seeking to apply it. ................... ......................... ........... ... ........................... .. ... ...... .. ...................... ... 6

The Defendant Insurer should be equitably estopped from denying coverage in this case. 6

COUNTER STATEMENT OF FACTS .. ................... ... ...................... ......... ..... .. ........... ................ 7

A. BACKGROUND FACTS ............................. ...... ................................... ......................... 7

B. DEFENDANT'S STATED REASONS, FOR DENIAL OF PLAINTIFFS' DECEMBER 2013 CLAIM AND RELEVANT DEPOSITION TESTIMONY OF DEFENDANT'S AGENTS IN THAT REGARD ..... ................ ..... .......... .............. ...... ........ 10

C. THE PARTIES' SUMMARY DISPOSITION MOTIONS; THE TRIAL COURT'S RULING; THE PLAINTIFFS' APPEAL; THE COURT OF APPEALS DECISION; AND DEFENDANT'S APPLICATION FOR LEAVE TO APPEAL ..... .... ............ ............ ......... 22

ARGUMENT .................. .................. .. ....... ....... .......... ............. ..... ............ ... .......................... ....... 23

I. THE PLAIN LANGUAGE OF THE INSURANCE POLICY (HOP) DID NOT PRECLUDE COVERAGE BUT RATHER PROVIDED COVERAGE .................................. 23

A. STANDARD OF REVIEW .............................. ...... ......... ........... ............ ..................... . 23

B. ON DECEMBER 25, 2013, PLAINTIFFS' SECOND HOME ON WEST LAKE WAS NOT "VACANT" AND PLAINTIFFS WERE "OCCUPYING" IT (AS THOSE WORDS ARE DEFINED UNDER THE HOP) .......................................... ................... ...... ....... ..... .... 23

C. INACCURATE FACTUAL ALLEGATIONS IN DEFENDANT'S BRIEF .... ...... .... 29

D. BECAUSE PLAINTIFFS' SECOND HOME WAS NOT "VACANT" AND NOT NOT "OCCUPIED" ON DECEMBER 25, 2013, THE PLAIN LANGUAGE OF THE INSURANCE POLICY (HOP) DID NOT PRECLUDE COVERAGE OF PLAINTIFFS'

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

WATER DAMAGE LOSS WHICH WAS INSURED AGAINST AS A "SPECIAL PERIL" BUT RATHER PROVIDED IT .......... ...... ...... .. ............................................................. ... .... 32

II. CIRCUMSTANCES UNDER WHICH THE DOCTRINE OF EQUITABLE ESTOPPEL MAY BE APPLIED TO REQUIRE AN INSURER TO EXPAND COVERAGE THAT IS CONTRARY TO THE EXPRESS TERMS OF AN INSURANCE CONTRACT ............ ....... 33

A. STANDARD OF REVIEW ...................... .. ..................................... .. ........................... 33

B. THE MICHIGAN LAW OF EQUITABLE ESTOPPEL ......................................... .... 33

C. INSTANCES IN MICHIGAN INSURANCE LAW WHERE A PARTICULAR PROVISION IN AN INSURANCE CONTRACT, WHICH NORMALLY WOULD OPERATE TO END AN INSURER'S LIABILITY, IS NOT RIGIDLY ENFORCED BECAUSE OF THE PRINCIPAL OF EQUITABLE ESTOPPEL. .......................... ........... 34

D. FORFEITURE OF A CONDITION VERSUS EXPANSION OF COVERAGE .. ...... 35

E. THE KIRSCHNER EXCEPTIONS ............. ...... .............................................. ............. 36

III. MICHIGAN SUPREME COURT OPINIONS APPLYING THE DOCTRINE OF EQUITABLE ESTOPPEL SOMETIMES SEEM TO ASSUME THAT A PARTY, AGAINST WHOM THE DOCTRINE IS TO BE APPLIED, HAS ACCESS TO "FULL KNOWLEDGE" OF THE RELEVANT FACTS AND CIRCUMSTANCES. HOWEVER, MOST OPINIONS DO NOT SPECIFICALLY DISCUSS "FULL KNOWLEDGE." APPLICATION OF THE DOCTRINE DOES, HOWEVER, CLEARLY REQUIRE A SHOWING OF JUSTIFIABLE RELIANCE ON THE PART OF THE PARTY SEEKING TO APPLY IT ..................... ......... 37

A. STANDARD OF REVIEW ....... .. ........................... ..... .. ..... ........ .......... ........................ 37

B. OF WHAT RELEVANT FACTS AND CIRCUMSTANCES WAS DEFENDANT IGNORANT AFTER DEFENDANT'S ADJUSTER LINDA RICKS COMPLETED HER INVESTIGATION OF PLAINTIFFS' FIRST WATER DAMAGE CLAIM IN FEBRUARY OF 2013? DID DEFENDANT HAVE ACCESS TO THOSE RELEVANT FACTS AND CIRCUMSTANCES FROM FEBRUARY 2013 UNTIL NOVEMBER 2013 WHEN DEFENDANT RENEWED PLAINTIFFS' HOP? AND DID PLAINTIFFS DELIBERATELY CONCEAL ANY RELEVANT FACTS AND CIRCUMSTANCES FROM DEFENDANT? ............. .... ........ .......... ....... ........... ......... ...... ..... ... ............. ....... ...... .. 37

C. DISCUSSION OF LEGAL AUTHORITY CITED BY DEFENDANT ...................... 41

IV. THE DEFENDANT-INSURER SHOULD BE EQUITABLY ESTOPPED FROM DENYING COVERAGE IN THIS CASE . ....................................... .. ............. ......................... 46

A. STANDARD OF REVIEW ............................ ...... .................. .. .. ..... .................... .. ....... 46

B. THE RELEVANT FACTS OF THIS CASE CALL FOR APPLICATION OF THE MICHIGAN DOCTRINE OF EQUITABLE ESTOPPEL .................... ...................... ... ...... 46

CONCLUSION AND REQUEST FOR RELIEF ......................................................................... 50

11

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

INDEX OF AUTHORITIES

Cases

Allstate Ins. Co. v. Snarski, 174 Mich. App. 148, 435 NW2d 408 (1988) ............ ................. 33, 35

BlackhawkDev Corp v Village ofDexter, 473 Mich 33,700 NW2d 364 (2005) ............ 33, 37, 46

Bonham v Northwestern Nat Ins Co, 230 Mich 349, 202 NW 995 (1925) ............... .. ................ .. 34

Cincinnati Ins Co v Citizens Ins Co, 454 Mich 263; 562 NW2d 648 (1997) ............... ... ..... ........ 42

Citizens Ins. Co. v. Pro-Steel Serv. Group, Inc. , 477 Mich. 75, 730 N.W.2d 682 (2007) ............ 23

Fleckenstein v. Citizens' Mut. Auto Ins. Co., 326 Mich. 591, 40 NW2d 733 (1950) ......... .. ..... ... 33

Friedbergvins. Co. ofNorthAmerica, 257 Mich. 291,241 N.W. 183 (1932) ... ........ .............. .. 43

Gardner v League Life Ins Co, 48 Mich App, 574,210 NW2d 897 (1973) ................................ . 34

Heniser v Frankenmuth Mut Ins Co, 449 Mich 155; 534 NW2d 502 (1995) ....................... . passim

Hetchler v Am Life Ins Co, 266 Mich 608,254 NW 221 (1934) ................. .... ......... ................ 5, 34

In re Bradley Estate, 494 Mich 367, 376; 835 NW2d 545 (2013) ..... ... .................. .. ..... ........ 23, 33

Industro Motive Corp v Morris Agency Inc, 76 Mich App 390, 256 NW2d 607 (1977) ............. 34

Keys v Pace, 358 Mich 74; 99 NW2d 547 (1959) .... .................................... .... ........ .......... ...... 6, 44

Kirschner v Process Design Assocs, Inc, Mich 587; 592 NW2d 707 (1999) ........... .. .. .... 34, 36, 37

Klapp v. United Ins. Group Agency, Inc. , 468 Mich. 459,663 N.W.2d 447 (2003) .................... 23

Kole v Lampen, 191 Mich 156; NW 392,393 .......... ............. ....................... .......... ................ ........ . 5

Lichon v American Universal Ins Co, 435 Mich 408, 415; 459 NW2d 288 (1990) ...... .. . 44, 45, 46

Mate v Wolverine Mut Ins Co, 233 Mich App 14, 22; 592 NW2d 3 79 (1998) ......... .......... ....... .. 45

McGrath v Allstate Ins Co, 290 Mich App 434, 439, 802 NW2d 619, 623 (201 0) ............... passim

Michigan Tp Part Plan v Federal Ins Co, 233 Mich App 422, 592 NW2d 760 (1999) ............... 35

Morales v Auto-Owners Ins Co, 458 Mich 288; 582 MW2d 776 (1998) ........... ............. ... 6, 33, 45

1ll

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

Morley v Automobile Club of Michigan, 458 Mich 459, 581 NW2d 237 (1998) ......................... 37

Parmet Homes Inc v Republic Ins Co, 111 Mich App, 140,314 NW2d 453 (1981) ............. 35,45

Pastucha v Roth, 290 Mich 1, 287 NW 355 (1939) ........... .................................................... . 33, 34

Raska v. Farm Bureau Mut. Ins. Co. a,( Mich., 412 Mich. 355,314 N.W.2d 440 (1982) ........ .... 24

Rory v Continental Ins Co, 473 Mich 457; 703 NW2d 23 (2005) ................................................ 23

Ruddock v Detroit L(fe Ins Co, 209 Mich 638; 177 NW2d 242 (1920) .................................. 41, 42

Staffan v. Cigarmakers' Int'l Union of America, 204 Mich. 1, 169 NW 876 (1918) ........... ......... 33

Vushaj v. Farm Bureau., 284 Mich.App. 513, 773 N.W.2d 758 (2009) .......... ............................ 24

lV

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

COUNTER-STATEMENT OF QUESTIONS INVOLVED

In its December 20, 2017 order granting leave to appeal, this Court directed the parties to address

the following issues:

I. WHETHER THE PLAIN LANGUAGE OF THE INSURANCE POLICY PRECLUDED COVERAGE?

Defendant/ Appellant says: Yes. Plaintiffs/Appellees say: No. The Trial Court said: Yes. Court of Appeals said: Majority did not answer. Dissent said yes.

II. IF SO, WHETHER AND UNDER WHAT CIRCUMSTANCES THE DOCTRINE OF EQUITABLE ESTOPPEL MAY BE APPLIED TO REQUIRE AN INSURER TO EXPAND COVERAGE THAT IS CONTRARY TO THE EXPRESS TERMS OF AN INSURANCE CONTRACT?

Defendant/ Appellant says: Only in situations pertaining to liability coverage when an insurer defends without issuing a reservation of rights letter or filing a declaratory action that there is no coverage, but an insurer may later raise additional grounds for non-coverage if there is no unreasonable delay and no demonstrable prejudice to the insured.

Plaintiff/Appellees say: An insurer may be estopped from enforcing a provision in an insurance contact, which arguably could be relied upon to deny coverage, when the insurer negligently, by its acts, representations, admissions or by its silence, when it ought to speak out, induces an insured to believe that she has coverage, when the insured rightfully relies on and acts on that belief, and when the insured will be prejudiced if the insurer is permitted to deny coverage based upon the provision.

The Trial Court said: did not address Court of Appeals said: did not address.

III. WHETHER AN EQUITABLE ESTOPPEL CLAIM REQUIRES THAT (A) A PARTY AGAINST WHOM THE DOCTRINE OF EQUITABLE ESTOPPEL IS TO BE APPLIED HAS FULL KNOWLEDGE OF THE FACTS AND CIRCUMSTANCES INVOLVED, AND (B) JUSTIFIABLE RELIANCE ON THE PART OF THE PARTY SEEKING TO INVOKE IT IS SHOWN?

Defendant/ Appellant says: Yes. Plaintiffs/Appellees say: No as to full knowledge. Yes as to justifiable reliance. The Trial Court said: Did not address. Court of Appeals said: Majority said no. Dissent did not address.

IV. WHETHER THE DEFENDANT-INSURER SHOULD BE EQUITABLY ESTOPPED FROM DENYING COVERAGE IN THIS CASE?

v

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

Defendant/ Appellant says: No. Plaintiffs/ Appellees say: Yes. The Trial Court said: No. Court of Appeals said: Majority said yes. Dissent said no.

Vl

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

INTRODUCTION

The plain language of the insurance policy did not preclude coverage but rather provided coverage.

The "Declarations"1 portion of the subject "Homeowners Polici' ("HOP") evidences the

fact that Plaintiffs' "Residence Premises" at 1724 Forest Drive, Portage, Michigan, with frontage

on West Lake, was insured for the period from 12/08/2013 to 12/08/2014. In the "Residence

Premises" section (on page 1) ofthe Declarations is the following entry:

Perils Insured Against: Dwelling: SPECIAL PERILS

Those "Special Perils" are described in the four-page (policy) endorsement (GH-63-02-1 0-

1 0) at Exhibit E, Appendix 168A - 171A. At page 20 of the transcript of the deposition of

Defendant's agent Dan Gregart, Mr. Gregart explained "Special Perils" insurance coverage (see

Plaintiffs' Exhibit 2, Appendix 38b ). He testified that such coverage does not list the perils that

are insured against. "Instead [quoting Mr. Gregart] it only names the perils that are not covered

and everything else is."

The "Special Perils" insuring language in the HOP is set out at the top of Appendix 168A

and it states:

SECTION I- PERILS INSURED AGAINST

COVERAGE A - DWELLING and COVERAGE B - OTHER STRUCTURES

We insure against risk of direct loss to property described in Coverages A and B (if such coverages appear in the Declarations of this policy under Section I) only if that loss is a physical loss to property. We do not insure, however, for loss: ...

1 The two pages of "Declarations" (form GH-60-0 1-1 0-12) are at Appendix 144A and 145A.

1

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

(Losses not insured against are listed)

Defendant has not asserted that the loss in this case was for a peril (i.e. water damage) that

was not insured against. However, Defendant has asserted that Plaintiffs' loss was not covered

because Plaintiffs did not reside in their West Lake home on December 25, 2013, and because of

the "Increase in Hazard" resulting from Plaintiffs' lack of residence. The insuring "Agreement"

portion ofthe 19-page "Homeowners Policy" (HOP) stated (see Exhibit E, Appendix 148A):

AGREEMENT

This policy, together with the Declarations, Perils Form, Loss Evaluation Form, and endorsements (if any), make up your policy. We will provide the insurance described in this policy, subject to all its provisions, in return for your payment of the premium and your compliance with all applicable provisions of this policy.

At pages 2 and 3 (of 19) of the HOP (Appendix 147A and 148A) are "DEFINITIONS" of

words and phrases used in the HOP. Relevant "Definitions" include:

14. "Occupied" means being lived in with regular and continuous legal presence ofhuman inhabitants . . . (emphasis added)

20. "Residence premises" means: a. The one family dwelling, other structures,2 and grounds;

where you reside and which is shown in the Declarations ofthis policy.

24. "Vacant" and "vacancy" mean the absence of furnishings, utilities, and the amenities minimally necessary for human habitation ...

At pages 3 and 4 (of 19) of the HOP, "POLICY CONDITIONS" (Appendix 148A and

149A) are listed. The "Condition" at issue in this case reads:

2 "Residence Premises" included the garage (i .e. "Other Structure") in which many of Plaintiffs' lake home furnishings were placed so that the home would "show better" when it was listed for sale, in June 2013, after it had been extensively remodeled during the period from February to June of2013.

2

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

14. increase in Hazard.

Unless otherwise provided in writing, we will not be liable for loss occurring:

b. while a described building, whether intended for occupancy by owner or tenant, is vacant beyond a period of 60 consecutive days or is unoccupied beyond a period of six consecutive months. However, if "Location (Seasonal)" appears in the Declarations of this policy, we will not be liable for loss occurring while a described building is unoccupied beyond a period of 12 consecutive months. (emphasis added)

At page 5 (of 19) of the HOP (Appendix 150A), coverage of "other structures," 1s

discussed. Relevant portions read:

COVERAGEB-OTHERSTRUCTURES

We cover other structures on the residence premises that are not attached to the dwelling. Structures attached to the dwelling by only a fence, utility line, or decorative connection are considered to be other structures.

Plaintiff Song Yu•s November 11 , 2015 affidavit (Defendanfs Exhibit F) and his May 14,

2014 Examination Under Oath testimony (Defendanfs Exhibit G) establish that:

1. The "Residence premises" was not 11Vacant•• (as vacant is defined in the HOP) for

a period beyond 60 consecutive days prior to the water damage loss on December 25,

2. The "Residence premises" was not not 110ccupied•• (as occupied is defined in the

HOP) 4 during a period beyond six consecutive months prior to the water damage loss on

December 25, 2013; and

3 Sec Song Yu's 5/14/2014 EUO testimony (Exhibit A, Appendix 64A-65A) that many of the "Residence premises" furnishings had been placed in the garage ("other structure") at the suggestion of the listing realtor so the remodeled house would "show better." 4 Plaintiffs' lake home was not "lived in with regular and continuous physical presence" during that six-month period, but it was lived in with regular and continuous "legal presence" during that six-month period. (e.g. Plaintiffs had not sold the Residence premises on land contract as had the insured in Heniser, infra.

3

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

3. Plaintiffs intended to reside in (i.e. "occupy") the "residence premises" as their

second home on December 25,2013.

During 2013 Plaintiffs "lived in" (i.e. "resided" in; i.e. "occupied") both their primary home

in East Lansing and their second home on West Lake, just as did the other 1 00 insureds who

insured their second homes with Defendant's agent Dan Gregart. 5

When an insured insures a "residence premises" (either a primary home or a second home)

with Defendant and that home is not "vacant beyond a period of 60 consecutive days" or is not

"unoccupied beyond a period of six consecutive months" then, when one reads Defendant's

standard HOP "as a whole," it is logical to conclude from the unambiguous (or ambiguous) policy

language that the insured is residing in that "residence premises."

In this regard, why did Defendant include the definitions of "vacant" and "occupied" in its

standard HOP if Defendant did not consider its insureds (who insured second homes with

Defendant) to be residing in those second homes as long as the second homes were not "vacant

beyond a period of 60 consecutive days or . . . unoccupied beyond a period of six consecutive

months?"

In addition:

1. Why did Defendant's employee Linda Ricks in a December 27, 2013 email to a fellow

employee (see Plaintiffs' Exhibit 3, Appendix 53b), state: "I'm sure he is going to say that [sic]

stay there on weekends"; and

5 See pages 59-63 of Dan Gregart's 5/28/2015 deposition transcript at Plaintiffs' Exhibit 2, Appendix 48b-49b.

4

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

2. Why does the policy definition of occupied state that occupied "means being lived in with

regular and continuous legal presence of human inhabitants . . . " (rather than regular and

continuous physical presence?

Circumstances under which the doctrine of equitable estoppel may be applied to require an insurer to expand coverage that is contrary to the express terms of an insurance contract.

Under the express terms of the HOP, the risk of water damage was a "special peril" which

was insured against; and, on December 25,2013, Plaintiffs' West Lake home was not "vacant" or

not not "occupied" as those words are defined in the HOP. Because the water damage loss was a

covered "special peril," under the express terms of the HOP, there should be no need, in this case,

to address circumstances under which equitable estoppel may be applied to require an insurer to

"expand coverage" that is contrary to the express terms of an insurance contract.

However, assuming arguendo that Plaintiffs' West Lake home (the "residence premises")

was "vacant" and/or not "occupied" on December 25, 2013 (as those words are defined in the

HOP), then under what circumstances may the doctrine of equitable estoppel be applied to require

an insurer to expand coverage that is contrary to the express terms of an insurance contract?

An often quoted statement of estoppel law from Hetchler v Am Life Ins Co, infra, is:

It is a familiar rule of law that an estoppel arises when one by his acts, representations, or admissions, or by his silence when he ought to speak out, intentionally or through culpable negligence induces another to believe certain facts to exist and such other rightfully relies and acts on such belief, so that he will be prejudiced if the former is permitted to deny the existence of such facts. Kole v Lampen, 191 Mich 156; NW 392,393 (emphasis added)

With respect to the Hetchler standard for applying equitable estoppel, it is apparent from

the relevant facts in this case: (1) that defendant Farm Bureau's acts induced plaintiffs to believe

that their HOP was in effect in December of2013, (2) that plaintiffs rightly relied on this belief,

5

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

and (3) that plaintiffs will be prejudiced if Defendant is not estopped from denying Plaintiffs'

December 25,2013 water damage claim.

Michigan Supreme Court opinions applying the doctrine of equitable estoppel sometimes seem to assume that a party, against whom the doctrine is to be applied, has access to "full knowledge" of the relevant facts and circumstances. However, most of those opinions do not specifically discuss "full knowledge." Application of the doctrine does, however, clearly require a showing of justifiable reliance on the part of the party seeking to apply it.

Michigan law sometimes seems to assume that a party, against whom the doctrine of

equitable estoppel is to be applied, has access to "full knowledge" of relevant facts and

circumstances. However, a party, who has such access, may not negligently ignore (or fail to take

into account) those relevant facts and circumstances. If it does, the doctrine (unlike the doctrine

of"waiver") can be applied in spite of the party's claimed ignorance. See Keys v Pace, infra.

A party seeking to invoke the doctrine of equitable estoppel is clearly required to show

justifiable reliance upon the conduct of the party against whom the doctrine is to be invoked. Such

justifiable reliance has frequently been found by Michigan Courts under varied circumstances,

including the circumstances in Morales v Auto Owners, infra.

The Defendant Insurer should be equitably estopped from denying coverage in this case.

Defendant had access, at the time it investigated and paid Plaintiffs' first water damage

claim, in February of2013, to the following facts:

1. That Plaintiffs had moved their primary home to the Lansing area or (at the very least) were

in the process of (then) moving it; and

2. That Plaintiffs were, in February 2013, "occupying" (as occupying is defined in the HOP)

their West Lake home (i.e. the "residence premises") as their second home.

6

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

In light of these facts, Defendant should be equitably estopped from denying Plaintiffs'

December 2013 claim for water damage (a covered "Special Peril" under the HOP) to Plaintiffs'

West Lake home:

1. Because, between February and November 2013, Defendant neglected to determine (find out)

that, in fact, Plaintiffs had moved their primary home to the Lansing area in 201 0;

2. Because, in November of 2013, Defendant renewed Plaintiffs' HOP, for another year (from

December 8, 2013 to December 8, 2014); and

3. Because Defendant mistakenly concluded that, on December 25, 2013, Plaintiffs' West Lake

home (their second home) was "vacant" and/or not "occupied," as those terms are defined in

the HOP.

COUNTER STATEMENT OF FACTS

A. BACKGROUND FACTS

On December 8, 2006, Plaintiff/Appellees, Dr. Song Yu and his wife Sang Chung

(hereafter Plaintiffs) purchased real property (the "residence premises"6) including a home

("'dwelling"7) and garage ("other structure"8) with frontage on West Lake and with the address of

1724 Forest Drive, Portage, Michigan (a copy of the Deed of Purchase is Exhibit A to Song Yu's

November 11 , 2015 Affidavit9 at Appendix 174A- 177 A).

Song Yu's Affidavit also evidences the following additional facts:

1. At the time of purchase (see paragraph 3 of the Affidavit), Plaintiffs began to insure the

6 As defined in the "Homeowners Policy" between the parties. 7 As used in the policy definition of"residence premises." 8 As used in the policy definition of"residence premises." 9 Attached at Plaintiffs' Exhibit I is a copy of Dr. Yu's November II , 2015 Affidavit (plus exhibits to the Affidavit). This Affidavit was also attached (as Exhibit 5) to Plaintiffs' Brief in Support of their November II, 2015 Motion for Summary Disposition and as Exhibit I to Plaintiffs' answer to Defendant's Application for Leave to Appeal.

7

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

"residence premises" under a "Homeowners Policy" (HOP) issued by Defendant-Appellant,

Farm Bureau General Insurance Company of Michigan (hereinafter Defendant). A copy of the

HOP is at Appendix 143A - 172A.

2. At the time Plaintiffs purchased their West Lake home, Song Yu was working as a family

practice physician at Bronson Hospital in Kalamazoo. Plaintiffs lived in the home as their

primary residence from December of2006 until June of2010 (see paragraphs 2 and 3).

3. In June of 2010 Song Yu accepted employment with Sparrow Hospital in Lansing, and

Plaintiffs moved their primary residence to an apartment in Okemos. In early 2013, after living

in the apartment for approximately 2-1 /2 years, Plaintiffs began shopping for a new home in

the East Lansing area; and on March 29, 2013, they closed the purchase of the home at 1866

Cricket Lane in East Lansing (see paragraphs 4, 5 and 6 and also Exhibit B to Song Yu's

Affidavit).

4. After moving their primary residence from Portage to the Lansing area in 2010, Plaintiffs

continued to live in their home on West Lake as their second home, and they continued to keep

"furnishings" in their home and garage; continued to keep the "utilities" on; and continued to

maintain the "amenities minimally necessary for human inhabitation" (see paragraphs 5 and 7

of Song Yu's Affidavit and also see the definition of"vacant" in the parties' HOP).

5. In early 2013 Plaintiffs decided to offer their West Lake home for sale. On February 7, 2013,

Dr. Yu met realtor Scott Lakey at Plaintiffs' West Lake home for the purpose of listing it for

sale, and, at that time, he discovered a relatively small amount of water damage which was

caused by a leak in the home's plumbing system. Dr. Yu reported the water damage to

Defendant, and Defendant investigated and paid Plaintiffs' claim for that February 2013 water

damage. (see paragraphs 8 - 11)

8

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

6. Approximately nine months later (on November 4, 2013), Defendant renewed Plaintiffs'

Homeowners Policy (HOP) for the period from December 8, 2013 to December 8, 2014 (see

paragraph 12 and also Exhibit D to Song Yu's Affidavit). The renewed policy continued to

insure Plaintiffs' "residence premises" (as defined in the HOP) including Plaintiffs' home

("dwelling") and garage ("other structure") from loss due to "special perils."10 The "special

perils" insurance language is at page 1 (of 4 pages) of policy endorsement GH-63-02-10-IOC

(at Appendix 167 A) and it states:

SECTION I - PERILS INSURED AGAINST COVERAGE A - DWELLING and COVERAGE B-OTHER STRUCTURES We insure against risk of direct loss to property described in Coverages A and B (if such coverages appear in the Declarations of this policy under Section I) only if that loss is a physical loss to property. We do not insure, however, for loss:

7. Thereafter, on December 25, 2013, water again escaped from the plumbing system in

Plaintiffs' West Lake home and damaged it. Plaintiffs were in East Lansing at the time, and,

when a neighbor notified Dr. Yu (by phone) that icicles were forming on the outside of the

home, Dr. Yu immediately drove to Portage and observed that water had caused extensive

damage to the home. Dr. Yu immediately notified Defendant of the damage (paragraph 13).

8. While Defendant was investigating Plaintiffs' second water damage claim, Plaintiffs' attorney

received a letter from Defendant, dated February 3, 2014 (copy at Exhibit G to the Yu

Affidavit) requesting a "Sworn Statement and Proof of Amount of Loss." And, on April 3,

2014 Plaintiffs' attorney delivered to Defendant, via facsimile, a $80,636.67 "Sworn Statement

10 On page 20 of the deposition transcript of Farm Bureau Agent Dan Gregard (see Plaintiffs' Exhibit 2, Appendix 38b) is the following question and answer: Q. And what's the number of perils covered under the special perils policy? A. Well, it's is not- that's the-- reason you chose special perils, special peri ls does not name the perils that are covered. Instead it only names the perils that are not covered and everything else is.

9

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

and Proof of Amount of Loss," (see paragraphs 17 and 18 and also Exhibit H to the Yu

Affidavit).

9. Thereafter, by certified letter dated June 20, 2014, (copy at Exhibit I to the Yu Affidavit),

Defendant notified Plaintiffs that it was denying Plaintiffs second water damage claim

(paragraph 19).

As a result of the denial of their claim, Plaintiffs filed a complaint against Defendant, on

December 18, 2014, in the Ingham County Circuit Court. In Count I of their two-count complaint,

Plaintiffs requested a declaratory judgment to determine liability under the terms of the subject

Homeowners Policy; and in Count II, Plaintiffs alleged that Defendant had breached its insurance

contract with Plaintiffs.

B. DEFENDANT'S STATED REASONS, FOR DENIAL OF PLAINTIFFS' DECEMBER 2013 CLAIM AND RELEVANT DEPOSITION TESTIMONY OF

DEFENDANT'S AGENTS IN THAT REGARD

Defendant's June 20, 2014letter (Defendant's Exhibit M, Appendix 314) notified Plaintiffs

that Defendant was denying Plaintiffs' second water damage claim because:

I. Your claim for the loss of the dwelling or any loss of use of the dwelling is barred because you did not reside in the dwelling at the time of the loss and therefore it was not a "residence premises" as required and defined by the policy of insurance.

2 . Your claims are also barred due to the increase in hazard at the subject property by means within your knowledge including, but not limited to, the vacancy of the subject home beyond a period of 60 consecutive days and the increases in hazards associated with that condition.

3. Your claims are also barred due to the increase in hazard at the subject property by means within your knowledge including, but not limited to, the fact that the subject home was unoccupied beyond a period of 6 consecutive months and the increases in hazards associated with that condition.

10

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

These reasons, for denial, raise the question of how others who own both a primary

dwelling (home) and a second dwelling (home) insure their second home against water damage of

the kind that occurred in this case. This issue was discussed by Defendant's insurance agent, Dan

Gregart, who serviced Defendant's Homeowners Insurance Policy with the Plaintiffs. Plaintiffs '

counsel took Mr. Gregart's deposition on May 28, 2015. On pages 60 - 63 of the deposition

transcript (Plaintiffs' Exhibit 2, Appendix 48b-49b) are a series of questions to and answers by Mr.

Gregart concerning homeowners insurance policies through which Defendant insures so called

"seasonal" homes as contrasted with "primary" homes. That exchange is:

11 Q I'll rephrase it. Let's assume that Song 12 Yu called you on February 21st, 2013, and said I 13 have moved to Lansing. I'm living in Lansing but 14 I am still visiting my home on West Lake. Is 15 there anything that I need to do to update my 16 insurance policy coverage; what would you have 17 told him? 18 MR. WILLISON: Objection to the 19 form. 20 THE WITNESS: It really depends. I 21 would have had to have the conversation. I would 22 have asked him what the usage of the house would 23 have been. 24 BY MR. NOUD: 25 Q And let's assume that he told you that he

1 2 3 4 5 6 7 8 9 10 11 12

A

Q

A

61 was spending his-- some ofhis off work time down at the home? It would have been I would have informed him about the -- I believe we had to make a change to change to a seasonal home, which is a simple change from an owner occupied to a seasonal -- I'm sorry, primary to seasonal home. And how would you have physically accomplished that change to a, quote, seasonal, end quote, home? Through a change form, Farm Bureau company change form.

11

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Q

Q

A Q A Q

A Q

A

62 Well, what's your understanding of the meaning of the word seasonal? It would be a secondary home that is not the primary home-- the primary owner occupied home of the insured. And do you write many -- or do you sell many homeowners insurance policies for seasonal homes? Yes. Approximately how many? 100. Back to the fact that you testified to earlier about just wanting to follow standard procedures, those weren't your exact words, they're as close as I can come, and that was the reason why you asked Monica Dixon 11 to notify Ms. Creighton 12 to cancel this policy. Urn-hum. Since you had written 100 policies for other insured customers on seasonal homes, why didn't you call up Song and ask him whether or not he wanted a seasonal policy on his home rather than just canceling? Well, because the home appeared vacant,

63 1 in which case it would be ineligible for a 2 seasonal home policy. 3 Q So you made the assumption that the home 4 was vacant and that's why you ordered the policy 5 to be canceled rather than calling up Song Yu and 6 asking him whether or not it was vacant; is that 7 correct? 8 MR. WILLISON : Objection to the form 9 of the question, the use of assumption. 10 THE WITNESS: I used what 11 infonnation I had at my disposal --12 BY MR. NOUD: 13 Q Well, how did --14 A -- and informed the underwriter of what I 15 found.

11 Monica Dixon is Mr. Gregart's office manager. 12 Ms. Creighton is an underwriter for Defendant.

12

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

16 17 18 19 20 21 22

Q

A Q A

Well, it wouldn't have been very hard to call Song on the phone and confirm whether or not your observation was correct, would it? I wanted to go through official channels. But why didn't you want to call Song? Because I wanted to go through official channels.

On pages 53- 56, (Plaintiffs' Exhibit 2, Appendix 46b-47b) Plaintiffs' counsel questioned

Mr. Gregart concerning why he decided to cancel Plaintiffs ' insurance policy rather than making

a "simple change" (Mr. Gregart' s term) to Plaintiffs ' homeowners policy to designate Plaintiffs'

lake home as a "seasonal" home rather than a "primary home." That exchange is:

18 19 20 21 22 23 24 25

1 2 3

Q

A Q A Q

A Q A

Did you go over and view the home on or about 12-11 of'13, the home on Forest Drive, I should say? Yes, I did. And did you take a picture of it? I took a picture of the for sale sign. And did you direct Monica to forward the picture and a request cancellation to KCreighton?

54 Yes. And who is KCreighton? My homeowners underwriter.

10 Q If you wanted to cancel one of your 11 customer's insurance policies would you contact 12 KCreighton? 13 MR. WILLISON: Objection, 14 foundation.

18 19 20 21 22 23 24 25

Q

A Q

A

Q

Well, why did you tell Monica to contact KCreighton under the circumstances of this case? Because I observed the home to be vacant. And why was KCreighton the person to call if the home was vacant? She is my homeowners underwriter assigned to my region of the state. Well , when you saw the for sale sign and

55

13

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

1 2 3 4 5 6 7 8 9 10 11

A Q A

Q A Q A Q A

Q

A Q A

Q

A Q A

Q

A

took a picture of it, did you think about calling up Song Yu and asking him about coverage which Farm Bureau or you might have available for a lake home which was being put on the market? No. Why not?

That option was a non Farm Bureau product, so my priority at that time was making sure that if the home was, in fact, vacant that we got it off the books. Did you go inside the home? I looked through windows. And what did you see? An empty house. Okay. didn't look -- an empty house. Yeah. Did it ever go through your mind that maybe this was a home since it was on the lake that Song Yu might be using periodically? That wasn't something I considered. Why not? It had the appearance ofbeing vacant, and so I wanted to make sure that we went through the channels to proceed with cancellation because it increased risk.

56 You didn't feel any sense of responsibility to Song Yu to call him up and talk to him about what you were going to do? No. Why not? I wanted to go through our official channels. And what did you understand would happen ifyou went through official channels? A letter of cancellation would be sent to the insured notifying them.

Though Mr. Gregart testified (see above) that Plaintiffs' West Lake home was "vacant" on

December 11 , 2013, Plaintiffs have presented evidence that it was not vacant as "vacant"13 is

l3 Vacant is defined in the subject Homeowners Policy as:" 'Vacant' and ' vacancy' mean the absence of furnishings, utilities, and the amenities minimally necessary for human habitation ... "

14

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

defined in the subject homeowners policy. That evidence includes paragraph 5 of Song Yu's

November 11 , 2015 Affidavit (Plaintiffs' Exhibit 1) and Song Yu's May 14, 2014 EUO testimony

(Defendant's Exhibit D). At pages 29 - 33 (Appendix pp 63A - 68A) Song Yu testified that when

he and Mrs. Yu moved to a 600 square foot apartment in Okemos in 2010, they left most of their

furniture in their West Lake home. And that when they prepared their home for sale in 2013 , they

moved most of the furniture from their West Lake home to the garage serving that home because

their realtor believed that the home would show better if the older furniture was removed from the

newly remodeled home. At page 23 (Appendix 57 A) and at pages 60 - 62 (Appendix pp 94A-

96A) of the transcript of the EUO, Song Yu discusses the remodeling of the lake home between

February 7, 2013 (the day that Song Yu and realtor Lakey discovered the February water damage)

and the time (during the summer of2013) that realtor Lakey listed the lake home. At lines 21 and

22 on page 61 (Appendix 95A) of Song Yu's EUO is the following statement:

"And it took me about 3 or 4 months to fix everything, and then so we listed it in June or July."

At lines 6 through 22 on page 23 (Appendix 57 A) of the EUO, Song Yu explains, that the

remodeling included a new hardwood floor throughout the first (main) floor; new carpeting in all

the rooms on the upper (second) floor; and repainting of the entire interior of the home.

On May 21,2015, Plaintiffs' counsel took the deposition of Linda Ricks, the Farm Bureau

adjuster who investigated both Plaintiffs' first (February 7, 2013) water damage claim and

Plaintiffs' second (December 25, 2013) water damage claim. With respect to Ms. Ricks'

investigation of the February 2013 water damage claim, the following exchange took place (see

pages 14- 19 ofthe transcript ofMs. Ricks' deposition at Appendix pp 240A-245A Exhibit H):

15

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

13 14 15 16

Q

A

And when you called and spoke with Song Yu on February 8th of2013, what discussion did you have with him? I don't remember the actual conversation but from

17 my notes, reading the summary of the conversation, it 18 was asking him what had happened, what they had found, 19 and that he said they had already called Servepro and so 20 they were in doing some demoing to dry out the 21 structure. And that he told me that he was in Lansing, 22 that they were moving and he was going back and forth on 23 the weekends and they were doing some repairs to prepare 24 it to go on the market.

10 Q Now, is it your testimony that Song Yu told you 11 that he was living in Lansing at the time? 12 A That he was-- he was in Lansing at the time that 13 I was talking to him and he just said that he had moved. 14 I wasn't certain that it was Lansing that he moved to. 15 Q If he was living in Lansing in February of 2013, 16 would that fact have had any bearing on whether this 17 water damage to the home at 1724 Forest in Portage was 18 covered by his homeowner's insurance policy with Farm 19 Bureau? 20 A Well, he told --21 MR. WILLISON: For the February loss? 22 MR. NOUD: Yes. 23 THE WITNESS: He told me that he was moving 24 to Lansing, that's my notes. 25 BY MR. NOUD:

1 2 3

1 2 3 4 5 6 7 8 9 10

Q A

Q

A

Q

A Q

16 Are you sure of that? In referencing my notes, which I can't remember the exact conversation.

17 Are you sure that he told you that he was moving to Lansing? Based on the notes that inputted in the file and my history of working claims and putting notes -making notes and referencing, yes. Would it surprise you to know that he had lived in Lansing since July of2010? Yes. Did you ask Song Yu whether he was living in the home at 1724 Forest when you talked to him on February

16

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

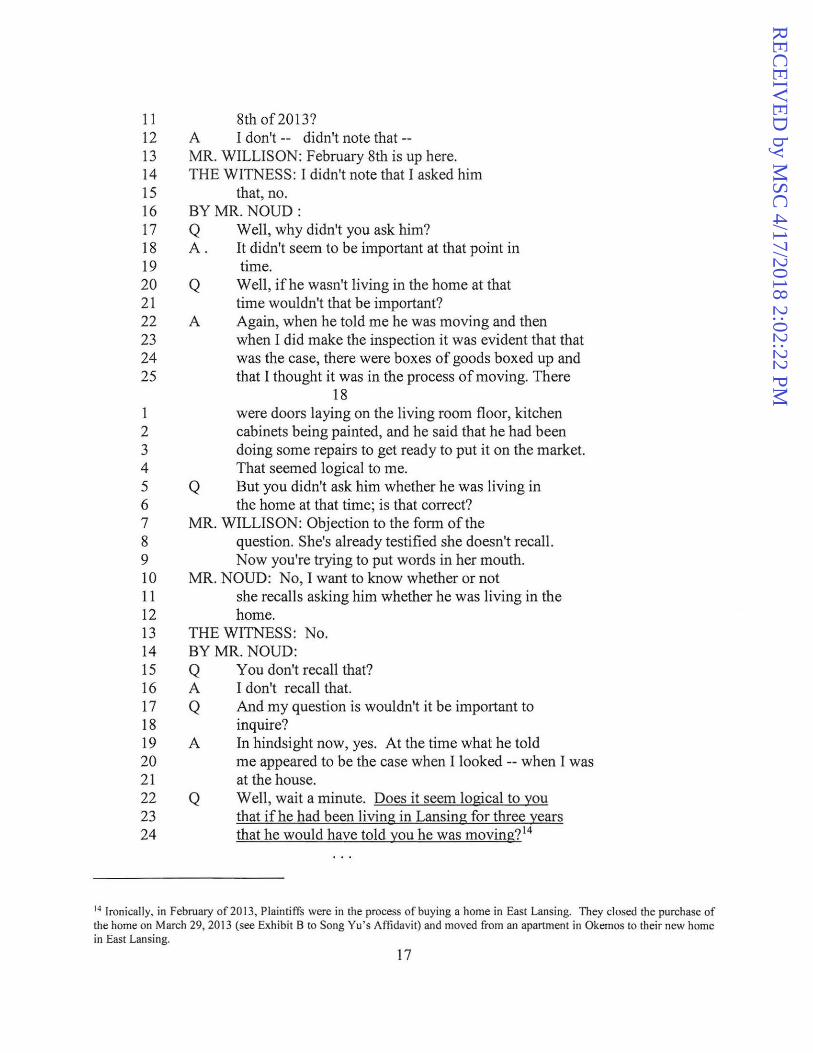

8th of2013? A I don't -- didn't note that --MR. WILLISON: February 8th is up here. THE WITNESS: I didn't note that I asked him

that, no. BYMR. NOUD: Q A.

Q

A

Q

Well, why didn't you ask him? It didn't seem to be important at that point in time.

Well, if he wasn't living in the home at that time wouldn't that be important? Again, when he told me he was moving and then when I did make the inspection it was evident that that was the case, there were boxes of goods boxed up and that I thought it was in the process of moving. There

18 were doors laying on the living room floor, kitchen cabinets being painted, and he said that he had been doing some repairs to get ready to put it on the market. That seemed logical to me. But you didn't ask him whether he was living in the home at that time; is that correct?

MR. WILLISON: Objection to the form of the question. She's already testified she doesn't recall. Now you're trying to put words in her mouth.

MR. NOUD: No, I want to know whether or not she recalls asking him whether he was living in the home.

THE WITNESS: No. BYMR. NOUD: Q A Q

A

You don't recall that? I don't recall that. And my question is wouldn't it be important to inquire? In hindsight now, yes. At the time what he told me appeared to be the case when I looked -- when I was at the house.

Q Well, wait a minute. Does it seem logical to you that if he had been living in Lansing for three years that he would have told you he was moving?14

14 Ironically, in February of 20 13, Plaintiffs were in the process of buying a home in East Lansing. They closed the purchase of the home on March 29,2013 (see Exhibit B to Song Yu's Affidavit) and moved from an apartment in Okemos to their new home in East Lansing.

17

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

19 13 THE WITNESS: No.

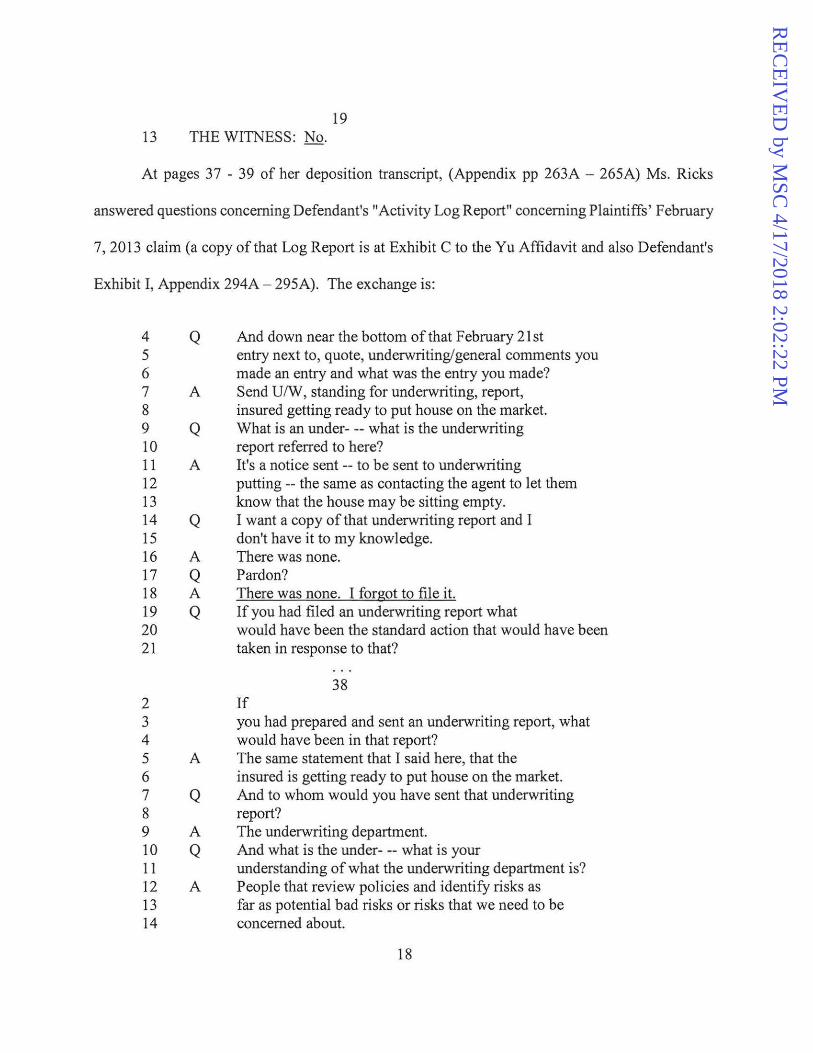

At pages 37 - 39 of her deposition transcript, (Appendix pp 263A - 265A) Ms. Ricks

answered questions concerning Defendant's "Activity Log Report" concerning Plaintiffs' February

7, 2013 claim (a copy of that Log Report is at Exhibit C to the Yu Affidavit and also Defendant's

Exhibit I, Appendix 294A - 295A). The exchange is:

4 Q And down near the bottom of that February 21st 5 entry next to, quote, underwriting/general comments you 6 made an entry and what was the entry you made? 7 A Send U/W, standing for underwriting, report, 8 insured getting ready to put house on the market. 9 Q What is an under- -- what is the underwriting 10 report referred to here? 11 A It's a notice sent -- to be sent to underwriting 12 putting -- the same as contacting the agent to let them 13 know that the house may be sitting empty. 14 Q I want a copy of that underwriting report and I 15 don't have it to my knowledge. 16 A There was none. 17 Q Pardon? 18 A There was none. I forgot to file it. 19 Q If you had filed an underwriting report what 20 would have been the standard action that would have been 21 taken in response to that?

38 2 If 3 you had prepared and sent an underwriting report, what 4 would have been in that report? 5 A The same statement that I said here, that the 6 insured is getting ready to put house on the market. 7 Q And to whom would you have sent that underwriting 8 report? 9 A The underwriting department. 10 Q And what is the under- -- what is your 11 understanding of what the underwriting department is? 12 A People that review policies and identify risks as 13 far as potential bad risks or risks that we need to be 14 concerned about.

18

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

25

1 2 3 4 5 6 7 8

Q

A Q A

And do you have an understanding of what the 39

underwriting department would have done with your report--Some---- ifyou had made it? Someone would have followed up on it, again, talking to the agent and to watch the house to see if it was-- appeared to be empty or if there was anybody living in it.

On pages 44 - 46 of the Ricks deposition transcript, (Appendix pp 270A - 272A) the

following exchange took place with respect to the issue of whether Plaintiffs' West Lake home

was "vacant" in February of2013:

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

44 Q And under what circumstances would Farm Bureau,

to your understanding, not have had responsibility to repair the water damage?

A If the house had been vacant for over 60 days. Q And did you do anything to investigate whether or

not the house had been vacant for more than 60 days? A

Q

No, I took the insured that he was in the process of moving, this is my interpretation of what he had told me, and that they were going back and forth and preparing it for-- to go on the market and that they had been there. I took it-- interpreted it that way, that it was within the 60 days. And what, again, may -- well, no, strike that. Do you now believe you misinterpreted what you learned from Song Yu?

A Yes. MR. WILLISON: Misinterpreted or misled?

Are you asking her whether she thinks it was -BY MR. NOUD: Q A Q A

Q

Do you now think you were misled by Song Yu? Yes. Why do you think you were misled by Song Yu? After finding out that they had been out of the house for such a long period of time. Did you ask him whether they'd been out of the

19

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

45 1 house for a long period of time? 2 A No, I did not. 3 Q Pardon? 4 A No, I did not. 5 Q Why didn't you? 6 A I didn't feel that it was necessary. I thought 7 what he told me was actually in the process of taking 8 place and it didn't cause me to ask any further 9 questions. 1 0 Q Did you ask him whether he was living in Lansing 11 at that time? 12 MR. WILLISON: Asked and answered. Go 13 ahead. 14 THE WITNESS: No, I didn't ask him where he 15 was living, he told me. 16 BY MR. NOUD: 17 Q Did you ask him how long he had been living in 18 Lansing? 19 MR. WILLISON: Again, we've established 20 this, we've asked and answered It. 21 MR. NOUD: I don't like the word misled and, 22 therefore, we're going to find out what it was that was 23 misleading. 24 BY MR. NOUD: 25 Q What was misleading about what Song Yu told you?

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Q

A

Q

A

46 That he didn't -- he made me believe that they were going back and forth, that they were actively moving, not that it had been sitting there for three years empty. And what did he say exact -- what were his exact words that led you to believe that he was actively going back and forth? He told me that they had been going back and forth and were preparing it for sale. The evidence that the doors were off of the cabinet and that they were being painted or they had been painted and were drying seemed that that was the case. So your inspection of the home led you to believe that they were in the process of moving rather than they had already moved; Is that your testimony? Yes.

20

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

On pages 61 - 63, (Appendix pp 287 A - 289A) Ms. Ricks was asked questions concerning

deposition Exhibit 7 (a copy of deposition Exhibit 7 is at Plaintiffs' Exhibit 3, Appendix page 53b ).

The subject of Exhibit 7 was whether Plaintiffs' home was "vacant" at the time of the December

2013 claim. That exchange is:

17 18 19 20 21 22 23 24 25

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Q

A Q

A Q A

I show you Exhibit 7 and ask you whether or not you recognize that? Yes. It's not long, it's an email from you to Monica Dixon dated Friday, December 27th, 2013, at 9:32a.m.; is that right? Yes. Please read it into the record. Thanks, Monica. I had a great Christmas, hope

62 you did as well. I was wondering if that might be an issue, do you have the returned mail notices that you could send me? That will help support my stand. I'm sure he's going to say that they stay there on weekends. Tony from Servepro told me it's the worst one he's ever seen. Insured hasn't called me back yet. Thanks. Happy New Year. Linda Ricks.

Q Why were you sure that Song Yu was going to say that he hadn't stayed there-- or that he had stayed there on weekends?

A

Q

I was thinking of worst case scenarios and what might be said to offset us. You weren't very objective at the time you made that comment, were you?

MR. WILLISON: Objection, form ofthe question. Go ahead.

THE WITNESS: I wasn't very objective? I was concerned.

BYMR. NOUD:

Q

A

Q

And why would you be concerned about him saying that he was staying there on weekends? I felt that there was a coverage issue here and I was trying to cover my bases as far as what the objections might be. And trying to find no coverage, weren't you?

63

21

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

1 MR. WILLISON: Objection, don't answer that.

C. THE PARTIES' SUMMARY DISPOSITION MOTIONS; THE TRIAL COURT'S RULING; THE PLAINTIFFS' APPEAL; THE COURT OF APPEALS DECISION; AND

DEFENDANT'S APPLICATION FOR LEAVE TO APPEAL

On November 11, 2015, Plaintiffs filed a Summary Disposition Motion and supporting

brief which included the above quotations from the depositions ofMs. Ricks and Mr. Gregart and

the Affidavit of Plaintiff Song Yu. And, at the time of the hearing on the motion, Plaintiffs'

counsel submitted two additional Exhibits to the court15•

On December 30, 2015, Defendant filed Response and Counter-Motion for Summary

Disposition which was supported by a certified copy of the subject homeowners policy, the

examination(s) under oath (EUO) of both Plaintiffs, some of the photos (of Plaintiffs' West Lake

home) taken by Defendant's adjuster, Linda Ricks on December 27, 2013 and Ms. Ricks'

deposition transcript.

At the conclusion of the January 6, 2016 hearing on the motions, the trial court orally

denied Plaintiffs' Motion for Summary Disposition and granted Defendant's Motion for Summary

Disposition Order. The stated factual grounds for the trial court's grant of Defendant's motion for

summary disposition are at pages 52-59 of the summary deposition transcript at Defendant's

Exhibit C, Appendix pp 29A-30A. They are not repeated here for lack of space. An order

implementing the court's decision was entered on January 28,2016.

On February 16, 2016, Plaintiffs filed a Claim of Appeal from the summary disposition

Order. On April 11 , 2017 the Court of Appeals issued an unpublished opinion reversing the trial

15 Copies of those exhibits are Plaintiffs' Exhibits I C and 4 at Appendix 12b-13b and 55b-58b. They are Defendant's Activity Log Report of february 2013 and additional photos of the inside of Plaintiffs' West Lake home which were taken by adjuster Ricks on December 27, 2013 but were not included as exhibits to Defendant's motion for summary disposition.

22

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

court's ruling and ordering the trial court to enter judgment in favor of the Plaintiffs. On May 23,

2017, Defendant filed an Application for Leave to Appeal; and on June 30, 2017 Plaintiffs filed

an Answer to Defendant's Application for Leave to Appeal. By order dated December 20, 2017,

this Court granted Defendant's Application and ordered the parties to address the issues which

addressed in this brief. On March 13, 2018, Defendant filed its "Brief on Appeal." This Brief on

Appeal, of Plaintiffs, is filed in response to Defendant's Brief on Appeal.

ARGUMENT

I. THE PLAIN LANGUAGE OF THE INSURANCE POLICY (HOP) DID NOT PRECLUDE COVERAGE BUT RATHER PROVIDED COVERAGE.

A. STANDARD OF REVIEW

This Court's review of a trial court's decision on a motion for summary disposition is de

novo. In re Bradley Estate, 494 Mich 367, 376; 835 NW2d 545 (2013). Issues of contract

construction are reviewed de novo. Rory v Continental Ins Co, 473 Mich 457, 464; 703 NW2d

23 (2005).

B. ON DECEMBER 25, 2013, PLAINTIFFS' SECOND HOME ON WEST LAKE WAS NOT "VACANT" AND PLAINTIFFS WERE "OCCUPYING" IT (AS THOSE

WORDS ARE DEFINED UNDER THE HOP).

The Court of Appeals, in McGrath v Allstate Ins Co, 290 Mich App 434, 439, 802 NW2d

619,623 (2010) stated (at page 439):

The rules of contract interpretation apply to the interpretation of insurance contracts. Citizens Ins. Co. v. Pro-Steel Serv. Group, Inc., 477 Mich. 75, 730 N.W.2d 682 (2007). The language of insurance contracts should be read as a whole and must be construed to give effect to every word, clause, and phrase. Klapp v. United Ins. Group Agency, Inc., 468 Mich. 459, 467, 663 N.W.2d 447 (2003). When the policy language is clear, a court must enforce the specific language of the contract. Heniser v. Frankenmuth Mut. Ins. Co., 449 Mich. 155, 160,534 N.W.2d 502 (1995). However, if an ambiguity exists, it should be construed against the insurer. !d. An insurance contract is ambiguous if its provisions are subject to more

23

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

than one meaning. Vushaj v. Farm Bureau Gen. Ins. Co. of Mich., 284 Mich.App. 513, 515, 773 N.W.2d 758 (2009) citing Raska v. Farm Bureau Mut. Ins. Co. of Mich., 412 Mich. 355, 362, 314 N.W.2d 440 (1982). (emphasis added)

During 2013 Plaintiffs "lived in" (i.e. "resided" in; i.e. "occupied") both their primary home

in East Lansing and their second home (the "residence premises" on West Lake) just as did the

other 1 00 insureds who insured their second homes with Defendant's agent Dan Gregart. The facts

which support this assertion are in Song Yu's Affidavit (Defendant's Exhibit Fat Appendix 174A

- 177 A), and in Song Yu's Examination Under Oath (EUO) testimony (Defendant's Exhibit D)

some of which is quoted below at pages 30 - 32 of the brief.

Under the terms of Defendant's standard HOP, when an insured insures a home with

Defendant, and then suffers a loss from a "special peril" at a time when the home has been not

"vacant beyond a period of 60 consecutive days" or has not been "unoccupied beyond a period of

six consecutive months," it is logical, when interpreting the HOP "as a whole," to conclude from

this unambiguous (or ambiguous) policy language that the insured is residing in that home at the

time of the loss.

If such an interpretation is not logical, then why did Defendant include the definitions of

"vacant" and "occupied" in its standard HOP? Because Defendant's insureds are not residing in

their insured homes when those homes are "vacant" beyond a period of 60 consecutive days or

when those homes are unoccupied beyond a period of six consecutive months, then aren't the

insureds residing in their homes when the homes are "vacant" for a period which is less than 60

consecutive days (e.g. 59 days) and/or when the homes are unoccupied for a period which is less

than six consecutive months (e.g. 5 months and 29 days)?

Addition support for this assertion are the facts:

24

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

I. That Defendant's adjuster Linda Ricks, in a December 27, 2013 email to a fellow

employee (see Plaintiffs' Exhibit 3, Appendix 53b), states: "I'm sure he is going to say

that [sic] stay there on weekends"; and

2. That the HOP definition of "occupied" "means being lived in with regular and

continuous legal presence of human inhabitants ... " (rather than regular and

continuous physical presence?

Defendant cites the cases of Heniser v Frankenmuth Mut Ins Co, 449 Mich 155; 534

NW2d 502 (1995) and McGrath v Allstate Ins Co, supra to support its argument that Plaintiffs

were not "living in" their West Lake home on December 25, 2013 . In Heniser, the Plaintiff and

his wife had purchased a vacation home in Honor, Michigan and had lived in the home

intermittently through the years until they divorced. Heniser retained possession of the home after

the divorce, but later, he sold the home on land contract without informing Frankenmuth of the

sale. This Court stated (at page 162):

" ... the conditions section of the policy requires the insured to notify the insurer of any 'changes in title or occupancy of the property during the term of the policy' before recovering for any loss ... " (emphasis added)

The only similar provision in the HOP (contract) between Plaintiffs and Defendant states:

SECTION I- CONDITIONS

Paragraph g. of2. Your duties After Loss is deleted and replaced by the following:

g. send to us, within 60 days after our request, your signed and notarized Sworn Statement in Proof of Amount of Los which sets forth:

( 4) changes in the title or occupancy of the property during the term of the policy; ...

25

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

Defendant waived this provision when it investigated and paid Plaintiff's February 2013 water

damage claim without requesting a written proof of loss from Plaintiffs.

In its opinion in Heniser, 16 this Court also stated (at pages 162 and 163):

While the definition of 'reside' may be ambiguous in other contexts, there is no ambiguity in this case ... In some contexts, the legal term means something more than actual physical presence; it includes the intent to live at the location at some time in the future, a meaning similar to the legal concept of domicile ... In other contexts, the term requires actual physical presence. (emphasis added)

The policy of interpreting ambiguities in a contract against insurers is rooted in the fact that insurers have superior understanding of the terms they employ, which should not bind relatively unsophisticated insureds. This goal is not furthered by allowing insureds to employ a sophisticated version of a term to create a claim of ambiguity.

Finally, any ambiguity created by the fact that the law ascribes multiple meanings to the term 'reside' is irrelevant because Mr. Heniser fails under either standard.10

Footnote 10 in the Heniser opinion states:

Whether Heniser actually had to live at the insured premises on a full time basis, or whether intermittent occupancy was sufficient, is not in dispute. In light of the fact that this policy was issued with the knowledge that Heniser used the property as a vacation home on an irregular and sporadic basis, it is likely that Frankenmuth Mutual contemplated noncontinuous occupancy.

By contrast, in this case, the question of whether "intermittent occupancy is sufficient" is

very much in dispute.

Now, applying the above quoted statements in Heniser, to this case, the relevant facts

include:

1. That, in February of 2013, Defendant's adjuster Linda Ricks concluded (and recorded) in her

"Activity Log Report" (Exhibit I at Appendix 294 A - 295 A) that Plaintiffs were moving to

16 There apparently were no definitions of vacant and occupied in the Heniser insurance policy.

26

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

Lansing and were putting their West Lake home on the market;

2. That Ms. Ricks forgot to make a report concerning her conclusion to Defendant's underwriting

department; and

3. That that approximately 9 months later (on November 4, 2013) Defendant renewed Plaintiffs'

HOP for an additional year from 12/8113 to 12/8114.

Why, if Defendant did not wish to insure Plaintiffs' second home, didn't Defendant cancel

Plaintiffs' HOP during the 9 months between February of2013 and November 4, 2013?

In McGrath, the Court of Appeals held that the phrase "where you reside," in the insurance

policy definition of covered "dwelling," was a "statement of coverage" that required that the

insured live in the premises at the time of the loss. There are several material facts which

distinguish McGrath from this case. First, there was no claim of equitable estoppel in McGrath.

We will never know how the Court of Appeals would have ruled:

1. If Allstate had paid a prior claim for a water damage loss while Mrs. McGrath was physically

living in Farmington Hills;

2. And, if after paying the first water damage claim, Allstate had renewed Mrs. McGrath's

homeowners policy;

3. And, if after renewing Ms. McGrath's homeowners policy, Allstate had later denied a second

claim for a water damage loss under circumstances that were not materially different than the

circumstances existing at the time of the first water damage loss.

Secondly, it is important to note that the McGrath Court stated (at pages 443 and 444):

"As in Heniser, there is no ambiguity in the Allstate policy issued to Ms. McGrath. Accordingly it was error for the trial court to ascribe a technical meaning to the term "reside" when the common understanding of the term required that Ms. McGrath live at the Gaylord address at the time of the loss. It is undisputed that

27

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

Ms. McGrath did not physically live at the Gaylord address when the pipes froze and burst or for two years before the loss and therefore, she did not satisfy the requirement that she 'reside' in the house when the loss occurred.2"

Footnote 2 in the McGrath opinion states in part:

... Were we to conclude that the phrase "where you reside" in the policy does not require that an insured be physically present in the dwelling throughout the policy period, plaintiff's position would suggest that Ms. McGrath had to at least reside in the Gaylord property when she received the renewal certificate, or on the date it became effective. However we decline to address this issue because our holding resolves the matter and because despite Plaintiff's assertions the parties did not attach evidence of a policy renewal to their briefs below and this issue was not argued before or decided by the court.

By contrast in this case, evidence ofDefendant's 11/4/13 renewal ofthe subject HOP for

another year, was attached to Song Yu's affidavit (Plaintiffs' Exhibit 1 D, Appendix 15b-16b) in

support of Plaintiff's motion for summary disposition; and it is clear that Plaintiffs have raised the

issue of whether Defendant should be precluded from denying coverage, because Defendant

renewed Plaintiffs' HOP nine months after Linda Ricks concluded that: "Insured is moving to

Lansing, this house is going on the market."

At the top of page 19 of its Brief, Defendant quotes a paragraph from the McGrath case,

but omits the middle portion of the quoted paragraph. That omitted part of the paragraph states:

As one example, the frozen-pipes exclusion limits an insured's ability to recover for a loss when a building structure is vacant or unoccupied unless the insured takes reasonable measures to prevent such damage. This exclusion implicitly recognizes that the insured may be away from the property, but be covered for the loss. This is not inconsistent with the definition of "reside" as defined above. Indeed, the fact that Ms. McGrath had established the habit of vacationing in Florida during the winters in the 1990s did not change the character of the dwelling or her living arrangements. During that time, she resided on the property, albeit for fewer than 12 months of the year, but it remained her home base and the residence to which she regularly returned. (emphasis added)

28

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

In this case, by analogy, the policy definitions of "vacant" and "occupied" call for the

conclusion that Defendant implicitly recognized (by using those specific definitions in its standard

HOP) that when a second home is not "vacant" or not "unoccupied," the insured is considered to

be residing in it.

In addition, in the definitions section of its HOP, Defendant makes a distinction between

the physical presence and the legal presence of its insureds. Because of Defendant's use of the

phrase "legal presence," it is clear that occupied does not mean "being lived in with regular and

continuous physical presence ofhuman inhabitants."

In light of these facts, Plaintiffs assert that the word "reside" in the definition of"residence

premises" (in the HOP) must be read "as a whole" along with the HOP definitions of"vacant" and

"occupied."

It is also important to note that in none of the cases cited by Defendant, is there any

discussion of the meaning of the word "reside" in an insurance policy in which "occupied" is

defined as being lived in with regular and continuous legal presence of human inhabitants.

Therefore:

1. Because there is no definition of reside in the HOP at issue in this case; and

2. Because "occupied" is defined (in the HOP) as "being lived in with regular and continuous

legal presence ofhuman inhabitants ... "

Plaintiffs respectfully contend that both the Heniser case and the McGrath case should be

distinguished by this Court.

C. INACCURATE FACTUAL ALLEGATIONS IN DEFENDANT'S BRIEF

Defendant argues (at least by implication) that Plaintiffs' West Lake home was "vacant"

for more than 60 continuous days and/or not "occupied" for more than 6 continuous months. This

29

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

(implied) argument is rebutted by the facts in the affidavit of Song Yu and by the facts in his EUO

testimony at Exhibit F, Appendix, pp 63A - 67 A and Exhibit F, Appendix 71 A - 73A. These facts

include:

1. That, at the time of Plaintiffs' December 25, 2013 water damage loss, there were furnishings,

utilities and the amenities minimally necessary for human habitation in Plaintiffs' West Lake

home and garage; and

2. That during the 6 months prior to the December 2013 water damage loss, Plaintiffs were using

their West Lake home as their second home.

Song Yu's EUO testimony discusses Plaintiffs' use of their West Lake home (as their

second home) during the period from mid-2010 through 2013 as follows (see Defendant's

Appendix 63A-67 A):

16 17 18 19 20 21 22 23 24 25

I 2 3 4 5 6 7 8 9 10 11 12

A

Q A

Q A Q A

30

Q A Q A Q

A Q A

the-- okay. Let's back up. You moved out in 2010; right? Correct. And took all your stuff to Okemos ; right? No. No? Okay. What did you leave? Everything. What did you sit on in Okemos? Remember, this is an apartment, a one-bedroom apartment. So I took my couch -- no, I didn't take my couch, took our--what we could, dishes, clothing. This was a 600-square-foot

apartment, so most all of the furnishings and household livings was still in Portage when we moved out to East Lansing in 201 0. So you took your clothes and your dishes and stuff? Uh-huh (affirmative). Yes? Yes. And then when you bought the house in East Lansing, you came and got the rest of the stuff? No. When did you come and get the rest of the stuff? They're still there in the garage in Portage.

30

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

13 Q Why? 14 A Most everything, furnishings that was bought, in East 15 Lansing is new. 16 Q Is that because the stuffthat was in the house in Portage 17 smells like old house? 18 A My wife thought so. 19 Q Okay . And so what was your intent with the stuff in the 20 garage? Why did you move it from the house to the garage? 21 A Because of the Listing for sale. The realtor said, "You 22 either have to .QUt brand new furnishings in there to make an 23 a.Q.Qearance or get everything out." 24 Q Okay. 25 A So he made me move from house to the garage for the showing.

31 1 Q And that was to get rid of the -- to help get rid of the 2 smell? 3 A Part of that was that maybe, but also just appearance of the 4 attractiveness of the home for showing. They either 5 wanted - - he either wanted a full furnishing with nice 6 looking things. 7 Q Or empty? 8 A or completely empty. 9 Q All right. So you moved everything out into the garage 10 when? Around the time of Exhibit 1, the listing agreement, 11 or before that? 12 A No; no. It was during; it was a process. Despite we moved 13 a lot of the furnishings that we moved; the blankets, beds 14 where we sleep, a blow-up bed, and clothings and dishes; all 15 the other amenities were still there. Only thing that we 16 moved was the dining tables, sofas. 17 Q Why did you leave your blow-up mattress in the house? Why 18 didn't you put that in the garage? 19 A To come there to spend time. 20 Q Well, you have access to the garage; right? I mean, you 21 could have gotten it out of the garage and used it then; 22 right? 23 A So that means I had to move every time I went over there? 24 Q No. I'm asking you if the goal was to have the house empty; 25 why did you leave the air mattress in the house?

32 1 A I just did it. 2 Q Okay. 3 A Because that wasn't getting in the way of the showing, 4 because they were in the closet. 5 Q Okay. So when the pipe burst due to freezing, was all the

31

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

1 2 3 4 5 6 7 8 9

A

Q A

Q A Q A Q A

Q A

Q A

Q A Q A

Q

A

stuff still in the house , or was it in the garage or what? Everything that I mentioned being in there; clothing, the bed, the things that we mentioned; are still there -- were still there. I thought you took your clothing to East Lansing? We have clothing to the East Lansing, part of it, when we had to move in May, but we did not move everything. Why would you have any clothing in Portage? Because that was my home. How often would you go there? Quite often in the summer months. I don 't know what that means. Quite often meaning that every time I had a chance to go from my work. I don't know what that means either, though. Well, the numbers-wise? Is that the number of the wise that you wanted? Yeah . I mean, how --In the summertime I'd probably be there at least once a month.

33 And that was true in 2013? '13, yes. Okay. And outside of summer? Only for maintenance of the home, so I would only maybe be there twice a season, just to clean up the leaves. So your wife 's estimate was about six times a year. It sounds like you kind of agree with that? My estimation would be slightly more than that. I would say more of ten times a year.

D. BECAUSE PLAINTIFFS' SECOND HOME WAS NOT "VACANT" AND NOT NOT "OCCUPIED" ON DECEMBER 25, 2013, THE PLAIN LANGUAGE OF THE

INSURANCE POLICY (HOP) DID NOT PRECLUDE COVERAGE OF PLAINTIFFS' WATER DAMAGE LOSS WHICH WAS INSURED AGAINST AS A "SPECIAL PERIL"

BUT RATHER PROVIDED IT

In summary, for the reasons stated above, Plaintiffs' lake home ("residence premises") was

not "vacant" and was not not "occupied" on December 25, 2013. Because Plaintiffs' lake home

was not "vacant" and was "occupied" on December 25, 2013, Plaintiffs were (implicitly if not

explicitly) residing there. And, because of these facts, the plain language of the HOP did not

32

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

preclude (but rather provided) coverage for Plaintiffs' December 25, 2013 water damage loss

which the HOP insured against as a "Special Peril."

II. CIRCUMSTANCES UNDER WHICH THE DOCTRINE OF EQUITABLE ESTOPPEL MAY BE APPLIED TO REQUIRE AN INSURER TO EXPAND COVERAGE THAT IS CONTRARY TO THE EXPRESS TERMS OF AN INSURANCE CONTRACT.

A. STANDARD OF REVIEW

This Court's review of a trial court's decision on a motion for summary disposition is de

novo. In re Bradley Estate, 494 Mich at 376. This Court reviews a trial court's equitable decisions,

including the application of equitable estoppel. Blackhawk Dev Corp v Village of Dexter, 473

Mich 33, 40; 700 NW2d 364 (2005).

B. THE MICHIGAN LAW OF EQUITABLE ESTOPPEL

The Michigan law of equitable estoppel, with respect to insurance contracts, is discussed

in the case of Morales v Auto-Owners Ins Co, 458 Mich 288; 582 MW2d 776 (1998). The

Morales case concerned a no-fault automobile insurance policy, and the facts are not similar to the

facts in the instant case. However, in Morales, the Supreme Court discussed the application of the

principle of equitable estoppel with regard to insurance contracts. The Court stated (at pages 295,

297 and 299):

The principle of estoppel is an equitable defense that prevents one party to a contract from enforcing a specific provision contained in the contract. (emphasis added)

Therefore, for equitable estoppel to apply, plaintiff must establish (1) that the defendant's acts or representations induced plaintiff to believe that the policy was in effect at the time of the accident, (2) that the plaintiff justifiably relied on this belief, and (3) that plaintiff was prejudiced as a result of his belief that the policy was still in effect. Fleckenstein v. Citizens' Mut. Automobile Ins. Co., 326 Mich. 591 , 599, 40 NW2d 733 (1950).

Indeed, there are many instances in Michigan insurance law where a particular provision of an insurance contract, which normally would operate to end an insurer's liability, is not rigidly enforced because of the principle of estoppel. See Pastucha, supra; Staffan v. Cigarmakers' Int'l Union of America, 204 Mich. 1, 169 NW 876 (1918); Allstate Ins. Co. v. Snarski, 174 Mich. App. 148, 435 NW2d 408 (1988). (emphasis added)

33

RE

CE

IVE

D by M

SC 4/17/2018 2:02:22 PM

C. INSTANCES IN MICHIGAN INSURANCE LAW WHERE A PARTICULAR PROVISION IN AN INSURANCE CONTRACT, WHICH NORMALLY WOULD

OPERATE TO END AN INSURER'S LIABILITY, IS NOT RIGIDLY ENFORCED BECAUSE OF THE PRINCIPAL OF EQUITABLE ESTOPPEL.