recording business transactions

TRANSCRIPT

.

Recording Business Transactions

.

Ayesha Khalil

The account

• Debit & credits• Shareholder

equity• Summary of DR

CR rules

Steps of Recording Process

• JOURNEL• LEDGER• POSTING

Recording process

• Summary

Trial balance

• Limitations of Trial balance

accounting involves recording, classifying, summarizing, and interpreting financial information..

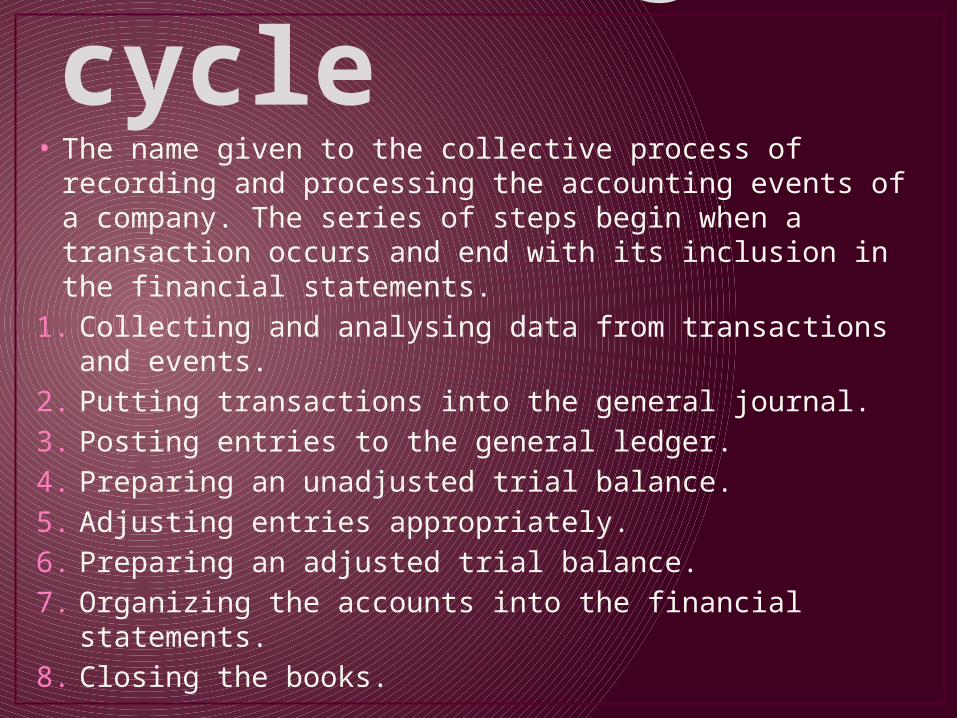

Accounting cycle

Accounting cycle• The name given to the collective process of recording and

processing the accounting events of a company. The series of steps begin when a transaction occurs and end with its inclusion in the financial statements.

1. Collecting and analysing data from transactions and events.

2. Putting transactions into the general journal.

3. Posting entries to the general ledger.

4. Preparing an unadjusted trial balance.

5. Adjusting entries appropriately.

6. Preparing an adjusted trial balance.

7. Organizing the accounts into the financial statements.

8. Closing the books.

,

The accounting cycle, also commonly referred to as accounting process, is a series of procedures in the collection, processing, & communication of financial information.

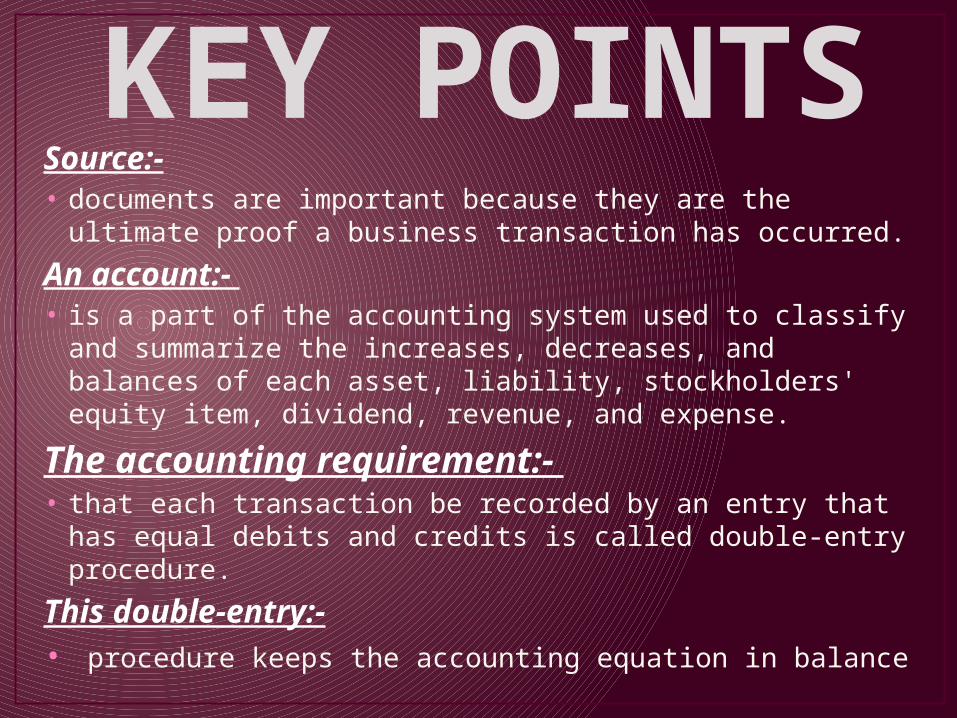

KEY POINTSSource:-• documents are important because they are the ultimate proof a

business transaction has occurred.

An account:- • is a part of the accounting system used to classify and summarize

the increases, decreases, and balances of each asset, liability, stockholders' equity item, dividend, revenue, and expense.

The accounting requirement:- • that each transaction be recorded by an entry that has equal debits

and credits is called double-entry procedure.

This double-entry:-• procedure keeps the accounting equation in balance

Terms

.

• account • A registry of pecuniary transactions; a written or printed statement of

business dealings or debts and credits, and also of other things subjected to a reckoning or review

• Account a written or printed statement of business dealings or debts and credits, and also of other things

• accounting • The development and use of a system for recording and analysing the

financial transactions and financial status of a business or other organization.

• Accounts Receivable • Amounts that customers owe the company for normal credit purchases.

• Accumulated Depreciation• Accumulated depreciation is known as a contra account, because it

separately shows a negative amount that is directly associated with another account.

,Asset• Something or someone of any value; any portion of one's property

or effects so considered

• Asset Items of ownership convertible into cash; total resources of a person or business, as cash, notes and accounts receivable; securities and accounts receivable, securities, inventories, goodwill, fixtures, machinery, or real estate (as opposed to liabilities)

• assets Any property or object of value that one possesses, usually considered as applicable to the payment of one's debts

• Assets A resource with economic value that an individual, corporation, or country owns or controls with the expectation that it will provide future benefit

Bad Debt • A debt which cannot be recovered from the debtor, either

because the debtor doesn't have the money to pay or because the debtor cannot be found and/or forced to pay

• bad debts A bad debt is an amount owed to a business or individual that is written off by the creditor as a loss (and classified as an expense) because the debt cannot be collected and all reasonable efforts to collect it have been exhausted. This usually occurs when the debtor has declared bankruptcy or the cost of pursuing further action in an attempt to collect the debt exceeds the debt itself.

Balance Sheet balance sheet A summary of a person's or organization's assets, liabilities. and equity as of a specific date. Balance Sheet A balance sheet is often described as a "snapshot of a company's financial condition." A standard company balance sheet has three parts: assets, liabilities, and ownership equity

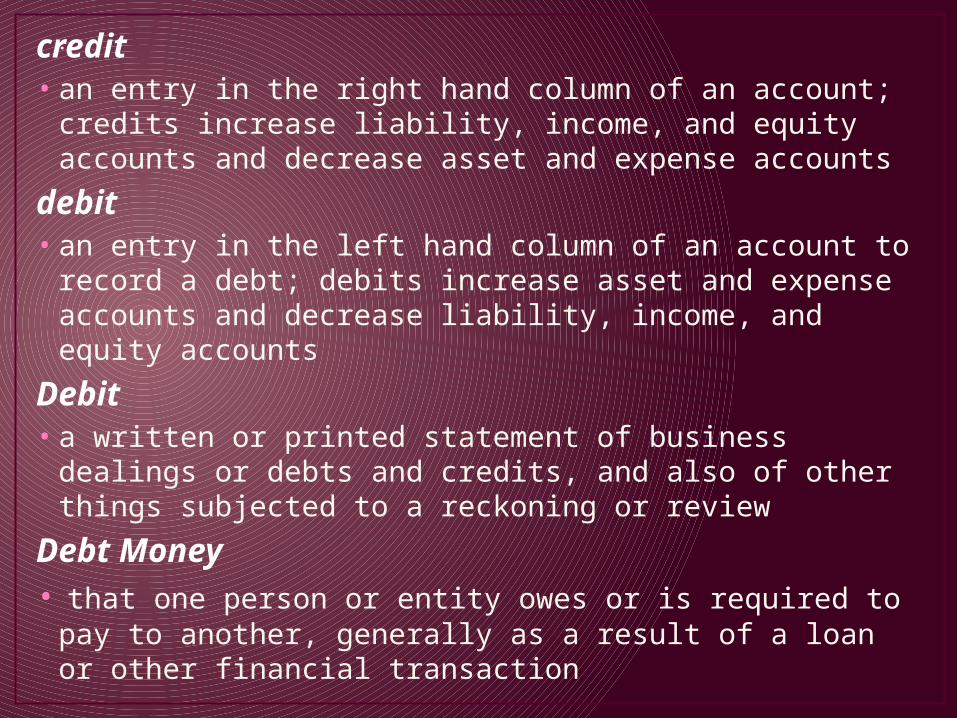

.credit • an entry in the right hand column of an account; credits

increase liability, income, and equity accounts and decrease asset and expense accounts

debit • an entry in the left hand column of an account to record a debt;

debits increase asset and expense accounts and decrease liability, income, and equity accounts

Debit • a written or printed statement of business dealings or debts and

credits, and also of other things subjected to a reckoning or review

Debt Money• that one person or entity owes or is required to pay to another,

generally as a result of a loan or other financial transaction

The measurement of the decline in value of assets. Not to be confused with impairment, which is the measurement of the unplanned, extraordinary decline

in value of assets.Depreciation subtracts a specified amount from the original purchase price to account for the wear and tear on the asset.

Depreciation

dividend

dividend A pro rata payment of money by a company to its shareholders, usually made periodically (e.g., quarterly or annually)

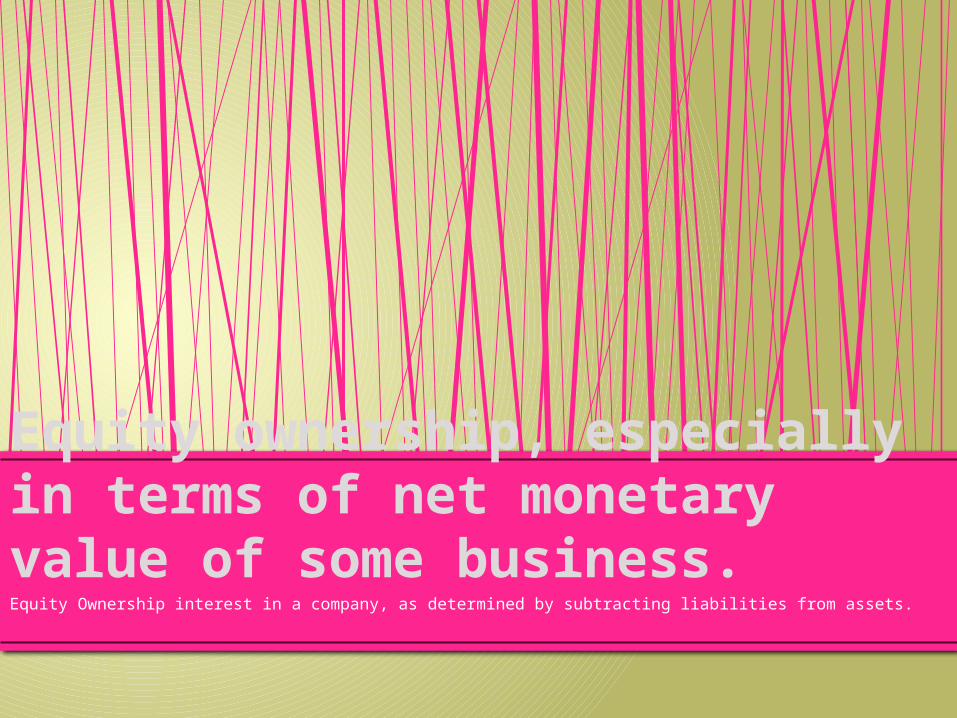

Equity Ownership interest in a company, as determined by subtracting liabilities from assets.

Equity ownership, especially in terms of net monetary value of some business.

‘

Expense in accounting, an expense is money spent or costs incurred in an businesses efforts to generate revenue

.inventory

A detailed list of all of the items on hand.Inventory includes goods ready for sale, as well as raw material and partially completed products that will be for sale when they are completed.

Types of Ledger AccountsAssets

Liabilities

Stockholders’ Equity

Revenues

Expenses

Categories of General Ledger Accounts•The five types of accounts fall into

one of two categoriesReal Accounts

Nominal Accounts

Categories of General Ledger Accounts

Real Accounts Nominal Accounts

This category includes Assets, Liabilities, and Stockholders’ Equities (i.e., Balance Sheet accounts)

Accounts are permanent.Account balances are

carried forward from one fiscal year to the next.

Nominal accounts include revenues and expenses.

Nominal accounts are temporary.

Nominal account balances are closed out to zero at the end of the fiscal year

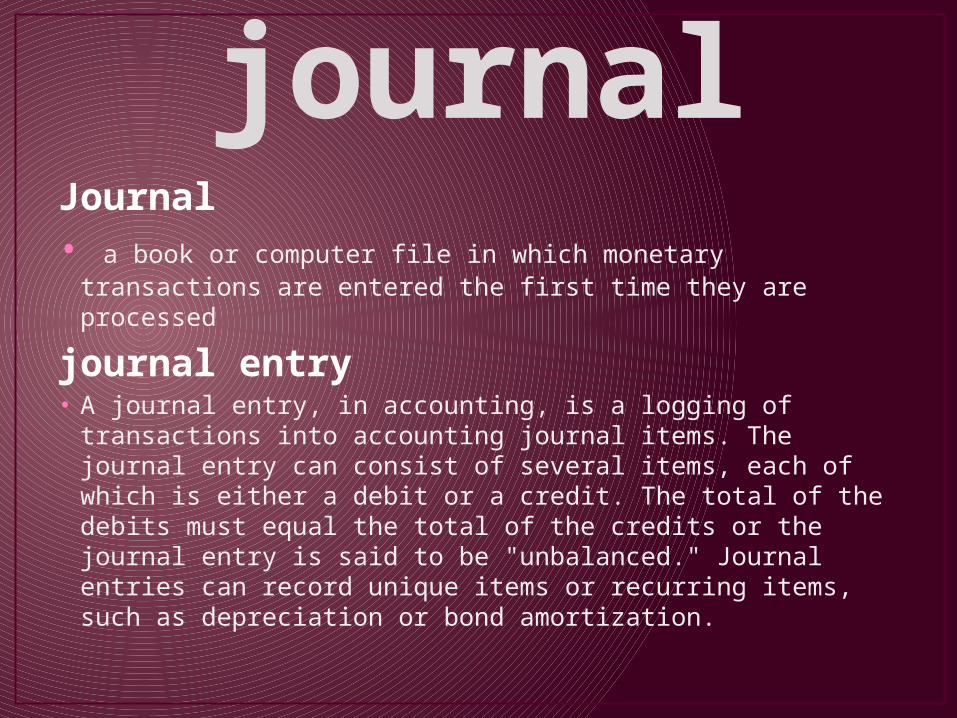

journalJournal• a book or computer file in which monetary transactions are

entered the first time they are processed

journal entry • A journal entry, in accounting, is a logging of transactions into

accounting journal items. The journal entry can consist of several items, each of which is either a debit or a credit. The total of the debits must equal the total of the credits or the journal entry is said to be "unbalanced." Journal entries can record unique items or recurring items, such as depreciation or bond amortization.

ledgerledger

• A collection of accounting entries consisting of credits and debits.

Ledger

• A book for keeping notes, especially one for keeping accounting records.(accounting) A collection of accounting entries consisting of credits and debits.

Liabilities • liability An obligation, debt or responsibility owed to

someone.• liabilities An amount of money in a company that is

owed to someone and has to be paid in the future, such as tax, debt, interest, and mortgage payments

•Liabilities Probable future sacrifices of economic benefits arising from present obligations to transfer assets or providing services as a result of past transactions or events.

TERMSdebit• an entry in the left hand column of an account to record a

debt; debits increase asset and expense accounts and decrease liability, income, and equity accounts

account• A registry of pecuniary transactions; a written or printed

statement of business dealings or debts and credits, and also of other things subjected to a reckoning or review

credit• an entry in the right hand column of an account; credits

increase liability, income, and equity accounts and decrease asset and expense accounts

Recording Process .

Shareholder

Equity

Common stock +

Retained Earning

Revenues - Expense- Dividend

Assetsliabilities+ =

Analysing Transactions

Account• Record of increases and decreases in a specific asset, liability,

equity, revenue, or expense item.• Debit = “Left”• Credit = “Right”

Account Name

Debit / Dr. Credit / Cr.

An Account can be illustrated in a T-Account form.

Debits & CreditsDouble-entry accounting system• Each transaction must affect two or more

accounts to keep the basic accounting equation in balance.• Recording done by debiting at least one

account and crediting another.

DEBITS must equal CREDITS.

Account Debit Credit

Assets Increase Decrease

Contra Assets Decrease Increase

Liabilities Decrease Increase

Equity Decrease Increase

Contributed Capital Decrease Increase

Revenue Decrease Increase

Expenses Increase Decrease

Distributions Increase Decrease

Summary of debit & credit

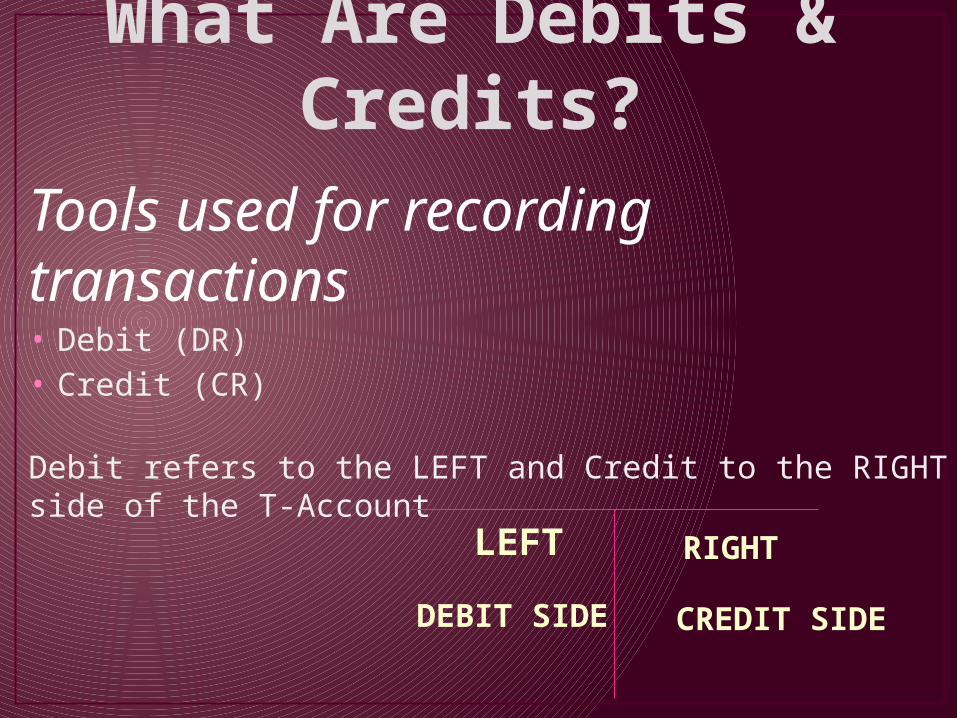

What Are Debits & Credits?

Tools used for recording transactions• Debit (DR)• Credit (CR)

Debit refers to the LEFT and Credit to the RIGHT side of the T-Account

LEFT RIGHT

DEBIT SIDE CREDIT SIDE

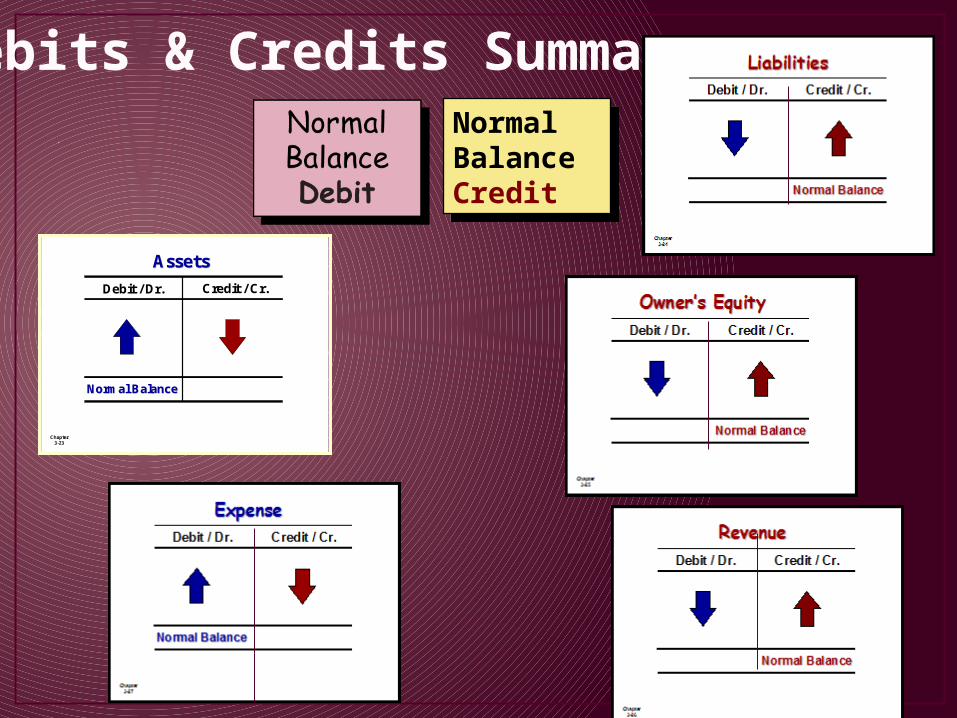

Debits & Credits Summary,

Chapter 3-23

AssetsAssets

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Normal Balance Credit

Normal Balance Credit

Debits & credits affect the Balance Sheet

Assets=liabilities +shareholder equities

Shareholders’ EquityCapital Stock + Retained Earnings

Balance Sheet Income Statement

= + -Asset Liability Equity Revenue Expense

Debit

Credit

Debits and Credits Summary

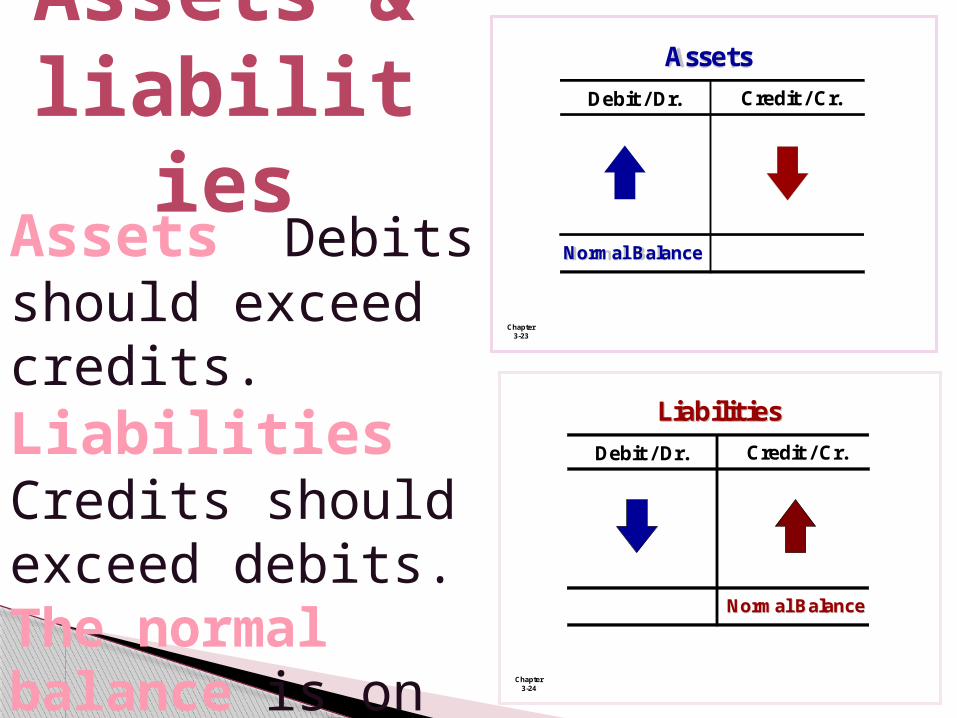

Assets &liabilities

Chapter 3-23

Assets

Debit / Dr. Credit / Cr.

Normal Balance

Chapter 3-24

LiabilitiesLiabilities

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Assets Debits should exceed credits.Liabilities Credits should exceed debits. The normal balance is on the increase side.

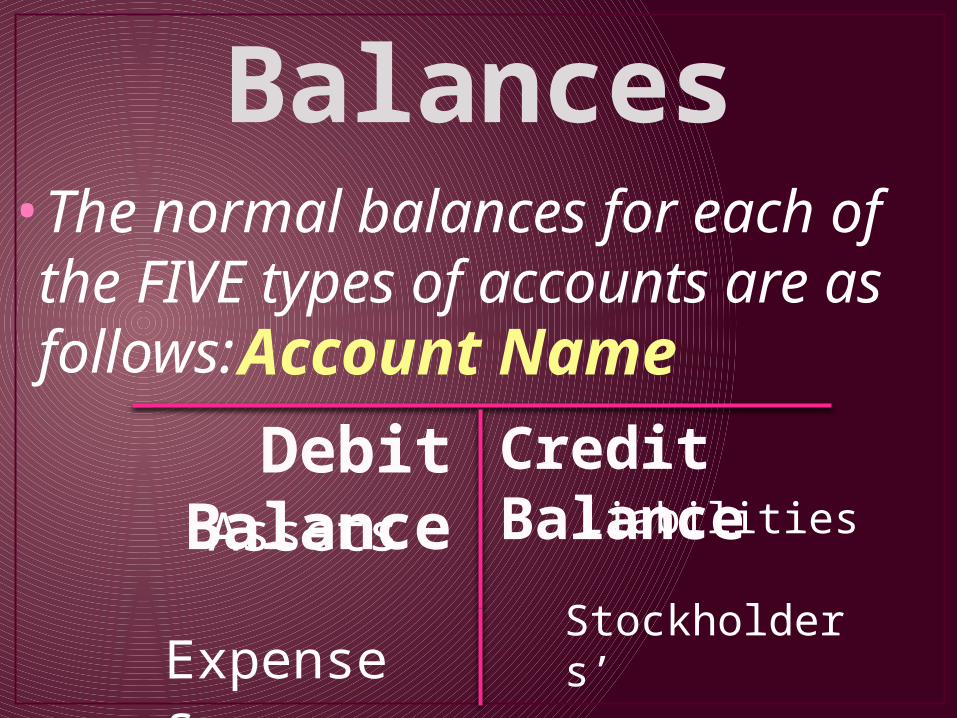

Normal Balances•The normal balances for each of the FIVE types of accounts are as follows:

Account Name

Debit Balance Credit Balance

Assets Expenses

Liabilities Stockholders’ Equity Revenues

Owner’s investments & revenues increase owner’s equity (credit).

Owner’s drawings & expenses decrease owner’s equity (debit).

Owners’ Equity

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Owner’s CapitalOwner’s Capital

Chapter 3-23

Owner’s DrawingOwner’s Drawing

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Owner’s EquityOwner’s Equity

Relationship among the assets, liabilities & owner’s equity of a business:

Expansion of the Basic Equation

The equation must be in balance after every transaction. For every Debit there must be a Credit.

Assets Liabilities= Owner’s EquityBasic Equation

Expanded Basic Equation

+

The purpose of earning revenues is to benefit the owner(s).

The effect of debits and credits on revenue accounts is the same as their effect on Owner’s Capital.

Expenses have the opposite effect: expenses decrease owner’s equity.

Revenue & Expense

Chapter 3-27

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

ExpenseExpense

Chapter 3-26

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

RevenueRevenue

The Journal• Book of original entry.• Transactions recorded in chronological order.

Contributions to the recording process:• Discloses the complete effects of a transaction.• Provides a chronological record of transactions.• Helps to prevent or locate errors because the debit

and credit amounts can be easily compared

General Journal Page

On January 1, 19X7, Caldwell Company borrows $10,000 from the bank.

Prepare the appropriate general journal entry for the above transaction.

Journal EntriesExample 1

Two accounts are affected: Cash is increased by $10,000. Notes Payable is increased by $10,000.

Journal Entries

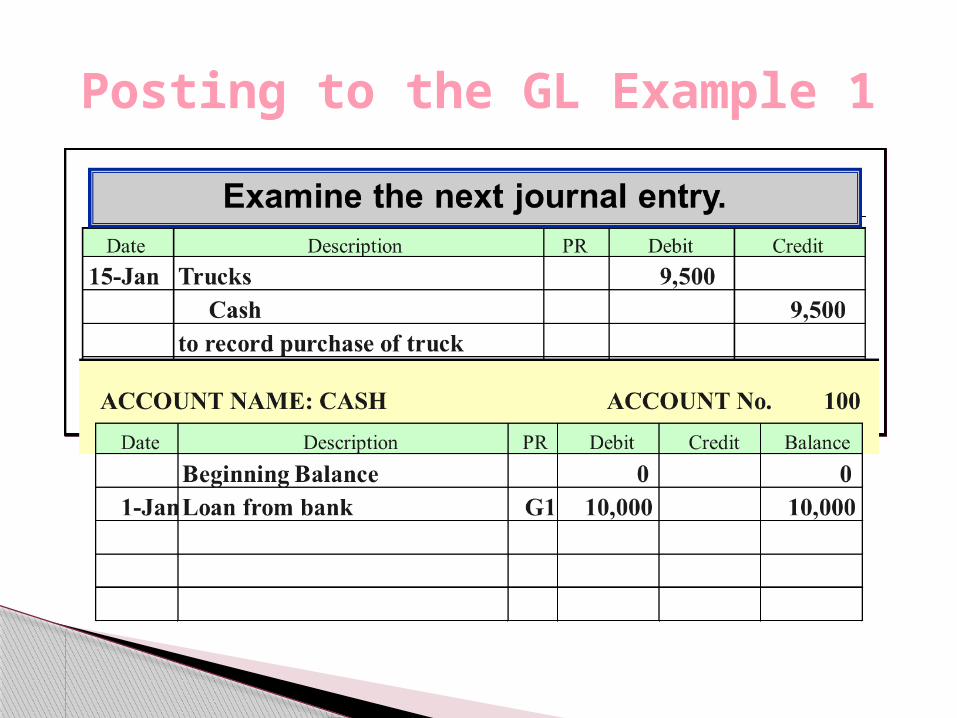

On January 15, 19X7, Caldwell Company purchases a truck for $19,500 cash.

Prepare the appropriate journal entry for the above transaction.

solution

Example 2

Two accounts are affected:Trucks is increased by $19,500.Cash is decreased by $19,500.

Example 2

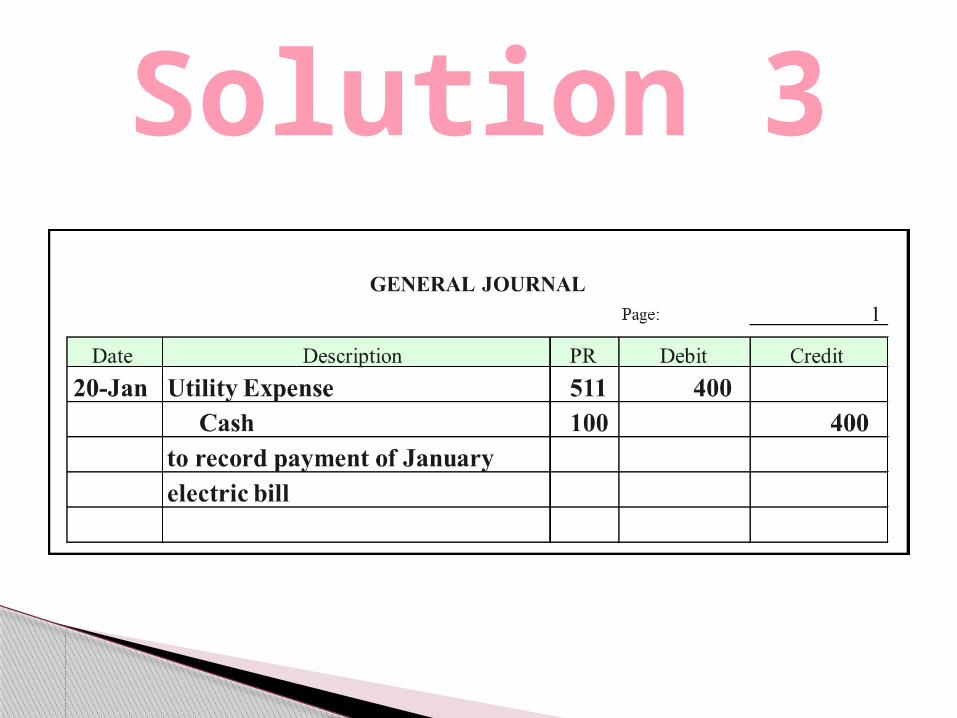

On January 20, 19X7, Caldwell Co. pays the $400 electric bill for January.

Prepare the appropriate journal entry for the above transaction.

Solution

Example 3

Two accounts are affected:Utility Expense is increased by $400.Cash is decreased by $400.

Solution 3

On Oct. 3 Purchases office furniture for $1,900, on account.

solution

Example 4

Oct.27 Pays $700 on balance related to transaction of Oct. 3.

Example 5

Oct. 30 Pays the administrative assistant $2,500 salary for Oct.

Example 6

Simple Entry Two accounts, one debit and one credit.

Compound Entry Three or more accounts.

.

Example – On June 15, H. Burns, purchased equipment for $15,000 by paying cash of $10,000 and the balance on account (to be paid within 30 days).

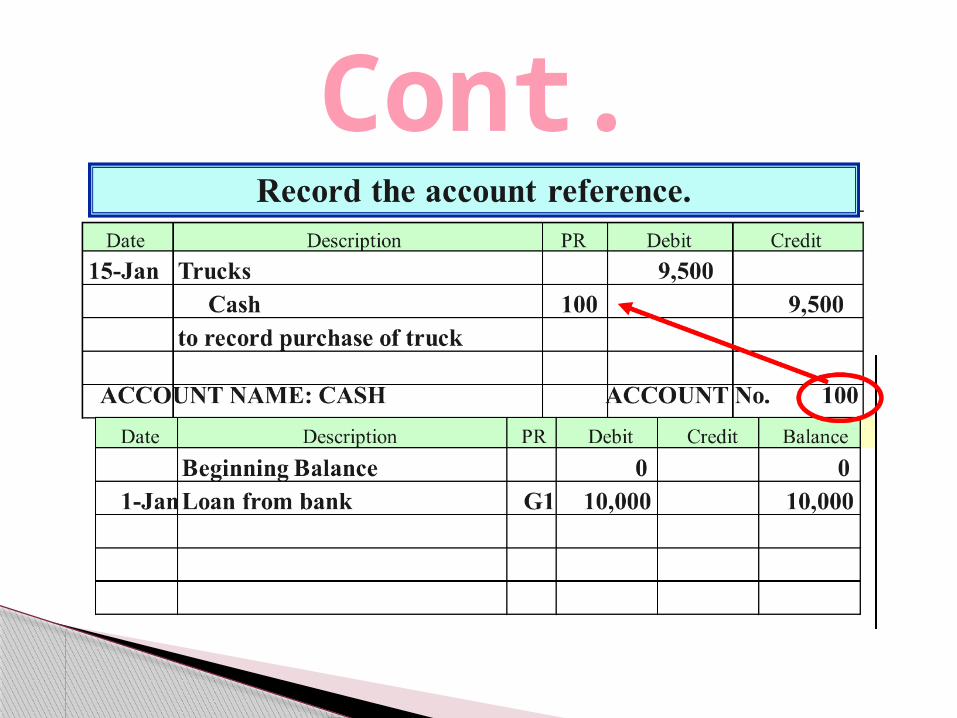

Posting

process of transferring amounts from the journal to the ledger accounts

posting

Posting to the GL Example 1

Cont.

cont.

Cont.

.

The Trial Balance

The Trial Balance•A list of accounts and their balances at a given time.Purpose is to prove that debits equal credits.

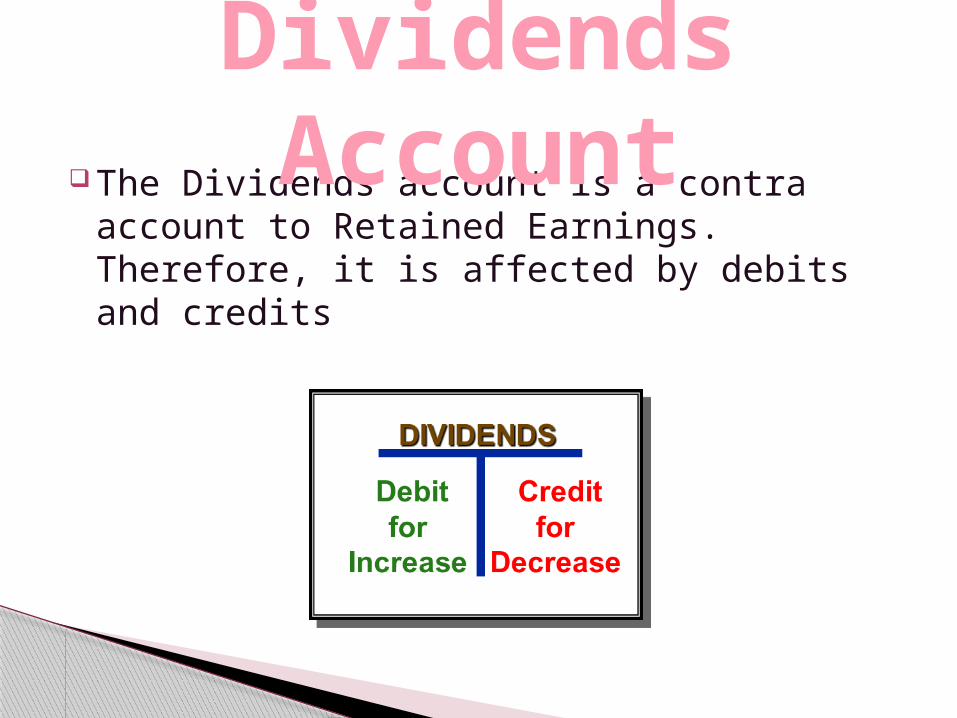

,Dividends Account

.

A general ledger contains the entire group of accounts maintained by a company. The general ledger includes all the asset, liability, owner’s equity, revenue and expense accounts.

The Dividends account is a contra account to Retained Earnings. Therefore, it is affected by debits and credits

Dividends Account

Question???