regional and bilateral trade agreements lance graef

TRANSCRIPT

Regional and Bilateral Trade Agreements

Lance Graefwww.nathaninc.com

22

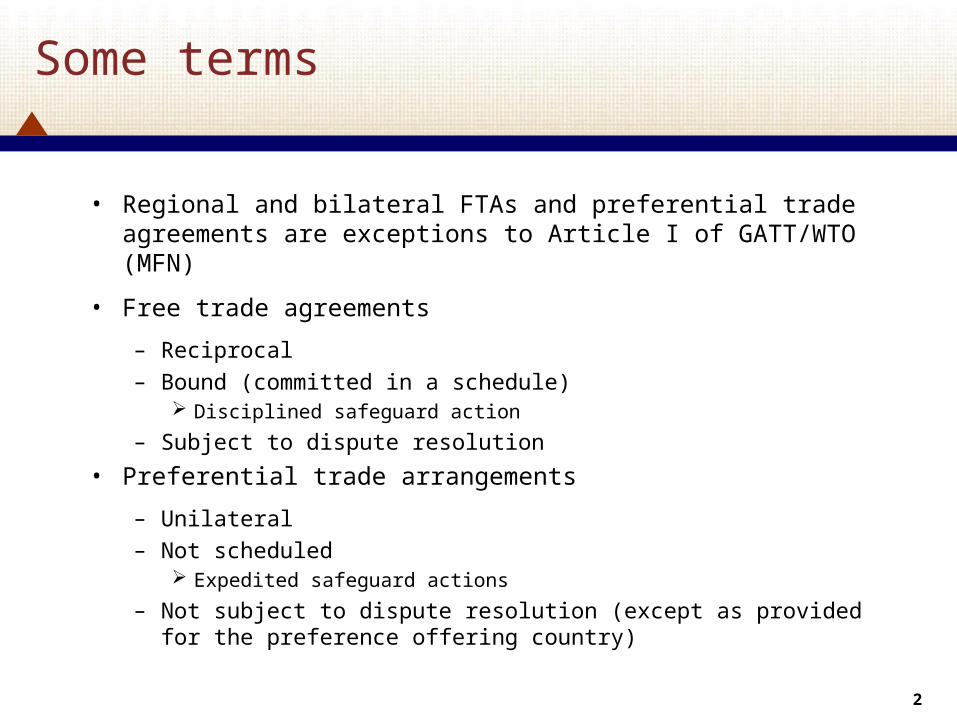

Some terms

• Regional and bilateral FTAs and preferential trade agreements are exceptions to Article I of GATT/WTO (MFN)

• Free trade agreements

– Reciprocal

– Bound (committed in a schedule) Disciplined safeguard action

– Subject to dispute resolution

• Preferential trade arrangements

– Unilateral

– Not scheduled Expedited safeguard actions

– Not subject to dispute resolution (except as provided for the preference offering country)

33

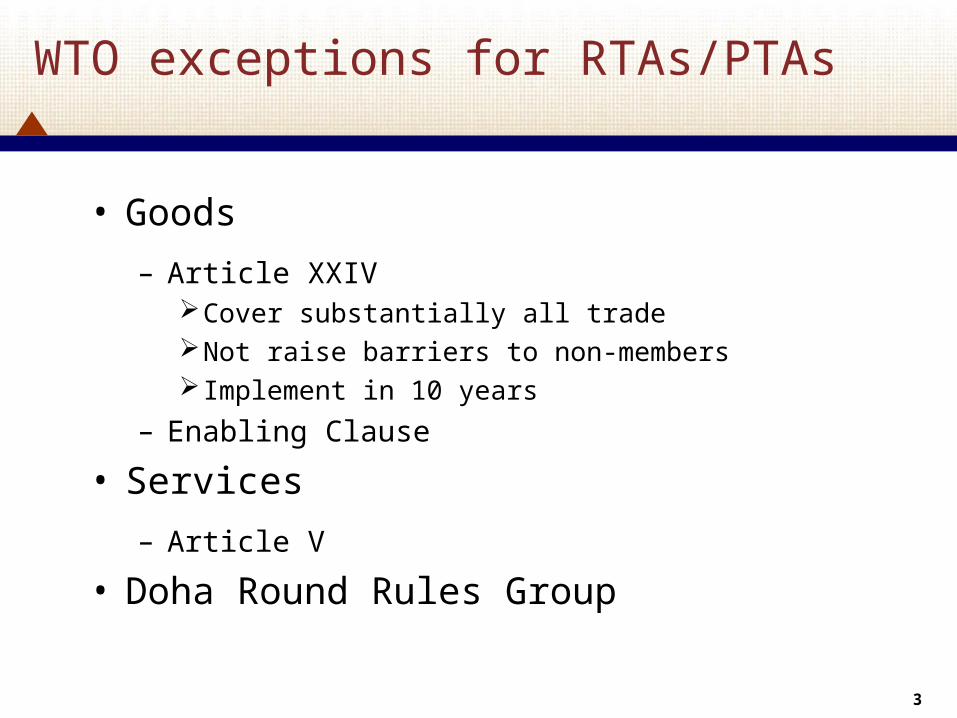

WTO exceptions for RTAs/PTAs

• Goods

– Article XXIVCover substantially all tradeNot raise barriers to non-members Implement in 10 years

– Enabling Clause

• Services

– Article V

• Doha Round Rules Group

44

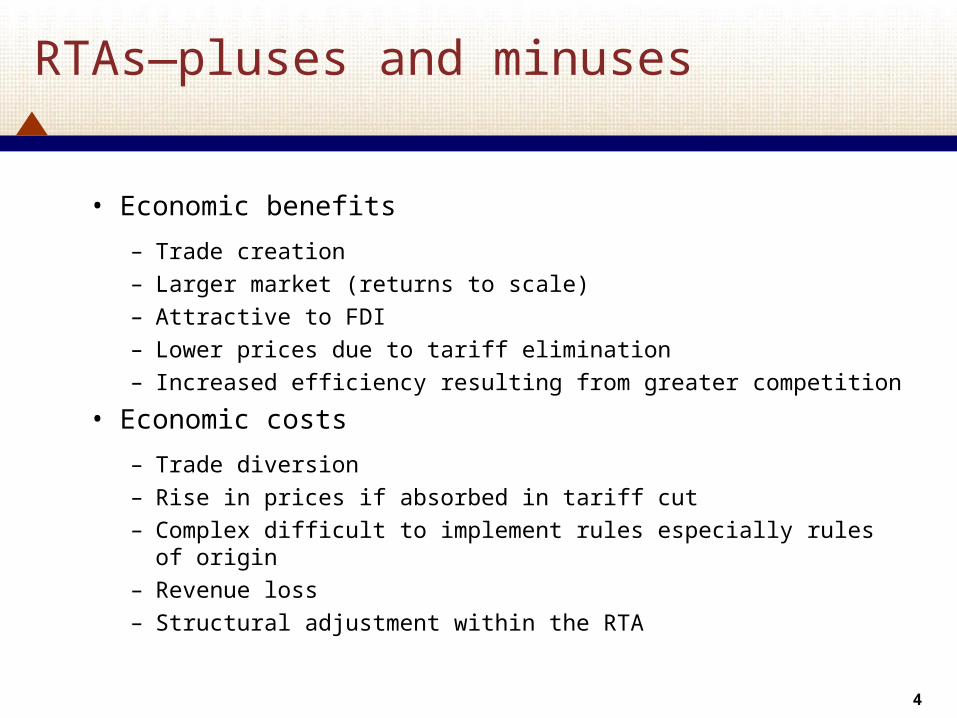

RTAs—pluses and minuses

• Economic benefits

– Trade creation– Larger market (returns to scale)– Attractive to FDI

– Lower prices due to tariff elimination

– Increased efficiency resulting from greater competition

• Economic costs

– Trade diversion

– Rise in prices if absorbed in tariff cut– Complex difficult to implement rules especially rules of origin

– Revenue loss

– Structural adjustment within the RTA

55

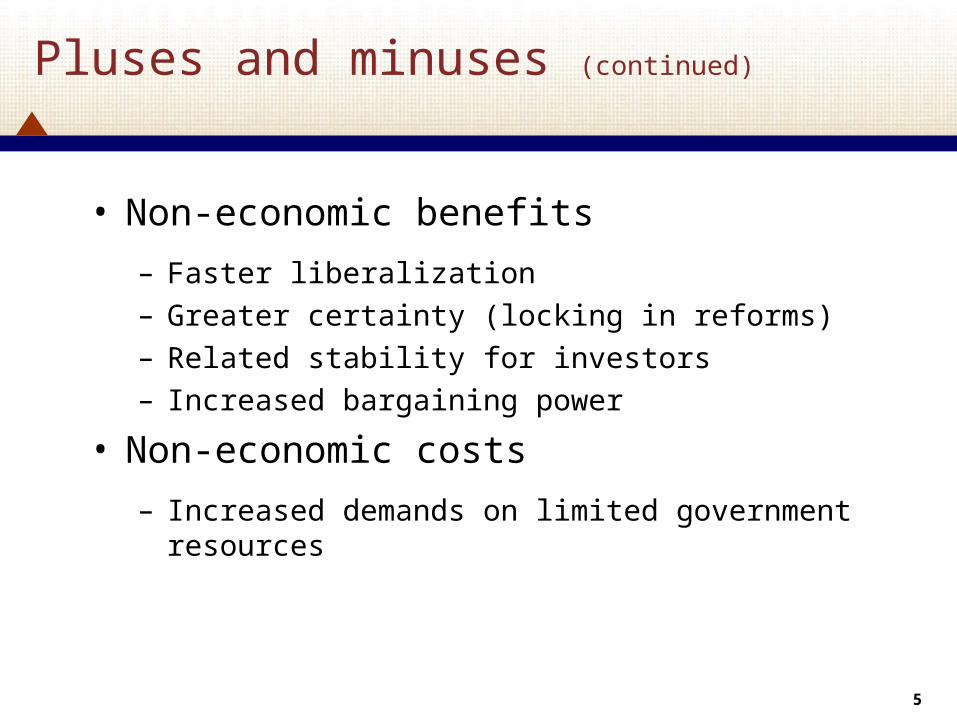

Pluses and minuses (continued)

• Non-economic benefits

– Faster liberalization

– Greater certainty (locking in reforms)

– Related stability for investors

– Increased bargaining power

• Non-economic costs

– Increased demands on limited government resources

66

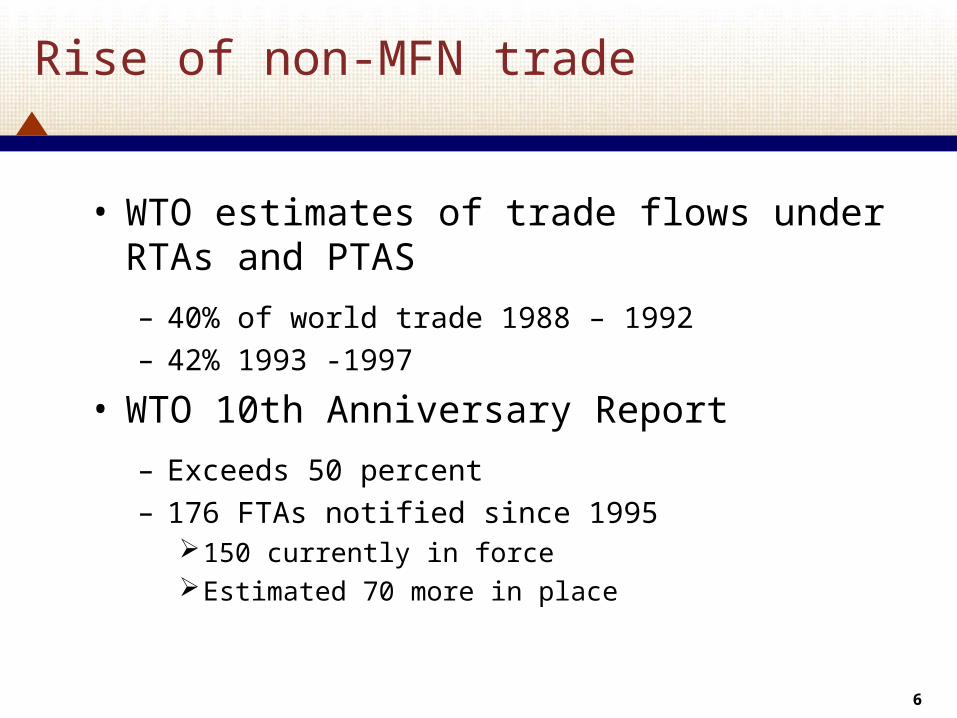

Rise of non-MFN trade

• WTO estimates of trade flows under RTAs and PTAS

– 40% of world trade 1988 – 1992

– 42% 1993 -1997

• WTO 10th Anniversary Report

– Exceeds 50 percent

– 176 FTAs notified since 1995150 currently in forceEstimated 70 more in place

77

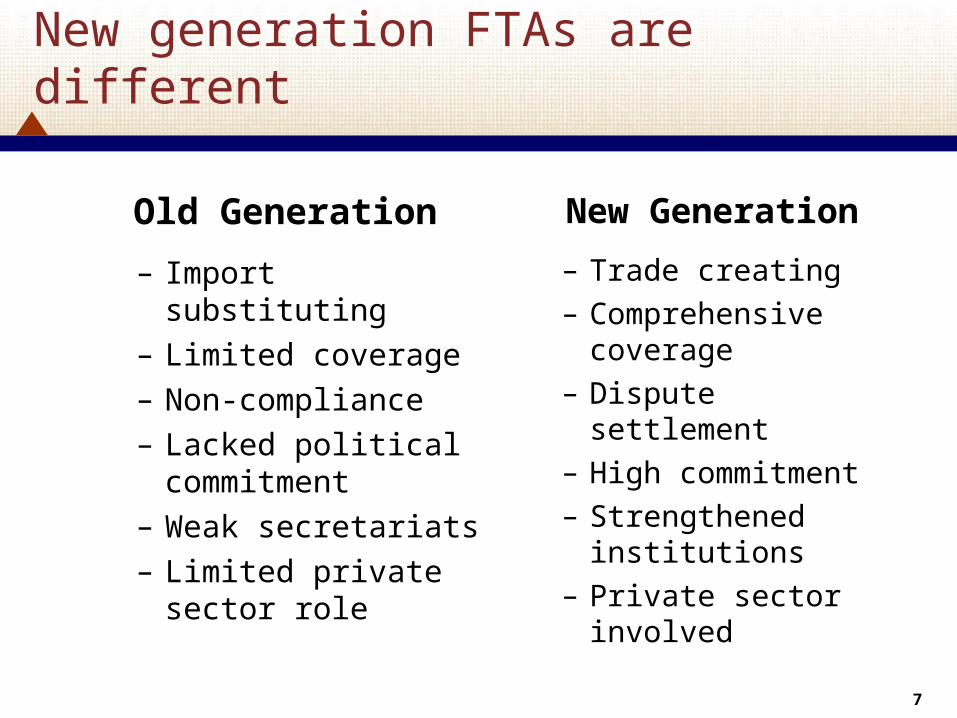

New generation FTAs are different

Old Generation

– Import substituting– Limited coverage– Non-compliance– Lacked political

commitment– Weak secretariats– Limited private sector

role

New Generation

– Trade creating– Comprehensive

coverage– Dispute settlement– High commitment– Strengthened

institutions– Private sector

involved

88

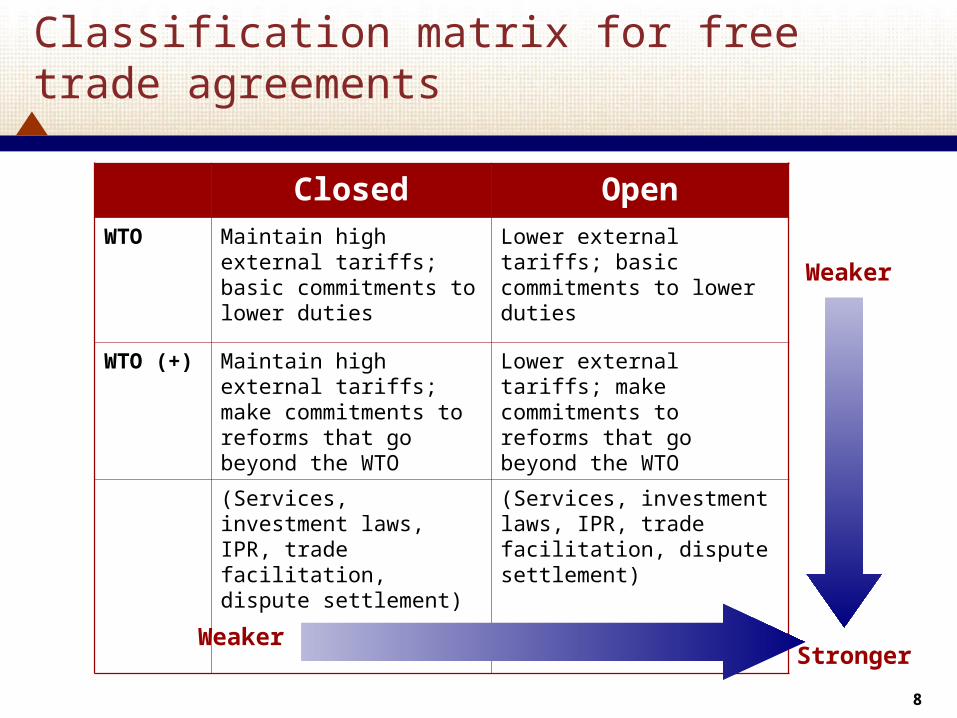

Classification matrix for free trade agreements

Closed OpenWTO Maintain high external

tariffs; basic commitments to lower duties

Lower external tariffs; basic commitments to lower duties

WTO (+) Maintain high external tariffs; make commitments to reforms that go beyond the WTO

Lower external tariffs; make commitments to reforms that go beyond the WTO

(Services, investment laws, IPR, trade facilitation, dispute settlement)

(Services, investment laws, IPR, trade facilitation, dispute settlement)

WeakerStronger

Weaker

99

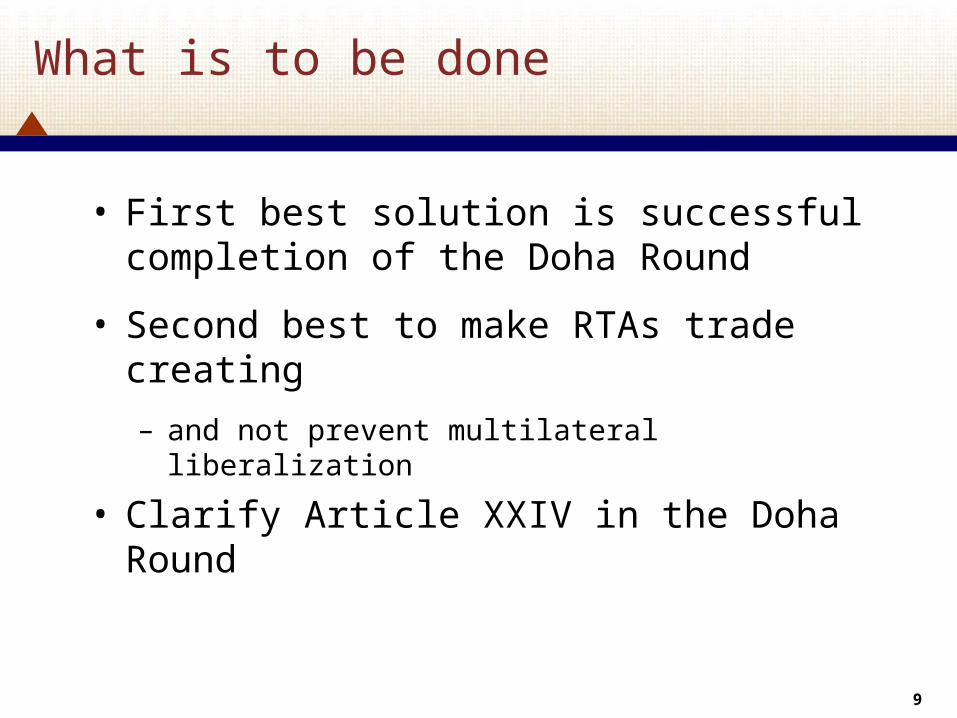

What is to be done

• First best solution is successful completion of the Doha Round

• Second best to make RTAs trade creating

– and not prevent multilateral liberalization

• Clarify Article XXIV in the Doha Round

Trends in Mozambique’s Trade with SADC—the Agenda

1111

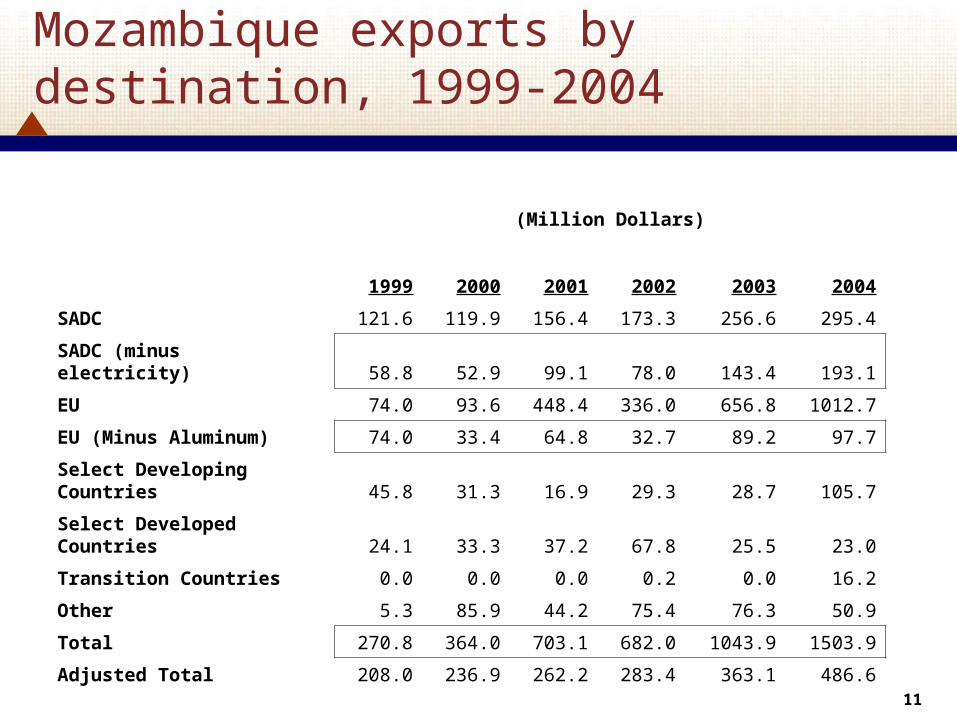

Mozambique exports by destination, 1999-2004

(Million Dollars)

1999 2000 2001 2002 2003 2004

SADC 121.6 119.9 156.4 173.3 256.6 295.4

SADC (minus electricity) 58.8 52.9 99.1 78.0 143.4 193.1

EU 74.0 93.6 448.4 336.0 656.8 1012.7

EU (Minus Aluminum) 74.0 33.4 64.8 32.7 89.2 97.7

Select Developing Countries 45.8 31.3 16.9 29.3 28.7 105.7

Select Developed Countries 24.1 33.3 37.2 67.8 25.5 23.0

Transition Countries 0.0 0.0 0.0 0.2 0.0 16.2

Other 5.3 85.9 44.2 75.4 76.3 50.9

Total 270.8 364.0 703.1 682.0 1043.9 1503.9

Adjusted Total 208.0 236.9 262.2 283.4 363.1 486.6

Source:INE

1212

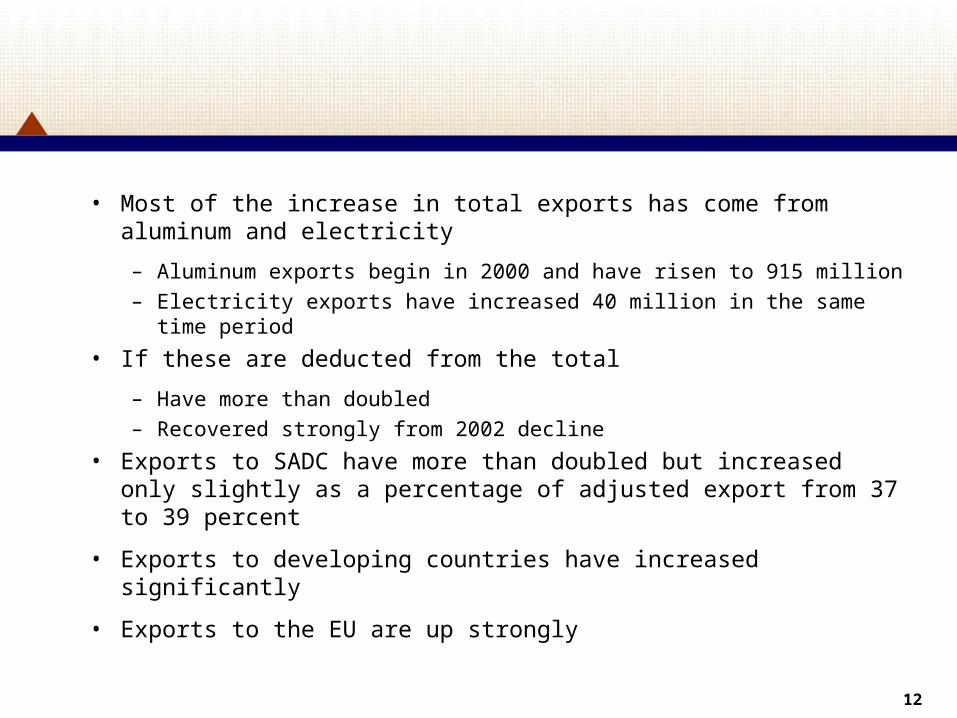

• Most of the increase in total exports has come from aluminum and electricity

– Aluminum exports begin in 2000 and have risen to 915 million

– Electricity exports have increased 40 million in the same time period

• If these are deducted from the total

– Have more than doubled

– Recovered strongly from 2002 decline

• Exports to SADC have more than doubled but increased only slightly as a percentage of adjusted export from 37 to 39 percent

• Exports to developing countries have increased significantly

• Exports to the EU are up strongly

1313

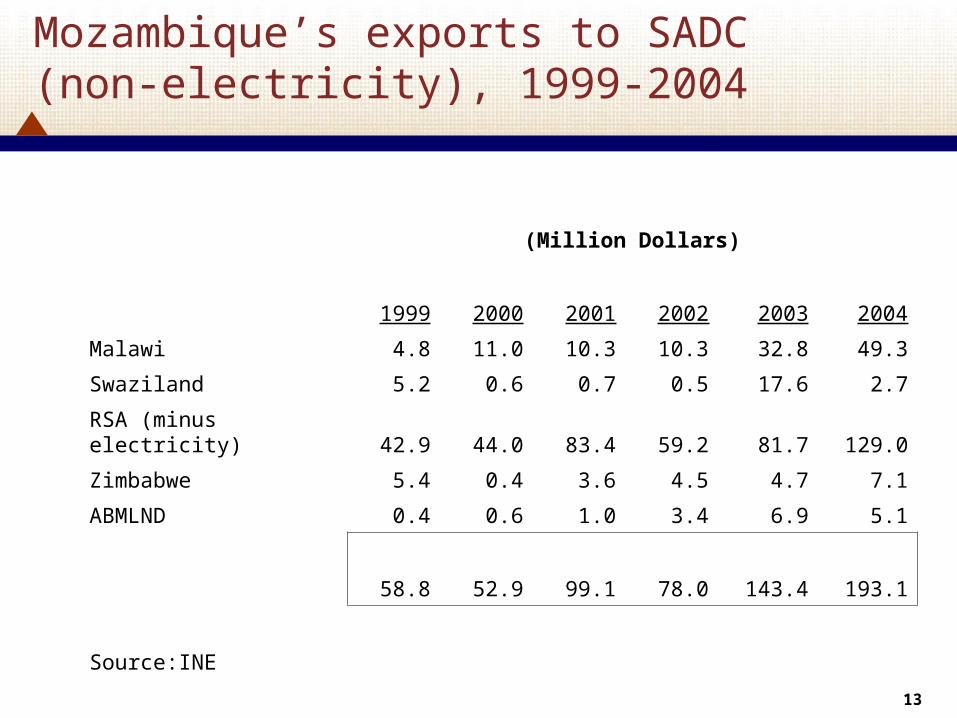

Mozambique’s exports to SADC (non-electricity), 1999-2004

(Million Dollars)

1999 2000 2001 2002 2003 2004

Malawi 4.8 11.0 10.3 10.3 32.8 49.3

Swaziland 5.2 0.6 0.7 0.5 17.6 2.7

RSA (minus electricity) 42.9 44.0 83.4 59.2 81.7 129.0

Zimbabwe 5.4 0.4 3.6 4.5 4.7 7.1

ABMLND 0.4 0.6 1.0 3.4 6.9 5.1

58.8 52.9 99.1 78.0 143.4 193.1

Source:INE

1414

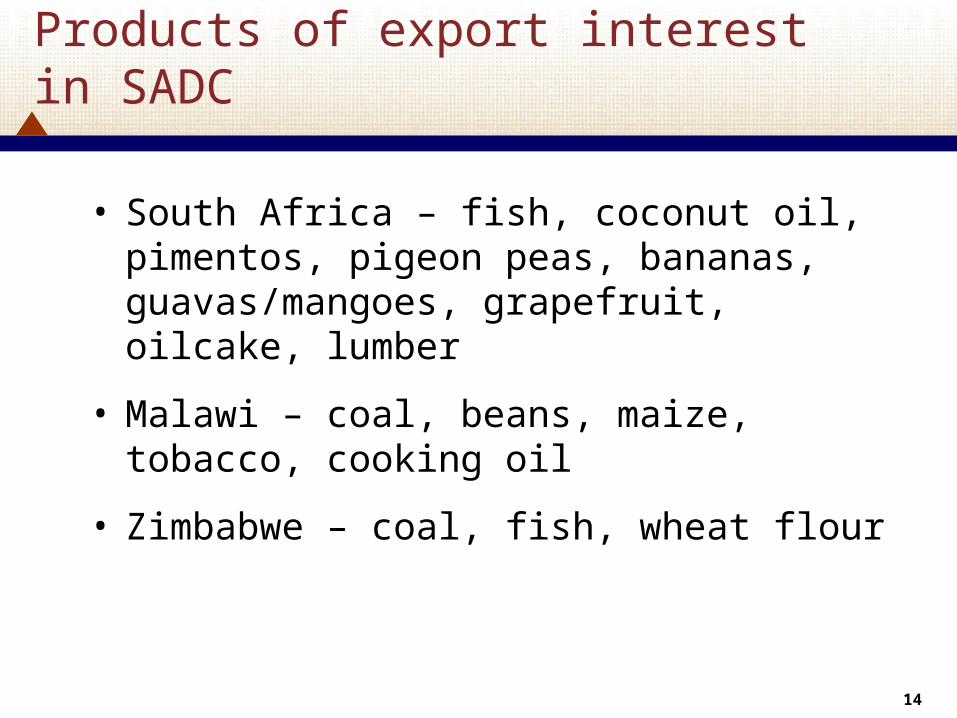

Products of export interest in SADC

• South Africa – fish, coconut oil, pimentos, pigeon peas, bananas, guavas/mangoes, grapefruit, oilcake, lumber

• Malawi – coal, beans, maize, tobacco, cooking oil

• Zimbabwe – coal, fish, wheat flour

1515

Disappointments

• Declines in some traditional exports

– Tires, apparel, wood products

• Expected non-traditional exports have not appeared

– Footwear

– Recorded agricultural trade with Malawi

– Sugar to SADC

1616

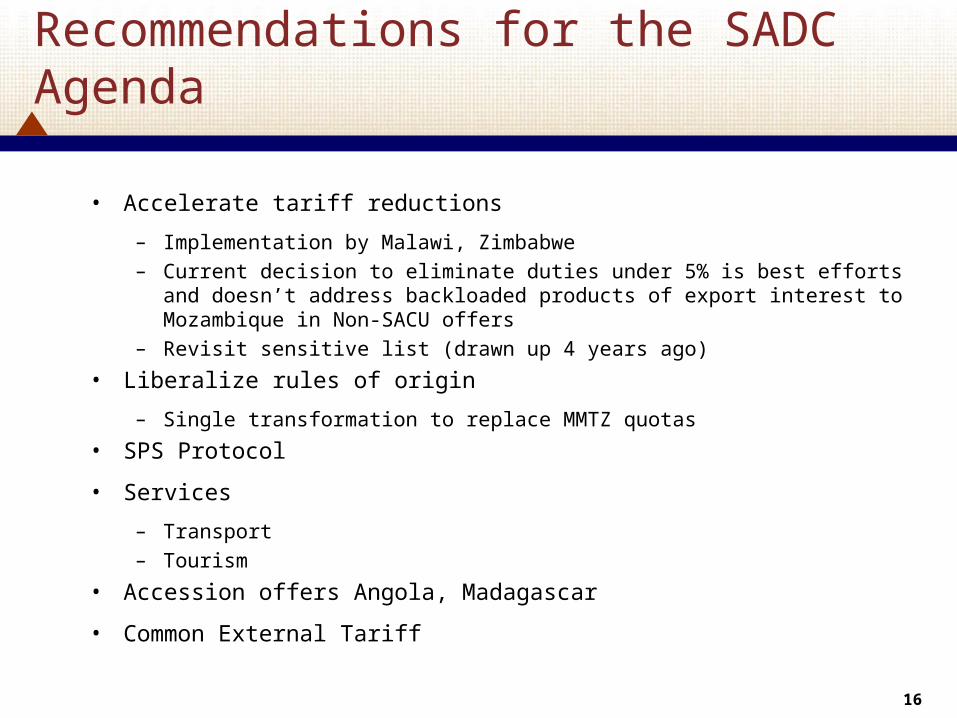

Recommendations for the SADC Agenda

• Accelerate tariff reductions

– Implementation by Malawi, Zimbabwe– Current decision to eliminate duties under 5% is best efforts and doesn’t

address backloaded products of export interest to Mozambique in Non-SACU offers

– Revisit sensitive list (drawn up 4 years ago)

• Liberalize rules of origin

– Single transformation to replace MMTZ quotas

• SPS Protocol

• Services

– Transport– Tourism

• Accession offers Angola, Madagascar

• Common External Tariff

1717

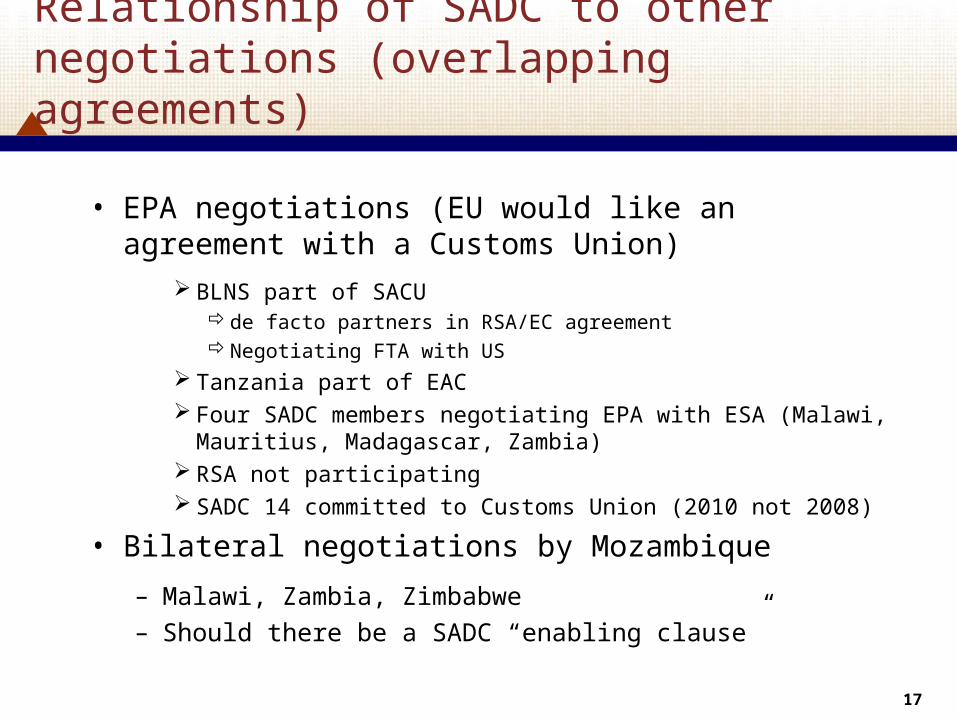

Relationship of SADC to other negotiations (overlapping agreements)

• EPA negotiations (EU would like an agreement with a Customs Union)

BLNS part of SACU de facto partners in RSA/EC agreementNegotiating FTA with US

Tanzania part of EAC Four SADC members negotiating EPA with ESA (Malawi, Mauritius,

Madagascar, Zambia) RSA not participating SADC 14 committed to Customs Union (2010 not 2008)

• Bilateral negotiations by Mozambique

– Malawi, Zambia, Zimbabwe

– Should there be a SADC “enabling clause”

Economic Partnership Agreement

1919

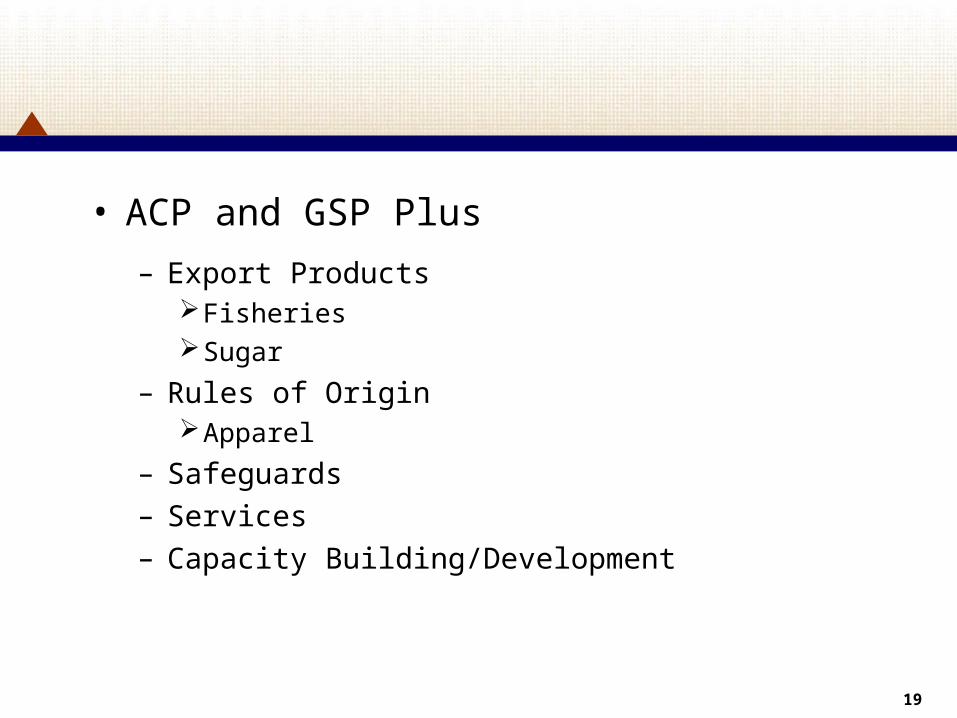

• ACP and GSP Plus

– Export ProductsFisheriesSugar

– Rules of OriginApparel

– Safeguards

– Services

– Capacity Building/Development

2020

Relationship to other negotiations and events

• ESA EPA negotiations include SADC partners

• SADC Customs Union

• GSP/EBA Reform in EU

– Still an option to withdraw

2121

Mozambique’s assignment

• Negotiating strategy for non-agricultural and fisheries market access

Export Trade

2323

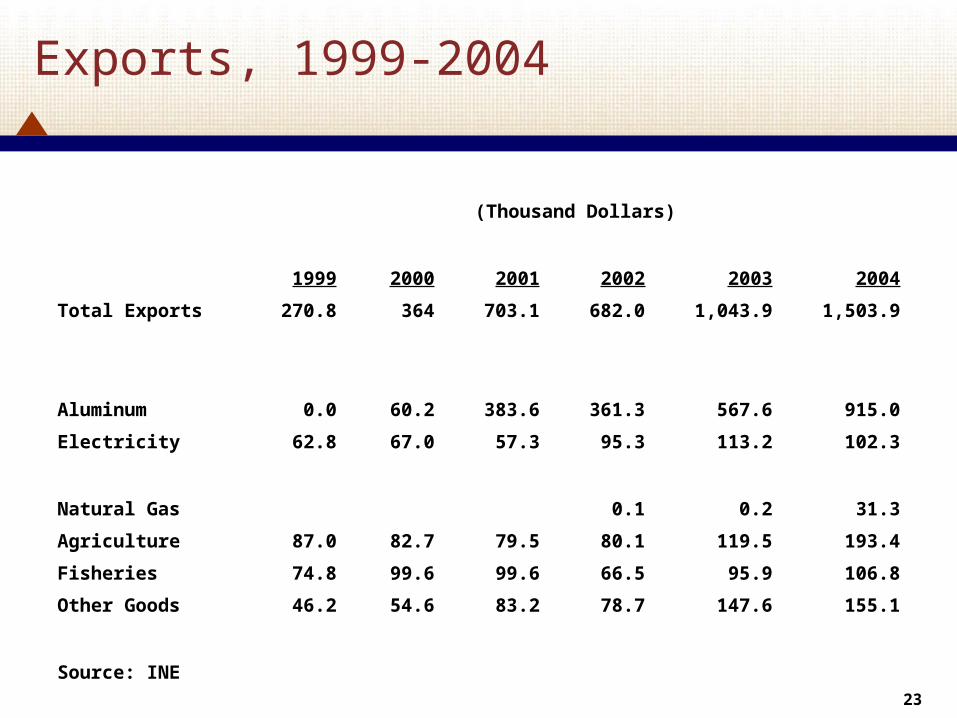

Exports, 1999-2004

(Thousand Dollars)

1999 2000 2001 2002 2003 2004

Total Exports 270.8 364 703.1 682.0 1,043.9 1,503.9

Aluminum 0.0 60.2 383.6 361.3 567.6 915.0

Electricity 62.8 67.0 57.3 95.3 113.2 102.3

Natural Gas 0.1 0.2 31.3

Agriculture 87.0 82.7 79.5 80.1 119.5 193.4

Fisheries 74.8 99.6 99.6 66.5 95.9 106.8

Other Goods 46.2 54.6 83.2 78.7 147.6 155.1

Source: INE

Preferential Arrangements—GSP, EBA, AGOA

2525

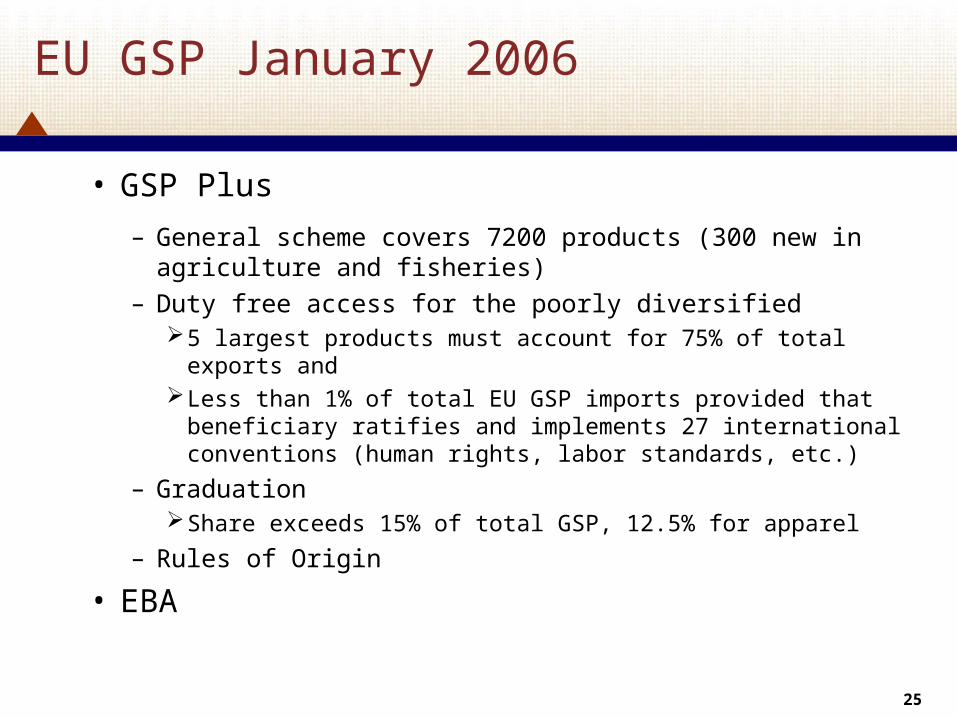

EU GSP January 2006

• GSP Plus

– General scheme covers 7200 products (300 new in agriculture and fisheries)

– Duty free access for the poorly diversified5 largest products must account for 75% of total exports andLess than 1% of total EU GSP imports provided that beneficiary

ratifies and implements 27 international conventions (human rights, labor standards, etc.)

– GraduationShare exceeds 15% of total GSP, 12.5% for apparel

– Rules of Origin

• EBA

2626

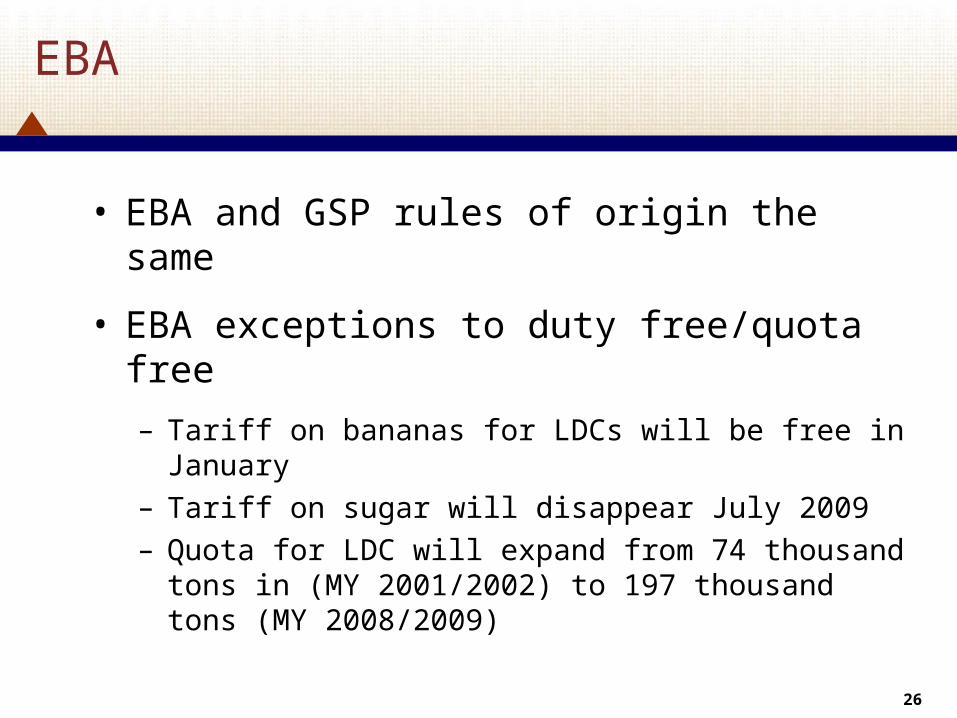

EBA

• EBA and GSP rules of origin the same

• EBA exceptions to duty free/quota free

– Tariff on bananas for LDCs will be free in January

– Tariff on sugar will disappear July 2009

– Quota for LDC will expand from 74 thousand tons in (MY 2001/2002) to 197 thousand tons (MY 2008/2009)

2727

AGOA

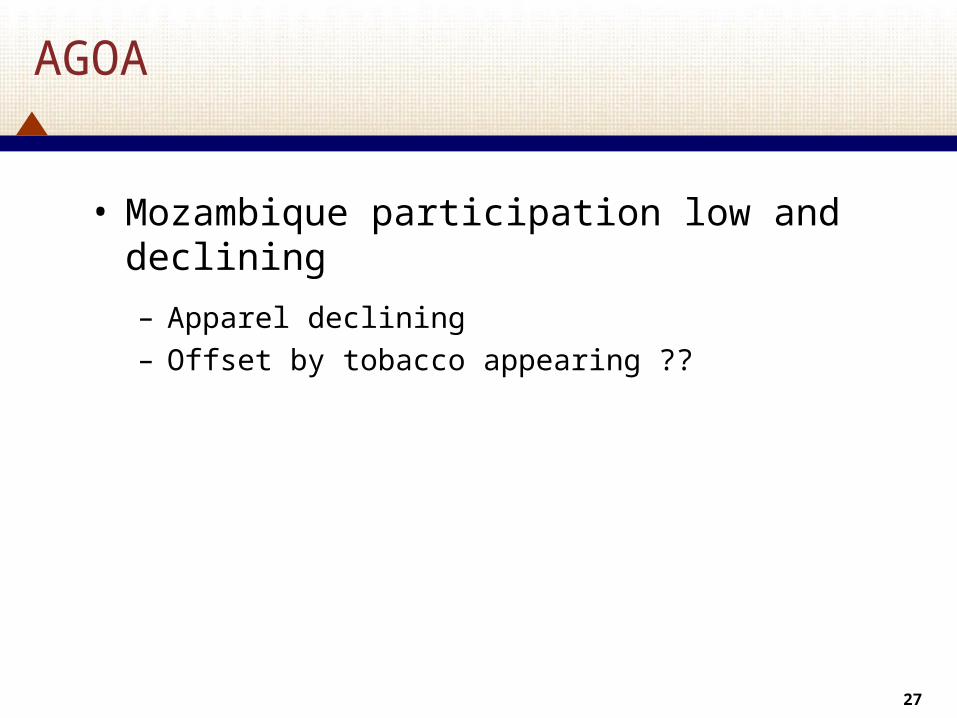

• Mozambique participation low and declining

– Apparel declining

– Offset by tobacco appearing ??

Exports, Destinations, and WTO Negotiations

2929

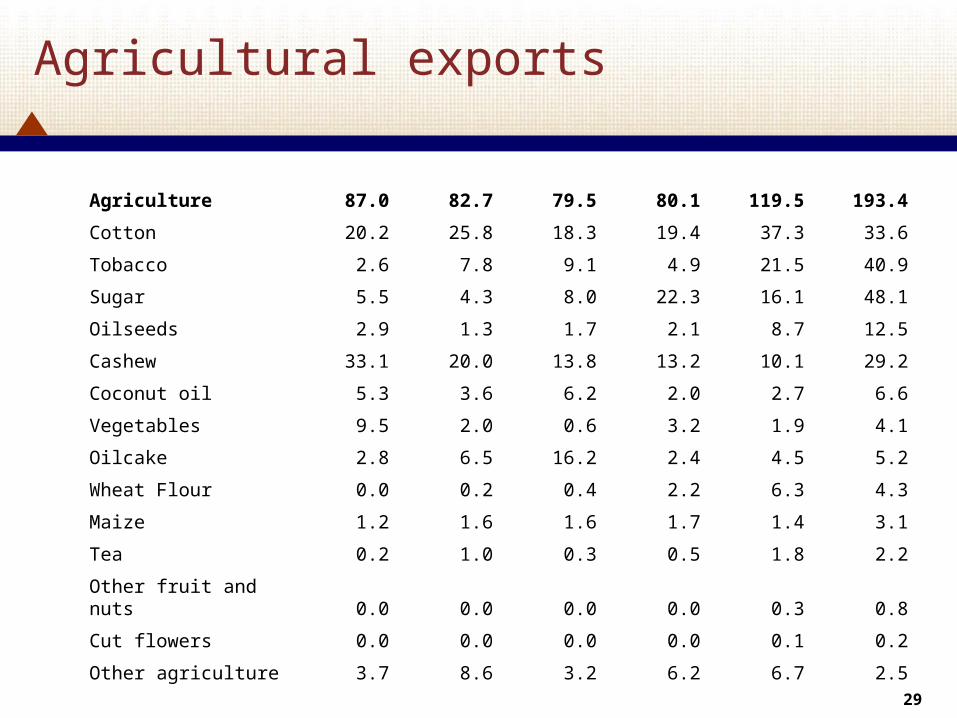

Agricultural exports

Agriculture 87.0 82.7 79.5 80.1 119.5 193.4

Cotton 20.2 25.8 18.3 19.4 37.3 33.6

Tobacco 2.6 7.8 9.1 4.9 21.5 40.9

Sugar 5.5 4.3 8.0 22.3 16.1 48.1

Oilseeds 2.9 1.3 1.7 2.1 8.7 12.5

Cashew 33.1 20.0 13.8 13.2 10.1 29.2

Coconut oil 5.3 3.6 6.2 2.0 2.7 6.6

Vegetables 9.5 2.0 0.6 3.2 1.9 4.1

Oilcake 2.8 6.5 16.2 2.4 4.5 5.2

Wheat Flour 0.0 0.2 0.4 2.2 6.3 4.3

Maize 1.2 1.6 1.6 1.7 1.4 3.1

Tea 0.2 1.0 0.3 0.5 1.8 2.2

Other fruit and nuts 0.0 0.0 0.0 0.0 0.3 0.8

Cut flowers 0.0 0.0 0.0 0.0 0.1 0.2

Other agriculture 3.7 8.6 3.2 6.2 6.7 2.5

3030

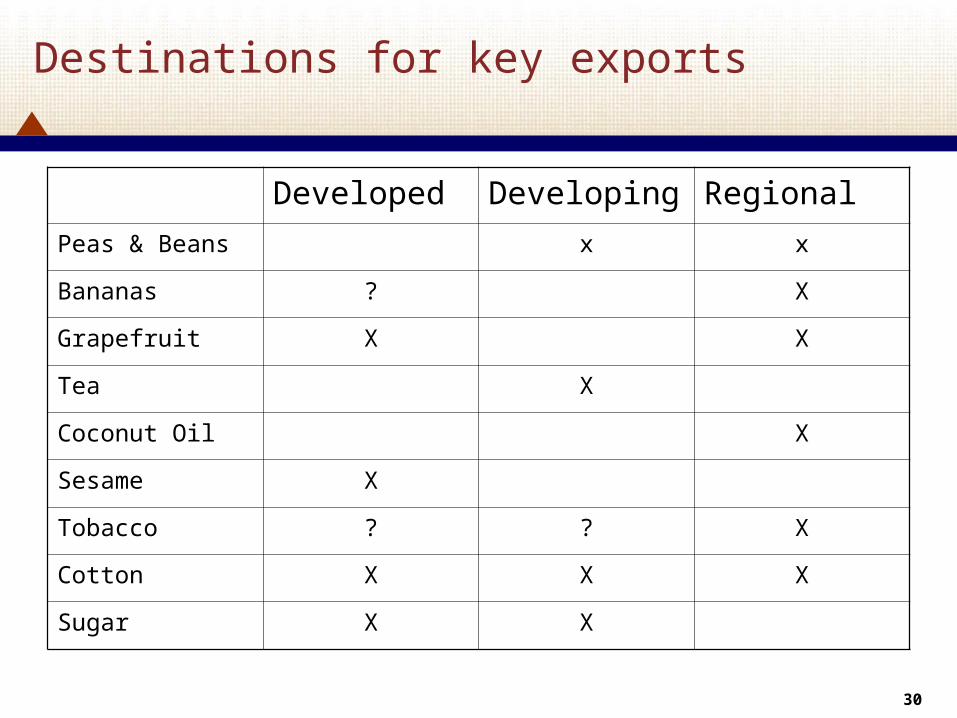

Destinations for key exports

Developed Developing Regional

Peas & Beans x x

Bananas ? X

Grapefruit X X

Tea X

Coconut Oil X

Sesame X

Tobacco ? ? X

Cotton X X X

Sugar X X

3131

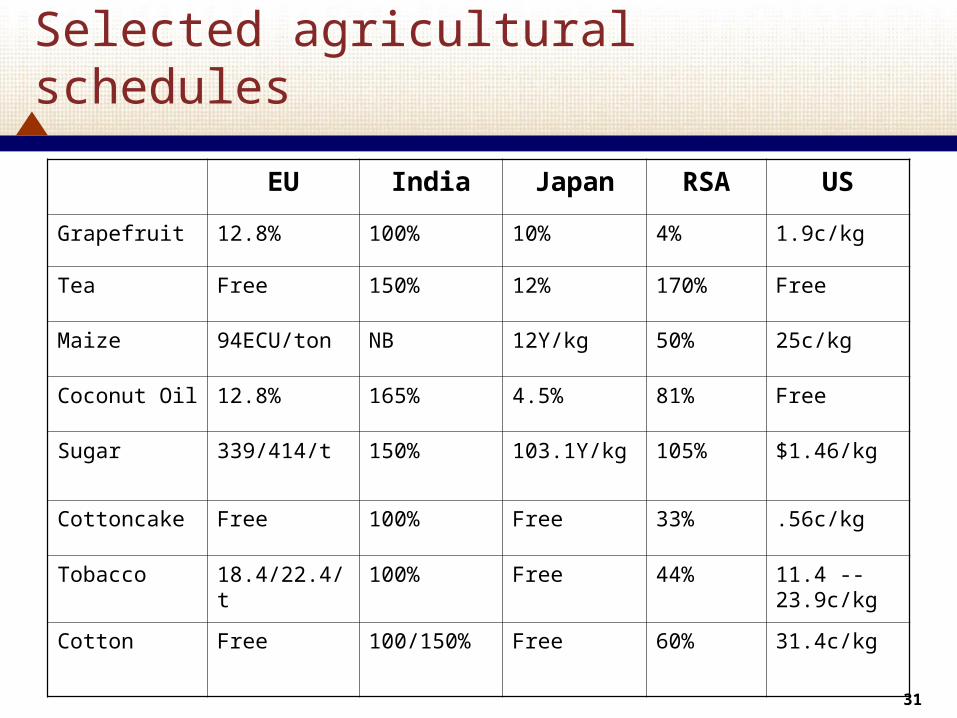

Selected agricultural schedules

EU India Japan RSA US

Grapefruit 12.8% 100% 10% 4% 1.9c/kg

Tea Free 150% 12% 170% Free

Maize 94ECU/ton NB 12Y/kg 50% 25c/kg

Coconut Oil 12.8% 165% 4.5% 81% Free

Sugar 339/414/t 150% 103.1Y/kg 105% $1.46/kg

Cottoncake Free 100% Free 33% .56c/kg

Tobacco 18.4/22.4/t 100% Free 44% 11.4 --23.9c/kg

Cotton Free 100/150% Free 60% 31.4c/kg

3232

WTO negotiations on agriculture

• Three Pillars

– Market Access High levels of tariffied products

Minimum market access (TRQs)

– Domestic Support Not addressed in RTAs

– Export Subsidies

• Development Dimension

– Cotton– Flexibilities for developing countries– Special and differential treatment for LDCs

Reserve portion of expansion of TRQs for LDCs, especially new supplier LDCs

3333

Exports of non-agricultural goods

Fisheries 74.8 99.6 99.6 66.5 95.9 106.8

Prawns 64.6 91.2 90.2 63.7 75.7 91.7

Other seafood 10.2 8.4 9.4 2.8 20.1 15.1

Other Goods 46.2 54.6 83.2 78.7 147.6 155.1

Wood 9.2 14.3 12.3 17.4 16.0 30.4

unprocessed 7.0 10.8 8.7 14.0 11.0 23.5

processed 2.2 3.5 3.6 3.4 5.0 6.9

Apparel 5.8 6.7 18.1 6.0 13.5 3.9

Coal 0.5 0.4 0.8 0.1 0.5 2.5

Steel containers/cables 0.3 0.4 3.5 0.6 1.0 2.3

3434

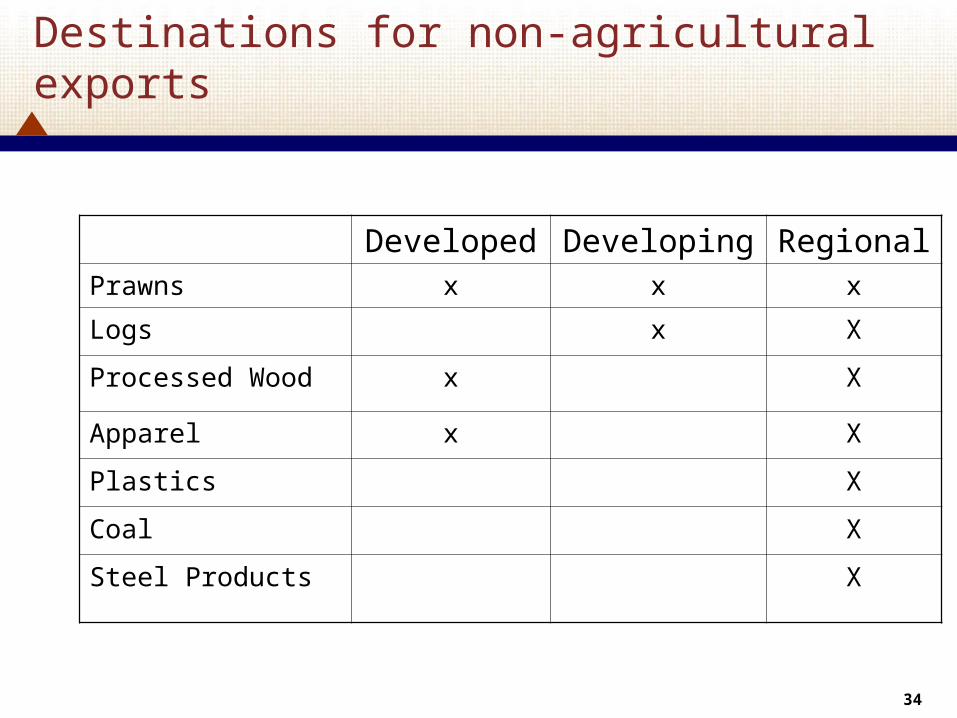

Destinations for non-agricultural exports

Developed Developing RegionalPrawns x x x

Logs x X

Processed Wood x X

Apparel x X

Plastics X

Coal X

Steel Products X

3535

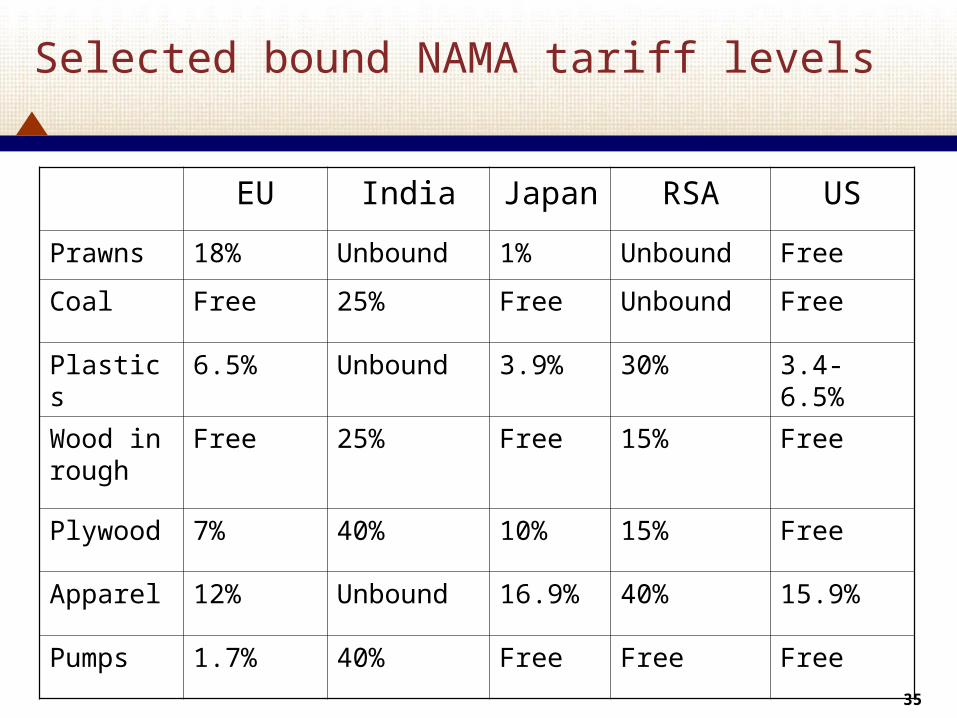

Selected bound NAMA tariff levels

EU India Japan RSA US

Prawns 18% Unbound 1% Unbound Free

Coal Free 25% Free Unbound Free

Plastics 6.5% Unbound 3.9% 30% 3.4-6.5%

Wood in rough

Free 25% Free 15% Free

Plywood 7% 40% 10% 15% Free

Apparel 12% Unbound 16.9% 40% 15.9%

Pumps 1.7% 40% Free Free Free

3636

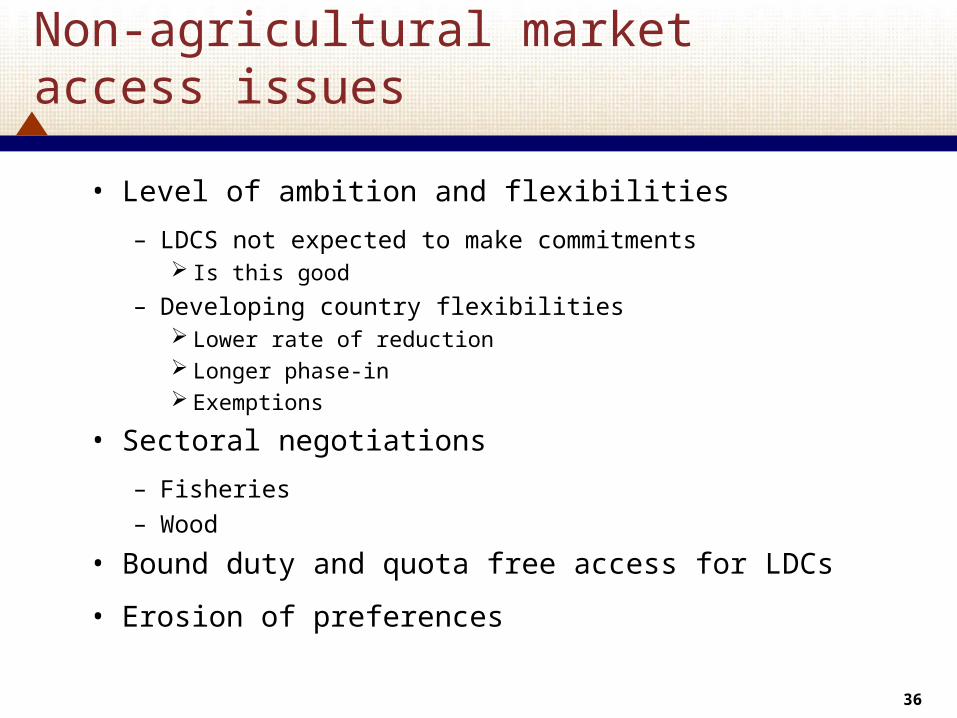

Non-agricultural market access issues

• Level of ambition and flexibilities

– LDCS not expected to make commitments Is this good

– Developing country flexibilities Lower rate of reduction Longer phase-in Exemptions

• Sectoral negotiations

– Fisheries– Wood

• Bound duty and quota free access for LDCs

• Erosion of preferences

3737

Other WTO interests

• Services

– Tourism

– Telecommunications

– Other reforms ???

3838

Why trade facilitation?

• Increase in competitive position

– Equivalent of reducing tariff on inputs between 26.5 points

• Increase in transparency equals increase in predictability

– Uniform application of procedures/regulations– Advance ruling

• Improved investment environment

• Facilitation measures already widely used

– Especially in Asia

3939

Trade facilitation mandate

• Clarify and improve GATT to expedite the movement, release and clearance of goods

– Article V Transit

– Article VIII Fees and Formalities

– Article X Transparency

• Enhance technical assistance/capacity building

– During Negotiations

– Post-Negotiations

• Establish provisions for effective cooperation between customs and other appropriate authorities

• Facilitation issues

• Compliance issues

4040

Trade facilitation mandate (continued)

• Special and Differential Treatment

– Developing countries and LDCs separate

– LDC’s consistent with administrative/institutional capabilities

• Take into account implementation capacities

• Including investment in infrastructure

• Negotiations required to address concerns related to cost implications of proposed measures

4141

All concepts are not new

• Transparency (concepts in the Agreement on Rules of Origin)

– Notification and Publication

– Advance Rulings

– Appeals

4242

Trade facilitation

• Other important proposals/concepts

– Fees and charges

– Reduction in procedures/formalities

– Expedited release in goods Pre-arrival clearances Risk management Post-clearance audits

• Regional agreements

• Transit