regional materials - maybank2u.com · the upside is weak iron ore prices/costs. china’s exports...

TRANSCRIPT

March 9, 2015

Regio

nal

SEC

TO

R R

ESEA

RC

H |

SEE PAGE 23 FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATIONS

Regional Materials

Gems, Picks & Shovels

Material Headlines Clean air in China by 2020? Thermal coal consumption fell in

2014 – the first YoY decrease in 10 years. Targets for thermal power and coal point to low growth and some declines ahead – good for the air quality but not for coal companies (IHS, MKE).

China’s weak steel demand and rising exports pose a threat to

regional steel producers (Japan Iron & Steel Federation) – but

the upside is weak iron ore prices/costs. China’s exports of

finished steel in Jan 2015 reached 10.29mt, a new all-time

high, up 1.2% from Dec and 52% YoY. New capacity in higher-

value markets is exceeding demand growth.

Supply side rebalancing and improving market sentiment have lifted copper prices 9% to USD2.69/lb from the late Jan low. The same can’t be said of nickel where China continues to find nickel units to offset those lost from the Indonesian ore ban.

Total nickel ore inventories at China’s five major ports were 11.8mt last week, up 65kt from the level on Feb. 13 (Shanghai Metals Market). While down from a high of about 20mt one year ago, inventory has been roughly stable since 3Q14.

The earnings season for mining stocks in HK/China kicks off this week with MMG on March 11. Several companies have provided downside warnings ahead of full results with consensus numbers falling by the day. Further downgrades are expected (MKE).

Impact on Stock Recommendations

We look for low but improving global demand growth. Soft materials prices reflect supply imbalances, with higher U.S. int. rates particularly negative for gold. Our 1 BUY in HK/China is copper growth play MMG (1208 HK; HKD2.22; BUY; TP HKD2.80).

We have 5 SELLs (3 coal, 2 steel/metals), incl. Shenhua (1088 HK; HKD19.18; SELL), which recently warned of a 10% fall in coal volumes in 2015 YoY. We look for earnings to decrease for a third consecutive year in 2015 (-20% YoY; report link below).

Our regional analyst’s top picks are nickel plays Nickel Asia (NIKL PM; PHP28.75; BUY; TP PHP51.94) and Vale Indonesia (INCO IJ; IDR3,445; BUY; TP IDR4,600). For exposure to India infrastructure we like L&T (LT IN; IDR1,862; BUY; TP IDR1,967).

Recent reports Aneka Tambang – Earnings and TP adjustments (3/2/15)

Philex Mining – Waiting for copper price recovery (3/2/15)

Vale Indonesia –Position for nickel price rally (2/27/15)

China Shenhua – D/G to contrarian sell on weak EPS (2/24/15)

Indonesia Coal – Another tax (2/24/15)

Tambang Batubara Bukit Asam – Lower target price (2/6/15)

China Mining – Tough 2015: Grab yield, growth (2/10/15)

Analyst

HK/CHINA Alexander Latzer (metals, coal, steel) Regional Sector Head INDIA Anubhav Gupta (metals, steel) INDONESIA Isnaputra Iskandar, CFA (metals, coal, cement) PHILIPPINES Ramon Adviento (metals, coal) (Full materials team details on page 2)

LME copper price and inventory

Source: Bloomberg.

LME nickel price and inventory

Source: Bloomberg.

Bottom falls out on Chinese steel prices

Source: Steelhome, Bloomberg.

2.25

2.50

2.75

3.00

3.25

3.50

0

200

400

600

800

1,000

Aug-1

3

Oct-

13

Dec-1

3

Feb-1

4

Apr-

14

Jun-1

4

Aug-1

4

Oct-

14

Dec-1

4

Feb-1

5

Inventory (LHS, '000 t)

Price (RHS, USD/lb)

6

7

8

9

10

120

200

280

360

440

Aug-1

3

Oct-

13

Dec-1

3

Feb-1

4

Apr-

14

Jun-1

4

Aug-1

4

Oct-

14

Dec-1

4

Feb-1

5

Inventory (LHS, '000 t)

Price (RHS, US$/lb)

2,500

3,000

3,500

4,000

4,500

0

50

100

150

200

一月

…

三月

…

五月

…

七月

…

九月

…

十一

…

一月

…

三月

…

五月

…

七月

…

九月

…

十一

…

一月

…

三月

…

Iron ore (LHS)

Rebar price China (RHS)

HRC price China (RHS)USD/t CNY/t

March 9, 2015 2

Regional Materials

Our views on the materials news

Clean air in China by 2020? Thermal coal consumption fell in 2014 –

the first YoY decrease in 10 years. Targets for thermal power and coal point to low growth and some further declines ahead – good for the air quality but not for coal companies (IHS CCM, MKE).

China’s Industrial Technology and Finance Ministries are preparing a blueprint to enhance clean and efficient use of coal products in industrial sectors (50% of the coal demand) outside of power generation (the other 50%), which if fully enacted could cut coal consumption by about 160mt by 2020 (-1%/year) (China Stocks).

What’s Our View?

The Chinese government has formalized plans to reduce the share of

thermal power in the total energy mix, posing great challenges for coal

miners and thermal power generators. We see total coal consumption

growth slowing to 0-2%/year through 2020 with some years negative such

as last year (Fig. 1). We expect more sector M&A with the large SOEs

being strongly encouraged to take the lead in restricting output.

China plans to cap coal consumption at 4.2 bt/year by 2020 vs. 3.61 bt in

2013 with the share of power generation falling to 62% from 73% in 2011,

and 66% in 2014. The plan for thermal power generation (50% of coal

demand in China) caps the coal burn at all new thermal units at 300

g/kWh, similar to those at gas-fired units.

Existing thermal units with capacity of more than 600 MW will have to

upgrade within five years to cut their consumption to less than 300 g/kWh

by 2020 from an average burn of 321 g/kWh in 2013. We calculate this

could reduce total coal consumption in China by over 1%/year by 2020.

Overall, thermal power operating rates are expected to continue to fall.

Similarly, railway capacity additions are expected to eliminate the

bottleneck so prevalent in prior years. With investment levels remaining

high in the sector (USD142b in 2014), total coal railing capacity is

expected to approach 3bt/year, up 50% from 2010. While capacity is being

expanded, coal deliveries have slowed with last year’s total of 2.29bt

down 1.3% YoY. Growth rates averaged from 7-10% from 2006-2010 but

have slowed to a rate of 2-4% prior to last year.

Figure 1: China total raw coal supply and demand outlook

Raw Coal (million tons) 2005 2010 2011 2012 2013 2014A 2015E 2016E 2017E 2018E 2019E 2020E

Production 2,113 3,240 3,519 3,660 3,690 3,600 3,645 3,718 3,792 3,849 3,907 3,965 Incremental Prod 157 190 279 141 30 37 45 73 74 57 58 59 Incremental Prod (%) 8.0% 6.2% 8.6% 4.0% 0.8% -2.4% 1.3% 2.0% 2.0% 1.5% 1.5% 1.5% Export 72 18 15 9 7 5 4 3 3 4 5 6 Import 26 165 183 289 327 292 273 278 285 292 300 307 Net Export (Import) 46 -147 -169 -280 -319 -287 -269 -275 -282 -288 -295 -301 Inventory (total EOY) 140 223 313 347 312 323 293 274 275 279 285 292 Inventory change 36 51 91 34 -35 11 -30 -19 2 4 6 8 Days of supply (total inv.) 25 24 32 32 28 30 27 25 25 25 25 25 Domestic Consumption 2,031 3,336 3,597 3,906 4,044 3,876 3,943 4,013 4,073 4,134 4,196 4,259 Incremental Cons (Mt) 137 166 262 309 138 -169 68 69 60 61 62 63 Incremental Cons (%) 7.2% 5.3% 7.8% 8.6% 3.5% -4.2% 1.8% 1.8% 1.5% 1.5% 1.5% 1.5%

Qinhuangdao coal price (CNY/t)* 424.3 779.4 898.6 744.0 616.8 553.5 537.2 540.1 530.6 534.0 534.0 534.0 USD/t ex-VAT (Rmb appreciation lifts L.T. price) 44.3 98.5 118.8 100.8 85.7 76.8 74.4 76.0 75.6 76.1 76.1 76.1 % chg. YoY CNY price -5.0% 23.6% 15.3% -17.2% -17.1% -10.3% -2.9% 0.5% -1.8% 0.6% 0.0% 0.0%

Source: McCloskey, CCTD, Maybank Kim Eng forecasts.

Regional Materials Team

HK/CHINA Alexander Latzer (metals, coal, steel) (852) 2268 0647 [email protected]

INDIA Jigar Shah (cement, oil/gas) (91) 22 6623 2601 [email protected]

Anubhav Gupta (metals, steel) (91) 22 6623 2605 [email protected]

INDONESIA Isnaputra Iskandar, CFA (metals, coal, cement) (62) 21 2557 1129 [email protected]

MALAYSIA Lee Yen Ling (steel, building materials) (603) 2297 8691 [email protected]

PHILIPPINES Ramon Adviento (metals, coal) (63) 2 849 8845 [email protected]

Lovell Sarreal (cement, consumer, media) (63) 2 849 8841 [email protected]

SINGAPORE Yeak Chee Keong, CFA (oil/gas services, gem technology) (65) 6231 5842 [email protected]

THAILAND Sutthichai Kumworachai (coal, energy, oil/gas, petrochemical) (66) 2658 6300 x 1400 [email protected]

Surachai Pramualcharoenkit (steel, construction, contractors, automotive) (66) 2658 6300 x 1470 [email protected]

VIETNAM Trung Thai (construction, materials, property) (84) 444 55 58 88 x 8180 [email protected]

March 9, 2015 3

Regional Materials

China is also rolling out a carbon trading system, which should be fully

functional and active nationwide by 2020. Carbon trading started in 2011

under pilot programmes in Shenzhen, Beijing, Shanghai, Tianjin,

Guangdong, Hubei and Chongqing. The country is seeking to reduce its CO2

emissions by 40-45% by 2020 vs 2005 levels with carbon trading being seen

as an important driver when trading matures in 2020.

China’s steel demand is decreasing and its exports increasing, posing

a continuous threat to the export market share of regional steel

producers (Japan Iron & Steel Federation). China’s exports of

finished steel in Jan. 2015 reached 10.29mt, up 1.2% from

December and an increase of 52% YoY to a new all-time high.

What’s Our View?

Global steel prices have moved sharply lower over the past nine months

due to slowing demand growth, lower iron ore costs, and plentiful low-

priced exports (Fig 2). Operating rates have fallen industry wide, reflecting

the downturn in prices and profit margins. Perhaps the most reactive have

been producers in the US where operating rates have recently fallen to 70%

from a high of 80% before the price decrease.

Chinese steel producers ramped up output starting from 2Q14 in response

to improving profit margins on falling iron ore costs. As a result, prices

have fallen and profit margins shrunken during 2H from levels earlier last

year. Spare capacity remains high, with operating rates 72-75% (Fig. 3).

During 2014, China announced the closure of approximately 31mt of steel

capacity (3% of total capacity) as part of its industry rationalization drive

to reduce pollution, improve safety, and upgrade output. Chinese exports

hit a record in January, indicating more closures are needed.

Figure 2: Global steel prices (domestic hot rolled coil. China price is ex-VAT)

Source: Steelhome, SBB, AMM.

We would often hear Chinese steel industry participants complain that iron

ore costs were the main reason for low profit margins. However, our view

was that it was only part of the problem, the other being oversupply and

pricing discipline. In fact, when global growth was strong and iron ore

prices were close to peaking prior to the GFC, steel producers globally

more than passed through the increase. Global consumption supported

higher steel prices and the pass through of raw material costs.

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300USD/t China Europe US Japan Korea

March 9, 2015 4

Regional Materials

Chinese steel prices have fallen 35-38% since early 2013 (Fig. 4). During the

same period, regional Asia/Australia iron ore prices have fallen 59% and

coking coal prices 28%. Taking into consideration the cost mix of Chinese

steel producers (approximately 45% iron ore, 35% coking coal) raw material

prices have fallen on average by 36%. However, the fall in steel prices

impacts 100% of steel revenues but the fall in costs 80% in our example,

with the other 20% having moved higher (labour, regulatory, other

consumables). Overall, we look for supply pressures to remain high in

China, with exports forecast to decrease to 80mt in 2015 vs. 94mt in 2014,

and production to increase 1.5% with consumption flat to negative YoY.

Figure 3: Chinese crude steel production and oper. rates Figure 4: Chinese steel prices giving back iron ore cost gains

Source: CISA, Steelhome, MKE estimates. Source: Steelhome, Bloomberg.

We remain negative on the outlook for steel industry profitability in China

and see the rally in the shares during 2H14 as having run its course. The

collapse in profit margins should become apparent during 1Q15 results.

Sectors with priority spending by the government include railway and

energy, which should prove marginally beneficial to some of the related

niche players in those markets relative to other steel producers

(Maanshan; 323 HK; HKD2.18; HOLD) (Angang; 347 HK; HKD5.87; SELL).

92 94

100

96

93 94

91

87

79

82 81 79

76 78

73 72 72 72

70

75

80

85

90

95

100

0

200

400

600

800

1,000

1,200

1,400

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014A

2015E

2016E

2017E

% mt

Steel production (LHS) Steel capacity (LHS)

Utilization rate (RHS)

2,500

3,000

3,500

4,000

4,500

0

50

100

150

200

一月

13

二月

13

三月

13

四月

13

五月

13

六月

13

七月

13

八月

13

九月

13

十月

13

十一

月 1

3

十二

月 1

3

一月

14

二月

14

三月

14

四月

14

五月

14

六月

14

七月

14

八月

14

九月

14

十月

14

十一

月 1

4

十二

月 1

4

一月

15

二月

15

三月

15

Iron ore (LHS)Rebar price China (RHS)HRC price China (RHS)

USD/t CNY/t

March 9, 2015 5

Regional Materials

Supply side rebalancing and improving market sentiment have lifted copper prices by 9% to USD2.69/lb from the late Jan low. The same can’t be said of nickel where China continues to find nickel units to offset those lost from the Indonesian ore ban.

What’s Our View?

Supply side rebalancing appears to be progressing in the copper market,

helping to reduce the forecast market oversupply during 2015. Low prices

and production difficulties have helped to reduce supply growth by 150–

300kmt (1-2% of consumption). We had already incorporated supply

disruptions into our forecast of double that amount and as a result have

made no changes to our market forecast (Fig. 5).

Figure 5: Refined copper global and China production/consumption outlook

2010 2011 2012A 2013 2014 2015E 2016E 2017E

Global prod./cons.

Production 18,934 19,675 20,131 21,059 21,341 22,457 23,321 23,982

YoY chg. 3.6% 3.9% 2.3% 4.6% 1.3% 5.2% 3.8% 2.8%

Consumption 19,306 19,747 19,697 20,740 21,598 22,322 23,160 24,015

YoY chg. 11.2% 2.3% -0.3% 5.3% 4.1% 3.4% 3.8% 3.7%

Balance: surplus (deficit) (373) (72) 434 319 (257) 136 161 (33)

Total inventories 2,841 2,769 3,203 3,522 3,265 3,401 3,562 3,529

Weeks of supply 7.7 7.3 8.5 8.8 7.9 7.9 8.0 7.6

Price (USD/mt) $7,536 $8,835 $7,957 $7,335 $6,866 $5,842 $6,614 $7,165

Price (USD/lb) $3.42 $4.01 $3.61 $3.33 $3.11 $2.65 $3.00 $3.25

China prod./cons. Production 4,534 5,197 5,828 6,245 6,750 7,423 8,048 8,511

YoY chg. 10.3% 14.6% 12.2% 7.1% 8.1% 10.0% 8.4% 5.8%

Consumption 7,204 7,815 8,230 9,116 9,705 10,191 10,751 11,342

YoY chg. 10.8% 8.5% 5.3% 10.8% 6.5% 5.0% 5.5% 5.5%

Source: WMS, Wood Mackenzie, Bloomberg, BGRIMM, Maybank Kim Eng forecasts.

Despite our forecast slowdown in Chinese consumption growth to 5-6% the

next few years, the absolute growth in demand should slowly exert

pressure on existing and new supply growth. At roughly half of global

demand growth, China’s consumption requires at least one Las Bambas

project per year (approx.. 400kmt). Smaller mines must be developed to

achieve the same result, but are not being funded in the current

environment. Older mines are also facing disruptions and grade declines.

Figure 6: Refined copper consumption growth in China Figure 7: China copper consumption by end-use (2013E)

Source: WMS, Wood Mackenzie, BGRIMM, Maybank Kim Eng forecasts. Source: Wood Mackenzie, BGRIMM, Maybank Kim Eng forecasts.

0

2,000

4,000

6,000

8,000

10,000

12,000

-20%

-10%

0%

10%

20%

30%

40%

80 83 86 89 92 95 98 01 04 07 10 13A 16E

'000 t YoY chg. Consumption (RHS) YoY Chg. (LHS)

Power infra. 40%

Consumer appliance

22%

Building and construction

26%

Automotive 7%

Other 5%

March 9, 2015 6

Regional Materials

We believe our forecast for a slowly improving copper price is reasonable

in light of the fundamentals. The recent trends in copper (and nickel)

inventory and price show more time is needed for fundamental support to

build in order to lift prices. While copper prices have increased from the

recent low levels, inventory is rising both on the LME and Shanghai

exchanges, and is high at the China state level after purchases in 2014.

Figure 8: LME copper price and inventory Figure 9: LME nickel price and inventory

Source: Bloomberg. Source: Bloomberg.

Nickel price lacks upside catalyst

While the rate of increase in LME nickel inventory has slowed its

continuation has undermined market confidence and the metal price (Fig.

9). Prices have returned to low levels before Indonesia’s ore export ban.

We continue to look for a market deficit to appear later this year as China

draws down its nickel ore inventory. But the process has taken longer than

even our conservative forecast relative to market expectations. Closures of

nickel pig iron plants in China may help tighten the domestic market.

At these low price levels we believe there is more upside potential than

downside risk for the price. However, we acknowledge that the upside

catalyst remains elusive. Stainless steel demand growth globally remains

weak reflecting adequate industrial capacity to meet demand growth, and

consumer demand has slowed also.

Figure 10: Refined nickel global and China production/consumption outlook

2010 2011 2012A 2013 2014 2015E 2016E 2017E

Global prod./cons.

Production 1,509 1,585 1,792 1,952 1,991 2,010 2,063 2,157

YoY chg. 10% 5% 13% 9% 2% 1% 3% 5%

Consumption 1,542 1,595 1,674 1,786 1,923 2,023 2,116 2,178

YoY chg. 16% 3% 5% 7% 8% 5% 5% 3%

Balance: surplus (deficit) (33) (10) 117 166 68 (12) (53) (21)

Total inventories 325 322 369 562 663 651 597 576

Weeks of supply 11.0 10.5 11.5 16.4 17.9 16.7 14.7 13.8

Price (USD/mt) $21,814 $22,917 $17,538 $15,046 $16,882 $16,419 $18,739 $16,535

Price (USD/lb) 9.89 10.40 7.96 6.82 7.66 7.45 8.50 7.50

China prod./cons.

Production in all forms 390 490 550 710 670 620 589 598

YoY chg. 34% 26% 12% 29% -6% -7% -5% 1%

NPI Production 235 300 385 485 455 400 350 325

YoY chg. 34% 28% 28% 26% -6% -12% -13% -7%

Consumption 581 650 720 830 920 984 1,058 1,111

YoY chg. 20% 12% 11% 15% 11% 7% 8% 5%

Source: WMS, Wood Mackenzie, Bloomberg, SMM, Maybank Kim Eng forecasts.

2.25

2.50

2.75

3.00

3.25

3.50

0

200

400

600

800

1,000

Aug-1

3

Sep-1

3

Oct-

13

Nov-1

3

Dec-1

3

Jan-1

4

Feb-1

4

Mar-

14

Apr-

14

May-1

4

Jun-1

4

Jul-

14

Aug-1

4

Sep-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan-1

5

Feb-1

5

Inventory (LHS, '000 t) Price (RHS, USD/lb)

6.0

7.0

8.0

9.0

10.0

120

200

280

360

440

Aug-1

3

Sep-1

3

Oct-

13

Nov-1

3

Dec-1

3

Jan-1

4

Feb-1

4

Mar-

14

Apr-

14

May-1

4

Jun-1

4

Jul-

14

Aug-1

4

Sep-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan-1

5

Feb-1

5

Inventory (LHS, '000 t) Price (RHS, US$/lb)

March 9, 2015 7

Regional Materials

The key problem for nickel is that its major end-user, stainless steel

producers in China, have advanced metallurgical controls to the extent

that they can use a variety of non-pure nickel feed material to blend with

pure nickel to make the product. Copper is different in that its major uses

remain oriented towards the pure form of the material.

The availability of other nickel ores from the Philippines, ferro-nickel from

Asia, and nickel concentrate from Australia, have made up for the loss of

supply from the Indonesian nickel ore ban. A ban on the export of raw ores

from the Philippines would provide such a catalyst but thus far the

measure has not gained broad support making it unlikely to be

implemented anytime soon.

China’s push to close highly polluting obsolete capacity has reached into

the nickel pig iron market. Northeast China's Linyi city in Shandong

province shut nine nickel pig iron plants over February 26 to March 4 due

to environmental concerns, China Metallurgical Standardization Research

Institute reported recently. Shandong accounts for around 20% of China's

ferronickel production. This could be positive if it reduces domestic NPI

supply more than demand causing a need for additional nickel units.

Otherwise, it would simply be a closure of surplus obsolete capacity

without moving the market into deficit.

Earnings season for mining stocks in HK/China kicks off this week

with MMG on March 11. Several companies have provided downside

warnings ahead of full results with consensus numbers falling by the

day. Further downgrades are expected (MKE).

What’s Our View?

The low materials prices and structural changes underway in China are so

significant that we have been expecting to see a heavy impact on the

results of the materials companies. This factor and overly optimistic

consensus earnings forecasts have largely driven the negative bias to our

investment recommendations.

Further, the quality of earnings remains low. For example, we note that

very few Chinese companies have taken asset write-downs, despite

overseas acquisitions made at higher price levels. Unlike western

companies, Chinese corporates tend not to make timely adjustments to

book valuations preferring to await it out (Yanzhou Coal; 1171 HK; SELL;

Jiangxi Copper; 358 HK; HOLD; Zijin; 2899 HK; Not Rated).

Accounting changes have also led to longer asset lives that has reduced

non-cash charges for fixed assets and flattered net profit (steel

companies). Further, local governments have been providing subsidies on

power and taxes to help support struggling companies in coal and steel.

Asset sales at inflated valuations to state owned parent groups have also

boosted cash flow and reported net profit (Chalco; 2600 HK; SELL).

Most recently, Shenhua provided very weak 2015 business targets over CNY

that we believe are not fully incorporated into consensus estimates. These

included a 15% fall in revenues vs 11% in COGS YoY, and a 16% increase in

SG&A plus net finance costs.

Shenhua’s coal production and sales volumes were weak in Jan., down 4%

and 44% YoY, respectively. Coal sales have been weak after lengthy price

March 9, 2015 8

Regional Materials

negotiations between coal miners and power producers in light of above-

normal inventory levels and seasonally slowing demand.

Just this week, Shenhua rolled out a new policy enabling it to offer pricing

discounts of CNY27-37/t ($4.40-6.03/t) to users in eastern and southern

China for cargoes sourced from small producers and delivered to unloading

ports. The cuts are a reaction to Shenhua losing market share in the past

two months, when the company met the government’s request to stabilize

prices and offered no discounts in eastern and southern China.

High levels of investment among coal companies into the coal/chemicals

segment also raises questions about the expected long-run returns given

low energy prices, high capital and operating costs, and resource scarcity

(water). The CO2 emissions from the sector are also very high and seem

misaligned with the environmental targets that the Chinese government is

aggressively pursuing. Within our coverage China Coal continues to

allocate high levels of capex into coal/chemicals (1898 HK; SELL).

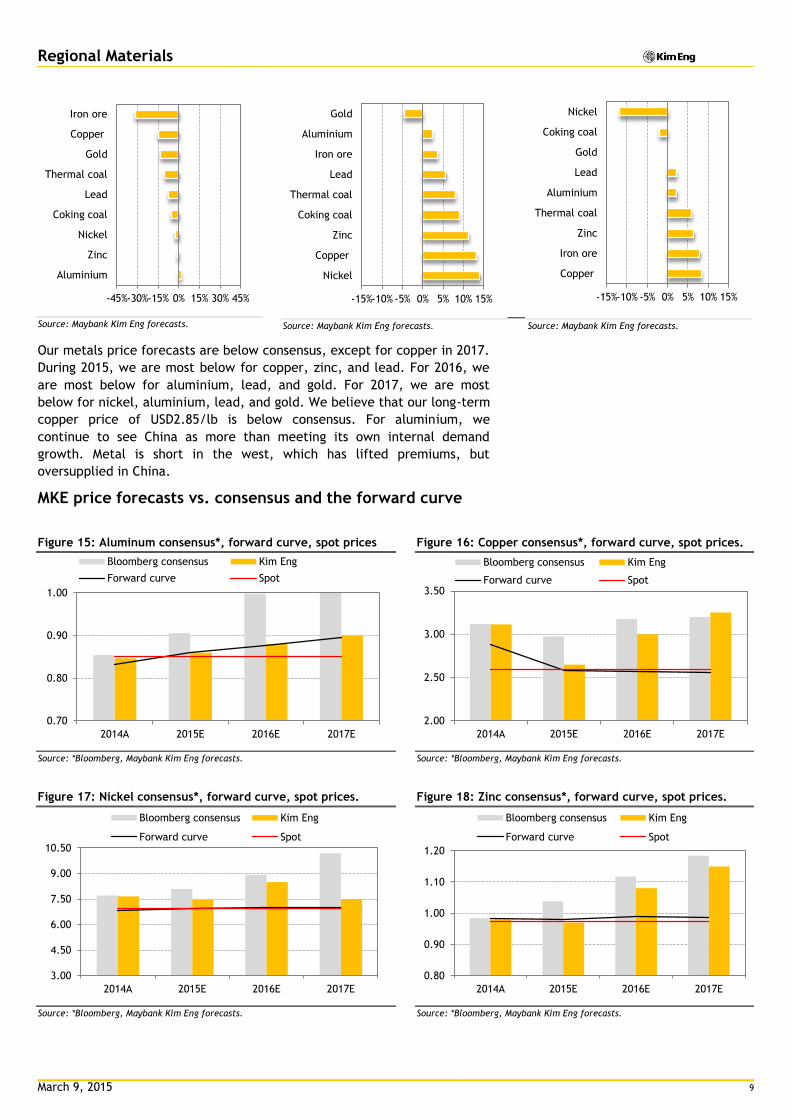

Metals price forecasts and rankings 2015-17

We see 2015 as a transition year that will be tough for higher cost mining

companies, particularly those in over-supplied sectors. Our recovery

outlook for 2016 is predicated on slowing supply and improving demand

growth. Our view of nickel is that the ore shortage is a two-year

phenomenon until the Chinese rebuild supply lines, hence the price

underperformance in 2017E. During 2017, we look for supply side cuts to

lift the prices for copper, iron ore, and zinc from low levels.

Figure 11: Metals price forecasts

(USD/lb., gold USD/oz.) 2013

2014A 2015E 2016E 2017E L-term

Aluminum 0.84 0.85 0.86 0.88 0.90 0.95 YoY chg. -9% 1% 2% 8% 2% 0% Copper 3.33 3.11 2.65 3.00 3.25 2.85 YoY chg. -8% -6% -15% 13% 8% -12% Nickel 6.82 7.66 7.45 8.50 7.50 7.00 YoY chg. -14% 12% -3% 14% -12% -7% Lead 0.97 0.95 0.88 0.93 0.95 0.88 YoY chg. 4% -2% -7% 6% 2% -7% Zinc 0.87 0.98 0.97 1.08 1.15 1.10 YoY chg. -2% 13% -1% 11% 6% -4% Gold 1,412 1,267 1,100 1,050 1,050 1,000 YoY chg. -15% -10% -13% -5% 0% -5% Source: Bloomberg, Maybank Kim Eng forecasts.

Figure 12: 2015 forecasts (YoY chg.) Figure 13: 2016 forecasts (YoY chg.) Figure 14: 2017 forecasts (YoY chg.)

March 9, 2015 9

Regional Materials

Source: Maybank Kim Eng forecasts. Source: Maybank Kim Eng forecasts. Source: Maybank Kim Eng forecasts.

Our metals price forecasts are below consensus, except for copper in 2017.

During 2015, we are most below for copper, zinc, and lead. For 2016, we

are most below for aluminium, lead, and gold. For 2017, we are most

below for nickel, aluminium, lead, and gold. We believe that our long-term

copper price of USD2.85/lb is below consensus. For aluminium, we

continue to see China as more than meeting its own internal demand

growth. Metal is short in the west, which has lifted premiums, but

oversupplied in China.

MKE price forecasts vs. consensus and the forward curve

Figure 15: Aluminum consensus*, forward curve, spot prices Figure 16: Copper consensus*, forward curve, spot prices.

Source: *Bloomberg, Maybank Kim Eng forecasts. Source: *Bloomberg, Maybank Kim Eng forecasts.

Figure 17: Nickel consensus*, forward curve, spot prices. Figure 18: Zinc consensus*, forward curve, spot prices.

Source: *Bloomberg, Maybank Kim Eng forecasts. Source: *Bloomberg, Maybank Kim Eng forecasts.

-45%-30%-15% 0% 15% 30% 45%

Aluminium

Zinc

Nickel

Coking coal

Lead

Thermal coal

Gold

Copper

Iron ore

-15%-10% -5% 0% 5% 10% 15%

Nickel

Copper

Zinc

Coking coal

Thermal coal

Lead

Iron ore

Aluminium

Gold

-15%-10% -5% 0% 5% 10% 15%

Copper

Iron ore

Zinc

Thermal coal

Aluminium

Lead

Gold

Coking coal

Nickel

0.70

0.80

0.90

1.00

2014A 2015E 2016E 2017E

Bloomberg consensus Kim Eng

Forward curve Spot

2.00

2.50

3.00

3.50

2014A 2015E 2016E 2017E

Bloomberg consensus Kim Eng

Forward curve Spot

3.00

4.50

6.00

7.50

9.00

10.50

2014A 2015E 2016E 2017E

Bloomberg consensus Kim Eng

Forward curve Spot

0.80

0.90

1.00

1.10

1.20

2014A 2015E 2016E 2017E

Bloomberg consensus Kim Eng

Forward curve Spot

March 9, 2015 10

Regional Materials

Figure 19: Lead: consensus*, forward curve, spot prices. Figure 20: Gold consensus*, forward curve, spot prices.

Source: *Bloomberg, Maybank Kim Eng forecasts. Source: *Bloomberg, Maybank Kim Eng forecasts.

0.70

0.80

0.90

1.00

1.10

1.20

2014A 2015E 2016E 2017E

Bloomberg consensus Kim Eng

Forward curve Spot

600

900

1,200

1,500

2014A 2015E 2016E 2017E

Bloomberg consensus Kim Eng

Forward curve Spot

March 9, 2015 11

Regional Materials

APPENDIX: Valuation comps. materials, coal, and steel (EV/EBITDA, P/BV, EBITDA margin, ROE) (Source: Bloomberg Consensus data)

Figure 21: Metals & Mining EV/EBITDA 2015 (x) Figure 22: Metals & Mining P/BV 2015 (x)

Source: Bloomberg consensus Source: Bloomberg consensus

2.4

3.1

3.6

3.9

4.1

4.2

4.5

4.5

4.6

4.7

4.8

4.8

4.9

5.0

5.0

5.3

5.4

5.4

5.6

5.6

5.8

5.8

5.9

5.9

6.1

6.3

6.3

6.4

6.5

6.7

6.7

6.9

7.0

7.1

7.3

7.3

7.3

8.3

8.4

8.7

9.0

9.5

9.7

10.0

10.3

10.6

11.1

11.4

12.4

12.8

16.2

19.4

0.0 5.0 10.0 15.0 20.0 25.0

Oz Minerals

Pan Aust

Hongqiao

China Vanadium…

Kinross

Goldfields

Atlas Minerals

Freeport McMoRan

Harmony

Nickel Asia

PT Inco

Lonmin

Sesa Sterlite

Anglogold

Anglo American

Vale (Brazil)

Teck Resources

First Quantum

Korea Zinc

Norsk Hydro

Rio Tinto

Press Metals

Antofagasta

Vedanta

Alcoa

Chinalco Mining

Iluka

Yamana

Barrick Gold

BHP Billiton

Amplats

MMG

Hindalco

Newmont

Glencore Xstrata

Cliffs Natural Res.

Fortescue Metals

Newcrest Mining

United Co Rusal

Agnico-eagle

Goldcorp

ERA

Polyus Gold

Lynas

Philex

Jiangxi Copper

Paladin Energy

Zhaojin Mining

Aneka Tambang

Zijin Mining

Mitsubishi

Chalco

0.3

0.4

0.4

0.4

0.5

0.5

0.6

0.6

0.6

0.6

0.6

0.6

0.7

0.7

0.7

0.7

0.7

0.7

0.7

0.7

0.8

0.8

0.8

0.9

0.9

0.9

1.0

1.1

1.1

1.1

1.1

1.2

1.2

1.2

1.2

1.3

1.3

1.3

1.3

1.4

1.4

1.4

1.5

1.5

1.5

1.6

1.6

1.7

2.0

2.2

2.6

2.6

2.7

3.0

3.7

6.1

0.0 2.0 4.0 6.0 8.0

Molycorp

Harmony

Lonmin

Lingbao Gold

Yamana

Oz Minerals

Teck Resources

Kinross

Lynas

Pan Aust

MMG

First Quantum

Mitsubishi

Vale (Brazil)

Hindalco

Buenaventura

Glencore Xstrata

Vedanta

Hongqiao

Jiangxi Copper

Anglo American

Aneka Tambang

Sesa Sterlite

Paladin Energy

Goldfields

Goldcorp

Freeport McMoRan

Norsk Hydro

Chalco

Atlas Minerals

Newmont

Newcrest Mining

Zhaojin Mining

Barrick Gold

Alcoa

Zijin Mining

China Molybdenum

Korea Zinc

Alumina

ERA

PT Inco

Anglogold

United Co Rusal

Press Metals

Agnico-eagle

Amplats

Antofagasta

Philex

Iluka

Polyus Gold

Rio Tinto

Chinalco Mining

Norilsk Nickel

Nickel Asia

BHP Billiton

Fortescue Metals

March 9, 2015 12

Regional Materials

Figure 23: Metals & Mining EBITDA margin 2015 (%) Figure 24: Metals & Mining ROE 2015 (%)

Source: Bloomberg consensus Source: Bloomberg consensus

2.6 2.9

4.2

5.1

6.1

6.4

11.1

11.9

12.5

14.9

15.6

17.6

17.7

17.8

18.2

18.7

18.8

19.2

24.4

25.0

26.1

28.0

28.4

28.5

28.9

29.9

30.1

30.5

30.9

32.0

32.2

32.6

33.6

33.9

34.7

36.1

36.7

37.2

38.9

39.0

39.9

40.4

40.7

40.8

41.2

42.0

42.0

43.8

44.0

44.7

45.2

46.0

47.5

48.2

50.4

54.3

59.1

68.7

0.0 20.0 40.0 60.0 80.0

Mitsubishi

Jiangxi Copper

Molycorp

Chalco

Glencore Xstrata

African Minerals

Hindalco

ERA

Aneka Tambang

Zijin Mining

Cliffs Natural Res.

Harmony

Lynas

Alcoa

Norsk Hydro

Korea Zinc

Press Metals

Lonmin

Amplats

United Co Rusal

Sylvania Platinum

Hongqiao

Anglo American

Vedanta

Paladin Energy

Sesa Sterlite

Fortescue Metals

Anglogold

Zhaojin Mining

Vale (Brazil)

Pan Aust

MMG

Kinross

Teck Resources

Newmont

China Molybdenum

Buenaventura

Rio Tinto

Goldfields

Oz Minerals

Newcrest Mining

Yamana

Freeport McMoRan

First Quantum

Antofagasta

BHP Billiton

Agnico-eagle

Barrick Gold

Iluka

Polyus Gold

PT Inco

Atlas Minerals

Goldcorp

Philex

Norilsk Nickel

Chinalco Mining

Bumi Res. Min.

Nickel Asia

-16.4

-8.7

-6.8

-4.2

-1.1

-0.7

0.4

1.8

1.8

2.3

2.6

2.7

2.9

3.2

3.2

3.3

3.9

4.5

4.5

5.1

5.3

5.4

5.6

5.6

6.5

7.0

7.2

7.6

7.7

7.8

7.8

8.1

8.2

8.2

8.4

8.5

8.7

9.0

9.3

10.0

10.1

10.4

10.7

11.3

11.5

12.7

13.8

14.1

14.4

14.7

14.7

14.8

16.6

20.4

20.8

28.5

31.3

35.9

-20.0 0.0 20.0 40.0

Molycorp

Cliffs Natural Res.

Chalco

African Minerals

Paladin Energy

Lynas

Harmony

Kinross

Vedanta

Aneka Tambang

Lingbao Gold

Oz Minerals

Lonmin

MMG

Yamana

Buenaventura

Goldfields

Goldcorp

Agnico-eagle

Jiangxi Copper

Teck Resources

Newmont

Vale (Brazil)

Fortescue Metals

Zhaojin Mining

Mitsubishi

Newcrest Mining

China Molybdenum

Zijin Mining

Anglo American

Sesa Sterlite

Glencore Xstrata

Hindalco

Nalco

Barrick Gold

Anglogold

Pan Aust

Antofagasta

Philex

Norsk Hydro

Alumina

BHP Billiton

Polyus Gold

Alcoa

First Quantum

PT Inco

Freeport McMoRan

Iluka

Chinalco Mining

Korea Zinc

Amplats

Rio Tinto

Hongqiao

Atlas Minerals

Press Metals

United Co Rusal

Nickel Asia

Norilsk Nickel

March 9, 2015 13

Regional Materials

Figure 25: Coal EV/EBITDA 2015 (x) Figure 26: Coal P/BV 2015 (x)

Source: Bloomberg consensus Source: Bloomberg consensus

Figure 27: Coal EBITDA margin 2015 (%) Figure 28: Coal ROE 2015 (%)

Source: Bloomberg consensus

Source: Bloomberg consensus

3.4

4.5

5.2

5.4 5.5

6.7

7.5

7.6

7.7

7.8

8.7

9.0

10.0

10.6

10.6

10.8

10.9

11.6

13.4

18.1

20.3

0.0 5.0 10.0 15.0 20.0 25.0

Shougang Fushan

Indo Tamb. Megah

Indika Energy

Adaro

Shenhua

Raspadskaya

Bumi Resources

Peabody Energy

Harum Energy

Consol Energy

PT Bukit Asam

Coal India

Banpu Pcl

Alpha Natural

Mechel

White Haven

Arch Coal

Yanzhou Coal

China Coal

Walter Energy

Mongolian Mining

0.2

0.2

0.3

0.3

0.4

0.5

0.5

0.5

0.6

0.6

0.6

0.8

0.8

1.0

1.0

1.1

1.4

1.6

0.0 0.5 1.0 1.5 2.0

Alpha Natural

Hidili

Indika Energy

Arch Coal

Shougang…

China Coal

White Haven

Mongolian…

Yanzhou Coal

Raspadskaya

Mechel

Peabody Energy

Adaro

Banpu Pcl

Shenhua

Harum Energy

Consol Energy

Indo Tamb.…

4.4

6.8

7.9

11.3 11.5

12.8

13.7

14.4

14.9

15.2

15.4

15.9

16.9

17.1

17.8

18.4

18.9

23.8

25.3

25.6

31.9

33.0

41.6

0.0 10.0 20.0 30.0 40.0 50.0

Southgobi

Harum Energy

Alpha Natural

Walter Energy

Mechel

Yanzhou Coal

Arch Coal

Mongolian Mining

Peabody Energy

Indo Tamb.…

China Coal

Bumi Resources

PT Bukit Asam

Hidili

Banpu Pcl

Raspadskaya

White Haven

Adaro

Coal India

Indika Energy

Shenhua

Consol Energy

Shougang Fushan

(27.9)

(27.6)

(19.4)

(10.6)

(7.7)

(6.5)

(3.4)

(1.3)

0.7

1.1

1.7

2.9

3.3

4.8

5.3

7.3

8.0

12.1

18.5

22.1

34.8

(40) (30) (20) (10) 0 10 20 30 40

Arch Coal

Alpha Natural

Mechel

Mongolian Mining

Raspadskaya

Hidili

Bumi Resources

Peabody Energy

White Haven

Indika Energy

China Coal

Shougang Fushan

Yanzhou Coal

Harum Energy

Consol Energy

Banpu Pcl

Adaro

Shenhua

Indo Tamb. Megah

PT Bukit Asam

Coal India

March 9, 2015 14

Regional Materials

Figure 29: Steel EV/EBITDA 2015 (x) Figure 30: Steel P/BV 2015 (x)

Source: Bloomberg consensus Source: Bloomberg consensus

Figure 31: Steel EBITDA margin 2015 (%) Figure 32: Steel ROE 2015 (%)

Source: Bloomberg consensus Source: Bloomberg consensus

4.2

4.5

4.6

5.0

5.3

5.4

5.5

5.6

5.9

6.7

6.7

6.8

6.8

6.9

6.9

6.9

7.0

7.1

7.2

7.3

7.4

7.4

8.8

9.8

10.5

0 3 6 9 12 15

U.S. Steel

Tata Steel

Arcelor Mittal

Evraz

JSW Steel

Hyundai Hysco

Thyssen Krupp

AK Steel

Steel Dynamics

Kobe Steel

Allengheny Technology

Nucor

Hyundai Steel

Bluescope Steel

POSCO

Jindal Steel & Power

Nippon Steel

Baosteel

Angang

Bhushan Steel

Steel Authority

JFE Holding

Maanshan

Wuhan

China Steel

0.2

0.2

0.4

0.5

0.5

0.5

0.6

0.6

0.7

0.7

0.8

0.8

0.8

0.9

0.9

0.9

0.9

1.0

1.1

1.2

1.3

1.3

1.3

1.3

0.0 0.5 1.0 1.5

Bhushan Steel

Dongkuk Steel

Arcelor Mittal

Hyundai Steel

POSCO

Maanshan

Bluescope Steel

Steel Authority

Angang

Jindal Steel &…

U.S. Steel

Tata Steel

Evraz

JFE Holding

Baosteel

JSW Steel

Nippon Steel

Wuhan

Kobe Steel

Hyundai Hysco

Steel Dynamics

Allengheny…

Severstal

China Steel

4.9

7.0

7.9

8.3

8.7

9.0

9.3

9.5

10.1

10.4

11.2

11.6

11.6

11.7

12.1

12.2

12.5

13.1

13.9

14.8

16.6

17.7

18.6

18.9

23.2

26.9

29.0

0.0 5.0 10.0 15.0 20.0 25.0 30.0

Dongkuk Steel

Thyssen Krupp

AK Steel

Bluescope Steel

U.S. Steel

Hyundai Hysco

Maanshan

Wuhan

Arcelor Mittal

POSCO

Angang

Tata Steel

Kobe Steel

JFE Holding

Baosteel

Steel Dynamics

Steel Authority

Nucor

Nippon Steel

Allengheny Technology

Hyundai Steel

Evraz

China Steel

JSW Steel

Severstal

Jindal Steel & Power

Bhushan Steel

3.2

3.4

4.1

5.1

5.5

5.5

6.6

6.8

6.9

7.0

7.1

7.7

7.7

8.4

8.5

9.3

9.3

10.4

10.9

12.5

13.2

14.1

17.9

0.0 10.0 20.0

Wuhan

Angang

Arcelor Mittal

Bluescope Steel

Bhushan Steel

POSCO

Hyundai Steel

Baosteel

Steel Authority

China Steel

Evraz

Allengheny…

U.S. Steel

Jindal Steel &…

Tata Steel

Kobe Steel

JFE Holding

Nippon Steel

JSW Steel

Nucor

Steel Dynamics

Severstal

Hyundai Hysco

March 9, 2015 15

Regional Materials

Share price performance: materials, coal and steel (YTD, 3 months)

Figure 33: Asia regional materials stocks YTD Figure 34: Asia regional materials stocks past three months

Source: Bloomberg. Source: Bloomberg.

Figure 35: Asia regional coal stocks YTD Figure 36: Asia regional coal stocks past three months

Source: Bloomberg. Source: Bloomberg.

-27% -18%

-16% -16% -15% -14%

-12% -11% -10% -10% -10%

-8% -7% -7% -5% -5% -5% -4% -3% -2% -2% -1%

0% 0% 0% 1% 1% 1% 2% 2% 2% 3% 3% 3% 3% 4% 6% 6% 7% 8% 9% 10% 11% 12%

14% 15% 15% 17% 17% 18% 19%

26%

-40% -20% 0% 20% 40%

Bumi Res. Min.Sinoma

PanAustNickel Asia

IRCHaranga

FortescueNALCOLynasMMG

Anhui ConchCR Cement

Yunnan CopperVALE IndonesiaChinalco Mining

Atlas MineralsBaotou Rare Earth

Aneka TambangTaiwan CementJiangxi Copper

HindalcoAsia Cement

CNBMSterlite Inds

IndophileHongqiao

China VanadiumChalco

Sesa SterliteHindustan Zinc

WCCVedanta

Korea ZincAlumina

Zijin MiningHunan Nonferrous

China MolyOZ Minerals

ERAPhilex

BHP BillitonRio Tinto

Ultratech CementRUSAL

Ambuja CementACC

ICEMPaladin Energy

ShanshuiShree CementZhaojin Mining

Newcrest

-33% -30% -29% -27% -25% -22% -20% -19% -18% -16% -13% -11% -11%

-9% -7% -7% -7% -6% -6% -6% -4% -3% -3% -3% -3% -2% -2%

0% 0% 1% 1% 2% 2% 2% 2% 4% 4% 6% 8% 10% 10% 11% 11% 11% 14% 14%

18% 25% 26%

38% 52%

63%

-60% -40% -20% 0% 20% 40% 60% 80%

PanAustBumi Res. Min.

HarangaVedanta

IRCNALCO

MMGFortescue

VALE IndonesiaAtlas Minerals

CR CementHongqiao

China VanadiumTaiwan Cement

Sesa SterliteHindalco

Jiangxi CopperPhilex

Nickel AsiaICEM

Korea ZincAsia CementOZ Minerals

RUSALSinoma

BHP BillitonChina Moly

Sterlite IndsChinalco Mining

CNBMAnhui Conch

LynasIndophile

ERAAneka TambangHindustan Zinc

WCCChalco

AluminaRio Tinto

Zijin MiningPaladin Energy

ACCBaotou Rare Earth

Zhaojin MiningAmbuja Cement

Ultratech CementShree Cement

Yunnan CopperNewcrestShanshui

Hunan Nonferrous

-16%

-16%

-14%

-13%

-12%

-10%

-8%

-6%

-4%

-3%

-1%

0%

0%

0%

12%

13%

15%

21%

37%

-40% -20% 0% 20% 40%

PT Bukit Asam

China Coal

Hidili

Shenhua

Shougang Fushan

Winsway

Indika Energy

Adaro

Yanzhou Coal

Mongolia Mining

Harum Energy

Coal India

Southgobi

Borneo Lumbung

Bayan

Banpu pcl

Indo Tam. Megah

Bumi Resources

Berau

-31%

-27%

-27%

-21%

-21%

-21%

-16%

-10%

-7%

-4%

-1%

0%

1%

3%

3%

5%

8%

9%

10%

-40% -20% 0% 20% 40%

Winsway

Hidili

Mongolia Mining

Shougang Fushan

PT Bukit Asam

Indika Energy

China Coal

Adaro

Shenhua

Indo Tam. Megah

Yanzhou Coal

Borneo Lumbung

Southgobi

Banpu pcl

Bumi Resources

Harum Energy

Bayan

Berau

Coal India

March 9, 2015 16

Regional Materials

Figure 37: Asia regional steel stocks YTD Figure 38: Asia regional steel stocks past three months

Source: Bloomberg. Source: Bloomberg.

Metal prices and inventory

Figure 39: Copper exchange prices and inventories Figure 40 Aluminium exchange prices and inventories

Source: Bloomberg Source: Bloomberg

Figure 41: Nickel exchange prices and inventories Figure 42: Zinc exchange prices and inventories

Source: Bloomberg Source: Bloomberg

-14%

-11%

-11%

-10%

-9%

-8%

-8%

-6%

-5%

-1%

-1%

1%

1%

3%

5%

7%

8%

9%

24%

-20% -10% 0% 10% 20% 30%

Angang

Steel Authority

Maanshan

Hyundai Hysco

BlueScope Steel

Shougang

Tata Steel

Baosteel

JSW Steel

Posco Steel

Dongkuk steel

China Steel

Bhushan

Hyundai Steel

Nippon Steel

Kobe Steel

Wuhan Steel

JFE Holding

Jindal Steel & Power

-23%

-19%

-17%

-16%

-15%

-14%

-12%

-8%

-5%

-3%

1%

2%

2%

3%

20%

23%

26%

40%

42%

-40% -20% 0% 20% 40% 60%

Tata Steel

JSW Steel

Hyundai Hysco

Steel Authority

Posco Steel

Dongkuk steel

Bhushan

Shougang

Maanshan

Hyundai Steel

Angang

China Steel

Nippon Steel

BlueScope Steel

JFE Holding

Kobe Steel

Jindal Steel & Power

Baosteel

Wuhan Steel

March 9, 2015 17

Regional Materials

Figure 43: Gold exchange prices Figure 44: Silver exchange prices

Source: Bloomberg Source: Bloomberg

Figure 45: Platinum exchange prices Figure 46: Palladium exchange prices

Source: Bloomberg Source: Bloomberg

0

80

160

240

320

400

-

400

800

1,200

1,600

2,000

Jan-0

0O

ct-

00

Jul-

01

Apr-

02

Jan-0

3O

ct-

03

Jul-

04

Apr-

05

Jan-0

6O

ct-

06

Jul-

07

Apr-

08

Jan-0

9O

ct-

09

Jul-

10

Apr-

11

Jan-1

2O

ct-

12

Jul-

13

Apr-

14

Jan-1

5

Pri

ce (

Rm

b p

er

gra

m)

Pri

ce (

USD

per

oz)

LME Spot Price (LHS) Shanghai Spot Price (RHS)

2,200

4,200

6,200

8,200

10,200

12,200

0

20

40

60

80

100

Jan-0

0O

ct-

00

Jul-

01

Apr-

02

Jan-0

3O

ct-

03

Jul-

04

Apr-

05

Jan-0

6O

ct-

06

Jul-

07

Apr-

08

Jan-0

9O

ct-

09

Jul-

10

Apr-

11

Jan-1

2O

ct-

12

Jul-

13

Apr-

14

Jan-1

5

Pri

ce (

Rm

b p

er

gra

m)

Pri

ce (

USD

per

ounce)

LME Spot Price (LHS) Shanghai Spot Price (RHS)

-

80

160

240

320

400

200

600

1,000

1,400

1,800

2,200

Jan-0

0O

ct-

00

Jul-

01

Apr-

02

Jan-0

3O

ct-

03

Jul-

04

Apr-

05

Jan-0

6O

ct-

06

Jul-

07

Apr-

08

Jan-0

9O

ct-

09

Jul-

10

Apr-

11

Jan-1

2O

ct-

12

Jul-

13

Apr-

14

Jan-1

5

Pri

ce (

Rm

b p

er

gra

m)

Pri

ce (

USD

per

oz)

LME Spot Price (LHS) Shanghai Spot Price (RHS)

0

40

80

120

160

200

240

-

200

400

600

800

1,000

1,200

Jan-0

0O

ct-

00

Jul-

01

Apr-

02

Jan-0

3O

ct-

03

Jul-

04

Apr-

05

Jan-0

6O

ct-

06

Jul-

07

Apr-

08

Jan-0

9O

ct-

09

Jul-

10

Apr-

11

Jan-1

2O

ct-

12

Jul-

13

Apr-

14

Jan-1

5

Pri

ce (

Rm

b p

er

gra

m)

Pri

ce (

USD

per

ounce)

LME Spot Price (LHS) Shanghai Spot Price (RHS)

March 9, 2015 18

Regional Materials

China coal inventory and prices, and power data

Figure 47: Thermal coal price Qinhuangdao vs. Newcastle* Figure 48: Thermal coal prices in China and Australia*

Source: Bloomberg, McCloskey, Maybank Kim Eng estimates.*Prices are adjusted for coal calorific content and estimated transportation cost for delivery to southern China for comparison purposes.

Source: Bloomberg, McCloskey, Maybank Kim Eng estimates. *China coal price includes 17% VAT basis 5,800 kcal. Australia price is FOB basis 6,000 kcal.

Figure 49: China coal inventory at power plants and total Figure 50: China total raw coal production and YoY change

Source: Bloomberg, McCloskey, Maybank Kim Eng estimates. Source: CCTD, McCloskey.

Figure 51: Monthly power generation and YoY change Figure 52: YoY change in power generation by source

Source: China NBS. Source: China NBS.

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

0

25

50

75

100

125

150

175

200

Jan-0

1Aug-0

1M

ar-

02

Oct-

02

May-0

3D

ec-0

3Jul-

04

Feb-0

5Sep-0

5Apr-

06

Nov-0

6Jun-0

7Jan-0

8Aug-0

8M

ar-

09

Oct-

09

May-1

0D

ec-1

0Jul-

11

Feb-1

2Sep-1

2Apr-

13

Nov-1

3Jun-1

4Jan-1

5

Premium (discount)

(USD/t)

Qinhuangdao coal price (LHS)Newcastle coal price (LHS)Qinhuangdao premium (discount)

0

25

50

75

100

125

150

175

200

Jan-0

7M

ay-0

7Sep-0

7Jan-0

8M

ay-0

8Sep-0

8Jan-0

9M

ay-0

9Sep-0

9Jan-1

0M

ay-1

0Sep-1

0Jan-1

1M

ay-1

1Sep-1

1Jan-1

2M

ay-1

2Sep-1

2Jan-1

3M

ay-1

3Sep-1

3Jan-1

4M

ay-1

4Sep-1

4Jan-1

5

USD/t Qinhuangdao coal price Newcastle coal price

Current prices Qinhuangdao 5,800 kcal USD85/t (incl. 17% VAT) Newcastle 6,000 kcal USD67/t (FOB)

5

10

15

20

25

30

35

40

Jan-0

5

Jul-

05

Jan-0

6

Jul-

06

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

Jul-

14

Power plants TotalDays

(30%)(20%)(10%)0%10%20%30%40%50%

0

100

200

300

400

一月

-03

六月

-03

十一

月-0

3

四月

-04

九月

-04

二月

-05

七月

-05

十二

月-0

5

五月

-06

十月

-06

三月

-07

八月

-07

一月

-08

六月

-08

十一

月-0

8

四月

-09

九月

-09

二月

-10

七月

-10

十二

月-1

0

五月

-11

十月

-11

三月

-12

八月

-12

一月

-13

六月

-13

十一

月-1

3

四月

-14

九月

-14

mt

Production (LHS)

YoY Chg. (RHS)

6 per. Mov. Avg. (YoY Chg. (RHS)) YoY Chg.

-14

-7

0

7

14

21

28

0

100

200

300

400

500

600

Jan&

Feb-0

7M

ay-0

7Aug-0

7N

ov-0

7M

ar-

08

Jun-0

8Sep-0

8D

ec-0

8Apr-

09

Jul-

09

Oct-

09

Jan&

Feb-1

0M

ay-1

0Aug-1

0N

ov-1

0M

ar-

11

Jun-1

1Sep-1

1D

ec-1

1Apr-

12

Jul-

12

Oct-

12

Jan&

Feb-1

3M

ay-1

3Aug-1

3N

ov-1

3M

ar-

14

Jun-1

4Sep-1

4D

ec-1

4

YoY % bn kWh Power gen. (LHS) % YoY (RHS)

(30)(20)(10)

0102030405060

Jan&

Feb-0

7M

ay-0

7Aug-0

7N

ov-0

7M

ar-

08

Jun-0

8Sep-0

8D

ec-0

8Apr-

09

Jul-

09

Oct-

09

Jan&

Feb-1

0M

ay-1

0Aug-1

0N

ov-1

0M

ar-

11

Jun-1

1Sep-1

1D

ec-1

1Apr-

12

Jul-

12

Oct-

12

Jan&

Feb-1

3M

ay-1

3Aug-1

3N

ov-1

3M

ar-

14

Jun-1

4Sep-1

4YoY % Thermal Hydro Nuclear

March 9, 2015 19

Regional Materials

China steel inventory and prices

Figure 53: Steel market prices in eastern China Figure 54: China company list prices vs. market prices

Source: Steelhome. Source: Steelhome.

Figure 55: Coking coal prices China and the region Figure 56: Comparison - imported iron ore vs steel prices

Source: Steelhome. Source: Steelhome.

Figure 57: China crude steel production and YoY growth Figure 58: Long-term view China steel price and input costs

Source: Steelhome Source: Steelhome, AMM, Maybank Kim Eng forecasts.

2,000

3,000

4,000

5,000

6,000

7,000

8,000

一月

04

六月

04

十一月

04

四月

05

九月

05

二月

06

七月

06

十二月

06

五月

07

十月

07

三月

08

八月

08

一月

09

六月

09

十一月

09

四月

10

九月

10

二月

11

七月

11

十二月

11

五月

12

十月

12

三月

13

八月

13

一月

14

六月

14

十一月

14

Rebar ψ12 Plate 20mmHRC 2.75mm CR sheet 1mmHDG 0.5mm

Rmb/t

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

一月

04

六月

04

十一月

04

四月

05

九月

05

二月

06

七月

06

十二月

06

五月

07

十月

07

三月

08

八月

08

一月

09

六月

09

十一月

09

四月

10

九月

10

二月

11

七月

11

十二月

11

五月

12

十月

12

三月

13

八月

13

一月

14

六月

14

十一月

14

Co. avg. HRC price (VAT excl.)

Market price (2.75mm, VAT excl.)Rmb/t

0

50

100

150

200

250

300

350

400

一月

07

五月

07

九月

07

一月

08

五月

08

九月

08

一月

09

五月

09

九月

09

一月

10

五月

10

九月

10

一月

11

五月

11

九月

11

一月

12

五月

12

九月

12

一月

13

五月

13

九月

13

一月

14

五月

14

九月

14

一月

15

Shanxi premium coking coal (ex-VAT)

Newcastle hard coking coal (FOB Australia)USD/t

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0

50

100

150

200

250

300

一月

06

五月

06

九月

06

一月

07

五月

07

九月

07

一月

08

五月

08

九月

08

一月

09

五月

09

九月

09

一月

10

五月

10

九月

10

一月

11

五月

11

九月

11

一月

12

五月

12

九月

12

一月

13

五月

13

九月

13

一月

14

五月

14

九月

14

一月

15

Iron ore (CIF China, 62%, LHS)Rebar price China (VAT incl., RHS)HRC price China (VAT incl., RHS)USD/t CNY/t

-20%

-10%

0%

10%

20%

30%

40%

50%

10

20

30

40

50

60

70

80

一月

06

五月

06

九月

06

一月

07

五月

07

九月

07

一月

08

五月

08

九月

08

一月

09

五月

09

九月

09

一月

10

五月

10

九月

10

一月

11

五月

11

九月

11

一月

12

五月

12

九月

12

一月

13

五月

13

九月

13

一月

14

五月

14

九月

14

一月

15

Monthly crude production (LHS)

YoY growth (RHS)YoY chg. mt

100

150

200

250

300

350

400

450

500

550

300

400

500

600

700

800

900

1,000

1,100

1,200

1Q

'06

3Q

'06

1Q

'07

3Q

'07

1Q

'08

3Q

'08

1Q

'09

3Q

'09

1Q

'10

3Q

'10

1Q

'11

3Q

'11

1Q

'12

3Q

'12

1Q

'13

3Q

'13

1Q

'14

3Q

'14

1Q

'15E

3Q

'15E

Raw materials cost ex-freight (RHS)China HRC 2.75mm, VAT excl. (LHS)US HRC price (LHS)

USD/ USD/t

March 9, 2015 20

Regional Materials

China metals trade watch (imports/exports in ‘000 t)

Figure 59: Refined copper trade (net import recovery) Figure 60: Copper concentrate trade (rising to high levels)

Source: China Customs Data. Source: China Customs Data.

Figure 61: Alumina trade (sharp increase) Figure 62: Bauxite trade (stabilizing at lower levels)

Source: China Customs Data. Source: China Customs Data.

Figure 63: Refined nickel trade (net exporting has ended Figure 64: Nickel ore trade (imports fall to lower levels)

Source: China Customs Data. Source: China Customs Data.

(400)

(350)

(300)

(250)

(200)

(150)

(100)

(50)

0

50

(400)

(350)

(300)

(250)

(200)

(150)

(100)

(50)

-

50

Jan-1

0M

ar-

10

May-1

0Jul-

10

Sep-1

0N

ov-1

0Jan-1

1M

ar-

11

May-1

1Jul-

11

Sep-1

1N

ov-1

1Jan-1

2M

ar-

12

May-1

2Jul-

12

Sep-1

2N

ov-1

2Jan-1

3M

ar-

13

May-1

3Jul-

13

Sep-1

3N

ov-1

3Jan-1

4M

ar-

14

May-1

4Jul-

14

Sep-1

4N

ov-1

4

import export net export

(1,200)

(1,000)

(800)

(600)

(400)

(200)

0

200

(1,400)

(1,200)

(1,000)

(800)

(600)

(400)

(200)

-

200

Jan-1

0M

ar-

10

May-1

0Jul-

10

Sep-1

0N

ov-1

0Jan-1

1M

ar-

11

May-1

1Jul-

11

Sep-1

1N

ov-1

1Jan-1

2M

ar-

12

May-1

2Jul-

12

Sep-1

2N

ov-1

2Jan-1

3M

ar-

13

May-1

3Jul-

13

Sep-1

3N

ov-1

3Jan-1

4M

ar-

14

May-1

4Jul-

14

Sep-1

4N

ov-1

4Jan-1

5M

ar-

15

May-1

5Jul-

15

Sep-1

5N

ov-1

5Jan-1

6M

ar-

16

May-1

6Jul-

16

Sep-1

6N

ov-1

6Jan-1

7M

ar-

17

May-1

7Jul-

17

Sep-1

7N

ov-1

7Jan-1

8M

ar-

18

May-1

8Jul-

18

Sep-1

8N

ov-1

8Jan-1

9M

ar-

19

May-1

9Jul-

19

Sep-1

9N

ov-1

9

import export net export

(800)

(600)

(400)

(200)

0

200

(800)

(600)

(400)

(200)

-

200

Jan-1

0M

ar-

10

May-1

0Jul-

10

Sep-1

0N

ov-1

0Jan-1

1M

ar-

11

May-1

1Jul-

11

Sep-1

1N

ov-1

1Jan-1

2M

ar-

12

May-1

2Jul-

12

Sep-1

2N

ov-1

2Jan-1

3M

ar-

13

May-1

3Jul-

13

Sep-1

3N

ov-1

3Jan-1

4M

ar-

14

May-1

4Jul-

14

Sep-1

4N

ov-1

4

import export net export

(8,400)

(7,000)

(5,600)

(4,200)

(2,800)

(1,400)

0

(8,400)

(7,000)

(5,600)

(4,200)

(2,800)

(1,400)

-Jan-1

0M

ar-

10

May-1

0Jul-

10

Sep-1

0N

ov-1

0Jan-1

1M

ar-

11

May-1

1Jul-

11

Sep-1

1N

ov-1

1Jan-1

2M

ar-

12

May-1

2Jul-

12

Sep-1

2N

ov-1

2Jan-1

3M

ar-

13

May-1

3Jul-

13

Sep-1

3N

ov-1

3Jan-1

4M

ar-

14

May-1

4Jul-

14

Sep-1

4N

ov-1

4Jan-1

5M

ar-

15

May-1

5Jul-

15

Sep-1

5N

ov-1

5Jan-1

6M

ar-

16

May-1

6Jul-

16

Sep-1

6N

ov-1

6Jan-1

7M

ar-

17

May-1

7Jul-

17

Sep-1

7N

ov-1

7Jan-1

8M

ar-

18

May-1

8Jul-

18

Sep-1

8N

ov-1

8Jan-1

9M

ar-

19

May-1

9Jul-

19

Sep-1

9N

ov-1

9

import export net export

(30)

(20)

(10)

0

10

20

(30)

(20)

(10)

-

10

20

Jan-1

0M

ar-

10

May-1

0Jul-

10

Sep-1

0N

ov-1

0Jan-1

1M

ar-

11

May-1

1Jul-

11

Sep-1

1N

ov-1

1Jan-1

2M

ar-

12

May-1

2Jul-

12

Sep-1

2N

ov-1

2Jan-1

3M

ar-

13

May-1

3Jul-

13

Sep-1

3N

ov-1

3Jan-1

4M

ar-

14

May-1

4Jul-

14

Sep-1

4N

ov-1

4

import export net export

(8,000)

(7,000)

(6,000)

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

0

(8,000)

(7,000)

(6,000)

(5,000)

(4,000)

(3,000)

(2,000)

(1,000)

-

Jan-0

8Apr-

08

Jul-

08

Oct-

08

Jan-0

9Apr-

09

Jul-

09

Oct-

09

Jan-1

0Apr-

10

Jul-

10

Oct-

10

Jan-1

1Apr-

11

Jul-

11

Oct-

11

Jan-1

2Apr-

12

Jul-

12

Oct-

12

Jan-1

3Apr-

13

Jul-

13

Oct-

13

Jan-1

4Apr-

14

Jul-

14

Oct-

14

import export net export

March 9, 2015 21

Regional Materials

China macro data indicators

Figure 65: China quarterly GDP growth (YoY % chg.) Figure 66: China industrial prod. growth (YoY % chg.)

Source: Bloomberg, China NBS. Source: Bloomberg, China NBS.

Figure 67: China monthly loan growth Figure 68: China sector FAI (monthly YoY % chg.)

Source: PBOC, Maybank Kim Eng. Source: CEIC, China NBS.

Figure 69: China producer price index (YoY % chg.) Figure 70: China export/import growth (YoY % chg.)

Source: Bloomberg, China NBS. Source: China Customs Data.

5

6

7

8

9

10

11

12

13

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

0

5

10

15

20

25

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

10.0

10

11

12

13

14

15

16

17

Dec-1

2Jan-1

3Feb-1

3M

ar-

13

Apr-

13

May-1

3Jun-1

3Jul-

13

Aug-1

3Sep-1

3O

ct-

13

Nov-1

3D

ec-1

3Jan-1

4Feb-1

4M

ar-

14

Apr-

14

May-1

4Jun-1

4Jul-

14

Aug-1

4Sep-1

4O

ct-

14

Nov-1

4D

ec-1

4Jan-1

5

CNYtn % RMB loan growth (RHS)

RMB deposit growth (RHS)

(40)

0

40

80

120

Jan-0

4

Jul-

04

Jan-0

5

Jul-

05

Jan-0

6

Jul-

06

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

Jul-

14

Mining Real EstateManufacturing Construction

-12

-6

0

6

12

18

Feb-9

9O

ct-

99

Jun-0

0Feb-0

1O

ct-

01

Jun-0

2Feb-0

3O

ct-

03

Jun-0

4Feb-0

5O

ct-

05

Jun-0

6Feb-0

7O

ct-

07

Jun-0

8Feb-0

9O

ct-

09

Jun-1

0Feb-1

1O

ct-

11

Jun-1

2Feb-1

3O

ct-

13

Jun-1

4

PPI PPI: Raw Materials PPI: Manufacturing

-40

-20

0

20

40

60

80

一月

-08

四月

-08

七月

-08

十月

-08

一月

-09

四月

-09

七月

-09

十月

-09

一月

-10

四月

-10

七月

-10

十月

-10

一月

-11

四月

-11

七月

-11

十月

-11

一月

-12

四月

-12

七月

-12

十月

-12

一月

-13

四月

-13

七月

-13

十月

-13

一月

-14

四月

-14

七月

-14

十月

-14

一月

-15

Export Growth Import Growth

March 9, 2015 22

Regional Materials

Research Offices

REGIONAL

WONG Chew Hann, CA

Regional Head of Institutional Research

(603) 2297 8686 [email protected]

ONG Seng Yeow

Regional Head of Retail Research

(65) 6432 1453

Alexander GARTHOFF

Institutional Product Manager

(852) 2268 0638

ECONOMICS

Suhaimi ILIAS

Chief Economist

Singapore | Malaysia

(603) 2297 8682

Luz LORENZO

Philippines

(63) 2 849 8836

Tim LEELAHAPHAN

Thailand

(66) 2658 6300 ext 1420

JUNIMAN

Chief Economist, BII

Indonesia

(62) 21 29228888 ext 29682

STRATEGY

Sadiq Currimbhoy

Global Strategist

(65) 6231 5836 [email protected]

Willie Chan

Hong Kong / Regional

(852) 2268 0631 [email protected]

MALAYSIA

WONG Chew Hann, CA Head of Research (603) 2297 8686 [email protected] • Strategy • Construction & Infrastructure

Desmond CH’NG, ACA (603) 2297 8680 [email protected] • Banking & Finance

LIAW Thong Jung (603) 2297 8688 [email protected] • Oil & Gas - Regional • Shipping

ONG Chee Ting, CA (603) 2297 8678 [email protected] • Plantations - Regional

Mohshin AZIZ (603) 2297 8692 [email protected] • Aviation - Regional • Petrochem

YIN Shao Yang, CPA (603) 2297 8916 [email protected] • Gaming – Regional • Media

TAN Chi Wei, CFA (603) 2297 8690 [email protected] • Power • Telcos

WONG Wei Sum, CFA (603) 2297 8679 [email protected] • Property & REITs

LEE Yen Ling (603) 2297 8691 [email protected] • Building Materials • Glove Producers

CHAI Li Shin, CFA (603) 2297 8684 [email protected] • Plantation • Construction & Infrastructure

Ivan YAP (603) 2297 8612 [email protected] • Automotive

Kevin WONG (603) 2082 6824 [email protected] • REITs

LEE Cheng Hooi Regional Chartist (603) 2297 8694 [email protected]

Tee Sze Chiah Head of Retail Research

(603) 2297 6858 [email protected]

HONG KONG / CHINA

Howard WONG Head of Research (852) 2268 0648 [email protected] • Oil & Gas - Regional

Alexander LATZER (852) 2268 0647 [email protected] • Metals & Mining – Regional

Benjamin HO (852) 2268 0632 [email protected] • Consumer & Auto

Jacqueline KO, CFA (852) 2268 0633 [email protected] • Consumer Staples & Durables

Ka Leong LO, CFA (852) 2268 0630 [email protected] • Consumer Discretionary & Auto

Karen KWAN (852) 2268 0640 [email protected] • Property & REITs

Mitchell KIM (852) 2268 0634 [email protected] • Internet & Telcos

Osbert TANG, CFA (86) 21 5096 8370 [email protected] • Transport & Industrials

Ricky WK NG, CFA (852) 2268 0689 [email protected] • Utilities & Renewable Energy

Steven ST CHAN (852) 2268 0645 [email protected] • Banking & Financials - Regional

Warren LAU (852) 2268 0644 [email protected] • Technology – Regional

INDIA

Jigar SHAH Head of Research

(91) 22 6632 2632

• Oil & Gas • Automobile • Cement

Anubhav GUPTA

(91) 22 6623 2605

• Metal & Mining • Capital Goods • Property

Urmil SHAH

(91) 22 6623 2606 [email protected]

• Technology • Media

Vishal MODI

(91) 22 6623 2607 [email protected]

• Banking & Financials

Abhijeet Kundu

(91) 22 6623 2628 [email protected]

• Consumer

SINGAPORE

NG Wee Siang Head of Research (65) 6231 5838 [email protected] • Banking & Finance

Gregory YAP (65) 6231 5848 [email protected] • SMID Caps – Regional • Technology & Manufacturing • Telcos

YEAK Chee Keong, CFA (65) 6231 5842 [email protected] • Offshore & Marine

Derrick HENG, CFA (65) 6231 5843 [email protected] • Transport (Land, Shipping & Aviation)

WEI Bin (65) 6231 5844 [email protected] • Commodity • Logistics • S-chips

John CHEONG (65) 6231 5845 [email protected] • Small & Mid Caps • Healthcare

TRUONG Thanh Hang (65) 6231 5847 [email protected] • Small & Mid Caps

INDONESIA

Wilianto IE Head of Research (62) 21 2557 1125 [email protected] • Strategy

Rahmi MARINA (62) 21 2557 1128 [email protected] • Banking & Finance

Aurellia SETIABUDI (62) 21 2953 0785 [email protected] • Property

Isnaputra ISKANDAR (62) 21 2557 1129 [email protected] • Metals & Mining • Cement

Pandu ANUGRAH (62) 21 2557 1137 [email protected] • Infra • Construction • Transport• Telcos

Janni ASMAN (62) 21 2953 0784 [email protected] • Cigarette • Healthcare • Retail

Adhi Tasmin (62) 21 2557 1209 [email protected] • Plantations

PHILIPPINES

Luz LORENZO Head of Research (63) 2 849 8836 [email protected] • Strategy • Utilities • Conglomerates • Telcos

Lovell SARREAL (63) 2 849 8841 [email protected] • Consumer • Media • Cement

Rommel RODRIGO (63) 2 849 8839 [email protected] • Conglomerates • Property • Gaming • Ports/ Logistics

Katherine TAN (63) 2 849 8843 [email protected] • Banks • Construction

Ramon ADVIENTO (63) 2 849 8845 [email protected] • Mining

Michael Bengson (63) 2 849 8840 [email protected] • Conglomerates

Jaclyn Jimenez (63) 2 849 8842 [email protected] • Consumer

Arabelle Maghirang (63) 2 849 8838 [email protected] • Banks

THAILAND

Maria LAPIZ Head of Institutional Research Dir (66) 2257 0250 | (66) 2658 6300 ext 1399 [email protected] • Consumer • Materials • Ind.Estates

Jesada TECHAHUSDIN, CFA (66) 2658 6300 ext 1394 [email protected] • Financial Services

Kittisorn PRUITIPAT, CFA, FRM (66) 2658 6300 ext 1395 [email protected] • Real Estate • Telcos

Sittichai DUANGRATTANACHAYA (66) 2658 6300 ext 1393 [email protected] • Services Sector • Transport

Sukit UDOMSIRIKUL Head of Retail Research (66) 2658 6300 ext 5090 [email protected]

Mayuree CHOWVIKRAN (66) 2658 6300 ext 1440 [email protected] • Strategy

Padon VANNARAT (66) 2658 6300 ext 1450 [email protected] • Strategy

Surachai PRAMUALCHAROENKIT (66) 2658 6300 ext 1470 [email protected] • Auto • Conmat • Contractor • Steel