regional watch for managing agents and brokers international markets market intelligence june 2010...

TRANSCRIPT

Regional Watch

FOR MANAGING AGENTS AND BROKERS

International Markets

Market Intelligence

June 2010

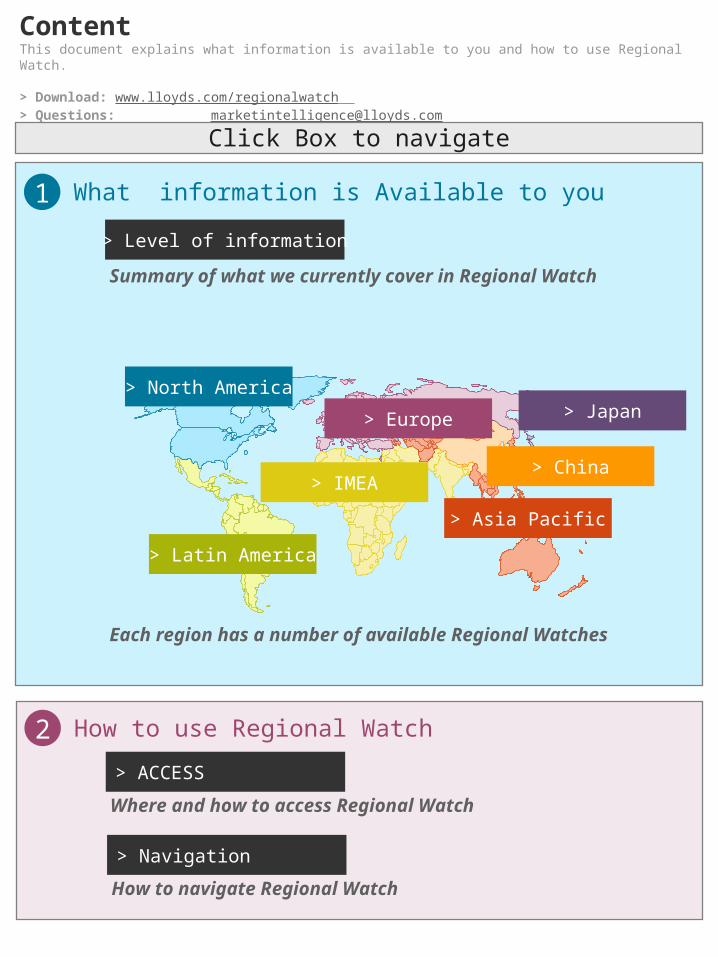

What info is Available to you 1

How to use Regional Watch2

1 What information is Available to you

Summary of what we currently cover in Regional Watch

> Asia Pacific

> Latin America

> North America

> Europe

> IMEA

> Level of information

How to use Regional Watch 2

ContentThis document explains what information is available to you and how to use Regional Watch.

> Download: www.lloyds.com/regionalwatch > Questions: [email protected]

Where and how to access Regional Watch

> ACCESS

How to navigate Regional Watch

> Navigation

Click Box to navigate

Each region has a number of available Regional Watches

> Japan

> China

CLASS OF BUSINESSIntelligence of business

classes in a territory which can range from high-level and detailed overview of

premiums, loss ratios and growth drivers to basic news stories regarding a particular business class.

DISTRIBUTIONIntelligence of distribution in

a territory which can range from high-level and detailed overview of core strengths and weaknesses of brokers

to basic news stories regarding a broker.

COMPETITIONIntelligence of competitors

in a territory which can range from detailed overview of

core strengths and weaknesses to low level info such as basic news stories

regarding a competitor.

Regional Watch has different LEVELS OF INFORMATION, which are exemplified by the matrix below.

Soft

Inte

llig

ence

Fact

She

etSo

ft In

tell

igen

ce Fa

ct S

heet

COMOPANY X

X have a 50% market share in liability: X’s largest liability classes are (sometimes driven by government regulation – i.e. medical malpractice); largest liability classes are carriers’liability followed by public liability, employers’ liability and medical malpractice. X are currently reviewing their treaty book, which could in turn affect its FAC purchases. The agricultural account of X is believed to have performed badly in 2009 due to natural disasters such as drought in the northern part of China.

For the first half of 2009, X posted net income of USD 47m, compared with a loss of USD 41m. Country’s largest non-life insurer, trimmed its underwriting loss to around USD 172m from nearly USD 302m through June 2008.

The 2008 period was impacted negatively by claims for natural disasters, including an earthquake in May 2008 and massive snowstorms in central and southern parts of the country.

From an obvious position of strength X are concentrating more on profit than market share. However newer companies need to gain market share and this leads to price competition.

X is expanding into the telephone marketing of auto insurance. The regulator allows insurers with a telephone marketing licensein auto insurance to offer a further 15 reduction to the officially approved 30%.

Local Market Issues

Strategy

Financials

Distribution Channels

Estimated Ranking Largest non-life insurer

Key business classes All business classes; however more interested in main stream classes (Motor, Property etc.)

Approximate Size USD 14.6bn (2008)

Licence Top national insurer with headquarter in XXAdditional Info

Total Loss RatioBusiness Class

PerformanceGeographic Split

Soft

Inte

llig

ence

Fact

She

etSo

ft In

tell

igen

ce Fa

ct S

heet

Sub-Class

CLASS X

Local Market Issues

Distribution Channels

Premium Income Trends

Profitability

X has received significant attention in the local market. Product Liability policies tend to be one year policies. It is estimated that it accounts for 20% of the X market; high profile product re-calls; increased litigiousness; role of government –particular regard to “food safety” are important. Key local players such as A and B now have partnerships with law firms and adjuster’s expertise, which has helped them to overtake D for class X.

Growth in exports is a major driver as this product is driven byvendor requirements. High profile product re-call and increased litigiousness are long term drivers.

owever, there continues to be only a fraction of Y’s exports covered by product liability and product liability for the domestic market is virtually non-existent. Current Treaty Reinsurance capacity is subject to a long list of excluded products.

Direct (some success with cold calling for SMEs) and via brokers. Vendors are pushing suppliers to purchase product liability. International vendors like buying cover from “reputable”insurance companies. D used to have a strong position via its direct sales force; the majority of these agents have migrated over to G and other insurance companies or new start up such as I. In the developed segment / geographic area (coastal regions) product liability is estimated to be mostly brokered (around 80%).

Rates are competitive (except for products excluded by the reinsurance treaty arrangements).

Typical market loss ratio is estimated to be between 60% - 70%.

Product liability tends to require high limits for exports.

Key Competitors

Strong: A, B, CMedium: D

Niche: E, F

Size (in USD)

Growth

2008E 2009F 2010F 2011F

70m 10% 20% 20%

Key Competitors

Strong: A, B, CMedium: D

Niche: E, F

Size (in USD)

Growth

2008E 2009F 2010F 2011F

70m 10% 20% 20%E: Estimate; F = Forecast based on Interviews, Shanghai, October 2009

BUSINESS CLASSBUSINESS CLASS

Soft

Inte

llig

ence

Fact

She

etSo

ft In

tell

igen

ce Fa

ct S

heet

Local Market Issues

Strategy

Premium Income Trends

Major Classes

X has been ranked as the number one international broker in country A for 2008 & 2009 by the Regulator.

X has received regulatory approval at the beginning of 2009 from the CIRC to open a new branch in Dalian, Liaoning province.

Around 95% of business is renewal business.

It is thought that approximately 70% of X portfolio in A is global client business.

X’s Business Development Team works on cross-selling potentials.

X has been in A for 25 years, first as a risk management consultant and later started providing broking services. X, through B, was the first foreign broker in A. X’s strategy is to become the largest broker in A and to balance the level of indigenous business that they generate versus global client business.

Y is by far the top broker for agricultural treaties in A which is a growing area. X is quite strong in in financial lines through its CC unit.

X has recently set up a client services group which targets local enterprises investing overseas

X has traditionally been a leader in the marine and energy sector. They will continue to be a dominant player given their strong team on the ground.

Lloyd’s Premium Placing Model

Lloyd’s broker; Retail (both indigenous & global client) Headquartered in X, offices in Y and Z; 130 staff

Estimated Ranking

Links N/A

Website

www.company.com

BrokerBroker4th largest broker in 2007

tota

l GW

P by

insu

rer

(in m

illi

on U

SD) i

n 20

07

Risks have a high retention rate as the main players have signif icant capacity. Reinsurance cessions are declining and the level of reinsurance premium in 2006 (USD 637m) is significantly lower than the 2002 level (USD 804 m). However, the local association hosts more than 200 international reinsurers writing non-domiciled business and numbers continue to rise. Captive reinsurance companies have been set up by major corporations as well as large global commercial reinsurers and several Bermudian reinsurers. There are also several agency reinsurers, that is subsidiaries of commercial insurance companies, particularly large and medium-sized European mutuals, set up to consolidate their reinsurance programmes.

Rein

sure

rs

Reinsur er A

Reinsur er B

Reinsur er C

Reinsur er D

Motor Pr oper tyPr oper ty Liabil ityLiabil ity Miscel l aneous*Miscel l aneous*

0

100

200

300

400

500

600

700

A B C D E F G H

© Lloyd’s189

Time Per iod

Cover edYY: Sof t Intel l igence on l ocal insur er s

Soft

Inte

llig

ence

COMPANY XX has appointed Ms YY as Country Manager for X, based in… office. She will assume full management responsibility for X’s P&C product lines distributed through its Y offices. She has extensive experience in the insurance industry having worked in a variety of management roles in the UK and Ireland for Z and X..

A spokesman noted that the market is going through "an exciting time," but expressed confidence in X’s ability to present "a very attractive proposition for insureds and brokers in Y amid current volatile market conditions."

Insurance Journal, “X Europe Names YY to Head P/C Unit in Y”, (December 2008)

© Lloyd’s180

YY: Sof t Intel l igence by cl ass

Soft

Inte

llig

ence

BUSINESS CLASS XMotor and home insurance costs could rise by up to 10% during 2009, according to XX.Along with other insurers, a company spokesman said that the company has seen an increase in claims during 2008. The spokesman also pointed out that the resulting higher risks were driving up the cost of insurance.Market Intelligence based on: Irish Times, “Warning of 10% rise in home and motor cover”, (May 2009)

.

Market Intelligence based on: Irish Insurance Federation Factfifle 2009, (August 2009); http://www.iif.ie/

Dire

ct M

arke

t GW

P (in

bil

lion

USD

)Ca

tego

ries

Cl asses2007*

Miscel l aneousMotorPA & Heal thMATLiabil it yPr oper ty

Incl udes:1.0% Surety. Bonds &

Credit

20%

14%

30%

25%

9%

6.0

8.3

9.0 9.2

10.210.9

4.6

3.53.43.0

9.0

0

2

4

6

8

10

12

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Dire

ct M

arke

t GW

P (in

bil

lion

USD

)Ca

tego

ries

Cl asses2007*

Miscel l aneousMotorPA & Heal thMATLiabil it yPr oper ty

Incl udes:1.0% Surety. Bonds &

Credit

20%

14%

30%

25%

9%

20%

14%

30%

25%

9%

6.0

8.3

9.0 9.2

10.210.9

4.6

3.53.43.0

9.0

0

2

4

6

8

10

12

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

6.0

8.3

9.0 9.2

10.210.9

4.6

3.53.43.0

9.0

0

2

4

6

8

10

12

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

DISTRIBUTION OVERVIEW

A is essentially a broker market and there has been significant

consolidation over the past few years.

Broking groups outside XX have been particularly active in mergers and

companies such as D, F, G are reported to have gained significant

market share: their domestic size could be approaching that of the major

global brokers.

YY estimates that 95% of commercial business is controlled by

brokers with about 40% for private business.

J, in particular, has achieved a very powerful position through mergers.

In October 2004 P acquired Q and more recently, there have been

several mergers of regional brokers and firms

DISTRIBUTION OVERVIEW

A is essentially a broker market and there has been significant

consolidation over the past few years.

Broking groups outside XX have been particularly active in mergers and

companies such as D, F, G are reported to have gained significant

market share: their domestic size could be approaching that of the major

global brokers.

YY estimates that 95% of commercial business is controlled by

brokers with about 40% for private business.

J, in particular, has achieved a very powerful position through mergers.

In October 2004 P acquired Q and more recently, there have been

several mergers of regional brokers and firms

KEY BROKERS

D

C

B

A

KEY BROKERS

D

C

B

A

© Lloyd’s199

YY: Sof t Intel l igence on l ocal Br oker s

Soft

Inte

llig

ence

BROKER XPlans to open a new research and development (R&D) centre in City Z have been outlined by Y, the US insurance and reinsurance brokerage. Y said the new centre will use analytical and mathematical techniques to develop new products. The opening of the new centre will create 100 jobs.

The centre, which is based in the IFSC in City Z, will be the fi rst research and development insurance operation in Ireland. The purpose of the centre is to collect information from Y's operations around the world and use mathematical and analytical techniques to devise new products for clients. The company has operations in City Z, City Y. The company’s operations are divided into retail insurance, which employs 280 people; pensions, which has a staff of 80; and risk management consulting, which employs 100 people.

Stephen Cross, chief executive of Y Global Risk Consulting, said insurance was more important to businesses now than 24 or 36 months ago due to the financial crisis. Mr Cross said Y chose Ireland for its RD centre, which is being supported with an investment from IDA Ireland, due to its geographical location and the availability of a well-educated workforce in Ireland

Construction

Y is the largest Insurance Broker in the construction sector in Ireland. Y Construction is a dedicated division established recently to service the specific needs of construction companies, contractors and developers. Y believes that the current downturn being experienced in the construction sector in Ireland means that companies - now more than ever - require innovative and sustainable solutions to their risk and insurance needs which deliver the best possible cover at the most competitive price. Y is broker to the Construction Industry Federation and has been working closely with them to provide value added services for CIF Members

Market intelligence based on : Irish Times, 10 Dec 2008, online; Esmerk, (December 2008);

About Regional WatchThis is a tool for managing agents and brokers detailing market intelligence on Lloyd's key market development territories. The dashboards contain up-to-date soft and hard intelligence on the insurance environment at different levels of detail.

> Download: www.lloyds.com/regionalwatch > Questions: [email protected]

MICRO

LEVEL

MESO

LEVEL

MACRO

LEVEL

DETAIL

S

DETAIL

S

DETAIL

S

SUMM

ARY

SUMM

ARY

SUMM

ARY

OVERVIE

W

OVERVIE

W

OVERVIE

W

Back To > Content

IN MARKET RESEARCH

DESK-BASED RESEARCH

AD HOC RESEARCH

COMPETITION BUSINESS CLASS DISTRIBUTION

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

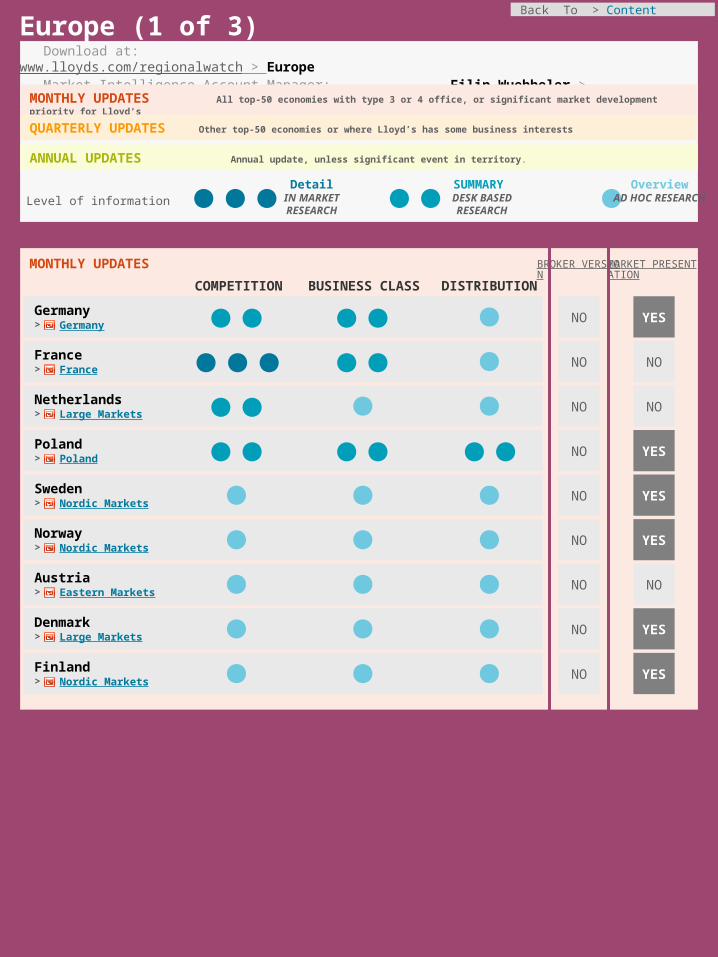

Europe (1 of 3) Download at: www.lloyds.com/regionalwatch > Europe Market Intelligence Account Manager: Filip Wuebbeler > [email protected]

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

MONTHLY UPDATES BROKER VERSION

Netherlands> Large Markets

NO NO

Germany> Germany

NO

France> France

NO NO

NOPoland> Poland

Sweden> Nordic Markets

NO

Finland> Nordic Markets

NO

Austria> Eastern Markets

NO NO

Denmark> Large Markets

NO

MARKET PRESENTATION

Norway> Nordic Markets

NO

YES

YES

YES

YES

YES

YES

Back To > Content

COMPETITION BUSINESS CLASS DISTRIBUTION

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

MONTHLY UPDATES BROKER VERSION

Switzerland> Large Markets

NO NO

Russia> Russia

YES NO

MARKET PRESENTATION

COMPETITION BUSINESS CLASS DISTRIBUTION

QUARTERLY UPDATES

Turkey>Small Markets

NO NO

Belgium> Small Markets

NO NO

Greece> Small Markets

NO NO

Israel> Small Markets

NO NO

BROKER VERSION

MARKET PRESENTATION

Europe (2 of 3) Download at: www.lloyds.com/regionalwatch > Europe Market Intelligence Account Manager: Alex Milne > [email protected]

Back To > Content

COMPETITION BUSINESS CLASS DISTRIBUTION

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

MONTHLY UPDATES BROKER VERSION

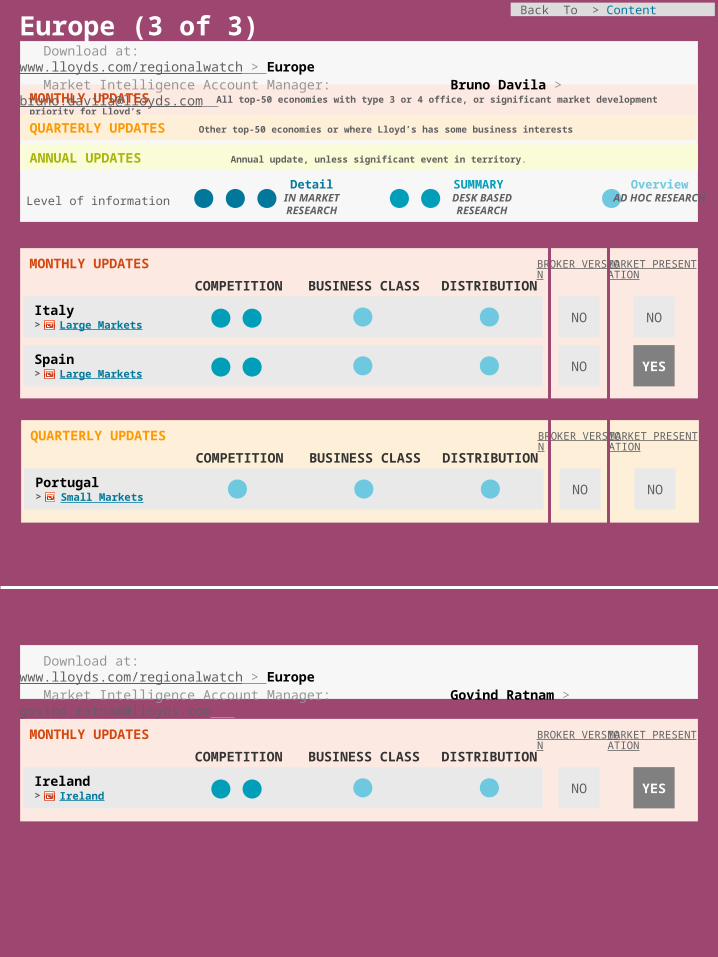

Italy> Large Markets

NO NO

Spain> Large Markets

NO YES

MARKET PRESENTATION

COMPETITION BUSINESS CLASS DISTRIBUTION

QUARTERLY UPDATES

Portugal> Small Markets

NO NO

BROKER VERSION

MARKET PRESENTATION

Europe (3 of 3) Download at: www.lloyds.com/regionalwatch > Europe Market Intelligence Account Manager: Bruno Davila > [email protected]

COMPETITION BUSINESS CLASS DISTRIBUTION

MONTHLY UPDATES BROKER VERSION

MARKET PRESENTATION

Download at: www.lloyds.com/regionalwatch > Europe Market Intelligence Account Manager: Govind Ratnam > [email protected]

Ireland> Ireland

NO YES

Back To > Content

COMPETITION BUSINESS CLASS DISTRIBUTION

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

North America (1 of 3) Download at: www.lloyds.com/regionalwatch > North America Market Intelligence Account Manager: Bruno Davila > [email protected]

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

MONTHLY UPDATES

USCalifornia >

NO NO

USTexas>

NO NOLLOYD’S ONLY

Florida> US

NO NOLLOYD’S ONLY

Illinois> US

NO NONONE LLOYD’S ONLY

New York> US

NOLLOYD’S ONLY NO

COMPETITION BUSINESS CLASS DISTRIBUTION

MONTHLY UPDATES

USUS Surplus Lines Total >

NO NO

Kentucky> US

NO NONONE LLOYD’S ONLY

BROKER VERSION

MARKET PRESENTATION

BROKER VERSION

MARKET PRESENTATION

Back To > Content

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

North America (2 of 3) Download at: www.lloyds.com/regionalwatch > North America Market Intelligence Account Manager: Bruno Davila > [email protected]

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

COMPETITION BUSINESS CLASS DISTRIBUTION

QUARTERLY UPDATES

PennsylvaniaUS

NO NONONE LLOYD’S ONLY LLOYD’S ONLY

New JerseyUS

NO NONONE LLOYD’S ONLY LLOYD’S ONLY

Georgia> US

NO NONONE LLOYD’S ONLY LLOYD’S ONLY

Louisiana> US

NO NONONE LLOYD’S ONLY LLOYD’S ONLY

South Carolina> US

NO NONONE LLOYD’S ONLY LLOYD’S ONLY

BROKER VERSION

MARKET PRESENTATION

Back To > Content

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

North America (3 of 3) Download at: www.lloyds.com/regionalwatch > North America Market Intelligence Account Manager: Bruno Davila > [email protected]

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

COMPETITION BUSINESS CLASS DISTRIBUTION

MONTHLY UPDATES

Ontario> Canada

NO NO

British Columbia> Canada

NO NOLLOYD’S ONLY

Alberta>Canada

NO NOLLOYD’S ONLY

Quebec> Canada

NOLLOYD’S ONLY NO

COMPETITION BUSINESS CLASS DISTRIBUTION

MONTHLY UPDATES

Canada Total > Canada

NO

LLOYD’S ONLY

LLOYD’S ONLY

BROKER VERSION

MARKET PRESENTATION

YES

Back To > Content

COMPETITION BUSINESS CLASS DISTRIBUTION

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

Asia Pacific (1 of 2) Download at: www.lloyds.com/regionalwatch > Asia Pacific Market Intelligence Account Manager: Govind Ratnam > [email protected]

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

MONTHLY UPDATES

ChinaChina>

NO NO

JapanJapan>

NO

Singapore> Singapore

NO NO

Australia> Australasia

YES NO

Hong Kong SAR> Hong Kong

NO NO

QUARTERLY UPDATES

COMPETITION BUSINESS CLASS DISTRIBUTION

Vietnam> Emerging Markets

NO NO

South Korea> Emerging Markets

NO NO

BROKER VERSION

MARKET PRESENTATION

BROKER VERSION

MARKET PRESENTATION

YES

Back To > Content

COMPETITION BUSINESS CLASS DISTRIBUTION

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

Asia Pacific (2 of 2) Download at: www.lloyds.com/regionalwatch > Asia Pacific Market Intelligence Account Manager: Govind Ratnam > [email protected]

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

ANNUAL UPDATES

Indonesia> Emerging Markets

NO NO

Taiwan> Emerging Markets

NO NO

Thailand> Emerging Markets

NO NO

Malaysia> Emerging Markets

NO NO

Philippines> Emerging Markets

NO NO

New Zealand> Australasia

NO NO

Macau> Emerging Markets

NO NONONE LLOYD’S ONLY LLOYD’S ONLY

BROKER VERSION

MARKET PRESENTATION

Back To > Content

COMPETITION BUSINESS CLASS DISTRIBUTION

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

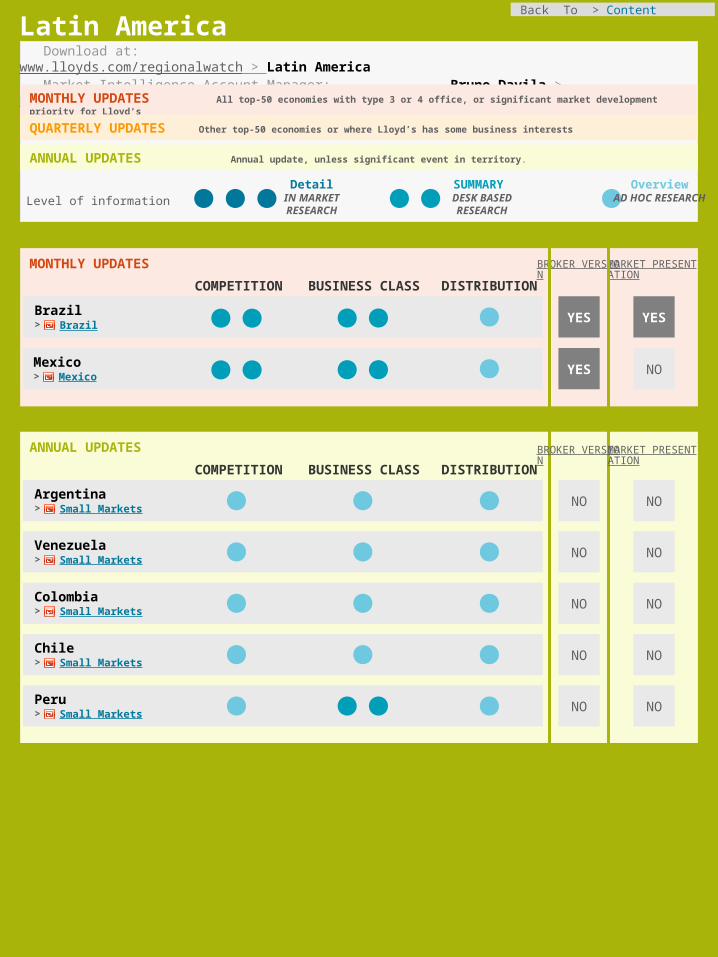

Latin America Download at: www.lloyds.com/regionalwatch > Latin America Market Intelligence Account Manager: Bruno Davila > [email protected]

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

MONTHLY UPDATES

MexicoMexico>

NO

BrazilBrazil>

COMPETITION BUSINESS CLASS DISTRIBUTION

ANNUAL UPDATES

Argentina> Small Markets

NO NO

Venezuela> Small Markets

NO NO

Colombia> Small Markets

NO NO

Chile> Small Markets

NO NO

Peru> Small Markets

NO NO

BROKER VERSION

MARKET PRESENTATION

BROKER VERSION

MARKET PRESENTATION

YES

YES

YES

Back To > Content

COMPETITION BUSINESS CLASS DISTRIBUTION

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

MONTHLY UPDATES

South Africa> IMEA

NO NO

QUARTERLY UPDATES

COMPETITION BUSINESS CLASS DISTRIBUTION

India> IMEA

NO NO

Saudi Arabia> IMEA

NO

UAE> IMEA

NO

Qatar> IMEA

NO

Bahrain> IMEA

NO

YES

YES

YES

YES

BROKER VERSION

MARKET PRESENTATION

BROKER VERSION

MARKET PRESENTATION

IMEA (1 of 2) Download at: www.lloyds.com/regionalwatch > IMEA Market Intelligence Account Manager: Govind Ratnam > [email protected]

Download at: www.lloyds.com/regionalwatch > IMEA Market Intelligence Account Manager: Filip Wuebbeler > [email protected]

Back To > Content

Level of informationDetail

IN MARKET RESEARCH

SUMMARY DESK BASED RESEARCH

OverviewAD HOC

RESEARCH

IMEA (2 of 2) Download at: www.lloyds.com/regionalwatch > IMEA Market Intelligence Account Manager: Filip Wuebbeler > [email protected]

MONTHLY UPDATES All top-50 economies with type 3 or 4 office, or significant market development priority for Lloyd’s

QUARTERLY UPDATES Other top-50 economies or where Lloyd’s has some business interests

ANNUAL UPDATES Annual update, unless significant event in territory.

ANNUAL UPDATES

COMPETITION BUSINESS CLASS DISTRIBUTION

Iran> IMEA

NO NO

Nigeria> IMEA

NO

Algeria> IMEA

NO

Pakistan> IMEA

NO

NO

NO

NO

Kuwait> IMEA

NONO

Egypt> IMEA

NONO

Bangladesh> IMEA

NONO

Kenya> IMEA

NONO

Sri Lanka> IMEA

NONO

BROKER VERSION

MARKET PRESENTATION

Back To > Content

How to use Regional Watch> ACCESS: www.lloyds.com/regionalwatch

Broker Version: Brokers and Managing Agents have access to summary version which can be downloaded without a password.

Managing Agent Version: Managing Agents have access to all Regional Watch dahsboards.

Managing agents can obtain their password from [email protected].

Managing Agent PASSWORD

> NAVIGATION:

All Regional Watch publications contain dahsboards, which are hyperlinked to more detailed information.

While the format may differ from dashboard to dashboard, the navigation principle remains constant.

© Lloyd ’s

Foreign InsurersDashboard

Distribution Dashboard

Insurance Dashboard

(Re- )Insurers Dashboard

Cli

ck A

ny B

ox T

o N

avig

ate

Shanghai Dashboard

Economy Dashboard

Premium Dashboard

DisclaimerDisclaimer

Macro Themes

Market Premium

Market Players

Lloyd’s

Distribution

Content

Lloyd’s Dashboard

Click Flagto navigate toContent

Glossary / Definitions

Links to Info Sources

Lloyd’s Data Limitations

UK / China Financial Sector Stakeholders

© Lloyd ’s

Foreign InsurersDashboard

Distribution Dashboard

Insurance Dashboard

(Re- )Insurers Dashboard

Cli

ck A

ny B

ox T

o N

avig

ate

Cli

ck A

ny B

ox T

o N

avig

ate

Shanghai Dashboard

Economy Dashboard

Premium Dashboard

DisclaimerDisclaimerDisclaimerDisclaimer

Macro Themes

Market Premium

Market Players

Lloyd’s

Distribution

Content

Lloyd’s Dashboard

Click Flagto navigate toContent

Glossary / Definitions

Links to Info Sources

Lloyd’s Data Limitations

UK / China Financial Sector Stakeholders

CN:Economy Dashboard

DisclaimerDisclaimer

Map and regional

economic output

> CLICK ANY BOX FOR DETAIL

Macro drivers of economy

Growth sectors of economy

Summary

Ways of Doing

business

Strong economic growth amid domestic stimuliChina as an export-driven economyis vulnerable to the external environment.

Shrinking external demand, overcapacity in some sectors, difficult business conditions fo r enterprises, rising unemployment in urban areas and greater downwardpressure on economic growth.

Stimulus to focus on internal demand growth; tax reductions for enterprises

Series of interest rate cutsand other policy developments to improve business and consumer confidence. Lending has been improving, easing credit situati on.

Foreign exchange reserves of USD 1.95 trillion

Fundamentals remain strong, domestic demand to improve. China’s economic growth will depend on access to an alternative market for its exports. China to drive Asian Growth.

China’s Stimulus Packageof USD 586bn:

Stimulus package with focus on infrastructure development: housing, transport and rural

Tax reformsto reduce burden on large, small and medium industries

Industry specific support for Automotive and Steel

Support plans for the auto, steel, shipbuilding, textile and machinerymanufacturing, electronics, petrochemicals and light industry

Successive interest rate cutsto boost liquidity

Market Intelligence based on: Berkley APEC Study Center, “Responding to the Global Crisis:Market and Nonmarket Strategies for Success”, (March 2009)

Back To > Content

CN:Economy Dashboard

DisclaimerDisclaimerDisclaimerDisclaimer

Map and regional

economic output

> CLICK ANY BOX FOR DETAIL

Macro drivers of economy

Growth sectors of economy

Summary

Ways of Doing

business

Strong economic growth amid domestic stimuliChina as an export-driven economyis vulnerable to the external environment.

Shrinking external demand, overcapacity in some sectors, difficult business conditions fo r enterprises, rising unemployment in urban areas and greater downwardpressure on economic growth.

Stimulus to focus on internal demand growth; tax reductions for enterprises

Series of interest rate cutsand other policy developments to improve business and consumer confidence. Lending has been improving, easing credit situati on.

Foreign exchange reserves of USD 1.95 trillion

Fundamentals remain strong, domestic demand to improve. China’s economic growth will depend on access to an alternative market for its exports. China to drive Asian Growth.

China’s Stimulus Packageof USD 586bn:

Stimulus package with focus on infrastructure development: housing, transport and rural

Tax reformsto reduce burden on large, small and medium industries

Industry specific support for Automotive and Steel

Support plans for the auto, steel, shipbuilding, textile and machinerymanufacturing, electronics, petrochemicals and light industry

Successive interest rate cutsto boost liquidity

Market Intelligence based on: Berkley APEC Study Center, “Responding to the Global Crisis:Market and Nonmarket Strategies for Success”, (March 2009)

Back To > Content

Click

©Lloyd’s

Energy / Resources

Environment / Health

Growth Sectors

Ports

Aviation

Exports & Imports

Regional GDP Per Capita

Map of China

Labour Force

Legal / IPR

Middle Class

Brand Consciousness

Stock Markets

Currency

Government Priorities

Macro Indicators

Business Culture

©Lloyd’s

Energy / Resources

Environment / Health

Growth Sectors

Ports

Aviation

Exports & Imports

Regional GDP Per Capita

Map of China

Labour Force

Legal / IPR

Middle Class

Brand Consciousness

Stock Markets

Currency

Government Priorities

Macro Indicators

Business Culture

Click

Foreign InsurersDashboard

Distribution Dashboard

Insurance Dashboard

(Re- )Insurers Dashboard

Shanghai Dashboard

Economy Dashboard

Premium Dashboard

Lloyd’s Dashboard

Click

Foreign InsurersDashboard

Distribution Dashboard

Insurance Dashboard

(Re- )Insurers Dashboard

Shanghai Dashboard

Economy Dashboard

Premium Dashboard

Lloyd’s Dashboard

Foreign InsurersDashboard

Distribution Dashboard

Insurance Dashboard

(Re- )Insurers Dashboard

Shanghai Dashboard

Economy Dashboard

Foreign InsurersDashboard

Distribution Dashboard

Insurance Dashboard

(Re- )Insurers Dashboard

Shanghai Dashboard

Economy Dashboard

Premium Dashboard

Lloyd’s Dashboard

Premium Dashboard

Lloyd’s Dashboard

©Lloyd’s

CN:Economy

Business Culture (2 of 2)

Business meetingsare punctual.It is advisable to arrive a bit early at meetings. Negotiationsoften proceed at a slow pace and conversations may initially be very non-committal – instead of saying “yes” or “no”, more likely comments are “we will think about it” or “we will see”. You should always have your own interpreter at any meeting, to ensure the

translation is done correctly and to pick up on conversations between the opposite party.

Gifts indicate a desire to establish a relationship. Gifts need not be expensive, but they should always be wrappedand you should avoid using black or white paper. Gifts normally will not be opened in your presence.

Something representative of your country or your town will be particularly appreciated. Never give a clock or white flowers, as these signify death. Never give sharp objects such as knives or scissors as they signify cutting of a relationship. Four is an unlucky number. Lucky numbers are six and eight.

Learn a few simple Chinese words. This not only shows respect and interest in the Chinese language and culture, but also provides a good icebreaking topic. Try to avoid discussing political or religious topics publicly. Chinese food, places to visit and entertainment are good topics.

Market Intelligence based on: British Chambers of Commerce, “The British Chamber of Commerce Shanghai”, (November 2009)Soft

In

tellig

en

ce

DisclaimerDisclaimer

Back To > Economy DashboardBack To > Economy DashboardBack To > Economy Dashboard

Click

Back To > Content

Click

Back To > ContentBack To > Content

All Regional Watch

presentations use dashboards

which lead to more information

More details can be viewed in

subsections by clicking:

BOXES

ARROWS >

UNDERLINED WORDS

OR

OR

To Return to the summary

dashboard just click the

appropriate link on the top of each slide

Regional Dashboard

Back To > Content

DisclaimerThis document is intended for general information purposes only. Whilst all care has been taken to ensure the accuracy of the information Lloyd's does not accept any responsibility for any errors or omissions. Lloyd's does not accept any responsibility or liability for any loss to any person acting or refraining from action as a result of, but not limited to, any statement, fact, figure, expression of opinion or belief obtained in this document.