regulation, supervision, and risk management ofand risk management of financial ... ·...

TRANSCRIPT

1

Regulation Supervision and Risk Management ofand Risk Management of Financial Institutions

An OECD perspective

Stephen A LumpkinPrincipal Administrator OECD Financial Affairs Division

February 2012

1

The interlinked components of risk management

Market disciplineCompetition

Haircuts

In finance discipline always has to be imposed if not by governance or the market then by regulators and supervisors

2

2

Risk is inherent to financial intermediation

Banks Securities Insurers PurposeBanks

bull Lendingbull Maturity

transformationbull =gt credit risk

liquidity risk market risk

Securities firms

bull Mark-to-market basis

bull Short-term funding

bull =gt Funding and liquidity risks

Insurersbull Technical risks

(under-pricing under-provisioning)

bull Investment risks

bull Other risks

Purposebull Match surplus

of capital with demand

bull Facilitate real economic activity

bull Through coverage and proper management of risks

3

What can go wrong

bull Take on risks as long as the cost of doing so makes sense from the institutionrsquos own point of view of its balance sheet (ie profit maximisation)

bull There may be little economic incentive to internalise costs associated with the protection of third parties or th t h l

Own goals vs collective

rationalitythe system as a whole

bull Errors of judgment flawed business models (risks to safety and soundness)

bull Failures pose significant problems for customers and clients especially individuals and SMEs (risks to clients)Some institutions

will err in the

4

bull Asset quality problems can lead banks to become reluctant to extend new loans or refuse requests for rollovers

bull Contagion (risks to the system)

process

3

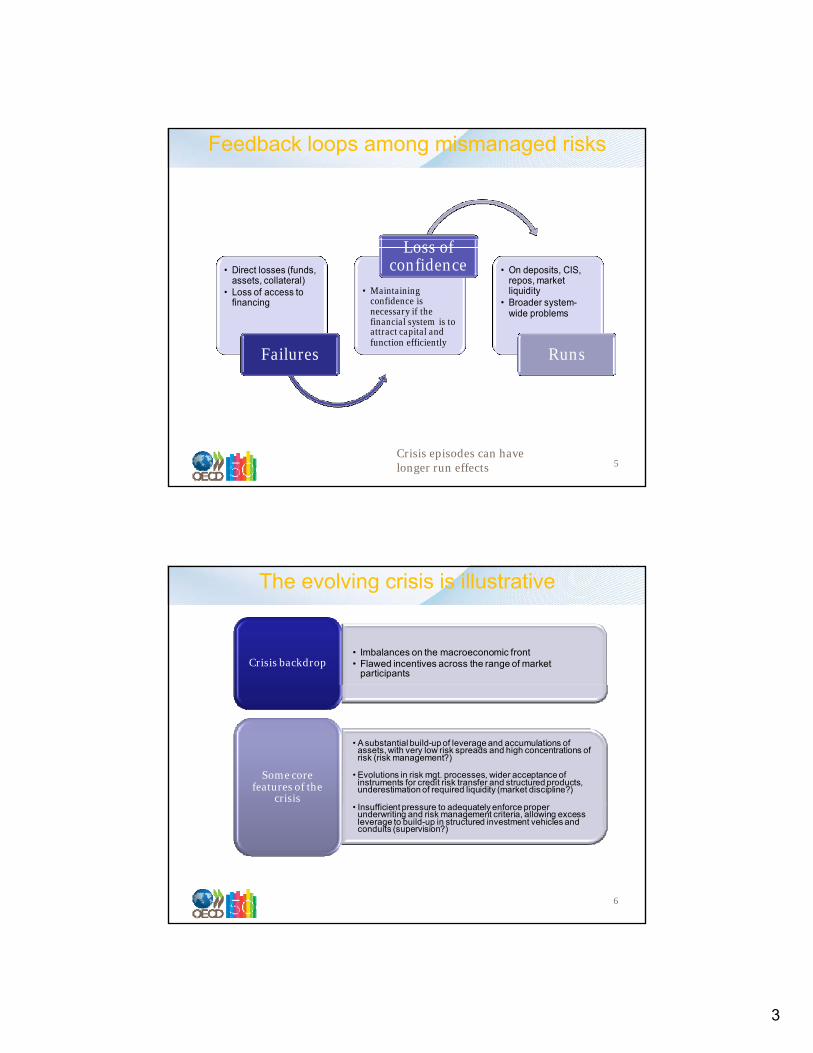

Feedback loops among mismanaged risks

Loss of bull Direct losses (funds

assets collateral)bull Loss of access to

financing

Failures

bull Maintaining confidence is necessary if the financial system is to attract capital and function efficiently

Loss of confidence bull On deposits CIS

repos market liquidity

bull Broader system-wide problems

Runs

Crisis episodes can have longer run effects 5

The evolving crisis is illustrative

bull Imbalances on the macroeconomic frontbull Flawed incentives across the range of market

participantsCrisis backdrop

bull A substantial build-up of leverage and accumulations of assets with very low risk spreads and high concentrations of risk (risk management)

bull Evolutions in risk mgt processes wider acceptance of instruments for credit risk transfer and structured products underestimation of required liquidity (market discipline)

I ffi i t t d t l f

Some core features of the

crisis

6

bull Insufficient pressure to adequately enforce proper underwriting and risk management criteria allowing excess leverage to build-up in structured investment vehicles and conduits (supervision)

4

Crisis outcomes are not so rare hellip

70

80

90

1200

1400

October87 crash

AsiaTCM

Tech bust

Worldcom accounting scandals

Sep 08 GSEtakeoverLehman collapse

20

30

40

50

60

400

600

800

1000

Volatility inde

x

Spreads (bps)

SampLLBO crisis

Sep11 2001

JulAug07 severe sub‐prime effects on money markets

Mar‐08 Bear Sterns collapse

AprilMay 2010 Start

of EUsovereigndebt crisis

7

0

10

0

200

High yield ‐ US (BofA‐ML) EMBI global (JPM) VIX (rhs)

hellipand the effects can be significant

Growth of SME business loans1 2008-10

Year-on-year growth rate as a percentage

Country 2008 2009 2010Country 2008 2009 2010

Canada -01 37 -09

Chile 113 69 88

Denmark -137 -192 229

Finland 26 -163 -220

France 43 10 57

Hungary 49 -68 13

Italy 21 12 66

Korea 141 55 -10

The Netherlands -50 -242 51

Portugal 92 18 -20

Slovakia 341 -03

Financing SMEs and Entrepreneurs An OECD Scoreboard forthcoming in April

8

Slovenia 167 -09 -88

Sweden 72 204

Switzerland 59 53 13

Thailand 95 74 72

United Kingdom 82 14 -61

United States 36 -23 -62

Notes 1 Definitions differ across countries

5

Enterprises by size class in 2007

100

1‐9 10‐19 20‐49 50‐249 250+

20

30

40

50

60

70

80

90

OECD Entrepreneurship at a Glance 2011

9

0

10

20

Employment by size class in 2007

90

100

1‐9 10‐19 20‐49 50‐249 250+

20

30

40

50

60

70

80

90

OECD Entrepreneurship at a Glance 2011

10

0

10

6

hellip and the costs have sometimes been high

11

Source S Schich and B Kim (2010) ldquoSystemic Financial crises how to fund resolutionrdquo OECD

What should be done

bull Prevention is better than cure but how best to do it

High costs of widespread distress

B d b l h

Limits of risk managementbull Boom-and-bust cycles are recurrent phenomenabull Systemic risks can hide in the interactions between institutions products

and markets and not necessarily with particular institutions

bull Only as effective as the broader governance frameworkbull Weak mgt systems or ineffective or incompetent boards =gt cannot rely

solely on firewalls and related control mechanisms to control or mitigate conflicts of interest or other risks

Limits of market discipline

12

bull Difficult in practice to directly control behaviour without sacrificing some measure of efficiency and innovation or creating adverse incentive effects

Limits of supervision

7

What about structure

250

300

350

400

250

300

350

400

300

350

400

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

GBR

CAN

USA

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

CHN

IND

IDN

300

350

400

13

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

AUS

JPN

KOR

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

BRA

MEX

ARG

Total assets of largest 3 banks as share of GDP

Balance sheets of large financial groups

bull Large integrated institutions may not have a greater risk of failure than smaller institutions

bull Might fare better because of the diversity of their activities or the diversity of their funding sources

More risky elements but more

diversification activities or the diversity of their funding sources

bull Increases in cross-sector cross-border or cross-risk type correlations limit diversification benefits

bull If not properly managed these risk exposures can precipitate institutional failures or have broader implicationsBut risk factors

14

precipitate institutional failures or have broader implications

bull And given cross-sector and cross-border inter-linkages once problems do erupt they tend to be transferred from one market segment or region to another

can interact

8

The structure-behaviour nexus

Regulate Regulate Structure

Some activities not compatible from a direct risk or moral

hazard standpoint

Should not be combined

Regulate BehaviourIssue is not structure per se

But implications of structure for risk management amp internal controls

15

Opaque universal banking model vs Non-operating holding company structure with firewalls

Would the separation of traditional and non-traditional bank business make the sector safer

Commercial

Bank external funding

trading etc

BrokerDir equity sales IPSs etc

Invest Banking position taking

securities business

BrokerDir equity sales IPSs etc

Commercial Bank

InsuranceInvestmentBank

Source The Financial Crisis Reform and Exit Strategies OECD September 2009 Paris available at wwwoecdorgdataoecd554743091457pdf 16

Wealth management

private clients etc

Insurance general life reinsurance

Wealth Broker Management Dealer

9

Linked components of risk management

bull Possible risk of contagion across group members from shared brand name and damage to grouprsquos reputation

bull Entire governance framework must be appropriate for risk profile and business model

Structure alone not sufficient

bull Direct but not sole responsibility for ensuring a proper mix and mgt of institutionrsquos assets and liabilities

Role of managers in risk mgt

bull Should provide an external constraint on managerial discretionbull External governance mechanisms are at a disadvantage in the case of

complex structures

Effective market discipline

Normal competitive mkt function

17

bull Some institutionrsquos asset-liability mix risk mgt techniques or entire business model will prove to be deficient and result in losses or failure

p

bull Is the problem idiosyncratic likely to spread to other institutions having a similar structure or business model or further still

Implications

Thanks very much for tt tiyour attention

Any questions

18

2

Risk is inherent to financial intermediation

Banks Securities Insurers PurposeBanks

bull Lendingbull Maturity

transformationbull =gt credit risk

liquidity risk market risk

Securities firms

bull Mark-to-market basis

bull Short-term funding

bull =gt Funding and liquidity risks

Insurersbull Technical risks

(under-pricing under-provisioning)

bull Investment risks

bull Other risks

Purposebull Match surplus

of capital with demand

bull Facilitate real economic activity

bull Through coverage and proper management of risks

3

What can go wrong

bull Take on risks as long as the cost of doing so makes sense from the institutionrsquos own point of view of its balance sheet (ie profit maximisation)

bull There may be little economic incentive to internalise costs associated with the protection of third parties or th t h l

Own goals vs collective

rationalitythe system as a whole

bull Errors of judgment flawed business models (risks to safety and soundness)

bull Failures pose significant problems for customers and clients especially individuals and SMEs (risks to clients)Some institutions

will err in the

4

bull Asset quality problems can lead banks to become reluctant to extend new loans or refuse requests for rollovers

bull Contagion (risks to the system)

process

3

Feedback loops among mismanaged risks

Loss of bull Direct losses (funds

assets collateral)bull Loss of access to

financing

Failures

bull Maintaining confidence is necessary if the financial system is to attract capital and function efficiently

Loss of confidence bull On deposits CIS

repos market liquidity

bull Broader system-wide problems

Runs

Crisis episodes can have longer run effects 5

The evolving crisis is illustrative

bull Imbalances on the macroeconomic frontbull Flawed incentives across the range of market

participantsCrisis backdrop

bull A substantial build-up of leverage and accumulations of assets with very low risk spreads and high concentrations of risk (risk management)

bull Evolutions in risk mgt processes wider acceptance of instruments for credit risk transfer and structured products underestimation of required liquidity (market discipline)

I ffi i t t d t l f

Some core features of the

crisis

6

bull Insufficient pressure to adequately enforce proper underwriting and risk management criteria allowing excess leverage to build-up in structured investment vehicles and conduits (supervision)

4

Crisis outcomes are not so rare hellip

70

80

90

1200

1400

October87 crash

AsiaTCM

Tech bust

Worldcom accounting scandals

Sep 08 GSEtakeoverLehman collapse

20

30

40

50

60

400

600

800

1000

Volatility inde

x

Spreads (bps)

SampLLBO crisis

Sep11 2001

JulAug07 severe sub‐prime effects on money markets

Mar‐08 Bear Sterns collapse

AprilMay 2010 Start

of EUsovereigndebt crisis

7

0

10

0

200

High yield ‐ US (BofA‐ML) EMBI global (JPM) VIX (rhs)

hellipand the effects can be significant

Growth of SME business loans1 2008-10

Year-on-year growth rate as a percentage

Country 2008 2009 2010Country 2008 2009 2010

Canada -01 37 -09

Chile 113 69 88

Denmark -137 -192 229

Finland 26 -163 -220

France 43 10 57

Hungary 49 -68 13

Italy 21 12 66

Korea 141 55 -10

The Netherlands -50 -242 51

Portugal 92 18 -20

Slovakia 341 -03

Financing SMEs and Entrepreneurs An OECD Scoreboard forthcoming in April

8

Slovenia 167 -09 -88

Sweden 72 204

Switzerland 59 53 13

Thailand 95 74 72

United Kingdom 82 14 -61

United States 36 -23 -62

Notes 1 Definitions differ across countries

5

Enterprises by size class in 2007

100

1‐9 10‐19 20‐49 50‐249 250+

20

30

40

50

60

70

80

90

OECD Entrepreneurship at a Glance 2011

9

0

10

20

Employment by size class in 2007

90

100

1‐9 10‐19 20‐49 50‐249 250+

20

30

40

50

60

70

80

90

OECD Entrepreneurship at a Glance 2011

10

0

10

6

hellip and the costs have sometimes been high

11

Source S Schich and B Kim (2010) ldquoSystemic Financial crises how to fund resolutionrdquo OECD

What should be done

bull Prevention is better than cure but how best to do it

High costs of widespread distress

B d b l h

Limits of risk managementbull Boom-and-bust cycles are recurrent phenomenabull Systemic risks can hide in the interactions between institutions products

and markets and not necessarily with particular institutions

bull Only as effective as the broader governance frameworkbull Weak mgt systems or ineffective or incompetent boards =gt cannot rely

solely on firewalls and related control mechanisms to control or mitigate conflicts of interest or other risks

Limits of market discipline

12

bull Difficult in practice to directly control behaviour without sacrificing some measure of efficiency and innovation or creating adverse incentive effects

Limits of supervision

7

What about structure

250

300

350

400

250

300

350

400

300

350

400

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

GBR

CAN

USA

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

CHN

IND

IDN

300

350

400

13

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

AUS

JPN

KOR

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

BRA

MEX

ARG

Total assets of largest 3 banks as share of GDP

Balance sheets of large financial groups

bull Large integrated institutions may not have a greater risk of failure than smaller institutions

bull Might fare better because of the diversity of their activities or the diversity of their funding sources

More risky elements but more

diversification activities or the diversity of their funding sources

bull Increases in cross-sector cross-border or cross-risk type correlations limit diversification benefits

bull If not properly managed these risk exposures can precipitate institutional failures or have broader implicationsBut risk factors

14

precipitate institutional failures or have broader implications

bull And given cross-sector and cross-border inter-linkages once problems do erupt they tend to be transferred from one market segment or region to another

can interact

8

The structure-behaviour nexus

Regulate Regulate Structure

Some activities not compatible from a direct risk or moral

hazard standpoint

Should not be combined

Regulate BehaviourIssue is not structure per se

But implications of structure for risk management amp internal controls

15

Opaque universal banking model vs Non-operating holding company structure with firewalls

Would the separation of traditional and non-traditional bank business make the sector safer

Commercial

Bank external funding

trading etc

BrokerDir equity sales IPSs etc

Invest Banking position taking

securities business

BrokerDir equity sales IPSs etc

Commercial Bank

InsuranceInvestmentBank

Source The Financial Crisis Reform and Exit Strategies OECD September 2009 Paris available at wwwoecdorgdataoecd554743091457pdf 16

Wealth management

private clients etc

Insurance general life reinsurance

Wealth Broker Management Dealer

9

Linked components of risk management

bull Possible risk of contagion across group members from shared brand name and damage to grouprsquos reputation

bull Entire governance framework must be appropriate for risk profile and business model

Structure alone not sufficient

bull Direct but not sole responsibility for ensuring a proper mix and mgt of institutionrsquos assets and liabilities

Role of managers in risk mgt

bull Should provide an external constraint on managerial discretionbull External governance mechanisms are at a disadvantage in the case of

complex structures

Effective market discipline

Normal competitive mkt function

17

bull Some institutionrsquos asset-liability mix risk mgt techniques or entire business model will prove to be deficient and result in losses or failure

p

bull Is the problem idiosyncratic likely to spread to other institutions having a similar structure or business model or further still

Implications

Thanks very much for tt tiyour attention

Any questions

18

3

Feedback loops among mismanaged risks

Loss of bull Direct losses (funds

assets collateral)bull Loss of access to

financing

Failures

bull Maintaining confidence is necessary if the financial system is to attract capital and function efficiently

Loss of confidence bull On deposits CIS

repos market liquidity

bull Broader system-wide problems

Runs

Crisis episodes can have longer run effects 5

The evolving crisis is illustrative

bull Imbalances on the macroeconomic frontbull Flawed incentives across the range of market

participantsCrisis backdrop

bull A substantial build-up of leverage and accumulations of assets with very low risk spreads and high concentrations of risk (risk management)

bull Evolutions in risk mgt processes wider acceptance of instruments for credit risk transfer and structured products underestimation of required liquidity (market discipline)

I ffi i t t d t l f

Some core features of the

crisis

6

bull Insufficient pressure to adequately enforce proper underwriting and risk management criteria allowing excess leverage to build-up in structured investment vehicles and conduits (supervision)

4

Crisis outcomes are not so rare hellip

70

80

90

1200

1400

October87 crash

AsiaTCM

Tech bust

Worldcom accounting scandals

Sep 08 GSEtakeoverLehman collapse

20

30

40

50

60

400

600

800

1000

Volatility inde

x

Spreads (bps)

SampLLBO crisis

Sep11 2001

JulAug07 severe sub‐prime effects on money markets

Mar‐08 Bear Sterns collapse

AprilMay 2010 Start

of EUsovereigndebt crisis

7

0

10

0

200

High yield ‐ US (BofA‐ML) EMBI global (JPM) VIX (rhs)

hellipand the effects can be significant

Growth of SME business loans1 2008-10

Year-on-year growth rate as a percentage

Country 2008 2009 2010Country 2008 2009 2010

Canada -01 37 -09

Chile 113 69 88

Denmark -137 -192 229

Finland 26 -163 -220

France 43 10 57

Hungary 49 -68 13

Italy 21 12 66

Korea 141 55 -10

The Netherlands -50 -242 51

Portugal 92 18 -20

Slovakia 341 -03

Financing SMEs and Entrepreneurs An OECD Scoreboard forthcoming in April

8

Slovenia 167 -09 -88

Sweden 72 204

Switzerland 59 53 13

Thailand 95 74 72

United Kingdom 82 14 -61

United States 36 -23 -62

Notes 1 Definitions differ across countries

5

Enterprises by size class in 2007

100

1‐9 10‐19 20‐49 50‐249 250+

20

30

40

50

60

70

80

90

OECD Entrepreneurship at a Glance 2011

9

0

10

20

Employment by size class in 2007

90

100

1‐9 10‐19 20‐49 50‐249 250+

20

30

40

50

60

70

80

90

OECD Entrepreneurship at a Glance 2011

10

0

10

6

hellip and the costs have sometimes been high

11

Source S Schich and B Kim (2010) ldquoSystemic Financial crises how to fund resolutionrdquo OECD

What should be done

bull Prevention is better than cure but how best to do it

High costs of widespread distress

B d b l h

Limits of risk managementbull Boom-and-bust cycles are recurrent phenomenabull Systemic risks can hide in the interactions between institutions products

and markets and not necessarily with particular institutions

bull Only as effective as the broader governance frameworkbull Weak mgt systems or ineffective or incompetent boards =gt cannot rely

solely on firewalls and related control mechanisms to control or mitigate conflicts of interest or other risks

Limits of market discipline

12

bull Difficult in practice to directly control behaviour without sacrificing some measure of efficiency and innovation or creating adverse incentive effects

Limits of supervision

7

What about structure

250

300

350

400

250

300

350

400

300

350

400

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

GBR

CAN

USA

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

CHN

IND

IDN

300

350

400

13

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

AUS

JPN

KOR

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

BRA

MEX

ARG

Total assets of largest 3 banks as share of GDP

Balance sheets of large financial groups

bull Large integrated institutions may not have a greater risk of failure than smaller institutions

bull Might fare better because of the diversity of their activities or the diversity of their funding sources

More risky elements but more

diversification activities or the diversity of their funding sources

bull Increases in cross-sector cross-border or cross-risk type correlations limit diversification benefits

bull If not properly managed these risk exposures can precipitate institutional failures or have broader implicationsBut risk factors

14

precipitate institutional failures or have broader implications

bull And given cross-sector and cross-border inter-linkages once problems do erupt they tend to be transferred from one market segment or region to another

can interact

8

The structure-behaviour nexus

Regulate Regulate Structure

Some activities not compatible from a direct risk or moral

hazard standpoint

Should not be combined

Regulate BehaviourIssue is not structure per se

But implications of structure for risk management amp internal controls

15

Opaque universal banking model vs Non-operating holding company structure with firewalls

Would the separation of traditional and non-traditional bank business make the sector safer

Commercial

Bank external funding

trading etc

BrokerDir equity sales IPSs etc

Invest Banking position taking

securities business

BrokerDir equity sales IPSs etc

Commercial Bank

InsuranceInvestmentBank

Source The Financial Crisis Reform and Exit Strategies OECD September 2009 Paris available at wwwoecdorgdataoecd554743091457pdf 16

Wealth management

private clients etc

Insurance general life reinsurance

Wealth Broker Management Dealer

9

Linked components of risk management

bull Possible risk of contagion across group members from shared brand name and damage to grouprsquos reputation

bull Entire governance framework must be appropriate for risk profile and business model

Structure alone not sufficient

bull Direct but not sole responsibility for ensuring a proper mix and mgt of institutionrsquos assets and liabilities

Role of managers in risk mgt

bull Should provide an external constraint on managerial discretionbull External governance mechanisms are at a disadvantage in the case of

complex structures

Effective market discipline

Normal competitive mkt function

17

bull Some institutionrsquos asset-liability mix risk mgt techniques or entire business model will prove to be deficient and result in losses or failure

p

bull Is the problem idiosyncratic likely to spread to other institutions having a similar structure or business model or further still

Implications

Thanks very much for tt tiyour attention

Any questions

18

4

Crisis outcomes are not so rare hellip

70

80

90

1200

1400

October87 crash

AsiaTCM

Tech bust

Worldcom accounting scandals

Sep 08 GSEtakeoverLehman collapse

20

30

40

50

60

400

600

800

1000

Volatility inde

x

Spreads (bps)

SampLLBO crisis

Sep11 2001

JulAug07 severe sub‐prime effects on money markets

Mar‐08 Bear Sterns collapse

AprilMay 2010 Start

of EUsovereigndebt crisis

7

0

10

0

200

High yield ‐ US (BofA‐ML) EMBI global (JPM) VIX (rhs)

hellipand the effects can be significant

Growth of SME business loans1 2008-10

Year-on-year growth rate as a percentage

Country 2008 2009 2010Country 2008 2009 2010

Canada -01 37 -09

Chile 113 69 88

Denmark -137 -192 229

Finland 26 -163 -220

France 43 10 57

Hungary 49 -68 13

Italy 21 12 66

Korea 141 55 -10

The Netherlands -50 -242 51

Portugal 92 18 -20

Slovakia 341 -03

Financing SMEs and Entrepreneurs An OECD Scoreboard forthcoming in April

8

Slovenia 167 -09 -88

Sweden 72 204

Switzerland 59 53 13

Thailand 95 74 72

United Kingdom 82 14 -61

United States 36 -23 -62

Notes 1 Definitions differ across countries

5

Enterprises by size class in 2007

100

1‐9 10‐19 20‐49 50‐249 250+

20

30

40

50

60

70

80

90

OECD Entrepreneurship at a Glance 2011

9

0

10

20

Employment by size class in 2007

90

100

1‐9 10‐19 20‐49 50‐249 250+

20

30

40

50

60

70

80

90

OECD Entrepreneurship at a Glance 2011

10

0

10

6

hellip and the costs have sometimes been high

11

Source S Schich and B Kim (2010) ldquoSystemic Financial crises how to fund resolutionrdquo OECD

What should be done

bull Prevention is better than cure but how best to do it

High costs of widespread distress

B d b l h

Limits of risk managementbull Boom-and-bust cycles are recurrent phenomenabull Systemic risks can hide in the interactions between institutions products

and markets and not necessarily with particular institutions

bull Only as effective as the broader governance frameworkbull Weak mgt systems or ineffective or incompetent boards =gt cannot rely

solely on firewalls and related control mechanisms to control or mitigate conflicts of interest or other risks

Limits of market discipline

12

bull Difficult in practice to directly control behaviour without sacrificing some measure of efficiency and innovation or creating adverse incentive effects

Limits of supervision

7

What about structure

250

300

350

400

250

300

350

400

300

350

400

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

GBR

CAN

USA

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

CHN

IND

IDN

300

350

400

13

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

AUS

JPN

KOR

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

BRA

MEX

ARG

Total assets of largest 3 banks as share of GDP

Balance sheets of large financial groups

bull Large integrated institutions may not have a greater risk of failure than smaller institutions

bull Might fare better because of the diversity of their activities or the diversity of their funding sources

More risky elements but more

diversification activities or the diversity of their funding sources

bull Increases in cross-sector cross-border or cross-risk type correlations limit diversification benefits

bull If not properly managed these risk exposures can precipitate institutional failures or have broader implicationsBut risk factors

14

precipitate institutional failures or have broader implications

bull And given cross-sector and cross-border inter-linkages once problems do erupt they tend to be transferred from one market segment or region to another

can interact

8

The structure-behaviour nexus

Regulate Regulate Structure

Some activities not compatible from a direct risk or moral

hazard standpoint

Should not be combined

Regulate BehaviourIssue is not structure per se

But implications of structure for risk management amp internal controls

15

Opaque universal banking model vs Non-operating holding company structure with firewalls

Would the separation of traditional and non-traditional bank business make the sector safer

Commercial

Bank external funding

trading etc

BrokerDir equity sales IPSs etc

Invest Banking position taking

securities business

BrokerDir equity sales IPSs etc

Commercial Bank

InsuranceInvestmentBank

Source The Financial Crisis Reform and Exit Strategies OECD September 2009 Paris available at wwwoecdorgdataoecd554743091457pdf 16

Wealth management

private clients etc

Insurance general life reinsurance

Wealth Broker Management Dealer

9

Linked components of risk management

bull Possible risk of contagion across group members from shared brand name and damage to grouprsquos reputation

bull Entire governance framework must be appropriate for risk profile and business model

Structure alone not sufficient

bull Direct but not sole responsibility for ensuring a proper mix and mgt of institutionrsquos assets and liabilities

Role of managers in risk mgt

bull Should provide an external constraint on managerial discretionbull External governance mechanisms are at a disadvantage in the case of

complex structures

Effective market discipline

Normal competitive mkt function

17

bull Some institutionrsquos asset-liability mix risk mgt techniques or entire business model will prove to be deficient and result in losses or failure

p

bull Is the problem idiosyncratic likely to spread to other institutions having a similar structure or business model or further still

Implications

Thanks very much for tt tiyour attention

Any questions

18

5

Enterprises by size class in 2007

100

1‐9 10‐19 20‐49 50‐249 250+

20

30

40

50

60

70

80

90

OECD Entrepreneurship at a Glance 2011

9

0

10

20

Employment by size class in 2007

90

100

1‐9 10‐19 20‐49 50‐249 250+

20

30

40

50

60

70

80

90

OECD Entrepreneurship at a Glance 2011

10

0

10

6

hellip and the costs have sometimes been high

11

Source S Schich and B Kim (2010) ldquoSystemic Financial crises how to fund resolutionrdquo OECD

What should be done

bull Prevention is better than cure but how best to do it

High costs of widespread distress

B d b l h

Limits of risk managementbull Boom-and-bust cycles are recurrent phenomenabull Systemic risks can hide in the interactions between institutions products

and markets and not necessarily with particular institutions

bull Only as effective as the broader governance frameworkbull Weak mgt systems or ineffective or incompetent boards =gt cannot rely

solely on firewalls and related control mechanisms to control or mitigate conflicts of interest or other risks

Limits of market discipline

12

bull Difficult in practice to directly control behaviour without sacrificing some measure of efficiency and innovation or creating adverse incentive effects

Limits of supervision

7

What about structure

250

300

350

400

250

300

350

400

300

350

400

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

GBR

CAN

USA

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

CHN

IND

IDN

300

350

400

13

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

AUS

JPN

KOR

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

BRA

MEX

ARG

Total assets of largest 3 banks as share of GDP

Balance sheets of large financial groups

bull Large integrated institutions may not have a greater risk of failure than smaller institutions

bull Might fare better because of the diversity of their activities or the diversity of their funding sources

More risky elements but more

diversification activities or the diversity of their funding sources

bull Increases in cross-sector cross-border or cross-risk type correlations limit diversification benefits

bull If not properly managed these risk exposures can precipitate institutional failures or have broader implicationsBut risk factors

14

precipitate institutional failures or have broader implications

bull And given cross-sector and cross-border inter-linkages once problems do erupt they tend to be transferred from one market segment or region to another

can interact

8

The structure-behaviour nexus

Regulate Regulate Structure

Some activities not compatible from a direct risk or moral

hazard standpoint

Should not be combined

Regulate BehaviourIssue is not structure per se

But implications of structure for risk management amp internal controls

15

Opaque universal banking model vs Non-operating holding company structure with firewalls

Would the separation of traditional and non-traditional bank business make the sector safer

Commercial

Bank external funding

trading etc

BrokerDir equity sales IPSs etc

Invest Banking position taking

securities business

BrokerDir equity sales IPSs etc

Commercial Bank

InsuranceInvestmentBank

Source The Financial Crisis Reform and Exit Strategies OECD September 2009 Paris available at wwwoecdorgdataoecd554743091457pdf 16

Wealth management

private clients etc

Insurance general life reinsurance

Wealth Broker Management Dealer

9

Linked components of risk management

bull Possible risk of contagion across group members from shared brand name and damage to grouprsquos reputation

bull Entire governance framework must be appropriate for risk profile and business model

Structure alone not sufficient

bull Direct but not sole responsibility for ensuring a proper mix and mgt of institutionrsquos assets and liabilities

Role of managers in risk mgt

bull Should provide an external constraint on managerial discretionbull External governance mechanisms are at a disadvantage in the case of

complex structures

Effective market discipline

Normal competitive mkt function

17

bull Some institutionrsquos asset-liability mix risk mgt techniques or entire business model will prove to be deficient and result in losses or failure

p

bull Is the problem idiosyncratic likely to spread to other institutions having a similar structure or business model or further still

Implications

Thanks very much for tt tiyour attention

Any questions

18

6

hellip and the costs have sometimes been high

11

Source S Schich and B Kim (2010) ldquoSystemic Financial crises how to fund resolutionrdquo OECD

What should be done

bull Prevention is better than cure but how best to do it

High costs of widespread distress

B d b l h

Limits of risk managementbull Boom-and-bust cycles are recurrent phenomenabull Systemic risks can hide in the interactions between institutions products

and markets and not necessarily with particular institutions

bull Only as effective as the broader governance frameworkbull Weak mgt systems or ineffective or incompetent boards =gt cannot rely

solely on firewalls and related control mechanisms to control or mitigate conflicts of interest or other risks

Limits of market discipline

12

bull Difficult in practice to directly control behaviour without sacrificing some measure of efficiency and innovation or creating adverse incentive effects

Limits of supervision

7

What about structure

250

300

350

400

250

300

350

400

300

350

400

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

GBR

CAN

USA

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

CHN

IND

IDN

300

350

400

13

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

AUS

JPN

KOR

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

BRA

MEX

ARG

Total assets of largest 3 banks as share of GDP

Balance sheets of large financial groups

bull Large integrated institutions may not have a greater risk of failure than smaller institutions

bull Might fare better because of the diversity of their activities or the diversity of their funding sources

More risky elements but more

diversification activities or the diversity of their funding sources

bull Increases in cross-sector cross-border or cross-risk type correlations limit diversification benefits

bull If not properly managed these risk exposures can precipitate institutional failures or have broader implicationsBut risk factors

14

precipitate institutional failures or have broader implications

bull And given cross-sector and cross-border inter-linkages once problems do erupt they tend to be transferred from one market segment or region to another

can interact

8

The structure-behaviour nexus

Regulate Regulate Structure

Some activities not compatible from a direct risk or moral

hazard standpoint

Should not be combined

Regulate BehaviourIssue is not structure per se

But implications of structure for risk management amp internal controls

15

Opaque universal banking model vs Non-operating holding company structure with firewalls

Would the separation of traditional and non-traditional bank business make the sector safer

Commercial

Bank external funding

trading etc

BrokerDir equity sales IPSs etc

Invest Banking position taking

securities business

BrokerDir equity sales IPSs etc

Commercial Bank

InsuranceInvestmentBank

Source The Financial Crisis Reform and Exit Strategies OECD September 2009 Paris available at wwwoecdorgdataoecd554743091457pdf 16

Wealth management

private clients etc

Insurance general life reinsurance

Wealth Broker Management Dealer

9

Linked components of risk management

bull Possible risk of contagion across group members from shared brand name and damage to grouprsquos reputation

bull Entire governance framework must be appropriate for risk profile and business model

Structure alone not sufficient

bull Direct but not sole responsibility for ensuring a proper mix and mgt of institutionrsquos assets and liabilities

Role of managers in risk mgt

bull Should provide an external constraint on managerial discretionbull External governance mechanisms are at a disadvantage in the case of

complex structures

Effective market discipline

Normal competitive mkt function

17

bull Some institutionrsquos asset-liability mix risk mgt techniques or entire business model will prove to be deficient and result in losses or failure

p

bull Is the problem idiosyncratic likely to spread to other institutions having a similar structure or business model or further still

Implications

Thanks very much for tt tiyour attention

Any questions

18

7

What about structure

250

300

350

400

250

300

350

400

300

350

400

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

GBR

CAN

USA

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

CHN

IND

IDN

300

350

400

13

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

AUS

JPN

KOR

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

BRA

MEX

ARG

Total assets of largest 3 banks as share of GDP

Balance sheets of large financial groups

bull Large integrated institutions may not have a greater risk of failure than smaller institutions

bull Might fare better because of the diversity of their activities or the diversity of their funding sources

More risky elements but more

diversification activities or the diversity of their funding sources

bull Increases in cross-sector cross-border or cross-risk type correlations limit diversification benefits

bull If not properly managed these risk exposures can precipitate institutional failures or have broader implicationsBut risk factors

14

precipitate institutional failures or have broader implications

bull And given cross-sector and cross-border inter-linkages once problems do erupt they tend to be transferred from one market segment or region to another

can interact

8

The structure-behaviour nexus

Regulate Regulate Structure

Some activities not compatible from a direct risk or moral

hazard standpoint

Should not be combined

Regulate BehaviourIssue is not structure per se

But implications of structure for risk management amp internal controls

15

Opaque universal banking model vs Non-operating holding company structure with firewalls

Would the separation of traditional and non-traditional bank business make the sector safer

Commercial

Bank external funding

trading etc

BrokerDir equity sales IPSs etc

Invest Banking position taking

securities business

BrokerDir equity sales IPSs etc

Commercial Bank

InsuranceInvestmentBank

Source The Financial Crisis Reform and Exit Strategies OECD September 2009 Paris available at wwwoecdorgdataoecd554743091457pdf 16

Wealth management

private clients etc

Insurance general life reinsurance

Wealth Broker Management Dealer

9

Linked components of risk management

bull Possible risk of contagion across group members from shared brand name and damage to grouprsquos reputation

bull Entire governance framework must be appropriate for risk profile and business model

Structure alone not sufficient

bull Direct but not sole responsibility for ensuring a proper mix and mgt of institutionrsquos assets and liabilities

Role of managers in risk mgt

bull Should provide an external constraint on managerial discretionbull External governance mechanisms are at a disadvantage in the case of

complex structures

Effective market discipline

Normal competitive mkt function

17

bull Some institutionrsquos asset-liability mix risk mgt techniques or entire business model will prove to be deficient and result in losses or failure

p

bull Is the problem idiosyncratic likely to spread to other institutions having a similar structure or business model or further still

Implications

Thanks very much for tt tiyour attention

Any questions

18

8

The structure-behaviour nexus

Regulate Regulate Structure

Some activities not compatible from a direct risk or moral

hazard standpoint

Should not be combined

Regulate BehaviourIssue is not structure per se

But implications of structure for risk management amp internal controls

15

Opaque universal banking model vs Non-operating holding company structure with firewalls

Would the separation of traditional and non-traditional bank business make the sector safer

Commercial

Bank external funding

trading etc

BrokerDir equity sales IPSs etc

Invest Banking position taking

securities business

BrokerDir equity sales IPSs etc

Commercial Bank

InsuranceInvestmentBank

Source The Financial Crisis Reform and Exit Strategies OECD September 2009 Paris available at wwwoecdorgdataoecd554743091457pdf 16

Wealth management

private clients etc

Insurance general life reinsurance

Wealth Broker Management Dealer

9

Linked components of risk management

bull Possible risk of contagion across group members from shared brand name and damage to grouprsquos reputation

bull Entire governance framework must be appropriate for risk profile and business model

Structure alone not sufficient

bull Direct but not sole responsibility for ensuring a proper mix and mgt of institutionrsquos assets and liabilities

Role of managers in risk mgt

bull Should provide an external constraint on managerial discretionbull External governance mechanisms are at a disadvantage in the case of

complex structures

Effective market discipline

Normal competitive mkt function

17

bull Some institutionrsquos asset-liability mix risk mgt techniques or entire business model will prove to be deficient and result in losses or failure

p

bull Is the problem idiosyncratic likely to spread to other institutions having a similar structure or business model or further still

Implications

Thanks very much for tt tiyour attention

Any questions

18

9

Linked components of risk management

bull Possible risk of contagion across group members from shared brand name and damage to grouprsquos reputation

bull Entire governance framework must be appropriate for risk profile and business model

Structure alone not sufficient

bull Direct but not sole responsibility for ensuring a proper mix and mgt of institutionrsquos assets and liabilities

Role of managers in risk mgt

bull Should provide an external constraint on managerial discretionbull External governance mechanisms are at a disadvantage in the case of

complex structures

Effective market discipline

Normal competitive mkt function

17

bull Some institutionrsquos asset-liability mix risk mgt techniques or entire business model will prove to be deficient and result in losses or failure

p

bull Is the problem idiosyncratic likely to spread to other institutions having a similar structure or business model or further still

Implications

Thanks very much for tt tiyour attention

Any questions

18