relationship trading in otc markets

TRANSCRIPT

Relationship Trading in OTC Markets

Terry Hendershott1 Dan Li2 Dmitry Livdan1 Norman Schurhoff3

1UC Berkeley 2Federal Reserve Board

3University of Lausanne, Swiss Finance Institute, CEPR

October 2016

Disclaimer: The views presented herein are our own and do not necessarily reflect those of the Board of Governors of the Federal Reserve System.

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 1

OTC markets

40% of U.S. financial assets OTC-traded: Corporates, muni, agency, deriv.

Regulatory & technological changes

Transparency, centralization, best-execution: TRACE, Dodd-Frank, MiFID I/II

Bilateral phone trading vs. electronic RfQs: MarketAxxess, TruMid, ...

10/28/15, 7:42 AMBond platforms look to bury archaic phone trading - FT.com

Page 1 of 6http://www.ft.com/intl/cms/s/0/89…-00144feab7de.html#axzz3ppisZEOc

Share Author alerts Print Clip Gift Article Comments

Options are more complex to trade which accounts forthe continued presence of the human trader

Last updated: May 5, 2015 12:39 pm

Robin Wigglesworth

When bond traders fancy lunch, they canorder from a panoply of smartphone apps andget a burrito or pad thai delivered promptly tothe desk. When they want to buy somecorporate bonds, an archaic landline phone isstill usually required. But that may soon bechanging.

The downturn in bond trading volumes forissued debt — so acute that even regulators,

central bankers and the International Monetary Fund are getting worried — hastriggered a Cambrian explosion in the electronic bond trading ecosystem.

About a dozen start-ups have mushroomed over the pastfew years focusing primarily on modernising and improving the old-fashioned andanaemic corporate bond trading system, where the liquidity crisis is the deepest. Thequestion, however, is whether technology can facilitate bond investors selling largeamounts of paper without generating significant market turmoil.

Bond platforms look to bury archaic phonetrading

©AP

10/28/15, 7:39 AMThiel, Soros Said to Lead $25 Million Investment in TruMid - Bloomberg Business

Page 1 of 9http://www.bloomberg.com/news/articles/2015-10-27/thiel-soros-said-to-lead-25-million-investment-in-trumid

Thiel, Soros Said to Lead $25Million Investment in TruMid

TruMid gets boost in electronic bond-trading competition

A dozen firms including TruMid seek to transform bond market

PayPal Co-Founder Peter Thiel Photographer: David PaulMorris/Bloomberg

Venture capitalist Peter Thiel and billionaire George Soros are leading a $25 millioninvestment in electronic bond-trading startup TruMid Financial LLC.

The New York-based company is among a dozen firms competing to transform the

October 27, 2015 — 4:00 AM PDT

Tracy AllowayTRACYALLOWAY

Matthew Leising

How do client-dealer relations affect trading/pricing in OTC markets?

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 2

Functioning of decentralized OTC markets

No formal structure, no centralized trading, no law-of-one-price

Opacity & fragmentation impose search & matching frictions on investors

Dealers provide liquidity (matching, inventory & interdealer network)

Dealers'

C

CC

C

D

D D

D D

C C

1 How do investors trade: flip coin or build rolodex?2 Investor heterogeneity: How many dealers to trade with, why?

Tradeoff between competition & repeat relations

3 What is impact of connections on execution cost?4 Dealer heterogeneity: Which dealers to trade with, why?

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 3

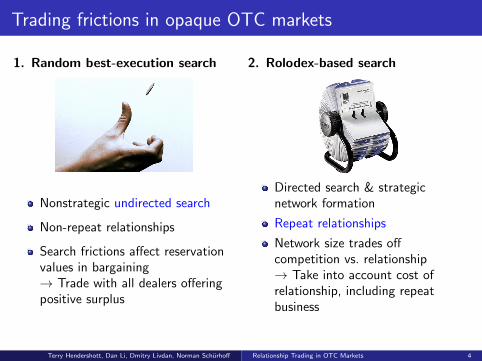

Trading frictions in opaque OTC markets

1. Random best-execution search

Nonstrategic undirected search

Non-repeat relationships

Search frictions affect reservationvalues in bargaining→ Trade with all dealers offeringpositive surplus

2. Rolodex-based search

Directed search & strategicnetwork formation

Repeat relationships

Network size trades offcompetition vs. relationship→ Take into account cost ofrelationship, including repeatbusiness

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 4

Our setting: Insurer trading in corporate bonds

Our data reveals the identities of the traders on both sides (insurer & dealer)

NAIC comprehensive trades for all 4,000+ US insurers (Health, Life, P&C)

FISD corporate bond characteristics

Corporate bond market is a classic OTC market

Important source of public financing for corporations($7.8tn market cap, $1.4tn issuance, 20k+ CUSIPs)

Large and active OTC secondary market (>400 active broker-dealers)

Illiquid, fragmented & opaque (no tape until early 2000s)

Important investment vehicle for insurers

Long-term buy & hold investors (30% holding, 10% trading)

Subject to liquidity shocks, while little adverse selection risk from insurers

Heterogeneous trading needs (based on size, rating & type)

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 5

Literature on OTC markets, search, matching & networks

Microstructure of OTC Financial Markets

Transaction costs and impact of transparency (Edwards, et al., 2005; Bessembinder et al.,2006; Harris & Piwowar, 2007; Green, et al., 2007; Pagano & Volpin, 2012)

OTC vs. electronic trading (Biais, 1993; Hendershott & Madhavan, 2015)

Role of interdealer market (Hollifield et al., 2015; Li & Schurhoff, 2015)

Best execution in OTC markets (O’Hara et al., 2015; Harris, 2015)

Search & Matching

Search frictions in OTC markets (Wright, many; Duffie et al., 2005/7; Weill, 2007; Lagos& Rocheteau, 2007/9; Feldhutter, 2011; Gofman, 2011; Neklyudov, 2014)

Directed search, assortative matching & heterogeneity in labor/marriages (Acemoglu &Shimer, 1999; Shimer & Smith, 2000; Shi, 2001)

Strategic Network & Relationship Formation

OTC network formation & contracting with externalities (Leitner, 2005; Gale & Kariv,2007; Afonso et al., 2011; Condorelli, 2011; Babus, 2012; Farboodi, 2014; Neklyudov &Sambalaibat, 2015; Chang & Zhang, 2015)

Repeat relations, relational contracts & loyalty (Levin, 2002; Bernhardt et al., 2004; Board,2011; Fernando et al., 2011; DiMaggio et al., 2015)

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 6

Agenda

1 Data on insurers & bond trading

2 Empirical findings:

Insurer heterogeneity in trading needsDeterminants of insurers’ choice of trading network

3 Model of trading in OTC markets & testable predictions

4 Execution costs & dealer relationships

5 Structural estimation of model

6 Dealer heterogeneity, which insurers choose which dealers (not in paper)

7 Diff-in-diff analysis of Lehman collapse (not in paper)

8 Summary & conclusion

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 7

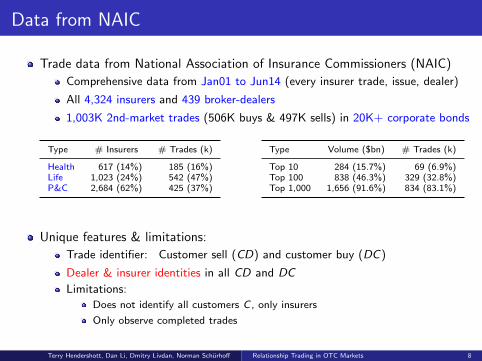

Data from NAIC

Trade data from National Association of Insurance Commissioners (NAIC)

Comprehensive data from Jan01 to Jun14 (every insurer trade, issue, dealer)

All 4,324 insurers and 439 broker-dealers

1,003K 2nd-market trades (506K buys & 497K sells) in 20K+ corporate bonds

Type # Insurers # Trades (k)

Health 617 (14%) 185 (16%)Life 1,023 (24%) 542 (47%)P&C 2,684 (62%) 425 (37%)

Type Volume ($bn) # Trades (k)

Top 10 284 (15.7%) 69 (6.9%)Top 100 838 (46.3%) 329 (32.8%)Top 1,000 1,656 (91.6%) 834 (83.1%)

Unique features & limitations:

Trade identifier: Customer sell (CD) and customer buy (DC)

Dealer & insurer identities in all CD and DC

Limitations:

Does not identify all customers C , only insurers

Only observe completed trades

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 8

Insurers have heterogenous trading activity

Insurer buys per year: Insurer sells per year:

.001

.01

.1.5

1Fr

actio

n of

insu

rers

1 10 100 1000No. of trades

DataInterpolation

.001

.01

.1.5

1Fr

actio

n of

insu

rers

1 10 100 1000No. of trades

DataInterpolation

Insurers trade up to 2,200 times every year (Mean=16, median=14)

Trading correlates with insurer size, type, quality; bond types & varieties

Distribution follows a power law: p(X ) ∝ X−1.21; use later

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 9

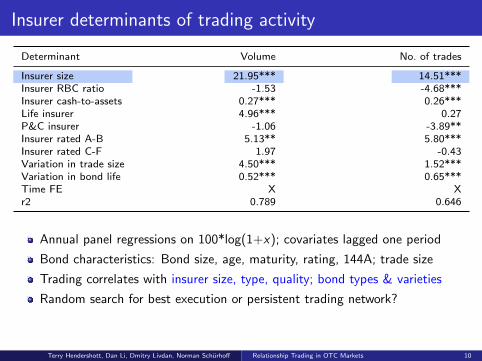

Insurer determinants of trading activity

Determinant Volume No. of trades

Insurer size 21.95*** 14.51***Insurer RBC ratio -1.53 -4.68***Insurer cash-to-assets 0.27*** 0.26***Life insurer 4.96*** 0.27P&C insurer -1.06 -3.89**Insurer rated A-B 5.13** 5.80***Insurer rated C-F 1.97 -0.43Variation in trade size 4.50*** 1.52***Variation in bond life 0.52*** 0.65***Time FE X Xr2 0.789 0.646

Annual panel regressions on 100*log(1+x); covariates lagged one period

Bond characteristics: Bond size, age, maturity, rating, 144A; trade size

Trading correlates with insurer size, type, quality; bond types & varieties

Random search for best execution or persistent trading network?

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 10

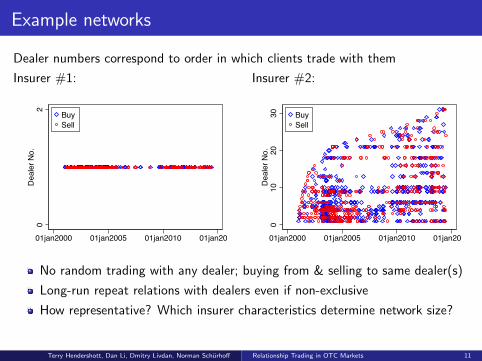

Example networks

Dealer numbers correspond to order in which clients trade with them

Insurer #1: Insurer #2:

02

Dea

ler N

o.

01jan2000 01jan2005 01jan2010 01jan2015

BuySell

010

2030

Dea

ler N

o.

01jan2000 01jan2005 01jan2010 01jan2015

BuySell

No random trading with any dealer; buying from & selling to same dealer(s)

Long-run repeat relations with dealers even if non-exclusive

How representative? Which insurer characteristics determine network size?

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 11

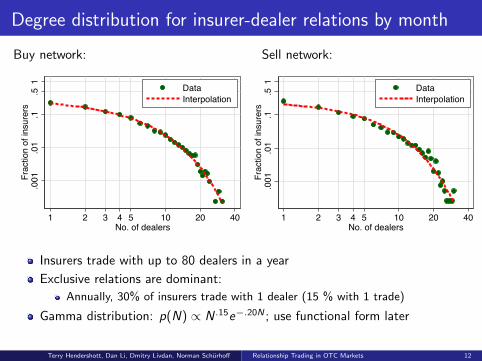

Degree distribution for insurer-dealer relations by month

Buy network: Sell network:

.001

.01

.1.5

1Fr

actio

n of

insu

rers

1 2 3 4 5 10 20 40No. of dealers

DataInterpolation

.001

.01

.1.5

1Fr

actio

n of

insu

rers

1 2 3 4 5 10 20 40No. of dealers

DataInterpolation

Insurers trade with up to 80 dealers in a year

Exclusive relations are dominant:

Annually, 30% of insurers trade with 1 dealer (15 % with 1 trade)

Gamma distribution: p(N) ∝ N .15e−.20N ; use functional form later

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 12

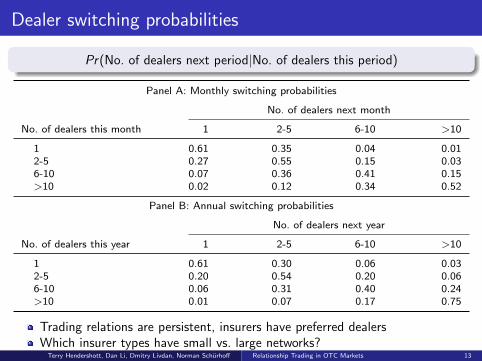

Dealer switching probabilities

Pr(No. of dealers next period|No. of dealers this period)

Panel A: Monthly switching probabilities

No. of dealers next month

No. of dealers this month 1 2-5 6-10 >10

1 0.61 0.35 0.04 0.012-5 0.27 0.55 0.15 0.036-10 0.07 0.36 0.41 0.15>10 0.02 0.12 0.34 0.52

Panel B: Annual switching probabilities

No. of dealers next year

No. of dealers this year 1 2-5 6-10 >10

1 0.61 0.30 0.06 0.032-5 0.20 0.54 0.20 0.066-10 0.06 0.31 0.40 0.24>10 0.01 0.07 0.17 0.75

Trading relations are persistent, insurers have preferred dealersWhich insurer types have small vs. large networks?

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 13

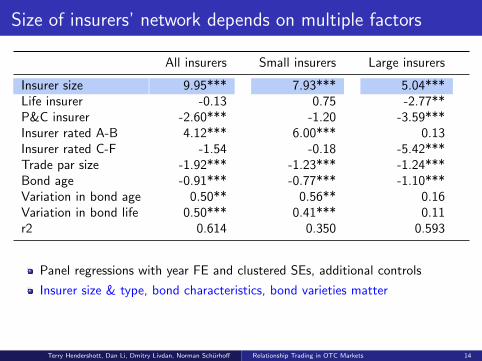

Size of insurers’ network depends on multiple factors

All insurers Small insurers Large insurers

Insurer size 9.95*** 7.93*** 5.04***Life insurer -0.13 0.75 -2.77**P&C insurer -2.60*** -1.20 -3.59***Insurer rated A-B 4.12*** 6.00*** 0.13Insurer rated C-F -1.54 -0.18 -5.42***Trade par size -1.92*** -1.23*** -1.24***Bond age -0.91*** -0.77*** -1.10***Variation in bond age 0.50** 0.56** 0.16Variation in bond life 0.50*** 0.41*** 0.11r2 0.614 0.350 0.593

Panel regressions with year FE and clustered SEs, additional controls

Insurer size & type, bond characteristics, bond varieties matter

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 14

OTC model with repeat relations

DGP (2005) type setupDiscount rate r , perpetual bond with coupon flow CNon-owner receives trading shock with intensity ηOwner receives trading shock L with intensity κClient buy and sell prices, Pb&P s , set through Nash bargaining

Dealer marketAs in Lester et al. (2015) interdealer market, but with search frictions

Interdealer prices are exogenous: Mbid , Mask

Symmetric dealers search interdealer market for counterparty with intensity λClients choose N dealers to contact, dealers search simultaneously:

Effective search rate Λ = Nλ

First dealer to locate the bond ’wins’ the tradeIf bargaining fails relationship with dealer is severed, new dealer added

Dealers take into account future trading opportunities

Cost per trade per dealer is K , total cost is NK

Steady-state valuationsClients and dealers transition through states of non-owner, buyer, owner,seller, non-owner, etc.Valuations in states (V no ,V b,V o ,V s) are linked through transitionprobabilities

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 15

Model cycle, including dealer valuations

Vno, Uno

Vb, Ub

Vo, Uo

Client receives liquidity shock to buy (intensity η)

Client receives liquidity shock to sell (intensity κ)

Dealers search for seller (intensity λN)

Dealers search for buyer (intensity λN)

Vs, Us

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 16

OTC market model solution

Transaction prices are set by Nash bargaining:

Pb = (V o − V b)w + (Mbid−Uo)(1− w)

Ps = (V s − V no)w + (Mask+Uno)(1− w)

Model is non-linear, limiting cases and numerical solutions

For example as N →∞ prices are:

PbN→∞ = Mask +

w

1− wK ,

PsN→∞ = Mbid − w

1− wK .

w1−wK is markup to access interdealer prices

When λ→∞, N∗ = 1 and prices are:

Pbλ→∞ = Mask +

w

1− wK − Uo

λ→∞,

Psλ→∞ = Mbid − w

1− wK + Uno

λ→∞.

Uoλ→∞ and Uno

λ→∞ are discounts due to future business (relationship value)

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 17

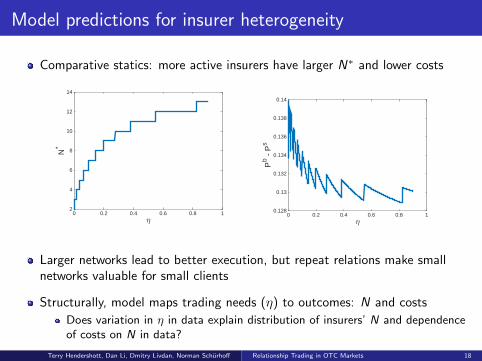

Model predictions for insurer heterogeneity

Comparative statics: more active insurers have larger N∗ and lower costs

20 0.2 0.4 0.6 0.8 1

N*

2

4

6

8

10

12

14

20 0.2 0.4 0.6 0.8 1

Pb -

Ps

0.128

0.13

0.132

0.134

0.136

0.138

0.14

Larger networks lead to better execution, but repeat relations make smallnetworks valuable for small clients

Structurally, model maps trading needs (η) to outcomes: N and costs

Does variation in η in data explain distribution of insurers’ N and dependenceof costs on N in data?

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 18

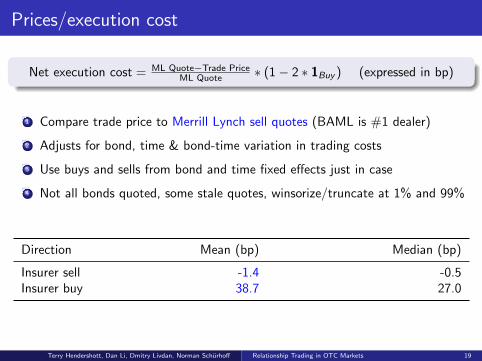

Prices/execution cost

Net execution cost = ML Quote−Trade PriceML Quote ∗ (1− 2 ∗ 1Buy ) (expressed in bp)

1 Compare trade price to Merrill Lynch sell quotes (BAML is #1 dealer)

2 Adjusts for bond, time & bond-time variation in trading costs

3 Use buys and sells from bond and time fixed effects just in case

4 Not all bonds quoted, some stale quotes, winsorize/truncate at 1% and 99%

Direction Mean (bp) Median (bp)

Insurer sell -1.4 -0.5Insurer buy 38.7 27.0

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 19

Execution costs and the insurer-dealer network

Determinant (1) (2) (3) (4)

Insurer size -4.89*** -3.72*** -3.59***Insurer no. of dealers -0.37*** -0.22*** 0.32***ln(Insurer no. of dealers) -6.29***

Insurer RBC ratio -3.57*** -0.67 -3.51*** -4.19***Insurer cash-to-assets -0.04** -0.02 -0.04** -0.04**Life insurer 4.66*** 3.32*** 4.43*** 4.47***P&C insurer 2.26*** 2.10*** 1.72** 1.73**r2 0.154 0.154 0.154 0.155N 918,279 918,279 918,279 918,279

Panel regressions with dealer, bond, & day FEs and clustered SEs

Execution costs are smaller for larger insurers and larger networks

Use coefficients in (4) to assess model fit

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 20

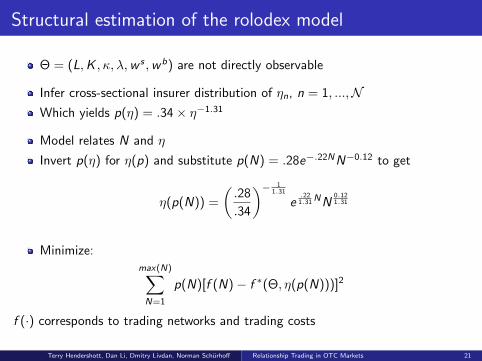

Structural estimation of the rolodex model

Θ = (L,K , κ, λ,w s ,wb) are not directly observable

Infer cross-sectional insurer distribution of ηn, n = 1, ...,NWhich yields p(η) = .34× η−1.31

Model relates N and η

Invert p(η) for η(p) and substitute p(N) = .28e−.22NN−0.12 to get

η(p(N)) =

(.28

.34

)− 11.31

e.22

1.31 NN0.121.31

Minimize:max(N)∑N=1

p(N)[f (N)− f ∗(Θ, η(p(N)))]2

f (·) corresponds to trading networks and trading costs

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 21

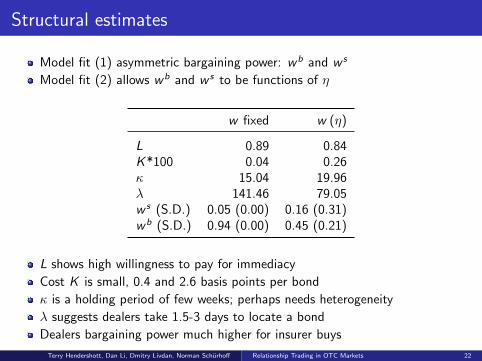

Structural estimates

Model fit (1) asymmetric bargaining power: wb and w s

Model fit (2) allows wb and w s to be functions of η

w fixed w (η)

L 0.89 0.84K*100 0.04 0.26κ 15.04 19.96λ 141.46 79.05w s (S.D.) 0.05 (0.00) 0.16 (0.31)wb (S.D.) 0.94 (0.00) 0.45 (0.21)

L shows high willingness to pay for immediacy

Cost K is small, 0.4 and 2.6 basis points per bond

κ is a holding period of few weeks; perhaps needs heterogeneity

λ suggests dealers take 1.5-3 days to locate a bond

Dealers bargaining power much higher for insurer buys

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 22

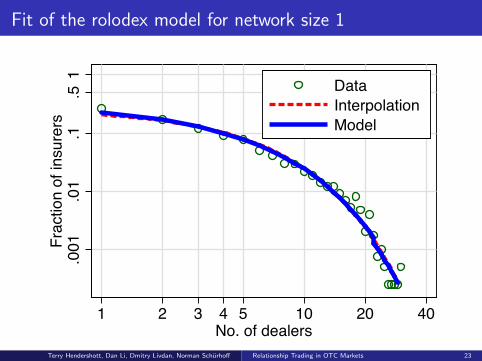

Fit of the rolodex model for network size 1

.001

.01

.1.5

1Fr

actio

n of

insu

rers

1 2 3 4 5 10 20 40No. of dealers

DataInterpolationModel

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 23

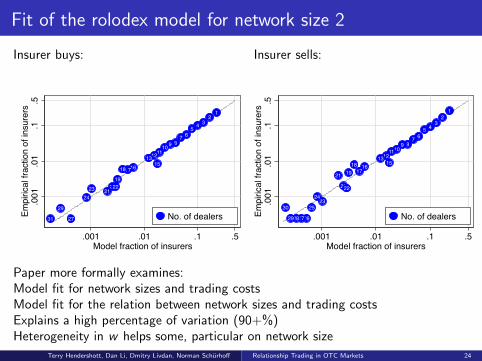

Fit of the rolodex model for network size 2

Insurer buys: Insurer sells:

12

34567

8910111213

15161718

1920

212223

24

27

29

31

.001

.01

.1.5

Empi

rical

frac

tion

of in

sure

rs

.001 .01 .1 .5Model fraction of insurers

No. of dealers

12

345

6789

10111213

1516

1718

19

20

21

22

2324

25

26272829

30

.001

.01

.1.5

Empi

rical

frac

tion

of in

sure

rs

.001 .01 .1 .5Model fraction of insurers

No. of dealers

Paper more formally examines:Model fit for network sizes and trading costsModel fit for the relation between network sizes and trading costsExplains a high percentage of variation (90+%)Heterogeneity in w helps some, particular on network size

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 24

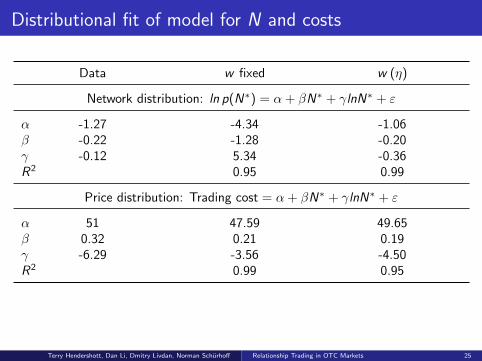

Distributional fit of model for N and costs

Data w fixed w (η)

Network distribution: ln p(N∗) = α + βN∗ + γlnN∗ + ε

α -1.27 -4.34 -1.06β -0.22 -1.28 -0.20γ -0.12 5.34 -0.36R2 0.95 0.99

Price distribution: Trading cost = α + βN∗ + γlnN∗ + ε

α 51 47.59 49.65β 0.32 0.21 0.19γ -6.29 -3.56 -4.50R2 0.99 0.95

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 25

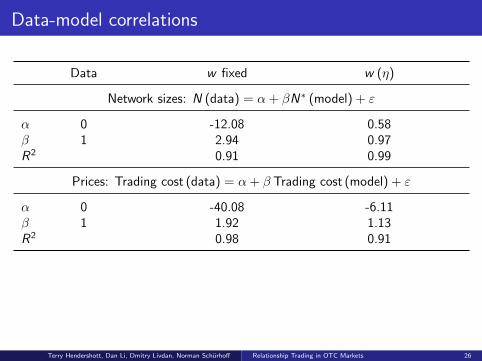

Data-model correlations

Data w fixed w (η)

Network sizes: N (data) = α + βN∗ (model) + ε

α 0 -12.08 0.58β 1 2.94 0.97R2 0.91 0.99

Prices: Trading cost (data) = α + β Trading cost (model) + ε

α 0 -40.08 -6.11β 1 1.92 1.13R2 0.98 0.91

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 26

Counterfactual without repeat relations

Use estimated set of parameters, resolve model setting Uo = Uno = 0

-60

-40

-20

020

40Bi

d-as

k sp

read

1 2 3 4 5 10 20 40No. of dealers

ModelCounterfactual

Benefits largely on the sell-side for small clients

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 27

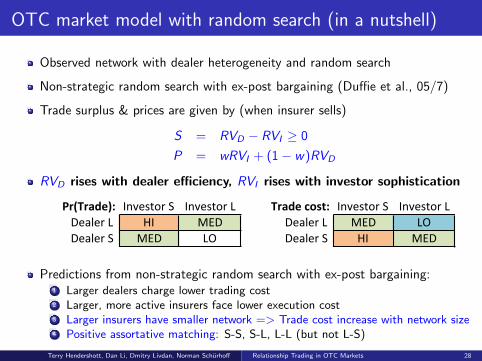

OTC market model with random search (in a nutshell)

Observed network with dealer heterogeneity and random search

Non-strategic random search with ex-post bargaining (Duffie et al., 05/7)

Trade surplus & prices are given by (when insurer sells)

S = RVD − RVI ≥ 0

P = wRVI + (1− w)RVD

RVD rises with dealer efficiency, RVI rises with investor sophistication

Pr(Trade): Investor)S Investor)L Trade*cost: Investor)S Investor)LDealer)L) HI MED Dealer)L) MED LODealer)S) MED LO Dealer)S) HI MED

Predictions from non-strategic random search with ex-post bargaining:1 Larger dealers charge lower trading cost2 Larger, more active insurers face lower execution cost3 Larger insurers have smaller network => Trade cost increase with network size4 Positive assortative matching: S-S, S-L, L-L (but not L-S)

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 28

Different model predictions for trading & pricing

Predictions from non-strategic random search with ex-post bargaining:1 Larger dealers charge lower trading costs2 Larger, more active insurers face lower trading costs3 Larger insurers have smaller network => Trade cost increase with network size4 Positive assortative matching: S-S, S-L, L-L (but not L-S)

Pr(Trade): Investor)S Investor)L Trade*cost: Investor)S Investor)LDealer)L) HI MED Dealer)L) MED LODealer)S) MED LO Dealer)S) HI MED

Predictions from Rolodex model:1 Larger dealers charge lower trading costs2 Larger, more active insurers face lower trading costs3 Larger insurers have larger network => Trade cost decrease with network size4 Negative assortative matching: L-L, L-S, S-L (but not S-S)

Pr(Trade): InvestorS InvestorL Tradecost: InvestorS InvestorLDealerL MED Hi DealerL MED LODealerS LO MED DealerS HI MED

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 29

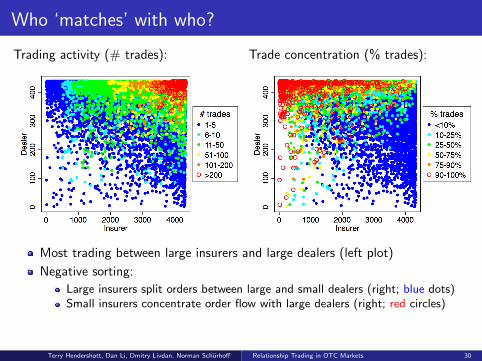

Who ‘matches’ with who?

Trading activity (# trades): Trade concentration (% trades):

Most trading between large insurers and large dealers (left plot)

Negative sorting:

Large insurers split orders between large and small dealers (right; blue dots)Small insurers concentrate order flow with large dealers (right; red circles)

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 30

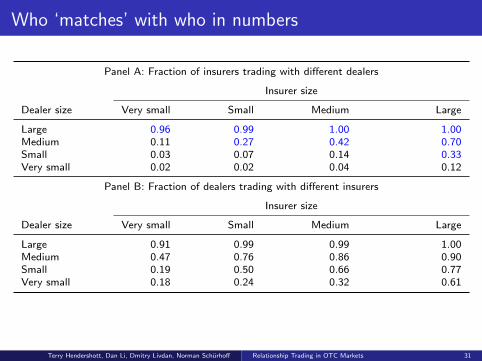

Who ‘matches’ with who in numbers

Panel A: Fraction of insurers trading with different dealers

Insurer size

Dealer size Very small Small Medium Large

Large 0.96 0.99 1.00 1.00Medium 0.11 0.27 0.42 0.70Small 0.03 0.07 0.14 0.33Very small 0.02 0.02 0.04 0.12

Panel B: Fraction of dealers trading with different insurers

Insurer size

Dealer size Very small Small Medium Large

Large 0.91 0.99 0.99 1.00Medium 0.47 0.76 0.86 0.90Small 0.19 0.50 0.66 0.77Very small 0.18 0.24 0.32 0.61

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 31

Main results with insurer and dealer heterogeneity

1 Small insurers trade repeatedly with same large dealers at fair prices

2 Large insurers trade with small & large dealers at best prices

0.0

2.0

4.0

6.0

8D

ensi

ty

-25 0 25 50 75 100Net execution cost (bp)

Insurer buyInsurer sell

12

34

56

78

910

Dea

ler d

ecile

1 2 3 4 5 6 7 8 9 10Insurer decile

-10

0

10

20

30

40

50

60

70

Net

exe

cutio

n co

st (b

p)

→ Trade-off between relationship scope and dealer competition

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 32

Diff-in-diff analysis around Lehman collapseLehman’s trading activity and number of counterparties

Lehm

an c

olla

pse

010

020

030

040

0Tr

ades

per

mon

th

04/08 07/08 10/08 01/09 04/090

5010

015

020

0N

o. o

f ins

urer

s

04/08 07/08 10/08 01/09 04/09

Insurers with larger exposure to Lehman are hit harder by collapse

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 33

Diff-in-diff analysis around Lehman collapseAbnormal execution costs

Insurer sells Insurer buys

Month Control = All Matched All Matched

t − 3 (Jun 08) 41.18 61.74* -17.63 -19.37t − 2 (Jul 08) 51.10 66.92* -38.92 -24.63t − 1 (Aug 08) 0.00 0.00 0.00 0.00Event month t 4.42 33.01 5.10 -11.62t + 1 (Oct 08) 121.59** 126.37* 3.49 -8.61t + 2 (Nov 08) 137.53*** 141.94*** -60.20 -53.72t + 3 (Dec 08) 98.66*** 116.27*** -10.54 -15.77t + 4 (Jan 09) 47.80 73.68 103.33** 94.76*t + 5 (Feb 09) 24.42 68.83** -52.27 -58.17t + 6 (Mar 09) 11.51 13.48 18.38 0.04

Treatment sample: Insurers with large exposure to Lehman before collapse

Large exposure = Lehman share in 2007 in top 1% of all insurers (43%+)

Control sample: Insurers propensity score matched on size, risk-based capital,cash-to-assets, credit rating, insurer type (health, life, P&C), averageexecution costs & trading frequency in 2007

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 34

Placebo analysisBear Stearns & JP Morgan trading activity and number of counterparties

Bear

Ste

arns

col

laps

e

020

040

060

0Tr

ades

per

mon

th

10/07 01/08 04/08 07/08 10/08

JP MorganBear Stearns 0

5010

015

020

025

0N

o. o

f ins

urer

s

10/07 01/08 04/08 07/08 10/08

Insurers with large exposure to Bear Stearns moved to JP Morgan

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 35

Placebo analysisAbnormal execution costs

Insurer sells Insurer buys

Month Control = All Matched All Matched

t − 3 (Dec 07) 15.36 15.73 -24.54 -27.24t − 2 (Jan 08) 32.69 40.69 -40.18 -52.58t − 1 (Feb 08) 0.00 0.00 0.00 0.00Event month t -3.82 -14.73 43.58 28.21t + 1 (Apr 08) 31.38 5.29 1.28 -13.60t + 2 (May 08) -12.26 -8.95 -3.79 -20.08t + 3 (Jun 08) 12.39 10.72 7.66 -10.32t + 4 (Jul 08) -9.59 -11.06 52.68** 17.42t + 5 (Aug 08) 31.02 12.71 33.82 20.73t + 6 (Sep 08) 18.94 27.53 20.77 6.73

No abnormal execution costs for Bear Stearns clients around its collapse

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 36

Conclusions #1: Who trades with who?

.000

01.0

001

.001

.01

.1.5

1Fr

actio

n of

insu

rers

1 2 3 4 5 10 20 40No. of dealers

12

34

56

78

910

Dea

ler d

ecile

1 2 3 4 5 6 7 8 9 10Insurer decile

0.00.10.20.30.40.50.60.70.80.91.0

Pr(T

rade

)

Insurers’ Trading Network

Investors form few long-lasting dealer relationships50% of insurers trade repeatedly with 1 dealer (up to 40 dealers every month)Buy & sell from same dealer => No ‘random’ best-execution searchLarger, higher quality, more active insurers have larger dealer network

Sorting/matching: small-large, large-large & large-small, rarely small-small

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 37

Conclusions #2: Relations matter for trading costs

0.0

2.0

4.0

6.0

8D

ensi

ty

-25 0 25 50 75 100Net execution cost (bp)

Insurer buyInsurer sell

12

34

56

78

910

Dea

ler d

ecile

1 2 3 4 5 6 7 8 9 10Insurer decile

-10

0

10

20

30

40

50

60

70

Net

exe

cutio

n co

st (b

p)

Insurers’ Trading Costs

Trading costs are relationship specific:Large dealers give better execution than small dealers => Dealer efficiencySmall insurers with single large dealer receive fair execution => Repeat relation effectLarge insurers with large network receive best execution => Competitive effect

Consistent with Rolodex model of OTC markets

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 38

Summary & conclusions

Relationships matter for trading patterns in OTC markets

Persistence & assortative matching in insurer-dealer networksExecution costs depend on investor, dealer, network size & relations

Small insurers concentrate on a few dealers & receive decent (poor)execution from large (small) dealers

Large insurers with many connections receive best execution from all dealers

Qualitatively and quantitatively consistent with Rolodex model where insurerstrade off repeat relations with competition

Client heterogeneity is importantElements of random-search models can describe data wellAsymmetry in bargaining power, reasonable? Nash bargaining?

How would regulations affect repeat business relations?

Terry Hendershott, Dan Li, Dmitry Livdan, Norman Schurhoff Relationship Trading in OTC Markets 39