remedial action - davis brown law firm action... · ©2013 davis brown koehn shors & roberts...

TRANSCRIPT

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

REMEDIAL ACTION

Courtney A. Strutt Todd Davis Brown Law Firm

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

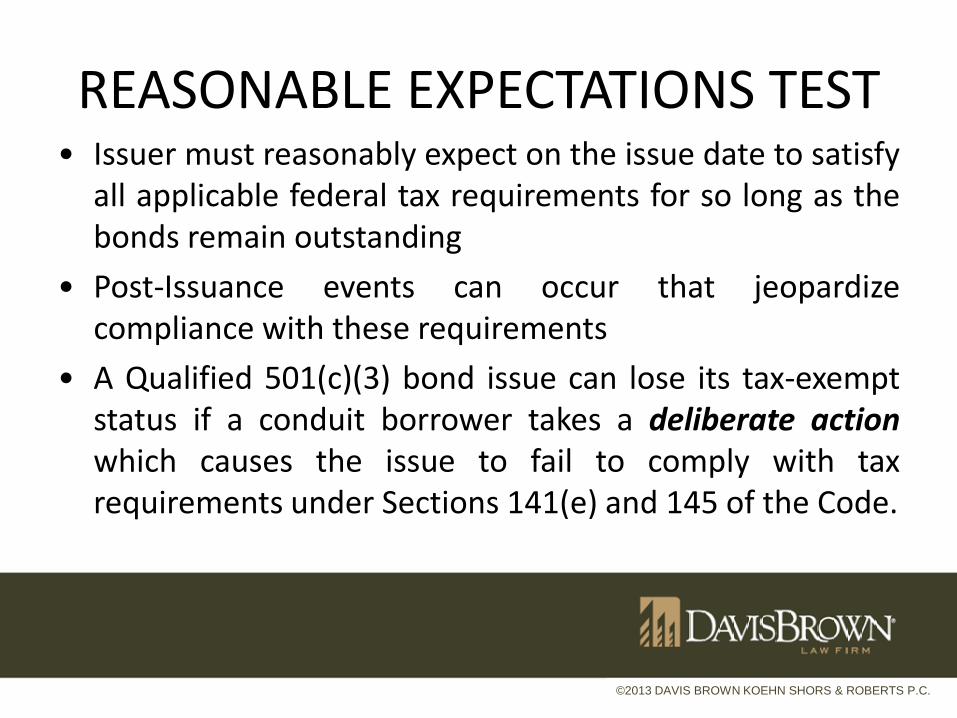

REASONABLE EXPECTATIONS TEST • Issuer must reasonably expect on the issue date to satisfy

all applicable federal tax requirements for so long as the bonds remain outstanding

• Post-Issuance events can occur that jeopardize compliance with these requirements

• A Qualified 501(c)(3) bond issue can lose its tax-exempt status if a conduit borrower takes a deliberate action which causes the issue to fail to comply with tax requirements under Sections 141(e) and 145 of the Code.

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

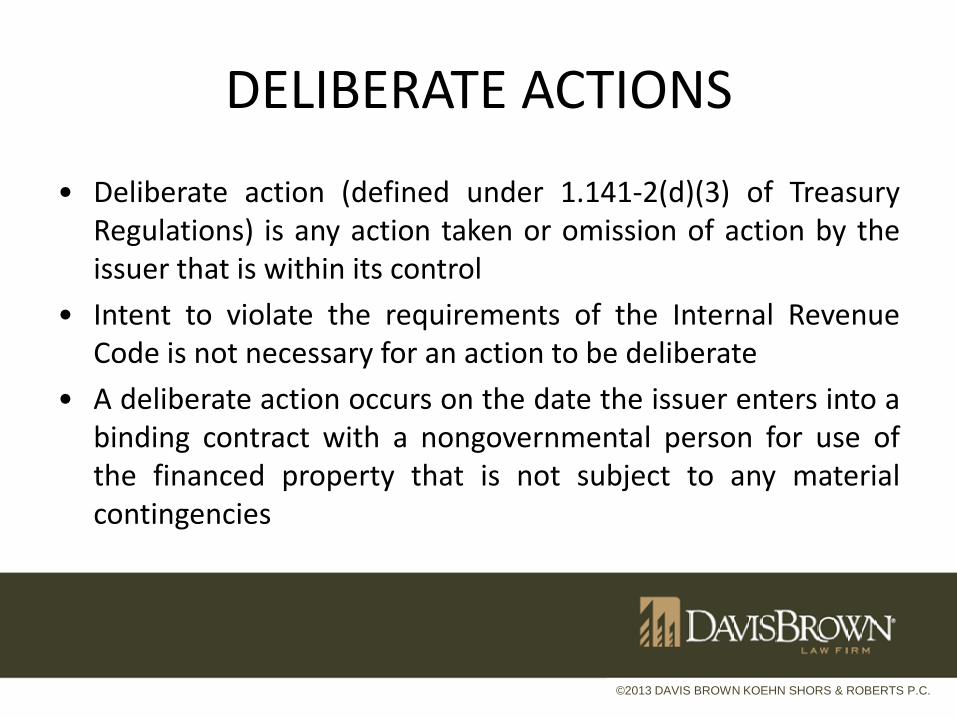

DELIBERATE ACTIONS

• Deliberate action (defined under 1.141-2(d)(3) of Treasury Regulations) is any action taken or omission of action by the issuer that is within its control

• Intent to violate the requirements of the Internal Revenue Code is not necessary for an action to be deliberate

• A deliberate action occurs on the date the issuer enters into a binding contract with a nongovernmental person for use of the financed property that is not subject to any material contingencies

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

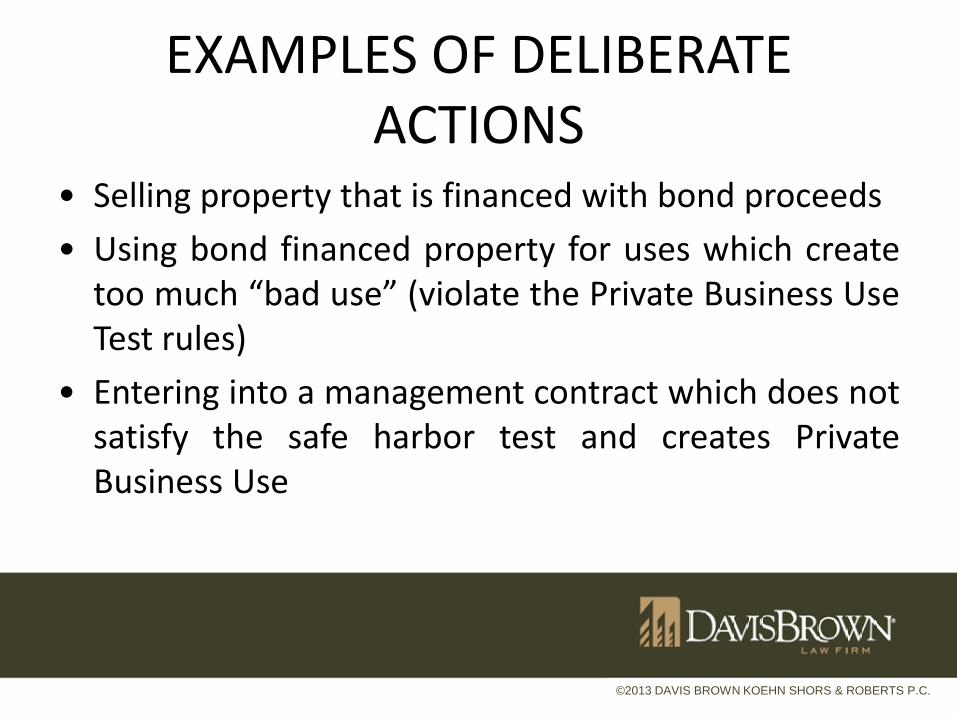

EXAMPLES OF DELIBERATE ACTIONS

• Selling property that is financed with bond proceeds • Using bond financed property for uses which create

too much “bad use” (violate the Private Business Use Test rules)

• Entering into a management contract which does not satisfy the safe harbor test and creates Private Business Use

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

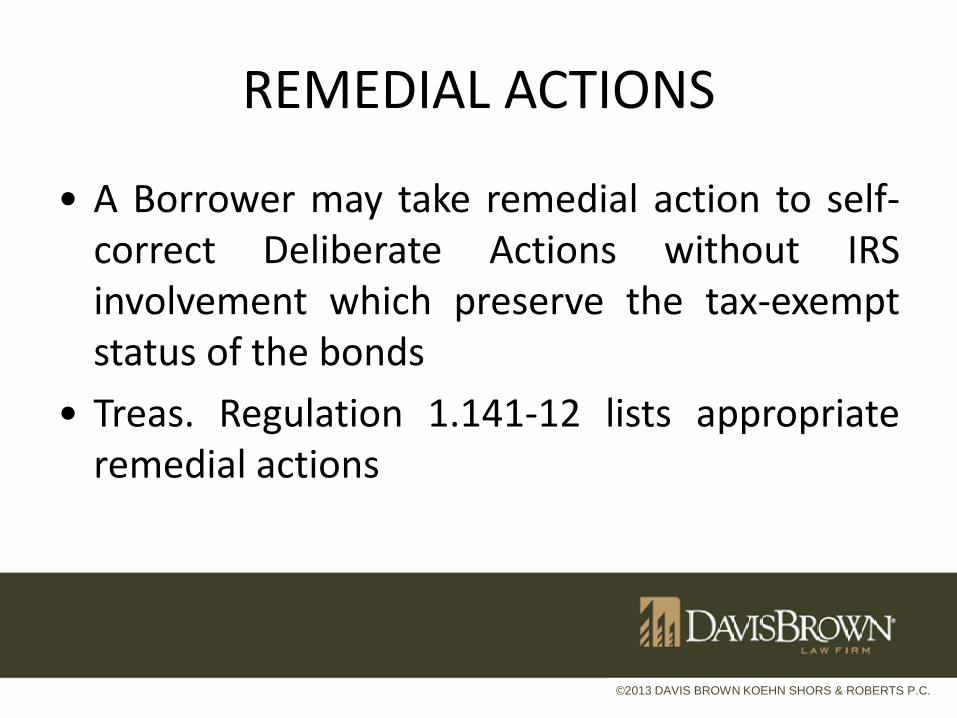

REMEDIAL ACTIONS

• A Borrower may take remedial action to self-correct Deliberate Actions without IRS involvement which preserve the tax-exempt status of the bonds

• Treas. Regulation 1.141-12 lists appropriate remedial actions

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

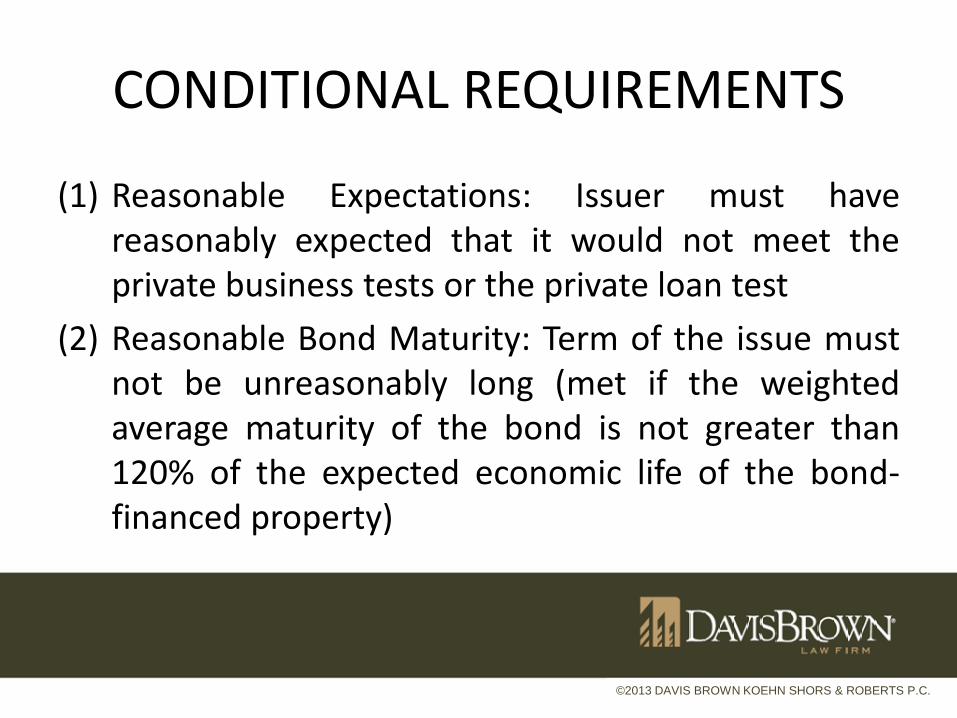

CONDITIONAL REQUIREMENTS

(1) Reasonable Expectations: Issuer must have reasonably expected that it would not meet the private business tests or the private loan test

(2) Reasonable Bond Maturity: Term of the issue must not be unreasonably long (met if the weighted average maturity of the bond is not greater than 120% of the expected economic life of the bond-financed property)

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

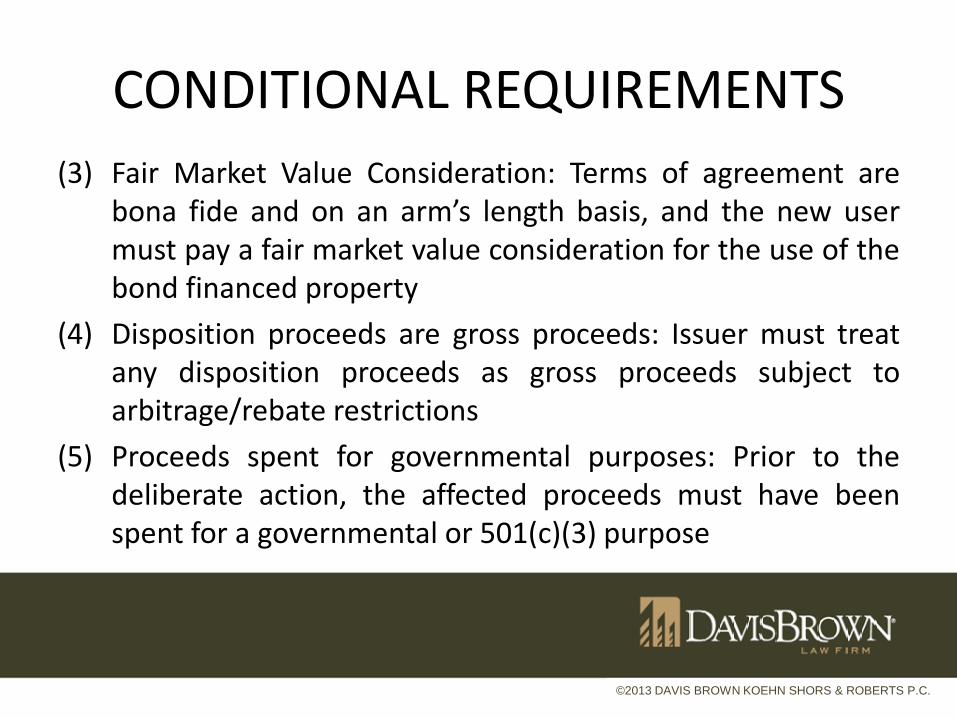

CONDITIONAL REQUIREMENTS (3) Fair Market Value Consideration: Terms of agreement are

bona fide and on an arm’s length basis, and the new user must pay a fair market value consideration for the use of the bond financed property

(4) Disposition proceeds are gross proceeds: Issuer must treat any disposition proceeds as gross proceeds subject to arbitrage/rebate restrictions

(5) Proceeds spent for governmental purposes: Prior to the deliberate action, the affected proceeds must have been spent for a governmental or 501(c)(3) purpose

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

TYPES OF REMEDIAL ACTION

(1) Redemption or Defeasance of non-qualified bonds

(2) Alternative use of Disposition proceeds (3) Alternative Use of Facility

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

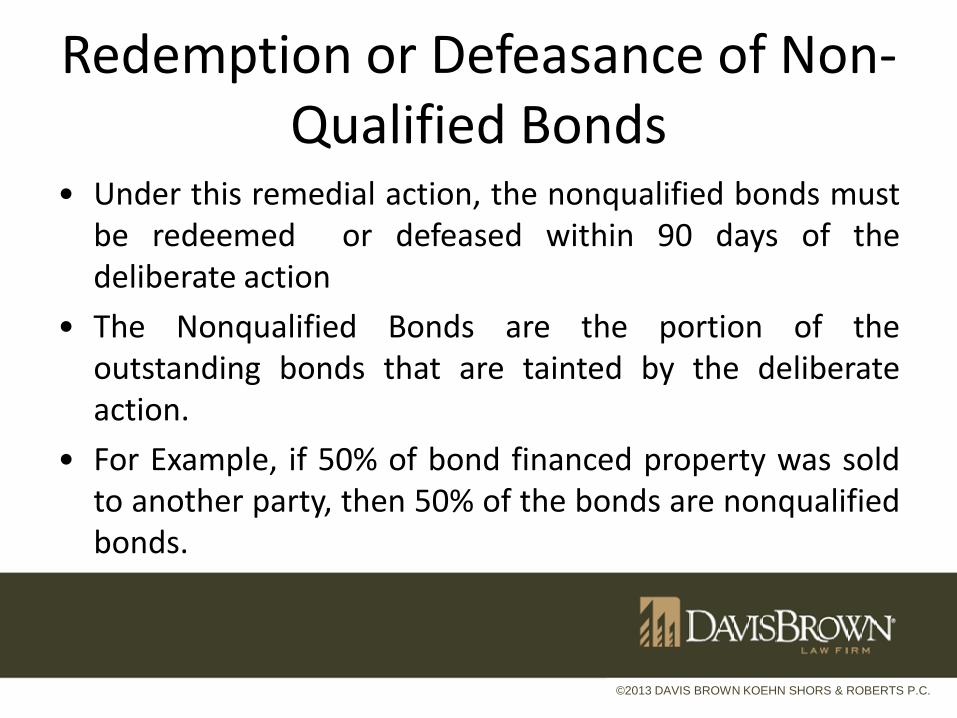

Redemption or Defeasance of Non-Qualified Bonds

• Under this remedial action, the nonqualified bonds must be redeemed or defeased within 90 days of the deliberate action

• The Nonqualified Bonds are the portion of the outstanding bonds that are tainted by the deliberate action.

• For Example, if 50% of bond financed property was sold to another party, then 50% of the bonds are nonqualified bonds.

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

Redemption or Defeasance of Non-Qualified Bonds

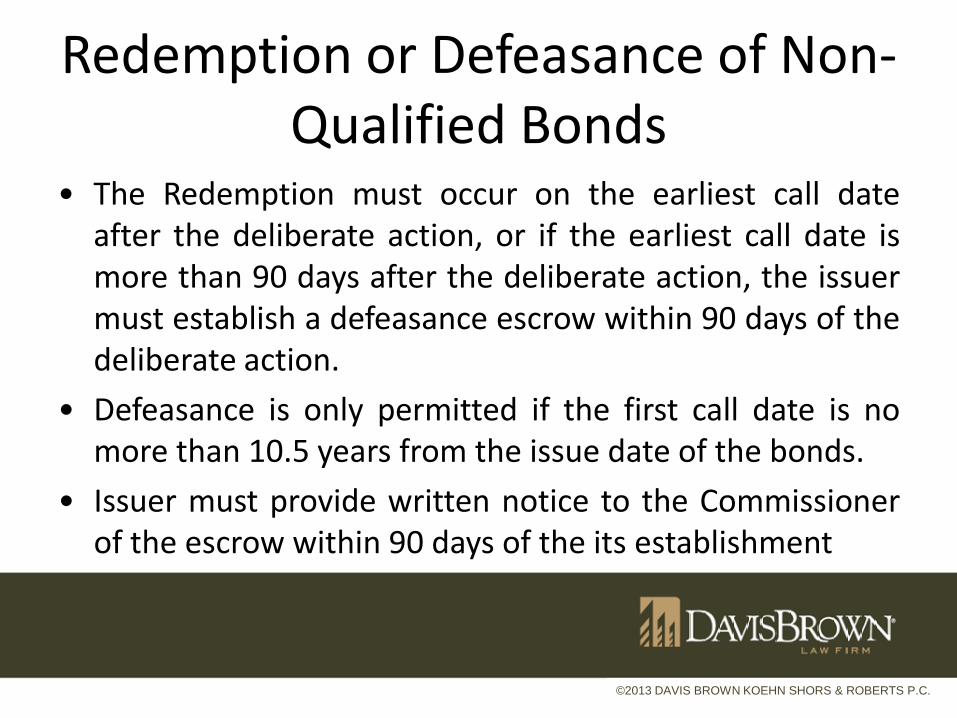

• The Redemption must occur on the earliest call date after the deliberate action, or if the earliest call date is more than 90 days after the deliberate action, the issuer must establish a defeasance escrow within 90 days of the deliberate action.

• Defeasance is only permitted if the first call date is no more than 10.5 years from the issue date of the bonds.

• Issuer must provide written notice to the Commissioner of the escrow within 90 days of the its establishment

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

Alternative Use of Disposition Proceeds

• This action is available when the borrower sells bond financed property for cash

• The Borrower must spend the proceeds from the sale within two years of the sale date for an alternative qualifying use.

• If the full amount of the proceeds aren’t used then the balance must be used to redeem or defease nonqualified bonds

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

Alternative Use of Facility

• Available when the financed property is used after the sale for a purpose that qualifies for another type of tax-exempt bond (as long as the purchaser doesn’t use tax-exempt bond proceeds for the purchase to avoid double dipping)

• The Proceeds from the sale must be used either to pay the debt service on the bonds on the next available payment date or deposit the proceeds into an escrow within 90 days of receipt

• If an escrow is established, the investment yield on the proceeds must be restricted to the yield on the bonds and the escrow used to pay debt service on the next available payment date.

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

EXAMPLE 1

IHELA issues $10 million of bonds and loans the proceeds to DavisBrown College for construction of a science building. It later sells the building for $5 million and all Bonds are still outstanding.

• Deliberate Action: DavisBrown College must own the financed property and upon sale no longer owns the property.

• Nonqualified Bonds: All $10 million

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

EXAMPLE 1 Remediation includes: • Using all $5 million in proceeds to redeem within 90 days

or establish a defeasance escrow for a pro rata portion of the $10 million of nonqualified bonds. Remaining outstanding $5 million would not be private activity bonds because the issuer remediated as required.

• Apply the $5 million to a qualifying alternative use within two years

The Proceeds are considered gross proceeds of the bonds and subject to yield restriction and arbitrage rebate rules

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

EXAMPLE 2 IHELA issues $10 million of Bonds and loans the proceeds to

StruttTodd College for construction of a Business School and used the proceeds to purchase land for $5 million and construct the building for $5 million. Later while all the bonds are still outstanding, the College sells a portion of the land for $3 million (of which $2 million in bond proceeds were spent to purchase)

• Deliberate Action: College must own the financed property and upon sale no longer owns a portion of the property.

• Nonqualified Bonds: $2 million

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

EXAMPLE 2 Remediation includes: • The Issuer may redeem $2 million of outstanding

bonds (which leaves the Borrower with $1 million of gross proceeds); or

• The $3 million in proceeds must be applied towards a qualifying use within two years

The proceeds are considered proceeds of the bonds and are subject to yield restriction and arbitrage rebate rules

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

EXAMPLE 3 IHELA issues $6 million of tax-exempt bonds and loans

to VanSickel College. College contributes an additional $4 million in cash to finance a $10 million Art Studio. Later College sells studio for $12 million and all bonds are still outstanding

• Deliberate Action: College must own the financed property and upon sale no longer owns the property.

• Nonqualified Bonds: $6 million

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

EXAMPLE 3 Remediation includes: • Redeeming all $6 million of nonqualified bonds; or • Using $12 million of proceeds for an alternative use

within two years Only $6 million of the proceeds are considered gross proceeds

and subject to yield restriction and arbitrage rebate rules. When all of the Bonds are redeemed, the remaining $6 million of the proceeds are not subject to the federal tax restrictions since the amount of gross proceeds cannot exceed the amount of the outstanding bonds of the issue.

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

VOLUNTARY CLOSING AGREEMENT PROGRAM (VCAP)

If Remediation is not available, then an Issuer or conduit borrower must use the Voluntary Compliance Agreement Program to resolve federal tax violations relating to bonds or risk getting audited and losing the tax-exemption on the bonds

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

Voluntary Compliance Agreement Program (VCAP)

• Implemented in 2001 • IRS is encouraging issuers to resolve violations • Result is generally lower settlement amount

that achieved through an audit

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

VCAP Eligibility • Not available if remedial action can be taken • Not available if bond issue is under audit • Not available if tax-exempt status of bonds is

issue in a court proceeding or considered by Office of Appeals

• Not available if violation due to willful neglect • Can apply anonymously

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

Selection of a Bond Issue for Audit • Random • Review of returns filed by issuers (8038) or conduit

borrowers (990, schedule K) • Referrals from other federal agencies, news articles

or internal sources • Information item prepared by IRS revenue agents for

follow-up action • Picked up due to claim in a field examination

©2013 DAVIS BROWN KOEHN SHORS & ROBERTS P.C.

Thank you

Courtney A. Strutt Todd Davis Brown Law Firm