renaissance: rails, capital & capacity under challenge anthony b. hatch – abh consulting 155...

TRANSCRIPT

Renaissance: Rails, Capital & Capacity Under Challenge

Anthony B. Hatch – abh consulting 155 W68th Street NYC 10023 (212) 595-0457

Fall Forum ATLP/NITL 2007Fall Forum ATLP/NITL 2007

Washington DCWashington DC

October 15, 2007October 15, 2007

Railroads at historic tipping point Capacity issues across all modesCapacity issues across all modes Volume increasing Volume increasing – right?– right? Share increasingShare increasing Rates increasing Rates increasing Services levels (yes) increasingServices levels (yes) increasing Returns increasingReturns increasing But pushback (shipper/regulator/union also increasing)But pushback (shipper/regulator/union also increasing) A A secularsecular, not a cyclical story, not a cyclical story Capacity and infrastructure – and competitor - issues remainCapacity and infrastructure – and competitor - issues remain Not fully reflected in the market? Or is this just another cyclical Not fully reflected in the market? Or is this just another cyclical

slowdown?slowdown?

Street influence on RRs – and Why that affects ALL stakeholders Battle for cashBattle for cash Management’s reactions to pressuresManagement’s reactions to pressures Investors, competitors, regulators, Investors, competitors, regulators,

politicians, labor – oh, yes, and customerspoliticians, labor – oh, yes, and customers Short term decisions/long term Short term decisions/long term

consequencesconsequences

Show Me the Money

Share Price is Share Price is thethe Indicator – over time! Indicator – over time! Cash (Flow) is KingCash (Flow) is King High ROIC = High Stock PriceHigh ROIC = High Stock Price And Vice VersaAnd Vice Versa Key is the phrase “through a cycle”Key is the phrase “through a cycle” Old Model: DisinvestmentOld Model: Disinvestment New Model: TBD (But CP gives us a clue)New Model: TBD (But CP gives us a clue)

Spending $: Mgmt.’s #1 Decision

Capex for Maintenance – “base”Capex for Maintenance – “base” Capex for Capacity, Service & GrowthCapex for Capacity, Service & Growth DividendsDividends Share BuybacksShare Buybacks M&A – StrategicM&A – Strategic M&A – Non-strategic (conglomeracy)M&A – Non-strategic (conglomeracy) How management allocates indicates confidence How management allocates indicates confidence

& direction and impacts all stakeholders& direction and impacts all stakeholders

Virtuous Circle 2004-07

Better returns (half Better returns (half finallyfinally earn returns earn returns equal to the cost of capital)equal to the cost of capital)

Better stock prices Better stock prices Better revenue prospects – up double digit Better revenue prospects – up double digit

’04-06’04-06 Equals more investment – capex up sharply Equals more investment – capex up sharply Equals more capacity, better serviceEquals more capacity, better service ……equals better returns and growth….equals better returns and growth….

Sources of capital

FCF – booming at most carriers (capex vs. ROIC)FCF – booming at most carriers (capex vs. ROIC) Governments – states, PAs, FedsGovernments – states, PAs, Feds Governments – Canada as contrastGovernments – Canada as contrast Traditional Street sources & BanksTraditional Street sources & Banks Institutional investorsInstitutional investors Hedge fundsHedge funds Private Equity/Infrastructure Funds (still?)Private Equity/Infrastructure Funds (still?)

New Sources of Capital – Threat or Opportunity? Fortress-RailAmerica/FEC (etc)Fortress-RailAmerica/FEC (etc) Infrastructure Funds (Toll Roads)Infrastructure Funds (Toll Roads) Hedge Funds & “Activists” (TCI)Hedge Funds & “Activists” (TCI) Share repos – UNP, BNSF and especially Share repos – UNP, BNSF and especially

CSXCSX C-1 Buyouts (CP)C-1 Buyouts (CP)

Threats to the Renaissance?

Cyclical vs. secular argumentCyclical vs. secular argument New Congress –impacting labor & shippersNew Congress –impacting labor & shippers Rereg – the MAD answerRereg – the MAD answer Execution: serviceExecution: service Execution: mergerExecution: merger Hedge fund investment reality – or the perception Hedge fund investment reality – or the perception Liquidity?Liquidity?

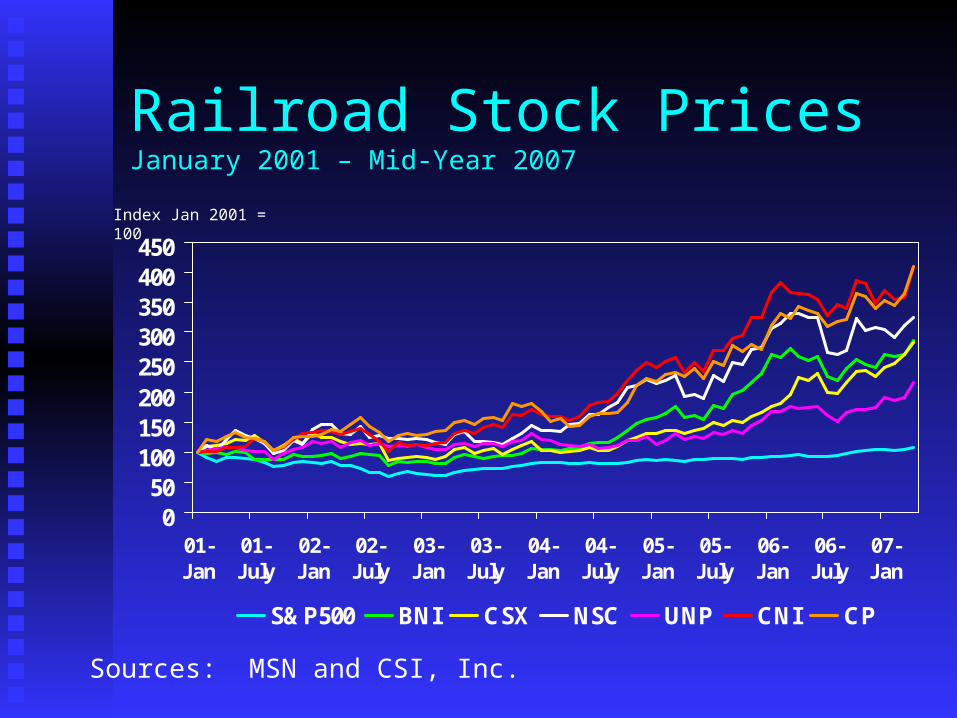

Railroad Stock PricesJanuary 2001 – Mid-Year 2007

050

100150200250300350400450

01-Jan

01-July

02-Jan

02-July

03-Jan

03-July

04-Jan

04-July

05-Jan

05-July

06-Jan

06-July

07-Jan

S&P500 BNI CSX NSC UNP CNI CP

Index Jan 2001 = 100

Sources: MSN and CSI, Inc.

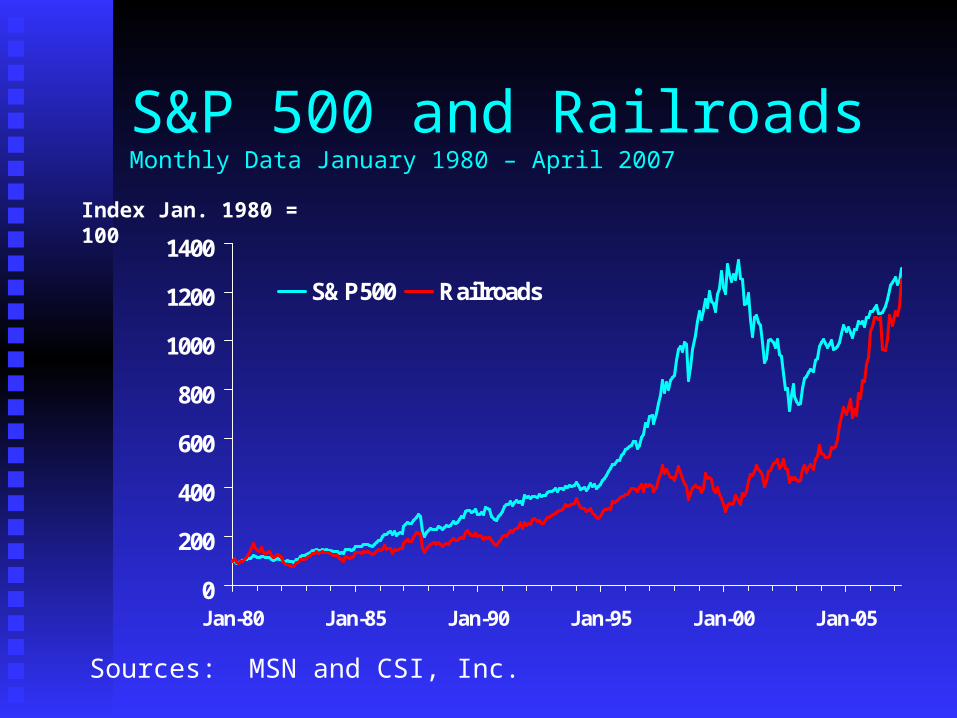

S&P 500 and RailroadsMonthly Data January 1980 – April 2007

Index Jan. 1980 = 100

Sources: MSN and CSI, Inc.

0

200

400

600

800

1000

1200

1400

Jan-80 Jan-85 Jan-90 Jan-95 Jan-00 Jan-05

S&P500 Railroads

10.3%

11.3%

12.3%

16.1%

16.9%

18.7%

28.4%

24.9%

Forest Products

Electric Utilities

Railroads*

All Industries

Autos & Parts

Chemicals

Pharmaceuticals

Oil & Gas

*BNSF, CSX, NS, and UP Source: Business Week

Even With Booming Traffic, Rail Earnings Are SubstandardMedian Return on Equity in 2005 (S&P 500 companies)

RR CoC vs. ROIC -stocks have done well but… they still trade at a discount to all stocks

0%2%4%6%8%

10%12%14%16%18%20%

81 84 87 90 93 96 99 02 05

Source: Surface Transportation Board

Cost of Capital

Return on Investment

Railroad Capital ExpendituresClass I Railroads

$0

$2

$4

$6

$8

$10

80 82 84 86 88 90 92 94 96 98 00 02 04 06

Billions

Source: Railroad Facts, AAR

Capital Expenditures as % of Revenue

Source: Census Bureau, EEI, AAR

Food – 2.6%

Transportation equipment – 2.8%

Petroleum & coal products – 3.0%

Wood products – 3.0%

Average all manufacturing – 3.5%

Chemicals – 4.4%

Nonmetallic mineral prod. – 5.4%

Paper – 4.7%

Fabricated metal products – 3.5%

Electric utilities – 11.6%

Class I RRs – 17.8%

Railroad PerformanceClass I Railroads

050

100150200250300

64 68 72 76 80 84 88 92 96 00 04

Index 1981 = 100

Source: Railroad Facts, AAR

Productivity

Volume

Revenue

Price

Intermodal Growth DriversDomestic and International GlobalizationGlobalization TradeTrade Railroad Cost Railroad Cost

AdvantagesAdvantages Share Recovery From Share Recovery From

HighwayHighway Truckload IssuesTruckload Issues

RRs and Investment

Is growth affordable? Capex up 10% in ’07?Is growth affordable? Capex up 10% in ’07? Can the intermodal model extend to carload?Can the intermodal model extend to carload? Is additional capacity necessary? Desirable?Is additional capacity necessary? Desirable? Wall Street’s constrictive role (“fighting the Wall Street’s constrictive role (“fighting the

last war”) – last war”) – changing?changing? Is this disconnect between the Renaissance Is this disconnect between the Renaissance

and the Street the opportunity of a lifetime?and the Street the opportunity of a lifetime?

Serious U.S. Transportation and Congestion Problems High Cost of Highway High Cost of Highway

Maintenance and Maintenance and ConstructionConstruction

Interdependence of ModesInterdependence of Modes $67 billion per Year Drag $67 billion per Year Drag

on Economyon Economy Demand for Freight Demand for Freight

Transportation to Double Transportation to Double by 2020by 2020

Railroad Issues Fall 2007 #1 is #1 is Economic/industrial statusEconomic/industrial status – recession? Perfect Landing? Etc? – recession? Perfect Landing? Etc? Service metricsService metrics – recovery or a meltdown (again)? The key behind – recovery or a meltdown (again)? The key behind

shipper/regulatory angst?shipper/regulatory angst? Trucking s/t surplus but – l/t troubles a Trucking s/t surplus but – l/t troubles a secularsecular issue issue Capacity – coming shortage? Capacity – coming shortage? Or “creative tension”?Or “creative tension”? Intermodal – new king of the hillIntermodal – new king of the hill Coal and Grain: Comeback? Thanks to oil!Coal and Grain: Comeback? Thanks to oil! Ethanol – growth or Paying Peter…Ethanol – growth or Paying Peter… Is Growth Affordable?Is Growth Affordable? (Who will pay?) (Who will pay?) Alliances vs. Mergers? Big projects in Canada, Mexico and WyomingAlliances vs. Mergers? Big projects in Canada, Mexico and Wyoming Labor – Coming shortage?Labor – Coming shortage? Safety and security – new risk? Who pays?Safety and security – new risk? Who pays?

Intermodal’s Enduring Questions

Lots of moving partsLots of moving parts The improved ROIC of RR Intermodal The improved ROIC of RR Intermodal

’03-’06 is the essence of the ’03-’06 is the essence of the Railroad Railroad RenaissanceRenaissance

Long term volume growth rate of 5-7%Long term volume growth rate of 5-7% Long term pricing growth rate 3-4%Long term pricing growth rate 3-4% True International drives the trainTrue International drives the train Will “True” Domestic join the party?Will “True” Domestic join the party?

Coal and Ag – Bulk Comeback

New growth mode?New growth mode? Emissions and environmental issuesEmissions and environmental issues Oil prices and coalOil prices and coal Politics and coal; and grain/reregPolitics and coal; and grain/rereg EthanolEthanol ExportsExports FeedFeed

Railroad Rates- the old story Class I Railroads, Revenue Per Ton-Mile

01234567

80 82 84 86 88 90 92 94 96 98 00 02 04 06

Cents

Source: Railroad Facts, AAR

Current $: Down 1% since 1980

Constant $: Down 54% since 1980

Pricing - the new paradigm Rates up 3% in ’04 – post-Staggers bestRates up 3% in ’04 – post-Staggers best Up 11%Up 11% in ’05 (Secular rate of 2-3%?) in ’05 (Secular rate of 2-3%?) Fuel surcharges similar to TLFuel surcharges similar to TL Yet Price Gap to the highway Yet Price Gap to the highway widening, even in ’05 and widening, even in ’05 and

’06 YTD’06 YTD Capacity (still) short across all freight modes, despite Capacity (still) short across all freight modes, despite

temporary surplusestemporary surpluses Rails moving toward tariff and spot marketsRails moving toward tariff and spot marketsConclusion: Conclusion: Best Ever Rate EnvironmentBest Ever Rate Environment““The new Golden era” – cost of capital The new Golden era” – cost of capital within sightwithin sight; not there ; not there

yetyet

Railroad Employee ProductivityClass I Railroads, Ton-Miles Per Freight Service Employee

0

2

4

6

8

10

12

80 82 84 86 88 90 92 94 96 98 00 02 04 06

Source: Railroad Facts, AAR

Millions

Rail Service Cycles

Is the recent improvement in the metrics Is the recent improvement in the metrics sustainable? Systemic? sustainable? Systemic?

Is it a product of huge capex injection and Is it a product of huge capex injection and IT?IT?

Or, is it merely a product of lower Or, is it merely a product of lower volumes/less stress on the network…volumes/less stress on the network…

Rail Regulatory Risk CTA reform not a major issue; Canadian shipper/provincial/carrier CTA reform not a major issue; Canadian shipper/provincial/carrier

cooperation at all time levelscooperation at all time levels STB reviewing a number of issues, with some expected minor shipper STB reviewing a number of issues, with some expected minor shipper

“wins”, as rates improve after years of subsidy“wins”, as rates improve after years of subsidy F/S covers 15-20% of revenues (less than 10% of CP)F/S covers 15-20% of revenues (less than 10% of CP) Small shipper, Small shipper, cost of capitalcost of capital,, paper barrierspaper barriers, other STB issues under , other STB issues under

review also BUT:review also BUT: Labor a wild cardLabor a wild card Potential new Revenue Adequacy rules not (at all) linked to realityPotential new Revenue Adequacy rules not (at all) linked to reality Haz-Mat/Security an emerging problemHaz-Mat/Security an emerging problem AAR best lobby in DC – re-reg chances virtually zero, but too much AAR best lobby in DC – re-reg chances virtually zero, but too much

time will be spent on DEFENSEtime will be spent on DEFENSE ITC chances reducedITC chances reduced

ABH ConsultingAnthony B. Hatch155 W. 68th StreetNew York, NY 10023(212) [email protected]