report no. 151la-in appraisal of the industrial credit and...

TRANSCRIPT

FILE COPYReport No. 151la-IN

Appraisal of the Industrial Credit andInvestment Corporation of India Limited India

June 22, 1977

Industrial Development and Finance DivisionSouth Asia Projects Department

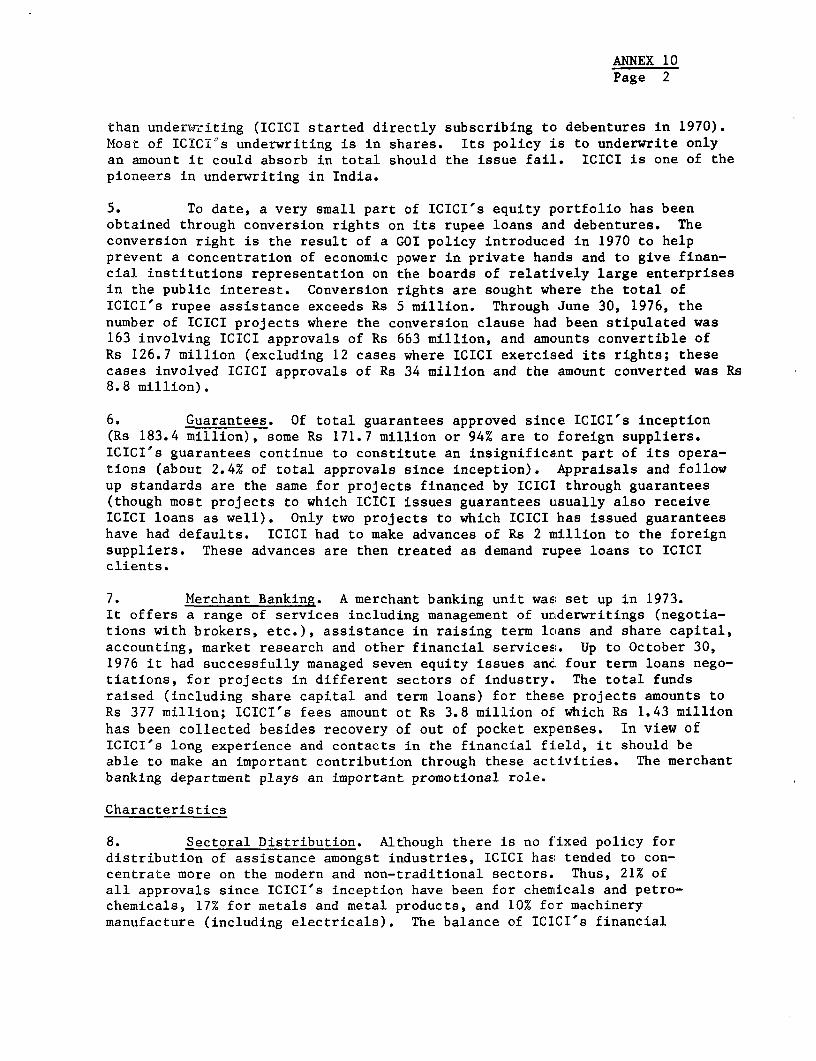

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

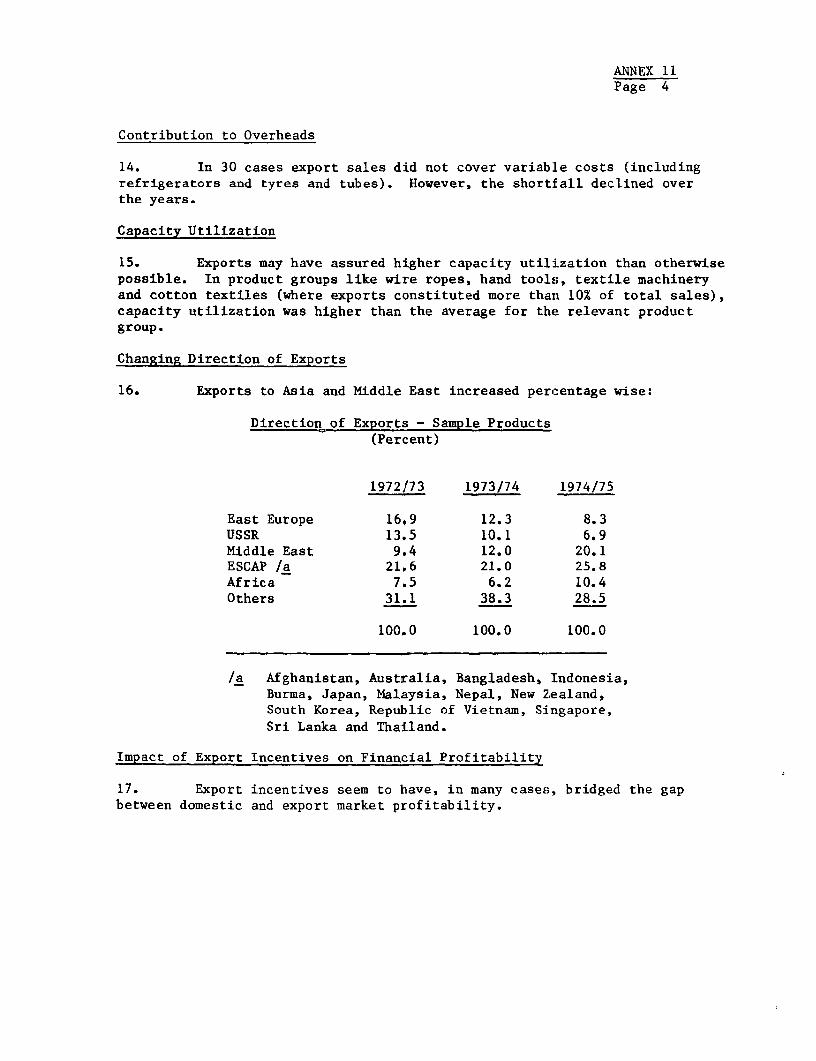

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

US$1.00 = Rs 9.00Rs 1 US$0.111Rs 10 million = US$111,000Rs 1.0 million US$111 million

ABBREVIATIONS

CDFC - Commonwealth Development Finance CorporationCGC - Capital Goods CommitteeDEC - Deutsche Gesellschaft fuer Wirtschaftliche

Zusammenarbeit (Entwicklungsgesellschaft)DFC - Development Finance CompaniesDRC - Domestic Resource CostERR - Economic Rate of ReturnFRR - Financial Rate of ReturnGIC - General Insurance Corporation of IndiaGOI - Government of IndiaICICI - Industrial Credit and Investment Corporation of

IndiaIDBI - Industrial Development Bank of IndiaIFCI - Industrial Finance Corporation of IndiaIIG - Inter-Institutional Group1IM - Inter Institutional MeetingIRCI - Industrial Reconstruction Corporation of IndiaKfW - Kreditanstalt fuer WiederaufbauKITCO - Kerala Industrial and Technical Consultancy

OrganizationLIC - Life Insurance CorporationMRTP - Monopolies and Restrictive Trade Practices ActNEITCO - iNorth Eastern Industrial and Technical Consultancy

OrganizationNSIC - National Small Industries CorporationRBI - Reserve Bank of IndiaSBI - State Bank of IndiaSFC - State Financial CorporationSIA - Secretariat for Industrial ApprovalsSIDC - State Industrial Development CorporationSISI - Small Industries Service InstituteSSI - Small Scale IndustrySSIC - State Small Industries CorporationSSIDC - State Small Industries Development CorporationUTI - Unit Trust of India

FISCAL YEARS

GOI, SFCs - April 1 - March 31ICICI - January 1 - December 31IDBI, IFCI, IRCI, RBI - July 1 - June 30

FOR OFFICIAL USE ONLY

INDIA

APPRAISAL OF THEINDUSTRIAL CREDIT AND INVESTMENT CORPORATION OF INDIA LIMITED

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS ............................. i - iii

I. INTRODUCTION ................ 1.......1

II. ENVIROMIENT . ..

General ........ 1............Industrial Sector- Structure andPast Performance . ..... 2

The Environment for Industry. 3Industrial Policies Affecting the

Private Sector . ...... 4

Industrial Finance . . ............... . ... 6

Prospects... 8

III. INSTITUTIONAL ASPECTS. 9Share Capital and Ownership .9

Organization and Staff .9

Procedures and Standards .10Operating Policies .11Relations with Government and Business

Community ... 12

IV. RESOURCES AND OPERATIONS ............................ 12

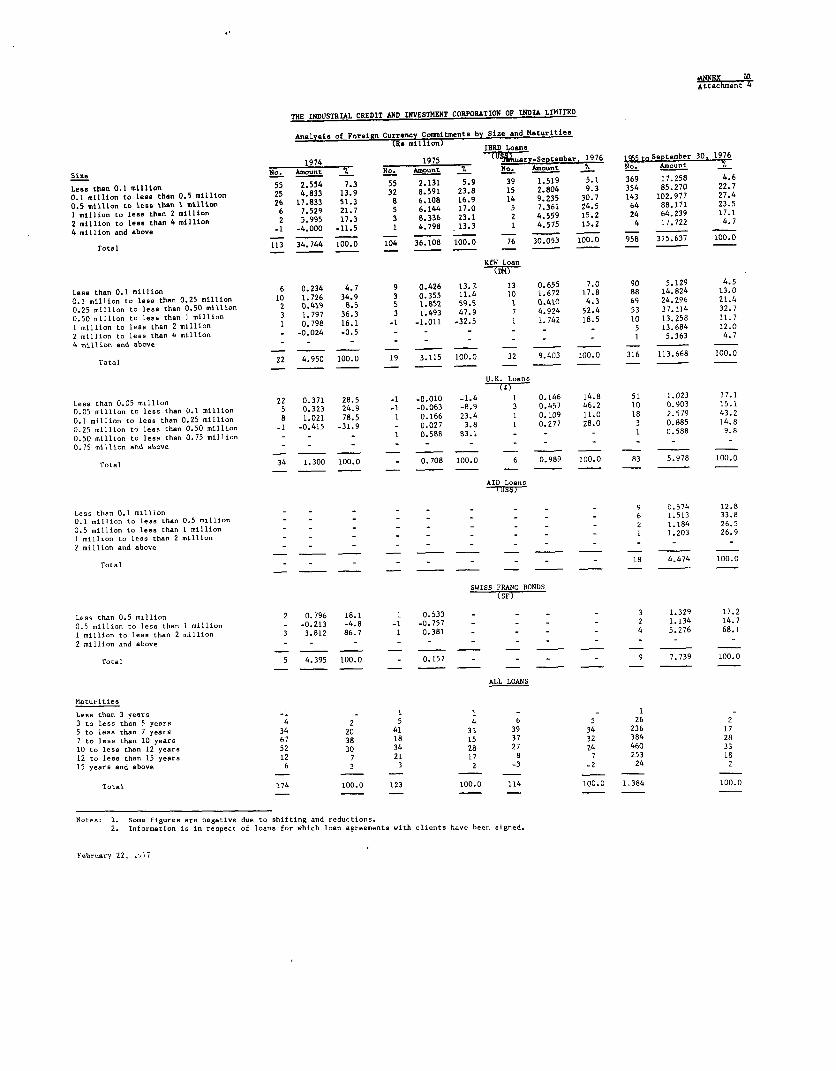

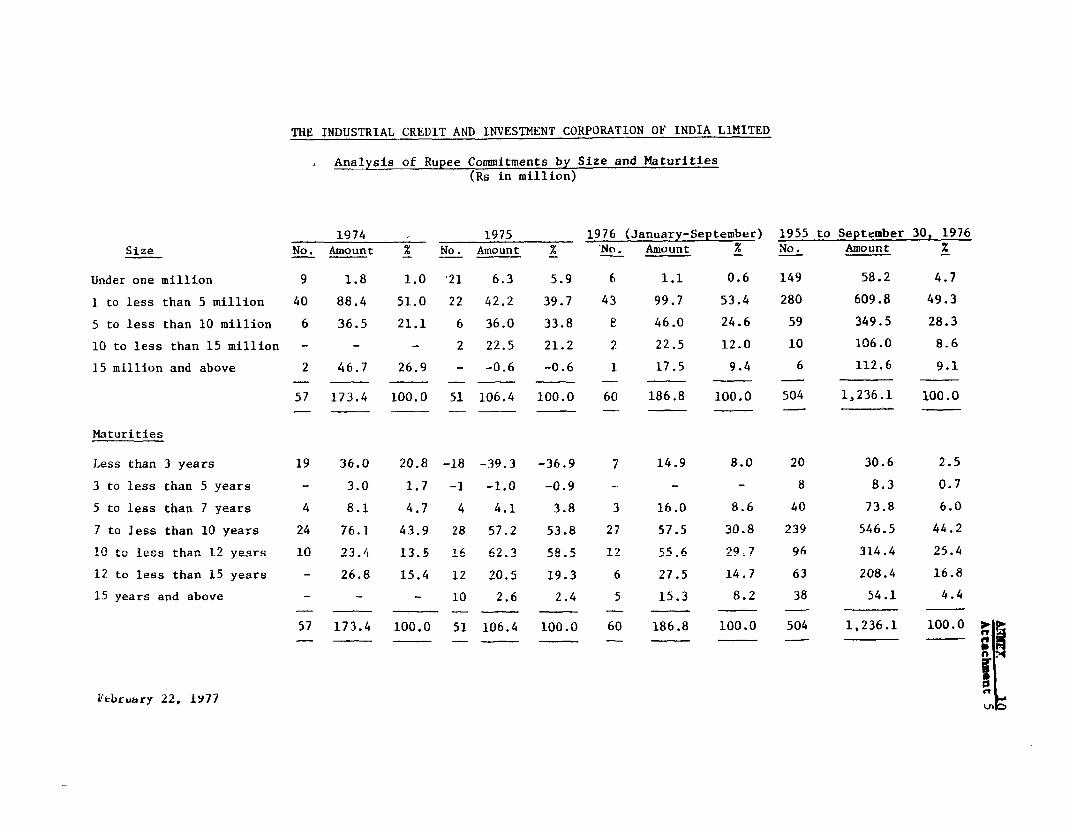

Resource Mobilization ... 12Resource Allocation ... 14Promotional Activity . 14Development Impact .................. ... 16

V. FINANCIAL ASPECTS ...... 16

Quality of Portfolio . ......... 16

Financial Position ..... . . .. 18

This report is based on an appraisal mission consisting of Messrs. E. Elejaldeand W. Schaefer in November/December, 1976.

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank/IFC authorizaion.

-2-

Page No.

V 3PECTS .................... ................ 20GOI Policy on Import Licensing andForeign Exchange Allocation 20

Business Forecast . . .................... . 20Resource Requirements . .21

Financial Projections ......................... 22

VII. AGREEMENTS REACHED ....... ............. ..... ............ .. . 23

LIST OF ANNEXES

1. Institutional Finance for Industry in India2. Selected Borrowing and Lending Rates - FY73-August 30, 19763. Distribution of Shareholding as of October 31, 19764. Members of the Board of Directors as of October 31, 19765. ICICI's Financing Strategy for 1977-796. Main Terms and Conditions for Assistance as on October 31, 19767. Resource Position as of September 30, 19768. Details of Foreign Currency Borrowings Concluded up to

October 31, 19769. Details of Rupee Borrowings Concluded up to October 31, 197610. ICICI's Overall Operations11. ICICI's Export Study12. Outline of the Proposed Study of Selected Subsectors

of the Engineering Industry13. Economic Indicators for Projects Approved14. Trend in Arrears (1965 to September 1976)15. Classification of Arrears as of September 30, 197616. Analysis of Equity Portfolio as of September 30, 197617. Income Statements - 1971-75 and Jan.-Sept. 30, 197618. Balance Sheets - 1975-75 and September 30, 197619. Cash Flow Statements - 1971-75 and Jan.-Sept. 30, 197620. Forecast of Approvals, Commitments and Disbursements - 1976-8021. Projected Foreign and Domestic Currency Resource Position - 1976-8022. Projected Income Statements - 1976-8023. Projected Balance Sheets - 1976-8024. Projected Cash Flow Statements - 1975-8025. Estimated Disbursement Schedule

Organization Chart (as on June 30, 1976).

Map - IBRD 3873

INDIA

APPRAISAL OF THEINDUSTRIAL CREDIT AND INVESTMENT CORPORATION OF INDIA LIMITED

SUMMARY AND CONCLUSIONS

i. The Industrial Credit and Investment Corporation of India (ICICI)was established in 1955 with the active participation of the IBRD, which hascontinued to maintain close contact with ICICI, through the provision ofeleven loans amounting to $425 million. The most recent was a $100 millionloan in April 1975, of which $85 million had been credited and $37 milliondisbursed by the end of April 1977.

ii. Over the last 20 years, ICICI has developed into a well managedinstitution with a successful record in industrial financing. The objectivesof the proposed loan of $80 million would be to continue to utilize ICICI asan efficient channel for financing high priority industrial projects many ofwhich are export oriented and/or are located in backward areas. ICICI willcontinue to undertake studies of specific industrial development problems,which will be of direct assistance to ICICI in its operations.

iii. ICICI is a major source of institutional finance for India'sindustry. In 1976, ICICI accounted for about 72% of total foreign exchangeapprovals by the country's industrial term lending institutions. IBRDaccounts for 85% of ICICI's foreign currency resources. ICICI has alsoreceived foreign funds from other official sources such as the USAID, KfW andthe UK. Finally, ICICI has been making efforts to diversify its sources offoreign exchange into commercial funds and has already raised $2 millionthrough a Swiss bond issue. In 1976, ICICI's foreign and rupee disbursementsaccounted for 14% of total disbursements by industrial term lending institu-tions and about 2.5% of total private industrial investment in India. ICICI'srupee funds have been raised through Government borrowings, share issues,internal cash generation, and more recently through a successful series oflarge debenture issues.

iv. ICICI's ownership structure is composed of public sector enterprises(76%), foreign enterprises (14%) with the balance (10%) from the Indian privatesector. ICICI has continued to enjoy strong management and benefit from astrong, well trained staff. Though ICICI maintains close contact with Govern-ment on industrial policy matters, it retains its operational autonomy.

v. ICICI's approvals fell slightly in 1975 to Rs 712 million comparedto Rs 723 million in 1974 due to reduced industrial demand in key subsectors.However, during the first ten months of 1976, approvals were 18% higher (Rs841 million) than in the twelve months of 1975. ICICI has emphasized themodern non traditional industries such as chemicals and petrochemicals (21%),metals and metal products (17%) and machinery manufacture (10%).

- ii -

vi. ICICI's- developmental impact has been substantial. ICICI's ex anteeconomic rates of return (ERRs) calculated on its projects continue to besatisfactory; e.g. weighted ERRs for the larger projects have been 22.6% in1975 and 29.5% for the first half of 1976. ICICT has also increased itslending to backward areas to 40% from 1974 to 1976 compared to 12% from 1955to 1970, Further, the total exports of ICICI's clients increased by 56% from$230 million in 1973/74 to $355 million in 1974/75, the latter representing17% of India's total industrial exports. Similarly, the direct employmentimpact has been satisfactory (fixed cost per job of $16,000 in 1975) consid-ering the size of ICICI's clientele. Finally, ICICI has expanded its promo-tional activities and provides training for many development banking stafffrom both India and abroad, assists clients in the formulation of foreigntechnical and financial collaboration agreements, and gives financial coun-selling and underwriting assistance through its merchant banking unit.

vii. In conjunction with the eleventh loan, ICICI undertook a study ofthe export experience of its clients and the role of incentives, the firstdraft of which was completed at the end of 1976. The study has alreadyprovided valuable insights into the problems and prospects of export manufac-turers and the impact of incentives. Similarly, ICICI intends to undertake twoadditional studies as part of the proposed loan namely (a) review of existingcompany data from the export study to test certain hypotheses concerning"1penetration pricing" in export marketing and (b) a review of the problemsand prospects of selected subsectors of the engineering industry. Finally,ICICI has completed a preliminary study for the creation of a specializedinstitution to finance lower and middle income housing for which it is seekingparticipation by IFC.

viii. ICICI's financial position remains satisfactory, though arrears havecontinued to increase in the past year, as total principal outstanding of loansaffected by arrears was about 18% of the outstanding loan portfolio comparedto 7% in 1973 due to power cuts, credit restrictions, and business recession.The collection ratio was 85% in 1976 compared to 90% from 1971 to 1973. Thearrears position is expected to improve in 1977; ICICI is taking appropriatemeasures to improve collection performance. Loan provisions amounted to Rs 27million at the end of 1975, but will probably increase when the 1976 audit iscompleted. ICICI's net profit as a percentage of average equity has remainedat 11% over the past four years, a satisfactory level. ICICI's debt/ equityratio (Bank definition) was 8.6:1 as of September 30, 1976, or below thecontractual limit of 9:1.

ix. While the prospects for improved industrial growth appear good,the level of ICICI's future operations has been forecast with caution dueto the slackness in demand in certain manufacturing subsectors as well asthe possibility that GOI may allocate more free foreign exchange funds toindustrial capital goods imports thereby reducing the potential demand onICICI should some firms prefer to borrow rupees and buy foreign exchangeto avoid carrying the foreign exchange risk. On the basis of ICICI's presentresource position and of its own and the private industrial sector's foreignresource requirements for the two year period beginning September 1977, a

- iii -

twelfth loan of $80 million is recommended which would account for about 60%of ICICI's foreign currency commitments during this period. ICICI also ex-pects to obtain a $17 million from the Kuwait Investment Company in 1977 which,due to its short lump sum maturity of 5 years, should be blended with Bankfunds. As a consequence, at a maximum, repayments to the Bank of $17 millionwould be spread over years 6-17 rather than years 4-5. Thus, the loan wouldbe made on a flexible amortization schedule including 3 years grace normally,and up to 5 years grace in selected cases. ICICI would relend the proceeds ofthe loan at its normal foreign currency rate (presently 11% ordinary and 10%for backward areas) thereby providing a spread of between 1.5-2.5% which isadequate. The proposed free limit is $4 million the same as in the last fourBank loans.

INDIA

APPRAISAL OF THEINDUSTRIAL CREDIT AND INVESTMENT CORPORATION OF INDIA LIMITED

I. INTRODUCTION

1.01 The Industrial Credit and Investment Corporation of India (ICICI)was established in 1955 with IBRD assistance. Since then, it has receivedeleven loans from IBRD totalling $425 million. The eleventh loan ($100million) was approved in April 1975. By end April 1977, IBRD had credited$85 million and disbursed $37 million, in line with the original schedule.Previous loans were by then fully committed. Only $9 million remained un-disbursed from the tenth loan ($70 million), which is ahead of schedule.

1.02 Over the last 20 years, ICICI has developed into a well managedinstitution with a successful record in industrial financing. A jointstudy undertaken in 1973 by ICICI and IBRD to evaluate ICICI's developmentalimpact, which included ex-post analyses on a representative sample of itsprojects in operation, confirmed that ICICI was allocating resources toeconomically efficient projects. A performance audit by the Bank Group'sOperations Evaluation Department during 1975 for the sixth, seventh andeighth loans also concluded that ICICI's achievements were satisfactory.This report appraises ICICI for a $80 million twelfth loan. It focusseson ICICI's overall performance since the eleventh loan was made. 1/

1.03 While ICICI is making efforts to diversify its sources of foreignexchange, it still needs IBRD support. The objectives of the proposed loanwould be: (i) to continue to utilize ICICI as an efficient channel forfinancing high priority industrial projects many of which are export orientedand/or are located in backward areas; and (ii) to continue to encourage ICICI,to undertake studies of specific industrial development problems, which willbe of direct assistance to ICICI in its operations.

II. ENVIRONMENT

General

2.01 A full assessment of India's present economic position is containedin the Bank's latest Economic Report No. 1529-IN dated April 25, 1977.

2.02 To summarize the current situation: India entered FY76 havingbeen through one of the most difficult periods since Independence. Progressin dealing with long-term development problems had been limited by poor crops,

iJ Appraisal Report No. 637a-IN of March 14, 1975.

-2-

dramatic shifts against India in the terms of trade, and inflation. Adjust-ments to ;:hese immediate difficulties thus became the principal preoccupa-tion in economic management. However, with favorable monsoons and additionalforeign assistance, it now appears that India has successfully weathered theproblems of the recent past. Once again there is the basis for an upturn inthe growth rate of the economy.

2.03 Most important among the favorable factors has been a bumper har-vest which followed years of poor or modest agricultural output. Foodgrainproduction in FY76, estimated at around 117 million tons, exceeded the pre-vious record of FY71 by 8%. Oilseeds, sugarcane and cotton also reached newproduction peaks and provided ample supplies for the agro-industries. In FY77,a good harvest is again expected of at least 110 million tons of foodgrains.Secondly, deficiencies in the supply of basic commodities and of infrastruc-tural inputs such as energy and transport, which had been prevalent in thepast, have been eased. Electricity generation and domestic production ofcoal, oil, cement and steel all increased by over 10% during FY76 and by afurther 15% in the first eight months of FY77. Finally, the increased supplyof agricultural and industrial products and of services, together with thedemand restraint imposed by the Government since mid-1974, put a virtual stopto inflation. From April 1975 to March 1976, the Wholesale Price Index fellby 8.1%o Although from April to September 1976 the Index rose by 11%, it wasstill 5% lower in September 1976 than in September 1974.

2.04 On the balance of payments front, there have been a number of en-couraging developments. Firstly, the rapid build-up of foodgrain stocks toa level of 17 million tons by December 1976 provides a buffer against theimpact of a future crop failure on the balance of payments and has reducedcurrent import requirements. Secondly, despite generally unfavorable worldtrading conditions, export earnings rose by 9% in FY76, and seem likely torise by more than this in FY77. Thirdly, the value of petroleum imports wasstabilized in FY76 (although thete is likely to be a rise in FY77), and steelimports have been progressively reduced in FY76 and FY77 as a result ofincreased domestic production. Finally, increased production and loweredworld prices have reduced fertilizer import values quite sharply. As a resultof these factors, imports rose only 5% in value in FY76 and the trade deficitfell by almost $100 million. Developments so far in FY77 suggest a moredramatic improvement in the trade balance this year. Moreover, since net aidrose 49% in FY76 and India received substantial inflows of private remittancesduring the past one and a half years, reserves rose by almost $800 million inFY76, and are continuing to rise at a comparable rate in FY77. These reservesgive India added flexibility in adjusting to a higher rate of growth in thefuture.

Industrial Sector - Structure and Past Performance

2.05 India's industrial output has grown on average by only about 3.5%per annum since 1965 and manufacturing presently accounts for 16% of NDP,

-3-

as opposed to 14% in FY61. 1/ Within the manufacturing sector, there havebeen gradual changes in structure which reflect the priorities of the Gov-ernment's industrial development strategy with consumer goods industriesnow contributing less to value added. For example, the food processing andtextile industries' combined share has fallen from 43% in FY61 to 28% inFY75. Over the same period, the share of "basic" industries, (defined toinclude basic metals industries, chemicals and fertilizers), together withthe engineering industry, increased from roughly 40% of value added in manu-facturing to somewhat more than 50%.

2.06 While some two-thirds of manufactured output is estimated to comefrom registered plants, which are predominantly medium and large scale, themore labor-intensive unregistered, mainly small scale, sector employs two-thirds of the industrial labor force. The Government dominates mining andpower generation and, to an increasing extent, the "basic" industries withinthe manufacturing sector. Nonetheless, according to the 1970 Annual Surveyof Industry, almost 80% of industrial value added originated in the privatesector, and within the manufacturing sector, the figure was 85%. Even allow-ing for the recent nationalization of part of the textile industry, privateindustry must still account for at least three-quarters of output from themanufacturing sector. Within the private sector, food, paper, tobacco anda number of other industries make important contributions, but textiles,chemicals and engineering goods continue to be dominant.

2.07 In the last three years, industrial performance has improved sub-stantially. In FY74, industry grew by a mere 1%, and in FY75 growth was2.5%. With an improved supply position the industrial growth rate roseto 5.5% in FY76. Production of key manufacturing inputs, like steel, coal,and electric power improved dramatically in that year; capital goods produc-tion, which had declined by 4% in FY75, also recovered to the level of FY74;but the output of consumer goods slumped by 1.9%. In FY77, overall industrialgrowth (defined to include electricity and mining) is expected to be about10%. Selected data for the first nine months of the fiscal year show thatthe growth in the output of capital goods over the corresponding period ofFY76 was 8.5%, while consumer goods production has increased by 15.8%. Thesustained buoyancy of intermediate goods producing industries is indicated bythe 22.3% increase in steel production and the 14.2% rise in electricitygeneration. However, inventories of intermediate goods are high by historicalstandards, which indicates a continued constraint on final demand.

The Environment for Industry

2.08 Over the last fifteen years, both supply and demand factors havehindered industrial growth. Supply constraints have perhaps been more per-sistent. Through much of this period prior claims on foreign exchange con-strained the availability of essential intermediate inputs not manufactured

1/ If industry is more broadly defined to include the remainder of thesecondary sector - utilities and construction - then value added inindustry constitutes about 23% of NDP.

-4-

in India, and affected the supply of inputs, such as steel, at times whendomestic production was unable to match demand. Equally the unpredictableeffect of the monsoon on the supply of agricultural raw materials, such ascotton, has constrained industrial growth. Moreover, agricultural supplybottlenecks have tended to coincide with power shortages, since hydro supplyis also dependent on the monsoon.

2.09 However, when these supply constraints have not been binding, de-mand has usually been depressed. All of the four possible sources of growingdemand - import substitution, exports, the derived demand from the growth ofother major sectors and investment - have been weak. Thus, the principalopportunities for import substitution were largely exhausted by the mid-1960s;while exports have recently contributed to growth, they still constitute avery small part of total sales; the relatively slow growth trend of agricul-ture of little more than 2% has restricted demand for consumer goods; and,finally, Government real investment has remained stagnant, although this haschanged recently (para 2.24).

Industrial Policies Affecting the Private Sector

2.10 General, The Government has placed central emphasis on rapid in-dustrialization and national self-sufficiency as the keys to development. Atthe same time, the Government has sought to curb the concentration of economicpower through expanded public ownership, restrictions on the growth of "largehouses" and "dominant undertakings"; reservation of many products to the small-scale sector as well as special assistance to it; and finally support fordevelopment in backward regions. The aim of self-sufficiency has largelymanifested itself in the pursuit of import substitution as well as curbs onforeign-owned firms and other forms of foreign involvement in industry.

2011 The main instruments of industrial policy have been central licen-sing of investment and imports, physical allocation of "scarce" domesticallyproduced raw materials and controls on industrial prices. This system hasitself tended to conflict with other aims, especially that of curbing economicconcentration, since large firms are much better able to bear the overhead costsof dealing with a centralized bureaucracy. Controls have also restricted theability of firms to respond to changed opportunities, especially in overseasmarkets, and thus hampered exports. The extent of excess capacity indicatesthat the planning, which is the basis of the industrial licensing system hasbeen far from successful. Finally, price controls appear to have had a harmfuleffect on investment and modernization in such crucial industries as cottontextiles, sugar, and cement.

2.12 In the last two years there have been a number of important develop-ments in industrial policy. In the face of poor industrial performance andmuch underutilized or inefficiently utilized capacity, GOI has been reconsi-dering elements of its strategy. It recognized that existing capacity mustbe utilized more efficiently; that public sector enterprises should meet morecommercially oriented criteria for output, price, and profitability; and thatthere must be an increasing emphasis on exporting. It has taken a number ofmeasures to boost industrial growth, including liberalization of licensingprocedures, relaxation of import and other controls, fiscal incentives andmore emphasis on industrial modernization.

- 5 -

2.13 Liberalization of Licensing Procedures. The process of simplifyingprocedures for the issue of industrial and other licenses started in 1973 whena time limit on the disposal of licensing applications was established. 1/Subsequent changes towards liberalization of licensing have taken four majorforms. Firstly, diversification of production has been allowed in industrialmachinery, machine tools, electrical equipment, steel castings, and steelforging industries within the overall licensed capacity of a particular under-taking, in order to facilitate fuller utilization of installed capacity.Secondly, 15 export-oriented engineering industries are now allowed to growautomatically in a five-year period by 25% over their licensed capacity.Thirdly, 21 selected industries in the medium-scale sector have been exemptedfrom licensing and "Large Houses" and foreign companies (as defined in theForeign Exchange Regulation Act, FERA, 1974 2/) have been permitted to expandin 30 other industries subject to certain conditions. Finally, 29 selectedindustries have been allowed to utilize their installed capacity fully. Ingeneral, the obstacles posed by licensing procedures have been virtuallyeliminated for all except the Large Houses and FERA companies, for which theobstacles have been reduced.

2.14 Relocation of Controls and Fiscal Incentives. Import controls havebeen significantly liberalized and the procedures for obtaining export incen-tives and necessary raw materials have been streamlined. Export duties havebeen abolished on a number of commodities. Excise duties also have been re-duced for 45 industries and the rate of income tax has been lowered. 3/ Fur-ther, price controls have been lifted for many finished manufactures and priceincreases permitted for cement, coal and coke, commercial vehicles and aluminum.Distribution controls on industrial materials have been lifted for almost allitems. The Dividend Ordinance of 1974 was allowed to lapse in July 1976 thusremoving the restriction on payment of dividends.

2.15 Modernization. GOI has announced a modernization program for thetextiles, cement, jute, sugar and engineering industries. The scheme will bemonitored by IDBI, although ICICI will take the lead in the engineering in-dustry. GOI's disbursement targets are Rs 2,000 million per year for the nextthree years of which the engineering sector would account for about 20%, al-though it is unlikely that this level of disbursements can be achieved. Themodernization funds will be on-lent at 7.5%, compared with a normal lendingrate of 11%.

1/ The procedural changes then effected have had a marked impact in clearingthe backlog of cases and accelerating the process of issuing industriallicenses/letters of intent and approvals of applications for capital goodsclearances and foreign collaboration.

2/ FERA was also amended during 1976 to make the maximum foreign ownershipallowed more flexible if the company was exporting at certain levels.

3/ The FY77 budget provided for a reduction in the marginal rate of incometax from 77% to 66%. The basic exemption level was also raised. Tostimulate investment, the FY77 budget permitted companies an investmentallowance of 25% on the value of plant and machinery.

-6-

2.16 isodernization is, of course, an ongoing process which has beentaking place for some time - about 10% of ICICI's approvals over the lasttwo years have been for financing modernization, replacement and balancingequipment. Therefore, the main change will be the additional incentive forfirms to modernize as a result of the availability of cheaper funds. How-ever, the Government has not yet announced many of the details of theseprograms nor, more importantly, of how the basic structural problems ofthese industries are to be tackled.

2.17 The modernization fund will largely be used for financing localequipment, and will, therefore, not affect the demand for the proposed loan.The proceeds of the loan may be used in part to support the modernizationneeds of ICICI's clients (although not on a subsidized basis) as has beendone in the past. As such, the loan will complement the Government's mod-ernization fund. However, there are wider issues that need to be tackledand, with this in mind, ICICI will undertake studies of selected engineeringsubsectors which would include an analysis of their modernization require-ments.

2.18 Conclusion. These various changes mark a cumulatively significanteffort on the part of GOI to tackle the problems of India's private industrywithin the context of the overall policy framework. However, major tasks doremain, especially the generation of a satisfactory demand growth and increasedemphasis on efficiency in the use of resources. The improved export perform-ance and increased Government expenditures on top of the higher agriculturalincome from recent good harvests help explain the recent upturn in industrualdemand. To sustain it, the Government will have to continue efforts to en-courage exports and private investment and, of greatest importance for theimmediate future to raise the level of public expenditure. Within such frame-work, ICICI has an important role to play in providing funds for investmentand, through its project appraisal, in guiding resources in an efficientdirection.

Industrial Finance

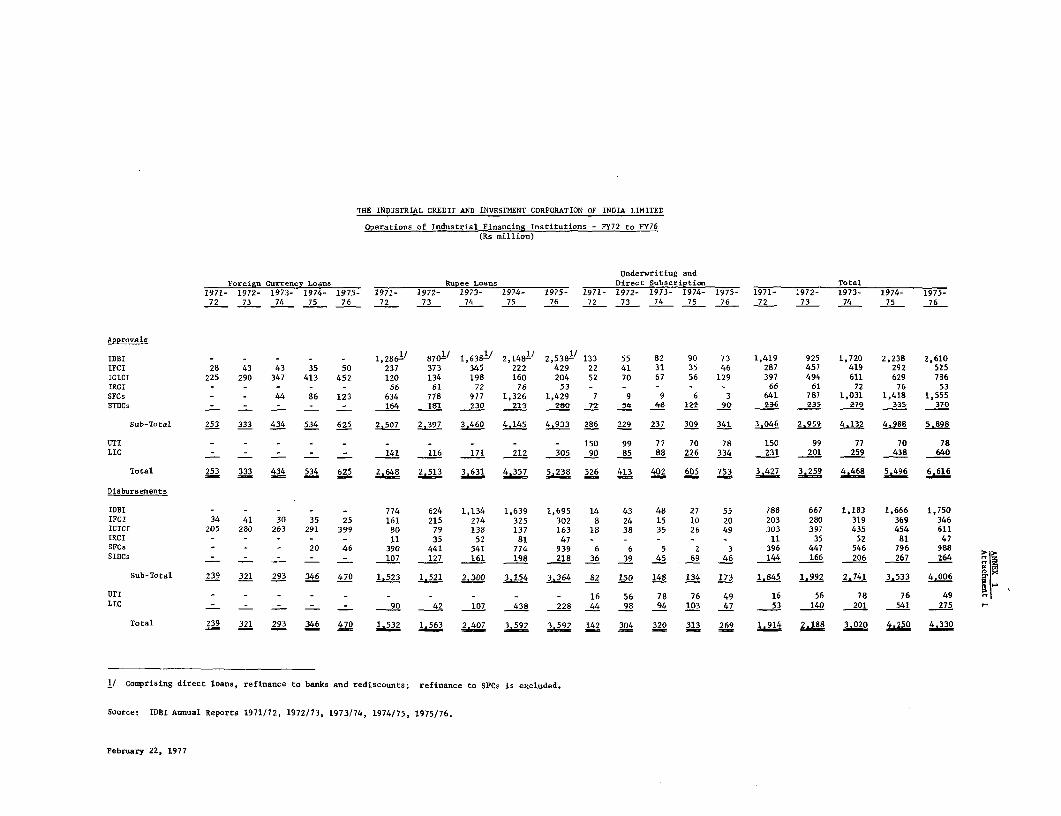

2.19 Financial Institutions. Annex 1 describes the institutional struc-ture for industrial financing in India. The system is well developed andthere are sufficient institutions to cover the different needs both at theState and at the all-India levels. During FY76, disbursements by the finan-cial institutions (excluding commetcial banks) accounted for about 15% ofgross fixed capital formation in industry. The Industrial Development Bankof India (IDBI), the apex institution for industrial financing in the country,accounted for 30% of the institutions' disbursements, followed by all theState Financial Corporations (SFCs) together (23%) and ICICI (14%). 1/ ICICI

1/ Total disbursements by all the institutions were Rs 4.3 billion. IDBIand the SFCs are associated with the World Bank Group through two linesof credit where IDBI refinances the foreign exchange lending operationsof the SFCs at the state level in the medium- and small-scale industry.

-7-

accounts for about three quarters of the institutional financing in foreignexchange. There is extensive joint financing among the financial institu-utions 1/ working at the all-India level and coordination is working well.One problem with the financial system has been the lack of equity capitalfor new entrepreneurs. In the medium- and large-scale sector, this is beingtackled through the institution of the joint sector where a private firm joinswith the State Government to implement a project. This "joint sector" is alsobeing used as a promotional tool by State Governments, as it offers the at-tractiveness of combining private sector management with Government resourcesand leverage in matters affecting licensing, availability of infrastructureand raw materials, etc. 2/. For small-scale industries, a "special capital"mechanism has been established to bridge the equity gap. 3/ Overall, w^Jhilemost of the State level institutions need strengthening, the financing systemis adequate.

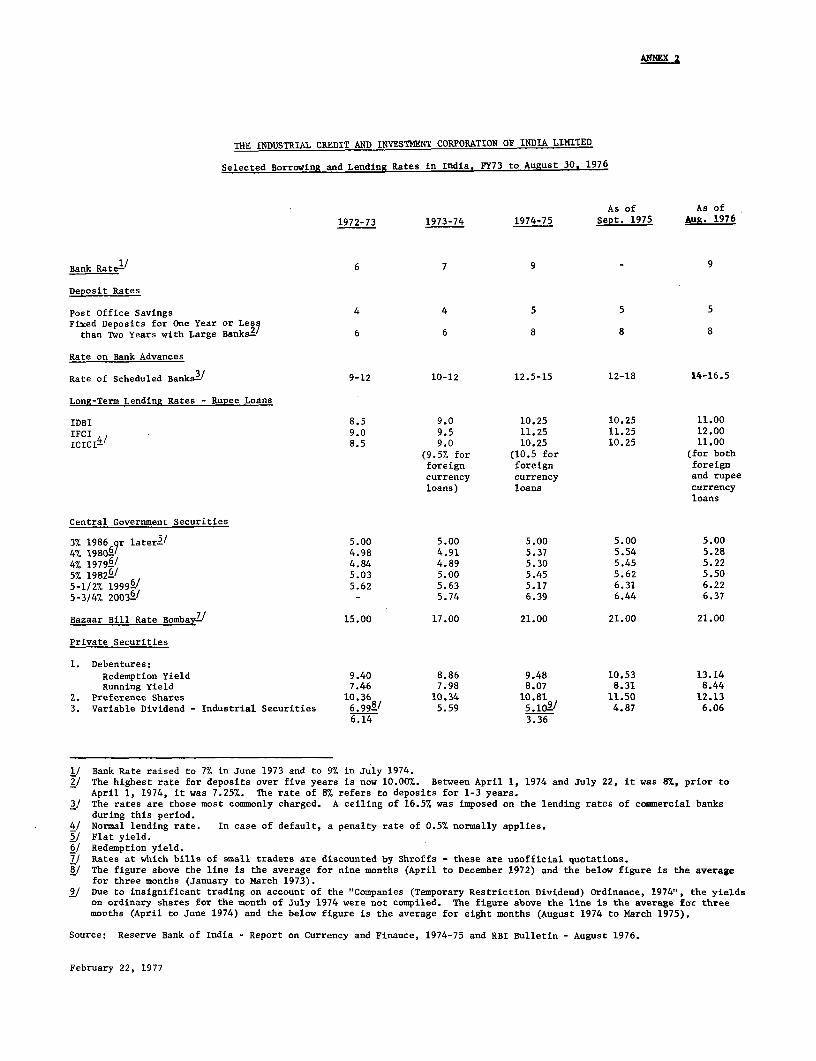

2.20 Interest Rates. The Central Bank rate was raised from 6% to 7% inJune 1973 and again to 9% in July 1974. The resources available to banks forlending were curtailed and the cost to banks of its borrowings and deposits,as well as the cost to borrowers of bank funds, was raised. Further, ceilingson credit expansion were imposed and commercial banks' liquidity ratios mademore stringent. Also, in July 1974, a tax of 7% on commercial bank interestincome was imposed, and is passed on to final borrowers. As shown in Annex 2,the rate of interest on fixed deposits is now 8% (1-3 years), and the maximumrate (for deposits of over 5 years) is 10%. Long-term lending rates byfinancial institutions range from 9.5%-12%. The commercial banks' primelending rate is now 15%, though most banks charge more (up to 16.5% includingabout 1% tax). ICICI's lending rates are in line with the country's ratestructure (para 3.11).

2.21 Capital Market. The capital market has been weak during the pastfew years. Total capital 4/ raised fell from Rs 902 million in FY73 to Rs 703million in FY74, and to Rs 613 million in FY75 although it increased to Rs 939million in FY76. The decline was mainly in the issue of debentures due tothe weak secondary markets; the capital raised as ordinary and preferenceshares (inclusive of rights issues) actually increased from Rs 569 million

1/ About half of ICICI's financing (by amount) during 1974 and 1975 wasjoint financed either with IDBI and the Industrial Finance Corporationof India (IFCI), or both.

2/ IBRD is considering a loan for financing this type of project throughIDBI which would include technical assistance for project identificationand preparation at the State level. ICICI also finances the jointsector (para 4.08).

3/ Refer to the appraisal report for the IDBI/SFCs II project (No. 1158-IN,of May 6, 1976; para 4.03).

4/ Including bonds but excluding bonus issues,

- 8 -

in FY73 to Rs 687 million in FY74, although it declined to Rs 423 million inFY75 and again increased to Rs 812 nkillion in FY76. RBI's price index forordinary shares increased from 103.1 at the end of FY73 to 125.5 at the endof FY74, but declined to 99.4 at the end of FY75 as a result of legislativerestrictions on the distribution of dividends. The index rose to 102.4 atthe end of FY76 and to 106.8 by August 1976 after the dividend restrictionswere lifted (para 2.14). However, the lapsing of the Dividend RestrictionsOrdinance did not have a substantial impact on the market because the highinterest rates make deposits with commercial banks quite attractive. Dataon capital issues for the first half of FY77 also reflect the slump in thestock market. The total capital raised between April to September 1976 wasRs 516 million compared with Rs 650 million in the corresponding period in1975.

2.22 The limited available data on underwriting reveals that in FY75, 90%of the total amount of equity issued to the public was underwritten; in FY74the corresponding figure was 97%. In FY75, underwriters, as part of theirobligation, had to take up equity shares for Rs 31 million compared with Rs 39million in FY74. During the early 1970s, brokers were active underwriters.Subsequently, with the slackening of activity in the capital market, brokerslost interest in this activity and the bulk of the underwriting is now beingdone by the financial institutions. The stock market should improve graduallyas the impact of the recent incentives by GOI (para 2.14) begins to be felt.

Prospects

2.23 After the improved economic performance in FY76, India startedFY77 with foreign exchange reserves equal to more than 4 months' imports,improved foodstocks, a growing export performance, and a substantiallybetter supply of energy and other inputs. These improvements do not rule outthe reappearance of supply shortages in the future as general prospects de-pend on uncontrollable factors such as the behavior of the monsoon, the per-formance of foreign economies, etc. Thus, the opportunities for growth aremuch better. The need remains for GOI to boost industrial exports, to con-tinue liberalizing imports, and to increase public investment because of itsdirect relationship to growth and because of the underutilization of capacityin the capital goods industries. Apart from the steps that GOI has taken toboost the investment climate, its budget for FY77 provides for a substantialincrease in investments and plan expenditures. 1/ Further, domestic savingsas a percentage of national income, which were around 13% during FY73-FY75,increased to 14.5% in FY76. All in all it is likely that over the next fewyears, India will be able to achieve real GDP growth of 4%-6% and exportgrowth of more than 7%.

1/ The overall Plan outlay (including states) for FY77 has been increasedby about Rs 19 billion or 32% on top of an increase of 25% in FY76.

-9-

III. INSTITUTIONAL ASPECTS

Share Capital and Ownership

3.01 ICICI's original paid-up capital was Rs 50 million and it has beengradually increased to Rs 150 million at present. Annex 3 shows ICICI'sprincipal shareholders as of October 31, 1976. With the latest capital inflowof Rs 25 million in 1975, the Indian public sector shareholding increased to76%, compared with 71% at the end of 1974. 1/ Foreign shareholding decreasedfrom 18% to 14% and the share of Indian private investors, from 11% to 10%.After an amendment to the Indian Company Act in February 1975, ICICI is nowconsidered a Government Company (its direct and indirect public sector share-holding is more than 50%). Except for a minor change in the procedure forselecting auditors (para 5.09), this has not had any impact on ICICI's opera-tions.

Organization and Staff

3.02 Board of Directors. ICICI's Board is competent and experienced.Of the 16 members, 4 have been appointed since 1975. The members representleading industrial groups (4), foreign shareholders (2), ICICI (3), publicfinancial institutions (3), GOI (2) and state level institutions (2) (Annex 4).Mr. H.T. Parekh continues to be ICICI's Board Chairman. The Board meets oncea month, with good attendance, and decides on all project proposals above Rs Imillion. 2/ It takes a keen interest in ICICI's affairs and is kept wellinformed.

3.03 Management. ICICI's management has not changed much over the lasttwo years and remains effective. Mr. Parekh, formerly Executive Chairman, hasnow delegated all executive power to the Managing Director although he con-tinues to be the Chairman of the Board. Mr. S.S. Mehta remains ManagingDirector and has responsibility for all operational aspects of ICICI. ICICI'smiddle management is also capable and experienced. The management style isflexible and informal.

3.04 Staff. As of June 30, 1976, ICICI's staff numbered 454 of whom187 were professionals, compared to 154 professionals as of June 1974. Mostof the new staff were assigned to support departments, such as accounts, legal,personnel and administration. The staff in the Projects Department, ProjectsPromotion Department, and Regional Offices also increased as envisioned ear-lier but they remain understaffed due to recent resignations/transfers inparticular the Project Promotion Department and the Regional Offices. ICICI's

1/ As in previous issues, a number of foreign shareholders either did notparticipate or sold their shares entirely.

2/ Smaller loans are decided by a committee headed by the Managing Director(up to a limit of Rs 10 million a month). Equity and debenture sales byICICI are decided upon by an Investment Committee headed by the Chairman.

10 -

recrui;rev program for the first half of 1977 should fill these gaps. l/For undt -A-ing the modernization program (paras 2.15-2.17). ICICI intends toexpand its staff gradually as necessary taking into account ICICI's absorptivecapacity and the need to maintain the high quality of its "normal" operations.

3.05 The quality of ICICI's staff remains high and its personnel andtraining policies continue to be sound. Staff morale is good and turnoverlow. Over 60% of the professionals have worked for ICICI for more than 5years.

3.06 Organization. ICICI's organizational structure (see attached chart)is sound. The Managing Director is the top executive assisted by the GeneralManager who concentrates on personnel, follow-up, accounts, legal and resourcemobilization, whereas the Deputy General Manager concentrates on projectevaluation and promotion, administration and the Regional Offices. Two newoperational units were established in 1976: an internal audit cell and aspecial operations cell. Apart from dealing with problem projects, the latteris also responsible for the sales from ICICI's investment portfolio under theguidance of the Investment Committee of the Board. Standard follow-up workhas also been reorganized (para 3.08). The role of the Regional Offices hasbecome more important, particularly in follow-up, legal work, appraisals ofloans below Rs I million, and "routine" project promotion. Moreover, a newRegional Office was recently established in Delhi. 2/ ICICI has employedmanagement consultants to help improve present data processing techniquesand to computerize the foreign exchange repayment schedules and other partsof its accounts. The new system should become operational by mid-1977.

Procedures and Standards

3.07 Appraisal. ICICI's appraisal standards continue to be of highquality. Appraisal reports remain precise and incisive. The analysis oftechnical, financial and market aspects is thorough and the economic analysisis adequate.

3.08 Follow-Up. ICICI's follow-up activities have been reorganized re-cently. Apart from the creation of a separate department in charge of problemprojects, the Follow-up Department has reorganized its activities into fourcells, i.e., implementation, rehabilitation, normal follow-up, and arrears.Further, the reporting responsibilities for follow-up between Regional Officesand headquarters have been defined more clearly. Coordination between ap-praisal and follow-up work remains good through weekly meetings to discussspecific projects under follow-up. The clients submit detailed quarterly

1/ ICICI intends to recruit four more professionals for the Project Depart-ment, two more for the Promotion Department, two more for the EconomicsDepartment and one for each of the three Regional Offices during thefirst half of 1977.

2/ ICICI has Regional Offices also in Calcutta and Madras. Over the pasttwo years the professional staff increased by 2 on a net basis in theCalcutta Office, by 1 net in the Madras Office, and by 6 net in thenewly-created Delhi Office.

- 11 -

progress reports which ICICI regularly reviews. Those companies which showpotential problems and those already on the problem list, are visited byICICI's staff at least once a year. ICICI also reserves the right to appointa director on the borrowers' board and has done so in 79 cases.

3.09 Procurement and Disbursement. ICICI insists upon competitive quota-tions from three or more reputed manufacturers/suppliers. The price and thesuitability of the equipment proposed to be purchased is subject to a carefulcheck by the staff, increasingly supplemented by comparisons on the basis ofexperience with similar projects. ICICI's procurement procedures are appro-priate given the nature of its business. Disbursement procedures also remainsatisfactory. Since November 1975, ICICI has opened its owfn letters of creditin order to provide speedier service to its clients.

Operating Policies

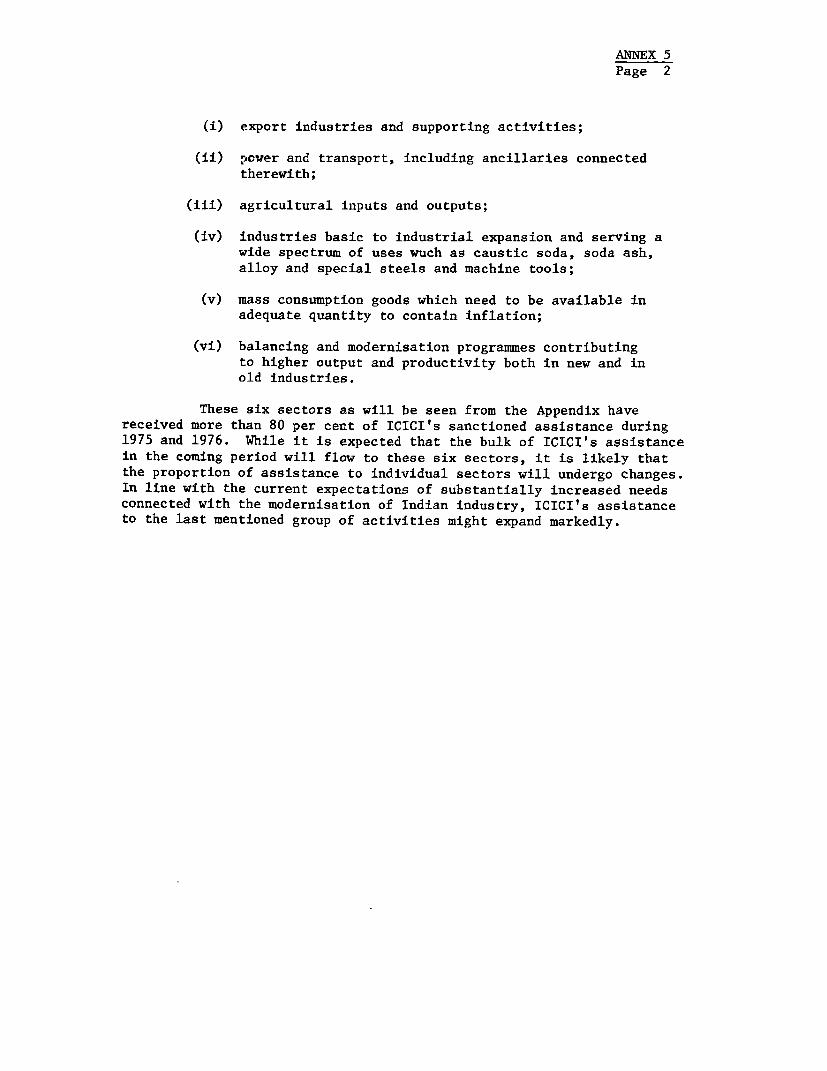

3.10 General. While ICICI has no formal policy statementD, its Memorandumof Association, complemented by Board resolutions adopted from time to timesand Government guidelines, provide satisfactory guidelines for ICICI0s activ-ities, which are satisfactory. 1/ ICICI's Board of Directors has approved astatement of financing strategy for the next two years (Annex 5) which showsthat it intends to continue to concentrate its investments in the followingsix priority sectors: (a) export industries; (b) power and transport; (c)agricultural inputs and outputs; (d) industries basic to industrial expansion;(e) mass consumption goods; and (f) balancing and modernization projects.About 80% of ICICI's lending by amount in 1975, and 88% in the first 10 monthsof 1976 as well as 82% of ICICI's pipeline of projects is in these sectors.

3.11 Terms of Assistance. Annex 6 shows ICICI's interest rates and othercharges as of October 1, 1976. ICICI's lending rates were last increased onDecember 1975. For ordinary loans, local currency rates were increased from10.25% to 11%, and foreign currency rates from 10.5% to 11%. 2/ For conces-sionary loans (backward areas), local currency rates were increased from 805%to 9.5%, and foreign currency rates from 9.5% to 10%. With inflation runningat a rate of 8% in FY77, ICICI is now lending at positive real rates ofinterest of 1.3%-2.8%, and with long-term inflation expected at around 8%-9%,its rates are expected to remain positive in real terms.

1/ For example, decisions on exposure in individual enterprises continueto be made on the merits of each case. As of June 30, 1976 ICICI hadan exposure of more than 10% (amount of approvals net of cancellationsand repayments as percent of ICICI's equity) in 17 companies with thelargest exposure amounting to 31%, which is still acceptable, consider-ing the quality of the companies. None of them is in financial dif-ficulties and all have satisfactorily serviced their debts to ICICIand others.

2/ ICICI also charges an additional interest rate of 1% to private limitedcompanies since it does not have the opportunity to enjoy equity parti-cipation.

- 12 -

Relations with Government and Business Community

3.12 Relations between GOI and ICICI continue to be good. ICICI's Re-gional Office in Delhi keeps close contact with GOI officials and GOI has tworepresentatives on ICICI's Board. ICICI is represented in 7 GOI Committees/Public Bodies concerned with industrial investment. ICICI enjoys full oper-ating autonomy within the framework of GOI policies.

3.13 ICICI's relations with other financial institutions remain good.Coordination between them is working well both at the all-India and Statelevel through Inter Institutional Meetings (IIMs) and Inter InstitutionalGroups (IIGs) respectively (Annex 1, para 7 to 11). ICICI works closelywith its clients and provides them various forms of assistance in projectpreparation and arrangement of technical and financial collaboration agree-ments with foreign partners.

IV. RESOURCES AND OPERATIONS

Resource Mobilization

4.01 General. As of September 30, 1976 ICICI's resources totalled Rs 5.1billion, of which foreign exchange accounted for Rs 2.8 billion (55%). ICICI'sresource position is summarized in Annex 7.

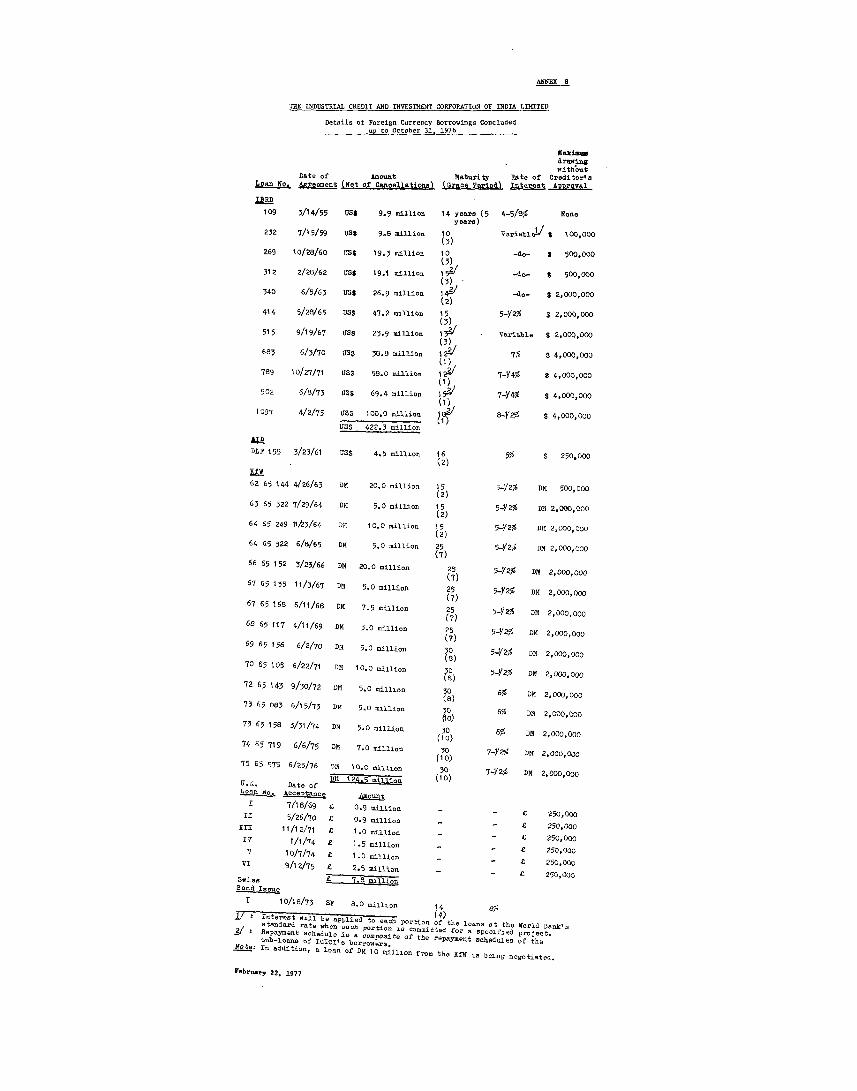

4.02 Foreign Currency. Most of ICICI's foreign currency resources(Annex 8) have come from IBRD. Of total foreign exchange resources of $492million as of October 31, 1976, eleven IBRD lines of credit account for $422million (85%). Fifteen KfW lines of credit (latest in 1976) account for 10%and six UK lines of credit (latest in 1975) for 3% of foreign currency re-sources; the rest (1%) was provided by one USAID line of credit (1961) and oneSwiss bond issue (1973). The latter was the first commercial diversificationof ICICI's sources of foreign exchange. ICICI has meanwhile continued to makeattempts to mobilize new foreign commercial funds, and is finalizing negotia-tions for a Kuwait Dinars 5 million ($17 million) loan from the Kuwait Invest-ment Company in mid 1977, at about 8.75% and repayable in lump sum after fiveyears. It also has been negotiating a $5 million loan with a foreign commer-cial bank. ICICI's plans for further diversification of its foreign exchangesources are satisfactory (para 6.04).

4.03 Blending. The Kuwaiti borrowing will be repayable in lump sumafter five years. Since most of ICICI's projects require longer maturities(maximum 15 years), this presents an operational problem for ICICI. For spe-cific subprojects financed from both IBRD and Kuwaiti funds, IBRD would allowICICI to allocate relatively more of the earlier maturities (years four andfive) for repayments to the Kuwait Investment Company. The size of theproposed loan offers ICICI the opportunity to blend effectively. From pastexperience, some 40% of an average ICICI subloan is repaid in the first fiveyears. Thus, to obtain a reflow of $17 million by the fifth year, ICICI wouldonly have to lend some $43 million (or $26 million in IBRD funds). Thus

- 13 -

the impact of the proposed blending operation on the repayment schedule byICICI to IBRD would be small. At the maximum, 1/ it would imply repayments toIBRD of $17 million over years 6-17 rather than in years 4-5. The proposedamortization schedule of 17 years, including 3 years grace normally and 5years grace in selected cases, would be within present IBRD guidelines on loanrepayment terms for India.

4.04 Foreign Exchange Risk on 1977 Kuwaiti Dinar Loan. ICICI would bor-row the Kuwaiti Dinars in a lump sum and would convert them into US dollarsand invest the dollars until disbursment. At commitment (loan signature)of these funds to subprojects, ICICI would pass on the exchange risk to sub-borrowers by denominating the sub-loan in Kuwaiti Dinars at the exchangerate which prevailed at the time when ICICI converted these funds into dol-lars. ICICI expected to commit these funds in an average period of about6 months, during which it would be taking some exchange risk. Since thealternative to bearing the risk might be more costly in view of: (i) the highcost of hedging (about 4%); and (ii) the past stable relationship between theUS dollar and the Kuwaiti Dinar coupled with the relatively short time ICICIwould be exposed in that currency (the exposure would reduce gradually overthe six month period) ICICI is prepared to accept the small exchange risk. 2/

4.05 Local Currency. The bulk of ICICI's total local resources of Rs 1.6billion as of September 30, 1976 was financed from ICICI's own bond issues(40%). The rest was financed from GOI and IDBI loans (37%) and share capitaland reserves (23%) (Annex 9). Prior to 1975, ICICI had difficulties in rais-ing rupee resources for its expanding rupee lending (para 4.07), because itsdebentures did not have trustee security status. GOI has meanwhile grantedthis status to ICICI debentures so that ICICI could issue rather large semi-annual bond issues totaling Rs 303 million in 1976, and Rs 193 million in1975 compared to Rs 55-80 million annual bond issues before. Though ICICI'seffort in helping develop the financial markets by floating these debenturesis laudable, little actual mobilization of primary savings is generated inthis process. ICICI, like other financial institutions is mostly tappingresources which have already been mobilized by commercial banks and otherinstitutions (primarily insurance companies). This is, however, the resultof traditional investment habits and the lack of secondary markets for deben-tures, which are major obstacles to attracting funds directly from the public.Also, RBI controls all debenture issues by determining amounts, maturity andrates of interest, thus limiting ICICI from making the yield on its debenturesmore attractive.

4.06 Mobilization at Project Level. ICICI's financing constitutes onaverage about 20% of total project cost. That means that for every rupeeinvested by ICICI an additional four rupees are invested from other sources.

1/ However, ICICI would actually select subprojects for blending on a caseby case basis giving preference to those requiring shorter maturities.Thus, repayments to IBRD would be delayed in only few cases.

2/ ICICI took a similar exchange risk at the time of its Swiss bond issue($2.1 million equivalent) in 1973.

14 -

Some 20% a. e~ financed by other financial institutions and the balance by thepromoters contribution and internal cash generation. ICICI also financesprojects jointly with foreign financial institutions, such as IFC, CDFC andDEG, thus serving as catalyst for iavestment.

Resource Allocation

4.07 Overall Operations. Characteristics of ICICI's operations and adiscussion of recent trends are in Annex 10. Reflecting the stagnating eco-nomic conditions in 1975 and the economic recovery in 1976, ICICI's total netapprovals fell slightly in 1975 to Rs 712.3 million as compared to Rs 722.6million in 1974, but picked up substantially in the first ten months of 1976when approvals were 18% higher (Rs B41.3 million) than in the twelve monthsof 1975. Commitments present a similar picture. They dropped slightly fromRs 585.0 million in 1974 to Rs 546.3 million in 1975, but increased sharplyto Rs 745.8 million in the first ten months of 1976. Disbursements, whichshow a time lag compared to approvals and commitments, fell from Rs 555.3million in 1974 to Rs 545.8 million in 1975 although they are estimated toreach Rs 655 million in 1976. ICICI's loan disbursements account for about15% of those of all-India financial institutions and about 2.5% of totalprivate industrial investment in India.

4.08 As a result of improved availability of domestic capital goods, rupeeloan approvals increased as a percentage of total approvals from 24% in 1974to 43% in the first ten months of 1976, as compared to 71% and 42% respectivelyfor foreign currency loans. The percent for guarantee, underwriting and directsubscription approvals varied from 5% to 15%. ICICI has continued to emphasizelending to the modern and non-traditional sectors such as chemicals/petrochem-icals (21%), metals and metal products (17%) and machinery manufacture (10%).Joint sector projects amounted for 13% from 1974 to 1976. Half of its loansare to new clients and some 7% of its loans to new entrepreneurs. 39% of itslending during 1975 and the first 10 months of 1976 was for projects in back-ward areas. The financial performance of ICICI clients improved from 16%return on total capital employed in 1973/74 to 18% in 1974/75.

Promotional Activity

4.09 ICICI's traditional promotional activity includes (i) training oflocal development bank staff from SFCs and SIDCs; (ii) participation in in-dustrial surveys conducted throughout India and assistance in implementationof project ideas; (iii) coordination and cooperation with both State and All-India institutions through Inter-Institutional Group meetings; 1/ and (iv)financing the preparation of feasibility studies and supporting technicalconsulting services (Annex 1, para 6). IDBI, as the apex financing institu-tion in the country, usually takes the lead in the above activity, and ICICI'spromotional contribution is more significant in non-traditional activities.

1/ Annex 1, para 11 discusses the functions of the IIG. ICICI has lead res-ponsibility for initiating promotional activities through the IIGs inAndhra Pradesh, Gujarat, Karnataka, Maharashtra and Tamil Nadu.

- 15

4.10 ICICI's new promotional activity can be classified irnto: (i) iden-tification of projects that would fill gaps in the industrial sector; (ii)support to the financial system; and (iii) preparation of sectoral/policystudies. ICICI's project gap identification activity started in late 1973with the creation of the Project Promotion Department. One of the projectideas (an industrial estate for small-industry in West Bengal) has alreadybeen financed and two others (sand beneficiation and sponge iron) are underconsideration. A fourth project (methyl chlorosilane) has met with dif-ficulties in completing collaboration arrangements. Seven other projectsare under active preparation of identification. The performance of the Pro-motion Department has been good but it needs to be allocated more staff (para3.04).

4.11 ICICI's recent support to the financial system has been mainly byits merchant banking activities which started in 1973. Through these activ-ities, ICICI provides financial services and advice to companies for raisingcapital (Annex 10, para 7). More recently, ICICI has prepared a feasiblitystudy for the creation of a specialized institution to finance lower andmiddle income housing. Its creation is under discussion with GOI. ICICIexpects to provide 5% of the initial Rs 100 million share cap4 tal and isseeking participation by IFC.

4.12 ICICI involvement in the preparation of sector/policy studies wasinitiated under the eleventh IBRD loan, when ICICI undertook to prepare astudy on the problems and prospects of manufactured exports based on a sampleof its clients. The study, which is summarized in Annex 11, provides a con-siderable amount of useful information and is unique in its attempt to analyzeissues related to exports at the firm level. ICICI intends to review existingcompany data from the export study to test certain hypotheses for a penetra.tion pricing study, in particular the determination of the factors responsiblefor the observed increase over time in the ratio of export to domestic prices.Knowledge of the underlying causes for low initial export prices might permitimproved understanding of the efficiency of different export marketing strat-egies. This first stage of study would be completed by September 30, 1977.Provided the first stage shows sufficient evidence that penetration pricingexists, ICICI would agree with IBRD on an outline for the second stage ofthis study, and would assess work to be done, including possibly an analysisof prices and quality of product in third countries for comparison.

4.13 ICICI will also undertake a study on selected subsectors of theengineering industry at the company level to analyze the factors affectinginvestment demand in particular for modernization and replacement. The studywould, among others, focus on (i) demand prospects both in the domestic andexport markets; (ii) upgrading of technology; (iii) domestic subcontractingarrangements to ancillaries; and (iv) the overall employment impact of alter-native investment strategies. The study would initially concentrate on theautomobile industrial subsector, and a first draft questionnaire is scheduledto be ready by July 15, 1977 and to be sent to IBRD for comments. A draftreport would be ready by March 1978. The content and timing of the study foranother subsector would be determined subsequently. An outline of the studyis in Annex 12.

- 16 -

Development Impact 1/

4.14 In 1975, ICICI calculated ex ante economic rates of return (ERR)on on 30 projects 2/ (Annex 13) which ranged from 11.0% to 70.0%. Theweighted 3/ average economic rate of return was 22.6% while the weightedaverage financial rate of return (FRR) was 14.8% which is satisfactory. Sim-ilarly, for six months of 1976, ex ante ERR calculations on 17 projects rangedfrom 9.0% to 40.0% with a weighted average ERR of 29.5% and FRR of 15.6%. Theaverage fixed investment per employee was $16,000 in the case of 108 projectsapproved in 1975 which is satisfactory considering the fact that ICICI financesthe medium and large scale sector. Further, to promote regional development,ICICI has increased its lending to backward areas from 12% of total approvals(1955 to 1970) to around 40% (1974 to 1976). Finally, from FY74 to FY75, thetotal exports of ICICI's clients increased by 56% from $230 million to $355million, or from 15% to 17% of India's total industrial exports (Annex12). 4/

V. FINANCIAL ASPECTS

Quality of Portfolio

5.01 Loans. Annex 14 shows the trend in ICICI's arrears for 1965 to1976. As of September 30, 1976, ICICI's overdues of principal and interestwere Rs 98 million, (but dropped slightly to Rs 94 million as of December 31,1976), compared with Rs 60 million as of December 1975, Rs 51 million as ofDecember 1974, and Rs 41 million as of December 1973. The total principaloutstanding of loans affected by arrears was Rs 455 million, or about 18% ofthe outstanding loan portfolio, compared with 7% in 1973. The increase inarrears was due mainly to the special problems faced by Indian industry since1972; power cuts in 1973; credit restrictions in 1974; and in particular,business recession in 1975. From past experience, it takes some time after

1/ ICICI's developmental impact which included ex post analysis on the proj-ects it has financed was examined in a Special Study undertaken in 1973jointly by the Bank and ICICI, the results of which were incorporated inthe appraisal report of the eleventh loan to ICICI (Report No. 637a-INdated March 14, 1975). One of the major conclusions of this study wasthat ex post economic and financial rates of return have generally beensimilar to those calculated ex ante.

2/ As agreed with IBRD under previous loans, ICICI calculates the ERR forall new and expansion projects when its proposed assistance is morethan Rs 5 million and total capital cost is more than Rs 25 million.

3/ Weighted according to capital costs at market prices.

4/ This relates to 374 companies for which information was available.

- 17 -

the start of business revival for firms showing liquidity problems during arecessionary phase to normalize operations. Thus, the arrears problem is notlikely to start improving substantially until around mid-1977.

5.02 Annex 15 shows the characteristics of ICICI's arrears as ofSeptember 30, 1976. Compared with the position in 1974, two sub-sectors,metals and metal products, and electrical equipment, account for a majorportion of the increase in arrears (40% and 33%, respectively). As a per-centage of the total portfolio affected by arrears, they account for 19% and18% respectively. The performance of both sub-sectors was considerably in-fluenced by past developments including power cuts and recession (parti-cularly the recession in the construction industry for metal products), andit should improve gradually. Further, ICICI has proposed to GOI a reductionin excise duties for some of the products and in the case of electricals,(dry cells), a review of export incentives. Other subsectors which account fora major portion of the increase in arrears such as chemicals/petro-chemicals(15%), 1/ are also those that were particularly affected by recession andincreases in excise duties.

5.03 ICICI's arrears list now covers 120 companies (out of over 1,000),of which some 30 are facing long-term management, marketing or environmentalproblems. The rest comprise certain new companies passing through initialteething difficulties, market entry, or others whose cash flows have beenaffected in various degrees by recession. ICICI and its auditors have re-viewed each project in ICICI's portfolio, and based on security considera-tions as well as long-term viability, concluded that provisions are suffi-cient to cover possible losses. 2/ Further, ICICI is now undertaking a majoreffort to improve arrears. It has reorganized its normal follow-up work and

1/ Chemicals and petrochemicals account for 18% of the portfolio affectedby arrears.

2/ Provisions for loans (principal) amount to Rs 27 million or about 1% ofthe outstanding loan portfolio in 1975. This compares favorably withan actual write off of bad debts amounting to Rs 4 million over thepast five years. Only one of ICICI's clients is among the "sick units"that have resorted to IRCI for assistance. Provisions are likely toincrease after the audit for the 1976 financial year is completed.These reserves against doubtful debts provide for possible losses onprincipal repayments; they are not passed through the revenue/expenseaccounts but allocated directly in the balance sheets as reserves.Prior to 1973, doubtful interest income was included in the revenueaccounts and a provision was made as an expense against their recovery.For the 1973 to 1975 accounts this doubtful interest income is notaccrued as income, but added directly to current assets in the balancesheets against a current liability account called "interest in suspense".This "interest in suspense" procedure has been adopted to avoid paymentof tax on income that might not be realized (provisions are not deduc-tible in India).

18 -

created a .,-arate cell to concentrate on difficult projects (paras 3.06,3.08), Inri idual accounts continue to be watched closely and loans arerescheduledl, where appropriate. ICICI in many cases has assisted clientsin obtaining working capital finance, and has also taken up policy problemswith GOI. ICICI has also imposed changes in some projects, for example,new management. 1/ From a discussion on the problems of some 40 of ICICI'smost difficult projects, it seems clear that ICICI is taking satisfactoryaction. ICICI is in control of the situation and no major divergence fromits present approach is recommended.

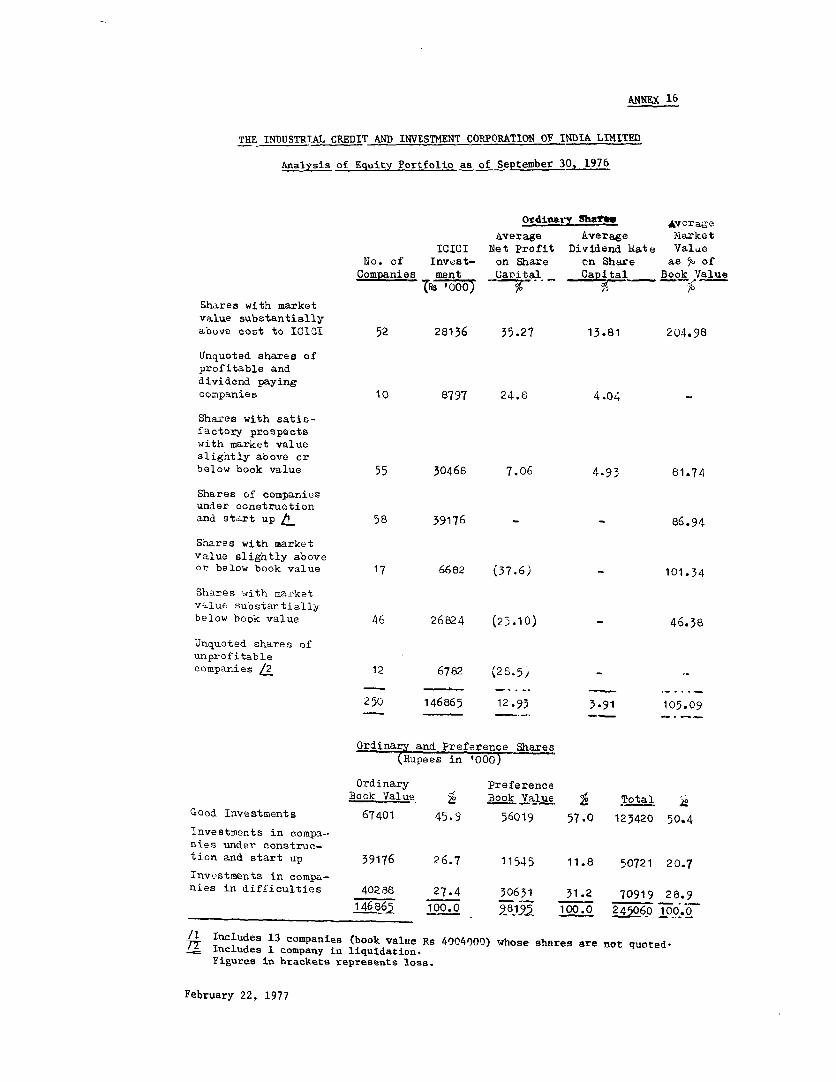

5.04 Investments. As of September 30, 1976 ICICI's equity portfoliocomprised common share investments of Rs 146.9 million in 250 companies andpreference shares of Rs 91.8 million in 67 companies. Some 50% of the equityportfolio was in companies operating profitably and paying dividends, 21%in companies under construction or start-up and 29% in companies in difficul-ties, of which about 2% was in some jeopardy (Annex 16). 2/ The averagemarket price of the common shares was 105% above book value, substantiallylower than the 132% on June 30, 1974, reflecting the trends in the stockmarket (para 2.22). The average dividend yield was about 4.4% in 1976, al-though taking into account also capital gains after tax the average yieldwas 6.4% which is satisfactory. As of December 31, 1975, ICICI also helddebentures of Rs 150.3 million in 67 companies. In 1975, the average yieldon debentures was 7.7%. ICICI's investment portfolio continues to be sound,and is well managed.

Financial Position

5.05 Profitability. Annex 17 shows income statements from 1971 toSeptember 1976. Net profits after tax increased from Rs 25.0 million in 1973to Rs 26.6 million in 1974, Rs 35.0 million in 1975 and are estimated atRs 35.2 million in 1976. The relatively sharp increase in 1975 was mainlydue to tax concessions, including the reversion of excess provisions forincome tax and surtax to income. 3/ ICICI's net profit as percent of averageequity stayed over the four years at about 11%, a satisfactory level. ICICIincreased dividend payments in 1975 to 11% as compared to 10% in the pre-vious years, partly to show a good dividend record for its next capital issuewhich is expected in 1977. Such dividends allowed for a satisfactory profit

1/ Only 2 cases were pending in the courts as of October 1976. ICICI'swillful defaulters are very few.

2/ ICICI makes no specific provisions for its equity investments, but thenet capital gains realized from the sale of investments is earmarkedto a capital reserve fund which was Rs 38 million as of October 1976.This is an adequate cushion.

3/ Profits before tax increased from Rs 51 million to Rs 52 million, Rs 56million and Rs 65.3 million respectively.

- 19 -

plough-back of 53%. Administrative expenses remained under control at 0O5[-0.6% of average total assets. However, because the average cost of bor-ow--ings increased faster than the return on loans (partly due also to increasedlending in backward areas at concessional rates), the spread on lending oper-ations declined from 2.8% in 1973-74 to 2.5% in 1975-76. As a result, pzofitafter tax and provisions declined from 1.3% of an average total assets in1973 to 1.1% in 19760 Profitability, although relatively lo0, 4is sti-il ade-quate, and the declining trend is expected to be reversed by 1978 (para 6.07footnote).

5.06 Capital Structure, Annex 18 shows ICICI"s balance shees s as ofDecember 31, 1971-1975, and September 30, 19760 Total assets almost doubledfrom Rs 1.8 billion in 1972 to Rs 3,0 billion in 1975 and Rs 3.4 billion in1976, There was a particularly Large increase (30%) in 1975 mailn7y becauseof a 40% increase in foreign currency loans outstanding. Thls, however, isnot due to particularly large disbursements, but rather, the result of adifferent method of converting the foreign currencies in rupee equivalent. 1/As of December 1975, net worth plus provisions constituted 1-% of the loanand investment portfolio. Foreign currency loans accounted for 59% and rupeeloans for 30% of total assets while IBRD borrowings were 48% of ICICII's equityand liabilities. The debt/equity ratio was 8.6:1 as of September 30, 1976,below the 9:1 contractual limit, which will be maintained since ICICI isalready a highly leveraged company.

5.07 Liquidity. Annex 19 shows ICICI's cash flow statements for 1971through 1975 and the first nine months of 1976. ICICI's liquidity has re-mained adequate with a debt service coverage at about 1,2:1 exceot for 1975when it fell to 1.03:1 due to a lump sum repayment of a Rs 60 million bond.It is estimated at 1.13:1 for 1976 (1,05:1 assuming pro-rata allocations onbonds outstanding which have not yet fallen due). This is the minimum accept-able level. The debt service coverage should increase further as the arrearssituation begins to improve (para 6.11).

5.08 Market Quotation. ICICI's net worth as of December 1975 Was Rs 277million, so that the book value of each of its 1,5 million shares was Rs 185compared to Rs 100 par value. From January to October 1976, the market priceranged from Rs 95 to Rs 101 per share, or about 51% to 55% of the book value.During this period only 5% of the shares were traded. At the closing priceof Rs 93 in December 1975, ICICI's dividend yield was 11.8% and the price/earnings ratio was about 4.0:1. The relatively low share price reflects thepoor stock market conditions.

5.09 Audit. Because ICICI is now considered a Government Company (para3.01), GOI, on the advice of the Comptroller Auditor-General, can appoint theauditors of ICICI. However, N.M. Raiji & Co. and Ray & Ray continued to auditICICI's accounts for 1975 which were presented without qualification0 For

1/ Before 1975, ICICI converted its foreign currency loans and borrowingsinto rupees at the central exchange rate at the time of disbursement.Now ICICI uses the current exchange rate, which results in substantiallylarger loans and borrowings in rupee equivalent as most foreign curren-cies had substantially appreciated against the rupee over the past years.

- 20 -

1976, a new auditor, Lodha Co., replaced Ray & Ray. GOI follows the practiceof appointing new auditors about every three years and for reasons of con-tinuity N.M. Raiji & Co. continues as ICICI's auditor for the time being.

VI. PROSPECTS

GOI Policy on Import Licensing and Foreign Exchange Allocation

6.01 Recent dramatic improvements in India's foreign exchange positionshould permit GOI to pursue an increasingly expansionary macro-economicpolicy. If adopted, this would also increase the demand for private invest-ment and lead to an increased demand for loans from the industrial financialinstitutions. At the same time, GOI is likely to increase the allocationof free foreign exchange for industrial purposes. In this situation, somefirms may prefer to use rupees, either their own or borrowed, and convertthem into foreign exchange loans. The foreign exchange financing require-ments for ICICI over the next two years have been conservatively assessedin recognition of some possible preference for rupee loans.

Business Forecast

6.02 Annex 20 shows the forecast of ICICI's approvals, commitments anddisbursements through 1980. Total approvals, which were about Rs 950 mil-lion in 1976, are projected to increase annually by 10% in nominal terms toRs 1.4 billion by 1980. Total approvals would be equally divided betweenforeign currency loans and rupee loans and investments. Thus, the trendtowards an increasing proportion of local currency financing 1/ is expectedto continue as the Indian capital goods industry develops further. Commit-ments and disbursements of foreign currency loans would grow annually at 10%and 12%, respectively, although for local currency the growth will be fasteras the backlog of uncommitted approvals is larger. 2/ ICICI's pipeline ofprojects, particularly for foreign exchange financing, mainly includes in-dustries of high priority. 3/ Further, ICICI's proven capability foridentifying and appraising economically viable projects is evidence that itwill continue to allocate IBRD funds efficiently under the new loan. Giventhe improved economic conditions, it is likely that investment activity willbe at least maintained, and ICICI's projections have been prepared on thatbasis.

1/ Local currency approvals accounted for 46% during 1974-1976.

2/ There was a large increase in rupee approvals during 1976.

3/ Refer to para 3 of Annex 5 (Strategy Statement). It should be borne inmind that the pipeline is only indicative of the projects to be financedin the future, as most of the projects in it are yet to be appraised andICICI will undertake further project identification and promotion in thecourse of the proposed loan.

- 21 -

6.03 The above forecasts do not take into account the impact of themodernization program (paras 2.15-2.18) since at the time of negotiationsmany details had not been worked out and the level of demand for the schemewas not clear. The modernization scheme should not affect the forecast offoreign currency operations since of the five industries covered, onlyengineering would require some imported equipment, roughly estimated at10% of disbursements for the sector. 1/ However, it may affect the projec-tion of rupee operations in terms of amounts (these would probably increase)and also in terms of the nature of the financing (some balancing and modern-ization proposals which ICICI would have financed under its normal operationswill now come under the subsidized scheme). Regarding the impact of the mod-ernization program on ICICI's financial position, as ICICI will be appraisingthe projects to be financed and will have the power to accept or rejectproposals, it will only get involved with operations it considers viable.Further, any additional funds required for the program will be provided byGOI/IDBI so that ICICI's resource position will not be affected. However,there may be an impact on ICICI's capital structure (para 6.10) and ICICI'sprofitability (para 6.08).

Resource Requirements

6.04 Foreign. The proposed loan would cover the gaps in ICICI's foreigncurrency resource requirements between September 1977 (the time when the loanwould become effective) and September 1979. Annex 21 shows ICICI's projectedforeign currency resource position through 1980. From January 1977 throughSeptember 1979 foreign currency commitments would be about $174 million.Against this, ICICI had foreign currency resources available for commitmentof about $40 million on December 31, 1976 and expects to raise throughSeptember 1979, some $30 million from traditional sources (about $4 millionper year from KfW and $6 million per year from UK). It expects to obtain$17 million from the Kuwait Investment Company during 1977 and further com-mercial borrowings of $5 million in 1978 (para 4.02). 2/ This leaves a gapof about $82 million which forms the basis for the proposed $80 million IBRDloan. It would account for about 60% of ICICI's foreign currency commitmentsbetween September 1977 and September 1979. For 1979 and 1980, ICICI also plansto obtain an additional $30 million from non-traditional sources.

6.05 The loan would be made to ICICI to meet the foreign cost of capitalgoods and services of subprojects sponsored by productive enterprises. Aswith other IBRD loans to development finance companies, eligible enterpriseswould be broadly defined so as to include not only manufacturing, but also

1/ Or about $5 million assuming half of GOI's targets for the next 3 yearsare achieved. Further, engineering units eligible for the program (thoseover 15 years old) are mostly additional to ICICI's normal clientele inthis sector (the most modern firms). Moreover, it is not clear whetherimported equipment would be included under the subsidized scheme.

2/ This excludes the modernization programs as any funds required for thispurpose will be provided separately by GOI/IDBI.

- 22 -

no;- only manufLcturing, but also agro-iadustries, mining, and transportation.The loan is expected to finance mainly private enterprises, although projectsin the public and joint sector would also be eligible. It is proposed thatthe free limit be kept as in the past four loans, at $4 million (with noaggregate).

6.06 Domestic. Annex 21 shows ICICI's rupee resource position through1980. 1/ From 1977 to 1980, disbursements for local currency loans and in-vestments are expected to be Rs 2,015 million. The total rupee requirements,Rs 2,308 million, would be funded by borrowings, mainly debenture issues(57%), loan collections (25%), internal cash generation (5%), share capitalincreases (4%), IDBI counterpart funds from the UK credits (4%), and salesfrom portfolio (3%). The balance of 2% is expected to be financed fromICICI's resources on hand from previous borrowings. ICICI should be ableto raise the required resources as it no longer faces problems placing itsdebenture issues (para 4.05).

Financial Projections

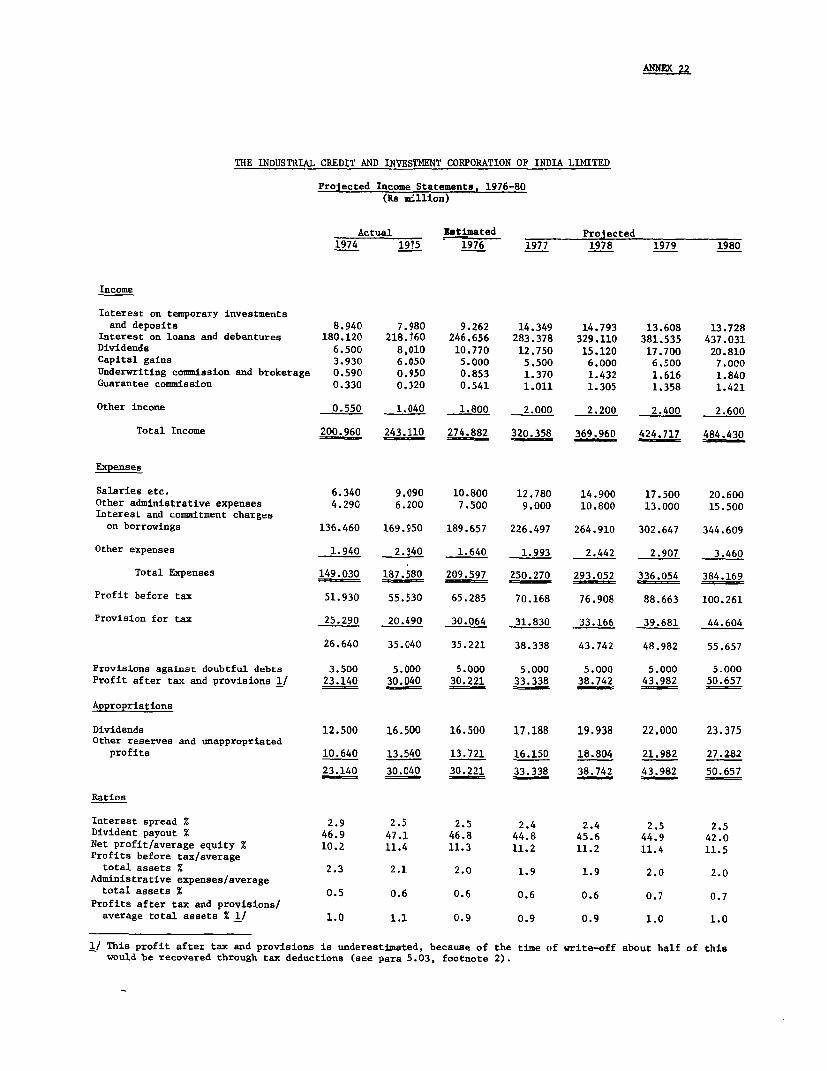

6.07 Annex 22 shows projected income statements for 1976 to 1980. Netprofit after tax and provisions should grow from Rs 30.2 million in 1976 toRs 50.7 million in 1980, or by about 12% per year. The return on average networth would remain at around 11% (due to share capital increases). Profitafter tax and provisions would stay at about 1% on average total assets whichis relatively low but still adequate. 2 Administrative expenses would riserather rapidly by about 18% annually in view of ICICI's increased promotionalactivities, but should remain under control at 0.6%-0.7% of average totalassets. The projected annual dividend rate is 11% implying a satisfactorypayout ratio of about 45%.

6.08 At the margin, ICICI's lending spread now is 2% for foreign cur-rency loans and about 3.5% for rupee loans. To prevent a further declinein profitability IBRD and ICICI reached an understanding that ICICI wouldreview its lending rates periodically and adjust them if necessary taking intoaccount the need to maintain its profitability, inflationary conditions, andother factors. On the basis of existing spreads for foreign and rupee loansand assuming the modernization funds are lent with a spread of about 2% on theaverage with half the modernization program being implemented, ICICI's averagespread at the margin would be 2.5% which is satisfactory.

1/ This excludes the modernization ptograms as any funds required for thispurpose will be provided separately by GOI/IDBI.

2/ The declining trend in ICICI's profitability (para 5.05) is expected tobe stopped around 1978 as the impact of the lending rate increases of1974 and 1975 becomes felt. The average spread on lending operationsis expected to remain at around 2.5% over the projected period, whichis satisfactory.

- 23 -