report no. 168194 - documents & reports - all … eqiivalents currncy unit = yuan (y)= 100 fe...

TRANSCRIPT

ES~ESMAPGo 6II Wmsr*T

_NW Ifin qi~'c St Manement Assistance Prgramme

at /qq4t

ChinaEnergy Efficiency and Pollution Control In

Township and Village Enterprices (TVE)Industry

Report No. 168194

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

4

JOINT UNDP / WORLD BANKENERG'C SECTOR MANAGEMENT ASSISTANCE PROGRAMME (ESMAP)

PURPOSE

The Joint UNDP/World Bank Energy Sector Management Assistance Programme (ESMAP) waslaunched in 1983 to complement the Energy Assessment Programme, established three years earlier.ESMAP's original purpose was to implement key recommendations of the Energy Assessmentreports and ensure that proposed investments in the energy sector represented the most efficient useof scarce domestic and external resources. In 1990, an international Commission addressedESMAP's role for the 1990s and, noting the vital role of adequate and affordable energy ineconomic growth, concluded that the Programme should intensify its efforts to assist developingcountries to manage their energy sectors more effectively. The Commission also recommended thatESMAP concentrate on making long-term efforts in a smaller number of countries. TheCommission's report was endorsed at ESMAP's November 1990 Annual Meeting and prompted anextensive reorganization and reorientation of the Programme. Today, ESMAP is conducting EnergyAssessments, performiuig preinvestment and prefeasibility work, and providing institutional andpolicy advice in selected developing countries. Through these efforts, ESMAP aims to assistgovernments, donors, and potential investors in identifying, funding, and implementing economicallyand environmentally sound energy strategies.

GO VERIVAANCE AND OPERATIONS

ESMAP is governed by a Consultative Group (ESMAP CG), composed of representatives of theUNDP and World Bank, the governments and institutions providing fimancial support, andrepresentatives of the recipients of ESMAP's assistance. The ESMAP CG is chaired by the WorldBank's Vice President, Finance and Private Sector Development, and advised by a TechnicalAdvisory Group (TAG) of independent energy experts that reviews the Programme's strategicagenda, its work program, and other issues. ESMAP is staffed by a cadre of engineers, energyplanners and economists from the Industry and Energy Departnent of the World Bank. TheDirector of this Department is also the Manager of ESMAP, responsible for administering theProgramme.

FUNDING

ESMAP is . cooperative effort supported by the World Bank, UNDP and other United Nationsagencies, the European Community, Organization of American States (OAS), Latin AmericanEnergy Organization (OLADE), and countries including Australia, Belgium, Canada, Denmark,Germany, Finland, France, Iceland, Ireland, Italy, Japan, the Netherlands, New Zealand, Norway,Portugal, Sweden, Switzerland, the United Kingdom, and the United States.

PURTHER INFORMATION

For further information or copies of completed ESMAP reports, contact:

ESMAPc/o Industry and Energy Department

The World Bank1818 H Street N.W.

Washington, D.C. 20433U.S.A.

China

Energy Efficien.y and Pollution Control in Townshipand Village Enterprises (TVE) Industry

December 1994

Results of a Joint Study by ESMAP and theChina Ministry ofAgriculture 's Department of Energy and

Environmental Protection, the Department of Township Enterprises,and the State Planning Commission's Energy Research Institute.

Power Development, Efficiencyand Household Fuels DivisionIndustry and Energy DepartmentThe World Bank1818 H Street N.W.Washington, D.C. 20433

This document has restricted distribution and may be used by recLpients onlyin the petfonnance of their official duties. Its contents may not oth.wisebe d rlosed wihout tNDP or World Bank authicontan.

ABBREVIATIONS AND ACRONYMS

ABC Agricuktural Bank of ChinaBAU Business as usualCO2 Carbon dioxideGDP Gross domestic productESMAP Energy Sectr Maagement Assistance ProgrammeFYP Five-Year PlanGEF Global Environment FacilityIRkR innal rte of retrnKgce Kilogram of coal equivalentkW KilowattkWh Kilowatt hourMOA Ministry of AgiculteMTCE Million tons of coal equivalentNEPA National Environmental Protction AgencySOE State-owned enterpriseSO2 Sulphur dioxideTCE Tons of coal equivalentTVCE Township and village collective enterpriseWVE Township and village enterpisetpa tons per annumIpy tonsperyear

CURRENCY EQIIVALENTS

Currncy Unit = Yuan (Y)= 100 fe

1US$ = Y 4.7 (1990)lUS$ =Y S.5 (1992)1US$ =Y 8.7 (1994)

FISCAL YEAR

January 1 - Decemnber 31

WEIGHTS AND MEASURES

bDlmon = 1,000 nilokWh (of electricity) = 0.1229 kgce (heating value)

= 0.392 kgce (themal replacment value in 1990)muI = 1/l5 hectare

= 2,000/3 m2TCE = 7 million kilocaloriesTOE = 1.4 tceTWh = 1 bilion kWhton of coal = 0.7143 toe on avemeton of crude oil = 1.43 tce

TABLE OF CONTENTS

PREFACEEXECUITIV SUIvMARY ................. i

I. OVERVIEW 1.

Role of Township Enterprises in the National Economy .Key Chamaeteristics of TVEs .TVE hie ... 2Energy TUitization .3Environmental Issues .4Objectives and Methodology of the Study ............................ , . 5Key TVE Industries Selected for the Study .6

IL. INDUSTRY PROFILES .7

A. The Brick Industry .7Introduction .7Technologies Currently Used .8Technical Improvements .9Size and Scale Factors . 1Environmental Factors .12

B. TheCokeIndustry .12Introduction .12Technologies Currently Used .13Technical Improvements .1Size and Scale Factors .16

C. Metal Castings Industry .17Introduction .17Technologies currently used .18Technical Improvements .19Size and Scale Factors .20Environmental Factors .20

m. CASE STUDIES OF INVESTMENT OPTIONS .22

A. The Brick Industry .22Specific Investment Cases .22Results of Case Studies .24Energy and Pollution Impacts .26

B. The Coke Industry .26Specific Investnent Cases .26Case A Data and Assumptions .27Case B Data and Assumptions .27Case C Data and Assumptions .27Results of Case Study .28Energy and Pollution Impacts .29

C. The Metal Castings Indusy ....................................... . 29Specific Investnent Cases ....................................... 29Results of Case Studies ....................................... 31Energy and Pollution Impacts ....................................... 3 1

Net Costs of Energy Savings and Carbon Dioxide Abatement ...................................... 32Summary ............................... 33

IV. CONCLUSION4S AND RECO0MMENDATIONS .34Introduction .34Directions gor Technical Improvements . 34

Brickmaking .35Metal Casing .36Cokemaking .37

Policy Implications .37Recommendations .39

REFERENCES ............................................. 41

ANNEXESAnnex A Accelerated Investment Scenarios ............................................. 42Annex I. Output Shares under Accelerated Scenarios ............................................. 53Annex II. Cash Flow and Sensitivity Tables ............................................. 55Annex Im. Energy Consumption of Metl casting Industry .......................................... 78Annex IV. Brick Industry: Additional Information ............................................. 80Annex V. Metal castings Industry: Intenational Comparisons .................................... 82

Preface

This report is one of the outputs of a technical assistance activity to China by theUNDP/World Bank Energy Sector Management Assistance Program (ESMAP). Part of thefinancing for the activity was provided by the UNDP Project e:. Greenhouse Gas Emissionsexecuted by the World Bank, into which results of the study was provided as inI;4L The studywas conducted jointly by a World Bank/ESMAP team and a Chinese team consisting of staff ofthe Ministry of Agriculture's Department of Energy and Environmental Protection and theDepartment of Township Enterprises, the State Planning Commissior's Energy ResearchInstitute and several local experts. Four reports were prepared by the Chinese teatn during thecourse of the study. In addition, short technical papers on the subject industries werecommissioned with the Energy Technology Support Unit (ETSU) and the Coal ResearchEstablishment, both of the United Kingdom. Thesr materials were used as bases for writing theoverall report.

The ESMAP team consisted of Ernesto N. Terrado, Principal Energy Planner (TaskManager), Barry Tunnah, Energy Conservation Specialist (Consultant) and Peter Johanssen,Industrial Policy Analyst (Consultant). The Chinese team was led by Mme. Deng Keyun and Mr.Zhang Lujiang of the Ministry of Agriculture. The valuable assistance of the local team as wellas by officials in the cities of Chengdu, Jiexiu and Tianjin are gratefully acknowledged. Researchassistance at the World Bank was provided by Zhang Zhihong. Donald Hertzmark (Consultant)assisted in the economic and financial analyses. The final report was writen by Emesto Terradoand Barry Tmnnah. Robert Taylor, Todd Johnson and Kurt Schenk reviewed the drafts andprovided valuable suggestions.

ExecuiveSummary

Overview: Role of Township Enterprises in the National Economy

1. As a consequence of China's rual economic reform, township and villageenterprises in China experienced remarkable growth in the last decade and now play a vital rolein the overall economy. Table I summarizes the breakdown by ownersnip types.

Table 1. TVE Ownership Breakdown (1993)No. of Enterprises Output Value Number of

Ownership (million) (bin Yuan) Employees(million)

Collective (Township and Village) 1.5 (7%) 1170 (677%) 51.5 (49%/)Private (Joint and Individual) 19.3 (93 %) 588 (33%) 54.3 (51%)All TVEs 20.8 (100%) 1751 (100%) 105.8 (100%)

Source: Sttical Digest of Township Enterpises (1993)

2. The output of TVEs increased at an average rate of about, 30% annually from1985-1992. In 1992 they accounted for 32 % of the national social product and 66 % of the ruralsocial product. Operating outside the framework of state ownership, TVEs are characterized bymarket orientation and autonomous financial operation. State control of TVEs is exercised onlythrough taxation, allocation of credits, rules on employment of labor, safety regulations,environmental regulations and other indirect means. Despite their smaller scale, older equipmentand less educated staff studies have shown that TVEs are generally more efficient in economicterms than State Owned Enterprises (SOEs). The reason appears to be the TVEs higherflexibility (due to their relatively small size) and their better ability to exploit local resources(due to close ties to the community). Furthermore, TVEs generally do not have the SOE's burdenof financing employee social security and other benefits. The TVEs are administered by the localgovernments in accordance with the national and provincial economic and social developmentplan and the state industrial policy.

lVE Induy

3. In this study, attention is focused on the collective enterprises because a vastmajority of the industries in the three analyzed sub-sectors belong to this category. IndustrialTVEs account for about two-thirds of total output value by all township enterprises, as shown inT-,le 2. It is projected that by the year 2000 TVEs will make up 50% or more of total nationalin istrial production.

Table 2. Relative Share of Industrial Enterprises Compared to All TVEs, 1992Number of Output Value Number of EmployeesEnterprise (bin Yuan) (million)(million)

Indusirial TVEs 7.9 1319 63.4All TVEs 20.8 1758 105.8Shae of Industrial Enwrises 38% 75% 60%

Souce: Statistical Digest of Township Etrpise (1993)

H ii -

4. In 1990, TVE industry consumed 142 million tce, consisting of 79 % coal, 16%electricity and 5.4% fuel oil. (See Figure 1). This represented 14.5% of total national energyconsumption and about 24% of total industrial energy consumption.

SeuaWm of EEnera S. TVEs tend to pay higher prices forconsurnp (1#) fuels than SOEs (which until recently obtained fuelsTotl: 142 million t largely at lower, in-plan prices) and thus may have

more incentive to adopt energy conservation practices.16ecttcIty Fue Oil Nevertheless, considering their generally small

production scale, aging equipment and often outdatedproduction processes, there is substantial potential forenergy savings in. TVE industry. That energy

79% conservation efforts are imperative is underscored byprojections indicating that TVE energy consumptionwill reach 240 million tce (of which raw coal will

reach 230 million tons) in 2000 and 330 million tee (of which raw coal will be 290 million tons)in 2010.

M.yectives and MebOdOQlog of e Stdv

6. Previous studies conducted by the Bankl (See, for example Ref 3) and othershave already examined macroeconomic policy issues and have identified key structural reformsthat need to be implemented to ensure the continued growth of the TVE sector. These studiesrecomn ended broad policy initiatives to improve the current legislative and incentiveframeworks, the provision of services to rural firms, and reforms in coal allocation and pricing.The present study is focused on technical improvements in energy efficiency, and aims toidentify specific policy measures, strategies and programs at the plant level that would promoteenergy conservation and help improve the economic efficiency of the WVE industry sector. Themethodology involved conducting case studies for energy efficiency improvements in selectedTVE industies, analyzing the costs and benefits of generic investment options and determiningindustry-wide replicability of the findings.

7. Brick and tile, coke and metal castings were selected for the case studies. Thesethree TVE inductries collectively account for about 40% of raw coal consumed, almost half ofthe total energy consumed and almost half of the total CO2 released to the atmosphere by allTVE industries in China.

Industry Profles

Brickmaking

8. Bricks are the leading construction materials in China and WVE industries nowproduce over 90% of total market demand (See Table 3). The rest are produced by a few largestate-run enterprises. Thirteen provinces account for about 85% of all TVE industry brick or atotal of about 355 billion pieces in 1990.

- iii -

Table 3. Position of TVE Brickmaking Industries(Outputs in 100 million pcs)

Year 1985 1986 1987 1988 1989 1990 1991 1992National Output 2942 3750 3911 4688 4716 4572TVE Output 2573 3447 3824 4528 4346 4174 4254 4955% TVE 87.5 91.9 95.8 96.6 92.2 91.3

Soure: Reference I

9. The most common brick production method in use in TVE industry todayutilizes the basic annular kiln (also knowr as the "Hoffman" type) with natural drying, i.e.,laying out in stacks in the open air and direct sunlight, of the green bricks. Over 90% of bricksare produced ir, this manner. The breakdown of production by kiln type for 1990 is shown inTable 3.

Table 4. TVE Brick Output According to Kiln Type (1990)

Kiln Type Output, Percent of TVE100 million pcs Output

Primitive indigenous kilns 313 7.5Annular kiln

Natal drying; solid bricks 3790 90.8Artificial drying; solid bricks 54 1.3Artificial dryig; hollow bricks 13 0.3

Tunnel kilnsArtificial drying; solid bricks 3 0.07Artificial drying; hollow bricks 1 0.03

Total 4174 100.0Source: Reference I

10. Improvements that have been made over the last few years include theincorporation of increasing amounts of coal dust and high carbon fly ash (e.g. from power plants)in the raw material clay that contribute to the energy required in firing. A second development isthe shift to the artificial drying process where combustion gases exhausted from the stack arechannelled into a drying section through which the green bricks are passed.The typical Hoffmankiln operation is characterised by a relatively large land use, both for the production of the mainraw material (clay) and for the stacking of green bricks for drying. A typical brick works makingsay 10 million standard bricks per year occupies 30 mu (20,000 M2). Artificial drying results insignificant land savings and higher productivity (year round operation) but may result in higherenergy intensity due to the need for supplemental fuel. Another relatively recent development isthe production of hollow or perforated bricks that enable significant savings in material andenergy with little effect on brick structural properties.

Cok Making

11. Most of the coke used in China is produced by large (greater than 100,000tonnes/yr) mechanized ovens in state-run enteprises. In 1990, of the total of 73 million tonnes ofcoke produced in China, about 70% was produced by mechanized ovens. The rest was producedin numerous, small scale TVE industries mainly by non-mechanized means, 90% of them in justseven provinces. A breakdown of TVE coke output by type of oven in 1990 is as follows:

iv.

Iable 5. TVE Coke Output by Oven Type (1990)

Coke Oven Type Million tonnes PelcentPrmiive Indigenous 4 6 24.7PX 11.8 63AJX-1 1.0 5.4Types P9, 75 0.7 3.8Small Mechanical 0.5 2.7Large Mechanical 0.0 0.0

Total 18.6 100.0Source: Reference I

12. Many of the ovens still used in TVE cokemaking, including the PX and JX-1types, are relatively simple and do not recover the chemicals, tars or gases released in theprocess. Very roughly, this represents a loss of 3.2 to 4.0 million TCE annually, as well as severepollution impacts from gaseous emissions and liquid effluents discharge.

13. The third generation Types 75 and 89 designs either burn most of the byprodu-.tsor recover the tar. Coal consumption is improved to about 1.4 TCE per ton coke and pollution issubstantially reduced compared to the earlier models. However, there is little motivation forretrofit-conversion of an existing operational PX or JX- oven to Type 75 or 89 since the cost isnot significantly less than building an improved oven on a clear site. Without stronger regulatroymeasures, technical improvements are therefore only attractive to producers when an existingoven or plan' reaches the end of its economic life - typically ten years for most ypes of ovenused in the TVE industry- and a new plant musi be built As regards mechanical ovens, only thevery large ones (over 200,000 tpy) that recover and market gas products are likely to beeconomic. Their substantially higher cost is certain to be a major constaint to adoption by TVEsin the near term.

Mestal Csings Idy

14. In 1990, Chinese industries used 10 million tonnes of metal castings, secondhighest in the world. About 42% of these were produced by 13,200 TVE enterprises. The outputvalue of this contribution was about 6.3 billion Yuan. Eleven provinces account for nearly 80%of the total TVE castings output.. Nearly all (99%) of TVE metal casting work is on ferrousmaterials, i.e., iron and steel. The quality and durability of the products are way behind thoseproduced by developed countries. The position and profitability of the China's TVE castingindustry in the future will depend on how quickly it can upgrade the quality of its products that,in turn, depends on how quickly it can convert to more modern and efficient production methods.Such conversion will very likey also result in significant reduction in cool use per unit output.

15. TVE castings enterprises are divided in this report into four rough categories: (a)Backward -- typically using manual production methods, producing say 1000 tonnes of castingsper year, (b) Less Backward -- using mostly manual methods and a small proportion ofmechanized molding facilities, making say 3000 tonnes per year; (c) Moderate or General level -- using mechanized molding, a hot blast cupola, and making about 5000 tonnes per year, and (d)Advanced level -- using a mechanized or semi-automatic molding line, a complete sandprocessing system, using a hot blast cupola with computer controlled charging system or aduplex melting set, and making 5000 tonnes per year or more.

.V.

16. The shares of total output of the various categories in 1990 are shown below:

Table 6. Output Distribution of Castings Industry by Technology Category (1990)

Technology Output Percentmillion tonnes

Backward 2.058 49.0Less backward 2.100 50.0Moderate level 0.042 1.0Advanced level 0.0 0.0

4.200 100.0Source: Reference I

Case Studies of Investment Options

17. The technical improvements examined include conversion or retrofit of existingoperation, consolidation into larger scale operation, establishment of new, more efficient plantsand a combination of such actions. The base cases were chosen so that they represent typicalsituations in each industry, such that potential replicability of desirable improvements ismaximized.

TheBricdkIndugIr

18. Two basic cases were chosen for economic investigations:

£aase A, involving the consolidation of several small plants producing solidbricks and using artificial drying into one large plant producing solid bricks (Al)or hollow bricks (A2) and using artificial drying; and

Case B the conversion of an existing plant producing solid bricks and usingnatnral dtying to one producing hollow bricks and using artificial drying.

19. Case A takes care of the prevalent situation where most brickworks are smalland may need first to be consolidated before any technical renovation is carried out. Foranalytical purposes, Case A is broken into two discrete steps or subcases (Al and A2), asfollows:

Al Consolidating production in a larger plant and conversion to artificialdrying.: replacement of ten typical small plants (each making 5 million solidbricks/yr. using Hoffman kilns, natural drying) by one larger plant (50 millionsolid bricks/yr. using the Hoffman kiln, artificial drying).

AZ Conversion to hollow brick production: conversion of one existing largeplant producing 50 million solid bricks /yr. using a Hoffman kiln with artificialdrying to a plant of the same capacity, same kiln, with artificial drying butproducing standard clay hollow bricks.

20. Case B, meanwhile, is analyzed by using three different plant capacities: 5, 10and 20 million solid bricks/yr. (subcases B1, B2 and B3). The purpose of the exercise is todetennine the minimum economic scale for this type of conversion.

.vi-

Coke Makin

21. The case studies chosen for the cokemaking industry were as follows:

Case A. The replacement of 5 typical PX coke ovens of 10,000 tpy capacity byone new plant producing 50,000 tpy, either with JKH-89 (Case Al) or TJ-75oven,; (Case A2);

Case B. The establishment of a small mechanized coke oven (HQ-3) of 50,000tpy capacity, as a replacement for 5 PX ovens, each of 10,000 tpy capaeity;

Case (C. The establishment of a refinery processing 3000 tpy tar, collected fromadjacent Type 89 plants.

Meta Castinags,

22. The two case studies chosen for the metal castings industry involve theintroduction of more energy-efficient technology and more modern casting processes to typicalTVE foundries:

Case A Transformation of five 3,000 t/yr foundries using standard cold blastcupola melting and manual molding with clay-bonded sand, to three 5,000 t/yrfoundries with duplex melting (cold blast cupola plus electric holding furnace)and using automated resin-bonded sand molding.

as B Establishment of one new 5,000 t/yr plant with internally heated hotblast cupola and automated resin-bonded sand molding line, as an alternative tofive 1,000 tfyr traditional foundries using cold blast cupola and manual clay-bonded sand molding.

Results of Case Studies

23. The results of financial and economic analysis for the three industries aresummarized in Table 7 below.

24. Brick. Consolidation of small brickworks and conversion to artificial drying(Case Al) is clearly a highly beneficial investment from both the TVE's and the country'sviewpoint (large land savings, high IRRs). Extending Case Al to the production of hollow bricks(not shown in the above but also investigated) is also a viable inrvestment but less so than Alalone. However, it does not make economic sense to take an existing plant already usingartificial drying and convert it to hollow brick production (Case A2) mainly because of theadditional extruder cost Existing plants still using natural drying can be viably converted tonatural drying and hollow brick production if the scale is at least 20 million bricks/yr (CaseB3).The major constraints to more rapid implementation of the above identified viableconversions are: (1) the difficulty of consolidating small brickworks, especially when owned byseveral townships, and (2) the high cost of special extuders for hollow brick production.

25. Coke. Replacing small PX plants with a larger third-generation model JKH-89 orType 75 (Case A) appears to have acceptable economic rates of return but low financial rates ofreturn. However, in all cases it was found that these indicators are extremely sensitive tovariations in operating costs and coke prices. Just a fall of 3-5% in coke prices from current

. vii -

levels, for example, can make the investments completely uneconomic. Replacing the small PXplants with a mechanical oven of only 50,000 tpy capacity (type HQ-3) has marginal rates ofreturn and, like the previous case, the economics is extremely sensitive to changes in operatingcost and coke prices. Thus, while these options represent improvements over the highlypolluting PX models, they do not appear to be viable long-term alternatives to the currentsituation; the only valid reason for renovations would be environmental concerns. Theestablishment of a centralized tar refinery of at least 3,000tpy is the only positive case analyzed;it is clearly a highly beneficial investment in economic and environmental terms.

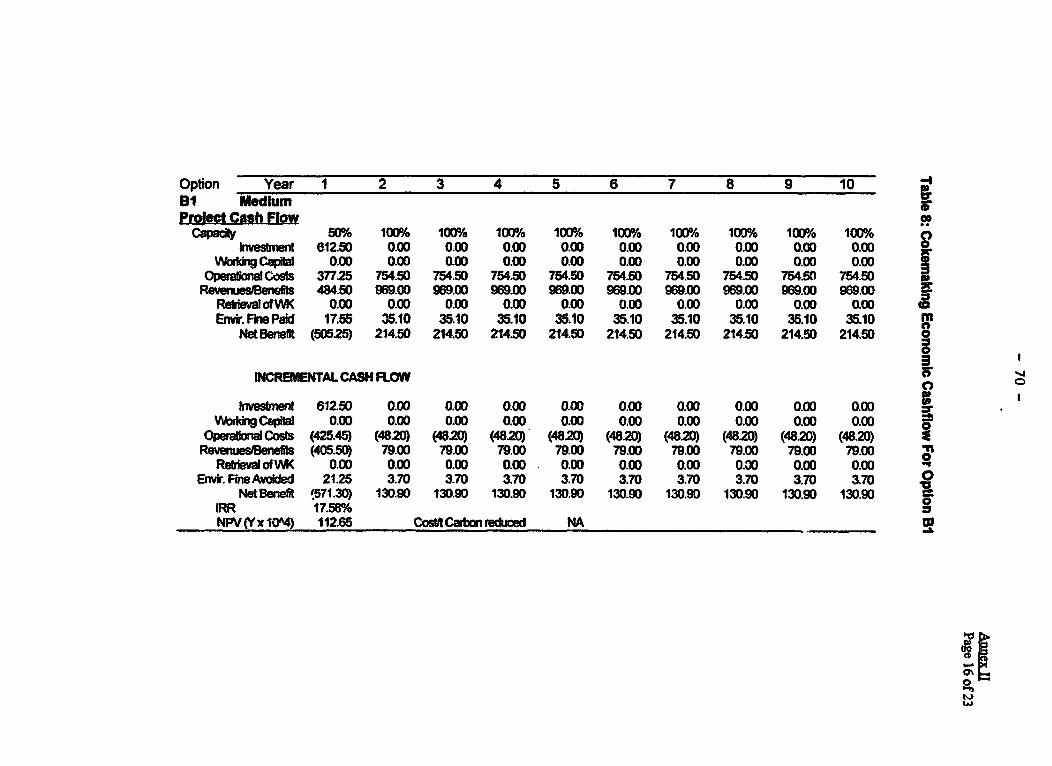

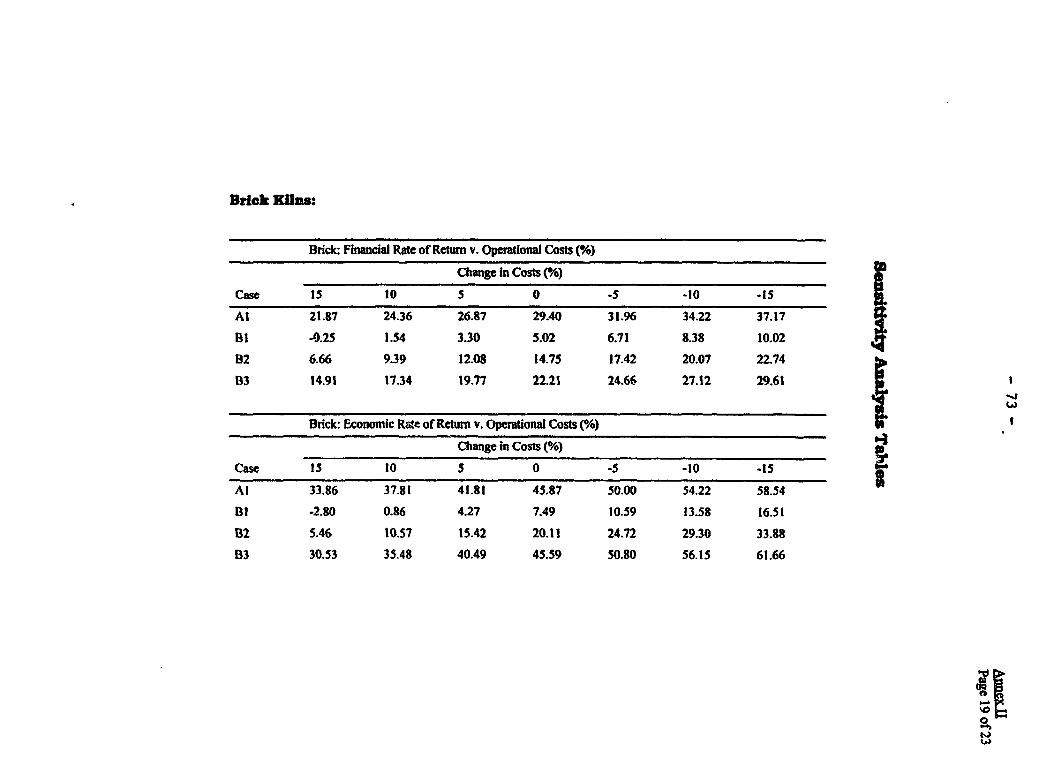

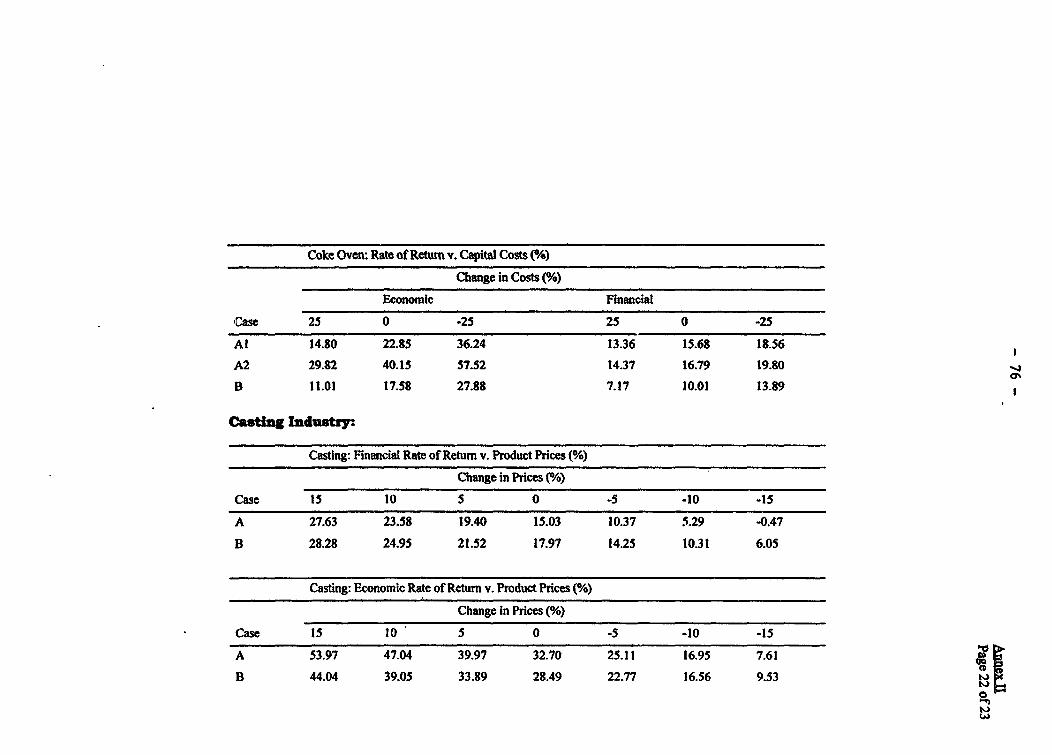

Table 7. Summary of Feasibility Analyses

Incremental DiscountedCase Investment, Financial Analysis Economic Analysis Payback,

'000 Yuan NPV IRR, % NPV IRR, % YearsBrick.Al 2,183 1,648 29.4 3,705 47.2 6-7

(1,283-1,782) (23-31) (3,218-3,906) (37-52)A2 500 Negative Negative Negative Negative NABi 621 -192 5.0 -111 8.25 NA

937 (-172 to -318) (2-6) (-vQ to -279) (4-10)B2 850 100 14.8 274 20.1 6-7

1,062 (-42 to +140) (11-16) (85-380) (14-23)

B3 1,105 636 22.2 1,725 45.6 4-51,381 (451-716) (20-33) (1,478-1,937) (36-48)

Coke:Al 2,905 819 15.7 950 22.8 7-8

(-1,164 to (7-27) (-2,550 to +5,374) (<0 to +73)+3,324)

A2 2,865 1,501 16.8 2,858 40.1 5-6(-929 to (8-28) (-643 to +7,281) (4-90)+3,559)

B 6,125 -569 10.0 1,126 17.6 NA(-1,829 to (5-30) (-1,087 to +11,261) (6-68)+5,171)

C 3,199 27,620 30.8 66,787 53.4 4-5Metal Castings:

A 31,590 6,000 15.0 42,860 32.7 8-9(-37,390 to (<0 to 32) (-32,690 to (<0 to 61)42,040) 1^5,500)

B 9,930 3,730 18.0 11,270 28.5 6-7(-7,450 to (-2 to (-7,7100 to (4 to 49)13,080) +32) 27,310)

26. Metal Castings. The two investment cases examined are attractive from thecountry's viewpoint but the financial rates of return are both less than 20%. Both cases representmajor changes in the operational process, and the use of relatively high-technology equipment.These are reflected in the higher investment requirements compared to the brick and coke casesand, in the case of A, a relatively longer payback period. While both cases are sensitive to bothinput and output pri^es, they are much less so than in the coke cases. Considering the continuingimportant role of the TVE castings industry to the overall industrial devlopment of China, and

- viii -

the recognized need to upgrade the currently backward status of this industry, the aboveidentified economic investments deserve support. The major barrier to faster adoption of theseoptions by the TVE metal casting sector is the high capital cost-and correspondingly longpayback periods--and the need for special training in the new expertise required.

Energ and Pollution mpacts

27. Except for the conversion of brickworks from natural to artificial drying thatresults in greater energy consumption', all of the cases shown to be economically viable alsoresult in coal savings and reduction of smoke, dust and CO2 and SO2 emissions (see Chapter 3).In addition, the phasing out of indigenous and PX ovens reduce groundwater pollution from tarand other chemical discharges. The net cost of carbon dioxide abatement are negative forinvestments found to be viable in all three industries, reflecting that these benefits are onlyadditional to the profitability gains.

Accelerated Investment Programs

23. The identified economic investments in the TVE brickmaking and metal castingsindustries may not be undertaken at any significant pace due to various constraints mentionedabove. Well-designed interventions, such as capacity building, intermediation of the infonnationmarket and fiscal incentives, can accelerate the level of investments in the more efficientprocesses. The discussions below examine accelerated investment programs that could havegreater impact on TVE-wide coal savings and reduction of CO2 and S02 emissions. Theseimpacts were estimated at two levels of accelerated investments: Low Accelerated scenario andHigh Accelerated scenario (See Annex A).

29. The Business-as-Usual (BAU) scenario was first determined; it represents thebest estimate of what the industry situation up to the year 2010 would be if no interventions byway of promoting improved technologies or raising new investment funds are made. The twoaccelerated scenarios were then used to estimate the impacts of active industiy upgradingprograms implemented starting in 1995. Implicit in the two accelerated cases am the additionalefforts on human resources development and the promotion of new technologies and bestprctices that will be crucial to achieving higher rates of adoption of new processes.

30. The estimated investment under the BAU scenario and the incrementalinvestment required for the accelerated upgrading scenarios in the two industries are shown inTable 7.

1 This Is because, aside ftom increased coal ase, more electlty input is required for the blowers. The benefitsof conversion to the brlckworks are in shorter drying time, extended plant operatrng period per year (since the process isno longer affected by bad weather conditions) and thus Increased brick output greater labor productivity and, mostimportantly. substantially reduced land requirement.

I ix-

Table 7. Investment Levels, Million YuanBrickmaking and Metal Castings

BAU (rotal) Low vs. BAU High vs. BAU(Difference) (Difference)

1995-2000 7,909 7,246 12,6002000-2005 13,866 5,765 13,1952005-2010 22,540 5,224 11,883

31. The resulting estimated incremental impacts on coal savings and reduction ofS02 and C02 emissions are shown in Table 8.

Table 8. Incremental Impacts of Accelerated ProgramsBrickmaking and Metal Castings

Low vs. BAU High vs. BAU

Coal, C02, S02, Coal C02, S02,thousand thousand thousand thousand thousand thousandTCE tonnes C tonnes TCE tonnes C tonnes

1995-2000 147 3,957 180 296 4,035 1852000-2005 415 3,617 163 825 5,264 2382005-2010 755 3,536 154 1,531 9,760 420

Conclusions

32. Energy efficiency initiatives for TVEs must be approached at two levels:through structural or policy reforms, and through cechnical improvements. There is scope foreffective interventions at the plant level in TVEs, to ensure that industry transformation is guidedto the use of appropriate technologies and efficient practices in the medium term. Although anumber of Government initiatives in technology transfer are beginning to be implemented, mostTVEs still have very limited access to technologies and best practices. The present study hasfocussed on brickmaking, coke making and metal casting because they collectively account forabout half of total coal use by TVEs; furthermore, these industries represent vital inputs toinfrastructure (bricks) and machinery (coke and castings), the demand for which can be expectedto keep pace with the very rapid growth of the overall economy. The study found that in Chinatoday relatively low-cost technical innovations that are highly appropriate to TVE conditionsexist in the brick and cokemaking industries and need to be more widely disseminated. Incokemaking, however, the study found that efficiency improvements confined to the currentscales of production are only marginally economic and do not represent long-term solutions tothe problems faced by this particular TVE enterprise.

Policv Implications

33. In TVEs the driving force for energy conservation is not the desire to save coalbut the need to maintain a market share in an increasingly competitive environment. Inenterprises with high energy consumption, energy conservation can help streamline costs andenable them to adapt to changing market conditions. The TVEs are more likely than the SOEs toface realistic, market-based input prices and this fact, together with their profit-oriented nature,will predispose them to adapt efficient technologies if not hindered by lack of relevant technical

_x_

information or access to up-to-date capital goods. Improving access by TVEs to these factors islikely to prove more effective in consenring energy than regulations and administrative sanctions

34. Ownership issues can be a barrier to implementing technical upgradingprograms. The intimate relationship that exists between the TVEs and local governments canlead to conflicts of interest between regulatory and ownership functions. This could bemanifested in, inter alia, inadequate enforcement of environmental regulations and slow phasingout of highly inefficient plants. Strengthening enterprise law and clarifying property rights aswell as promoting share-holding may help some TVEs outgrow their present communityorientation and induce cross-sectoral cooperation.

35. It is important to continue efforts to create a "level playing field" between TVEsand SOE's regarding access to finance, capital goods, inputs, skilled manpower and technicalassistance. The "1986 Regulations" established an institutional framework and supportmechanisms for energy conservation but these seem to be directed more at the larger SOEs thanat TVEs. Technological support to TVEs needs to be strenghtened. The knowledge about energyefficient technologies and the operational experience of plants who have successfully introducedsuch technologies need to be disseminated through training courses, workshops or other types ofpromotional events.

36. On environmental policy, it should be noted that in areas where air pollution isalready serious, the construction of even a new, energy efficient plant will firther worsen localair quality. This implies that a program to support introduction of efficient technologies in TVEsmust ensure that old plants are shut down when new ones are being constructed in order toachieve an actual improvement of air quality in very polluted areas.

Recommendations

37. Considering the significant economic and environmental benefits of thetechnical improvements described in this study, it is recommended that a prgmm to gp=de theTVE brickworks and metal casting industies be prepared. The program will consist of: (a)inlesmen in technical process improvements and restructuring initiatives, i.e., establishmentof larger, more efficient plants to replace a number of smaller, inefficient ones--along the lines ofthe cases studied in this report; (b) cApa&i builig activities-including industry-specifictraining on good practices and other energy saving approaches; sector-wide awarenesscampaigns, and the development of capabilites in existing county level energy conservationcenters to effectively support specific technical needs of the subject industries, and (c) activeenforcement of environmental regulations at the local level. The upgrading program to beprepared for the suject industries could be structured into three phases: a three-year pilot phasestarting inl995, followed by a five-year expansion phase and a full implementation phasethereafter

38. The future of coke production in China points inexorably to the direction ofWestern type large-scale mechanical (LSM) ovens which are environmentally cleaner and moreeconomic. The TVE sector should be encouraged to phase out its support for small-scaleindigenous co-ke production. A more active program of inspection, application of environmentalpenalties and shutting down of highly polluting PX plants should be carried out by TVEs.Existing JKH-89, TJ-75 and similar improved models should be allowed to continue operationbut should not be extended any subsidies or special assistance. The establishment of new

-xi-

cokeworks that do not recover their gas byproducts should be discouraged over the mediumterm. If new small-scale cokeworks are to be built, they should, at a minimum, be required toutilize new designs such as the JKH-89 and TJ-75 or later models. For all new cokeworks, acomprehensive environmental impact statement should be made to show that there will be no netincrease in pollutant emission in the area.

39. The preparation of the proposed prgm should be made a major compnent ofthe proposed UNDP GEF technical assistance project ($5-6 million) directed at TVEs that MOAexpects to be approved shortly. Availability of these resources provide an opportunity to: (a)prepare the proposed program, including the conduct of additional supporting investigations, and(2) implement the pilot phase. The additional work needed are more detailed techno-economicinvestigations of the promising investment cases that were identified broadly in the presentstudy, and more incisive determination of realistic options for addressing the various policy andimplementation issues that were raised but not resolved in the present study. There is need, forexample, to make a deeper assessment of the barriers and possible approaches to encouragingconsolidation of several small-scale TVE operations to a larger one-an implementation issuethat has not often been successfully resolved in past projects. There is also need for a moreintensive review of the various existing programs for dissemination of technical information toTVEs, how effective they have been and how best to integrate them under a coherent overallsystem. These additional preparatory work could be conducted within the framework of aninstitutional study on "how to efficiently implement energy conservation initiatives in TVEs ".

40. The objectives of pilot phase implementation would be to demonstratefeasibility, develop the human resource base needed to appraise, implement and sustain thesetype of projects in TVEs, and acquire experience in institutional coordination. The pilot phasecould start with several typical plants representing the three industries in one or a few provinces.The communities/provinces chosen should have a record of being active in implementingtechnical renovations, where the chances of program success are maximized. These sites may ormay not be the same ones where the present case studies were done. Based on the experienceacquired in the pilot phase and the availability of financing sources, the upgrading programwould be expanded into several more provinces. The third phase would aim for a nationwideprogram. The output of the pilot phase would include a detailed definition of the follow-upexpanded investment project.

L Overview

Role of Township Enterprises in the National Economy

1.1 As a consequence of China's rural economic reform, township and villageenterprises in China experienced remarkable growth in the last decade and now play a vital rolein the overall economy. Known as brigades and communes before 1983, "township enterprises"or "township and village enterprises (TVEs)" is now the general term applied to all enterprises ofdifferent ownership as long as they are non-state owned. Business activities by TVEs permeateevery part of the national economy and every aspect of social commodity production andexchange, including industry, construction, transportation, commerce, food service, serviceindustry and collectively run agricultural and livestock farms in rural areas. TVEs includecollective enterprises (owned by townships or villages), joint enterprises (owned by severalhouseholds) and individual enterprises (owned by one household). Table 1 summarizes thebreakdown by ownership types.

Table 1.1 TVE Ownership Breakdown (1993)

No. of Output Value Number ofOwnership Enterprises (bln Yuan) Employees

(million) (million)Collective (Township and 1.5 (7%) 1170(67%) 51.5 (49/)Village) 19.3 (93 %) 588 (33%) 54.3 (5 1%)Private (Joint and Individual)All TVEs 20. 8 (1 00%) 1751 (100%) 105.8 (100%)

Source: Statistical Digest of Township Enterpre (1993)

1.2 The output of TVEs increased at an average rate of about 30% annually from1985-1992. In 1992 they accounted for 32 % of the national social product and 66 % of the mralsocial product. The emergence of numerous township enterprises has accelerated the formationand development of small towns in mrual areas: there were only about 9,000 small towns in 1986but over 40,000 in 1990.

Key Characteristics of TVEs

1.3 Operating outside the framework of state ownership, TVEs are characterized bymarket orientation and autonomous financial operation. Market needs and trends generallydetermine production paerns, pricing of goods and other day to day decisions. On average,more than 85% of needed raw materials and fuel are obtained in the competitive market. Statecontrol of TVEs is exercised only through taxation, allocation of credits, rules on employment oflabor, safety regulations, environmental regulations and other indirect means.

1.4 Compared to state-owned enterprises (SOEs), equipment and technology used inTVEs are generally older, mostly of 1950 to 1970 vintage, although acquisition of modemequipment has intensified in recent years. While the average educational level of TVEemployees and managers is still far below that of SOEs, the number of employees with collegelevel education has increased by over 300% since 1986. Despite these deficiencies, studies haveshown that TVEs are generally more efficient in economic terms than SOEs. The reason appears

-2 -

to be the TVEs higher flexibility (due to their relatively small size) and their better ability toexploit local resources (due to close ties to the community). A major advantage over SOEs is thatTVEs are not required to allocate funds for social security and similar benefits to its employees.

1.5 Extemal financing of TVEs are commonly in the form of revolving capital loansand fixed asset loans obtained mainly from the Agricultural Bank of China (ABC) and ruralcredit cooperatives. Revolving capital loans supplement regular enterprise funds for day-to-daymanagement and production, and for seasonal purchase of raw materials. The loan periodusually does not exceed a production cycle, i.e., a maximum of one year. Fixed asset loanssupplement funds for capital goods investment of newly-established enterprises, and providefunds for technical innovation and large-scale equipment repair. The loan period ranges from Ito 4 years, depending on the specific purpose. Interest rates for ABC loans are set uniformly bythe state and are relatively low. Rural credit cooperatives are allowed to charge higher interestrates and generally do so.

1.6 At the state level, ail TVEs come under the jurisdiction of the Ministry ofAgriculture (MOA) and its "Department of Township Enterprises". At the provincial level,control is exercised through a Provincial Rural Enterprise Bureau; similar offices also exist at thecity and township levels. The local Rural Enterprises Bureau have the power to issue and revokelicenses to operate to TVEs. The TVCE enterprises are administered by the local govermments inaccordance with the national and provincial economic and social development plan and the stateindustrial policy.

TVE Industry

1.7 In this study, attention is focused on the collective enterprises, also oftenabbreviated TVCE's (Township and Village owned Collective Enterprises) because a vastmajority of the industries in the three analyzed sub-sectors belong to this category. IndustrialTVEs account for about 75% of total output value by all township enterprises, as shown in Table2, and roughly one-third of total industrial output in China. It is projected that by the year 2000TVEs will make up 50% or more of total national industrial production.

Table 1.2. Relative Share of Industial Enterprises Compared to All TVEs, 1992

Number of Output Value Number of EmployeesEntaprises (bin Yuan) (million)(million)

Industri TVEs 7.9 1319 63.4All TVEs 20.8 1758 105.8Share of Industrial Enterprise 38% 75% 60%

Sowce: Stistical Digest of Township Enteprises (1993)

1.8 The phenomenal growth experienced by TVE industry during the brief span of adecade is shown in Table 3. Between 1981 to 1990, the average increase in annual total outputvalue was about 39 %.

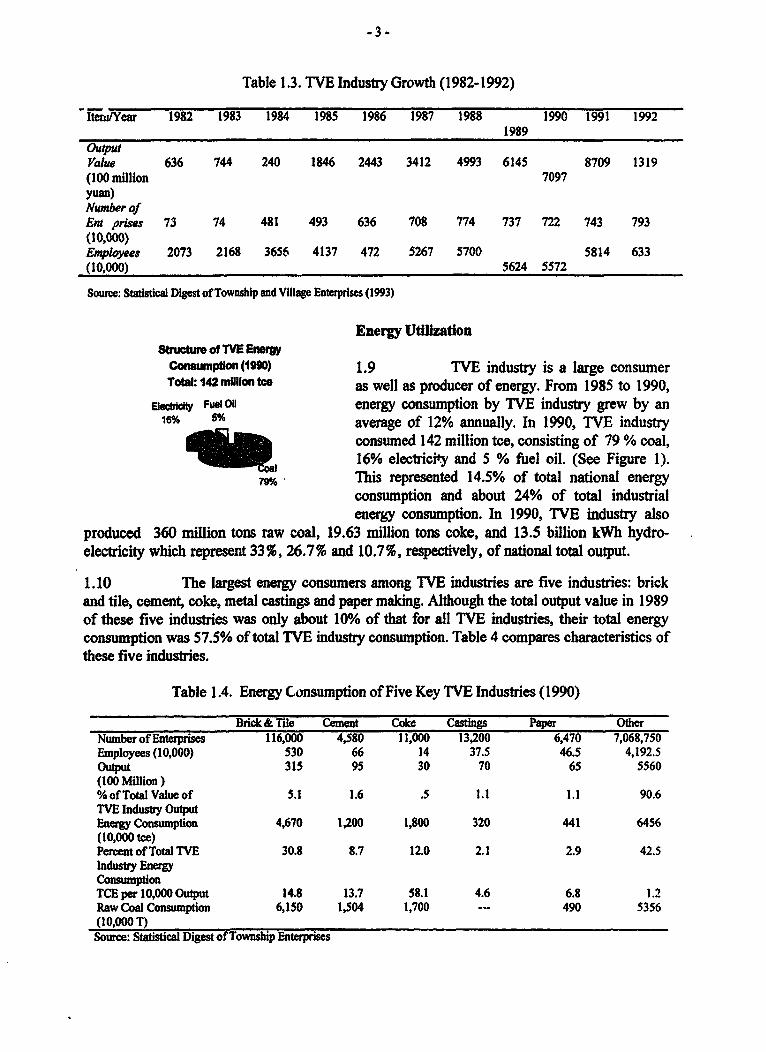

Table 1.3. TVE Industry Growth (1982-1992)

IiGenwYear 1982 1983 1984 1985 1986 1987 1988 1990 1991 19921989

OutpValue 636 744 240 1846 2443 3412 4993 6145 8709 1319(100 million 7097yuan)Number ofEn prises 75 74 481 493 636 708 774 737 722 743 793(10,000)Employees 2073 2168 3656 4137 472 5267 5700 5814 633(10,000) 5624 5572

Source: Statstical Digest of Township and Village Enterprises (1993)

Energy UtilizationStrucWte of TVE Enerw

Consumpton (190) 1.9 TVE industry is a large consumerTotal: 142 millon1tee as well as producer of energy. From 1985 to 1990,

Ebltict Fuel OU energy consumption by TVE industry grew by an16% 5% verage of 12% annually. In 1990, TVE industry

consumed 142 million tce, consisting of 79 % coal,16% electricity and 5 % fuel oil. (See Figure 1).

79% This represented 14.5% of total national energyconsumption and about 24% of total industrialenergy consumption. In 1990, TVE industry also

produced 360 million tons raw coal, 19.63 million tons coke, and 13.5 billion kWh hydro-electricity which represent 33%, 26.7% and 10.7%, respectively, of national total output.

1.10 The largest energy consumers among TVE industries are five industries: brickand tile, cement, coke, metal castings and paper making. Although the total output value in 1989of these five industries was only about 10% of that for all TVE industries, their total energyconsumption was 57.5% of total TVE industry consumption. Table 4 compares characteristics ofthese five industries.

Table 1.4. Energy Consumption of Five Key TVE Industries (1990)

Brick & Tile Cement Coke Castings Paper OtherNumber of Enterprises 116,000 4,580 11,000 13,200 6,470 7,068,750Employees (10,000) 530 66 14 37.5 46.5 4,192.5Output 315 95 30 70 65 5560(100 Million )%ofTotalValueof 5.1 1.6 .5 1.1 1.1 90.6TVE Industry OulputEner Consumption 4,670 1,200 1,800 320 441 6456(10,000 toe)Percent of Total TVE 30.8 8.7 12.0 2.1 2.9 42.5Industry EnergyConsumptinTCE per 10,000 Output 14.8 13.7 58.1 4.6 6.8 1.2Raw Coal Consumption 6,150 1,504 1,700 - 490 5356(10,000T)Source: Statstical Digest of Township Enterprises

-4-

1.11 No definitive studies exist that compare energy efficiencies of State-ownedindustries and TVE plants engaged in similar production lines. SOEs as a group consume muchmore energy than TVE industry b-i this is due mainly to their larger scale and heavy-industryconcentration. . Although small-scale TVEs employing traditional methods are clearly wastefulof energy (such as traditional coke making kilns, small iron smelters, etc), these are graduallybeing phased out by a combination of environmental regulations and market factors. TVEs tendto pay higher prices for fuels than SOEs (which until recently obtained fuels largely at lower, in-plan prices) and thus may have more incentive to adopt energy conservation practices.Nevertheless, considering their generally small production scale, aging equipment and oftenoutdated production processes, there is substantial potential for energy savings in TVE industry.

1.12 That energy conservation efforts are imperative is underscored by projectionsindicating that T1VE energy consumption will reach 240 million tce (of which raw coal will reach230 million tons) in 2000 and 330 million tce (of which raw coal will be 290 million tons) in2010. For China as a whole, the primray energy consumption per unit of GDP is higher thanmost other countries, including some low-income countries such as India. A major reason is theinordinately high-share of the industrial sector in the GDP in the Chinese economy (46% in 1988as compared to only 30% for India); in general, the industry sector in all countries has a higherenergy intensity of output than the other sectors. Compounding this factor is the predominance oflow-value goods in China's current industrial mix, resulting in relatively higher energy input fora given value of output goods (Ref. 2). For the TVE sector, the energy consumed per unit ofproduct for heavy coal-using industries is much higher than Westem equivalents. For example,bricks produced in indigenous kilns in China consume about 2.6 TCE/10,000 bricks incomparison with about 0.9 TCE/10,000 bricks in the U.K. Significant reductions in currentenergy intensity could be achieved, however, without necessarily adopting high-technologyprocesses in the West. Many locally developed energy-efflcient innovations are already practicedin some parts of China and need only to be disseminated widely.

1.13 The Chinese Government puts a high priority on energy conservation. Some ofthe key policy pronouncements on energy management that have been made officially include:the "Temporary Regulations on Issues of Comprehensive Utilization of Resources," issued bythe former State Economic Commission and reissued by the State Council in 1985; the"Temporary Regulations of Energy Conservation Management" issued by the State Council in1986,; and the "Regulations on further Strengthening Electricity usage" originally issued by theformer State Economic Commission and the State Planning Commission and reissued by theState Council in 1987. Primarily through Govenment mandated structural reforns, commercialenergy intensity has in fact been reduced by about 30% during the last decade.

Environmental Issues

1.14 The five industries previously mentioned are also the heaviest polluters amongall TVE industries. The paper making industry is responsible for most of the water pollution,accounting for almost half of the sewage discharge by all TVE industries. The brick and tileindustry, on the other hand, discharges the largest amount of waste gases, mainly emissions fromcoal combustion. These are shown in Table 1.5.

- 5 -

Table 1. 5. Waste Gas Emissions of TVE Industries, 1989

Brick & Tile Cement Coke Casting Paper Making OtherWaste Gas Emissions 5, 2,540 39 49 520 3,582(100 million standard m3)%ofTotal 41.9 20.8 3.3 0.4 4.3 29.3S02 125 21 6.1 3.6 10CO, 2,879 620 1000 94 278 3498Source: Nadonal Study on Pollution Sources of TVE Indiuty, 1990.

1.15 Pollution monitoring and control in TVEs are the responsibility ofenvironmental protection bureaus situated at the provincial, municipal, county and townshiplevels. Maximum permissible emission levels and penalty schedules are set at the state level bythe National Environmental protection Agency (NEPA), in coordination with environmentalprotection units within most of the ministries and state enterprises. Although there has beenmuch improvement in recent years, enforcement of regulations at the local level is generally stillspotty and inadequate. TVEs desiring to upgrade their processes and reduce polluting dischargesare hampered by lack of access to appropriate abatement technologies and financing.

1.16 From the global warming standpoint, the brick and tile, cement, coke and metalcastings industries --all heavy coal users-are responsible for most of the greenhouse gases(mainly carbon dioxide) emitted into the atmosphere.

Objectives and Methodology of the Study

1.17 Previous studies conducted by the Bank (See, for example Ref. 3) and othershave already examined macroeconomic policy issues and have identified key structral reformsthat need to be implemented to ensure the continued growth of the TVE sector. These studiesrecommended broad policy initiatives to improve the cuffent legislative and incentiveframeworks, and the provision of services to rural firms. There is no doubt that in all aspects ofTVE operation, including energy use, fundamental policy reforms that provide the rightincentives to enterprises to improve their overall economic efficiency have greater impact thanspecific programs. There is, however, also an important role for initiatives at the plant level thatbuild upon and concretize broad policy prescriptions. The present study is focused on energyaspects, and aims to identify specific policy measures, strategies and programs at the plant levelthat would promote energy conservation and help improve the economic efficiency of the TVEindustry sector. The methodology involved conductng case studies for energy efficiencyimprovements in selected TVE industries, analyzing the costs and benefits of generic investmentoptions and determining industry-wide replicability of the findings.

1.18 It was initially intended to also examine local pollution issues and identify cost-effective means to reduce TVE industry emissions. Lack of resources prevented this particulareffort. The study thus limited itself to the energy efficiency aspects plus the quantification of thepotential for reduction in carbon dioxide gas emissions that would be achieved by improvementsin coal utilization efficiency2. The latter data would be an input to the UNDP-GEF/World Bankstudy on controlling greenhouse gas emissions in China.

2 Sorne of the technical upgrading for energy efficiency tiat were eventuaily Identiffed by this study also result insignificant reduction of iocal pollution Impacts. For example, te conversion of indigenous coking kilns into modifiedmodels that retover tar drastically reduces ground water pollution by effluents.

-6 -

1.19 A Chinese team drawn from the Ministry of Agriculture's Departnent of Energyand Environmental Protection and the Department of Township Enterprises, the State PlanningCommission's Energy Research Institute and several local experts was constituted for the study.The team, assisted by ESMAP staff and international consultants, conducted the selection of keyTVE industries, identified specific plants in suitable counties that would be subjected to the casestudies, conducted the field work and prepared the economie and financial analysis of identifiedenergy efficiency investnent options. Three major reports prepared by the Chinese team resultedfro,m these efforts. The present report summarizes the overall findings.

Key TVE Industries Selected for the Study

1.20 The subject industries were selected based mainly on their share of TVE energyconsumption, the potential for greenhouse gas abatement resulting from the proposed fuelefficiency investments, gross output value and employment. The five industries previouslymentioned clearly topped the list. Cement and paper making w!ere then excluded becauseongoing or upcoming Bank studies or loans would be dealing with these particular industries andwill likely cover similar ground, as well. Thus, brick and tile, coke and rnetal castings werefinally selected for the case studies. These three TVE industries collectively account for about40% of raw coal consumed, almost half of the total energy consumed and almost half of the totalC02 released to the atmosphere by all TVE industries in China.

-7-

IL Industry Profiles

2.1 This Chapter provides an overview of the position of each of the subjectindustries in the national context, reviews the production technologies currently in use in Chinaand discusses the types of technical improvements that are worth introducing in the immediatetenm (See also Annex III for additional industry data). The constraints to technical upgradingimposed by existing plant sizes are then considered, as well as the environmental impacts ofpresent practices.

A. The Brick InduntryIntroduction

2.2 Brick and tile production has long been a major rural industry in China, withbrickworks located in almost every municipality, province and astonomous region. The earlybrickworks required little itnput; they utilized a very simple technology that needed only laborand required almost no capital investment. The raw materials, mainly clay, is available all overthe country. Bricks are the leading construction materials in China and TVE industries nowproduce over 90% of total market demand (See Table 2.1). The rest are produced by a few largestate-run enterprises.

Table 2. 1. Position of TVE Brickmaking Industries(Outputs in 100 million pcs)

Year 1985 1986 1987 1988 1989 1990 1991 1992National Output 2942 3750 3911 4688 4716 4572TVE Output 2573 3447 3824 4528 4346 4174 4254 4955% TVE 87.5 91.9 95.8 96.6 92.2 91.3

Source: Statistic Di#es of Township Enteprise in China

2.3 Thirteen provinces account for about 85% of all TVE industry brick or a total ofabout 355 billion pieces in 1990 (See Table 2.2).

Table 2.2. Major Brick-Producing Provinces (1990)Eterprses Employees - Ouput - Percent of TV

Province Number (10,000) (lOOmllpcs) (100 mill. Yuan) OutputHenan 10300 47.1 558 28.7 13.4Shandong 10310 65.4 539 55 12.9Jiangsu 10810 62.2 472 44.9 11.3Hebei 5550 14 382 22.2 9.2Anhui 5800 36.7 249 18.2 6.0Guangdong 5690 16.3 208 14.3 5.0Hubei 5170 25.7 199 17.2 4.8Zhejiang 2670 25 192 15.9 4.6Sichuan 9050 25.4 189 13.6 4.5Shanxi 5960 14 173 8.4 4.1Shanxi 5420 17.4 163 9.8 3.9Liaoning 2100 17 117 11 2.8Hunan 2000 8.9 108 5.7 2.6Totat 80,830 375.) 3,S49 264.9 85.1

Source: Staiftic Digest ofTownship Enterpris in China

*8-

Technologies Currently Used

A.4. The most common brick production method in use in TVE industry todayutilizes the basic annular kiln (also known as the "Hoffman" type) with natural drying, i.e.,laying cat in stacks in the open air and direct sunlight, of the green bricks. Over 90% of bricksare produced in this manner. About 8% of total production, however, is still by batch process 'nprimitive indigenous kilns. Although some TVE brickworks already use modern tunnel kilns(which are highly efficient but very capital intensive), bricks produced this way account for lessthan 1% of total TVE output. The breakdown of production by kiln type for 1990 is shown inTable 3.

Table 2.3. TVE Brick Output According to K:ln Type (1990)

Kiln Type Output, Percent of TVE Output100 milion PCs

Primitive indigenous kilns 313 7.5Annular kiln

Naural drying; solid bricks 3790 90.8Artificial drying; solid bricks 54 1.3Artificial drying; hollow bricks 13 0.3

Tunnel kilnsArtificial drying; solid bncks 3 0.07Artfficial drg; holow bricks 1 0.03

Total 4174 100.0Source: Ener Efficiency and Pollution Contol bI TVE Industries, Mmistry of Agriculum, Beijing, July 1993

2.5 The process of brick production using the annular kiln can be briefly describedas follows: raw material clay is usually dug from agricultural land and is blended and mixed withwater in an agitator, then passed through rollers to produce a smooth paste. The material isextruded under pressure into blocks; individual bricks are made by wire-cutting the blocks.

2.6 The extruded green bricks must then be dried before firing in the kiln itself Inthe conventional process, the bricks are stacked outside and allowed to dry naturally in the sun.Most plants protect the bricks from bad weather by covering the piles with straw matting. Thetypical Hoffman kiln operation is thus characterised by a relatively large land use, both for theproduction of the main raw material (clay) and for the stacking of green bricks for drying. Atypical brickworks making say 10 million standard bricks per year occupies 30 mu (20,000 MI).

2.7 Following drying, which may take from one to two weeks depending onmoisture content and the weather, the green bricks are stacked in the inlet section of the kiln.Here they are dried firther and preheated by exhaust combustion gases from the section of thekiln being fired. As the firing chambers in the kiln are ignited in turn, the green bricks enter thefiring zone. Firing takes about 7-8 days, after which the bricks are allowed to cool beforeunloading. Cool combustion air is passed over the hot bricks to accelerate the cooling and topreheat the air before it enters the fring chambers.

2.8 The annular kiln operates continuously, with the bricks staying stationary andthe fiing chamber moving around the kiln (in the unmnel kiln previously mentioned, the bricksare stacked onto cars which move through the kin countercurrent to the combustion gases). Theaverage energy consumption of a Hoffman kiln is 1.0 to 1.1 TCE per 10,000 bricks. This heavyuse of cooal makes the TVE brick industry ia major source of C02 and S02 emissions.

-9-

Technical Improvements

2.9 A well designed Hoffman kiln utilizes as much as possible the waste heatobtained from firing the fuel. Improvements that have been made over the last few years includethe incorporation of increasing amounts of coal dust and high carbon fly ash (e.g. from powerplants) in the raw material clay w}ich is then extruded into green bricKs. In some plants, the levelof fuel fired "internally" has reached 100 percent for most practical purposes - that is, theamount of fuel fired from the roof of the standard Hoffman kiln is ai>ost zero. While thisprocedure has been widely adopted by about 8000 plants representing aboxut 20 percent of brickoutput), some plants still have not tried it and could no doubt benefit from the procedure byusing low grade and waste materials as fuels.To encourage wider use of this innovation, theincremental energy provided by internally-fired low-grade fuels are allowed, by SPC regulations,to be excluded in the official accounting of total energy used for production.

2.10 The natural brick drying process is highly vulnerable to the weather. Thedestruction of green bricks during stormy weather can be substantial and conventionalbrickmaking plants are therefore usually only able to work for about 8 months per year in mostregions of China - the rainy regions of the south prevent longer operation of brick plants, whilecold and frosty weather in the north prevents the drying of green bricks also. There is thereforean interest in most regions in the recent application of artificial drying methods to prolong thebrick producing time and to remove the risk of storm damage.

2.11 In the artificial drying process, combustion gases exhausted from the stack arechannelled into a drying section through which the green bricks are passed. Usually acountercurrent arrangement is used to make full use of the available waste heat, with the hotgases being passed into the end of the dryer from which the dried bricks are withdrawn. Thecoldest gases emerge at the end of the dryer into which the fresh green bricks are passed. Toensure adequate drying in a reasonable period, it is usually necessary to fire supplementary fuelin the dryer section or to use steam. The artificial drying process therefore results in an increaseof conventional energy use because of the replacement of solar energy by the extra fuel or steam.

2.12 However, even with some increase in specific energy use, the ni iin advantage ofthe artificial drying system is the increase in productivity that results - the brick plant canproduce for 12 months of the year as green brick drying is no longer subject to weatherconditions. The need for land area for stacking bricks is also essentially eliminated, withsubstantial savings in land cost and the release of the land for productive agricultural use. Brickquality control is improved and the plant is not dependent on the weather to produce high qualitybricks.

2.13 These may take the form of bricks with a wide range of different configurationsof holes, - square, rectangular or round. The void fraction also varies widely although themajority of hollow bricks made in China today have void spaces up to about 25 percent only.The manufacture of hollow bricks is much the same as that of standard solid bricks but there isusually a need for a higher pressure extruder to be used (or vacuum extrusion) to maintain thesharp edges and compacted texture of the brick. The manufacture of hollow bricks brings anumber of advantages:

(1) Less weight of clay for a given volume of brick (savingspercent);

(2) Faster firing and lower energy use per unit of productvolume (saving in drying time typically 15 percent, bakingrate say 10 percent faster, enery saving 20-50 percent);

-10-

(3) Better heat insulation properties of walls made with hollowbricks, and lower thermal mass of the building as a whole(saving up to say 30 percent of space heating energy);

(4) Lower weight of brick per volume of wall built, making iteasier for bricklayers to handle and allowing faster workin the construction industry, and

(5) Lower transport costs per unit volume of building material(saving say 20 percent).

2.i4 Hollow bricks have been used for many years in many countries but the idea isquite new in China. In 1990, only about 1.4 billion hollow bricks were produced out of a total of417.4 billion bricks or 0.3 percent of TVE brick output. In recent experiments in the UK, it wasfound that higher than customary perforation volumes in clay bricks up to 40 percent had littleeffect on brick properties3.

2.15 At present, it is estimated that more than 80 percent of bricks in the UK have aperforation volume of 15 to 25 percent: for structural design purposes, no distinction is madebetween solid bricks and those containing up to 25 percent perforations. Tests showed that it wasfeasible to manufacture bricks in standard format with much higher levels of perforation withoutany major modification to the manufacturing process itself. The requirements of current designcodes relating the strength of bricks to the strength of masonry walls are still met by bricks with40 percent perforations and masonry constructed of 20 and 40 percent perforated bricks showedno practical differences in durability, resistance to rain penetration or fire resistance.

2.16 The tests suggested that significant energy savings could therefore be achievedby increasing the proportion of bricks made with at least 25 percent perforations andsubsequently by manufacturing bricks with perforation levels even higher. It has been estimatedthat the fuel savings for drying and firing are about X/2 percent when an increase in perforationof X percent is made (e.g. an increase from 20 to 40 percent perforation will give fuel savings of10 percent). In addition, increasing the level of perforation reduces the mass of clay materialsprocessed per brick and specific electricity requirements change by about 6.5 kWh per tonne ofoutput in a typical clay preparation plant.

2.17 Finally, it is worth noting that alternatives to the traditional raw materials used inbrickmaking are being investigated. Some minerals such as shales are already being used tomake high quality bricks: shale is quarried from hills around Chengdu, for example, and thus theuse of valuable agricultural land is avoided. Other potential raw materials include industrialwastes of vanous kinds, such as power plant fly ash, colliery waste and gangue from coalwashing. Many of these materials contain carbon and therefore contribute some energy to thekiln when mixed in with the usual raw materials.

2.18 In summary, the main technical characteristics of Chinese brick kilns are asfollows:

3 ETSU Future Practice Report No 27, The Developrnent of Highly Petforated Bricks, Energy TechnologySupport Unit, Harwell, England, March 1992

-11-

Table 2.4. Characteristics of Chinese Brick Kilns

Kiln Type Drying Method Energy Consumed per 10,000 pcsCoal Electricity, Overall,TCE kWh TCE

Indigenous Natual 2.0-2.5 0 2.0-2.5Annular, solid brick Natural 1.10 150-200 1.12Annular

solid bricks Artificial 1.12 300-400 1.15hollow bricks Artificial 0.60 400-500 0.64

Continuous tunnelsolid bricks Artificial 1.30 330-430 1.34hollow bricks Arificial 0.80 450-550 0.85

Source: Refrce I

2.19 Figures for capital investmnent are presented below:

Type of Kiln or Conversion Capital Cost, Yuan per10,000 Mcs. per year

Annular/Hoffian kilnnatural drying, solid bricks 430artificial drying, solid bricks 400artificial drying, hollow bricks 600

Tunnel kilnartificial drying, solid bricks 2000artificial drying, hollow bricks 2100

Conversionnatural drying to artificial/solid bricks. 440natural.dryinglsolid to artificial/hollow 820artificial drying/solid to hollow bricks 60

Source: Reference I

2.20 These figures suggest that replacement of annular (Hoffman) type kilns bymodem tunnel kilns is not likely to happen in China for some time, as potential advantages inlower operating labour and improvements in quality control - factors which make thecontinuous tunnel kiln the dominant equipment used in western brick plants - are not at presentable to offset the large capital cost disadvantage of the tunnel kiln. The added cost of hollowbrick kiln systems compared with the traditional Hoffman kiln making solid bricks can howeverbe overcome by the savings in fuel.

Size and Scale Factors

2.21 As was shown in previous tables, a total of 100,500 TVE plants produced 417.4billicn bricks in 1990, an average of a little over 4 million bricks per plant. Since there arerelatively few plants producing 50 million bricks per year or more, this means there are a largenumber of very small producers.

2.22 In general, new brickworks are unlikely to be built to produce under 10 millionbricks per year and it is thought unlikely that a small kiln could justify the retrofitting of anartificial dryer (see also Case Study B). A regulation in Xinjin County, Sichuan Province,requires new plants to produce at least 10 million bricks per year otherwise permission to buildand operate a new works vill not be given. In addition, the regulation requires plants producing50 million bricks/yr to occupy less than 30 mu (about 2 hectares): this in effect means that such

- 12 -

plants must use artificial drying to comply with the area limitation. There are of course variationsin the regulations from county to county.

Environmental Factors

2.23 The TVE brick industry is the largest emitter of CO2 anongst TVE industries. In1989, 28.7 million tonnes of C02 were discharged, about one-third of the total C02 emissions ofTVE industry. Typical emissions are as follows:

Table 2.5. Pollutant Emissions from Various Brick Kilns

Kiln Type CO2 emission S02 emissiontonnes C110,000 pcs tonnes per O,000 pcs

Indigenous 1.13 0.05Annular/Hoffinan

natual drying, solid br 0.62 0.027artificial drying, solid br. 0.63 0.027artificial drying, hollow br 0.37 0.016

Tunnelartificial drying, solid br. 0.8 0.035artificial drying, hollow br. 0.48 0.02

Souwe: Refeeuce 1

2.24 The extensive use of land for raw materials and for drying green bricks by thenatral method is another important factor. At present, about 1 million mu are occupied: asalready mentioned, a typical brickworks producing 10 million bricks per year using naturaldrying occupies 30 mu (20,000 M2). In rainy and humid areas in the south of China, even largerareas are necessary.

2.25 With respect to the basic technologies used, the emissions of smoke and dust arenormally well controlled, with the possible exception of plants using batch-type indigenous typekilns. These are still used to produce a significant quantity of bricks each year (over 310 millionbricks or 7.5 percent of TVE brick production) and emit smoke at ground level. Nationalstandards are not met and the pollution is serious. The continued operation of such kilns is underpressure from authorities and it is anticipated that most will be phased out within about 7-10years.

The Coke Industry

Introduction

2.26 Coke, the product obtained from destructive distillation of coal, is an importantraw material for the chemical, metallurgical and machinery manufacturing industries. Most ofthe coke used in China is produced by large (greater than 100,000 tonnes/yr) mechanized ovensin state-run enteprises. In 1990, of the total of 73 million tonnes of coke produced in China,about 70% was produced by mechanized ovens. The rest was produced in numerous, small scaleTVE industries mainly by non-mechanized means, 90% of them in just seven provinces. Theproduction growth in these provinces between 1985 to 1989 is shown in Table 2.6.

2.27 There are few TVE-run mechanized coke ovens. They are generally small (about50,000 tpy capacity) and total production in 1989 was less than 0.5 million tonnes. The morenumerous non-mechanized ovens (also called "indigenous") range from primitive batch typekilns to highly improved, modified models that were developed locally. The most widely used

- 13 -

modified klilns today are the so-called PX , JX-1, Type JKH-89 and Type TJ-75 ovens. Asinvestment in the simplest indigenous kilns is estimated to be only 1 yuan per tonne coke,farmers in heavy coal producing provinces entered the cokemaking business in large numbers inthe last decade. By 1990, there were 10,000 TVE enterprises engaged in cokemaking, employingover 150,000 people and generating output value of 3.5 billion yuan. The average coalconsumption for the TVE industry is about 1.9 TCE per tonne of coke produced. Many of theovens still used in TVE cokemaking, including the early generation modified types, are relativelysimple and do not recover the chemicals, tars or gases released in the process. Very roughly, thisrepresents a loss of 3.2 to 4.0 million TCE annually, as well as severe pollution impacts fromgaseous emissions and liquid effluents discharge.

Table 2.6. Coke Production by TVEs (Non-Mechanized Ovens)(10,000 tonnes)

Year 1985 1986 1987 1988 1989National TVETotal 881 1088 1317 1477 1852Provinca Breakdown:Shanxi 192 397 474 652 959Guizhou 131 144 158 151 187Sichuan 113 138 145 156 84Yunnan 99 120 153 147 185Shandong 108 87 94 82 67Henan 119 64 118 78 66Hebei 20 19 51 67 60talof 7provinces 782 969 1193 1333 1681

% ofNational TVE Total 88.8 89.1 90.6 90.3 90.8Source: Statistical Digest of Townhip Eutpries

Technologies Currently Used

2.28 A breakdown of TVE coke output by type of oven in 1990 is as follows:

Table 2.7. TVE Coke Output by Oven Type (1990)dCoke Oven Type Million tonnes Percent

Primitive Indigenous 4.6 24.7PX 11.8 63.4lX-I 1.0 5.4Types89,75 0.7 3.8Small Mechanical 0.5 2.7Large Mechanical 0.0 0.0

Total 18.6 100.0Souce: Refence I

2.29 The most basic type of coking oven still in use today .s the primitive indigenousoven: this consists of little more than a heap of coal which is ignited at the bottom. Coalconsumption is usually in the range 2.0-2.5 TCE per tonne of coke, all the byproducts are burnedand thus lost, and the quality of coke produced is low. The pollution caused by the indigenousovens is serious as the combustion products are released about 2 metres above ground level.Water used for coke quenching can easily permeate through the soil and contaminategroundwater resources. Most provinces officially prohibit the operation of indigenous ovens butthis is apparently not strictly enforced: in 1990, about 4.6 million tonnes of coke (around one

- 14-

quarter of TVE coke production) was still made from indigenous ovens, although the total isexpected to drop sharply in the next 5 years or so.

2.30 Various improved ovens have been developed, the first generation of whichincludes the PX type. This consists of a rectangular pit into which coal is loaded and coveredwith a fire channel made of refractory bricks. A tar ditch is built in the centre of the bottom ofthe oven. The bricks are covered with coal ashes and small chimneys - typically 20, each about0.5 meters high - are installed along the centre of the top. The coal is ignited using gas fromadjacent ovens. A mixture of gas and tars is collected through the tar ditch: about 4-5 kgs of tarper tonne of coke are collected and the gas is burned off (unless required to ignite other ovens).Coal consumption amounts to 1.56 TCE per t coke. Coke quality is somewhat improved (someup to first grade metallurgical grade). However, combustion products are released at ground leveland this causes serious pollution.

2.31 Representative of the second generation of improved oven is the JX-1 type oven.This oven has modified gas passages in which gases and tars are burned, leading to shortercoking times and higher coke quality. The byproducts are more completely burned before releaseto atmosphere through a 30-40 meter stack. Coal consumption is reduced to about 1.43 TCE per tcoke, which is only 20 percent greater than the figure for large scale mechanical ovens (1.2 TCEper t coke). Although pollution is reduced, the top of the JX-I oven is still covered by coal ashesand combustion products can leak through, in addition to which a great deal of dust is releasedduring the coke quenching stage. As for the PX oven, water and chemicals can escape into theground from the tar ditch at the bottom of the oven.

2.32 The third generation of improved ovens includes the Type JKH-89 and the TypeTJ-75 ovens. The T3-75 oven is built with a brick roof and has modified firing channels at thebottom of the oven which result in faster heating of coal, shorter time for coke production andhigher coke quality. Coal consumption is in the range 1.35-1.40 TCE coal per t coke but nobyproducts are recovered: all are burned in the gas passages and combustion gases aredischarged through a 45 meter stack. Pollutant emissions are greatly reduced and the risk ofgroundwater contamination is minimal.