report no. 3187-ma recop malaysia's file copy...

TRANSCRIPT

Report No. 3187-MA RECOP

Malaysia's Manufacturing Sector: FILE COPYDevelopment Issues and Policy Options(In Three Volumes)

Volume II: The Main ReportApril 9, 1981

Projects DepartmentEast Asia and Pacific Regional Office

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipients

only in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit - Ringgit (M$)

1 M$ = US$0.45

1 US$ = M$ 2.20

ABBREVIATIONS

BNM Bank Negara MalaysiaDRC Domestic Resource CostEPRs Effective Protection RatesEPU Economic Planning UnitFFMP Fourth Malaysia PlanFTZs : Free Trade ZonesGOM : Government of MalaysiaICA : Investment Coordinating ActIEs Industrial EstatesIIP Index of Industrial ProductionLIs Locational IncentivesLUR : Labor Utilization ReliefMIDA : Malaysian Industrial Development AuthorityMIDF : Malaysian Industrial Development Finance Co.MIS Monthly Industrial StatisticsMTI Ministry of Trade and IndustryNEP New Economic PolicyPS Pioneer StatusQLFS Quarterly Labor Force SurveySACT Special Advisory Committee on TariffsSEDCs: State Economic Development CorporationsSMIs : Small and Medium IndustriesTAB : Tariff Advisory BoardTMP Third Malaysia Plan

FISCAL YEAR

January 1 - December 31

FOR OFFICIAL USE ONLY

MALAYSIA-S MANUFACTURING SECTOR:

DEVELOPMENT ISSUES AND POLICY OPTIONS

Volume II: The Main Report

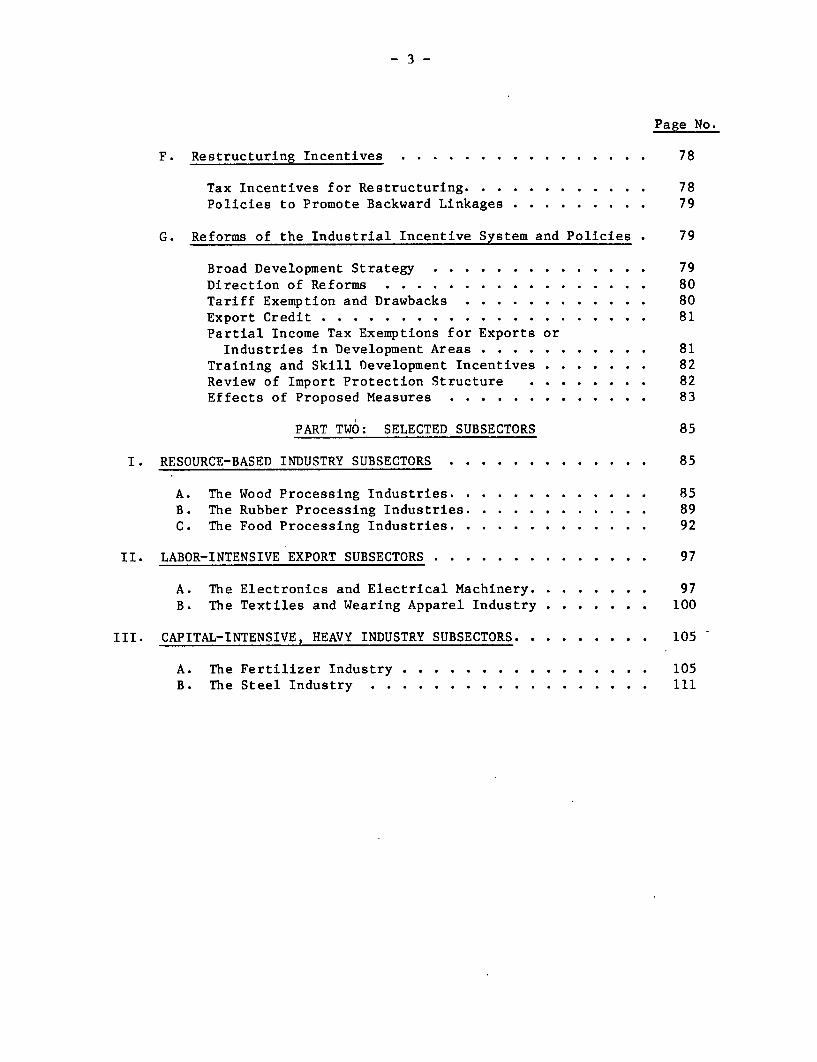

Table of Contents

Page No.

PREFACE . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4-5

BASIC DATA .. 6-7

PART ONE: THE GENERAL MANUFACTIJRING SECTOR 8

I. INTRODUCTION AND OVERVIEW OF GROWTH PERFORMANCE . . . . . . . 8

A. Introduction .... . . . . . . . . . . . . . . . . . . 8

B. Growth and Structural Changes in Manufacturing .10

Historical Pespective and Growth Performance . . . . . 10

Structural Changes in the Sector . . . . . . . . . . . 13

II. POPULATION, LABOR FORCE AND MANUFACTURING EMPLOYMENT . . . . 24

Population and Labor Force . . . . . . . . . . . . . . 24

Employment in the Manufacturing Sector . . . . . . . . 24

Trends in Subsectoral Employment . . . . . . . . . . . 27

Ethnic Composition of the Manufacturing Labor Force . . 28

Trends in Wages and Earnings . . . . . . . . . . . . . 30

Trends in Labor Productivity and Capital Intensity . . 31

Labor Market Segmentation . . . . . . . . . . . . . . 32

Skill Shortages and Incentive System . . . . . . . . . 33

Concluding Remarks .. 35

III. MANUFACTURED EXPORTS .36

Growth Performance . . . . . . . . . . . . . . . . . . 36

Export Markets .. 38

Achievement of Export Growth . . . . . . . . . . . . . 40

Manufacturing Sector Export Prospects . . . . . . . . . 42

IV. INVESTMENT IN THE MANUFACTURING SECTOR . . . . . . . . . . . 47

Introduction .. 47

Overview of Investment in Malaysia . . . . . . . . . . 48

-2-

Page No.

Investment in Manufacturing . . . . . . . . . . . . . 49Investment Profiles and Problems of Estimation . . . 54

V. THE ROLE OF PUBLIC ENTERPRISE IN MANUFACTURING . . . . . . . 58

Introduction .... . . . . . . . . . . . . . . . . . . . 58Performance and Achievements . . . . . . . . . . . . . . . 59The Issue of Objectives and the Role of PublicManufacturing Enterprise ... . . . . . . . . . . . . . 59

Relationship to Private Sector: Price and IncentivesFramework . . . . . . . . ... . . . . . . . . . . . . . . 60

Issues in Financial Administration . . . . . . . . . . . . 62Ensuring Proper Control and Accountability . . . . . . . . . 62The Key Issue . . . . . . . . . . . . . . . . . . . . . . . 63Guidelines for the Future . . . . . . . . . . . . . ... . 64

VI. INCENTIVE SYSTEM AND POLICIES ... . . ..... . . . . . . 66

A. Introduction .... . . . . . . . . . . . . . . . . . . 66

B. Tariff Protection and Import Restriction . . . . . . . . 67

Case-by-Case System ... . . . . . . . . . . . . . . . 67Subsector Development Strategies . . . . . . . . . . . 68Tariff Exemptions ... . . . . . . . . . . . . . . . . 69Infant Industry Protection . . . . . . . . . . . . . . 70

C. Export Incentives .... . . . . . . . . . . . . . . . . 71

Exchange Rate .... . . . . . . . . . . . . . . . . . 71Trade Bias and Nonfree Trade Zone Exports . . . . . . 71Preferential Export Loans . . . . . . . . . . . . . . . 73Export Allowance . . . . . . . . . . . . . . . . . . . 73Streamlining of Export Incentives Administration . . 74

D. Investment Incentives ... . . . . . . . . . . . . . . . 75

Case-by-Case System ... . . . . . . . . . . . . . . . 75Pioneer Status (PS) Incentives . . . . . . . . . . . . 75Labor Utilization Relief (LUR) . . . . . . . . . . . . 76

E. Industrial Dispersion Incentives . . . . . . . . . . . . 77

Locational Incentives (LIs) . . . . . . . . . . . . . . 77Industrial Estates (IEs) . . . . . . . . . . . . . . . 77

-3-

Page No.

F. Restructuring Incentives ... . . . . . . . . . . . . . 78

Tax Incentives for Restructuring . . . . . . . . . . . . 78Policies to Promote Backward Linkages . . . . . . . . . 79

G. Reforms of the Industrial Incentive System and Policies . 79

Broad Development Strategy . . . . . . . . . . . . . . 79Direction of Reforms .80Tariff Exemption and Drawbacks . . . . . . . . . . . . 80Export Credit .81Partial Income Tax Exemptions for Exports or

Industries in Development Areas . . . . . . . . . . . 81Training and Skill Development Incentives . . . . . . . 82Review of Import Protection Structure . . . . . . . . 82Effects of Proposed Measures . . . . . . . . . . . . . 83

PART TWO: SELECTED SUBSECTORS 85

I. RESOURCE-BASED INDUSTRY SUBSECTORS . . . . . . . . . . . . . 85

A. The Wood Processing Industries. . . . . . . . . . . . . 85B. The Rubber Processing Industries. . . . . . . . . . . . 89C. The Food Processing Industries. . . . . . . . . . . . . 92

II. LABOR-INTENSIVE EXPORT SUBSECTORS . . . . . . . . . . . . . . 97

A. The Electronics and Electrical Machinery. . . . . . . . 97B. The Textiles and Wearing Apparel Industry . . . . . . . 100

III. CAPITAL-INTENSIVE, HEAVY INDUSTRY SUBSECTORS. . . . . . . . . 105

A. The Fertilizer Industry .105B. The Steel Industry .................. 111

- 4 -

PREFACE

This report presents an overview of the findings of an Industrial

Sector Mission which visited Malaysia from February 18 to March 11, 1980.

Two basic objectives of the mission were: (a) to review the past performance

and assess the growth potential of the manufacturing sector in terms of its

likely contribution to increased output, employment and exports; and (b) to

highlight, where appropriate, policies and incentives that will help to

ensure that Malaysia's manufacturing potential is fully exploited and the

benefits to the national economy maximized.

The present report is intended as a contribution to the preparation

of the Fourth Malaysia Plan (FMP: 1981-1985). From the very start the work of

the mission was seen as a cooperative effort of the Government and the Bank.

Recognizing the collaborative nature of the task, the Economic Planning Unit

(EPU) established a counterpart steering committee, drawing its members from

the Ministry of Trade and Industry, Treasury, Bank Negara Malaysia, Ministry

of Labor, Ministry of Public Enterprises and the Department of Statistics.

This committee contributed substantially to the success of the mission both

during the formulation of the terms of reference for the study and during the

field visit of the mission. Given the tight time schedule set for the pre-

paration of the FMP, the mission focused mainly on highlighting the

development issues and the changing role of incentives and policies at this

stage of the manufacturing sector in Malaysia.

This mission consisted of the following members:

Fateh M. Chaudhri - Chief of Mission

Keith Marsden - Employment Policies & Incentives

Ozay Mehmet (Consultant) - Labor Market Analysis

Hugo Molina (UNIDO) - Light Industry Subsectors

Vinod Prakash - Sector Performance and Prospects

Yung Rhee - Incentives and Policy Framework

Bertil Walstedt (Consultant) - Public Enterprises and Heavy Industry

In the processing of this report and in reviewing some of the working papers,

Mr. S. Talbot gave substantial support to the mission. Mr. F.M. Iqbal,

Senior Field Advisor, UNIDO, also provided the mission with notes on the

Institutional Framework for Industrial Development in Malaysia.

A preliminary draft of the report was submitted to EPU in July 1980

and technical discussions on that draft took place with government officials

in Kuala Lumpur during August 23-September 1, 198U. Follow-up policy level

discussions were conducted by a Bank mission consisting of Messrs. Jaycox,

Gould, Tsantis and Chaudhri in January-February 1981. This report reflects

those discussions.

This report consists of three volumes:

Volume I : Summary-Report and Recommendations

Volume II : The Mlain Report

Volume III: Annex and Statistical Tables

The following background working papers prepared in connectionwith the report have been issued individually in white cover and areavailable upon request from the East Asia and Pacific Projects Department.

1. A Study of Growth Performance and Outlook of the ManufacturingSector in Malaysia.

2. Incentive Systems and Policies for the Manufacturing Industriesin Malaysia.

-6- Page 1 of 2 pages

MALAYSIA - BASIC DATA - MANUFACTURIG4C SECTOR

M$ billion at 1970 prices Anntual growth rates (%)1971 1973 1975 1978 1980 1961-65 1965-70 1971-75 1975-80

GDP 13.0 15.9 17.4 22.3 25.7 5.6 5.5 7.5 8.1Manufacturing 1.9 2.5 2.9 4.3 5.3 12.1 9.9 11.3 13.0% of GOP 14.3 15.8 16.4 19.1 20.5

Manufacturing Value Added (current prices) Structure Annual Contribution(VA = Value added, GO = Gross Output, of value growth rates (1) to growth (%)GO* = Gross Output approximated by Sales added (%) 1968-73 1968-73 1973-78 1968-73 1973-78

of Ilanufactured Own Products) 1968 1973 GO VA GO* GO GO*

31 Food, beverages & tobacco products 28.0 23.9 15.9 17.8 13.8 27.3 18.332 Textiles, clothing & footwear 3.2 6.1 30.2 39.0 26.7 6.7 10.333 Wood & wood products 11.8 13.9 23.7 26.0 12.4 12.0 2.034 Paper, paper products, printing &

puhlishing 6.7 5.7 18.3 17.7 14.2 3.8 2.6

35 Chemicals, petroleum, rubber & coalproducts 28.1 21.2 15.2 13.6 17.2 21.8 26.0

36 Nonmetallic mineral products 7.0 5.3 14.8 14.7 20.0 2.7 2.937 Basic metal products 2.5 3.7 31.0 32.0 23.0 4.1 2.038 Fabricated metals, machinery, etc. 12.4 19.8 30.2 34.0 31.6 20.1 25.839 Miscellaneous industries 1.5 10.1

Manufacturing Total 100.0 100.0 19.4 21.6 20.1 100.0 100.0

Monthly indus- AnnualCensus trial statistics growth rates (%)

Mlanufacturing Employment ('000 no.) 1968 1973 1973 1978 1968-73 1973-78

31 Food, beverages & tobacco products 26.7 46.2 23.9 31.3 11.6 5.532 Textiles, clothing & footwear 8.8 34.9 29.0 53.1 32.0 12.933 Wood & wood products 21.9 44.9 15.0 17.9 15.4 3.634 Paper, paper products, printing &

publishing 10.9 17.4 11.6 16.1 9.8 6.8

35 Chemicals, petroleum, rubber & coalproducts 25.8 42.7 35.9 49.4 10.6 6.6

36 Nonmetallic mineral products 7.3 13.0 3.3 5.5 12.2 10.837 Basic metal products 3.1 6.8 2.7 4.0 17.0 8.238 Fabricated metals, machinery, etc. 20.6 65.9 40.0 85.9 26.0 16.5

Manufacturing Total 125.5 273.5 181.2 240.8 16.9 9.9

JuneManufacturing Production Index (1968=100) Weight 1969 1971 1973 1975 1977 1978 1979

311/2 Food products 16.5 109 112 130 136 162 172 172321 Textiles 2.2 112 122 197 214 314 356 395331 Wood & wood products 11.9 108 140 203 190 286 274 303351/2 Indtustrial chemicals & products 9.6 112 122 166 155. 180 204 235

353/4 Refined petroleum & products 5.0 100 92 99 118 169 189 19935591 Rubber remilled & latex processed 8.4 107 107 98 82 83 82 70

Other rubber products 6.4 109 132 166 164 196 193 198369 Nonmetallic mineral products 7.6 112 119 147 161 196 246 261

37 Basic metal products 2.7 144 166 226 228 284 318 318381 Fabricated metal products 4.2 107 141 243 186 233 292 311383 Electrical machinery, etc. 2.0 129 189 201 287 432 466 468384 Transport equipment 2.3 210 282 393 412 481 573 f 633

Manufacturing Total 100.0 116 138 187 216 284 312 337

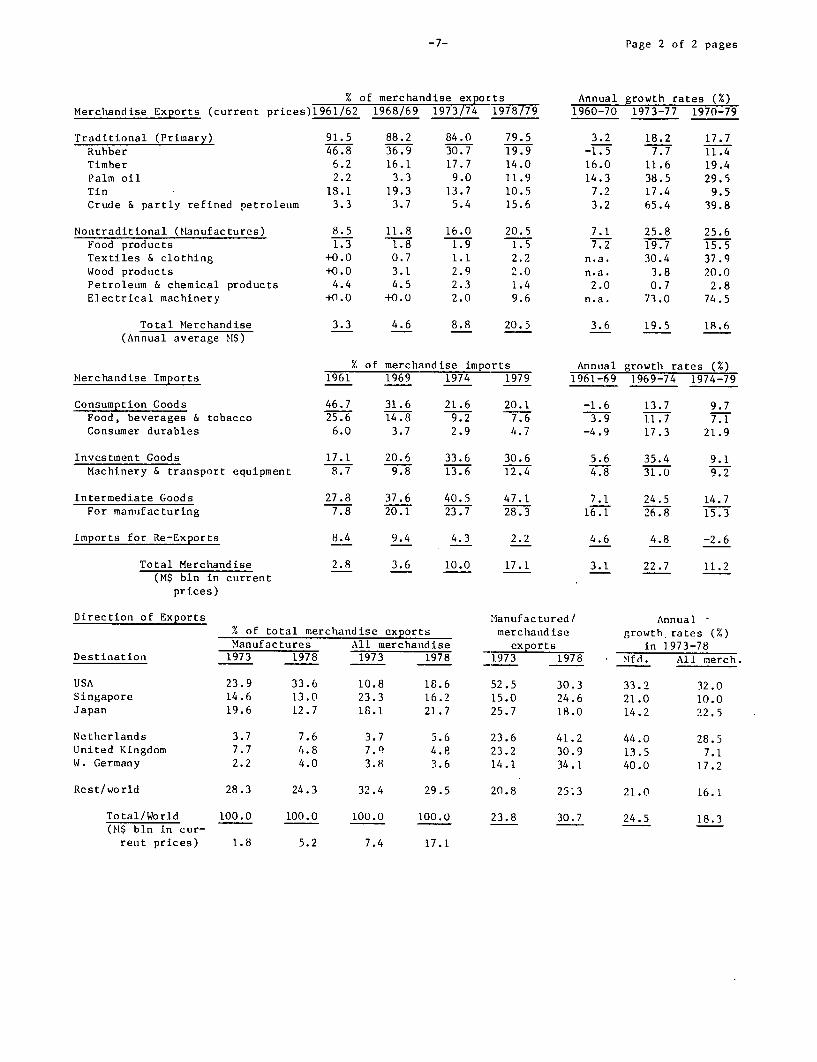

-7- Page 2 of 2 pages

% of merchandise exports Annual growth rates (%)Merchandise Exports (current prices)1961/62 1968/69 1973/74 1978/79 1960-70 1973-77 1970-79

Traditional (Primary) 91.5 88.2 84.0 79.5 3.2 18.2 17.7Rubber 46.8 36.9 30.7 19.9 -1.5 7.7 11.4Timber 6.2 16.1 17.7 14.0 16.0 11.6 19.4Palm oil 2.2 3.3 9.0 11.9 14.3 38.5 29.5Tin 18.1 19.3 13.7 10.5 7.2 17.4 9.5Crude & partly refined petroletim 3.3 3.7 5.4 15.6 3.2 65.4 39.8

Nontraditional (Manufactures) 8.5 11.8 16.0 20.5 7.1 25.8 25.6Food products 1.3 1.8 1.9 1.5 7.2 19.7 15.5Textiles & clothing +0.0 0.7 1.1 2.2 n.a. 30.4 37.9Wood products +0.0 3.1 2.9 2.0 n.a. 3.8 20.0Petroleum & chemical products 4.4 4.5 2.3 1.4 2.0 0.7 2.8Electrical machinery +0.0 +0.0 2.0 9.6 n.a. 73.0 74.5

Total Merchandise 3.3 4.6 8.8 20.5 3.6 19.5 18.6(Annual average M$)

X of merchandise imports Annual growth rates (%)Merchandise Imports 1961 1969 1974 1979 1961-69 1969-74 1974-79

Consumption Goods 46.7 31.6 21.6 20.1 -1.6 13.7 9.7Food, beverages & tobacco 25.6 14.8 9.2 7.6 3.9 11.7 7.1Consumer durables 6.0 3.7 2.9 4.7 -4.9 17.3 21.9

Investment Goods 17.1 20.6 33.6 30.6 5.6 35.4 9.1Machinery & transport equipment 8.7 9.8 13.6 12.4 4.8 31.0 9.2

Intermediate Goods 27.8 37.6 40.5 47.1 7.1 24.5 14.7For manufacturing 7.8 20.1 23.7 28.3 16.1 26.8 15.3

Imports for Re-Exports 8.4 9.4 4.3 2.2 4.6 4.8 -2.6

Total Merchandise 2.8 3.6 10.0 17.1 3.1 22.7 11.2(M$ bln in current

prices)

Direction of Exports Manufactured/ Annual -% of total merchandise exports merchandise growth rates (X)Manufactures All merchandise exports in ]973-78

Destination 1973 1978 1973 1978 1973 1978 Mffd. All merch.

USA 23.9 33.6 10.8 18.6 52.5 30.3 33.2 32.0Singapore 14.6 13.0 23.3 16.2 15.0 24.6 21.0 10.0Japan 19.6 12.7 18.1 21.7 25.7 18.0 14.2 22.5

Netherlands 3.7 7.6 3.7 5.6 23.6 41.2 44.0 28.5United Kingdom 7.7 4.8 7." 4.8 23.2 30.9 13.5 7.1W. Germany 2.2 4.0 3.8 3.6 14.1 34.1 40.0 17.2

Rest/world 28.3 24.3 32.4 29.5 20.8 25:3 21.0 16.1

Total/World 100.0 100.0 100.0 100.0 23.8 30.7 24.5 18.3(M$ bln in cur-

rent prices) 1.8 5.2 7.4 17.1

-8-

PART ONE: THE GENERAL MANUFACTURING SECTOR

I. INTRODUCTION AND OVERVIEW OF GROWTH PERFORMANCE

A. Introduction

1.01 The Government considers the eradication of poverty and

restructuring of employment and ownership as key factors in maintaining the

delicate balance of Malaysia's pluralistic, democratic society. With an

estimated annual growth of GDP around 7.5% during the last decade, spear-

headed by manufacturing value added growing at 12-13%, progress toward the

objectives of the New Economic Policy (NEP) has been substantial. The

continued higher growth performance of the manufacturing sector is indeed

crucial to maintain the progress already achieved. In order to assess the

current situation and prospects of the sector, the mission first reviewed

its performance over the past two decades. This is presented in Section B

of this Chapter. Besides reviewing the growth performance, structural

changes and operational characteristics, this section also discusses the

severe data deficiences in current manufacturing statistics./l

1.02 Since the continuation of a rapid increase in productive employ-

ment in the manufacturing sector is critical to attaining the NEP objective,

the mission paid special attention (Chapter II) to reviewing overall

employment trends during the last few years, the structure of employment at

end-1979, the nature of labor market segmentation and trends of average

earnings in manufacturing. As with output statistics, the mission felt that

a summary critique of employment data was necessary in view of the Govern-

ment s heavy reliance on the employment-generating capacity of the manufac-

turing sector and of its importance in monitoring the impact of employment

and skill development policies.

1.03 While the domestic market will continue to be a substantial factor

in industrial expansion, a relatively small domestic market cannot sustain the

continued rapid expansion of the manufacturing sector necessary to generate

the desired number of productive jobs in the modern sector. Therefore, a

review of the growth in manufactured exports, sources of such growth and a

discussion of export markets has been included in Chapter III. This section

concludes with a brief discussion of the key issues and manufactured export

prospects.

/1 See Annex I, Volume III, on Inadequacy of the Manufacturing Data Base.

-9-

1.04 The level, structure and trend in manufacturing sector investmentare crucial to assessing the current situation and prospects of this sector,but again severe data deficiencies defy a thorough and critical analysis.The mission had to rely on several indirect estimates (presented in ChapterIV) to develop an overview of investment in the manufacturing sector. Thissection ends with a discussion of the main conclusions and key issues inthis area.

1.05 In the course of the last decade a public manufacturing enterprisesector has developed in Malaysia. In the last few years it has grown veryrapidly largely due to the desire to achieve substantial restructuring ofindustrial ownerships and employment by 1990. Chapter V addresses some keyquestions in this area: How rapidly and in what directions has the publicmanufacturing sector grown? What has been the performance of publicenterprises in terms of profitablility and investment? What particularissues have surfaced in terms of its relation to the private sector? Whatproblems of administration, coordination, supervision, control andaccountability have to be reviewed before assessing the future of the publicmanufacturing sector in Malaysia? What future direction should the publicmanufacturing sector take?

1.06 Industrial development strategy - the incentives system and policyframework - is the key instrument in influencing the rate of growth, pros-pects and guiding the directions of the manufacturing sector. It is apowerful instrument which encourages or discourages certain activities inthe manufacturing sector, determines its orientation to domestic or exportmarkets, affects the locational choices made by industrial investors and ofcourse it influences the overall efficiency of the sector. A major part ofthe mission's work was therefore geared to an assessment of the existingimport tariff protection, export, investment and locational incentives, thebearing of the incentive system on the restructuring objectives anddiscussion of key issues in each of these areas. The existing incentivessystem and policies have made a substantial contribution to the growth of themanufacturing sector but its general efficiency remains an open question.The mission feels, therefore, that for continued growth of the sector inchanged and more difficult international circumstances, a reorientation inthe incentives framework is now highly desirable. The whole of Chapter VIis devoted to a discussion of possible adjustments in the incentives andpolicy framework which, in the mission's judgement, would enhance the exportperformance and its linkages to the domestic economy, the more effective useof labor and the regional dispersion of industry, all of which correspond tothe Government's development objectives.

-10-

1.07 Even though the time framework for the preparation of this reportwas extremely short, the mission also felt it necessary to study several keyindustries because of their importance in furthering manufacturing growth.We selected three resource-based industries (the wood, rubber and foodprocessing industries), two labor-intensive, export-oriented subsectors (the

electronics and textiles industries) and two capital-intensive, heavyindustries (the fertilizer and steel production subsectors) for briefsubsector-specific analyses. In these reviews, presented in Part Two of thereport, the mission sought to examine the growth performance, discuss thenature of problems and constraints and assess the growth potential of therespective sectors. This part also discusses certain measures which shouldimpart greater efficiency and competitiveness to activities in these various

industries, leading to the creation of more productive jobs and increasedefficiency of the sector in the medium and long-run.

1.08 The assessment of current and proposed policies has to be seen

against the perspective of growth performance and structural changes inmanufacturing over the last several years. The following section of thisintroductory chapter therefore provides an overview of growth performanceand discusses the strengths and weaknesses of the sector which emerge fromthis analysis.

B. Growth and Structural Changes in Manufacturing

Historical Perspective and Growth Performance

1.09 Over the past two decades, the industrial sector has received thepolicymakers special attention. As early as 1958, the Pioneer IndustrialOrdinance was introduced, to be replaced a decade later by the InvestmentIncentives Act. By 1970, the New Economic Policy (NEP) added a freshdimension to the industrialization process in Malaysia./l The MalaysianIndustrial Development Finance (MIDF) Institute was set up in 1960 and the

Malaysian Industrial Development Authority (MIDA) was established in 1965as the key industrial sector institutions.

1.10 In the beginning the policymakers interest was to use the process

of industrialization as a vehicle to diversify the country's excessive

reliance on rubber and tin and to generate additional productive employment.Industrial growth depended primarily on the initiative of the private sectorwith the Government fostering a conducive environment by providinginfrastructural facilities and incentives for investment. More recently,industrialization has become an important vehicle to achieve restructuringof employment and ownership of assets as well as alleviation of poverty.Thus, the Government began to participate more actively and directly in the

/1 The main objectives of the NEP are: the eradication of absolutepoverty and the restructuring of society to achieve racial balance.

-11-

overall development process by investing in industries. In 1975 theIndustrial Coordination Act was introduced for accelerating the pace ofindustrialization and achieving the NEP objectives. Pragmatic changes inthe role of industrial sector policies, reinforced by sustained politicaland price stability, bouyant balance of payments, favorable investmentclimate and natural resources, together with a fairly well-educated laborforce have helped Malaysia achieve substantial industrial growth over thelast two decades. Table 1 illustrates the annual growth rates andcontribution to GDP of the various sectors.

1.11 Manufacturing has been by far the fastest growing economicactivity on a sustained basis - almost twice the 6% rate of average annualgrowth of GDP in the 1960s and one and a half times the high 7.5% p.a. GDPgrowth in the 1970s. The contribution of manufacturing to the growth inGDP has increased from 20% to 26% from early 1960s to late 1970s. The shareof manufacturing in GDP rose from about 9% in 1960 to about 20% two decadeslater, compensating for the declining share of the primary sectors (agricul-ture, livestock, fisheries, etc.). The great emphasis given to the role ofthe manufacturing sector in the Malaysian economy shows up in anotherstudy /1 which compares the "observed" ratio of value added in asector to GDP in Malaysia with the typical 'predicted' pattern obtained froma hypothetical country of Malaysia's population size, per capita income andexport orientation (measured by the ratio of primary exports and manufac-tured exports to GNP). During the 1960s the observed share of manufacturingin total GDP was 4-5 percentage points below the predicted share; by 1970,the gap had narrowed and finally closed in 1975, before reversing itself by1980 when the observed share was about 20% compared with the predicted 18%.

1.12 What have been the sources of this substantial growth of themanufacturing sector in the past? The available evidence shows that thegrowth in domestic demand and import substitution were the dominant directsources (about 90%) of industrial development during the 1960s. By the late1960s and early 1970s, the scope of 'easy' or first stage of importsubstitution was substantially reduced. Further, beginning around themid-1960s, manufactured exports (mainly the resource-based processed goods)gradually became an important direct source of growth accounting for about afifth of the sector growth./2 In more recent years, 1974-78, manufacturedexports have maintained their contribution to growth at about 20% andadditional import substitution appears to have contributed 12-13% to growthin these years.

/1 The ongoing World Bank Research Project No. 671-08 "Pattern ofIndustrial Development".

/2 The contribution of export expansion is overestimated because PeninsularMalaysia's foreign trade statistics also include trade with Sabah andSarawak (almost 25% in 1973).

-12-

Table 1: MALAYSIA: GROWTH IN GDP BY KIND OF ECONOMICACTIVITY, 1961-1980 AT CONSTANT PRICES /a

Annual growth rates (%) Contributions of growth (x)1961- 1965- 1971- 1975- 1961- 1965- 1971- 1975-

65 70 75 80 65 70 75 80

Kind of EconomicActivity

Agriculture, live-stock, forestry,& fishing 3.3 6.9 5.7 4.5 17.9 40.2 22.3 12.8

Mining & quarrying 2.8 1.1 -1.3 10.2 4.2 1.6 -1.0 5.3

Manufacturing 12.1 9.9 11.3 13.0 19.5 20.4 22.8 25.8

Construction 11.5 4.1 4.8 12.0 8.5 3.0 2.6 2.1

Services 5.8 4.4 8.6 7.7 49.9 34.8 53.3 54.0

GDP 5.6 5.5 7.5 8.1 100.0 100.0 100.0 100.0

Per capita income 2.7 2.6 4.8 5.4

/a Estimates of growth rates or contributions to growth of the manufactur-ing sector suffer from severe deficiencies in the basic statistics aswell as in the methodology used in estimating them. In brief, thenational accounts framework was changed in the early 1970s, and compar-able time-series over the 1960s are not available. Even for the 1970sreasonably reliable estimates are available only for 1971 and 1973. Theestimates for 1974 to 1977 are still preliminary, because they are basedon the short-cut methods necessitated by the availability of very lim-ited information. Malaysia has adopted an integrated and comprehensiveapproach to estimate its national accounts, in accordance with theUnited Nations: A System of National Accounts Rev. 3 (SNA 3). Althoughthis sophisticated approach leads to very detailed, accurate and usefulaccounts, the whole exercise takes an enormous time (say, four to fiveyears), and by the time the sectoral and national accounts are final-ized, they are out of date. For a further discussion of the extremelyserious data deficiencies and means of alleviating them, see Annex I.

Source: Annex Table 1.1

-13-

Structural Changes in the Sector /1

The Period 1959 to 1973

1.13 The growth of the overall manufacturing sector has been uneven but

fairly substantial. During the 15-year period, 1959-73, total the number of

establishments more than doubled, the number of paid full-time employeesincreased from 57,400 to 268,200 (about four times), gross value added

jumped by about six times and gross output four-five times in real terms.The continuously rising ratio of value added to gross output during this

period perhaps indicates Malaysia's success in increasing the domestic value

added content of its manufacturing gross output.

1.14 During 1963-68 and 1968-73 there was remarkable acceleration of

annual growth rates compared to the 1959-63 period. Gross value added inreal terms increased at 14% and 18% respectively as against 8-9% p.a.increase during 1959-63; gross output in real terms increased at 11% and 16%

annual rates compared to 6% in the earlier period. Full-time employmentcreation in manufacturing progressed at a much faster rate (13% p.a.) during

1963-73 compared to its increase during the previous ten years. With

virtually no increases during 1959-63, labor productivity in real termsincreased at an annual rate of about 3% during the subsequent ten years./2It is also important to mention here that manufactured exports in the latter

period were rising at a much faster rate than the previous two periodsmentioned above.

/1 The available data on manufacturing sector activities suffer from severe

deficiencies. The 1959 census, the first, is known to have incomplete

coverage. Also the 1959, 1963 and 1968 censuses used the two industrialclassifications that have been replaced by the new classification(called "MIS-1972, updated") since the 1973 census. The mission had to

convert the old classification into the new one for comparativeanalysis. Despite the utmost care it might have resulted in somemismatching. Beyond 1973, the data are highly aggregative and subject

to further qualifications. The more detailed analysis of the 1959-73period is therefore separated from the analysis of the more recent

years, 1974-78.

/2 The deflator used in converting the nominal data into real values is the

official Consumer Price Index.

Employment

1.15 At a somewhat disaggregated level, the two top most contributors to

direct employment creation were the wood processing and electrical machineryindustries - each providing 25,000-28,000 jobs during the decade 1963-73

(when total increase in employment amounted to about 190,000 persons). The

next in line were food products and textiles, each contributing about 21,000

jobs. Thus, these four subsectors together were responsible for almost halfof the total jobs created in the entire manufacturing sector during 1963-73.Other leading industrial groups in generating direct manufacturing employ-

ment were fabricated metal products, followed by wearing apparel (excludingfootwear), rubber products, machinery (except electrical and transport) and

plastic products. These five groups together generated the majority of jobscreated in the entire manufacturing sector. (For greatei details, seeChapter II, paras. 2.01-3.06 below.)

Labor Productivity

1.16 The gains in labor productivity and earnings differed substan-tially among various subsectors during the 1963-73 period. The beverageindustry had the highest growth both in labor productivity and earnings:/113.3% and 6.2% p.a., respectively (in nominal terms). Next in line was thetobacco industry with gains of 9.9% and 4.5% respectively, whereas theaverage annual gains for the whole manufacturing sector were 5.5% and 1.6%

respectively. The industries lagging most in terms of productivity gainswere wearing apparel, electrical machinery and paper and paper products. Aninteresting feature of the gains in labor productivity is that the three

leading contributors to employment creation viz. wood and wood products/foodproducts and textiles, also had substantial gains in labor productivity from

about 5-8% p.a. (more details are provided in Chapter II, paras. 6.01-6.04below).

Labor Earnings Per Worker

1.17 On the earnings side, with the exception of the footwear industry,growth of labor earnings per worker was invariably below that of laborproductivity. This extraordinary phenomenon in the footwear industry mightbe a result of the consolidation of the industry that led to the decline inthe number of establishments (from 189 in 1963 to 169 in 1973) and the

creation of a fivefold increase in the number of paid full-time employees(from 300 to 1,600) together with the pressure from export markets for the

/1 Labor earnings include payments of bonuses, cash allowances, employeescontribution to E.P.F. etc., but exclude overtime payment, payment inkind to paid employees and employers contribution to provident funds andsocial security schemes.

-15-

supply of high quality products which in turn needed better qualified personscapable of earning higher wages. The most conspicuous industriesexperiencing a substantial fall in average labor earnings per worker wereprecision instruments, electronics and electrical machinery, glass and glassproducts and tobacco products. Out of these four industries, only the caseof electronics and electrical machinery appears to be well-recognized: thegrowth of this industry has been dominated by the enormous expansion ofelectronic assembly and subassembly which needed unskilled (mostly urban,female) labor that was both abundant and cheap. (For further details, seeChapter II, paras. 5.01-5.05 below.)

Value Added

1.18 Total value added in manufacturing registered an almost sixfoldincrease during the decade, 1963-1973. In current prices, the gross valueadded in electrical machinery, textiles and wearing apparel (exceptfootwear) rose most rapidly: 40, 25 and 15-fold respectively in the courseof the decade. The growth of value added in wood and wood products as wellas in fabricated metal products was as much as the overall sector aroundfive to six times.

1.19 The three leading contributors to the overall growth of themanufacturing sector, however, were food products, wood and wood productsand electrical machinery, which together shared more than 40% of theincremental value added in the sector. Next in line were rubber products,tobacco products and textiles which accounted for another 20% of thesectoral value added.

Structural Shifts and Changes in Product-Mix

1.20 The mission analyzed the changes in product-mix during 1963-73 byregrouping the 27 industrial groups into two types: Consumer- andproducer-oriented industries, which were further divided into twocategories: consumer durables and nondurables, and intermediate and capitalgoods respectively. During 1963-68, the per annum growth rates of consumerdurable, nondurable and intermediate goods was about the same (17% incurrent prices) with capital goods lagging behind, but still growing at animpressive rate of 14% p.a. During the second half of the period consumerdurables were increasing at a very high rate of 34% p.a. compared to about20% annual growth registered in consumer nondurable and intermediate goodsand 28% in capital goods. But it is important to look at the contributionthat these various categories have made to increased overall value addedbecause of their different initial bases. In this respect. the contributionof nondurable consumer goods and intermediate goods declined from 37.3% to33.7% and from 49.9% to 41.1% respectively from the 1963-68 period to the1968-73 period. Over this decade the contribution of durable consumer goodsincreased from 10.0% to 20.4% and that of capital goods from 2.8% to 4.8%.

-16-

The smallness of the capital goods' contribution is as conspicuous as thesubstantial contribution made by intermediate products. Throughout theperiod, the production of consumer durable and intermediate productscontinued to account for about 60% of the total increase in value added inthe manufacturing sector. This indicates that despite the sluggish growthof the capital goods sector some deepening of the manufacturing sector in-the Malaysian economy has been achieved.

1.21 Looking at it from another angle it is clear that during the1963-73 period, import substitution was more prominent among consumer goodse.g. food products, textiles, wearing apparel, bicycles, automobiles andelectrical goods - (more so among consumer durables) than among capitalgoods. By 1973, gross domestic output as a percentage of domestic marketwas 90% for consumer durables, 95% for consumer nondurables, 87% forintermediate goods and about 48% for capital goods./l

1.22 Yet another classification of the structural shift that themission analyzed was the growth performance and extent of contribution madeby the resource-based and nonresource-based industries. Given the richresource base of Malaysia and the policymakers' natural preference toharness these resources, the resource-based industries (both agriculturaland mineral) expanded rapidly during 1963-68 and contributed about 60% tothe sector's overall growth during this period. This contribution fell toabout 50% during the 1968-73 period. But most prominent is the increase inthe contribution made by the so-called footloose industries (electronics,clothing, textiles, etc.) from about 27% during 1963-68 to about 36% during1968-73. By the mid-1970s, the contribution made by these two categoriesof industries was catching up fast with the overall contribution made by theresource-based, agro-processing industries. It is clear that during thelate 1960s and early 1970s the Government shifted its emphasis fromdomestic-oriented, import-substitution activities to export-orientedindustrial development. Consequently, not only the structure ofmanufacturing production shifted in favour of nonresource-based industries,but among them it also shifted in favour of the export-oriented (even iffootloose) industries mainly in the Free Trade Zones.

Structural Changes and Factor Intensity

1.23 In order to ascertain the nature of factor intensity of manu-facturing activity during the period under review, the mission reclassifiedthe 27 major industrial groups into high, medium and low capital intensity

/1 See Chee Peng Lim From Import Substitution to Export Promotion; A Studyof Malaysia's Industrial Policy, Faculty of Economics and Administra-tion, University of Malaysia, Kuala Lumpur, January 1980 (unpublished).

-17-

in terms of the three indicators, K/L, V/L and V/W./1 All three indicatorssuggest that during 1963-68 some capital deepening of fhe manufacturingsector took place as industries with relatively low capital/labor ratio(such as furniture, footwear, leather) grew at substantially lower rates(11-13% p.a.) whereas industries with relatively high capital/labor ratio(e.g. beverages, glass and glass products, basic iron and steel, nonferrousmetal and products) expanded at substantially higher annual rates of 17% to22%. In the subsequent period, 1968-73, relatively more labor-intensiveindustries (wearing apparel, plastic products, electrical and othermachinery) expanded more rapidly - 25% to 31% - than the capital-intensiveindustries which grew at below the average rate. As a result themanufacturing sector directly generated almost 150,000 jobs during 1968-73as against 40,000 jobs during the previous five years and the annual employ-ment growth rate also doubled from 8.3% (1963-68) to 17% during 1968-73./2

Size-Distribution of Establishments

1.24 How did the rapid growth of the manufacturing sector affect thesize distribution of establishments in Malaysia? By the mid-1970s /3 80% ofestablishments had assets below M$50,000 (in terms of their book value) and90% had assets less than M$200,000./4 The majority of establishments hadless than 5 paid (full-time) employees, the bottom 80% had less than 20employees and the bottom 90%, less than 50 employees. Therefore, at leastfour fifths of establishments belonged to the category of small-scaleindustry. They contributed only 8% to the sectoral value added, generatingabout 12% of the paid full-time jobs (plus 90% of the unpaid workers and 60%of the paid part-time workers).

/1 The first indicator (K/L) is the ratio between the measures of twostocks (capital and labor), the second (V/L) is a ratio between a flow(value added) and stock (labor) while the third is a ratio between twoflows (value added and salaries and wages). All ratios, in terms ofthe 1973 census data are grouped into three ranges (high, medium andlow) by distributing the 28 industrial groups somewhat evenly (at thesame time avoiding cut-off points falling within a cluster ofobservations) and ensuring that the average ratio for the overallmanufacturing sector falls in the middle range.

/2 Aggregative evidence beyond 1973 indicate the reversal of the 1968-73trend in capital-intensity discussed here.

/3 Based mainly on an analysis of the 1973 census.

/4 It is interesting to note that the 1975 Industrial Coordination Act(ICA) applies to those establishments with share capital in excess ofM$250,000 (or 25 employees), thereby excluding at least 90% of estab-lishment in mid-1970s.

-18-

1.25 While data limitations are substantial, our analysis neverthelessshows that: (a) labor productivity (i.e. value added per paid full-timeemployee); (b) capital-intensity (fixed assets per paid, full-timeemployee); and (c) gross "surplus" (value added minus wages and salaries)sharply increase with the rise in asset size of the establishment. Like theasset size distribution, the employment size distribution also shows anincrease in labor productivity, capital intensity and "surplus" subject toan important exception of the largest-sized category of establishments(employing 500 or more workers)./l

1.26 The mission further analyzed these changes (during 1968-73) in thegrowth pattern by employment size in relation to several characteristics -viz. number of establishments, number of paid full-time employees, number ofpaid employees, salaries and wages, value added, gross output, and "surplus".It was found that the growth rate of each of the above characteristicincreased with employment size - in part reflecting the influence of theincentive system that strongly favored relatively larger establishments.The number of small establishments (employing less than 20 paid full-timeworkers) rose only by 14% whereas the number of medium and large establish-ments grew by about 80%; the value added by the small establishments grew byonly 70% whereas that among the medium and large establishments grew by180%, and among the large alone by 250%. It would be deirable to provide anincentives environment and support program which remove constraints on smallestablishments and provide them the necessary growth stimulus.

1.27 The slow growth of the relatively small establishments is furtherconfirmed by looking at the longer ten year period, 1963-73. The number ofsmall establishments rose by about 900 (from 6,500 in 1963 to 7,400 in 1973)whereas medium and large establishments rose by more than 1,300 (from 2,400to 3,700) during the same period./2

!Growth Scenario in Recent Years: 1974-78

1.28 According to the Index of Industrial Production, the manufacturingsector grew at an annual real rate of 13% in the second half of the 1970s,showing the growth elasticity with respect to GDP over 1.5. During thisperiod manufacturing activities contributed 26% to GDP growth twice thecontribution of the primary sector. The main sources of growth sustainingthis expansion during 1974-78 were domestic demand expansion (contributingabout two-thirds to overall growth), increase in manufactured exports

/1 The last category is dominated by traditionally labor-intensivelarge electronics and textile firms.

/2 Curiously enough, the official statistics show that the total number ofestablishments in wearing apparel (except footwear) fell from 214 (inthe 1963 census) to 111 (in the 1968 census), in wood and wood productsfrom 918 to 874 and in furniture and fixtures from 682 to 630.

-19-

(about one-fifth) and additional import-substitution about 12-13%. Withsustained rapid growth of the domestic market and a widening of theindustrial base, the manufacturing sector appears to have acquired duringthe last five-to-six years a favorable environment for the next phase ofimport substitution.

1.29 Can we say something more about the performance of the manufactur-ing subsectors over this period? As stated above no statistical informationis available for the entire manufacturing sector for any year beyond 1973.The Index of Industrial Production and Statistics on the Production of MajorCommodities is based on partial coverage, uses outdated weights andindustrial classification and shows no clear-cut relationship or linkageswith any annual surveys pertaining to the entire manufacturing sector. Themission, therefore, used sales value of domestically produced goods as asurrogate measure of gross output for analyzing the growth and structuralchanges in the Malaysian manufacturing sector for recent years./I

1.30 These data show that the overall manufacturing sector has perhapsgrown during the two quinquennial periods - 1968-73 and 1973-78 - at aboutthe same rate - 19% to 20% p.a. in current prices. Since the producersprice index (approximated by the available consumer price index forPeninsular Malaysia) rose more rapidly during the latter period - 6.7%annually as against 3.3% - the annual growth of manufacturing activity inreal terms may have been 16% during 1968-73 and 13% during 1973-78, thelatter being consistent with the overall growth mentioned in para. 1.28above. At the disaggregated level, the sales data at current prices show /2that manufacturing of machinery and equipment grew most rapidly in bothperiods - 30 to 32% annually - mainly due to the electronics components andassembly that grew by almost 50% p.a. throughout the decade. The textileindustry showed an annual growth of 31%. The implied real rates ofgrowth in these industries would be lower but still very substantial. Severalother industries which grew quite rapidly during the 1973-78 period were:palm oil, edible oils and fats and motor vehicle bodies. Industries which -

/1 Because of inventory changes this represents only an approximation ofgross output. Sales data also pertain to some 1,600 to 2,500 (rela-tively large) manufacturing establishments (including some 100 pioneerstatus estabishments).

/2 Because of the lack of individual price series it is not possible tocompute the growth rates in real terms for various subsectors mentionedhere.

-20-.

showed a decline in real terms /1 were: remilling and latex processingof rubber, food industries (mainly estate processing/refining of coconutoil, rice milling and canning of pineapples). Other industries which showedconsiderable deceleration in growth rates were plywood, hardboard andparticle board industries, and food beverage and tobacco industries to alesser extent. Most of these are resource-based manufacturing or processingactivities.

1.31 The most prominent contributors to manufacturing growth during1973-78 were electrical machinery and electronics, and textiles (both ofwhich quadrupled in sales value to M$1,720 million and M$950 millionrespectively by 1978). Together with rubber products which increased fromM$1,160 to M$1,730, these three groups of industries accounted for abouthalf of the increase in sales from 1973 to 1978./2

1.32 How reliable are the growth rates for recent years discussedabove? In the mission's judgement, the scope for a wrong estimation ofgrowth rate is not confined to the various factors discussed in Annex I,Volume III. In fact the possibilities of errors in estimating growth ratesof individual industrial groups or industries are real. As an illustration,the index of industrial production (IIP) suggests that electronics andelectrical machinery grew annually at 18.0 and 18.4% respectively during1973-78 in real terms; the "sales" data suggest that the growth rates in

/1 Based mainly on the Index of Industrial Production which has many short-comings briefly mentioned in para. 1.29 above and elaborated in Annex I,Volume III.

/2 The mission intended to study the growth of manufacturing value addedand the associated structural changes for the 1973-78 period butabsolutely no statistics on manufacturing values added are availablebeyond 1974. In the absence of this information, the mission studiedthe behavior of the ratio of value added to gross output (or 'sales')for the 1968-73 period and found it so unstable at the subsector levelas to be totally unsuitable for measuring the growth of value added fromthe growth of gross output or sales. Also, the official index ofindustrial production suggests that manufacturing value added grew inreal terms at 13.4% during 1968-73. Since the 1968-73 censuses indicatea growth of 22% p.a. in nominal terms, the implicit inflation rate is8.6% which is substantially more than the actual rate of about 3.3%.Therefore the index of industrial production may well underestimate the"true" growth of value added over the period, 1968-73. On the otherhand there is some evidence that the effective protection rates and,therefore, the discrepancy between the domestic and internationalprices may have increased during the 1970s. This would suggest thatsome of the recent industrial growth shown by the inadequate statisticsmay be more apparent than real.

-21-

nominal terms were 46 and 49% - the implied price rise being 27-28% which is

far greater than the price increases of these products on the internationalmarkets and the official Producers' Price Index showing about 7% p.a.

increase. Similarly, the implicit price rise in textiles (16%) is fargreater than the price increases in the international market and theProducers' Price Index. This clearly demonstrates that industrial sectordata are mutually inconsistent even in certain key subsectors. Since these

two industries have been among the most important contributors to Malaysia'sindustrial progress and some important policy decisions may impinge upon

their growth rates (which are subject to a substantial margin of error) theneed for policymakers to assign high priority to the improvement of the

industrial data base is obvious.

1.33 To measure the contribution that various subsectors are working

to the advance of the economy more accurately, it is also important to takeinto account that high rates of effective protection may lead to large

discrepancies between changes in value added measured in the conventionalway, and real contributions to the economy (there are examples in theliterature of industries producing negative value added in internationalprices). Also, especially in the case of Malaysia with its largepercentage of industries under foreign ownerships, it is important todevelop indices that reflect increases in national rather than domestic

income.

1.34 Furthermore the 1968 weights used in the current production index

for individual industrial groups or industries do not represent the structure

of production reflected by the 1973 manufacturing census. For instance,weight of electronics is 0.8 in the current official index, whereas it is

6.3 according to the 1973 census; weight of textiles is 2.2 and 4.5respectively and that of basic metal products 2.7 and 3.7 respectively.On the other hand, several industrial groups have lost substantial ground

during 1968-73. Prominent among them are "other dairy products" from 4.0to 1.0, petroleum and coal products from 5.0 to 2.2, rubber products from14.8 to 9.6, cement from 5.9 to 1.9. "Other pioneer" firms should berevised from 4.5 to zero as they should belong to appropriate manufacturing

industry groups in the production index. Other serious limitations of theofficial index are: (a) all the industries specified in the index together

contributed only 76% of manufacturing value added in 1973; and (b) this

index does not include 11 (out of 28) major industrial groups such aswearing apparel and footwear; leather and leather products, furniture and

fixtures; printing, publishing and allied industries, plastic products,pottery, china and earthenware; glass and glass products; machinery exceptelectrical; and precision instruments. The omission of so many importantindustrial groups casts doubts on the usefulness and accuracy of the

outdated official production index. (See Annex I, Volume III, for a moredetailed discussion of manufacturing statistics and their weaknesses in

Malaysia).

-22-

Achievements and New Challenges

1.35 The problems of measuring growth rates precisely are enormous andshould be kept in proper perspective when reviewing the achievements of thepast. The available statistics show that the Malaysian manufacturing sectormade considerable progress over the last two decades, both in terms ofoverall growth rate and structural changes. The manufacturing sector grewat an accelerated pace of 10 to 11 to 13% annually during the first, secondand third plan periods, respectively. As a result of Government's keennessto overcome the (urban) unemployment problem, manufacturing employmenttripled in a decade thereby directly creating 250,000 new jobs; the growthelasticity of manufacturing employment continuously increased from 0.7(1963-68) to 0.9 (1968-73) to 1.1 (1973-78)./l

1.36 Policymakers' success in directing an accelerated growth wasfacilitated to a considerable extent by a favorable world economic environ-ment owing to a buoyant demand for Malaysia's commodity exports (petroleum,timber, rubber, palm oil, etc.); a rapidly expanding market for nonresource-based footloose manufactured exports (textiles, clothing, electronics, etc.)from developing economies; a ready access to urban, easy-to-train laborforce and ample natural resources. The present volatile world economicsituation as well as vulnerability and deceleration in the growth of certainmanufacturing industries, however, pose new challenges for continuation ofthe rapid industrial growth so necessary to meet the NEP objectives ofpoverty alleviation and restructuring of employment. Meeting thesechallenges would require new policy initiatives and strengthening of themonitoring, evaluation and implementation system, both at the subsector andgeneral levels, and are briefly discussed in Chapter VI below.

1.37 of particular interest to the policymakers should be the analysisof changes in size distributions which revealed that the number of smallmanufacturing establishments remained almost stationary. Small establish-ments provide a substantial proportion of paid part-time as well as "unpaid",jobs, and thus help to reduce underemployment. These results are reinforcedby a detailed cross-sectional field study of some 400 establishments con-ducted by Chee Peng Lim./2 Another recent study discusses the importance of

/1 There are some obvious contradictions: increase in employment as wellas increase in employment elasticity coupled with increase in laborproductivity do not seeem to be consistent with declining or low levelof manufacuring sector investment, discussed in Section "E", in thepost-1974 era and reinforce the mission's suggestion that weaknesses ofthe manufacturing statistics deserve serious attention of the plannersand policy makers.

/2 Chee Peng Lim, "A Study of the Pattern of Employment and Wages in SmallIndustry in Malaysia," The Developing Economies, March 1978.

-23-.

small industries and the problems they face in the Malaysian economy, andevaluate various official programs for promoting small industry development;besides conducting a sample survey of the rubber processing machinery andtin mining machinery industries./I The mission's impressions are reinforcedby this study which concludes that small industry in Malaysia could notdevelop to its full potential due to the inherent difficulties that it facesand to an unfavorable, albeit unintended, government policy environmentwhich favored growth of relatively large establishments, mainly through avariety of incentives./2 The development experience suggests that awell-balanced industrial structure requires small, medium and largeestablishments and that each has a role to play in industrialization of aneconomy, despite an accelerated use of sophisticated technology and modernindustrial organization. In Malaysia the general interest in Bumiputradevelopment makes the establishment of "new" small industry an even moreattractive target for promotional efforts. Certain industries seem to bewell suited for small-scale operations; they include industrial machinerycomponents foundries, motor vehicle bodies, furniture, leather footwear,clothing and bakeries. Specific problems faced by SMIs in Malaysia deservefurther analysis.

1.38 The growth of the manufacturing sector value added and output aswell as changes in product mix and the sources of growth have beensubstantial. In the mission's judgement, however, the growth in employmentand its distribution, trends in wages and earnings, differentiation in laborproductivity and capital intensity as well as labor market conditions areeven more important from the viewpoint of the NEP objectives and theirfulfillment. The following chapter therefore reviews the extent of progressmade and the nature of outstanding issues in these various areas.

/1 See Chee Peng Lim and Foong Wai Fong, An Analysis of Small Industry inMalaysia (Faculty of Economics and Administration, University of Malaya,Kuala Lumpur, September 1979, unpublished). This study is sponsored bythe Asian Regional Team for Employment Promotion as a research projecton Asean Comparative Study of Labour-Intensive Industries in Malaysia.

/2 See Chapter VI for a more detailed discussion.

-24-

II. POPULATION, LABOR FORCE AND MANUFACTURING SECTOR EMPLOYMENT

Population and Labor Force

2.01 Malaysia is one of the medium-sized countries in terms of itspopulation which is estimated around 14 million in 1980. Its 2.6% p.a.population growth places it among the group of 39 countries showing a littlemore than moderate growth in their population size./l Almost 85% of thispopulation is in Peninsular Malaysia (Sabah 6%, Sarawak 9%) and 54% of themare Malays, 35% Chinese, 10% Indian and 1% others./2 Some of the othercharacteristics of the Malaysian population are: (a) its youngness (around40% are in the 0-14 age group) - therefore, the dependency ratio is high;and (b) 65% of the people live in rural areas and the majority of the ruralpopulation (about two thirds) are Malays, and (c) in recent years the Malayurban population has been rising fast because of the lure of manufacturingand commercial sector jobs.

2.02 Expanding at an annual rate of about 3.5% and with some 80,900 newentries into the labor force over the Third Plan period, the total laborforce is expected to reach about 5.1 million in 1980. About 89% of thislabor force is in Peninsular Malaysia - comprising about 52% Malays, 36%Chinese, 11% Indians and 1% others. According to the Mid-Term Plan Review,total employment during 1975-80 is estimated to rise at 3.7% p.a. and thecurrent unemployment rate is about 6%. About 42% of those employed in 1980were in agriculture, 14% in manufacturing industry, 14% in governmentservices,/3 13.7% in finance, insurance and commerce, 4.7% in constructionand the rest in other services.

Employment in the Manufacturing Sector: Overall Situation

2.03 The Third Malaysia Plan (TMP) assigned highest priority to a rapidgrowth of the economy, the manufacturing sector being the most dynamic forcebehind this growth. The principal government strategy for reducing ruralpoverty is to encourage people to transfer from low productivity ruraloccupations to higher income opportunities in the modern sector through therapid development of the industrial and service sectors. The manufacturing

/1 The World Bank "ATLAS", 1979.

/2 Malaysia, "Mid-Term Review of the Third Malaysia Plan, 1976-80" (to becalled the Mid-Term Plan Review).

/3 Including public administration, defence, health, education and publicutilities.

-25-

sector is expected to contribute almost 30% to the total new jobs to becreated during the plan period.

2.04 In spite of the enormous importance assigned to the manufacturingsector in terms of its contribution to the creation of new jobs, the database to evaluate the performance of the sector in this respect remains veryweak and deficient. Analysis of the trends at the disaggregated and sub-sectoral level is particularly difficult since the only source of consistenttime series - viz. the Monthly Industrial Statistics (MIS) at the five-digitlevel - present data derived from full enumeration of only 49 out of 95industry subsectors covered by MIS. Others involve industry-specificcut-off points varying from industry-to-industry but in many cases excludingestablishments with less than 20 employees, and more importantly excludingcertain important subsector completely e.g. furniture, fish canning, made-uptextiles, repairs of frig, air-conditioners, etc., resulting in seriousunder-coverage./l But the other alternative data source - viz. theQuarterly Labor Force Surveys (QLFS) also suffers from major deficiencies:(a) it is based on a small sample of 18,000 households (from a total ofabout 2.6 million estimated households in 1980); and, (b) in 1976 theunemployed were differentiated by "passive" and "active" - making the laborforce participation rates (LFPR) incomparable over time.

2.05 Despite the numerous inconsistencies and limitations in primarydata sources, which make reliable labor market analysis a very difficulttask, various statistics do indicate a rapid growth in manufacturing sectoremployment in the second half of the 1970s. The growth of aggregateemployment in the manufacturing sector, as shown in the table below rangesfrom 9% to 12% p.a. during 1974-78. Industrial sector employment derived asa difference and shown in the last column perhaps contains a substantialelement of employment in the small-scale segment of the industrial sector.Even that appears to have grown at 6% to 8% p.a. The mission did not havetime to look deeply into the performance and characteristics of the SSIsegment of the manufacturing sector but clearly this sector is important anddeserves much greater attention in future work.

2.06 Even over a longer period, 1967/68 to 1978, the QLFS data show aremarkable increase in manufacturing employment in Peninsular Malaysia - anaverage annual growth of 12%. The expansion in more recent years (1974-78)has slowed down but is still substantial. Based on these data, the share of

/1 MIS reports manufacturing sector employment level which is about half ofthat reported by alternative sources. Many of the nonreportedestablishments are small (employing less than 20 workers) but aconsiderable number would also be medium-sized establishments.

-26-

Table 2: AGGREGATE EMPLOYMENT IN THE MANUFACTURING SECTOR, 1974-78

(C)(A) (B) Treasury/

QLFS MIS EPU /a Difference

(End Dec) Estimates (C-B) (A-B)1974 460.3 193.9 448 254 266.41975 533.4 211.6 498 286 321.81976 581.3 241.5 535 293 339.81977 622.6 262.5 587 324 360.11978 666.4 307.8 630 322 358.61974-78 9.7 12.2 9.0 6.1 7.7Growth rates

QLFS = Quarterly Labor Force Surveys

MIS = Monthly Industrial Statistics

/a Mid-Term Review of the Third Malaysia Plan and Economic Report,1979/80.

manufacturing in total employment went up from 9.1% in 1967/68 to 16.7% in1978./i In commerce the increase was from 10.8% to 14.5%. As a result theproportion of employment in agriculture declined from 51.5% to 39% over the

same ten-year period. The intersectoral transfers have created some laborshortages in agriculture (particularly for young workers) and have set inmotion an important long-term mechanism for raising per capita incomesthrough moderate mechanization. Despite a fairly rapid growth inemployment, however, not all the slack has disappeared. In September 1979,the QLFS disclosed that 5.3% of the labor force was still unemployed.

2.07 Data limitations are even more severe at disaggregate levels butan analysis of labor market trends is desirable for discussion of futureindustrial strategy, employment and manpower policy and other key socio-economic objectives of the Government during the Fourth Malaysia Planperiod. The deficiencies of the MIS data have been noted above but that is

the only source of data for discussion at the disaggretate level. Thereforethe finding and conclusions which 'emerge cannot be better, than the primary

/1 EPU/Treasury (adjusted) data show the share of manufacturing employmentin total around 14%.

-27-

data underlying the analysis. There are nevertheless some very interestingfeatures of recent developments at the subsectoral level and the series doesgive a useful indication of broad trends in the enterprises which accountfor the bulk of industrial output. The next section, therefore, discussesthe trends in employment at disaggregated levels.

Trends in Subsectoral Employment

2.08 Among the 12 growing specific industries during recent years(1973-79), leading the list was the electronics/electrical machinerysubgroups which quadrupled its labor force. It was followed by the motorvehicle parts and accesories showing a net growth of employment in 1979almost 3.5 times the level in 1973. Industries which succeeded in increas-ing their employment twice or almost twice over this period were metal andmiscellaneous products, pulp, paper and paper boards, and planing windowsand door mills and joinery works. A total of 7 other industries, chemicalproducts, medical and pharmaceutical preparations, breweries, clothing, ironfoundries, textiles (major group 321) and chemical fertilizers/pesticidesincreased their employment by about 100% within the six years under review.

2.09 In terms of the absolute employment gains, particularly conspicuousis the contribution made by the electronic machinery and apparatus sector(mostly electronic subassembly) rising from 22,562 in 1973 to 60,957 in1978. This is a labor-intensive industry dominated by multinationalcorporations which have been attracted to Malaysia by its relatively lowlabor costs, political stability, generous tax incentives, good workingenvironment for expatriate executives, and reasonably good transportfacilities. It has benefitted from the world-wide boom in demand forsemiconductor components (US semiconductor industry shipments alone areexpected to reach M$7.7 billion in 19780)./1 Malaysian exports of machineryand equipment (principally electronic components) totalled M$1. billion in1978 and grew by 78.8% p.a. between 1971-78.

2.10 A second rapidly growing industrial group has been textiles andclothing. Combined employment nearly doubled in five years, rising from28,531 in 1973 to 51,793 in 1978 (16.8% of the total manufacturing employ-ment recorded by the survey). Here a major stimulus to growth has beenimport substitution behind a moderate tariff protection (nominal rate of35%), together with a rapid expansion of domestic demand. Total consumptionexpenditure rose by more than 9% p.a. in real terms in this period.Domestic demand for textiles and clothing will have increased at a higherrate because the income elasticity of demand for textiles-is above unity.Nevertheless, exports also contributed significantly to the growth,

/1 Asian Wall Street Journal, February 1980.

-28-

especially in the clothing sector. Clothing exports reached M$255 millionin 1978. The sales value of output from the clothing factories covered bythe monthly industrial statistics amounted to only M$207 million in 1978.As the official cut-off point was 5 workers or more for this subsector,these figures suggest either under-coverage in the survey or a significantvolume of exports emanating from very small establishments (possibly on asubcontract basis to export traders). Exports of textiles on the other handreached M$196 million compared with a total sales value of M$957 million in1978 recorded in the monthly industrial statistics where the coverage ofestablishments in this sector was supposed to be complete. Collectively,the three subgroups: electronics, textiles and clothing accounted for almost40% of total manufacturing employment reported in MIS.

2.11 Another major employer is the food and beverage industry. Herethe expansion of employment has been less rapid (33% over the five-yearperiod) but still accounted for 10.4% of total employment in 1978. Theindustry depends largely on the domestic market. Processed food exportsaccounted for 1.5% of total exports in 1978 (7% of manufactured exports).Food exports grew by 14% p.a. between 1971-78 compared with 24.8% for totalmanufactured exports.

2.12 The Bank Negara estimates that 20% of total manufacturing outputis now exported. As a high proportion of manufactured exports are labor-intensive products (electronics, textiles and clothing), upwards of one outof every four jobs in industry can be attributed to overseas demand and theproportion is growing.

2.13 The rate of job creation was rather disappointing in rubberproducts, plywood and particle boards, printing and publishing and plasticproducts. During 1973-79, some specific industries even showed a decline inemployment. They were: pineapple canning, coconut oil, sugar factories,and in more recent years (1976-79), this group included large rice mills,rubber remilling and latex processing off estates as well as sago andtapioca establishments. In fact during mid-1976 and mid-1979, all thefive-digit manufacturing industries in MIS, with just three exceptions,/lregistered slower rates of employment growth. The rate of manufacturingoverall employment in recent years has therefore decelerated.

Ethnic Composition of the Manufacturing Labor Force

2.14 A major objective of the Government's New Economic Policy (NEP) isthe absorption of a higer proportion of Malays in the modern sectors of theeconomy. Although the percentage of Malays employed in the secondary andtertiary sectors has increased from 34.2% in 1967/68 to 48.5% in 1978,

/1 These exceptions are: other grain mills, soft drinks and carbonatedbeverages and iron foundries.

-29-

progress has been relatively slow in manufacturing alone. Bumiputrasconstituted 35.1% of manufacturing employment in 1978 compared with 32.3%ten years previously. One reason perhaps is the slower rate of appropriateskill development in Malay labor force in line with the needs of themanufacturing sector. No breakdown is available showing the distribution byoccupational categories within the manufacturing sector. In the economy asa whole, 50% of those employed in professional and technical occupationswere Malays in 1978, close to their proportion in the total labor force(48.8%). But they accounted for just 27.7% of administrative and managerialgrades and 24.3% of sales and related workers.

2.15 The relatively low penetration of Mlalays into managerial/ adminis-trative sales posts may be explained by: (a) a traditional preference amongeducated Malays for public administration and professional jobs (e.g.doctors); and (b) the predominance of family-owned businesses established bynon-Malay entrepreneurs who, as with family businesses throughout the world,tend to reserve managerial posts for family members. The 1973 ManufacturingCensus showed that 10,527 enterprises out of a total of 11,060 wereindividual proprietorships, partnerships or private limited companies. Inthe subsidiaries of multinational corporations, the percentage of Malays isrelatively high. A survey conducted by the Malaysian International Chamberof Commerce and Industry (MICCI) in December 1978 revealed that 44.6% oftotal employees in the international companies were Bumiputras and theyrepresented 49.2% of the skilled worker category, 23.1% at the supervisorygrades and 20.6% of executives. These latter two percentages had almostdoubled in six years. In public sector companies the Bumiputra proportionis likely to be substantially greater but no data were available to themission for further analysis.

2.16 The MICCI forecasts a gradual but continued rise in the Malayshares. Already around 50% of their recruits coming from institutions ofhigher learning are Bumiputras. They are given training within companyprograms and/or courses run by the National Productivity Center. Thistraining, combined with on-the-job experience, should result in a betterracial balance among senior personnel in the future. In the mission'sjudgement the prospects of this happening naturally within the fast-growingmanufacturing sector and the Malaysian economy are very good. As thesecondary and tertiary sectors continue to grow rapidly, the manufacturingand commercial enterprises will outgrow the family-oriented management styleand as the more competitive export manufacturing and trading keep theirmomentum and the investment climate remains attractive, the demand fortechnically and professionally trained Malays will rise rapidly. What theGovernment should make sure of is that there is an adequate supply of M4alaysin these skill categories to take advantage of the emerging situation. Themission therefore places very strong emphasis on appropriate skilldevelopment among the Mfalay labor force. This contributes both to a morebalanced racial distribution of employment and income levels enjoyed bythem - the key socio-economic objectives of the NEP.

-30-

Trends in Wages and Earnings

2.17 It is difficult to trace the trends in wages and labor earnings.No wage indices are prepared by the Department of Statistics or the Ministryof Labor and the coverage of the industrial surveys varies from year toyear.

2.18 During the two census years - 1968 and 1973 - for which reliabledata are available, the yearly wage levels in manufacturing remainedstationary, averaging M$2,210 in 1968 and M$2,190 in 1973. This reflectssubstantial unemployment and underemployment which prevailed during thisperiod. During 1973-78 when the manufacturing growth was rapid and thelabor market tightened, average annual wages among the pioneer statusestablishments increased from M$2,056 to M$3,519 - raising money wages by71% as compared with 39% increase in the Official Consumer Price Index.

2.19 Information on the broader concept of average earnings per month(AEM) reported in the Monthly Industrial Statistics (MIS) also shows that innominal terms they increased from about M$190 to M$320 at an annual compoundrate of about 9%. In constant 1973 prices the overall sector AEM increaseduring 1973-79 was 18.6% - or 2.9% p.a. The increase was 2 to 3 timesfaster than the overall sector average in motor vehicle bodies, ironfoundries, plywood and particle board, textile manufacturing and 1-1/2 to 2times the average sector growth in such subsectors as footwear, clothingfactories, planning mills, cement and concrete, assembly of automobiles,etc. The largest employing industry, viz. electronics and electrical ranked17th among 21 industries showing,AEM increases during 1973-79 (25.3%) - onlymoderately above the industry average. The second and the third largestemploying industries, viz. textiles and clothing were significantly higherthan the sector average.

2.20 Looking at the trend in real AEM during 1973-76 and 1976-79separately, the mission found that among the 8 largest employing industries,growth remained stationary in electronics and plywood/particle board mills;decelerated substantially in textiles, plastic products, printing/publishing, etc. from the first to the second period but acceleratedconsiderably for such subgroups as clothing, and rubber products.

2.21 This fragmentary evidence on average real earnings suggests thatthere are perhaps some industry-specific shortages, reflecting quitepossibly rigidities in local supply conditions rather than a generalshortage of labor facing the manufacturing sector in the Malaysian economy.During the last three years, acceleration in AEM has occurred and laborshortages have been reported in some industries but they have regionalconcentration and sex bias. For example, labor scarcity has been created insome regions by a heavy concentration of new industries like electronics ina few localities (e.g. Penang) and their rapid growth has exhausted theavailable supply of labor in the immediate neighborhood. This seems toapply particularly to female labor whose mobility is restricted by

-31-

conventional social/cultural barriers. Another factor explaining laborscarcity in some areas of the economy is the fragmented character of thelabor market and the wage negotiation system. Less than half a million(out of a total of about 5 million) workers throughout the economy aremembers of trade unions and collective agreements, lasting 2 or 3 years, arenegotiated at the plant or subsectoral level. Thus, although both nominaland real wages appear to have risen in recent years there are substantialdifferences in the wage rates for the same jobs in different firms andindustries. This tends to induce job-hopping, thereby creating temporaryshortages for certain employers.

Trends in Labor Productivity and Capital Intensity