report of abhineet

TRANSCRIPT

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 1/108

MBA 2009-11

INTRODUCTION

HDFCSLC is one of India’s leading private insurance companies. It offers both

individual and group insurance solution. It is a joint venture between HDFC and a

group of company of Standard Life. I have chosen insurance sector as the place for

summer training because in these days this sector is in boom and it will never go

down. All people invest their money in insurance and get more benefited. In the

sector the work of marketing is more challenging then the other sector because

there is 17 insurance companies in the market who are giving competition to each

other and the work of convince people for investment in respective company is a

challenging work and success in the sector proves that the respective person is a

good marketer. Today insurance sector India is on boom because all people want to

invest. Those who don’t know about investment in share market and don’t want to

invest in mutual funds they invest in insurance sector. Insurance sector gives them

investment plus risk cover. Those who don’t want to take risk in the investment go

to insurance sector. It also gives income tax benefits to the peoples. Insurance

company are now launching ULIP plan and gives chance to the investor to choose

their investment pattern according to their fund investment table(this table is

included in the product information of the product of HDFC Standard life). This

fund investment tells us that how much the investor want to take risk. Generally in

the ULIP plan, the thesis is that “The more you risk the more you have profit.”

HDFCSLIC stands for Housing Development Finance corporation standard life

insurance company. It is incorporated in 1977 as a public limited company with the

specialization in provision of housing finance to individuals’ cooperative societies

and the corporate sector. One significant matter about the HDFC is that it is first

private sector retail housing finance company and it is listed on both BSE and NSE.

Its market capitalization in June 2002.

Abhineet Anand[0953870001] Page 1

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 2/108

MBA 2009-11

Standard life insurance is founded in 1825. Standard life was reincorporated as a

mutual assurance company in 1925. It’s largest mutual life insurance company in

Europe. For the joint venture between HDFC and SLIC, the discussion commenced

in January 1995 and the agreement signed in October 1995. Further joint venture

agreement renewed in October 1998. In January 2000 the life insurance project

teem established in Mumbai. At last the company officially incorporated in 14th

August 2000. It is the matter of great happiness for HDFCSLIC is that it is the first

private sector life. insurance company to be granted a certificate of registration in

23rd October, 2000. Today 75% shareholding in the hand of HDFC and Standard

life has 25% shareholding in this joint venture

Abhineet Anand[0953870001] Page 2

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 3/108

MBA 2009-11

OBJECTIVE OF THE STUDY

This project aims to know about the “ Financial product in Indian sub-continent ”

for the HDFCSLC to know how much people know and think about the insurance

specially in government employees like PWD engineers, Nagar nigam engineers etc.

the objective was to identify the scope of financial products in Indian subcontinent

and another objective was to find out potential investors who are seeking for new

investment and they are likely to join HDFCSLC as an activity partner,

Abhineet Anand[0953870001] Page 3

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 4/108

MBA 2009-11

SCOPE AND LIMITATION OF STUDY

SCOPE OF STUDY

The scope of study was to know about the all financial product of insurance sector

specially of the HDFCSLC. It helps to know what are the benefits of the product &

are people aware or not about the benefits of insurance.

LIMITATIONS

1) Small Sample size:

In my survey, I have taken a sample size of 100 customers, but only with

these samples I can’t make a proper conclusion.

2) Time Constraint:

Time for this project is not sufficient. As I go for the survey at the various

Government department and residence then time for completing and filling

the questionnaires is not sufficient.

3) Sample Area:

The study was conducted in LUCKNOW only. Hence, the study may not be

useful for projection of behavioral aspect of consumers living in other cities.

4) Money Constraint:

Budget and finance are always been constraints in doing any project.

Abhineet Anand[0953870001] Page 4

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 5/108

MBA 2009-11

5) Negative response

Some people shows negative response to the survey by not

Answering the questionnaire.

Abhineet Anand[0953870001] Page 5

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 6/108

MBA 2009-11

RESEARCH METHODOLOGY

Research Methodology is a way to systematically solve the problem. It may be

understood as a science of studying how research is done scientifically. In it we

study the various steps that are generally adopted by the researcher in studying his

research problem along with logic behind them . it is necessary for the researcher to

know not only the research methods/techniques but also the methodology used.

Researchers not only need to know how to develop certain indices or tests , how to

calculate mean or median or mode, how to apply particular research techniques but

must also know which of these methods or techniques are relevant and what would

they mean and indicate and why Research process consists of series of actions or

steps necessary to effectively carry out the research.

RESEARCH DESIGN

A research design is the detailed blueprint used to guide a research study toward its

objectives. The process of designing a research study involves many interrelated

decisions. The most significant decision is the choice of research approach, because

it determines how the information will be obtained. To design something also means

to ensure that the pieces fit together. The achievement of this fit among objective,

research approach, and research tactics is inherently an iterative process in which

earlier decisions are constantly reconsidered in light of subsequent decisions.

The function of research design is to provide for collection of relevant evidence with

minimal expenditure of time effort and money

The following methodology was adopted for the study purpose:

Abhineet Anand[0953870001] Page 6

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 7/108

MBA 2009-11

Source of data

Data is the key activity of marketing research. The design of the data collecting

method is backbone of research design.

Data can be obtained from two important sources, namely:

1. Primary Data

2. Secondary Data

I – Primary sources

• Personal interview through questionnaire

II-Secondary data

The secondary data was collected through following sources

• Through company’s website

• Through insurance book provided by IRDA

SAMPLE DESIGN

Area of Sample:

• The areas covered up in this survey was LUCKNOW

Selection of units under study:

Abhineet Anand[0953870001] Page 7

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 8/108

MBA 2009-11

AREA OF LUCKNOW WHERE SURVEY IS DONE

1. PWD department

2. Nagar nigam office

3. Jankipuram

4. Kapoorthala

5. Gomtinager

6. Various branches of HDFCSLC

Source list (Sampling Frame):

GOVERNMENT EMPLOYEES: 59

NON GOVT EMPLOYEES: 26

RETIERED PERSON: 15

Sample size: 100

Sampling Procedure: Probability Sampling (Simple Random Sampling)

Abhineet Anand[0953870001] Page 8

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 9/108

MBA 2009-11

METHOD OF DATA COLLECTION

Research Method/Technique:

In the project report the researcher used following techniques while conducting his

study:

• Analysis of documents

• Survey Method: A market survey was done on how much people are aware

of financial products of insurance & they know about its benefits or not.

• Questionnaire (Structured): A structured designed comprehensive

questionnaire was framed and Protested for data collection from the people

(scheduleing method) .

Survey:

Survey was done with the questionnaire as well as personal interaction

Personal interviews

This method of date collection involves the interviewers asking question in a face to

face contact situation there in direct personal investigation and the interview

innproperly structured as it involves the use of set of predetermined questions

which are asked in the form and order pre-decided that is given in questionnaire.

This technique is preferred as it is economical, more informative, non responses are

low, spontaneous reaction which are realistic. Lots of supplementary information

comes up.

Abhineet Anand[0953870001] Page 9

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 10/108

MBA 2009-11

Secondary Data

Secondary data consists of information that already exists some where and may

have collected for a different purpose, it provide a starting point. As information

was taken for company profile as well as to know about financial product as well as

to know about the insurance.

To know about the company as well as about insurance the secondary data was

used.

Abhineet Anand[0953870001] Page 10

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 11/108

MBA 2009-11

THE COMPANY”S BACKGROUND

When we talk about company profile then HDFC standard life insurance company

is targeting insurance sector. It is launching various type of insurance plan and

product which is enticing people to buy its plan. As a insurance company it focus

mainly in the recruitment of financial consultant and the whole company based on it

because the main aim of company is to get business and sell lots number of policy

and this work is done by financial consultant.

HDFC Standard Life Vision and Values

Vision of HDFCSL

The most successful and admired life insurance company, which mean that we are

the most trusted company, the easiest to deal with, offer the best value for money,

and set the standards in the industry. In short, “The most obvious choice for all”

For retention in the market and highest market share, we need trust of our

customer. The customer should trust on our policies, services, employs and they

should be friendly with us. It wants to live in the eye and heart of the customer. It

wants to give them the easiest deal so that they can be understood the terms and

policies. As we know that profit is the main aim of any business but it think not only

about his profit but also profit of the customer. It wants to be the choice of all

people on the basis of trust of customer, delivering high value to the customer, and

deliver of best value of the money

Abhineet Anand[0953870001] Page 11

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 12/108

MBA 2009-11

Value that will be observed while we work with HDFCSLC

1. Integrity

HDFCSL believes in honest and trustfulness in every action. Transparency in

dealing with customers. It is stick to principles irrespective of outcome. When we

work in HDFCSL then we observed that its rules and activity of every person in the

organization is just and fair to every one.

Integrity is the bedrock on which the company and the expectations of the

customers and employees are built. Integrity gives inner feeling to both customer

and the employees to work with it. It establishes the credibility of the person, defines

the character and empowers one to do justice to the job. It enables confidence and

trust, achieving transparency and laying a strong foundation for a binding

relationship. It guide principle for all walks of life.

2. Innovation

It is the process of building a store house of treasures through experiences. Lots of

product is going to be launched by the competitors. So it is very important to look

every product and process through fresh eyes everyday. It is the significant part of

the business that attracts customer.

Innovation is essential to exceed customer expectation and maximize customer

retention because it is the sector of investment so you need to fulfill the customer

expectation which help you to retain customer. Innovation helps to achieve

competitive advantage. It promotes growth and upgrade standards in the industry.

It fosters creativity amongst employees and partners. It opens a world of new

possibilities because it brings new concept which helps to entice the customer.

Abhineet Anand[0953870001] Page 12

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 13/108

MBA 2009-11

3. Customer centric

Customer becomes the main properties of any organization. Whatever work done

by the organization runs around the expectations of the customer. Customer

becomes centre point of the organization and the main focus of the organization

becomes to understand his expectations by keeping him as the centre point. It gives

more focus on customer activity and saying. It tries to understand customer needs

and deliver solutions. As we know that the market is changed. Lots of competitors is

here who search chance to increase their market share and entice your customer so

customer interest become always supreme.

4. People Care

Genuinely try to understand those people who are working with HDFCSL. It guides

their development through training and support. It helps them to develop their

requisite their skills so that they can reach their true potential. It tries to know them

on a personal front because it works as a performance appraisal. It try to create an

environment of trust and openness so that all people who are working here behave

friendly and helps to each other because team work is most important for getting

success and give respect for the time of others.

People are the most valuable assets of the company so it tries to motivate individual

to give his/her best. It wants to establish a valuable relationship with them to create

a joyful working environment. The most important thing is that it tries to provide

job satisfaction for their people.

5. Team work “One for all and all for one”

Here whole team takes the ownership of the deliverables. It consults all involved in

the work and try to understand their opinion and then arrive ant a common

objective. There is a cooperation and support across departmental boundaries. It

Abhineet Anand[0953870001] Page 13

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 14/108

MBA 2009-11

identifies strengths and weaknesses accordingly allocate responsibility to achieve

common objectives.

Team work helps everyone to achieve more. it adds joy at work place which add

interest in the work and new stamina in the work. It generates synergy and provides

a focused approach. When an idea or activity performed in a group, it has greater

acceptability. “Team work proves one for all and all for one”.

6. Joy and simplicity

It believes in joy and simplicity so that people in the organization will be more

dedicated towards work and they will give more business to the organization. Work

with joy and simplicity brings creativity and new imagination which also brings new

innovative ideas that promote competitive advantage to the organization.

MISSION OF HDFSLIC

We aim to be the top new life insurance company in the market.

This does not just mean being the largest or the most productive company in the

market, rather it is a combination of several things like- Customer service of the

highest order Value for money for customers Professionalism in carrying out

business Innovative products to cater to different needs of different customers

Use of technology to improve service standards Increasing market sha

HDFC GROUP COMPANIES

HDFC Limited

HDFC Bank

HDFC Asset Management Co. Limited

Abhineet Anand[0953870001] Page 14

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 15/108

MBA 2009-11

HDFC Securities LIMITED

HDFC Standard Life Insurance Company Intelnet Global

CIBIL–Credit Information Bureau Investigation Ltd

HDFC Chubb General Insurance

Abhineet Anand[0953870001] Page 15

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 16/108

MBA 2009-11

THE PROMOTERS

Brief Profile of The Board of Directors

Mr. Deepak S. Parekh is the Chairman of the Company. He is also the Chairmanand Director of Housing Development Finance Corporation Limited (HDFC

Limited). He joined HDFC Limited in a senior management position in 1978. He

was inducted as a whole-time director of HDFC Limited in 1985 and was appointed

as its Chairman in 1993. Mr. Parekh is a Fellow of the Institute of Chartered

Accountants (England & Wales).

Mr. Keki M. Mistry joined the Board of Directors of the Company in December,

2000. He is currently the Vice Chairman and Chief Executive Officer of HDFC

Limited. He joined HDFC Limited in 1981 and became an Executive Director in

1993. He was appointed as its Managing Director in 2000. Mr. Mistry is a Fellow of

the Institute of Chartered Accountants of India and a member of the Michigan

Association of Certified Public Accountants.

Abhineet Anand[0953870001] Page 16

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 17/108

MBA 2009-11

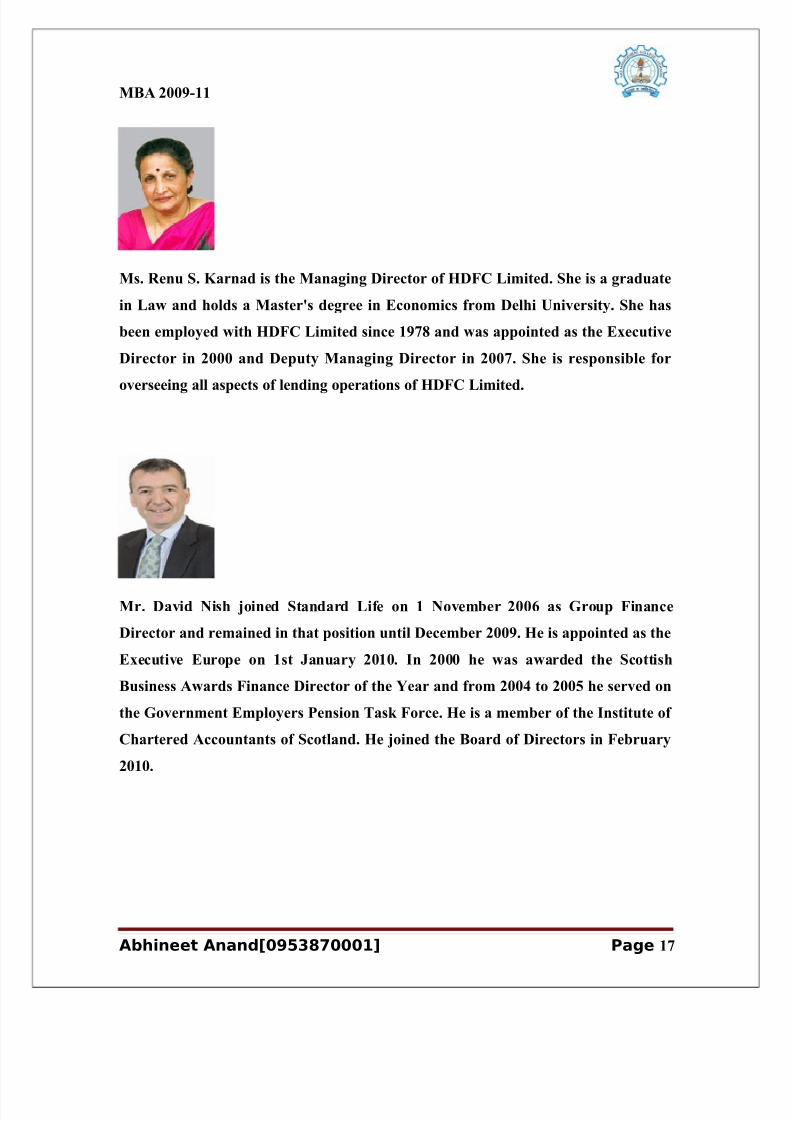

Ms. Renu S. Karnad is the Managing Director of HDFC Limited. She is a graduate

in Law and holds a Master's degree in Economics from Delhi University. She has

been employed with HDFC Limited since 1978 and was appointed as the Executive

Director in 2000 and Deputy Managing Director in 2007. She is responsible for

overseeing all aspects of lending operations of HDFC Limited.

Mr. David Nish joined Standard Life on 1 November 2006 as Group Finance

Director and remained in that position until December 2009. He is appointed as the

Executive Europe on 1st January 2010. In 2000 he was awarded the Scottish

Business Awards Finance Director of the Year and from 2004 to 2005 he served on

the Government Employers Pension Task Force. He is a member of the Institute of

Chartered Accountants of Scotland. He joined the Board of Directors in February

2010.

Abhineet Anand[0953870001] Page 17

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 18/108

MBA 2009-11

Mr. Nathan Parnaby is appointed as the Chief Executive,

Europe & Asia of Standard Life in the year 2010. Nathan joined Standard Life in

1982 as Investment Manager, He is a Mathematics graduate from Oxford University

and the Member of the Securities Institute. He joined the Board of Directors in

December 2009. . He was appointed a Director of the Standard Life Investments’

board. He is responsible for all UK net funds

Mr. Norman K. Skeoch is currently the Chief Executive in Standard Life

Investments Limited and is responsible for overseeing Investment Process & Chief

Executive Officer Function. Prior to this, Mr. Skeoch was working with M/s. James

Capel & Co. holding the positions of UK Economist, Chief Economist, Executive

Director, Director of Controls and Strategy HSBS Securities and Managing

Director International Equities. He was also responsible for Economic and

Investment Strategy research produced on a worldwide basis. Mr. Skeoch joined the

Board of Directors in November 2005.

Abhineet Anand[0953870001] Page 18

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 19/108

MBA 2009-11

Mr. Gautam R. Divan is a practicing Chartered Accountant and is a Fellow of

the Institute of Chartered Accountants of India. Mr. Divan was the Former

Chairman and Managing Committee Member of Midsnell Group International, an

International Association of Independent Accounting Firms and has authored

several papers of professional interest. Mr. Divan has wide experience in auditing

accounts of large public limited companies and nationalized banks, financial and

taxation planning of individuals and limited companies and also has substantial

experience in structuring overseas investments to and from india.

Mr. Ranjan Pant is a global Management Consultant advising CEO/Boards on

Strategy and Change Management. Mr. Pant, until 2002 was a Partner & Vice-

President at Bain & Company, Inc., Boston, where he led the worldwide Utility

Practice. He was also Director, Corporate Business Development at General Electric

headquarters in Fairfield, USA. Mr. Pant has an MBA from The Wharton Schooland BE (Honors) from Birla Institute of Technology and Sciences.

Abhineet Anand[0953870001] Page 19

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 20/108

MBA 2009-11

Mr. Ravi Narain is the Managing Director & CEO of National Stock Exchange of

India Limited. Mr. Ravi Narain was a member of the core team to set-up the

Securities & Exchange Board of India (SEBI) and is also associated with various

committees of SEBI and the Reserve Bank of India (RBI).

Mr. A. K.T. Chari has joined HDFC Standard Life as a Director on March 10, 2010.

Mr. Chari has completed his Electrical Engineering from Madras University in

1962. He is associated with Infrastructure Development Finance Company Ltd.

(IDFC) for last 11 years. Currently he is handling project finance for infrastructure

projects at IDFC. Prior to this he was associated with Infrastructure Development

Bank of India (IDBI) from 1975 to 1999.

Abhineet Anand[0953870001] Page 20

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 21/108

MBA 2009-11

Mr. Gerald E. Grimstone was appointed Chairman of Standard Life in May 2007,

having been Deputy Chairman since March 2006. He became a director of the

Standard Life Assurance Company in July 2003. He is also Chairman of Candover

Investments plc and was appointed as one of the UK’s Business Ambassadors by the

Prime Minister in January 2009. Gerry held senior positions within the Department

of Health and Social Security and HM Treasury until 1986. He then spent 13 years

with Schroders in London, Hong Kong and New York, and was Vice Chairman of

Schroders’ worldwide investment banking activities from 1998 to 1999. He is the

Alternate Director to Mr. David Nish.

Mr. Michael G Connarty is responsible for Standard Life's investments in life

assurance Joint Ventures in India and China. He holds a degree in Law and MBA.

He has worked with Standard Life for 33 years in managerial positions covering a

number of fields such as Pensions law, International Marketing, Operational

Management, Strategy, Risk, Compliance, Company Secretarial and Banking. He

has acted as Project Manager for the start-up project of the Company in 2000. He is

the Alternate Director to Mr. Norman K. Skeoch.

Abhineet Anand[0953870001] Page 21

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 22/108

MBA 2009-11

Mr. Amitabh Chaudhry is the MD and CEO of HDFC Standard Life. Before joining

HDFC Standard Life, he was the MD and CEO of Infosys BPO and was also

heading an Independent Validation Services unit in Infosys Technologies. He started

his career with Bank of America delivering diverse roles ranging from Head of

Technology Investment Banking for Asia, Regional Finance Head for Wholesale

Banking and Global Markets and Chief Finance Officer of Bank of America (India).

He moved to Credit Lyonnais Securities in 2001 in Singapore where he headed their

investment banking franchise for South East Asia and structured finance practice

for Asia before joining Infosys BPO in 2005. Mr. Chaudhry completed his

Engineering in 1985 from Birla Institute of Technology and Science, Pilani and

MBA in 1987 from IIM, Ahmedabad.

Mr. Paresh Parasnis is the Executive Director and Chief Operating Officer of the

company. A fellow of the Institute of Chartered Accountants of India, he has been

associated with the HDFC Group since 1984. During his 16-year tenure at HDFC

Limited, he was responsible for driving and spearheading several key initiatives. As

one of the founding members of HDFC Standard life, Mr. Parasnis has been

responsible for setting up branches, driving sales and servicing strategy, leading

Abhineet Anand[0953870001] Page 22

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 23/108

MBA 2009-11

recruitment, contributing to product launches and performance management

system, overseeing new business and claims settlement, customer interactions etc.

Brief Profile of The Management Team

Mr. Amitabh Chaudhry

Managing Director and Chief Executive Officer

Mr. Amitabh Chaudhry is the Managing Director and Chief Executive Officer of

HDFC Standard Life. Before joining HDFC Standard Life in January 2010, he was

the Managing Director and CEO of Infosys BPO and was also heading an

Independent Validation Services unit in Infosys Technologies. Mr. Chaudhry

started his career with Bank of America delivering diverse roles ranging from Headof Technology Investment Banking for Asia, Regional Finance Head for Wholesale

Banking and Global Markets and Chief Finance Officer of Bank of America (India).

He moved to Credit Lyonnais Securities in 2001 in Singapore where he headed their

investment banking franchise for South East Asia and structured finance practice

for Asia before joining Infosys BPO in 2005. Mr. Chaudhry completed his

Engineering in 1985 from Birla Institute of Technology and Science, Pilani and

MBA in 1987 from IIM, Ahmedabad.

Abhineet Anand[0953870001] Page 23

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 24/108

MBA 2009-11

Mr. Paresh Parasnis

Executive Director and Chief Operating Officer

Mr. Paresh Parasnis is the Executive Director and Chief Operating Officer of

HDFC Standard Life. A fellow of the Institute of Chartered Accountants of India,

he has been associated with the HDFC Group since 1984. During his 16-year tenure

at HDFC Limited, he was responsible, for driving and spearheading several key

initiatives. As one of the founding members of HDFC Standard life, Mr. Parasnis

has been responsible for setting up branches, driving sales and servicing strategy,

leading recruitment, contributing to product launches and performance

management system, overseeing new business and claims settlement, customer

interactions etc.

Ms. Vibha Padalkar

Chief Financial Officer

Ms. Vibha Padalkar is the Chief Financial Officer of HDFC Standard Life.

Ms. Padalkar joined HDFC Standard Life in August 2008 after a seven year stint as

Executive vice President-Finance at WNS Global Services, a NYSE listed leading

global business process outsourcing company. Vibha’s key achievement during her

Abhineet Anand[0953870001] Page 24

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 25/108

MBA 2009-11

tenure at WNS was to lead a team that successfully completed the Group’s IPO on

the New York Stock Exchange in a short span of six months. Prior to WNS, Vibha

was with Colgate Palmolive India for 7 years, including a short posting to the

Group's New York headquarters. Ms.Padalkar became a member of the Institute of

Chartered Accountants in England and Wales in 1992, after having completed the

last part of her schooling as well as college education in London.

Mr. Ashley Rebello

Chief Actuary and Appointed Actuary

Mr. Ashley Rebello is the Chief Actuary and Appointed Actuary of HDFC Standard

Life. He completed his degree in Mathematics at Imperial College, London, before

joining Prudential UK in 1996. During his six years at Prudential he worked in

Product Development and Pricing, Valuation and in the Appointed Actuary's team.

Subsequently he worked as an actuarial consultant at PricewaterhouseCoopers for

five years, working for over 20 life insurance companies on a large variety of

assignments in the UK, Netherlands, Switzerland, Greece and the US. He joined

Standard Life in April 2008 and immediately moved to HDFC Standard Life.

Mr. Rebello is a Fellow of the Institute of Actuaries of India and Fellow of The

Institute of Actuaries (UK).

Abhineet Anand[0953870001] Page 25

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 26/108

MBA 2009-11

Mr. Vikram Mehta

General Manager, Sales and Marketing

Mr.Vikram Mehta heads the Sales and Marketing function for HDFC Standard

Life. Mr. Mehta joined HDFC Standard Life in February 2009. Before joining

HDFC Standard Life, he was associated with Citibank for 16 years serving various

responsibilities including the Head for Direct Sales - Citibank Credit Cards division

in Germany, Regional Director East - Citibank NA, India, and Acquisitions Head –

Credit Cards, Central and Eastern Europe cluster. Mr. Mehta started his career

with Reckitt and Colman (now Reckitt Benckiser) in 1988, and was associated with

the company for 4 years. He has been a part of FMCG and banking industry for

over 20 years. Mr. Mehta has completed Chemical Engineering from the Indian

Institute of Technology (IIT) Delhi and holds a PGDM from IIM Calcutta.

Mr. Prasun Gajri

Chief Investment Officer

Mr. Prasun Gajri is the Chief Investment Officer of HDFC Standard Life. Mr.

Gajri joined HDFC Standard Life in April 2009 with a rich experience of 14 years

Abhineet Anand[0953870001] Page 26

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 27/108

MBA 2009-11

in investments and banking industry. He started his career in 1995 with Citibank

and was associated with it for over 6 years delivering various roles. He joined Tata

AIG Life Insurance Company in October 2001 to start the investment function and

stayed there until April 2009, the last role being that of the Chief Investment

Officer. He holds a PGDM from IIM Ahmedabad and is also a CFA Charter holder.

Associate Companies

HDFC Limited

HDFC Bank

HDFC Mutual Fund

HDFC Sales

HDFC ERGO General Insurance

Abhineet Anand[0953870001] Page 27

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 28/108

MBA 2009-11

Other Companies

• HDFC Trustee Company Ltd.

• GRUH Finance Ltd.

• HDFC Developers Ltd.

• HDFC Property Ventures Ltd.

• HDFC Ventures Trustee Company Ltd.

• HDFC Investments Ltd.

• HDFC Holdings Ltd.

• Credit Information Bureau (India) Ltd

• HDFC Securities

Abhineet Anand[0953870001] Page 28

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 29/108

MBA 2009-11

THE COMPANY’S PRODUCT LINE

• Protection Plans

• HDFC Term Assurance Plan

• HDFC Premium Guarantee Plan

• HDFC Loan Cover Term Assurance Plan

• HDFC Home Loan Protection Plan

• Children's Plans

• HDFC Children's Plan

• HDFC Young Star Super

• HDFC Young Star Supreme

• HDFC YoungStar Super Suvidha

• HDFC Young Star Supreme Suvidha

• HDFC SL YoungStar Champion Suvidha

• Health Plans

• HDFC Critical Care Plan

• HDFC SurgiCare Plan

• Savings & Investment Plans

• HDFC Endowment Super

• HDFC Endowment Supreme

•

HDFC SimpliLife

• HDFC Endowment Super Suvidha

• HDFC Endowment Supreme Suvidha

• HDFC SL Endowment Champion Suvidha

Abhineet Anand[0953870001] Page 29

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 30/108

MBA 2009-11

• HDFC Wealth Builder

• HDFC Endowment Assurance Plan

• HDFC Money Back Plan

• HDFC Single Premium Whole of Life Insurance Plan

• HDFC Assurance Plan

• HDFC Savings Assurance Plan

• Retirement Plans

• HDFC Personal Pension Plan

• HDFC Pension Super

• HDFC Pension Supreme

• HDFC SL Pension Champion

• HDFC SL Unit Linked Pension Maximiser II

• HDFC Immediate Annuity

• Rural Products

• HDFC Gramin Bima Kalyan Yojana

• HDFC Gramin Bima Mitra Yojana

• HDFC Bima Bachat Yojana

• Social Products

• HDFC Development Insurance Plan

• Products Closed for Sale

(Serviced by Customer Service)

• HDFC Unit Linked Pension

• HDFC Unit Linked Pension Plus

Abhineet Anand[0953870001] Page 30

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 31/108

MBA 2009-11

• HDFC Unit Linked Endowment

• HDFC Unit Linked Endowment Plus

•

HDFC Unit Linked Endowment Suvidha

• HDFC Unit Linked Endowment Suvidha Plus

• HDFC Unit Linked Young Star Suvidha

• HDFC Unit Linked Young Star Suvidha Plus

• HDFC Unit Linked Young Star

• HDFC Unit Linked Young Star Plus

• HDFC Unit Linked Pension II

• HDFC Unit Linked Wealth Maximiser Plus

• HDFC Unit Linked Endowment Winner

• HDFC Unit Linked Wealth Multiplier

• HDFC Unit Linked Endowment II

• HDFC Unit Linked Endowment Plus II

• HDFC Unit Linked Enhanced Life Protection II

• HDFC Unit Linked YoungStar II

• HDFC Unit Linked YoungStar Plus II

• HDFC Unit Linked YoungStar Champion

Abhineet Anand[0953870001] Page 31

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 32/108

MBA 2009-11

FEATURES OF THE PRODUCT OF HDFCSLC

1) PROTECTION PLAN

Why do we need Protection Plans?

Protection Plans help you shield your family from uncertainties in life due to

financial losses in terms of loss of income that may dawn upon them incase of your

untimely demise or critical illness. Securing the future of one’s family is one of the

most important goals of life. Protection Plans go a long way in ensuring your

family’s financial independence in the event of your unfortunate demise or critical

illness. They are all the more important if you are the chief wage earner in your

family. No matter how much you have saved or invested over the years, sudden

eventualities, such as death or critical illness, always tend to affect your family

financially apart from the huge emotional loss.

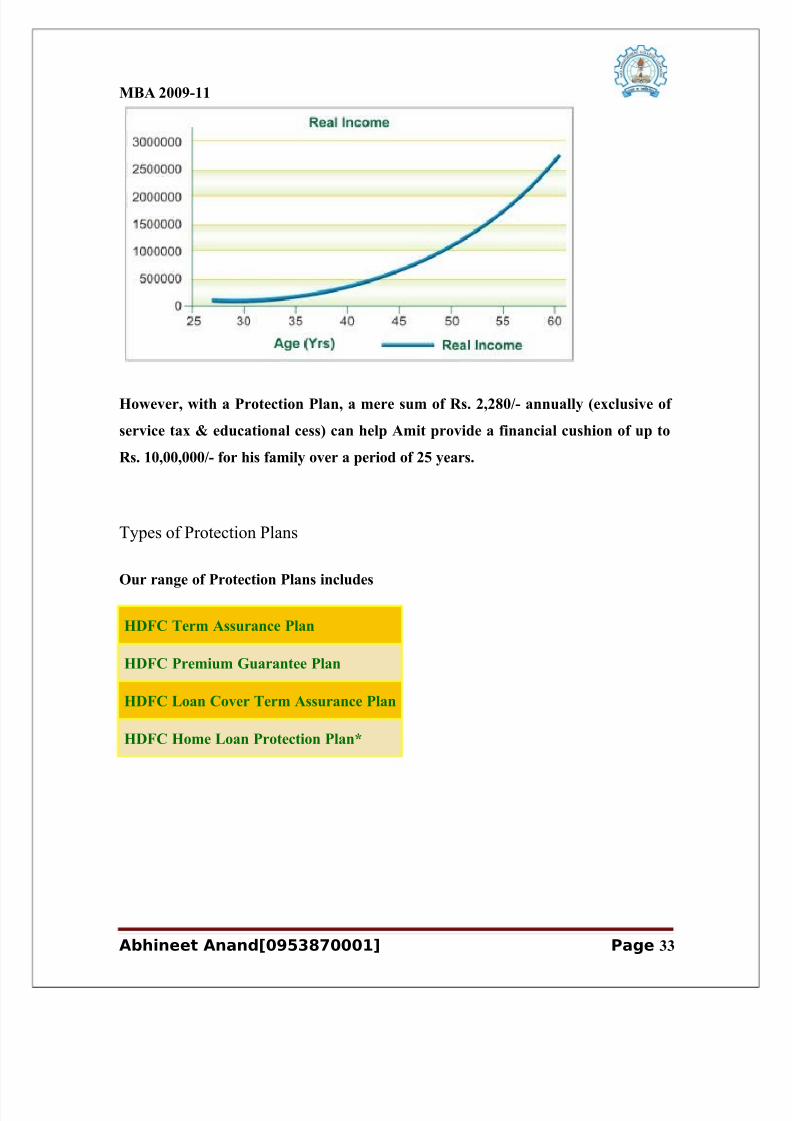

For instance, consider the example of Amit who is a healthy 25 year old guy with a

income of Rs. 1,00,000/- per annum. Let's assume his income increases at a rate of

10% per annum, while the inflation rate is around 4%; this is how his income chart

will look like, until he retires at the age of 60 years. At 50 years of age, Amit’s real

income would have been around Rs. 10,00,000/- per annum. However, in case of

Amit’s unfortunate demise at an early age of 42 years, the loss of income to his

family would be nearly Rs. 5,00,000/- per annum.

Abhineet Anand[0953870001] Page 32

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 33/108

MBA 2009-11

However, with a Protection Plan, a mere sum of Rs. 2,280/- annually (exclusive of

service tax & educational cess) can help Amit provide a financial cushion of up to

Rs. 10,00,000/- for his family over a period of 25 years.

Types of Protection Plans

Our range of Protection Plans includes

HDFC Term Assurance Plan

HDFC Premium Guarantee Plan

HDFC Loan Cover Term Assurance Plan

HDFC Home Loan Protection Plan*

Abhineet Anand[0953870001] Page 33

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 34/108

MBA 2009-11

2) Retirement Plans

• Monetary security

• Financial independence even after retirement

• Live carefree in your golden years

Retirement Plans provide you with financial security so that when your professional

income starts to ebb, you can still live with pride without compromising on your

living standards. By providing you a tool to accumulate and invest your savings,

these plans give you a lump sum on retirement, which is then used to get regular

income through an annuity plan. Given the high cost of living and rising inflation,

employer pensions alone are not sufficient. Pension planning has therefore become

critical today.

India’s average life expectancy is slated to increase to over 75 years by 2050 from

the present level of close to 65 years. Life spans have been increasing due to better

health and sanitation conditions in the country. However, the average number of

years of employment has not been rising commensurately. The result is an increase

in the number of post-retirement years. Accordingly, it has become necessary toensure regular income for life after retirement, so that you can live with pride and

enjoy your twilight years.

Priorities at different stages of life:-

Abhineet Anand[0953870001] Page 34

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 35/108

MBA 2009-11

However, skyrocketing costs can throw even a well-laid plan off balance. With costs

rising every day, you can just imagine how high they will be when you are ready to

hang up your boots. So, what should you do to counter this? It’s time to plan your

retirement and that too sooner than later.

.

Abhineet Anand[0953870001] Page 35

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 36/108

MBA 2009-11

The above illustration shows how with each passing year your annual savings

requirement would increase. For instance, if you are 30 years old and plan to retire

at 60, then, with a current annual expenditure of Rs. 3,00,000/- , you would need a

corpus in excess of Rs. 2,00,00,000/- to maintain your living standards, assuming you

live till 85 years and the inflation rate is 4%. To build this retirement corpus, you

need to invest Rs 3,60,000/- per annum in a retirement plan that offers 8% returns

per annum. In case you delay planning your retirement by 5 years then the

investment amount would increase to Rs 6,90,000/- per annum.

Types of Retirement Plans

Our range of Retirement Plans includes

Type Conventional Plans Unit Linked Insurance Plans

Regular

Premium

HDFC Personal Pension

Plan

HDFC Pension Super

HDFC Pension Supreme

HDFC SL Pension Champion

Single

Premium/

Investment

HDFC SL Unit Linked Pension

Maximiser II

Let Us Help You Choose The Right Plan For You

Would you prefer to take a

a) Traditional plan in which the insurance company takes all the investment

decisions on your behalf over the entire policy term

b) Return on the policy is in the form of bonus payable on maturity

Abhineet Anand[0953870001] Page 36

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 37/108

MBA 2009-11

Would you prefer to take a Unit Linked plan, where

a)You can regularly monitor and review your investment decision according to your

need

b) The choice of investment and the investment risk you take is in your control.

c) Return is in the form of growth in the NAV

• HDFC Personal Pension Plan

• HDFC Pension Super

• HDFC Pension Supreme

• HDFC SL Pension Champion

• HDFC SL Unit Linked Pension Maximiser II

• HDFC Immediate Annuity

3)Savings & Investment Plans

• Dual benefit of protection and long term savings

• Provide an assured sum for future needs

• Inculcate a habit of regular savings

Why do we need Savings & Investment Plans?

You have always given your family the very best. And there is no reason why they

shouldn’t get the very best in the future too. As a judicious family man, your

Abhineet Anand[0953870001] Page 37

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 38/108

MBA 2009-11

priority is to secure the well-being of those who depend on you. Not just for today,

but also in the long term. More importantly, you have to ensure that your family’s

future expenses are taken care, even if something unfortunate were to happen to

you.

A big factor that you need to consider while building your wealth is inflation. It has

a dual impact on your hard-earned savings. Inflation not only erodes your current

purchasing power but also magnifies your monetary requirements for the future.

Sample this: An 35 Year individual needs to invest Rs. 36,000/- per year with 8%

returns to build a corpus of Rs. 10,00,000/- by the age of 50 Years.

However, Rs. 10,00,000/- after 15 years would be worth roughly around half of what

it is today once adjusted for inflation at the rate of 4%. Therefore, an individual will

need to save nearer to Rs 50,000/- annually to reach your targeted savings at the age

of 50 Years, if you consider inflation.

Our Savings & Investment Plans provide you the assurance of lump sum funds for

your and your family’s future expenses. While providing an excellent savings tool

for your short term and long term financial goals, these plans also assure your

family a certain sum by way of an insurance cover. With HDFC Standard Life’s

Abhineet Anand[0953870001] Page 38

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 39/108

MBA 2009-11

range of Saving & Investment Plans, you can therefore ensure that your family

always remains financially independent, even if you are not around.

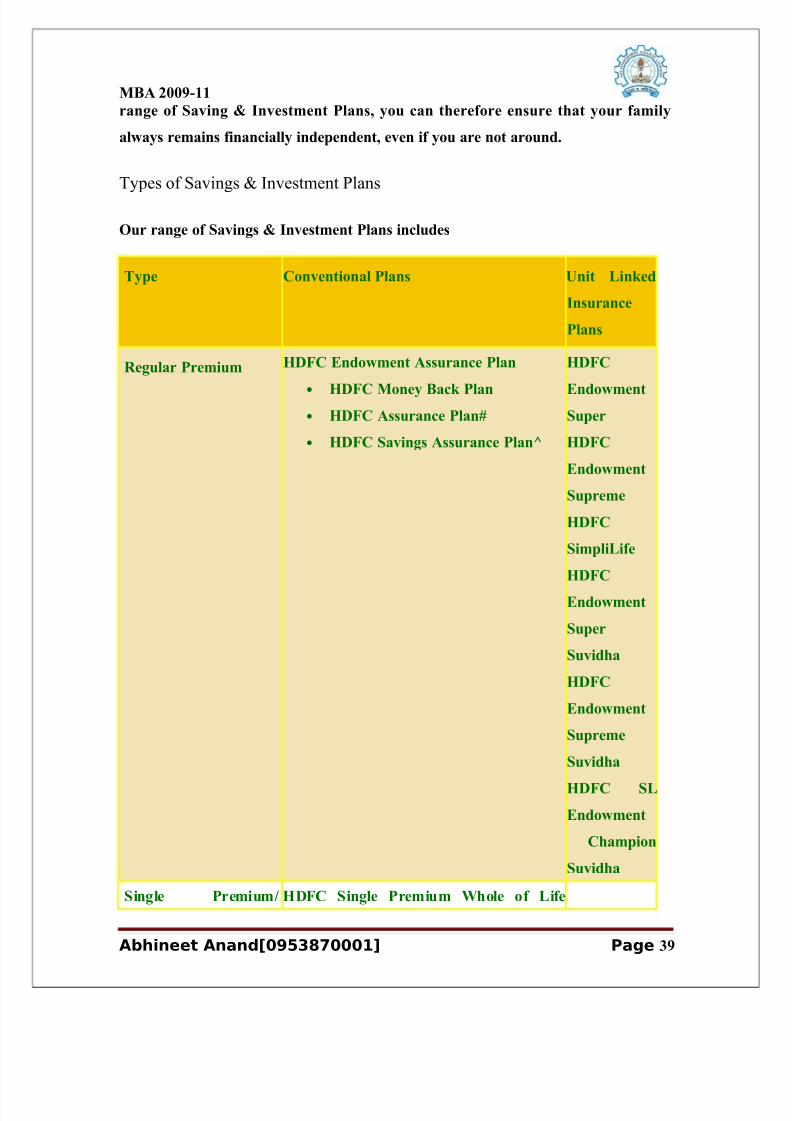

Types of Savings & Investment Plans

Our range of Savings & Investment Plans includes

Type Conventional Plans Unit Linked

Insurance

Plans

Regular Premium HDFC Endowment Assurance Plan

•

HDFC Money Back Plan• HDFC Assurance Plan#

• HDFC Savings Assurance Plan^

HDFC

EndowmentSuper

HDFC

Endowment

Supreme

HDFC

SimpliLife

HDFC

Endowment

Super

Suvidha

HDFC

Endowment

Supreme

Suvidha

HDFC SL

Endowment

Champion

Suvidha

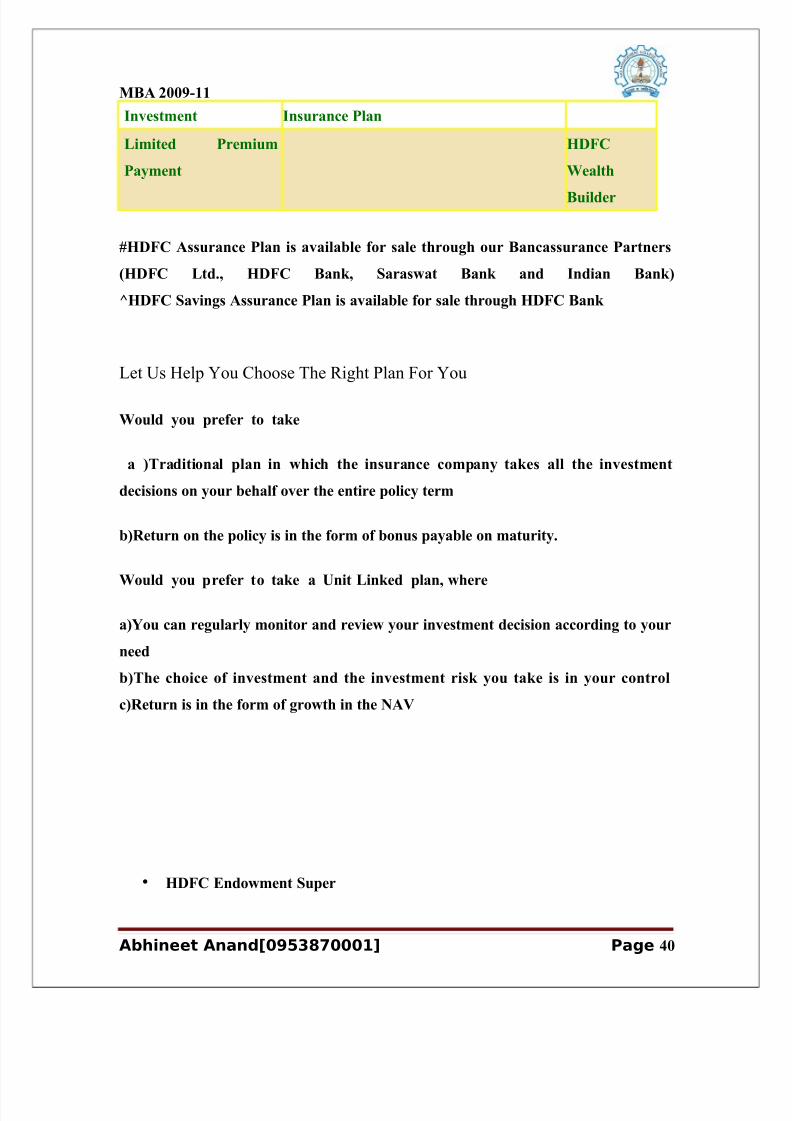

Single Premium/ HDFC Single Premium Whole of Life

Abhineet Anand[0953870001] Page 39

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 40/108

MBA 2009-11

Investment Insurance Plan

Limited Premium

Payment

HDFC

Wealth

Builder

#HDFC Assurance Plan is available for sale through our Bancassurance Partners

(HDFC Ltd., HDFC Bank, Saraswat Bank and Indian Bank)

^HDFC Savings Assurance Plan is available for sale through HDFC Bank

Let Us Help You Choose The Right Plan For You

Would you prefer to take

a )Traditional plan in which the insurance company takes all the investment

decisions on your behalf over the entire policy term

b)Return on the policy is in the form of bonus payable on maturity.

Would you prefer to take a Unit Linked plan, where

a)You can regularly monitor and review your investment decision according to your

need

b)The choice of investment and the investment risk you take is in your control

c)Return is in the form of growth in the NAV

• HDFC Endowment Super

Abhineet Anand[0953870001] Page 40

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 41/108

MBA 2009-11• HDFC Endowment Supreme

• HDFC SimpliLife

• HDFC Endowment Super Suvidha

• HDFC Endowment Supreme Suvidha

• HDFC SL Endowment Champion Suvidha

• HDFC Wealth Builder

• HDFC Endowment Assurance Plan

• HDFC Money Back Plan

• HDFC Single Premium Whole of Life Insurance Plan

• HDFC Assurance Plan

• HDFC Savings Assurance Plan

4)Health Plans

• Secure your health costs

• Financial independence despite illnesses

• Meeting medical expenses effortlessly

Why do we need Health Plans?

Health plans give you the financial security to meet health related contingencies.

Due to changing lifestyles, health issues have acquired completely new dimension

overtime, becoming more complex in nature. It becomes imperative then to have a

Abhineet Anand[0953870001] Page 41

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 42/108

MBA 2009-11

health plan in place, which will ensure that no matter how critical your illness is, it

does not impact your financial independence.

In the race to excel in our professional lives and provide the best for our loved ones,

we sometimes neglect the most important asset that we have – our health. With

increasing levels of stress, negligible physical activity and a deteriorating

environment due to rapid urbanization, our vulnerability to diseases has increased

at an alarming rate.

Source: National Commission on Macroeconomics and Health Report 2005.

Note: Current figures are for the year 2000(Cardiovascular diseases)), 2001 (COPD

and Asthma), 2004 (Cancer) and 2005(Diabetes and Mental Health). All figures

above are on a per lakh basis.

As can be seen in the above chart, lifestyle diseases are set to spread at disturbing

rates. The result – increased expenditure. In many cases, people need to borrow

money or sell assets to cover their medical expenses. All it takes is a suitable plan to

Abhineet Anand[0953870001] Page 42

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 43/108

MBA 2009-11

help you overcome the financial woes related to your health by paying marginal

amounts as premiums. For example, if you are 30 years old, then a mere sum of

approximately Rs 3500* annually (exclusive of taxes) can provide you a health

insurance plan of Rs 5 lakh over a period of 20 years, and a worry-free future foryou and your family.

*Note: The assumption is based on the HDFC Critical Care Plan. The figure is only

indicative and the actual premium may depend upon numerous factors such as age,

sum assured, gender, policy term, premium payment frequency and additional

benefits opted for. It also differs from plan to plan and option to option

Types Of Health Plans

Our range of Health Plans includes

HDFC Critical Care Plan

HDFC SurgiCare Plan

Let Us Help You Choose The Right Plan For You

I wish to have protection against critical illnesses that I may suffer from.

I prefer to financially safeguard my self against major surgical procedures that I

may undergo.

Children’s Plans

Abhineet Anand[0953870001] Page 43

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 44/108

MBA 2009-11

• Helps you secure your child’s dreams

• Economic support when your child needs it most

• Funding major milestones

What is the need of Children’s Plans?

Children’s Plans helps you save so that you can fulfill your child’s dreams and

aspirations. These plans go a long way in securing your child’s future by financing

the key milestones in their lives even if you are no longer around to oversee them. As

a parent, you wish to provide your child with the very best that life offers, the best

possible education, marriage and life style.

Most of these goals have a price tag attached and unless you plan your finances

carefully, you may not be able to provide the required economic support to your

child when you need it the most. For example, with the high and rising costs of

education, if you are not financially prepared, your child may miss an opportunity

of a lifetime.

Today, a 2-year MBA course at a premiere management institute would cost you

nearly Rs. 3,00,000/- At a assumed 6% rate of inflation per annum, 20 years later,

you would need almost Rs. 9,07,680/- to finance your child's MBA degree.

An illustration of how education expenses could rise with passing time due to

inflation

Abhineet Anand[0953870001] Page 44

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 45/108

MBA 2009-11Source: HDFC

Standard Life Survey 2008. Inflation assumed as 6% p.a.

So, how can you cope with these costs? Children’s Plans help you save steadily over

the long term so that you can secure your child’s future needs, be it higher

education, marriage or anything else. A small sum invested by you regularly can

help you build a decent corpus over a period of time and go a long way in providing

your child a secured financial future alongwith

Types of Children’s Plans

Our range of Children's Plans includes

Conventional Plans Unit Linked Insurance Plans

HDFC Children's

Plan

HDFC YoungStar Super

HDFC YoungStar SupremeHDFC YoungStar Super Suvidha

HDFC YoungStar Supreme Suvidha

HDFC SL YoungStar Champion Suvidha

Abhineet Anand[0953870001] Page 45

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 46/108

MBA 2009-11

Let Us Help You Choose The Right Plan For You

Would you prefer to take a

a)Traditional plan in which the insurance company takes all the investment

decisions on your behalf over the entire policy term

b)Return on the policy is in the form of bonus payable on maturity.

Would you prefer to take a Unit Linked plan, where

a)You can regularly monitor and review your investment decision according to your

need

b)The choice of investment and the investment risk you take is in your control

c)Return is in the form of growth in the NAV

• HDFC Children's Plan

• HDFC YoungStar Super

• HDFC YoungStar Supreme

• HDFC YoungStar Super Suvidha

• HDFC YoungStar Supreme Suvidha

• HDFC SL YoungStar Champion Suvidha

Abhineet Anand[0953870001] Page 46

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 47/108

MBA 2009-11

Group Plans

Group Term Insurance Plan

This plan offers Protection to an organisation's employees

Group Term Insurance Plan

GROUP TERM INSURANCE PLAN

Whatever the business – It’s the people who make it a success. Everybody requires

some type of life insurance, especially when others depend on them financially

The Group Term Insurance (GTI) plan meets this need and serves as an ideal way

for companies to reinforce their bond with their employees. The sort of needs, you,

as an employer need to cater to could be in form of:

• Employee benefits

• Cover for housing or vehicle loans given by you to your employees

• A GTI cover for future service gratuity liability to be taken along with the

HDFC Group Unit Linked Plan

The HDFC Group Term Insurance is a cost-effective plan that addresses these

needs. In addition you have the choice to opt for a GTI with an experience discount

feature ("Profit Share"), where a discount is given on future premiums in case of

favorable claim experience (subject to group size).

Abhineet Anand[0953870001] Page 47

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 48/108

MBA 2009-11

The HDFC group term insurance plan will have the following structure:

• One year renewable term insurance plan

• One master policy issued covering all members of the group

• Sum assured is payable on death (either due to natural causes or accidents)

The plan covers death due to any cause; accidental or natural, and hence is more

comprehensive than Group Personal Accident Insurance. Several multinational

corporations, large Indian companies, foreign banks and software companies have

already chosen the HDFC Group Term Insurance, an innovative product from

HDFC Standard Life Insurance, to protect their employees.

Optional Rider Benefits

• Accidental Death Benefit

• Total Permanent Disability

• Total Permanent and Partial Diability Benefit

• Critical Illness Benefit

• Terminal Illness Benefi

Abhineet Anand[0953870001] Page 48

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 49/108

MBA 2009-11

Group Variable Term Insurance Plan

This Protection plan is a tailor made insurance policy for third party institutions

Group Variable Term Insurance Plan

GROUP VARIABLE TERM INSURANCE

The Group Variable Term Insurance is a tailor made insurance policy for third

party institutions. HDFC Standard Life Insurance Company will offer life insurance

to customers of one or more of the third party’s specific products in order that in

the event of their death, there will be a lump sum available.

The Group Variable Term Insurance:

• On death, will pay a lump sum known as a sum assured. The sum assured

varies over time in order that the customer receives the cover that they need

• Is a group policy

• Has no lengthy underwriting procedure

• Is simple to administer

The policy is without any participation in the insurer’s

profits

Abhineet Anand[0953870001] Page 49

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 50/108

MBA 2009-11

Group Gratuity Solutions

This plan is a flexible and cost effective way to fund your Gratuity liability

Group Unit Linked Plan

Gratuity schemes

GROUP UNIT LINKED PLAN

Gratuity Schemes

Most employers have a statutory obligation to pay a gratuity to its employees on

termination of employment. This gratuity is in the form of a one-off payment made

on termination of employment. It depends on salary and number of years of service,

so will therefore increase with time. The HDFC Group Unit Linked plan is a new

and innovative unit-linked plan, which offer employers and gratuity scheme trustees

a flexible and cost effective way to fund this gratuity liability. The plan helps a

corporate by:

• Building a fund systematically, which will be used to meet your future

gratuity liability

• Providing the opportunity to maximise investment returns and thus provide

the benefit in a cost-effective manner One factor that helps you to maximise

the investment returns is low charges. Our charges are the lowest in the

industry and therefore can improve your long-term returns.

Abhineet Anand[0953870001] Page 50

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 51/108

MBA 2009-11

Group superannuation plan

This plan helps you manage your employees Superannuation funds

Group Unit Linked Plan

Superannuation Schemes

GROUP UNIT LINKED PLAN

Superannuation Schemes

Many organisations realise that the statutory requirement benefits are not sufficient

for their trusted employees to continue enjoying their quality of life after they retire.

The HDFC Group Unit Linked Plan is a great way for an employer to show his

employees that he not only takes care of them while in service, but has also ensured

that they can lead a comfortable life after retirement.

The HDFC Group Unit Linked plan is also a great employee retention and

motivation tool that helps employers to fund their employees’ post-retirement needs

in a systematic, tax-efficient and cost-effective manner. Moreover, as a unit-linked

plan, it gives you tremendous flexibility and freedom to customise individual

retirement funds for your employees based on their appetite for risk and the stage of

life they are in.

Abhineet Anand[0953870001] Page 51

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 52/108

MBA 2009-11

This plan helps an organisation by:

• Providing an investment vehicle to trustees for making the contribution for

each member

• Helping build a substantial retirement fund for each member

• Presenting a potential to provide higher benefits to employees

• Offering tax benefits for investments made through the formation of a trust

Group Leave Encashment Solution

This plan is an effective way to fund your company's Leave Encashment liability

Group Unit Linked Plan Leave

Encashment Schemes

GROUP UNIT LINKED PLAN

Leave Encashment Schemes

Many employers provide their employees with the option of encashing their leave to

their credit at the time of retirement or resignation. Accounting Standard 15

requires that an actuarial valuation of a company leave encashment liability be

carried out and reflected in the books of accounts. The HDFC Group Unit Linked

Plan is an innovative plan, which offers employers a flexible and cost effective way

to fund this Leave Encashment liability. The plan helps an organisation by:

Abhineet Anand[0953870001] Page 52

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 53/108

MBA 2009-11

• Creating a fund that can be built up to meet your future leave encashment

liability

• Providing the opportunity to maximise investment returns and thus provide

the benefit in a cost-effective manner

One factor that helps maximise investment returns is low charges. Our fund

management charges are the lowest in the industry today and therefore can improve

your long-term returns

HDFC SL Group Savings Plan

Exclusive plans that will let your cherished member's save effectively

HDFC SL GROUP SAVINGS PLAN

As a company or an affinity group, you want to express to your group members that

you care for them, and want them to have stronger financial future.

HDFCSLC GROUP SAVINGS PLAN is a simple conventional group plan wherein

the company/affinity group is the policyholder & the group members

/employees/depositors are the scheme members.

This ‘with profits’ group plan would enable your scheme members to

• Provide financial protection to their loved ones

• Build savings in a simple & systematic manner

Abhineet Anand[0953870001] Page 53

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 54/108

MBA 2009-11

• Pay premiums only for a limited period of 5 years

• Is simple to administer

• Is without lengthy documentation

Abhineet Anand[0953870001] Page 54

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 55/108

MBA 2009-11

Marketing strategies of HDFCSLC In India

HDFC Standard Life believes that establishing a strong and ethical foundation is an

essential prerequisite for long-term sustainable growth. To ensure this, they have

concentrated our focus on expansion of branch network, organizing an efficient and

well trained sales force, and setting up appropriate systems and processes with

optimum use of technology. As all these areas form the basic infrastructure for

establishing the highest possible customer service standards.

The core values are drilled down to all levels of employees, as these are inviolable.

We continue to promote high integrity in business practices and shun short cuts and

unethical practices, as we wish to be perceived as an institution with high moralstanding. Since our inception in 2000, when the Indian insurance space was opened

for private participation, we have consistently focused on setting benchmarks in all

aspect on insurance business. Being the first private player to be registered with the

IRDA and the first to issue a policy on December 12, 2000,

Strong Promoter

HDFC Standard Life is a strong, financially secure business supported by two

strong and secure promoters – HDFC Ltd and Standard Life. HDFC Ltd’s excellent

brand strength emerges from its unrelenting focus on corporate governance, high

standards of ethics and clarity of vision. Standard Life is a strong, financially secure

business and a market leader in the UK Life & Pensions sector.

Preferred and Trusted Brand

Their brand has managed to set a new standard in the Indian life insurance

communication space. We were the first private life insurer to break the ice using

the idea of self-respect instead of ‘death’ to convey our brand proposition (Sar Utha

Ke Jiyo). Today, they are one of the few brands that customers recognize, like and

Abhineet Anand[0953870001] Page 55

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 56/108

MBA 2009-11

prefer to do business. Moreover, our brand thought, Sar Utha Ke Jiyo, is the most

recalled campaign in its category.

Investment Philosophy

They follow a conservative investment management philosophy to ensure that their

customer’s money is looked after well. The investment policies and actions are

regularly monitored by a formal Investment Committee comprising non-executive

directors and the Principal Officer & Executive Director.

As a life insurance company, they understand that customers have invested their

savings with us for the long term, with specific objectives in mind. Thus, our

investment focus is based on the primary objective of protecting and generating

good, consistent, and stable investment returns to match the investor’s long-term

objective and return expectations, irrespective of the market condition.

Need-Based Selling Approach

Despite the criticality of life insurance, sales in the industry have been characterized

by over reliance on tax benefits and limited advice-based selling. Our eight-step

structured sales process ‘Disha’ however, helps customers understand their latent

needs at the first instance itself without focusing on product features or tax benefits.

Need-based selling process, 'Disha', the first of its kinds in the industry, looks at the

whole financial picture. Customers see a plan not piecemeal product selling

Risk Control Framework

HDFC Standard Life has fully implemented a risk control framework to ensure that

all types of risks (not just financial) are identified and measured. These are

regularly reported to the board and this ensures that the company management and

board members are fully aware of any risks and the actions taken to ensure they are

mitigated

Abhineet Anand[0953870001] Page 56

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 57/108

MBA 2009-11

Focus on Training

Training is an integral part of our business strategy. Almost all employees have

undergone training to enhance their technical skills or the softer behavioural skills

to be able to deliver the service standards that our company has set for itself.

Besides the mandatory training that Financial Consultants have to undergo prior to

being licensed, we have developed and implemented various training modules

covering various aspects including product knowledge, selling skills, objection

handling skills and so on.

Focus on long term value

HDFC Standard Life do not focus in the business of ramping up the topline only,

but to create maximization of stakeholder's value. Today, we are extremely satisfied

with the base that we have created for the long-term success of this company.

Transparent Dealing

They are one of the few companies whose product details, pricing, clauses are

clearly communicated to help customers take the right decision.

Strict compliance with Regulations

They have initiated and implemented many new processes, some of which were

found useful by the IRDA and later made mandatory for the entire industry. The

agents who successfully completed this training only, were authorized by the

company to sell ULIPs. This has now been made compulsory by IRDA for all

insurance companies under the new Unit Linked Guidelines.

Abhineet Anand[0953870001] Page 57

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 58/108

MBA 2009-11

Diversified Product Portfolio

HDFC Standard Life’s wide and diversified product portfolio help individuals meet

their various needs, be it:

• Protection: Need for a sound income protection in case of your

unfortunate demise

• Health: Cover for health related exigencies

• Savings: Save for the milestones and protect your savings too

• Pension: Need to save for a comfortable life post retirement

• Investment: Need to ensure long-term real growth of your

money

Abhineet Anand[0953870001] Page 58

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 59/108

MBA 2009-11

COMPETITORS OF HDFCSLC

1. Max New York Life Insurance Co. Ltd.

. Max New York Life Insurance Company Limited is a joint venture that brings

together two large forces - Max India Limited, a multi-business corporate, together

with New York Life International, a global expert in life insurance. With their

various Products and Riders, there are more than 400 product combinations to

choose from. They have a national presence with a network of 57 offices in 37 cities

across India

2. ICICI Prudential Life Insurance Company Ltd

ICICI Prudential Life Insurance Company is a joint venture between ICICI Bank, a

premier financial powerhouse and prudential plc, a leading international financial

services group headquartered in the United Kingdom. ICICI Prudential was

amongst the first private sector insurance companies to begin operations in

December 2000 after receiving approval from Insurance Regulatory Development

Authority (IRDA). The company has a network of about 56,000 advisors; as well as

7 banc assurance and 150 corporate agent tie-ups.

3. Om Kotak Mahindra Life Insurance Co. Ltd.

Kotak Mahindra Old Mutual Life Insurance Ltd. is a joint venture between Kotak

Mahindra Bank Ltd. (KMBL), and Old Mutual plc.

Abhineet Anand[0953870001] Page 59

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 60/108

MBA 2009-11

4.Birla Sun Life Insurance Company Ltd.

Birla Sun Life Insurance Company is a joint venture between Aditya Birla Group

and Sun Life financial Services of Canada.

Other life insurance companies

Tata AIG Life Insurance Company Ltd.

SBI Life Insurance Company Limited

ING Vysya Life Insurance Company Private Limited

Allianz Bajaj Life Insurance Company Ltd.

Metlife India Insurance Company Pvt. Ltd.

AMP SANMAR Assurance Company Ltd.

Dabur CGU Life Insurance Company Pvt. Ltd

GENERAL INSURANCE COMPANIES

1.Royal Sundaram Alliance Insurance Company Limited

The joint venture bringing together Royal & Sun Alliance Insurance and Sundaram

Finance Limited started its operations from March 2001. The company is Head

Quartered at Chennai, and has two Regional Offices, one at Mumbai and another

one at New Delhi

2.Bajaj Allianz General Insurance Company Limited

Bajaj Allianz General Insurance Company Limited is a joint venture between Bajaj

Auto Limited and Allianz AG of Germany. Both enjoy a reputation of expertise,

stability and strength.

Abhineet Anand[0953870001] Page 60

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 61/108

MBA 2009-11

Bajaj Allianz General Insurance received the Insurance Regulatory and

Development Authority (IRDA) certificate of Registration (R3) on May 2nd, 2001 to

conduct General Insurance business (including Health Insurance business) in India.

The Company has an authorized and paid up capital of Rs 110 crores. Bajaj Auto

holds 74% and the remaining 26% is held by Allianz, AG, Germany.

3. ICICI Lombard General Insurance Company Limited

ICICI Lombard General Insurance Company Limited is a joint venture between

ICICI Bank Limited and the US-based $ 26 billion Fairfax Financial Holdings

Limited. ICICI Bank is India's second largest bank, while Fairfax Financial

Holdings is a diversified financial corporate engaged in general insurance,

reinsurance, insurance claims management and investment management. Lombard

Canada Ltd, a group company of Fairfax Financial Holdings Limited, is one of

Canada's oldest property and casualty insurers. ICICI Lombard General Insurance

Company received regulatory approvals to commence general insurance business in

August 2001.

4. Cholamandalam General Insurance Company Ltd.

Cholamandalam MS General Insurance Company Limited (Chola-MS) is a joint

venture of the Murugappa Group & Mitsui Sumitomo. Chola-MS commenced

operations in October 2002 and has issued more than 1.4 lakh policies in its first

calendar year of operations. The company has a pan-Indian presence with offices in

Chennai, Hyderabad, Bangalore, Kochi, Coimbatore, Mumbai, Pune, Indore,

Ahmedabad, Delhi, Chandigarh, Kolkata and Vizag.

Abhineet Anand[0953870001] Page 61

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 62/108

MBA 2009-11

5. TATA AIG General Insurance Company Ltd.

Tata AIG General Insurance Company Ltd. is a joint venture company, formedfrom the Tata Group and American International Group, Inc. (AIG). Tata AIG

combines the strength and integrity of the Tata Group with AIG's international

expertise and financial strength. The Tata Group holds 74 per cent stake in the two

insurance ventures while AIG holds the balance 26 per cent stake.

Tata AIG General Insurance Company, which started its operations in India on

January 22, 2001, offers the complete range of insurance for automobile, home,

personal accident, travel, energy, marine, property and casualty, as well as several

specialized financial lines.

6. Reliance General Insurance Company Limited.

7. IFFCO Tokio General Insurance Co. Ltd

8. Export Credit Guarantee Corporation Ltd.

9. HDFC-Chubb General Insurance Co. Ltd.

Abhineet Anand[0953870001] Page 62

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 63/108

MBA 2009-11

GOVERNMENT POLICIES

The Insurance Act 1938, which came into effect from 1st july 1939, and was

amended in 1950 and later in 1999, is the principal enactment relating to the

business of insurance in India. The act contains provisions regarding licensing of

agents and their remunerations, prohibition of rebates, and protection of

policyholder’s interest

Till the constitution of the IRDA Act in 1999, the controller of insurance was

responsible for the administration of the insurance Act since 1999, the IRDA has

replaced the controller of insurance.

The insurance Act vest the IRDA with power to

1. Register insurance companies & also cancel their registration.

2. Monitor & certify the soundness of the terms of life insurance

business

3. Make reggulation relating to the conduct of the business of the

insurance

4. Inspect the document of insurers5. Appoint additional directors

6. Issue directions

7. Take over the management of an insurer & appoint administrators

8. Adjudicate on disputes between isurers and intermediaries or between

intermediaries.

9. Decide on disputes relating to settlement of claims of amounts not

exceeding 2000.

Abhineet Anand[0953870001] Page 63

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 64/108

MBA 2009-11

TAXATION ASPECTS

The tax law of India have always encouraged people to save through life insurance

and other instruments, by providing relief from tax liabilities. The taxation law can

change at any time through budget provisions or otherwise. The agent should keep

himself up-to-date with the changes.

Any sum received under a life insurance policy,including the bonus additions is

exempt from income tax. That means that income tax does not have to be paid on

policy claim & surrender amounts. This is subject to the premium being not more

than 20% of the sum assured on any policy during the year. There are someexceptions to this rule.one is the amount to be refunded under certain plans, meant

for the handicapped dependents. The other is a claim under a key-man insurance

policy.

The income of the assesse is reduced by the aggregate of amounts paid towards

insurance premiums contribution to provident fund or approved superannuation

funds, NSC etc,upto a maximum amount of 1 lakh. If the premium during the policy

exceeds 20% of SA, only 20% will be taken into account for debate.

Commuted values of pensions are exempt from income tax.

Abhineet Anand[0953870001] Page 64

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 65/108

MBA 2009-11

Achievements

2006

The year witnessed the launch of ‘My Account’, a web-based facility with various

policy servicing options such as switch, premium redirection to be executed by

clients, without recourse to visiting a branch

As against a regulatory requirement of writing 18% of all policies in rural areas, the

company issued over 1, 21,000 policies accounting for more than 23% of all policies

issued during the year.

The company had been awarded the “Intelligent Enterprise” Award by the Express

Computer Magazine – Part of the Indian Express Group, for investing in workflow

and imaging technology which helped in increasing volumes without affecting

service standards.

Was selected as the '4Ps Power Brand 2006', for being one of India's Top 25 'Most

Innovative Companies' in an exclusive survey conducted by ICMR (Indian Council

of Market Research) and 4Ps - Business and Marketing (a Business and Marketing

magazine published by Planman Media).

Biggest NGO covered on 28th March 2006 with 14000 lives

2007

HDFCSL expanded its reach in the Bancassurance channel by arrangements with

co-operative banks in the rural areas.

Continued to increase its focus on quality service, by putting in place a robust

mechanism to capture ‘Voice of the Customer’ through service audits across its

Abhineet Anand[0953870001] Page 65

8/4/2019 Report of Abhineet

http://slidepdf.com/reader/full/report-of-abhineet 66/108

MBA 2009-11

offices. This was complemented by use of technology that enabled capture of all

interactions with customers across all touch points

Sar Utha Ke Jiyo was honoured as ‘Among India’s 60 Glorious Advertising

Moments. The advertisements of the company were ranked 6th amongst ‘The 10

most effective Advertisements’ in September 2007.

Received the PCQuest Best IT Implementation Award 2007 for Wonders, its path-

breaking implementation of an enterprise-wide workflow system. In addition the