report on valuation of distribution assets of mula pravara ...mercindia.org.in/pdf/order 58...

TRANSCRIPT

1

Report on valuation of distribution assets of Mula Pravara Electric

Co-operative Society Ltd in accordance with the judgement issued by ATE in appeal

Number 221 of 2014

This report is submitted to the Maharashtra Electricity Regulatory Commission on the 31st of

March, 2016

Prepared by:

44, Maker Chambers III, Nariman Point, Mumbai- 400021 022-49265000

2

Table of Contents

Chapter 1 Executive Summary ........................................................................................................ 6

1.1 Background ...................................................................................................................................... 6

1.2 Scope of work .................................................................................................................................. 6

1.3 Sampling methodology..................................................................................................................... 7

1.4 Valuation methodology..................................................................................................................... 7

1.5 User charge determination ............................................................................................................... 9

1.6 Applicability of wheeling charge to the current case ...................................................................... 10

Chapter 2 Introduction .................................................................................................................... 11

2.1 Mula-Pravara Electric Co-operative Society Ltd ............................................................................ 11

2.2 Sequence of events ....................................................................................................................... 13

Chapter 3 Scope & Methodology ................................................................................................... 15

3.1 Scope of the assignment................................................................................................................ 15

3.2 Methodology for physical verification ............................................................................................. 16

3.3 Methodology for valuation .............................................................................................................. 18

3.4 Scrutiny of Asset Register and other documents ........................................................................... 20

3.5 Approach to physical verification ................................................................................................... 21

Chapter 4 Technical assessment .................................................................................................. 24

4.1 Observations from physical verification ......................................................................................... 24

4.2 Survey observations ....................................................................................................................... 25

4.3 Assessment of useful life of assets ................................................................................................ 31

Chapter 5 Valuations of assets of MPECS ................................................................................... 34

5.1 Valuation as per replacement cost ................................................................................................. 35

5.2 Reconciliation with ASCI report ..................................................................................................... 39

Chapter 6 User charge determination ........................................................................................... 40

6.1 User charges .................................................................................................................................. 40

6.2 Payout to MPECS going forward ................................................................................................... 44

6.3 Applicability of wheeling charge to the current case ......................................................................... 46

Chapter 7 Annexures ...................................................................................................................... 49

7.1 Documents received from MPECS and MSEDCL ......................................................................... 49

7.2 Inspection of records at MPECS head office ................................................................................. 51

7.3 Computation of weighted average Interest rates (State Bank of India) ......................................... 52

7.4 Monthly pay out schedule .............................................................................................................. 53

7.5 Physical verification schedule ........................................................................................................ 60

7.6 Assessment of replaced assets of MPECS ................................................................................... 61

7.7 Quantity of assets owned by MPECS ............................................................................................ 64

7.8 Land area and cost ........................................................................................................................ 68

3

7.9 References used ............................................................................................................................ 69

4

Table 1: Sample size for verification of distribution assets of MPECS Table 2: Valuation of assets by replacement cost Table 3: Illustrative weighted average cost of capital computation for 2011-12 Table 4: Sequence of events Table 5: Sample size for verification of distribution assets of MPECS Table 6: Quantity details of the distribution assets of MPECS Table 7: Data collected from 20 sub-stations during physical verification Table 8: Representation of major additions/modification in infrastructure MPECS network Table 9: Balance life from 2011 calculation based on the capacity (MVA) added. Table 10: Book value of distribution assets of MPECS Table 11: Quantity details of distribution assets as per MPECS asset register Table 12: Cost of construction as per MSEDCL rates Table 13: Valuation of MPECS distribution assets as per replacement cost method Table 14: Illustrative weighted average cost of capital computation for 2015-16 Table 15: Depreciation table Table 16: User charge table for annual pay out Table 17: Pay out table adjusted for amount already deposited Table 18: Wheeling charge computation for FY 2011-12

5

Figure 1: Nodal Officer MSDCL teams, Alia Consulting Project Leader and Nodal Officer MPECS.

Figure 2: Sub-station survey at Rahuri Sub-station

Figure 3: Sub-station feeder

Figure 4: MPECS Power Transformers in working condition

Figure 5: MPECS Power Transformer in yard (In working condition)

Figure 6. DTC on RSJ Poles (New DTR installed by MSEDCL)

Figure 7: Scrap DTR in Sutgirni, Shreerampur

6

Chapter 1 Executive Summary

1.1 Background

The Mula Pravara Electric Co-operative Society (“MPECS”), Shrirampur was established in 1969

as a farmers' cooperative society by the support of the Government of India to supply electricity

to rural consumers. It was one of the five pilot rural electric co-operative societies established in

India. MPECS area comprises 183 villages of the Shrirampur, Rahuri, Rahata, Newasa and

Sangamner talukas of Ahmednagar district including 3 municipal councils at Shrirampur, Rahuri

and Deolali Pravara in Ahmednagar district in the state of Maharashtra. The Head Office of the

society is situated at Shrirampur. MPECS started its commercial operation in 1971 to distribute

power in four specific Talukas (MPECS area) in the District of Ahmednagar in Maharashtra. The

MPECS commenced its functioning w.e.f. 1 March, 1971 and took over the electrical distribution

network of Maharashtra State Electricity Board (“MSEB”). The GoM renewed the said license for

another 20 years i.e. from 1991 to 2011. MPECS serves a total of 183 villages in 5 talukas. The

term of license of MPECS expired on 31 January, 2011.

In 2011, upon expiry of the license, the Maharashtra Electricity Regulatory Commission (MERC)

directed the Maharashtra State Electricity Distribution Co. Ltd. (MSEDCL) to take over the

distribution of electricity in the MPECS area. As a consequence of this decision and a series of

orders from various authorities (outlined in section 2.1) it was concluded that fair valuation be

undertaken of the assets owned by MPECS and used by MSEDCL and charges to be paid to

MPECS for use of these assets.

1.2 Scope of work

The scope of work covered in this project includes two part – valuation of assets and charge

determination. In order to arrive at an accurate valuation, important tasks included scrutiny of

asset register, physical verification of asset, asset classification and categorization and employing

industry and regulator accepted valuation tools. The scope of work included valuation of

distribution assets only. General assets, directly linked to distribution operations which includes

land and buildings are included. For charge determination, there is no standard industry

methodology available for the given context. The wheeling charge computation is one of the

options considered along with other options that uses standard finance theory led “rental charge”

for usage of assets (further explained in section 3.1 chapter 3).

7

1.3 Sampling methodology

Given the physically dispersed nature of the assets and the quantum of assets involved, it was

required that a sampling methodology be used that can give an accurate representation of the

entire asset base. We have followed a sampling methodology based on the practices of the

Bureau of Energy Efficiency Projects and Indian standard 5002 of 1969 (Method for determination

of sample size) in order to arrive at an optimal number of samples to be reviewed from the asset

register. This sampling methodology assumes a 95% confidence level of the universe of

distribution assets of MPECS. The samples physically verified is given below.

Table 1: Sample size for verification of distribution assets of MPECS

Sr. No. Work Scope Units Total Quantity

Sample Size

1 Physical verification of substation Nos 20* 20*

2 Physical verification of 33 kV line KM 233 68

3 Sample basis physical verification of 11 kV line KM 2494 93

4 Sample basis physical verification of DTC's Nos 3378 99

5 Sample basis physical verification of LT line KM 9157 95

*Note: 100% of sub-station (Sr. No 1) and its equipment’s is considered for verification.

1.4 Valuation methodology

We have evaluated four options for the purpose of valuation of assets.

Discounted cash flow method

Book value method

Comparable method

Replacement cost method

We have determined that the replacement cost methodology is the only appropriate method for

estimating value of the assets – given the nature of business, illiquid nature of assets and no

similar transactions available in the market. Further details of each of the methodology is given in

section 3.3 of chapter 3. The results from the same are given in the table below.

8

Table 2: Valuation of assets by replacement cost (Rs. In crs)

Distribution Assets Units

Qty Handed over as on 2011

Total life of Asset

Remaining

life of asset

Total Material Cost at 2011-12 (In crs)

Total build Cost

(In crs)

Replacement cost

(In crs)

Replacement

cost for Balance

life* (In crs)

High voltage plants

Land Sq.Mtr 1,33,700 0.59 2.59 2.59

Land Leasehold 0.04 0.04 0.04

Buildings 1.72 1.72 1.72

Sub-stations Nos 20 25 14 35.09 15.90 50.99 28.56

High voltage line 33KVA

Km 233 25 14 10.02 4.54 14.55 8.15

Total A 45.11 20.43 65.55 36.71

High voltage plants

T/C above 100KVA Nos 2,146 25 14 96.91 43.90 140.81 78.85

T/C below 100KVA Nos 1,232 25 14 19.85 8.99 28.84 16.15

H.T Line (11kV Lines) Km 2,494 25 14 67.41 30.54 97.95 54.85

Metering equipment Nos 189 25 14 0.08 0.04 0.12 0.07

Total B 184.25 83.47 267.72 149.92

Medium and low voltage

L.T Line km 9,157 25 14 154.20 69.85 224.05 125.47

S.C Metering equipment

Nos 1,19,741 25 14 15.57 7.05 22.62 12.67

Capacitor banks Nos 83 25 14 0.85 0.38 1.23 0.69

Three phase metering Nos 5,168 25 14 7.33 3.32 10.65 5.96

Total C 177.94 80.61 258.55 144.79

Total A+B+C 407.31 596.17 335.77

*The balance life determined is 14 years (please refer section 4.3).

The replacement cost adjusted for residual life comes to Rs. 335.77 crores as on

February 2011.

9

1.5 User charge determination

For determining user charges due to MPECS for the use of its distribution assets, we have used

standard finance principles of compensating MPECS for the cost of capital (as indicated by the

value of assets) and the value of assets over the lifetime of the assets. Further, in computing the

actual payout to MPECS, we have factored in the carrying cost on past due amount which have

as yet not been paid to MPECS while adjusting for the interim amount deposited MSEDCL with

the commission. Key assumptions / principles are outlined below:

Depreciation schedule: The asset value of Rs. 335.77 cr has been depreciated linearly

over 14 years at 7.14% annually in line with the remaining useful life of assets.

Cost of Capital: The cost of capital has been calculated using a 70:30 mix of debt and

equity, 15.5% as cost of equity and “Weighted average of SBI Base Rates + 2.0%” for cost

of debt. Cost of debt has been taken in line with what institutions such as MPECS will bear

if they were to take market loans. The cost of capital is calculated for each year in the

past. For future years, we have carried forward the FY’16 cost of capital.

Carrying cost: Carrying cost for unpaid past due charges have been taken at “SBI Base

Rate + 1.5%". The carrying cost considered has been arrived at a nominal interest that

can be charged for past due amounts - taking into account the SBI base rate and what

could be a nominal premium on top of that. Such interest rates are charged as per

standard practice in multiple industries. The number used is also in line with MYT

regulations 2015.

Adjustment for interim payment: As interim relief to MPECS, the Commission in its

interim Order dated 15 October, 2012 determined an interim amount as Rs. 1 crore per

month, i.e, Rs. 12 crore per annum to be paid by MSEDCL to MPECS, on an ad hoc basis

as charges for continuation of existing arrangement. A total amount of Rs. 62.64 crores in

principle has been deposited from October of 2015 by MSEDCL for a period of 5 years

from 2011 to 2016. The same has been assumed as charges which have been paid by

MSEDCL and therefore does not incur carrying cost. All amount in this account

including any accrued interest should come due to MPECS.

Payout schedule: We have assumed the first payout in March 2016 and all subsequent

payouts annually up until March 2025.

10

Table 3: Illustrative weighted average cost of capital computation for 2011-12

Particulars Cost Weight WACC

Cost of Equity 15.50% 30% 4.65%

Cost of Debt 11.71% 70% 8.20%

Weighted Average Cost of Capital 12.85%

Coming from this, Rs. 325.11 Crs is due to MPECS in March 2016, which includes

past due charges with carrying cost built in and charges for the year 2015-16.

Further, all proceeds in the account where MSEDCL has been depositing the

interim relief payout should be made available to MPECS (Rs. 62.64 cr + accrued

interest)

Going forwards, MSEDCL should pay user charges as given in section 6.2 based

on the principles outlined above.

1.6 Applicability of wheeling charge to the current case

The wheeling charge (Annual Revenue Requirement) methodology was developed with the

specific purpose of ensuring that any entity that builds distribution assets and wheels electricity

on those assets is able to get a suitable return from the project that covers both the cost of capital

and cost of operations and maintenance of those assets. The wheeling charge therefore is meant

to determine what should be the appropriate unit charge (to consumers) that can provide the

appropriate return to the operating entity.

In the current scenario at hand, this methodology is not appropriate for the reasons which are

detailed out in section 6.3 of chapter 6.

11

Chapter 2 Introduction

2.1 Mula-Pravara Electric Co-operative Society Ltd

The Mula Pravara Electric Co-Operative Society Ltd. (“MPECS”) was granted a Distribution

license with a validity of 20 years under the Indian Electricity Act, 1910 by the Government of

Maharashtra (“GoM”) on 28th January 1971 for distribution of electricity in 183 villages spread

over an area of 1880 sq.km in five talukas namely Shrirampur, Rahuri, Nevasa, Sangamner and

Rahata talukas of Ahmednagar District. Further this license was extended for a period of 20 years,

i.e. up to 2011 with effect from 1st February 1991 by GoM vide Government Resolution (GR)

dated 21st May 1999. The Distribution License of MPECS was expiring on 31st January 2011.

MPECS had submitted an application for grant of Distribution License before the Maharashtra

Electricity Regulatory Commission (the Commission). Another application was received for the

same area from Maharashtra State Electricity Distribution Co. Ltd. (MSEDCL).

By an order dated 27 January, 2011, the Commission granted license to MSEDCL and amended

the license of MSEDCL by merging MPECS’ area of supply with MSEDCL’s area of supply. The

application of MPECS was rejected for the reasons provided in the said order. MPECS was

directed to handover the distribution network and allied equipment’s etc., belonging to MPECS to

MSEDCL with the qualification that MPECS will be entitled to claim value for the assets handed

over, for which MPECS may file a separate petition before the Commission for deciding transfer

value of their assets, with all relevant documentary evidence. MPECS filed an appeal before the

Hon’ble Appellate Tribunal for Electricity (“ATE”) challenging the order of the Commission. By

Judgment dated 16 December, 2011 in Appeal No. 39 of 2011, Hon’ble ATE remanded the

aforesaid Case to the Commission with the direction to reconsider the application of license of

MPECS and to dispose of on merits with a further direction to consider for grant of license to both

the Parties by allowing them to operate in the same area. Hon’ble ATE also directed as follows:-

“After pronouncement of judgment, the learned Counsel for the parties request for issuing of

consequential directions with regard to the existing arrangements and the time frame.

Accordingly, we direct the Commission that the process to be completed within three months from

today and in the meantime, the existing arrangement may be continued subject to payment of

charges to the Appellant to be decided by the Commission after hearing all the parties concerned.”

12

MPECS had filed the present Petition on 7 March, 2012 for determination of the aforesaid charges

for the use of the distribution network and connected equipments and allied assets with effect

from February 1, 2011 by MSEDCL. The Commission had passed an interim Order dated 15

October, 2012 for granting interim relief to MPECS, the Commission in its interim Order in the

present matter dated 15 October, 2012 has considered only capital expenditure related expenses

and determined the interim amount as Rs. 1 crore per month, i.e, Rs. 12 crore per annum to be

paid by MSEDCL to MPECS, on an adhoc basis as charges for continuation of existing

arrangement and directed MSEDCL to carry out valuation of distribution assets of MPECS before

30 November, 2012. The Commission directed that the Commission will pass an order revisiting

the charges aforesaid once valuation of the distribution network is available. In spite of several

directives of the Commission, the valuation of assets was not completed by MSEDCL.

Accordingly, vide Order dated 18 June, 2014, the Commission disposed of the Petition of MPECS

in Case No. 24 of 2012 directing MPECS to submit the asset register to the Commission and

MSEDCL and further directing MSEDCL to carry out asset valuation within 3 months of the receipt

of asset register.

This Order was challenged by MPECS before the Appellate Tribunal for Electricity (ATE), ATE

vide, its Judgment dated 13 March, 2015 remanded the matter back to the Commission to decide

the said petition on merits. The Commission was directed to get the evaluation of the assets of

MPECS done through some independent agency or through some impartial agency or the

Commission itself.

With this, it was concluded that fair valuation be undertaken of the assets owned by MPECS and

used by MSEDCL and user charges to be paid to MPECS for use of these assets.

13

2.2 Sequence of events

Table 4: Sequence of events

Year Event

1969 MPECS was established as a Farmer's Co-operative Society for rural electrification and

distribution of electricity.

1971 GoM (Government of Maharashtra) granted 20 year Distribution license to MPECS.

2011 MPECS & MSEDCL’s files for application for grant of Distribution License for MPECS

Area of Supply as MPECS license is due to expire

MERC order dated 27-01-2011 rejects the application of MPECS for grant of distribution

license and amends the license of MSEDCL by merging MPECS area of supply with

MSEDCL area of supply and directs MPECS to hand over the distribution network and

allied equipment to MSEDCL without any wheeling charges from zero hours on

February 1, 2011. (Case No 85 and 87 of 2010, MERC Order dated 27-01-2010)

MPECS challenges MERC order to transfer the assets to MSEDCL. Hon’ble APTEL

concludes that MPECS is entitled to claim compensation for the assets handed over

APTEL order dated 16-12-2011 Appeal No 39 of 2011:

Sets aside the MERC Order 27-01-2011 on revocation of MPECS license as due

process under the EA 2003 was not followed under Section 15(6) and 15 (b)(6).

-The directions to MPECS to “transfer the assets to the MDESCL is not in accordance

with the law” and is liable to be set aside.

In the same order, APTEL clarified that the present arrangement may be continued i.e.

payment of charges to MPECS by MSEDCL for use of its distribution network.

2012 In order to determine a charge, MERC orders MSEDCL to carryout valuations of the

assets of MPECS. (MSEDCL has not carried out any valuation of MPECS)

MERC's Order Case No 24 of 2012 dated 15-10-2012 determines an interim amount of

Rs.1 cr per month i.e. Rs 12 crs p.a. to be paid by MSEDCL to MPECS on an ad hoc

basis as charges for continuing the existing arrangements until the matter of grant of

license is finally determined by the Commission. The final charges would be decided

once the valuation of assets of MPECS is done.

2013 MERC reiterates and confirms its Order of 12-10-2012 and rejects the review petition.

MERC directs MPECS to submit a copy of asset register of electricity business within a

week of issuance of this Order to MSEDCL. MSEDCL shall carry out the valuation

14

Year Event

exercise of assets of MPECS and submit the valuation report to the Commission within

a month of issuance of this Order. Case No 121 of 2012 and No 6 of 2012, 03-09-2013.

2014 ATE in case 221 of 2014 directs that the existing arrangement namely use of distribution

line / network of the appellant petitioner (MPECS) by the respondent No.2(MSEDCL),

distribution licensee may be continued subject to payment of charges to the appellant

which is to be decided by the State Commission after hearing all the parties concerned

2015 MERC published a notice for appointment of an External Independent

Agency/Consulting Firm for asset valuation of MPECS in accordance with the

judgement issued by APTEL in Appeal No. 221 of 2014 and invited EOI from

independent agencies & consulting firms

2016 Valuation report consists of the following:

1. Valuation of distribution assets of MPECS

2. Charge payable by MSEDCL to MPECS for the use of the distribution assets

15

Chapter 3 Scope & Methodology

3.1 Scope of the assignment

Our scope of work is to value the distribution assets of MPECS which is presently being used by

MSEDCL for distribution of electricity to consumers in MPECS’s license area of supply. The

distribution assets include all facilities, lines, meters, utilities, plants, premises, works, substations,

distribution transformer centres/distribution transformers, connected equipment and allied assets.

Based on the project timeline and deliverables as per our scope, below mentioned objectives has

been completed.

1. Scrutiny of asset register submitted by Mula-Pravara: Reviewing current stock of

physical assets based on the reports duly submitted by the MPECS. As this being the

starting approach for the project. Verifying the accounting methods used to record the

transactions reported in asset register. To completely rely on the asset register a physical

verification has been conducted.

2. Physical verification of assets jointly with Mula Pravara and MSEDCL. We have

completed the physical verification and analysis of the current state of physical assets

deployed in the area of the assessed sites.

3. Identify the assets of Mula-Pravara being used by MSEDCL and categorize the same:

As part of the scope is also to determine the assets utilized or altered by MSEDCL, we have

captured this information and analysed this claim against records submitted. But it is

confirmed fact that an entire distribution network was handed over to MSEDCL in February

of 2011 which was also verified physically.

4. Deciding principles for valuation of assets based on accounting principles or any

other applicable principle including Tariff Regulations of MERC: After verifying the

accuracy of the asset register, we have looked further into valuing them. Industry methods

to value these assets have been adopted. Valuation methods have been explained for the

understanding of the best approach possible for the current situation of MPECS.

16

5. Submission of draft Asset Valuation report to the Commission: The report will collate

all the valuation of assets utilised, the impact of utilisation and the right methodology

adopted.

6. Based on final Asset valuation, determination of the compensation to be paid by the

MSEDCL to Mula Pravara: We have computed the amount that MSEDCL has to pay Mula-

Pravara for utilising its assets during the period of operations after February, 2011 as per

the directions of the Hon’ble ATE

7. Incorporating the feedback received on draft report: Based on milestone completion

review session & interaction with the state commission, feedback/comments on the draft

valuation report will be duly reflected while presenting the final report & order will be

prepared as per the scope of this service.

8. Preparation of draft order and finalization of the order: We will be preparing the draft

order in this matter.

3.2 Methodology for physical verification

Given the physically dispersed nature of the assets and the quantum of assets involved, it was

required that a sampling methodology be used that can give an accurate representation of the

entire asset base. As part of the project, we followed best industry practices for sampling of

assets. The sampling methodology adopted is based on the references taken from the Bureau of

Energy Efficiency Projects (India) and Indian standard 5002 of 1969 (Method for determination of

sample size) in order to arrive at an optimal number of samples to be reviewed from the asset

register. This sampling methodology provides a 95% confidence level of the universe of

distribution assets. Our field sampling indicates that the asset registry provided by MPECS is

accurate.

The formula for calculation the sample Size as follows

SS = {Z2 *(p)*(1-p)} / (C2)

Where,

17

Z= Z value (e.g. 1.96 for 95% confidence Level)

P = Percentage Picking a Choice, expressed as decimal

C = Confidence Interval (Expressed as Decimal)

Sample Size – Finite Population

SS = SS1 / {(1 + (SS1 – 1)/ Pop)}

Where,

Pop = Population

The minimum sample size calculation is as follows for 33 kV line,

Pop = 233, population size

Z = 1.96 for 95% Confidence interval

P = 0.05 Picking percentage

5% as standard practice

C = 0.1 as 10% confidence interval

Therefore, as per formula, SS1 = (1.96*1.96)*(0.05)*(1-0.05) = 96.04

(0.1)2

New sample size for the finite population of 233 km,

SS = SS1 / {(1 + (SS1 – 1)/ Pop)}

= 96.04

1+ (96.04 - 1)

233

= 68.23 ~ 68

The table below illustrates the sample sizes of the asset type for physical verification

18

Table 5: Sample size for verification of distribution assets of MPECS

Sr. No. Work Scope Units Total Quantity

Sample Size

1 Physical verification of substation Nos 20 20

2 Physical verification of 33 kV line KM 233 68

3 Sample basis physical verification of 11 kV line KM 2494 93

4 Sample basis physical verification of DTC's Nos 3378 99

5 Sample basis physical verification of LT line KM 9154 95

Physical scrutiny of assets as per the above methodology indicated that the asset register shared

by MPECS is accurate. Relevant purchase registers/vouchers have been verified against the

sample surveyed. MSEDCL and MPECS have signed the survey reports which confirms our

sample verification. (Survey reports submitted separately)

3.3 Methodology for valuation

There are four methods to value the assets of MPECS as being used by MSEDCL.

1. Discounted Cash flow Method (Net Present Value Method)

2. Book Value

3. Comparable method

4. Replacement cost

1. Discounted Cash Flow Method assumes the entity to be a going concern and generates

enough surplus that creates value for the business. Given the nature of the business of

electricity distribution (regulated tariffs, collection issues etc.), it is difficult to estimate future

Valuation methods for MPECS

Discounted Cash Flow

Comparable Method Book Value Replacement Cost

19

cash flows and the discounting rate. Thus, we are of the opinion that DCF will not be an

appropriate method to compute the value of the assets.

2. The Book Value method estimates the value of the assets coming from standard accounting

principles as captured in the financial statements of the company. This method is conservative

and often leads to under-valuing the business as depreciation of assets follows accounting

principles (typically takes as over 10 years and sometimes accelerated even more for taxation

purposes).

3. The Comparable method estimates the value of the assets by benchmarking the assets

against a similar transaction that may have happened in the market. The benchmark

transaction is then adjusted for size (number of assets, number of households connected etc)

before determining the value of the assets. Given, there were no viable comparable transaction

in the market, this method was not used. Further, given regulated nature of business marketing

the assets and finding a willing buyer is not an option.

4. Replacement cost method is based on the principle of substitution. For the acquiring party,

the cost of setting up a similar infrastructure is determined. Since book value of MPECS assets

follows a conservative accounting approach (in order to take taxation benefits from accelerated

depreciation), the real value of the assets is higher than those reported in the books. To be fair

to both parties, transfer of assets should happen at market prices or cost of replacements.

The cost so determined is then adjusted for the remaining life of the existing assets to arrive

at the valuation number.

We have determined that replacement cost methodology is the only appropriate method for

estimating value of the assets – given the nature of business, illiquid nature of assets and no

similar transactions available in the market. This method estimates the cost that will be incurred

both in terms of material / components costs and the cost to build / construct. Moreover, as the

distribution assets were operational at the time of takeover, this method is considered to be

appropriate.

20

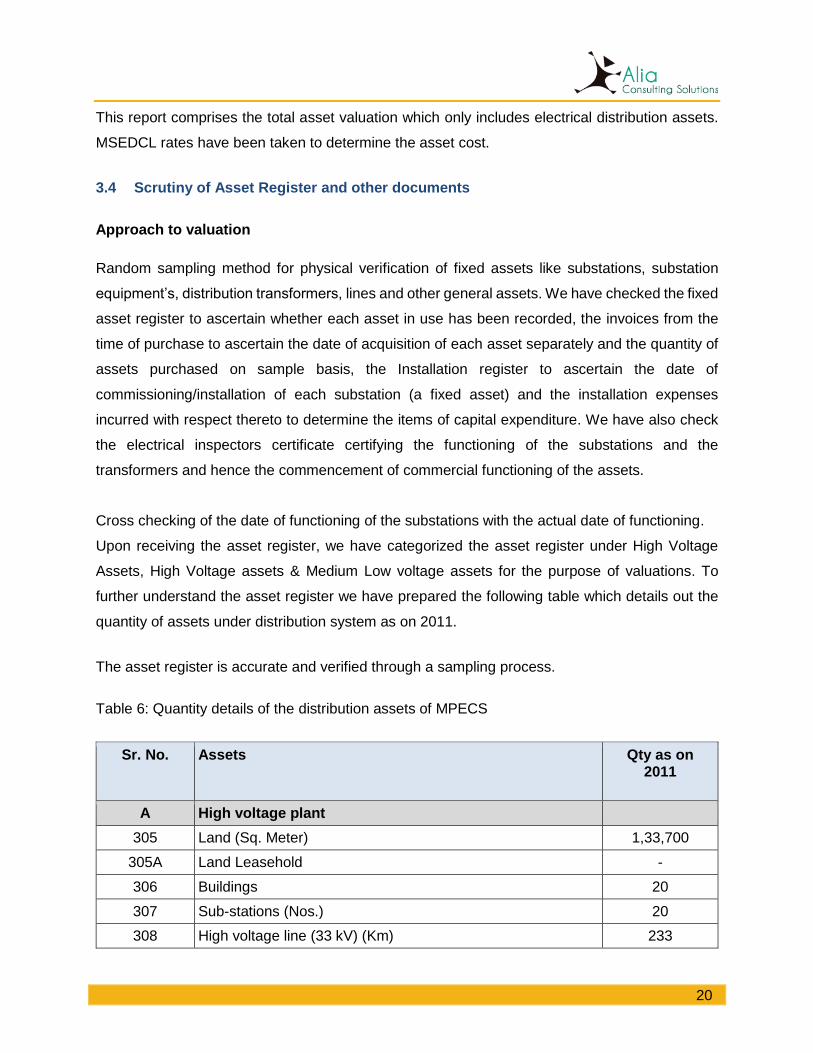

This report comprises the total asset valuation which only includes electrical distribution assets.

MSEDCL rates have been taken to determine the asset cost.

3.4 Scrutiny of Asset Register and other documents

Approach to valuation

Random sampling method for physical verification of fixed assets like substations, substation

equipment’s, distribution transformers, lines and other general assets. We have checked the fixed

asset register to ascertain whether each asset in use has been recorded, the invoices from the

time of purchase to ascertain the date of acquisition of each asset separately and the quantity of

assets purchased on sample basis, the Installation register to ascertain the date of

commissioning/installation of each substation (a fixed asset) and the installation expenses

incurred with respect thereto to determine the items of capital expenditure. We have also check

the electrical inspectors certificate certifying the functioning of the substations and the

transformers and hence the commencement of commercial functioning of the assets.

Cross checking of the date of functioning of the substations with the actual date of functioning.

Upon receiving the asset register, we have categorized the asset register under High Voltage

Assets, High Voltage assets & Medium Low voltage assets for the purpose of valuations. To

further understand the asset register we have prepared the following table which details out the

quantity of assets under distribution system as on 2011.

The asset register is accurate and verified through a sampling process.

Table 6: Quantity details of the distribution assets of MPECS

Sr. No. Assets Qty as on 2011

A High voltage plant

305 Land (Sq. Meter) 1,33,700

305A Land Leasehold -

306 Buildings 20

307 Sub-stations (Nos.) 20

308 High voltage line (33 kV) (Km) 233

21

B High voltage plants

313 T/c Above 100kVA (Nos.) 90

314 T/c 100kVA & Below (Nos.) 3,288

317 H/T Line (Km) 2,496

345B Metering equipment’s (TOD Meter) (Nos.) 187

C Medium and low voltage plant

337 L.T. line (KM) 8,937

344 S.C. Metering equipment’s (Nos.) 1 Phase 1,19,741

345 S.C. Metering equipment’s (Nos.) 3 Phase 5,168

345A Capacitor / Capacitor banks (Nos.) 83

3.5 Approach to physical verification

Approach to physical valuation involves 4 distinct steps

1) Data collection from MPECS

In order to prepare a plan for physical verification and survey the assets of MPECS, it was

important to check the validity of the documents (eg. Asset register, maintenance register, sample

purchase notes, etc.) Documents are required to identify the asset type, quantity and its

distribution across the geography. Documents requested from the MPECS are mentioned below.

2) Format preparation and deciding the physical verification plan

After receiving the documents, a format for the verification of the assets was prepared outlining

the specifications of the assets to be checked and sample quantity to be verified at the site. (The

same has been circulated to MPECS and MSEDCL before the survey)

Following which a plan for physical verification outlining the dates, areas to be visited,

requirements of engineers/officials, etc. was prepared and circulated in advance.

3) Joint verification with MPECS & MSEDCL

As part of the scope of our work, the verification was to be conducted in the presence of both the

parties involved that is MPECS and MSEDCL given the current arrangement. The physical

verification was successfully conducted with the participation of both the parties. The survey

sheets/ formats have been signed by both the entities during the time of survey.

22

4) Inspection of documents of MPECS

During and after the physical verification process, our engineers and chartered accountants

inspected various records of MPECS to ascertain the accuracy of the asset register, validity of

important documents, etc. Many documents were requested when the physical verification was

on going. (The same has been communicated to MERC)

3.5.1 Note on physical verification

Survey of 33kV lines

a. Electrical Inspectors notes was verified before survey

b. During survey conductor type and respective length was noted

c. Poles type verified

d. Span Length verified

e. Condition of the lines assessed

f. 2 km length of each sample feeder was surveyed by walking alongside and rest of the feeders

will be reviewed with the use of vehicles.

Survey of the substation & its components

a. Team visited 20 substations and conducted physical verification of the power transformers

and major equipment’s like VCBs and Panels.

b. During visit to substation, control room area and substation area was reviewed and cross

verified with valid documents.

c. GPS location of the Substation captured.

d. Observations on physical condition of the substation

Survey of 11 kV lines

a. As per the Network Diagram obtained from the MPECS, the field team visited 11 kV line

samples. Up to 5km for each feeder.

b. Conductor type and respective length verified

c. Poles type information for the sample feeders will be collected

d. Span Length of the sample feeder collected

23

e. Condition of the lines assessed

g. 2 km length of each sample feeder was surveyed by walk and rest of the feeders will be

reviewed through vehicles

Survey of LT lines survey

a. Randomly selected DTR’s based LT line surveyed

b. Connected DTR’s also observed in the process

c. Conductor type and respective length verified

d. Pole type verified

e. Span Length verified

Survey of DTR’S on sample basis

a. DTR’S on sample basis (up to 100 for entire network)

b. DTR’s type i.e. Aluminum or Copper wound

c. Count of DTR’s matched of randomly selected feeder

d. Condition of the DTR’s will be assessed

3.5.2 Documents verified

1. The Electrical Distribution Assets Register

2. The General Assets Register

3. The Substations Installation Register

4. Land Drawings

5. Electrical Inspectors Certificate

6. Government Notifications/Circulars

7. Bills for Assets purchased

8. Letter of Intent of MPECS

9. Fixed Assets Maintenance Record

10. Audited Statements of Account and the Auditor’s Report

11. Line diagrams

Please refer Annexure 7.2 for list documents verified at the MPECS head office in Shrirampur.

24

Chapter 4 Technical assessment

4.1 Observations from physical verification

Our team, jointly carried out the survey with MSEDCL and Mula Pravara team for the MPECS

assets under the possession of MSEDCL, as per the Sample sizes decided for the 33kV,11kV,

DTR’s and LT lines respectively.

Figure 1: Nodal Officer MSDCL teams, Alia Consulting Project Leader and Nodal Officer MPECS.

Figure 2: Sub-station survey at Aradgoan sub-station

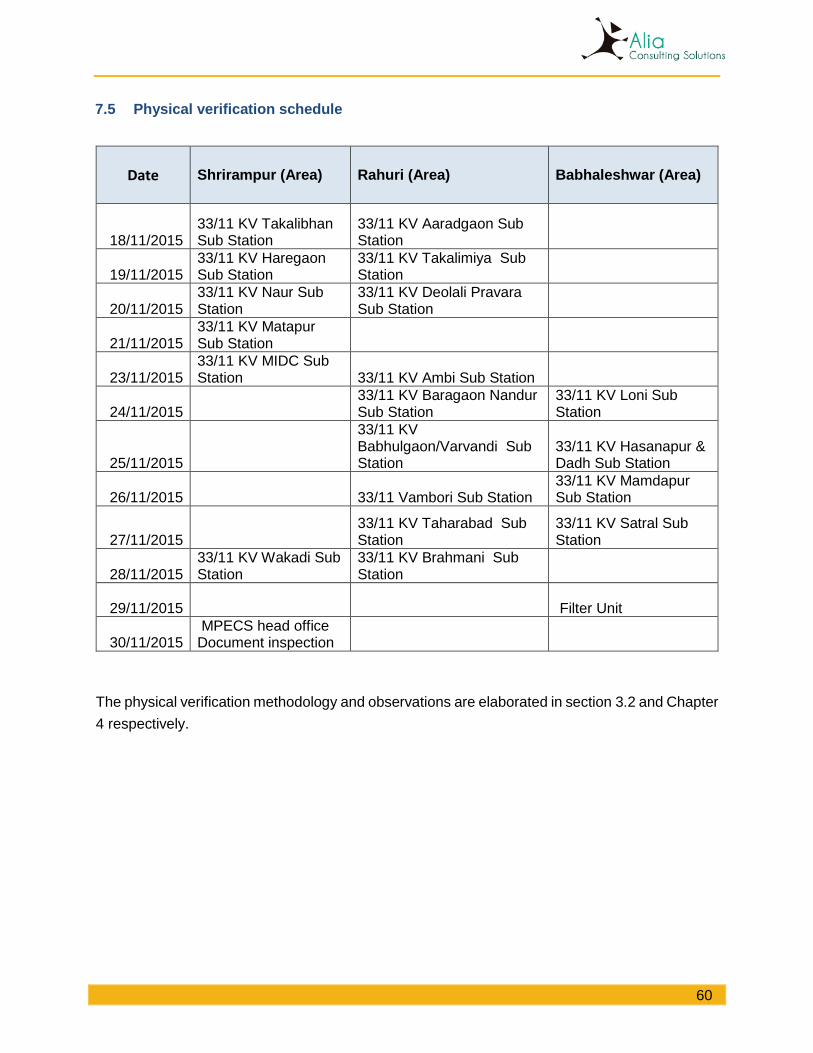

Before initiating the actual physical verification survey, a joint meeting was held with employees

of MPECS & officials of MSEDCL on 7th November, 2015 and a sample verification process was

demonstrated to them at Shrirampur, MIDC sub-station. Also a detailed physical verification plan

was shared with both parties. Physical verification plan was circulated in advance to both the

parties. The physical verification commenced on 18th November, 2015.

The physical verification of all (100%) 33/11 kV Substations was carried out. The physical

verification of the HT Line, DTR’s and LT lines respectively has been carried out on sample basis,

to acquire the present status of the power distribution network and equipment’s being used by

MSEDCL.

25

Observations during physical verification

a) MSEDCL has replaced major substation equipment’s.

b) Replaced equipment’s of MPECS includes working items & failed items, most equipment’s

are stored in the open yard outside or inside the sub-station.

c) MSEDCL has not made any major changes in the HT lines, LT lines.

d) MSEDCL holds custody of all replaced items of MPECS.

e) MSEDCL has constructed new sub-station rooms/building in the MPECS owned sub-

station land.

f) Disagreement on quantity of certain equipment’s like distribution transformers, structures

(to be resolved by the commission).

Challenges faced during physical verification

a) While evaluating MPECS sub-station equipment, there were minor disagreement with

respect to quantity handed over in 2011. Also, as MSEDCL has inadequate staff it was

difficult for them to remember the quantity handed over in 2011. But the records submitted

by MPECS along with valid inspector certificates and material lists, conclude the asset

register to be accurate.

b) Replaced items were difficult to locate as they were not stored in systematic manner.

4.2 Survey observations

1. 33 kV Lines

The 33 kV Lines feeder during survey were found to be as per the records.

a) 233.18 km of 33 KV line is under the custody of MSEDCL, most of the feeders remain

unchanged.

b) The span length of the 33kV during survey was found to be 0.8 meters.

c) There have been no changes observed in the 33kV lines in our samples visited.

26

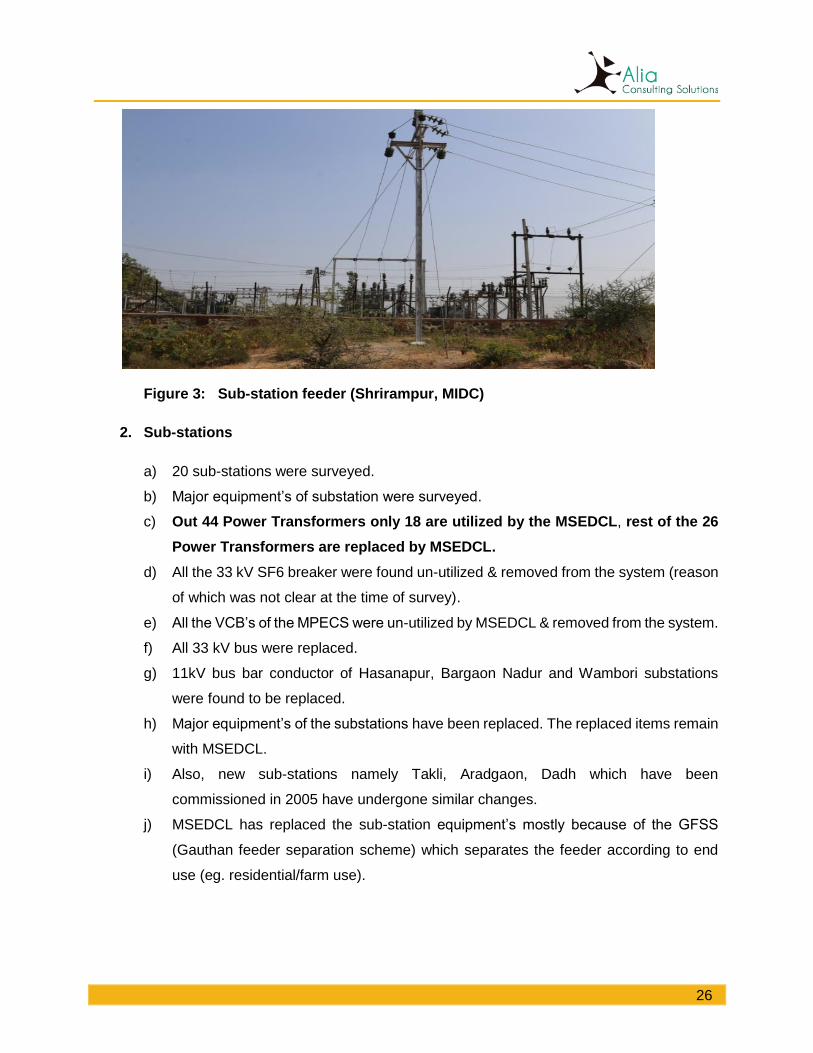

Figure 3: Sub-station feeder (Shrirampur, MIDC)

2. Sub-stations

a) 20 sub-stations were surveyed.

b) Major equipment’s of substation were surveyed.

c) Out 44 Power Transformers only 18 are utilized by the MSEDCL, rest of the 26

Power Transformers are replaced by MSEDCL.

d) All the 33 kV SF6 breaker were found un-utilized & removed from the system (reason

of which was not clear at the time of survey).

e) All the VCB’s of the MPECS were un-utilized by MSEDCL & removed from the system.

f) All 33 kV bus were replaced.

g) 11kV bus bar conductor of Hasanapur, Bargaon Nadur and Wambori substations

were found to be replaced.

h) Major equipment’s of the substations have been replaced. The replaced items remain

with MSEDCL.

i) Also, new sub-stations namely Takli, Aradgaon, Dadh which have been

commissioned in 2005 have undergone similar changes.

j) MSEDCL has replaced the sub-station equipment’s mostly because of the GFSS

(Gauthan feeder separation scheme) which separates the feeder according to end

use (eg. residential/farm use).

Figure 3. 33 KV Incoming Line

27

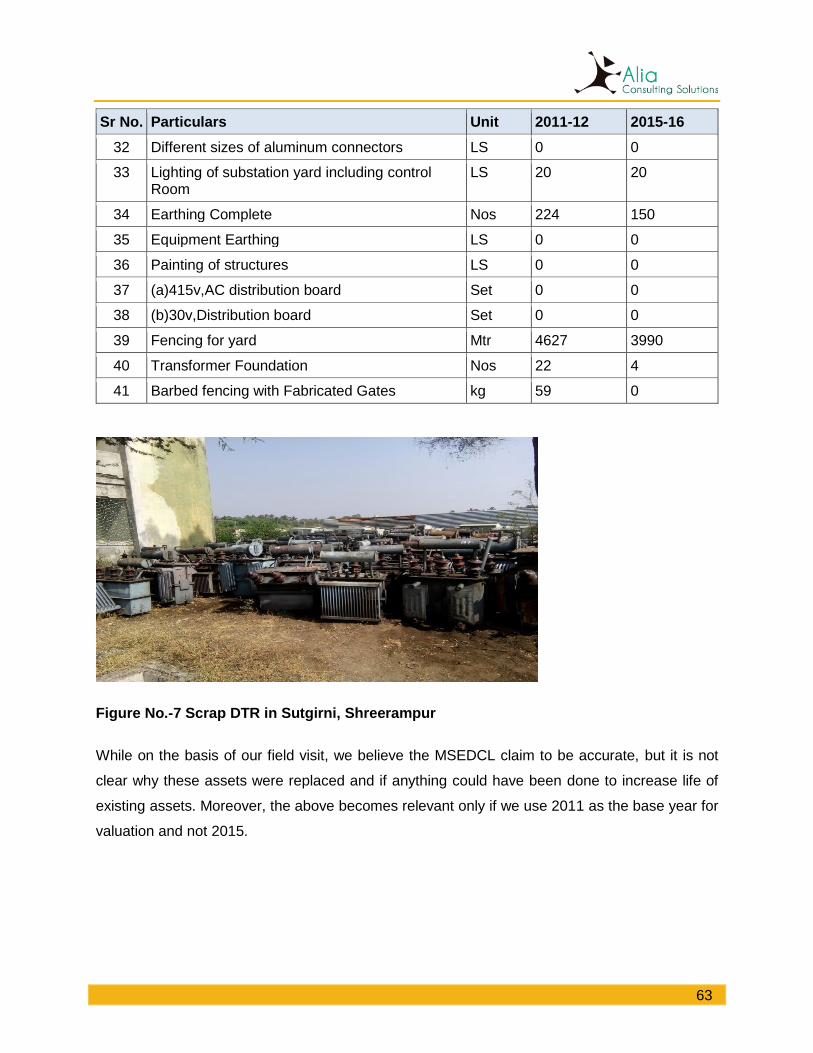

Table 7: Data collected from 20 sub-stations during physical verification

Sr No. Particulars

Unit

2011-12

2015-16 2015-16 2015-16

Assets of 33kv/11kv Substation Utilized Replaced

1 Gantry Column for 33Kv incoming and outgoing feeder

No. 20 20 19 1

2 Structure for 33Kv & and 11Kv Swing bus

No. 20 20 8 12

3 Structure for top mounted AB switch on 11 & 33 Kv Bus (Bus Coupler)

No. 0

4 Structure for 11kv take off with top mounted AB switch & division of lighting arrestor

No. 55 42

33

9

5 Structure for 33Kv & and 11Kv isolators

No. 177 232 89 143

6 Structure of installation of 33 Kv /110v.PT

No. 20 20 20

7 Structure of installation of 11Kv /110v.PT

No. 20 20 20

8 Structure of installation of 33kv CT

No. 20 36 12 24

9 Structure of installation of 11kv CT

No. 51 51 51

10 33Kv post insulator structure No. 40

11 11Kv post insulator structure No. 82

12 33 kV, 1250A Outdoor SF6 CB No. 20 20 11 9

13 33/11Kv Power transformer 3.15MVA

No. 38 44 18 26

14 33Kv/110volts, potential transformer

Set 20 18 5 13

15 11Kv/110volts, potential transformer

Set 51 51 51

16 33Kv CT Set 20 20 20

17 11Kv CT Set 51 51 51

18 Disc. Ins for 33Kv Swing bus & Incoming Bay

Set 0

19 33Kv Lighting arrestor Set 40 37 26 11

28

Sr No. Particulars

Unit

2011-12

2015-16 2015-16 2015-16

20 33Kv post insulator No. 18

21 11kv Vacuum circuit breaker with panel etc.

Set 76 74 74

22 11Kv post insulator No. 0 0 0 0

23 Disc. ins for 11Kv Swing bus & Take off structure

No. 0 0 0 0

24 33Kv 3 pin type AB switch:630 AMPS

Set 0 0 0 0

25 33Kv vacuum circuit Breaker with panel etc.

Set 0 20 11 9

26 11 kV AB Switch ( 630A ) No. 99 65 16 49

27 11Kv lighting arrestor Set 76 36 15 21

28 ACSR Raccon conductor kM 0.9 0.9 0.9

29 Battery with battery charging unit complete(32V):as per REC specification

Set 20 19 12 7

30 Control cable : various sizes as per requirement

LS 1 0 0 0

31 Aluminum pipe: 65mm. Dia as per requirement

LS 0 0 0 0

32 Different sizes of aluminum connectors

LS 0 0 0 0

33 Lighting of substation yard including control Room

LS 20 20 0 20

34 Earthing Complete Nos 224 150 0 150

35 Equipment Earthing LS 0 0 0

36 Painting of structures LS 0 0 0 0

37 (a)415v, AC distribution board Set 0 0 0 0

38 (b)30v, Distribution board Set 0 0 0 0

39 Fencing for yard Mtr 4627 3990 0 3990

40 Transformer Foundation Nos 22 22 18 4

41 Barbed fencing with Fabricated Gates

kg 59 0

29

Figure 4: MPECS Power Transformers in

working condition

Figure 5: MPECS Power Transformer in yard

(In working condition)

3. 11 KV lines

The 11 kV line feeders during survey were found to be as per the records.

a) On an average, 10 PSC and 3 RSJ poles were found during the survey.

b) Span length on an average was 0.7 to 0.8km.

4. Distribution Transformer Centre (DTC)

The DTC during survey were found to be as per the records.

a) As per the survey samples of DTC (99 samples), 56 were found to be to be utilized and

43 were found to be replaced by the MSEDCL.

b) Most of the transformers replaced are stored in a filter unit.

c) Working transformers also stored in filter warehouses of MSEDCL.

d) Repairable transformers are not utilized and remain in the custody with MSEDCL (may

lead to deterioration as observed).

30

Figure 6. DTC on RSJ Poles (New DTR installed by MSEDCL)

5. Low Voltage Lines

The LT lines during survey were found to be as per the records.

a) Most of the LT lines network is been utilized by MSEDCL.

b) The LT lines network is being strengthened by the MSEDCL by inserting the poles to between

existing MPSEC network.

6. Sub-station land

a) MSEDCL has built its own control rooms at almost all sub-stations adjacent to the sub-station

land owned by MPECS.

b) Old control rooms are also utilized by MSEDCL staff for various administrative and other

purpose.

c) All replaced equipment’s of MPECS are removed and stored either inside the sub-station or

outside.

d) Land where control rooms are constructed is owned by MPECS.

31

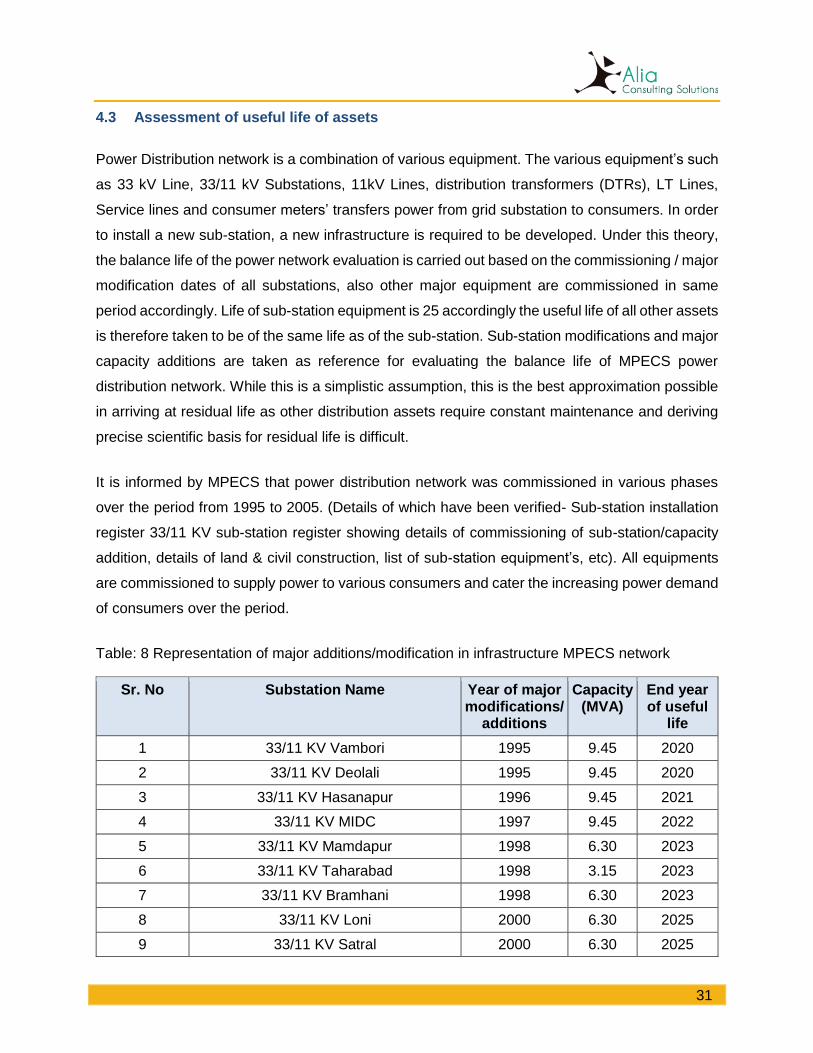

4.3 Assessment of useful life of assets

Power Distribution network is a combination of various equipment. The various equipment’s such

as 33 kV Line, 33/11 kV Substations, 11kV Lines, distribution transformers (DTRs), LT Lines,

Service lines and consumer meters’ transfers power from grid substation to consumers. In order

to install a new sub-station, a new infrastructure is required to be developed. Under this theory,

the balance life of the power network evaluation is carried out based on the commissioning / major

modification dates of all substations, also other major equipment are commissioned in same

period accordingly. Life of sub-station equipment is 25 accordingly the useful life of all other assets

is therefore taken to be of the same life as of the sub-station. Sub-station modifications and major

capacity additions are taken as reference for evaluating the balance life of MPECS power

distribution network. While this is a simplistic assumption, this is the best approximation possible

in arriving at residual life as other distribution assets require constant maintenance and deriving

precise scientific basis for residual life is difficult.

It is informed by MPECS that power distribution network was commissioned in various phases

over the period from 1995 to 2005. (Details of which have been verified- Sub-station installation

register 33/11 KV sub-station register showing details of commissioning of sub-station/capacity

addition, details of land & civil construction, list of sub-station equipment’s, etc). All equipments

are commissioned to supply power to various consumers and cater the increasing power demand

of consumers over the period.

Table: 8 Representation of major additions/modification in infrastructure MPECS network

Sr. No Substation Name Year of major modifications/

additions

Capacity (MVA)

End year of useful

life

1 33/11 KV Vambori 1995 9.45 2020

2 33/11 KV Deolali 1995 9.45 2020

3 33/11 KV Hasanapur 1996 9.45 2021

4 33/11 KV MIDC 1997 9.45 2022

5 33/11 KV Mamdapur 1998 6.30 2023

6 33/11 KV Taharabad 1998 3.15 2023

7 33/11 KV Bramhani 1998 6.30 2023

8 33/11 KV Loni 2000 6.30 2025

9 33/11 KV Satral 2000 6.30 2025

32

Sr. No Substation Name Year of major modifications/

additions

Capacity (MVA)

End year of useful

life

10 33/11 KV Haregaon 2001 6.30 2026

11 33/11 KV Taklibhan 2001 9.45 2026

12 33/11 KV B'Nandur 2001 3.15 2026

13 33/11 KV Naur 2002 3.15 2027

14 33/11 KV Wakadi 2003 3.15 2028

15 33/11 KV Matapur 2005 3.15 2030

16 33/11 KV Dadh 2005 3.15 2030

17 33/11 KV Babhulgaon 2005 3.15 2030

18 33/11 KV Ambi 2005 6.30 2030

19 33/11 KV Taklimiya 2005 3.15 2030

20 33/11 KV Aradgaon 2005 9.45 2030

Total 119.75

Table 9: Balance life from 2011 calculation based on the capacity (MVA) added.

Sr. No Year of modification /

commissioning

Balance life Capacity (MVA)

Weighted average

1 1995 9 18.9 170.10

2 1996 10 9.45 94.50

3 1997 11 9.45 103.95

4 1998 12 15.75 189.00

5 2000 14 12.60 176.40

6 2001 15 18.90 283.50

7 2002 16 3.15 50.40

8 2003 17 3.15 53.55

9 2005 19 28.35 538.65

Total 119.75 1660.05

Average balance life (in years) ~14

The above table explains that almost 25% of the capacity was built in year 2005 and around 35%

after year 2000 and around 40% before year 2000. Life of substation equipments is 25 years.

33

Based on the above date of operationalization, the average life of asset comes to 11 years and

therefore 14 years of balance life. Similarly, it is assumed that all the other power distribution

infrastructure (Line, DTCs, etc.) is incorporated according to substations incorporation year and

assumes the same life of the sub-station.

Hence weighted average is taken to establish the overall balance life which is 14 years.

34

Chapter 5 Valuations of assets of MPECS

The date of transfer of asset from MPECS to MSEDCL was 2011. We were presented with the

option of estimating the value of the assets as of 2011 or 2015. This gives rise to issues related

to whether the assets are still under use and all the assets that MSEDCL has replaced over the

last five years. MSEDCL has replaced ~30% of the assets of MPECS from 2011 to 2015. It is not

clear why these assets were replaced and if anything could have been done to increase life of

existing assets

Given that MSEDCL took over a fully operational asset in 2011, we have considered the following:

The assets should be valued as of 2011 and user charges computed keeping that date in

mind. Therefore the base year is taken as 2011.

All charges so computed can then be implemented with a carrying cost as per the MYT

guidelines, 2015 (Weighted average SBI base rate + 1.5%) added to address the four-

year lag in the pay-out of the charges. This should adjust for any interim payment made

by MSEDCL.

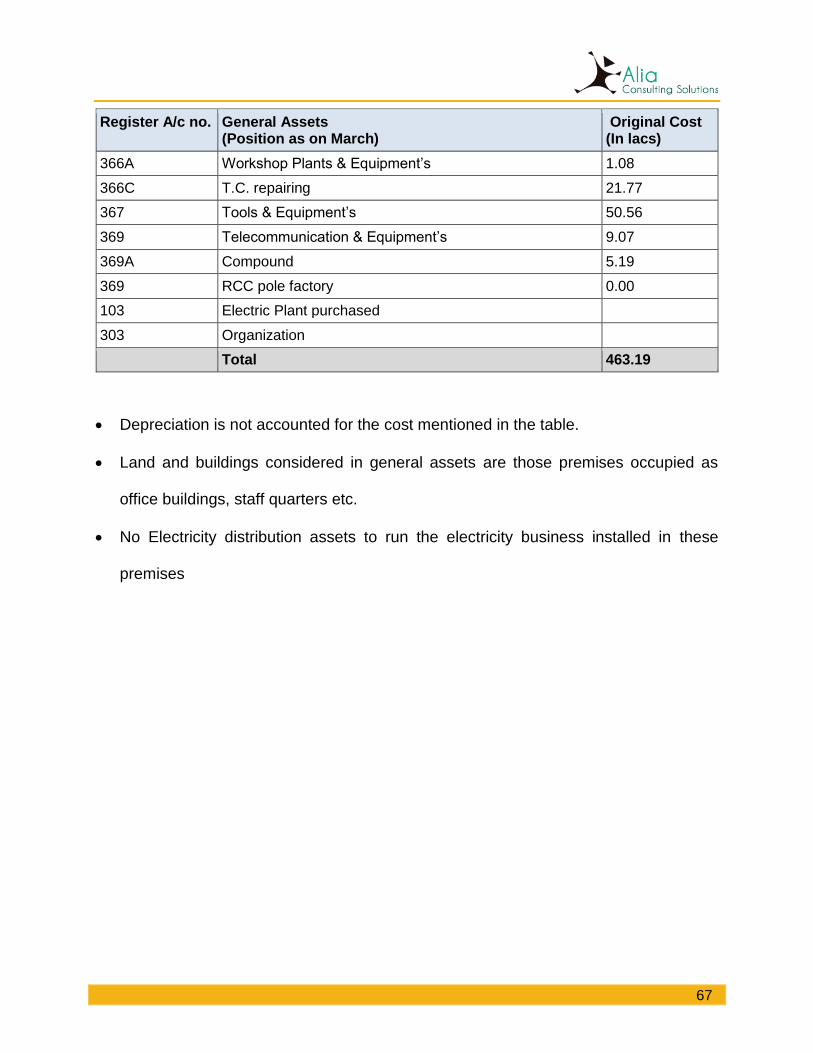

Electricity Distribution Assets shown in the table 11 have been built by MPECS over the past 40

years. These acquisition details are easily traceable to the fixed assets register, substation

installation register, purchase orders and several other documents which have been verified by

us. Land and leasehold land as mentioned in the table are lands used specifically for constructing

substations. Hence land is an important component of the electricity distribution assets. Land

means the freehold land owned by MPECS. Leasehold land means land obtained from third party

on annual lease payments for a lease period of 99 years. Building means building constructed

near the substation area. The study of the asset register after all write-offs and scrap sale

produces original cost of acquisition of Rs.157.80 crores as on 2011.

Table 10: Book value of distribution assets of MPECS

Distribution Assets Asset value (Amount in Rs.)

Depreciation (Amount in Rs.)

Book value 2011 (Amount in Rs.)

High voltage plants

Land 59,14,476 - 59,14,476

Land Leasehold 4,16,180 - 4,16,180

35

Distribution Assets Asset value (Amount in Rs.)

Depreciation (Amount in Rs.)

Book value 2011 (Amount in Rs.)

Buildings 104,04,127 21,43,564 82,60,562

Sub-stations 3020,33,520 1529,53,933 1490,79,586

High voltage line 33KVA 666,49,166 369,20,282 297,28,883

Total A 854,17,470 1920,17,781 1933,99,688

High voltage plant

T/C above 100KVA 1658,51,728 686,75,035 971,76,692

T/C below 100KVA 1434,91,262 783,53,981 651,37,280

H.T Line 44,14,461 936,22,693 1007,91,768

Metering equipment 30,21,451 6,30,443 23,91,007

Total B 5067,78,904 2412,82,154 2654,96,749

Medium and low voltage

L.T Line 4670,51,110 2540,46,236 2130,04,873

S.C Metering equipment 1964,94,223 832,70,221 1132,24,001

Capacitor banks 222,41,004 127,71,397 94,69,607

Total C 6857,86,338 3500,87,855 3356,98,482

Total A+B+C 15779,82,712 7833,87,791 7945,94,921

5.1 Valuation as per replacement cost

Table 11: Quantity details of distribution assets as per MPECS asset register

Sr. No. Assets 2010-2011 Quantity

A High voltage plants

305 Land (Sq. mtr) 1,33,700

305A Land Leasehold

306 Buildings 20

307 Sub-stations (Nos.) 20

308 High voltage Line (33 kV) (Km) 233

B High voltage assets

313 T/c above 100kVA (Nos.) 90

314 T/c 100kVA & below (Nos.) 3,288

36

Sr. No. Assets 2010-2011 Quantity

317 H/T Line (Km) 2,496

345B Metering equipment’s (TOD meter) (Nos.) 187

C Medium & low voltage plants

337 L.T. Line (Km) 8,937

344 S.C. Metering equipment’s (Nos.) 1 Phase 1,19,741

345 S.C. Metering equipment’s (Nos.) 3 Phase 5,168

345A Capacitor / Capacitor banks (Nos.) 83

To evaluate the MPECS assets, the REC approved MSEDCL cost data is used.

Land value is based on the prevalent government rate of 2011 (Annexure attached 7.3)

S.C metering 3 phase quantity is 5,168 as per the records in the MPECS asset register

Table 12: Cost of construction as per MSEDCL rates

Sr. No.

Particulars % of total cost of material

Cost of Material 100

1 Erection on material (Labour) 10.00% 10.0

2 Transportation on material 5.00% 5.0

3 Insurance on material 1.00% 1.0

4 Service tax @ (12.24% on 1+2+3) 1.96% 2.0

5 Contingencies on material 3.00% 3.0

6 T & P on material 1.50% 1.5

7 Contractor supervision on charges on material 5.00% 5.0

Sub-Total -I 127.46

8 Contractor profit on total project cost i.e. on sub-total-I 5.00% 6.37

Sub-Total -II 133.83

9 Price escalation on material cost 0.00% 0.0

Sub-Total -III 133.83

10 H.O. supervision charges @ 1.5% (i.e. 15% of 10% on erection of material)

1.50% 2.01

37

Sr. No.

Particulars % of total cost of material

Sub-Total -IV 135.84

11 Interest during construction period (on total project cost) i.e. on Sub-Total-IV

7% 9.5

Total cost 145.34

Note:

1. The construction cost is 45.34% of the material cost which is taken from MSEDCL

rate sheets

2. Interest contribution assumes 70% debt funding, 10% rate of interest, 2-year

construction time, linear draw down of material cost over construction period.

Table 13: Valuation of MPECS distribution assets as per replacement cost method

Distribution Assets Units Qty Handed over as on 2011

Total life of Asset

Remaining life of asset

Total Material Cost at 2011-12 (In crs)

Total build Cost (In crs)

Replacement cost (In crs)

Replacement cost for Balance life (In crs)

High voltage plants

Land Sq.Mtr 1,33,700 0.59 2.59 2.59

Land Leasehold 0.04 0.04 0.04

Buildings 1.72 1.72 1.72

Sub-stations Nos 20 25 14 35.09 15.90 50.99 28.56

High voltage line 33KVA

Km 233 25 14 10.02 4.54 14.55 8.15

Total A 45.11 20.43 65.55 36.71

High voltage plants

T/C above 100KVA Nos 2,146 25 14 96.91 43.90 140.81 78.85

T/C below 100KVA Nos 1,232 25 14 19.85 8.99 28.84 16.15

H.T Line (11kV Lines) Km 2,494 25 14 67.41 30.54 97.95 54.85

Metering equipment Nos 189 25 14 0.08 0.04 0.12 0.07

Total B 184.25 83.47 267.72 149.92

Medium and low voltage

38

Distribution Assets Units Qty Handed over as on 2011

Total life of Asset

Remaining life of asset

Total Material Cost at 2011-12 (In crs)

Total build Cost (In crs)

Replacement cost (In crs)

Replacement cost for Balance life (In crs)

L.T Line km 9,157 25 14 154.20 69.85 224.05 125.47

S.C Metering equipment

Nos 1,19,741 25 14 15.57 7.05 22.62 12.67

Capacitor banks Nos 83 25 14 0.85 0.38 1.23 0.69

Three phase metering Nos 5,168 25 14 7.33 3.32 10.65 5.96

Total C 177.94 80.61 258.55 144.79

Total A+B+C 407.31 596.17 335.77

Note:

1. Only land under sub-station has been considered and not the adjoining land parcel also owned

by MPECS. While commercial usage of the overall (adjoining) land parcel may not be possible

by MPECS, given the scope of this assignment to value distribution assets only, we have not

considered the entire land parcel.

2. Remaining life of assets is explained in section 4.3 of chapter 4.

3. For Distribution transformation centers:

Cost taken for DCT above 100 KVA is the average cost of DCT 100KVA, DCT 200 KVA,

DCT 315 KVA, DCT 500 KVA: Rs.4,51,586/-

Cost taken for DCT below 100 KVA is the average cost of DCT 15 KVA, DCT 25 KVA, DCT

50 KVA, DCT 63 KVA: Rs.1,61,115/-

4. Fire extinguishers have not been located on site, hence it is not considered in valuation.

The asset value without accounting for residual life is Rs. 596.17 crores based on

the replacement cost principle as on February 2011.

The replacement cost adjusted for residual life is Rs. 335.77 crores as on February

2011

39

5.2 Reconciliation with ASCI report

MPECS approached the Administrative Staff College of India (ASCI) to undertake a study on the

valuation of the Distribution Network of the MPECS in October 2013.

The scope of services determined by the MPECS to ASCI covers:

1. To undertake fair valuation of the Distribution Network of the society on a going concern basis

at the date of handing over the network to Maharashtra Electricity Distribution Co. Ltd.

(MSEDCL) i.e. 1st Feb 2011, by using appropriate method/ methods and engaging experts &

consultants thereof;

2. To evaluate the Distribution Network in two parts.

Valuation of the distribution network handed over to MSEDCL for its use to distribute

electricity in the area of operation of the society

Valuation of the General Assets retained by the Society

3. To advise what should be the rate of return/ charges to be applied for use of society's assets

Consistent with our approach, ASCI also considered the same valuation methodology. As per

ASCI report, the value of the asset as per replacement cost methodology came to Rs. 411.52

crores – higher than our estimated value by Rs. 85 crores. The difference arises due to three

reason:

The balance life assumed for the distribution assets in the ASCI report is 40 years for LT

lines and 15 years for all other distribution assets whereas we have taken 14 years for all

assets.

There is a Rs. 10 cr difference between ASCI and our report within general assets. We

have not been able to identify the basis for the difference as we do not have back up

calculations that has gone behind the calculations.

40

Chapter 6 User charge determination

6.1 User charges

For determining user charges due to MPECS for the use of its distribution assets, we have used

standard finance principles of compensating MPECS for the cost of capital (as indicated by the

value of assets) and the value of assets over the lifetime of the assets.

Capital cost determination

Charge determination requires as the first step, to compute an appropriate capital cost from the

perspective of MPECS. For the purpose of computing the cost of capital, we have made the

following assumptions:

The assets are assumed to be funded 30:70 by equity and debt as per Multi Year Tariff

(MYT) regulations.

Cost of equity is taken as 15.5% as per MYT regulations, 2011

Cost of debt is calculated by taking the weighted average of SBI base rates in a

particular year + 2%. (The methodology for computation of SBI base rates is given in

annexure 7.3)

o Cost of debt for 2015-2016 is as 9.53% + 2%= 11.53%

o Cost of debt for 2014-2015 is as 10.00%+ 2%= 12.00%

o Cost of debt for 2013-2014 is as 9.84% + 2%= 11.84%

o Cost of debt for 2012-2013 is as 9.85% + 2%= 11.85%

o Cost of debt for 2011-2012 is as 9.71% + 2%= 11.71%

Table 14: Illustrative weighted average cost of capital computation for 2015-16

Particulars Cost Weight WACC

Cost of Equity 15.50% 30% 4.65%

Cost of Debt 11.53% 70% 8.07%

Weighted Average Cost of Capital 12.72%

Coming from the above, the Weighted Average Cost of Capital comes to 12.72% for 2015- 16.

Similarly we have calculated for the every year starting 2011.

Weighted average cost of capital 2015-16 is 12.72%

41

Weighted average cost of capital 2014-15 is 13.05%

Weighted average cost of capital 2013-14 is 12.94%

Weighted average cost of capital 2012-13 is 12.95%

Weighted average cost of capital 2011-12 is 12.85%

Asset depreciation and useful life

As discussed in section 4.3, the weighted average remaining useful of the distribution assets has

been determined to be 14 years. In line with this, we have made a depreciation assumption that

reduces the value of these assets linearly over a period of 14 years to zero by 2025 – an effective

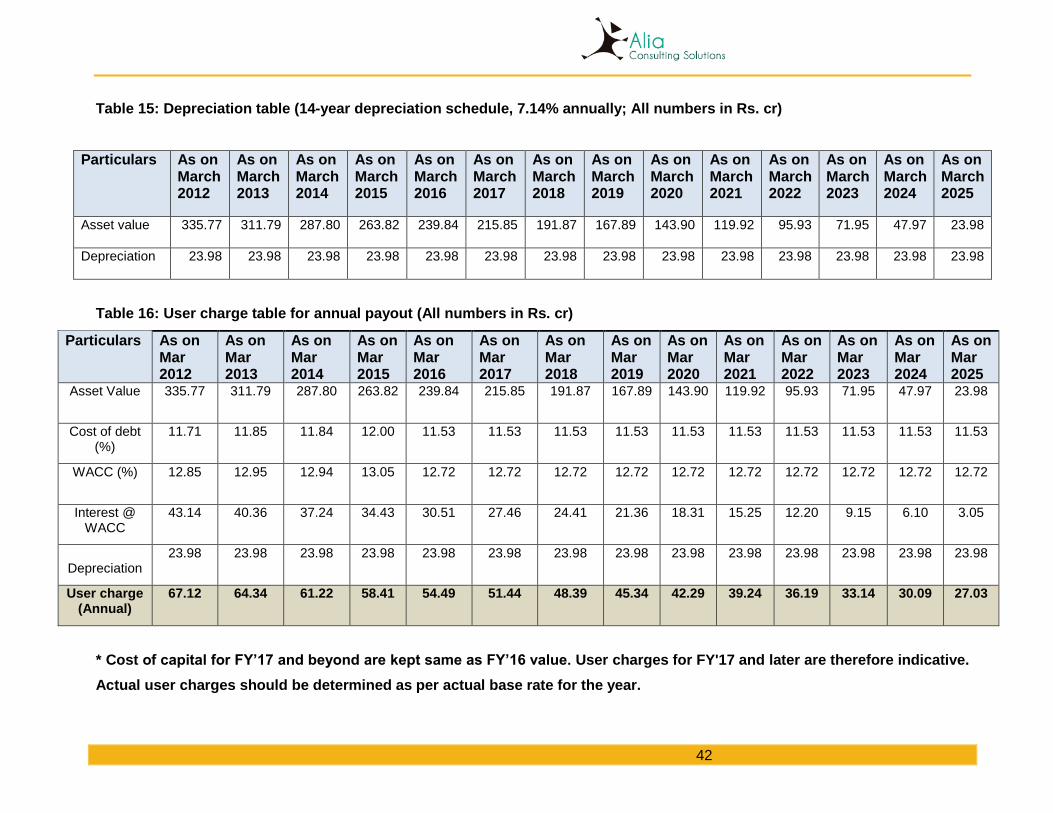

depreciation rate of 7.14% every year. At a value Rs. 335.77 cr as of March 2012, the annual

depreciation amount comes to Rs. 23.98 cr. The same will need to be included as part of the user

charges paid to MPECS by MSEDCL.

Tables 15 and 16 below gives the year-on-year depreciation, cost of capital and the user charges

due to MPECS over the lifetime of the assets – from 2012 to 2025.

42

Table 15: Depreciation table (14-year depreciation schedule, 7.14% annually; All numbers in Rs. cr)

Particulars As on March 2012

As on March 2013

As on March 2014

As on March 2015

As on March 2016

As on March 2017

As on March 2018

As on March 2019

As on March 2020

As on March 2021

As on March 2022

As on March 2023

As on March 2024

As on March 2025

Asset value

335.77 311.79 287.80 263.82 239.84 215.85 191.87 167.89 143.90 119.92 95.93 71.95 47.97 23.98

Depreciation

23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98

Table 16: User charge table for annual payout (All numbers in Rs. cr)

Particulars As on Mar 2012

As on Mar 2013

As on Mar 2014

As on Mar 2015

As on Mar 2016

As on Mar 2017

As on Mar 2018

As on Mar 2019

As on Mar 2020

As on Mar 2021

As on Mar 2022

As on Mar 2023

As on Mar 2024

As on Mar 2025

Asset Value 335.77 311.79 287.80 263.82 239.84 215.85 191.87 167.89 143.90 119.92 95.93 71.95 47.97 23.98

Cost of debt (%)

11.71 11.85 11.84 12.00 11.53 11.53 11.53 11.53 11.53 11.53 11.53 11.53 11.53 11.53

WACC (%) 12.85 12.95 12.94 13.05 12.72 12.72 12.72 12.72 12.72 12.72 12.72 12.72 12.72 12.72

Interest @ WACC

43.14 40.36 37.24 34.43 30.51 27.46 24.41 21.36 18.31 15.25 12.20 9.15 6.10 3.05

Depreciation

23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98 23.98

User charge (Annual)

67.12 64.34 61.22 58.41 54.49 51.44 48.39 45.34 42.29 39.24 36.19 33.14 30.09 27.03

* Cost of capital for FY’17 and beyond are kept same as FY’16 value. User charges for FY'17 and later are therefore indicative.

Actual user charges should be determined as per actual base rate for the year.

43

** Base rate calculation from FY’12 to FY’16 is given in annexure 7.3. Similar principle should be followed for future years

Note: We have used FY 2011-2012 as the starting year as that year is the first complete year after the transfer of assets in

February of 2011.

44

6.2 Payout to MPECS going forward

In determining the actual payout to MPECS going forward, we have made the following

assumptions and adjustments:

The payouts start 31st March 2016 and the first payout will cover all past due charges

Carrying cost for unpaid past due charges have been taken at “SBI Base Rate + 1.5%".

The carrying cost considered has been arrived at a nominal interest that can be charged

for past due amounts - taking into account the SBI base rate and what could be a nominal

premium on top of that. Such interest rates are charged as per standard practice in multiple

industries. The number used is also in line with MYT regulations 2015.

The payout will adjust for the amount deposited by MSEDCL in compliance with the interim

Order dated 15 October, 2012 issued by MERC that determined an interim amount as Rs.

1 crore per month, i.e, Rs. 12 crore per annum to be paid by MSEDCL to MPECS, on an

ad hoc basis as charges for continuation of existing arrangement. A total amount of Rs.

62.64 crores in principle has been deposited by MSEDCL over a period of 5 years from

2011 to 2016.

The actual annual payout table is given in Table-17 below.

45

Table 17: Pay out table adjusted for amount already deposited (All numbers in Rs. cr)

Particulars As on Mar 2012

As on Mar 2013

As on Mar 2014

As on Mar 2015

As on Mar 2016

As on Mar 2017

As on Mar 2018

As on Mar 2019

As on Mar 2020

As on Mar 2021

As on Mar 2022

As on Mar 2023

As on Mar 2024

As on Mar 2025

User charge for the year 67.12 64.34 61.22 58.41 54.48 51.43 48.38 45.33 42.28 39.23 36.18 33.13 30.08 27.03

Carrying cost (%) 11.21 11.35 11.34 11.50 00.00 00.00 00.00 00.00 00.00 00.00 00.00 00.00 00.00 00.00

WACC (%) 12.85 12.95 12.94 13.05 12.72 12.72 12.72 12.72 12.72 12.72 12.72 12.72 12.72 12.72

Payout carry forward

67.12 138.99 215.98 298.89 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Amount deposited by MSEDCL** 62.64 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Carrying cost on unpaid due amount

7.52 15.78 24.49 34.37 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Payout* 325.11 51.44 48.39 45.34 42.29 39.24 36.19 33.14 30.09 27.03

* Payout for FY'17 and later will be updated as per the actual cost of debt and WACC for the year

** Additionally, the entire amount of Rs. 62.64 cr deposited by MSEDCL with MERC and the interest accrued in that account will

be paid out to MPECS in March 2016

*** The above user charge and pay out assumes annual payment mode. Payment schedule if monthly mode followed is given

in Annexure 7.4

46

6.3 Applicability of wheeling charge to the current case

Computation of Wheeling Charges

Section 2 (76) of EA 2003 defines “wheeling” as the operation whereby the distribution system

and associated facilities of a transmission licensee or distribution licensee, as the case may be,

are used by another person for the conveyance of electricity on payment of charges to be

determined under section 62.

The wheeling charges for Distribution Wires Business of the Distribution Licensee shall provide

for the recovery of the Aggregate Revenue Requirement, as provided in Regulation 78 of these

Regulations and shall comprise the following:

Aggregate Revenue Requirement:

(a) Return on Equity Capital;

(b) Interest on Loan Capital;

(c) Depreciation;

(d) Operation and maintenance expenses;

(e) Interest on working capital and deposits from consumers and Distribution System Users;

(f) Provision for Bad and doubtful debts; and

(g) Contribution to contingency reserves.

Wheeling charges = Aggregate Revenue Requirement, as above, minus:

(h) Non-tariff income; and

(i) Income from Other Business, to the extent specified in these Regulations, and

(j) Receipts on account of additional surcharge on charges of wheeling.

The wheeling charge (Annual Revenue Requirement) methodology was developed with the

specific purpose of ensuring that any entity that builds distribution assets and wheels electricity

on those assets is able to get a suitable return from the project that covers both the cost of capital

and cost of operations and maintenance of those assets. The wheeling charge therefore is meant

to determine what should be the appropriate unit charge (to consumers) that can provide the

appropriate return to the operating entity.

Wheeling charges calculation: This option evaluated is the wheeling charge (ARR) as per

MERC regulations, 2011. Wheeling charges are used to determine tariff by calculating aggregate

47

revenue requirements of the entity wheeling electricity. The computation allows for entity to

recover return on its capital expenditure and allowable expenses and other provisions. We have

calculated the same for MPEC for the year of 2011-2. Computation for subsequent years is not

possible, as we have insufficient data because year-wise break up of replaced assets is not

available. Assets of MPECS have undergone major replacement (outlined in the annexure7.4)

The amount payable as on March 2012 is Rs.26.78 Crores.

Table 18: Wheeling charge computation for FY 2011-12

Particulars Amount (Rs. In crores)

Return on Equity 7.34

Interest on Loan Capital 11.99

Depreciation 4.55

Operation and Maintenance Expenses (Pl refer MYT Regulation 2015 page no. 99 Item 59)

N.A

Salary / dues N.A

Other 0.54

R and M Expenses 0.00

Interest on Working Capital and Deposits from Consumers 0.62

Contribution to Contingency Reserves 0.41

Other Expenses 0.00

Total 25.45

Provision for Bad and Doubtful Expenses 1.33

Annual Revenue Requirement 26.78

NOTE:

1. Return on equity: 15.50% (Applied on 30% on gross block of Rs.157 crores – As per MPECS

audited balance sheet figure of FY 2011-12)

2. Interest on debt: 10.91% (Applied on 70% on gross block of Rs.157 crores – As per MPECS

audited balance sheet figure of FY 2011-12)

3. Operations and Maintenance is not considered as system is operated by MSEDCL

4. Expenses linked to voluntary retirement scheme amounting to Rs. 121 Crores have not

been considered as they are not linked to core operations of the distribution franchise.

48

Handling of this cost (both accuracy of the claim and resolution of this claim) should be

handled outside of the scope wheeling charge computation.

In the current scenario at hand, this methodology is not appropriate for the following

reasons.

The entity to whom the charge is due (MPECS) is not the operating entity of the assets.

The expenses linked to operations and maintenance are borne by MSEDCL and therefore

if such costs of MPECS are added, it will lead to inaccuracy and double counting.

The wheeling charge exercise is an annual exercise that looks at performance of assets

of the prior year and any adjustment required towards net addition and deletion of assets

(for any replacement or addition) and re-computes the charge for the following year. Given

that the data on assets replaced are maintained by one party of the dispute, there is an

inherent conflict which may lead to further disputes in the future.

Most importantly, the charge that MSEDCL should pay for usage of MPECS assets should

be linked to the opportunity cost paved by MSEDCL in not having to build the assets. This

is best represented by replacement cost methodology as that represents the true value of

MPECS assets. The gross block, on the basis of which wheeling charges are determined,

do not truly represent this value as factors such as inflation, procurement and build

efficiency of MPECS do not get factored in.

49

Chapter 7 Annexures

7.1 Documents received from MPECS and MSEDCL

Documents received from MPECS

1. Copy of Asset Register duly certified by practicing Chartered Accountant (in soft & hard

copies)

2. ASCI Valuation Report (in soft & hard copies)

3. List of location of 183 villages

4. Latest report on number of assets with locations

Location wise list of sub stations (AC No. 307) with associated 33 KV lines (AC No. 308)

and 11 KV lines (AC No. 317)

Location wise list of Distribution Transformer Centers (DTC)/Distribution Transformers

100 KVA & Above (AC No. 313) and below 100 KVA (AC No. 314)

Location wise list of consumers/service connections with metering equipment’s (AC No.

344 & 345)

Address of land & building of MPECS

5. Line Diagrams

The point of supply diagram of 33 KV and 11 KV lines

Compilation of copies of (Sample) DTC LT line diagrams along with corresponding DTC

details

Topographical map showing 33 KV & 11 KV network, with locations of the sub stations

6. Sub Station installation register

33/11 KV sub-station register showing details of commissioning of sub-station/capacity

addition, details of land & civil construction, list of sub-station equipment’s, 7/12 abstracts

and lease agreements, Electrical Inspector's respective permission letters and approved

sub-station layout drawings

7. Fixed asset maintenance records

Circulars issued

Compliance reports for periodical/annual and pre-monsoon maintenance

Maintenance register for sub stations, HT lines, Transformers (DTCs) and LT lines

8. Trial Run Certificates

33/11 KV Sub Station trial Run Certificates (Samples)

50

Copies of Electrical Inspector, I.E. & L. Deptt; Govt. of Maharashtra Annual Inspection Fee

Notes for 33/11 KV Sub Stations (Samples)

Copies of Electrical Inspector, I.E. & L. Deptt; Govt. of Maharashtra Annual Inspection Fee

Notes for Dist. Transformer Centers (Samples)

Copy of Certificate of Calibration for Single Phase R.S.S. meter issued by IDEMI, Mumbai

(Sample)