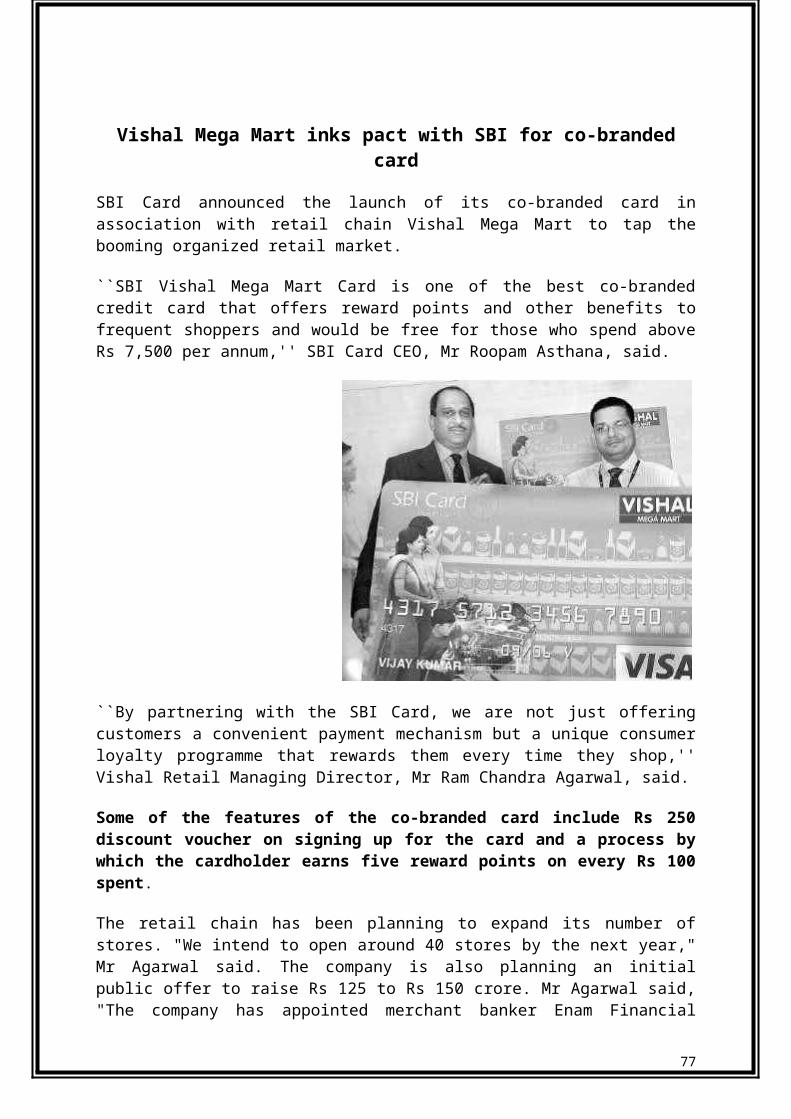

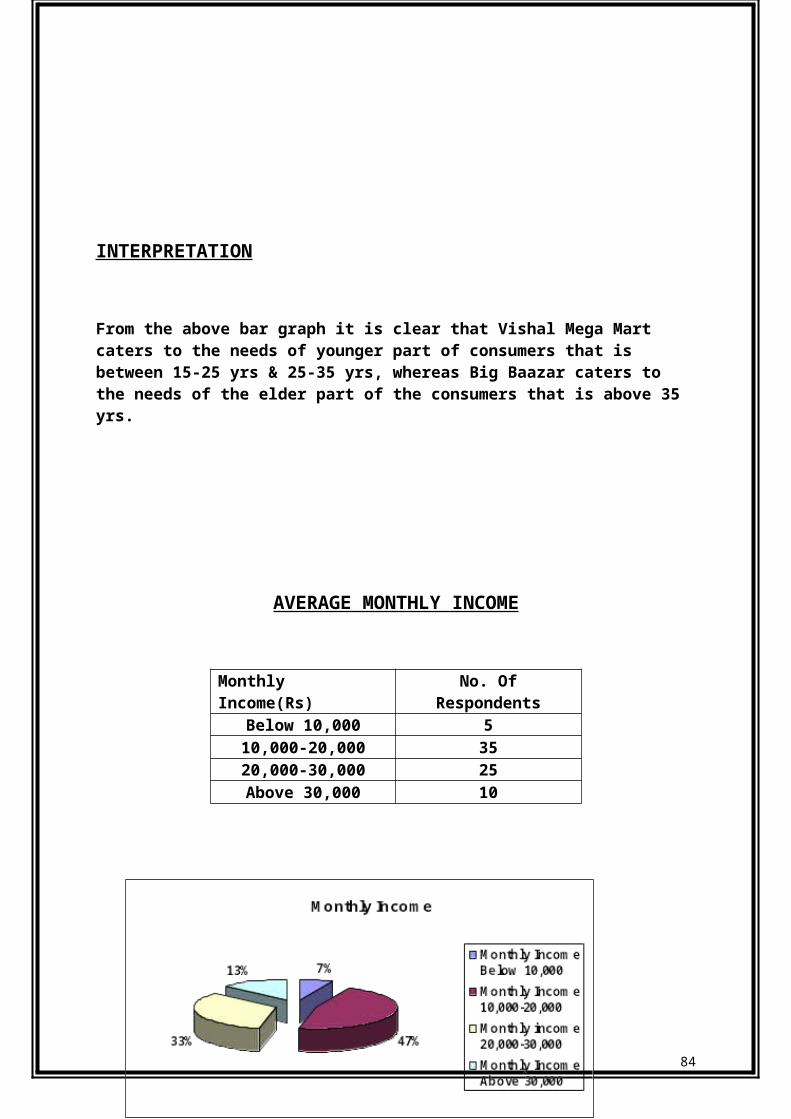

report retail emerging trends

TRANSCRIPT

EMERGING TRENDS OFRETAIL IN INDIA

&A COMPARATIVE ANALYSIS OF

&

SUBMITTED IN FULFILLMENT FOR DEGREE OFM.B.A

Under the Guidance of:Mrs.Richa Sharma(AVP)

SUBHIKSHA TRADING SERVICES LTD.

SUBMITTED BY: -SYED SHADAB ALI

ROLL NO-001246198 ,STUDY CENTRE- 2704

IGNOUNEW DELHI

1

INDEXSr No. Contents Pg. No.

1 Executive Summary 5

2 Introduction 6

3 Present scenario of retail sector in India. 9

4 Literature Review 11

5 Major Formats Of Retail In India 14

6 Evolution of organized retailing 17

7 Retail Model 19

8 Critical success factors in retailing 20

9 Key strategic factors in retailing 23

10 Retailing In India 25

11 Recent trends of retailing in India 30

12 Major players in Retailing in India 37

13 Challenges of Retailing in India 39

14 Barriers of Retailing in India 41

15 Guideline for establishing a new retail business 44

16 FDI in retailing 45

17 Introduction of Big Baazar 48

18 SWOT Analysis of Big Baazar 51

19 Introduction of Vishal Mega Mart 52

20 SWOT Analysis of Vishal Mega Mart 56

21 Objective of the study & research methodology 57

22 Data Analysis 58

23 Survey discussions 71

24 Recommendation 73

25 Conclusion 75

26 Appendix(Questionnaire) 79

27S Bibliography 82

2

Certificate

This is to certify that this project titled “Emerging trends of Retailing in India” is the original work of SYED SHADAB ALI, Roll No: 001246198, MBA ( MARKETING), Region:Lucknow Region Code:27 Study Centre Code:2704, IGNOU, New Delhi.

This dissertation is done under the guidance and supervision of Mrs.Richa Sharma (Associate Vice President) Subhiksha Trading Services Ltd. ‘ This dissertation report has not been submitted to any other institution or organization for any kind of assessment or consideration, to the best of my knowledge.

Mrs.RICHA SHARMA SYED SHADAB ALIAssociate Vice President MBA MARKETING,IGNOUSubhiksha Trading Services Ltd, ROLL NO.-001246198New Delhi. REGION CODE-27 STUDY CENTRE - 2704

3

ACKNOWLEDGEMENT

It is high privilege for me to express my deep sense of gratitude to all those people who helped me in the completion of the project, especially my guide Mrs. Richa Sharma Associate Vice President ,Subhiksha Trading Services Ltd. who was always there at hour of need.

My special thanks to IGNOU staff and faculty for helping me in the completion of project work and its report submission.Finally, I would like to thank all the people, without whose insights and opinions, this project would have been impossible.

SYED SHADAB ALI

4

EXECUTIVE SUMMARY

So far, it has been seen that retailing is a vital and involuntary action performed by the living structure of the market economy (as opposed to the case in a barter economy). In a barter economy, bane; transactions take place between consumers themselves. Consumers interact directly whereas in a centralized market economy, transactions taking place at a larger scale (both in terms of volume and variety) necessitate an interface between the manufacturers and final consumers. Hence we reinforce the fact that retailing is not a new deal. This industry is extant as an interface between production and consumption, from times immemorial, benefiting us - consumers or producers in the various ways discussed above.

Our study concentrates on organized retailing, which consists of shopping malls, super markets, chain stores, and like. In the last few years a shift has occurred in India from individual retail outlets owned separately and managed distinctively to professionally managed retailing. This is an industry, which has now started attracting better investments and talent. Things changed primarily because of the rising expectations of Indian consumers and the corporates responding quickly.

Today the industry (in India) seems to be functioning somewhere between the accelerated development and maturity stages, with high growth rates, intense competition and moderate profitability.

In order to get an idea of the magnitude of the issue we are dealing with, we look at the international scenario. During 1992, the largest 100 retailers in the world generated over $1.1 trillion in revenues.

5

INTRODUCTION

Retailing consists of those business activities involved in the sale of goods and services to consumers for their personal, family or household use. It is the final stage in a channel of distribution, which comprises all of the businesses and people involved in the physical movement and transfer of ownership of goods and services from producer to consumer.

“Any business that directs its marketing efforts towards satisfying the final consumer based upon the organization of seiting goods and services as a means of distribution"

A typical distribution channel is shown below

In a distribution channel, retailing plays an important role as an intermediary between manufacturers, wholesalers, and other suppliers and final consumers. The retailer collects an assortment of goods and services from various sources and offers them to consumers. This procedure is called the sorting process. To maximize their efficiency, many manufacturers would like to make one basic type of item and sell the entire inventory to as few buyers as possible. Yet, many customers want to choose from a variety of goods and services and purchase a limited quantity. Through the sorting process, the retailer bridges the gap between manufacturers and final consumers.

Another distribution function that retailers perform is to communicate with their customers and with their manufacturers and suppliers. Customers are informed about the availability and characteristics of goods and services, special sales etc. via ads, sales personnel and store displays. Manufacturers and wholesalers are informed about sales forecasts, customer complaints, defective products etc. from retailers. Many goods and services have been modified as a result of retailer feedback to suppliers.

6

Manufacture Final ConsumerRetailerWholesaler

Over the last twenty years, retailing has changed as a result of following developments:

The development of a 'motor car economy'. This has led to one stop shopping where families buy all of their supplies at one shop.

Own branding- large retailers have developed brands of their own made by large leading manufacturers,

New technology at the checkout and in the packaging and preserving of food has been developed, which has speeded up the checkout process and reduced the delivery times from suppliers.

Faster transport links across the world, which has made available a wider range of goods.

The growing sophistication of the customers and a general rise in the standard of living, which has led to the fierce competition in the market.

New technology in the home, which may cause a revolution in the shopping methods in the future.

Since the consumer is God, he has to be kept in mind when deciding on a retailing strategy. Consumers do not want something to be sold to them; it is enough to merely facilitate a sale. They want their retail outlets to do more for them in terms of service and convenience. They know what they wish to buy even before they enter a store, and, often, even before they leave the house. So, despite whatever marketers say about impulse-purchases, they are actually rare occurrences. The large number of repeat customers in a store implies that customers are driven more by their feelings towards the store than those towards the brand. This presents super-retailers with an opportunity to build store-brands.

However, supermarkets would do well to start with non-store brands, build a loyal customer-base through schemes similar to frequent-flier programmes, and then, launch store-brands. Significantly, since the expectations of most customers from super markets have not crystallized yet, a super-retailer can, actually, drive expectations by developing need- based retail formats.

There were 5.13 million retail outlets in 1996; today, the figure is closer to 6 million. Most of them are either grocers or paan-plus stores that stock everything from cigarettes to smuggled Scotch. But these figures could be misleading. Just 3 per cent of the country's retail outlets can be called large; 64 per cent are small.

7

For functional products like plain-vanilla FMCGs, traditional formats will do. For innovative products, like high-value FMCGs, cosmetics, garments, or consumer durable, innovative formats are a must.

It has been noticed that, while supermarkets have a computerized billing system, they make no effort to capture any other information about their customers. Marketers will find this information invaluable: ''Data on preferences, family background, and purchase-patterns will help companies address specific consumer needs.''

Keeping the consumer in mind, the study attempts to find whether a shift from the kirana store to the supermarket exists today or not.

8

PRESENT SCENARIO IN RETAIL SECTOR IN INDIA

The organized retail sector is expected to grow at 6% by 2010 and touch a retail business of $ 17 billion as against its current growth level of 3% which at present is estimated to be $ 6 billion, according to the Study undertaken by The Associated Chambers of Commerce and Industry of India (ASSOCHAM). The Study has revealed that the retail sector will grow at GDP 7% by 2010 and enlarge its market share to $ 280 billion from its present estimated level of $ 200 billion. Cities and metropolitans in which retailing will show booming prospects include Mumbai, Delhi, Chennai, Kolkata, Bangalore and Kanpur and the popular mode adopted for building shopping malls in these cities will be based on build, operate, lease and sell basis. This system, as per the findings of ASSOCHAM will lead to establishments of closer linkages and relationship between real estate developers, state governments, financial institutions and retail industry. As per ASSOCHAM’s estimates, investment opportunities that the retail sector will create in next 4-5 years will result into continued urbanization and increase the per capita income of Indian populace which will finally lead to greater consumerism. The growth of retail sector will lead to greater shift towards service economy in which need for real estate will be paramount. Franchising in retailing will emerge as a popular mode of retailing as their will be proliferation of availability of brands with both foreign and Indian companies acquiring strong brand equity for their products in near future.

The retail boom currently being witnessed in India is likely to have a significant impact on the commercial real estate sector as the large metropolitans will have sizable retail construction projects underway.

However, there will be few stumbling blocks that may restrict the growth of retail sector. These include very high stamp duties on transfer of property which vary from state to state level. A case in example is Gujarat, Uttar Pradesh and few other states where the stamp duty is charged at 12.5%, while there are certain states like Delhi in which the stamp duty levied is within the range of 8%.

Urban Land Ceiling Act, Rent Control Act and Land Acquisition Act until amended will continue to distort property markets and cities, leading to exceptionally high property prices. Presence of strong pro-tenancy laws will also make it difficult for retailers to grow as this problem is compounded by lack of clarity over titles to ownership.

The government should encourage People of Indian Origin (PIO) to invest in real estate and township building should encourage People of Indian Origin (PIO) to invest in real estate and township building and

9

foreign investment in real estate business and retailing should also be opened up.

On the domestic taxation front, sales tax rates differ across the various Indian states, making supply chain management a challenging task for organized retailers. Inter-state sales attracts Central Sales Tax while for some categories of products, certain states levy import duties namely entry tax on entry of goods into their territory. Simultaneously, states levy export duties where goods are moved for sale outside state border.

Sales tax evasion by small retailers to offer lower prices, fetch higher margins is also commonplace in local markets. In addition to state taxes, certain local authorities also levy octroi.

All these things put together cause irritation and therefore, restrict the growth of our economy. If retailing has to grow than the corrective measures will be needed to be initiated for correcting the aforesaid anomalies to lure investment in Indian retailing.

10

LITERATURE REVIEW

Retail has played a major role world over in increasing productivity across a wide range of consumer goods and services .The impact can be best seen in countries like U.S.A., U.K., Mexico, Thailand and more recently China. Economies of countries like Singapore, Malaysia, Hong Kong, Sri Lanka and Dubai are also heavily assisted by the retail sector.

Retail is the second-largest industry in the United States both in number of establishments and number of employees. It is also one of the largest world wide. The retail industry employs more than 22 million Americans and generates more than $3 trillion in retail sale annually. Retailing is a U.S. $7 trillion sector.

Wal-Mart is the world’s largest retailer. Already the world’s largest employer with over

1million associates, Wal-Mart displaced oil giant Exxon Mobil as the world’s largest company when it posted $219 billion in sales for fiscal 2001. Wal-Mart has become the most successful retail brand in the world due its ability to leverage size, market clout, and efficiency to create market dominance. Wal-Mart heads Fortune magazine list of top 500 companies in the world. Forbes Annual List of Billionaires has the largest number (45/497) from the retail business.

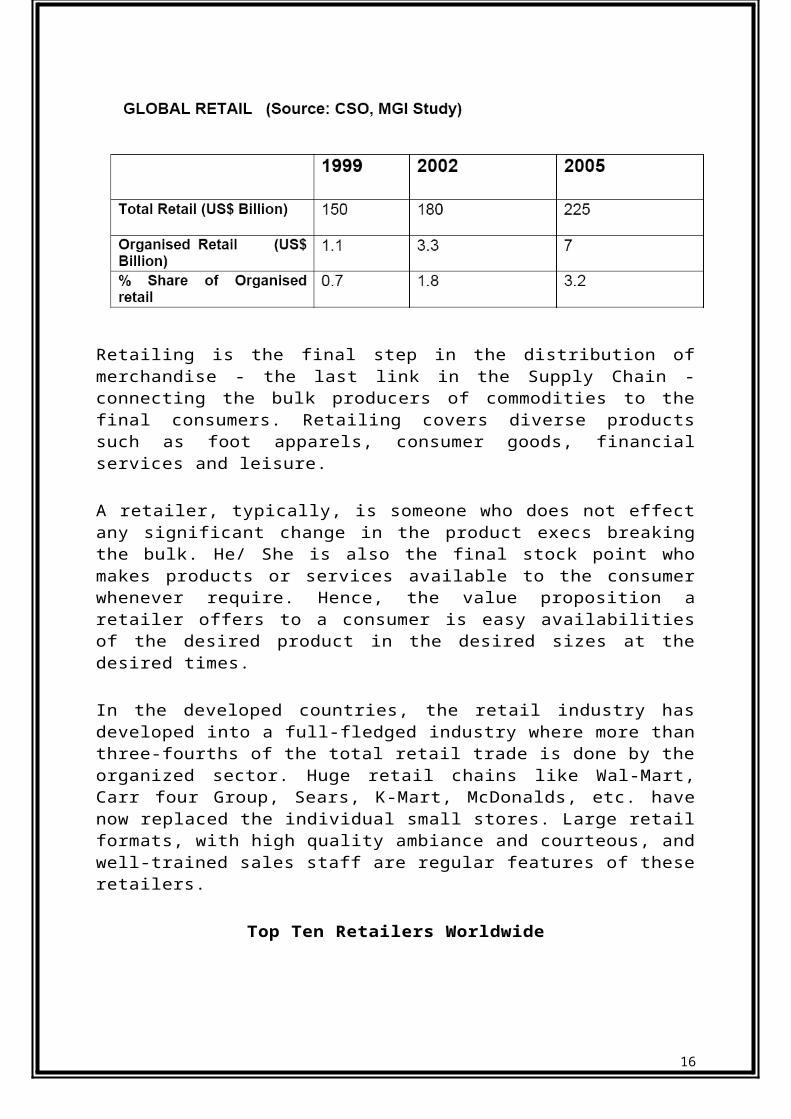

Retailing is the final step in the distribution of merchandise - the last link in the Supply Chain - connecting the bulk producers of commodities to the final consumers. Retailing covers diverse products such as foot apparels, consumer goods, financial services and leisure.

A retailer, typically, is someone who does not effect any significant change in the product execs breaking the bulk. He/ She is also the final

11

stock point who makes products or services available to the consumer whenever require. Hence, the value proposition a retailer offers to a consumer is easy availabilities of the desired product in the desired sizes at the desired times.

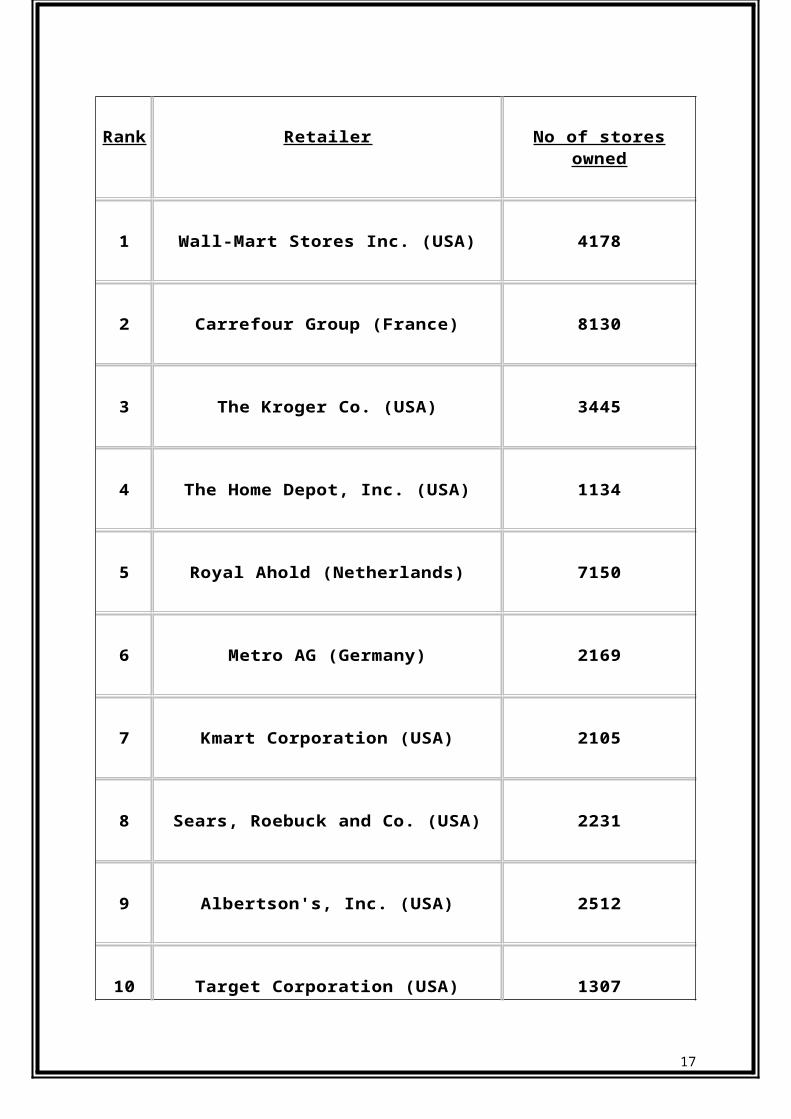

In the developed countries, the retail industry has developed into a full-fledged industry where more than three-fourths of the total retail trade is done by the organized sector. Huge retail chains like Wal-Mart, Carr four Group, Sears, K-Mart, McDonalds, etc. have now replaced the individual small stores. Large retail formats, with high quality ambiance and courteous, and well-trained sales staff are regular features of these retailers.

Top Ten Retailers Worldwide

Rank Retailer No of stores owned

1 Wall-Mart Stores Inc. (USA) 4178

2 Carrefour Group (France) 8130

3 The Kroger Co. (USA) 3445

4 The Home Depot, Inc. (USA) 1134

5 Royal Ahold (Netherlands) 7150

6 Metro AG (Germany) 2169

7 Kmart Corporation (USA) 2105

12

8 Sears, Roebuck and Co. (USA) 2231

9 Albertson's, Inc. (USA) 2512

10 Target Corporation (USA) 1307

Broadly the organized retail sector can be divided into two segments, In-Store Retailers, who operate fixed point-of-sale locations, located and designed to attract a high volume of walk-in customers, and the non-store retailers, who reach out to the customers at their homes or offices.

Apart from using the internet for communication (commonly called e-tailing), non-store retailers did business by broadcasting of infomercials, broadcasting and publishing of direct-response advertising publishing of traditional and electronic catalogues, door-to-door solicitation and temporary displaying of merchandise (stalls).

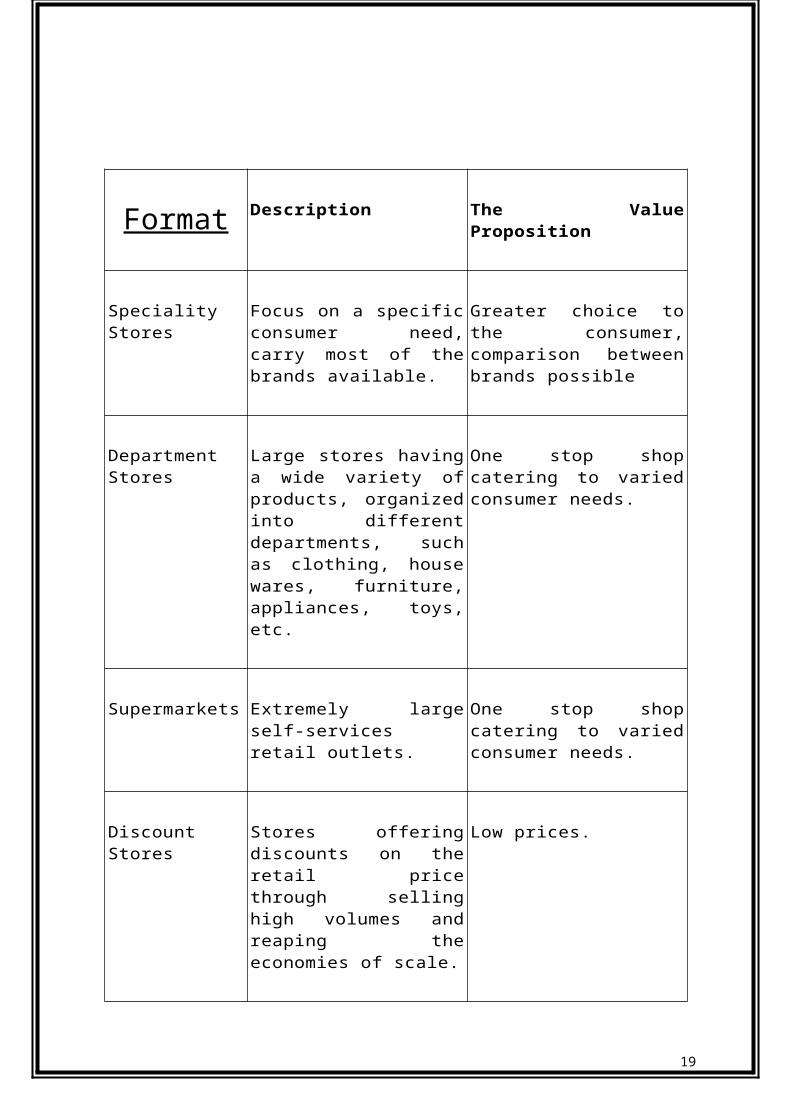

Major formats of In-Store Retailing have been listed in Table given below:

13

Format Description The Value Proposition

Speciality Stores

Focus on a specific consumer need, carry most of the brands available.

Greater choice to the consumer, comparison between brands possible

Department Stores

Large stores having a wide variety of products, organized into different departments, such as clothing, house wares, furniture, appliances, toys, etc.

One stop shop catering to varied consumer needs.

Supermarkets Extremely large self-services retail outlets.

One stop shop catering to varied consumer needs.

Discount Stores Stores offering discounts on the retail price through selling high volumes and reaping the economies of scale.

Low prices.

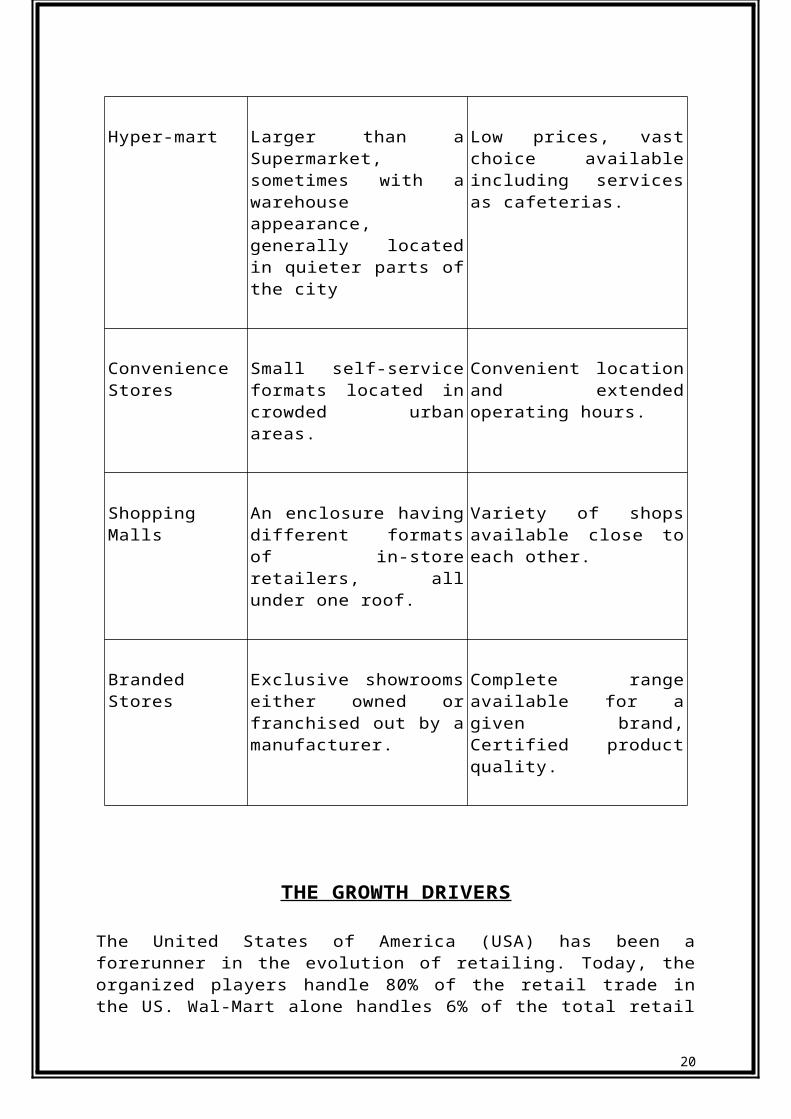

Hyper-mart

Larger than a Supermarket, sometimes with a warehouse appearance, generally located in quieter parts of the city

Low prices, vast choice available including services as cafeterias.

14

Convenience Stores

Small self-service formats located in crowded urban areas.

Convenient location and extended operating hours.

Shopping Malls An enclosure having different formats of in-store retailers, all under one roof.

Variety of shops available close to each other.

Branded Stores Exclusive showrooms either owned or franchised out by a manufacturer.

Complete range available for a given brand, Certified product quality.

THE GROWTH DRIVERS

The United States of America (USA) has been a forerunner in the evolution of retailing. Today, the organized players handle 80% of the retail trade in the US. Wal-Mart alone handles 6% of the total retail trade and the top 50 retailers control 36% of the organized retail. The factors that contributed towards the growth and consolidation of organized retailing in the US are described below:

Baby boomers

The single largest contributor to the growth of organised retailing was the boom in consumer spending after the Second World War. This was caused largely due an increasing population, when America witnessed 64 million births in an 18 year period. Consumer preferences changed and spending patterns became significant drivers for detail expansion thus making retailing an attractive business.

Increased per capita spending

The effect of population increase was further accentuated by an increase in per capita spending. Per capita personal consumption expenditure in the US, rose form $1,796 in 1959 to $22,391 in 1999.

15

Even after adjusting for inflation, the per Capita Expenditure in 1999, was more than double of that in 1959.

Dual income families

Advent of dual income families also helped in the growth of retail sector. A dual family can spend more but has very little time available for shopping. Thus, convenience and speed of service became crucial parameters.

Urbanization

Increased urbanization has led to high customer density areas thus enabling retailers to use lesser number of stores to target the same number of customers. Aggregation of demand that occurs due to urbanization helps a retailer in reaping the economies of scale.

Covering distances has become easier

With increased automobile penetration and an overall improvement in the transportation infrastructure, covering distances has become easier than before. Now a customer can travel miles to reach a particular shop, if he/she sees value in shopping from there.

From the supply side also, a number of developments fueled the growth of the retail industry. Retailers understood the needs of the customers and realized efficiencies through investments in Technology Infrastructure and Employees. The outcomes were improved supply chains, increased service levels and satisfied customers.

16

Evolution of Organized Retailing

American mass retailing began in the late 1800s with Montgomery Ward marketing its products through general merchandise mail order catalogs, which was very effective at that time for reaching a largely rural society.

In the 1940s, the population began its movement to the suburbs as the economy shifted from an agricultural base to an industrialised nation. The first shopping center was opened, which would eventually be a significant factor in the decline of downtown retailing in the 1960s and 70s. JCPenney and Sears began their national mass retailing expansion, and the use of credit cards as major retail chains began.

The 1950s witnessed the reaffirmation of the traditional family. The first planned mall and franchised food restaurant opened. As people continued to flock to the suburbs, the downtown areas began to decline. Larger suburban malls were created and anchored by traditional downtown department store merchants. Freeways were expanded and the sales of private automobiles grew, giving the consumer a wider accessible area in which to shop. Discounters were born, Korvetta being one of the firsts.

The 1960s witnessed the growth of enclosed shopping centers, with department stores anchors and specialty retail chains. The baby boomers were teenagers at this point, leading to the growth of juniors-oriented stores and vendors. Women became targets not just as mothers or wives as they entered the workforce and consumers became more demanding in their expectation of quality and service.

In the 1970s, promotional pricing started to pick up the department stores as off-price retailer emerged. The growth of retail space slowed, as sales increase came at the expense of competition, not of market growth. This competitive market led to the under performance of several retailers as gross margins experienced downtown pressure from increased competition. Retailers in large upscale markets recognised the time shortage created by dual-career families and began to offer more services to assist in saving time.

The 1980s witnessed the growth of off price retailing as a distinct, enduring retail format. Retailers began to drop low profit lines. Acquisitions and mergers were actively utilised as growth strategies, private brands were redeveloped to enhance uniqueness and margins and offshore sourcing was developed to compensate for margins.

17

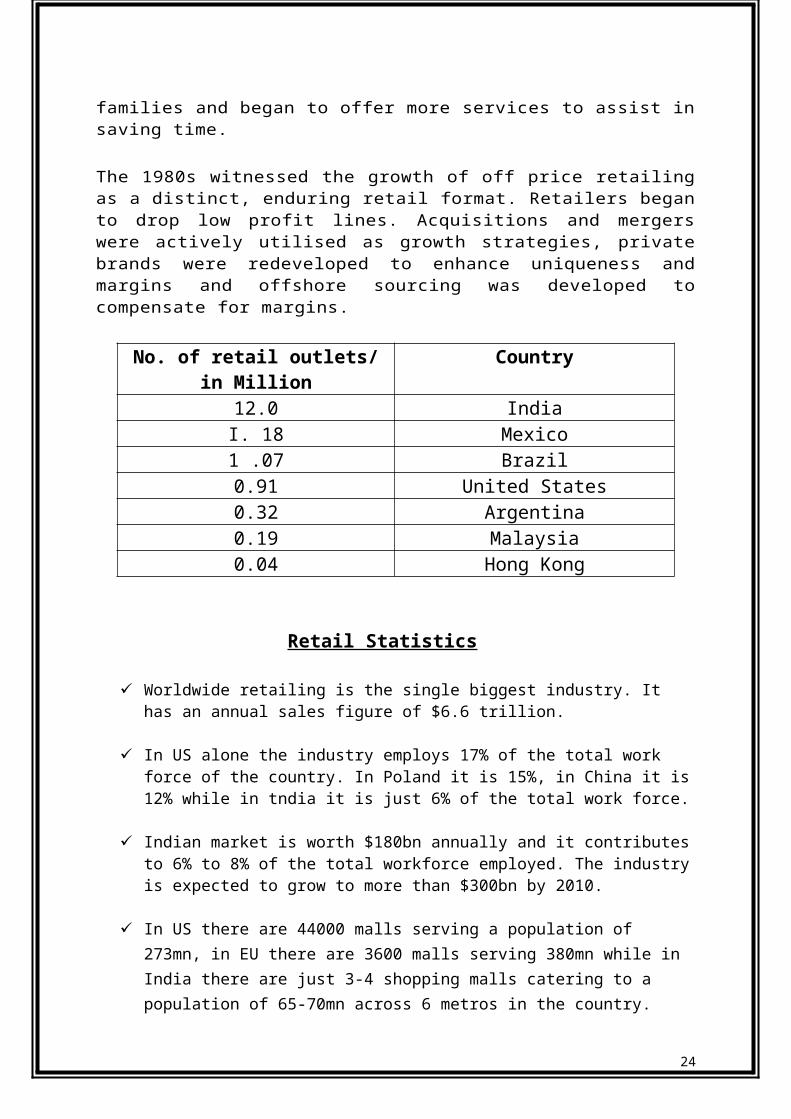

No. of retail outlets/ in Million Country12.0 IndiaI. 18 Mexico1 .07 Brazil0.91 United States0.32 Argentina0.19 Malaysia0.04 Hong Kong

Retail Statistics

Worldwide retailing is the single biggest industry. It has an annual sales figure of $6.6 trillion.

In US alone the industry employs 17% of the total work force of the country. In Poland it is 15%, in China it is 12% while in tndia it is just 6% of the total work force.

Indian market is worth $180bn annually and it contributes to 6% to 8% of the total workforce employed. The industry is expected to grow to more than $300bn by 2010.

In US there are 44000 malls serving a population of 273mn, in EU there are 3600 malls serving 380mn while in India there are just 3-4 shopping malls catering to a population of 65-70mn across 6 metros in the country.

18

RETAIL MODEL

On a basic level, retail is a combination of three components; Product, Process and People. Within these components are elements that when put together form a retail model. Here are the model's main components and elements.

1. Product Selection

Product selection is made up of three elements: Market segment-this determines the type of products to be sold · Scope-the range of the segments· Quality-the characteristics of the segment and scope.

2. Price

The price the consumer pays for the goods offered by the retailer. Process

3. Operational activity

Includes inventory procurement, inventory management, and all necessary administrative activity

4. Structure

The organizational structure is necessary to operate the retail enterprise.

5. Location and site management

The physical plant and location

6. The customer experience

What the customer experiences when conducting business with the retailer.

7. The employee experience

What the employee does and experiences when working for the retailer and interacting with the customer

8. Services

Services such as delivery, installation, in home sales, and personal shoppers are just a few examples. Services are considered a people component as they are most

19

often performed by people and their quality is determined as such share of the market, its image and status and finally its survival.

CRITICAL SUCCESS FACTORS IN RETAILING

Sourcing the Right Merchandise: In an ideal world, before the world beats a path to his door, a retailer would have the right quantity of the right merchandise in the right place, at the right time, while meeting the needs of the customer and maximizing the financial gains at the same time. Sophisticated techniques and advanced technology are being put to use to ensure that the merchant understands what the customer wants, the supplier produces that and the customer gets the merchandise of choice.

Breadth and Depth of Merchandise: This deal with the merchandise mix that the merchandise manager feels would sell in the coming year. The key factors considered while making an assortment plan are the range of prices, brands and sizes to be purchased, based on the merchandise strategy of the store. This assortment plan differs from category to category. Today's reality of a large assortment of merchandise is the biggest challenge for retailers worldwide. It requires technology and people 10 manage, with lots of real-life experience of understanding the consumer and his/her shopping behavior.

Pricing: The pricing policy is a key element of the overall store positioning and merchandising strategy. Most customers today are looking for good value for money, which is often embedded in their demand for lower prices, acceptable quality and service. Retail cost structures in India are similar to those of the western world, but the retail price and the margin structure are lower by about IO per cent. For the retail chains to become successful, retailers have to exhibit very high cost efficiency and get higher margins through private labels or greater cash margins by faster rotation and higher output.

Psychological dimensions: The objective dimensions include among others, credit, physical facilities, warranties, repair services and packaging. The psychological dimensions, which are intangible, include courtesy, attention, knowledge, trust and a sense of security and confidence.

Customer support services: A primary way in which retailers differentiate their outlets from those of the competitors. Many outlets offer the same merchandise at the same price with similar promotion programs. Services provide an opportunity to create a unique image in consumers' minds.

Integrated Marketing: Efficient service and appropriate merchandise are only part of the story to draw in repeat customers. In addition, retail communication that is clear, focused and fully comprehended by the target customer is a must. Most retailers' favor integrated marketing

20

communications, which is the strategic integration of multiple communication methods to form a comprehensive, consistent message. The elements in the retail communication program must work together and reinforce each other so the retailer can achieve its objectives. Without this coordination, the communication methods might work at cross purposes. For example, the retailer's TV advertising campaign might attempt to build an image of exceptional customer service, but the firm's sales promotions might all emphasize low prices.

Promotional Plan: A crucial step in the retail management decision-making process is developing and implementing a promotion program to attract customers to stores and encourage them to buy merchandise. The promotion program informs customers about the store as well as the merchandise and services it offers. The ultimate aim of the retail promotion program is to generate sales from customers in the retailer's target market. To accomplish the goal, retailers use a variety of methods to inform, persuade, and remind customers about the retailer. Promotion is any form of communication from the retailer to the consumer and includes mass media advertising, coupons, price discounts, premium offers, point of purchase displays and publicity. Retailers must decide on who to reach, the message to get across, the number of messages to reach the audience, and the means of reaching the audience. Promotion should be viewed as a sales building investment.

Operational Economies of Scale: All retailers are concerned about the costs of providing their retail offering. Costs are important even to retailers that offer excellent service and sell high priced merchandise to customers who aren't very price sensitive. If a retailer can offer the same merchandise quality of service as its competitor at a lower cost, then it will make either a higher profit margin .fits to attract more customers and increase sates.Space constraints limit stores to narrow product mixes. Companies can leverage cost benefits of all kinds from a larger store base. Corporate overheads can be spread over a larger volume of sales, lowering expense ratios. Greater size can also mean lower occupancy costs, wider product mix, greater buying power and clout- to negotiate with manufactures for volume discounts and cooperative advertising. The lower product costs can be passed on to the consumers in the form of lower prices.

Location: The right location decision for a retailer means being at the right place at the right time. For several reasons, store location is often the most important decision made by a retailer. First, location is typically the prime consideration in a customer's store choice. Second, location decisions have strategic importance because they can be used to develop a sustainable competitive advantage. The important issues in location decisions are the site's accessibility, terms and rates of occupancy and legal considerations. Choosing a site involves evaluation of a series of tradeoffs, in terms of cost and value of the site for a particular retailing format.

21

Store design and ambience: There is more to selling than locations, merchandise and customer service, for which most organizations can develop procedural codes. According to a study by A.T. Kearney, retail design is responsible for about 10% increase in sale. The biggest challenge for a mega-mall or a hypermarket is to create an environment that pulls in people and makes them spend more time shopping. Two major factors that set one store apart from another-store layout (the design or interior architecture), and visual merchandising. Interiors and display are effective tools for store differentiation.

Store design refers to the style or atmosphere of a store that helps project an image to the market. Store design elements include such exterior factors as the storefront and window displays and such interior factors as colors, lighting, flooring and fixtures. It is an important image-creating element and should begin with an understanding of preferences, desires and expectations of the store's target market. When designing a store, managers must consider three objectives. First the store's atmosphere must be consistent with the store's image and overall strategy. Second, it should help influence customer's buying decisions. And finally, the productivity of the retail space-how many sales can be generated out of each square foot of space.

Supply Chain Management and Logistics: Logistics is the organized process of managing the flow of merchandise from the source of supply-the vendor, wholesaler, or distributor-through the internal processing functions warehousing and transportation -until the merchandise is sold and delivered to the customer. Today, many retailers work closely with their vendors to predict customer demand, shorten lead times for receiving merchandise, and reduce inventory investment. They've established on line systems that link their point of sale cash registers to computer terminals on their desks. They can determine exactly what's selling by item classification, store, or vendor on a minute by-minute basis. As a result, inventory investment can be reduced and customer service levels improved

22

KEY STRATEGIC FACTORS IN RETAILING

The key to success is identifying a superior value-promise and who is in a better position to do it than retailers? Retailers are the closest to the point of purchase and have access to a wealth of information on consumer shopping behavior. Retailers have some unique advantages for managing brands such as continuous and actionable dialogue with consumers, control over brand presentation at point-of sale, control over shopping environment, display location/adjacencies, and signage. And they have used this advantage with tremendous success.

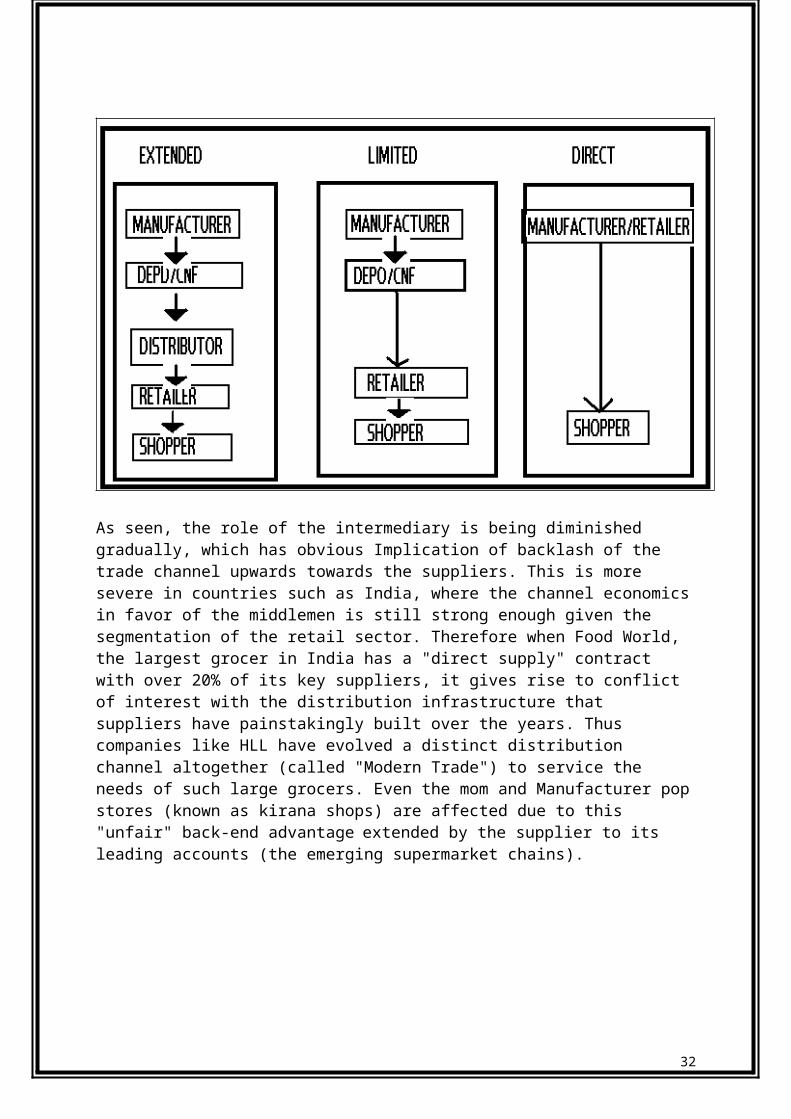

The 3 stages of evolution of the trade channel are shown in the exhibit below:

As seen, the role of the intermediary is being diminished gradually, which has obvious Implication of backlash of the trade channel upwards towards the suppliers. This is more severe in countries such as India, where the channel economics in favor of the middlemen is still strong enough given the segmentation of the retail sector. Therefore when Food World, the largest grocer in India has a "direct supply" contract with over 20% of its key suppliers, it gives rise to conflict of interest with the distribution infrastructure that suppliers have painstakingly built over the years. Thus companies like HLL have evolved a distinct distribution channel altogether (called "Modern Trade") to service the needs of such large grocers. Even the mom and Manufacturer pop stores (known as kirana shops) are affected due to this "unfair" back-end advantage extended by the supplier to its leading accounts (the emerging supermarket chains).

23

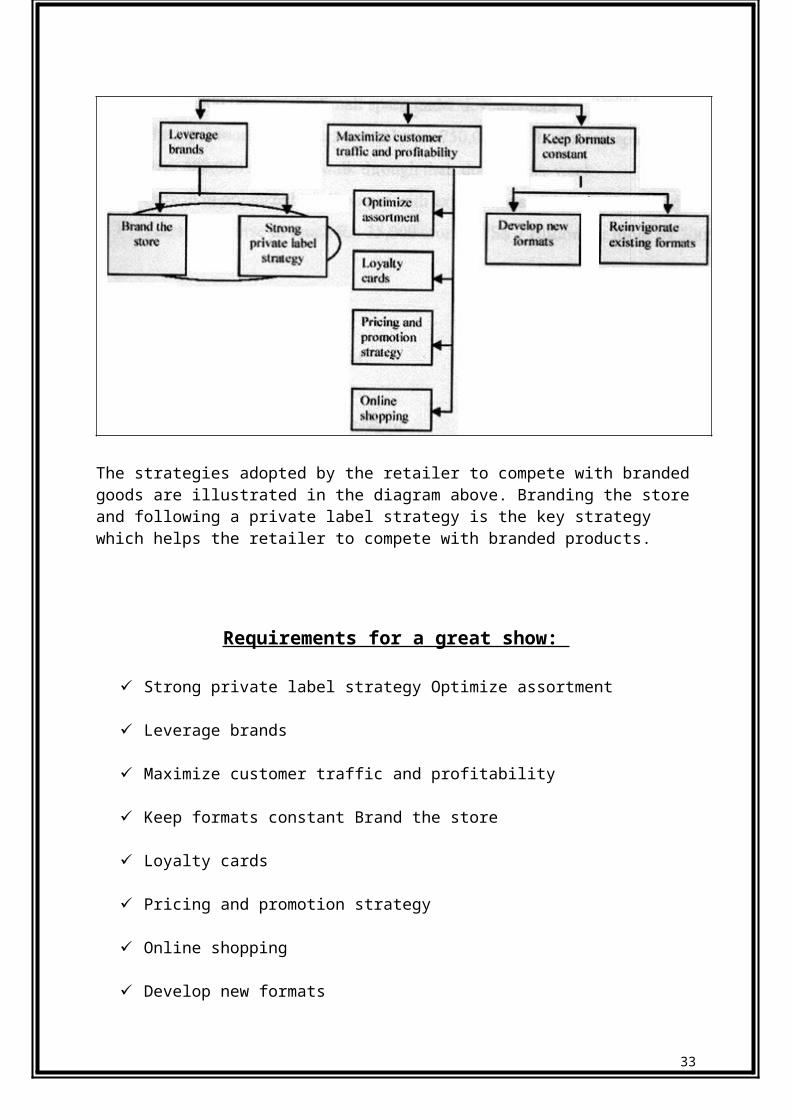

The strategies adopted by the retailer to compete with branded goods are illustrated in the diagram above. Branding the store and following a private label strategy is the key strategy which helps the retailer to compete with branded products.

Requirements for a great show:

Strong private label strategy Optimize assortment

Leverage brands

Maximize customer traffic and profitability

Keep formats constant Brand the store

Loyalty cards

Pricing and promotion strategy

Online shopping

Develop new formats

Reinvigorate existing formats

24

Retailing in India

The retail market size in India is estimated to be around $180 billion. Retailing provides jobs to almost 15 percent of employable Indian adults and it is perhaps the largest contributor to India's GDP.

But the flip side of the coin is that the average size of each of the retail outlets in India is only 50 square feet and though a large employer, the industry is very unorganized, fragmented and with a rural bias.

The Indian retail industry is unorganized

There are nearly twelve million retail outlets in India and the number is growing. Two thirds of these stores are in rural location. The vast majority of the twelve million stores are small "father and son" outlets. According to the "Retailing in India" report published by the PwC Global Retail Intelligence Program, share of the unorganized sector is 98%.

Some Key Facts about Indian Retail Industry

INDIA – A Vibrant Economy & Resplendent Market

4th Largest economy in PPP terms after USA, China & Japan.

To be the 3 rd largest economy in terms of GDP in next 5 years.

2nd fastest growing economy in the world.

The US $ 580 billion economy grew 8.2 percent in the year 03-04

Among top 10 FDI destinations

Stable Government with 2 nd stage reforms in place

Growing Corporate Ethics (Labour laws, Child Labour regulations,

environmental protection lobby, intellectual and property rights, social

responsibility).

Major tax reforms including implementation of VAT.

2nd Second most attractive developing market, ahead of China

5th among the 30 emerging markets for new retailers to enter

25

With over 600 million effective consumers by 2010 India to emerge as one of the

largest consumer markets of the world by 2010.

Five Reasons why Indian Organized Retail is at the brink of Revolution:

Scalable and Profitable Retail Models are well established for most of the

categories

Rapid Evolution of New-age Young Indian Consumers

Retail Space is no more a constraint for growth

Partnering among Brands, retailers, franchisees, investors and malls

India is on the radar of Global Retailers Suppliers

Looking Ahead

Many strong regional and national players emerging across formats and product

categories Most of these players are now geared to expand far more rapidly than the

initial years of starting up Most have regained / improved profitability after going

through their respective learning curves.

Malls in India

A decade ago – not a single mall

A year ago – less than half a dozen

Today – 40 malls

2 years from now – 300 malls

26

THE INDIAN RETAIL INDUSTRY

Retail stores in India are mostly small individually owned businesses. The average size of an outlet is 50 sq.ft. ft. and though India has the highest number of retail outlets per capita in the world, the retail space per capita at 2 sq.ft. ft per person is amongst the lowest in the world.

Nearly two thirds of the stores are located in rural areas. The retail industry in rural India has typically two forms: "Haats" and "melas". Haats are the weekly markets: they serve groups of 10-50 villages and sell day-to-day necessities. They are frequently used as replenishment point for the small village retailer. Melas are larger in size and more sophisticated in terms of the goods sold. Mela merchandise would include more complex manufactured products such as televisions.

THE EVOLUTION OF INDIAN RETAIL INDUSTRY

For Indian retailing, things started to change slowly in the 1980s,

when India first began opening its economy. Textiles sector (which companies like Bombay Dyeing,

Raymond's, S Kumar's and Grasim) was the first to see the

emergence of retail chains. Later on, Titan, maker of premium

watches, successfully created an organized retailing concept in

India by establishing a series of elegant showrooms.

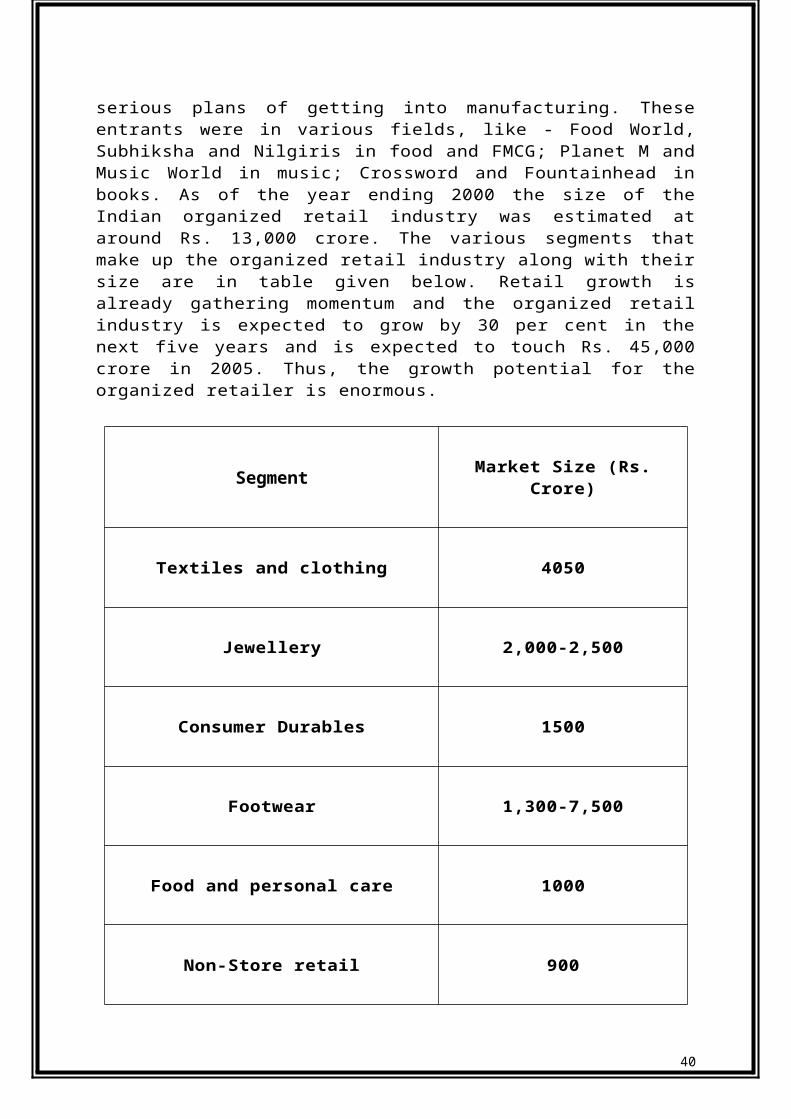

For long, these remained the only organized retailers, but the latter half of the 1990s saw a fresh wave of entrants in the retailing business. This

27

time around it was not the manufacturer looking for an alternative sales channel. These were pure retailers with no serious plans of getting into manufacturing. These entrants were in various fields, like - Food World, Subhiksha and Nilgiris in food and FMCG; Planet M and Music World in music; Crossword and Fountainhead in books. As of the year ending 2000 the size of the Indian organized retail industry was estimated at around Rs. 13,000 crore. The various segments that make up the organized retail industry along with their size are in table given below. Retail growth is already gathering momentum and the organized retail industry is expected to grow by 30 per cent in the next five years and is expected to touch Rs. 45,000 crore in 2005. Thus, the growth potential for the organized retailer is enormous.

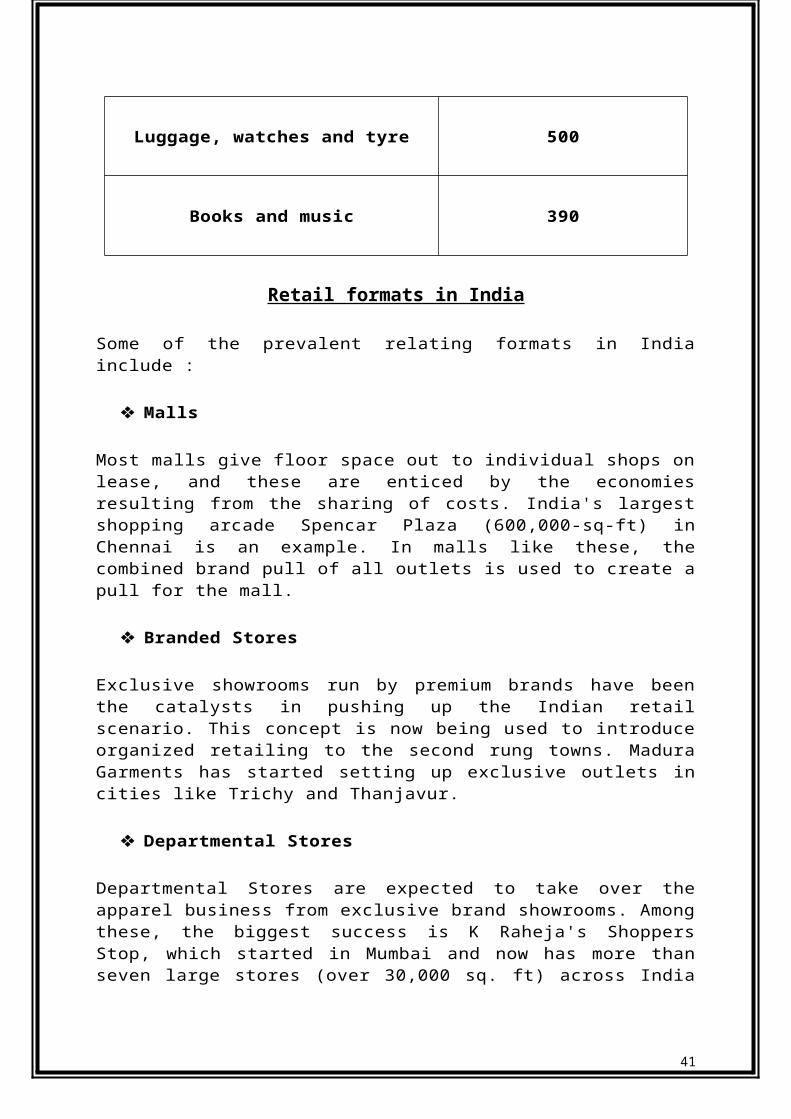

Segment Market Size (Rs. Crore)

Textiles and clothing 4050

Jewellery 2,000-2,500

Consumer Durables 1500

Footwear 1,300-7,500

Food and personal care 1000

Non-Store retail 900

Luggage, watches and tyre 500

Books and music 390

28

Retail formats in India

Some of the prevalent relating formats in India include :

Malls

Most malls give floor space out to individual shops on lease, and these are enticed by the economies resulting from the sharing of costs. India's largest shopping arcade Spencar Plaza (600,000-sq-ft) in Chennai is an example. In malls like these, the combined brand pull of all outlets is used to create a pull for the mall.

Branded Stores

Exclusive showrooms run by premium brands have been the catalysts in pushing up the Indian retail scenario. This concept is now being used to introduce organized retailing to the second rung towns. Madura Garments has started setting up exclusive outlets in cities like Trichy and Thanjavur.

Departmental Stores

Departmental Stores are expected to take over the apparel business from exclusive brand showrooms. Among these, the biggest success is K Raheja's Shoppers Stop, which started in Mumbai and now has more than seven large stores (over 30,000 sq. ft) across India and even has its own in store brand for clothes called Stop!.

Specialty Stores

Chains such as the Bangalore based Kids Kemp, the Mumbai books retailer Crossword, RPG's Music World and the Times Group's music chain Planet M, are focusing on specific market segments and have established themselves strongly in their sectors.Absence of discounting as a dominant format of retailing in India is a glaring peculiarity. The reasons are two-fold. Unlike most Western countries, Indian retailers have much less bargaining power. They thrive as small store and don't have the clout to negotiate terms with the manufacturers. The other reason is that the retailers themselves have no economies of scale to offer discounts on their own. However, the scenario is now changing. Increased investments and the entry

29

of big business houses in retailing is leading to the emergence of bigger retailers, who can both bargain with the suppliers, as well as, reap economies of scale. Hence, discounting is becoming an accepted practice.

RECENT TRENDS IN RETAILING

Retailing is the second largest industry in the world, one of the largest employers of the world and an index of economic growth. In India there are about 5 million retail outlets varying in sizes and nomenclatures. India has the highest number of retail outlets per capita in the world but has the lowest retail space per capita in the world (2 ft / person). Out of these 5 million outlets 96% are smaller than 500 sq. ft. in area 3. There are about 3 million outlets in India’s 3700 designated towns and more than 6,00,000 villages. About 350 million people live, within one-minute walk of these retail shops. According to retail census conducted by market researcher ORG-MARK, Rs.4,79,568 crore worth of products were sold through theses million retail outlets Manufacturers owned and retail chain store are springing up in urban areas to market consumer goods to the middle class in a much similar style as malls around the globe. At present about 8% of the Indian population is employed in the retailing industry as against 20% in USA. As India moves towards the service oriented economy, a rise in this percentage is expected. The number of the retail outlets is growing at about 8.5% annually in the urban areas and in towns with population between 1, 00,000 to I million; the growth rate is about 4.5%.

Retailing in India is at a nascent stage of is evolution, but within a small period of time certain trends are clearly emerging which are in line with the global experiences. Organised retailing is witnessing a wave of players entering the industry. These players are experimenting with various retail formats. Yet, Indian retailing has still not been able to come up with many successful formats that can be scaled up and applied across India. Some of the notable exceptions have been garment retailers like Madura Garments & Raymonds who was scaled their exclusive showroom format across the country.

According to Kurt Salmon Association, a global management consulting firm, organized retailing seems all set to power ahead from Rs. 5000 crore currently to about Rs.30,000 crore in next live years. A. T. Kearney reports that organized retailing will account for about 20% of the total $8 trillion retail market in India in the next 5-7 years as against 1-2% today.

30

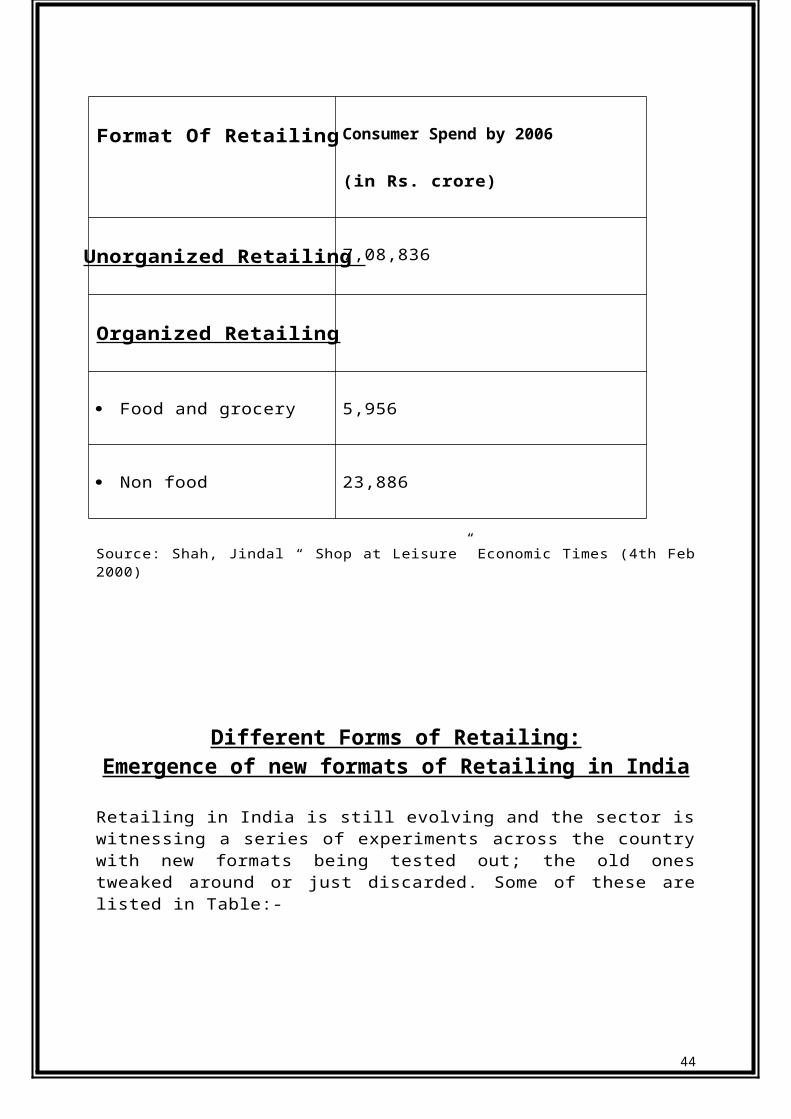

Format Of Retailing Consumer Spend by 2006

(in Rs. crore)

Unorganized Retailing 7,08,836

Organized Retailing

Food and grocery 5,956

Non food 23,886

Source: Shah, Jindal “ Shop at Leisure” Economic Times (4th Feb 2000)

Different Forms of Retailing:Emergence of new formats of Retailing in India

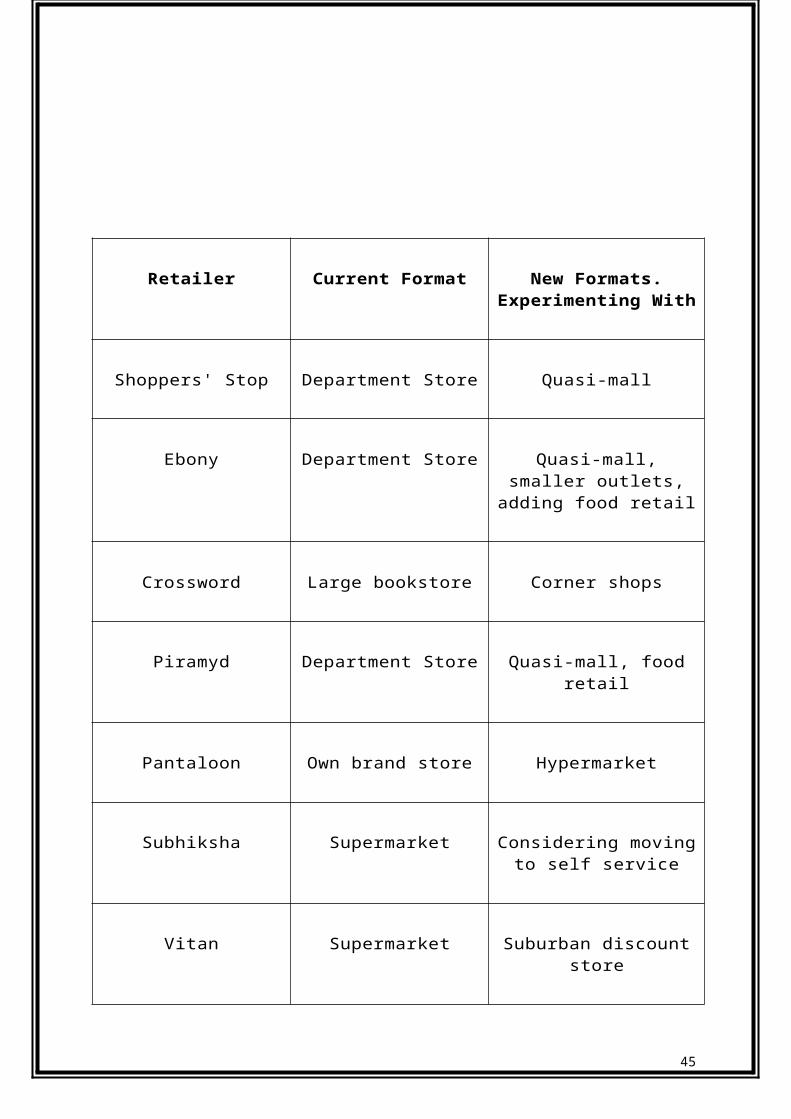

Retailing in India is still evolving and the sector is witnessing a series of experiments across the country with new formats being tested out; the old ones tweaked around or just discarded. Some of these are listed in Table:-

31

Retailer Current Format New Formats. Experimenting With

Shoppers' Stop Department Store Quasi-mall

Ebony Department Store Quasi-mall, smaller outlets, adding food

retail

Crossword Large bookstore Corner shops

Piramyd Department Store Quasi-mall, food retail

Pantaloon Own brand store Hypermarket

Subhiksha Supermarket Considering moving to self service

Vitan Supermarket Suburban discount store

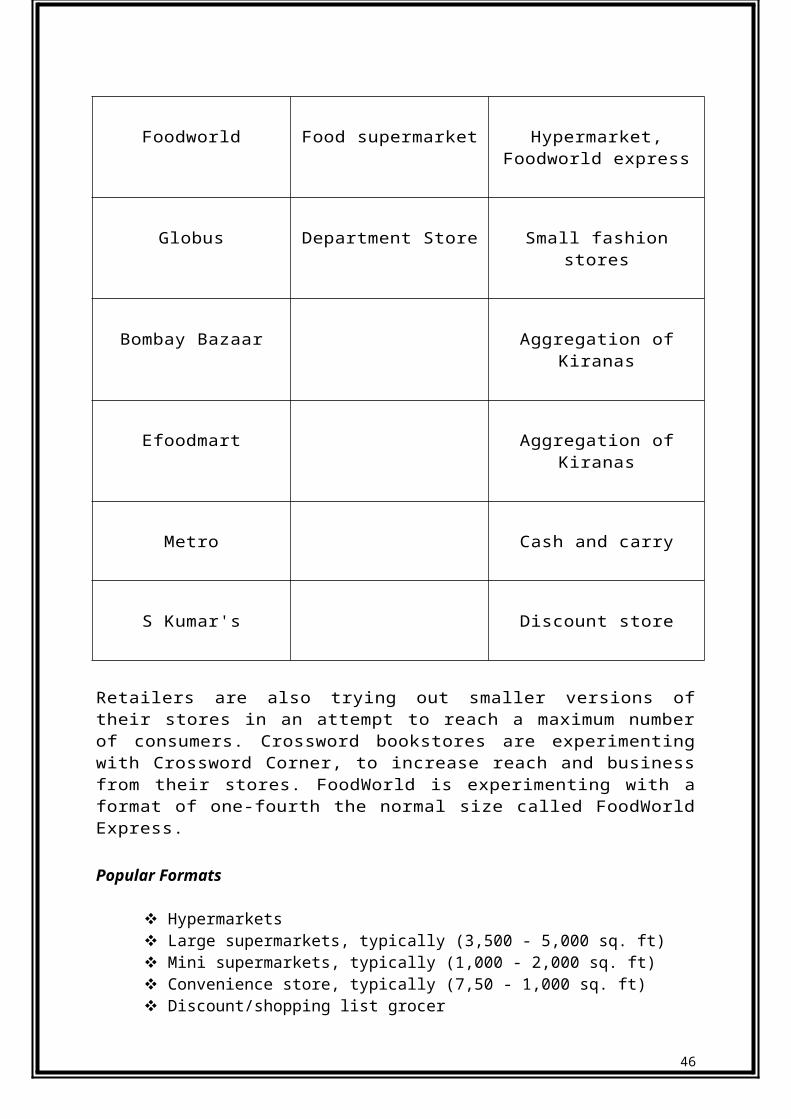

Foodworld Food supermarket Hypermarket, Foodworld express

Globus Department Store Small fashion stores

32

Bombay Bazaar Aggregation of Kiranas

Efoodmart Aggregation of Kiranas

Metro Cash and carry

S Kumar's Discount store

Retailers are also trying out smaller versions of their stores in an attempt to reach a maximum number of consumers. Crossword bookstores are experimenting with Crossword Corner, to increase reach and business from their stores. FoodWorld is experimenting with a format of one-fourth the normal size called FoodWorld Express.

Popular Formats

Hypermarkets Large supermarkets, typically (3,500 - 5,000 sq. ft) Mini supermarkets, typically (1,000 - 2,000 sq. ft) Convenience store, typically (7,50 - 1,000 sq. ft) Discount/shopping list grocer Traditional retailers trying to reinvent by introducing self-service formats as

well as value-added services such as credit, free home delivery etc.

The Indian retail sector can be broadly classified into:

a) FOOD RETAILERS

There are large number and variety of retailers in the food-retailing sector.Traditional types of retailers, who operate small single-outlet businesses mainly using family labor, dominate this sector .In comparison, super markets account for a small proportion of food sales in India. However the growth rate of super market sales has being significant in recent years because greater numbers of higher incomeIndians prefer to shop at super markets due to higher standards of hygiene and attractive ambience.

33

b) HEALTH & BEAUTY PRODUCTS

With growth in income levels, Indians have started spending more on health and beauty products .Here also small, single-outlet retailers dominate the market. However in recent years, a few retail chains specializing in these products have come into the market. Although these retail chains account for only a small share of the total market , their business is expected to grow significantly in the future due to the growing quality consciousness of buyers for these products .

c) CLOTHING & FOOTWEAR

Numerous clothing and footwear shops in shopping centers and markets operate all over India. Traditional outlets stock a limited range of cheap and popular items; in contrast, modern clothing and footwear stores have modern products and attractive displays to lure customers. However, with rapid urbanization, and changing patterns of consumer tastes and preferences, it is unlikely that the traditional outlets will survive the test of time.

d) HOME FURNITURE & HOUSEHOLD GOODS

Small retailers again dominate this sector. Despite the large size of this market, very few large and modern retailers have established specialized stores for these products. However there is considerable potential for the entry or expansion of specialized retail chains in the country.

e) DURABLE GOODS

The Indian durable goods sector has seen the entry of a large number of foreign companies during the post liberalization period. A greater variety of consumer electronic items and household appliances became available to the Indian customer.Intense competition among companies to sell their brands provided a strong impetus to the growth for retailers doing business in this sector.

f) LEISURE & PERSONAL GOODS

Increasing household incomes due to better economic opportunities have encouraged consumer expenditure on leisure and personal goods in the country.There are specialized retailers for each category of products (books, music products, etc.) in this sector. Another prominent feature of this sector is popularity of franchising agreements between established manufacturers and retailers.

34

RETAILING, INDIA'S LARGEST INDUSTRY AND ONE OF THE BIGGEST SOURCES OF EMPLOYMENT IN THE COUNTRY GENERATES MORE THAN 10 PER CENT OF INDIA'S GDP. ORGANISED RETAILING HOWEVER. OCCUPIES A MINISCULE TWO TO THREE PERCENT OF THE OVERALL INDIAN RETAILING INDUSTRY. WITH AROUND 13°/ CONTRIBUTION TO THE GDP AND 7% EMPLOYMENT OF THE NATIONAL WORKFORCE. RETAILING NO DOUBT IS A STRONG PILLAR OF THE INDIAN ECONOMY. WHAT IT REOUIRES IS MORE CORPORATE BACKED RETAIL OPERATIONS THAT HAVE STARTED TO EMERGE OVER THE PAST COUPLE OF YEARS.

Store design

Irrespective of the format, the biggest challenge for organized retailing is to create an environment that pulls in people and makes them spend more time shopping and also increases the amount of impulse shopping. Research across the world shows that the chances of senses dictating sales are as much as 10-15% for certain categories. This reason is good enough for organized retailers to bring in professional designers while developing a new property. And, that is why retail chains like MusicWorld, Barista, Pyramid and Globus and laying major emphasis & investing heavily in store design.

MusicWorld spent three months in college campuses and metros studying the market and talking to youngsters before starting work. The brand identity was created after extensive research: a logo was designed and the look of the stores across the country was decided upon. Apart from the visual impact, the functionality of the store design was also taken care of. Listening posts have been created for people to listen to their favorite album and an area in the center of the stores has been earmarked for celebrity visits and promotions.

Emergence of Discount Stores

What does Subhiksha In Chennai, Margin Free in Kerala and recent entrants like Bombay Bazaar in Mumbai, RPG's - Giant in Hyderabad, Big Bazaar in Kolkata, Hyderabad and Bangalore have in common? Their products are below MRP.

Discount stores have finally arrived in India and they are expected to spearhead the revolution in organization retailing. Though this segment is growing, it is small compared to international standards where around 60 per cent of the business comes from this format. Internationally, the largest retailer in the world Wal-Mart is a discounter. These discount stores have advantages of price, assortment dominance and quality assurance and have the ability to quickly build scale and pass on the benefits. However, the success would be for retailers who are able to

35

build the scale fast and manage their operations efficiently while offering value to the customer consistently.

Unorganized Retailing is getting Organized

To meet the challenges of organized retailing that is luring customers away from the unorganized sector, the unorganized sector is getting organized. 25 stores in Delhi under the banner of Provision mart are joining hands to combine monthly buying.Bombay Bazaar and Efoodmart have also been formed which are aggregations of Kiranas.

In a novel move, six Delhi based restaurants have come together and formed a consortium: NFC, to promote New Friends Colony, a posh locality in the Capital, as a branded place in town. The aim is to increase footballs in the area, which is fast losing its sheen to its closest and upcoming destinations such as large Cineplex’s, and malls, which are backed by the corporate house such as 'Ansals' and 'PVR'.

The Indian retail sector is estimated to have a market size of about $ 180 billion; but the organized sector represents only 2% share of this market. Most of the organized retailing in the country has just started recently, and has been concentrated mainly in the metro cities. India is the last large Asian economy to liberalize its retail sector. In Thailand, more than 40% of all consumer goods are sold through the super markets and departmental stores. A similar phenomenon has swept through all other Asian countries. Organized retailing in India has a huge scope because of the vast market and the growing consciousness of the consumer about product quality and services.A study conducted by Fitch, expects the organized retail industry to continue to grow rapidly, especially through increased levels of penetration in larger towns and metros and also as it begins to spread to smaller cities and B class towns. Fuelling this growth is the growth in development of the retail-specific properties and malls. According to the estimates available with Fitch, close to 25mn sq. ft. of retail space is being developed and will be available for occupation over the next 36-48 months. Fitch expects organized retail to capture 15%-20% market share by 2010.

McKinsey report on India says organized retailing would increase the efficiency and productivity of entire gamut of economic activities, and would help in achieving higher GDP growth. At 6%, the share of employment of retail in India is low, even when compared to Brazil (14%), and Poland (12%).

36

Present Indian Scenario - Retail Realities:

Unorganized market: Rs. 583,000 crores Organized market: Rs.5,000 crores Over 4,000 new modern retail outlets in the last 3 years Over 5,000,000 sq. ft.

of mall space under development The top 3 modem retailers control over 750,000 sq. ft. of retail space Over 400,000 shoppers walk through their doors every week Growth in organized retail on par with expectations and projections of the last

5 Years on course to touch Rs. 35,000 crores (US$ 7 Billion) or more by 2005-06

Major players:

FoodWorld

Shoppers' Stop

Subhiksha

Westside

Big Bazzar

Planet M

Nilgris

Vishal Mega Mart

Lifestyle

Music World

Adani-Rajiv's

Piramyd Crossword Nirma-Radhey

Globus

Lifespring Ebony

Pantatoon

37

A SNAPSHOT OF RETAIL OUTLETS IN INDIA

38

Challenges of Retailing in India

Retailing as an industry in India has still a long way to go. To become a truly flourishing industry, retailing needs to cross the following hurdles:

Automatic approval is not allowed for foreign investment in retail. Regulations restricting real estate purchases, and cumbersome local

laws. Taxation, which favors small retail businesses. Absence of developed supply chain and integrated IT management. Lack of trained work force. Low skill level for retailing management. Intrinsic complexity of retailing – rapid price changes, constant threat of

product obsolescence and low margins.

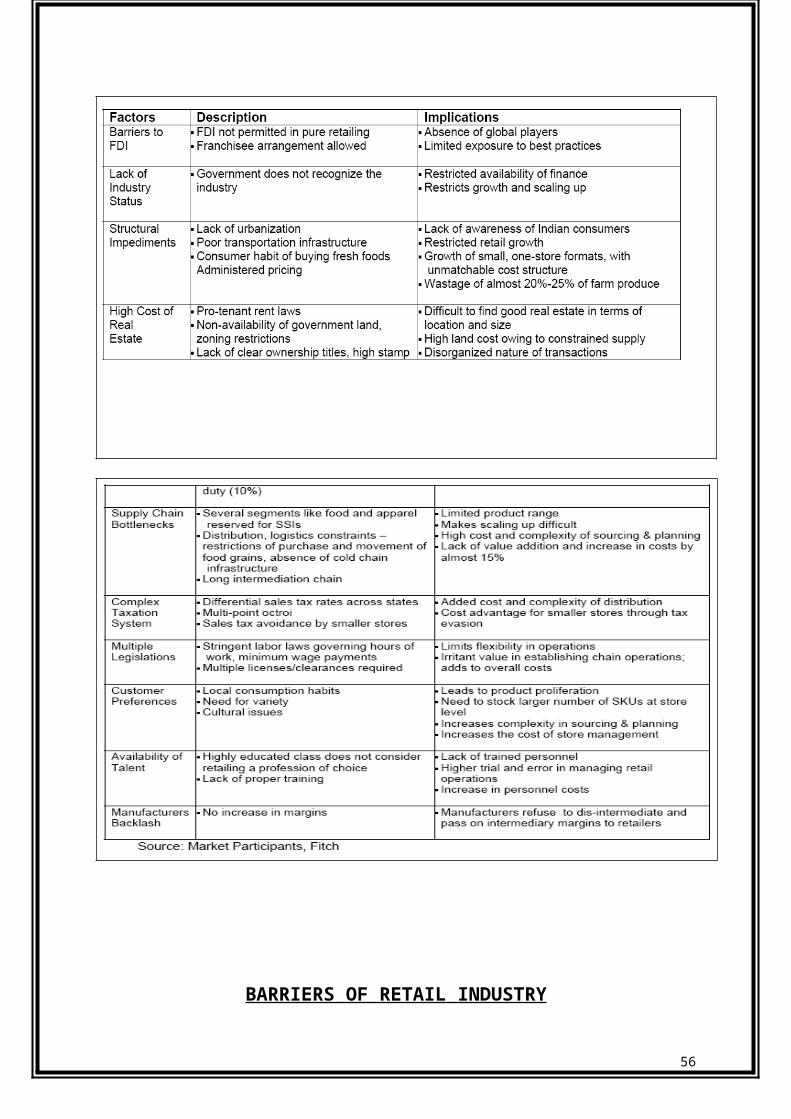

The retailers in India have to learn both the art and science of retailing by closely following how retailers in other parts of the world are organizing, managing, and coping up with new challenges in an ever-changing marketplace. Indian retailers must use innovative retail formats to enhance shopping experience, and try to understand the regional variations in consumer attitudes to retailing. Retail marketing efforts have to improve in the country - advertising, promotions, and campaigns to attract customers; building loyalty by identifying regular shoppers and offering benefits to them; efficiently managing high-value customers; and monitoring customer needs constantly, are some of the aspects which Indian retailers need to focus upon on a more pro-active basis.Despite the presence of the basic ingredients required for growth of the retail industry inIndia, it still faces substantial hurdles that will retard and inhibit its growth in the future. One of the key impediments is the lack of FDI status. This has largely limited capital investments in supply chain infrastructure, which is a key for development and growth of food retailing and has also constrained access to world-class retail practices. Multiplicity and complexity of taxes, lack of proper infrastructure and relatively high cost of real estate are the other impediments to the growth of retailing. While the industry and the government are trying to remove many of these hurdles, some of the roadblocks will remain and will continue to affect the smooth growth of this industry. Fitch believes that while the market share of organized retail will grow and become significant in the next decade, this growth would, however, not be at the same rapid pace as in other emerging markets. Organized retailing in India is gaining wider acceptance. The development of the organized retail sector, during the last decade, has begun to change the face of retailing, especially, in the major metros of the country. Experiences in the developed and developing countries prove that performance of organized retail is strongly linked to the performance of the economy as a whole. This is mainly on account of the reach and penetration of this business and its scientific approach in dealing with customers and their needs. In spite of the

39

positive prospects of this industry, Indian retailing faces some major hurdles (see Table 1), which have stymied its growth. Early signs of organized retail were visible even in the 1970s when Nilgiris (food), Viveks (consumer durables) and Nallis (sarees) started their operations. However, as a result of the roadblocks (mentioned in Table 1), the industry remained in a rudimentary stage. While these retailers gave the necessary ambience to customers, little effort was made to introduce world-class customer care practices and improve operating efficiencies. Moreover, most of these modern developments were restricted to south India, which is still regarded as a ‘Mecca of Indian Retail’.

40

BARRIERS OF RETAIL INDUSTRY

Presently, retailing in India is highly unorganized. There is no supply chain management perspective and virtually no economies of scale. The major entry barriers faced by modem retailers in tackling the Indian market are as listed below:

a) The unorganized

The first and major challenge facing the organized retail industry in India is competition from the unorganized sector. Traditional retailing has been established in India for many centuries. The local kirana shop or the street grocer still commands the business. Estimates show that this unorganized sector accounts for nearly 95 to 99 percent of the total retail business in the country. This sector has a low cost structure; is mostly owner-operated; and little or no taxes to pay. Consumer familiarity that runs from generation to generation is a major advantage for this traditional retailing sector.

In contrast, players in the organized sector have big expenses to meet, and yet need to keep prices low enough to be able to compete with the traditional sector. High costs for the organized sector arise from higher real estate costs (as most of these retail stores are located on prime real estates in big cities), high labour costs, costs

41

for providing comfort facilities such as air-conditioning, value added services like home delivery, back-up power supply, high inventory costs, taxes etc.

b) Supply chain management

Product availability and efficient transportation systems have historically been limited, which made merchandising difficult for large modem retailers.

c) Sourcing economics

The absence of large retail chains does not allow large purchases, and hence no sourcing economies are possible.

d) Automobile ownership

In India, automobile owners are limited to around 1 percent of the population. This makes difficult, the development of out-of town shopping malls and superstores. This also limits the ability of customers to make large purchases; while large shopping baskets from the very essence of shopping in retail superstores.Thus the retailers have to establish its store at the center of the town i.e. Main markets which are very costly areas and thus add to high initial cost.

e) Infrastructure

Poor communications Infrastructure, as well as local government regulations like octroi, makes the development of an efficient logistics and inventory management system difficult.This again makes the organized player at disadvantage as they have high cost, pays high taxes (unorganized players escapes from taxes) which add to high prices of products whereas as in west, Big retailers maintains low cost of product due to efficient logistic & inventory management.

f) Middle class psyche (Big is Costly)

Another major bottleneck is the middle-class psychology that bigger and brighter sales outlets automatically translate to higher prices. While this is partially a myth; unlike the retail stores in the west, this is yet to be proven wrong in India. The local grocer still continues to be cheaper than the large supermarkets.

g) Large-scale diversity

42

India is a large country with a wide diversity in language, culture, religion etc. The preferences of people evening neighboring town/cities may vary significantly. This difference in life-styles and preferences also exist between neighborhoods within the same town. This diversity increases dependence on local suppliers for goods to match the preferences of the local customers, while hindering large-scale purchases from consolidated sources. The above drawbacks, while discouraging setting up of large retail chains, also presents a unique opportunity to international and/or professionally managed Indian corporations to pioneer a currently non-existent modem retailing industry in India, and subsequently benefit from it.

h) Timing

Another major pitfall for the retail Industry is Timings. According to shop Act, each shop has to keep a day of as per Market Norms and also we are require to work strictly under 9A.M to 8 P.M norm.

This restriction does not allow the retailer to draft the suitable time as per the consumer as they would prefer to shop on Sundays and also late hours

FACTORS THAT WOULD LEAD TO GROWTH IN RETAIL SECTOR

Increasing growth in disposable income.

Increasing demand of products by consumers,

Changing life styles.

Better product and shopping options available with consumers

Relaxation of a number of regulations by government.

Rethinking on existing Real estate laws (like governmental plans for ULCA).

Restructuring in Tax regime (like uniform sales tax for all states).

Increased investment and focus on infrastructure by Government.

43

GUIDELINE FOR ESTABLISHING A NEW RETAIL BUSINESS

In a bid to provide a guideline to those who might be considering starting a new retail business, we present a checklist to be followed by them:

A. Self-Assessment and Business Choice

Evaluate your strengths and weaknesses vis-a-vis your target segment. Answer the questions: Why should you be in business for yourself? Why open

a new business rather than acquire an existing one or become a member of a franchise chain?

Decide the differentiating factor for the business and the way in which you intend to capitalize on competitors' weaknesses.

Consider the effect that owning this business will have on your life-style and your family relationships.

B. Overall Retail Plan

State your philosophy of the business.

44

Choose an ownership form (sole proprietorship, partnership or corporation).

State long- and short-run goals, Analyze customers from their point of view. Research your market size and store location. Analyze your competition. Quantify your potential market share. Develop a specific retail strategy

C. Financial Plan

Decide the level of funds you will need to get started and to get through the first year and where they will come from.

Determine the first year profit and return on investment. Project monthly cash flow and profit-and-loss statements for the first two

years Find out the amount of sales needed to breakeven in the time you stipulate.

Decide upon the contingency plan if these sales are not reached in the specified time period.

D. Organizational Details Plan (Administrative Management)

Describe your personnel plan (hats to wear), organizational plan and policies. Outline your inventory and accounting systems. Note your insurance plans. Specify how day-to-day operations would be conducted for each aspect of

yow strategy. Lay down clearly the do's and don'ts for each aspect. Review the risks you face and how you plan to cope with them.

FDI IN RETAILING

In the current investment regime, no foreign investment is allowed in domestic retail trading. This is based on the perception that opening up retail trading for FDI investment could impact local Venders and lead to job losses. However, manufacturing companies are allowed to carry out wholesale trading of high value items purely to institutional customers or wholesale distributors on a cash and carry basis.

Indian retail trade is of enormous size ($180 billion), nearly 10 per cent of GDP, employing 21 million persons, which is about 7 per cent of the labour force. It is six times bigger than Thailand and five times larger than South Korea and Taiwan. China's retail trade is 8 per cent of GDP and 6 per cent of employment. But the trade in India is fragmented, unorganized, un-networked, and individually small.

The 12 million kirana shops are mostly family or 'ma-pa' owned, with little capital for expansion or credit to receive or to extend to consumers. About 96 per cent of these shops have 500 sq ft or less of space with limited stock or choice to offer. During all

45

these years, instead of shedding tears for indigenous trade and resisting FDI, had the government declared it an industry, it would done the trade a world of goodModern retailing is designed not only to provide consumers with a wide variety of products under one roof, but also of assured home delivery and information feedback between consumers and producers. A modem retail outlet will also make it easy to buy on credit and provide for servicing and repair of products sold. With IT application, the modem retail store can cut transaction costs such as due to inventory, delivery and handling. That is precisely how the US based Wal-Mart grew to be a giant because it reduced its distribution costs to 3 per cent of sales compared to 4.5 per cent of others.

Wal-Mart had entered the Chinese market a few years ago (in 1996). Now it wants to enter India and bring FDI to set itself up to network. India is today the only major economy that still does not permit FDI in retail trade. In China, 35 of the world's top 70 retailers have already entered and set up business. They have helped in boosting their exports. Wal-Mart alone exported in 2002 about $12 billion worth of goods. These retailers source their goods from inside China.

India is targeting for its GDP to grow by 8 to 10 per cent per year. This requires raising the rate of investment as well as generating demand for the increased goods and services produced. Exports are one way of generating that demand. Encouraging private consumption expenditure is another way. Both these can be facilitated by allowing market-savvy, market-intelligent and best management practices, through corporations such as Wal-Mart, Carrefour, Ahold, JC Penny to enter India.These retail giant houses can bring their better managerial practices and IT-friendly techniques to cut wastage and set up integrated supply chains to gradually replace the presented disorganized and fragmented retail market. As India's urbanization grows, these modem food delivery systems are required. Foreign companies want to come in, and we need their money and techniques to prepare our transition to the inevitable globalised market of the future.

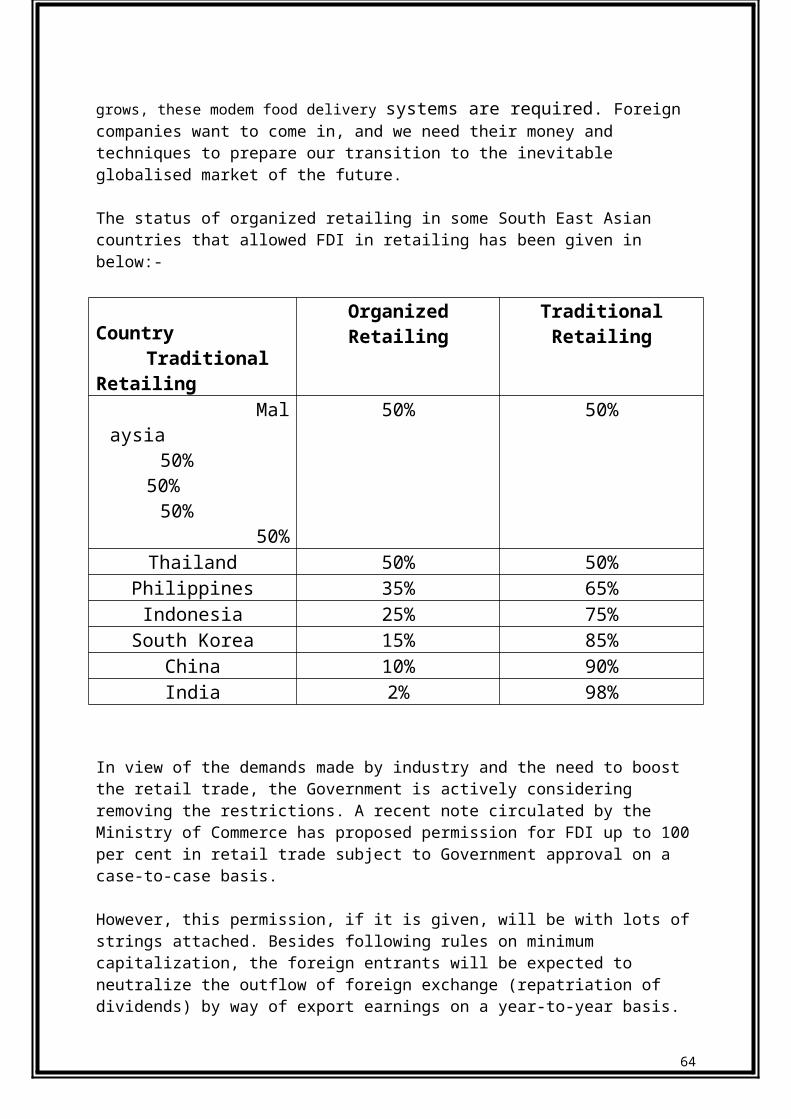

The status of organized retailing in some South East Asian countries that allowed FDI in retailing has been given in below:-

CountryTraditional

Retailing

Organized Retailing Traditional Retailing

Malaysia50%

50% 50%

50%

50% 50%

Thailand 50% 50%Philippines 35% 65%Indonesia 25% 75%

South Korea 15% 85%

46

China 10% 90%India 2% 98%

In view of the demands made by industry and the need to boost the retail trade, the Government is actively considering removing the restrictions. A recent note circulated by the Ministry of Commerce has proposed permission for FDI up to 100 per cent in retail trade subject to Government approval on a case-to-case basis.

However, this permission, if it is given, will be with lots of strings attached. Besides following rules on minimum capitalization, the foreign entrants will be expected to neutralize the outflow of foreign exchange (repatriation of dividends) by way of export earnings on a year-to-year basis.

FDI in retail sector has been a key driver of productivity growth in Brazil, Poland and Thailand. This has resulted in lower prices to the consumer, more consumption and higher profit for the producer. FDI in retail trade has forced the wholesalers and food processors to improve, raised exports, and triggered growth by outsourcing supplies domestically. The availability of standardized products has also boosted tourism in these countries.

The biggest opposition to allowing l00% FDI is the feared exit of the small retailers. Currently, moves are on to counter these apprehensions and the players are keenly awaiting the final decision from the Government.

47

Pantaloon Retail (India) Ltd. The Company's principal activity is to operate chain retails stores in names of Big Bazaar, Food Bazaar, Central and Pantaloons. The Big Bazaar is the discount store which offers a wide range of products under one roof. The products include apparels and non-apparels such as utensils, sports goods and footwear. The Company also has its presence into gold retailing by launching Gold Bazaar. The Company's Food Bazaar provides a range of food and grocery products ranging from fresh fruits and vegetables, staples, FMCG products and ready-to-cook products. The Central offers a chain of stores including books and music stores, global brands in fashion, sports and lifestyle accessories grocery store and restaurants. The Pantaloon retail stores focus largely apparels and accessories.

Pantaloon: Fashion by Pantaloon

Pantaloon is the company's departmental store and part of life style retail format. In fact, PRIL took its very initial steps in the retail journey by setting up the first Pantaloon store in Kolkata in 1997. ln a short time Pantaloon has been able to carve a special place for it self in the hearts and minds of the aspirational Indian customers. The company has depth of offering for both men and women at affordable prices. A striking characteristic of Pantaloon has been the strength of its private label programme. John Miller, Ajile. Scottsvile, Lombard Annabelle is some of the successful brands created by the company. With13 stores across the country and an ever-increasing stable of private brands, Pantaloon - in the coming years is poised to become a leading fashion trendsetter.

Food Bazaar- Wholesale prices

Food Bazaar's core concept is to create a blend of a typical Indian Bazaar and International supermarket atmosphere with the objective of giving the customer all the advantages of Quality, Range and Price associated with large format stores and also the comfort to See Touch and Feel the products. The company has recently launched an aggressive private label programme with its own brands of tea, salt, spices, pulses, jams, ketchups etc. With unbeatable prices and vast variety (there are 42 varieties of rice on sale), Food Bazaar has proved to be a hit with customers all over the country.

Big Bazaar: Is se sasta aur acha kahin nahin

Big bazaar is the company's foray into the world of hypermarket discount stores, the first of its kind in India. Price and the wide array of products are the USP's in Big

49

Bazaar. Close to two lakh products are available under one roof at prices lower by 2 to 60 per cent over the corresponding market prices. The high quality of service, good ambience, implicit guarantees and continuous discount programmes have helped in changing the face of the Indian retailing industry. A leading foreign broking house compared the rush at Big Bazaar to that of a local suburban train.

1, 70,000 products at 5- 5O % discount.

At Big Bazaar, you will get: A wide range of products at 6 - 60 % lower than the corresponding market price, coupled with an international shopping experience.

Apparel and Accessories for Men, Women and Children. Baby Accessories. Cosmetics Crockery Dress Materials Suiting & Shirting Electrical Accessories Electronics Footwear Home Textiles Home Needs Household Appliances Household Plastics Hardware Home Décor Luggage Linens Sarees Stationery Toys Utensils & Utilities

Big Bazaar is both big and a bazaar. It is unlike, say, a Wal-Mart or even a Food world. Big Bazaar is almost an aircon8itioned version of any Indian bazaar. It is a slightly orderly and organized version of, say Chickpet for Bangalore guys or Dadar for Mumbaiites. There is a huge crowd which can move in almost any direction. You can buy anything (pretty much everything is available at Big Bazaar). It is not a place where you can browse through at leisure and pick up a few things here and there. This is a place if you are serious about your shopping.

Life at Big Bazaar is pretty self-sufficient. If you were trapped in there for a week, you could live a good life. But to appreciate the nuances of home economics, one should try comparing prices. The clothes especially deserve an independent feature of their own.

Particularly designed for the regular middle-class family that requires clothing that lasts and doesn’t burn holes into the pockets of existing clothing, this store offers good bargains. What you won't get here is designs your friends will drool over.

50

Checks and stripes are like the far end of the creative exercise here, and the best bet for the fashion conscious would be the plain colors on display.

Choice is one factor that suffers here, as there is immense quantity but hardly any variety. If you want to clothe an entire troupe of extras in executive stuff for a dance number, this is the place! You get hordes of stuff, but it's all the same. If you are looking for anything in particular, then this is really not such a hot place.The accessories are good, though predictable. Brands make an appearance here as watches of Casio and Titan are displayed, and the prices range from 300 to some really heart-in-mouth figures

The rest of the stuff is not really very interesting as the prices are just a shade below the MRP. Groceries, home appliances, plastic goods, luggage, stationery, cosmetics... you name it, this place has it. Again, choice may suffer and you may not get that particular deo of yours which has the opposite sex going randy.

There are small sub-departments for footwear, music cassettes and even consumables. There is an in-house cafeteria that offers pretty good chow at reasonable rates. And now that the bazaar is spread over only two floors as opposed to the earlier four floors, I guess the intimidation factor stands reduced too.Big Bazaar has an exchange offer where you can get rid any old item and get yourself a new one. The offer is applicable to products like utensils, plastics, footwear, luggage accessories, garments, toys, Watches, glass, electronics items, and so on. Customers can get their old household items valued. Big Bazaar says it offers better value because old, broken utensils and plastics can be exchanged for as much as Rs. 40 a kilo.What is more, consumers need not exchange their old items for similar items. They can bring in an old piece of luggage and walk off with a salwar kameez instead. Similarly, old shoes and can exchanged for an electric rice cooker.

Food Bazaar had announced a special shopping offer which attracted around 20,000 shoppers. On a normal day, Center One's. Food Bazaar has 10 security guards. However, on July 26 the management had to call in around 30 guards on special duty.

In the last week of February 2006, Big Bazaar, through a television commercial, announced an exchange offer in which customer can bring junk and get discount on certain items.

January, the bazaar had offered massive discount on a particular day called Sabse Sasta Din. "About 2 million people showed up that day, which is almost four times than those visited the shop on Sunday before Diwali.

Meanwhile, sales at Big Bazaar have been growing steadily. In January 2005 the sales were of Rs 56.21 crore but in January 2006, it rose to Rs 129.61 crore.

51

SWOT Analysis Of Big Baazar

Strengths

Prime location, presence in malls etc. Large floor space allowing for better visual merchandising Large area also allows to stock a large variety of products under one roof Financial backing from Pantaloon Group. Experienced and competent management Good goodwill in the market. Bulk purchases leads to "economies of scale" Pan India Presence. Various schemes launched from time to time. Goods available at the cheapest rates.

Weaknesses

Large scale of operations sometimes acts as a barrier to personalized customer relations

Large scale operations lead to reduced flexibility by increasing the amount of overheads and a huge commitment in terms of fixed costs

Sometimes its discount & exchange schemes lead to hamper its brand image.

Employees are unable to cater to the large customers especially on exchange schemes days like on 26th of January etc.

Opportunity

In India Retailing is still a new concept. Hence there is still much of untapped market left out.