report to the finance and labour relations sub …...audit including comments on misstatements,...

TRANSCRIPT

CONFIDENTIAL

Report to the Finance and Labour Relations Sub-Committee – Communications of audit results

The Corporation of the City of Stratford For the year ended December 31, 2012

GrantThornton

Grant Thornton LLP Suite 406 140 Fullarton Street London, ON N6A 5P2

T (519) 672-2930 F (519) 672-6455 www.GrantThornton.ca

Grant Thornton LLP Suite 406 140 Fullarton Street London, ON N6A 5P2

T (519) 672-2930 F (519) 672-6455 www.GrantThornton.ca

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd

Members of the Finance and Labour Relations Sub-Committee of the Corporation of the City of Stratford 1 Wellington Street Stratford, ON N5A 6W1 August 27, 2013

To the members of the Finance and Labour Relations Sub-Committee of

the Corporation of the City of Stratford

We are pleased to report that we have now substantially completed our audit of the

consolidated financial statements of The Corporation of the City of Stratford, the Stratford City

Centre Committee, and the Perth & Stratford Housing Corporation (hereinafter the “City”) for

the years ended December 31, 2012. We enclose our Report to those charged with governance -

Communication of audit results to continue our dialogue with the Committee on the audit of The

Corporation of the City of Stratford. This report provides an overview of the results of our

audit including comments on misstatements, significant accounting policies, sensitive

accounting estimates, and other matters that may be of interest to the committee.

This communication has been prepared to comply with the requirements outlined in CAS 260

Communication with those Charged with Governance. The information in this document is intended

solely for the information and use of the Finance and Labour Relations Sub-Committee,

Council and management. It is not intended to be distributed or used by anyone other than

these specified parties.

We express our appreciation for the cooperation and assistance received from the management

and staff of the City during the course of our audit.

If you have any particular comments or concerns, please do not hesitate to raise them at our

scheduled meeting.

Yours sincerely, Grant Thornton LLP Melanie Dugard, CPA, CA Principal cc: Members of management

GrantThornton

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

Contents

Page

Status of the audit 1

Audit results 2

Reportable matters 3

Technical updates 6

Appendix A – Draft Independent auditor’s report 7

Appendix B – Draft Management representation letter 9

Appendix C – Internal control letter 13

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

1

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

Status of the audit

Outstanding items

We have substantially completed our audit of the consolidated financial statements of The Corporation

of the City of Stratford, and the financial statements of the Stratford City Centre Committee and the

Perth & Stratford Housing Corporation for the years ended December 31, 2012 and the results of these

audits are included in this report.

We have attached our draft independent auditor’s report for the City as Appendix A. We will finalize

the report once the Finance and Labour Relations Sub-Committee and Council have approved the

financial statements. The following items were outstanding as at the date of this report:

Receipt of signed management representation letter (draft has been attached as Appendix B);

Approval of the financial statements by the Finance and Labour Relations Sub-Committee and

Council;

Responses from legal inquiries.

Planned audit approach

We have successfully executed our audit strategy in accordance with the plan presented to the

committee on December 14, 2012.

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

2

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

Audit results

Summary of misstatements

Non-trivial misstatements noted during the course of our audit but not adjusted in the consolidated

financial statements were as follows:

Over/(Under) statement of:

Unadjusted misstatements Assets Liabilities Accumulated Surplus

Annual Surplus

Impact of prior year unadjusted items $ 175,681 $ (175,681)

Total unadjusted misstatements $ Nil $ Nil $ 175,681 $ (175,681)

We have discussed the unadjusted misstatements with management. The amounts have not been

adjusted as they are not material to financial statement presentation and are merely the reversing impact

of prior period unadjusted amounts.

Summary of disclosure matters

Our audit did not identify any unadjusted non-trivial misstatements from disclosure matters.

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

3

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

Reportable matters

Internal control

Management is responsible for the design and operation of an effective system of internal control that

provides reasonable assurance that the accounting system provides timely, accurate and reliable

financial information, and safeguards the assets of the City.

The audit is designed to express an opinion on the consolidated financial statements. Our

understanding of internal control is sufficient to enable us to plan the audit and to determine the

nature, timing and extent of tests to be performed. However, if we become aware of a deficiency in

your internal controls systems, auditing standards requires us to communicate to the Finance and

Labour Relations Sub-Committee those deficiencies we consider significant or material. However, a

financial statement audit is not designed to provide assurance on internal control.

During the course of performing our audit, we identified one weakness in internal control, as well as

one advisory item. Our comments and recommendations on these matters are presented in an internal

control letter attached as Appendix C.

Significant new accounting policies

There were no significant new accounting policies noted in the year.

Sensitive accounting estimates and disclosures

During the course of our audit, we noted the following sensitive accounting estimates and disclosures:

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

4

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

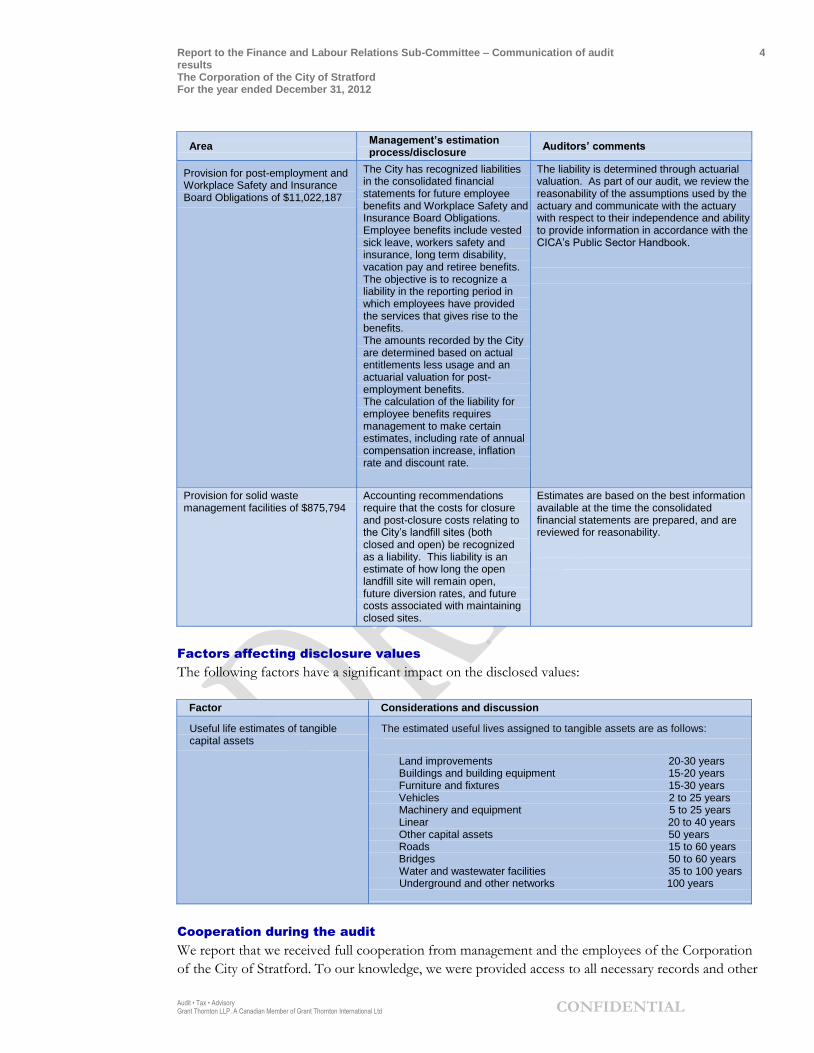

Area Management’s estimation process/disclosure

Auditors’ comments

Provision for post-employment and Workplace Safety and Insurance Board Obligations of $11,022,187

The City has recognized liabilities in the consolidated financial statements for future employee benefits and Workplace Safety and Insurance Board Obligations. Employee benefits include vested sick leave, workers safety and insurance, long term disability, vacation pay and retiree benefits. The objective is to recognize a liability in the reporting period in which employees have provided the services that gives rise to the benefits. The amounts recorded by the City are determined based on actual entitlements less usage and an actuarial valuation for post-employment benefits. The calculation of the liability for employee benefits requires management to make certain estimates, including rate of annual compensation increase, inflation rate and discount rate.

The liability is determined through actuarial valuation. As part of our audit, we review the reasonability of the assumptions used by the actuary and communicate with the actuary with respect to their independence and ability to provide information in accordance with the CICA’s Public Sector Handbook.

Provision for solid waste management facilities of $875,794

Accounting recommendations require that the costs for closure and post-closure costs relating to the City’s landfill sites (both closed and open) be recognized as a liability. This liability is an estimate of how long the open landfill site will remain open, future diversion rates, and future costs associated with maintaining closed sites.

Estimates are based on the best information available at the time the consolidated financial statements are prepared, and are reviewed for reasonability.

Factors affecting disclosure values

The following factors have a significant impact on the disclosed values:

Factor Considerations and discussion

Useful life estimates of tangible capital assets

The estimated useful lives assigned to tangible assets are as follows:

Land improvements 20-30 years Buildings and building equipment 15-20 years Furniture and fixtures 15-30 years Vehicles 2 to 25 years Machinery and equipment 5 to 25 years Linear 20 to 40 years Other capital assets 50 years Roads 15 to 60 years Bridges 50 to 60 years

Water and wastewater facilities 35 to 100 years Underground and other networks 100 years

Cooperation during the audit

We report that we received full cooperation from management and the employees of the Corporation

of the City of Stratford. To our knowledge, we were provided access to all necessary records and other

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

5

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

documentation and any issues that arose as a result of our audit were discussed with management and

have been resolved to our satisfaction.

Consultations with other accountants

To our knowledge, management did not seek the advice or opinion of other external accountants on

financial reporting or accounting matters.

Fraud and illegal acts

Our inquiries of management did not reveal any fraud or illegal acts.

Independence

As external auditors of the Corporation of the City of Stratford, we are required to be independent in

accordance with Canadian professional standards. These standards require that we disclose to the

Finance and Labour Relations Sub-Committee all relationships that, in our professional judgement, may

reasonably be thought to bear on our independence. We have provided a letter to the Finance and

Labour Relations Sub-Committee, dated December 14, 2012, which confirms our independence with

respect to the Corporation of the City of Stratford.

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

6

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

Technical updates

Accounting standards

Recent changes in accounting standards were communicated to the Finance and Labour Relations Sub-

Committee in our last letter dated December 14, 2012. There have been no changes of note since this

date.

Auditing standards

Recent changes in auditing standards were communicated to the Finance and Labour Relations Sub-

Committee in our last letter dated December 14, 2012. There have been no changes of note since this

date.

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

7

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

Appendix A – Draft Independent auditor’s report

To the Members of Council, Inhabitants and Taxpayers of the Corporation of the City of Stratford

We have audited the accompanying consolidated financial statements of the Corporation of the

City of Stratford, which comprise the consolidated statement of financial position as at December

31, 2012, and the consolidated statements of operations, changes in net debt and cash flows for the

year then ended, and a summary of significant accounting policies and other explanatory

information.

Management’s responsibility for the financial statements

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with Canadian public sector accounting standards, and for such internal control as

management determines is necessary to enable the preparation of financial statements that are free

from material misstatement, whether due to fraud or error.

Auditor’s responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We

conducted our audit in accordance with Canadian generally accepted auditing standards. Those

standards require that we comply with ethical requirements and plan and perform the audit to

obtain reasonable assurance about whether the financial statements are free from material

misstatement, whether due to fraud or error.

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the financial statements. The procedures selected depend on the auditor’s judgment,

including the assessment of the risks of material misstatement of the financial statements, whether

due to fraud or error. In making those risk assessments, the auditor considers internal control

relevant to the City’s preparation and fair presentation of the financial statements in order to design

audit procedures that are appropriate in the circumstances, but not for the purpose of expressing

an opinion on the effectiveness of the City’s internal control. An audit also includes evaluating the

appropriateness of accounting policies used and the reasonableness of accounting estimates made

by management, as well as evaluating the overall presentation of the financial statements.

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

8

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements present fairly, in all material respects, the

consolidated financial position of the Corporation of the City of Stratford as at December 31,

2012, and the results of its operations, changes in net assets and cash flows for the year then ended

in accordance with Canadian public sector accounting standards.

London, Canada Chartered Accountants

August 27, 2013 Licensed Public Accountants

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

9

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

Appendix B – Draft Management representation letter

August 27, 2013 Grant Thornton LLP Chartered Accountants Suite 406 140 Fullarton Street London, ON N6A 5P2 Dear Sir/Madam:

We are providing this letter in connection with your audit of the consolidated financial statements of

the Corporation of the City of Stratford (“the City”) as of December 31, 2012, and for the year then

ended, for the purpose of expressing an opinion as to whether the consolidated financial statements

present fairly, in all material respects, the financial position, results of operations, changes in net debt

and cash flows of the Corporation of the City of Stratford in accordance with Canadian public sector

accounting standards.

We acknowledge that we have fulfilled our responsibilities for the preparation of the consolidated

financial statements in accordance with Canadian public sector accounting standards and for the design

and implementation of internal controls to prevent and detect fraud and error. We have assessed the

risk that the consolidated financial statements may be materially misstated as a result of fraud, and have

determined such risk to be low. Further, we acknowledge that your examination was planned and

conducted in accordance with Canadian generally accepted auditing standards (GAAS) so as to enable

you to express an opinion on the consolidated financial statements. We understand that while your

work includes an examination of the accounting system, internal controls and related data to the extent

you considered necessary in the circumstances, it is not designed to identify, nor can it necessarily be

expected to disclose, fraud, shortages, errors and other irregularities, should any exist.

Certain representations in this letter are described as being limited to matters that are material. An item

is considered material, regardless of its monetary value, if it is probable that its omission from or

misstatement in the consolidated financial statements would influence the decision of a reasonable

person relying on the consolidated financial statements.

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

10

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

We confirm, to the best of our knowledge and belief, as of August 27, 2013, the following

representations made to you during your audit.

Financial statements

1 The consolidated financial statements referred to above present fairly, in all material respects, the

financial position of the City as at December 31, 2012 and the results of its operations, changes in

net debt and its cash flows for the year then ended in accordance with Canadian public sector

accounting standards, as agreed to in the terms of the audit engagement.

Completeness of information

2 We have made available to you all financial records and related data and all minutes of the meetings of Council and committees of Council, as agreed in the terms of the audit engagement. Summaries of actions of recent meetings for which minutes have not yet been prepared have been provided to you. All significant Council and committee actions are included in the summaries.

3 We have provided you with unrestricted access to persons within the City from whom you determined it necessary to obtain audit evidence.

4 There are no material transactions that have not been properly recorded in the accounting records underlying the consolidated financial statements. The adjusting journal entries which have been proposed by you are approved by us and will be recorded on the books of the City.

5 There were no restatements made to correct a material misstatement in the prior period consolidated financial statements that affect the comparative information.

6 We are unaware of any known or probable instances of non-compliance with the requirements of regulatory or governmental authorities, including their financial reporting requirements.

7 We are unaware of any violations or possible violations of laws or regulations the effects of which should be considered for disclosure in the consolidated financial statements or as the basis of recording a contingent loss.

8 We have disclosed to you all known deficiencies in the design or operation of internal control over financial reporting of which we are aware.

9 We have identified to you all known related parties and related party transactions, including revenues, purchases, loans, transfers of assets, liabilities and services, leasing arrangements guarantees, non-monetary transactions and transactions for no consideration.

Fraud and error

10 We have no knowledge of fraud or suspected fraud affecting the City involving management; employees who have significant roles in internal control; or others, where the fraud could have a non-trivial effect on the consolidated financial statements.

11 We have no knowledge of any allegations of fraud or suspected fraud affecting the City’s consolidated financial statements communicated by employees, former employees, analysts, regulators or others.

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

11

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

12 We acknowledge our responsibility for the design, implementation and maintenance of internal control to prevent and detect fraud.

13 We believe that the effects of the uncorrected financial statement misstatements summarized in the accompanying schedule are immaterial, both individually and in the aggregate, to the consolidated financial statements taken as a whole.

Recognition, measurement and disclosure

14 We believe that the significant assumptions used by us in making accounting estimates, including those used in arriving at the fair values of financial instruments as measured and disclosed in the consolidated financial statements, are reasonable and appropriate in the circumstances.

15 We have no plans or intentions that may materially affect the carrying value or classification of assets and liabilities, both financial and non-financial, reflected in the consolidated financial statements.

16 All related party transactions have been appropriately measured and disclosed in the consolidated financial statements.

17 The nature of all material measurement uncertainties has been appropriately disclosed in the consolidated financial statements, including all estimates where it is reasonably possible that the estimate will change in the near term and the effect of the change could be material to the consolidated financial statements.

18 All outstanding and possible claims, whether or not they have been discussed with legal counsel, have been disclosed to you and are appropriately reflected in the consolidated financial statements.

19 All liabilities and contingencies, including those associated with guarantees, whether written or oral, have been disclosed to you and are appropriately reflected in the consolidated financial statements.

20 With respect to environmental matters:

a) at year end, there were no liabilities or contingencies that have not already been disclosed to you;

b) liabilities or contingencies have been recognized, measured and disclosed, as appropriate, in the consolidated financial statements; and

c) commitments have been measured and disclosed, as appropriate, in the consolidated financial statements.

21 The City has satisfactory title to (or lease interest in) all assets, and there are no liens or encumbrances on the City’s assets nor has any been pledged as collateral.

22 We have disclosed to you, and the City has complied with, all aspects of contractual agreements that could have a material effect on the consolidated financial statements in the event of non-compliance, including all covenants, conditions or other requirements of all outstanding debt.

23 The Harmonized Sales Tax (HST) transactions recorded by the City are in accordance with the federal and provincial regulations. The HST liability/receivable amounts recorded by the City are considered complete.

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

12

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

24 Employee future benefit costs, assets, and obligations have been determined, accounted for and disclosed in accordance with the requirements of Section PS3255 Post-employment Benefits, Compensated Absences and Termination Benefits of the Canadian Public Sector Handbook.

25 There have been no events subsequent to the date of the statement of financial position up to the date hereof that would require recognition or disclosure in the consolidated financial statements. Further, there have been no events subsequent to the date of the comparative consolidated financial statements that would require adjustment of those consolidated financial statements and related notes.

Other

26 We have considered whether or not events have occurred or conditions exist which may cast significant doubt on the City’s ability to continue as a going concern and have concluded that no such events or conditions are evident.

Yours very truly, Manager of Financial Services Treasurer

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

13

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

Appendix C – Internal control letter

Members of the Finance and Labour Relations Sub-Committee of the Corporation of the City of Stratford 1 Wellington Street Stratford, ON N5A 6W1

August 27, 2013

Dear Sir/Madam:

RE: Internal Control Findings from the 2012 Audit

We have audited the financial statements of The Corporation of the City of Stratford as at December

31, 2012 for the year then ended, and reported thereon to the members under the date of August 27,

2013.

Our approach to internal control involves gaining an understanding of the City’s controls pertinent to

reliable financial reporting and evaluating our findings against the internal control framework. More

specifically, our process involves:

understanding the processes that impact financial reporting

documenting an understanding of the controls within the user fee and other revenues and

operating expense cycles that prevent or detect errors, including fraud

assessing the effectiveness of the design of those controls and identifying potential controls “gaps”,

operating deficiencies, and other weaknesses or advisory comments

The standards of the public accounting profession require us to report annually to you our findings on

weaknesses and deficiencies in your internal controls. These accounting standards require that the

internal controls letter/management letter contain all material weaknesses and significant deficiencies

regardless of their practicality or management’s current ability to correct the weaknesses or deficiencies.

We categorize such findings as follows:

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

14

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

Material weaknesses (individual or aggregated deficiencies that could result in a material

misstatement in the financial statements due to fraud or error).

Significant deficiencies

Other deficiencies and advisory comments

Significant Deficiencies:

Matter carrying forward from prior years:

Journal Entry Controls

During the course of our audit in prior years, we noted that all employees in the finance group continue

to have the ability to record general ledger journal entries up to $10,000. Entries above $10,000 still

require approval by the Manager of Financial Services. The creation of journal entries is not normally

limited, but the approval and actual recording of entries would ideally be limited to appropriate

personnel, as a review process to ensure accuracy and appropriateness. By not limiting this function, or

requiring review and approval, there is an increased risk of errors that may not be detected on a timely

basis.

Recommendation:

Management should restrict the ability to create general ledger entries, as well as consider limiting the

number of finance staff able to approve these entries. Management should also consider creating a

process to document the approval of journal entries, especially those over a certain dollar threshold.

Management Comments:

Management analyzed manual journal entries made by staff to the general ledger from 2012. The number of journal

entries made was 3,037. Accounting for almost half of these entries are preauthorized utility payments. We implemented

this process to reduce cheque payments and postage and eliminate late fees. Each of these entries is backed up with an

invoice and posted to the expense and a clearing account by one staff member and then posted from the clearing account and

the bank by another staff member. The bank account is then reconciled by a third staff member allowing opportunity to

find any errors. Of the remaining entries approximately 700 are over $10,000 and therefore authorized by the Senior

Accounting Clerk or the Manager of Financial Services. This leaves less than 1,000 entries under $10,000 which finance

staff can process. All of these entries have backup documentation attached. Given the small size of the finance department

Management feels that sufficient journal entry internal controls are in place.

Advisory Comments:

Festival Hydro Revenues

During the course of our audit, we noted that there were no monitoring controls in place with respect

to revenues received from Festival Hydro Inc. and Festival Hydro Services Inc. Cheques are received

by Festival Hydro, accompanied by a billing report on either a monthly or quarterly basis and amounts

are recorded in the general ledger by the Finance department. There is minimal review of the

information provided from Festival Hydro for reasonableness by either the Finance or the Operations

departments. Without a review taking place, the City is unable to gain comfort over the amounts being

remitted with respect to user fees and service charges.

Report to the Finance and Labour Relations Sub-Committee – Communication of audit results The Corporation of the City of Stratford For the year ended December 31, 2012

15

Audit • Tax • Advisory Grant Thornton LLP. A Canadian Member of Grant Thornton International Ltd CONFIDENTIAL

Recommendation:

Management should put a policy and controls in place whereby billings received from Festival Hydro

Inc. and Festival Hydro Services Inc. are reviewed for reasonableness both at the operational and

financial level. Billing amounts and rates should be assessed against expectations to verify the overall

reasonableness.

It is management’s responsibility to weigh the costs of implementing controls against the benefits that

the controls will achieve. The purpose of this letter is to provide you with the information related to

the identified risks so that you can make the necessary decisions.

The matters discussed herein are those that have been noted as of August 27, 2013, and we have not

updated our procedures regarding these matters to the current date. In addition, this communication is

prepared solely for the information of management and is not intended for any other purposes; we

accept no responsibility to a third party who uses this communication.

Thank you for the opportunity to contribute to the present and future success of the City of Stratford.

Yours sincerely, Grant Thornton LLP Melanie Dugard, CPA, CA Principal