reporting requirements and dca resources doaa 2019 ... · amount of hmt receipts during fiscal year...

TRANSCRIPT

Reporting Requirements and DCA Resources

DOAA 2019 Governmental Accounting and

Reporting Issues Seminar

Georgia Center for Continuing Education

Athens, GA

Tyler Reinagel, Ph.D.

Director, DCA Office of Planning and ResearchSeptember 23, 2019

Agenda

Financial Reporting Requirements

Report of Local Government Finance (RLGF)

Debt Issuance

Hotel-Motel Excise Tax

Local Government Authorities (AARF)

Tax Exempt Bond Allocation Program

Grant Programs and Applications

Uniform Chart of Accounts (UCOA) Update

DCA Office of Research

Local Governments

(689)

• Cities

• Consolidated Governments

• Counties

Local Government Authorities

(1,246)

• Examples include:

• Development

• Hospital

• Housing

• Recreation

• Solid Waste

• Water/Sewer

• Others

Office of Research

Role of the DCA Office of Research

Office of Research Responsibilities

Maintain Local Government and Authority Contact Information

Build user-friendly government reporting systems for seven

reports/surveys used by 1,935 jurisdictions/authorities

Management-oriented and financial-oriented

Track compliance, but not enforcement

Explanation of legal requirements, but not interpretation

Remind local governments and authorities of report due dates and

requirements

Serve as state repository for data and reports

Dissemination of reported data

Reporting Requirements: Local

Governments (Cities, Counties, Cons.)

Georgia’s Local Governments

Number of Chartered Counties 151

Number of Chartered Cities 530

Number of Consolidated Governments 8

Total Local Governments in Georgia 689As of September 2019

Local Government Annual Financial

Reporting Responsibilities

Local Governments

Report of Local

Government Finances (RLGF)

Hotel/Motel Tax Report

Debt Issuance Report

Report of Local Government Finances

(RLGF)

Annual report of all revenues, expenditures, assets, and

debts of all funds and agencies of the local government

Mandated in 1985 for all local governments

OCGA 36-81-8(b)(1)(a)

To be submitted within six months of local government’s FYE

Revised for FY2016 to better meet stakeholder needs and

more closely conform with the Uniform Chart of Accounts

All local governments (689) are required to have

submissions for the most recent three (3) fiscal years

Without the three most recent RLGF submissions, a local government is ineligible for state or federal grant/loan funding administered by DCA

Local Government Fiscal Years

FYE Total LGs

(689)

RLGF Due Date

January 2 July 31

February 2 August 31

March 2 September 30

April 5 October 31

May 3 November 30

June 270 December 31

July 6 January 31 (following calendar year)

August 10 February 28/29 (following calendar year)

September 58 March 31(following calendar year)

October 3 April 30 (following calendar year)

November 2 May 31 (following calendar year)

December 326 June 30 (following calendar year)

RLGF Audited Financial Statements

Audited figures not required for RLGF submission

Starting in 2016, the RLGF captures audited/unaudited status

Many jurisdictions prefer to have an audit, but it does not change deadline

Georgia DOAA exempts certain local governments from audit requirements, so not all 689

jurisdictions will have audited figures

If a local government has less than $300K of expenditures, it is not required to submit an audit

In their most recent filings, 128 local governments (18.6%, all cities) are under $300K

If an audit is completed after the six month window, local governments may submit

corrections to the RLGF if appropriate

Tax and Expenditure Data Center (TED)

Local Government Annual Financial

Reporting Responsibilities

Local Governments

Report of Local

Government Finances (RLGF)

Hotel/Motel Tax Report

Debt Issuance Report

Debt Issuance Report

Each local government that issues debt in excess of

$1,000,000 is required to report that issuance to the Office

of Research;

“A political subdivision which issues general obligation bonds, revenue bonds, or any other bonds, notes, certificates of participation, or other such obligations of that political subdivision in an amount exceeding $1 million, shall file a report with the Department of Community Affairs…” OCGA 36-82-10(b)

The same section applies to local authorities

The due date for debt issuance reports is within 60 days of

debt issuance

Debt Issuance Annual Report

Local Government Annual Financial

Reporting Responsibilities

Local Governments

Report of Local

Government Finances (RLGF)

Hotel/Motel Tax Report

Debt Issuance Report

The Lodging Receipt

Base Hotel/Motel

Rate

Sales-Use Tax

6.0%-8.9%

State Hotel-Motel Fee

$5 Per Room/Per

Night

Local Hotel-Motel Excise

Tax2.0%-8.0%

LOST

SPLOST

E-LOST

MARTA

TSPLOST

MOST

4% State

HOST

Hotel-Motel Tax Authorization Paragraphs

O.C.G.A. § 48-13-51(a)1

O.C.G.A. § 48-13-51(a)3

O.C.G.A. § 48-13-51(b)*Requires act of General Assembly

Changes to HMT Authorizations

In 2008, HB 1168 reduced the number of authorizations for newly adopted HMT or changes in existing HMT to three (3) options

1-3%

5%

6-8%

“Grandfathered” Authorization Paragraph

Jurisdictions

As of May 2019

Mechanics of Restricted Spending

Defining the Spending Restrictions - Purpose

Depending on the authorization paragraph used to

impose the HMT, a percentage of revenue goes toward

restricted spending

Always a percentage, never a flat/fixed amount

Tourism, Conventions, and Trade Shows (TCT)

“Planning, conducting, or participating in programs of information and publicity designed to attract or advertise tourism, conventions, or trade shows.”

Expended by the Destination Marketing Organization (DMO)

O.C.G.A. § 48-13-50.2

Defining the Spending Restrictions - Recipient

For TCT spending, the Destination Marketing Organization (DMO)

“A private sector non-profit organization or other private entity which is exempt…under Section 501(c)(6) of the IRS Code of 1986” Primary responsibilities are to “encourage travelers to visit their destinations,

encourage meetings and expositions in the area, and provide visitor assistance and support as needed.”

Can be a Chamber of Commerce, CVB, Regional Travel Association, or other private group, so long as it is a tax-exempt 501(c)(6)

Also, any recreation Authority or CVB created by General Assembly or the State, a Department of State Government, or State Authority

For TPD spending, any municipal, county, or consolidated government

O.C.G.A. § 48-13-50.2

How about DDAs, Main Street?

DDAs, Tourism Authorities,

and other Local Authorities

Main Street 1

Organization Local Authority created by

General Statute, Local Law, or

Local Constitutional

Amendment

Department within local government, or

Stand-alone non-profit organization, or

Component of Chamber of Commerce

Flexibility from DCA ODD

Structure and

Restrictions

As defined by OCGA 36-42 If City department, defined by Mayor/Council;

If non-profit/Chamber component, as defined by

bylaws

Relationship

with City

“Creature” of city government If department, part of city government; if non-

profit/Chamber, contractual relationship with city

Hotel-Motel

Tax Revenue

No. Local Authorities in

Georgia are inherently public

entities and not eligible.

It depends.

If the Main Street program is a city department,

it is a public entity and not eligible. If the Main

Street program is a stand-alone 501(c)6 non-

profit, it is eligible.

Non-Profit Status – (c)3 versus (c)6

501(c)3 501(c)6

Hotel-Motel Tax Revenue Not eligible to receive Eligible to receive

Purpose Charitable Organization Business/Membership

Organization

Donation Tax deductible for donor Not tax deductible

Lobbying Prohibited from political

activity

Political activity permitted,

but taxable

Social Activities Social activities must be

“insubstantial”

Social activities permissible,

not “primary”

Examples Charitable foundations,

universities, churches,

charitable support groups

Business league, Chamber

of Commerce, CVB

Main Street programs in Georgia are largely self-determined. For

those that are stand-alone non-profits, some have status as 501(c)3

and some as 501(c)6. Always confirm the tax-exempt status of a

DMO receiving/potentially receiving Hotel-Motel Tax revenue

restricted to TCT

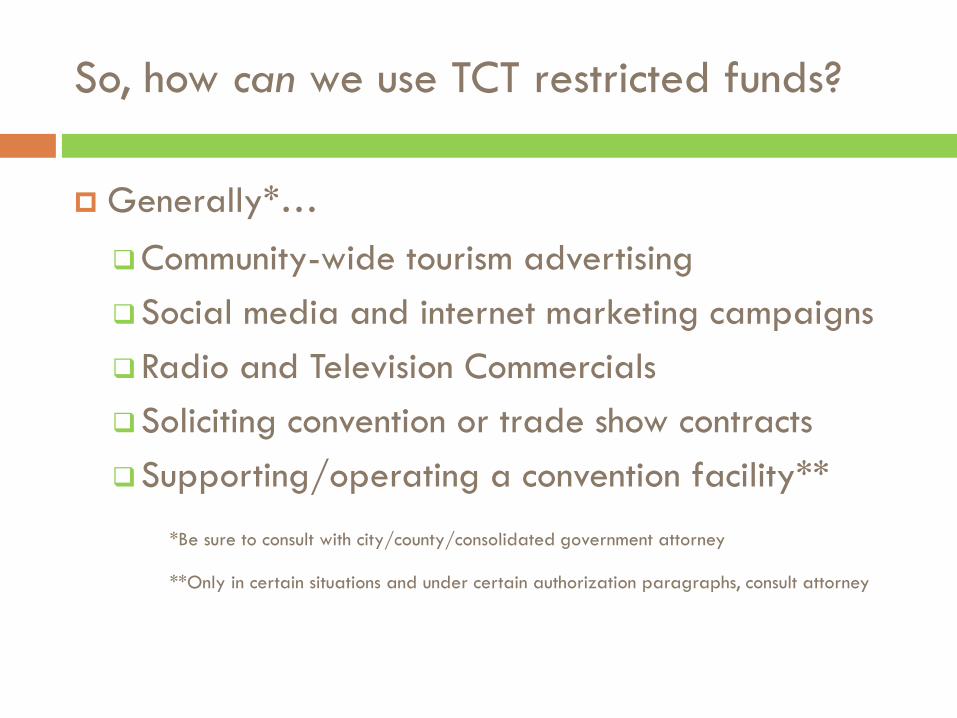

So, how can we use TCT restricted funds?

Generally*…

Community-wide tourism advertising

Social media and internet marketing campaigns

Radio and Television Commercials

Soliciting convention or trade show contracts

Supporting/operating a convention facility**

*Be sure to consult with city/county/consolidated government attorney

**Only in certain situations and under certain authorization paragraphs, consult attorney

So, how can’t we use TCT restricted funds?

Fireworks

Not “programs of information and

publicity” or an advertisement for an

event

They are the event

Defining the Spending Restrictions - Purpose

Depending on the authorization paragraph used to impose the HMT, a

percentage of revenue goes toward restricted spending

Always a percentage, never a flat/fixed amount

Tourism Product Development (TPD)

“Creation or expansion of physical attractions which are available and open to the public and which improve destination appeal to visitors, support visitors' experience, and are used by visitors. Such expenditures may include capital costs and operating expenses.” Project should be identified as TPD in jurisdiction’s annual budget

Must involve physical renovation of existing tourism facility, or construction of a new tourism facility

Expended directly by LG or entity other than DMO

O.C.G.A. § 48-13-50.2

What qualifies as TPD?

As identified in O.C.G.A. § 48-13-50.2(6)(A-P),

Tourism Product Development may include

Information Centers

Hunting Preserves

Wayfinding Signs

Golf Courses

Sightseeing Planes and Helicopters

Performing Arts Facilities

Meeting/Convention Facility

Amusement Parks

Auto Racetracks

RV/Trailer/Camper Sites

Exhibit HallSports Stadium

Arenas

Fishing Preserves

Parks and Trails

Drag Strips

Permanent Carnivals Sightseeing Boats

Campsites

Zoos

Aquariums

Museums

What qualifies as TPD?

And other “creation or expansion of physical attractions which are available

and open to the public and which improve destination appeal to visitors,

support visitors’ experience, and are used by visitors.”

Understanding Restricted Spending

O.C.G.A. § 48-13-51(a)(1) – 1-3%

Non-Restricted

Proceeds can be used for any legal general fund purpose in

the city, county, or consolidated government

100% of HMT

Revenue

Restricted

None

*Potential requirements for TCT based on local-specification and

previous TCT spending

O.C.G.A. § 48-13-51(a)(3) – 5%

Non-Restricted

Proceeds can be used for any legal general fund purpose in

the city, county, or consolidated government

60% of HMT

Revenue

Restricted

At least 40% of HMT revenue must be used for

TCT.

40% TCT

O.C.G.A. § 48-13-51(b) – 6%

Non-Restricted

Proceeds can be used for any legal general fund purpose in

the city, county, or consolidated government

50% Non-

Restricted

Restricted

At least 41⅔% of HMT revenue must be used for

TCT

41⅔% TCT Restricted

Up to 8⅓% of HMT may be used for TPD, otherwise

used for TCT

8⅓% TPD

O.C.G.A. § 48-13-51(b) – 7%

Non-Restricted

Proceeds can be used for any legal general fund purpose in

the city, county, or consolidated government

42.86% Non-

Restricted

Restricted

At least 42.86% of HMT revenue must be used for

TCT

42.86% TCT Restricted

Up to 14.28% of HMT may be used for TPD, otherwise used for TCT

14.28% TPD

O.C.G.A. § 48-13-51(b) – 8%

Non-Restricted

Proceeds can be used for any legal general fund purpose in

the city, county, or consolidated government

37.5% Non-

Restricted

Restricted

At least 43.75% of HMT revenue must be used for

TCT

43.75% TCT Restricted

Up to 18.75% of HMT may be used for TPD, otherwise used for TCT

18.75% TPD

After the Fiscal Year…

Local Government Requirements

State-mandated Audit to DOAA

Determination of compliance with authorization paragraph’s expenditure requirements

Identification of any non-compliance

Amount of HMT receipts during fiscal year

Expenditures, as a percentage of tax receipts O.C.G.A. § 48-13-51(a)(9)(B)

State-required Reporting to DCA

Verify authorization paragraph and rate Unique form for each authorization paragraph

Report HMT revenues received

Project Contractor Information Schedule (PCIS) O.C.G.A. § 48-13-56

Tourism Product Development (TPD) List If under Paragraph 51(b)

O.C.G.A. § 48-13-50.2

Reporting to DCA Office of Research

Within six (6) months of the end of the fiscal year, each jurisdiction

imposing a HMT is responsible for completing an online Hotel Motel

Tax Report with DCA

Reporting to DCA Office of Research

Within six (6) months of the end of the fiscal year, each jurisdiction

imposing a HMT is responsible for completing an online Hotel Motel

Tax Report with DCA

Project-Contractor Information Schedule

Maintain open communication with your Chamber, CVB, or other 501(c)(6) (DMO)

receiving restricted HMT funds

Remember restricted spending is percentage based, regardless of authorization paragraph – not a fixed dollar amount

Have an established mutual agreement on how restricted HMT funds will be expended – additional funds can go to the DMO, but PCIS form to DCA focuses only on restricted funds

Have contracting entity (DMO) complete PCIS and submit to local government for

review and upload to HMT Report

Local Government Reporting Guidance

Reporting Requirements: Local

Government Authorities

Georgia’s Local Authorities

Authority Type # of

AuthoritiesAuthority Type # of

Authorities

Airport 45 Public Transit 4

Building 38 Recreation 22

Development 205 Regional Jail 3

Downtown Development 225 Residential Care of the Elderly 9

Hospital 107 Resource Recovery 4

Housing 179 Solid Waste Management 26

Industrial Development 81 Stadium and Coliseum 6

Joint Development 74 Tourism 22

Land Bank 12 Urban Redevelopment 41

Parking 3 Water and Sewer 63

Public Facilities 44 E-911 6

Public Service 7 Other 20

As of August 2019 Total Local Authorities 1,246

HB257 – Combined Reporting

Local Authorities

Authority Registration

Debt Issuance Report

Report of Authority Finances

(RAF)

HB257 combines Registration and Financial Reporting into a single report

Due within six months of Authority FYE

“Annual Authority Registration and Finance Report,” or AARF

Beginning with FY18

Report of Authority Finances (RAF)

Since 1985, each authority is required to submit an annual financial report;

“(2) Each local independent authority shall submit an annual report of indebtedness to the Department of Community Affairs. Such report shall include the revenues, expenditures, assets, and debts of all funds of the local independent authority and shall describe any actions taken by such local independent authority to incur indebtedness.” (OCGA 36-81-8(b)(2))

Annual report of all revenues, expenditures, assets, and debts of the local authority

OCGA does not dictate a timeline, but rather says they “shall be submitted within

the requested time periods established by the department” (OCGA 36-81-8(b)(3))

The current requirement is 6 months from the end of the authority’s fiscal year

Like RLGF, audited figures are preferred but not required

Submitted online with authority User ID and Password from Office of Research

All authorities are required to have submissions for the most recent 3 fiscal years

Local Authority Annual Reporting

Responsibilities

Local Authorities

Authority Registration

Debt Issuance Report

Report of Authority Finances

(RAF)

Debt Issuance Report

Each authority that issues debt in excess of $1,000,000 is required

to report that issuance to the Office of Research;

“A political subdivision which issues general obligation bonds, revenue bonds, or any other bonds, notes, certificates of participation, or other such obligations of that political subdivision in an amount exceeding $1 million, shall file a report with the Department of Community Affairs…” OCGA 36-82-10(b)

The same section applies to cities, counties, and consolidated governments issuing debt.

The longstanding due date for debt issuance reports has been within

60 days of debt issuance

Same 2-page .XLS form as local governments, combined annual

reporting on DCA website

Tax Exempt Bond Allocations

Bond Allocation Program Background

Local & state governments/authorities may apply to issue "private

activity tax exempt bonds“

Tax Exempt Bond Allocations are not cash changing hands or the state issuing debt

Allows for lower than normal financing costs, resulting in the creation

or retention of jobs and expansion of affordable housing.

Fund-able projects include traditional industrial development bond

(IDB) for manufacturing concerns and mortgage revenue bonds

(MRB) for single family mortgages to bonds for multi-family housing

development and exempt facility bonds.

To receive an allocation, the local issuing authorities must approve

the project, hold a public hearing, have local government approval,

and general financing in place.

2019 Tax Exempt Bond Allocation Formula

State Population 10,519,475 ($105 Per) $1,104,544,875

Economic Development

Period #1 1/1/19-3/31/19 $187,772,629

Period #2 4/1/19-6/30/19 $187,772,629

Period #3 7/1/19-9/30/19 $93,886,314 $469,431,572

Housing

GHFA Reservation 1/1/19-9/30/19 $291,047,575

URFA Reservation 1/1/19-9/30/19 $89,191,999

Local Reservation 1/1/19-9/30/19 $89,191,999 $469,431,573

Flexible Share 1/1/19-12/31/19 $165,681,731 $165,681,731

Total State Cap $1,104,544,875

Bond Allocation Applications

Inducement Resolution

Publisher’s Affidavit (TEFRA)

Public notice published at least 14 days prior to public hearing

Public Official’s Approval of TEFRA

State Law/Legal Counsel Opinion

Financial Commitment Letter

Application Fee

Inducement Resolution

TEFRA Documentation

Bond Allocation Fee Schedule

Bond Application Fee: $250.00

Bond Carryforward Fee: $250.00

Bond Adjustment (change in amount of allocation or

one -time 30 day extension) Fee: $100.00

Bond Issuance Fee: 1/10 of 1% (0.001)

$20,000 on a $20M allocation

Economic Development Share

Must create/retain one permanent job for each $125K

in allocation sought

“Flex Share” funds can be used at the discretion of

the Commissioner with/without jobs requirement

Applicant must provide a “but for” statement as a

part of the “Jobs Test” portion of application

After nine months (September 30), all unused Economic

Development share and Housing share are transferred

to “Flex Share” for the duration of the calendar year

Grant Programs and Applications

DCA Community and Economic

Development Programs

Funding Programs Appalachian Regional

Commission Economic Development Grant Program

Community Development Block Grant (CDBG)

Downtown Development Revolving Loan Fund (DDRLF)

Neighborhood Stabilization Program

OneGeorgia Programs (EDGE and Equity)

Regional Economic Business Assistance (REBA) Program

State Small Business Credit Initiative (SSBCI)

Incentive Programs Enterprise Zones

Georgia Agribusiness and Rural Jobs Act (GARJA)

Georgia Tourism Development Act

Job Tax Credits

Military Zones

Opportunity Zones (State)

Opportunity Zones (Federal)

Regional Economic Assistant Program (REAP)

Rural Zones

Compliance and Funding/Program Eligibility

For many funding/incentive programs, permitting, and community

designations, certain compliance requirements exist…

QLG Status – Comprehensive Plan/Plan Update, E-Verify

Service Delivery Strategy (County and Resident Cities)

Local Governments (all municipalities, counties, and consolidated governments) must have the three most recent years of GOMI and RLGF submissions on file with DCA to be eligible for any state/federal funding (i.e. CDBG) or permits administered by DCA

Compliance listing is available at

https://apps.dca.ga.gov/LocalGovStatus/planning.asp

Questions regarding QLG Status and SDS should be emailed to [email protected]

Questions regarding reporting requirements should be emailed to [email protected]

2019 UCOA Update

Background on UCOA

• The UCOA was established by the General Assembly

(HB491) during the 1997-1998 legislative session

• The Georgia Department of Community Affairs (DCA) was

to develop and maintain a uniform chart of financial

accounts to be used by all local governments in Georgia

• The UCOA was developed with input from local government

finance stakeholders, and implemented by cities, counties,

and consolidated governments beginning in 2001

UCOA>>RLGF

Beginning in

FY2016, the

Report of Local

Government

Finances (RLGF) -

required by all

cities, counties,

and consolidated

governments

within six months

of the conclusion

of their fiscal

year – was

reflective of the

UCOA

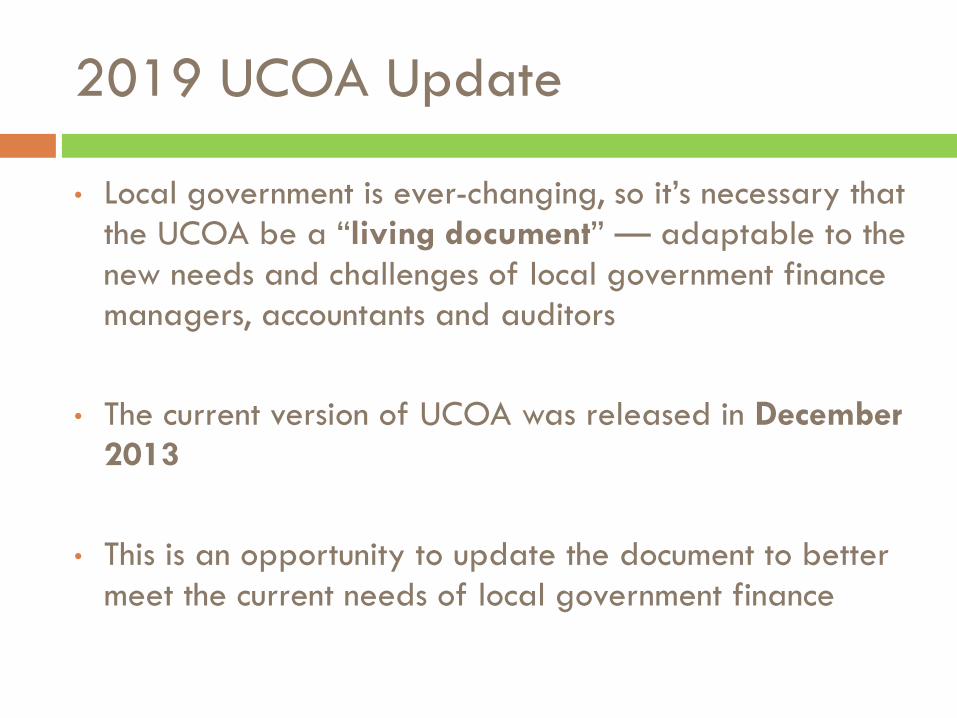

2019 UCOA Update

• Local government is ever-changing, so it’s necessary that

the UCOA be a “living document” — adaptable to the

new needs and challenges of local government finance

managers, accountants and auditors

• The current version of UCOA was released in December

2013

• This is an opportunity to update the document to better

meet the current needs of local government finance

2019 UCOA Update

Workshop at DCA Office in Atlanta on

Thursday, November 7

Representatives from:

Georgia Department of Community Affairs

Georgia Department of Audits and Accounts (DOAA)

Carl Vinson Institute of Government/University of Georgia

Georgia Municipal Association (GMA)

Association County Commissioners of Georgia (ACCG)

Revisions will be presented to the DCA Board

and State Auditor for approval

4th Edition should be released in 2Q 2020

Providing Feedback for UCOA

Update

UCOA Update – Providing Feedback

Option 1: Feedback Form

- A hard-copy feedback

form is available

- Can be returned to

DCA in person, by

email, or via USPS

- Should be received by

October 15, 2019 for

full consideration

UCOA Update – Providing Feedback

Option 2: Web-Based Form

UCOA Update – Providing Feedback

Option : Email

Email feedback, questions, or concerns to

Email by October 15, 2019 for full consideration

Additional Questions and Assistance

For report system log-in, PCIS form, ordinance requirements, sample

ordinances, and other information on the hotel-motel tax in Georgia,

visit:

https://www.dca.ga.gov/local-government-assistance/research-surveys/hotel-

motel-excise-tax

DCA cannot provide legal interpretations or opinions, but if you have a

question specific to your jurisdiction, or something unaddressed on the

DCA website, please contact:

Tyler Reinagel, Ph.D.

Director,

Office of Planning and Research

404.679.4996