reports on the audit of federal financial assistance

TRANSCRIPT

Harvard University

Reports on the Audit of Federal Financial Assistance Programs In Accordance with OMB Circular A-133 For the

Year Ended June 30, 2001

Entire A-133 Part I- Financial Statements Part II- Schedule of Federal Expenditures of Federal Awards Part III-Reports on Internal Control and Compliance Part IV-Findings OMB Circular A-133 involves the audits of States, Local Governments, and Non-Profit Organizations who receive federal funding exceeding $300,000. Harvard University’s A-133 report includes Harvard Medical School and Harvard School of Public Health. Please refer to Section IV for findings and corrective action plans. Each of these sections can be downloaded and printed. You will need Adobe Acrobat Readers 3.X. in order to view theses documents. The reader is available for download at the Acrobat web site.

Employee Identification Number: 042103580

Harvard University Report on Federal Awards in Accordance with OMB Circular A-133 For the Year Ended June 30, 2001

Harvard University Report on Federal Awards in Accordance with OMB Circular A-133 for the Year Ended June 30, 2001 Table of Contents Page(s) Part I - Financial Statements Report of Independent Accountants on Financial Statements and Supplementary Schedule of Expenditures of Federal Awards I-1 Financial Statements for the years ended June 30, 2001 and 2000 I-2 Notes to the Financial Statements I-6 Part II - Schedule of Expenditures of Federal Awards Schedule of Expenditures of Federal Awards for the year ended June 30, 2001 II-1 Notes to the Schedule of Expenditures of Federal Awards II-2 Part III - Reports on Internal Control and Compliance Report on Compliance and on Internal Control Over Financial Reporting Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards for the year ended June 30, 2001 III-1 Report on Compliance with Requirements Applicable to Each Major Program and Internal Control over Compliance in Accordance with OMB Circular A-133 for the year ended June 30, 2001 III-3 Part IV - Findings Schedule of Findings and Questioned Costs - June 30, 2001 IV-1 Summary Schedule of Prior Audit Findings IV-6 Management's Corrective Action Plan IV-8

Part I

Financial Statements

Part II

Schedule of Expenditures of Federal Awards

Harvard UniversitySchedule of Expenditures of Federal AwardsFor the Year Ended June 30, 2001

DHHS

NIH Other NSF Defense AID Energy NASA Education NEH Justice EPA HUD State Others Total

CFDA Federal Agency Code 47 12 02 81 43 84 06 16 66 14 19

Major Programs:

Research and Development and Research Training:

Direct awards 225,207,669$ 14,742,717$ 23,726,221$ 9,884,738$ 6,312,880$ 5,628,093$ 7,615,245$ 2,813,605$ 347,389$ 3,540,697$ 3,531,395$ 1,842,332$ 1,057,060$ 1,758,911$ 308,008,952$

Subagreements 15,670,975 3,514,254 1,398,046 2,955,478 1,891,664 2,588,585 1,675,692 681,202 - 3,606 864,046 96 - 731,520 31,975,164

Total Research and Development and Research Training 240,878,644 18,256,971 25,124,267 12,840,216 8,204,544 8,216,678 9,290,937 3,494,807 347,389 3,544,303 4,395,441 1,842,428 1,057,060 2,490,431 339,984,116

Student Financial Assistance

Direct awards - 133,442 3,687,170 - - - - 8,153,182 - - - - - 14,870 11,988,664

Subagreements - - - - - - - - - - - - 13,445 - 13,445

Total Student Financial Assistance - 133,442 3,687,170 - - - - 8,153,182 - - - - 13,445 14,870 12,002,109

Total Major Programs 240,878,644 18,390,413 28,811,437 12,840,216 8,204,544 8,216,678 9,290,937 11,647,989 347,389 3,544,303 4,395,441 1,842,428 1,070,505 2,505,301 351,986,225

Nonmajor Programs:

Direct awards 683,079 449,121 1,938,352 539,365 - 102,314 - 1,672,296 633,510 - - - - 179,944 6,197,981

Subagreements 4,737 403,171 1,024,212 235,848 285,767 109,226 47,722 347,196 - - 2,219 - 99,612 43,369 2,603,079

Total Nonmajor Programs 687,816 852,292 2,962,564 775,213 285,767 211,540 47,722 2,019,492 633,510 - 2,219 - 99,612 223,313 8,801,060

Total 241,566,460$ 19,242,705$ 31,774,001$ 13,615,429$ 8,490,311$ 8,428,218$ 9,338,659$ 13,667,481$ 980,899$ 3,544,303$ 4,397,660$ 1,842,428$ 1,170,117$ 2,728,614$ 360,787,285$

93

The accompanying notes are an integral part of this schedule of expenditures of federal awards.

II-1

Harvard University Notes to Schedule of Expenditures of Federal Awards For the Year Ended June 30, 2001

II-2

1. Basis of Presentation The accompanying Schedule of Expenditures of Federal Awards (the "Schedule") summarizes the

expenditures of Harvard University (the "University") under programs of the federal government for the year ended June 30, 2001. The information in this schedule is presented in accordance with the requirements of Office of Management and Budget (OMB) Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. Therefore, some amounts presented in this schedule may differ from amounts presented in, or used in the preparation of, the basic financial statements of the University.

For purposes of the Schedule, Federal awards include all grants, contracts and similar agreements entered

into directly by the University with agencies and departments of the federal government and all subawards to the University by nonfederal organizations pursuant to federal grants, contracts and similar agreements. The awards are classified into major program and nonmajor program categories in accordance with the provisions of OMB Circular A-133. The major programs are:

Research and Development and Research Training - Includes awards for research and development

work at the University's Medical School and School of Public Health and for work at the University's academic divisions, primarily under grants with agencies and divisions of the Department of Health and Human Services. This program also includes awards to support research training for graduate and other students, primarily under programs of the National Institutes of Health.

Student Financial Assistance - Includes certain awards to provide financial assistance to students,

primarily under the Federal Work-Study (FWS), Pell Grant (Pell) and Supplemental Educational Opportunity Grant (SEOG) and similar programs of the Department of Education (see Note 8). The University receives awards to make loans to eligible students under certain federal student loan programs and federally guaranteed loans are issued to students of the University. These loans are considered for purposes of determining whether student financial aid is a Type A or Type B program. These loans are included in Note 9 to this schedule.

Nonmajor programs include certain awards for other sponsored activities (i.e., other than instruction and

organized research) at the University's Medical School and School of Public Health and for work at the University's academic divis ions, primarily under grants from the Department of Education and the National Science Foundation. Examples of such programs include conferences and symposia, library collections and preservations, health service projects, and community service programs.

2. Summary of Significant Accounting Policies for Federal Award Expenditures Expenditures reported in the Schedule are reported on the accrual basis of accounting. Such expenditures

are recognized following the cost accounting principles contained in OMB Circular A-21, Cost Principles for Educational Institutions, wherein certain types of expenditures are not allowable or are limited to reimbursement. Moreover, expenditures include a portion of costs associated with general university activities which are allocated to awards under negotiated formulas commonly referred to as facilities and administrative cost rates.

Harvard University Notes to Schedule of Expenditures of Federal Awards For the Year Ended June 30, 2001

II-3

3. Summary of Sponsoring Agencies The full names of the sponsoring agencies included in the Schedule and notes to the Schedule are as

follows:

DHHS - Department of Health and Human ServicesNIH - National Institutes of HealthNSF - National Science FoundationDefense - Department of Defense, including Defense agenciesAID - United States Agency for International DevelopmentEnergy - Department of EnergyNASA - National Aeronautics and Space AdministrationEducation - Department of EducationNEH - National Endowment for the HumanitiesJustice - Department of JusticeEPA - Environmental Protection AgencyHUD - Housing and Urban DevelopmentState - Department of State

For purposes of the Schedule, agencies which provided less than $700,000 of federal awards expended by the University have been combined as "Other." These agencies include the Departments of Commerce, Labor, Transportation, Agriculture and Veteran Affairs; the Central Intelligence Agency; the National Endowment for the Arts; the United States Institute of Peace; the U.S. Geological Survey; the Japan - U.S. Friendship Commission; the National Oceanic and Atmospheric Administration; the National Park Service; the Institute of Museum and Library Services; the National Institute of Standards and Technology; the National Security Agency; the General Services Administration; the U.S. Information Agency; and the Internal Revenue Service.

4. Summary of Facilities and Administrative Costs Facilities and administrative cost recoveries for the year ended June 30, 2001 are as follows: Research and development and research training $ 97,413,986 Other $ 1,005,738

$ 98,419,724 The University recovers facilities and administrative costs associated with sponsored agreements pursuant

to arrangements negotiated with federal cognizant agencies by the Medical School, School of Public Health, and the University Area. Predetermined facilities and administrative rates have been established for the Medical School, the University Area, and the School of Public Health through fiscal year 2002. The Radcliffe Institute for Advanced Study has a separate facilities and administrative rate established prior to the merger of Radcliffe College and the University.

Facilities and administrative cost recoveries associated with train ing programs generally represent the

maximum administrative overhead allowance allowed by the sponsors. The University also recovers administrative cost allowances from certain campus-based student financial assistance programs.

Harvard University Notes to Schedule of Expenditures of Federal Awards For the Year Ended June 30, 2001

II-4

5. Expenditures under Awards from the Department of Health and Human Services In addition to NIH, federal awards from DHHS include awards from various centers, divisions and

institutes of DHHS. Federal award expenditures by funding source within DHHS for the year ended June 30, 2001 are summarized as follows:

Public Health Service Agency for Healthcare Research and Quality (AHRQ) $ 6,490,168 Center for Disease Control and Prevention (CDC) 6,162,274 Health Resources and Services Administration (HRSA) 2,329,683 Office of the Assistant Secretary for Health (OASH) 217,877 Other Public Health Service Sources 3,271,337 Substance Abuse and Mental Health Services Administration (SAMHSA) 771,366

$19,242,705 6. Awards to Subrecipients Certain federal funds are provided to subrecipient organizations by the University. The following

expenditures incurred by these subrecipients are reimbursed by the University and included on the Schedule as a part of major program direct awards for the year ended June 30, 2001.

Agency CFDA# Amount

NIH 93 27,602,299$ Other DHHS 93 2,561,149AID 2 1,300,852Defense 12 2,394,740NSF 47 1,063,914Education 84 2,036,687NASA 43 596,768HUD 14 642,946EPA 66 628,116Energy 81 949,663Other 372,271

Total 40,149,405$

7. Pass-Through Awards/Subrecipients In addition to direct awards, the University receives awards via pass-through entities. The total amount

expended by the University and reimbursed by pass-through entities for the year ended June 30, 2001 was $34,591,688. See Appendix A for a listing of subagreements, sorted by federal sponsor agency and pass-through entity.

Harvard University Notes to Schedule of Expenditures of Federal Awards For the Year Ended June 30, 2001

II-5

8. Expenditures under Awards from Student Financial Assistance Programs For the year ended June 30, 2001, federal student financial assistance program expenditures, exclusive of

loan programs (see Note 9) are summarized as follows: Department of Education Pell $ 1,327,424

Federal Supplemental Educational Opportunity Grant (SEOG) 2,108,735 Federal Work Study (FWS) 3,030,807 2000 Jacob K. Javits Fellowship Program 780,327 Foreign Language and Area Studies Fellowships 574,136 Fullbright – Hays Doctoral Dissertation Research Abroad 23,892 Graduate Fellowship 162,350 National Resource Centers and Foreign Language Area Studies 140,752

Robert Byrd Scholarship Program* 1,415,625 Total $ 9,564,048 Department of Health and Human Services Public Health Traineeship $ 62,593 Scholarship for Disadvantaged Students 70,849 Total $ 133,442 National Science Foundation Graduate Research Fellowship Program $ 3,687,170 Other $ 28,315 *Robert Byrd scholarships are not included in the schedule of expenditures, but are federal funds awarded directly to students. 9. Federal Student Loan Programs The Perkins, Health Professions Student Loan Program (HPSL), Loans for Disadvantaged Students (LDS),

and certain FFEL Stafford and SLS/PLUS loans are administered directly by the University and the balances and transactions relating to these programs are included in the University's general purpose financial statements. The balances of these loans outstanding at June 30, 2001 consist of:

Perkins $ 55,091,743 FFEL (includes FISL, PLUS, and SLS) $ 52,624,127 HPSL/LDS/PCL $ 5,851,843

Harvard University Notes to Schedule of Expenditures of Federal Awards For the Year Ended June 30, 2001

II-6

Loans made by the University to eligible students under federal student loan programs and federally guaranteed loans issued to students during the year ended June 30, 2001 and included in the University’s balance sheet are summarized as follows:

Direct Subsidized Stafford $ 34,578,805 Direct Unsubsidized Stafford 36,364,794 Direct PLUS 3,920,807 Perkins 9,362,268 HPSL/PCL 300,175 LDS - Federal Family Education Loan Programs (FFELP) interest subsidy, only 879,155 FFELP Stafford issued by banks 470,009 FFELP Unsubsidized Stafford issued by banks 543,131

$ 86,419,144 The University is not a lender under the Health Education Assistance Loan program (HEAL) and is

responsible only for the performance of certain administrative duties with respect to HEAL. Accordingly, these loans are not included in the University's general purpose financial statements and it is not practical to determine the balance of loans outstanding to students and former students of the University under these programs at June 30, 2001. Nonetheless, students of the University may participate in this loan program by borrowing from participating banks.

10. Contingencies In July 1999, the University commenced a comprehensive investigation of certain grants funded by the

National Institute on Aging. The University reported its initial findings of the investigation to the National Institutes of Health. The University is in discussions with the government about the situation, and the ultimate outcome cannot be determined at this time.

In April 1996, the Harvard Institute for International Development (HIID) learned of an investigation by

the Inspector General's Office of the U.S. Agency for International Development (USAID) into the activities of two individuals engaged by HIID. USAID had awarded amounts to HIID under two cooperative agreements to provide assistance to Russia in implementing economic and legal reforms. The U.S. Attorney's Office also conducted a grand jury investigation into certain activities related to the Moscow project, although it declined to bring criminal indictments. In September 2000, the United States filed an eleven-count complaint against the University and others seeking recovery damages of the full amount of the awards ($40 million), together with other remedies available under the False Claims Act. Since then, certain counts have been dismissed. Discovery is ongoing for the remaining counts, including those under the False Claims Act.

While it is not possible to predict accurately or determine the eventual outcome of the above described

legal matters or various other legal proceedings involving the University, management believes that the outcome of these proceedings will not have a material adverse effect on the University's financial position.

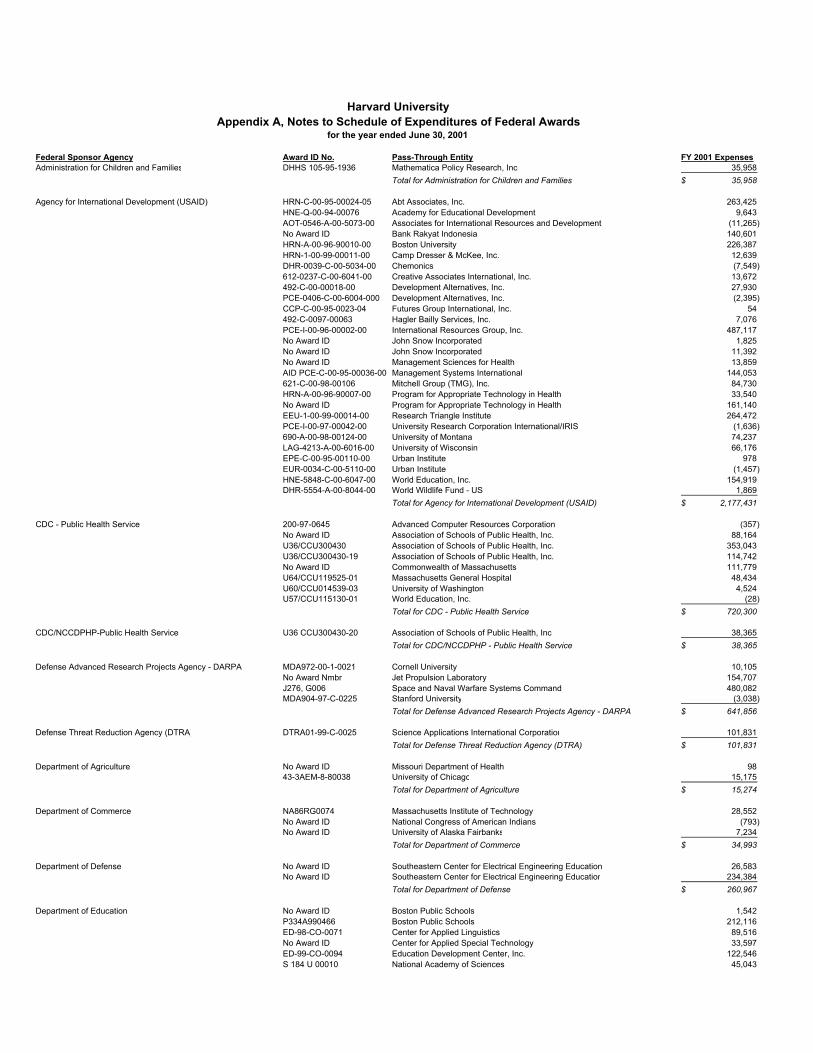

Federal Sponsor Agency Award ID No. Pass-Through Entity FY 2001 ExpensesAdministration for Children and Families DHHS 105-95-1936 Mathematica Policy Research, Inc. 35,958

Total for Administration for Children and Families 35,958$

Agency for International Development (USAID) HRN-C-00-95-00024-05 Abt Associates, Inc. 263,425 HNE-Q-00-94-00076 Academy for Educational Development 9,643 AOT-0546-A-00-5073-00 Associates for International Resources and Development (11,265) No Award ID Bank Rakyat Indonesia 140,601 HRN-A-00-96-90010-00 Boston University 226,387 HRN-1-00-99-00011-00 Camp Dresser & McKee, Inc. 12,639 DHR-0039-C-00-5034-00 Chemonics (7,549) 612-0237-C-00-6041-00 Creative Associates International, Inc. 13,672 492-C-00-00018-00 Development Alternatives, Inc. 27,930 PCE-0406-C-00-6004-000 Development Alternatives, Inc. (2,395) CCP-C-00-95-0023-04 Futures Group International, Inc. 54 492-C-0097-00063 Hagler Bailly Services, Inc. 7,076 PCE-I-00-96-00002-00 International Resources Group, Inc. 487,117 No Award ID John Snow Incorporated 1,825 No Award ID John Snow Incorporated 11,392 No Award ID Management Sciences for Health 13,859 AID PCE-C-00-95-00036-00 Management Systems International 144,053 621-C-00-98-00106 Mitchell Group (TMG), Inc. 84,730 HRN-A-00-96-90007-00 Program for Appropriate Technology in Health 33,540 No Award ID Program for Appropriate Technology in Health 161,140 EEU-1-00-99-00014-00 Research Triangle Institute 264,472 PCE-I-00-97-00042-00 University Research Corporation International/IRIS (1,636) 690-A-00-98-00124-00 University of Montana 74,237 LAG-4213-A-00-6016-00 University of Wisconsin 66,176 EPE-C-00-95-00110-00 Urban Institute 978 EUR-0034-C-00-5110-00 Urban Institute (1,457) HNE-5848-C-00-6047-00 World Education, Inc. 154,919 DHR-5554-A-00-8044-00 World Wildlife Fund - US 1,869

Total for Agency for International Development (USAID) 2,177,431$

CDC - Public Health Service 200-97-0645 Advanced Computer Resources Corporation (357) No Award ID Association of Schools of Public Health, Inc. 88,164 U36/CCU300430 Association of Schools of Public Health, Inc. 353,043 U36/CCU300430-19 Association of Schools of Public Health, Inc. 114,742 No Award ID Commonwealth of Massachusetts 111,779 U64/CCU119525-01 Massachusetts General Hospital 48,434 U60/CCU014539-03 University of Washington 4,524 U57/CCU115130-01 World Education, Inc. (28)

Total for CDC - Public Health Service 720,300$

CDC/NCCDPHP-Public Health Service U36 CCU300430-20 Association of Schools of Public Health, Inc 38,365 Total for CDC/NCCDPHP - Public Health Service 38,365$

Defense Advanced Research Projects Agency - DARPA MDA972-00-1-0021 Cornell University 10,105 No Award Nmbr Jet Propulsion Laboratory 154,707 J276, G006 Space and Naval Warfare Systems Command 480,082 MDA904-97-C-0225 Stanford University (3,038)

Total for Defense Advanced Research Projects Agency - DARPA 641,856$

Defense Threat Reduction Agency (DTRA) DTRA01-99-C-0025 Science Applications International Corporation 101,831 Total for Defense Threat Reduction Agency (DTRA) 101,831$

Department of Agriculture No Award ID Missouri Department of Health 98 43-3AEM-8-80038 University of Chicago 15,175

Total for Department of Agriculture 15,274$

Department of Commerce NA86RG0074 Massachusetts Institute of Technology 28,552 No Award ID National Congress of American Indians (793) No Award ID University of Alaska Fairbanks 7,234

Total for Department of Commerce 34,993$

Department of Defense No Award ID Southeastern Center for Electrical Engineering Education 26,583 No Award ID Southeastern Center for Electrical Engineering Education 234,384

Total for Department of Defense 260,967$

Department of Education No Award ID Boston Public Schools 1,542 P334A990466 Boston Public Schools 212,116 ED-98-CO-0071 Center for Applied Linguistics 89,516 No Award ID Center for Applied Special Technology 33,597 ED-99-CO-0094 Education Development Center, Inc. 122,546 S 184 U 00010 National Academy of Sciences 45,043

Harvard UniversityAppendix A, Notes to Schedule of Expenditures of Federal Awards

for the year ended June 30, 2001

R306F60077 Regents of the University of California - Santa Cruz 10,991 EA96009001 Research Triangle Institute 54,976 R3086A60003 University of Pennsylvania 315,928 R3086A60003-01A University of Pennsylvania 142,143

Total for Department of Education 1,028,398$

Department of Energy O-KC75-00055-00 Argonne National Laboratory 11,856 W-31-109-Eng-38 Argonne National Laboratory (1,046) DE-FC26-0NT40771 CONSOL Energy, Inc 88,975 DE-AC02-76CH03000 Fermi National Accelerator Laboratory 646,338 W-7405-ENG-48 Lawrence Livermore Laboratory 43,534 W-7405-ENG-36 Los Alamos National Laboratory 44,021 C95-175002 Massachusetts Institute of Technology (1,272) DE-A07-991013727 Massachusetts Institute of Technology 75,060 DE-AC36-99-GO10337 National Renewable Energy Laboratory 38,579 DE-AC36-99GO10337 National Renewable Energy Laboratory 152,003 No Award ID Oak Ridge Institute For Science And Education 34,375 ENG-9812731 Rand Corporation 109,226 DE-FC03-90ER61010 Regents of the University of California - Davis 1,378,469 DE-FG02-98ER62702 Resources for the Future, Inc. 26,413 No Award ID Sandia National Laboratories 40,432

Total for Department of Energy 2,686,963$

Department of Health & Human Services 282-98-0029 American Institutes for Research 70,948 90-YD-0017/01 Education Development Center, Inc. 15,198 R01 RR13213-04 Massachusetts General Hospital 111,097

Total for Department of Health & Human Services 197,243$

DHHS/Office of Acquisition Management HHS-100-00-0025 ROW Sciences 107,929 Total for DHHS/Office of Acquisition Management 107,929$

Department of Housing and Urban Development C-OPC-21356 Westat Corporation 96 Total for Department of Housing and Urban Development 96$

Department of Justice 2000-DT-CX-K001 Dartmouth College 3,606 Total for Department of Justice 3,606$

Department of State AEMA-0018 Institute of International Education, Inc. 43,952 AEMA-1018 Institute of International Education, Inc. 55,660 S-OPRAQ-99-H-0036 Open Society Institute 13,445

Total for Department of State 113,057$

Department of Transportation 1700.18B Massachusetts Institute of Technology 35,000 DTRS99-G-0001 Massachusetts Institute of Technology 68,952 No Award ID Massachusetts Institute of Technology 48,068

Total for Department of Transportation 152,020$

Department of Veterans Affairs V101(93)P-1637 TO 10 National Academy of Sciences 58,576 Total for Department of Veterans Affairs 58,576$

Department of the Air Force F49620-99-1-0272 Brown University 143,431 F49620-97-1-0382 Dartmouth College 59,135 F33615-99-1-1499 New York University 108,193 F49620-96-1-0478 Regents of the University of California - Berkeley 119,622 F49620-97-1-0247 Regents of the University of California - Santa Barbara 174 F30602-99-C-0187 SRI International 49,694

Total for Department of the Air Force 480,249$

Department of the Army DAAG55-98-1-0468 Academy of Applied Science, Inc. 35,805 DAAH55-98-1-0468 Academy of Applied Science, Inc. (29) DAAH04-96-1-0445 Brown University 155,290 DAAG55-98-1-0266 California Institute of Technology 147,032 DAAG55-98-1-0491 Desert Research Institute 21,331 DACA87-00-H-0019 Desert Research Institute 159,864 DAMD17-00-2-0052 Desert Research Institute 53,661 BC961685 Hoechst-ARIAD Genomics Center, LLC 4,647 No Award ID Massachusetts General Hospital 3,044 DAMD17-99-2-9001 Massachusetts General Hospital 46,722 DAAL03-92-G-0115 Massachusetts Institute of Technology (4,935) DAAG55-98-1-0270 Princeton University 217,522 DAAH04-95-1-0102 Princeton University 1,285 DAAD13-00-C-5003 Radiation Monitoring Devices, Inc. 23,310 DAAD19-99-1-0158 Regents of the University of California - Santa Barbara 128,540 DAAD-19-99-1-0215 University of Rochester 275,428 DAMD17-97-1-7081 University of Southern California 532 DAAD 19-00-1-0169 Yale University 198,599

Total for Department of the Army 1,467,646$

Department of the Navy N00014-98-C-0220 Immersion Human Interface Corporation (4,661) N00014-97-11-1066 Massachusetts Institute of Technology 36,590

N00014-00-1-0438 Princeton University 47,587 N0001496-1-1215 Regents of the University of California - Santa Barbara 96,882 N00014-98-1-0669 Stanford University 62,379

Total for Department of the Navy 238,777$

Environmental Protection Agency 68-D-99-011 Battelle Memorial Institute 74,958 826780-01-0 Brigham & Women's Hospital 37,144 11008 Environmental Health & Engineering 2,047 68D20134 Environmental Science and Engineering, Inc. (10,800) R 824835 Health Effects Institute 117,662 R-824835 Health Effects Institute 148,670 R824835 Health Effects Institute 7,188 No Award ID IT Corporation 4,051 No Award ID Mickey Leland National Urban Air Toxics Research Center 194,532 R826373 Pennsylvania State University 27,194 R826373-01 Pennsylvania State University 36,884 R827058-01-0 Suffolk County Conservation District 79,263 CR827232-01-0 Tufts University School of Medicine 6,756 CR827033 Univ of Med+Dentistry of NJ-RWJ Med. School 2,219 R-82805801 Washington University 138,496

Total for Environmental Protection Agency 866,264$

Food & Drug Administration DHHS P50 DA10223 Brandeis University 11,059 FD-U-001641-02 Harvard Pilgrim Health Care, Inc 34,896

Total for Food & Drug Administration DHHS 45,956$

HRSA - Public Health Service No Award ID Association of Schools of Public Health, Inc. 7,543 U76 AH10002-04 Association of Schools of Public Health, Inc. 100 1 D20 HP00003-01 Boston University 45,214 HRSA-240-93-0050 Mathematica Policy Research, Inc. (4,869)

Total for HRSA - Public Health Service 47,988$

HRSA Maternal & Child Health Bureau - Public Health Service 1 R40 MC00117 American Academy of Pediatrics 16,980 5 H16 MC00050 Harvard Pilgrim Health Care, Inc 29,704

Total for HRSA Maternal & Child Health Bureau - Public Health Service 46,684$

Health Care Financing Administration 500-95-0057 Barents Group LLC 20,115 500-95-0057 Picker Institute 547,714 500-95-0056 Rand Corporation 1,164,798

Total for Health Care Financing Administration 1,732,627$

Internal Revenue Service TIRNO-98-D-00012 Science Applications International Corporation (12,243) Total for Internal Revenue Service (12,243)$

Jet Propulsion Laboratory 1223696 Cornell University 7,200 Total for Jet Propulsion Laboratory 7,200$

NASA Headquarters 10167 Jet Propulsion Laboratory 24,989 NAS7-918 Jet Propulsion Laboratory 9,792 No Award ID National Institute of Standards and Technology 36,511 NCC9-58 National Space Biomedical Rsch Inst/Baylor Coll of Med 620,374 NCC9-58 National Space Biomedical Rsch Inst/Morehouse School of Med (22) No Award ID Space Telescope Science Institute 40,687

Total for NASA Headquarters 732,331$

NASA - Ames Research Center NCC 2-1169 American Museum of Natural History 47,722 NAG2-1361 Regents of the University of California - Berkeley 61,855

Total for NASA - Ames Research Center 109,577$

NASA - Goddard Space Flight Center NAG5-4839 Children's Hospital Corporation 31,920 NAG5-9605 Duke University 55,593 NAGW5-3665 Duke University (1,666) NAG5-6656 Pennsylvania State University 90,750 NAG5-7547 Pennsylvania State University 52,892 NAS5-26555 Space Telescope Science Institute 326,965 NAG5-9752 University of Massachusetts - Dartmouth 87,281

Total for NASA - Goddard Space Flight Center 643,735$

NASA - Marshall NAS8-39073 Smithsonian Astrophysical Observatory 230,571 Total for NASA - Marshall 230,571$

NIH - Public Health Service No Award ID Brigham & Women's Hospital 3,389 Total for NIH - Public Health Service 3,389$

NIH/FIC - Public Health Service D43 TW00018-12 Weill Medical College of Cornell University 67,543 Total for NIH/FIC - Public Health Service 67,543$

NIH/NCCAM - Public Health Service R01 AT00402 Beth Israel Deaconess Medical Center 70,740 Total for NIH/NCCAM - Public Health Service 70,740$

NIH/NCI - Public Health Service CA62462-04 American College of Radiology (39) R01 CA67264 Board of Regents of the University of Wisconsin - Madison 128,582 R01 CA70818 Boston Medical Center 57,196 R01 CA84506 Boston Medical Center 53,162 1 R01 CA82838-02 Brigham & Women's Hospital 110,643 1 R01 CA90792-01 Brigham & Women's Hospital 8,846 2 R01 CA50597-10 Brigham & Women's Hospital 79,310 5 R01 CA49449-11 Brigham & Women's Hospital 246,908 5 R01 CA65725-05 Brigham & Women's Hospital 52,547 5 R01 CA70817-04 Brigham & Women's Hospital 264 R01 CA42182 Brigham & Women's Hospital 141,356 R01 CA58684 Brigham & Women's Hospital 171,773 U01 CA49449-09 Brigham & Women's Hospital (7,241) 5 R01 CA28735-17 Children's Hospital Corporation 43,557 1 R01 CA84384-01 Dana Farber Cancer Institute 77,079 1 R01 CA91753-01 Dana Farber Cancer Institute 12,064 2 P30 CA06516-37 Dana Farber Cancer Institute 962,781 5 P01 CA50661-13 Dana Farber Cancer Institute 240,732 5 R01 CA72663-03 Dana Farber Cancer Institute (8,719) P01 CA50661 Dana Farber Cancer Institute 332,281 P50 CA89393 Dana Farber Cancer Institute 130,325 R01 CA68087 Dana Farber Cancer Institute (29) R01 CA72663 Dana Farber Cancer Institute (24,878) 5 R01 CA72570-04 Harvard Pilgrim Health Care, Inc 12,728 2 P01 CA69246-05 Massachusetts General Hospital 152,880 5 R01 CA83960-02 Massachusetts General Hospital 37,993 5 P50 CA84719-02 Miriam Hospital 115,816 NO1-CN-65107 Northern California Cancer Center 9,193 R01 CA52689-09 Regents of the University of California - San Francisco 75,232 R01 CA59706 Regents of the University of California - San Francisco 213 5 R01 CA79593-02 Regents of the University of Minnesota 59,715 R01 CA75450 University of North Carolina - Chapel Hill (746) 1 P01 CA80111-01 Whitehead Institute for Biomedical Research (433) 5 P01 CA80111-03 Whitehead Institute for Biomedical Research 194,709

Total for NIH/NCI - Public Health Service 3,465,802$

NIH/NCRR - Public Health Service 5 R01 RR13601-04 Beth Israel Deaconess Medical Center 132,316 R01 RR13150 Beth Israel Deaconess Medical Center 154,005 5 R21 RR14465-02 Brigham & Women's Hospital 65,724 R01 RR14447 Dana Farber Cancer Institute 197,101 7 R01 RR13601-02 Oklahoma State University (72) R01 RR13156-04 Thomas Jefferson University 81,179 R01 RR13537 Tufts University 137,708 R01 RR13843 Tufts University 215,374

Total for NIH/NCRR - Public Health Service 983,334$

NIH/NHGRI - Public Health Service 2-RO1-HG01257-04 Health Research, Inc. 7,294 P01 AG/HD11952 Rand Corporation 13,895

Total for NIH/NHGRI - Public Health Service 21,190$

NIH/NHLBI - Public Health Service 1 RO1 HL63737-02 Beth Israel Deaconess Medical Center 25,109 5 R01 HL61940-04 Beth Israel Deaconess Medical Center 25,839 P01 HL43510 Beth Israel Deaconess Medical Center 178 P60 HL15157-29 Boston Medical Center 199,688 1 R01 HL64075-02 Brigham & Women's Hospital 80,560 1 R01 HL66386-01 Brigham & Women's Hospital 8,042 2 P50 HL52320 Brigham & Women's Hospital 352,632 5 P50 HL52320 Brigham & Women's Hospital 321 5 P50 HL56383-06 Brigham & Women's Hospital 212,861 5 R01 HL54098-03 Brigham & Women's Hospital 9,083 5 R01 HL56371-04 Brigham & Women's Hospital 381,443 5 R01 HL63927-02 Brigham & Women's Hospital 39,890 P50 HL56383 Brigham & Women's Hospital 72,487 5 P50 HL56398-05 Children's Hospital Corporation 20,662 R01 HL41786 Children's Hospital Corporation 78,140 1 U01 HL66678-01 Massachusetts General Hospital 149,198 R01 HL55718 Massachusetts General Hospital 339 P01 HL42443 New England Medical Center Hospitals, Inc. (317) 5 P01 HL59139-03 Pennsylvania State University 23,929 U01 HL55981 Regents of the University of California - San Francisco 41,798 RO1 HL55162 Regents of the University of Michigan (67) HL34174 Stanford University (486) 1 RO1 HL65405-01 Vanderbilt University 158,623 U01 HL58946 Washington University 22,097

Total for NIH/NHLBI - Public Health Service 1,902,049$

NIH/NIA - Public Health Service R01 AI48489 Board of Regents of the University of Wisconsin - Madison 99,079 5 P01 AG09975-08 Brigham & Women's Hospital 139,847 P01 AG14366 Brigham & Women's Hospital 112,873 R01 AG15478 Massachusetts General Hospital 35,070

U01 AG14282-05 New England Research Institutes, Inc. 9,988 AG17058-01 Regents of the University of California - Los Angeles 27,459 5 P01 AG04390-17 University of Pittsburgh 21,674

Total for NIH/NIA - Public Health Service 445,990$

NIH/NIAID - Public Health Service N01-AI35176 Abt Associates, Inc. 3,656 1 R01 AI42006-01 Boston Medical Center 53,966 R21 AI42006 Boston Medical Center (74,598) 5 U01 AI39769-05 Boston University 36,288 AI 34856 Brigham & Women's Hospital 2,023 R01 AI35786 Brigham & Women's Hospital 78,629 1 R21 AI47479-01 Center for Blood Research Incorporated 87,287 P01 AI42257 Center for Blood Research Incorporated 486,074 5 P01 AI31541-10 Children's Hospital Corporation 237,743 5 R01 AI41365-04 Children's Hospital Corporation 369,215 P01 AI39619 Children's Hospital Corporation 93,025 P01 AI43649 Children's Hospital Corporation 173 U19 AI31541 Children's Hospital Corporation (22,350) R01 AI42402 Connecticut Children's Medical Center 147,285 1 P01 AI45757 Dana Farber Cancer Institute 189,532 P01 AI37833 Dana Farber Cancer Institute (76,509) P01 AI43649 Dana Farber Cancer Institute 68,515 5 U01 AI46749-02 Family Health International 15,718 1 U01 A146703-01 Fred Hutchinson Cancer Research Center 39,916 5 R01 AI42006-05 Massachusetts General Hospital 79,424 P01 AI39755 Massachusetts General Hospital 86,095 1 U19 AI45955-01 Michigan State University 64,203 7 U01 AI039776-03 RHO Federal Systems Division, Inc. 204,542 P01 AI45992-02 Regents of the University of California - San Diego 231,173 U01 AI38858 Social & Scientific Systems, Inc. 521,576 1 P01 AI48244-01 Thomas Jefferson University 30,641 5 R21 AI46253-02 Thomas Jefferson University 63,087 5 R01 AI42390-03 University of Arkansas 234,468 1 P30 AI42845-01 University of Massachusetts - Worcester 39,048 5 P30 AI42845-03 University of Massachusetts - Worcester 22,075 5 R21 AI44338-02 University of Massachusetts - Worcester 3,648 R01 AI39400 University of Massachusetts - Worcester 138 5 U19 AI31448-10 University of Washington 85,433 R01 AI41440 Yale University 8,471

NIH/NIAID - Public Health Service 3,409,611$

NIH/NIAMS - Public Health Service R01 AR40321 Beth Israel Deaconess Medical Center (18) 5 P60 AR44811 University of Pittsburgh 38,729

Total for NIH/NIAMS - Public Health Service 38,711$

NIH/NICHD - Public Health Service 1 R01 HD38561-01 A1 Beth Israel Deaconess Medical Center 30,762 1 R41 HD35769-01 Cell & Molecular Technologies Inc. (46,211) R42 HD35769 Cell & Molecular Technologies Inc. 203,739 1 P01 HD 39530-01 Center for Applied Linguistics 52,085 1 P01 HD39530-01 Center for Applied Linguistics 13,953 5 P01 HD24926-12 Dana Farber Cancer Institute 188,354 R01 HD36093 Johns Hopkins University 219,668 K12 HD00850-15 Yale University 972 N01-HC-55148 Yale University 284,373

Total for NIH/NICHD - Public Health Service 947,695$

NIH/NIDA - Public Health Service 1 R01 DA11541-01A1 Georgia Institute of Technology 101,727 N01 DA78081 Organix, Inc. 18,270 R01 DA11542 Organix, Inc. 22,076 R01 DA12189 Research Foundation of SUNY (State University of New York) 772

NIH/NIDA - Public Health Service 142,846$

NIH/NIDCD - Public Health Service R01 DC03425 Board of Regents of University of Arizona 27,414 R01 DC03604 University of Cincinnati 87,507 P01 DC000347 University of Maryland, Baltimore (627)

Total for NIH/NIDCD - Public Health Service 114,293$

NIH/NIDCR - Public Health Service 5 R01 DE11939-04 Boston University 63,886 5 P30 DE11814-03 Forsyth Dental Center (4,299) 5 P30 DE11814-04 Forsyth Dental Center 10,704 R01 DE11646 New England Medical Center Hospitals, Inc 20,436

NIH/NIDCR - Public Health Service 90,727$

NIH/NIDDK - Public Health Service P01 DK55495 Albert Einstein College of Medicine 108,146 R43 DK56581 Biostream, Inc. 24,070 5 P30 DK46200-09 Boston Medical Center 15,175 P30 DK46200 Boston Medical Center 71,880 2 P30 DK34854-17 Children's Hospital Corporation 56,699 5 P30 DK34854-17 Children's Hospital Corporation 43,854 R01 DK55086 Children's Hospital Corporation 51,657 P30 DK40561 Massachusetts General Hospital 4,523

P30 DK46200 New England Medical Center Hospitals, Inc. 112 R01 DK53512 University of Florida (86) 5 P01 DK53369-04 University of Washington 53,977 R24 DK56954 Washington University 331,167

Total for NIH/NIDDK - Public Health Service 761,176$

NIH/NIEHS - Public Health Service R01 HS09099 Beth Israel Deaconess Medical Center 16 1 R01 ES10932-01 Brigham & Women's Hospital 16,097 5 R01 ES05257-09 Brigham & Women's Hospital 163,913 R01 ES05257 Brigham & Women's Hospital (28) R01 ES07821 Brigham & Women's Hospital 33,218 ES10165-01 Columbia University 20,415 No Award ID Courtesy Associates 4,737 R01 HS08395 Georgetown University (432) R01 ES07198 Johns Hopkins University 35,423 2 R44 ES09038-03 OSI Pharmaceuticals 71,631 5 P30 ESO5707 Regents of the University of California - Davis 35,569 ES06198 Regents of the University of California - Davis 78,615 ES06516 Regents of the University of California - Davis (54,704) 5 R01 ES06717-06 Regents of the University of California - San Francisco 83,706 5 U01 ES09720-02 University of Cincinnati 216,121

Total for NIH/NIEHS - Public Health Service 704,299$

NIH/NIGMS - Public Health Service 5 R01 GM31318-40 Boston University 41,448 5 P50 GM52585-07 Brigham & Women's Hospital 318,263 5 P01 GM58448-03 Massachusetts General Hospital 269,008 5 R01 GM53452-05 Regents of the University of California - San Francisco 909 P01 GM54160 Yale University 163,402

NIH/NIGMS - Public Health Service 793,030$

NIH/NIMH - Public Health Service 5 R01 MH510428-05 Board of Regents of University of Arizona 10,594 1 R01 MH59254-01A1 Boston University 81,606 R24 MH57933 Boston University 24,013 R01 MH57735 Brown University 6,723 P50 MH43703 Johns Hopkins University 9,514 NO1MH80001 Massachusetts General Hospital 75,848 1-R01-MH60651-01A1 Massachusetts Institute of Technology 31,198 1R01 MH58240-02 McLean Hospital 27,090 P01 MH31154 McLean Hospital 69,854 5 R01 MH59575-04 Regents of the University of Michigan 58,624 5 P50 MH48408-10 Stanford University 62,556 R01 MH057139-02 University of Massachusetts - Worcester 9,732

Total for NIH/NIMH - Public Health Service 467,351$

NIH/NINDS - Public Health Service 5 P01 NS40043-02 Beth Israel Deaconess Medical Center 258,788 P01 NS40043 Beth Israel Deaconess Medical Center 160,568 R01 NS34626-06 Massachusetts General Hospital 67,039 R01 NS36524 New England Medical Center Hospitals, Inc. 39,232 NS35138-13 University of Pennsylvania 233,610 P01 NS35138-13 University of Pennsylvania 269,961 RO1 NS32228 Washington University 216,738

NIH/NINDS - Public Health Service 1,245,935$

National Endowment for the Arts DCA 97-16 (CFDA 45026) Council of Chief State School Officers 52,083 Total for National Endowment for the Arts 52,083$

National Renewable Energy Laboratory AAD-9-18668-17 Regents of the University of California - Santa Barbara 10,848 Total for National Renewable Energy Laboratory 10,848$

National Science Foundation IIS-9988575 Boston University 34,345 AST-9318785 Brown University (9) SBR-9513040 Carnegie Mellon University 25,954 SBR-9521914 Carnegie Mellon University 50,274 PHY 97-22537 Columbia University 1,024,212 EAR-9529992 Incorporated Research Institutions for Seismology (IRIS) 53,036 EEC-9731748 Johns Hopkins University 71,552 DEB-9708092 Marine Biological Laboratory 68,785 DMR-9808941 Massachusetts Institute of Technology 15,599 PHY-0071311 Massachusetts Institute of Technology 174,205 PHY-9722639 Massachusetts Institute of Technology 28,093 PHY-9808941 Massachusetts Institute of Technology 35,078 EEC-9986821 Northeastern University 43,764 AST-9802568 Ohio State University Research Foundation 1,750 DMS-9615854 Regents of the University of California - Los Angeles 1,280 SES-9B18897 Regents of the University of New Mexico 8,698 OCE-0084032 Rutgers University 10,300 DBI-98346603 Tufts University School of Medicine 28,667 ACI-9619019 University of Illinois at Urbana - Champaign 185,693 AST-98-3137 University of Illinois at Urbana - Champaign 155,108 IIS-9811129 University of North Carolina - Chapel Hill 77,194 SBR-9873477 University of Rochester 58,136

EAR-89-20136 University of Southern California 65,531 EAR-8920136 University of Southern California 77,865 DMR-0080630 University of Texas - Austin 38,937 EAR-9909657 Woods Hole Oceanographic Institution 10,702 CCR-9980058 Yale University 77,507

National Science Foundation 2,422,258$

Public Health Service - AHRQ 5 R01 HS10131-02 Beth Israel Deaconess Medical Center 24,235 1U18 HS/CA1039-01 Harvard Pilgrim Health Care, Inc 14,861 5 R01 HS10060-02 Harvard Pilgrim Health Care, Inc 63,808 R01 HS10063 Harvard Pilgrim Health Care, Inc 81,523 R01 HS10247 Harvard Pilgrim Health Care, Inc 51,348 1 U18 HS11073-01 Minneapolis Medical Research Foundation 24,676 R01 HS10227 Rand Corporation 43,938 U01 HS 08578 Rand Corporation (1,014) 290-95-2005 Westat Corporation 16,267

Public Health Service - AHRQ 319,644$

Public Health Service - SAMHSA/CMHS 280-99-4005 Abt Associates, Inc. 17,689 270-96-002 Brandeis University 38,163 UD1 SM52229-02 Brigham & Women's Hospital 20,032 UDI SM52229 Brigham & Women's Hospital 93,219 No Award ID Commonwealth of Massachusetts/Department of Public Health 294,531 283-98-9008 Research Triangle Institute 147,606

Public Health Service - SAMHSA/CMHS 611,240$

Public Health Service - SAMHSA/CSAT UD1 TI11414 Brown University 13,490 Public Health Service - SAMHSA/CSAT 13,490$

U.S. Information Agency IA-AEMA-G8190011 American Council of Learned Societies (84,285) IA-AEMA-G9190003 American Council of Learned Societies 366,870 IA-AEMA-G9190007 American Council of Learned Societies 3,430

U.S. Information Agency 286,015$

Veterans Health Administration No Award ID PricewaterhouseCoopers 188,172 Veterans Health Administration 188,172$

Grand Total 34,591,688

PART III

REPORTS ON INTERNAL CONTROL AND COMPLIANCE

PART IV

FINDINGS

Harvard University Schedule of Findings and Questioned Costs For the Years Ended June 30, 2001

IV-1

Section I. Summary of Auditors' Results Financial Statements Type of auditor's reports issued: Unqualified Internal control over financial reporting: Material weakness(es) identified No Reportable condition(s) identified that are not considered to be material weaknesses None reported Noncompliance material to financial statements noted No Federal Awards Internal control over major programs: Material weakness(es) identified No Reportable condition(s) identified that are not considered to be material weakness(es) None reported Type of auditor's report issued on compliance for major programs: Unqualified Audit findings required to be reported in accordance with

OMB Circular A-133, Section .510(a): Yes, see Section III of this schedule Identification of Major programs: Research, Development and Training See Schedule of Expenditures of Financial Assistance Federal Awards Dollar threshold for Type A and B programs $3,000,000 Auditee qualifies as a low-risk auditee No Section II. Financial Statement Findings None

Harvard University Schedule of Findings and Questioned Costs For the Years Ended June 30, 2001

Section III. Federal Awards Findings and Questioned Costs 01-1 Allowable Costs/Cost Principles OMB A-21, section F.6.b requires that costs incurred for the same purpose in like circumstances be treated consistently as either direct or as facilities and administrative costs. Items such as administrative salaries, office supplies, local telephone costs and postage are normally charged as facilities and administrative costs. OMB A-21, section J.2 states that costs incurred for the purchase of alcoholic beverages are unallowable. Section J.15 states that costs of entertainment are unallowable. Section J.18 states that fines and penalties are unallowable. Section J.27 states that direct material cost should include only the materials and supplies actually used, and due credit should be given for any excess materials retained. Section J.48.a states that airfare costs in excess of the lowest available commercial discount airfare, Federal Government contract airfare, or customary standard airfare, are unallowable. Of the 120 transactions selected at the University for direct cost testing totaling $526,096, we noted transactions totaling approximately $13,006 where there was not supporting documentation to directly attribute the costs to the award or where specific awards had been charged in error. Of the twenty costs listed below, ten were unallowable costs related to such items as the purchase of alcoholic beverages, mathematical errors, or the improper appointment of a trainee, eight questioned or unallowable direct costs related to items normally charged as facilities and administrative costs, and two questioned costs related to lack of documentation.

Federal grant number Agency Number of transactions

Amount

Description

K-PIH-99156 HUD 1 $ 4.50 Alcoholic beverages erroneously charged to the award.

K-PIH-99156 HUD 2 444.25 Items purchased in advance but not used by year end.

K-PIH-99156 HUD 1 3.79 Late fee erroneously charged to the award. K-PIH-99156 HUD 1 85.02 Mathematical errors on invoice resulted in

charges erroneously charged to the award. 5 R01 A132475-09 NIH-NIAID 1 1.65 Hotel movie erroneously charged to the

award. 5 P01 DE012467-04 NIH-NIDCR 1 66.33

Unallowable charges removed from awards after sample selected

5 P01 CA55075-10 NIH-NIAID 1 206.00 Unallowable charges removed from awards after sample selected

5 T32 HL07374-20 NIH-NHLBI 2 8,134.56 Stipend for trainee who was improperly appointed to the training grant.

K-PIH-99156 HUD 2 418.76 Postage charges not directly allocable to the award due to lack of attribution.

K-PIH-99156 HUD 1 176.25 Long distance phone charges not directly allocable to the award due to lack of attribution.

5 R01 A132475-09

NIH-NIAID 1 147.18 Copy charges not directly allocable to the award due to lack of attribution.

5 P01 DE012467-04 NIH-NIDCR 1 1,730.00 Reprint charges not directly allocable to the award due to lack of attribution.

MCB-9817885 National Science Foundation

1 402.99 Clerical salary not directly allocable to the award due to lack of attribution.

5 R01 MH43518-13 NIH-NIMH 1 186.99 Office supplies not directly allocable to the award due to lack of attribution.

5 R01 MH43518-13 NIH-NIMH 1 93.26 Local and long distance phone charges not directly allocable to the award due to lack of attribution.

K-PIH-99156 HUD 1 254.75 Insufficient evidence that this air ticket was the lowest available fare.

5 P01 DE012467-04 NIH-NIDCR 1 649.68 Insufficient evidence that this air ticket was the lowest available fare.

20 $13,005.96

In addition to the questioned or unallowable costs identified as part of our original sample, additional questioned costs of $90,647.58 related to a training grant totaling $1,345,939 (NIH-NHLBI award number 5 T32 HL07374-20) for the award period 7/1/94 to 8/31/00 were identified.

Harvard University Schedule of Findings and Questioned Costs For the Years Ended June 30, 2001

Recommendation: The University should strengthen controls over the direct charging of costs to awards. We recommend that the University continue to educate departments about documentation and attribution requirements for costs which are normally treated as facilities and administrative costs. We recommend that period expense reports be monitored timely, both departmentally and centrally, to correct erroneous charges on awards. We also recommend that controls over monitoring of invoices from vendors and affiliated hospitals be strengthened. 01-2 Cost Transfers Circular A-21, Section C.4 states that any costs allocable to a particular sponsored agreement may not be shifted to other sponsored agreements in order to meet deficiencies caused by overruns, avoid restrictions, or for other reasons of convenience. In addition, the NIH Grants Policy Statement pg. II-35 states that transfers must be supported by documentation that fully explains how the error occurred and a certification of the correctness of the new charge. We noted seven instances of 45 cost transfers selected where the reason for the transfer was not adequately documented. The awards affected are: NSF, DEB-0080592; NIH-NHLBI, 5 P50 HL61036-03; NIH-NIMH, 5 R01 MH50647-09; NIH-NIGMS, 5 R01 GM48027-09; NIH-NIGMS, 5 R01 GM23928-24; NIH-NIGMS, 2 R01 GM39023-15; NIH-NCI, 5 F32 CA72203-03. To identify cost transfers, the University encourages a standard naming convention, but adherence is not uniform. Because of this, it is difficult to identify cost transfers completely and to monitor compliance with the University's cost transfer policies. Recommendation: We recommend the University develop a process to more completely monitor cost transfers. Explanations for cost transfers should be clearly documented on cost transfer forms or journal vouchers, as appropriate, to ensure adequate justification for the transfer. 01-3 Equipment and Real Property Management Circular A-110, Subpart C, paragraph 34 outlines equipment standards for equipment acquired by a recipient with Federal funds. 34(f)(1) requires that equipment records be maintained accurately, including information concerning the ultimate disposition of the equipment. 34(f)(3) requires that differences between the physical inventory and the accounting records be investigated to determine the causes of the difference, and that, in connection with the inventory, the recipient verify the existence and current utilization of the equipment. 34(f)(4) requires that a control system be in effect to insure adequate safeguards to prevent loss, damage, or theft of the equipment. During our testing of the physical inventory, we noted three exceptions of 57 items selected. Two of these items were listed on the inventory listing, but the identifying tag was missing from the equipment. One item was listed on the inventory listing, but had been disposed of. Recommendation: We recommend the University improve communication between the departments and the equipment management office in order to improve the accuracy of its equipment records.

Harvard University Schedule of Findings and Questioned Costs For the Years Ended June 30, 2001

01-4 Effort Reporting OMB Circular A-21, J.8 requires at least an annual certification under the plan confirmation method, and at least monthly activity reports under the after-the-fact activity method. Section J.8.c.2.e requires that the after-the-fact reports be signed by the employee, principal investigator, or responsible official using suitable means of verification that the work was performed. The University primarily uses the plan confirmation method for faculty and the after-the-fact activity method for other staff. We tested 45 effort reports for timely completion and proper certification and submission. Of our sample, we noted 10 effort reports were not dated, and 18 reports were submitted between 13 and 204 days after the deadline. We noted that the lab administrator for one award, and not the principal investigator, signed the monthly effort certification forms. We also noted the payroll charges and effort report for one employee were not confirmed orally. The employee on the effort report represented to us in an interview that the actual effort on the award was 5% - 10% less than as certified by the responsible official. Recommendation: The University should ensure that effort certifications are completed in accordance with federal and University policies in a timely manner. In addition, the University should ensure that individuals responsible for signing demonstrate first-hand knowledge of the research being performed. 01-5 Reporting Circular A-110 Section 51 requires that annual reports shall be due 90 calendar days after the grant year; quarterly or semiannual reports shall be due 30 days after the reporting period. Additionally, certain awards require programs reports be submitted at various intervals. In testing the completion of 15 progress reports, we noted one that was not submitted timely as specified in the terms and conditions of the award (NIH-NIAID award 5 R01 A132475-09). Section 52 requires that the Financial Status Report for each project or program be submitted no less frequently than annually, and the awarding agency will determine the frequency of the report. In examining 35 awards for which an annual or final financial report was required, we noted 17 that were not submitted within the terms specified by the grantor agency. Of those, seven were submitted within one month of the due date, four were submitted within three months of the due date, and six were submitted after three months of the due date. Recommendation: We recommend the University strengthen controls for monitoring due dates of both technical and financial reports and ensure that they are filed in a timely manner.

Harvard University Schedule of Findings and Questioned Costs For the Years Ended June 30, 2001

01-6 Subrecipient Monitoring OMB Circular A-133 Compliance Supplement Part 3M requires a pass-through entity to monitor a subrecipient’s activities to provide reasonable assurance that the subrecipient administers Federal awards in compliance with Federal requirements. The departments conduct various levels of subrecipient monitoring, although no formal University-wide subrecipient monitoring policy exists. Monitoring procedures for subrecipients that are foreign entities are not well established. Additionally, while the University does request copies of the A-133 reports from the subrecipients for whom the reports are required, there is insufficient monitoring of the results of those reports. For those domestic subrecipients for whom an A-133 audit is not required, only audited financial statements are received, which is not an adequate monitoring procedure. Recommendation: The University should institute subrecipient monitoring policies and procedures which encompass monitoring compliance with Federal regulations by subrecipients, including those from whom an A-133 audit is not required. 01-7 Incorrect Cost of Attendance The OMB Circular A133 Compliance Supplement Part 5.N “Coordination of Student Aid Programs” requires the institution to ensure that it uses all information in its possession to evaluate a student’s Title IV eligibility. It was noted during testing of 37 students receiving student financial aid that two individuals were awarded aid based on incorrect calculations of cost of attendance. As a result, one student was under-awarded by $20, and the other was under-awarded by $500. Recommendation: The University should closely monitor the calculation of cost of attendance in connection with awarding Federal monies, to ensure that aid is calculated and awarded correctly. 01-8 Change of Documentation The OMB Circular A133 Compliance Supplement Part 5.N “Coordination of Student Aid Programs” requires that when a student financial aid officer makes changes in a student’s cost of attendance, the change be properly documented. In testing of 37 students receiving student financial aid, we noted insufficient documentation supporting changes in the calculation of students’ awards in three instances. Recommendation: When making changes with professional judgment, the financial aid administrators should take care to maintain the proper supporting documentation in the student’s file. Additionally, the University should consider offering periodic training to student financial aid officers on the documentation necessary to support changes based on professional judgment.

00-1 Cost Transfers – prior year reportable condition The University allowed a grace period whereby documentation requirements for certain cost transfers were waived. Status: Addressed within Corrective Action Plan to current year’s finding 01-2. 00-2 Effort Reporting – prior year reportable condition The University suspended monthly effort reporting requirements for the period July 1, 1999 to March 31, 2000. Status: Addressed within Corrective Action Plan to current year’s finding 01-4. 00-3 Internal Controls Regarding Payables – prior year reportable condition The designed controls over the purchase-to-pay activities and the lack of segregation of duties for purchases less than $50,000 did not effectively mitigate the risks of the creation of fictitious suppliers, unauthorized purchases, unrecorded liabilities, and duplicate payments. Status: The Web Voucher System was adjusted in fiscal year 2001 to not allow purchases in excess of $5,000 to be prepared and approved by the same individual. A report is distributed to financial deans when this occurs for purchases less than $5,000. 00-4 Allowable Costs/Cost Principles 11 out of 120 direct costs were identified as questioned costs. Status: All of the 11 questioned costs noted above were removed from the federal awards. 00-5 Reporting 35 awards were examined for timely completion and submission of financial status reports, and 15 performance reports were tested for timely completion and submission. There were 17 instances where financial status reports were not submitted within the terms specified by the grantor agency, and there was one instance where a performance report was not submitted timely as specified in the terms and conditions of the award. In addition, six semi-annual reports that chart progress in meeting subcontracting plan goals were tested, five were submitted late. Status: Addressed within Corrective Action Plan to current year’s finding 01-5.

00-6 Subrecipient Monitoring Monitoring procedures for subrecipients that are foreign entities are not well established, and only audited financial statements are received for those domestic subrecipients for whom an A-133 audit is not required. Status: Addressed within Corrective Action Plan to current year’s finding 01-6. 00-7 Equipment and Real Property Management Four exceptions out of 57 items tested were found. The University did not investigate differences between the physical inventory and the equipment management system in a timely manner. Status: These exceptions were investigated and reconciled upon identification in the A-133. 00-8 Service Centers/Recharge Centers For the service center tested, we noted that there was not an adequate basis for the determination of rates based on costs charged to users. Status: The office of Sponsored Research has been actively engaged with service center personnel to ensure that rates are timely and accurate. 00-9 Over-awards of Student Financial Aid Of 36 undergraduate and graduate students tested, one student was awarded student financial aid in an amount greater than his/her cost of attendance. Status: The College established a reconciliation process for all funds including Outside Awards (with Student Receivables) and FWSP earnings (with Student Employment Office). The reconciling uses the University's ADAPT accounting system and has been in place for well over a year, enabling the College to identify, and resolve if necessary, funds received from all sources which do not necessarily arrive first to the Financial Aid Office for approval. 00-10 Work-study Timecards During testing of 13 timecards for college work study, we noted one instance where the timecard was not signed by a responsible individual. Status: Additional outreach and communication from the Student Employment Office has reduced the incidence of missing signatures on timecards. In FY01, all timecard reviewed were signed, appropriately.