republic of indonesia - djppr.kemenkeu.go.id · this presentation may not be reproduced, ......

TRANSCRIPT

Republic of Indonesia

2018 Investor Update

Stability at the Forefront with Unwavering

Reforms Commitment

June 2018

2

This presentation has been prepared by the Republic of Indonesia (the “Republic”). This presentation is being presented solely for your

information and is subject to change without notice. By accessing this presentation, you are agreeing to be bound by the restrictions set out

below. Any failure to comply with these restrictions may constitute a violation of applicable securities laws.

This presentation contains forward-looking statements that involve risks and uncertainties. All statements other than statements of historical

facts are forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors that may cause the

actual results, performance or achievements of the Republic to be materially different from those expressed or implied by the forward-looking

statements.

The Republic has filed a registration statement (including the prospectus) with the U.S. Securities and Exchange Commission (the “SEC”). You

should read the prospectus in that registration statement (file no. -223441), any prospectus supplement and other documents that the Republic

has filed with the SEC for more complete information about the Republic. A copy of the prospectus can be obtained for free by visiting EDGAR

on the SEC web site at www.sec.gov, from Deutsche Bank Securities Inc. at 60 Wall Street, New York, NY 10005, USA, Attention: Prospectus

Group, by calling 1-800-503-4611, or by emailing [email protected].

A prospectus of the Republic, dated March 16, 2018, is available from the SEC website at

https://www.sec.gov/Archives/edgar/data/1719614/000119312518070289/d714087dsb.htm

This presentation may not be reproduced, disseminated or quoted without the prior written consent of the Republic.

Disclaimer

3

Outline

Recent Macroeconomic Development2

3 Financial Market Condition

2018 State Budget Realization Performance4

5 Fiscal Incentive to Support Investment and Export

6 Medium Term Fiscal Objectives & 2019 Macro-Fiscal Framework

7 Monetary Policy and Banking Sector

Executive Summary1

8 Debt Management and Budget Financing

Executive Summary

01Widi Island in North Maluku,

Indonesia

5

Executive SummaryIndonesia in Snapshot

…. with more potential to come

One of the Best GDP

Growth Performer

Infrastructure Development Acceleration

Strategic national projects supported by budget

and non-budget financing (private sector)

Strong GDP Growth

Supported by robust domestic activity and

increasing role of investment

Credit Rating Improvement

International recognition from global rating agencies

Reform on the Move

1. Taxation

2. Investment Regulation

3. Bureaucratic

…. Fiscal, monetary and Real sector

Continuous Reform

Prudent Debt Management

Maintain productive use of public debt….followed by International Recognitions

Credible Policy Framework

….improving creditworthiness

Preserved Fiscal Prudence

6

Indonesia’s GDP Growth Has Been RobustConsumption and investment remain as the main engines of growth

GDP breakdown by expenditure

(%, YoY)

2016 2017 2018

Q1 Q2 Q3 Q4 Y Q1 Q2 Q3 Q4 Y Q1

Household Consumption 4.98 5.10 5.04 5.03 5.04 5.00 5.02 4.95 4.98 4.98 5.01

Government Consumption 3.43 6.21 (2.95) (4.03) (0.14) 2.69 (1.92) 3.48 3.81 2.14 2.73

Gross Fixed Capital Formation 4.67 4.18 4.24 4.79 4.47 4.77 5.34 7.08 7.27 6.15 7.95

Export (3.10) (1.50) (5.75) 4.15 (1.57) 8.41 2.80 17.01 8.50 9.09 6.17

Import (5.04) (3.47) (4.13) 2.72 (2.45) 4.81 0.20 15.46 11.81 8.06 12.75

GDP 4.94 5.21 5.03 4.94 5.03 5.01 5.01 5.06 5.19 5.07 5.06

7.2 7.1

6.0

5.1

3.0 2.5 2.4 2.3 2.2 2.2 2.1

1.7 1.5 1.3 1.1 0.7

0.3 0.3

(0.5)

India

Ch

ina

Turk

ey

Indon

esia

Kore

a

Me

xic

o

Austr

alia

Saud

i A

rabia

Un

ite

d K

ing

dom

Un

ite

d S

tate

s

Ca

nad

a

Germ

any

South

Afr

ica

Japa

n

Fra

nce

Arg

entina

Ita

ly

Ru

ssia

Bra

zil

Avg. GDP Growth 5 Years Std. Dev. GDP Growth 5 Years

Institutions2018 GDP Growth

Projection

Government of Indonesia (2018 Budget) 5.4%

IMF (WEO Apr 2018) 5.3%

World Bank (IEQ June 2018) 5.2%

ADB (ADO Apr 2018) 5.3%

S&P (May 2018) 5.3%

Fitch (Dec 2017) 5.4%

Domestic and foreign direct investment have

been picking up thanks to the acceleration of

infrastructure spending.

International trade is rebounding and supporting

growth, partly attributed to the increase of

commodity prices, but also signals that global

demand improves.

Indonesia’s growth is still stable and higher than

most of its G20 peers

Medium term growth is well maintained through

improving investment climate and fiscal incentive

Indonesia GDP ProjectionGDP Growth Comparison Amongst G-20 Countries

7

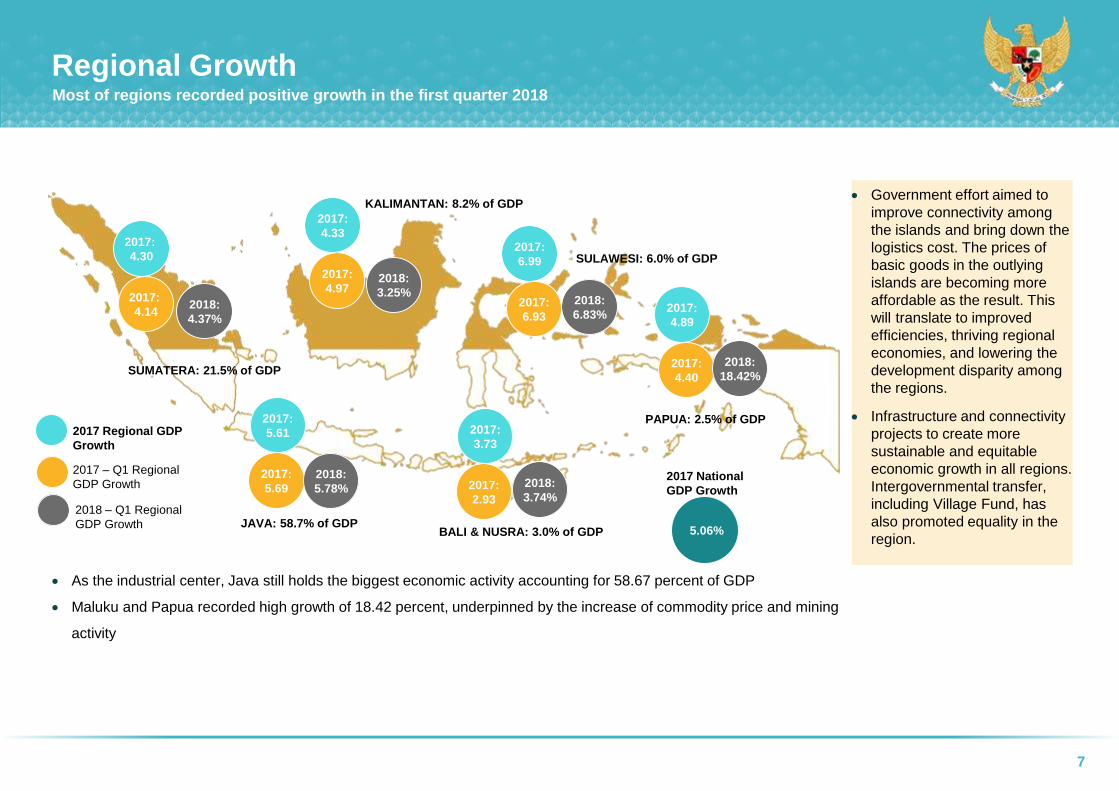

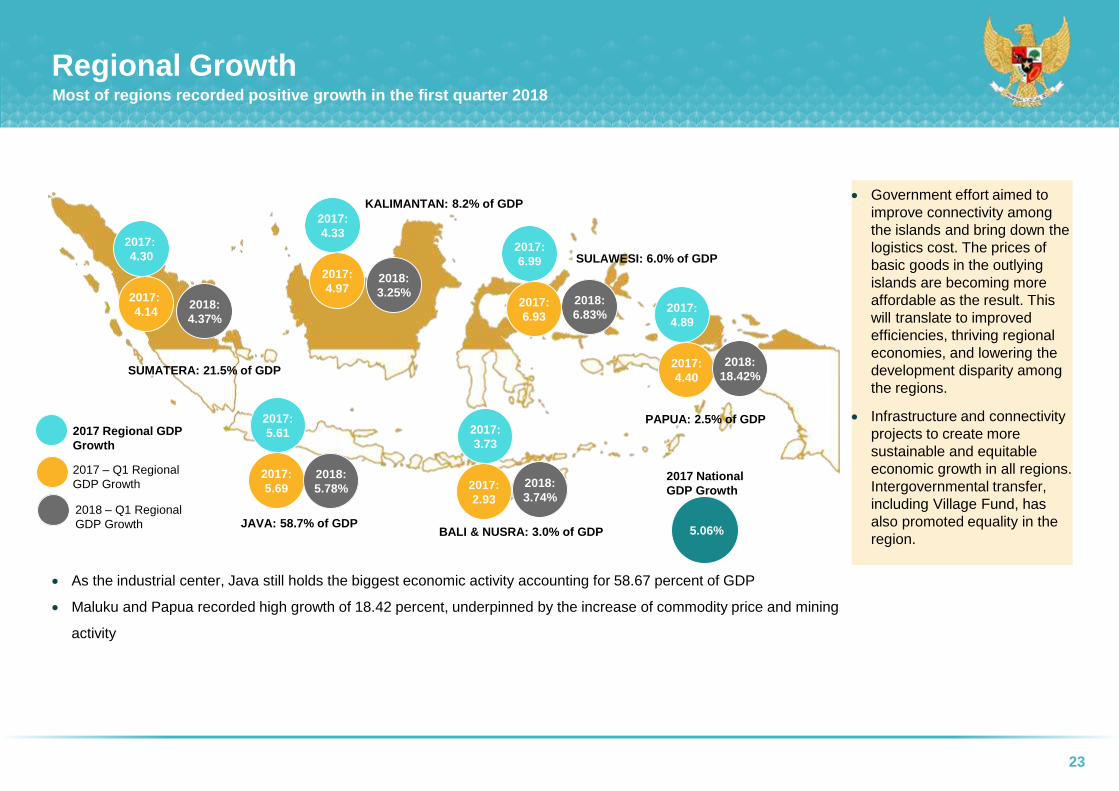

Regional GrowthMost of regions recorded positive growth in the first quarter 2018

5.06%

2017 National

GDP Growth

SUMATERA: 21.5% of GDP

2018:

4.37%

2017:

4.14

2017:

5.69

2018:

5.78%

2018:

3.25%

2017:

4.972018:

6.83%2017:

6.93

2018:

3.74%2017:

2.93

2017:

4.40

JAVA: 58.7% of GDP

KALIMANTAN: 8.2% of GDP

SULAWESI: 6.0% of GDP

PAPUA: 2.5% of GDP

BALI & NUSRA: 3.0% of GDP

2018:

18.42%

As the industrial center, Java still holds the biggest economic activity accounting for 58.67 percent of GDP

Maluku and Papua recorded high growth of 18.42 percent, underpinned by the increase of commodity price and mining

activity

2017:

4.30

2017:

5.61

2017:

4.332017:

6.99

2017:

3.73

2017:

4.89

2017 Regional GDP

Growth

2017 – Q1 Regional

GDP Growth

2018 – Q1 Regional

GDP Growth

Government effort aimed to

improve connectivity among

the islands and bring down the

logistics cost. The prices of

basic goods in the outlying

islands are becoming more

affordable as the result. This

will translate to improved

efficiencies, thriving regional

economies, and lowering the

development disparity among

the regions.

Infrastructure and connectivity

projects to create more

sustainable and equitable

economic growth in all regions.

Intergovernmental transfer,

including Village Fund, has

also promoted equality in the

region.

8

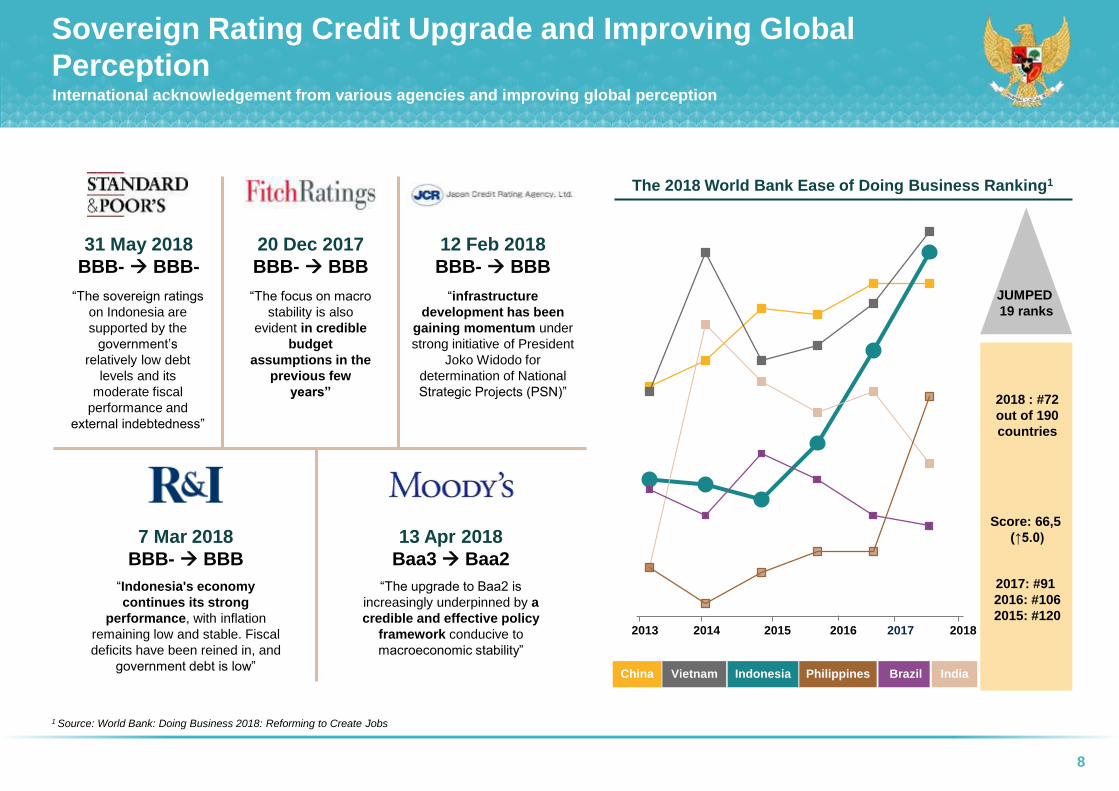

Sovereign Rating Credit Upgrade and Improving Global

PerceptionInternational acknowledgement from various agencies and improving global perception

1 Source: World Bank: Doing Business 2018: Reforming to Create Jobs

The 2018 World Bank Ease of Doing Business Ranking1

JUMPED

19 ranks

2017: #91

2016: #106

2015: #120

2018 : #72

out of 190

countries

Score: 66,5

(↑5.0)

China Vietnam Indonesia Philippines Brazil India

2013 2014 2015 2016 2017 2018

31 May 2018

BBB- BBB-

20 Dec 2017

BBB- BBB

12 Feb 2018

BBB- BBB

7 Mar 2018

BBB- BBB

13 Apr 2018

Baa3 Baa2

“The upgrade to Baa2 is

increasingly underpinned by a

credible and effective policy

framework conducive to

macroeconomic stability”

“The sovereign ratings

on Indonesia are

supported by the

government’s

relatively low debt

levels and its

moderate fiscal

performance and

external indebtedness”

“The focus on macro

stability is also

evident in credible

budget

assumptions in the

previous few

years”

“infrastructure

development has been

gaining momentum under

strong initiative of President

Joko Widodo for

determination of National

Strategic Projects (PSN)”

“Indonesia's economy

continues its strong

performance, with inflation

remaining low and stable. Fiscal

deficits have been reined in, and

government debt is low”

9

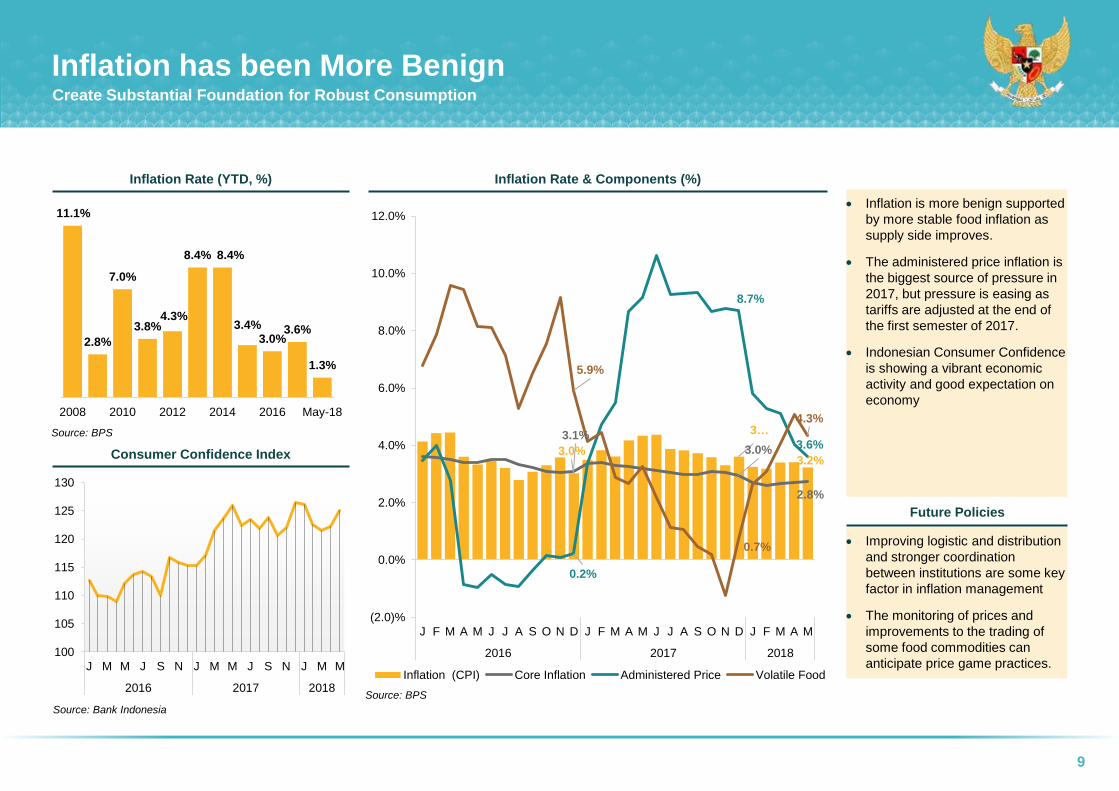

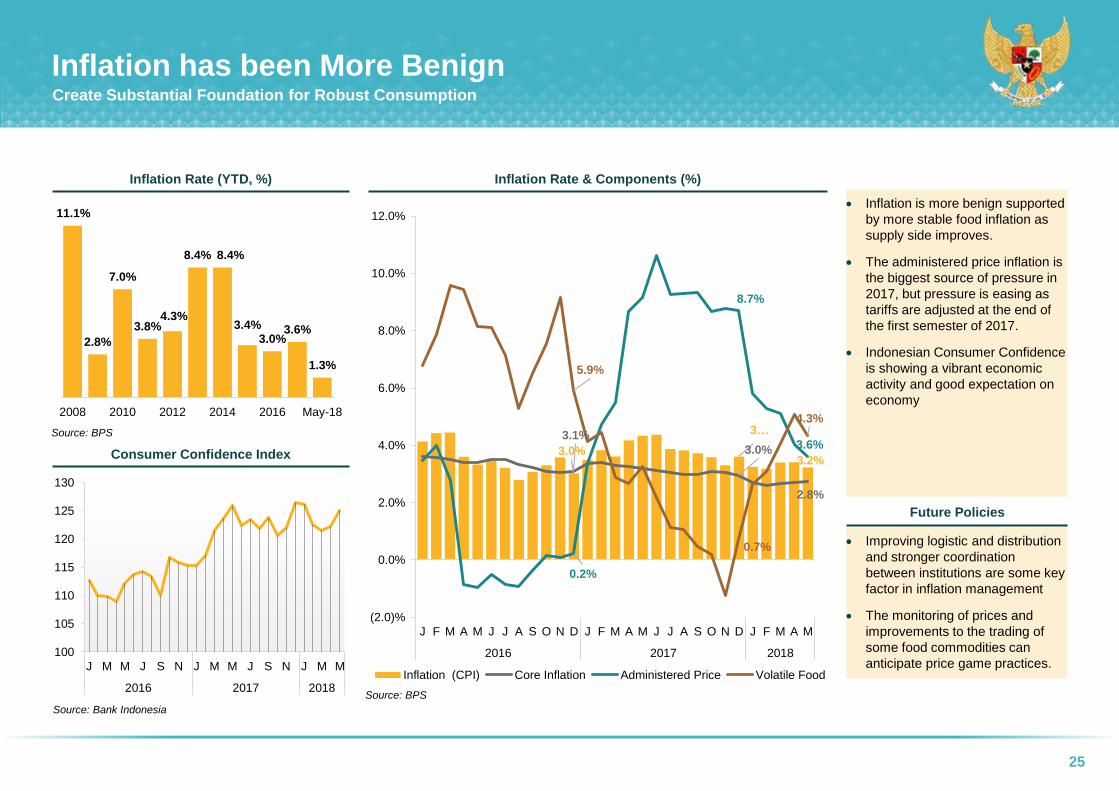

Inflation has been More BenignCreate Substantial Foundation for Robust Consumption

Inflation Rate & Components (%)Inflation Rate (YTD, %)

3.0%

3…

3.2%

3.1%

3.0%

2.8%

0.2%

8.7%

3.6%

5.9%

0.7%

4.3%

(2.0)%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M

2016 2017 2018

Inflation (CPI) Core Inflation Administered Price Volatile Food

Future Policies

Improving logistic and distribution

and stronger coordination

between institutions are some key

factor in inflation management

The monitoring of prices and

improvements to the trading of

some food commodities can

anticipate price game practices.

Inflation is more benign supported

by more stable food inflation as

supply side improves.

The administered price inflation is

the biggest source of pressure in

2017, but pressure is easing as

tariffs are adjusted at the end of

the first semester of 2017.

Indonesian Consumer Confidence

is showing a vibrant economic

activity and good expectation on

economy

Consumer Confidence Index

Source: Bank Indonesia

100

105

110

115

120

125

130

J M M J S N J M M J S N J M M

2016 2017 2018

11.1%

2.8%

7.0%

3.8%4.3%

8.4% 8.4%

3.4%3.0%

3.6%

1.3%

2008 2010 2012 2014 2016 May-18

Source: BPS

Source: BPS

10

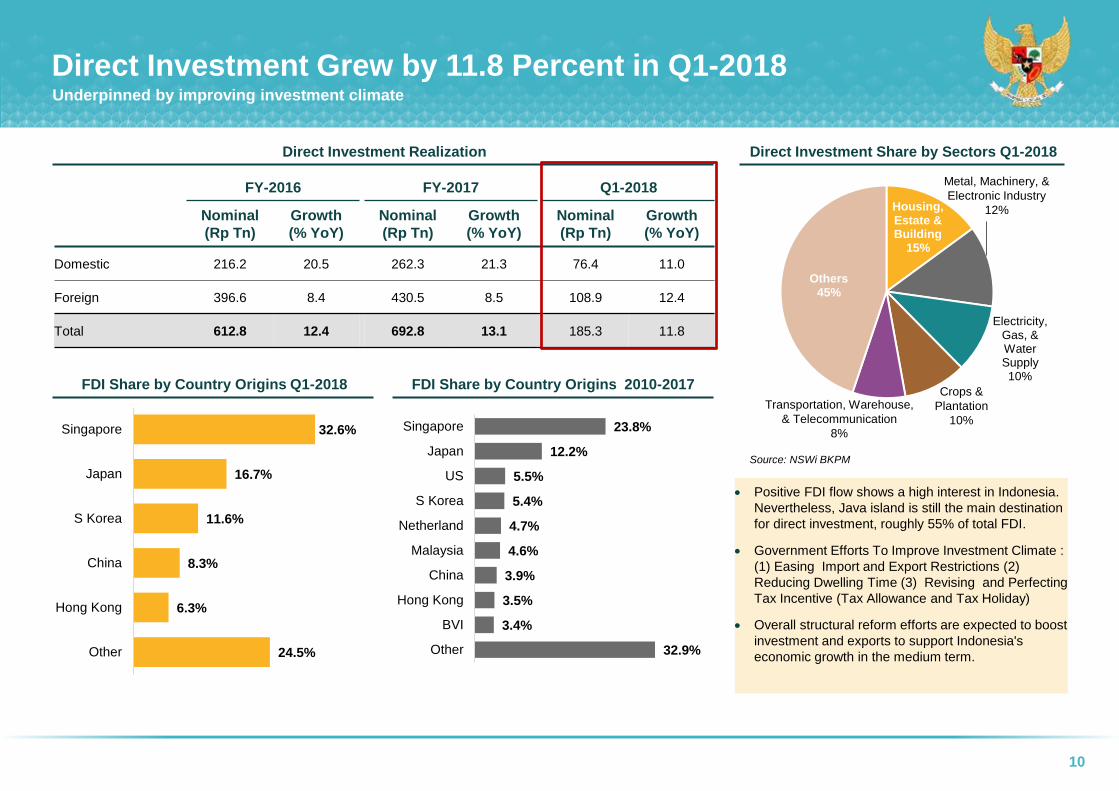

Direct Investment Grew by 11.8 Percent in Q1-2018Underpinned by improving investment climate

Direct Investment Share by Sectors Q1-2018Direct Investment Realization

FY-2016 FY-2017 Q1-2018

Nominal

(Rp Tn)

Growth

(% YoY)

Nominal

(Rp Tn)

Growth

(% YoY)

Nominal

(Rp Tn)

Growth

(% YoY)

Domestic 216.2 20.5 262.3 21.3 76.4 11.0

Foreign 396.6 8.4 430.5 8.5 108.9 12.4

Total 612.8 12.4 692.8 13.1 185.3 11.8

FDI Share by Country Origins Q1-2018 FDI Share by Country Origins 2010-2017

32.6%

16.7%

11.6%

8.3%

6.3%

24.5%

Singapore

Japan

S Korea

China

Hong Kong

Other

23.8%

12.2%

5.5%

5.4%

4.7%

4.6%

3.9%

3.5%

3.4%

32.9%

Singapore

Japan

US

S Korea

Netherland

Malaysia

China

Hong Kong

BVI

Other

Housing, Estate & Building

15%

Electricity, Gas, & Water Supply10%

Others45%

Metal, Machinery, &

Electronic Industry

12%

Transportation, Warehouse,

& Telecommunication

8%

Crops &

Plantation

10%

Source: NSWi BKPM

Positive FDI flow shows a high interest in Indonesia.

Nevertheless, Java island is still the main destination

for direct investment, roughly 55% of total FDI.

Government Efforts To Improve Investment Climate :

(1) Easing Import and Export Restrictions (2)

Reducing Dwelling Time (3) Revising and Perfecting

Tax Incentive (Tax Allowance and Tax Holiday)

Overall structural reform efforts are expected to boost

investment and exports to support Indonesia's

economic growth in the medium term.

11

(2.0)

(1.0)

0.0

1.0

2.0

3.0

M J J A S O N D

201

7-J F M A M J J A S O N D

201

8-J F M A

Non O&G O&G Total

Import Growth Upholds Increasing Domestic Economic

ActivitiesUntil April 2018, Trade Balance is Recording a Deficit of USD1.31 billion

Source: BPS

Cumulative Growth of Export CommodityTrade Balance (USD Billion)

Trade balance is recording deficit

cumulatively in April 2018, due to

high import growth that supports

growing domestic production

Import grew by 23.65% (YTD)

supported by higher demand for

festive seasons of Ramadhan and

Idul Fitri; capital good increase to

support infrastructure development

and military equipment; and raw

material increase that highlights

improving domestic productivity and

economic activity

Export grew by 8.77% (YTD),

underpinned by mining commodity

growth of 33.4% and manufacturing

of 5.3%

Deficit Jan-Apr

2018:

USD1.31 billion

Surplus FY 2016:

USD9.5 billion

Surplus FY 2017:

USD11.8 billion

Cumulative Growth of Import Goods

Contribution to

Total Import

Capital Goods

16.3%

Consumption

Goods 9.1%

Raw Materials

74.6%

Top 4 Export/Import (Non-O&G) by Country

April 2018 (USD Billion)

Export (Non O&G) Import (Non O&G)

China 3.4

Japan 1.6

United States 1.0

Thailand 0.9

1

2

3

4

China 1.8

United States 1.4

Japan 1.4

India 1.0

1

2

3

4

26.1%

21.9%

31.0%

(30.0)%

(10.0)%

10.0%

30.0%

50.0%

M J S N

201

7-J M M J S N

201

8-J M

Consumption goods Raw materials Capital goods

(5.1)%

5.3%

33.4%

4.0%

(60.0)%

(40.0)%

(20.0)%

0.0%

20.0%

40.0%

60.0%

M J J A S O N D

201

7-J F M A M J J A S O N D

201

8-J F M A

Agriculture Manufacturing Mining O&G

12

Macroeconomic Indicators Remain Strong

1 Q1 figures.2 As of April.

Indicators

2016 2017 2018 2019

Revised

Budget

(APBN-P)

Realized

31 May APBN

Realized

31 May

Budget

(APBN)

Realized

31 May

Submitted

to

Parliament

Economic growth (%, yoy) 5.2 4.941

5.2 5.011 5.4 5.061 5.4 – 5.8

Inflation (%, yoy) 4.0 3.3 4.3 4.3 3.5 3.2 2.5 – 4.5

3-Month Treasury Bill

(SPN) (%)5.5 5.8 5.2 5.1 5.2 4.2 4.6 – 5.2

Exchange Rate

(Average, IDR/USD)13,500 13,435 13,400 13,336 13,400 13,714

13,700 –

14,000

ICP (USD/barrel) 40 34 48 50 48 64 60 – 70

Oil Production

(thousands of barrel/day)820 805 815 784 800 7422 722 – 805

Gas Production

(millions of barrels/day)1.15 1.18 1.15 1.14 1.20 1.142 1.21 – 1.30

Indonesia has been able to

maintain robust economic

performance which expected to

continue in 2018 and 2019.

Inflation is benign supported by

improving logistic and

infrastructure acceleration

Interest rate and exchange rate

are stable, benefiting from strong

fundamental and positive investor

perception in the midst of

uncertain global condition.

Increasing commodity price

helped in boosting external

position and revenue.

Indonesia's economy is currently

in the process of transitioning.

However, Indonesia economy

cannot be separated from

external conditions (technology,

trade, and geopolitics) as well as

domestic challenges.

13

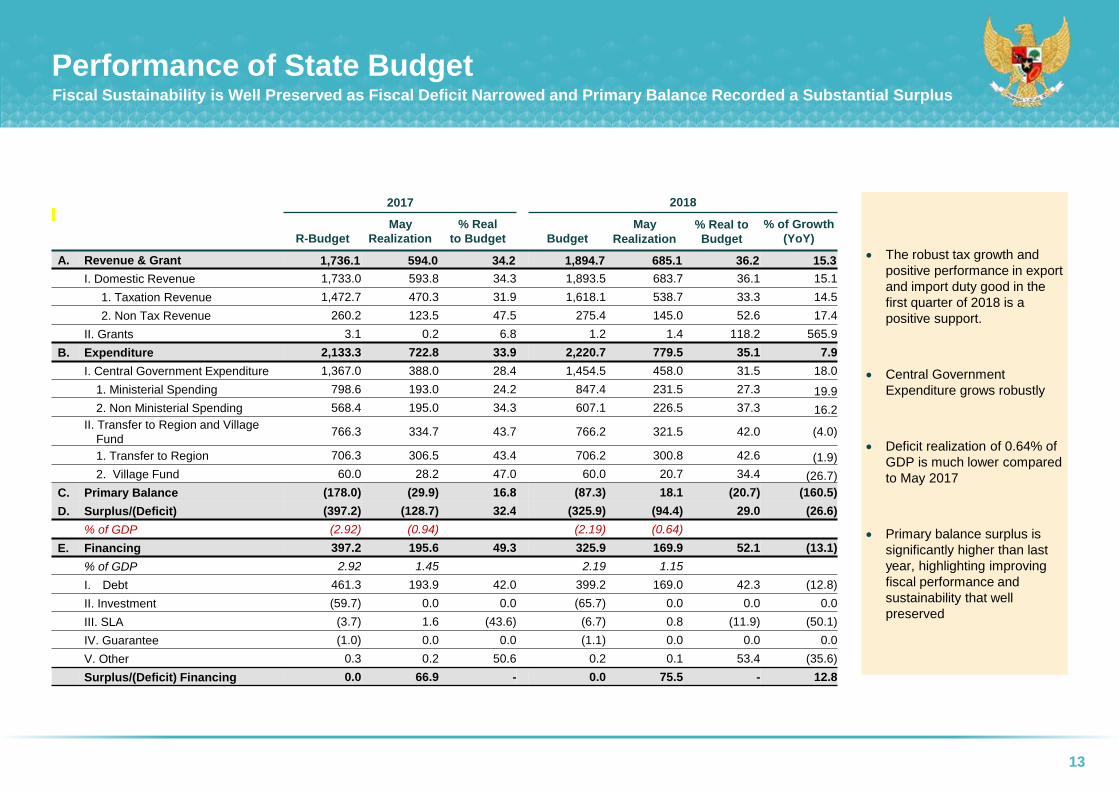

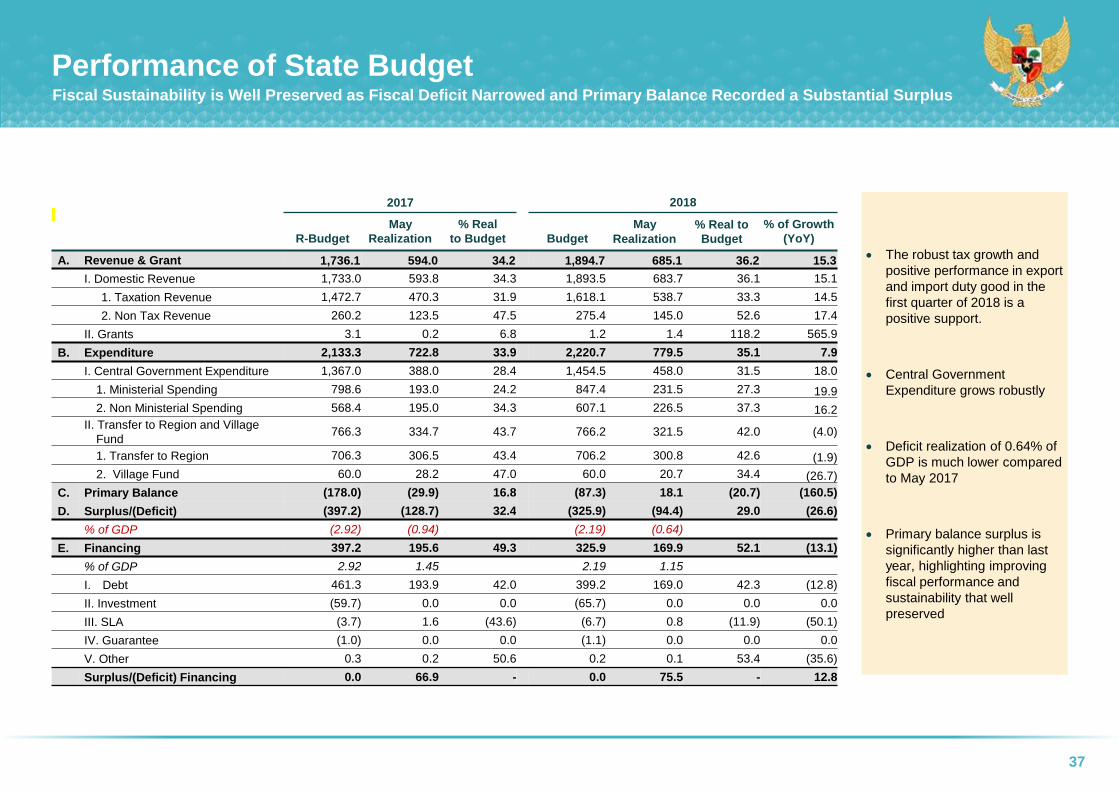

Performance of State BudgetFiscal Sustainability is Well Preserved as Fiscal Deficit Narrowed and Primary Balance Recorded a Substantial Surplus

The robust tax growth and

positive performance in export

and import duty good in the

first quarter of 2018 is a

positive support.

Central Government

Expenditure grows robustly

Deficit realization of 0.64% of

GDP is much lower compared

to May 2017

Primary balance surplus is

significantly higher than last

year, highlighting improving

fiscal performance and

sustainability that well

preserved

2017 2018

R-Budget

May

Realization

% Real

to Budget Budget

May

Realization

% Real to

Budget

% of Growth

(YoY)

A. Revenue & Grant 1,736.1 594.0 34.2 1,894.7 685.1 36.2 15.3

I. Domestic Revenue 1,733.0 593.8 34.3 1,893.5 683.7 36.1 15.1

1. Taxation Revenue 1,472.7 470.3 31.9 1,618.1 538.7 33.3 14.5

2. Non Tax Revenue 260.2 123.5 47.5 275.4 145.0 52.6 17.4

II. Grants 3.1 0.2 6.8 1.2 1.4 118.2 565.9

B. Expenditure 2,133.3 722.8 33.9 2,220.7 779.5 35.1 7.9

I. Central Government Expenditure 1,367.0 388.0 28.4 1,454.5 458.0 31.5 18.0

1. Ministerial Spending 798.6 193.0 24.2 847.4 231.5 27.3 19.9

2. Non Ministerial Spending 568.4 195.0 34.3 607.1 226.5 37.3 16.2

II. Transfer to Region and Village

Fund766.3 334.7 43.7 766.2 321.5 42.0 (4.0)

1. Transfer to Region 706.3 306.5 43.4 706.2 300.8 42.6 (1.9)

2. Village Fund 60.0 28.2 47.0 60.0 20.7 34.4 (26.7)

C. Primary Balance (178.0) (29.9) 16.8 (87.3) 18.1 (20.7) (160.5)

D. Surplus/(Deficit) (397.2) (128.7) 32.4 (325.9) (94.4) 29.0 (26.6)

% of GDP (2.92) (0.94) (2.19) (0.64)

E. Financing 397.2 195.6 49.3 325.9 169.9 52.1 (13.1)

% of GDP 2.92 1.45 2.19 1.15

I. Debt 461.3 193.9 42.0 399.2 169.0 42.3 (12.8)

II. Investment (59.7) 0.0 0.0 (65.7) 0.0 0.0 0.0

III. SLA (3.7) 1.6 (43.6) (6.7) 0.8 (11.9) (50.1)

IV. Guarantee (1.0) 0.0 0.0 (1.1) 0.0 0.0 0.0

V. Other 0.3 0.2 50.6 0.2 0.1 53.4 (35.6)

Surplus/(Deficit) Financing 0.0 66.9 - 0.0 75.5 - 12.8

14

(0.33)

(0.85)

(1.19)

(1.67)

(1.76)

(1.91)

(2.08)

(2.75)

(3.48)

(3.90)

(6.26)

(8.43)

(1.50)

(0.85)

(1.22)

0.13

(1.02)

(1.41)

(1.46)

(1.11)

(1.12)

(3.57)

(5.84)

(10.15)

(12.00) (10.00) (8.00) (6.00) (4.00) (2.00) 0.00 2.00

PHP

KRW

CNY

IDR

SGD

MYR

THB

INR

ZAR

EUR

BRL

TRY

May vs April 2018

Point to Point Average

Source: BPS, Bank Indonesia

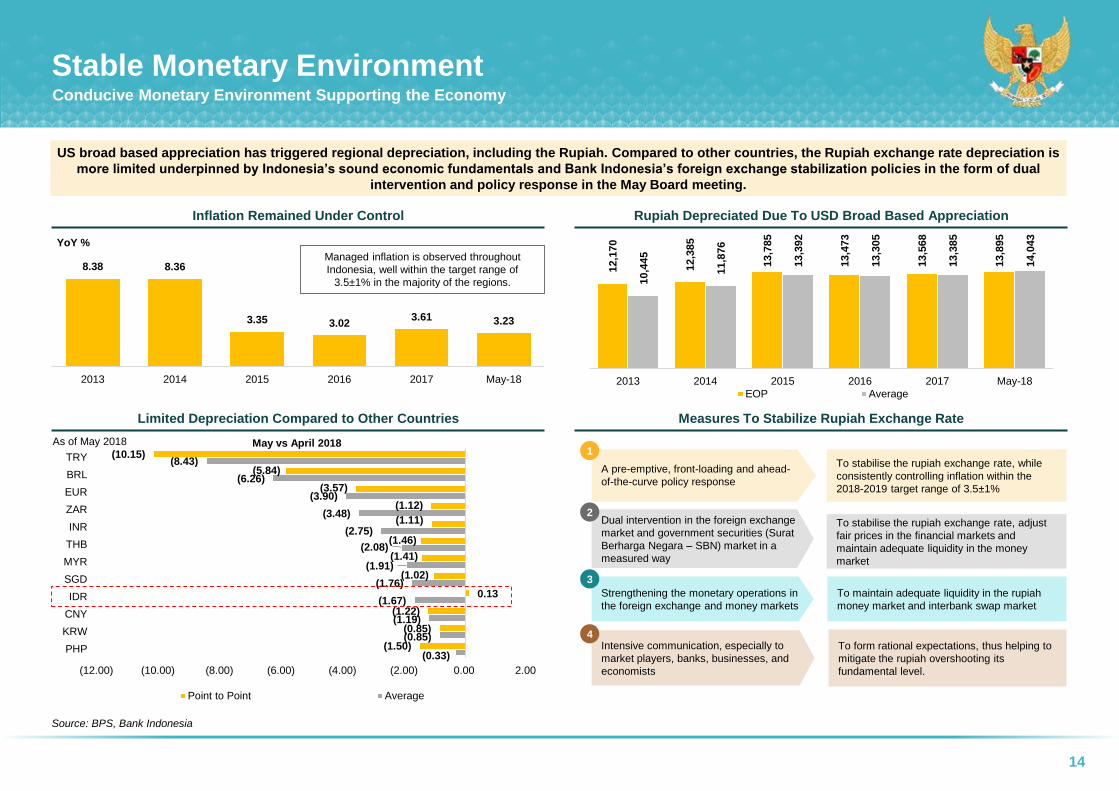

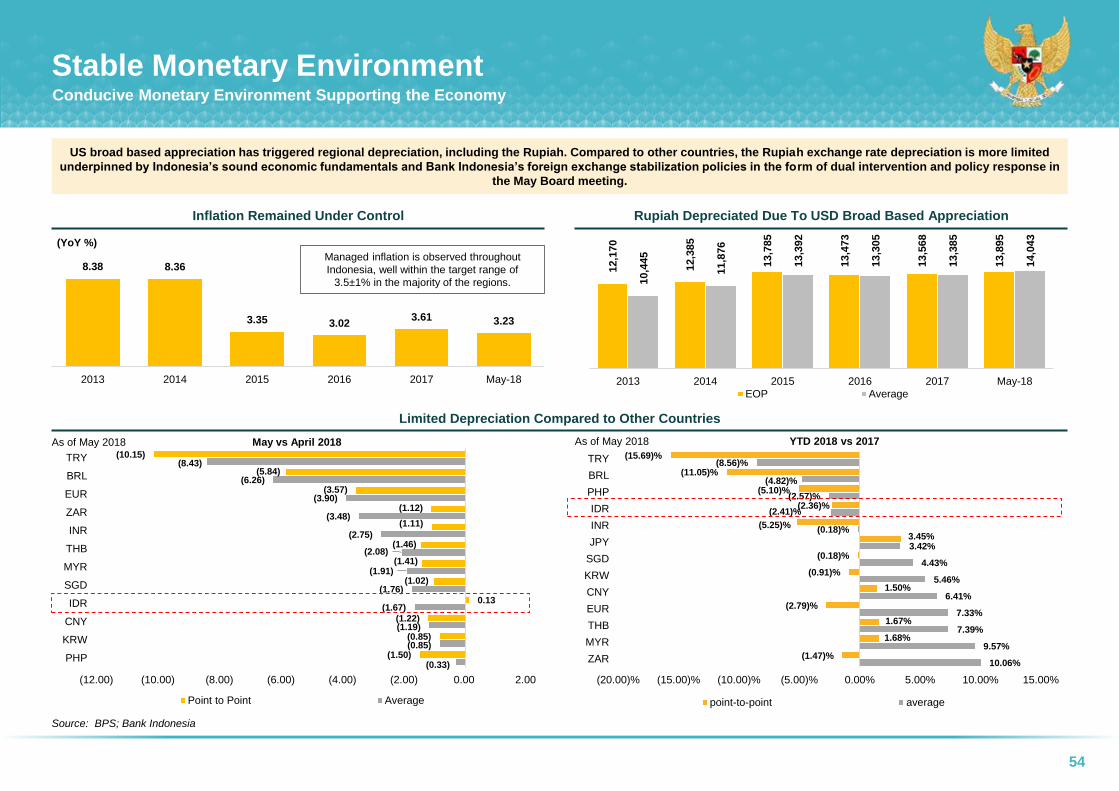

Stable Monetary EnvironmentConducive Monetary Environment Supporting the Economy

8.38 8.36

3.35 3.023.61 3.23

2013 2014 2015 2016 2017 May-18

YoY %

12,1

70

12,3

85

13,7

85

13,4

73

13,5

68

13,8

95

10,4

45

11,8

76

13,3

92

13,3

05

13,3

85

14,0

43

2013 2014 2015 2016 2017 May-18

EOP Average

US broad based appreciation has triggered regional depreciation, including the Rupiah. Compared to other countries, the Rupiah exchange rate depreciation is

more limited underpinned by Indonesia’s sound economic fundamentals and Bank Indonesia’s foreign exchange stabilization policies in the form of dual

intervention and policy response in the May Board meeting.

Managed inflation is observed throughout

Indonesia, well within the target range of

3.5±1% in the majority of the regions.

Rupiah Depreciated Due To USD Broad Based AppreciationInflation Remained Under Control

Measures To Stabilize Rupiah Exchange RateLimited Depreciation Compared to Other Countries

As of May 2018

A pre-emptive, front-loading and ahead-

of-the-curve policy response

Strengthening the monetary operations in

the foreign exchange and money markets

To stabilise the rupiah exchange rate, while

consistently controlling inflation within the

2018-2019 target range of 3.5±1%

To stabilise the rupiah exchange rate, adjust

fair prices in the financial markets and

maintain adequate liquidity in the money

market

To maintain adequate liquidity in the rupiah

money market and interbank swap market

To form rational expectations, thus helping to

mitigate the rupiah overshooting its

fundamental level.

Dual intervention in the foreign exchange

market and government securities (Surat

Berharga Negara – SBN) market in a

measured way

Intensive communication, especially to

market players, banks, businesses, and

economists

3

2

1

4

15

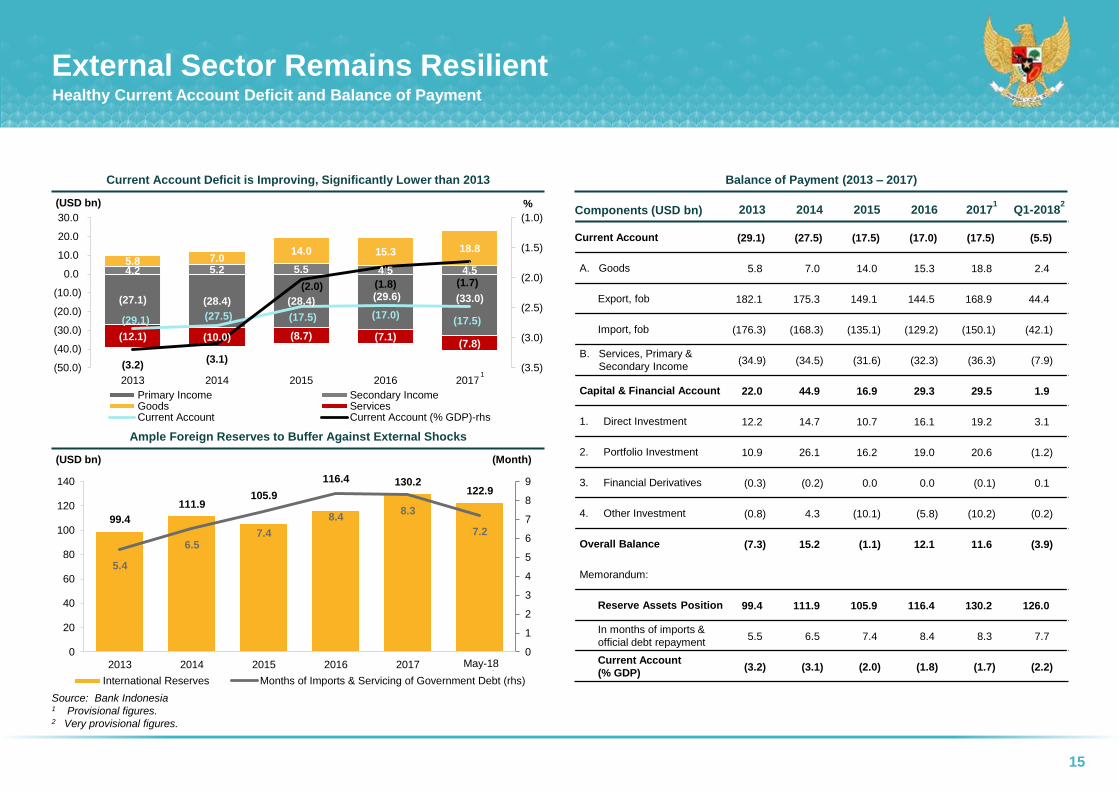

(27.1) (28.4) (28.4) (29.6) (33.0)

4.2 5.2 5.5 4.5 4.55.8 7.0

14.0 15.3 18.8

(12.1) (10.0) (8.7) (7.1)(7.8)

(29.1) (27.5) (17.5) (17.0)(17.5)

(3.2)(3.1)

(2.0) (1.8) (1.7)

2013 2014 2015 2016 2017*

(3.5)

(3.0)

(2.5)

(2.0)

(1.5)

(1.0)

(50.0)

(40.0)

(30.0)

(20.0)

(10.0)

0.0

10.0

20.0

30.0

%(USD bn)

Primary Income Secondary IncomeGoods ServicesCurrent Account Current Account (% GDP)-rhs

Source: Bank Indonesia1 Provisional figures.2 Very provisional figures.

External Sector Remains ResilientHealthy Current Account Deficit and Balance of Payment

Components (USD bn) 2013 2014 2015 2016 20171

Q1-20182

Current Account (29.1) (27.5) (17.5) (17.0) (17.5) (5.5)

A. Goods 5.8 7.0 14.0 15.3 18.8 2.4

Export, fob 182.1 175.3 149.1 144.5 168.9 44.4

Import, fob (176.3) (168.3) (135.1) (129.2) (150.1) (42.1)

B. Services, Primary &

Secondary Income(34.9) (34.5) (31.6) (32.3) (36.3) (7.9)

Capital & Financial Account 22.0 44.9 16.9 29.3 29.5 1.9

1. Direct Investment 12.2 14.7 10.7 16.1 19.2 3.1

2. Portfolio Investment 10.9 26.1 16.2 19.0 20.6 (1.2)

3. Financial Derivatives (0.3) (0.2) 0.0 0.0 (0.1) 0.1

4. Other Investment (0.8) 4.3 (10.1) (5.8) (10.2) (0.2)

Overall Balance (7.3) 15.2 (1.1) 12.1 11.6 (3.9)

Memorandum:

Reserve Assets Position 99.4 111.9 105.9 116.4 130.2 126.0

In months of imports &

official debt repayment5.5 6.5 7.4 8.4 8.3 7.7

Current Account

(% GDP)(3.2) (3.1) (2.0) (1.8) (1.7) (2.2)

Balance of Payment (2013 – 2017)Current Account Deficit is Improving, Significantly Lower than 2013

1

99.4

111.9105.9

116.4 130.2122.9

5.4

6.57.4

8.48.3

7.2

0

1

2

3

4

5

6

7

8

9

0

20

40

60

80

100

120

140

2013 2014 2015 2016 2017 18-May

(Month)(USD bn)

International Reserves Months of Imports & Servicing of Government Debt (rhs)

May-18

Ample Foreign Reserves to Buffer Against External Shocks

16

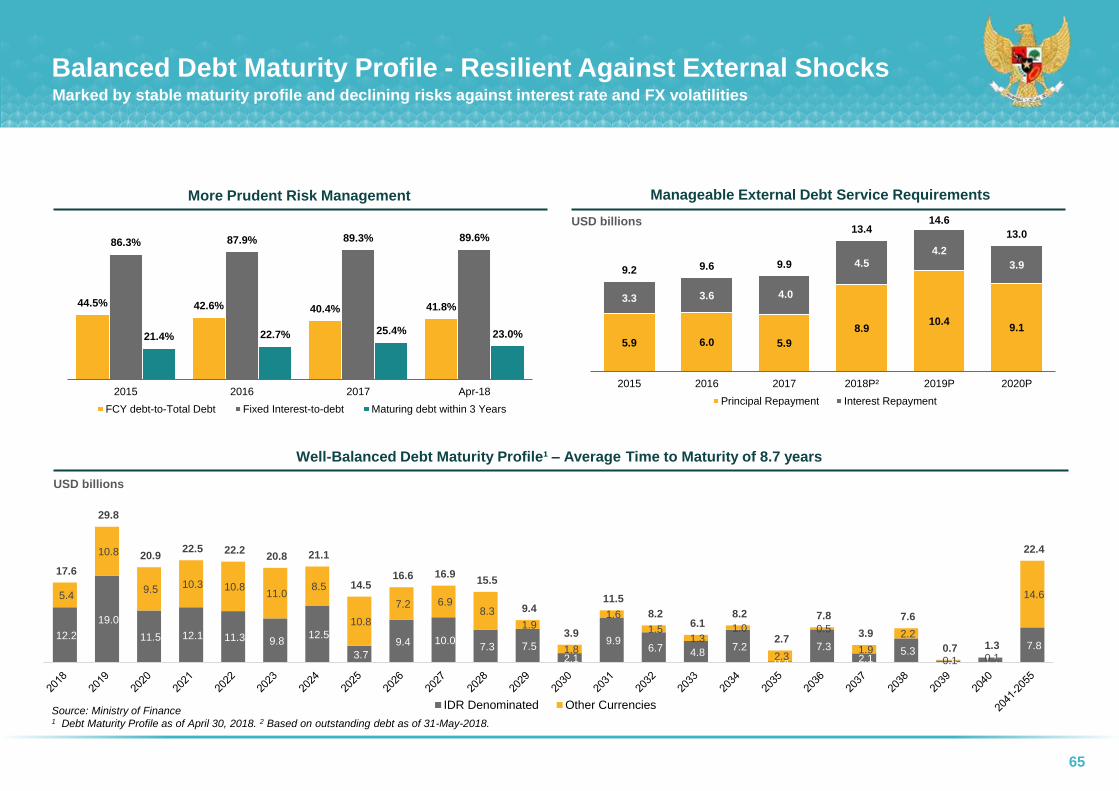

12.2

19.0

11.5 12.1 11.3 9.8 12.5

3.7

9.4 10.0 7.3 7.5

2.1

9.9 6.7 4.8

7.2

0.4

7.3 2.1

5.3 0.5 1.1

7.8

5.4

10.8

9.5 10.3 10.8 11.0

8.5

10.8

7.2 6.9 8.3

1.9

1.8

1.6

1.5 1.3

1.0

2.3

0.5

1.9

2.2

0.1 0.1

14.6

17.6

29.8

20.9 22.5 22.2

20.8 21.1

14.5 16.6 16.9

15.5

9.4

3.9

11.5

8.2 6.1

8.2

2.7

7.8

3.9

7.6

0.7 1.3

22.4

IDR Denominated Other CurrenciesSource: Ministry of Finance1 Debt Maturity Profile as of April 30, 2018. 2 Based on outstanding debt as of 31-May-2018.

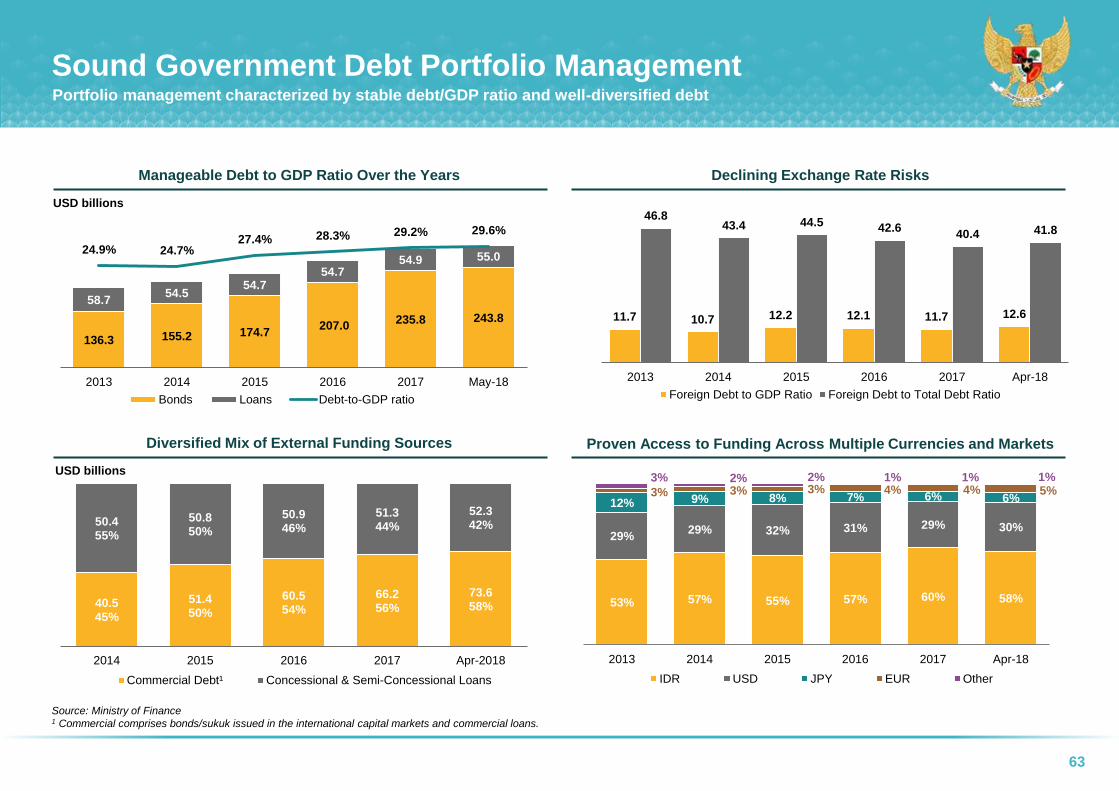

Manageable External Debt Service RequirementsMore Prudent Risk Management

Well-Balanced Debt Maturity Profile¹ – Average Time to Maturity of 8.7 years

Balanced Debt Maturity Profile - Resilient Against External ShocksMarked by stable maturity profile and declining risks against interest rate and FX volatilities

USD billions

44.5% 42.6% 40.4% 41.8%

86.3% 87.9% 89.3% 89.6%

21.4% 22.7% 25.4% 23.0%

2015 2016 2017 Apr-18

FCY debt-to-Total Debt Fixed Interest-to-debt Maturing debt within 3 Years

5.9 6.0 5.9

8.910.4

9.1

3.3 3.6 4.0

4.54.2

3.99.2 9.6 9.9

13.414.6

13.0

2015 2016 2017 2018P² 2019P 2020P

Principal Repayment Interest Repayment

USD billions

17

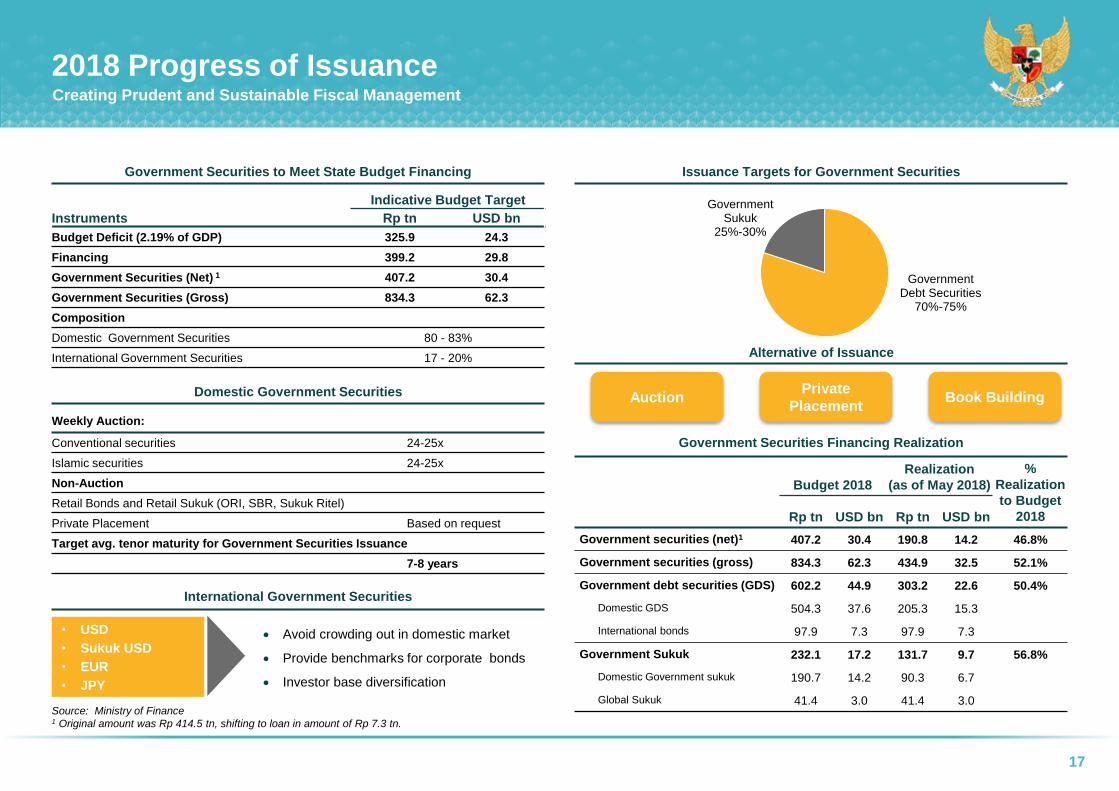

Source: Ministry of Finance1 Original amount was Rp 414.5 tn, shifting to loan in amount of Rp 7.3 tn.

Domestic Government Securities

2018 Progress of IssuanceCreating Prudent and Sustainable Fiscal Management

Government Debt Securities

70%-75%

Government Sukuk

25%-30%

Weekly Auction:

Conventional securities 24-25x

Islamic securities 24-25x

Non-Auction

Retail Bonds and Retail Sukuk (ORI, SBR, Sukuk Ritel)

Private Placement Based on request

Target avg. tenor maturity for Government Securities Issuance

7-8 years

Instruments

Indicative Budget Target

Rp tn USD bn

Budget Deficit (2.19% of GDP) 325.9 24.3

Financing 399.2 29.8

Government Securities (Net) 1 407.2 30.4

Government Securities (Gross) 834.3 62.3

Composition

Domestic Government Securities 80 - 83%

International Government Securities 17 - 20%

International Government Securities

Avoid crowding out in domestic market

Provide benchmarks for corporate bonds

Investor base diversification

• USD

• Sukuk USD

• EUR

• JPY

Alternative of Issuance

Private

PlacementAuction Book Building

Government Securities Financing Realization

Budget 2018

Realization

(as of May 2018)

%

Realization

to Budget

2018Rp tn USD bn Rp tn USD bn

Government securities (net)1 407.2 30.4 190.8 14.2 46.8%

Government securities (gross) 834.3 62.3 434.9 32.5 52.1%

Government debt securities (GDS) 602.2 44.9 303.2 22.6 50.4%

Domestic GDS 504.3 37.6 205.3 15.3

International bonds 97.9 7.3 97.9 7.3

Government Sukuk 232.1 17.2 131.7 9.7 56.8%

Domestic Government sukuk 190.7 14.2 90.3 6.7

Global Sukuk 41.4 3.0 41.4 3.0

Issuance Targets for Government SecuritiesGovernment Securities to Meet State Budget Financing

18

Source: Ministry of Finance; Bappenas; KPPIP: “Komite Kebijakan Percepatan Penyediaan Infrastruktur” or National Committee for the Acceleration of Infrastructure Provision; OBC: Outline Business Case; PDF:

Project Development Facility; GCA: Government Contracting Activity

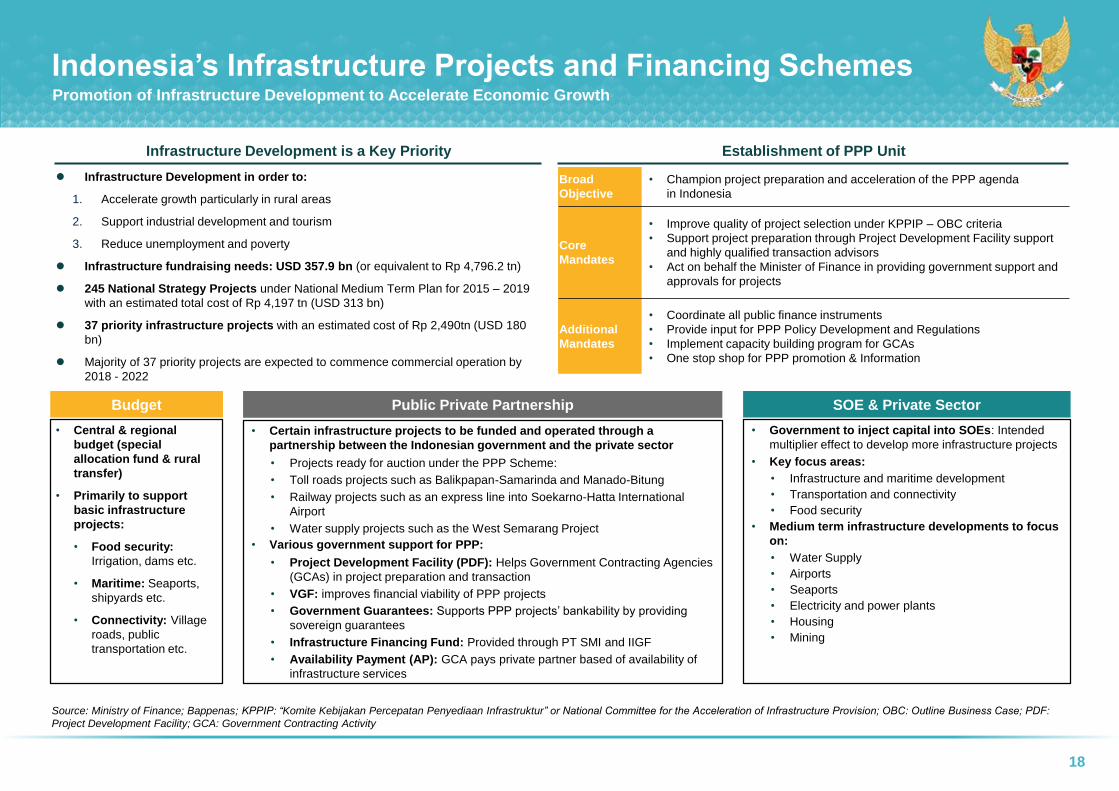

Indonesia’s Infrastructure Projects and Financing SchemesPromotion of Infrastructure Development to Accelerate Economic Growth

Broad

Objective

• Champion project preparation and acceleration of the PPP agenda

in Indonesia

Core

Mandates

• Improve quality of project selection under KPPIP – OBC criteria

• Support project preparation through Project Development Facility support

and highly qualified transaction advisors

• Act on behalf the Minister of Finance in providing government support and

approvals for projects

Additional

Mandates

• Coordinate all public finance instruments

• Provide input for PPP Policy Development and Regulations

• Implement capacity building program for GCAs

• One stop shop for PPP promotion & Information

Establishment of PPP Unit

Budget Public Private Partnership SOE & Private Sector

• Central & regional

budget (special

allocation fund & rural

transfer)

• Primarily to support

basic infrastructure

projects:

• Food security:

Irrigation, dams etc.

• Maritime: Seaports,

shipyards etc.

• Connectivity: Village

roads, public

transportation etc.

• Certain infrastructure projects to be funded and operated through a

partnership between the Indonesian government and the private sector

• Projects ready for auction under the PPP Scheme:

• Toll roads projects such as Balikpapan-Samarinda and Manado-Bitung

• Railway projects such as an express line into Soekarno-Hatta International

Airport

• Water supply projects such as the West Semarang Project

• Various government support for PPP:

• Project Development Facility (PDF): Helps Government Contracting Agencies

(GCAs) in project preparation and transaction

• VGF: improves financial viability of PPP projects

• Government Guarantees: Supports PPP projects’ bankability by providing

sovereign guarantees

• Infrastructure Financing Fund: Provided through PT SMI and IIGF

• Availability Payment (AP): GCA pays private partner based of availability of

infrastructure services

• Government to inject capital into SOEs: Intended

multiplier effect to develop more infrastructure projects

• Key focus areas:

• Infrastructure and maritime development

• Transportation and connectivity

• Food security

• Medium term infrastructure developments to focus

on:

• Water Supply

• Airports

• Seaports

• Electricity and power plants

• Housing

• Mining

Infrastructure Development in order to:

1. Accelerate growth particularly in rural areas

2. Support industrial development and tourism

3. Reduce unemployment and poverty

Infrastructure fundraising needs: USD 357.9 bn (or equivalent to Rp 4,796.2 tn)

245 National Strategy Projects under National Medium Term Plan for 2015 – 2019

with an estimated total cost of Rp 4,197 tn (USD 313 bn)

37 priority infrastructure projects with an estimated cost of Rp 2,490tn (USD 180

bn)

Majority of 37 priority projects are expected to commence commercial operation by

2018 - 2022

Infrastructure Development is a Key Priority

19

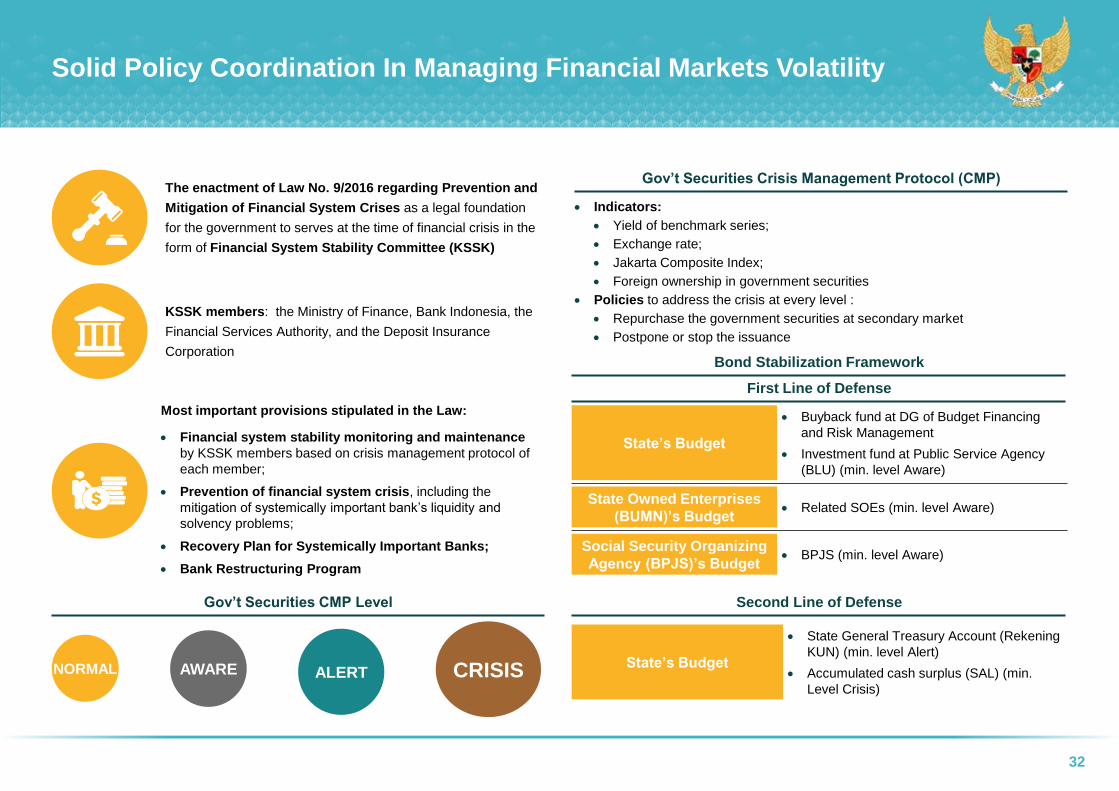

The enactment of Law No. 9/2016 regarding Prevention and

Mitigation of Financial System Crises as a legal foundation

for the government to serves at the time of financial crisis in the

form of Financial System Stability Committee (KSSK)

Most important provisions stipulated in the Law:

Financial system stability monitoring and maintenance

by KSSK members based on crisis management protocol of

each member;

Prevention of financial system crisis, including the

mitigation of systemically important bank’s liquidity and

solvency problems;

Recovery Plan for Systemically Important Banks;

Bank Restructuring Program

KSSK members: the Ministry of Finance, Bank Indonesia, the

Financial Services Authority, and the Deposit Insurance

Corporation

NORMAL AWARE ALERT CRISIS

Second Line of DefenseGov’t Securities CMP Level

First Line of Defense

State’s Budget

Buyback fund at DG of Budget Financing

and Risk Management

Investment fund at Public Service Agency

(BLU) (min. level Aware)

State Owned Enterprises

(BUMN)’s Budget Related SOEs (min. level Aware)

Social Security Organizing

Agency (BPJS)’s Budget BPJS (min. level Aware)

Indicators:

Yield of benchmark series;

Exchange rate;

Jakarta Composite Index;

Foreign ownership in government securities

Policies to address the crisis at every level :

Repurchase the government securities at secondary market

Postpone or stop the issuance

Bond Stabilization Framework

State’s Budget

State General Treasury Account (Rekening

KUN) (min. level Alert)

Accumulated cash surplus (SAL) (min.

Level Crisis)

Solid Policy Coordination In Managing Financial Markets Volatility

Gov’t Securities Crisis Management Protocol (CMP)

Recent Macroeconomic

Development

02Ampera Bridge in South Sumatera,

Indonesia

21

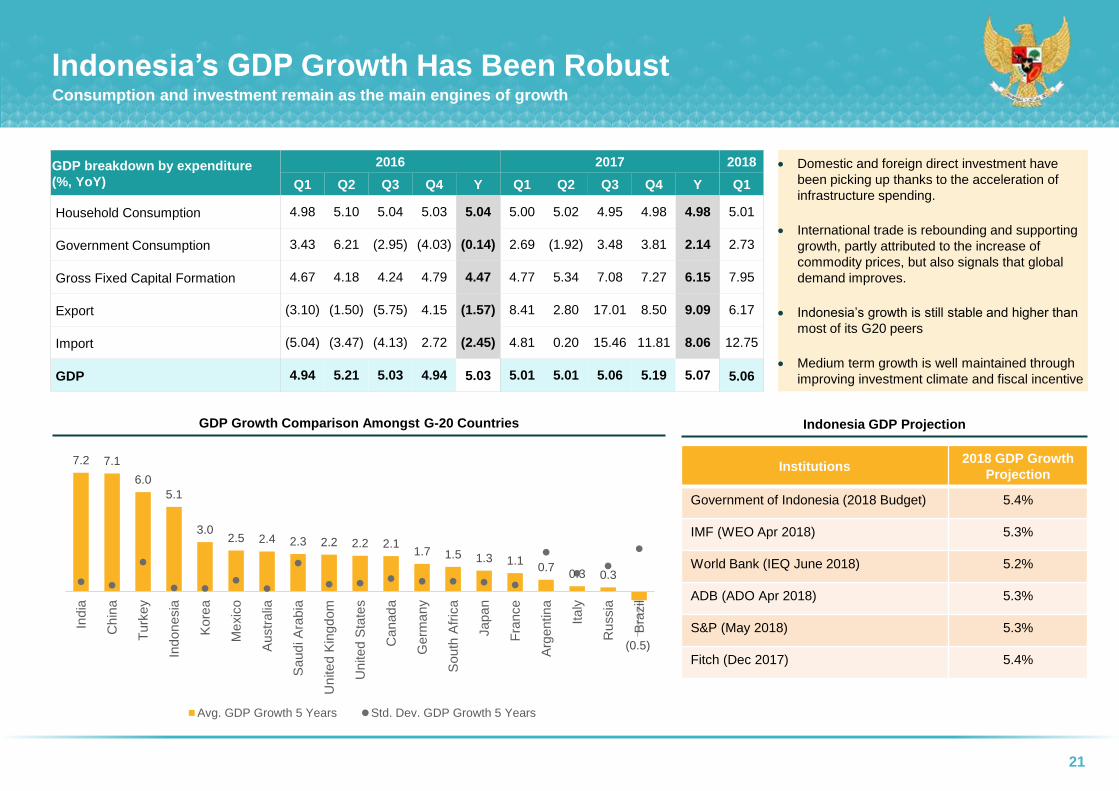

Indonesia’s GDP Growth Has Been RobustConsumption and investment remain as the main engines of growth

GDP breakdown by expenditure

(%, YoY)

2016 2017 2018

Q1 Q2 Q3 Q4 Y Q1 Q2 Q3 Q4 Y Q1

Household Consumption 4.98 5.10 5.04 5.03 5.04 5.00 5.02 4.95 4.98 4.98 5.01

Government Consumption 3.43 6.21 (2.95) (4.03) (0.14) 2.69 (1.92) 3.48 3.81 2.14 2.73

Gross Fixed Capital Formation 4.67 4.18 4.24 4.79 4.47 4.77 5.34 7.08 7.27 6.15 7.95

Export (3.10) (1.50) (5.75) 4.15 (1.57) 8.41 2.80 17.01 8.50 9.09 6.17

Import (5.04) (3.47) (4.13) 2.72 (2.45) 4.81 0.20 15.46 11.81 8.06 12.75

GDP 4.94 5.21 5.03 4.94 5.03 5.01 5.01 5.06 5.19 5.07 5.06

7.2 7.1

6.0

5.1

3.0 2.5 2.4 2.3 2.2 2.2 2.1

1.7 1.5 1.3 1.1 0.7

0.3 0.3

(0.5)

India

Ch

ina

Turk

ey

Indon

esia

Kore

a

Me

xic

o

Austr

alia

Saud

i A

rabia

Un

ite

d K

ing

dom

Un

ite

d S

tate

s

Ca

nad

a

Germ

any

South

Afr

ica

Japa

n

Fra

nce

Arg

entina

Ita

ly

Ru

ssia

Bra

zil

Avg. GDP Growth 5 Years Std. Dev. GDP Growth 5 Years

Institutions2018 GDP Growth

Projection

Government of Indonesia (2018 Budget) 5.4%

IMF (WEO Apr 2018) 5.3%

World Bank (IEQ June 2018) 5.2%

ADB (ADO Apr 2018) 5.3%

S&P (May 2018) 5.3%

Fitch (Dec 2017) 5.4%

Domestic and foreign direct investment have

been picking up thanks to the acceleration of

infrastructure spending.

International trade is rebounding and supporting

growth, partly attributed to the increase of

commodity prices, but also signals that global

demand improves.

Indonesia’s growth is still stable and higher than

most of its G20 peers

Medium term growth is well maintained through

improving investment climate and fiscal incentive

Indonesia GDP ProjectionGDP Growth Comparison Amongst G-20 Countries

22

GDP by Production SideManufacturing improves while service sector generally keeps on recording high growth

Agriculture (%, YoY) Mining (%, YoY)

3.363.81

3.14

2016 2017 Q1-2018

0.95 0.69 0.74

2016 2017 Q1-2018

Manufacturing (%, YoY) Construction (%, YoY)

4.26 4.27 4.50

2016 2017 Q1-2018

5.22

6.79 7.35

2016 2017 Q1-2018

Trade (%,YoY)

Transportation

(%, YoY)

Comm & Info

(%, YoY)

Financial Service

(%, YoY)

4.034.44

4.96

2016 2017 Q1-18

8.90

5.48

4.38

2016 2017 Q1-18

Se

co

nd

ary

Te

rtia

ryP

rim

ary

Primary sector grew marginally:

Agriculture slowed due to production decrease in food

crops

Mining growth increased supported by increasing metal

ores production, but the decline in energy commodity

production weighed on overall growth

Secondary sector on an improving trend:

Manufacturing sector growth increased particularly

supported by F&B, textile, and metal industries

Construction recorded high growth driven by

infrastructure acceleration program

Tertiary sector continues to show strong growth:

Trade accelerated in line with increasing export-import

as well as vehicle sales

Transportation, communication, and information

sectors consistently posted high growth supported by

improving logistic and digital economy

Financial service sector grew moderately as credit

growth remains soft

8.889.81

8.69

2016 2017 Q1-18

7.45

8.49 8.59

2016 2017 Q1-18

23

Regional GrowthMost of regions recorded positive growth in the first quarter 2018

5.06%

2017 National

GDP Growth

SUMATERA: 21.5% of GDP

2018:

4.37%

2017:

4.14

2017:

5.69

2018:

5.78%

2018:

3.25%

2017:

4.972018:

6.83%2017:

6.93

2018:

3.74%2017:

2.93

2017:

4.40

JAVA: 58.7% of GDP

KALIMANTAN: 8.2% of GDP

SULAWESI: 6.0% of GDP

PAPUA: 2.5% of GDP

BALI & NUSRA: 3.0% of GDP

2018:

18.42%

As the industrial center, Java still holds the biggest economic activity accounting for 58.67 percent of GDP

Maluku and Papua recorded high growth of 18.42 percent, underpinned by the increase of commodity price and mining

activity

2017:

4.30

2017:

5.61

2017:

4.332017:

6.99

2017:

3.73

2017:

4.89

2017 Regional GDP

Growth

2017 – Q1 Regional

GDP Growth

2018 – Q1 Regional

GDP Growth

Government effort aimed to

improve connectivity among

the islands and bring down the

logistics cost. The prices of

basic goods in the outlying

islands are becoming more

affordable as the result. This

will translate to improved

efficiencies, thriving regional

economies, and lowering the

development disparity among

the regions.

Infrastructure and connectivity

projects to create more

sustainable and equitable

economic growth in all regions.

Intergovernmental transfer,

including Village Fund, has

also promoted equality in the

region.

24

Direct Investment Grew by 11.8 Percent in Q1-2018Underpinned by improving investment climate

Direct Investment Share by Sectors Q1-2018Direct Investment Realization

FY-2016 FY-2017 Q1-2018

Nominal

(Rp Tn)

Growth

(% YoY)

Nominal

(Rp Tn)

Growth

(% YoY)

Nominal

(Rp Tn)

Growth

(% YoY)

Domestic 216.2 20.5 262.3 21.3 76.4 11.0

Foreign 396.6 8.4 430.5 8.5 108.9 12.4

Total 612.8 12.4 692.8 13.1 185.3 11.8

FDI Share by Country Origins Q1-2018 FDI Share by Country Origins 2010-2017

32.6%

16.7%

11.6%

8.3%

6.3%

24.5%

Singapore

Japan

S Korea

China

Hong Kong

Other

23.8%

12.2%

5.5%

5.4%

4.7%

4.6%

3.9%

3.5%

3.4%

32.9%

Singapore

Japan

US

S Korea

Netherland

Malaysia

China

Hong Kong

BVI

Other

Housing, Estate & Building

15%

Electricity, Gas, & Water Supply10%

Others45%

Metal, Machinery, &

Electronic Industry

12%

Transportation, Warehouse,

& Telecommunication

8%

Crops &

Plantation

10%

Source: NSWi BKPM

Positive FDI flow shows a high interest in Indonesia.

Nevertheless, Java island is still the main destination

for direct investment, roughly 55% of total FDI.

Government Efforts To Improve Investment Climate :

(1) Easing Import and Export Restrictions (2)

Reducing Dwelling Time (3) Revising and Perfecting

Tax Incentive (Tax Allowance and Tax Holiday)

Overall structural reform efforts are expected to boost

investment and exports to support Indonesia's

economic growth in the medium term.

25

Inflation has been More BenignCreate Substantial Foundation for Robust Consumption

Inflation Rate & Components (%)Inflation Rate (YTD, %)

3.0%

3…

3.2%

3.1%

3.0%

2.8%

0.2%

8.7%

3.6%

5.9%

0.7%

4.3%

(2.0)%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M

2016 2017 2018

Inflation (CPI) Core Inflation Administered Price Volatile Food

Future Policies

Improving logistic and distribution

and stronger coordination

between institutions are some key

factor in inflation management

The monitoring of prices and

improvements to the trading of

some food commodities can

anticipate price game practices.

Inflation is more benign supported

by more stable food inflation as

supply side improves.

The administered price inflation is

the biggest source of pressure in

2017, but pressure is easing as

tariffs are adjusted at the end of

the first semester of 2017.

Indonesian Consumer Confidence

is showing a vibrant economic

activity and good expectation on

economy

Consumer Confidence Index

Source: Bank Indonesia

100

105

110

115

120

125

130

J M M J S N J M M J S N J M M

2016 2017 2018

11.1%

2.8%

7.0%

3.8%4.3%

8.4% 8.4%

3.4%3.0%

3.6%

1.3%

2008 2010 2012 2014 2016 May-18

Source: BPS

Source: BPS

26

(2.0)

(1.0)

0.0

1.0

2.0

3.0

M J J A S O N D

201

7-J F M A M J J A S O N D

201

8-J F M A

Non O&G O&G Total

Import Growth Upholds Increasing Domestic Economic

ActivitiesUntil April 2018, Trade Balance is Recording a Deficit of USD1.31 billion

Source: BPS

Cumulative Growth of Export CommodityTrade Balance (USD Billion)

Trade balance is recording deficit

cumulatively in April 2018, due to

high import growth that supports

growing domestic production

Import grew by 23.65% (YTD)

supported by higher demand for

festive seasons of Ramadhan and

Idul Fitri; capital good increase to

support infrastructure development

and military equipment; and raw

material increase that highlights

improving domestic productivity and

economic activity

Export grew by 8.77% (YTD),

underpinned by mining commodity

growth of 33.4% and manufacturing

of 5.3%

Deficit Jan-Apr

2018:

USD1.31 billion

Surplus FY 2016:

USD9.5 billion

Surplus FY 2017:

USD11.8 billion

Cumulative Growth of Import Goods

Contribution to

Total Import

Capital Goods

16.3%

Consumption

Goods 9.1%

Raw Materials

74.6%

Top 4 Export/Import (Non-O&G) by Country

April 2018 (USD Billion)

Export (Non O&G) Import (Non O&G)

China 3.4

Japan 1.6

United States 1.0

Thailand 0.9

1

2

3

4

China 1.8

United States 1.4

Japan 1.4

India 1.0

1

2

3

4

26.1%

21.9%

31.0%

(30.0)%

(10.0)%

10.0%

30.0%

50.0%

M J S N

201

7-J M M J S N

201

8-J M

Consumption goods Raw materials Capital goods

(5.1)%

5.3%

33.4%

4.0%

(60.0)%

(40.0)%

(20.0)%

0.0%

20.0%

40.0%

60.0%

M J J A S O N D

201

7-J F M A M J J A S O N D

201

8-J F M A

Agriculture Manufacturing Mining O&G

27

2018 Growth OutlookEconomy is projected to further accelerate in the midst of robust domestic demand and improving international trade

1 Mid-point of 5.4% and 5.8% economic growth assumption, submitted to parliament.

GDP Growth Projection (%, YoY)

2018 Growth Projection from Various Institutions

Challenges:

Consumption growth needs to be boosted more

Competitiveness needs to be enhanced particularly to fulfill growing

domestic demand

Credit growth needs to be accelerated more

External uncertainties: US monetary normalization, trade wars and

protectionism, and geopolitical tension

Opportunities:

Stable consumption supported by benign inflation

Rising investment driven by infrastructure development and improving

business climate

Increasing export as external demand recovering and commodity prices

increasing

Additional contribution from various special occasions such as Asian

Games, regional election, general election preparation, and IMF-WB

annual meeting

IMF (WEO Apr 2018) 5.3%

World Bank (IEQ June 2018) 5.2%

ADB (ADO Apr 2018) 5.3%

S&P (May 2018) 5.3%

Fitch (Dec 2017) 5.4%

4.95.02 5.07

5.4

5.6

2015 2016 2017 2018 APBN 2019(Submitted toParliament)¹

Financial Market Condition

03Lake Toba in North Sumatera,

Indonesia

29

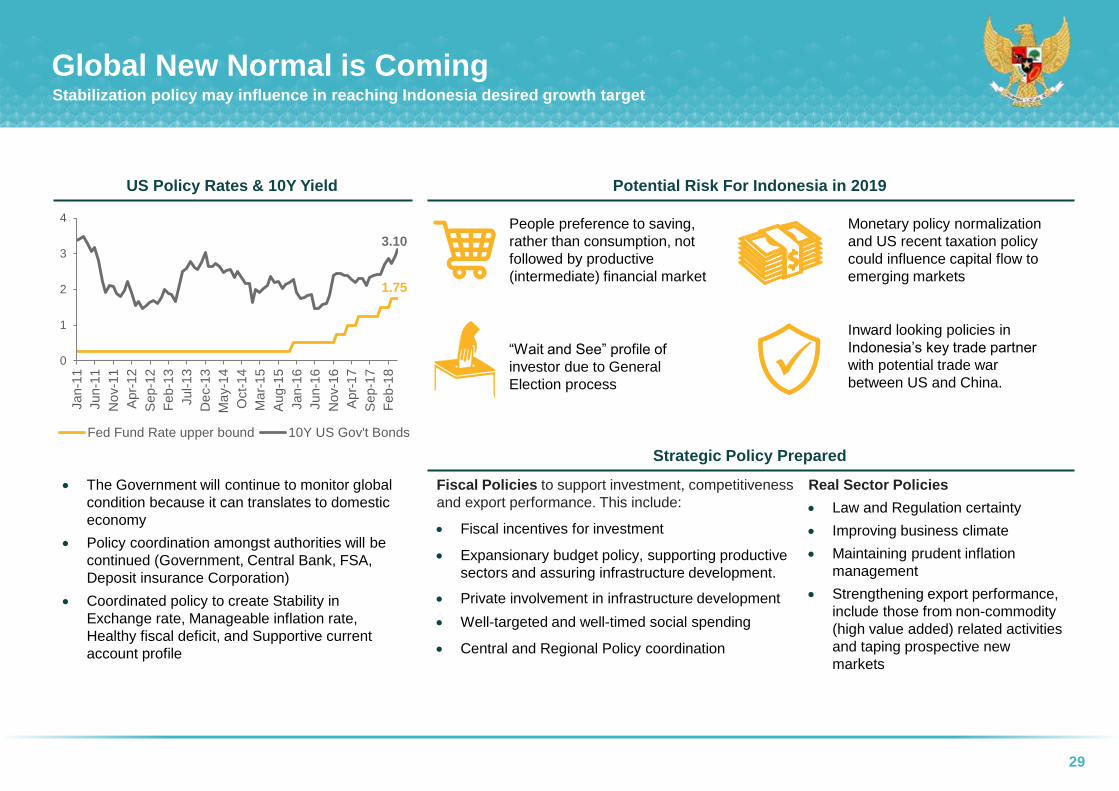

Global New Normal is Coming Stabilization policy may influence in reaching Indonesia desired growth target

The Government will continue to monitor global

condition because it can translates to domestic

economy

Policy coordination amongst authorities will be

continued (Government, Central Bank, FSA,

Deposit insurance Corporation)

Coordinated policy to create Stability in

Exchange rate, Manageable inflation rate,

Healthy fiscal deficit, and Supportive current

account profile

People preference to saving,

rather than consumption, not

followed by productive

(intermediate) financial market

“Wait and See” profile of

investor due to General

Election process

Monetary policy normalization

and US recent taxation policy

could influence capital flow to

emerging markets

Inward looking policies in

Indonesia’s key trade partner

with potential trade war

between US and China.

Fiscal Policies to support investment, competitiveness

and export performance. This include:

Fiscal incentives for investment

Expansionary budget policy, supporting productive

sectors and assuring infrastructure development.

Private involvement in infrastructure development

Well-targeted and well-timed social spending

Central and Regional Policy coordination

Real Sector Policies

Law and Regulation certainty

Improving business climate

Maintaining prudent inflation

management

Strengthening export performance,

include those from non-commodity

(high value added) related activities

and taping prospective new

markets

1.75

3.10

0

1

2

3

4

Jan-1

1

Jun-1

1

No

v-1

1

Apr-

12

Sep-1

2

Feb

-13

Jul-1

3

De

c-1

3

Ma

y-1

4

Oct-

14

Ma

r-1

5

Aug-1

5

Jan-1

6

Jun-1

6

No

v-1

6

Apr-

17

Sep-1

7

Feb

-18

Fed Fund Rate upper bound 10Y US Gov't Bonds

Strategic Policy Prepared

Potential Risk For Indonesia in 2019US Policy Rates & 10Y Yield

30

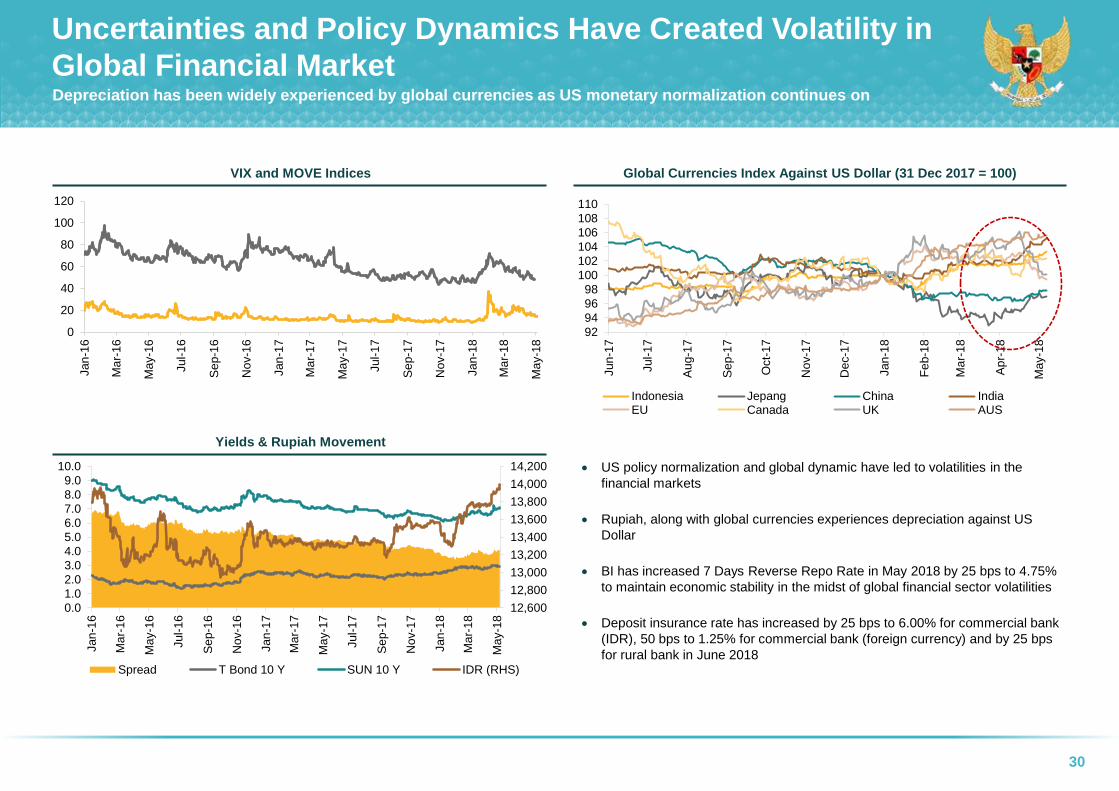

Uncertainties and Policy Dynamics Have Created Volatility in

Global Financial MarketDepreciation has been widely experienced by global currencies as US monetary normalization continues on

Global Currencies Index Against US Dollar (31 Dec 2017 = 100)VIX and MOVE Indices

Yields & Rupiah Movement

0

20

40

60

80

100

120

Jan

-16

Ma

r-1

6

Ma

y-1

6

Jul-

16

Se

p-1

6

Nov-1

6

Jan

-17

Ma

r-1

7

Ma

y-1

7

Jul-

17

Se

p-1

7

Nov-1

7

Jan

-18

Ma

r-1

8

Ma

y-1

8

92

94

96

98

100

102

104

106

108

110

Jun

-17

Jul-

17

Au

g-1

7

Se

p-1

7

Oct-

17

Nov-1

7

Dec-1

7

Jan

-18

Fe

b-1

8

Ma

r-1

8

Ap

r-18

Ma

y-1

8

Indonesia Jepang China IndiaEU Canada UK AUS

12,600

12,800

13,000

13,200

13,400

13,600

13,800

14,000

14,200

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Jan

-16

Ma

r-1

6

Ma

y-1

6

Jul-

16

Se

p-1

6

Nov-1

6

Jan

-17

Ma

r-1

7

Ma

y-1

7

Jul-

17

Se

p-1

7

Nov-1

7

Jan

-18

Ma

r-1

8

Ma

y-1

8

Spread T Bond 10 Y SUN 10 Y IDR (RHS)

US policy normalization and global dynamic have led to volatilities in the

financial markets

Rupiah, along with global currencies experiences depreciation against US

Dollar

BI has increased 7 Days Reverse Repo Rate in May 2018 by 25 bps to 4.75%

to maintain economic stability in the midst of global financial sector volatilities

Deposit insurance rate has increased by 25 bps to 6.00% for commercial bank

(IDR), 50 bps to 1.25% for commercial bank (foreign currency) and by 25 bps

for rural bank in June 2018

31

Uncertainties and Policy Dynamics Have Created Volatility in

Global Financial Market (Cont’d)

Price Performance of Stock Market Indices of

Emerging Market Peers (2018 YTD)

10-Year Local Government Yield of

Emerging Market Peers (2018 YTD) Commentary

There has been volatility in Indonesia’s financial

markets and yield of local government 10-year

bond in 2018, in line with other emerging markets.

However, Indonesia’s financial services sector

stability and liquidity has remained solid

throughout 2018. As of April 2018,

Financial services institutions have maintained

adequate capital and liquidity, with the Capital

Adequacy Ratio (CAR) in the banking industry

recorded at 22.38%

RBC of the general insurance and life insurance

industries recorded at 310% and 454%, respectively

Excess reserve in the banking industry was Rp 618

trillion

Credit and market risk remain credible – gross NPL

ratio of 2.79% in the banking industry and NPF ratio

3.01% as reported by finance companies

Deposit guarantee coverage of the Deposit

Insurance Corporation (LPS) has reached 99.9% of

customers and 52.15% in terms of value,

demonstrating public confidence and trust in the

national banking system

80%

90%

100%

110%

120%

130%

Jan-2018

Feb-2018

Mar-2018

Apr-2018

May-2018

Jun-2018

Ind

ex

ed

Pri

ce

s

JCI (Indonesia) KLCI (Malaysia)

SET (Thailand) Hochiminh (Vietnam)

PSEI (Philippines) CSI 300 (China)

BOVESPA (Brazil) SENSEX 30 (India)

0.9%

1.1%

4.2%

(1.9)%

(6.5)%

(5.9)%

(2.3)%

(10.8)%

0%

2%

4%

6%

8%

10%

12%

Jan-2018

Feb-2018

Mar-2018

Apr-2018

May-2018

Jun-2018

Yie

ld (%

)

Indonesia Malaysia Thailand

Vietnam Philippines China

Brazil India

11.3%

7.8%

7.1%

6.1%

4.7%

4.2%

3.6%

2.9%

Source: Data Stream as of 1-Jun-2018Source: Data Stream as of 1-Jun-2018

There has been volatilities in the stock market and local bond market. However, financial services sectors have

remained resilient

32

The enactment of Law No. 9/2016 regarding Prevention and

Mitigation of Financial System Crises as a legal foundation

for the government to serves at the time of financial crisis in the

form of Financial System Stability Committee (KSSK)

Most important provisions stipulated in the Law:

Financial system stability monitoring and maintenance

by KSSK members based on crisis management protocol of

each member;

Prevention of financial system crisis, including the

mitigation of systemically important bank’s liquidity and

solvency problems;

Recovery Plan for Systemically Important Banks;

Bank Restructuring Program

KSSK members: the Ministry of Finance, Bank Indonesia, the

Financial Services Authority, and the Deposit Insurance

Corporation

NORMAL AWARE ALERT CRISIS

Second Line of DefenseGov’t Securities CMP Level

First Line of Defense

State’s Budget

Buyback fund at DG of Budget Financing

and Risk Management

Investment fund at Public Service Agency

(BLU) (min. level Aware)

State Owned Enterprises

(BUMN)’s Budget Related SOEs (min. level Aware)

Social Security Organizing

Agency (BPJS)’s Budget BPJS (min. level Aware)

Indicators:

Yield of benchmark series;

Exchange rate;

Jakarta Composite Index;

Foreign ownership in government securities

Policies to address the crisis at every level :

Repurchase the government securities at secondary market

Postpone or stop the issuance

Bond Stabilization Framework

State’s Budget

State General Treasury Account (Rekening

KUN) (min. level Alert)

Accumulated cash surplus (SAL) (min.

Level Crisis)

Solid Policy Coordination In Managing Financial Markets Volatility

Gov’t Securities Crisis Management Protocol (CMP)

33

Additional Measures to Strengthen Stability and Growth of

Financial Markets

The Government, Bank Indonesia (BI), The Financial Services Authority (OJK) and The Indonesian Deposit Insurance Corporation are strengthening

coordination and implementing an optimal policy mix to maintain economic stability and ongoing development efforts

Stronger coordination prioritizes short-term stability of economy and financial markets while nurturing medium-term growth

In the Near Term, Bank Indonesia Will Prioritize Monetary Policy Oriented Towards

Rupiah Exchange Rate Stability

First, a pre-emptive, front-loading and ahead-of-the-curve policy response will be

pursued to stabilize the rupiah exchange rate, while consistently maintaining low and

controlled inflation within the 2018-2019 target corridor of 3.5±1%

Second, dual intervention in the foreign exchange market and SBN market will

constantly be optimized to stabilize the Rupiah exchange rate along with fair price

adjustments in the financial markets, while maintaining adequate liquidity in the money

market

Third, the monetary operations strategy will be oriented towards maintaining adequate

liquidity, particularly in the Rupiah money market and interbank swap market

Fourth, intensive communication with market players, the banking industry, business

community and economists will be used to form rational expectations, thus helping to

mitigate the rupiah overshooting the currency’s fundamental value

In addition, to maintain and build the current pace of domestic economic growth

momentum, Bank Indonesia is preparing follow-up measures to ease macroprudential

policy, while also coordinating with the Coordinating Ministry for Economic Affairs,

Ministry of Finance and the Financial Services Authority (OJK) to accelerate financial

market deepening, particularly for private sector infrastructure financing

Dualintervention in FX/ SBN markets

2

3Strengthening of monetary operations in FX and

money markets

1 Pre-emptive policy

response

Intensive Communication with key market ,

industry, business

stakeholders

4

34

Financial Sector Supervision Conducted by the Financial Services

Authority (OJK) is Focused on Maintaining a Healthy Financial

Sector

OJK continues to back the financial market deepening program in

terms of supply and demand, while strengthening market

infrastructure and facilitating municipal bond issuances and asset

securitization

OJK maintains financial services sector stability through industry

resilience, strengthening issuer fundamentals and implementing

appropriate policy measures when the financial markets experience

pressures

OJK nurtures credit growth and financial sector financing by

prioritizing financing that targets export commodities

In addition, OJK will continue to advocate financial inclusion to

stimulate quality economic growth through the development of

People’s Business Loan (KUR) clusters, waqf-based microfinance

and FinTech

Additional Measures to Strengthen Stability and Growth of

Financial Markets (Cont’d)

LPS is Open to Make Any Necessary Adjustments to the Guarantee

Rate

The Deposit Insurance Corporation (LPS) will intensify the monitoring

and evaluation of deposit guarantee schemes along with the Magnitude

and Guarantee Rate

LPS is open to make any necessary adjustments to the Guarantee Rate

at the first opportunity in accordance with the latest data available and

assessments of financial system stability

LPS will intensify monitoring and evaluation in order to maintain public

confidence in the national banking system of Indonesia

2018 State Budget Realization

Performance

04Komodo National Park in East Nusa

Tenggara, Indonesia

36

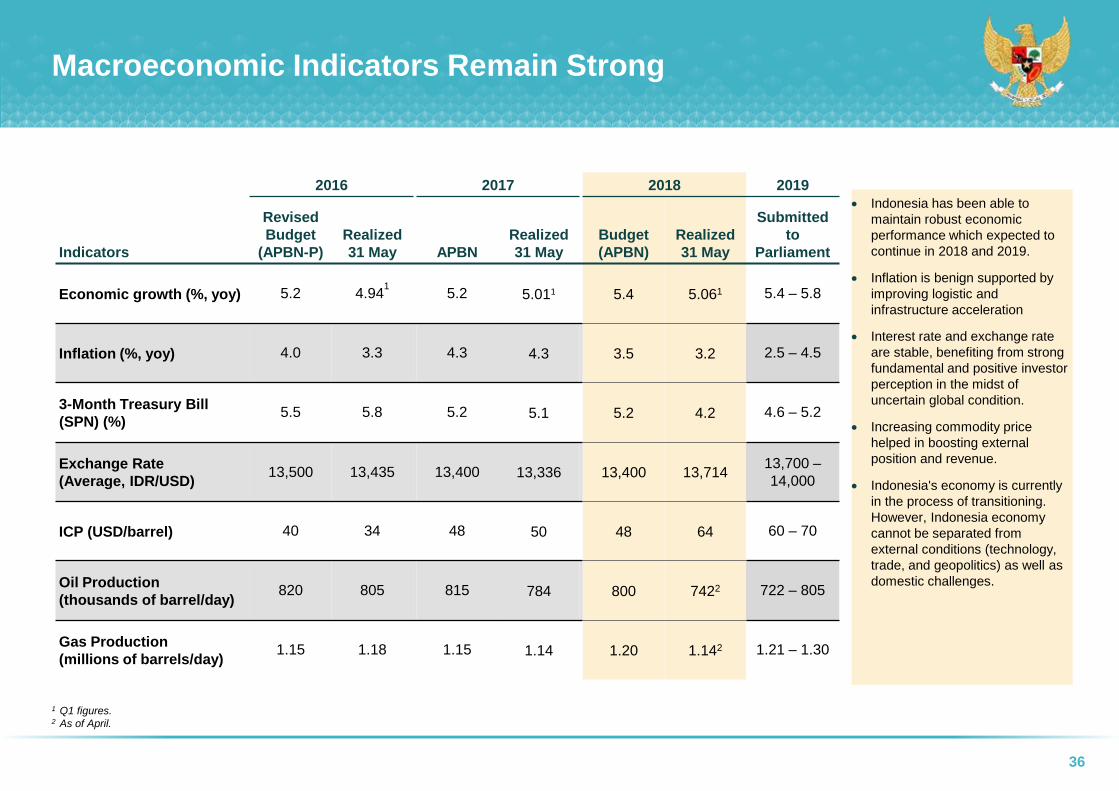

Macroeconomic Indicators Remain Strong

1 Q1 figures.2 As of April.

Indicators

2016 2017 2018 2019

Revised

Budget

(APBN-P)

Realized

31 May APBN

Realized

31 May

Budget

(APBN)

Realized

31 May

Submitted

to

Parliament

Economic growth (%, yoy) 5.2 4.941

5.2 5.011 5.4 5.061 5.4 – 5.8

Inflation (%, yoy) 4.0 3.3 4.3 4.3 3.5 3.2 2.5 – 4.5

3-Month Treasury Bill

(SPN) (%)5.5 5.8 5.2 5.1 5.2 4.2 4.6 – 5.2

Exchange Rate

(Average, IDR/USD)13,500 13,435 13,400 13,336 13,400 13,714

13,700 –

14,000

ICP (USD/barrel) 40 34 48 50 48 64 60 – 70

Oil Production

(thousands of barrel/day)820 805 815 784 800 7422 722 – 805

Gas Production

(millions of barrels/day)1.15 1.18 1.15 1.14 1.20 1.142 1.21 – 1.30

Indonesia has been able to

maintain robust economic

performance which expected to

continue in 2018 and 2019.

Inflation is benign supported by

improving logistic and

infrastructure acceleration

Interest rate and exchange rate

are stable, benefiting from strong

fundamental and positive investor

perception in the midst of

uncertain global condition.

Increasing commodity price

helped in boosting external

position and revenue.

Indonesia's economy is currently

in the process of transitioning.

However, Indonesia economy

cannot be separated from

external conditions (technology,

trade, and geopolitics) as well as

domestic challenges.

37

Performance of State BudgetFiscal Sustainability is Well Preserved as Fiscal Deficit Narrowed and Primary Balance Recorded a Substantial Surplus

The robust tax growth and

positive performance in export

and import duty good in the

first quarter of 2018 is a

positive support.

Central Government

Expenditure grows robustly

Deficit realization of 0.64% of

GDP is much lower compared

to May 2017

Primary balance surplus is

significantly higher than last

year, highlighting improving

fiscal performance and

sustainability that well

preserved

2017 2018

R-Budget

May

Realization

% Real

to Budget Budget

May

Realization

% Real to

Budget

% of Growth

(YoY)

A. Revenue & Grant 1,736.1 594.0 34.2 1,894.7 685.1 36.2 15.3

I. Domestic Revenue 1,733.0 593.8 34.3 1,893.5 683.7 36.1 15.1

1. Taxation Revenue 1,472.7 470.3 31.9 1,618.1 538.7 33.3 14.5

2. Non Tax Revenue 260.2 123.5 47.5 275.4 145.0 52.6 17.4

II. Grants 3.1 0.2 6.8 1.2 1.4 118.2 565.9

B. Expenditure 2,133.3 722.8 33.9 2,220.7 779.5 35.1 7.9

I. Central Government Expenditure 1,367.0 388.0 28.4 1,454.5 458.0 31.5 18.0

1. Ministerial Spending 798.6 193.0 24.2 847.4 231.5 27.3 19.9

2. Non Ministerial Spending 568.4 195.0 34.3 607.1 226.5 37.3 16.2

II. Transfer to Region and Village

Fund766.3 334.7 43.7 766.2 321.5 42.0 (4.0)

1. Transfer to Region 706.3 306.5 43.4 706.2 300.8 42.6 (1.9)

2. Village Fund 60.0 28.2 47.0 60.0 20.7 34.4 (26.7)

C. Primary Balance (178.0) (29.9) 16.8 (87.3) 18.1 (20.7) (160.5)

D. Surplus/(Deficit) (397.2) (128.7) 32.4 (325.9) (94.4) 29.0 (26.6)

% of GDP (2.92) (0.94) (2.19) (0.64)

E. Financing 397.2 195.6 49.3 325.9 169.9 52.1 (13.1)

% of GDP 2.92 1.45 2.19 1.15

I. Debt 461.3 193.9 42.0 399.2 169.0 42.3 (12.8)

II. Investment (59.7) 0.0 0.0 (65.7) 0.0 0.0 0.0

III. SLA (3.7) 1.6 (43.6) (6.7) 0.8 (11.9) (50.1)

IV. Guarantee (1.0) 0.0 0.0 (1.1) 0.0 0.0 0.0

V. Other 0.3 0.2 50.6 0.2 0.1 53.4 (35.6)

Surplus/(Deficit) Financing 0.0 66.9 - 0.0 75.5 - 12.8

38

Fiscal Deficit and Primary Balance on an Improving Trend

May Realization (RP Tn)

(71.1)

(189.1)

(128.7)

(94.5)

109.2

26.0

66.9 62.2(6.0)

(110.3)

(29.9)

18.0

2015 2016 2017 2018

Deficit Surplus of Financing Primary Balance

Fiscal deficit

realization(94.5) T

Primary surplus

Higher than previous

period, indicating that

fiscal sustainability

improves

18.0 T

62.2 T

Surplus of financing

realization in 30 May

2018 in-line with

previous year

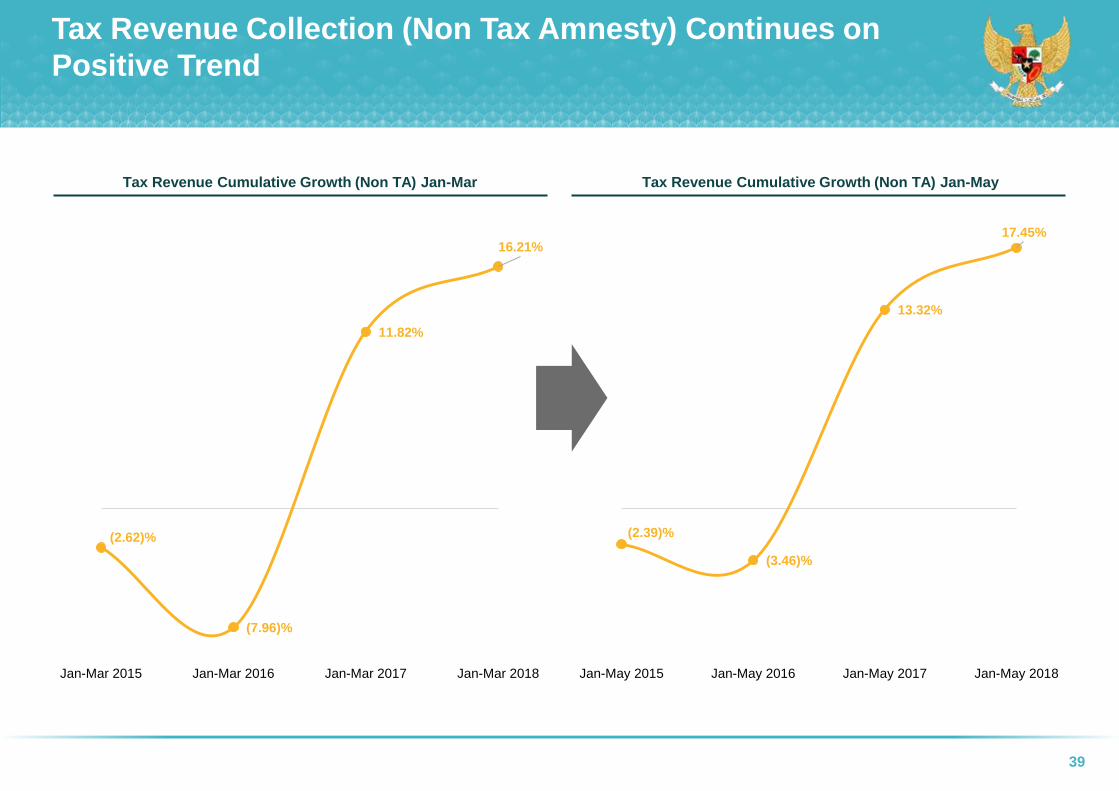

39

(2.62)%

(7.96)%

11.82%

16.21%

Jan-Mar 2015 Jan-Mar 2016 Jan-Mar 2017 Jan-Mar 2018

Tax Revenue Collection (Non Tax Amnesty) Continues on

Positive Trend

Tax Revenue Cumulative Growth (Non TA) Jan-MayTax Revenue Cumulative Growth (Non TA) Jan-Mar

(2.39)%

(3.46)%

13.32%

17.45%

Jan-May 2015 Jan-May 2016 Jan-May 2017 Jan-May 2018

40

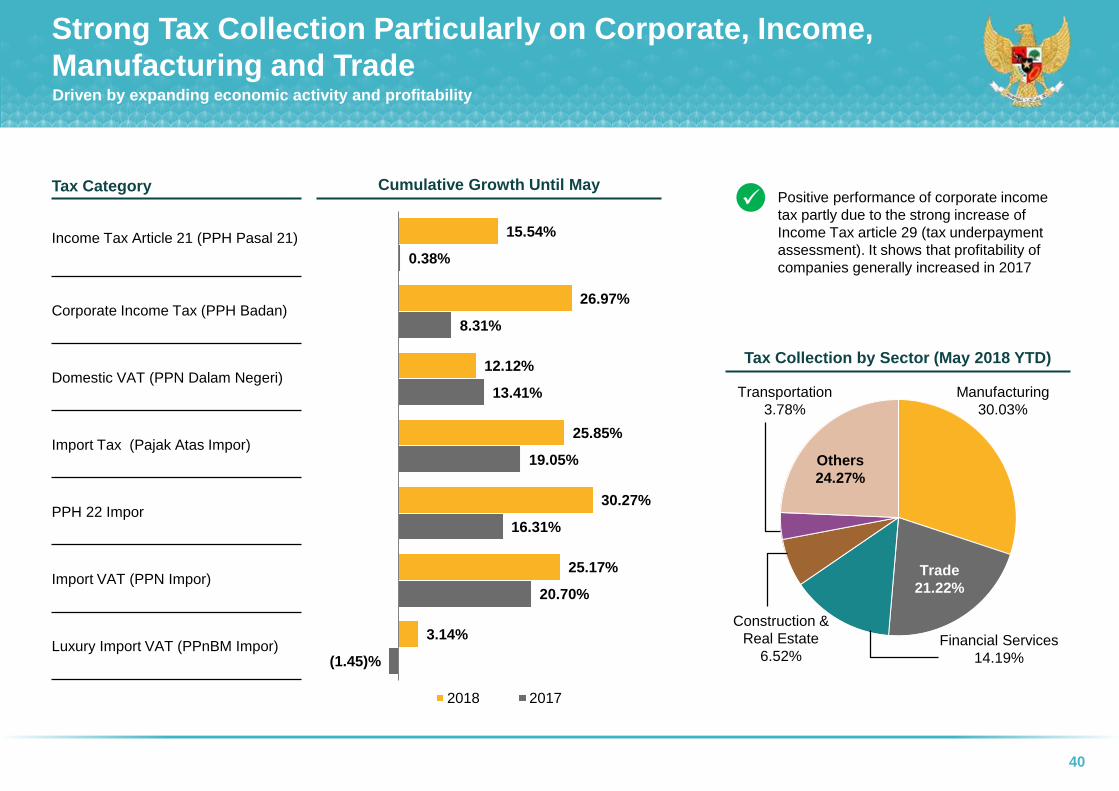

Strong Tax Collection Particularly on Corporate, Income,

Manufacturing and TradeDriven by expanding economic activity and profitability

Tax Category

Income Tax Article 21 (PPH Pasal 21)

Corporate Income Tax (PPH Badan)

Domestic VAT (PPN Dalam Negeri)

Import Tax (Pajak Atas Impor)

PPH 22 Impor

Import VAT (PPN Impor)

Luxury Import VAT (PPnBM Impor)

Cumulative Growth Until MayPositive performance of corporate income

tax partly due to the strong increase of

Income Tax article 29 (tax underpayment

assessment). It shows that profitability of

companies generally increased in 2017

Tax Collection by Sector (May 2018 YTD)

15.54%

26.97%

12.12%

25.85%

30.27%

25.17%

3.14%

0.38%

8.31%

13.41%

19.05%

16.31%

20.70%

(1.45)%

2018 2017

Manufacturing

30.03%

Trade

21.22%

Financial Services

14.19%

Transportation

3.78%

Construction &

Real Estate

6.52%

Others

24.27%

41

Source: EIS, CEISA, SPAN as of 1 May 2018

Custom and Excise Posted the Highest Growth in the Last

3 Years

Excise Revenue Growth (May YTD)Custom & Excise Revenue Growth (May YTD)

Export Duty Revenue Growth (May YTD)Import Duty Revenue Growth (May YTD)

(13.80)%

(26.46)%

6.97%

18.29%

May-2015 May-2016 May-2017 May-2018

(8.78)%

(35.49)%

7.83%

16.89%

May-2015 May-2016 May-2017 May-2018

(4.89)%

6.80%1.14%

14.11%

May-2015 May-2016 May-2017 May-2018

(75.27)%

(37.72)%

66.03%84.60%

May-2015 May-2016 May-2017 May-2018

42

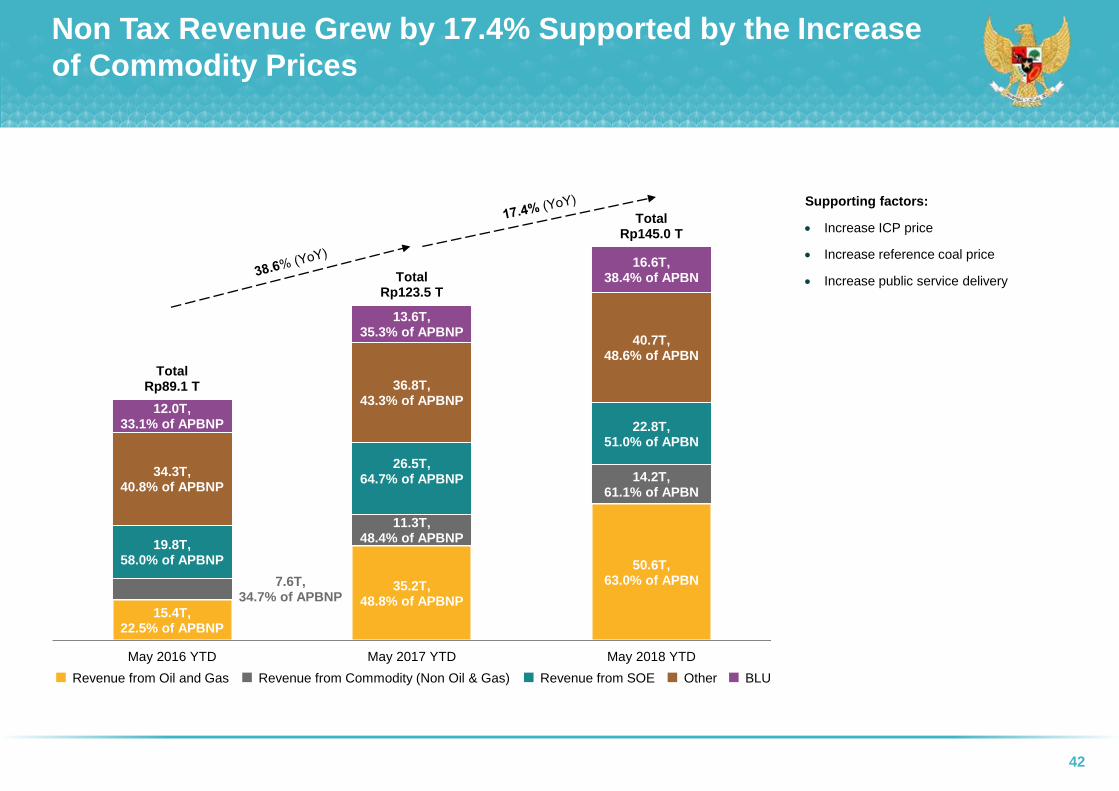

Non Tax Revenue Grew by 17.4% Supported by the Increase

of Commodity Prices

Revenue from Oil and Gas Revenue from Commodity (Non Oil & Gas) Revenue from SOE Other BLU

Supporting factors:

Increase ICP price

Increase reference coal price

Increase public service delivery

15.4T,22.5% of APBNP

35.2T,48.8% of APBNP

50.6T,63.0% of APBN7.6T,

34.7% of APBNP

11.3T,48.4% of APBNP

14.2T,61.1% of APBN

19.8T,58.0% of APBNP

26.5T,64.7% of APBNP

22.8T,51.0% of APBN

34.3T,40.8% of APBNP

36.8T,43.3% of APBNP

40.7T,48.6% of APBN

12.0T,33.1% of APBNP

13.6T,35.3% of APBNP

16.6T,38.4% of APBN

TotalRp89.1 T

TotalRp123.5 T

TotalRp145.0 T

May 2016 YTD May 2017 YTD May 2018 YTD

43

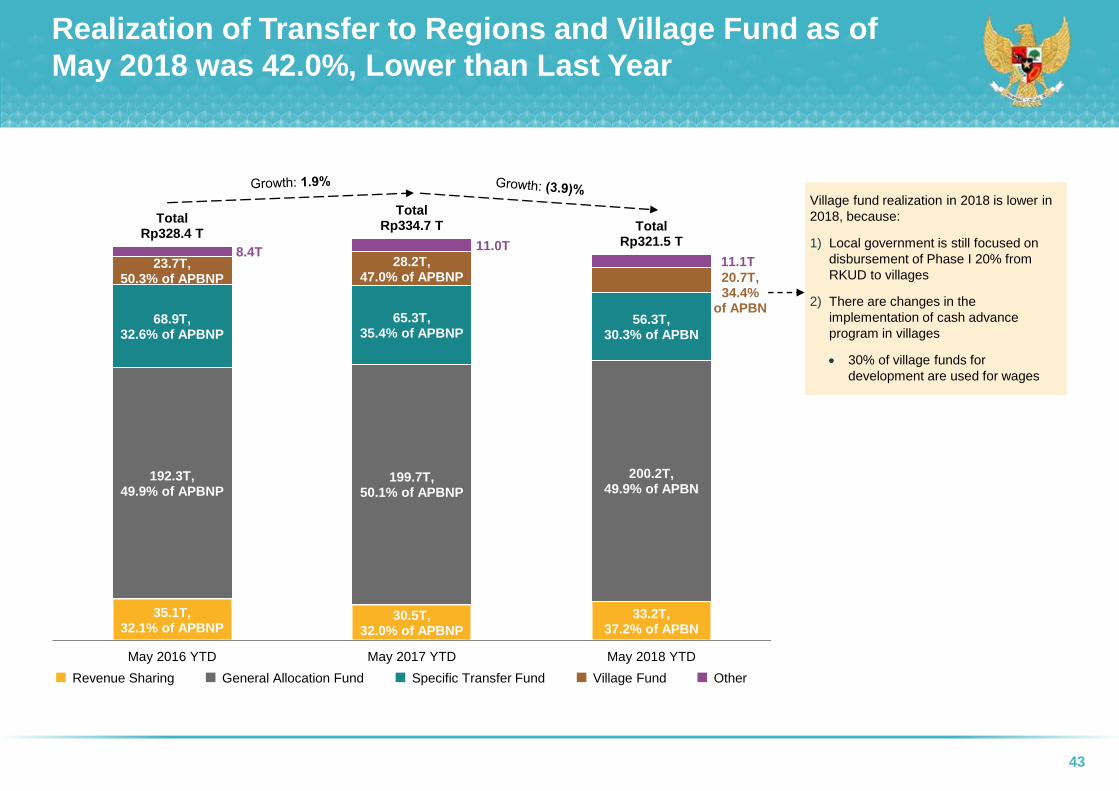

Realization of Transfer to Regions and Village Fund as of

May 2018 was 42.0%, Lower than Last Year

Revenue Sharing General Allocation Fund Specific Transfer Fund Village Fund Other

35.1T,32.1% of APBNP

30.5T,32.0% of APBNP

33.2T,37.2% of APBN

192.3T,49.9% of APBNP

199.7T,50.1% of APBNP

200.2T,49.9% of APBN

68.9T,32.6% of APBNP

65.3T,35.4% of APBNP

56.3T,30.3% of APBN

23.7T,50.3% of APBNP

28.2T,47.0% of APBNP 20.7T,

34.4%of APBN

8.4T 11.0T

11.1T

TotalRp328.4 T

TotalRp334.7 T Total

Rp321.5 T

May 2016 YTD May 2017 YTD May 2018 YTD

Village fund realization in 2018 is lower in

2018, because:

1) Local government is still focused on

disbursement of Phase I 20% from

RKUD to villages

2) There are changes in the

implementation of cash advance

program in villages

30% of village funds for

development are used for wages

44

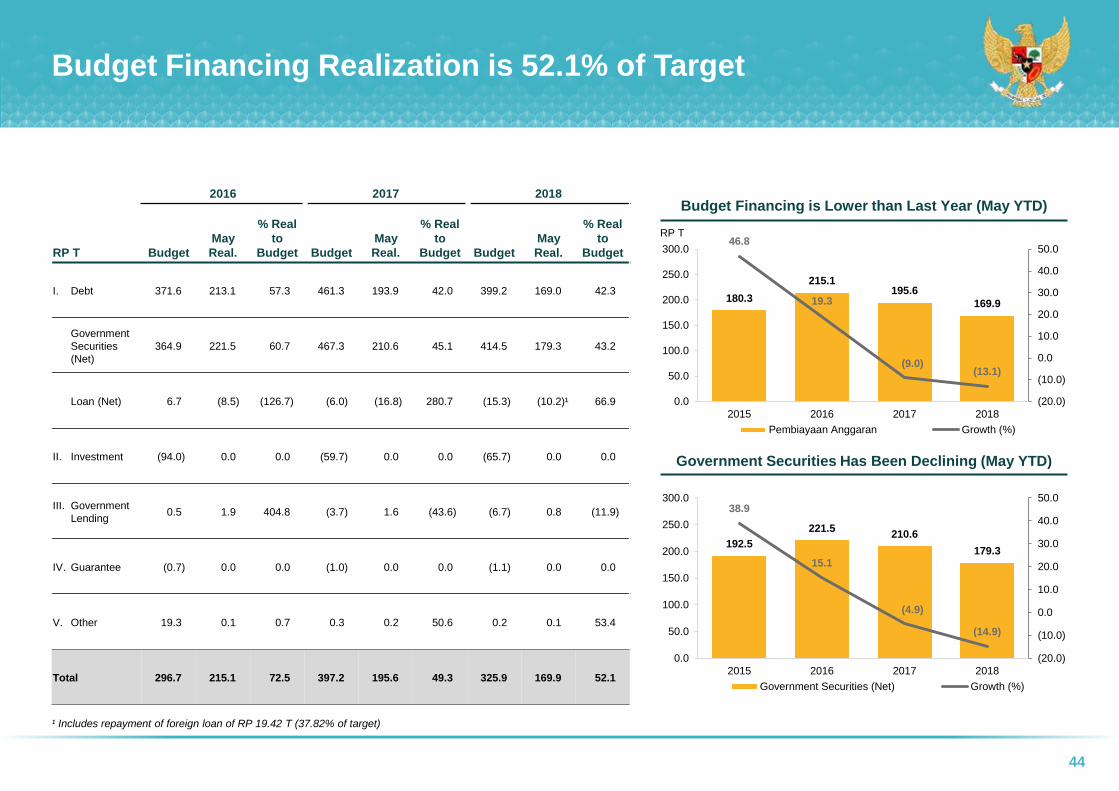

¹ Includes repayment of foreign loan of RP 19.42 T (37.82% of target)

Budget Financing Realization is 52.1% of Target

2016 2017 2018

RP T Budget

May

Real.

% Real

to

Budget Budget

May

Real.

% Real

to

Budget Budget

May

Real.

% Real

to

Budget

I. Debt 371.6 213.1 57.3 461.3 193.9 42.0 399.2 169.0 42.3

Government

Securities

(Net)

364.9 221.5 60.7 467.3 210.6 45.1 414.5 179.3 43.2

Loan (Net) 6.7 (8.5) (126.7) (6.0) (16.8) 280.7 (15.3) (10.2)¹ 66.9

II. Investment (94.0) 0.0 0.0 (59.7) 0.0 0.0 (65.7) 0.0 0.0

III. Government

Lending0.5 1.9 404.8 (3.7) 1.6 (43.6) (6.7) 0.8 (11.9)

IV. Guarantee (0.7) 0.0 0.0 (1.0) 0.0 0.0 (1.1) 0.0 0.0

V. Other 19.3 0.1 0.7 0.3 0.2 50.6 0.2 0.1 53.4

Total 296.7 215.1 72.5 397.2 195.6 49.3 325.9 169.9 52.1

180.3

215.1 195.6

169.9

46.8

19.3

(9.0)(13.1)

(20.0)

(10.0)

0.0

10.0

20.0

30.0

40.0

50.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

2015 2016 2017 2018

Pembiayaan Anggaran Growth (%)

Budget Financing is Lower than Last Year (May YTD)

Government Securities Has Been Declining (May YTD)

RP T

192.5

221.5 210.6

179.3

38.9

15.1

(4.9)

(14.9)

(20.0)

(10.0)

0.0

10.0

20.0

30.0

40.0

50.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

2015 2016 2017 2018

Government Securities (Net) Growth (%)

Fiscal Incentives to Support

Investment & Export

05Borobudur Temple in Central Java,

Indonesia

46

Taxation Incentive Scheme for Investment & Export (1/2)

Tax Incentive for

Upstream Oil & Gas

Gross Split & Cost

Recovery

Income Tax Incentive

for Local Incorporated

Bank

Income Tax and VAT

Incentives for the

development of

REIT/KIK DIRE

Income Tax Incentive

for Export Proceeds

Deposit

Income tax for deposit

interest from export

proceeds 0%-10%.

(normal tariff is 20%)

Tax Holiday

Income tax discount for

pioneer industries up to

100% between 5 to 20

years in accordance

with investment value.

Transition time for 2

years with tax deduction

of 50%

Tax Allowance

Investment allowance of

30% from investment

value (5% a year for 6

years), accelerated

depreciation and

amortization, Dividend

tariff for foreign

taxpayers up tp 10% or

according to tax treaty,

extended loss

compensation beyond 5

years (maximum 10

years)

Import Duties

Exemption Facility

For machineries and

capital goods for 2 years

and can be extended

(PMK 176/2009 stdtd

PMK 188/2015)

Import Duties Borne

By Government/

BMDTP

For specific industries

according to

recommendation from

Ministry of Industry for 1

year

Import Duty

Incentive for power plant

industries for public

VAT Exemption

For strategic goods

including macineries

and industrial equipment

Tax Incentive for General / Specific Sectors

47

Taxation Incentive Scheme for Investment & Export (2/2)

Special

Economic Zone

Facilities: Import

Duties, VAT,

Luxury goods

tax, excise, local

content

utilization

incentive, special

income tax

Industrial Zone

Facilities: tax

allowance, tax

holiday, import

duties, import

VAT

Free Trade

Zone

Exemption of

import duties,

VAT, luxury

goods tax,

excise

Bonded

Storage Area

(Kawasan

Penimbunan

Berikat)

Facilities: Import

duties, VAT,

luxury goods,

excise

Tax Incentive for Spatial/Zone

To reduce disparities and support economic growth

The ease of imports

used in the

production goods

which will be fully

exported

(Kemudahan Impor

Tujuan Ekspor)

Facilities: import duty

exemption, Import VAT

exemption of raw

materials used in

production goods will

be exported

Special Export

Assignment

(Penugasan Khusus

Ekspor)

Export financing for

specific sectors

through Indonesia’s

Export Financing

Agency (Lembaga

Pembiayaan Ekspor

Indonesia) that are

considered important

but commercially not

feasible

This assignment has

been given to PT INKA

(export of train coach

to Bangladesh), PT DI

(export of aircraft to

Africa) and small

medium industries

Bonded Storage Area

Facilities:

Import duties, VAT,

Import Income Tax

Special Tax Incentives to Support Export

48

Revision of Tax Holiday RegulationTo streamline administrative procedures and increase the effectiveness

PMK 103/2015 PMK 35/2018

Subject New Tax Payers New Investment

Percentage of tax

discount10-100%

100%

(single rate)

Timeline

5-15 years

can be extended up to 20 years with

Finance Minister’s discretion

Transition Not regulated 50% for 2 years

Coverage of Industry 8 pioneer industries 17 pioneer industries

Adjusted with investment value

Rp500 billion – less than Rp1 trillion : 5 years

Rp1 trillion - less than Rp5 trillion : 7 years

Rp5 trillion - less than Rp15 trillion : 10 years

Rp15 trillion - less than Rp30 trillion : 15 years

Minimum Rp30 trillion : 20 years

Medium Term Fiscal Objectives

& 2019 Macro-fiscal Framework

06Wayang – Traditional Puppet

Theaters, Indonesia

50

Macroeconomic Assumptions 2019

Indicators

2016 2017 2018 2019

Realized Realized APBN Outlook

a. Economic growth

(%, YoY)5.02 5.07 5.4 5.4 – 5.8

b. Inflation

(%, YoY)3.02 3.61 3.5 2.5 – 4.5

c. 3-Month Treasury Bill

(%)5.7 4.98 5.2 4.6 – 5.2

d. Exchange Rate

(Rp/US$)13,307 13,384 13,400 13,700 – 14,000

e. ICP

(US$/barrel)40.2 51.2 48 60 – 70

f. Oil Lifting

(thousands of barrel per

day)

829 803.91 800 722 – 805

g. Gas Lifting

(thousand barrels per day

oil equivalent)

1,180 1,142.33 1,200 1,210 – 1,300

51

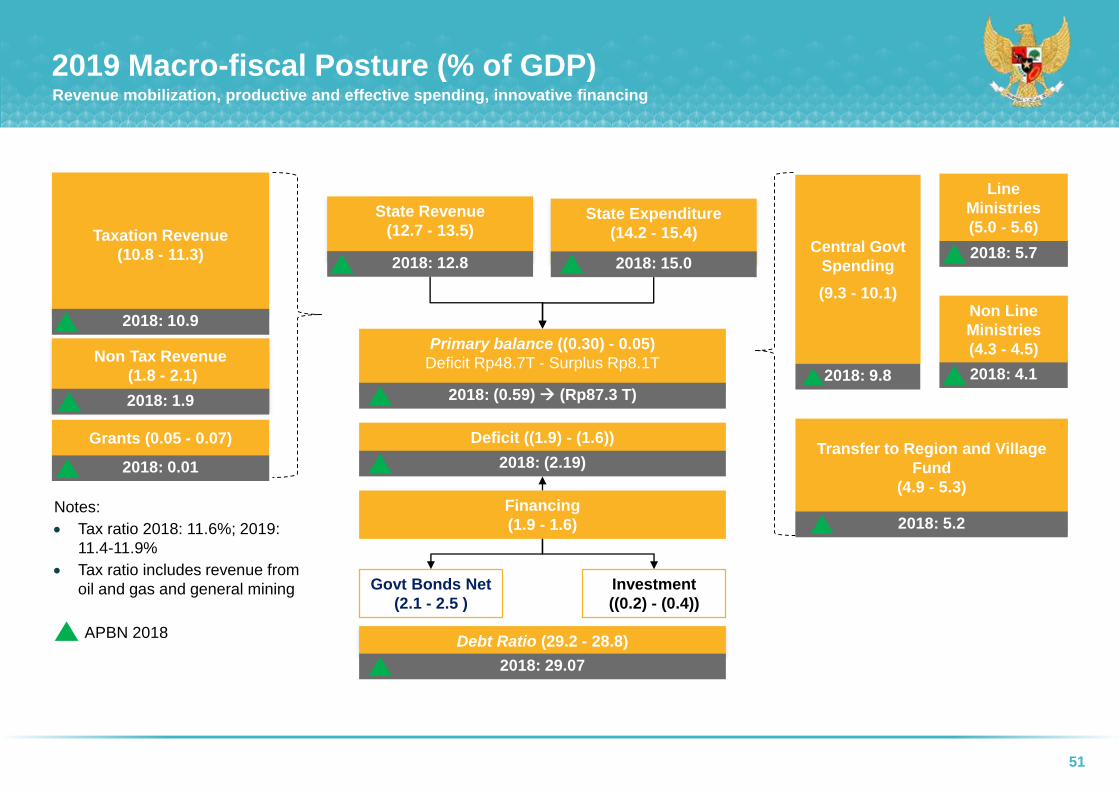

2019 Macro-fiscal Posture (% of GDP) Revenue mobilization, productive and effective spending, innovative financing

Taxation Revenue

(10.8 - 11.3)

Non Tax Revenue

(1.8 - 2.1)

State Revenue

(12.7 - 13.5)Central Govt

Spending

(9.3 - 10.1)

Transfer to Region and Village

Fund

(4.9 - 5.3)

Govt Bonds Net

(2.1 - 2.5 )

Deficit ((1.9) - (1.6))

Investment

((0.2) - (0.4))

Financing

(1.9 - 1.6)

Debt Ratio (29.2 - 28.8)

Grants (0.05 - 0.07)

Non Line

Ministries

(4.3 - 4.5)

Line

Ministries

(5.0 - 5.6)

Primary balance ((0.30) - 0.05)

Deficit Rp48.7T - Surplus Rp8.1T

State Expenditure

(14.2 - 15.4)

2018: 10.9

2018: 1.9

2018: 0.01

2018: 12.8

2018: 9.8

2018: 15.02018: 5.7

2018: 4.1

2018: 5.2

2018: (0.59) (Rp87.3 T)

2018: (2.19)

2018: 29.07

Notes:

Tax ratio 2018: 11.6%; 2019:

11.4-11.9%

Tax ratio includes revenue from

oil and gas and general mining

APBN 2018

52

1 Including revenue from oil & gas and general mining.2 Submitted to parliament for discussion.

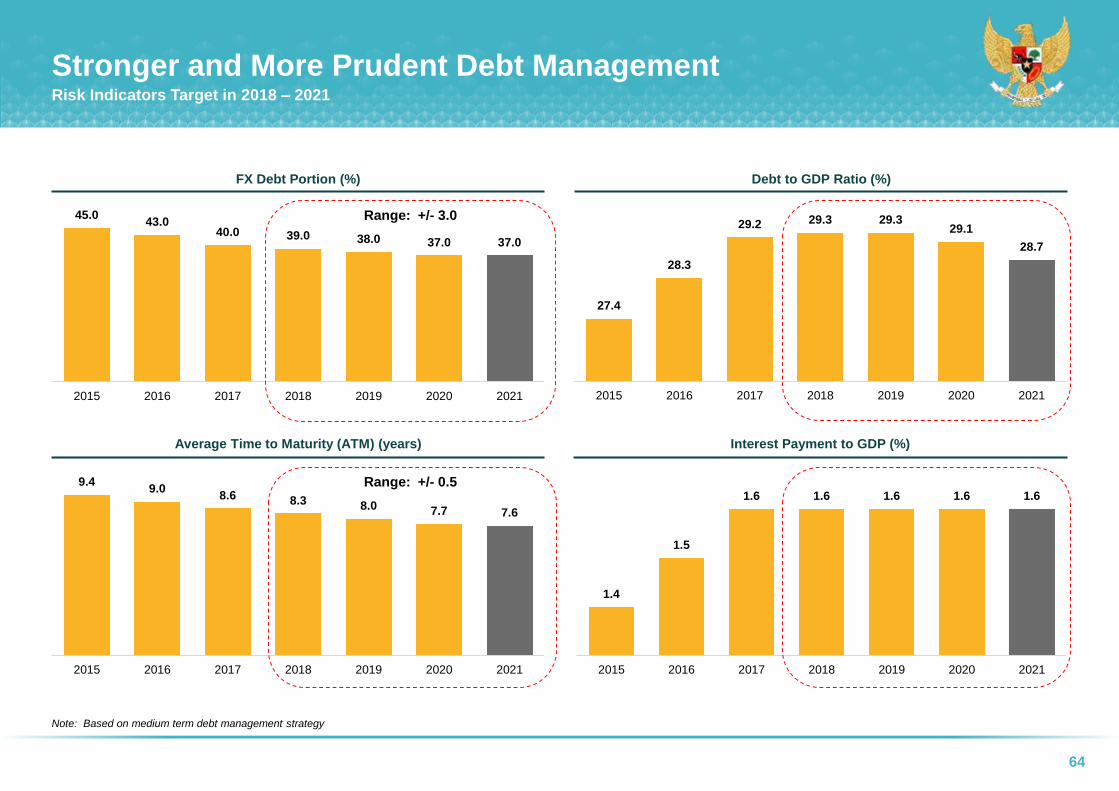

Medium Term Fiscal FrameworkFocusing on quality and productive spending, expanding fiscal space and sustainability

Items (% of GDP) APBN 2018 20192 2020 2021 2022

Revenue & Grants 12.8 12.7 – 13.5 12.7 – 13.9 13.5 – 14.0 13.6 – 14.4

Tax Ratio1 11.6 11.4 – 11.9 11.4 – 12.5 11.6 – 13.0 11.8 – 13.6

Total Spending 15.0 14.2 – 15.4 14.3 – 15.6 15.0 – 15.7 15.1 – 16.0

Capital Expenditure 1.4 1.5 - 1.7 1.8 – 2.3 2.2 – 2.7 2.3 – 3.0

Primary Balance (0.59) 0.05 - (0.30) 0.05 – 0.1 0.10 – 0.01 0.1 – 0.05

Budget Deficit (2.19) (1.6) - (1.9) (1.6) - (1.7) (1.5) - (1.7) (1.5) - (1.6)

Debt Ratio 29.07 28.8 – 29.2 28.5 - 28.6 27.8 – 28.3 26.3 – 27.9

Strengthening quality of spending by increasing productive avenues

Enlarging fiscal space through revenue increase

Efficiencies in non-priority spending

Developing creative and innovative financing

Manageable deficit and debt level

Positive primary balance in 2020

Monetary Policy and

Banking Sector

07Raja Ampat in West Papua,

Indonesia

54

(0.33)

(0.85)

(1.19)

(1.67)

(1.76)

(1.91)

(2.08)

(2.75)

(3.48)

(3.90)

(6.26)

(8.43)

(1.50)

(0.85)

(1.22)

0.13

(1.02)

(1.41)

(1.46)

(1.11)

(1.12)

(3.57)

(5.84)

(10.15)

(12.00) (10.00) (8.00) (6.00) (4.00) (2.00) 0.00 2.00

PHP

KRW

CNY

IDR

SGD

MYR

THB

INR

ZAR

EUR

BRL

TRY

May vs April 2018

Point to Point Average

Source: BPS; Bank Indonesia

Stable Monetary EnvironmentConducive Monetary Environment Supporting the Economy

8.38 8.36

3.35 3.023.61 3.23

2013 2014 2015 2016 2017 May-18

(YoY %)

12,1

70

12,3

85

13,7

85

13,4

73

13,5

68

13,8

95

10,4

45

11,8

76

13,3

92

13,3

05

13,3

85

14,0

43

2013 2014 2015 2016 2017 May-18

EOP Average

US broad based appreciation has triggered regional depreciation, including the Rupiah. Compared to other countries, the Rupiah exchange rate depreciation is more limited

underpinned by Indonesia’s sound economic fundamentals and Bank Indonesia’s foreign exchange stabilization policies in the form of dual intervention and policy response in

the May Board meeting.

Rupiah Depreciated Due To USD Broad Based AppreciationInflation Remained Under Control

Limited Depreciation Compared to Other Countries

As of May 2018

Managed inflation is observed throughout

Indonesia, well within the target range of

3.5±1% in the majority of the regions.

10.06%

9.57%

7.39%

7.33%

6.41%

5.46%

4.43%

3.42%

(0.18)%