republic of panama fiscal performance third quarter 2016 · pdf filerepublic of panama fiscal...

TRANSCRIPT

Republic of Panama

Fiscal Performance

Third Quarter 2016

Dulcidio De La GuardiaMinister of Economy and Finance

Iván ZarakVice Minister of Economy

Eyda Varela de ChinchillaVice Minister of Finance

January 2017

Contents:

Macroeconomic Overview

2

Fiscal Performance

Debt Profile

Future Prospects

Final Remarks

1

2

3

4

5

Contents:

Macroeconomic Overview

3

Fiscal Performance

Debt Profile

Future Prospects

Final Remarks

1

2

3

4

5

Panama continues to be one of the top performers of the region with a forecasted GDP growth for 2016 of 5.2% according to the IMF.

4

Economic Indicators

Foreign Direct Investment

Macroeconomic Overview1

-1.1%

1.3%

8.5%

12.1%

8.6%

1.6%

5.8%

11.8%

9.2%

6.6% 6.1% 5.8% 5.2%5.9%

3.1% 3.4%

Latam Panama World

Projected GDP growth for 2016 and 2017 remains positive despite global economic conditions.

Inflation levels are slowly rising, but still remain low due to oil prices and the strength of the dollar.

Source: IMF(F): forecasted

20%

18%

12%12%

8%

8%

5%

5%

4%

3% 3% 3%

Trade Construction

Real Estate and Business Services Communications and Transport

Other Other Non Market Production

Manufacturing Financial Intermediation

Hotels and Restaurants Electricity and Water

Investment Ratings

Agency Rating Outlook

Moody´s Baa2 Stable

Fitch BBB Stable

S&P BBB Stable

Source: INEC

Diversified economy: no sector accounts for more than 20% of GDP.

Investment Grade and Dollarized Economy

Logistics Hub and Tourism Industry

Competitive Advantages: Panama

Canal

Steadily Growing Financial Sector

Other Strengths:

Source: INEC

3.22.1

4.2

8.8

2.4

3.5

5.9 5.7

4.02.6

0.1 0.5

GDP by sector, as of September 2016 GDP Growth (%)

Inflation (%)

The path to fiscal consolidation is supported by improvements in tax collection, focused government expenditures, a Social Fiscal Responsibility Law with well-established limits, and a declining current account deficit.

5

Economic Indicators

Foreign Direct Investment

Macroeconomic Overview1

NFPS Cash Deficit is within the limits of the Social Fiscal Responsibility Law.The completion of large infrastructure projects contributed to a small increase in the openunemployment ratio, but will generate more growth in other sectors of the economy.

The increase in government revenues is due in part to improvements in taxcollection.

2.4

3.2

2.3

1.7

2013 2014 2015 3Q-2016

NFPS Cash Deficit (% of GDP) Open Unemployment (% of economically active population)

The debt-to-GDP ratio shows the path of the Central Government deficit.

Source: MEF, INEC, Office of Economic & Social Analysis.

Debt in US$ million and as a percentage of GDPGovernment Revenues (US$ million)

10,225 10,656

7,586 8,236

4,999 5,037 3,712 4,048

2014 2015 3Q-2015 3Q-2016

NFPS Total Tax Revenues

6.7

4.74.2

5.24.7

2.9 3.0 3.13.5 3.8

4.4

9,317 9,344 8,999 9,611 10,404 11,602

13,022 14,45016,945

18,99720,308

54%47%

37% 36% 36%

34% 33% 32% 34% 36% 37%

0%

10%

20%

30%

40%

50%

60%

0

5,000

10,000

15,000

20,000

25,000

Net Debt Net Debt/GDP

6

Economic Indicators

Foreign Direct Investment

Macroeconomic Overview1

3,943

4,458 4,494

3,576

4,211

2013 2014 2015 3Q-2015 3Q-2016

∆: +17.8%

-2,181

-1,544-1,280

3Q-2014 3Q-2015 3Q-2016

Foreign Direct Investment (FDI) was 17.8% higher in the third quarter of2016 than in the third quarter of 2015.

The Current Account Deficit (CAD) declined 17.1% in Q3-2016 compared toQ3-2015, in part due to the lower cost of imports due to global conditions.

Colombia, 29%

United States, 25%Switzerland, 7%

Mexico, 7%

Ecuador, 6%

Others, 26%

OTIS

PROCTER & GAMBLE

Western Union

CATERPILLAR

TETRA PAK

GRAINGER

HUAWEI TECHNOLOGIES

Wrigley

PHILIPS

ADIDAS

UNILEVER

EVERGREENGENERAL ELECTRIC

SAMSUNG GROUP

SONY CORPORATION

3M

TELEFÓNICA

Baxter

MARS

Johnson & Johnson

Supportive business policies have led to stronger and more diversified FDIinflows.

FDI inflows by country (average 2013-2015)

CAD in US$ million

FDI in US$ million

Source: MEF, INEC

Over 70 international enterprises have established headquarters inPanama.

Contents:

Macroeconomic Overview

7

Fiscal Performance

Debt Profile

Future Prospects

Final Remarks

1

2

3

4

5

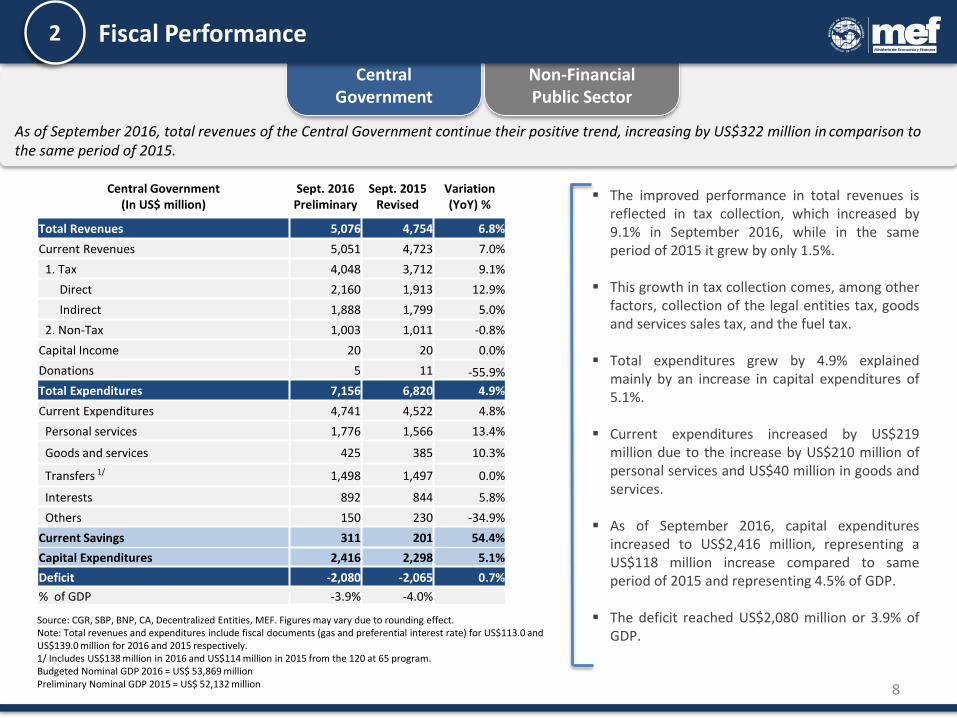

As of September 2016, total revenues of the Central Government continue their positive trend, increasing by US$322 million in comparison to the same period of 2015.

8

Source: CGR, SBP, BNP, CA, Decentralized Entities, MEF. Figures may vary due to rounding effect.Note: Total revenues and expenditures include fiscal documents (gas and preferential interest rate) for US$113.0 and US$139.0 million for 2016 and 2015 respectively.1/ Includes US$138 million in 2016 and US$114 million in 2015 from the 120 at 65 program.Budgeted Nominal GDP 2016 = US$ 53,869 millionPreliminary Nominal GDP 2015 = US$ 52,132 million

The improved performance in total revenues isreflected in tax collection, which increased by9.1% in September 2016, while in the sameperiod of 2015 it grew by only 1.5%.

This growth in tax collection comes, among otherfactors, collection of the legal entities tax, goodsand services sales tax, and the fuel tax.

Total expenditures grew by 4.9% explainedmainly by an increase in capital expenditures of5.1%.

Current expenditures increased by US$219million due to the increase by US$210 million ofpersonal services and US$40 million in goods andservices.

As of September 2016, capital expendituresincreased to US$2,416 million, representing aUS$118 million increase compared to sameperiod of 2015 and representing 4.5% of GDP.

The deficit reached US$2,080 million or 3.9% ofGDP.

Central Government (In US$ million)

Sept. 2016Preliminary

Sept. 2015Revised

Variation (YoY) %

Total Revenues 5,076 4,754 6.8%

Current Revenues 5,051 4,723 7.0%

1. Tax 4,048 3,712 9.1%

Direct 2,160 1,913 12.9%

Indirect 1,888 1,799 5.0%

2. Non-Tax 1,003 1,011 -0.8%

Capital Income 20 20 0.0%

Donations 5 11 -55.9%

Total Expenditures 7,156 6,820 4.9%

Current Expenditures 4,741 4,522 4.8%

Personal services 1,776 1,566 13.4%

Goods and services 425 385 10.3%

Transfers 1/ 1,498 1,497 0.0%

Interests 892 844 5.8%

Others 150 230 -34.9%

Current Savings 311 201 54.4%

Capital Expenditures 2,416 2,298 5.1%

Deficit -2,080 -2,065 0.7%

% of GDP -3.9% -4.0%

Central Government

Non-Financial Public Sector

Fiscal Performance2

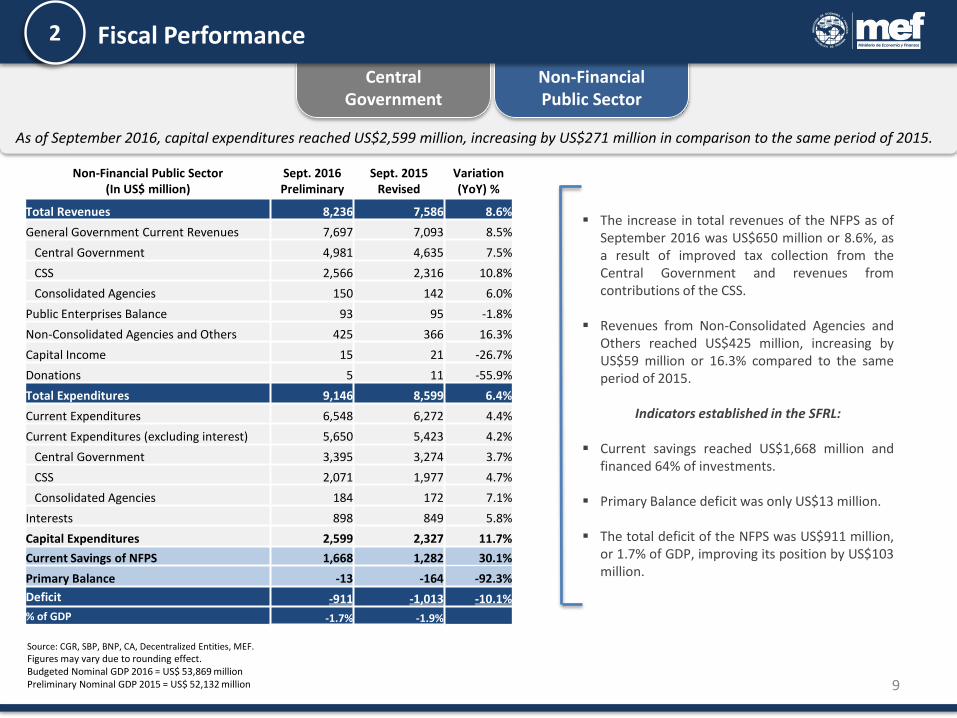

As of September 2016, capital expenditures reached US$2,599 million, increasing by US$271 million in comparison to the same period of 2015.

9

The increase in total revenues of the NFPS as ofSeptember 2016 was US$650 million or 8.6%, asa result of improved tax collection from theCentral Government and revenues fromcontributions of the CSS.

Revenues from Non-Consolidated Agencies andOthers reached US$425 million, increasing byUS$59 million or 16.3% compared to the sameperiod of 2015.

Indicators established in the SFRL:

Current savings reached US$1,668 million andfinanced 64% of investments.

Primary Balance deficit was only US$13 million.

The total deficit of the NFPS was US$911 million,or 1.7% of GDP, improving its position by US$103million.

Source: CGR, SBP, BNP, CA, Decentralized Entities, MEF.Figures may vary due to rounding effect.Budgeted Nominal GDP 2016 = US$ 53,869 millionPreliminary Nominal GDP 2015 = US$ 52,132 million

Non-Financial Public Sector(In US$ million)

Sept. 2016Preliminary

Sept. 2015Revised

Variation (YoY) %

Total Revenues 8,236 7,586 8.6%

General Government Current Revenues 7,697 7,093 8.5%

Central Government 4,981 4,635 7.5%

CSS 2,566 2,316 10.8%

Consolidated Agencies 150 142 6.0%

Public Enterprises Balance 93 95 -1.8%

Non-Consolidated Agencies and Others 425 366 16.3%

Capital Income 15 21 -26.7%

Donations 5 11 -55.9%

Total Expenditures 9,146 8,599 6.4%

Current Expenditures 6,548 6,272 4.4%

Current Expenditures (excluding interest) 5,650 5,423 4.2%

Central Government 3,395 3,274 3.7%

CSS 2,071 1,977 4.7%

Consolidated Agencies 184 172 7.1%

Interests 898 849 5.8%

Capital Expenditures 2,599 2,327 11.7%

Current Savings of NFPS 1,668 1,282 30.1%

Primary Balance -13 -164 -92.3%

Deficit -911 -1,013 -10.1%

% of GDP -1.7% -1.9%

Central Government

Non-Financial Public Sector

Fiscal Performance2

Contents:

Macroeconomic Overview

10

Fiscal Performance

Debt Profile

Future Prospects

Final Remarks

1

2

3

4

5

11

Portfolio Composition

Risk Profile

CapitalMarkets

Debt Profile3

77%

22%1%

External Debt

DomesticCapital Market

Other InternalFinancing

69%

31%

Loans

Bonds

97% 2.8%

US$

Othercurrencies

85% 15%

Fixed

Floating

Debt Profile as of September 2016Since 2010, the Weighted Average Cost of Debt (WACD) has gradually decreased due to market conditions and the debt strategy of this administration…

…which is led by medium-term issuances in the capital markets and similar interestrate movement as a 10-year UST.

WACD (2010-2016)

JPY 2.68%

KRW 0.05%

EUR 0.03%

Source: MEF - DFP

6.6% 6.1% 5.9% 5.5% 5.2% 5.0% 4.9%

3.7% 3.9%4.7% 4.6% 4.8% 4.3%

4.4%

6.3%

5.8% 5.6%5.3% 5.1% 4.8% 4.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

4%

14%

24%

34%

44%

54%

64%

74%

84%

94%

104%

2010 2011 2012 2013 2014 2015 3Q-16

External Internal WACD

0.00

1.00

2.00

3.00

4.00

5.00

2010 2011 2012 2013 2014 2015 2016

Yie

ld (

%)

UST 10 years UST 30 years

UST 10 year and 30 year comparison (2010-2016)

Portfolio Composition

Risk Profile

Capital Markets

Debt Profile3

-50

50

150

250

350

450

550

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16

Bas

is p

oin

ts (

BP

S)

EMBIG EMBIG COLOMBIA EMBIG PERU EMBIG MEXICO EMBIG PANAMA

Panama Papers 1 - 3 April Waked Case 3 May

Panama Papers 2 - 5 May

BREXIT - 23 June

FED Meeting 21 Sept

0

50

100

150

200

250

Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16

Bas

is p

oin

ts (

BP

S)

PANAMA USD CDS 10Y PANAMA USD CDS 5Y PANAMA USD CDS 2Y

Panama Papers 1 - 3 April Waked Case 3 May

Panama Papers 2 - 5 May

BREXIT - 23 June

FED Meeting 21 Sept

12

URU 2022

URU 2024 URU 2027

URU 2036URU 2050

PAN 2020PAN 2025 PAN 2028

PAN 2036 PAN 2053

MEX 2020

MEX 2023 MEX 2026

MEX 2040 MEX 2046

PER 2019

PER 2027 PERU 2027

PER 2037PER 2050

0

50

100

150

200

250

300

350

Panama 2020 Panama 2025 Panama 2028 Panama 2036 Panama 2053

Inte

rpo

late

d G

Sp

read

(b

ps)

Comparable Sovereign Bonds

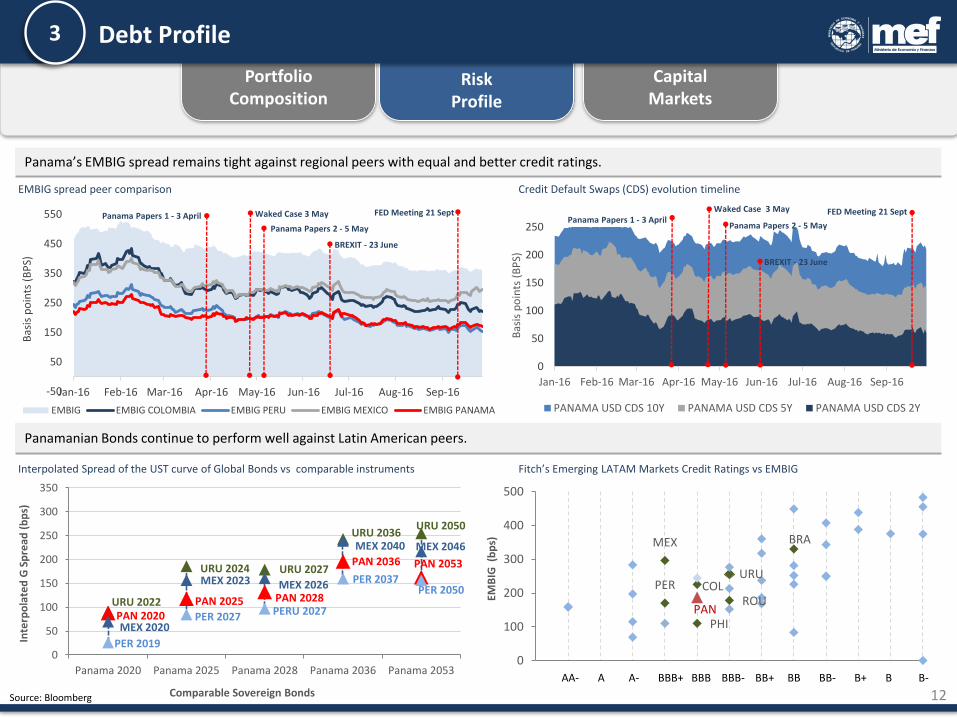

Panama’s EMBIG spread remains tight against regional peers with equal and better credit ratings.

Panamanian Bonds continue to perform well against Latin American peers.

Source: Bloomberg

Fitch’s Emerging LATAM Markets Credit Ratings vs EMBIG

Credit Default Swaps (CDS) evolution timelineEMBIG spread peer comparison

Interpolated Spread of the UST curve of Global Bonds vs comparable instruments

MEX

PERURU

PANPHI

COLROU

BRA

0

100

200

300

400

500

0 1 2 3 4 5 6 7 8 9 10 11 12

EMB

IG (

bp

s)

AA- A A- BBB+ BBB BBB- BB+ BB BB- B+ B B-

13

Portfolio Composition

RiskProfile

Capital Markets

Debt Profile3

The trading volume in the secondary market continues increasing due to efforts to deepen the domestic capital market.

Trading Volumes (in US$ million)

Outstanding Price Yield

669.6 106.0 1.4

607.7 102.1 2.2

665.2 108.9 2.7

1,364.0 114.2 2.9

700.0 108.9 3.6

2018 Note

2019 Note

2021 Note

2022 Bond

2024 Bond

Local Financial Instruments as of Sept 30th 2016

Spread vs UST

72

135

165

169

215

(US$ million)

2018

2019

20212022

2024

0.25

1.25

2.25

3.25

4.25

0 2 4 6 8

Yie

ld (

%)

Duration (years)

Internal Curve June 2016

Internal Curve September 2016 77 bps

Source: MEF - DFP

312

621

763 768

533 455

1,161

2011 2012 2013 2014 2015 3Q-15 3Q-16

Market Makers

Market Makers Candidates

(As of Sept. 2016)

Macroeconomic Overview

14

Fiscal Performance

Debt Profile

Future Prospects

Final Remarks

1

2

3

4

5

15

Approved 2017Budget

Investment Opportunities

Future Prospects4

Source: MEF

Sector Law N°69 (Budget 2016) Law N°63 (Budget 2017)

Tax Revenues 5,459 million 5,875 million

Panama Canal Authority Contributions 1,060 million 1,600 million

Adjusted NFPS Fiscal Deficit 1.5% (808 million) 1.0% (585 million)

NFPS CAPEX 4,538 million 5,063 million

Indicator 2016 2017

GDP Growth 6.3% 6.0%

Inflation 1.9% 1.1%

Nominal GDP 53,869 million 58,633 million

Economic Projections used for the budget elaboration

Budget

Panama continues investing more than 17% of GDP in education, health, and justice.

16

Approved 2017Budget

Investment Opportunities

Future Prospects4

Source: MEF

Budget Allocation by Area and Activity Sector (In US$ Million)

Sector 2016 2017

Social Services 9,406 9,026

Education and Culture 2,318 2,407

Health 3,622 3,864

Work 83 88

Protection and Social Security 2,049 2,155

Housing and Development 1,335 512

Environment and Technology 187 210

Environmental Development 64 67

Biodiversity Conservation 68 79

Technological Development 55 64

Infrastructure 2,318 2,667

Transport and Communications 2,092 2,399

Energy 225 269

Production 492 496

Agricultural 293 301

Industry, Commerce & Tourism 199 195

Financial Services 2,640 3,721

Banking and Financing 2,637 3,717

Insurance 3 3

Government and Justice 3,260 3,443

General Public Administration 2,139 2,220

Public Order and Security 751 823

Justice 371 400

Others 1,823 2,112

Total Budget 20,126 21,676

Protection & Social Security

US$2,155 million

56%4%

Health

US$3,864 million56%7%

4

Education & Culture

US$2,407 million56%4%

Financial Services

US$3,721 million

6%

Government & Justice

US$3,443 million

56%6%

Infrastructure

US$2,667 million

56%5%

Allocation by Sector (% of GDP)

17

Approved 2017Budget

InvestmentOpportunities

Future Prospects4

Source: MEF - DFP

Tourism Mining Energy Logistics

MINING• Copper mine under

construction by First Quantum:

• 50 billion pounds of copper; 12 million ounces of gold; and 250 tons of molybdenum expected

• Complete by 2017

• $2.0 billion in exports by 2018.

TOURISM

• Daily flights to 81 cities in America and Europe.

• Tocumen will double traffic to 15 million passengers by 2019.

• Panama is becoming the shopping capital of South America.

• New beach resorts under construction.

ENERGY HUB• Chevron and Vopak are

improving and enhancing a liquid energy terminal on the Atlantic end of Panama Canal

• Two LNG Terminals

• AES (Gas Natural Atlantic); $800 million investment, begins operations in 2018.

• Gas to Power Panama (GTPP); $900 million investment, begins operations in 2019.

LOGISTICS

• New port in the Pacific is under construction by the Panama Canal.

• PSA (formerly known as Port of Singapore Authority) is investing $450 million to enhance the Pacific terminal.

• The expanded Canal will open new opportunities for value-added logistics.

Macroeconomic Overview

18

Fiscal Performance

Debt Profile

Future Prospects

Final Remarks

1

2

3

4

5

19

2.

3.The NFPS deficit decreased by 10.1% to US$911 million in September 2016 compared tothe same period of 2015, reflecting the government’s commitment to the Social FiscalResponsibility Law.

1.Panama’s stable economic growth rate, supported by an environment of low inflation,unemployment and new opportunities for investments, exceeds the growth of the regionwith a GDP growth forecast for 2016 and 2017 of 5.2% and 5.9% respectively.

As of September 2016, central government revenues increased by 6.8% compared to thesame period in 2015, mainly due to a 9.1% increase in tax collection.

4.

Panama´s risk indicators continue to perform well against Latin American peers,reinforcing international investors’ trust in the country.

Current market conditions coupled with an efficient debt management strategy has led toa lower average cost of debt.

5.

Final Remarks5

This presentation does not constitute or form part of, and should not be construed as, an offer or invitation to sell securities of the Republic of

Panama (“Republic”), or the solicitation of an offer to subscribe for or purchase securities of the Republic, and nothing contained herein shall form

the basis of or be relied on in connection with any contract or commitment whatsoever. Any decision to purchase any securities of the Republic

should be made solely on the basis of conditions of the securities and the information to be contained in the prospectus, prospectus supplement or

equivalent disclosure document produced in connection with the offering of such securities. Prospective investors are required to make their own

independent investigations and appraisals of the business and financial condition of the Republic and the nature of any securities of the Republic

before taking any investment decision with respect to securities of the Republic. The contents of this presentation should not be the basis for

making investment decisions, nor should the presentation be construed as a recommendation to engage in investment transactions. This

presentation is not related to the provision of advisory services regarding investment, tax, legal, financial, accounting, consulting or any other

related services, nor is a recommendation being provided to buy, sell or purchase any good or product.

This presentation contains forward-looking statements, which include all statements other than statements of historical facts, including, without

limitation, any statements preceded by, followed by or including the words “targets,” “believes,” “projects,” “estimates,” “expects,” “aims,” “intends,”

“may,” “anticipates,” “would,” “could” or similar expressions or the negative thereof. Such forward-looking statements involve known and unknown

risks, uncertainties and other important factors beyond the Republic's control that could cause the Republic’s actual results, performance or

achievements to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements.

These forward-looking statements speak only as at the date of this presentation. The financial information in this presentation should be used for

reference purposes only with the understanding that market conditions may change and past performance is not an indicator of future performance.

The Republic expressly disclaims any obligation or undertaking to disseminate any updates or revisions to any forward-looking statements

contained herein to reflect any change in its expectations with regard thereto or any change in events, conditions or circumstances on which any of

such statements are based. However, the Republic reserves the right to update, amend or delete information contained in this presentation without

prior notice.

The Republic, the Ministry of Economy and Finance (MEF) and the Public Financing Directorate of MEF do not assume legal responsibility nor will

they be liable for the way that this information may be interpreted, including any inaccuracies, assumptions, or projections related to this

information. The Republic, MEF and the Public Credit Directorate of MEF will not be liable for any loss or damage that directly or indirectly arises

with respect to the use of this information.

LEGAL DISCLAIMER

21