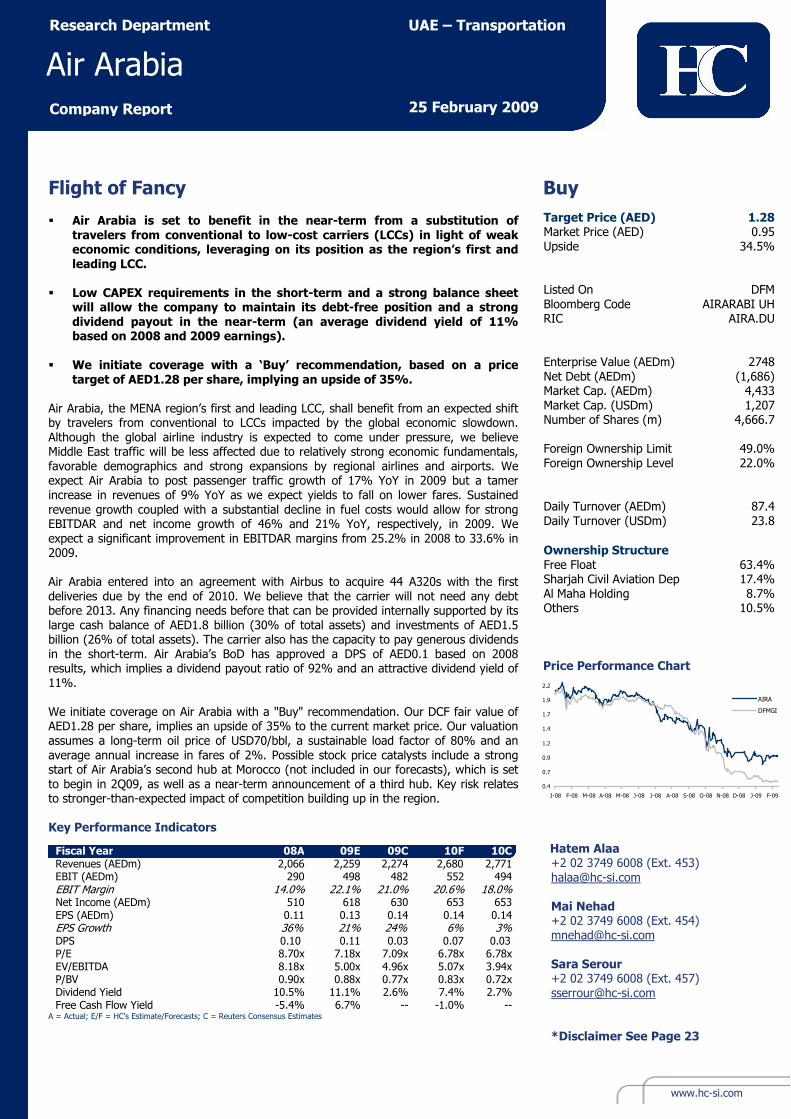

research department uae – transportation air arabia · company report 25 february 2009 ... other...

TRANSCRIPT

www.hc-si.com

Flight of Fancy � Air Arabia is set to benefit in the near-term from a substitution of

travelers from conventional to low-cost carriers (LCCs) in light of weak economic conditions, leveraging on its position as the region’s first and

leading LCC.

� Low CAPEX requirements in the short-term and a strong balance sheet will allow the company to maintain its debt-free position and a strong

dividend payout in the near-term (an average dividend yield of 11% based on 2008 and 2009 earnings).

� We initiate coverage with a ‘Buy’ recommendation, based on a price

target of AED1.28 per share, implying an upside of 35%.

Air Arabia, the MENA region’s first and leading LCC, shall benefit from an expected shift by travelers from conventional to LCCs impacted by the global economic slowdown.

Although the global airline industry is expected to come under pressure, we believe Middle East traffic will be less affected due to relatively strong economic fundamentals,

favorable demographics and strong expansions by regional airlines and airports. We expect Air Arabia to post passenger traffic growth of 17% YoY in 2009 but a tamer

increase in revenues of 9% YoY as we expect yields to fall on lower fares. Sustained

revenue growth coupled with a substantial decline in fuel costs would allow for strong EBITDAR and net income growth of 46% and 21% YoY, respectively, in 2009. We

expect a significant improvement in EBITDAR margins from 25.2% in 2008 to 33.6% in 2009.

Air Arabia entered into an agreement with Airbus to acquire 44 A320s with the first

deliveries due by the end of 2010. We believe that the carrier will not need any debt before 2013. Any financing needs before that can be provided internally supported by its

large cash balance of AED1.8 billion (30% of total assets) and investments of AED1.5 billion (26% of total assets). The carrier also has the capacity to pay generous dividends

in the short-term. Air Arabia’s BoD has approved a DPS of AED0.1 based on 2008 results, which implies a dividend payout ratio of 92% and an attractive dividend yield of

11%.

We initiate coverage on Air Arabia with a "Buy" recommendation. Our DCF fair value of AED1.28 per share, implies an upside of 35% to the current market price. Our valuation

assumes a long-term oil price of USD70/bbl, a sustainable load factor of 80% and an

average annual increase in fares of 2%. Possible stock price catalysts include a strong start of Air Arabia’s second hub at Morocco (not included in our forecasts), which is set

to begin in 2Q09, as well as a near-term announcement of a third hub. Key risk relates to stronger-than-expected impact of competition building up in the region.

Buy

Price Performance Chart

0.4

0.7

0.9

1.2

1.4

1.7

1.9

2.2

J-08 F-08 M-08 A-08 M-08 J-08 J-08 A-08 S-08 O-08 N-08 D-08 J-09 F-09

AIRA

DFMGI

Target Price (AED) 1.28 Market Price (AED) 0.95

Upside 34.5%

Listed On DFM

Bloomberg Code AIRARABI UH RIC AIRA.DU

Enterprise Value (AEDm) 2748

Net Debt (AEDm) (1,686) Market Cap. (AEDm) 4,433

Market Cap. (USDm) 1,207 Number of Shares (m) 4,666.7

Foreign Ownership Limit 49.0%

Foreign Ownership Level 22.0%

Daily Turnover (AEDm) 87.4

Daily Turnover (USDm) 23.8

Ownership Structure

Free Float 63.4% Sharjah Civil Aviation Dep 17.4%

Al Maha Holding 8.7% Others 10.5%

Key Performance Indicators

A = Actual; E/F = HC's Estimate/Forecasts; C = Reuters Consensus Estimates

Fiscal Year 08A 09E 09C 10F 10C Revenues (AEDm) 2,066 2,259 2,274 2,680 2,771 EBIT (AEDm) 290 498 482 552 494 EBIT Margin 14.0% 22.1% 21.0% 20.6% 18.0% Net Income (AEDm) 510 618 630 653 653 EPS (AEDm) 0.11 0.13 0.14 0.14 0.14 EPS Growth 36% 21% 24% 6% 3% DPS 0.10 0.11 0.03 0.07 0.03 P/E 8.70x 7.18x 7.09x 6.78x 6.78x EV/EBITDA 8.18x 5.00x 4.96x 5.07x 3.94x P/BV 0.90x 0.88x 0.77x 0.83x 0.72x Dividend Yield 10.5% 11.1% 2.6% 7.4% 2.7% Free Cash Flow Yield -5.4% 6.7% -- -1.0% --

Hatem Alaa +2 02 3749 6008 (Ext. 453)

Mai Nehad +2 02 3749 6008 (Ext. 454)

Sara Serour +2 02 3749 6008 (Ext. 457)

*Disclaimer See Page 23

UAE – Transportation Research Department

25 February 2009 Company Report

Air Arabia

UAE – Transportation

2

Financial Statements and Ratios

AED Million 2008a 2009e 2010f 2011f 2012f 2013f

Income Statement Number of Passengers (000) 3,561 4,180 4,900 5,782 6,727 8,098

Passenger Revenue 1,937 2,100 2,489 2,996 3,555 4,365

Other Revenue 129 159 190 229 272 334

Total Revenue 2,066 2,259 2,680 3,225 3,827 4,699

Revenue Growth 61% 9% 19% 20% 19% 23%

Staff Costs (282) (331) (402) (488) (582) (714)

Fuel Costs (814) (656) (777) (963) (1,176) (1,486)

Maintenance (146) (180) (212) (253) (298) (362)

Handling, Landing and Overflying Charges (189) (208) (245) (291) (342) (415)

Other Operating Costs (115) (125) (143) (177) (215) (272)

EBITDAR 521 758 902 1,054 1,215 1,451

EBITDAR Growth 23% 46% 19% 17% 15% 19%

EBITDAR Margin 25.2% 33.6% 33.6% 32.7% 31.7% 30.9%

Lease Rentals (195) (209) (264) (281) (298) (315)

EBITDA 326 550 637 773 917 1,135

Depreciation and Amortization (36) (52) (86) (143) (202) (307)

EBIT 290 498 552 630 715 829

Net Interest Income (Expense) 164 115 97 62 42 (43)

Other Income (Expense) 56 5 5 5 6 7

Net Income 510 618 653 697 763 793

Net Income Growth 35.7% 21.2% 5.8% 6.7% 9.5% 3.8% Net Margin 24.7% 27.3% 24.4% 21.6% 19.9% 16.9%

Balance Sheet

Cash and Equivalents 1,767 1,686 1,204 649 609 971

Other Current Assets 243 245 248 252 257 263

Total Current Assets 2,010 1,931 1,452 901 866 1,234

Net Property, Plant & Equipment 972 1,194 1,825 3,251 4,633 7,252

Investments 1,523 1,523 1,523 1,015 254 127

Goodwill and Other Intangibles 1,282 1,282 1,282 1,282 1,282 1,282

Other Non-Current Assets 74 102 133 168 207 253

Total Non-Current Assets 3,851 4,100 4,763 5,715 6,376 8,913

Total Assets 5,862 6,030 6,224 6,617 7,242 10,147

Total Current Liabilities 930 968 823 699 747 800

Total Non-Current Liabilities 14 22 24 28 32 2,290

Total Shareholders' Equity 4,917 5,040 5,367 5,890 6,463 7,057

Cash Flow Statement

Net Income 510 618 653 697 763 793

Non-Cash Items 41 57 86 144 204 309

Net Change in Working Capital 112 9 19 24 27 39

Operating Cash Flow 662 683 758 866 994 1,141

Net CAPEX (678) (262) (703) (1,548) (1,558) (2,891)

Other Investments (1,082) (36) (43) 455 699 49

Investing Cash Flow (1,760) (298) (746) (1,093) (860) (2,842)

Financing Cash Flow 0 (467) (494) (327) (174) 2,063 Change in Cash (1,098) (81) (482) (555) (40) 362

UAE – Transportation

3

Valuation

We initiate coverage on Air Arabia with a “Buy” recommendation

We have arrived at a DCF fair value for Air Arabia of AED1.28, which offers an upside of 35% to the current market

price. We have forecasted the company’s results and performance over ten years and applied a perpetual growth

rate of 3% thereafter given the company’s high growth profile as expansions are expected to continue at least until

2016. We have applied a WACC of 10.8% based on a risk free rate of 4.5% (the 10-year UAE swap rate), a beta of

0.9 and an equity risk premium of 7.5%, which we currently apply to all DFM-listed stocks.

Table 1: Air Arabia’s WACC Calculation

Debt Weight 0.0%

Equity Weight 100.0%

Risk Free Rate 4.5%

Beta 0.9

Equity Risk Premium 7.5%

Cost of Equity 10.8%

WACC 10.8%Source: HC Brokerage

Table 2: Air Arabia’s Discounted Cash Flow Calculation

AED Million 2009f 2010f 2011f 2012f 2013f

EBITDA 550 637 773 917 1,135

Change in Working Capital 9 19 24 27 39

Net CAPEX (262) (703) (1,548) (1,558) (2,891)

Free Cash Flow to Firm 296 (47) (751) (614) (1,717)

Present Value of FCFs 272 (39) (562) (415) (1,047)

Terminal Value 7,282

Enterprise Value 4,276

Less: Net Debt (1,686)

Equity Value 5,962

Price Target (AED) 1.28

Source: HC Brokerage

Table 3: Sensitivity Analysis of Value Per Share to WACC and Perpetual Growth Rate

WACC (%) Perpetual

Growth Rate (%) 9.8 10.8 11.8

2.0 1.47 1.16 0.94

3.0 1.64 1.28 1.02

4.0 1.88 1.42 1.12

Source: HC Brokerage

Our valuation is sensitive to oil prices, sustainable load factors and average fare growth

Our valuation is negatively correlated to oil prices. We have assumed an long-term sustainable oil (Brent) price of

USD70 per barrel. Fluctuations in long-term oil prices over the range of USD60-80 per barrel result in fluctuations

from our base case fair value of +27% to -28%.

UAE – Transportation

4

Our valuation is positively correlated to both long-term load factors (see Appendix II for a definition of key aviation

terms) and average growth in fares. We have assumed a sustainable load factor of 80%. Fluctuations in load factors

over the range of 75-85% result in fluctuations from our base case fair value of -11% to +11%. We have also

assumed an average growth in fares of 2%. Fluctuations in average fare growth over the range of 0-4% result in

fluctuations from our base case fair value of -19% to +19%.

Table 4: Sensitivity of Air Arabia’s Valuation to Oil Prices, Load Factors and Fare Growth*

Sustainable Oil Price AED Load Factor AED Average Fare Growth AED

Oil Price @ USD60/bbl 1.63 75% 1.14 0% 1.04

Oil Price @ USD70/bbl 1.28 80% 1.28 2% 1.28

Oil Price @ USD80/bbl 0.92 85% 1.42 4% 1.52

* Sensitivities assume a change in only one variable at a time

Source: HC Brokerage

Table 5: Air Arabia on Multiples in Comparison to LCC Peers

Airline Country Mkt. Cap. (USDm)

Net Debt (USDm)

EV/EBITDA (x) P/E (x) P/BV (x)

2008 2008 2009 2010 2008 2009 2010 2008 AirAsia Malaysia 636 796 14.05 9.16 6.63 - 8.62 6.02 1.21 easyJet UK 1,826 (37) 4.70 9.85 5.26 13.40 32.03 10.92 0.96 Gol Brazil 820 207 110.02 3.80 3.05 - 8.76 6.04 1.20 Jazeera Airways Kuwait 234 152 10.50 6.05 5.01 3.04 0.89 4.25 2.43 Jet Airways India 251 2,291 14.74 -- 13.18 -- -- -- 0.29 JetBlue Airways USA 1,163 2,584 11.93 5.14 5.45 -- 6.46 7.19 -- Norwegian AS Norway 156 (92) -- 2.33 1.32 -- 24.44 8.23 -- Ryanair Ireland 5,815 766 7.04 15.64 7.67 9.75 59.13 13.03 1.83 Southwest Airlines USA 4,774 1,858 5.37 4.05 4.05 16.13 10.29 9.71 0.96 Spicejet Ltd. India 70 (45) -- -- 4.82 -- -- 7.05 0.67 Virgin Blue Australia 185 570 3.24 5.32 3.34 2.06 0.52 6.25 0.31 vueling Spain 107 (109) -- 4.54 -- -- 25.38 126.73 2.08 Air Arabia UAE 1,207 (2,970) 8.18 5.00 5.07 8.70 7.18 6.78 0.88 Source: Reuters, Airline Financials, HC Brokerage

Key downside risks

Key downside risks to our valuation include: (i) stronger than expected competition from flydubai, other regional

LCCs and Indian LCCs, which could negatively impact Air Arabia’s load factors; (ii) higher than expected fuel prices;

(iii) a more severe drop in average fares in the short-term; and (iv) a shrinking population in the UAE that could

negatively affect air traffic.

UAE – Transportation

5

Middle East LCCs To Withstand Tough Times

� Middle East aviation passenger traffic witnesses growth in 2008 in spite of a decline in global

traffic.

� Middle East traffic to sustain growth in 2009 driven by favorable population demographics,

relatively strong economics, and regional airline and airport expansions.

� Low-cost carriers (LCCs) are set to outperform conventional airlines as the economic slowdown

entices passengers to shift to lower-priced alternatives.

Global economic woes to hurt global airline industry…

2008 was generally a tough year for the global airline industry as airlines struggled with skyrocketing fuel prices in

the earlier part of the year, peaking above USD140 per barrel in August, but once fuel prices tumbled so did

demand as the global economic crisis took its toll on passenger traffic. Accordingly, global passenger traffic fell by

0.6% YoY in 2008. The International Air Transport Association (IATA) estimates global passenger traffic to fall by

3% YoY in 2009 as the economic crisis deepens.

Chart 1: Global Monthly Passenger Traffic (2008)

100

120

140

160

180

200

220

240

260

280

300

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Passengers (m)

Source: International Air Transport Association (IATA), HC Brokerage

…but Middle East air traffic remains relatively strong

The Middle East was the best performing region in 2008 with healthy passenger traffic growth of 7% YoY (down

from 18% in 2007). The region remained somewhat resistant to a poor global economy, showing positive growth

and outperforming the global industry throughout 2008. IATA forecasts Middle Eastern traffic to grow by 1% in

2009 but it is worth noting that IATA’s growth estimate is understated as LCCs are not IATA members and are thus

not included in their numbers. We believe that Middle East passenger air traffic will continue to grow in 2009 due

to:

(i) favorable population demographics given a large GCC expatriate population especially in the UAE.

Nearly 80% of the UAE’s population are expatriates. The UAE expatriate population has grown at a 10-

year CAGR of 7% versus 4% for its national population. Although the expatriate population is

expected to slowdown in growth or even decline given the large layoffs taking place in the UAE, we

expect the ratio of nationals-to-expatriates to remain relatively unchanged. The UAE’s favorable

demographics ensure that a large portion of its air traffic is driven by visiting friends and relatives,

expatriates visiting their home countries and repeat business visitors (employees of companies

headquartered or with subsidiaries in the UAE), which are areas we believe will be minimally affected

by the economic slowdown;

(ii) the aggressive fleet expansion plans of Middle East carriers, with nearly no order cancellations so far.

The Middle East is expected to receive 8% and 9% of the worldwide aircraft deliveries in 2009 and

2010, respectively (see table 6 below);

UAE – Transportation

6

(iii) major Middle East airport expansions (see table 7 for details);

(iv) sustained economic growth with estimated MENA GDP growth of 4% in 2009 versus estimated world

GDP growth of 1%;

(v) the region’s unparalleled location given its geographic centrality, which makes the region independent

of particular routes for its development and a popular traffic diversion destination;

(vi) aviation industry deregulation and liberalization of Middle Eastern skies, which is opening up

opportunities for new destinations and routes, which have been previously protected by restrictive

bilateral agreements. Such industry trend has opted more countries to open up their skies to airlines

other than flag carriers. Iran, for instance, has granted 215 weekly flights to UAE carriers (including

Air Arabia) in December 2008.

Chart 2: Middle East Versus Global Monthly Passenger Traffic YoY Growth (2008)

13.9%

8.4%

6.5%

2.4%8.0%

13.1%13.6%9.6% 14.7%

17.3%15.3%

14.7%

-5.8%-7.8%

-3.4%

-2.1%

-4.2%

2.1%2.9%3.5%

6.1%

3.5%

0.6%-0.3%

-8%

-3%

2%

7%

12%

17%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Middle East Passenger Traffic Global Passenger Traffic

Source: IATA, HC Brokerage

Chart 3: UAE Population by Origin

South Asians,

50%

Others, 8%UAE Nationals, 19%

Arabs &

Iranians, 23%

Source: CIA World Factbook, HC Brokerage

UAE – Transportation

7

Table 6: Worldwide Aircraft Deliveries by Region in 2009 and 2010

2009 2010

Region

Aircrafts % of Total Aircrafts % of Total

Asia Pacific 419 31% 480 34% Europe 437 32% 417 30% North America 199 15% 239 17% Middle East 114 8% 122 9% Other 203 15% 155 11% Total 1,372 100% 1,413 100% Source: Center for Asia Pacific Aviation, HC Brokerage

Table 7: Middle East Airport Expansions

Airport

Country

Capacity (in Passengers)

Expansions

Abu Dhabi International Airport

UAE

12 Mil.

New terminal to handle up to 50 mil. passengers by 2012

Al Maktoum International Airport UAE Under Construction To be fully operational by 2015 with a capacity of up to 120 mil. passengers

Cairo International Airport

Egypt

11 Mil.

New terminal completed in 4Q08 to double capacity once operational

Dubai International Airport

UAE

60 Mil.

Capacity doubled in 2008 and expected to reach 70 mil. by 2016 and 100 mil. by 2025

King Abdul Aziz Intl. Airport KSA 13 Mil. Capacity to increase to 21 mil. by late 2010 Source: Airport Technology, Zawya Dow Jones, HC Brokerage

LCCs shall demonstrate more resilience than conventional carriers

LCCs should fare better than conventional carriers in times of economic downturn thanks to a more efficient cost-

structure and lower break-even load factors. More importantly, business and leisure travelers normally shift from

conventional airlines to LCCs in bad economic times, as travelers seek strong value propositions. We believe that

Middle Eastern LCCs have been, and will continue to be, a strong stimulus to the region’s passenger traffic growth

especially given the region’s low LCC penetration estimated at around 2%. The fleet of regional LCCs is expected to

increase nearly five-times over the coming ten years, proving the strong appetite for the LCC model in the region.

Chart 4: LCC Penetration by Region

Middle East Asia Pacific Europe North America

98%

2%

87%

13%

84%

16%

75%

25%

Source: Euro Control, Center for Asia Pacific Aviation, HC Brokerage

UAE – Transportation

8

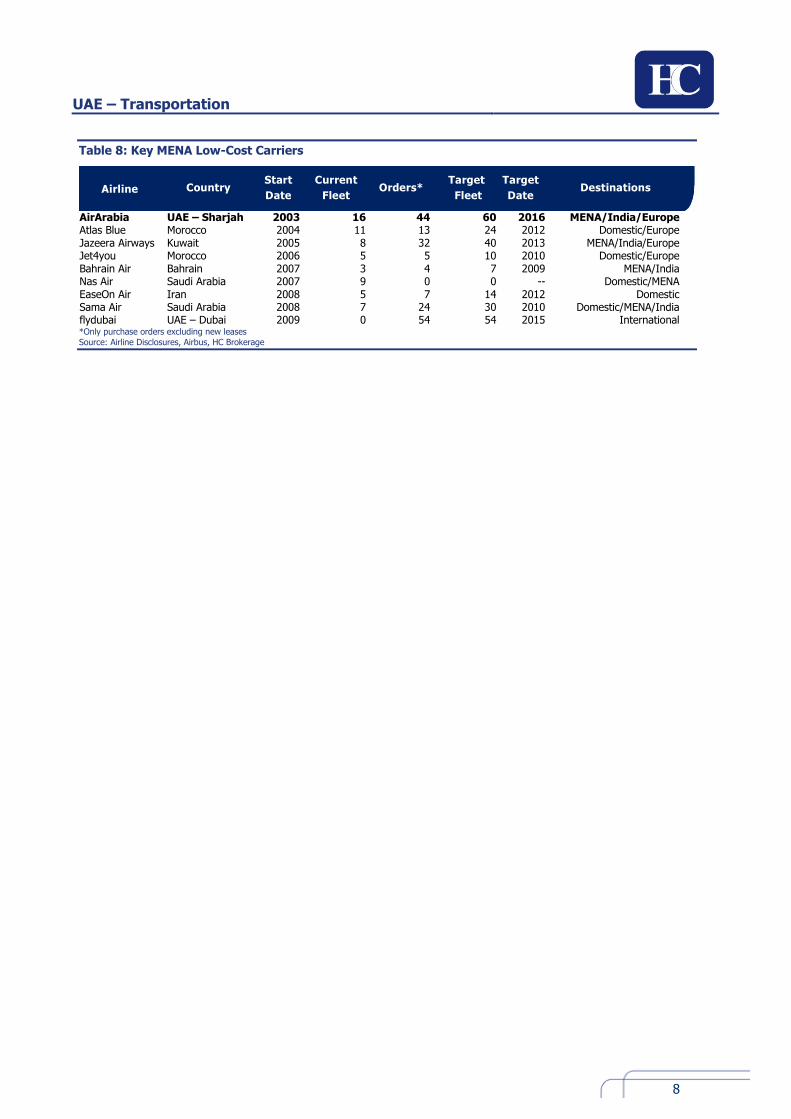

Table 8: Key MENA Low-Cost Carriers

Airline

Country Start

Date

Current

Fleet Orders*

Target

Fleet

Target

Date Destinations

AirArabia UAE – Sharjah 2003 16 44 60 2016 MENA/India/Europe Atlas Blue Morocco 2004 11 13 24 2012 Domestic/Europe Jazeera Airways Kuwait 2005 8 32 40 2013 MENA/India/Europe Jet4you Morocco 2006 5 5 10 2010 Domestic/Europe Bahrain Air Bahrain 2007 3 4 7 2009 MENA/India Nas Air Saudi Arabia 2007 9 0 0 -- Domestic/MENA EaseOn Air Iran 2008 5 7 14 2012 Domestic Sama Air Saudi Arabia 2008 7 24 30 2010 Domestic/MENA/India flydubai UAE – Dubai 2009 0 54 54 2015 International *Only purchase orders excluding new leases

Source: Airline Disclosures, Airbus, HC Brokerage

UAE – Transportation

9

Air Arabia: First Mover Advantage

� Air Arabia is set to benefit from a shift to LCCs, being the region’s first and leading LCC.

� An aggressive fleet expansion plan to support growth. No deliveries before end of 2010, enabling

the carrier to maintain its debt free position and a strong dividend payout in the short-term (an

average dividend yield of 11% based on 2008 and 2009 earnings).

� Expanding outside of Sharjah into other hubs will provide needed diversification and to minimize

the impact of growing competition.

Air Arabia is the region’s first and number one LCC

Air Arabia, the region’s first and leading low-cost carrier (LCC) and the official airline of the emirate of Sharjah,

commenced operations in October 2003 with a two-aircraft fleet and flights to five destinations. The carrier took

Sharjah International Airport as its hub operating frequent commercial flights on short- and medium-haul point-to-

point routes in the Indian subcontinent (47% of Air Arabia’s traffic currently) and the MENA region. The airline

operates a single aircraft type, the Airbus A320, with a single economy cabin configuration. Air Arabia had an

AED2.5 billion IPO and was listed on the DFM in July 2007. The carrier currently operates a fleet of 16 aircrafts and

flies to 44 destinations, and offers an average of 5% of weekly available aircraft seats in the UAE. Air Arabia’s

dominant position in the UAE and within the LCC segment ensures that it will benefit from an expected shift by

travelers to LCCs as the economy slows.

Table 9: Air Arabia’s Historical Milestones

Date Event

March 2003 Official Launch

October 2003 First Air Arabia flight to Bahrain

February 2005 Announcement of financial breakeven for 2004

June 2005 1-million passenger milestone reached

April 2007 Announcement of 300-room budget hotel project in Sharjah

April 2007 AED2.5 billion IPO closes attracting 40,000 subscribers

July 2007 Listing of Air Arabia’s shares on the DFM

Aug 2007 Launch of call center service

November 2007 Announcement of plan to open a new hub in Morocco

November 2007 Signature of USD3.5 billion agreement with Airbus to acquire 49 A320 aircrafts

January 2008 Launch of Air Arabia’s second hub in Nepal

March 2008 Acquisition of two new Airbus aircrafts

July 2008 Termination of Air Arabia’s second hub in Nepal

Source: Air Arabia, HC Brokerage

Chart 5: Geographic Distribution of Air Arabia’s Passenger Traffic

Ind ian Subcont inent

4 7%

GCC

2 7%

M idd le East ( Ex-

GCC )

15%

Nort h A f r ica

10%

Cent ral A sia

1%

Source: Air Arabia, HC Brokerage

UAE – Transportation

10

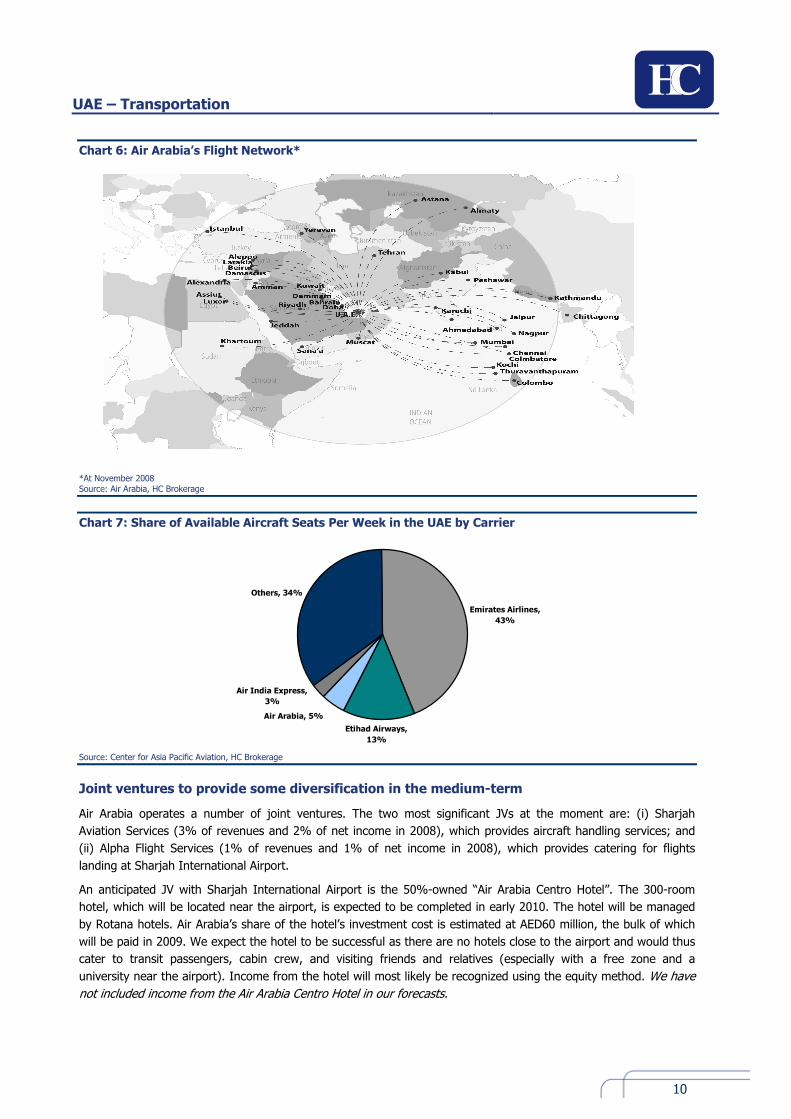

Chart 6: Air Arabia’s Flight Network*

*At November 2008

Source: Air Arabia, HC Brokerage

Chart 7: Share of Available Aircraft Seats Per Week in the UAE by Carrier

Emirates Airlines,

43%

Etihad Airways,

13%

Air Arabia, 5%

Air India Express,

3%

Others, 34%

Source: Center for Asia Pacific Aviation, HC Brokerage

Joint ventures to provide some diversification in the medium-term

Air Arabia operates a number of joint ventures. The two most significant JVs at the moment are: (i) Sharjah

Aviation Services (3% of revenues and 2% of net income in 2008), which provides aircraft handling services; and

(ii) Alpha Flight Services (1% of revenues and 1% of net income in 2008), which provides catering for flights

landing at Sharjah International Airport.

An anticipated JV with Sharjah International Airport is the 50%-owned “Air Arabia Centro Hotel”. The 300-room

hotel, which will be located near the airport, is expected to be completed in early 2010. The hotel will be managed

by Rotana hotels. Air Arabia’s share of the hotel’s investment cost is estimated at AED60 million, the bulk of which

will be paid in 2009. We expect the hotel to be successful as there are no hotels close to the airport and would thus

cater to transit passengers, cabin crew, and visiting friends and relatives (especially with a free zone and a

university near the airport). Income from the hotel will most likely be recognized using the equity method. We have

not included income from the Air Arabia Centro Hotel in our forecasts.

UAE – Transportation

11

Table 10: Air Arabia’s Joint Ventures and Subsidiaries (2008)

Joint Venture

% Owned

Activities

Red Marketing Communications 100% Marketing and advertising services Information System Associates 51% Trading and providing IT products and services Sharjah Aviation Services 50% Aircraft handling and passenger services Sharjah Airport Travel Agency 50% Travel & tourist agencies & air cargo Alpha Flight Services 51% In-flight catering within Sharjah Airport Source: Air Arabia, HC Brokerage

Aggressive fleet expansion plans…

Air Arabia currently operates a fleet of 16 A320 aircrafts. All existing aircrafts are leased with the exception of three

aircrafts that were purchased in 2008 due to favorable prices.

In November 2007, the carrier signed an agreement with Airbus for the acquisition of up to 49 A320 aircrafts with

an estimated book value then of USD3.5 billion. Air Arabia currently has firm orders for 44 aircrafts with deliveries

beginning in 2010 and are phased until 2016. Coupled with occasional additions of newly leased aircrafts, we

estimate that Air Arabia’s fleet will reach 80 aircrafts by 2018.

In 2009, the carrier will likely see its fleet grow to 19 aircrafts with the addition of four new leases and the return of

one. Two newly leased aircrafts are expected to be received in 2Q09 with the remaining two to enter Air Arabia’s

fleet in 4Q09. It is worth noting that fleet expansion plans can and are likely to change with market conditions as

the carrier has the option to add more (or fewer) aircrafts to its fleet. Regarding the 44 A320 firm orders, we are

skeptical that Air Arabia will reduce its firm orders but can alter its delivery schedule depending on market

conditions.

Chart 8: Air Arabia’s Fleet

3 3 59

1323

34 44 48 48 48

11

13 16

2021

2222 23 25 28 32

19

0%

20%

40%

60%

80%

100%

2007 2008 2009e 2010f 2011f 2012f 2013f 2014f 2015f 2016f 2017f 2018f

Owned Leased

Source: Air Arabia, HC Brokerage

UAE – Transportation

12

Chart 9: Air Arabia’s CAPEX and CAPEX/Sales

48%

33%

12%

26%

41%

62%

200

700

1200

1700

2200

2700

2008 2009e 2010f 2011f 2012f 2013f

0%

10%

20%

30%

40%

50%

60%

CAPEX (AED Mil.) CAPEX/Sales

Source: Air Arabia, HC Brokerage

…but no debt requirement before 2013

We believe that Air Arabia will sustain its debt-free position until 2013 as the hefty CAPEX begins in 2011. Any

CAPEX before 2013 can be financed internally. Air Arabia’s cash balance, which is mostly from the IPO proceeds,

stood at AED1.8 billion (30% of total assets) in 2008. Additionally, the carrier holds AED1.5 billion (26% of total

assets) in mostly unquoted available-for-sale investments, which we believe will be gradually liquidated to finance

its expanding fleet. Management has been discrete with regards to the nature of the investments but highlighted

that they are of a low risk profile. Our debt assumptions are a function of the CAPEX for the year.

Minor short-term financing needs allow for generous dividends

The Board of Directors of Air Arabia has proposed a dividend of AED0.1 per share, which implies a generous

dividend payout ratio of 92% and an attractive dividend yield of 11%. We expect the dividend to be distributed

sometime in the second half of April 2009 following the approval of the GAM to be held on March 23rd, 2009. The

reason for such a strong dividend is the lack of short-term major financing needs and the carrier’s strong balance

sheet. Although we view such generous dividends as not sustainable when the large CAPEX payments begin, we

believe there is room for a similar dividend based on 2009 earnings as well. We have assumed that the carrier will

maintain its minimum dividend payout ratio of 25% during the high CAPEX period from 2011-2015.

Sharing and contributing to the growth of its Sharjah Hub…

Located around 15 kilometers from Dubai and 10 kilometers from the Sharjah city center and with an annual

capacity of 8 million passengers, Sharjah International Airport, Air Arabia's hub, benefits from its geographic

centrality. The airport is easily accessible by residents of the different Emirates, and is well-connected to all major

international destinations. Sharjah International Airport recorded an impressive passenger growth in 2008 of 22%

YoY to 5.28 million in 2008. Air Arabia constitutes around 66% of available seat capacities at Sharjah International

Airport.

Chart 10: Sharjah International Airport Monthly Airport Traffic

490

441423407

491488

437

404

436431

392

440

366

460

386

342

393372

341339368

331

295

332

250

300

350

400

450

500

550

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Passenger Traffic ('000s)

2008 2007

Source: Sharjah International Airport, HC Brokerage

UAE – Transportation

13

Chart 11: Sharjah International Airport’s Capacity Breakdown by Carrier*

Air Arabia,

66%

Others, 10%

Air India

Express, 12%

Indian Airlines,

13%

*For the week commencing January 19th, 2009

Source: Center for Asia Pacific Aviation, HC Brokerage

…but growing competition is a threat

Air Arabia’s major competitive threat in our view is flydubai, Dubai’s own LCC which is set to commence operations

in 2Q09 and targets a fleet of 54 aircrafts by 2015. Although we do not have exact numbers, the threat pertains to

any Dubai business that Air Arabia has. There is also threat of transfer of Sharjah business if flydubai offers more

competitive rates. In general, we believe the impact of competition from flydubai will not be evident before 2010 as

it gradually builds its fleet and expand its destination offering. We are also skeptical that flydubai will offer more

competitive rates than Air Arabia given that it will initially operate at Dubai International Airport, which we believe is

more costly to operate from than Sharjah. flydubai will move its hub to Al Maktoum International Airport once it is

completed by 2010. There is also competition from regional LCCs (see table 8 above), particularly the rapidly-

expanding Kuwait’s Jazeera Airways that has Dubai as a secondary hub, and Indian LCCs since the Indian

subcontinent is Air Arabia’s most popular destination (see chart 5 above). India currently has six LCCs, but most fly

domestically with limited or no flights to the UAE. The clear exception is Air India Express, which captures 3% of the

available seat capacity in the UAE (and 12% of Sharjah’s capacity). The UAE represents around 42% of Air India

Express’ weekly flights. Additionally, the Indian carrier has been competing in the UAE for at least two years with no

significant impact on Air Arabia. The other Indian LCCs are expected to compete more heavily on UAE routes as

more permissions are granted to operate on international routes.

Table 11: Key Indian Low Cost Carriers

Airline Inception Current Fleet Orders No. of Destinations Destinations

JetLite 1991 24 10 28 Subcontinent

Kingfisher Red 2003 33 68 69 Domestic

SpiceJet 2005 19 17 17 Domestic

Air India Express 2005 21 4 32 Domestic/International

IndiGo 2006 19 -- 17 Domestic

Source: Airline Disclosures, HC Brokerage

Morocco hub to start operations in 2Q09

Air Arabia will launch operations at its second hub in Casablanca, Morocco in 2Q09. The 29%-owned joint venture

with Morocco’s Regional Airlines will be through a newly formed airline called “Air Arabia Maroc”. Air Arabia has

management control of the JV. The first destinations the new airline will fly to will include France, Italy, Spain and

the UK. Casablanca’s airport, known as Mohammed V International Airport, represented around 48% of Morocco’s

passenger traffic in 2008. The airport had larger passenger traffic than the Sharjah Airport in 2008 of 6.21 million

passengers, but demonstrated tamer growth of 6% YoY.

Although Morocco is somewhat competitive with two conventional airlines, two LCCs and one charter airline, we like

the expansion as it will provide exposure to destinations in Europe and North Africa that complement Air Arabia’s

current destinations. Key competition comes from Jet4u, a LCC that also has the Casablanca airport as its hub. “Air

UAE – Transportation

14

Arabia Maroc” will start off with 2 aircrafts (other than the 2009 target of 19 aircrafts for the Sharjah base). The JV

will be proportionately consolidated by Air Arabia given management control. Given Air Arabia’s small stake in the JV

and that it is a start-up, we believe the JV will not have a major financial impact before 2010. Given minor expected

material short-term impact and little management guidance, we have not included “Air Arabia Maroc” in our

forecasts.

Chart 12: Casablanca (Mohamed V) Airport Versus Total Moroccan Passenger Traffic

37.9%

39.3% 39.3%38.6% 39.3%

48.3% 48.3%

0

2

4

6

8

10

12

14

2002 2003 2004 2005 2006 2007 2008

30.0%

35.0%

40.0%

45.0%

50.0%

Morocco's Passenger Traffic (Mil.) Mohammed V's Passenger Traffic (Mil.) Mohamed V's Share of Moroccan Traffic (%)

Source: Office Nationale Des Aeroports (ONDA), HC Brokerage

Table 12: Moroccan Airline Industry Competitive Landscape

Airline Inception Type Hub Fleet Destinations

Royal Air Maroc 1957 Conventional Casablanca 46 86

Casa Air Service 1995 Charter Casablanca 3 N/A

Regional Air Lines 1996 Conventional Casablanca 10 18

Atlas Blue* 2004 LCC Marrakech 11 23

Jet4U 2006 LCC Casablanca 5 13

*LCC subsidiary of Royal Air Maroc

Source: Airline Websites, HC Brokerage

An impending announcement of a third hub

Air Arabia is expected to announce a third hub in early 2009. The likely options are Egypt and the Levant region.

We view the Egypt option as favorable as it is the Arab world’s most populous country and the LCC concept is

nearly non existent there. EgyptAir has a six-fleet LCC arm called EgyptAir Express, but only flies domestic flights

and is not well-advertised in the country. India is another option as it represents around 47% of the airline’s traffic.

Worth noting is that Air Arabia suspended operations at a hub in Kathmandu, Nepal in mid 2008 due to political

reasons. We like Air Arabia’s hub expansion strategy as it provides a diversification of routes and would help reduce

the impact of growing competition. The announcement of a third hub should serve as a short-term price catalyst.

UAE – Transportation

15

Air Arabia: Among the Best in Class

� We expect Air Arabia to deliver sales growth of 9% in 2009 despite declining yields.

� EBITDAR and net income are expected to grow in 2009 by 46% and 21% YoY, respectively,

helped by falling fuel prices.

� Revenue and EBITDAR to grow at a 5-year CAGR of 18% and 22%, respectively, driven by fleet

expansion plans.

We forecast strong passenger growth in 2009 but declining yields tame revenue growth

We expect Air Arabia’s passenger traffic to grow in 2009 by 17%, benefiting from a shift of travelers from

conventional to LCCs, a net increase of 3 aircrafts and the addition of new destinations. Air Arabia is expected to fly

to Athens, Iran and more India destinations in 2Q09. We also forecast a strong average load factor of 84% for

2009. But revenue growth is to come under pressure as yields (passenger revenue per available seat kilometers)

decline as we expect Air Arabia to reduce its fares due to lower fuel surcharges and to spur demand. A big chunk of

the 20% YoY increase in Air Arabia’s average fares in 2008 was due to high fuel surcharges to match the escalating

fuel prices. We expect a rebound in yields in 2010. It is worth noting that Air Arabia’s pricing strategy is strictly

demand-driven. The base fare is 40% below those offered by conventional carriers for the same route but if all

other airlines have no free seats for a particular destination at a particular time, it can charge even higher than

conventional carriers. Also, fares rise as the bookings are made closer to a flight’s date.

Chart 13: Change in Air Arabia’s Yields (Passenger Revenue per ASK)

-15%

-5%

5%

15%

25%

35%

2006 2007 2008 2009e 2010f

Source: Air Arabia, HC Brokerage

Long-term revenue forecasts are a function of fleet additions and load factors

Our passenger traffic forecasts post 2009 are strictly a function of the aircraft additions. We assume a sustainable

load factor of 80%, which is lower than the 85% achieved in 2009 but still at a significant premium to its LCC peers

(see chart 15 below). Our load factors capture growing competition particularly in the UAE. flydubai, Dubai’s own

LCC , which is set to begin operations in 2Q09, could prove a threat in the medium-term. We have assumed an

average annual increase in fares of 2% in the medium- to long-term.

UAE – Transportation

16

Chart 14: Air Arabia’s Passenger Traffic Forecasts

4.18

4.90

5.78

6.73

8.10

20%

18%

17%17%

16%

0

2

4

6

8

10

2009e 2010f 2011f 2012f 2013f

15%

17%

19%

21%

23%Number of Passengers (Mil.) Passenger Growth (%)

Source: HC Brokerage

Chart 15: Air Arabia’s Current Load Factors in Comparison to Other LCCs

81% 81%

79%78%

75%

71%70% 70%

62%

85%

60%

65%

70%

75%

80%

85%

Air Arabia easyJet Ryanair JetBlue vueling Air Asia Southwest Jazeera Jet Airways Gol

Source: Air Arabia, Airline Disclosures, HC Brokerage

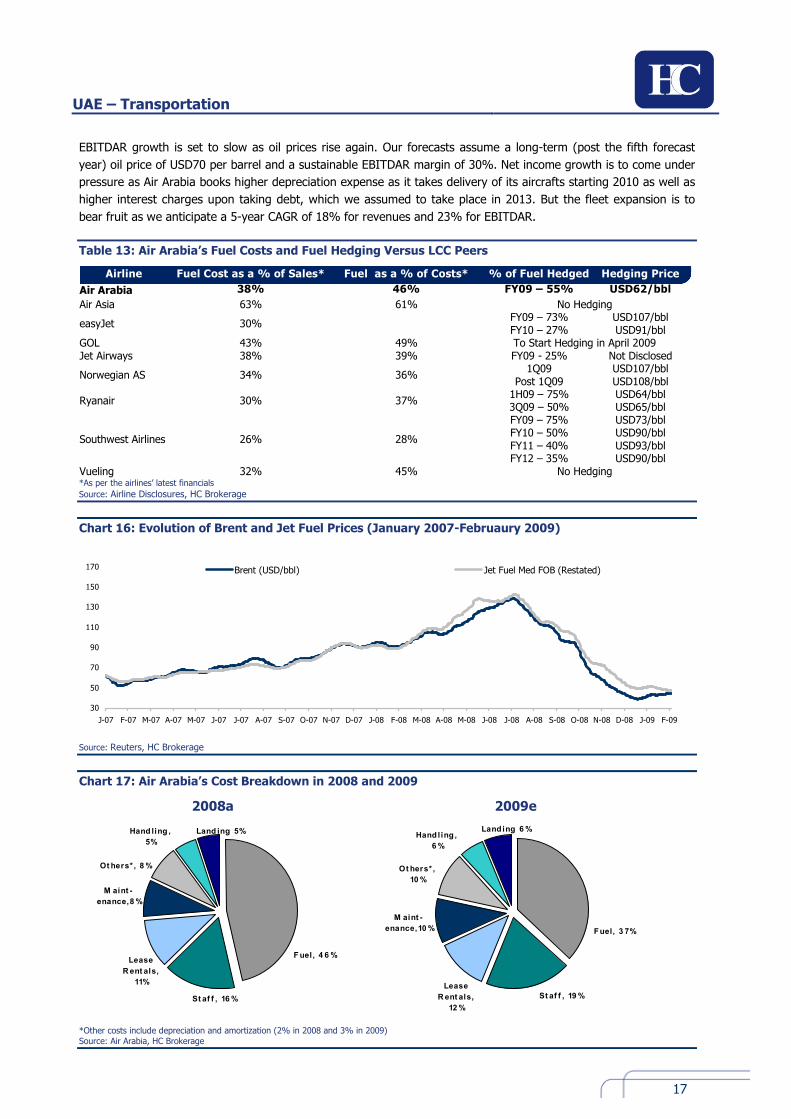

Air Arabia’s wise fuel hedging to bear favorably on 2009 results

A major challenge that the airline industry and Air Arabia faced in 2008 was record-high fuel costs with oil

exceeding USD140 per barrel. Air Arabia was not hedged throughout the period of escalating oil costs but managed

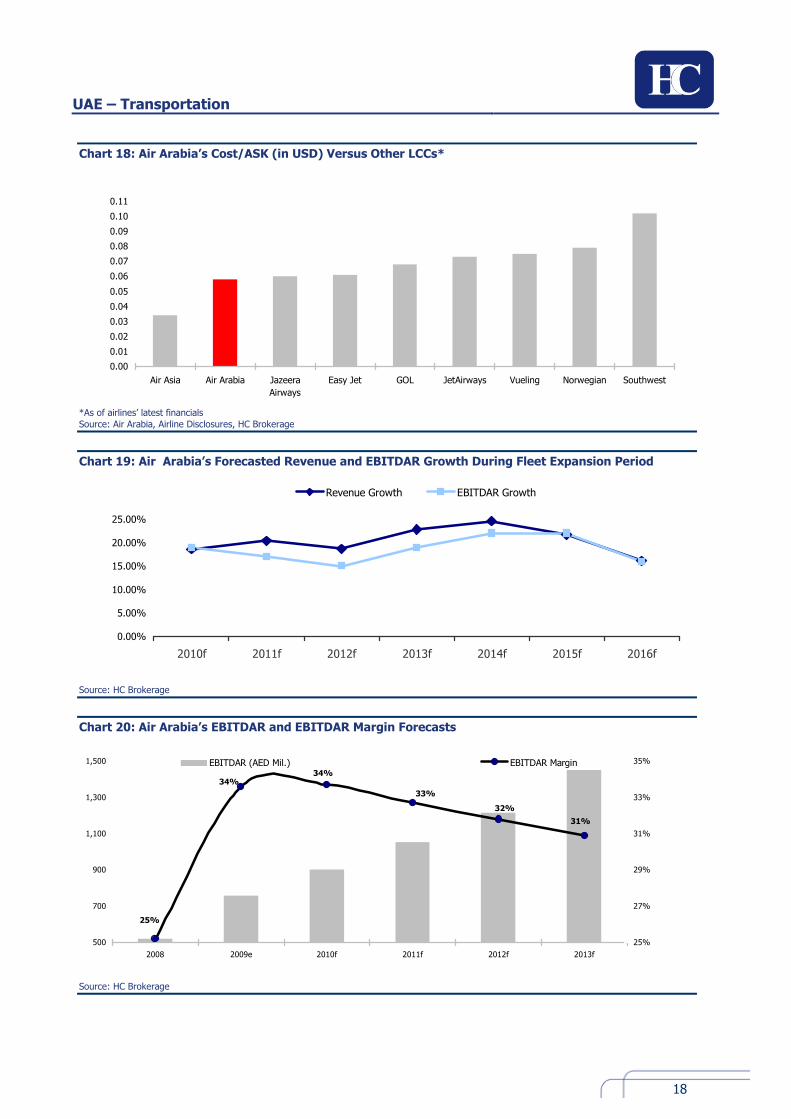

to deliver a solid set of results for 2008, remaining one of the most cost-efficient LCCs (see chart 18), as it passed

on the cost increases to its passengers through its fuel surcharges. When oil prices started to fall, many carriers

started to hedge but few were able to predict how low prices would go. Many airlines hedged in the USD100 per

barrel range, which, coupled with slower demand, deems 2009 a particularly difficult year. Going into 2009, Air

Arabia hedged 55% of its needs at around USD62 per barrel. We do not believe the company will do further

hedging for the year given the low levels that oil prices are settling at. We expect Air Arabia’s average oil price for

2009 to be USD59 per barrel (around USD597 per ton in jet fuel terms).

Accordingly, we forecast fuel costs to drop from 39% of sales (and 46% of costs) in 2008 to 29% of sales (and

37% of costs) in 2009 bearing favorably on Air Arabia’s margins. We forecast an impressive EBITDAR growth of

46% YoY for Air Arabia and a significant improvement in EBITDAR margin from 25.2% in 2008 to 33.6% in 2009.

Net income is estimated to grow at a strong but tamer 21% YoY as 2008 results were partly inflated by AED56

million in non-recurring dividend income.

UAE – Transportation

17

EBITDAR growth is set to slow as oil prices rise again. Our forecasts assume a long-term (post the fifth forecast

year) oil price of USD70 per barrel and a sustainable EBITDAR margin of 30%. Net income growth is to come under

pressure as Air Arabia books higher depreciation expense as it takes delivery of its aircrafts starting 2010 as well as

higher interest charges upon taking debt, which we assumed to take place in 2013. But the fleet expansion is to

bear fruit as we anticipate a 5-year CAGR of 18% for revenues and 23% for EBITDAR.

Table 13: Air Arabia’s Fuel Costs and Fuel Hedging Versus LCC Peers

Airline Fuel Cost as a % of Sales* Fuel as a % of Costs* % of Fuel Hedged Hedging Price

Air Arabia 38% 46% FY09 – 55% USD62/bbl

Air Asia 63% 61% No Hedging

easyJet 30% FY09 – 73% FY10 – 27%

USD107/bbl USD91/bbl

GOL 43% 49% To Start Hedging in April 2009 Jet Airways 38% 39% FY09 - 25% Not Disclosed

Norwegian AS 34% 36% 1Q09

Post 1Q09 USD107/bbl USD108/bbl

Ryanair 30% 37% 1H09 – 75% 3Q09 – 50%

USD64/bbl USD65/bbl

Southwest Airlines 26% 28%

FY09 – 75% FY10 – 50% FY11 – 40% FY12 – 35%

USD73/bbl USD90/bbl USD93/bbl USD90/bbl

Vueling 32% 45% No Hedging *As per the airlines’ latest financials

Source: Airline Disclosures, HC Brokerage

Chart 16: Evolution of Brent and Jet Fuel Prices (January 2007-Februaury 2009)

30

50

70

90

110

130

150

170

J-07 F-07 M-07 A-07 M-07 J-07 J-07 A-07 S-07 O-07 N-07 D-07 J-08 F-08 M-08 A-08 M-08 J-08 J-08 A-08 S-08 O-08 N-08 D-08 J-09 F-09

Brent (USD/bbl) Jet Fuel Med FOB (Restated)

Source: Reuters, HC Brokerage

Chart 17: Air Arabia’s Cost Breakdown in 2008 and 2009

2008a 2009e

Land ing 5%Hand ling ,

5%

Fuel, 4 6 %

M aint -

enance,8%

Lease

Rent als,

11%

St af f , 16%

Others* , 8%

Land ing 6%Handling ,

6%

Fuel, 3 7%

M aint -

enance,10%

Lease

Rent als,

12%

St af f , 19%

Others* ,

10%

*Other costs include depreciation and amortization (2% in 2008 and 3% in 2009)

Source: Air Arabia, HC Brokerage

UAE – Transportation

18

Chart 18: Air Arabia’s Cost/ASK (in USD) Versus Other LCCs*

0.00

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.10

0.11

Air Asia Air Arabia Jazeera

Airways

Easy Jet GOL JetAirways Vueling Norwegian Southwest

*As of airlines’ latest financials

Source: Air Arabia, Airline Disclosures, HC Brokerage

Chart 19: Air Arabia’s Forecasted Revenue and EBITDAR Growth During Fleet Expansion Period

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2010f 2011f 2012f 2013f 2014f 2015f 2016f

Revenue Growth EBITDAR Growth

Source: HC Brokerage

Chart 20: Air Arabia’s EBITDAR and EBITDAR Margin Forecasts

31%

32%

34%34%

25%

33%

500

700

900

1,100

1,300

1,500

2008 2009e 2010f 2011f 2012f 2013f

25%

27%

29%

31%

33%

35%EBITDAR (AED Mil.) EBITDAR Margin

Source: HC Brokerage

UAE – Transportation

19

Chart 21: Air Arabia’s 2009e EBIT Margin in Comparison to Other LCCs

14% 14% 14%

9% 9%

2%

7%

2%

22%

0%

5%

10%

15%

20%

Air Arabia AirAsia JetBlue Ryanair Jazeera Southwest Gol vueling easyJet

Source: Air Arabia, Reuters, HC Brokerage

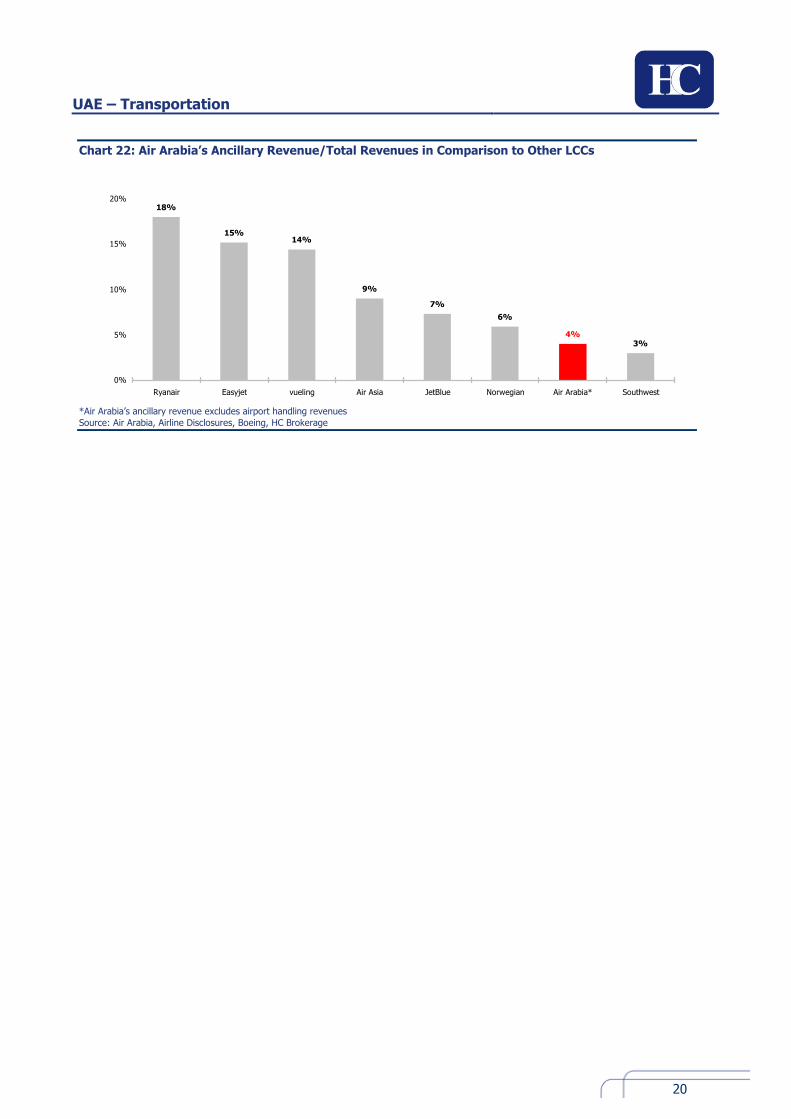

Ancillary revenue to remain a modest growth driver for Air Arabia

Air Arabia’s other revenue constituted 7% of total revenue in 2008. But not all of the carrier’s other revenue are

strictly ancillary revenue. 38% of other revenue is represented in airport handling revenue, as part of the

proportionate consolidation of its JV Sharjah Aviation Services, which is not in essence ancillary revenue. Core

ancillary revenue represented less than 4% of 2008 revenues, which is low compared to other LCCs. The main

source of ancillary revenue for Air Arabia is related to excess baggage. We believe that the level of ancillary revenue

is low for Air Arabia compared to other LCCs due to the relatively small variety of ancillary services offered and mild

management focus in that area. Thus, we forecast that other revenue (including airport handling) to remain at an

average of 7% of sales over our forecast horizon.

Chart 22: Air Arabia’s Other Revenue Breakdown (2008)

Airport Handling,

38%

Baggage, 22%

Catering, 14%

Cargo, 12%

Service, 6%

Other, 8%

Source: Air Arabia, HC Brokerage

UAE – Transportation

20

Chart 22: Air Arabia’s Ancillary Revenue/Total Revenues in Comparison to Other LCCs

15%14%

9%

7%

6%

4%3%

18%

0%

5%

10%

15%

20%

Ryanair Easyjet vueling Air Asia JetBlue Norwegian Air Arabia* Southwest

*Air Arabia’s ancillary revenue excludes airport handling revenues

Source: Air Arabia, Airline Disclosures, Boeing, HC Brokerage

UAE – Transportation

21

Appendix I: The Low-Cost Carrier (LCC) Business Model

A low-cost carrier is an airline that offers relatively low airfares while eliminating many conventionally offered

passenger amenities. The concept was pioneered in the United States in the 1940s by Pacific Southwest Airlines and

gradually evolved to its current form in the 1970s. The model later penetrated Europe with the most notable

success stories being Ireland’s Ryanair (1985) and London’s easyJet (1995). It then spread into Asia in the 2000s

and the Middle East in 2003 pioneered by Air Arabia. The cornerstones of the LCC model include:

(i) eliminating unnecessary costs and “frills”, which characterize conventional airlines such as free on-board

catering, pre-assigned seating, cargo/freight carriage, lounges, air miles, etc. These services are offered

for a fee thus generating “ancillary revenue”;

(ii) a single-type aircraft fleet, which allows for operational savings in the areas of maintenance, flight

operations, and crew training;

(iii) a single passenger class;

(iv) maximizing aircraft utilization through reducing turnaround times (keeping aircrafts in the air for the

longest time possible) as well as maintaining high seating density and load factors;

(v) a simple pricing system through: (1) offering low fares that only rise as flights fill up (i.e. cheaper fares

for earlier reservation); (2) having adjustable price bands based on demand; and/or (3) charging one-

way fares;

(vi) eliminating/reducing sales commissions by relying on direct booking through the internet and/or call

centers;

(vii) simplifying routes through using point-to-point networks instead of transferring through hubs, which also

maximizes aircraft utilization;

(viii) “paperless” operations, to significantly reduce the cost of issuing, processing and distributing millions of

tickets a year.

It is worth noting that it is rare to find a single LCC applying all the abovementioned cornerstones. Each LCC offers

variations on these points based on its management strategy.

UAE – Transportation

22

Appendix II: Key Aviation Industry Terms

Ancillary Revenue Airline revenue from sources other than ticket sales.

LCCs are typically highly dependent on ancillary

revenue. Examples include in-flight meals, excess

baggage, etc.

Available Seat Kilometers (ASK) Total available seats x kilometers flown. A measure of

an airline’s total capacity.

Block Hours Time an aircraft stays in the air on average from its

departure to landing.

Long-Haul Flights Flights longer than six hours.

Medium-Haul Flights Flights that are between three and six hours. LCCs

typically fly short- and medium-haul.

Passenger Load Factor RPK/ASK. A measure of an airline’s capacity utilization.

Short-Haul Flights Flights that are shorter than three hours. LCCs typically

fly short- and medium-haul.

Revenue Passenger Kilometers (RPK) Number of passengers x kilometers flown. A measure of

an airline’s production.

UAE – Transportation

23

Rating Scale

Recommendation Upside

Buy Greater than 25%

Hold 0-25%

Sell Less than 0%

Disclaimer

This memorandum is based on information available to the public. This memorandum is not an offer to buy or sell, or a solicitation of an offer to buy or sell the securities mentioned. The information and opinions in this memorandum were prepared by HC Brokerage from sources it believes to be reliable and from

information available to the public. HC Brokerage makes no guarantee or warranty to the accuracy and thoroughness of the information mentioned in this memorandum, and accepts no responsibility or liability for losses or damages incurred as a result of opinions formed and decisions made based on information presented in this memorandum. HC Brokerage does not undertake to advise you of changes in its opinion or information. HC Brokerage and its affiliates and/or

its directors and employees may own or have positions in, and effect transactions of companies mentioned in this memorandum. HC Brokerage and its affiliates may also seek to perform or have performed investment-banking services for companies mentioned in this memorandum.

UAE – Transportation

24

\

HC Research [email protected]

Karim Khadr Regional Head of Research [email protected] +971 4 2935381

NematAllah Choucri Telecoms [email protected] +202 37496008 (Ext. 451)

May Khamis Telecoms [email protected] +202 37496008 (Ext. 456)

Germaine Benyamin Banks & Financials [email protected] +971 4 2935382

Janany Vamadeva Banks & Financials [email protected] +971 4 2935384

Engy El Dishish Banks & Financials [email protected] +971 4 2935383

Roaa Alian Construction & Build. Materials [email protected] +202 37496008 (Ext. 452)

Mennatallah El Hefnawy Construction & Build. Materials [email protected] +202 37496008 (Ext. 455)

Hatem Alaa Industrials & Consumer Goods [email protected] +202 37496008 (Ext. 453)

Sara Serour Industrials & Consumer Goods [email protected] +202 37496008 (Ext. 457)

Mai Nehad Industrials & Consumer Goods [email protected] +202 37496008 (Ext. 454)

Siju Mathew Real Estate [email protected] +971 4 2935385

Nermeen Abdel Gawad Real Estate [email protected] +202 37496008 (Ext. 450)

Mohamed El Saiid, MFTA Head of TA Desk [email protected] +202 37496008 (Ext. 175)

Wael Atta, CFTe Senior Technical Analyst [email protected] +971 4 2935388

Sameh Khalil Technical Analyst [email protected] +202 37496008 (Ext. 361)

HC Brokerage – Cairo, Egypt [email protected] +202 37496008

Shawkat El-Maraghy Managing Director [email protected] Ext. 200

Mostafa Saad Local & Gulf Sales [email protected] Ext. 213

Yasser Mansour Local & Gulf Sales [email protected] Ext. 217

Hossam Wahid Local & Gulf Sales [email protected] Ext. 206

Yasser Seif Local & Gulf Sales [email protected] Ext. 319

Hassan Kenawi Local & Gulf Sales [email protected] Ext. 300

Abou Bakr Shaaban Local & Gulf Sales [email protected] Ext. 238

Nihal Hany Local & Gulf Sales [email protected] Ext. 219

Mohamed Helmy Foreign Sales [email protected] Ext. 207

Amr El Hemely GDR Trader [email protected] Ext. 222

Ahmed Nabil Fixed Income Trader [email protected] Ext. 218

Al-Futtaim HC Securities – Dubai, UAE

Hassan Aly Choucri General Manager [email protected] +971 4 293 5305

Mohamed Hegazy Head of Sales [email protected] +971 4 293 5365

Mohamed Galal Head of Foreign Inst. Sales [email protected] +971 4 293 5309

Hesham Bakry Institutional Sales Manager [email protected] +971 4 293 5353

Anne Marie Browne Foreign Institutional Sales [email protected] +971 4 293 5301

Richard Frost Foreign Institutional Sales [email protected] +971 4 293 5302