research report on the biscuits and cookies industry in india

TRANSCRIPT

Biscuits and Cookies Industry in India 2015 - 2019

Picture Courtesy: www.info.wowlogistics.com

2

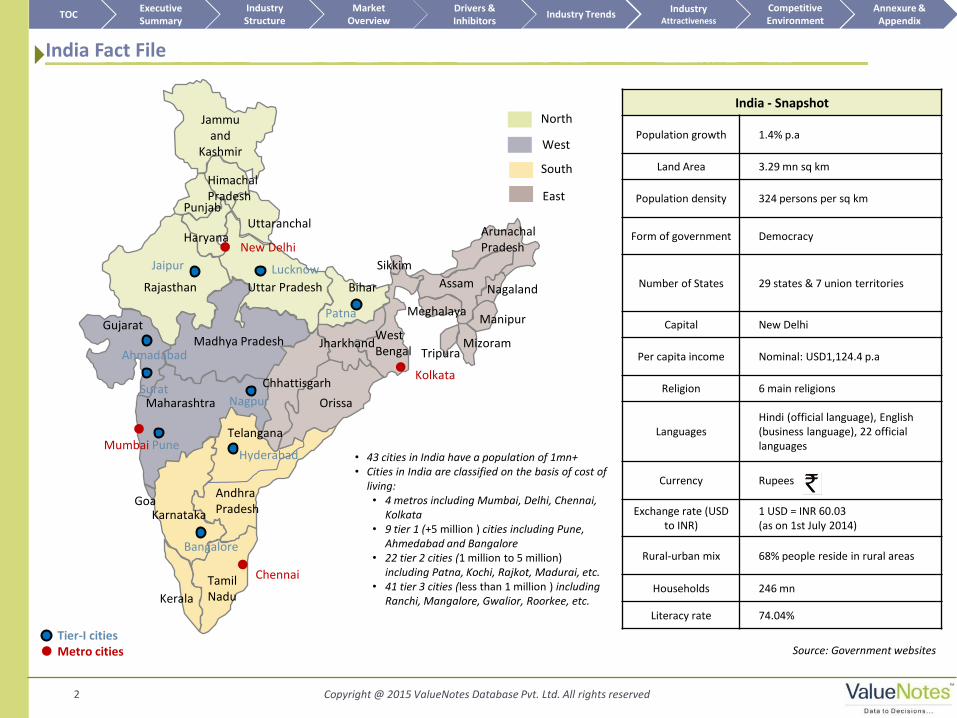

• 43 cities in India have a population of 1mn+ • Cities in India are classified on the basis of cost of

living: • 4 metros including Mumbai, Delhi, Chennai,

Kolkata • 9 tier 1 (+5 million ) cities including Pune,

Ahmedabad and Bangalore • 22 tier 2 cities (1 million to 5 million)

including Patna, Kochi, Rajkot, Madurai, etc. • 41 tier 3 cities (less than 1 million ) including

Ranchi, Mangalore, Gwalior, Roorkee, etc.

India - Snapshot

Population growth 1.4% p.a

Land Area 3.29 mn sq km

Population density 324 persons per sq km

Form of government Democracy

Number of States 29 states & 7 union territories

Capital New Delhi

Per capita income Nominal: USD1,124.4 p.a

Religion 6 main religions

Languages Hindi (official language), English (business language), 22 official languages

Currency Rupees

Exchange rate (USD to INR)

1 USD = INR 60.03 (as on 1st July 2014)

Rural-urban mix 68% people reside in rural areas

Households 246 mn

Literacy rate 74.04%

West

North

South

East

Source: Government websites Metro cities Tier-I cities

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

India Fact File

Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

Andhra Pradesh

Arunachal Pradesh

Assam Bihar

Chhattisgarh

Goa

Gujarat

Haryana

Himachal Pradesh

Jammu and

Kashmir

Jharkhand

Karnataka

Kerala

Madhya Pradesh

Maharashtra

Manipur Meghalaya

Mizoram

Nagaland

Orissa

Punjab

Rajasthan

Sikkim

Tamil Nadu

Tripura

Uttar Pradesh

Uttaranchal

West Bengal

Mumbai Pune Hyderabad

Bangalore

Jaipur

New Delhi

Kolkata

Chennai

Ahmadabad

Lucknow

Nagpur

Patna

Surat

Telangana

3 Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

Who is the reader?

Any participant or stakeholder in the biscuits and cookies industry, who would benefit from this report

The report will also help analysts, industry experts or any person looking for an in-depth understanding of the biscuits and

cookies industry

Purpose of the report

The report gives insights on how the biscuits and cookies industry is expected to grow in the coming years till 2019. It is

aimed at giving intelligent and actionable insights on the drivers and challenges for the industry and key segmentation, i.e.

by end users and by geography

Another important aspect of the report is the profiles of the top industry players in biscuits and cookies industry in India

Scope of the report

This report looks at the current scenario for biscuits and cookies industry in India

Small home and local bakeries/cafes do not come under the purview of this report

Preface to the report

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

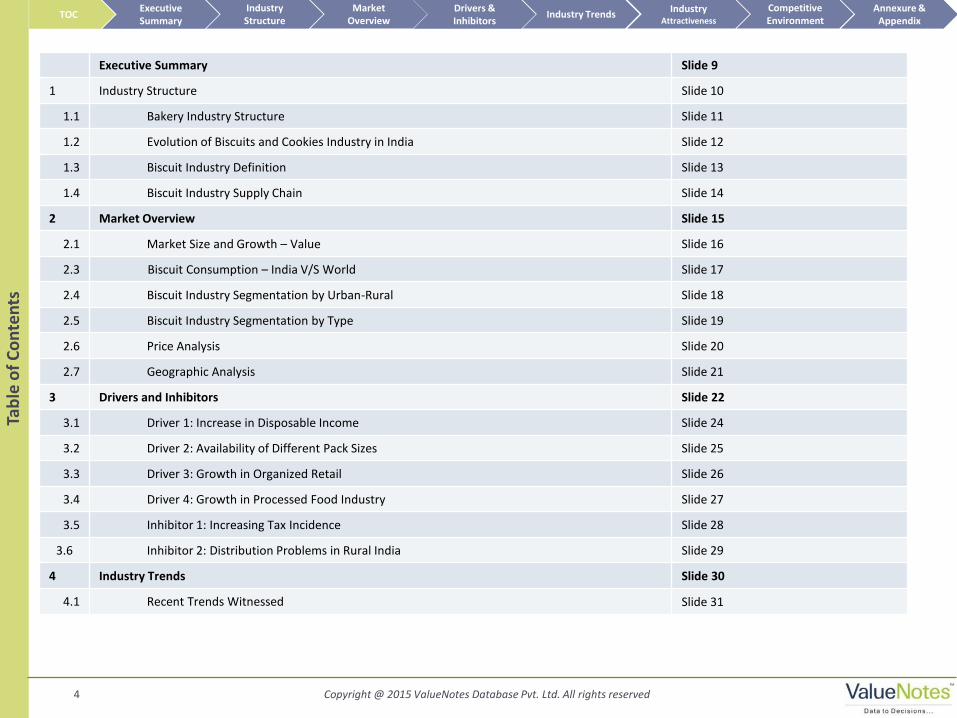

Executive Summary Slide 9

1 Industry Structure Slide 10

1.1 Bakery Industry Structure Slide 11

1.2 Evolution of Biscuits and Cookies Industry in India Slide 12

1.3 Biscuit Industry Definition Slide 13

1.4 Biscuit Industry Supply Chain Slide 14

2 Market Overview Slide 15

2.1 Market Size and Growth – Value Slide 16

2.3 Biscuit Consumption – India V/S World Slide 17

2.4 Biscuit Industry Segmentation by Urban-Rural Slide 18

2.5 Biscuit Industry Segmentation by Type Slide 19

2.6 Price Analysis Slide 20

2.7 Geographic Analysis Slide 21

3 Drivers and Inhibitors Slide 22

3.1 Driver 1: Increase in Disposable Income Slide 24

3.2 Driver 2: Availability of Different Pack Sizes Slide 25

3.3 Driver 3: Growth in Organized Retail Slide 26

3.4 Driver 4: Growth in Processed Food Industry Slide 27

3.5 Inhibitor 1: Increasing Tax Incidence Slide 28

3.6 Inhibitor 2: Distribution Problems in Rural India Slide 29

4 Industry Trends Slide 30

4.1 Recent Trends Witnessed Slide 31

4

Tab

le o

f C

on

ten

ts

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

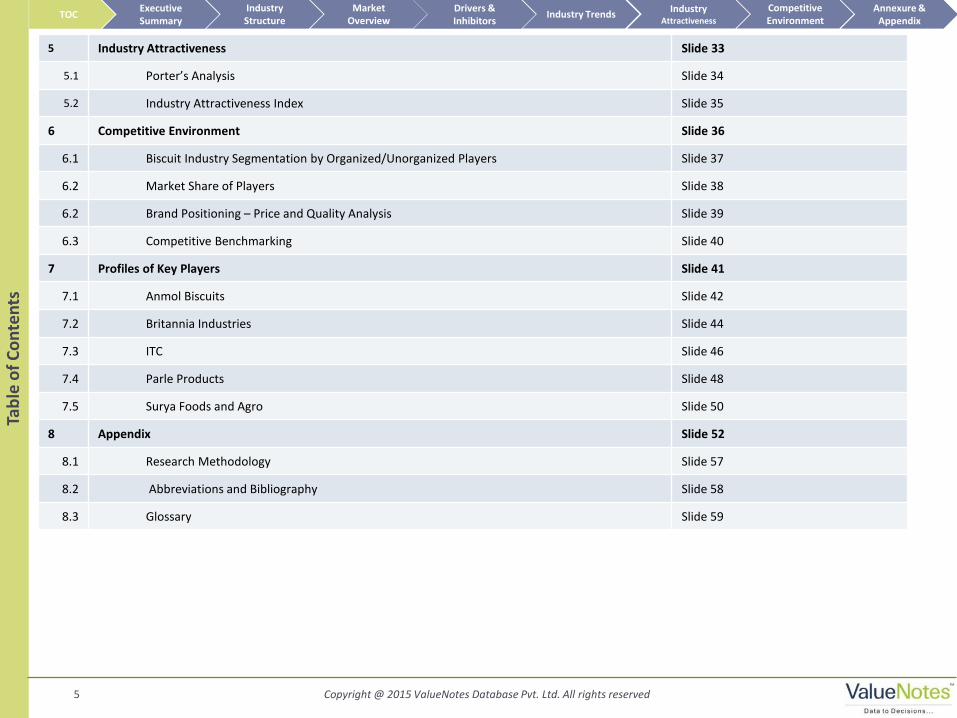

5 Industry Attractiveness Slide 33

5.1 Porter’s Analysis Slide 34

5.2 Industry Attractiveness Index Slide 35

6 Competitive Environment Slide 36

6.1 Biscuit Industry Segmentation by Organized/Unorganized Players Slide 37

6.2 Market Share of Players Slide 38

6.2 Brand Positioning – Price and Quality Analysis Slide 39

6.3 Competitive Benchmarking Slide 40

7 Profiles of Key Players Slide 41

7.1 Anmol Biscuits Slide 42

7.2 Britannia Industries Slide 44

7.3 ITC Slide 46

7.4 Parle Products Slide 48

7.5 Surya Foods and Agro Slide 50

8 Appendix Slide 52

8.1 Research Methodology Slide 57

8.2 Abbreviations and Bibliography Slide 58

8.3 Glossary Slide 59

5

Tab

le o

f C

on

ten

ts

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved 6

Tab

le o

f C

on

ten

ts |

Lis

t o

f C

har

ts &

Tab

les

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

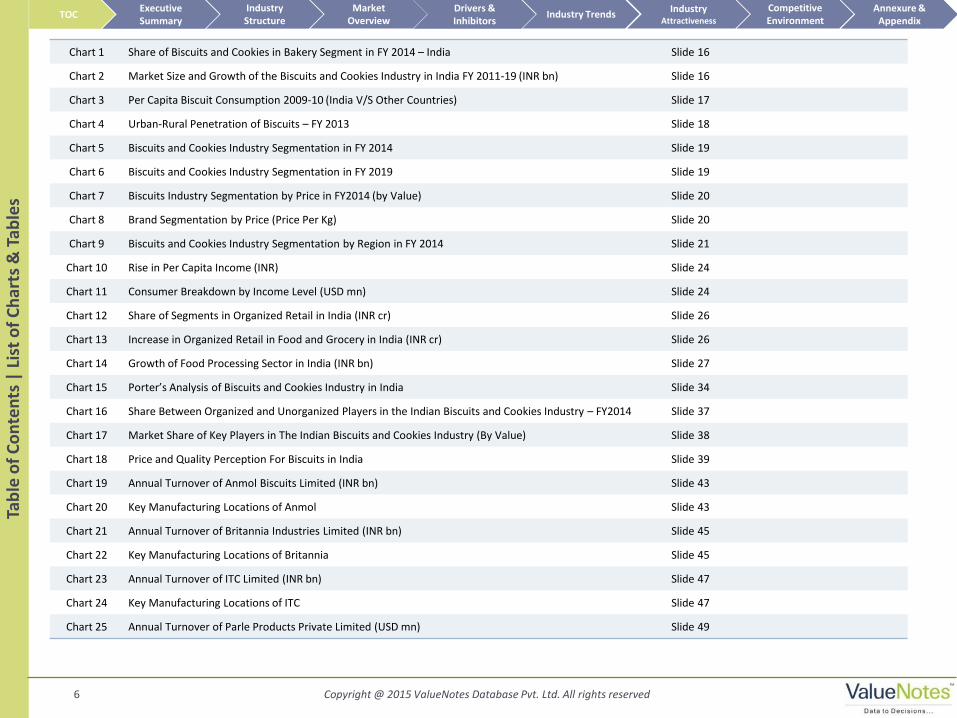

Chart 1 Share of Biscuits and Cookies in Bakery Segment in FY 2014 – India Slide 16

Chart 2 Market Size and Growth of the Biscuits and Cookies Industry in India FY 2011-19 (INR bn) Slide 16

Chart 3 Per Capita Biscuit Consumption 2009-10 (India V/S Other Countries) Slide 17

Chart 4 Urban-Rural Penetration of Biscuits – FY 2013 Slide 18

Chart 5 Biscuits and Cookies Industry Segmentation in FY 2014 Slide 19

Chart 6 Biscuits and Cookies Industry Segmentation in FY 2019 Slide 19

Chart 7 Biscuits Industry Segmentation by Price in FY2014 (by Value) Slide 20

Chart 8 Brand Segmentation by Price (Price Per Kg) Slide 20

Chart 9 Biscuits and Cookies Industry Segmentation by Region in FY 2014 Slide 21

Chart 10 Rise in Per Capita Income (INR) Slide 24

Chart 11 Consumer Breakdown by Income Level (USD mn) Slide 24

Chart 12 Share of Segments in Organized Retail in India (INR cr) Slide 26

Chart 13 Increase in Organized Retail in Food and Grocery in India (INR cr) Slide 26

Chart 14 Growth of Food Processing Sector in India (INR bn) Slide 27

Chart 15 Porter’s Analysis of Biscuits and Cookies Industry in India Slide 34

Chart 16 Share Between Organized and Unorganized Players in the Indian Biscuits and Cookies Industry – FY2014 Slide 37

Chart 17 Market Share of Key Players in The Indian Biscuits and Cookies Industry (By Value) Slide 38

Chart 18 Price and Quality Perception For Biscuits in India Slide 39

Chart 19 Annual Turnover of Anmol Biscuits Limited (INR bn) Slide 43

Chart 20 Key Manufacturing Locations of Anmol Slide 43

Chart 21 Annual Turnover of Britannia Industries Limited (INR bn) Slide 45

Chart 22 Key Manufacturing Locations of Britannia Slide 45

Chart 23 Annual Turnover of ITC Limited (INR bn) Slide 47

Chart 24 Key Manufacturing Locations of ITC Slide 47

Chart 25 Annual Turnover of Parle Products Private Limited (USD mn) Slide 49

Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved 7

Tab

le o

f C

on

ten

ts |

Lis

t o

f C

har

ts &

Tab

les

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

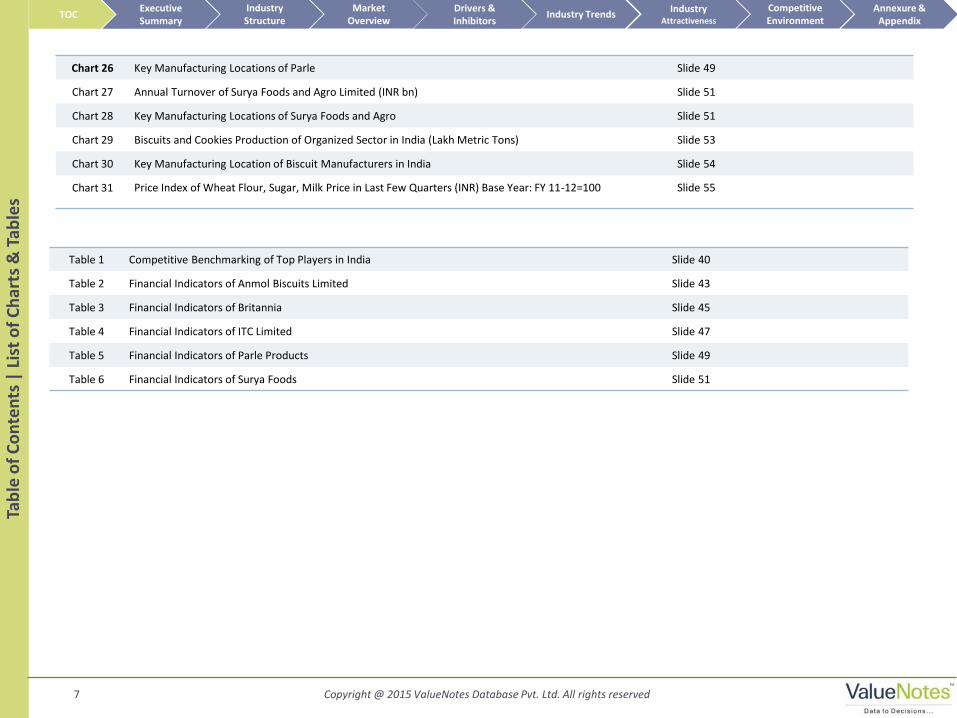

Table 1 Competitive Benchmarking of Top Players in India Slide 40

Table 2 Financial Indicators of Anmol Biscuits Limited Slide 43

Table 3 Financial Indicators of Britannia Slide 45

Table 4 Financial Indicators of ITC Limited Slide 47

Table 5 Financial Indicators of Parle Products Slide 49

Table 6 Financial Indicators of Surya Foods Slide 51

Chart 26 Key Manufacturing Locations of Parle Slide 49

Chart 27 Annual Turnover of Surya Foods and Agro Limited (INR bn) Slide 51

Chart 28 Key Manufacturing Locations of Surya Foods and Agro Slide 51

Chart 29 Biscuits and Cookies Production of Organized Sector in India (Lakh Metric Tons) Slide 53

Chart 30 Key Manufacturing Location of Biscuit Manufacturers in India Slide 54

Chart 31 Price Index of Wheat Flour, Sugar, Milk Price in Last Few Quarters (INR) Base Year: FY 11-12=100 Slide 55

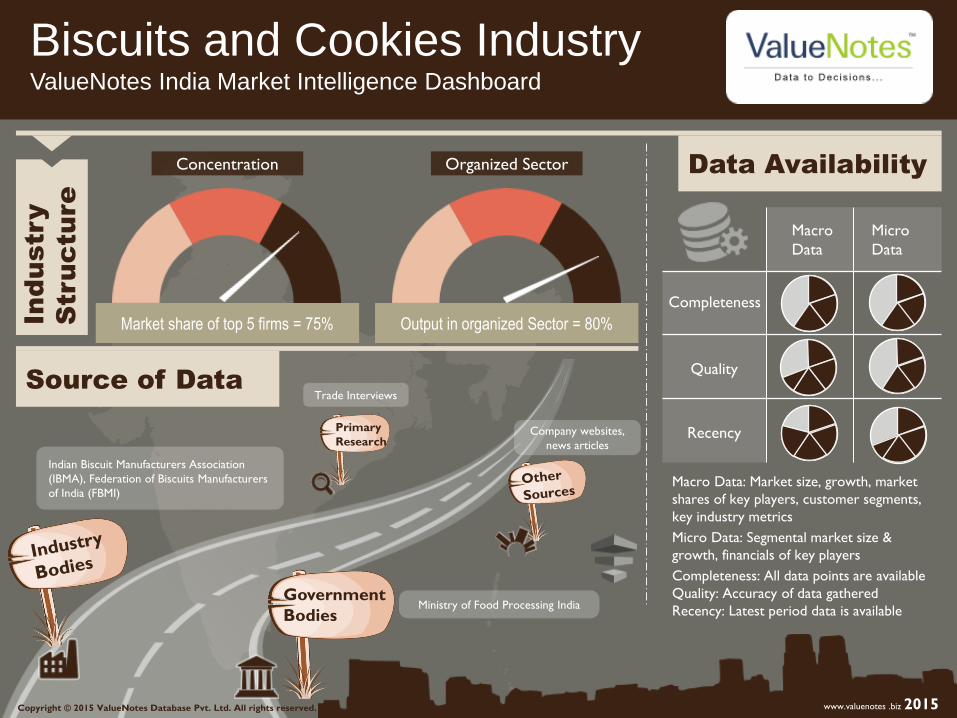

Biscuits and Cookies Industry ValueNotes India Market Intelligence Dashboard

Market share of top 5 firms = 75% Output in organized Sector = 80%

Organized Sector Concentration

Macro Data: Market size, growth, market

shares of key players, customer segments,

key industry metrics

Micro Data: Segmental market size &

growth, financials of key players

Completeness: All data points are available

Quality: Accuracy of data gathered

Recency: Latest period data is available

Source of Data

Data Availability

In

du

stry

Stru

cture

Ministry of Food Processing India

Company websites,

news articles

Indian Biscuit Manufacturers Association

(IBMA), Federation of Biscuits Manufacturers

of India (FBMI)

Copyright © 2015 ValueNotes Database Pvt. Ltd. All rights reserved. www.valuenotes .biz 2015

Government

Bodies

Primary

Research

Trade Interviews

Completeness

Quality

Recency

Macro

Data

Micro

Data

Market Size and Growth

Industry Segmentation

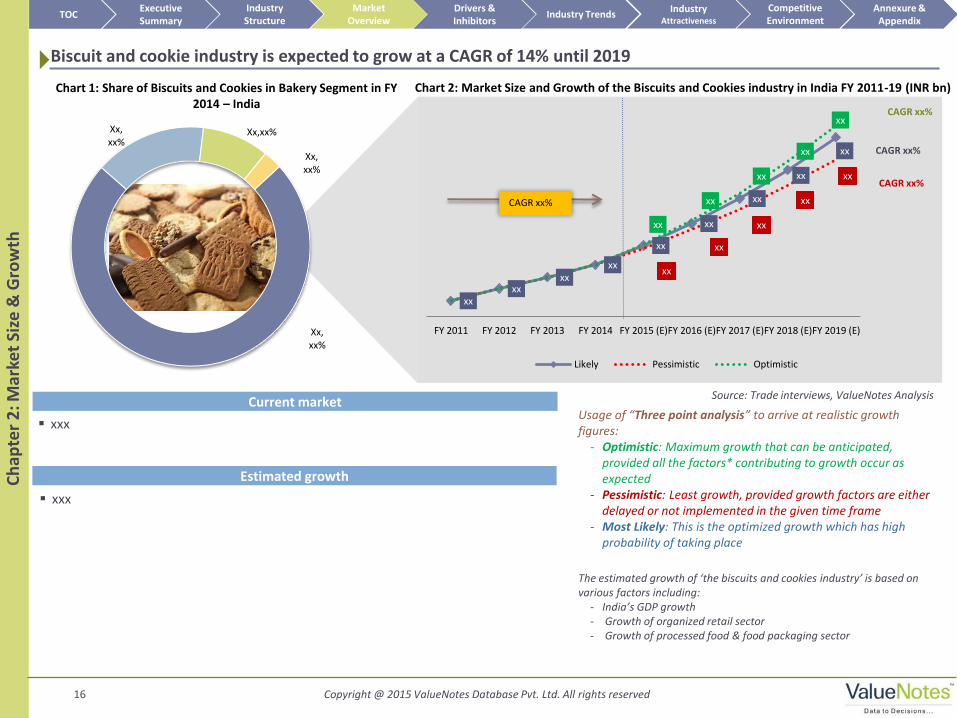

The biscuits and cookies industry in India has been growing at a CAGR of 10% for the last three years, and is currently valued at INR 145bn

India is currently the world’s largest biscuit consuming nation

The industry is expected to grow at a CAGR of 14% till FY 2019

ValueNotes estimates that the industry will be worth approximately INR 279bn (~USD 4.65bn) by FY 2019

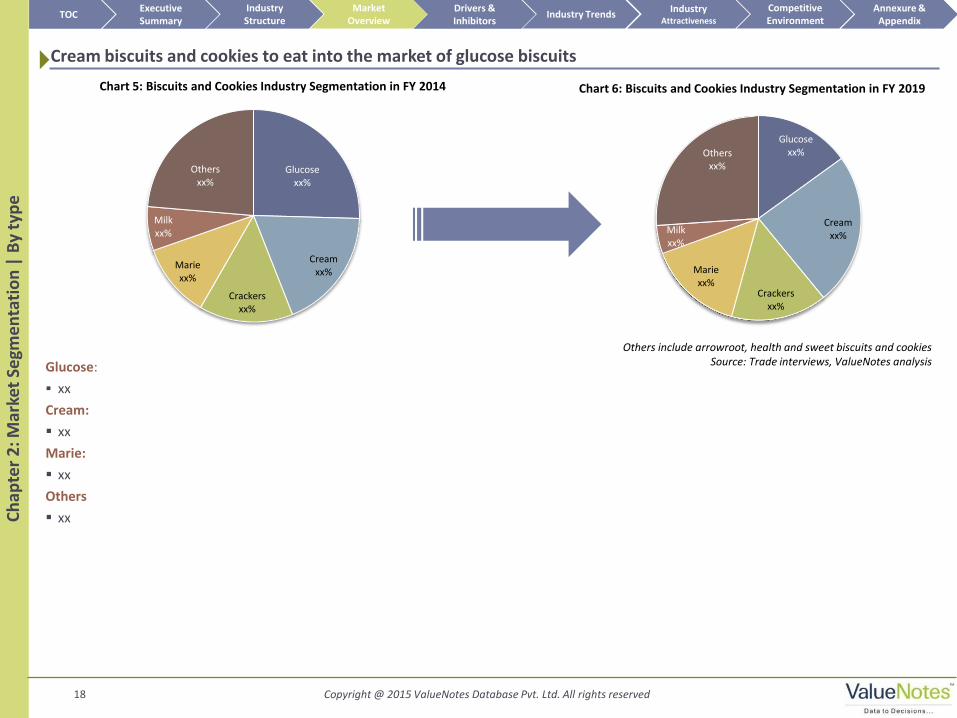

Glucose biscuits (~25%) have the highest share in the industry

Compared to other FMCG products, the penetration of biscuits and cookies, in both the urban and rural areas is quite high (94% and 83%, respectively)

East and North India have the highest consumption of biscuits and cookies in the country

Key Players

80% of the market is currently organized

The top four players in the market for biscuits and cookies are:

Parle Products, Britannia, ITC and Surya Foods and Agro

Both Britannia and Parle account for 61% share of the market

9 Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

Exe

cuti

ve S

um

mar

y

The biscuits and cookies industry in India has been given an Industry Attractiveness Rating of 6.7 as per the ‘ValueNotes Industry Attractiveness Rating Evaluation System’

Drivers and Challenges

Drivers:

Increasing disposable income, changing lifestyle, growth in organized retail and increasing consumption of processed and packaged food are the main drivers of the industry

Challenges:

Increasing tax incidence and rising input costs are the main challenges that the biscuits and cookies industry is currently facing

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

34%

27%

8%

4% 2%

25%

Parle

Britannia

ITC

Surya Foods

Anmol

Others

Industry Structure

Picture Courtesy: Daifuku

Insert appropriate picture

11 Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

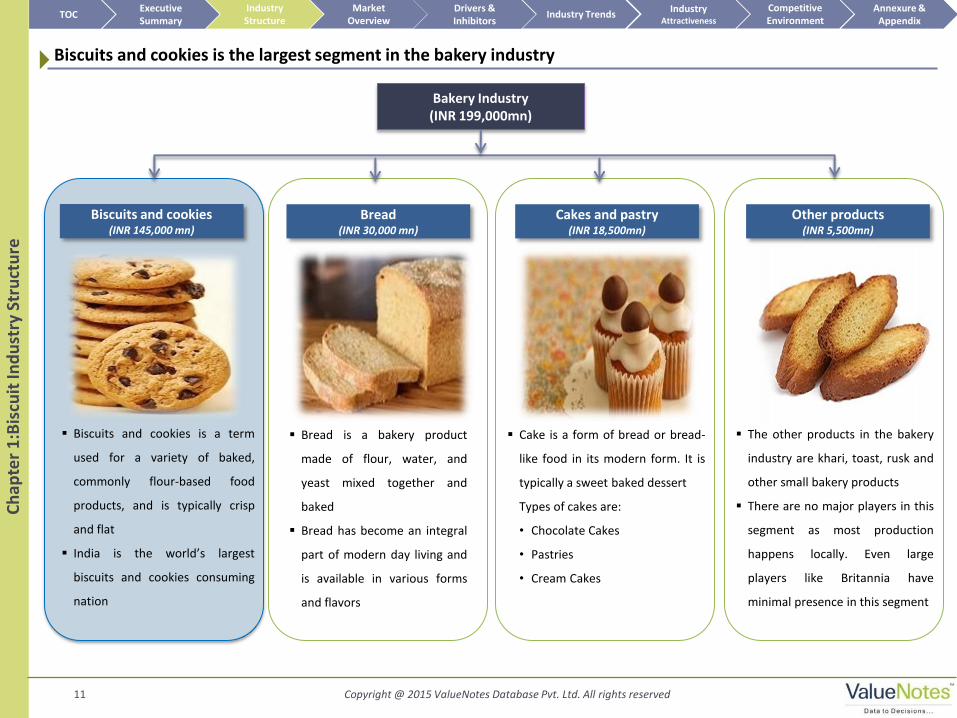

Biscuits and cookies is the largest segment in the bakery industry

Ch

apte

r 1

:Bis

cuit

Ind

ust

ry S

tru

ctu

re

Bread is a bakery product

made of flour, water, and

yeast mixed together and

baked

Bread has become an integral

part of modern day living and

is available in various forms

and flavors

Cake is a form of bread or bread-

like food in its modern form. It is

typically a sweet baked dessert

Types of cakes are:

• Chocolate Cakes

• Pastries

• Cream Cakes

Bakery Industry (INR 199,000mn)

Biscuits and cookies (INR 145,000 mn)

Bread (INR 30,000 mn)

Cakes and pastry (INR 18,500mn)

Other products (INR 5,500mn)

The other products in the bakery

industry are khari, toast, rusk and

other small bakery products

There are no major players in this

segment as most production

happens locally. Even large

players like Britannia have

minimal presence in this segment

Biscuits and cookies is a term

used for a variety of baked,

commonly flour-based food

products, and is typically crisp

and flat

India is the world’s largest

biscuits and cookies consuming

nation

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved 12

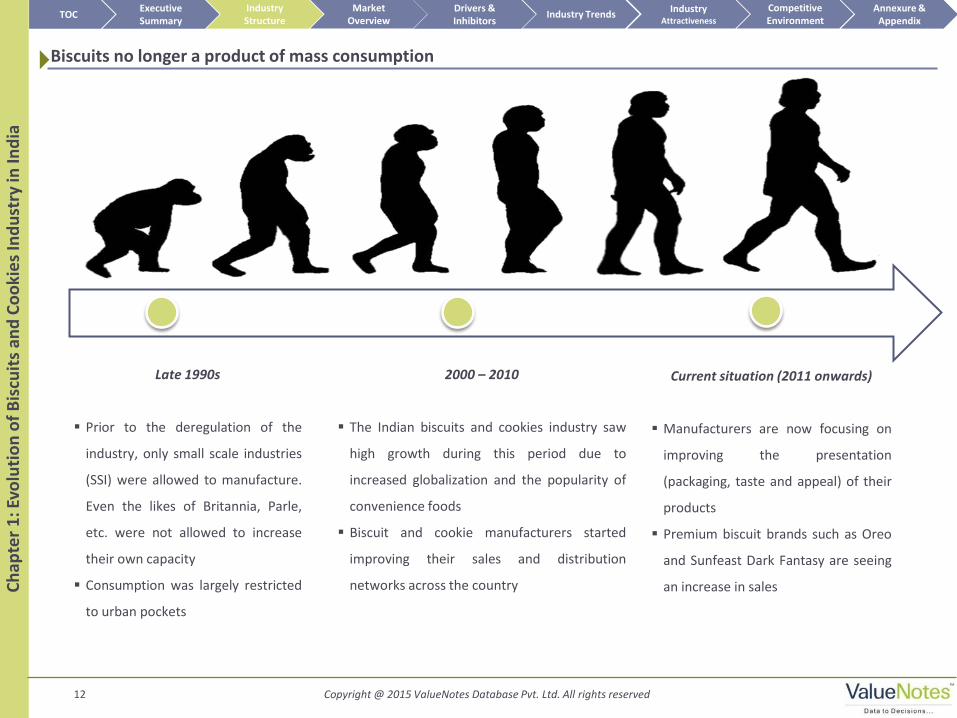

Biscuits no longer a product of mass consumption

Late 1990s

Prior to the deregulation of the

industry, only small scale industries

(SSI) were allowed to manufacture.

Even the likes of Britannia, Parle,

etc. were not allowed to increase

their own capacity

Consumption was largely restricted

to urban pockets

2000 – 2010

The Indian biscuits and cookies industry saw

high growth during this period due to

increased globalization and the popularity of

convenience foods

Biscuit and cookie manufacturers started

improving their sales and distribution

networks across the country

Current situation (2011 onwards)

Manufacturers are now focusing on

improving the presentation

(packaging, taste and appeal) of their

products

Premium biscuit brands such as Oreo

and Sunfeast Dark Fantasy are seeing

an increase in sales Ch

apte

r 1

: Evo

luti

on

of

Bis

cuit

s an

d C

oo

kie

s In

du

stry

in In

dia

TOC

Market Overview

Annexure & Appendix

Industry Trends Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved 13

Biscuits is a term used for a variety of baked, commonly flour-based food products

The types of biscuits based on ingredients are:

• Glucose: Small and rectangular flat-baked sweet biscuit

• Crackers: Thin crisp wafer or biscuit, usually made of unsweetened dough

• Milk: Biscuits with milk as the key ingredient

• Marie: Sweet round biscuit with its name embossed on its top surface; the edges embossed with an intricate design. Marie biscuits are

less sweet when compared to glucose biscuits

• Cream: Biscuits with a creamy filling

• Cookies: Small cake made from stiff, sweet dough rolled and sliced or dropped by spoonfuls on a large, flat pan (cookie sheet) and baked

This report covers:

• The organized sector of biscuits industry in India – which includes

private and public manufacturers registered with the India Biscuit

Manufacturers Association (IBMA) and Federation of Biscuit

Manufacturer of India (FBMI)

This report does not cover:

• Small home and local bakeries owned by individuals

Definition of biscuits and cookies

Ch

apte

r 1

: Def

init

ion

of

Bis

cuit

s an

d C

oo

kie

s TOC

Market Overview

Annexure & Appendix

Industry Trends Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

14 Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

Ch

apte

r 1

: In

du

stry

Su

pp

ly C

hai

n

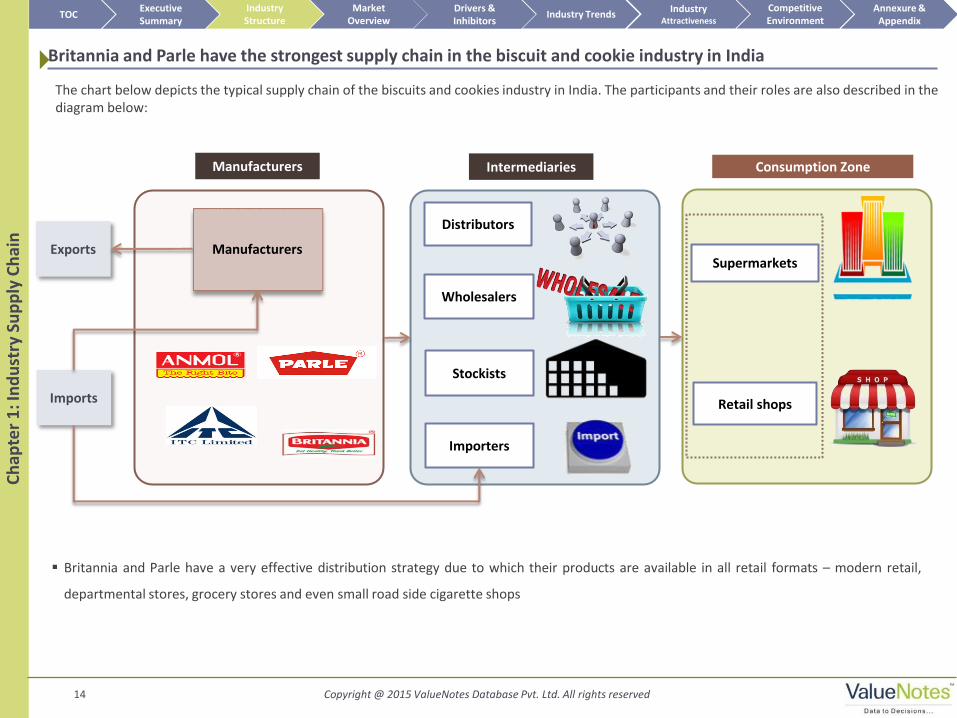

Britannia and Parle have the strongest supply chain in the biscuit and cookie industry in India

The chart below depicts the typical supply chain of the biscuits and cookies industry in India. The participants and their roles are also described in the diagram below:

Britannia and Parle have a very effective distribution strategy due to which their products are available in all retail formats – modern retail,

departmental stores, grocery stores and even small road side cigarette shops

Consumption Zone

Manufacturers

Manufacturers

Supermarkets

Retail shops

Intermediaries

Stockists

Distributors

Wholesalers

Exports

Importers

Imports

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Market Overview

xx xx

xx xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 (E)FY 2016 (E)FY 2017 (E)FY 2018 (E)FY 2019 (E)

Likely Pessimistic Optimistic

CAGR xx%

xxx Usage of “Three point analysis” to arrive at realistic growth figures:

- Optimistic: Maximum growth that can be anticipated, provided all the factors* contributing to growth occur as expected

- Pessimistic: Least growth, provided growth factors are either delayed or not implemented in the given time frame

- Most Likely: This is the optimized growth which has high probability of taking place

16 Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

Chart 2: Market Size and Growth of the Biscuits and Cookies industry in India FY 2011-19 (INR bn)

The estimated growth of ‘the biscuits and cookies industry’ is based on various factors including:

- India’s GDP growth - Growth of organized retail sector - Growth of processed food & food packaging sector

Source: Trade interviews, ValueNotes Analysis Current market

Estimated growth Ch

apte

r 2

: Mar

ket

Size

& G

row

th

Chart 1: Share of Biscuits and Cookies in Bakery Segment in FY 2014 – India

Biscuit and cookie industry is expected to grow at a CAGR of 14% until 2019

xxx

Industry Attractiveness

CAGR xx%

CAGR xx%

CAGR xx%

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Xx, xx%

Xx, xx%

Xx,xx%

Xx, xx%

xx

xx xx

xx xx xx

xx xx

xx xx

Ireland Netherland UK Italy Belgium Switzerland USA Japan India China

Per Capita Consumption (Kgs)

17 Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

Per capita consumption of biscuits is one of the lowest in India

Ch

apte

r 2

: Bis

cuit

Co

nsu

mp

tio

n –

Ind

ia v

/s W

orl

d

Chart 3: Per Capita Biscuit Consumption 2009-10 (India V/S Other Countries)

xx

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Source: FnB News, Indian Mirror

Glucose xx%

Cream xx%

Crackers xx%

Marie xx%

Milk xx%

Others xx%

Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved 18

Chart 5: Biscuits and Cookies Industry Segmentation in FY 2014 Chart 6: Biscuits and Cookies Industry Segmentation in FY 2019

Cream biscuits and cookies to eat into the market of glucose biscuits

Ch

apte

r 2

: Mar

ket

Segm

en

tati

on

| B

y ty

pe

Glucose:

xx

Cream:

xx

Marie:

xx

Others

xx

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Others include arrowroot, health and sweet biscuits and cookies Source: Trade interviews, ValueNotes analysis

Glucose xx%

Cream xx%

Crackers xx%

Marie xx%

Milk xx%

Others xx%

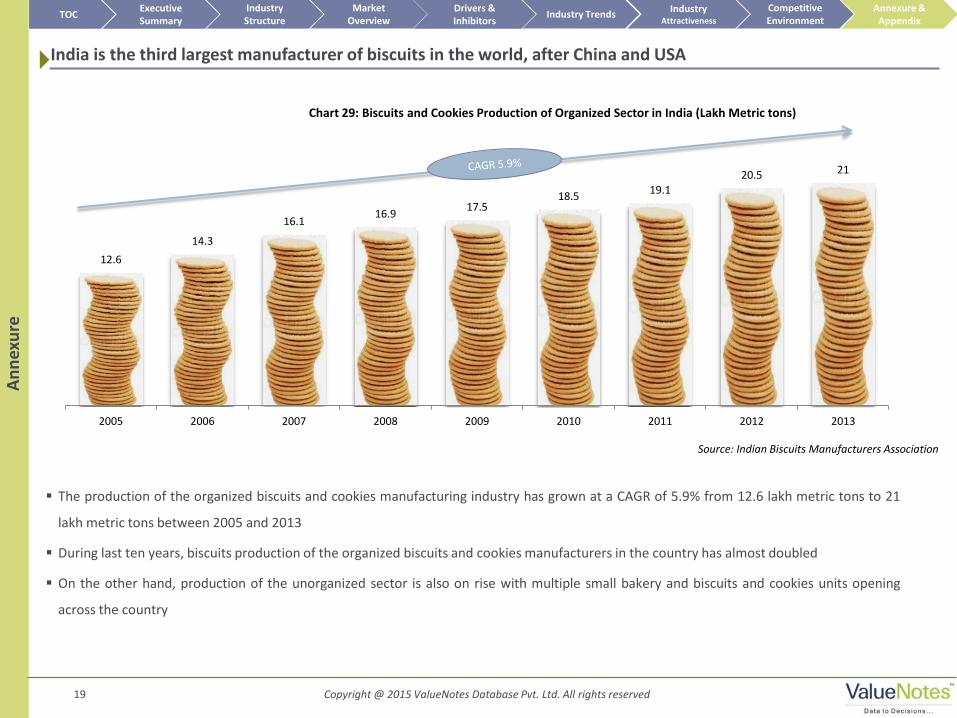

12.6

14.3

16.1 16.9

17.5 18.5

19.1 20.5 21

2005 2006 2007 2008 2009 2010 2011 2012 2013

19 Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

India is the third largest manufacturer of biscuits in the world, after China and USA

The production of the organized biscuits and cookies manufacturing industry has grown at a CAGR of 5.9% from 12.6 lakh metric tons to 21

lakh metric tons between 2005 and 2013

During last ten years, biscuits production of the organized biscuits and cookies manufacturers in the country has almost doubled

On the other hand, production of the unorganized sector is also on rise with multiple small bakery and biscuits and cookies units opening

across the country

Chart 29: Biscuits and Cookies Production of Organized Sector in India (Lakh Metric tons)

Source: Indian Biscuits Manufacturers Association

An

nex

ure

TOC

Market Overview

Annexure & Appendix

Industry Trends Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

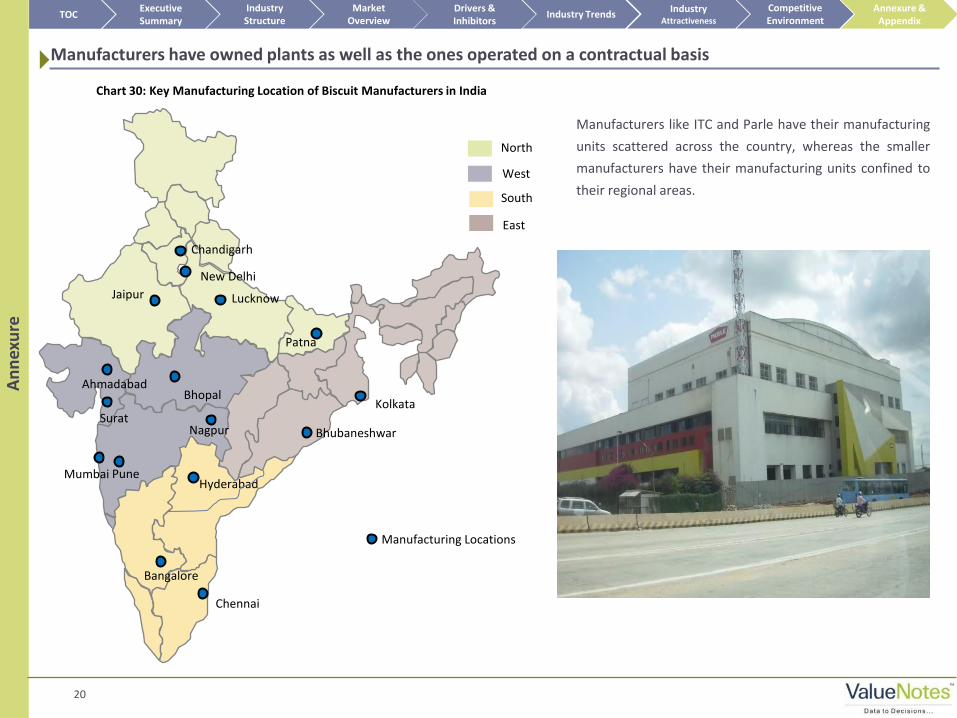

Manufacturers have owned plants as well as the ones operated on a contractual basis

Chart 30: Key Manufacturing Location of Biscuit Manufacturers in India

An

nex

ure

TOC

Market Overview

Annexure & Appendix

Industry Trends Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

20

Manufacturing Locations

Manufacturers like ITC and Parle have their manufacturing

units scattered across the country, whereas the smaller

manufacturers have their manufacturing units confined to

their regional areas. West

North

South

East

Mumbai Pune Hyderabad

Bangalore

Jaipur

New Delhi

Kolkata

Chennai

Ahmadabad

Lucknow

Nagpur

Patna

Surat

Bhopal

Chandigarh

Bhubaneshwar

Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved 21

An

nex

ure

Up till mid 2014, prices of wheat, vegetable oil, ghee and sugar were increasing on an average by ~20-22% each year. Increasing input cost had

resulted in increasing operating costs of manufacturers. This had left the biscuit manufacturers with very thin margins

However, the scenario seems to be changing in the last 1-2 quarter. The key input prices - wheat and sugar were flat, while palm oil declined y-o-

y during the quarter. This has resulted to increased profitability of the biscuit manufacturers

Chart 31: Price Index of Wheat Flour, Sugar, and Butter in Last Few Quarters (INR) Base Year: FY 11-12=100

Source: Company annual report, ValueNotes research

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Raw material prices for comprises more than 50% of retail price of biscuits and cookies

100

121

133 128

135 135

116 114 111

104

93

108 118

116

110

FY 11-12 FY 12-13 FY 13-14 Q1 14-15 Q2 14-15 Q3 14-15

Flour Sugar Butter

Appendix

ValueNotes is a full-service market and business research firm. Since 2000, we have helped customers, in India and around the globe, make

better business decisions by providing actionable intelligence. Our customized research solutions, by way of projects and continuing

engagements, have helped serve specific business needs - market entry strategy, choice of location, partner selection, competitive intelligence,

investment appraisal, due diligence, and customer need analysis.

Over the years, ValueNotes has developed considerable domain knowledge in a variety of sectors and industries. More important, we understand

how to develop and deploy appropriate research methodologies best suited for diverse markets. We've developed proprietary research methods

to deal with unorganized, information-scarce markets; and analytical techniques to triangulate, validate and correlate incomplete or unrelated

information

23 Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

Biscuits and Cookies Industry

in India

Government Websites & Publications

Industry Intelligence

Industry Associations Publications

& News Releases

Press Releases &

Publications by Industry

Players

Industry Reports/

Trade Publications

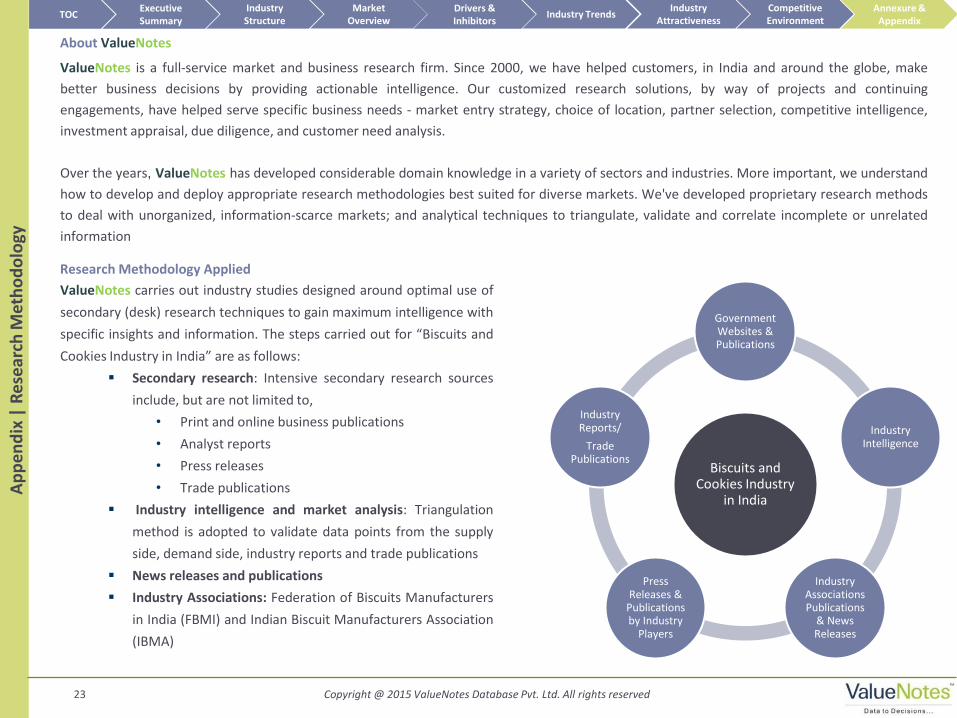

ValueNotes carries out industry studies designed around optimal use of

secondary (desk) research techniques to gain maximum intelligence with

specific insights and information. The steps carried out for “Biscuits and

Cookies Industry in India” are as follows:

Secondary research: Intensive secondary research sources

include, but are not limited to,

• Print and online business publications

• Analyst reports

• Press releases

• Trade publications

Industry intelligence and market analysis: Triangulation

method is adopted to validate data points from the supply

side, demand side, industry reports and trade publications

News releases and publications

Industry Associations: Federation of Biscuits Manufacturers

in India (FBMI) and Indian Biscuit Manufacturers Association

(IBMA)

About ValueNotes

Research Methodology Applied

Ap

pe

nd

ix |

Re

sear

ch M

eth

od

olo

gy

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

24 Copyright @ 2015 ValueNotes Database Pvt. Ltd. All rights reserved

Ap

pe

nd

ix |

Ab

bre

viat

ion

s &

Bib

liogr

aph

y

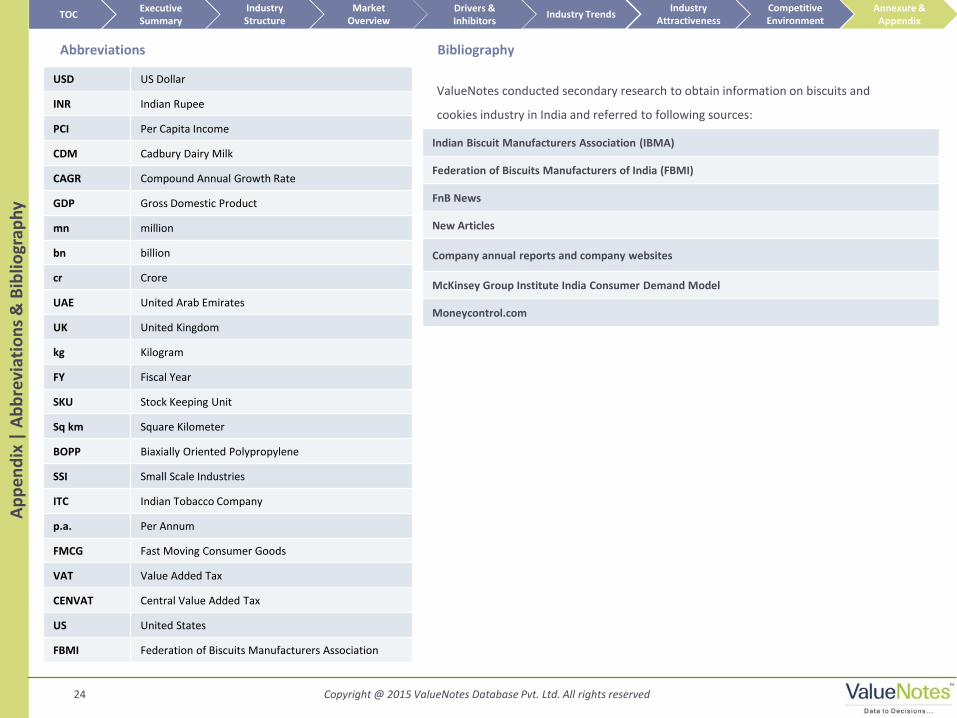

Abbreviations

USD US Dollar

INR Indian Rupee

PCI Per Capita Income

CDM Cadbury Dairy Milk

CAGR Compound Annual Growth Rate

GDP Gross Domestic Product

mn million

bn billion

cr Crore

UAE United Arab Emirates

UK United Kingdom

kg Kilogram

FY Fiscal Year

SKU Stock Keeping Unit

Sq km Square Kilometer

BOPP Biaxially Oriented Polypropylene

SSI Small Scale Industries

ITC Indian Tobacco Company

p.a. Per Annum

FMCG Fast Moving Consumer Goods

VAT Value Added Tax

CENVAT Central Value Added Tax

US United States

FBMI Federation of Biscuits Manufacturers Association

Indian Biscuit Manufacturers Association (IBMA)

Federation of Biscuits Manufacturers of India (FBMI)

FnB News

New Articles

Company annual reports and company websites

McKinsey Group Institute India Consumer Demand Model

Moneycontrol.com

Bibliography

ValueNotes conducted secondary research to obtain information on biscuits and

cookies industry in India and referred to following sources:

TOC Market

Overview Annexure &

Appendix Industry Trends

Competitive Environment

Industry Structure

Executive Summary

Drivers & Inhibitors

Industry Attractiveness

Author Profile

www.indianotes.com Indian Markets

www.sourcingnotes.com Outsourcing Intelligence

www.valuenotes.biz Research & Consulting

ValueNotes Database Pvt Ltd 1 Bhuvaneshwar Society, Abhimanshree Road Pashan, Pune 411 008, Maharashtra, India

Other Industry Reports by ValueNotes:

1. Chocolate industry in India

2. Bread industry in India

3. Heat and eat industry in India

Disclaimer: This short industry report is published for general information only. Although high standards have been used in the preparation, ValueNotes is not responsible for any loss or damage arising from use of this report. The information contained herein is from publicly available data or other sources believed to be reliable. While we would endeavor to update the information herein on reasonable basis, ValueNotes is under no obligation to update or keep the information current. This report is the sole property of ValueNotes and must not be copied, either in whole or in part, or distributed or redistributed to any other person in any form.

in case of any queries, mail us at [email protected]

[email protected] | +91 20 6623 1743

About the author:

As a senior analyst at ValueNotes, Tejaswee Shrestha has worked on opportunity assessment studies in manufacturing & engineering sector where she has been involved in the formulating recommendation and entry strategies. Her main focus of studies at ValueNotes has been customer engagement studies in various industries such as lighting and engineering industries. Her projects also include due diligence and industry tracking. She also is a regular writer for ValueNotes where she contributes actively to blogs and articles.