resource based view_3

TRANSCRIPT

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 1/26

© cademy of Management ournal1996, Vol. 39, No. 3. 519-543.

THE RESOURCE-BASED VIEW OF THE FIRM INTWO ENVIRONMENTS: THE HOLLYWOOD FILM

STUDIOS FROM 1936 TO 1965

DANNY MILLEREcole des Hautes Etudes Commerciales, Montreal,

and Columbia UniversityJAMAL SHAMSIE

New York University

This article continues to operationally define and test the resource-hased view of the firm in a study of the major U.S. film studios from1936 to 1965. We found that property-hased resources in the form ofexclusive long-term contracts with stars and theaters helped financialperformance in the stable, predictable environment of 1936 -50 . In con-trast, knowledge-based resources in the form of production and coordi-native talent and budgets boosted financial performance in the moreuncertain changing and unpredictable) post-television environmentof 1951-65.

The resource-based view of the firm provides a useful complement to

Porter's (1980) w ell-kno w n struc tural pe rspectiv e of strategy. This view shiftsthe emphasis from the competitive environment of firms to the resourcesthat firms have developed to compete in that environment. Unfortunately,although it has generated a great deal of conceptualizing (see reviews byBlack and Boal [1994] and Peteraf [1993]), the resource-based view is justbeginning to occasion systematic empirical study (Collis, 1991; H enderson

Cock burn, 1994; M ontgomery & W ernerfelt, 1988; M cGrath, MacM illan, &Venkatraman, 1995). Thu s, the concept of resources remains an am orpho usone that is rarely op erationally defined or tested for its performance imp lica-tions in different competitive environments.

In the interests of testing and advancing the application of the resource-based view, this research develops the distinction between property-basedand knowledge-based resources. We argue that the former are likely to con-tribute most to performance in stable and predictable settings, whereas thelatter w ill be of the greatest utility in un certain — that is, changing an d u np re-dictab le— env ironm ents (Miller, 1988; Th om pso n, 1967). Inde ed, in this arti-cle we attempt to move from a resource-based vie w toward a theo ry byprogressing from description to testable prediction. A view is a product

We would like to acknowledge the helpful suggestions of Ming-Jer Chen, Steve Zyglido-poulos, and two anonymous reviewers.

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 2/26

520 cademy of Managem ent Journal June

of evocative description, but theory demands the formulation of falsifiablepropositions.

T H E N T U R E O F R E S O U R C E S

Acco rding to W ernerfelt, resources can inc lud e any thin g that migh t hethought of as a strength or we akness of a given firm and so cou ld he definedas those [tangible and intangible assets] which are tied semipermanently tothe firm (1984: 172). Resources are said to confer end urin g com petitiveadvantages to a firm to the extent that they are rare or hard to imitate, haveno direct suhstitutes, and enable companies to pursue o ppo rtunities or avoidthreats (Barney, 1991). The last attribute is the most ob vious: resources m usthave some value—some capacity to generate profits or prevent losses. Butif all other firms have them , resources will be unable to contribute to sup eriorreturns: their general availability will neutralize any special advantage. Andfor the same reason, readily availahle suhstitutes for a resource will alsonullify its value. Th us, resources mu st be difficult to create, buy , sub stitute,or imitate. This last point is central to the arguments of the resource-basedview (Barney, 1991; Lippman Rum elt, 1982; Peteraf 1993). Un usual returnscannot be obtained when competitors can copy each other. Thus, the scopeof this study will he limited strictly to nonimitahle resources.

Clearly, there are many resources that may meet these criteria, albeit

w ith differing effectiveness un de r different c ircum stance s: im porta nt p aten tsor copyrights, brand nam es, prime d istribution locations, exclusive contractsfor unique factors of production, subtle technical and creative talents, andskills at collaboration or coordination (Black Boal, 1994).

There are a numher of ways in which the resource-based view can befurther developed. First, it may be useful to make some basic distinctionsamong the types of organizational resources that can generate unusual eco-nom ic return s. By specifying the distinctive advan tages of different type s ofresources, it may be possible to add precision to the research. Such distinc-tions will help avoid vague inferences that im pu te value to a firm's resource ssimply because it has performed well (cf. Black Boal, 1994; Fiol, 1991).

Second , to com plem ent its intern al focus, the resource-hased view nee dsto delineate the external environments in which different kinds of resourceswould be most productive. Just as contingency theory attempts to relatestructures and strategies to the contexts in which they are most appropriate(Burns & Stalker, 1 961 ; Th om pso n, 1967), so too m ust th e resource-basedview hegin to consider the contexts w ithin w hich various kinds of resourcew ill have the hest influence on performance (Amit & Schoem aker, 1993)Acco rding to Porter, Resou rces are only meaningful in the context of per-forming certain activities to achieve certain competitive advantages. Thecompetitive value of resources can he enhanced or eliminated by changes

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 3/26

1996 iller and Shamsie 521

Third, there is a nee d for more systematic em pirical studies to exam inethe conc eptua l claims of the resource-based scholars. Such stud ies, althoughgrowing in number (cf. Henderson Cockburn, 1994; McGrath et al., 1995;Montgomery W ernerfelt, 1988; Rob ins W iersema, 1995), rem ain too rare,perhaps because of the difficulties of pinning down the predictions of theresource-hased view and even of operationally defining the notion of re-sources (Black Boal, 1994; Fiol, 1991; Miller, 1996; Peteraf 1993).

This research begins to address each of these tasks. First, we derivea predictive classification that distinguishes between property-based andknow ledge-based resourc es. Second, we argue that the performance implica-tions each of these resources w ill differ in predictable as opposed to unc ertainenv ironm ents. Third, in order to test these notion s, we und ertook a longitudi-nal stud y of the seven major Hollywo od film studios durin g two very different

eras: the first, one of great stability and predictability, and the second, oneof much upheaval, change, and uncertainty.

THE CONCEPTUAL FRAMEWORK

Categorizing Resources

Several researchers have attempted to derive resource categorizationschem es. Barney (1991) suggested that resources could be grouped into phys i-cal, human, and capital categories. Grant (1991) added to these financial,technological, and reputational resources. Although very useful for the pur-poses for which they were designed, these categorizations bear no directrela tionship to Barney's (1991) initial criteria for utility, nam ely, value , rarity,difficulty of imitation, and unavailability of substitutes. In this article werevisit a pivotal one of these criteria—h arriers to imitability— to develop ourown typology. Imitability may be an important predictor of performance as,indeed, it is a central argument of the resource-based view that a firm canohtain unusual returns only when other firms are unable to imitate its re-sources (Barney, 1991; Lippman Rum elt, 1982). Othe rwise these resourceswo uld be less rare or valuable, and substitutability w ould be come irrelevant.

Property Based Versus Knowledge Based Resources

There app ear to be two fundam entally different ba ses of non imitability(Amit & Schoem aker, 1993; Hall, 1992, 1993; Lippm an & Rum elt, 1982).Some resources cannot be imitated because they are protected by propertyrights, such as contracts, deeds of ownership, or patents. Other resourcesare protected by knowledge barriers—by the fact that competitors do notknow how to imitate a firm's processes or skills.

Property based resources. Property rights control ap pro pria ble re-sources: those that tie up a specific and well-defined asset (Barney, 1991).When a company has exclusive ownership of a valuahle resource that c annothe legally imitated hy rivals, it controls that resource. It can thereby obtain

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 4/26

522 cademy of Managem ent fournol June

of its expected economic returns. Examples of property-based resources areenforceable long-term con tracts that mo nop olize scarce factors of prod uc tion ,embody exclusive rights to a valuable technology, or tie up channels ofdistribu tion. Property-based resources a pply to a specific p rod uc t or proc ess.

An d m any such resoiu-ces buffer an organ ization from com petition by creat-ing and protecting assets that are not available to rivals—at least not underequally favorable terms (Black Boal, 1994: 134). Typically, it is only thefortunate or insightful firms that are able to gain control over valuableproperty-based resources before their full value is publicly known.

Most competitors will be aware of the value of a rival's property-basedresources, and they may even have the knowledge to duplicate these re-sources. But they either lack the legal right or the historical endowment toimitate successfully. Indeed, it might be argued that in order for property-

based resources to generate unu sua l econo mic rents, they require protectionfrom exclusionary legal contracts, trade restrictions, or first-mover preemp-tion (Conner, 19 91 ; Grant, 1991).

Knowledge based resources. M any valuable resou rces are protec ted fromimitation not by property rights but by knowledge barriers. They cannot beimitated by competitors because they are subtle and hard to understand—because they involve talents that are elusive and whose connection withresults is difficult to discern (Lippman Rumelt, 1982). Knowledge-basedresources often take the form of particular skills: technical, creative, andcollaborative. For exam ple, some firms have the tec hnica l and creative exper-tise to develop competitive products and market them successfully. Othersmay have the collaborative or integrative skills that help experts to workand learn togethe r very effectively (Fiol, 1991; Hall, 1993; Itami, 1987; Lado Wilson, 1994).

Knowledge-based resources allow organizations to succeed not by mar-ket control or by precluding competition, but by giving firms the skills toadapt their products to market needs and to deal w ith com petitive challenges.Economic rents accrue to such skills in part because rivals are ignorant ofwhy a firm is so successful. It is often hard to know, for example, what goes

into a rival's creativity or teamw ork tha t makes it so effective. Such resource smay have wh at Lippm an and Rum elt (1982) called unc ertain imitability :they are protected from imitation not by legal or financial barriers, but byknowledge barriers. The protection of knowledge barriers is not perfect—itmay be possible for com petitors to develop sim ilar know ledge and ta lent.But this normally takes time, and by then, a firm may have gone on todevelop its skills further and to learn to use them in different ways (Lado

Wilson, 1994).Contrasts. The respective advantages of property-based and know ledge-

based resources are quite different. Property rights allow a firm to controlthe resources it needs to gain a competitive edge. They may, for example,tie up advantageous sources of supply, keeping them out of competitors'

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 5/26

1996 Miller and Shamsie 523

designed to respond and adapt to the challenges facing an organization.Creative skills, for instance, can be used to interpret customer desires andrespond to emerging market trends. Of course, property- and knowledge-based resources are not always independent, as the latter may sometimes be

used to develop or procure the former.A key them e of this article is that the benefits of property-based resou rces

are quite specific and fixed and thus, the resources are appropriate mostlyfor the environment for which they were developed. For example, a processpatent ceases to have value w hen it has been sup erseded by a new process;a prized location becomes useless when customers move away. In short, aparticular property right stops being valuable when the market no longervalues the property. Thus, when the environment changes, property-basedresources m ay lose their advantage . This is especially true if the enviro nm entalters in ways that could not have been predicted when the property wasdeveloped or acquired or when the fixed contract was made (GeroskiVlassopoulos, 1991). Thus, an uncertain environment—one that is changingand unpredictable—is the enemy of property-based resources.

Knowledge-based resources, on the other hand, often tend to be lessspecific and more fiexible. For example, a creative design team can inventproducts to meet an assortment of market needs. Such resources can help afirm respon d to a larger num ber of contingencies (Lado Wilson, 1994). Manyknowledge-based resources are in fact designed to cope with environmentalchange. Unfortunately, these resources are not protected by law from imita-tion, and many are unduly expensive in predictable settings, where moreroutine but far cheaper response mechanisms can be equally effective. Also,in placid environments, a firm's knowledge may evolve so slowly as to besubject to imitation by rivals. In short, property-based resources will be ofthe greatest utility in stable or predictable e nviron m ents, whe reas k now ledge-based reso urces w ill be most useful in uncertain that is, changing and u np re-dictable, environments.

YPOT S S

In order to establish the robustness of our distinction be twee n property-based an d know ledge-based res ources, we will examine two varieties of eachcategory: discrete resources and bundled, or systemic resources. Discreteresources stand alone and have value more or less independent of theirorganizational co ntexts. Exclusive contracts or tech nical sk ills are exam plesof such resou rces. Systemic resou rces, on the other hand , have value becau setheir components are part of a network or system. Outlets in an integrateddistribution network or skills within a well-coordinated team, for instance,are especially valuable w ithin the context of that system (Amit Schoemaker,1993). Stores in a retail chain may have extra value precisely because theybenefit from a national bran d nam e and econo mies of stand ardiza tion, prom o-tion, and administration. Scientists may be especially productive because of

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 6/26

524 Academy of Managem ent Journal June

discrete and systemic resources, calling them respectively elementary andhigher-level resources, and Black and Boal (1994) referred to traits versusconfigurations.

Discrete Property Based Resources

Discrete property-based resources may take the form of ow ners hip rightsor legal agreemen ts that give an organization c ontrol over scarce and valua bleinp uts , facilities, location s, or pate nts. Some resou rces, for exam ple, take theform of leases or contracts that give comp anies exclusive access to esp eciallyvaluable materials or to inputs of exceptionally low cost. Such resources areprotected by rule of law. And typically, the utility of any exclusive right orcontract will be a function of the ease and costs of its enforcement as wellas of its du ratio n (Conner, 1 991: 138).

Of course, not all firms can obtain su ch luc rative resou rces. The fortunateones may be those that were first to discover value in a resource or gainaccess to it, or that once had the power to negotiate favorable long-termagreeme nts (Lieberman Mo ntgomery, 1988). As most discrete resource sare independent of one another, a firm stands to gain by amassing as manyof these as it can, subject of course to their marginal costs and benefits. Forexample, some companies tie up so many sources of supply that their rivalsmust settle for inferior substitutes.

Because discrete property-based resources are prim arily design ed to pro-vide an organization with a high degree of control, they are likely to be of

most value in stable or predictable settings where the objects of controlmaintain their relevance. In such environments it is simpler to estimate thelife exp ectancy and thu s the value of most p rope rties, claims, and contrac ts. Itis also easiest there to plan for add itiona l resource acqu isition. Predictab ilityensu res that property-based resources w ill con tinu e to buffer a firm from itscompetition for quite some time (Wernerfelt Karnani, 1987).

Where the environment is changing unpredictably, however, property-based resources are in greater danger of obsolescence. A changing groupof competitors may devise new products or processes that nullify existingresource advantages. Customer tastes that alter rapidly may have the sameeffect. All such ch anges may be very difficult to foresee at the tim e of contract-ing. Exclusive sources of supply, for example, may lose their value whenthey are replaced by more up-to-date substitutes. Long-term leases on retail-ing space may be more of a liability th an a n asset w he n th e targeted c ustom ersshift to ano ther type of store or loca tion (Geroski V lassopou los, 1991).Similarly, discrete resources that rely on contracts supported by laws andstatutes are in danger of obsolescence the moment these laws change.

Hypothesis 1: Discrete property based resources will produce superior financial performance in predictable environments but will not do so in uncertain environmen ts.

Systemic Property Based Resources

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 7/26

1996 Miller and Shamsie 525

m ent. By them selves, most conc rete facilities are easily imitable: thu s, m uc hof their value relies on their role within and their links to an integratedsystem wh ose synergy is hard to du plicate (Barney, 1991 ; Black & Boal,1994). This is true of some integrated s upp ly, manufacturing, and distribution

systems. The units of a distribution network, for example, may be valuablebecause of their conne ction w ith a steady source of sup ply or with econom iesof administration and promotion engendered by a well-respected parentcom pany (Barney, 1991; Brumagin, 1994: 94).'

In the case of systemic resources, managers do not aim to tie up moreand m ore individua l assets, but to enhan ce the range and com prehensivenessof a pre-existing system. Resources are added not to substitute for existingassets but rather, to strengthen a system or competence that is already inplace. For example, one m ight acquire more d istributors or outlets to bolster

a distribution system (Lado, Boyd,

Wright, 1992: 86-87). The more elabo-rate the system, the more market pe netration it can provide, the more econom -ically it can allocate marketing, adm inistration, and even operating e xpen ses,and the more it can make use of an established brand image or reputation.

Like discrete property-based resource s, systemic resources w ill be m oreuseful in predictable than in uncertain competitive environments. When anenvironment is predictable, it is easier to appraise the value of systems andto augment them in an orderly way with the aim of increasing the scope ofmarket control. Predictability also allows a firm to determine the steps thatit needs to take to fortify its system. Indeed, it is only when the environmentis predictable and the existing system is secure that it makes sense for a firmto develop that system.

When the environment is changing unpredictably, however, managersmay be relu ctan t to bu ild onto a system w hos e longevity is difficult to estim ateor that is at risk of becoming obso lete. For exam ple, if distribu tion techno logychanges unpredictably, one cannot build onto existing networks. And in anuncertain environment in which clients' demands are ever-changing andhard to anticipate, most property-based systems are threatened with obso-lescense (Wernerfelt & Karnan i, 1987). Here the useful life of systemic re-

sources m ay be short and hard to predict, and a firm may find itself controllingassets that generate little revenue (Geroski Vlassospoulos, 1991).

Hypothesis 2: Systemic property based resources w ill produce superior financial performance in predictable environments but will not do so in uncertain environments.

' Of course, most fixed resources are eminently imitable. Superior mechanical equipment,for example, can usually be copied, as can most processes that are well understood (Nelson

Winter, 1982), Reed and DeF illippi claimed that a competitor can simply observe site-embodiedperformance effects and, through technological deduction, can deduce the same for physicalassets (1990: 93) Competitors may then gain access to the personnel or capital needed to

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 8/26

526 Academy of Mana gement Journal June

Discrete Knowledge Based Resources

To parallel our analysis of property-based resources, we examine bothdiscrete and systemic knowledge-based resources (Black Boal, 1994; Bru-mag in, 1994). Discrete know ledge-based resources may take the form of specific technical, functional, and creative skills (Itami, 1987; Winter, 1987).Such skills may be valuable because they are subject to uncer tain imitability(Lippman Rumelt, 1982). It is often hard to discern just what it is aboutthese skills that generates economic returns or customer loyalty. Therefore,com petitors do not know w hat to buy or imitate. This advantage is p rotectedprecisely because it is in some way ambiguou s and m ysterious, even to thosewho possess it (Lado W ilson, 1994; Reed De Fillippi, 1990). As w ithdiscrete property-based resources, firms can benefit from simultaneouslydeveloping as many of these knowledge resources as possible. For example

firms can at the same time pursue expertise in design, production, and mar-keting.Although unforeseeable changes in markets may render many property-

based resources obsolete, knowledge-based resources such as unusual cre-ative and technical skills may remain viable under varying conditions. In-deed , they m ay actually help a firm adap t its offerings to a changing env iron-m en t (Wernerf'elt Ka rnani, 1987). Some c reative skills are also quite fiexibleas they apply to different outputs and environments. And this makes themespecially useful in a changing, uncertain setting. For example, where theenvironment is particularly competitive and rivals are introducing manynew offerings, the skills of experts who can adapt and create better productswill be especially valuable.^

In a stable or predictable environment, firms may also benefit from dis-crete skills. But these afford less effective, less efficient, and less secureadvantages than do discrete property-based resources. Where a firm canenforce its legal property rights , it possesses almost perfect prote ction againstimitation. This is not true of the protection given by knowledge, which canbe lost, especially in stable settings in which knowledge and its applicationevolve more slowly and are thus easier to copy. Moreover, the high costs of

retaining very talented employees may not produce much net benefit instable contexts that do not demand the full exploitation of their unusualabilities. Predictable settings do not typically call for as deep or extensive aset of skills for prod uct or process inno vation and ada ptation as do un certa inand changing environments (Miller, 1988; Miller Friesen, 1984).

Hypothesis 3: Discrete knowledge based resources willproduce superior financial performance iri uncertain environments but will not do so in predictable environments.

A changing en vironm ent m ay itself confer un certain imitability on som e flexible resourcesIn uncertain settings, the situations facing each firm are constantly varying, as are the organiza-i l d I ld b diffi l h f fi i i h i

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 9/26

1996 iller and Shamsie 527

Systemic Knowledge Based Resources

Systemic knowledge-based resources may take the form of integrativeor coordinative skills required for multidisciplinary teamwork (Fiol, 1991;

Itami, 1987). Some organizations not only have a depth of technical, func-tional, and creative expe rtise but are also adept at integrating and coordinat-ing that expertise. They invest in team-building and collaborative efforts thatpromote adaptation and fiexibility. Indeed, it is not just skills in any onedomain, but rather, the way skills from several domains complement oneanother in a team, that gives many firms their competitive advantage (Hall,1993; Itami, 1987; Teece, Pisan o, Shu en, 1990; W inter, 1987).

Collaborative skills are most subject to uncertain imitability (Hall, 1993; eteraf 1993: 183). According to Reed and DeF illippi, am biguity may bederived from the complexity of skills and/or resource interactions within

com petenc ies and from interaction betw een com pete ncie s (1990: 93). The reis much subtlety in effective teamwork. The systemic nature of team andcoordinative skills makes them especially firm-specific—more valuable to afirm than to its com petitors (Dierickx & Cool, 1989: 1505). Team talents,therefore, are difficult for rivals to steal as they rely on the particular infra-structure, history, and collective experience of a specific organization.

Collaborative skills typically do not develop through programmed orroutin e activity. Instead, they require nu rturing from a history of challengingproduct development projects. These long-term projects force specialistsfrom different parts of an organization to work together intensively on acomplex set of problems. And such interaction broadens both the technicaland social knowledge of organizational actors and promotes ever more effec-tive collaboration (Itami, 1987; Schmookler, 1966).

The above argum ents suggest that team bu ilding is apt to be more ne ces-sary, more rewarding, and perhaps even more likely in uncertain than inpredictable environments (Hall, 1993; Porter, 1985). Collaborative ta lents arerobust—they apply to a wide variety of situations and products. In contrastwith fixed routines, teamwork enables companies to handle complex andchanging contingencies (Thomp son, 1967). M oreover, unlik e physical

assets, com petencies do not deteriorate as they are app lied and shared. . . .They gro w (Prahalad & Ham el, 1990: 82). Collaborative skills not onlyremain useful under changing environments, they also help firms to adaptand develop new products for evolving markets (Lawrence Lorsch, 1967;Th om pso n, 1967). Inde ed, the flexibility bo rn of m ultifunc tional collabora-tion will help firms to respond quickly to market changes and challenges(Mahoney Pandian, 1992; Wernerfelt Karnani, 1987).

In stable environments, on the other hand, the returns to collaborativeand adaptive skills may be small. Where tasks are unvarying, coordinationcan be routinized very efficiently, and thus coordinative or team skills willbe less important (Thompson, 1967). Moreover, when customer tastes andrivals' strategies are stable, there is little need to constantly rede sign or adap t

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 10/26

528 Academy of Mana gement Journal June

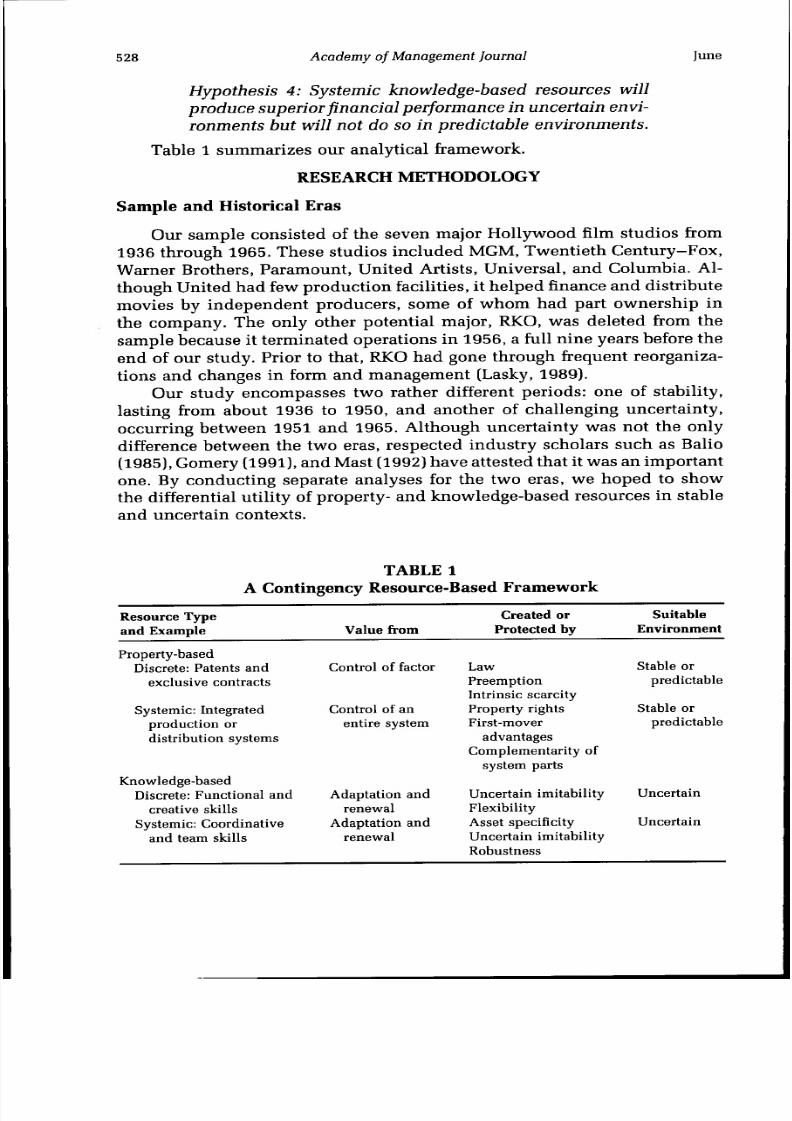

Hypothesis 4: Systemic knowledge based resources willproduce superior financial performance in uncertain environments but will not do so in predictable environments.

Table 1 sum m arizes our analytical framework.

RESEARCH METHODOLOGY

Sample and Historical Eras

Our sample consisted of the seven major Hollywood film studios from1936 through 1965. These studios included MGM, Tw entieth Ce ntury-F ox,Warner Brothers, Paramount, United Artists, Universal, and Columbia. Al-though Un ited had few pro duc tion facilities, it help ed finance and distributemovies by independent producers, some of whom had part ownership inthe company. The only other potential major, RKO, was deleted from thesam ple because it term inated operations in 1956, a full n ine years before theend of our study. Prior to that, RKO had gone through frequent reorganiza-tions and changes in form a nd mana gem ent Lasky, 1989).

Our study encompasses two rather different periods: one of stability,lasting fi-om about 1936 to 1950, and anothe r of challenging unc ertainty,occurring between 1951 and 1965. Although uncertainty was not the onlydifference between the two eras, respected industry scholars such as Balio 1985), Gomery 1991), and Mast 1992) have attested that it was an im portan t

one. By conducting separate analyses for the two eras, we hoped to showthe differential utility of property- and knowledge-based resources in stableand uncertain contexts.

TABLE 1A Contingency Resource Based Framework

Resource Typeand Example

Property-basedDiscrete: Patents and

exclusive contracts

Systemic: Integratedproduction ordistribution systems

Knowledge-based

Discrete: Functional andcreative skillsSystemic: Coordinative

Value from

Control of factor

Control of anentire system

Adaptation andrenewalAdaptation and

Created orProtected by

LawPreemptionIntrinsic scarcityProperty rightsFirst-mover

advantagesComplementarity of

system parts

Uncertain imitabilityFlexibilityAsset specificity

SuitableEnvironment

Stable orpredictable

Stable orpredictable

UncertainUncertain

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 11/26

1996 iller and Shamsie 529

The period from the early 1930s to the late 1940s is considered to bethe Golden Years of the major studios. Before then, there had been growingcon solidation in the film indu stry (Bordwell, Staiger, Th om pson , 1985:403). But the last significant merger took place between Fox and Twentieth

Century in 1935. Around the same time. Paramount reemerged from bank-ruptcy as a new organization. Thus, by 1936 the industry had matured intothe oligopoly that became known as the studio system. And for the nextdozen years or so, demand for Rims remained strong, reflected both by stablepatterns of attendance—80 to 90 million admissions per week throughoutthe entire period—and by gradually increasing box office revenues (Stein-berg, 1980). Also, stable customer preferences m eant tha t studios c ould p re-dict that particular stars, directors, and genres of films w ould rem ain pop ularfor a considerable time (Bohn, Stromgren, Johnson, 1978; Gomery, 1991).

Thus, the production process became quite routine as similar crews workedtogether under the supervision of a single production head or a few keyproducers (Staiger, 1985: 320).

All of the studios of the day developed their own stables of talent bysigning a wide variety of stars to exclusive, long-term contracts. Four of themajor studios also owned or leased theaters in significant locations acrossthe country. Collectively, the majors controlled fewer than 3,000 theaters ofthe 18,000 operating nationwide. These, however, included the preponder-ance of first-run cinemas in big cities that drew 75 percent of the nationalbox office (Balio, 1985: 255). Cinemas not associated with the major studioswere mostly in small towns and showed second-run films. Because manystudios co ntrolled their stars and w ere guaranteed distribution for their filmsvia their theaters, they were able to plan well in advance a steady stream offilm offerings (Gomery, 1991; W hitney, 1982). Stable dem and brought a veryreasonable chance of success, and control over theaters made sure all of astudio's films would have an audience.

The period from the early 1950s to the mid 1960s brought about signifi-cant transforma tions in the indu stry that greatly enhan ced the level of uncer-tainty (Balio, 1985; Mast, 1992). By 1950, television sets had entered 25percent of homes, and this penetration had doubled to 50 percent by 1952.As a result, cinema attenda nce declined significantly from 1949 to 1953 andthen stabilized at only about 40 to 50 million admissions per week. Firmsbegan groping to find new ways to attract moviegoers and soon started todifferentiate their films from television programs by making grander andmore lavish productions (Mast, 1992: 275; Stuart, 1982: 295). They experi-mented with new techniques involving color film, wide screens, and stereo-phonic sound. Thus, the technical and creative skills of studios became evermo re im portant as growing entertain m ent alternatives made moviegoers more

discrimina ting. Also, cycles of pop ularity ha d becam e mu ch shorter as jadedaudiences quickly grew tired of particular genres or stars (Bohn et al., 1978;G 1991) B ffi f il b f lli d d d

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 12/26

530 cademy of Manag ement Journal June

The concentration on more complex and expensive projects cut downon the number of films produced and made the success of each productionmore important. In response, some studios began to search for the few keystars, directors, or producers who could reduce the risks of their big budget

films (Kindem, 1982: 88). But now they were less apt to hire such peopleon a perm anen t basis as the pop ularity of talent could be rapidly ero ded andbecause talent would be underutilized with the few films made. As a result,the coordinative skills needed to assemble and direct nonpermanent castmembers in very complex productions became invaluable (Mast, 1992;Staiger, 1985). This was especially true as the complexity and variety ofproductions increased.

To contribute further to this climate of uncertainty, the studios beganto lose control over their distribution outlets and their stars. Although the

major studios were first targeted by antitrust proceedings in the late 1930s,the first truly effective steps to reduce their power were only taken in thelate 1940s. These culminated in a ruling by the U.S. Justice Department in1948 that ultimately forced the majors to sell off their theaters by the late1950s. But by then the movement of the population to the suburbs hadalready redu ced the value of man y of the stud ios dow ntow n theaters (Mast,1992: 277). This dec lining control over distribution increased the bu rde n onthe studios to produce only those films that would have the best chanceof being distributed—a great challenge in the more discriminating market(Whitney, 1982).

In the face of their reduc ed outp ut, the stud ios began gradually to aban-don the practice of signing stars to exclus ive co ntrac ts, and in fact dra sticallycut back on the nu m ber of stars during the late 1950s. These red uctio ns gavestudios less control over a key production factor. Moreover, given the morerapidly changing customer tastes, stars tended to have shorter productivelives, while at the same time, stars indepe nden ce from studio contracts bidup their value more quickly (Kindem 1982).

To recap, the era from 1936 to 1950 was one of much stability, but 1951to 1965 witness ed a far mo re uncerta in (that is, changing an d unpre dictable)

environment. We terminated our period of analysis in 1965, as after thatconglomerates began to buy u p m any of the stud ios. These purc hase s in largepart occurred because so many studios had fallen in value, and some wereapproaching bankruptcy. Also, by the late 1960s the studio system was re-placed by one dominated by independent producers and directors (Bohn etal., 1978).

In order to confirm these differences in uncertainty between the twoperiods, we assessed year-to-year industry stability in revenues, marketshares, and profits: this volatility was refiected by the correlation between

a firm s results in year t and its resu lts in year f - 1 for each of the e ras. Forthe first era, the interyear correlation coefficients for revenues, market shareand profits were 97 97 and 80; for the second era the numbers were 78

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 13/26

1996 iller and Shawsie 531

indicator of industry uncertainty, turnover in studio production heads, was40 percent higher in the second than in the first era (p < .01). In part thiswas bec ause of more frequent fiops at the box office and b ecau se of the morepressing need to introduce new kinds of films.

Although industry concentration ratios remained about the same forboth periods, the two eras differed greatly in uncertainty. This differencewas du e to declining dem and, w hich resulted in greater rivalry for audien ces,more fickle and rapidly changing customer tastes, increased emphasis onfewer, larger, and more risky film projects, and a loss of control over factorinputs and distribution. These qualitative contrasts seemed to be mirroredby our quan titative ind icators. Of course, becau se indu stry env ironm ents areso mu ltifaceted, our two eras no doubt also vary in aspects other than uncer-tainty.

Variables

Discrete property based resources. In the film indu stry, long-term con-tracts for stars represented a key discrete property-based resource (Kindem,1982). Each studio tried to develop its ow n pool of poten tial stars from am ongindividuals who were recruited early in their careers at relatively low costs.Even during the peak years of moviegoing, fewer than a hundred contractscon trolled stars who a cco unte d for the lion s sha re of box office r eve nues.Studios thus competed with each other to obtain exclusive long-term (typi-

cally, seven-year) contracts with such stars (Shipman, 1979). Often, starswere signed simply to prevent other studios from being able to benefit fromtheir talents. If rival studios wanted to borrow a star, they would have topay a substantial price and sometimes even split profits with the studio thatheld the star s contract. Stars who thre atene d to break a contract w ouldusually be punished by being given poor roles or by banishment from theindustry (Huettig, 1985: 253).

We obtained data on the number of long-term contracts with stars thatwere held by each studio or its producers for each of the years studied. Thesources of these data were two volum es by Shipm an (1972,1979) containingbiographical profiles of all the stars who had appeared in any significantfilms in either leading or supp orting roles. These biographies w ere all codedindividually to link the relevant stars to all the major studios for every yearof the study. All contracts for stars that ran for four or more years duringthe period between 1936 and 1965 were included in the data.

Systemic property based resources. Some might argue that studio plantand equipment represent valuable discrete resources. But resource-basedtheorists would maintain that these assets are imitable and purchasable andthus cannot confer any true competitive advantage (Conner, 1991). Everyone of the major studios e ither own ed or leased pro duc tion lots, prop s, sets,and camera equipment (Huettig, 1985). In fact, some of these studios even

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 14/26

532 Academy of Mana gement Journal June

Theaters controlled by each studio, in contrast, did represent a systemicproperty-based resource. Well-situated theaters that were either owned orleased long-term by the studios afforded control over valuable distributionoutlets. Indeed, theaters owned by the studios were almost all situated in

prime locations: collectively, the studios owned over 70 percent of the the-aters located in cities of over 100,000 people (Whitney, 1982: 166). Inferiorlocations in rural communities were left to the independent cinemas. Also,studios tend ed each to concen trate their theaters in different cities from oneanother to reduce direct competition. More important, a network of theatersprovided studios with an extensive and compliant showcase for films anddenied com petitors equal access to films and custom ers (Conant, 1960). Theclose integration of a studio and its theaters e nsure d that a firm's own cinem aswere given a steady supply of top-ranking films while independents were

left w ith sec ond-run mo vies. A network of theaters also gave studios reliableoutlets for all of the films they produ ced . In add ition, studio-ow ned theatersbenefited from paren t support of advertising, prom otion, and adm inistration,and economies of operation were effected by allocating costs across a largenetwork of cinemas. Even popcorn purchases were centralized. The resultwas that theaters controlled by the studios averaged annual revenues thatwere 15 times those of the independents (Balio, 1985: 255). Theaters, then,were made more valuable through their integration into a network and theirassociation with studios. Such systemic asset specificity and the control ofkey locations made theaters an especially hard-to-copy resource (BlackBoal, 1994).

We obtained information on the number of domestic theaters owned orunder long-term lease for each studio for each year from figures provided inMoody s Industrial Manuals.

Discrete knowledge based resources. In the film industry, the discreteknowledge-based resources of each studio lie in the creative and technicalskills that it has been able to build up. Each studio tried to develop uniqueabilities in various areas of film production that it could use to differentiateits films from those produ ced by its com petitors (Mast, 1992: 230 -231 ). The se

diverse skills include d expertise in script developm ent, set design, direction,camera w ork, sound, an d editing. Studios created large pools of skilled indi-viduals that they could draw upon to work on the many films that theypro du ced each year. MGM, the largest studio , developed a workforce of 6,000skilled employees distributed among 27 departments (Balio, 1985: 264).

Many studios tried to develop reputations aro und the ir various tec hnicalskills in order to attract more talent. The level of these skills is in partrefiected by the number of Academy Awards that a studio won each year.The majority of such skills were in creative and technical categories such

as screenplay, cinematography, editing, costumes, set design, and sound.Although these awa rds were given to individ uals of exceptional ability, theyalso refiected a studio's success in recruiting developing and supporting

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 15/26

1996 iller and Shamsie 533

listing of Acad em y A wa rds pu blished by M ichael (1968). It might be arguedthat Academy Awards also represent an outcome measure of performance:but for the purposes of this study we used awards to infer the existence oftalent that might later enhance financial returns.

Systemic kn owledge based resources. Although studios could try tobuild discrete abilities, they also needed to integrate these by developingcoordinative team skills (Balio, 1985). This was especially true in the secondera, w he n studios h ad to assemble large groups of tempo rary em ployees wh ohad little experience working together to collaborate on each complex, big-budget project. Such large, long-term projects with huge casts and crewsoperating on elaborate sets required studios to learn a great deal about howto get people to work together effectively. Studios with a history of suchlarge projects were most apt to learn the coordinative and integrative skills

need ed for success (Staiger, 1985: 30 0-33 6; Stua rt, 1982: 294; Robins, 1993).This process was a prime example of learning by doing.Team, coordinative, or integrative ability therefore may be reflected,

albeit imperfectly, by a studio s former inve stme nts in com plex, large-scalefilm projects. Large projects develop coordinative skills because they requirethe management of many talents and resources from many specialties overlong periods of time (Stuart, 1982: 295 -296 ). A history of having w orked onsuch major films promotes new learning about project management; it alsocreates team synergies that can be used to good effect in subsequent projects(Robins, 1993).

The scale and complexity of past projects is reflected in the last twoyears average.prod uction costs per film (Huettig, 1985: 306). We obtained thisdata on film costs and p rod uce rs fees from the ann ual financial statem ents ofeach s tudio. We averaged p rodu ction costs for the films that had bee n releasedby the studio over the previous two years to reflect the recent history ofexpenditures.

Trends in demand. The an nua l level of dema nd is a key index of industryhea lth that can infiuence pe rformance. Therefore, all of our analyses inclu deda control variable that measured the percentage of household recreational

spending devoted to movie attendance. These data were obtained from theU.S. Department of Commerce, Social and Economic Statistics Administra-tion (Steinberg, 1980).

Performance indexes. There are many alternative indexes of economicreturns—return on assets, return on sales, operating profits, market share,and even total revenues. For purposes of this study, we decided to look ata variety of financial performance indexes in order to establish the rangeand robustness of our findings.

We cou ld not use retvu-n on asset me asu res becau se of differences in theasset reporting and composition of the film companies. Some studios werediversified and did not segregate assets from nonfilm businesses in theirfinancial reports; United Artists did not own any production facilities. We

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 16/26

534 Academy of Man agement Journal June

theater operations. We did not measure operating profits with theaters asthis would have artificially penalized and rendered noncomparahle the stu-dios that did not own any theaters. Finally, we inclu ded the dom estic ma rketshare figures for each of the studios. In every instance, we were concernedonly w ith the reven ues and profits from a studio s film business.

Data on reven ues a nd profits for each studio w ere ohta ined firom Moody sIndustrial Manual and from company financial reports. For studios thatowned theaters, separate revenue and profit figures were obtained for theprod uction and distribution of films and for the o peration of theaters. Reve-nues and profits were also adjusted for any television business reported.Annual market share data for each studio were derived from its revenues asa percentage of total box office receipts for the year. This information wasobtained from the U.S. De partment of Com merce, Social and E conom ics a nd

Statistics Administration, n lyses

The data consisted of 30 years of observations across seven studios.Separate analyses were conducted for the predictable (through 1950) anduncertain (1951 onwards) periods. Each of the two periods consisted of 14years, after one year per era was lost as a result of the lagging and averagingof variables. Given the longitudinal nature of our study, it was necessary totransform our data to avoid any problems of autocorrelation and hetero-scedasticity. To do this transformation, we used pooled time series cross-sectional analyses (Kmenta, 1986: 616 -62 5). This proced ure first adjusts thedata for autocorrelation using the Prais-Winsten (1954) iterative transforma-tion. To establish the adequ acy of a first-order autocorrelation adjustment,we inspected the correlograms for the analyses. These declined rapidly athigher lags, confirming both the stationarity of the time series process andthe adeq uacy of a first-order correction. Sep arate autocorrelation adjustmentswere done for each firm.

A second transformation of the data was then employed to correct forheteroscedasticity. We divided the dependent and independent variablesby the firm-specific error variances obtained from the regressions on theautocorrelation-corrected data. The twice-transformed data could then bepooled and analyzed using ordinary-least-squares regression analysis (cf.Judge et al., 1988: Section 11.5; Sayrs, 1989).

To avoid specification error in the models, all of the analyses incorpo-rated measures of performance in the prior [t 1) period. Because of theinclusio n of this lagged dep en den t variable, we employ ed Du rbin s H testto ensu re an abse nce of bias in the estim ates of the re sidu als (Judge et al., 1988:401). Plots of residu als w ere inspec ted to confirm the absence of patterns due

to heteroscedasticity or autocorrelation (Sayrs, 1989). We also ascertainedthat multicollinearity w as not a problem in our analyses using the diagnosticsof Belsley Kuh and Welsch (1980) Finally to establish that the results were

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 17/26

1996 Miller and Shamsie 535

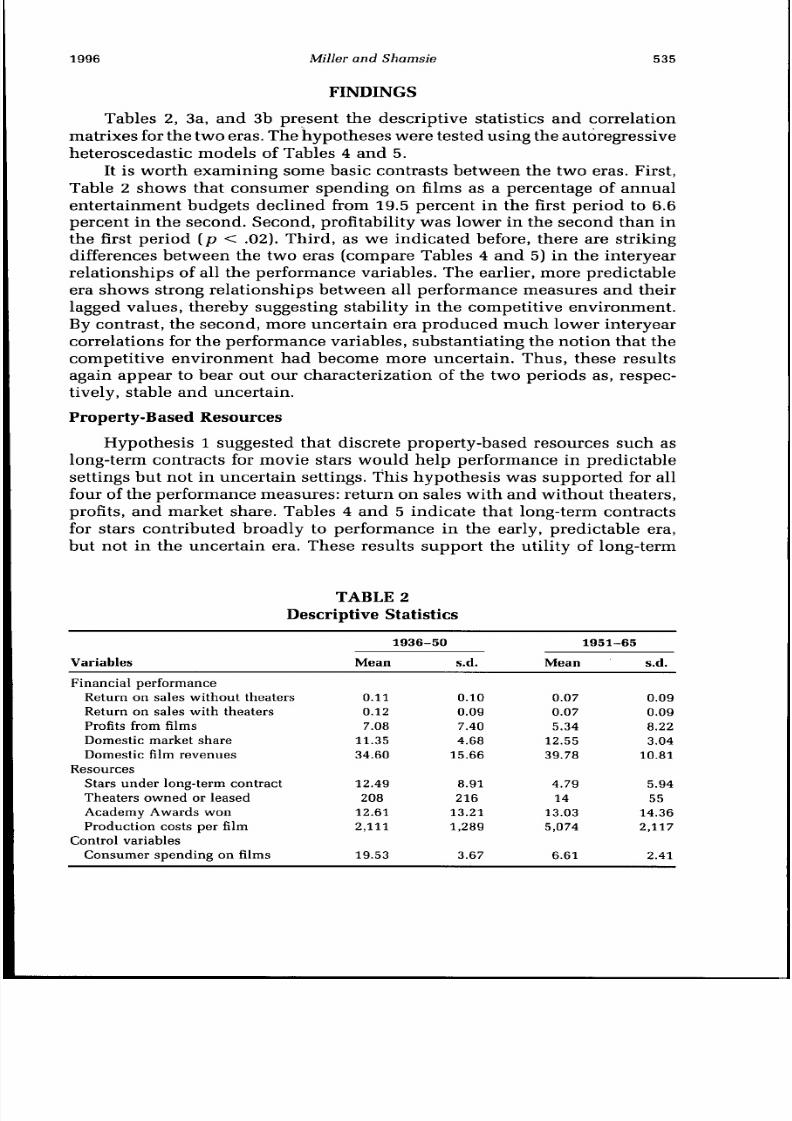

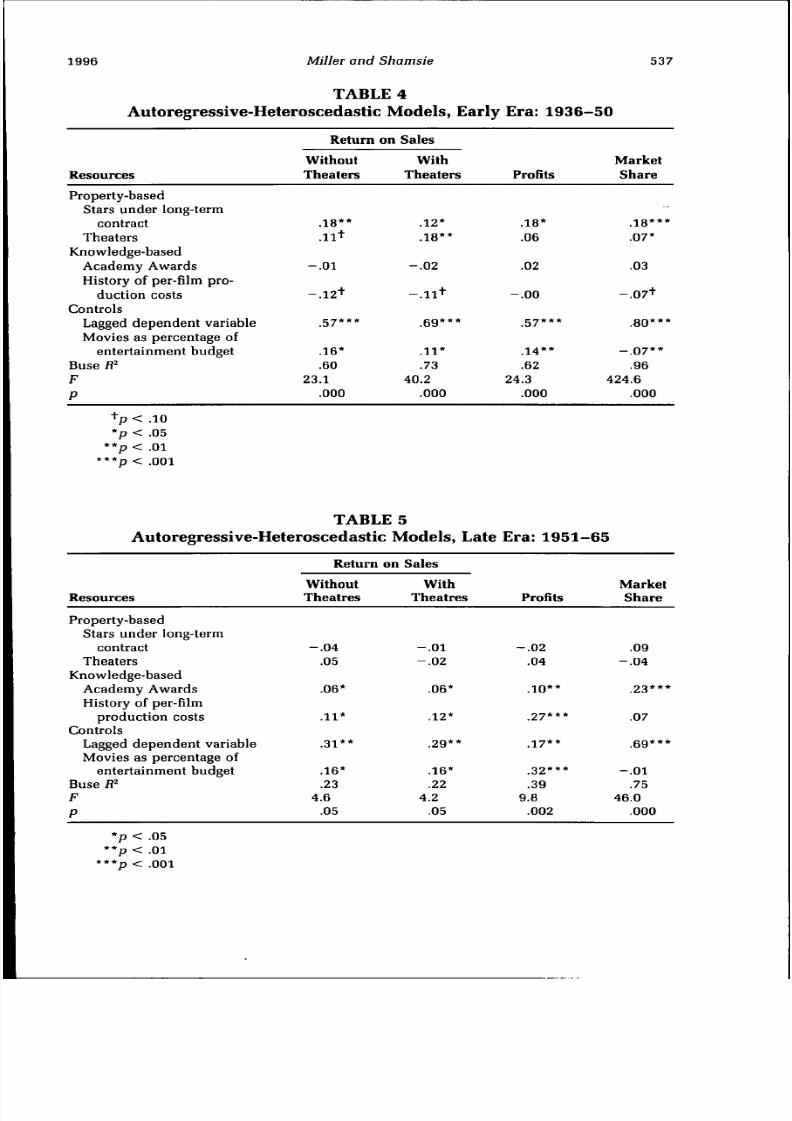

FINDINGS

Tables 2, 3a, and 3b present the descriptive statistics and correlationm atrixes for the two eras. The hyp othese s were tested using the autoregressive

heteroscedastic models of Tables 4 and 5.It is worth examining some basic contrasts between the two eras. First,Table 2 shows that consumer spending on films as a percentage of annualentertainment budgets declined from 19.5 percent in the first period to 6.6percent in the second. Second, profitability was lower in the second than inthe first period [p .02). Third, as we indicated before, there are strikingdifferences be twe en the two eras compare Tables 4 and 5) in the interyearrelationships of all the performance variables. The earlier, more predictableera shows strong relationships between all performance measures and theirlagged values, thereby suggesting stability in the competitive environment.By contrast, the second, more uncertain era produced much lower interyearcorrelations for the performanc e variables, substantiating th e notion that th ecompetitive environment had become more uncertain. Thus, these resultsagain appear to bear out our characterization of the two periods as, respec-tively, stable and uncertain.

Property Based Resources

Hypothesis 1 suggested that discrete property-based resources such aslong-term contracts for movie stars would help performance in predictable

settings but not in uncertain settings. This hypothesis was supported for allfour of the performance m easure s: return on sales with and w ithou t theaters ,profits, and market share. Tables 4 and 5 indicate that long-term contractsfor stars contributed broadly to performance in the early, predictable era,but not in the uncertain era. These results support the utility of long-term

TABLE 2Descriptive Statistics

Variables

Financial performanceReturn on sales without theatersReturn on sales with theatersProfits from filmsDomestic market shareDomestic film revenues

ResourcesStars under long-term contract

Theaters owned or leasedAcademy Awards wonProduction costs per film

1936 50Mean

0.110.127.08

11.3534.60

12.49

20812.612,111

s.d.

0.100.097.404.68

15.66

8.91

21613.211,289

1951 65Mean

0.070.075.34

12.5539.78

4.79

1413.035 74

s.d.

0.090.098.223.04

10.81

5.94

5514.362,117

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 18/26

6 cademy of Manag ement Journal

TABLE 3aPearson Correlations Early Era: 19 36 -50

June

Variables

1. ROS without theaters2, ROS with theaters3. Profits4. Revenues5. Mcirket share6. Stars7, Theaters8. Academy Awards9. Costs per film

10 . Consumer spending

1

.94,9 3,4 9,3 7,3 4,2 9,12

- , 0 7,5 0

2

.8 6

.5 5

.3 9

.3 0

.4 5,0 9.0 2,4 2

3

,6 7,5 0,5 3,3 8.2 5,3 1,4 0

4

,7 6,72,5 6,3 6,7 4

- . 1 0

5

.8 5,5 4,4 4,3 4,0 2

6

,2 9,4 0,4 4.0 9

7

,21,41,0 2

8

.2 2,0 5

9

- . 3 8

TABLE 3bPearson Correlations Late Era: 19 51 -65

Variables

1, ROS without theaters2, ROS with theaters3, Profits4, Revenues5. Market share6, Stars7, Theaters8, Academy Awards9, Costs per film

10, Consumer spending

1

,9 9,94,1 8,0 8,02,0 9,0 5,0 7,1 8

2

,94,1 7,0 8,0 0,0 3,0 4,0 7,1 6

3

,3 3,22,0 6,0 8,1 0,0 3,2 0

4

,8 7,5 9,2 7,2 5,0 9,3 7

5

,4 0,1 7,2 9,3 1

- , 0 5

6

,5 5,1 0

- , 25,5 0

7

.11- . 0 6

.28

8

,0 6,0 2

9

- . 6 4

contracts during an era when studios aggressively managed stars careersand thoroughly exploited their popularity hy casting them in two or threefilms per year. By contrast, during the uncertain era, long-term contractswith stars hecam e m ore risky in p art hecause of the increasingly fickle tasteof moviegoers.

As we noted, hy the late 1950s, studios hegan to ahandon the system olong-term contracts. Because of this change, our analyses of the seconduncertain era may have heen biased—but mainly in the years after 1958w hen the num ber of stars un de r contract bad begun to decline p recipitou slyTo assess this bias, we reran the analyses whose results are shown in Table5 using only the years 19 51 -5 8. The earlier results were replicated: stars dinot relate to any index of performance in the uncertain era.

According to Hypothesis 2, systemic property-hased resources, such acontrol over theaters, and thus over film distribution, would also contribte to financial performance again in predictable b t not in ncertain con

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 19/26

1996 Miller and Shamsie

TABLE 4Autoregressive-Heteroscedastic M odels, Early Era: 1 93 6-5 0

7

Resources

Property-basedStars under long-term

contractTheaters

Knowledge-basedAcademy AwardsHistory of per-film pro-

duction costsControls

Lagged dependent variableMovies as percentage of

entertainment budgetBuse R^

P

Return on

WithoutTheaters

.18

.11+

- . 0 1

- . 1 2 +

.57

.16

.6 023.1

.000

Sales

WithTheaters

.12

.18

- . 0 2

- . 1 1 +

.69

.11

.7 340.2

.000

Profits

.18

.06

.02

- . 0 0

.57

.14

.6 224.3

.000

MarketShare

.18

.07

.0 3

- . 0 7

.80

- . 0 7.9 6

424.6.000

+p < .10 p < .05

p < .01 p < .001

TABLE 5Autoregressive-Heteroscedastic M odels, Late Era: 1951-6 5

Resources

Property-based

Stars under long-termcontractTheaters

Knowledge-basedAcademy AwardsHistory of per-film

production costsControls

Lagged dependent variableMovies as percentage of

entertainment budgetBuse R^

P

Return

WithoutTheatres

- . 04.0 5

.06

.11

.31

.16

.2 34.6

.0 5

on Sales

WithTheatres

- . 0 1- .02

.06

.12

.29

.16

.224.2

.0 5

Profits

- . 02.04

.10

.27

.17

.32

.3 99.8

.002

MarketShare

.0 9- . 04

.23

.0 7

.69

- . 0 1.7 5

46.0.000

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 20/26

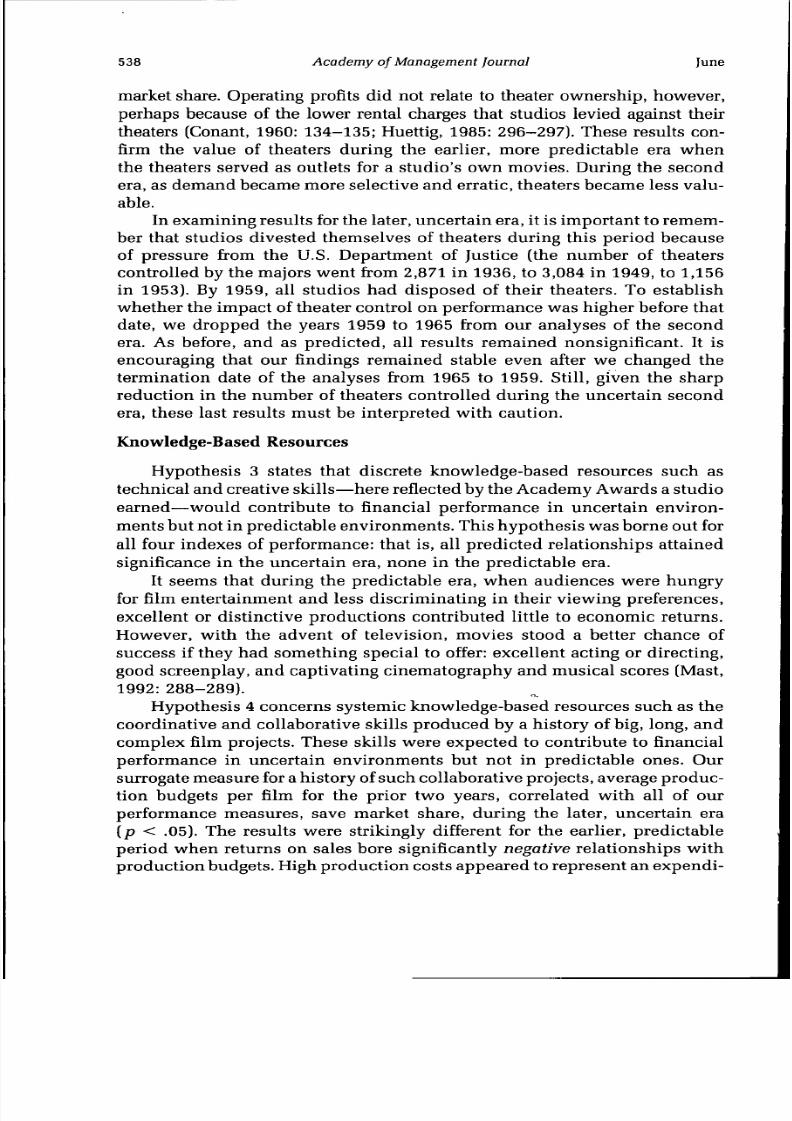

538 cademy of Man agement Journal June

market share. Operating profits did not relate to theater ownership, howeverperhaps because of the lower rental charges that studios levied against theirtheaters (Conant, 1960: 134-135; Huettig, 1985: 296-297). These results confirm the value of theaters during the earlier, more predictable era whenthe theaters served as outlets for a studio s own m ovies. During the secondera, as dem and he cam e more selective and erratic, theaters becam e less valuable.

In examining resu lts for the later, unc ertain era, it is im portan t to remem -her that studios divested themselves of theaters during this period becauseof pressure from the U.S. Department of Justice (the numher of theaterscontrolled by the majors went from 2,871 in 1936, to 3,084 in 1949, to 1,156in 1953). By 1959, all studios had disposed of their theaters. To estahlishwh ethe r the impac t of theater control on performance was higher hefore thatdate, we dropped the years 1959 to 1965 from our analyses of the secondera. As before, and as predicted, all results remained nonsignificant. It isencouraging that our findings remained stable even after we changed thetermination date of the analyses from 1965 to 1959. Still, given the sharpreduction in the number of theaters controlled during the uncertain secondera, these last results must he interpreted with caution.

Knowledge Based Resources

Hypothesis 3 states that discrete knowledge-hased resources such astechnical an d creative skills—he re reflected hy the Academ y Aw ards a studioearned—would contribute to financial performance in uncertain environ-m ents but not in predictable env ironm ents. This hyp othes is was borne out forall four indexes of performance: that is, all predicted relationships attainedsignificance in the uncertain era, none in the predictahle era.

It seems that during the predictable era, when audiences were hungryfor film entertainment and less discriminating in their viewing preferencesexcellent or distinctive productions contributed little to economic returns.

However, with the advent of television, movies stood a better chance ofsuccess if they had something special to offer: excellent acting or directing,good screenplay, and captivating cinematography and musical scores (Mast,1992: 288-289).

Hypothesis 4 concerns systemic knowledge-based resources such as thecoordinative a nd coUahorative skills produ ced hy a history of big, long, andcomplex film projects. These skills were expected to contribute to financialperformance in uncertain environments but not in predictable ones. Oursurrogate measu re for history of such coUahorative projects, average produ c-

tion hudgets per film for the prior two years, correlated with all of ourperformance measures, save market share, during the later, uncertain era

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 21/26

1996 iller and Shamsie 539

ture during this early period that was simply not justified hy the market re-sponse.

In the early period, the majority of films were produced quickly andcheap ly in order to me et a constant and relatively und iscrim inating dem and .Smaller projects did not demand great integrative skills; centralized film-making made coordination easy; and mega-films did not justify their higherexpenses in an easy-to-please market. In the later, more uncertain period,by contrast, films required bigger investments in both development andexecution in order to stand out and do well. These distinctive projectsrequired elahorate an d ex pensive coordinative efforts among a wid e range ofspecialists, many of whom were hired hy the studios only for the dura-tion of the project. Consequently, coordinative skills that were developedthrough recent exp erience w ith higger film projects ten ded to yield superiorreturns.

D I S C U S S I O N NfD C O N C L U S I O N

For the past two decades, the field of management strategy has heenmuch infiuenced by concepts and insights from the literature on economicsand indu strial organization (Rumelt, Sch ende l, Teece, 1991). Indeed ,the resource-based view is itself firmly rooted in economic notions ofmarket power and competition (Conner, 1991). Unfortunately, there remainsmuch to be done to test empirically the relevance of some economic

notions for firm performance, and this is true as well of the resource-based view. Although there are long lists of candidates for valuahleresources, there have been very few efforts to establish systematically if,when, and how these resources influence financial performance. Perhapsmore important, the literature contains many generalizations about themerits of some resources, conjectures that often fail to consider the contexts

within which these resources might he of value to an organization. Thus,after years of interesting conceptual work, we are still at an early stagein knowing what constitutes a valuahle resource, why, and when (AmitSchoemaker, 1993).

This article endeavors to make some progress in those directions. Itshows that hoth property- and knowledge-based resources that are hard tohuy or imitate contrihuted to performance: to returns on sales, operatingprofits, and market share. However, the environmental context was all-important in conditioning these relationships. Periods of stahility and pre-dictahility favored firms with property-hased resources hut did not rewardthose with knowledge-based resources. Precisely the opposite was true forperiods of uncertainty, even though the sample of firms was identical. Itfollows, then, that whether or not an asset can he considered a resourcewill depend as much on the context enveloping an organization as on theproperties of the asset itself It is misleading to attempt to define resources

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 22/26

540 cademy of Mana gement Journal June

This study also shows that property-based resources may quickly losetheir value when an industry changes (Barney, 1986; Geroski Vlassopou-lous, 1991). Static resources tha t are used for control usua lly d em and institutional or legal protection that is beyond the influence of a firm. Once thisprotection lapses, or as soon as the environment changes to devalue theresources, all competitive advantage is lost. This liability may not accrue tothe same degree to the more adaptable knowledge-based resources.

An auxiliary object of this research was to show how one might opera-tionally define and measure various potentially valuable resources. It is, itseems, possible to identify key resources for a particular industry and thenderive quantitative indicators that reflect, with greater or lesser accuracy, afirm s we alth in such resource s. Doing so is not a sim ple task, h ow ever.Considerable ingenuity no doubt will be required of subsequent researchersif they are to avoid trivial or tautological indexes, especially in assessingelusive notions such as skills and learning.

This study, however, is just a beginning. And as such, it has its shareof shortcomings. First, it is limited to a single industry: research in otherindus tries w ill be neede d to confirm the generality of its conclus ions. Secondwe have focused on only four kinds of resou rces, albeit ones that have beenshown to be most relevant to the film industry. Further research will beneeded to examine the usefulness of this framework with other types ofresources. Third, there may have been environmental differences between

our two historical eras that have little to do with unpredictability or uncer-tainty yet contribute to otir findings on the differential superiority of ourcategories of resources—in short, there may be alternative explanations forour results. A final limitation is that in historical stud ies su ch as this, m uchuse has to be made of secondary sources and archival records. Use of suchsources leads to problems of data availability. In this analysis, for example,historical reporting of assets was too aggregated to allow us to accuratelymeasure return on assets.

We hope tha t these sh ortcomings will spu r others to initiate more refinedresearch into the resource-based view. And we are indeed pleased that manyof the no tions of that view do seem to be imp ortant to the way organizationsmust craft their strategies to succeed in different environments. Further re-search might investigate whether tailoring resources to industry uncertaintycontributes to superior performance. Do knowledge-based resources have anedge in tiu-bulent industries such as software, semiconductors, and biotech-nology? Are property-based resources more useful in stable sectors such asmining, utilities, and industrial chemicals? And can mergers of companieswith complementarities among both kinds of resources—media and filmproduction companies, for instance—create especially powerful combina

tions?R F R N S

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 23/26

1996 Mj7/er and hamsie 541

Balio, T. (Ed.). 1985. The American film industry. Madison: University of Wisconsin Press.

Barney, J. 1986. Strategic factor m arkets: Expectations, luck an d bu siness strategy. ManagementScience 32: 1231-124 1.

Barney, J. 1991. Firm resources and sustained competitive advan tage. Journal of Managem ent17: 99-120.

Belsley, D., Kuh, E., Welsch, R. 1980. Regression diagnostics. New York: Wiley.

Black J. A., Boal, K. B. 1994. Strategic resources: Traits, configurations and paths to sustainab lecompetitive advantage. Strategic Management Journal 15: 131-148.

Bohn, T., Stromgren, R., Johnson , D. 1978. Light and shadows: A history of motion pictures(2nd ed.). Sherman Oaks, CA: Alfred.

Bord well, D., Staiger, J., Thom pson, K. (Eds.). 1985. Th e classical Hollywood cinema: Filmstyle an d mode of production to 1960. New York: Columbia University Press.

Brumagin, A. L. 1994. A hierarchy of corporate resources. In P. Shrivastava A. Huff (Eds.),

Advanc es in strategic man ageme nt vol. lOA: 81 -11 2. Creen wich, CT: JAI Press.Burns, T., Stalker, G. 1961. The management of innovation. London: Tavistock.

Collis, D. J. 1991. A resource-based analysis of global com petition: Th e case of the bearingsindustry. Strategic Management Journal 12: 49—68.

Conant, M. 1960. Antitrust in the motion picture industry. Berkeley: University of CaliforniaPress.

Conner, K. R. 1991. A historical com parison of resource-based theory and five schools of thoughtwithin industrial economics. Journal of Management 17: 121-154.

Dierickx, I., Cool, K. 1989. Asset stock accu mu lation and the susta inab ility of com petitiveadvantage. Management Science 35: 1504-1513.

Fiol, C. M. 19 91. Managing culture as a com petitive resource. Journal of Management 17:191-211.

Geroski, P., Vlassopoulos, T. 1991. The rise and fall of a marke t leader. Strategic Managem entJournal 12: 467-478 .

Gomery, D. 1991. Mo vie history: A su rvey. Belmont, CA: Wadsworth.

Grant, R. M. 1991. The resource-based theory of competitive advantage: Implications for strategyformulation. California Management Review 33(3): 11 4-13 5.

Hall, R. 1992. The strategic analysis of intangible resources. Strategic Management Journal13: 135-144.

Hall, R. 1993. A framework linking intangible resources and capabilities to sustainable com peti-tive advantage. Strategic Management Journal 14: 607-618 .

Hend erson, R., Cockburn, 1.1994. M easuring competence: Exploring firm-effects n pharmaceu-tical research. Strategic Management Journal 15: 63-8 4.

Huettig, M. D. 1985. Economic control of the motion picture industry. In T. Balio (Ed.), TheAmerican film industry: 285-310. Madison: University of Wisconsin Press.

Itami, H. 1987. Mob ilizing invisible assets. Cambridge, MA: Harvard University Press.

Judge, G., Hill, R,, Griffiths, W ., Lutkepohl, H., Lee, T. 1988. Introduction to the theory andpractice of econom etrics (2nd ed.). New York: Wiley.

Kindem , G. 1982. Hollywoo d's movie star system: A historical overview. In G. Kindem (Ed.),The American movie industry: 79-93 . Carbondale: Southern Illinois University Press.

Kmenta J 1986 Elements of econometrics (2nd ed ) New York: Macm illan

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 24/26

542 cademy of Mana gement Journal June

Lado, A. A., Wilson, M. C. 1994. Human resource systems and sustained competitive advantage: A competency-based perspective. Academ y of Manag ement R eview 19: 699-727 .

Lasky, B. 1989. RKO : The biggest little major of them all. Santa Monica, CA: Roun dtable Pub-lishing.

Lawrence, P., Lorsch, J. 1967. Organization and environment. Boston: Harvard UniversityPress.

Lieberman, M., Montgomery, D. 1988. First-mover advantages. Strategic Management Jour-nal 9: 41- 58.

Lippm an, S. A., Rum elt, R. 1982. Uncertain imitab ility: An analys is of interfirm differencesin efficiency under competition. B ell Journal of Economics 13: 418-4 38.

Mahoney, J. T., Pandian, J. 1992. The resource-based view within the co nversation of strategicmanagement. Strategic Management Journal 13: 363-380.

Mast, G. 1992. A short history of the movies (revised by B. Kawin). New York: Macmillan.

McGrath, R. G., MacMillan, I. C , Venkatraman, S. 1995. Defining and developing c om petence:A strategic process paradigm. Strategic Management Journal 16: 251-275 .

Michael, P. 1968. The Academ y Awards: A pictorial history. New York: Grown.

Miller, D. 1988. Relating Porter's business strategies to environment and structure. Academyof Management Journal 31: 280-309.

Miller, D. 1996. Gonfigurations revisited. Strategic Management Journal in press.

Miller, D., & Friesen, P. H. 1984. Organizations: A quantum view. Englewood Gliffs, NJ:Prentice-Hall.

Mon tgomery, C. A., Wernerfelt, B. 1988. Diversification, Ricardian rents, and Tobin's Q. Band

Journal of Economics 19: 623-632.Nelson, R., Winter, S. 1982. n evolutionary theory of economic change. Cambridge, MA:

Harvard University Press.Peteraf M. 1993. The co rnerstones of competitive advantage: A resource-based view. Strategic

Management Journal 14: 179-192.

Porter, M. E. 1980. Competitive strategy. New York: Free Press.

Porter, M. E. 1985. Competitive advantage. New York: Free Press.

Porter, M. E. 1991. Towards a dyn amic theory of strategy. Strategic Management Journal12: 95-117.

Praha lad, C. K., Hamel, G. 1990. The core com petence of the corpo ration. Harvard BusinessReview 68(3): 79-91 .

Prais, S. J., Winsten, C. 1954. Trend estimators and serial correlation. Cowles CommissionDiscussion Paper 383, Chicago.

Reed, R., & DeFillippi, R. J. 1990. Causal ambiguity, barriers to im itation, and sustainablecompetitive advantage. Academ y of Man agement Review 15: 88-10 2.

Robins, J. A. 1993. Organizations as strategy: Restructuring pro duction in the film industryStrategic Management Journal 14: 103-118.

Robins, J. A., & Wiersema, M. 1995. A resource-based approa ch to the mu ltibusiness firmStrategic Management Journal 16: 277-299.

Rumelt, R. P., Schendel, D., Teece, D. 1991. Strategic management and econom ics. StrategicManagement Journal 12: 5-30.

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 25/26

1996 iller and Shamsie 543

Shipman, D, 1972. The great m ovie stars: The international years. New York St, Ma rtin's Press.

Shipman, D. 1979. The great movie stars: The golden years. New York: St. Martin's Press.

Staiger, J. 1985. The Hollywood mod e of prod uction, 193 0-19 60. In D. Bordw ell, J. Staiger,K. Thompson (Eds.), The classical Hollywood cinema: ilm style and mode of productionto 1960: 309-338. New York: Columbia University Press.

Steinberg, C, 1980. ilm facts. New York: Facts on File.

Stuart, F. 1982. The effects of television on the motion picture industry. In G. Kindem (Ed.),The American movie industry: 257-307. Carbondale: Southern Illinois University Press.

Teece, D,, Pisan o, G., Shu en, A. 1990. Finn capabilities resources and the concept ofstrategy. Working paper. University of California, Berkeley.

Thompson, J D. 1967. Organizations in action. New York: McGraw-Hill.

Wernerfelt, B. 1984. A resource-based view of the firm. Strategic Management Journal 5:171-180.

Wernerfelt, B., Karnani, A. 1987. Gom petitive strategy un der uncertainty. Strategic Manage-ment Journal 8: 187-194.

Whitney, S. N. 1982. Antitrust policies and the motion picture industry. In G. Kindem (Ed.),The American movie industry: 161-204. Garbondale: Southern Illinois University Press.

Winter, S. 1987. Knowledge and competence as strategic assets. In D. Teece (Ed.), The competi-tive challenge: 159-184. Boston: Harvard Business School Press.

Danny Miller is a research professor of bus iness strategy at the Ecole des Hautes E tudesCommercials, University of Montreal, and a visiting scholar at the Graduate Schoolof Business, Golumbia University. His Ph.D. degree is from McGill University. Hisresearch interests are organizational evolution and configuration, strategic trajectories,and organizational simplicity.

Jamal Shamsie is an assistant professor at the Stern School of Business of New YorkUniversity. He holds a Ph.D. degree in business strategy and policy from McGill Univer-sity. His research interests include the impact of timing of market entry, developmentof sustainable ad vantages, and strategic responses of firms to comp etitive uncertainty.

8/10/2019 Resource Based View_3

http://slidepdf.com/reader/full/resource-based-view3 26/26