responsible finance: multiple borrowing and...

TRANSCRIPT

ResponsibleFinance:MultipleBorrowingandClientIndebtednessParulAgarwalandShambhaviSrivastava,IFMRLEAD

TheMicrofinancesectorinIndiahasshownsignificantgrowthoverthepast fewyears.Until 2014, Microfinance Institutions inIndia issued 12.7 million loans worth Rs.1508.61billion1.

Despite such efforts, two-fifths of ruralhouseholdsarestilldependentoninformalcredit2.Giventhedifficultiesintrackingthecash flows and actual debt burden of ahousehold,MFIs,unawareofothersourcesof borrowing, could potentially offerproducts topeoplewhomaybe at the riskofbeingover-indebtedandcoulddefaultinfuture. On the provider side, this can putthe institutional stability and sustainabilityof the industry at serious risk, On theborrower side, easily available loans couldlead to a situation where borrowerscontinuouslystrugglewithrepayment.

TheMurmurs

NationwidegrowthofMFIswasimpactedseverelybytheAndhraPradesh(AP)crisisof20103.WhiledatasuggeststhatMFIsactivitieshaverecoupedafterthe2010crisis,therehavebeenreportsoffreshincidentsofover-indebtednessinregionsofMadhyaPradesh,KarnatakaandUttarPradesh this year.Thesehavebeenassociatedwithpipeline loans(taking loans using their KYC for others and ending up with multiple loans), spending entire or more than therecommendedspendinglimitoftheloanonconsumptionpurposesratherthanincomegeneration4.

Some reports5haveargued that these incidents area causeofworry for theypoint todeeperproblemswithin thesystem.According to Inclusive Finance IndiaReport 2015,while theMFIportfolio grew toRs. 390billion in FY2015from Rs. 240 billion in FY 2014, this growth wasn’t accompanied with concurrent growth in the number of MFIbranches, employees and clients. This couldmean that the infrastructure, employees and clients ofMFIs are beingstretchedbeyondcapacity.Thisrunstheriskofmultipleborrowingbyclients,withoutproperchecksandgovernanceoftheseborrowings.Ontheotherhand,somereportssuchasarecentonebyIFMRCapital6arguesthatnewreportsof over-indebtedness are sporadic events and detailed analysis of data from credit bureaus does not indicateoverheatingofthesystem.

TheEvidence

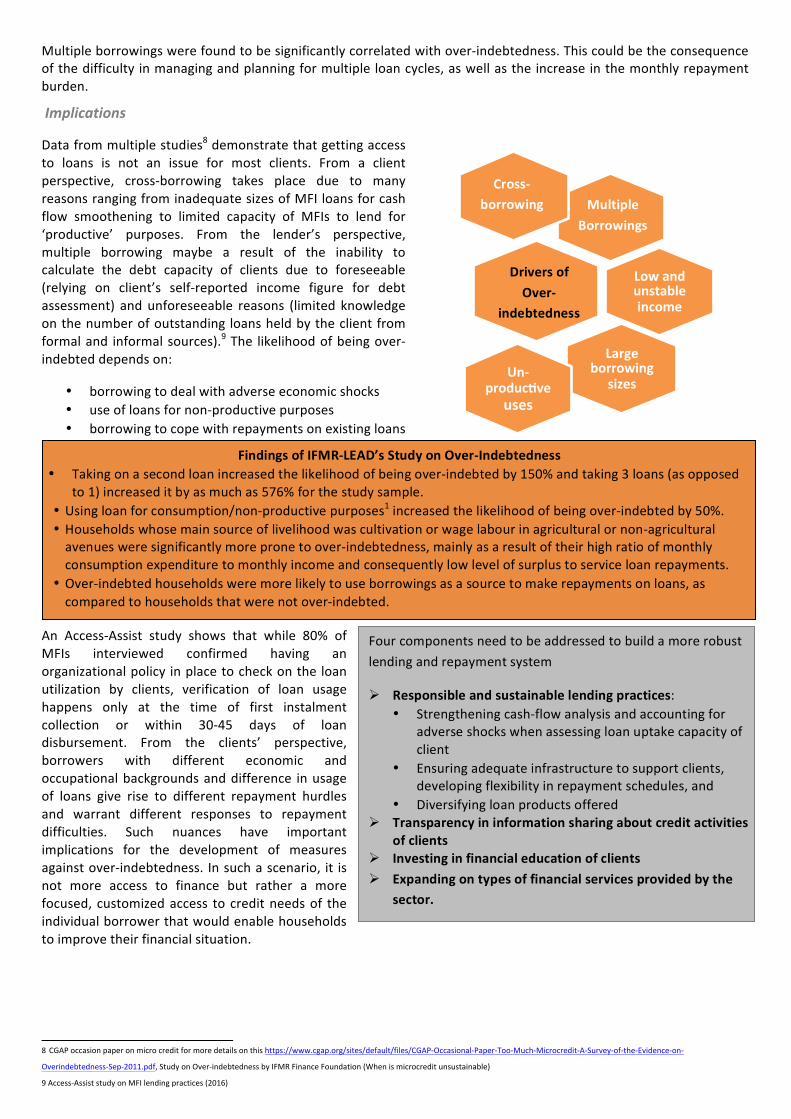

Although present evidence does not permit a conclusion about the actual prevalence of over-indebtedness in themarket,arecentstudy7carriedoutonover-indebtednessinfewsaturatedmarketareasofthreestates(UP,MPandKarnataka), identifies a series of factors (see chart) that pre-disposed MFI borrowers to be more likely to reachunsustainablelevelsofdebt.1AccessDevelopmentServices,‘Stateofthesectorreport’,2014http://www.accessdev.org/downloads/SOS_Report_2014.pdf

2PersistenceofInformalCreditinRuralIndia:Evidencefrom‘All-IndiaDebtandInvestmentSurvey’andBeyond.https://www.rbi.org.in/scripts/publicationsview.aspx?id=14986

3Backin2010,AndhraPradeshwashighlypenetratedbybothMFIsandSHGsgivingrisetomultipleborrowing.Someofthecausesidentifiedformultipleborrowingsincludeclientspoachingandloanpushingonthe

MFIsside,andloanrecyclingontheclients’side.ACGAP(ConsultativeGrouptoAssistthePoor)studyindicatedthattheaveragehouseholddebtinAPwasRs.65,000comparedtothenationalaverageofRs.7,700.

AndhraPradeshwitnessedaseriesofsuicideepisodes,whichwereattributedtotheallegedabusivepracticesofMFIssuchascharginghighinterestrates,adoptingcoercivecollectionpracticesetc.

4Accessdevelopmentservices,‘Stateofthesectorreport’,2015.http://indiamicrofinance.com/wp-content/uploads/2015/09/inclusive-finance-report-2015.pdf

5http://www.livemint.com/Opinion/Gn7z2lGvfvwgoyjxByRHpO/Murmurs-of-a-fresh-crisis-in-the-microfinance-sector.html

6http://www.ifmr.co.in/blog/2016/01/22/microfinance-through-a-data-lens/

7StudyontheDriversofOver-IndebtednessofMicrofinanceBorrowersinIndia:AnIn-depthInvestigationofSaturatedArea(IFMR-LEAD2016)

Fourcomponentsneedtobeaddressedtobuildamorerobustlendingandrepaymentsystem

Ø Responsibleandsustainablelendingpractices:• Strengtheningcash-flowanalysisandaccountingfor

adverseshockswhenassessingloanuptakecapacityofclient

• Ensuringadequateinfrastructuretosupportclients,developingflexibilityinrepaymentschedules,and

• DiversifyingloanproductsofferedØ Transparencyininformationsharingaboutcreditactivities

ofclientsØ InvestinginfinancialeducationofclientsØ Expandingontypesoffinancialservicesprovidedbythe

sector.

FindingsofIFMR-LEAD’sStudyonOver-Indebtedness• Takingonasecondloanincreasedthelikelihoodofbeingover-indebtedby150%andtaking3loans(asopposed

to1)increaseditbyasmuchas576%forthestudysample.• Usingloanforconsumption/non-productivepurposes1increasedthelikelihoodofbeingover-indebtedby50%.• Householdswhosemainsourceoflivelihoodwascultivationorwagelabourinagriculturalornon-agriculturalavenuesweresignificantlymorepronetoover-indebtedness,mainlyasaresultoftheirhighratioofmonthlyconsumptionexpendituretomonthlyincomeandconsequentlylowlevelofsurplustoserviceloanrepayments.

• Over-indebtedhouseholdsweremorelikelytouseborrowingsasasourcetomakerepaymentsonloans,ascomparedtohouseholdsthatwerenotover-indebted.

Lowandunstableincome

Largeborrowing

sizesUn-

producHveuses

Multipleborrowingswerefoundtobesignificantlycorrelatedwithover-indebtedness.Thiscouldbetheconsequenceofthedifficultyinmanagingandplanningformultipleloancycles,aswellastheincreaseinthemonthlyrepaymentburden.

Implications

Datafrommultiplestudies8demonstratethatgettingaccessto loans is not an issue for most clients. From a clientperspective, cross-borrowing takes place due to manyreasonsrangingfrominadequatesizesofMFIloansforcashflow smoothening to limited capacity of MFIs to lend for‘productive’ purposes. From the lender’s perspective,multiple borrowing maybe a result of the inability tocalculate the debt capacity of clients due to foreseeable(relying on client’s self-reported income figure for debtassessment) andunforeseeable reasons (limited knowledgeonthenumberofoutstanding loansheldbytheclientfromformaland informalsources).9The likelihoodofbeingover-indebteddependson:

• borrowingtodealwithadverseeconomicshocks• useofloansfornon-productivepurposes• borrowingtocopewithrepaymentsonexistingloans

An Access-Assist study shows that while 80% ofMFIs interviewed confirmed having anorganizationalpolicy inplacetocheckontheloanutilization by clients, verification of loan usagehappens only at the time of first instalmentcollection or within 30-45 days of loandisbursement. From the clients’ perspective,borrowers with different economic andoccupationalbackgroundsanddifference inusageof loans give rise to different repayment hurdlesand warrant different responses to repaymentdifficulties. Such nuances have importantimplications for the development of measuresagainstover-indebtedness. Insuchascenario, it isnot more access to finance but rather a morefocused, customizedaccess tocreditneedsof theindividualborrowerthatwouldenablehouseholdstoimprovetheirfinancialsituation.

8CGAPoccasionpaperonmicrocreditformoredetailsonthishttps://www.cgap.org/sites/default/files/CGAP-Occasional-Paper-Too-Much-Microcredit-A-Survey-of-the-Evidence-on-

Overindebtedness-Sep-2011.pdf,StudyonOver-indebtednessbyIFMRFinanceFoundation(Whenismicrocreditunsustainable)9Access-AssiststudyonMFIlendingpractices(2016)

Cross-borrowing Multiple

Borrowings

Unproductiveuse

DriversofOver-

indebtedness