restricted appraisal report river crossing - 55.92+ …

TRANSCRIPT

RESTRICTED APPRAISAL REPORT RIVER CROSSING - 55.92+ ACRES OF VACANT LAND

ON GREENWOOD ROAD CHATTANOOGA, HAMILTON COUNTY, TENNESSEE

TENNESSEE STATE BANK FILE#: 11169 BENCHMARK TRUST FILE #: 15-123

As of

JANUARY 12, 2015

Prepared for

TENNESSEE STATE BANK ATTN: JULIE KING

2210 PARKWAY P.O. BOX 1260

PIGEON FORGE, TN 37868

By

FRANCIS B. PEACOCK, MAI STATE CERTIFIED GENERAL REAL ESTATE APPRAISER No. 487 (TN) BENCHMARK TRUST CORPORATION 608 BELL AVENUE CHATTANOOGA, TENNESSEE 37405 TERRENCE J, PEACOCK ASSOCIATE MEMBER OF THE APPRAISAL INSTITUTE STATE REGISTERED TRAINEE APPRAISER STATE OF TN, ID NO: 4267

2

FRANCIS B. PEACOCK, MAI

PRESIDENT MEMBER OF APPRAISAL INSTITUTE STATE-CERTIFIED GENERAL REAL ESTATE APPRAISER (TENNESSEE, GEORGIA) REAL ESTATE APPRAISAL & CONSULTING 608 BELL AVENUE CHATTANOOGA, TN 37405-3308 (423) 266-0755 FAX (423) 266-4985 E-MAIL: [email protected]

BenchMark Trust C O R P O R A T I O N

January 14, 2015

Tennessee State Bank Attn: Julie King P.O. Box 1260 Pigeon Forge, TN 37868 Re: Restricted Appraisal Report Vacant Residential Land 55.92+ Acres off Greenwood Road Chattanooga, Tennessee 37406 To whom it may concern: As requested, we have appraised and inspected the subject tract of vacant land containing approximately 55.92+ acres of gross land area on Greenwood Road in East Chattanooga. This Restricted Appraisal Report of an Appraisal is intended to comply with the requirements from specific guidelines of the Uniform Standards of Professional Appraisal Practice for Restricted Appraisal Reports, effective January 1, 2014. This confidential report is prepared for the sole use and benefit of Tennessee State Bank and is based, in part, upon documents, writings, and information owned and possessed by Tennessee State Bank. This report is provided for informational purposes only to third parties authorized to receive it. The appraiser-client relationship is with Tennessee State Bank as the client. This report should not be used for any purpose other than to understand the information available to Tennessee State Bank concerning this property. Tennessee State Bank assumes no responsibility if this report is used in any other manner.

3

Page 2 January 14, 2015 Your attention is directed to the section entitled “Assumptions and Limiting Conditions” which provides the basis for all conclusions and the final value estimate, including consideration of environmental hazards and compliance with the Americans with Disabilities Act. Subject to the conditions and explanations contained in the following report, it is our opinion that the as is market value of the fee simple interest in the subject property, effective January 12, 2015, was $170,000. The market value estimate is believed to be obtainable within a marketing period of one to two years due to the recent decline in the economy and real estate market. This estimate is based on a combination of direct market evidence, the recent decline in sales of large tracts of residential land, and discussions with real estate brokers, investors, and property owners active in the Hamilton County commercial real estate market. The specified marketing period estimate is predicated on the assumption that the property in question will be diligently marketed to knowledgeable, prospective buyers by equally competent brokers or similar individuals or organizations at no more than the estimated as is market value. In that there have not been any significant changes in the subject market area in the previous one to two year this is also considered a reasonable exposure time. This letter of transmittal precedes the Restricted Appraisal report which further describes the subject property and fully details the reasoning and most pertinent data leading to the final value estimate. Your attention is directed to the “General Assumptions”, “General Limiting Conditions”, and “Certificate of Appraisal”, all of which are considered typical for this type of assignment and have been included within the report. It has been a pleasure to serve you in this manner. Respectfully submitted, BenchMark Trust Corporation Francis B. Peacock, MAI State Certified General Real Estate Appraiser No. 487 (TN) State Certified General Real Estate Appraiser No. 1044 (GA) Terrence J. Peacock State Registered Trainee Appraiser No. 4267 (TN)

4

Subject Property Summary Property: Vacant Residential Land Greenwood Road Chattanooga, Hamilton County, Tennessee Report: Property Rights Appraised: Fee Simple Interest

Value(s) Appraised: As Is USPAP Report Type: Restricted Appraisal Report Client: Tennessee State Bank Client File ID: 11169 Appraiser File Number: 15-123

Appraisal Dates: As Is Effective/Inspection: January 12, 2015

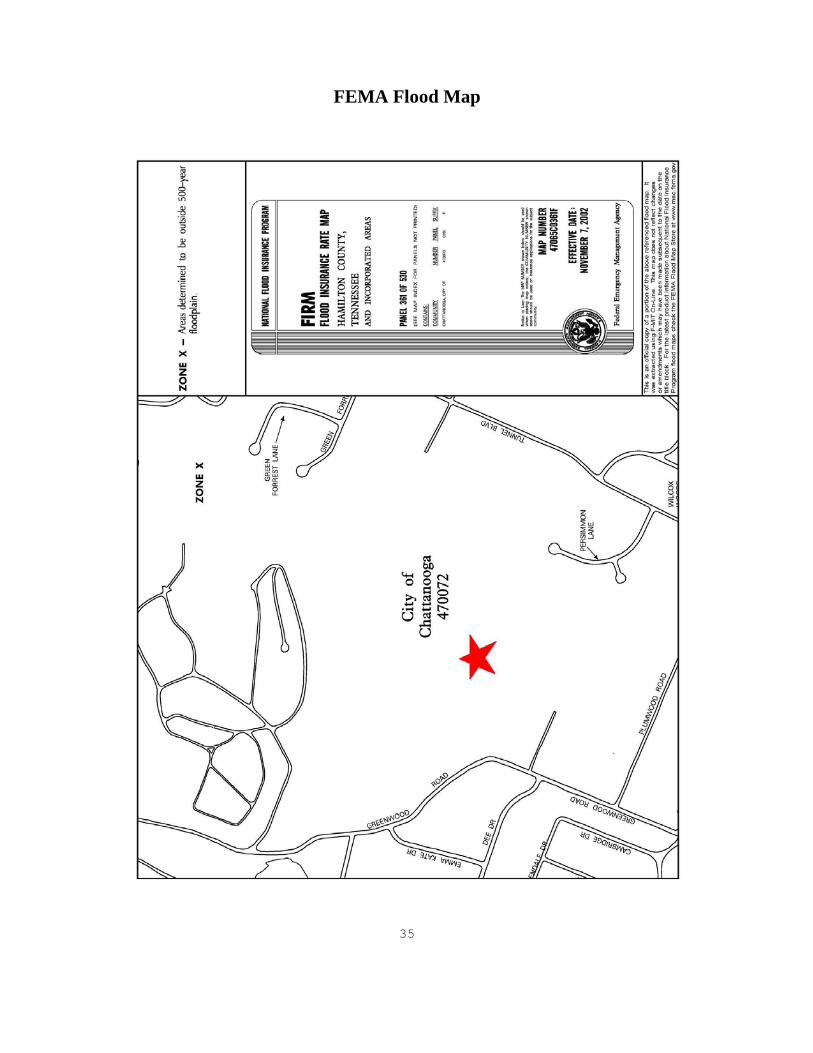

Report: January 14, 2015 Marketing Period: One to two years Site: Tax ID: 137I-E-023 Site Size: 55.92+ Acres of gross land area Zoning: R-1, Residential Zone by the City of Chattanooga Flood Zoning: Zone X – Areas outside the flood hazard area Site Improvements: None Topography: Sloping to steep hillside with over 150 feet in elevation change. Easements/Encroachment: None noted Streets/Access: The subject property consists of a large irregular shaped parcel

with no actual road frontage on Greenwood Road. Upon review and research we have found that in the State of Tennessee, it is required for an owner to be granted an access easement to their property if no direct frontage exists. It is expected that an access easement would be granted by the courts after paying the fair

Highest and Best Use: Because of the current condition of the economy, speculative

holding until residential development is financially feasible or further investigation into selling the property to the adjoining cemetery is considered the highest and best use of the subject site.

5

Current Assessment: The subject is currently appraised for tax purposes at $167,800 which is considered the market value by the Tax Assessors Office. The subject received a greenbelt status in 2013 which lowered the "use value" to $24,500 in 2013. The use value is utilized to determine the taxes while the market value is still considered the tax appraisal. The lower tax appraisal and subsequent city and county taxes is not based on the fair market value of the property but rather the current use as undeveloped forest. If the property were to be developed or sold the subject would most likely lose the greenbelt status and revert to the market value tax appraisal or relevant sales price which would increase the taxes. As of the effective date of this report the subject has an assessed value of $6,125 which is 25% of the greenbelt tax appraisal. City of Chattanooga taxes were $141.43 and Hamilton County taxes were $169.37. Based on the current use a tax appeal is not warranted at this time. The 2014 taxes were not paid as of the effective date of this report and due by February 28, 2015.

As Is Value: Cost Approach Value: N/A Sales Comparison Approach: $170,000 Income Approach Value: N/A Final “As if Completed” Value: $170,000 Use Restrictions: This confidential report is prepared for the sole use and benefit

of Tennessee State Bank and is based, in part, upon documents, writings, and information owned and possessed by Tennessee State Bank. This report is provided for informational purposes only to third parties authorized to receive it. The appraiser-client relationship is with Tennessee State Bank as the client. This report should not be used for any purpose other than to understand the information available to Tennessee State Bank concerning this property. Tennessee State Bank assumes no responsibility if this report is used in any other manner.

Valuation Process: The market value of the subject is being estimated utilizing the

Sales Comparison Approach to Value. Since the date of our last appraisal, there have been few recent sales of vacant land located in the Chattanooga market area which are considered sufficiently similar to the subject for validity in comparison. The sales and have been compared to the subject on the basis gross land area. Write-ups providing the particulars of the land sales are found on the following pages. In that the subject is a tract of vacant land, the income and cost approach are not considered applicable and have not been utilized.

6

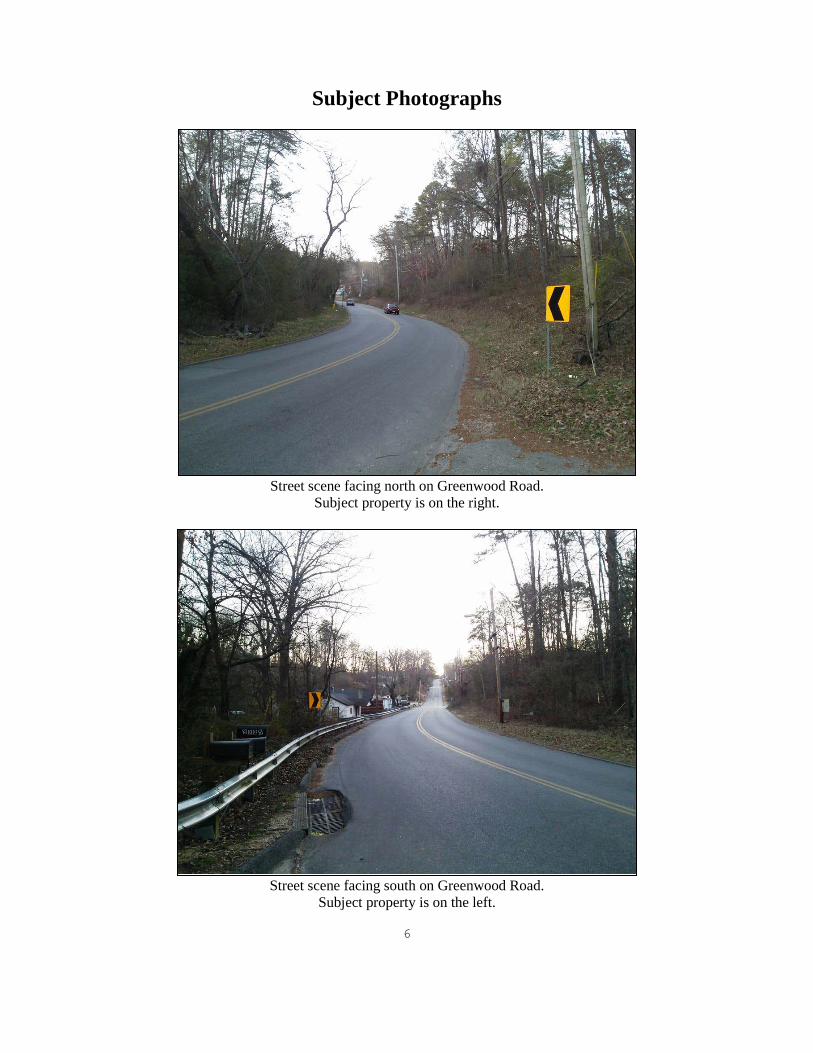

Subject Photographs

Street scene facing north on Greenwood Road.

Subject property is on the right.

Street scene facing south on Greenwood Road.

Subject property is on the left.

7

Interior view of the subject property.

Interior view of the subject property.

8

Geneal Lane, Subject is on the right

9

Sales Comparison Approach

The sales comparison approach is the process of comparing prices paid for properties having a satisfactory degree of similarity to the subject property. The Sales Comparison Approach is based on the “Principle of Substitution: which states that a prudent investor would pay no more to buy or rent a property than the cost to acquire a comparable substitute property. In applying the Sales Comparison Approach, appraisers deal with pertinent units of comparison. In this case the price per acre of gross land area was considered to be the most appropriate unit of comparison. The subject consists of a 55.92+ acre tract of vacant land zoned residential. Review of the most recent legal descriptions and surveys that were previously provided to us by the client during previous appraisals indicate that the subject does not have direct road frontage on Greenwood Road. The subject does appear to have some access on a private drive known as Geneal Lane although a recent survey is not available to confirm this. In the State of Tennessee, if no direct road frontage exists, any land locked parcel will be granted access to their property over an adjoining property. It has been of our experience that courts typically side with the owner of a land locked parcel. The cost to gain access would be the cost of purchasing the land in fee simple or purchasing an easement. In the Sales Comparison Approach we have identified comparable sales which are considered to exhibit a significant degree of similarity to the subject for validity in comparison. Complete write-ups and aerial photographs of the sales are on the following pages.

10

Land Sale 1 Location: Granada Street Chattanooga, Tennessee Grantor: Dart Properties, LLC Grantee: Harris Lee Toney Sale Date: 05/29/14 Sale Price: $4,500 Size: 3.01+ Acres Per Acre Price: $1,495 Topography: Level to Hillside Terms of Sale: Cash to Seller Deed Reference: 10227/133 Tax ID #: 128K-D-009

Zoning: R-1, Residential District The site included no actual road frontage from an existing throughway

similar to the subject. There is a transmission line easement through the subject and the northern portion is located in the 100- and 500-year flood hazard zones. The property was purchased by an adjoining property owner who had purchased the two small lots to he north in 2013.

11

Land Sale 2 Location: 2611 Revington Street Chattanooga, Tennessee Grantor: Elizabeth White, Judi Crowe, Daniel Crowe, Susan Crowe, Blanche

Crowe, George Crowe Jr., Sara Hodge, Joan Crowe, Sarah Barker Grantee: Jacob Altemus and Abigail Roberts Sale Date: 02/29/12 Sale Price: $95,000 Size: 9.90+ Acres Per Acre Price: $9,596 Topography: Steep Hillside Terms of Sale: Cash to Seller Deed Reference: 9590/427 Tax ID #: 137I-B-008 Zoning: R-1, Residential District This site has frontage on both Pearl and Marshall Streets on the side of

Missionary Ridge. The site offers scenic views of the city in the some spots. Both streets were single lane side roads.

12

Land Sale 3

Location: 3611 Parkway Drive Chattanooga, Tennessee Grantor: Fourus Properties, LLC Grantee: TCC Properties, LLC Sale Date: 04/09/12 Sale Price: $225,000 Size: 29.76+ Acres Per Acre Price: $7,560 Topography: Level to Steep Hillside

Terms of Sale: Cash to Seller Deed Reference: 9619/291 Tax ID #: 128J-G-023 Zoning: R-1, Residential Zone This site has access points on Parkway Drive, Ridgecrest Drive, and Bonny

Oaks Drive.

13

Land Sale 4 Location: Woolson Road Chattanooga, Tennessee Grantor: United Methodist Neighborhood Centers, Inc. Grantee: Mt. Everest Properties, LLC Sale Date: 04/08/10 Sale Price: $12,500 Size: 7.20+ Acres Per Acre Price: $1,736 Topography: Level to Steep Hillside Terms of Sale: Cash to Seller Deed Reference: 9147/715 Tax ID #: 137I-D-029

Zoning: R-1, Residential District The site included no actual road frontage from an existing throughway

similar to the subject but there is an easement for the extension of Woodson Avenue if the site were to be developed.

14

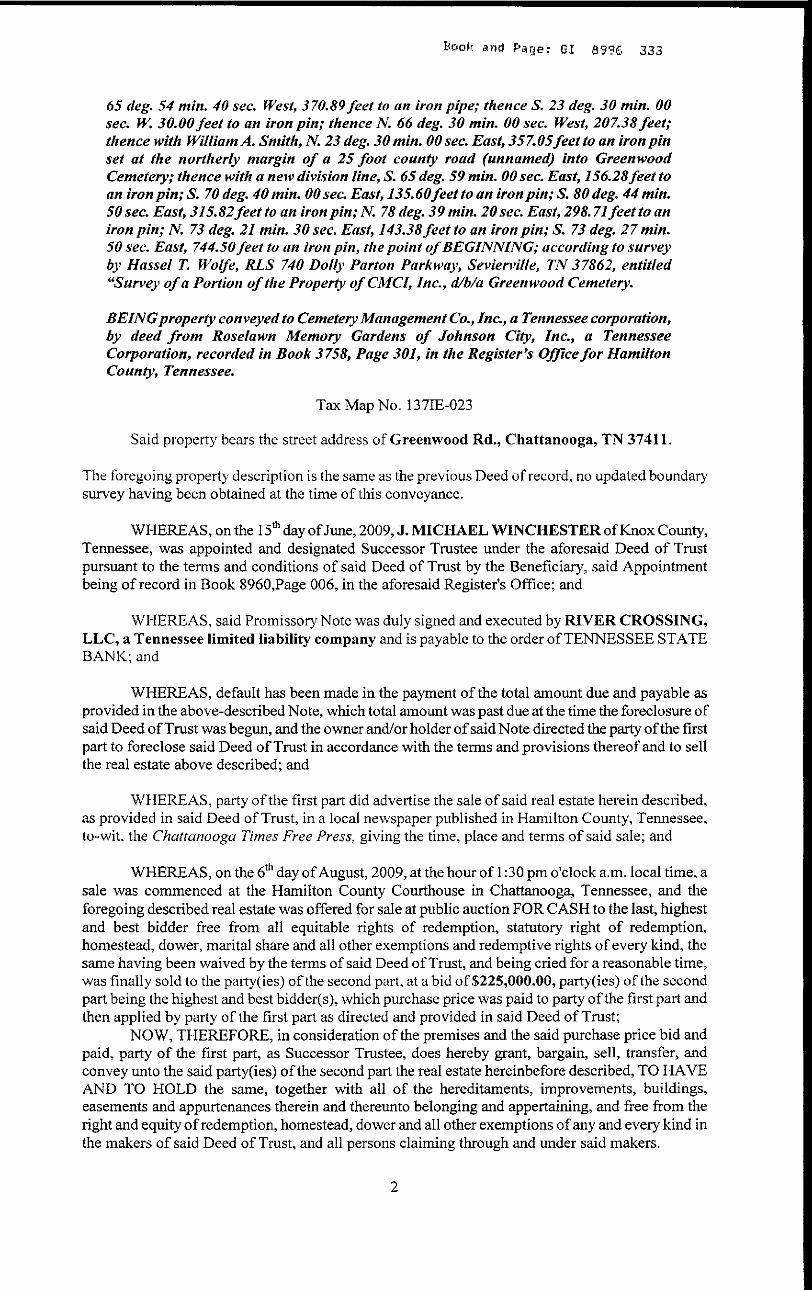

LAND SALES Sale 1 is located north of the subject property with no direct access on Granada Drive. This is a side street within a residential neighborhood. The sale’s topography ranges from level to hillside. The neighborhood overall is mostly lower to middle class income residences. Bordered to the east by a railway, there is a transmission wire easement which bisects the property and limits the development potential. Initially listed for $6,000, the subject was purchased for $1,495 per acre by an adjoining property owner which had purchased the two small lots adjoining north of the subject in 2013. This sale represents the only comparable vacant land sale over 3.00 acres in size in the neighborhood since the last appraisal in January of 2014. Sale 1 is considered to be similar as compared to the subject for location and access while superior for size and topography. The sale is inferior for easements because the site is bisected by a power line which limits the development potential. Additionally the site was purchased by an adjoining land owner which indicates added motivation by the buyer. Overall, a price per acre of gross land area above $1,450 is indicated for the subject property. Sale 2 is located approximately 0.50 miles west of the subject property on Missionary Ridge. Sale 2 has access from two inferior one-lane side streets which provide inferior access as compared to the subject but were located on the side/top of Missionary Ridge which provides good views of the city which is significantly superior as compared to the subject. The sale’s topography ranges from level to steep hillside which is similar to the subject. Sale 2 is superior to the subject in size. Overall, a price per acre below $9,596 is indicated for the subject property. Sale 3 is located north of the subject property with access points on Young Road, Bonny Oaks Drive, and Ridgecrest Drive. Bonny Oaks Drive is a high traffic throughway and is considered superior as compared to the subject for access. The sale’s topography ranges from level to steep hillside. The interior of the site has been primarily graded prior to the sale while the surrounding exterior borders are hillside transitioning into the surrounding neighborhoods. The neighborhood overall is mostly low to middle income residences with commercial developments scattered throughout the area along Bonny Oaks Drive. Sale 3 is considered to be similar as compared to the subject for location and size while significantly superior for access and topography due to the extensive amount of site work completed. Overall, a price per acre of gross land area of less than $7,560 is indicated for the subject property. Sale 4 is located approximately 0.25 miles west of the subject property with access from Woolson Road off N. Crest Road. North Crest Road which runs along the top of Missionary Ridge and includes high end and historical houses with values ranging from several hundred thousand into the millions. Although in close proximity to North Crest Road, Sale 4 is an interior parcel of irregular shape. The immediate areas on either side of Missionary Ridge are primarily low to middle income residences with dated commercial developments. Sale 4 is considered to be in the transitional area which is still not the highly attractive areas on the top Missionary Ridge to the south but better than the less desirable Glenwood area. The sale is located further from an established roadway and supportive access to the site other than a single lane driveway will be more difficult compared to the subject’s location to the roadway. The sale’s topography ranges from level to steep hillside which is similar to the subject. Sale 4 is superior to the subject in size. Overall, a price per acre above $1,736 is indicated for the subject property.

15

DISCUSSIONS The sales comparative approach has been applied as indicated above to estimate the market value of the fee simple interest in the subject property as of January 12, 2015, which is the date of the most recent inspection of the property. The comparative process provided a range of value indications for the subject greater than $1,495/AC and less than $9,596/AC. Sale 1 is a smaller parcel and inhibited by a transmission line easement which bisects the property. Sale 2 is located in close proximity to the subject but on the top rim with a good scenic view of the city. Sale 2 was significantly superior as compared to the subject due to this factor. Sale 3 is a larger site which had been partially graded and located with superior access off Bonny Oaks Drive. Sale 4 is an interior parcel of similar topography and location as the subject property. All of the sales were considered to be reasonable indicators of value for the subject in that all were vacant land sales located in the Chattanooga area which would be expected to appeal to basically the same buyer’s market for development. The subject property is located in a mostly low income residential neighborhood which is in a state of decline. There does not appear to be a demand for new development in the area and the majority of the existing properties are of older design. We have appraised the subject several times since 2009 and are familiar with the surrounding neighborhood and no new development was noted in the area during the previous years and the demand has not increased. Located directly across Greenwood Avenue from the subject is the Greenwood Terrace public housing complex operated by the Chattanooga Housing Authority. This development consists of 98 duplex type units on Dee Drive. Typically public housing developments are a deterrent for new residential development in that communities with a higher amount of renters as opposed to owners typically have a higher crime rate and less of an overall connection to the community. The public housing complex is considered a form of external obsolescence which negatively affects the subject property. Taking this, the subjects’ lack of road frontage, and steep topography, speculative residential development on the site at this time is not considered financially feasible at this time. Obtaining financing for this property would be difficult. Based on these factors, a lower unit value is indicated for the subject property. As can be seen by the above sales, there have been few sales of large tracts of land in the East Chattanooga area and no other current listings of similar style properties in the area. There does not appear to be a demand for vacant land or new development in the subjects’ immediate area. After reviewing the area for the past several years during appraisals of the subject and discussions with the tax assessor's office and real estate agents active in the community, it is of our opinion that the subject will continue to decline into the foreseeable future before any recovery is expected. FINAL VALUE ESTIMATE We have reconciled with a unit value estimate for the subject toward the lower end of the range due to the above discussion. We have estimated a unit value for the subject at $3,000 per acre of gross land area. Applying this unit value estimate to the approximate 55.92+ acres of gross land area included in the subject site indicates a value estimate for the subject, effective January 12, 2015, of $167,760. In that the market tends to deal in round numbers, we have rounded our value estimate to $170,000. In that the subject is a tract of vacant land and sole weight is given to the sales comparison approach, this is also the final reconciled value estimate. This fair market value is considered equal to the fair value of the subject. The appraiser is of the opinion that speculative holding of the subject site until residential development becomes finically feasible is the best option other than placing the property up for auction. New developments in this area are just not in demand at this time. We have appraised the property several times since 2009 and have not noticed any significant developments or changes in property demand in the immediate area since then.

16

USE RESTRICTIONS This confidential report is prepared for the sole use and benefit of Tennessee State Bank and is based, in part, upon documents, writing, and information owned and possessed by Tennessee State Bank. This report is provided for informational purposes only to third parties authorized to receive it. The appraiser-client relationship is with Tennessee State Bank as the client. This report should not be used for any purpose other than to understand the information available to Tennessee State Bank concerning this property. Tennessee State Bank assumes no responsibility if this report is used in any other manner. PROPERTY INTEREST APPRAISED The expressed value estimate considers the as is fee simple interest in the subject property. PURPOSE OF APPRAISAL The purpose of this Appraisal was to estimate the market value of the fee simple interest in the subject property. It is my understanding that this report will be used for internal purposes including but not necessarily limited to providing support for loan underwriting. Additional information regarding the subject property and rational for our reasoning can be found in the appraisers work file. EFFECTIVE DATE The date of the most recent thorough inspection of the subject property is January 12, 2015, which is also the effective date of this report. The report date is January 14, 2015. IDENTIFICATION AND HISTORY OF THE SUBJECT PROPERTY The subject property is identified by Hamilton County as Tax Parcel Folio Number 137I-E-023. Roselawn Memory Gardens of Johnson City, Inc. acquired the subject from James A. O’Hara, Director of Internal Revenue for the District of Nashville, Tennessee in 1975. This sale of the property is recorded in O.R. Book 2295, Page 365 in the Register’s Office of Hamilton County, Tennessee. The property was purchased in conjunction with parcel 137I-E-028 by Cemetery Management Co. Inc. on August 6, 1990 from Roselawn Memory Gardens of Johnson City, Inc. for the reported consideration of $200,000. This sale of the property is recorded in O.R. Book 3758, Page 301 in the Register’s Office of Hamilton County, Tennessee. The subject had gone into default with the bank and auctioned on August 6, 2009 at the Hamilton County Courthouse as where the Tennessee State Bank was the highest bidder at $225,000. There have been no arm’s length transactions involving the subject property in the five years preceding this report. This discussion has been presented for informational purposes only and should in no way be construed to substitute for a valid title search of the property. It is noted that the owner has the subject listed as a bank owned property for sale at $199,000 but no sales sign was noted on the property. After discussions with the listing agent, Paul Foster of Keller Williams Realty, there has been no interest in the property which has been listed for several years. SCOPE OF APPRAISAL The scope of this Restricted Appraisal has been to collect, confirm, and report data. Other general market data and conditions have been considered. Consideration has been given to the zoning of the subject property as well as zoning and surrounding improvements and neighborhood. The work performed for this assignment included: preliminary analysis of the appraisal problem; exterior and interior inspection of the property being appraised; consideration of the highest and best use of the land and property as improved; collection and analysis of comparable sales and listings for estimating the as is market value of the subject, completion of the Sales Comparison Approach as pertinent to the subject property as of the effective date of this report, and preparation of the written Restricted Use report.

17

APPRAISAL PROCEDURE FOLLOWED In that the subject is vacant land and not subject to any land lease, the Cost and Income Approaches to Value were not considered to be applicable to the subject property and have not been included in this assignment. The appraiser believes the only applicable approach to value is the Sales Comparison Approach and this is the approach on which the value estimate has been based. The depth of discussion contained in this report is specific to the needs of the client and for the intended use stated. The appraiser is not responsible for unauthorized use of this report. HIGHEST AND BEST USE Highest and Best use is defined as: “The reasonably probable and legal use of vacant land or an improved property, which is physically possible, appropriately supported, financially feasible, and that results in the highest value. The four criteria the highest and best use must meet are legal permissibility, physical possibility, financial feasibility, and maximum profitability.”1

When analyzing the Highest and Best use, the subject is considered vacant to identify the ideal improvements for the site, taking into consideration possible alternative uses to which the site could be placed under the current land use regulations as well as surrounding trends and developments. Next site is analyzed as improved to compare the existing improvements to the ideal improvements: this comparison concludes whether renovation, expansion, conversion, or demolition may be viable alternatives to bring the existing improvements closer to the ideal improvements. For the highest and best use analysis, the appraiser considers four criteria which are as follows: 1) legal permissibility, 2) physical possibility, 3) financial feasibility, and 4) maximum profitability. The criteria is considered in sequential order because it would be unreasonable to determine the highest and best use of a property which is financially feasible but not legally permissible or physically possible. Again, a separate analysis of each property will be performed and where similarities exist, reference will be made to the appropriate previous analysis to avoid redundancy. The subject is zoned R-1, Residential Zone which legally permits single family homes excluding mobile homes, schools, non-profit buildings and uses, gold courses, publicly owned-buildings such as fire stations, etc. Any of the previously mentioned uses could be legally developed on the subject site. Due to the steep undulation terrain, development would be difficult and would be best suited for one larger homestead or a few individual lots for single family residences. There have been very little recent development in the area and the general consensus of the real estate community and tax assessors is that the subject neighborhood is in decline and conditions will get worse before they start to show signs of improvement which could take years if not decades. The appraiser is of the opinion that speculative holding of the subject site until residential development becomes finically feasible is the best option other than placing the property up for auction. New developments in this area are just not in demand at this time. We have appraised the property several times since 2009 and have not noticed any significant developments or changes in property demand in the immediate area since then. Another option would be to inquire with the adjoining Beautiful Greenwood Cemetery about their need to possibly expand and market the northern portion or whole property for sale to the cemetery. It is noted that the property was previously owned by the cemetery and their need for space for possible expansion is not known at this time and expected to be unlikely. Speculative holding is considered the maximally productive and highest and best use of the subject property as is in that there is no demand in the area for new developments or vacant land in the subject neighborhood. 1 The Dictionary of Real Estate Appraisal, 3rd Edition, Appraisal Institute, Chicago, IL, Page 171

18

ZONING/ TOPOGRAPHY As previously indicated, the subject is zoned R-1, Residential Zone by the City of Chattanooga. The subject could be improved with a wide range of residential or public use developments allowable under the current zoning of the property. Zoning regulations for the R-1 zoning are included in the addendum of this report. As can be seen on the following Hamilton County GIS image, the terrain ranges from sloping to steep hillside with over 150 feet in elevation change. Terrain such as this typically makes development difficult and expensive.

Hamilton County GIS Zoning/Topography Map

19

IMMEDIATE NEIGHBORHOOD INFORMATION The subject property is located on Greenwood Road on the east side and adjacent to the Greenwood Cemetery in East Chattanooga, Hamilton County, Tennessee. The subject neighborhood would be considered the residential area immediately surrounding the subject property. The surrounding developments are mainly low to middle income residences, religious facilities, and the Greenwood Cemetery adjoining the subject property to the north. There is little evidence of recent development the immediate area. Truthfully, this is a depressed area and the general consensus of the real estate community and tax assessors is that the subject neighborhood is in decline and conditions will continue to decline before they start to show signs of improvement which could take years if not decades. Development patterns in the subject neighborhood would be expected to continue along the same residential patterns into the future. All necessary governmental services are provided by the City of Chattanooga and/or Hamilton County. The subject neighborhood would be considered to be in a stable state with little evidence of recent development in the area. The population base of the area is stable and sufficient to support the local businesses located in the surrounding areas but not enough to demand growth at this time. There have been no noticeable changes in the immediate neighborhood in the previous twelve months.

UTILITIES

Water Tennessee American Water Company

Sewer City of Chattanooga

Electric Electric Power Board of Chattanooga

Natural Gas Chattanooga Gas Company

Police Protection City of Chattanooga

Fire Protection City of Chattanooga

20

Definitions

Market Value2

The most probable price which a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently, knowledgeably and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and passing of title from seller to buyer under conditions whereby: Buyer and seller are typically motivated; Both parties are well informed or well advised and each acting in what he considers his own best interest; A reasonable time is allowed for exposure in the open market; Payment is made in terms of cash in US dollars or in terms of financial arrangements comparable thereto; and The price represents the normal consideration for the property sold unaffected by special or creative financing or sales concessions granted by anyone associated with the sale.

Fee Simple Estate3

Absolute ownership unencumbered by any other interest or estate: subject only to the limitations of imposed by the governmental powers of taxation, eminent domain, police powers, and escheat.

“As Is” Market Value As estimate of the market value of a property in the condition observed upon inspection and as it physically and legally exists without hypothetical conditions, assumptions, or qualifications as of the date the appraisal is prepared. Real Property4

All interests, benefits, and rights inherent in the ownership of physical real estate; the bundle of rights with which the ownership of real estate is endowed. In some states, real property is defined by statute and is synonymous with real estate.

Real Estate Physical land and appurtenances attached to the land, e.g., structures. An identified parcel or tract of land, including improvements, if any. Leased Fee Estate An ownership interest held by a landlord with the rights of use and occupancy conveyed by lease to others. The rights of the lessor (the leased fee owner) and the leased fee are specified by contract terms contained within the lease. Extraordinary Assumption5

An assumption, directly related to a specific assignment, which, if found to be false, could alter the appraiser’s opinions or conclusions. Extraordinary assumptions presume as fact otherwise uncertain information about physical, legal, or economic characteristics of the subject property; or about conditions external to the property such as market conditions or trends; or about the integrity of data used in an analysis.

2 Title XI, Financial Institutions Reform, Recovery, and Enforcement Act of 1989(“FIRREA”), [Pub. L. No. 101-73, 103 State. 183 (1989)], 12 U.S.C. 3310,3331-3351, and section 5(b) of the Bank Holding Company Act, 12 U.S.C. 1844(b); Part 225, Subpart G: Appraisals: Paragraph 225.62(f). Uniform Standards of Professional Appraisal Practice, Page 1-7 Federal Reserve System, 12 CFR Parts 208 and 225, Sec. 225.62 Office of the comptroller of the currency, 12 CFR part 34, Sec. 34.42 FDIC, 12 CFR Part 323, Sec .323.2 Office of Thrift Supervision, 12 CFR Part 564, Sec. 564.2 NCUA, 12CFR Part 722, Sec. 722.2 3 The Dictionary of Real Estate Appraisal, 3rd Edition, Appraisal Institute, Chicago, IL, Page 140 4 Ibid., Page 294 5 Ibid., 106-07.

21

Hypothetical Condition6

That which is contrary to what exists but is supposed for the purpose of analysis. Hypothetical conditions assume conditions contrary to known facts about physical, legal, or economic characteristics of the subject property; or about conditions external to the property, such as market conditions or trends; or about the integrity of data used in an analysis. A hypothetical condition may be used in an assignment only if: Use of the hypothetical condition is clearly required for legal purposes, for purposes of reasonable analysis, or for purposes of comparison; Use of the hypothetical condition results in a credible analysis; and the appraiser complies with the disclosure requirements set forth in USPAP for hypothetical conditions.

Marketing Time7

1) The time it takes an interest in real property to sell on the market subsequent to the date of an appraisal. 2) Reasonable marketing time is an estimate of the amount of time it might take to sell an interest in real property at its estimated market value during the period immediately after the effective date of the appraisal; the anticipated time required to expose the property to a pool of prospective purchasers and to allow appropriate time for negotiation, the exercise of due diligence, and the consummation of a sale at a price supportable by concurrent market conditions. Marketing time differs from exposure time, which is always presumed to precede the effective date of the appraisal. (Advisory Opinion 7 of the Appraisal Standards Board of The Appraisal Foundation and Statement on Appraisal Standards No. 6, "Reasonable Exposure Time in Real Property and Personal Property Market Value Opinions" address the determination of reasonable exposure and marketing time.)

Exposure Time8

1) The time a property remains on the market. 2) The estimated length being appraised would have been offered on the market prior to the hypothetical consummation of a sale at market value on the effective date of the appraisal; a retrospective estimate based on an analysis of past events assuming a competitive and open market. Exposure time is always assumed to occur prior to the effective date of the appraisal. The overall concept of reasonable exposure encompasses not only adequate, sufficient and reasonable time but also adequate, sufficient and reasonable effort. Exposure time is different for various types of real estate and value ranges and under various market conditions. (Appraisal Standards Board of The Appraisal Foundation, Statement on Appraisal Standards No. 6, "Reasonable Exposure Time in Real Property and Personal Property Market Value Opinions") Market value estimates imply that an adequate marketing effort and reasonable time for exposure occurred prior to the effective date of the appraisal. In the case of disposition value, the time frame allowed for marketing the property rights is somewhat limited, but the marketing effort is orderly and adequate. With liquidation value, the time frame for marketing the property rights is so severely limited that an adequate marketing program cannot be implemented. (The Report of the Appraisal Institute Special Task Force on Value Definitions qualifies exposure time in terms of the three above-mentioned values.)

6 Ibid., 141. 7 The Dictionary of Real Estate Appraisal, 4rd Edition, Appraisal Institute, Chicago, IL, Page 175 8 The Dictionary of Real Estate Appraisal, 4rd Edition, Appraisal Institute, Chicago, IL, Page 105

22

Assumptions and Conditions General Assumptions: The following appraisal report has been made with the following general assumptions: 1. No responsibility is assumed for legal description or for matters including legal or title

considerations. Title to the property is assumed to be good and marketable unless otherwise stated. 2. The property is appraised free and clear of any or all items or encumbrances unless otherwise

stated. 3. Responsible ownership and competent property management are assumed. 4. The information furnished by others is believed to be reliable. However, no warranty is given for

its accuracy. 5. All engineering is assumed to be correct. The plot plan(s) and illustrative materials in this report

are included only to assist the reader in visualizing the property. 6. The soil and subsoil, unless otherwise detailed, appear firm and solid. No engineering study has

been made and the appraiser is not to be held responsible for any adverse condition that may be found in these matters.

7. It is assumed that there are no hidden or unapparent conditions of the property, subsoil, or

structures that render it more or less valuable. No responsibility is assumed for such conditions or for arranging for engineering studies that may be required to discover them.

8. It is assumed that there is full compliance with all applicable federal, state, and local

environmental regulations and laws unless noncompliance is stated, defined, and considered in this appraisal.

9. It is assumed that all required licenses, certificates of occupancy, consents, or other legislative or

administrative authority from local, state, or national government or private entity or organization have been or can be obtained or renewed for any use on which the value estimate contained in this appraisal is based.

10. It is assumed that the utilization of the land and improvements is within the boundaries or property

lines of the property described and that there is no encroachment or trespass unless noted in the evaluation.

11. To the best of our knowledge, this evaluation conforms to the current requirements prescribed by

the Uniform Standards of Professional Appraisal Practice, of the Appraisal Standards Board, of the Appraisal Foundation and the Appraisal Institute.

12. The subject size is approximately 55.92+ acres of gross land area. Because there have been no

recent surveys of the subject property we have estimated the subject size using the Hamilton County Geographic Information Systems Map. This size estimate is assumed accurate for the purposes of this report and we reserve the right to adjust this report and value it if a new survey or information becomes available.

23

General Limiting Conditions: This appraisal has been made with the following general limiting conditions: 1. The distribution, if any, of the total valuation in this report between land and improvements

applies only under the stated program of utilization. The separate allocations for land and buildings must not be used in conjunction with any other report and are invalid if so used.

2. Possession of this appraisal, or a copy thereof, does not carry with it the right of publication. 3. The appraiser, by reason of this report, is not required to give further consultation, testimony, or

be in attendance in court with reference to the property in question unless arrangements have been previously made.

4. Neither all nor any part of the contents of this appraisal (especially any conclusions as to value, the

identity of the appraiser, or the organizations with which the appraiser is connected) shall be disseminated to the public through advertising, public relations, news, sales, or any other media without prior written consent and approval of the appraiser.

5. We do not have the required expertise for determining the presence of/or absence of hazardous

substances; defined as all hazardous or toxic materials, wastes, pollutants, or contaminants including, but not limited to, asbestos, PCB, UFFI, radon, lead based paints, or other raw materials, chemicals, or gases) used in construction, or otherwise present on the property. We assume no responsibility for the studies or analyses which would be required to determine the presence or absence of such substances. We do not assume responsibility for loss as a result of the presence of such substances.

6. The Americans with Disabilities Act (ADA) became effective January 26, 1992. We have not

made a specific compliance survey or analysis of this property to determine whether or not it is in conformity with the various detailed requirements of the ADA. It is possible that a compliance survey of the property together with a detailed analysis of the requirements of ADA could reveal that the property is not in compliance with one or more of the requirements of the act. If so, this fact could have a negative effect upon the value of the property. Since we have no direct evidence relating to this issue, we did not consider possible noncompliance with the requirements of ADA in estimating the value of the property.

24

Competency Statement

The Office of the Comptroller of the Currency has issued a ruling which requires lenders to evaluate appraisers competency for each specific appraisal assignment:

“Not all appraisers are competent to perform every type of appraisal that will be needed in connection with federally related transactions. For instance, an appraiser who is experienced in appraising shopping centers may not possess sufficient expertise to appraise a golf course. A financial institution should look beyond an individual’s title to determine if he or she has the experience and training needed to perform the appraisal. This provision is not intended to prohibit, in every instance, an individual from appraising a type of property with which he or she is not familiar. However, in such instances, an appraiser may perform the appraisal only in accordance with the Competency Provision in the USPAP.”

Francis B. Peacock, MAI, has appraised numerous commercial, professional office, industrial, multi-family residential and special-use facilities in Chattanooga, East Tennessee, North Georgia and surrounding areas. Therefore, Francis B. Peacock has met the requirements of USPAP’s Competency Provision. BenchMark Trust Corporation and Francis B. Peacock, MAI have experience in the appraisal of properties similar to the subject in this market. Francis B. Peacock is deemed qualified by education, training and experience in the preparation of such reports sufficient to comply with the competency provisions of USPAP. Terrence J. Peacock is a trainee under the supervision of Francis B. Peacock and has also appraised numerous tracts of vacant land.

25

Certification of Francis B. Peacock, MAI I certify that, to the best of my knowledge and belief: - The statements of fact contained in this report are true and correct. - The reported analyses, opinions, and conclusions are limited only by the reported assumptions and

limiting conditions and are my personal, impartial, and unbiased professional analyses, opinions, and conclusions.

- I have no present or prospective interest in the property that is the subject of this report and no

personal interest with respect to the parties involved. - I have no bias with respect to the property that is the subject of this report or to the parties involved

with this assignment. - My engagement in this assignment was not contingent upon developing or reporting predetermined

results. - My compensation for completing this assignment is not contingent upon the development or reporting

of a predetermined value or direction in value that favors the cause of the client, the amount of the value opinion, the attainment of a stipulated result, or the occurrence of a subsequent event directly related to the intended use of this appraisal.

- The reported analyses, opinions, and conclusions were developed, and this report has been prepared,

in conformity with the requirements of the Code of Professional Ethics & Standards of Professional Appraisal Practice of the Appraisal Institute.

- The reported analyses, opinions, and conclusions were developed, and this report has been prepared,

in conformity with the Uniform Standards of Professional Appraisal Practice. - The use of this report is subject to the requirements of the Appraisal Institute relating to review by its

duly authorized representatives. - Francis B. Peacock has appraised the subject property within the past three years, most recently as

can be found in the appraisers file 11-135, 12-126, 13-110, and 14-109. - I have made a personal inspection of the property that is the subject of this report. - No one provided significant real property appraisal assistance to the person signing this certification. - As of the date of this report, I Francis B. Peacock has completed the continuing education program of

the Appraisal Institute. ___________________________ Francis B. Peacock, MAI

26

Certification of Terrence J. Peacock I certify that, to the best of my knowledge and belief: - The statements of fact contained in this report are true and correct. - The reported analyses, opinions, and conclusions are limited only by the reported assumptions and

limiting conditions and are my personal, impartial, and unbiased professional analyses, opinions, and conclusions.

- I have no present or prospective interest in the property that is the subject of this report and no

personal interest with respect to the parties involved. - I have no bias with respect to the property that is the subject of this report or to the parties involved

with this assignment. - My engagement in this assignment was not contingent upon developing or reporting predetermined

results. - My compensation for completing this assignment is not contingent upon the development or reporting

of a predetermined value or direction in value that favors the cause of the client, the amount of the value opinion, the attainment of a stipulated result, or the occurrence of a subsequent event directly related to the intended use of this appraisal.

- The reported analyses, opinions, and conclusions were developed, and this report has been prepared,

in conformity with the requirements of the Code of Professional Ethics & Standards of Professional Appraisal Practice of the Appraisal Institute.

- The reported analyses, opinions, and conclusions were developed, and this report has been prepared,

in conformity with the Uniform Standards of Professional Appraisal Practice. - The use of this report is subject to the requirements of the Appraisal Institute relating to review by its

duly authorized representatives. - As of the date of this report, I have completed the Standards and Ethics Education Requirement of the

Appraisal Institute for Associate Members. - I have made a personal inspection of the property that is the subject of this report. - No one provided significant real property appraisal assistance to the person signing this certification. - Terrence Peacock has appraised the subject property within the past three years, most recently as can

be found in the appraisers file 11-135, 12-126, and 13-110. ___________________________ Terrence J. Peacock

27

Qualifications of Francis B. Peacock, MAI

Business Address

BenchMark Trust Corporation 608 Bell Avenue Chattanooga, Tennessee 37405 Telephone: (423) 266-0755

Education Graduated San Diego State University: BS 1974, MS 1977 Appraisal Institute - Courses

Real Estate Appraisal Principles -1987 Residential Valuation -1987 Standards of Professional Practice -1987 Seminar: Capitalization Overview -1988 Capitalization Theory and Techniques - Part A -1988 Capitalization Theory and Techniques - Part B -1989 Report Writing and Valuation Analysis -1991 Case Studies in Real Estate Valuation -1992

Additional Courses: Plans Reading and Cross Section Course Tennessee Department of Transportation -1989 Dynamics of Office Valuation Appraisal Institute -1996 Standards of Professional Practice (Part A) Appraisal Institute -1997 Standards of Professional Practice (Part B) Appraisal Institute -1997 Data Confirmation and Verification Appraisal Institute -1997 Loss Prevention Appraisal Institute -1998 Internet Search Strategies Appraisal Institute -1998 Eminent Domain & Condemnation Appraisal Institute -1999 Standards of Professional Practice (Part C) Appraisal Institute -2000 Partial Interest Valuation Appraisal Institute -2000 Standards of Professional Practice (Part C) Appraisal Institute -2000 Conservation Easements American Society of Farm Managers & Rural Appraisers -2000 Standards of Professional Practice (Part C) Appraisal Institute -2000 Special Purpose Properties Appraisal Institute -2001

28

Feasibility Analysis, Market Value & Investment Appraisal Institute -2002 Analyzing Commercial Lease Clauses Appraisal Institute -2003 Evaluating Residential Construction Appraisal Institute -2004 Numerous additional seminars and continuing education classes offered by the Appraisal Institute and various organizations over the last fifteen years.

Experience President/ Senior Appraiser - BenchMark Trust Corporation 1991- Current Fee Appraiser for Clayton, Roper & Marshall, Inc. 423 North Magnolia Ave., Orlando, Florida 32801 1989-91 Fee Appraiser, Affiliate Broker - Fidelity Trust Company 720 Cherry Street, Chattanooga, Tennessee 37402 1987-89 Expert Witness Experience Various Federal, State and local courts in East Tennessee and North Georgia. Professional Affiliations, Memberships and Licenses

Member of the Appraisal Institute (MAI No. 11002) State Certified Real Estate Appraiser - State of GA, Lic. No. 1044 State Certified Real Estate Appraiser - State of TN, Lic. No. CG-487 Certified General Real Estate Appraiser - State of VA, Lic. No. 4001 007145 Member Chattanooga Board of Realtors

Appraisals of most properties including:

Single Family Properties and Subdivisions Residential Apartments and Condominiums Shopping Centers Commercial Buildings and Sites Office Buildings Hospitality Properties Convenience Stores Restaurants Medical Clinics, Offices and Facilities Industrial Buildings and Sites Churches, Schools and Public Buildings Environmentally Endangered Lands-Waterfront, Lowlands Mobile Home Parks Special Use Properties Multi-Use Planned Unit Developments (PUD’s)

I have appraised properties in Virginia, South Carolina, Georgia, Tennessee, Florida, and

Alabama.

29

Partial List of Past Clients

Hamilton County State of Tennessee Department of Transportation SunTrust Bank, N.A. Regions Bank North Georgia Bank Southtrust Bank Union Planters Bank Bank of Cleveland North Georgia National Bank Southern Heritage Bank AmSouth Bank First Tennessee Bank First Volunteer Bank Cornerstone Community Bank Bank of East Ridge Norfolk Southern Railroad Northwest Georgia Bank Krystal Corporation U.S. Trust Company of New York Federal Deposit Insurance Corporation (FDIC) Unumprovdent Corporation Olan Mills Olin Chemical Company First National Bank & Trust of Athens Fidelity Savings Bank (Dalton) North Carolina National Bank (NCNB) Tennessee Wildlife Resource Management City of Chattanooga River Valley Partners MCI Telecommunications Corporation Phillip Services (Canada) Memorial Hospital Exxon Chattanooga Heart Institute U.S. Postal Service Tennessee Valley Authority Electric Power Board Chrysler Realty Corporation Orange County Florida Orlando Expressway Colonial Bank Bryan College Lee University Chattanooga State Community College First Management Services Chattanooga Heart Institute Tennessee Aquarium University of Tennessee CBL Ruby Falls John Alden Asset management Company Protective Life Insurance Company Numerous Attorneys

30

Qualifications of Terrence J. Peacock

Business Address

BenchMark Trust Corporation 608 Bell Avenue Chattanooga, Tennessee 37405 Telephone: (423) 266-0755

Education Graduated Kent State University: BBA-Marketing 2007. Appraisal Courses

General Appraiser Market Analysis and Highest & Best Use -2010 Appraisal Institute General Appraiser Report Writing and Case Studies -2010 Appraisal Institute General Appraiser Income Approach 1 -2010 Appraisal Institute General Appraiser Income Approach 2 -2010 Appraisal Institute General Appraiser Site Evaluation and Cost Approach -2010 Appraisal Institute Sales Comparison Approach -2010 Appraisal Institute Business Practices and Ethics -2009 Appraisal Institute Real Estate Finance Statistics and Valuation Modeling -2009 Appraisal Institute Real Estate Appraisal Principles -2007 Tennessee Real Estate Educational System Real Estate Appraisal Procedures -2007 Tennessee Real Estate Educational System Market Analysis & Highest and Best Use -2007 Tennessee Real Estate Educational System Uniform Standards of Professional Appraisal Practice -2007 Tennessee Real Estate Educational System

31

Additional Courses: Marketing Policy and Strategy -2007 Kent State University Service Marketing -2007 Kent State University Integrated Business Policy and Strategy -2006 Kent State University Business Finance -2006 Kent State University Business & Professional Writing -2005 Kent State University Managerial Accounting -2005 Kent State University Financial Accounting -2005 Kent State University Business Statistics. -2005 Kent State University Computer Applications -2004 Kent State University Legal Environment of Business -2004 Kent State University

Experience Associate Appraiser - BenchMark Trust Corporation 2007- Current Professional Affiliations, Memberships and Licenses

Associate Member of the Appraisal Institute State Registered Trainee Appraiser - State of TN, ID. No. 4267

Appraisals of properties including:

Commercial Buildings and Vacant Sites Industrial Buildings and Vacant Sites Office Buildings and Vacant Sites Medical Offices and Facilities

Eminent Domain Residential Sites

32

Addendum

33

Subject Location and Neighborhood Map

34

Hamilton County GIS Aerial Map

35

FEMA Flood Map

ZONING

Chapter 38– Page 31

ARTICLE V. ZONE REGULATIONS

DIVISION 1. R-1 RESIDENTIAL ZONE Section 38-41. Permitted uses.

(1) Single-family dwellings, excluding factory manufactured homes constructed as a single self-contained unit and mounted on a single chassis.

(Ord. No. 9661, 01/21/92) (2) Schools. (3) Parks, play grounds and community-owned not-for-profit buildings. (4) Golf courses, except driving ranges, miniature courses and other similar

commercial operations. (5) Fire stations and other publicly-owned buildings. (6) Churches and including a columbarium and/or mausoleum as an accessory use. (Ord. No. 12241, § 2, 5/19/09). (7) Home occupations. (8) Kindergartens operated by governmental units or religious organizations. (9) Day care homes. (10) Accessory uses and buildings customarily incidental and subordinate to the

above. (Code 1995, Appendix B, Art V, § 101; Ord. No. 12241, § 2, 5/19/09) Sec. 38-42. Uses permitted as special exceptions by the board of appeals.

The following uses and structures with their customary accessory buildings may be permitted as special exceptions by the Board of Appeals, subject to the requirements and restrictions as specified in Article VIII:

(1) Day care centers: Such uses shall require a Special Permit under the terms of Article VIII of this chapter.

(2) Kindergartens: Kindergartens not operated by governmental units or religious organizations shall require a Special Permit under the terms of Article VIII of this chapter.

(3) Assisted Living Facilities: The Board of Appeals may issue a Special Permit for an Assisted Living Facility under the terms specified in Article VIII of this chapter, provided that the facility shall contain no more than eight (8) residents. This facility may include two (2) additional persons (plus their dependants) acting as houseparents or guardians, who need not be related to the persons residing in the house.

(Ord. No. 10447, 07-16-96) (4) Communication Towers:

The Board of Appeals for Variances and Special Permits may issue a Special Permit for Communications Towers on publicly owned property under the terms specified in Article VIII.

(5) Special Permit for Equine for Personal Use. (Ord. No. 12508, §2, 5/24/11)

(Code 1995, Appendix B, Art V, § 102; Ord. No. 10705, 06/02/98; Ord. No. 11082, 10/17/00)

Chapter 38– Page 32

Sec. 38-43. Uses permitted as special exceptions by the city council.

The following uses may be permitted as special exceptions by the City Council, subject to the requirements and restrictions as specified in Article VI:

(1) Cemeteries: The City Council may permit the development of cemeteries (excluding crematoriums, embalming facilities or other such preparatory functions) within any R-1 Residential Zone, as a special exception under terms specified in Article VI of this chapter.

(2) Residential Homes for Handicapped and/or Aged Persons Operated on a Commercial Basis: The City Council may issue a Special Permit for a Residential Home for Handicapped and/or Aged Persons under the terms specified in Article VI of this chapter, provided that the Home shall not contain more than (8) handicapped and/or aged persons.

(3) Planned Unit Development: Flexibility in the arrangement of residential uses may be permitted by the City Council as special exceptions in any R-1 Residential Zone, provided that the minimum size of any tract of land sought to be used for the planned unit shall be two (2) acres and that a desirable environment through the use of good design procedures is assured, allowing flexibility in individual yard requirements to provide for multiple dwelling units, townhouses, and two-family units, except that such use or uses shall require a Special Permit under the terms of Article VI of this chapter.

(4) The City Council may issue a Special Exceptions Permit for a Two-Family Dwelling in the R-1 Residential Zone under the terms specified in Article VI of this chapter.

(5) Non-Profit Heritage Educational Facility under the terms specified in Article VI, Section 38-525.

(Ord. No. 12232, § 1, 4-21-09) (Code 1995, Appendix B, Art V, § 103; Ord. No. 11597, § 1, 08-17-04; Ord. No. 12046, § 1, 11-20-07; Ord. No. 12232, § 1, 4-21-09) Sec. 38-44. Height and area regulations.

(1) Height: No building shall exceed two and one-half stories or 35 feet in height

except that a building may exceed these height regulations provided that for every one (1) foot of additional height over thirty-five (35) feet the building shall be set back one (1) additional foot from all property lines.

(2) Front Setbacks: There shall be a front yard of not less than twenty-five (25) feet. For minimum Suburban Infill Lot Setback, see item (7)(f) of this section. For the Urban Infill Lot Compatibility Option, see Article V, Division 30.

(Ord. No. 11997, § 1, 8-21-07; Ord. No. 12277, §2, 8-18-09) (3) Side Setback: There shall be a side yard on each side of the building of not less

than ten (10) feet. For corner lot side yard requirements, see Article VI, Section 38-509.

(4) Rear Setback: There shall be a rear yard of not less than twenty-five (25) feet. (5) Minimum Lot Area: The only minimum lot area requirement is twenty-five

thousand (25,000) square feet for single-family lots on individual wells and septic tanks and seven thousand five hundred (7,500) square feet for single-family lots on sanitary sewers. In all other instances, a residential lot shall be

ZONING

Chapter 38– Page 33

large enough to construct the original subsurface sewage disposal system as required by the Health Department and to provide an area for one hundred percent (100%) duplication of that system. The area(s) for both original and duplicate systems shall meet the provision of the State Rules and Regulations to Govern Subsurface Sewage Disposal. The Health Department may limit the number of bedrooms and whirlpool tubs on the basis of effective capacity of the proposed sewage disposal facilities. The Health Department may require larger lots when septic tanks are used due to soil conditions, topography, drainage, presence of swimming pools, etc.

(6) Minimum Lot Frontage: The minimum lot frontage shall be sixty (60) feet on sewers and seventy-five (75) feet on septic tanks. For Suburban Infill Lot minimum frontage, see subsection (7). For Urban Infill Lot minimum frontage alternative, see Division 30, Urban Infill Lot Compatibility Option.

(Ord. No. 12277, § 2, 8/18/09) (7) Minimum Suburban Infill Lot Frontage and Setback: The minimum frontage

and front yard setback for Suburban Infill Lots shall be determined as follows: (a) Applicability. The Minimum Suburban Infill Lot Frontage Regulations

shall apply only to: i. Proposed or existing lots outside of the Urban Overlay Zone ii. Lots zoned R-1 Residential. iii. Proposed lot frontage less than one hundred twenty (120) feet. iv. Lots fronting an existing public street. v. Lots served by sewers.

(b) Exceptions. This rule shall not apply to: i. Planned Unit Developments (PUDs). ii. Lots created on a new street. iii. The consolidation of lots. iv. Lots at the terminus of permanent dead end streets with thirty-

five (35) feet of street frontage or more. v. Lots that are a combination of existing lots where all of the lots

are as large or larger than the previous lots and have equal or greater frontage than the previous lots.

vi. Lots, if, in the opinion of the Regional Planning Agency Staff, a smaller lot frontage is consistent with the Comprehensive Plan and the intent and purposes of these regulations.

(c) Compatible Lots. The following properties shall be used to determine the block character for purposes of establishing lot compatibility: i. Lots with on the same and opposing block faced within three

hundred (300) feet of the boundary of the boundary of the property proposed to be subdivided.

ii. Lots abutting each quadrant of an intersection when the proposal involves a corner lot; and

iii. Lots that abut or are directly across a public way, but not to the rear of the property, from the property proposed to be subdivided.

(d) Excluded Lots. The following properties shall not be used to determine the block character for purposes of establishing lot compatibility: i. Properties zoned non-residential or multi-family. ii. Properties zoned from single-family, but used for legal non-

residential uses or other legal non-conforming uses.

Chapter 38– Page 34

iii. Properties where development continuity cannot be provided due to a natural or man-made barrier, including but not limited to, arterial or collector streets, public land, railroad right-of-way, waterways, or

iv. Properties that face a block face within a non-residential zoning district.

v. Interior lots located to the rear of another lot but with a narrow portion extending to the street when that narrow portion is less than the frontage required by the Chattanooga Zoning Ordinance.

(e) Lot Frontage Compatibility Calculation. New residential infill lots shall have a minimum lot frontage that is no smaller than the smallest frontage on the same and opposing block face within three hundred (300) feet of the lot to be subdivided. i. The new infill lot frontage is not required to exceed one hundred

twenty (120) feet. ii. The new infill lot frontage shall not be less than the minimum

allowed by the R-1 Residential zone. iii. If, in the opinion of the Regional Planning Agency Staff, a

smaller lot frontage is not consistent with other lot frontages on the same and opposing block face or the intent and purposes of these regulations, a larger frontage may be required.

iv. Each lot frontage shall be the actual access to the property as well as the legal access (e.g. – no sole access via common easement).

(f) Front Setback. For Suburban Infill Lots recorded after July 9, 2007, the minimum front yard setback shall be the average of the two (2) front yard setbacks of existing dwellings on the abutting lots fronting on the same street if both abutting lots have dwellings within one hundred fifty (150) feet of the area to be subdivided. The Suburban Infill setback is not required to exceed fifty (50) feet, but shall not be less than the twenty-five (25) foot minimum front yard. This requirement does not apply to Planned Unit Development (PUDs).

(Ord. No. 11977, § 2, 6-19-07; Ord. No. 12277, § 2, 8-18-09) (Ord. No. 8527, 9/10/85; Code 1995, Appendix B, Art V, § 104; Ord. No. 11977, § 2, 6-19-07; Ord. No. 11997, § 1, 8-21-07; Ord. No. 12277, § 2, 8-18-09) Cross reference--Off-street parking requirements, Article V, Section 38-471, et seq., Ord. No. 11459, § 2, 09-16-03. Secs. 38-45 - 38-50. Reserved.