result presentation q2 2015

TRANSCRIPT

© Wärtsilä

WÄRTSILÄ CORPORATIONINTERIM REPORT JANUARY-JUNE 2015

17 JULY 2015Björn Rosengren,President & CEO

• Order intake EUR 1,159 million, +2%• Net sales EUR 1,230 million, +10%• Book-to-bill 0.94 (1.02)• EBIT EUR 137 million, 11.1% of net sales

(EUR 132 million or 11.8%)• EBITA EUR 144 million, 11.7% of net sales

(EUR 138 million or 12.4%) • EPS EUR 0.54 (0.42)• Cash flow from operating activities

EUR 47 million (61)• Order book at the end of the period

EUR 5,325 million, +20%• Acquisition of L-3 MSI finalised• Strategy fine-tuned, business names changed

EBIT is shown excluding non-recurring items.EBITA is shown excluding non-recurring items and purchase price allocation amortisation.As a result of the 2-stroke operations being classified as discontinued operations in 2014, comparison figures related to the statement of income have been restated.

Highlights Q2/2015

2 © Wärtsilä

© Wärtsilä

0

200

400

600

800

1000

1200

1400

Q2/2014 Q2/2015

2%

-23%

13%

2%

1,138

MEUR

Second quarter development

MEUR

3

Order intake growth supported by Services

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

2011 2012 2013 2014 2015

1,159

Q1-Q2 Q3-Q4

EnergySolutions

MarineSolutions

Services

© Wärtsilä

0

200

400

600

800

1000

1200

1400

Q2/2014 Q2/2015

Net sales in line with our expectations

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2011 2012 2013 2014 2015

10%

17%

-15%

40%

1,116

MEUR

Second quarter development

MEUR

1,230

4

Net sales developed well

Q1-Q2 Q3-Q4

EnergySolutions

MarineSolutions

Services

© Wärtsilä

Net sales by business 1-3/2012

Marine Solutions30% (37)

Energy Solutions23% (20)

Services47% (43)

5

Net sales by business 1-6/2015

© Wärtsilä

1.07 1.05 1.05 1.06 1.10

0,0

0,2

0,4

0,6

0,8

1,0

1,2

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

5500

2011 2012 2013 2014 1-6/2015

Order intake Net sales Book-to-bill

MEUR

6

Book-to-bill ratio remains above one

© Wärtsilä

Order book distribution

MEUR

7

Order book distribution

0

500

1000

1500

2000

2500

3000

3500

30.6.2014 30.6.2015

Delivery current year Delivery next year or later

© Wärtsilä

MEUR

8

Operating result and profitability

EBIT%EBIT

11.1% 10.9% 11.2%11.9%

0%

2%

4%

6%

8%

10%

12%

14%

0

100

200

300

400

500

600

2011 2012 2013 2014

EBIT is shown before non-recurring items. Figures for 2011-2013 and Q2/2014 include both discontinued and continuing operations.

Second quarter development

MEUR

10.8% 11.1%

0%

2%

4%

6%

8%

10%

12%

0

20

40

60

80

100

120

140

Q2/2014 Q2/2015

© Wärtsilä9

Challenging environment in the power generation markets

© Wärtsilä10

Energy Solutions’ quotation activity on a good level

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

Q1/2012

Q2/2012

Q3/2012

Q4/2012

Q1/2013

Q2/2013

Q3/2013

Q4/2013

Q1/2014

Q2/2014

Q3/2014

Q4/2014

Q1/2015

Q2/2015

MW

Multi-fuel

Gas

Liquid fuel

© Wärtsilä

0

200

400

600

800

1000

1200

1400

1600

1800

2011 2012 2013 2014 2015

MEUR Review period developmentTotal EUR 475 million (409)

IPP’s*

Utilities

Industrials

Oil 56%

Gas44%

Review period order intake by fuel in MW

x%

11

Growth in Energy Solutions’ order intake

49%

10%

41%

Q1-Q2 Q3-Q4

*IPP = Independent Power Producer

© Wärtsilä

40

584

31

Order intake 1-6/2015: 1,222 MW (986)

Americas 239 (76)

Asia 111 (284)

Africa and Middle East 175 (265)

UtilitiesIPP’sIndustrials

12

Energy Solutions’ orders globally

636

135

Europe 698 (361)

239

40

40

© Wärtsilä1313

21.5%

52.4%

10.3%

Market <500 MW4.7 GW (6.5)

15.0%

13

Market data includes all Wärtsilä power plants and other manufacturers’ gas and liquid fuelled turbine based power plants with prime movers above 5 MW, as well as estimated output of steam turbines for combined cycles. The data is gathered from the McCoy Power Report.Other combustion engines not included. In engine technology Wärtsilä has a leading position.

0.9%

Total market9.7 GW (11.0)

GE Siemens MHI Wärtsilä Other GTs

29.0%

43.3%

7.2%

20.1%

0.4%

Market for gas and liquid fuel based power plants 1-3/2015

© Wärtsilä14

Contracting volumes remain low

© Wärtsilä

0

1

2

3

4

5

0

50

100

150

200

250

01.0

903

.09

05.0

907

.09

09.0

911

.09

01.1

003

.10

05.1

007

.10

09.1

011

.10

01.1

103

.11

05.1

107

.11

09.1

111

.11

01.1

203

.12

05.1

207

.12

09.1

211

.12

01.1

303

.13

05.1

307

.13

09.1

311

.13

01.1

403

.14

05.1

407

.14

09.1

411

.14

01.1

503

.15

05.1

5

Mill

ion

CG

T

# of

ves

sels

Merchant Offshore Cruise and Ferry Special vessels 3 months moving average in CGT

15

Vessel contracting activity

Source: Clarkson Research Services, figures exclude late contracting* CGT= gross tonnage compensated with workload

*

*

06.1

5

© Wärtsilä

0

300

600

900

1200

1500

1800

2011 2012 2013 2014 2015

MEUR

Review period developmentTotal EUR 728 million (823)

Offshore15%

Traditional merchant

16%

Special vessels10%

16

Marine Solutions’ order intake

Others 4%

Q1-Q2 Q3-Q4

Gas carriers34%

Cruise & Ferry18%Navy

3%

© Wärtsilä

• Joint venture order intake totalled EUR 140 million (92) during January-June 2015

• Wärtsilä’s share of ownership in these companies is 50%, and the results are reported as a share of result of associates and joint ventures

MEUR

Marine Solutions order intake

Joint venture order intake, includes figures from Wärtsilä Hyundai Engine Company Ltd. and Wärtsilä Qiyao Diesel Company Ltd.

17

Joint venture ordering activity

0

100

200

300

400

500

600

700

Q1/2010

Q2/2010

Q3/2010

Q4/2010

Q1/2011

Q2/2011

Q3/2011

Q4/2011

Q1/2012

Q2/2012

Q3/2012

Q4/2012

Q1/2013

Q2/2013

Q3/2013

Q4/2013

Q1/2014

Q2/2014

Q3/2014

Q4/2014

Q1/2015

Q2/2015

© Wärtsilä

Wärtsilä’s market shares are calculated on a 12 months rolling basis, numbers in brackets are from the end of the previous quarter. The calculation is based on Wärtsilä’s own data portal.

Wärtsilä59% (56)

Others 16% (16)

MAN D&T15% (15)

Caterpillar10% (13)

Total market volume last 12 months:4,988 MW (5,711)

Medium-speed main engines

Wärtsilä5% (4)

Auxiliary engines

Total market volume last 12 months:4,078 MW (4,988)

Others95% (96)

18

Strong position in marine engine market

© Wärtsilä

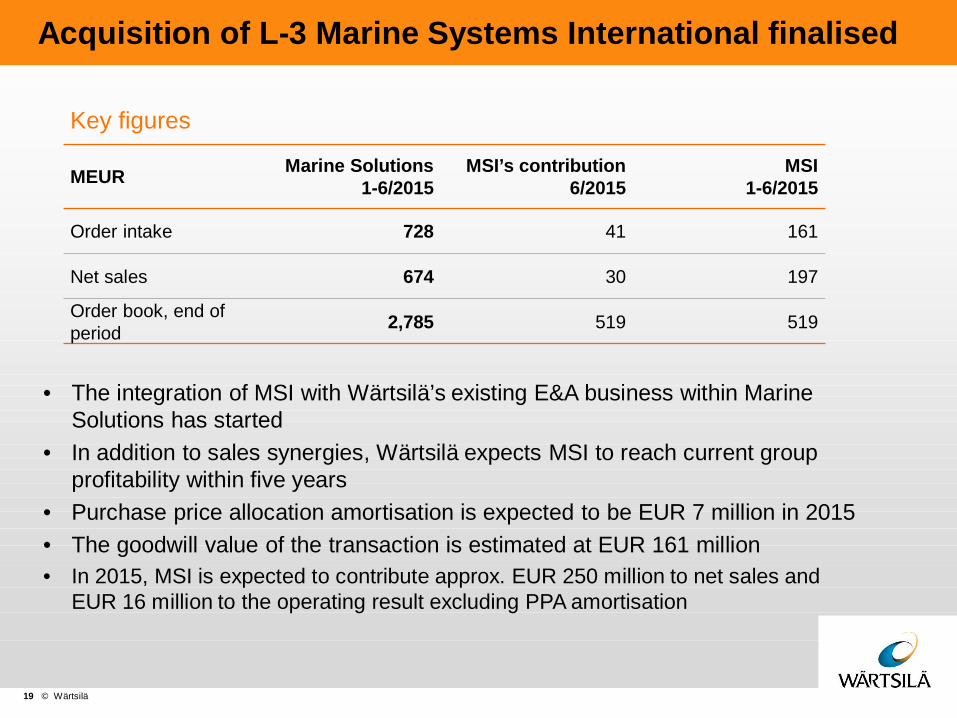

• The integration of MSI with Wärtsilä’s existing E&A business within Marine Solutions has started

• In addition to sales synergies, Wärtsilä expects MSI to reach current group profitability within five years

• Purchase price allocation amortisation is expected to be EUR 7 million in 2015• The goodwill value of the transaction is estimated at EUR 161 million• In 2015, MSI is expected to contribute approx. EUR 250 million to net sales and

EUR 16 million to the operating result excluding PPA amortisation

19

Acquisition of L-3 Marine Systems International finalised

Key figures

MEUR Marine Solutions1-6/2015

MSI’s contribution6/2015

MSI1-6/2015

Order intake 728 41 161

Net sales 674 30 197

Order book, end of period 2,785 519 519

© Wärtsilä

• Wärtsilä Marine Solutions plans to realign its organisation to maintain competitiveness in an environment of low demand

• Approx. 600 jobs will be reduced, of which 160 in Finland

• Wärtsilä seeks annual savings in the region of EUR 40 million

• The non-recurring costs related to the restructuring measures will be approximately EUR 25-30 million

• Currently, Wärtsilä Marine Solutions employs 7,217 people globally

20

Marine Solutions business to be adjusted to reflect the current market situation

© Wärtsilä21

Good activity in the service markets, market outlook remains positive

© Wärtsilä

0

200

400

600

800

1000

1200

1400

1600

1800

2000

2011 2012 2013 2014 2015

-3%

0

100

200

300

400

500

600

Q2/2014 Q2/2015

MEUR

Second quarter development

MEUR

468

17% 548

22

Services’ net sales increased by 14% in 1-6/2015

5%

Q1-Q2 Q3-Q4

5%

© Wärtsilä

Spare parts 51%(52)

Field service 24%(25)

Contracts 17%(17)

Projects7%(6)

23

Total EUR 1,034 million (903)

Services net sales distribution 1-6/2015

© Wärtsilä24

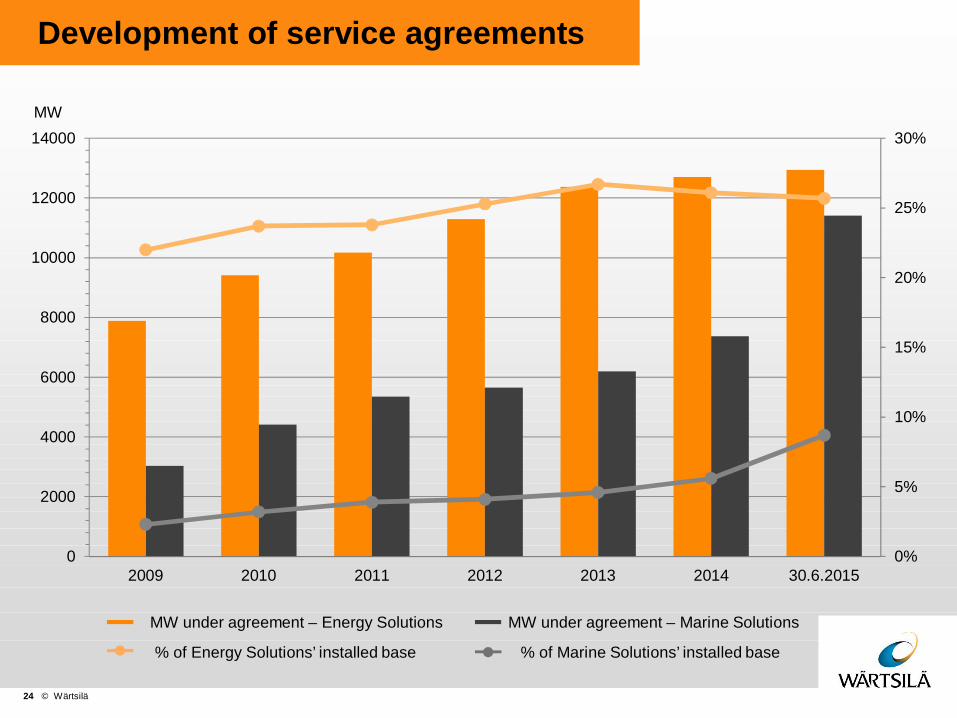

MW

Development of service agreements

MW under agreement – Energy Solutions MW under agreement – Marine Solutions

% of Marine Solutions’ installed base% of Energy Solutions’ installed base

0%

5%

10%

15%

20%

25%

30%

0

2000

4000

6000

8000

10000

12000

14000

2009 2010 2011 2012 2013 2014 30.6.2015

© Wärtsilä

• QuantiParts operates from the Netherlands and serves customers in the marine, locomotive and power plant industries worldwide

• QuantiParts trades OEM spare parts for selected mature Wärtsilä medium- and high-speed 4-stroke engines

• Establishing QuantiParts fits well with Wärtsilä Services strategy of aligning its organisation in order to ensure tailor-made services for its customers

25

QuantiParts B.V. – a new subsidiary to trade spare parts for classic 4-stroke Wärtsilä engines

© Wärtsilä26

Solid financial standing

© Wärtsilä27

Cash flow from operating activities

0

100

200

300

400

500

600

700

2011 2012 2013 2014

MEUR

0

20

40

60

80

100

120

140

160

180

1-6/2014 1-6/2015

Review period development

MEUR

© Wärtsilä

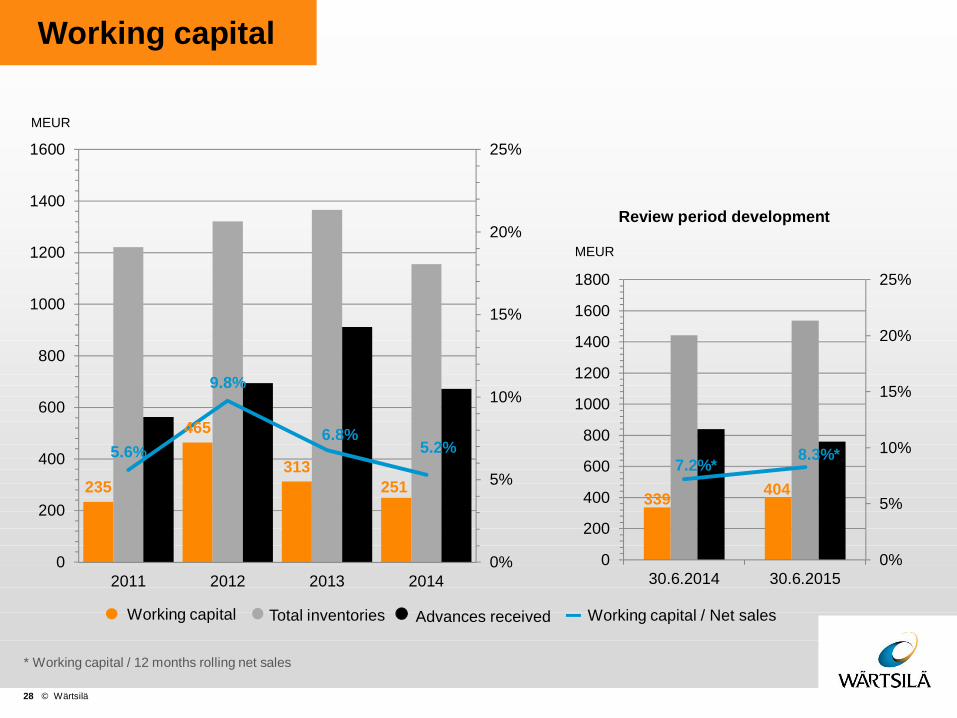

235

465

313251

5.6%

9.8%

6.8%5.2%

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1000

1200

1400

1600

2011 2012 2013 2014

Working capital Total inventories Advances received Working capital / Net sales

MEUR

28

Working capital

MEUR

Review period development

* Working capital / 12 months rolling net sales

339 4047.2%* 8.3%*

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1000

1200

1400

1600

1800

30.6.2014 30.6.2015

© Wärtsilä29

Gearing impacted by L-3 MSI acquisition

0,00

0,10

0,20

0,30

0,40

0,50

2011 2012 2013 2014 0,00

0,10

0,20

0,30

0,40

0,50

30.6.2014 30.6.2015

Review period development

© Wärtsilä

• Energy Solutions: Based on the market situation during 2014 and the GDP forecasts for 2015, the market for liquid and gas fuelled power generation is expected to remain challenging.

• Marine Solutions: The outlook for the shipping and shipbuilding market environment is challenging. Low oil prices are impacting demand for offshore vessels. The sentiment in the gas carrier market and cruise & ferry is healthy.

• Services: The overall service market outlook is positive with growth opportunities in selected regions and segments.

30

Market outlook

© Wärtsilä31

Wärtsilä expects its net sales for 2015 to grow by 5-10% and its operational profitability (EBIT% before non-recurring items) to be between 12.0-12.5%. The guidance includes the impact of the L-3 Marine Systems International acquisition.

Prospects for 2015 revised

© Wärtsilä

• Environmental awareness and changing energy needs are increasingly steering investments in the markets in which we operate

• We seek growth by offering energy efficient lifecycle solutions, gas based technology, as well as innovative solutions that leverage our project management and engineering competence

• Our growth ambitions are supported by our superior global service network

32

Company strategy fine-tuned

© Wärtsilä

• The Wärtsilä 31 engine is the marine industry’s most advanced, powerful, fuel efficient, fuel flexible, and environmentally sound engine

• The engine achieved a Guinness World Records title for the most efficient 4-stroke diesel engine

• Remarkable increases in fuel efficiency andfuel flexibility are matched by significant reductions in maintenance costs

• The engine comes in three alternative versions; diesel, dual-fuel and spark-ignited gas

33

A brand new medium-speed Wärtsilä 31 engine launched in June

IR Contact:Natalia ValtasaariDirector, Investor Relations Tel. +358 (0) 40 187 7809E-mail: [email protected]