results briefing presentation 2q 2018 - insage

TRANSCRIPT

© All Rights Reserved.

This material is confidential and property to IHH Healthcare Berhad. No part of this material

should be reproduced or published in any form by any means, nor should the material be

disclosed to third parties without the consent of IHH.

Results Briefing Presentation

2Q 2018

28 August 2018

2

Disclaimer

This document is and shall remain the exclusive property of IHH Healthcare Berhad (the “Company”) and nothing herein shall give, or shall be construed

as giving, to any party any right, title, ownership, interest, licence or any other right whatsoever in or to this document. Neither this document nor any part

thereof may be (i) copied, photocopied, duplicated or otherwise reproduced in any form or by any means; or (ii) redistributed, passed on or otherwise

disseminated, without the Company’s permission. Although care has been taken to ensure that the information in this document is accurate, and that the opinions expressed are fair and reasonable, the

information is subject to change without notice, its accuracy is not guaranteed, has not been independently verified and it may not contain all material

information concerning the Company and its subsidiaries and associate companies. None of the Company nor its subsidiaries or associate companies nor

any of its or their respective members, directors, officers, employees, affiliates or advisors make any representation or warranty (express or implied)

regarding, nor assumes any responsibility or liability for, the accuracy, reasonableness, fairness or completeness of, or any errors or omissions in, any

information contained herein. Accordingly, none of the above nor any other person accepts any liability (in negligence, or otherwise) for any loss arising

from or in connection with any use of this document or its contents. This document is for information purposes only and does not constitute or form part of any offer or invitation by or on behalf of the Company for sale or

subscription of or solicitation or invitation of any offer to or recommendation to buy or subscribe for any securities (“Securities”), nor shall it or any part of it

form the basis of or be relied on in connection with any contract, commitment or investment decision in relation to the Securities of the Company in

Malaysia, Singapore or any other jurisdiction. The information in this document does not take into consideration the investment objectives, financial

situation or particular needs of any particular investor, and should not be treated as giving investment advice. In addition, this document contains certain financial information and results of operation, and may also contain certain projections, plans, strategies, and

objectives of the Company, that are not statements of historical fact which would be treated as forward looking statements that reflect the Company’s

current views with respect to future events and financial performance. These views are based on a number of estimates and current assumptions which are

subject to business, economic, political and competitive uncertainties and contingencies as well as various risks which are in many cases outside the

control of the Company, and which may change over time and may cause actual events and the Company’s future results to be materially different than

expected or indicated by such statements. No assurance can be given that future events will occur, that projections will be achieved, or that the Company’s

assumptions are correct. Such forward‐looking statements are not guarantees of future performance and accordingly, the actual results, financial condition,

performance or achievements of the Company may differ materially from those anticipated by the Company in the forward looking statements. You are

cautioned not to place undue reliance on these forward looking statements. The Company does not undertake to provide you with access to any additional information or to update the information contained in the document or to

correct any inaccuracies therein which may become apparent.

3

Key Highlights for Q2 2018

Resilient core performance, PATMI (Excl EI) nearly triples Sustained organic growth on constant currency terms • Q2 2018 revenue down 4% year-on-year to RM2.7 billion; EBITDA down 1% to RM527.9

million on stronger Malaysian Ringgit • PATMI (Excl EI) at RM256.5 million in Q2 2018 given a low base last year; also driven by

stronger operational performance and boosted by foreign exchange gains

Strong balance sheet with prudent cash management: • Net gearing of 0.04 times with RM6.2 billion cash position • Cash flow from operations remained strong at RM951.5 million for the 1H 2018

Revenue

RM2.7 b (↓ 4%)

EBITDA

RM527.9 m (↓ 1%)

PATMI

RM165.1 m (↓ 48%)

PATMI (Excl EI)

RM256.5 m (↑ 197%)

© All Rights Reserved.

This material is confidential and property to IHH Healthcare Berhad. No part of this material

should be reproduced or published in any form by any means, nor should the material be

disclosed to third parties without the consent of IHH.

4

Financial Highlights

5

Sustained organic growth from existing operations

YoY growth eroded by stronger RM

RM'mil 2018 2017 Variance 2018 2017 Variance

Revenue 2,659.7 2,771.8 -4% 5,514.7 5,456.7 1%

EBITDA 527.9 535.8 -1% 1,136.8 1,101.4 3%

PATMI 165.1 316.6 -48% 222.3 786.6 -72%

PATMI (Excl EI) 256.5 86.2 197% 377.0 288.0 31%

QTD Jun YTD JunTotal Group Results

Q2 Commentary

• Revenue and EBITDA eroded by stronger RM upon translation of results from overseas operations.

• On constant currency, Revenue and EBITDA increased 14% and 13% respectively due to:

- Sustained organic growth at our existing operations; and

- Continuous ramp up of Gleneagles Hong Kong and Acibadem Altunizade (both opened in March 2017)

• PATMI decreased due to high base in Q2 2017 from the gain on disposal of remaining 4.78% equity stake in

Apollo Hospitals and higher FX losses from Acibadem’s non-Turkish Lira borrowing

• PATMI excluding exceptional items increased from a low base in Q2 2017 with the recognition of interest on

capital gains tax payable and additional tax provisions relating to prior years’ tax. The Group also recognised

FX gains on its USD cash balances.

RM'mil 2018 2017 Variance 2018 2017 Variance

Profit after tax and minority interests 165.1 316.6 -48% 222.3 786.6 -72%

Add back/(Less): Exceptional Items

Insurance compensation for Chennai flood 0.3 - (17.4) -

Gain on dispoal of quoted FVOCIi financial instruments

ii- (241.1) - (554.5)

Provision for financial guarantee given on a joint venture's

loan facilityiii

0.4 0.8 0.7 0.8

Exchange loss/(gain) on net borrowingsiv

189.2 20.8 349.0 114.8

189.9 (219.5) 332.4 (438.9)

Add/(less): Tax effects on exceptional items (37.8) (4.2) (69.8) (23.0)

152.0 (223.7) 262.6 (461.8)

Add/(less): Minority interest share of exceptional items (60.6) (6.7) (107.9) (36.7)

91.4 (230.3) 154.7 (498.6)

Profit after tax and minority interests

(Excluding exceptional itemsv) 256.5 86.2 197% 377.0 288.0 31%

Less: PATMI contribution from PLife REIT (17.5) (18.4) (32.6) (35.9)

Profit after tax and minority interests

(Excluding exceptional itemsv and PLife REIT) 239.0 67.8 NM 344.4 252.1 37%

YTD JunQTD Jun

6

Exceptional Items

Note:

i) Fair valued through other comprehensive income

ii) Gain on disposal of the Group’s 4.78% and 6.07% interest in Apollo Hospital Enterprise Limited in May 2017 and March 2017 respectively

iii) Proportionate share of corporate guarantee in relation to accrued interest on Khubchandani Hospital's loan

iv) Exchange differences arising from foreign currency denominated borrowings/payables net of foreign currency denominated cash/receivables, recognised

by Acibadem Holdings (As at 30 June 2018, Euro/TL=5.3092, USD/TL=4.5607)

v) Exceptional items, net of tax and non-controlling interests

As at

30 Jun 2018

As at

31 Dec 2017

RM'mil RM'mil

Total Assets 38,589 38,924

- Tangible Assets 26,029 25,954

- Intangible Assets

Goodwill 10,316 10,692

Other intangibles 2,245 2,278

Total Liabilities (13,584) (13,024)

Total Equity 25,006 25,901

Non-controlling Interests ("NCI") (1,663) (1,852)

Perpetual securities ("Perps") (2,156) (2,159)

Total Shareholders' Equity (excluding NCI and Perps) 21,187 21,890

Net Tangible Assets ("NTA") (excluding NCI and Perps) (A) 8,626 8,920

Total Debt (B) (7,246) (6,794)

Total Cash 6,193 6,079

Net Debt (C) (1,052) (715)

Net Debt / NTA (C)/(A) 0.12 0.08

Net Debt / Equity 0.04 0.03

Gross Debt / EBITDA* (times) (B)/(D) 3.13 2.98

Net Debt / EBITDA* (times) (C)/(D) 0.45 0.31

7 *: Based on last 12 months EBITDA

^: Excludes fixed deposits (>3 months) of R48.5 million (Dec 2017: RM163.6 million)

Healthy Balance Sheet

RM' mil

Projected

Disbursements

from Q3 2018

Pantai Hospital Kuala Lumpur Expansion 128.1

Pantai Hospital Ayer Keroh Expansion 153.5

Pantai Hospital Klang Expansion 155.8

Gleneagles Medini Greenfield 110.2

547.6

Gleneagles Hong Kong Hospital - 60% Greenfield 154.2

Gleneagles Shanghai Hospital - 70% Greenfield 581.8

Gleneagles Chengdu Hospital - 70% Brownfield 450.5

Gleneagles Nanjing Hospital - 60% Greenfield 89.3

1,121.6

Yangon Hospital - 52% Greenfield 341.8

IMU Expansion 29.1

Acibadem Maslak Expansion 95.2

Acibadem Atasehir Greenfield 203.4

Acibadem Kartal Greenfield 178.0

476.5

Total Unincurred Expansion Capital Expenditure 2,670.9 8

Expansion Capital Expenditure – Construction & Medical Equipment

*

*

*

*

*

Expect to invest approx. RM2.7 billion from Q3 2018 for the Group’s hospital projects

Funded from Malaysia’s operating cash flows

and new bank facilities, if required

*: Parkway will fund its share of the project cost

through its bank facility and the hospital

business partner will fund their respective

share. Amount shown is total capex

(% indicated shows the immediate holding

company’s ownership interest in these

hospitals)

Funded from Acibadem’s operating cash flows

and bank facilities

Based on the following exchange rates: 1 SGD : 2.9551 1TL : 0.9998 1 HKD : 0.5124 1 RMB : 0.6132 1 USD : 4.0216

^

^

^: Projects deferred

© All Rights Reserved.

This material is confidential and property to IHH Healthcare Berhad. No part of this material

should be reproduced or published in any form by any means, nor should the material be

disclosed to third parties without the consent of IHH.

9

Operational Highlights

10

Q2 2018 Operational Overview

Healthy revenue intensity across all home markets

1. Based on Singapore, Malaysia, India and Acibadem Holdings hospitals only. Excludes hospitals operated by joint venture companies, hospitals under hospital management agreements and other international hospitals.

2. Specialist fees not included in Singapore’s and Malaysia’s average revenue per inpatient admission

3. Based on a uniform exchange rate throughout the periods shown (SGD: 2.95508; INR:0.05895; TL:0.99982)

Inpatient Admission Volumes1 (Number)

Average Revenue per Inpatient Admission1 (RM)

Q12017

Q22017

Q12018

Q22018

27,720 28,034

29,120

30,502

PPL - MalaysiaPPL - Singapore2,3

Q12017

Q22017

Q12018

Q22018

5,861

6,179

6,427

6,701

PPL - MalaysiaPPL - Malaysia2

Q12017

Q22017

Q12018

Q22018

7,615 7,784

8,711 9,332

PPL - MalaysiaAcibadem2,3

Q12017

Q22017

Q12018

Q22018

7,280 7,252

7,907 7,939

PPL - MalaysiaPPL - India2,3

Q2 YoY Growth 0.4% Q2 YoY Growth -2.8% Q2 YoY Growth -5.5% Q2 YoY Growth 8.0%

Q2 YoY Growth 8.8% Q2 YoY Growth 8.4% Q2 YoY Growth 9.5% Q2 YoY Growth 19.9%

Q12017

Q22017

Q12018

Q22018

50,541

49,347

50,250

47,985

PPL - Malaysia

Q12017

Q22017

Q12018

Q22018

18,842 18,936

19,352 19,021

PPL - MalaysiaPPL - Singapore

Q12017

Q22017

Q12018

Q22018

52,581 52,995

60,166 57,239

PPL - MalaysiaAcibadem

Q12017

Q22017

Q12018

Q22018

16,008

17,194 17,075

16,242

PPL - MalaysiaPPL - India

11

Hospital Expansion Pipeline

2 projects due

to be completed

in 2018

2 projects due

to be completed

in 2019

4 projects due

to be completed

in 2020 and

beyond

Country Type Hospital Description

Malaysia Expansion Pantai Hospital Kuala Lumpur Block B Phase 2: 120 beds capacity

Turkey Expansion Acibadem Maslak 195 bed capacity

Country Type Hospital Description

China Greenfield Gleneagles Chengdu 350 bed capacity

China Greenfield Gleneagles Shanghai 450 bed capacity

Country Type Hospital Description

Malaysia Expansion Pantai Hospital Ayer Keroh 160 bed capacity (by 2020)

Malaysia Expansion Pantai Hospital Klang 140 bed capacity (by 2020)

Turkey Greenfield Acibadem Kartal, Istanbul 120 bed capacity

(To be evaluated)

Turkey Greenfield Acibadem Atasehir, Istanbul 128 bed capacity

(To be evaluated)

© All Rights Reserved.

This material is confidential and property to IHH Healthcare Berhad. No part of this material

should be reproduced or published in any form by any means, nor should the material be

disclosed to third parties without the consent of IHH.

12

Outlook and Key Takeaways

13

Outlook

Shifting demographics

in home and key

growth markets

Fast growing upper/

middle class in home

and key growth markets

Attract foreign patients

to established medical hubs

IHH will continue to draw from rapid growth over the past few years:

Expansion of existing and new facilities to support growth in demand for quality private healthcare:

Experienced

management team

with execution track

record

40-year track record

of delivering superior

clinical outcomes

Strong balance

sheet and

operating cash flows

Strong brands

and network

of hospitals

Strengthen service

offerings in existing

hospitals

Ramp up new hospitals

to achieve optimal

operating leverage

Consolidate newly

acquired assets

Prepare for progressive

opening of greenfields

hospitals

The Group remains resilient amid challenging operating environment expected for the year ahead:

14

The Group continued to deliver sustained organic growth as it ramps up new and existing

operations and maintained robust balance sheet through prudent cash management

Despite improved operational performance, EBITDA was partially eroded on a stronger Malaysian

Ringgit

Performance must be also viewed against a strong Q2 2017. Headline PATMI decreased against a

high base that included a one-off gain of RM241.1 million from the Apollo Hospitals stake

divestment

Positioning for sustainable growth through a differentiated portfolio strategy to maintain leadership,

explore new new markets, innovate, while driving organic operations.

Prudent cost management and assessment of growth opportunities to maximise value for investors

Remain well-placed to capture opportunities and manage near-term volatility:

India: Becoming a leading healthcare player in fast-growing India market: disciplined addition

of Fortis into IHH family; existing India operations ramping up to new level of excellence

Greater China: Growth pipeline will come onstream progressively

Turkey: Accelerating restructuring plans to reduce Acibadem’s foreign currency debt to

manage exposure to currency volatility

Resilient Core Financial Performance in Q2

Focused on delivering sustainable long-term value

Key Takeaways

© All Rights Reserved.

This material is confidential and property to IHH Healthcare Berhad. No part of this material

should be reproduced or published in any form by any means, nor should the material be

disclosed to third parties without the consent of IHH.

15

Questions & Answers

© All Rights Reserved.

This material is confidential and property to IHH Healthcare Berhad. No part of this material

should be reproduced or published in any form by any means, nor should the material be

disclosed to third parties without the consent of IHH.

16

Supplementary slides

17

Contribution across the Group

RM'mil

PPL-Singapore

PPL-Malaysia

PPL-China

PPL-HK

PPL-India

PPL-Others

Acibadem Holdings

IMU Health

REIT

Others

Check to highlights

Others, -20%

REIT, 12%

IMU Health, 12%

Acibadem Holdings, 10%

PPL-Others, -8%

PPL-India, -10%

PPL-HK, -55%

PPL-China, 5%

PPL-Malaysia, 40%

PPL-Singapore, 112%

-100% -50% 0% 50% 100% 150%

Others, 0%

REIT, 1%

IMU Health, 2%

Acibadem Holdings, 33%

PPL-Others, 2%

PPL-India, 6%

PPL-HK, 3%

PPL-China, 2%

PPL-Malaysia, 18%

PPL-Singapore, 34%

0% 10% 20% 30% 40%

Others, 0%

REIT, 1%

IMU Health, 2%

Acibadem Holdings, 34%

PPL-Others, 2%

PPL-India, 6%

PPL-HK, 1%

PPL-China, 2%

PPL-Malaysia, 16%

PPL-Singapore, 35%

0% 10% 20% 30% 40%

Others, -5%

REIT, 13%

IMU Health, 5%

Acibadem Holdings, 26%

PPL-Others, 2%

PPL-India, 1%

PPL-HK, -14%

PPL-China, 3%

PPL-Malaysia, 23%

PPL-Singapore, 47%

-20% -10% 0% 10% 20% 30% 40% 50% 60%

Others, -3%

REIT, 12%

IMU Health, 4%

Acibadem Holdings, 26%

PPL-Others, 0%

PPL-India, 0%

PPL-HK, -8%

PPL-China, 0%

PPL-Malaysia, 23%PPL-Singapore,

46%

-20% -10% 0% 10% 20% 30% 40% 50%

Others, -13%

REIT, 9%

IMU Health, 9%

Acibadem Holdings, 11%

PPL-Others, -4%

PPL-India, -6%

PPL-HK, -29%

PPL-China, -1%

PPL-Malaysia, 37% PPL-Singapore, 88%

-40% -20% 0% 20% 40% 60% 80% 100%

YTD 2018 PATMI (Excl EI)

YTD 2017 PATMI (Excl EI)

YTD 2018 Revenue YTD 2018 EBITDA

YTD 2017 Revenue YTD 2017 EBITDA

18

RM'mil 2018 2017 Variance 2018 2017 Variance

Revenue 2,626.5 2,737.3 -4% 5,448.8 5,389.6 1%

EBITDA 460.8 466.0 -1% 1,002.9 962.6 4%

PATMI 147.6 298.1 -50% 189.7 750.7 -75%

PATMI (Excl EI) 239.0 67.8 252% 344.4 252.1 37%

QTD Jun YTD JunExcluding PLife REIT’s Results

Sustained organic growth from existing operations

YoY growth eroded by stronger RM

19

Revenue QoQ & YoY Comparison

Revenue1

Q2 2018 Q1 2018 Variance Q2 2018 Q2 2017 Variance YTD 2018 YTD 2017 Variance

RM'mil RM'mil % RM'mil RM'mil % RM'mil RM'mil %

Parkway Pantai:

- Singapore 954.9 921.5 4% 954.9 957.6 0% 1,876.4 1,919.1 -2%

- Malaysia 481.7 484.0 0% 481.7 455.4 6% 965.6 896.9 8%

- Malaysia(New)

- - - - - - - - -

- India 159.7 173.0 -8% 159.7 173.8 -8% 332.7 335.2 -1%

- North Asia 60.1 56.4 7% 60.1 72.3 -17% 116.5 137.5 -15%

- North Asia (New)

70.4 54.9 28% 70.4 14.4 NM 125.3 14.8 NM

- PPL Others* 43.5 45.2 -4% 43.5 41.2 6% 88.7 85.4 4%

Parkway Pantai 1,770.2 1,734.9 2% 1,770.2 1,714.7 3% 3,505.2 3,388.8 3%

Acibadem Holdings 696.4 910.6 -24% 696.4 868.2 -20% 1,607.0 1,775.0 -9%

Acibadem Holdings(New)

94.0 112.7 -17% 94.0 85.4 10% 206.6 93.4 121%

Acibadem Holdings 790.4 1,023.3 -23% 790.4 953.6 -17% 1,813.7 1,868.4 -3%

IMU Health 64.6 64.1 1% 64.6 68.4 -5% 128.7 131.3 -2%

Others^ 1.2 - - 1.2 0.6 121% 1.2 1.1 13%

GROUP (Excl REIT) 2,626.5 2,822.3 -7% 2,626.5 2,737.3 -4% 5,448.8 5,389.6 1%

PLife REIT Total 82.9 82.7 0% 82.9 85.8 -3% 165.6 170.0 -3%

Less: PLife REIT Inter-segment (49.7) (50.0) 1% (49.7) (51.3) 3% (99.7) (103.0) 3%

PLife REIT 33.2 32.7 1% 33.2 34.6 -4% 65.9 67.1 -2%

GROUP 2,659.7 2,855.0 -7% 2,659.7 2,771.8 -4% 5,514.7 5,456.7 1%

Q-on-Q QTD Y-on-Y YTD Y-on-Y

1: Relates to external revenue only.

It excludes PLife REIT’s rental income earned from Parkway Pantai. Similarly, it excludes Parkway Pantai’s dividend and management fee income earned from PLife REIT.

*: PPL Others comprise mainly Parkway Pantai’s hospital in Brunei, corporate office as well as other investment holding entities within Parkway Pantai

^: Others comprise mainly IHH Group’s corporate office as well as other investment holding entities

20

Revenue Q2 revenue eroded by strengthening RM

Revenue Variance (RM’mil)

The above figures excludes PLife REIT

Actual@ Constant

Currency

Parkway Pantai 3% 8%

Acibadem Holdings -3% 28%

IMU Health -2% -2%

IHH Group (Excl PLife REIT) 1% 15%

YTD'18 vs YTD'17

Revenue - QTD Variance

Revenue - YTD Variance

5,389.6

278.9

162.5

527.9

582.6 2.6

0.1 5,448.8

YTD 2017 Parkway Pantai Parkway Pantai(TranslationDifference)

AcibademHoldings

AcibademHoldings

(TranslationDifference)

IMU Health Others YTD 2018

2,737.3

140.3

84.8

247.8

410.9 3.7

0.7 2,626.5

QTD 2017 Parkway Pantai Parkway Pantai(TranslationDifference)

AcibademHoldings

AcibademHoldings

(TranslationDifference)

IMU Health Others QTD 2018

Actual@ Constant

Currency

Parkway Pantai 3% 8%

Acibadem Holdings -17% 26%

IMU Health -5% -5%

IHH Group (Excl PLife REIT) -4% 14%

Q2'18 vs Q2'17

21

EBITDA QoQ & YoY Comparison

EBITDA1

Q2 2018 Q1 2018 Variance Q2 2018 Q2 2017 Variance YTD 2018 YTD 2017 Variance

RM'mil RM'mil % RM'mil RM'mil % RM'mil RM'mil %

Parkway Pantai:

- Singapore2

283.3 237.7 19% 283.3 257.3 10% 521.0 522.9 0%

- Malaysia 128.0 133.6 -4% 128.0 119.7 7% 261.5 248.7 5%

- Malaysia(New)

- - - - - - - - -

- India (4.7) 8.3 -156% (4.7) 4.5 NM 3.7 6.6 -44%

- North Asia 4.2 1.0 NM 4.2 18.3 -77% 5.2 28.9 -82%

- North Asia (New)

(48.8) (51.0) 4% (48.8) (72.4) 33% (99.7) (156.9) 36%

- PPL Others* (12.8) 10.7 NM (12.8) 7.2 NM (2.1) 19.0 -111%

Parkway Pantai 349.2 340.3 3% 349.2 334.7 4% 689.5 669.1 3%

Acibadem Holdings 79.1 153.9 -49% 79.1 127.3 -38% 233.1 278.8 -16%

Acibadem Holdings(New)

29.1 35.0 -17% 29.1 17.7 64% 64.1 12.5 NM

Acibadem Holdings 108.3 188.9 -43% 108.3 145.0 -25% 297.1 291.3 2%

IMU Health 23.4 26.5 -12% 23.4 24.6 -5% 49.9 52.0 -4%

Others^ (20.0) (13.6) -47% (20.0) (38.3) 48% (33.7) (49.8) 32%

GROUP (Excl REIT) 460.8 542.1 -15% 460.8 466.0 -1% 1,002.9 962.6 4%

PLife REIT3

67.1 66.8 0% 67.1 69.8 -4% 133.9 138.8 -4%

GROUP 527.9 608.9 -13% 527.9 535.8 -1% 1,136.8 1,101.4 3%

Q-on-Q QTD Y-on-Y YTD Y-on-Y

1: Relates to the EBITDA performance of each SBUs. After elimination of dividend income from within the Group

2: Includes rental expense incurred for lease of hospitals from PLife REIT

3: Includes rental income earned from lease of hospitals to Parkway Pantai

*: PPL Others comprise mainly Parkway Pantai’s hospital in Brunei, corporate office as well as other investment holding entities within Parkway Pantai

^: Others comprise mainly IHH Group’s corporate office as well as other investment holding entities

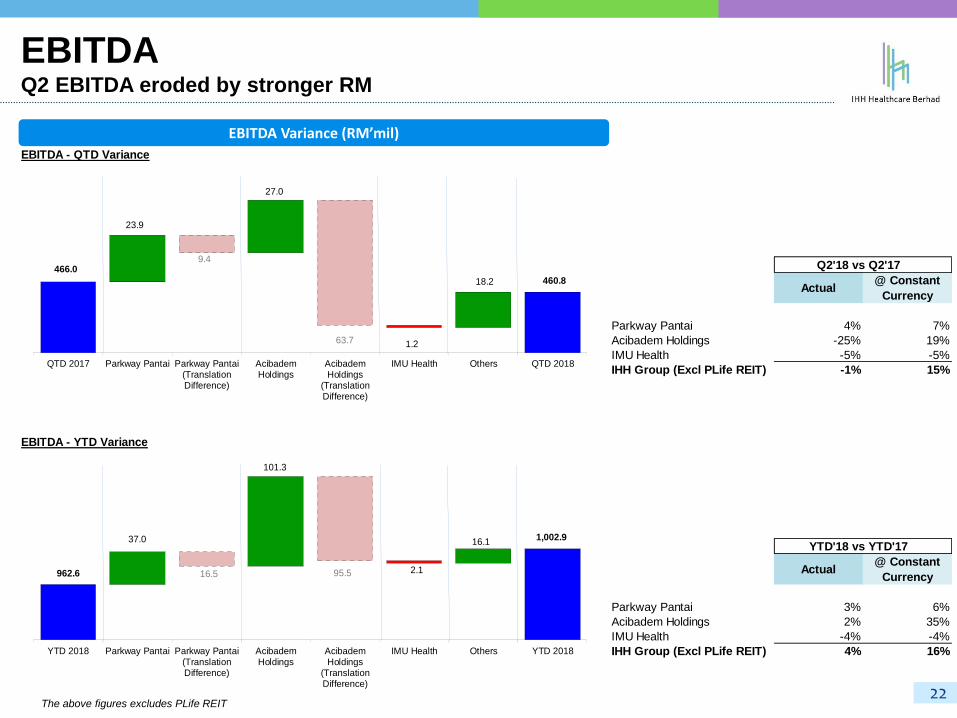

22

EBITDA Variance (RM’mil)

The above figures excludes PLife REIT

EBITDA Q2 EBITDA eroded by stronger RM

Actual@ Constant

Currency

Parkway Pantai 3% 6%

Acibadem Holdings 2% 35%

IMU Health -4% -4%

IHH Group (Excl PLife REIT) 4% 16%

YTD'18 vs YTD'17

EBITDA - QTD Variance

EBITDA - YTD Variance

Parkway Pantai

Acibadem Holdings

IMU Health

IHH Group (Excl PLife REIT)

Check:

962.6

37.0

16.5

101.3

95.5 2.1

16.11,002.9

YTD 2018 Parkway Pantai Parkway Pantai(TranslationDifference)

AcibademHoldings

AcibademHoldings

(TranslationDifference)

IMU Health Others YTD 2018

466.0

23.9

9.4

27.0

63.7 1.2

18.2 460.8

QTD 2017 Parkway Pantai Parkway Pantai(TranslationDifference)

AcibademHoldings

AcibademHoldings

(TranslationDifference)

IMU Health Others QTD 2018

Actual@ Constant

Currency

Parkway Pantai 4% 7%

Acibadem Holdings -25% 19%

IMU Health -5% -5%

IHH Group (Excl PLife REIT) -1% 15%

Q2'18 vs Q2'17

23

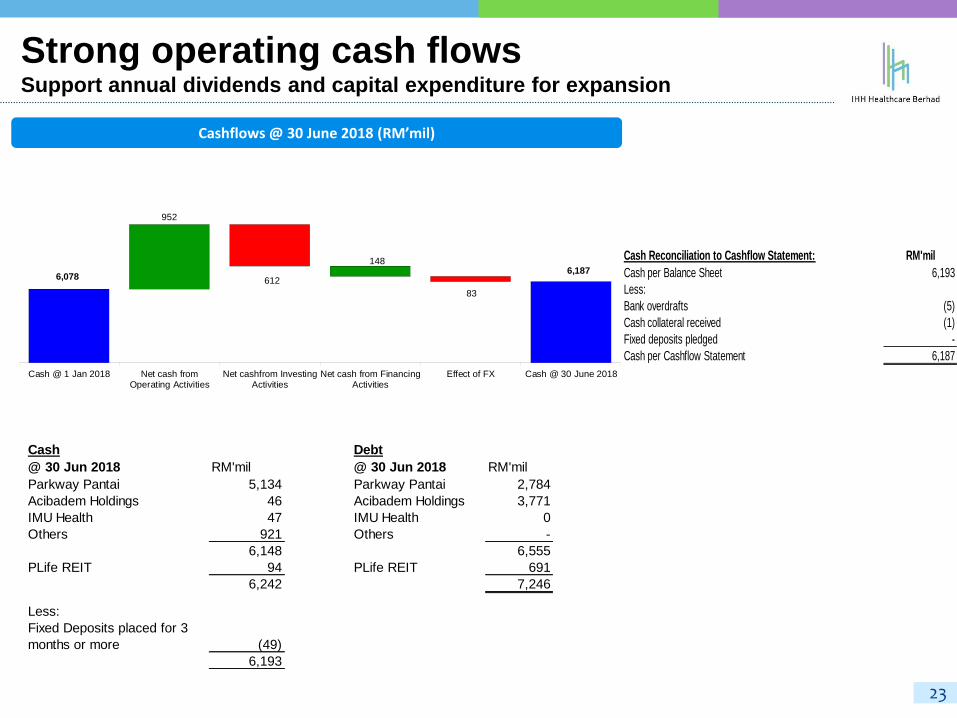

Strong operating cash flows Support annual dividends and capital expenditure for expansion

Cashflows @ 30 June 2018 (RM’mil)

Cash Reconciliation to Cashflow Statement: RM'mil

Cash per Balance Sheet 6,193

Less:

Bank overdrafts (5)

Cash collateral received (1)

Fixed deposits pledged -

Cash per Cashflow Statement 6,187

6,078

952

612

148

83

6,187

Cash @ 1 Jan 2018 Net cash fromOperating Activities

Net cashfrom InvestingActivities

Net cash from FinancingActivities

Effect of FX Cash @ 30 June 2018

Cash Debt

@ 30 Jun 2018 RM'mil @ 30 Jun 2018 RM'mil

Parkway Pantai 5,134 Parkway Pantai 2,784

Acibadem Holdings 46 Acibadem Holdings 3,771

IMU Health 47 IMU Health 0

Others 921 Others -

6,148 6,555

PLife REIT 94 PLife REIT 691

6,242 7,246

(49)

6,193

Less:

Fixed Deposits placed for 3

months or more