retail america: what [s ahead for your community

TRANSCRIPT

RETAIL AMERICA: What’s Ahead for Your CommunityICSC 2014 Wisconsin Alliance Program August 7, 2014

ABOUT THE RETAIL COACH

We have provided the research, the relationships and the strategies to achieve retail recruitment and development results that have helped over 250 communities throughout the U.S. become better, stronger places to live and work.

ABOUT THE RETAIL COACH

We develop and execute high-impact Retail Economic Development Plans:

• Corporate site selection with national retailers• Retail real estate brokerage• Retail leasing • Development/Redevelopment• Downtown retail revitalization• Land development with investment firms • Market analysis & land strategy

NATIONAL FOCUSCLIENT STATES 2014

AGENDA RETAIL & THE ECONOMY2014 RETAIL OUTLOOKRETAIL STRATEGIES FOR YOUR COMMUNITY

RETAIL & THE ECONOMY

Wisconsin’s Economic Growth Ranked 3rd in the Nation- Federal Reserve Bank of Philadelphia, 2013

Ranked 5th for “Top US States for New Manufacturing Jobs”- CNBC

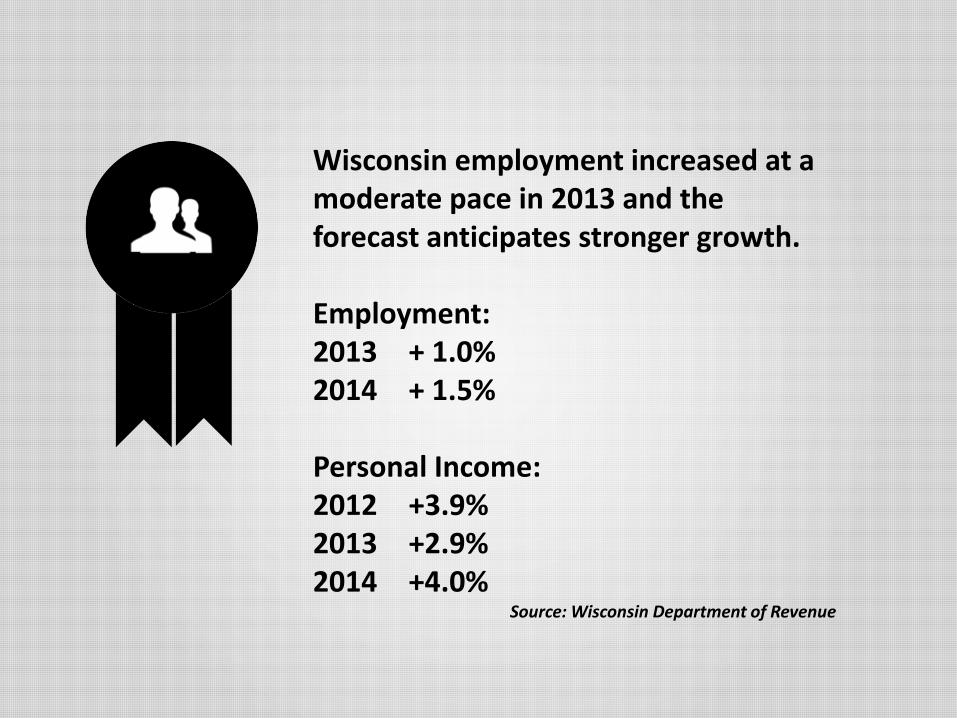

Wisconsin employment increased at a moderate pace in 2013 and the forecast anticipates stronger growth.

Employment:2013 + 1.0% 2014 + 1.5%

Personal Income:2012 +3.9% 2013 +2.9% 2014 +4.0%

Source: Wisconsin Department of Revenue

JOB GROWTH

Wisconsin's Unemployment Rate Declines to 5.7%...

Lowest since 2008

+ 38,100 JobsSince June 2013

Source: U.S. Bureau of Labor Statistics

Median Sales Prices June 2014 $145,000 +3.6%June 2013 $140,000

Source: Wisconsin Realtors Association

WISCONSIN HOME PRICES INCREASING;SALES INCREASE IN JUNE

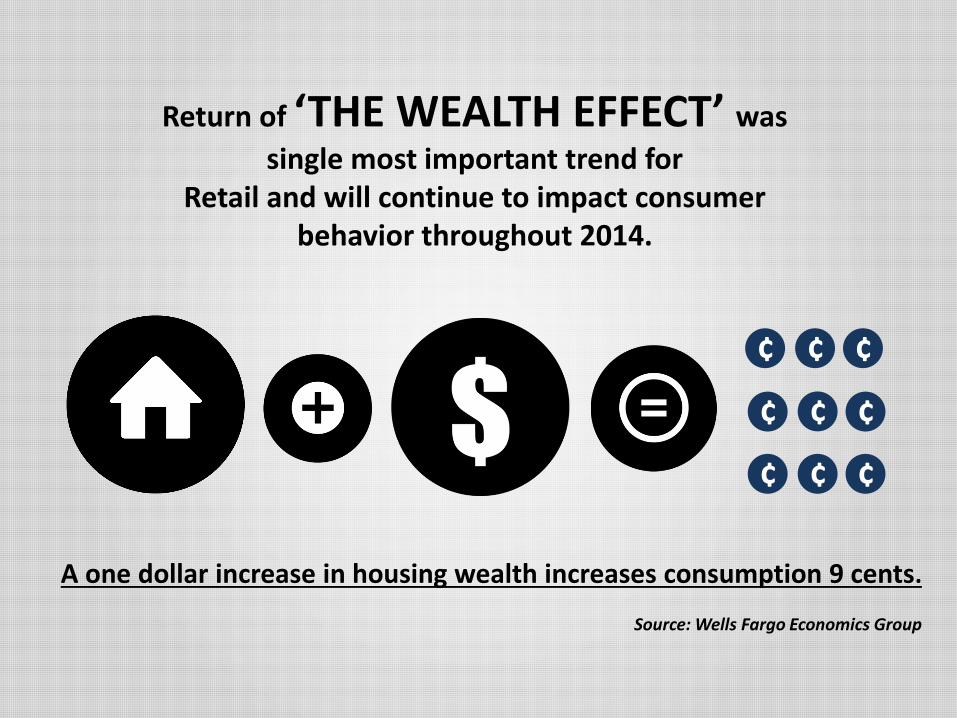

Return of ‘THE WEALTH EFFECT’ was

single most important trend for Retail and will continue to impact consumer

behavior throughout 2014.

A one dollar increase in housing wealth increases consumption 9 cents.

Source: Wells Fargo Economics Group

¢ ¢ ¢

¢ ¢ ¢

¢ ¢ ¢

U.S. Retail Sales in May Beat Expectations +4.4%

Level Off in June, Showing Continued Caution, Despite Job Growth +0.2%

Consumer Confidence Hit Highest Level in June since January 2008 85.2

High-End and Off-Price Retailers Remain Resilient

Source: Thomson Reuters/University of Michigan index

CONSUMER SPENDING IS INCREASING MODERATLY WITH IMPROVED CONSUMER CONFIDENCE

2014 RETAIL OUTLOOK

The retail industry’s evolution has accelerated over the last decade

Online retail sales will grow at compound annual rate of 10% from 2012-2017.

By 2017, the web will account for 10% of U.S. retail sales.

Smartphones/tablets account for 25% of those online sales.

Source: Forrester Research

RETAIL CONTINUES TO EVOLVE

POPULATION SHIFT BACK TO URBAN CENTERS PARTICULARLY AMONG GEN Y AGE GROUPS

CONVENIENCE IS A PRIORITY FOR YOUNG PROFESSIONALS

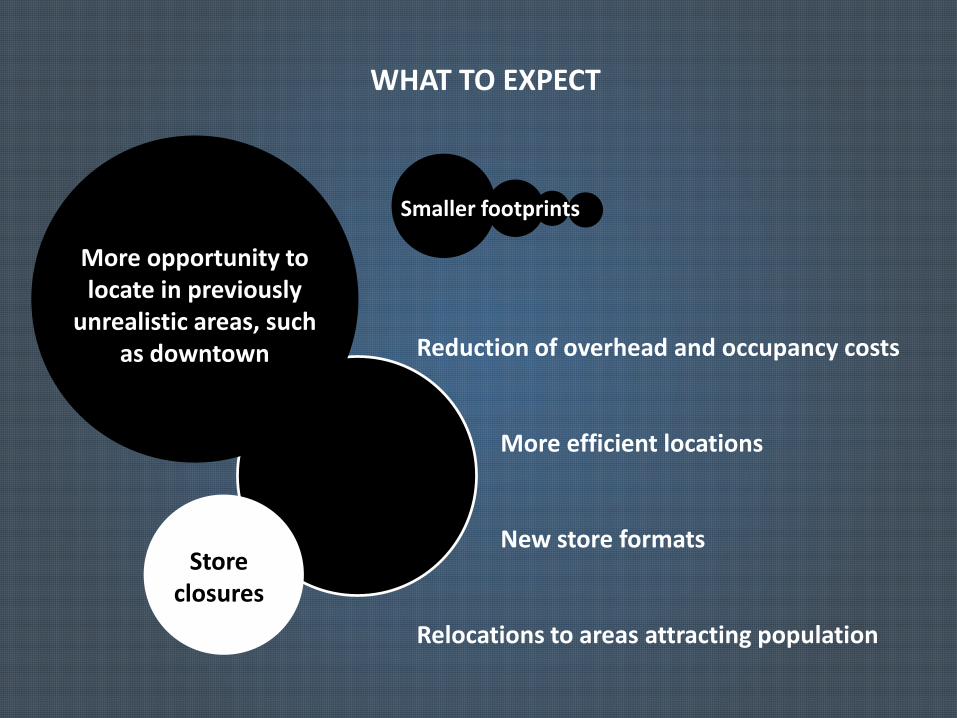

WHAT TO EXPECT

Reduction of overhead and occupancy costs

More efficient locations

New store formats

Relocations to areas attracting population

growth

More opportunity to locate in previously

unrealistic areas, such as downtown

Store closures

Smaller footprints

WHAT TO EXPECT

Continued emphasis on growth has led to fierce competition for prime retail space; this is expected to increase in 2014.

Competition in the casual restaurant segment is particularly intense.

Retail opportunities are less available than in the past 5 years.

POPULATION/RETAIL EXPOSURERETAIL EXPOSURE BY REGION 2013

Source: Cassidy Turley Research

POPULATION: 4.4%RETAIL EXPOSURE: 4.0%

POPULATION: 18.0%RETAIL EXPOSURE: 16.0%

POPULATION: 21.4%RETAIL EXPOSURE: 17.0%

POPULATION: 11.6%RETAIL EXPOSURE: 11%

POPULATION: 17.7%RETAIL EXPOSURE: 18.0%

POPULATION: 25.0%RETAIL EXPOSURE: 33.0%

OVERLOOKED OPPORTUNITY

Home equity lines of credit are the initial line of funding for most (an estimated 75%) of these start-ups.

We will see small business creation gradually accelerating over the next 24 months.

Most important economic trend impacting mom-and-pop demand in smaller communities is the return of housing appreciation.

WHO’S EXPANDING IN 2014

2 BASIC FACTORS IMPACTING RETAILER DEMAND/EXPANSION

THE ECONOMYStrong activity on the far ends

of the economic spectrum

Discount --- Luxury

1 2

ENCROACHMENT OF E-COMMERCE

TRACKING 3,000 NATIONAL RETAIL & RESTAURANT CHAINS

5% Increase in planned growth in 2014 from 2013.

Approximately 43% of growth is from restaurants.

Tenant mixes at local shopping centers become increasingly food-based.

.

RETAIL GROWTH 2014

• Fitness/Health/Spa Concepts

• Drug Stores• Thrift Stores• Grocery (Smaller Format)

-Discount-Ethnic-Organic-Upscale

• Fast Food• Fast Casual Dining• Automotive• Discounters• Dollar Stores• Off-Price Apparel• Pet Supplies• Sporting Goods• Wireless Stores

Source: Cassidy Turley Research

RETAIL CONTRACTION 2014

• Bookstores• Video Stores• Do-It-Yourself Home Stores• Mid-Priced Apparel• Mid-Priced Grocery• Office Supplies• Stationary/Gift Shops• Shipping/Postal Stores

Source: Cassidy Turley Research

RETAIL STRATEGIES FOR YOUR COMMUNITY

THE NEW ECONOMIC DEVELOPMENT

“…the application of public resources to stimulate private investment with an emphasis on new technologies, sustainability and local communities.”

- TIP Strategies

RETAIL Must Be A Component Of Your Community’s Comprehensive Economic Development Strategy

CAUTION PREVAILS

Despite an improving economy, recession-weary retailers remain cautious. The retailers and site selectors who survived the recession are taking an analytical, data-driven approach when choosing locations for new stores and restaurants.

Retailers are looking for the sure thing.

RETAILERS ARE LOOKING FOR OPPORTUNITIES – NOT JUST SITES

Understand the retailer’s essential location factors:

• Visibility• Accessibility• Regional exposure• Population density• Population growth• Operational convenience• Safety and security• Adequate parking• Adequate signage

UNDERSTAND THAT COMMUNITY DEVELOPMENT PRECEDES ECONOMIC DEVELOPMENT

Understand that first impressions are important

• Community appearance• Pride of ownership (residential and commercial)• Functional infrastructure• Evidence of crime• Codes and code enforcement• Downtown vitality

PEOPLE WANT TO LOCATE IN COMMUNITIES THAT OFFER EVERYTHING

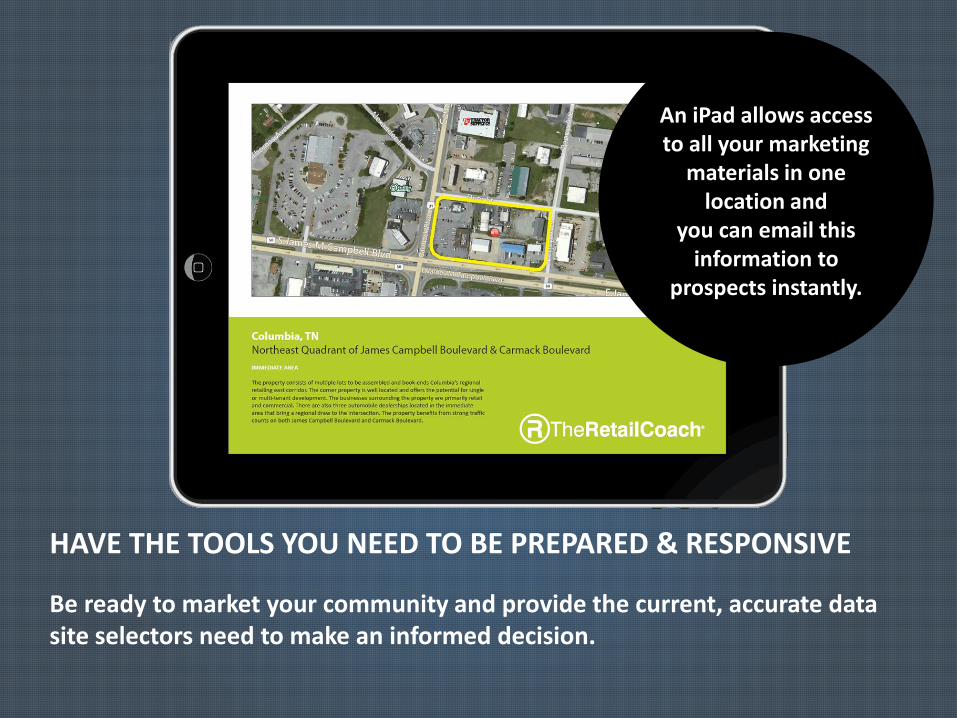

HAVE THE TOOLS YOU NEED TO BE PREPARED & RESPONSIVE

Be ready to market your community and provide the current, accurate data site selectors need to make an informed decision.

An iPad allows access to all your marketing

materials in one location and

you can email this information to

prospects instantly.

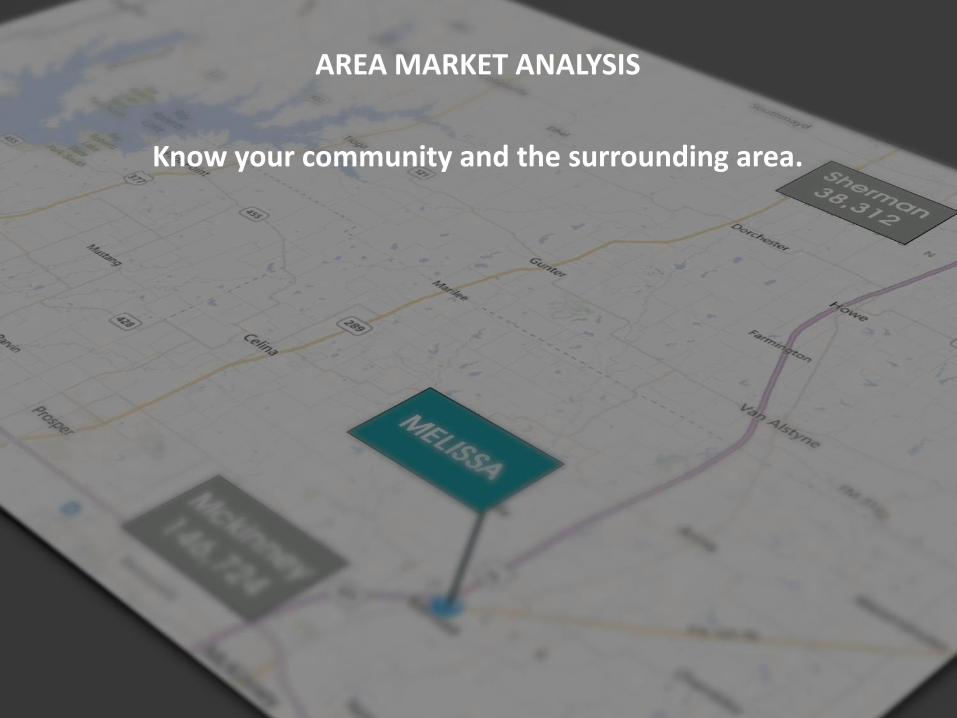

AREA MARKET ANALYSIS

Know your community and the surrounding area.

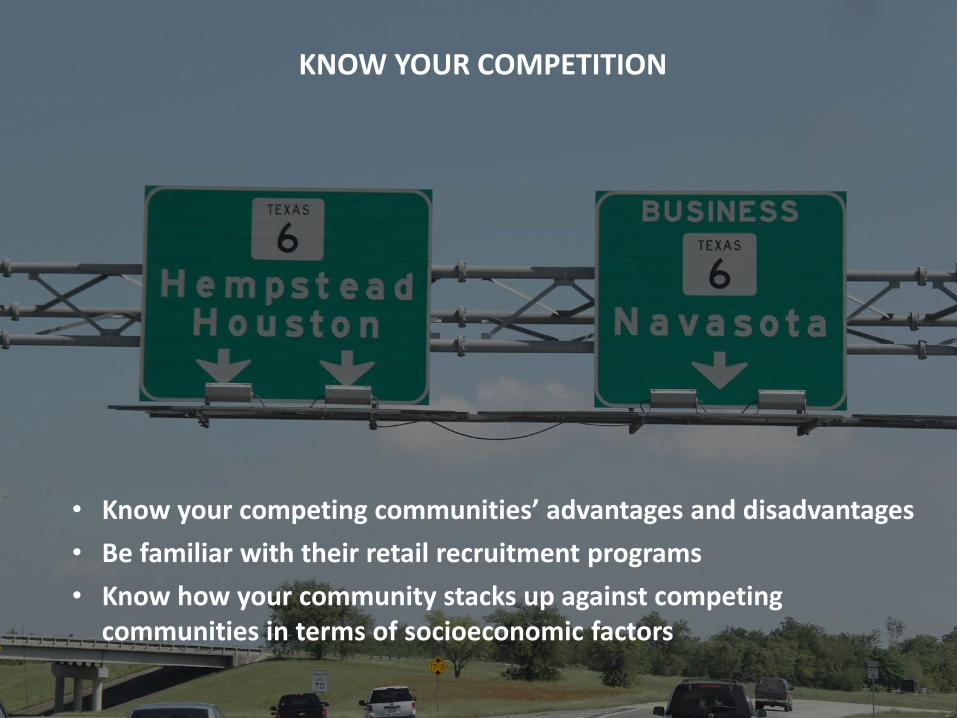

KNOW YOUR COMPETITION

• Know your competing communities’ advantages and disadvantages

• Be familiar with their retail recruitment programs

• Know how your community stacks up against competing communities in terms of socioeconomic factors

BE PROACTIVE

Perform a SWOT Analysis of your community from a retailer’s perspective.

• Know your advantages and understand your challenges

• Address challenges by coming up with an actionable “to do” plan based on priority

• Retailers, developers and/or investors want to know that something is being done

• Retailers, developers and/or investors look for stable or improving communities where their risk is minimized

KNOW WHERE EXISTING RETAIL IS LOCATED

KNOW YOUR RETAIL TRADE AREA SIZE

• The largest distance consumers are willing to travel to purchase retail goods and services

• Always greater than your community population

• Sell your community as a retail trade area population

CITY LIMITS

RETAIL TRADE AREA

RETAIL TRADE AREA DETERMINATION

PRIMARY RETAIL TRADE AREA Consumers likely to shop community retailers more than once per week.

SECONDARY RETAIL TRADE AREAConsumers likely to shop community retailers once per week, once every two weeks.

RETAIL TRADE AREA DETERMINATION

LICENSE PLATE SURVEY

KNOW YOUR RETAIL TRADE AREA DEMOGRAPHICS

• With an emphasis on average and median household incomes.

• The return of ‘the wealth effect’ is the single most important trend to watch for retail.

KNOW YOUR RETAIL TRADE AREA PSYCHOGRAPHICS

Consumer values and lifestyles drive a desire for particular products/services.

PSYCHOGRAPHICS

LIFESTYLE SEGMENTATION

All U.S. households fall into 1 of 68 lifestyle segments.

Divide your market into groups of consumers with similar demographic characteristics, lifestyles, purchase behaviors and work patterns.

IDENTIFY YOUR RETAIL TRADE AREA SALES GAP/OPPORTUNITY

Identifies sales leakage occurring when residents dine or purchase products outside of your community.

RETAIL GAP/OPPORTUNITY ANALYSIS

Measures consumer demand and retail opportunity.

Analyzes retail categories to identify which sectors have retail leakages and which have retail surpluses.

KNOW THE WORKFORCE/DAYTIME POPULATION

Particularly important for restaurants.

CONSUMER/COLLEGE STUDENT SPENDING SURVEY

• Purchasing habits/frequency

• % of purchases in community

• Where else do you shop/frequency

• Retailer-type preferences

• Specific retailer preferences

• Monthly retail expenditures

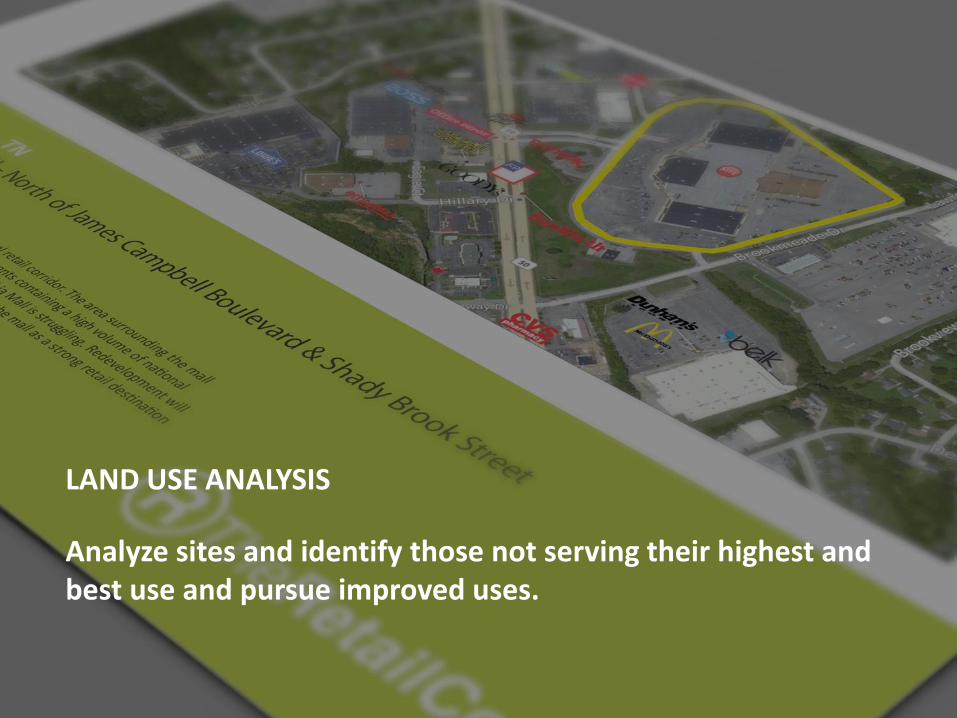

LAND USE ANALYSIS

Analyze sites and identify those not serving their highest and best use and pursue improved uses.

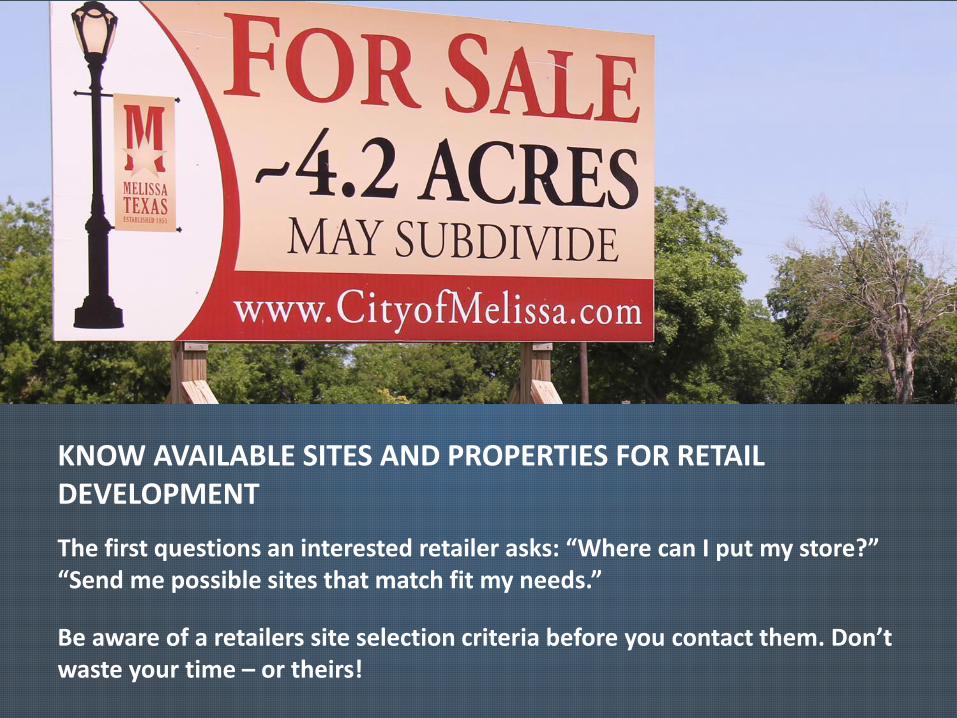

KNOW AVAILABLE SITES AND PROPERTIES FOR RETAIL DEVELOPMENT

The first questions an interested retailer asks: “Where can I put my store?” “Send me possible sites that match fit my needs.”

Be aware of a retailers site selection criteria before you contact them. Don’t waste your time – or theirs!

RETAILER MATCHING & RECRUITMENT

A community must utilize:

• Area Market Analysis

• Community Market Analysis

• Retail Trade Area Demographic Profile

• Dominant Lifestyle Profiles

• Retail Gap/Opportunity Analysis findings

• Available Properties

• Internal retailer and restaurant database

Contact the targeted retailers and developers to determine the level of interest they may have in your community.

COMMUNITY MARKETING

• Retail Market Profile

• Retail - Specific Brochure

• Community Video

• Retail - Specific Website

• Property Visuals

• Developer Packaging

RETAILER FEASIBILITY STUDY

HAVE A PRO-BUSINESS ATTITUDE AND DEVELOPMENT PROCESS

Retailers go where it’s easy to do business.

BE INNOVATIVE!

Interactive Mapping and Demographic Data

BE INNOVATIVE!

Data Driven Retail Website with Available Retail Site Locations and Interactive Data Visualization.

DON’T OVERLOOK YOUR EXISTING RETAILERS

• Retail retention is vital to the long-term economic strength of your community.

• The success of your existing retailers leads to increased sales tax revenue as well as job growth.

• These businesses are ambassadors who present a positive image for new retail and business recruitment.

BE SEEN AT ICSC EVENTS

PRACTICE RECRUITMENT PRIORITIES AND PROCESS

Sell your community first, then sell the sites.

Goal: Get the retailer to the community.

TAKE A LONG-TERM APPROACH

Retail recruitment is a process, not an event.

Your elected and staff leadership must commit to a long-term Retail Economic Development Plan tied to your vision for the community and its forecast for population growth and build-out.

CORPORATE OFFICEPh. 662.844.2155Fx. 662.844.2738

DALLAS OFFICEPh. 662.231.9078

AUSTIN OFFICEPh. 662.231.0608

800.851.0962