retail cities asia pacific: the fast fashion retail race

TRANSCRIPT

Retail Cities Asia Pacific

The Fast Fashion Retail Race

April 2015

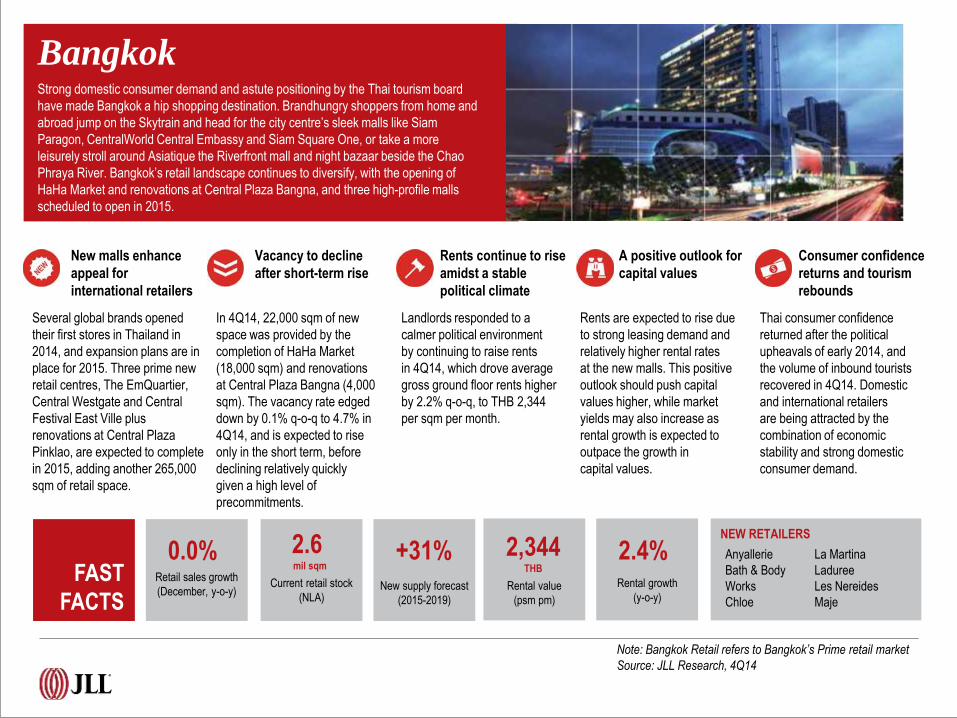

Bangkok Strong domestic consumer demand and astute positioning by the Thai tourism board

have made Bangkok a hip shopping destination. Brandhungry shoppers from home and

abroad jump on the Skytrain and head for the city centre’s sleek malls like Siam

Paragon, CentralWorld Central Embassy and Siam Square One, or take a more

leisurely stroll around Asiatique the Riverfront mall and night bazaar beside the Chao

Phraya River. Bangkok’s retail landscape continues to diversify, with the opening of

HaHa Market and renovations at Central Plaza Bangna, and three high-profile malls

scheduled to open in 2015.

New malls enhance

appeal for

international retailers

Several global brands opened

their first stores in Thailand in

2014, and expansion plans are in

place for 2015. Three prime new

retail centres, The EmQuartier,

Central Westgate and Central

Festival East Ville plus

renovations at Central Plaza

Pinklao, are expected to complete

in 2015, adding another 265,000

sqm of retail space.

Vacancy to decline

after short-term rise

In 4Q14, 22,000 sqm of new

space was provided by the

completion of HaHa Market

(18,000 sqm) and renovations

at Central Plaza Bangna (4,000

sqm). The vacancy rate edged

down by 0.1% q-o-q to 4.7% in

4Q14, and is expected to rise

only in the short term, before

declining relatively quickly

given a high level of

precommitments.

Rents continue to rise

amidst a stable

political climate

Landlords responded to a

calmer political environment

by continuing to raise rents

in 4Q14, which drove average

gross ground floor rents higher

by 2.2% q-o-q, to THB 2,344

per sqm per month.

A positive outlook for

capital values

Rents are expected to rise due

to strong leasing demand and

relatively higher rental rates

at the new malls. This positive

outlook should push capital

values higher, while market

yields may also increase as

rental growth is expected to

outpace the growth in

capital values.

Consumer confidence

returns and tourism

rebounds

Thai consumer confidence

returned after the political

upheavals of early 2014, and

the volume of inbound tourists

recovered in 4Q14. Domestic

and international retailers

are being attracted by the

combination of economic

stability and strong domestic

consumer demand.

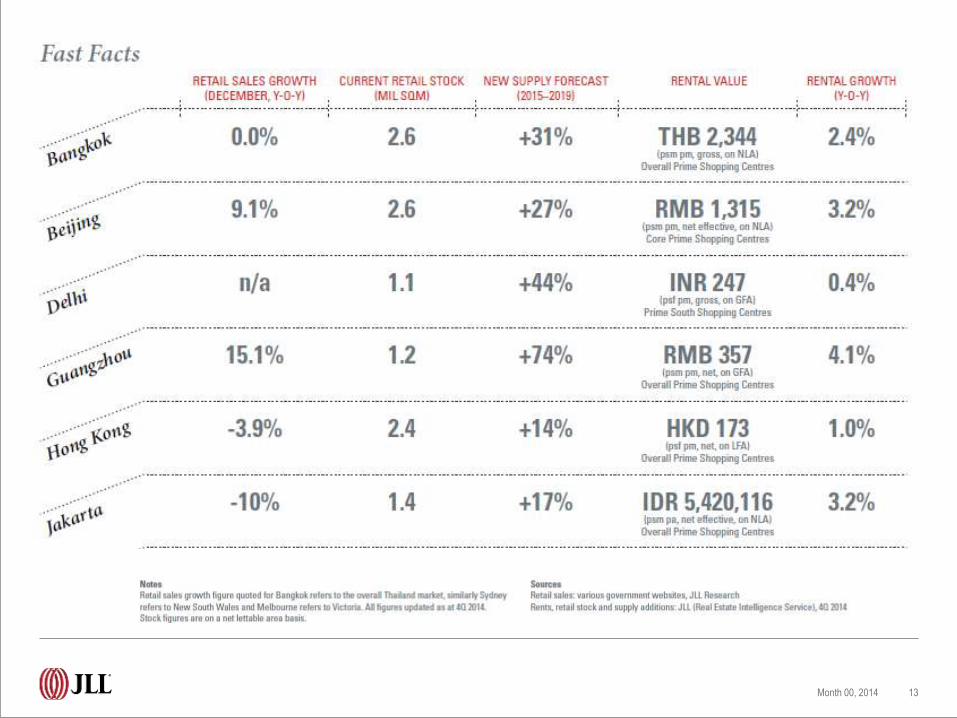

0.0% 2.6 mil sqm

+31% 2,344THB

2.4%

Note: Bangkok Retail refers to Bangkok’s Prime retail market

Source: JLL Research, 4Q14

FAST

FACTSCurrent retail stock

(NLA)New supply forecast

(2015-2019)

Rental value

(psm pm)

Rental growth

(y-o-y)

NEW RETAILERS

Anyallerie

Bath & Body

Works

Chloe

La Martina

Laduree

Les Nereides

Maje

Retail sales growth

(December, y-o-y)

Beijing The Chinese capital has emerged as a sophisticated retail centre since its pre-2008 Olympic

urban makeover. Several large mixed-use developments feature contemporary malls in a city

once famed for its open-air markets. Today, Beijing is a coveted location for international

retailers, with glitzy venues like Oriental Plaza, China World Mall and SKP appealing to both

brands and shoppers. Designer boutiques plus high-end dining and entertainment draw a hip,

fashion-conscious clientele to Taikoo Li Sanlitun and Parkview Green, while Indigo in

Jiuxianqiao, Solana in the Third Embassy Area and Wangfujing Street are popular with

families.

New openings boost

super-regional market

Five new retail centres opened

in Beijing in 4Q14, with four

– Wanda Tongzhou, Paradise

Walk, Livat and Beijing One

– being located in suburban

areas beyond the Fifth Ring

Road. By adding 740,000 sqm

of space, these new openings

represent a turning point in the

suburban super-regional mall

boom in Beijing.

Only new downtown

mall opens with 90%

occupancy

Located several blocks from

the landmark Taikoo Li mall

in Sanlitun, Yongli Mall was

the city centre’s only major

opening in 4Q14. Its ground

floor features dining and cafes

plus a multi-brand luxury store.

Niche designers

expand despite

luxury slowdown

Amid slower growth in the

luxury market, Vera Wang

opened her first Beijing

store at Taikoo Li North. The

store marks the designer’s

second location in China after

Shanghai.

Slower rental growth

may be the new

normal

Strong competition in key

areas resulted in rental growth

remaining subdued in 4Q14.

Urban chain-linked rents

increased by just 1.0% q-o-q,

similar to the previous quarter,

representing a new normal of

slower rental growth. Market

yields were also unchanged,

and cautious investor

sentiment resulted in no major

sales being transacted.

Vacancy slightly

declines

The core vacancy rate

declined slightly to 4.9% in

4Q14, from 5.4% in 3Q14, as

some properties upgraded

their tenant mixes and helped

brands enter new projects or

expand their market presence.

9.1% 2.6mil sqm

+27% 1,315 RMB

3.2%

Note: Beijing Retail refers to Beijing’s Urban Prime retail market.

Source: JLL Research, 4Q14

FAST

FACTSCurrent retail stock

(NLA)New supply forecast

(2015-2019)

Rental value

(psm pm)

Rental growth

(y-o-y)

NEW RETAILERS

Cesare Casadei

Marc O’Polo

Nicholas Kirkwood

Old Navy

Retail sales growth

(December, y-o-y)

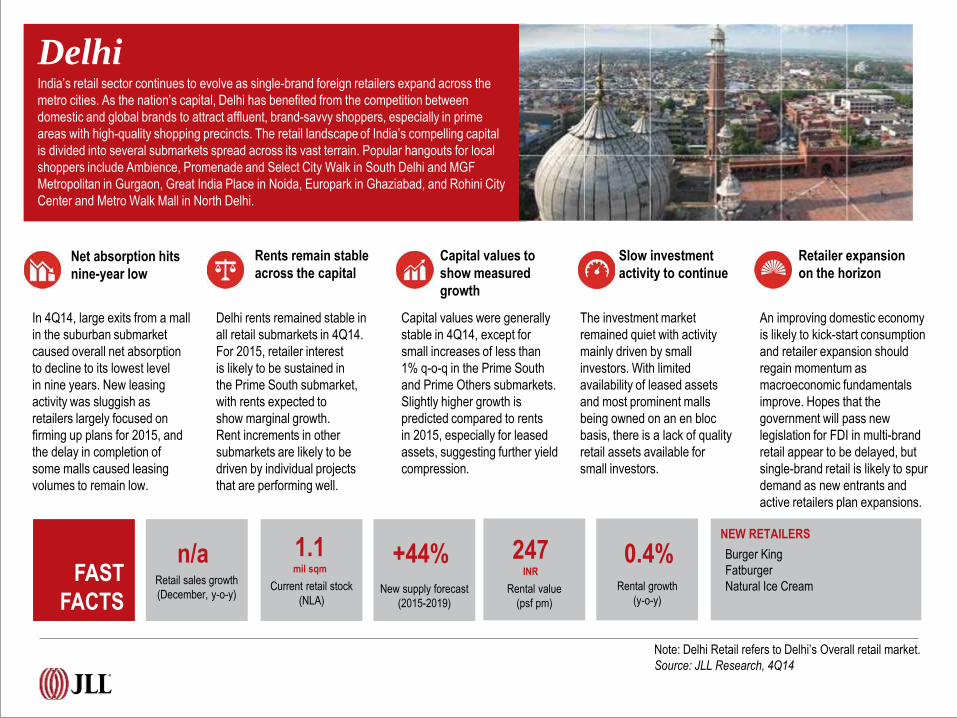

Delhi India’s retail sector continues to evolve as single-brand foreign retailers expand across the

metro cities. As the nation’s capital, Delhi has benefited from the competition between

domestic and global brands to attract affluent, brand-savvy shoppers, especially in prime

areas with high-quality shopping precincts. The retail landscape of India’s compelling capital

is divided into several submarkets spread across its vast terrain. Popular hangouts for local

shoppers include Ambience, Promenade and Select City Walk in South Delhi and MGF

Metropolitan in Gurgaon, Great India Place in Noida, Europark in Ghaziabad, and Rohini City

Center and Metro Walk Mall in North Delhi.

Net absorption hits

nine-year low

In 4Q14, large exits from a mall

in the suburban submarket

caused overall net absorption

to decline to its lowest level

in nine years. New leasing

activity was sluggish as

retailers largely focused on

firming up plans for 2015, and

the delay in completion of

some malls caused leasing

volumes to remain low.

Rents remain stable

across the capital

Delhi rents remained stable in

all retail submarkets in 4Q14.

For 2015, retailer interest

is likely to be sustained in

the Prime South submarket,

with rents expected to

show marginal growth.

Rent increments in other

submarkets are likely to be

driven by individual projects

that are performing well.

Capital values to

show measured

growth

Capital values were generally

stable in 4Q14, except for

small increases of less than

1% q-o-q in the Prime South

and Prime Others submarkets.

Slightly higher growth is

predicted compared to rents

in 2015, especially for leased

assets, suggesting further yield

compression.

Slow investment

activity to continue

The investment market

remained quiet with activity

mainly driven by small

investors. With limited

availability of leased assets

and most prominent malls

being owned on an en bloc

basis, there is a lack of quality

retail assets available for

small investors.

Retailer expansion

on the horizon

An improving domestic economy

is likely to kick-start consumption

and retailer expansion should

regain momentum as

macroeconomic fundamentals

improve. Hopes that the

government will pass new

legislation for FDI in multi-brand

retail appear to be delayed, but

single-brand retail is likely to spur

demand as new entrants and

active retailers plan expansions.

n/a 1.1mil sqm

+44% 247INR

0.4%

Note: Delhi Retail refers to Delhi’s Overall retail market.

Source: JLL Research, 4Q14

FAST

FACTS

NEW RETAILERS

Burger King

Fatburger

Natural Ice CreamRetail sales growth

(December, y-o-y)Current retail stock

(NLA)New supply forecast

(2015-2019)

Rental value

(psf pm)

Rental growth

(y-o-y)

Guangzhou China’s southern megacity continues to benefit from ongoing urban redevelopment catalysed

by hosting the 2010 Asian Games. Upgraded city infrastructure includes state-of-the-art new

malls in prime areas. The Zhujiang New Town CBD beside the Pearl River entices global and

local retailers because of its luxury hotels, offices, dining and entertainment. The Mall of the

World is Guangzhou’s largest subterranean mall, Rock Square in Haizhu district is a

commercial and residential property with a large shopping mall, and TaiKoo Hui and

Panyu Wanda Plaza are mixed-use developments featuring a shopping mall, office towers, a

hotel and residences.

F&B and fast fashion

retailers continue to

be the most active

Slower retail sales increased

diligence among retailers

about selecting new store

locations. F&B and fast fashion

continued to drive leasing

activity in 4Q14. New mid-tier

international retailers to enter

the market included Victoria’s

Secret, GAP and Etude House.

Wanda adds to city’s

retail stock

A slow quarter for new malls

saw Panyu Wanda Plaza,

the third Wanda Plaza in

Guangzhou, open in early

November with a a net

lettable area of 49,500 sqm. Its

completion increased the city’s

total prime retail stock to NLA

1.2 million sqm.

Mature malls to drive

rental growth

Positive rental growth in mature

malls was achieved through

tenant and trade mix adjustments.

However, the landlords of

underperforming malls softened

their rental stance to combat

vacancy pressures. As a result,

overall rents grew 1.0% q-o-q to

RMB 357.5 per sqm per month in

4Q14. Established malls should

continue to drive overall rental

growth of between 3–4% in 2015.

Capital values

remain stable

Investment market sentiment

was largely unchanged in 4Q14,

with potential buyers concerned

about a possible oversupply in

retail space. Consequently, capital

values held broadly stable.

Weak expansion

demand to continue

Slowing economic growth and

competition from e-commerce

are likely to depress expansion

demand and tighten rental

budgets. New-to-market

international brands, F&B

operators and other services

based retailers are expected to

continue to expand, albeit

cautiously.

15.1% 1.2mil sqm

+74% 357 RMB

4.1%

Note: Guangzhou Retail refers to Guangzhou’s Overall Prime retail market.

Source: JLL Research, 4Q14

FAST

FACTS

NEW RETAILERS

Ay Lazzaro

Bape

Chris Christy

Etude House

Gap

Givenchy

Holland & Barrett

Kenzo

Current retail stock

(NLA)New supply forecast

(2015-2019)

Rental value

(psm pm)

Rental growth

(y-o-y)

Retail sales growth

(December, y-o-y)

Hong Kong Self titled as Asia’s World City, Hong Kong is a dynamic international shopping destination.

Global fashion stores, luxury brand flagships and innovative food and beverage outlets

compete for prestige sites that attract high-spending locals and visitors, particularly from

Mainland China. Shopping hotspots include the impressive Pacific Place, Harbour City, Times

Square, The Landmark and ifc, plus the coveted street-front stores along Queen’s Road

Central and Canton Road in Tsimshatsui. Ongoing demand for retail space has resulted

in several brands hot-footing into non-core shopping areas, such as Shatin, Tuen Mun and

Tsuen Wan.

Rental correction in

some fringe streets

in core areas

The changing shopping patterns

of Mainland Chinese visitors

combined with the sustained

disruption caused by the

Occupy Hong Kong protest put

further pressure on rents.

Coupled with demand dwindling

among some big ticket item

retailers, rental corrections were

seen in some fringe streets in

core locations during 4Q14.

Mixed leasing

response to

Occupy protests

The leasing impact of the protests

was mixed during 4Q14. Some

retailers were still keen on leasing

shops in areas less affected by

the protests, such as Italian lingerie

retailer La Perla, which pre-leased

all four levels of a new

development on Russell Street.

Other retailers used the protests as

a bargaining chip to negotiate for

lower rents, especially for shops in

core locations whose leases

expired during the quarter.

Tai Wai Station

project awarded

The Tai Wai station project was

awarded to New World

Development for HKD 2.9

billion. Upon completion, the

project will provide a 650,000

sq ft shopping centre, with

expected completion in 2018.

Investors target

undervalued assets

in non-core areas

Investors continued to target

undervalued properties with

upgrading opportunities in 4Q14.

Due to the already low fields for

properties in core locations,

investors were unwilling to chase

yields down further, leading to a

quarterly fall in capital values for

high street shops.

Stronger sales growth

predicted for 2015

Retail sales should post stronger

growth in 2015, although the anti-

corruption drive and the changing

shopping patterns of Chinese

shoppers are downside risks.

International retailers remain keen to

open stores given Hong Kong’s

mature retail market and growth in

tourism arrivals, which exceeded 60

million for the first time in 2014, but

they will likely adopt a conservative

approach in leasing negotiations.

-3.9% 2.4 mil sqm

+14% 173 HKD

1.0%

Note: Hong Kong Retail refers to Hong Kong’s Overall Prime Shopping Centre and High Street retail markets.

Source: JLL Research, 4Q14

FAST

FACTS

NEW RETAILERS

Castaner

Jnby

Kumamon

Le Relais de

L’Entrecote

Moomin Café

Orobianco

Proenza Schouler

Rag & Bone New York

Valextra

Retail sales growth

(December, y-o-y)Current retail stock

(NLA)New supply forecast

(2015-2019)

Rental value

(psf pm)

Rental growth

(y-o-y)

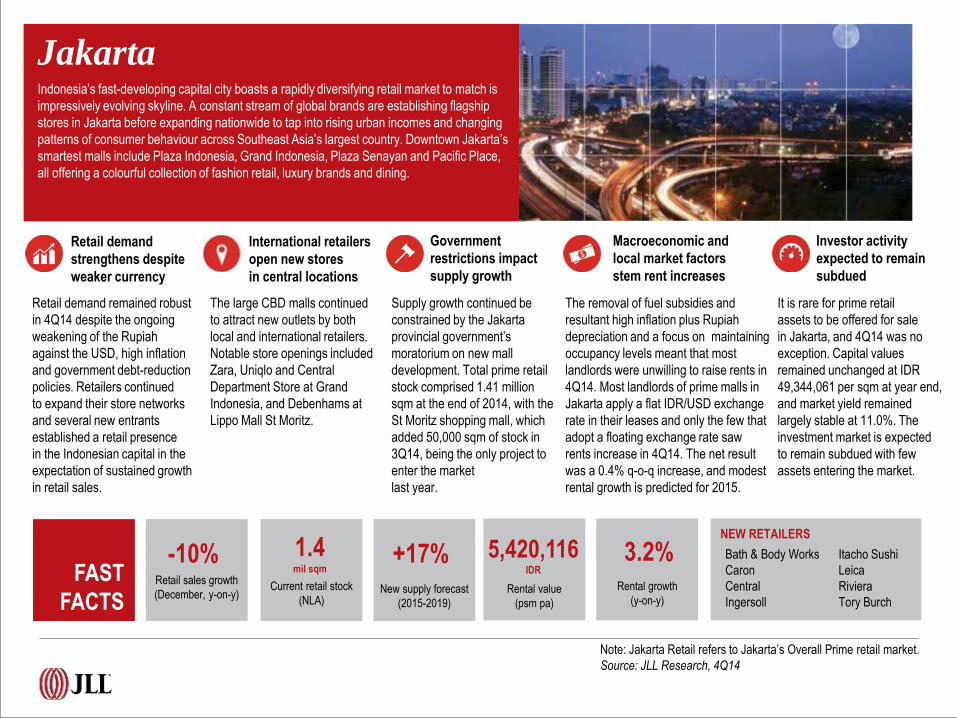

Jakarta Indonesia’s fast-developing capital city boasts a rapidly diversifying retail market to match is

impressively evolving skyline. A constant stream of global brands are establishing flagship

stores in Jakarta before expanding nationwide to tap into rising urban incomes and changing

patterns of consumer behaviour across Southeast Asia’s largest country. Downtown Jakarta’s

smartest malls include Plaza Indonesia, Grand Indonesia, Plaza Senayan and Pacific Place,

all offering a colourful collection of fashion retail, luxury brands and dining.

Retail demand

strengthens despite

weaker currency

Retail demand remained robust

in 4Q14 despite the ongoing

weakening of the Rupiah

against the USD, high inflation

and government debt-reduction

policies. Retailers continued

to expand their store networks

and several new entrants

established a retail presence

in the Indonesian capital in the

expectation of sustained growth

in retail sales.

International retailers

open new stores

in central locations

The large CBD malls continued

to attract new outlets by both

local and international retailers.

Notable store openings included

Zara, Uniqlo and Central

Department Store at Grand

Indonesia, and Debenhams at

Lippo Mall St Moritz.

Government

restrictions impact

supply growth

Supply growth continued be

constrained by the Jakarta

provincial government’s

moratorium on new mall

development. Total prime retail

stock comprised 1.41 million

sqm at the end of 2014, with the

St Moritz shopping mall, which

added 50,000 sqm of stock in

3Q14, being the only project to

enter the market

last year.

Macroeconomic and

local market factors

stem rent increases

The removal of fuel subsidies and

resultant high inflation plus Rupiah

depreciation and a focus on maintaining

occupancy levels meant that most

landlords were unwilling to raise rents in

4Q14. Most landlords of prime malls in

Jakarta apply a flat IDR/USD exchange

rate in their leases and only the few that

adopt a floating exchange rate saw

rents increase in 4Q14. The net result

was a 0.4% q-o-q increase, and modest

rental growth is predicted for 2015.

Investor activity

expected to remain

subdued

It is rare for prime retail

assets to be offered for sale

in Jakarta, and 4Q14 was no

exception. Capital values

remained unchanged at IDR

49,344,061 per sqm at year end,

and market yield remained

largely stable at 11.0%. The

investment market is expected

to remain subdued with few

assets entering the market.

-10% 1.4mil sqm

+17% 5,420,116IDR

3.2%

Note: Jakarta Retail refers to Jakarta’s Overall Prime retail market.

Source: JLL Research, 4Q14

FAST

FACTS

NEW RETAILERS

Bath & Body Works

Caron

Central

Ingersoll

Itacho Sushi

Leica

Riviera

Tory Burch

Retail sales growth

(December, y-on-y)Current retail stock

(NLA)New supply forecast

(2015-2019)

Rental value

(psm pa)

Rental growth

(y-on-y)

Melbourne Melbourne is famed for its eclectic dining and year-round calendar of major sporting events

and cultural festivals, and is emerging as a heartland of Australian fashion and design.

Australia’s second most populous city also boasts a vibrant retail scene, ranging from the

artisans of Flinders Lane, jewellery shops on Crossley Street and the fashionable new

Emporium Melbourne mall on Lonsdale Street to the high-end stores along Chapel Street and

Collins Street, Bourke Street Mall and Chadstone the Fashion Capital, the southern

hemisphere’s largest shopping centre. Impressive suburban developments beyond include

Highpoint Shopping Centre and Craigieburn Central.

Consumer spending

growth varies across

retail segments

Retail spending growth continued to

accelerate, rising to 6.2% y-o-y in

November 2014, with Victoria ranked

Australia’s third strongest state for retail

spend growth, after New South Wales

and Tasmania. Food, household goods

and cafes, restaurants and take-away

food retailing drove the rebound, while

growth in clothing, footwear and

personal accessories slowed in the

second half of the year.

International

retailers drive

leasing demand

Leasing markets continue to be

driven by new international retailers

who are expanding beyond the

CBD malls into regional shopping

centres. Redevelopments of major

shopping centres are facilitating

this trend, and demand from

domestic retailers is also likely to

increase in certain categories, led

by the improvement in trading

conditions.

Retail supply

declines as mall

completions slow

Three small projects totalling

19,600 sqm completed in 4Q14.

Supply completions declined

significantly in 2014 after

having risen steadily between

2010 and 2013. However, 2014

marked the low point for the

current construction cycle, and

completions are forecast to

gradually rise in 2015 and 2016.

Minimal annual

change in rents

While minor changes in rents

were recorded in 2014,

performance varied between

retail categories. The CBD,

bulky goods and in sub-regional

sub-sectors recorded a

moderate yearly rental uplift,

which contrasted with a modest

contraction in the regional and

neighbourhood sub-sectors.

Fundamentals

appear healthy

for 2015

The expansion of major

international retailers should

help to support leasing demand

and new developments, and

a modest level of new supply

combined with stronger retail

spending should result in a

modest recovery in rental growth

in 2015. Investors appear to

have priced in strong growth, as

reflected in the yield tightening

evident through 2014.

4.2% 2.6mil sqm

+10% 1,462 AUD

-0.5%

Note: Melbourne Retail refers to Melbourne’s Overall retail market.

Source: JLL Research, 4Q14

FAST

FACTS

NEW RETAILERS

Cos

Dior Perfume & Beauty

Zara HomeCurrent retail stock

(NLA)New supply forecast

(2015-2019)

Rental value

(psm pa)

Rental growth

(y-on-y)

Retail sales growth

(December, y-on-y)

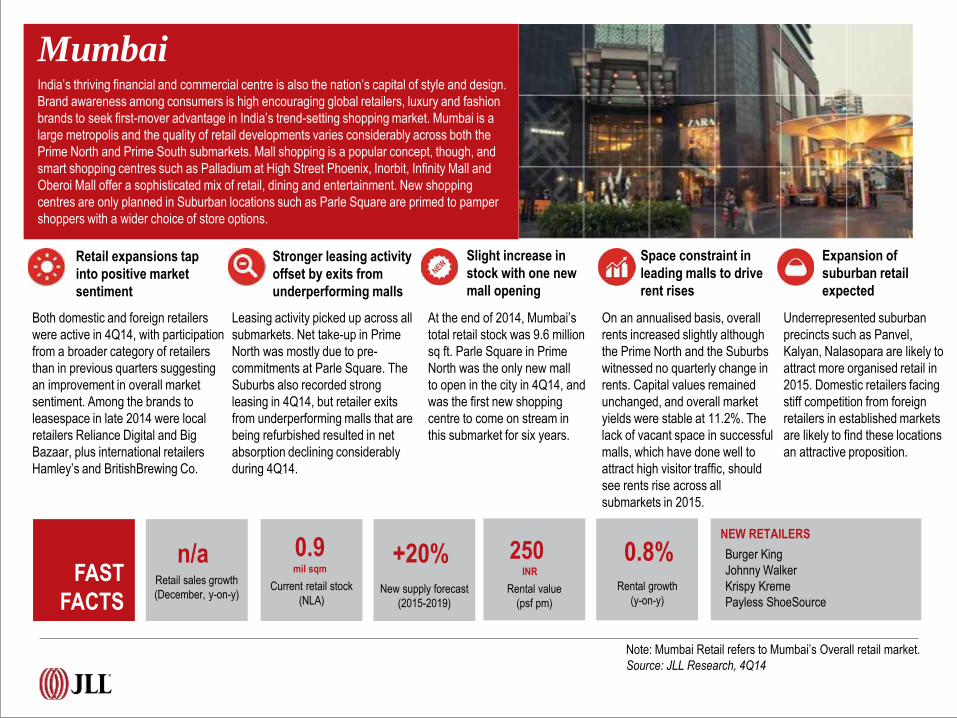

Mumbai India’s thriving financial and commercial centre is also the nation’s capital of style and design.

Brand awareness among consumers is high encouraging global retailers, luxury and fashion

brands to seek first-mover advantage in India’s trend-setting shopping market. Mumbai is a

large metropolis and the quality of retail developments varies considerably across both the

Prime North and Prime South submarkets. Mall shopping is a popular concept, though, and

smart shopping centres such as Palladium at High Street Phoenix, Inorbit, Infinity Mall and

Oberoi Mall offer a sophisticated mix of retail, dining and entertainment. New shopping

centres are only planned in Suburban locations such as Parle Square are primed to pamper

shoppers with a wider choice of store options.

Retail expansions tap

into positive market

sentiment

Both domestic and foreign retailers

were active in 4Q14, with participation

from a broader category of retailers

than in previous quarters suggesting

an improvement in overall market

sentiment. Among the brands to

leasespace in late 2014 were local

retailers Reliance Digital and Big

Bazaar, plus international retailers

Hamley’s and BritishBrewing Co.

Stronger leasing activity

offset by exits from

underperforming malls

Leasing activity picked up across all

submarkets. Net take-up in Prime

North was mostly due to pre-

commitments at Parle Square. The

Suburbs also recorded strong

leasing in 4Q14, but retailer exits

from underperforming malls that are

being refurbished resulted in net

absorption declining considerably

during 4Q14.

Slight increase in

stock with one new

mall opening

At the end of 2014, Mumbai’s

total retail stock was 9.6 million

sq ft. Parle Square in Prime

North was the only new mall

to open in the city in 4Q14, and

was the first new shopping

centre to come on stream in

this submarket for six years.

Space constraint in

leading malls to drive

rent rises

On an annualised basis, overall

rents increased slightly although

the Prime North and the Suburbs

witnessed no quarterly change in

rents. Capital values remained

unchanged, and overall market

yields were stable at 11.2%. The

lack of vacant space in successful

malls, which have done well to

attract high visitor traffic, should

see rents rise across all

submarkets in 2015.

Expansion of

suburban retail

expected

Underrepresented suburban

precincts such as Panvel,

Kalyan, Nalasopara are likely to

attract more organised retail in

2015. Domestic retailers facing

stiff competition from foreign

retailers in established markets

are likely to find these locations

an attractive proposition.

n/a 0.9mil sqm

+20% 250INR

0.8%

Note: Mumbai Retail refers to Mumbai’s Overall retail market.

Source: JLL Research, 4Q14

FAST

FACTS

NEW RETAILERS

Burger King

Johnny Walker

Krispy Kreme

Payless ShoeSource

Current retail stock

(NLA)New supply forecast

(2015-2019)

Rental value

(psf pm)

Rental growth

(y-on-y)

Retail sales growth

(December, y-on-y)

Shanghai China’s most fashion-conscious city boasts the nation’s most dynamic retail mix.

Sophisticated shopping resides on both banks of the Huangpu River that bifurcates this east

coast metropolis. In downtown Puxi, international and local brands vie for prime storefronts

on Nanjing Road and Huaihai Road, and in smart malls including Plaza 66, Réel, Hong

Kong Plaza, L’Avenue and the art-themed K11. Luxury brand flagships are a feature of

Xintiandi district and the restored heritage mansions lining the riverfront Bund. Across the

river in Pudong, ifc Tower and Superbrand Mall in the Lujiazui skyscraper district and Kerry

Parkside all offer upscale shopping and a classy range of dining.

Fast fashion and

affordable luxury

brands accelerate

store expansions

Fast fashion retailers stepped up

their store expansions with Zara

unveiling its largest Shanghai

flagship, Uniqlo opening three

outlets and Chamtime Plaza

welcoming a new H&M store.

Affordable luxury brands also

demonstrated an appetite for

expansion, with Michael Kors

committing to two new stores at

River Mall and Grand Gateway.

Vacancy rates

Show slight

increase

The ongoing government

crackdown on official entertaining

influenced an increase to 8.7% in

the vacancy rate in the core area

as several malls closed their

banquet-style upper-floor

restaurants. The non-core market

vacancy rate also increased to

7.3%, as new malls entered the

market with relatively high

vacancy.

Four new malls

Open across

Shanghai

Two new malls opened in both

the core and non-core areas

during 4Q14. The south section

of The Place, formerly known as

The HQ, opened in Hongqiao,

and the nearby Arch Walk held

a soft opening. Beyond the core

area, Chamtime Plaza opened

in Pudong, and Yangpu district

welcomed the Bailian Binjiang

Shopping Centre.

Rents rise slowly

in core and non-

core markets

Rents in the core area increased

by 1.3% q-o-q, to RMB 51.2 per

sqm per day, while non-core rents

rose by 0.7% q-o-q, to RMB 17.4

per sqm per day. In non-core

areas, a disparity exists between

mature regional centres and newer

malls which have little pricing

power. Landlords of new

properties are offering generous

terms to boost occupancy.

Large supply

Pipeline anticipated

in non-coremarket

Retailers should continue to seek

expansion opportunities in 2015,

and a large supply pipeline is

anticipated in the non-core

market. Higher quality suburban

malls are emerging, but these

projects may experience longer

stabilisation periods and mature

shopping centres in key retail

submarkets will likely enjoy strong

bargaining power.

8.3% 4.6 mil sqm

+62% 51 RMB

1.4%

Note: Shanghai Retail refers to Shanghai’s Overall Prime retail market.

Source: JLL Research, 4Q14

FAST

FACTS

NEW RETAILERS

Beasts

Bulgogi Brothers

Pret a Manger

Pringle of Scotland

Current retail stock

(NLA)New supply forecast

(2015-2019)

Rental value

(psm per day)

Rental growth

(y-o-y)

Retail sales growth

(December, y-o-y)

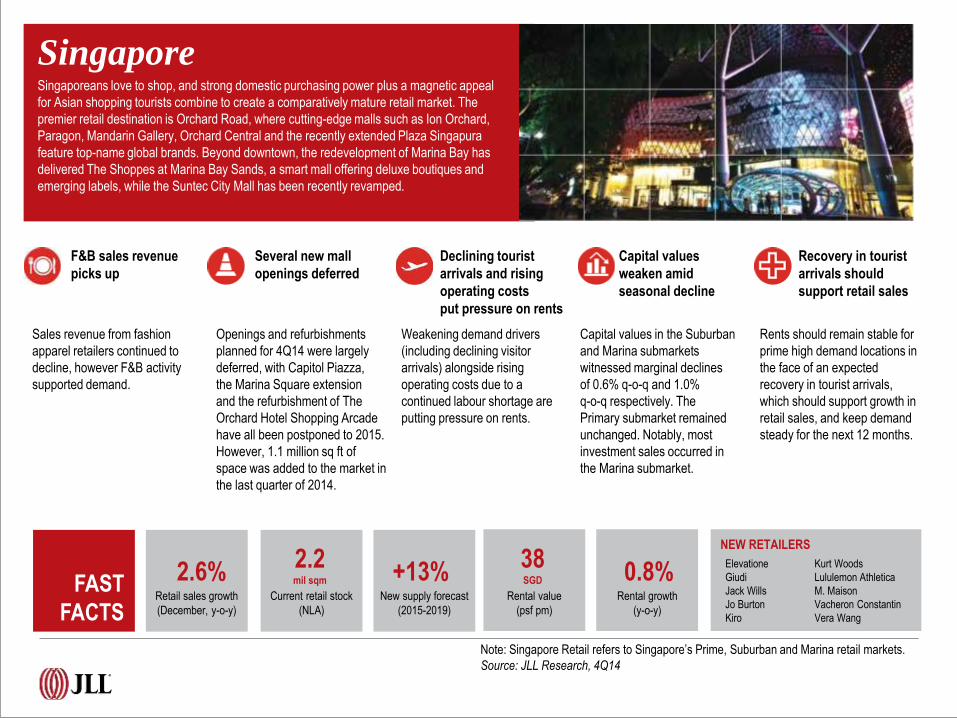

Singapore Singaporeans love to shop, and strong domestic purchasing power plus a magnetic appeal

for Asian shopping tourists combine to create a comparatively mature retail market. The

premier retail destination is Orchard Road, where cutting-edge malls such as Ion Orchard,

Paragon, Mandarin Gallery, Orchard Central and the recently extended Plaza Singapura

feature top-name global brands. Beyond downtown, the redevelopment of Marina Bay has

delivered The Shoppes at Marina Bay Sands, a smart mall offering deluxe boutiques and

emerging labels, while the Suntec City Mall has been recently revamped.

F&B sales revenue

picks up

Sales revenue from fashion

apparel retailers continued to

decline, however F&B activity

supported demand.

Several new mall

openings deferred

Openings and refurbishments

planned for 4Q14 were largely

deferred, with Capitol Piazza,

the Marina Square extension

and the refurbishment of The

Orchard Hotel Shopping Arcade

have all been postponed to 2015.

However, 1.1 million sq ft of

space was added to the market in

the last quarter of 2014.

Declining tourist

arrivals and rising

operating costs

put pressure on rents

Weakening demand drivers

(including declining visitor

arrivals) alongside rising

operating costs due to a

continued labour shortage are

putting pressure on rents.

Capital values

weaken amid

seasonal decline

Capital values in the Suburban

and Marina submarkets

witnessed marginal declines

of 0.6% q-o-q and 1.0%

q-o-q respectively. The

Primary submarket remained

unchanged. Notably, most

investment sales occurred in

the Marina submarket.

Recovery in tourist

arrivals should

support retail sales

Rents should remain stable for

prime high demand locations in

the face of an expected

recovery in tourist arrivals,

which should support growth in

retail sales, and keep demand

steady for the next 12 months.

2.6% 38SGD 0.8%

Note: Singapore Retail refers to Singapore’s Prime, Suburban and Marina retail markets.

Source: JLL Research, 4Q14

FAST

FACTS

NEW RETAILERS

Elevatione

Giudi

Jack Wills

Jo Burton

Kiro

Kurt Woods

Lululemon Athletica

M. Maison

Vacheron Constantin

Vera Wang

2.2mil sqm +13%

Current retail stock

(NLA)

New supply forecast

(2015-2019)

Rental value

(psf pm)

Rental growth

(y-o-y)

Retail sales growth

(December, y-o-y)

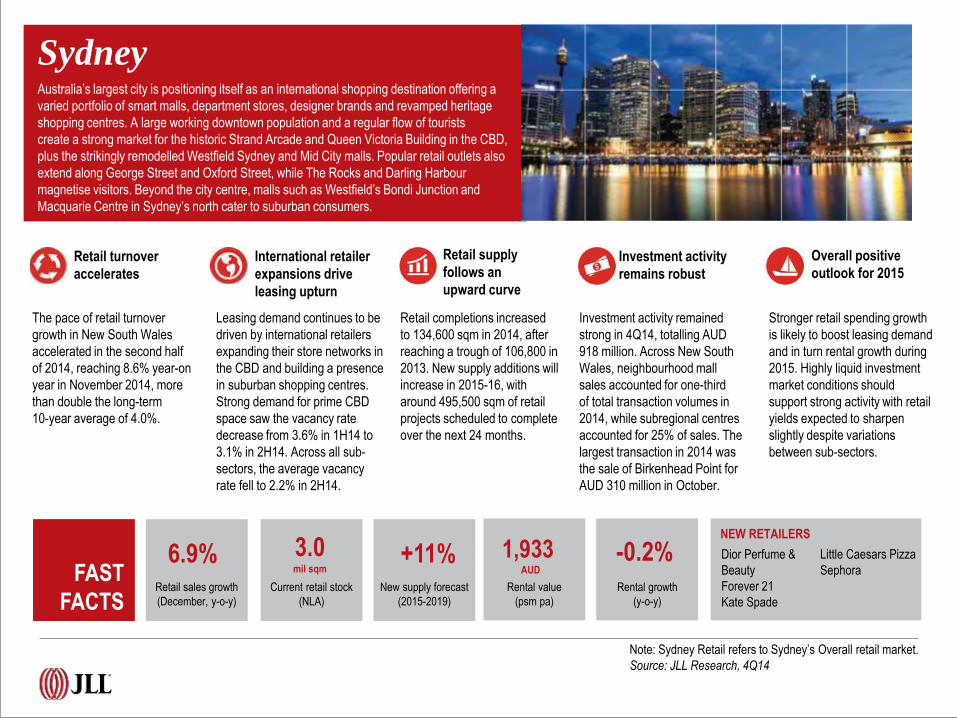

Sydney Australia’s largest city is positioning itself as an international shopping destination offering a

varied portfolio of smart malls, department stores, designer brands and revamped heritage

shopping centres. A large working downtown population and a regular flow of tourists

create a strong market for the historic Strand Arcade and Queen Victoria Building in the CBD,

plus the strikingly remodelled Westfield Sydney and Mid City malls. Popular retail outlets also

extend along George Street and Oxford Street, while The Rocks and Darling Harbour

magnetise visitors. Beyond the city centre, malls such as Westfield’s Bondi Junction and

Macquarie Centre in Sydney’s north cater to suburban consumers.

Retail turnover

accelerates

The pace of retail turnover

growth in New South Wales

accelerated in the second half

of 2014, reaching 8.6% year-on

year in November 2014, more

than double the long-term

10-year average of 4.0%.

International retailer

expansions drive

leasing upturn

Leasing demand continues to be

driven by international retailers

expanding their store networks in

the CBD and building a presence

in suburban shopping centres.

Strong demand for prime CBD

space saw the vacancy rate

decrease from 3.6% in 1H14 to

3.1% in 2H14. Across all sub-

sectors, the average vacancy

rate fell to 2.2% in 2H14.

Retail supply

follows an

upward curve

Retail completions increased

to 134,600 sqm in 2014, after

reaching a trough of 106,800 in

2013. New supply additions will

increase in 2015-16, with

around 495,500 sqm of retail

projects scheduled to complete

over the next 24 months.

Investment activity

remains robust

Investment activity remained

strong in 4Q14, totalling AUD

918 million. Across New South

Wales, neighbourhood mall

sales accounted for one-third

of total transaction volumes in

2014, while subregional centres

accounted for 25% of sales. The

largest transaction in 2014 was

the sale of Birkenhead Point for

AUD 310 million in October.

Overall positive

outlook for 2015

Stronger retail spending growth

is likely to boost leasing demand

and in turn rental growth during

2015. Highly liquid investment

market conditions should

support strong activity with retail

yields expected to sharpen

slightly despite variations

between sub-sectors.

Note: Sydney Retail refers to Sydney’s Overall retail market.

Source: JLL Research, 4Q14

FAST

FACTS

NEW RETAILERS

Dior Perfume &

Beauty

Forever 21

Kate Spade

Little Caesars Pizza

Sephora6.9% 3.0

mil sqm+11% 1,933

AUD

-0.2% Current retail stock

(NLA)

New supply forecast

(2015-2019)

Rental value

(psm pa)

Rental growth

(y-o-y)

Retail sales growth

(December, y-o-y)

Tokyo Shopping in the Japanese capital is a dazzlingly stylish experience. Tokyo’s vast size means

its retail landscape is subdivided into distinctive districts, each featuring a compelling blend of

marquee malls, department stores and classy boutiques created by top-name designers.

Ginza is a refined area where chic brand stores reside alongside art galleries and high-

society cafes. Roppongi’s HQ offices and deluxe hotels are more than matched by Roppongi

Hills, one of Tokyo’s sleekest shopping centres. Young consumers and a recent influx of

Chinese tourists make for the trendy malls, en vogue fashions and high-definition video imagery

of Omotesando, Shibuya and Shinjuku, while Tokyo Bay’s large mall appeals to families.

Private consumption

shows signs of

recovery

Consumer spending is

recovering with sales at large-

scale retail stores in Tokyo

increasing by 1.8% y-o-y in

December, while luxury goods

sales in department stores in

Tokyo rose 3.3% y-o-y. Nominal

private consumption is expected

to accelerate in 2015.

Tourism spending

boost for retailers

Tourist consumption continues

to be a bright spot for the retail

market, as visitor arrivals reach

record highs amid expanded

tax exemptions for visitors and

yen depreciation. An 80%

increase in the number of

high-spending Chinese visitors

to Japan in 2014 helped boost

tourist spending by 40% from

2013.

Rents maintain growth

amid limited supply

Rents in 4Q14 averaged JPY

69,195 per tsubo per month,

registering modest growth for

the ninth consecutive quarter.

With robust demand expected to

persist and most upcoming

supply in the prime market

already pre-committed, available

space is likely to remain scarce

thereby supporting the growth

trend of rents.

New Ginza malls

attract premium

brands

The 12-storey Kirarito Ginza

shopping centre opened in

4Q14 with high-profile tenants

including Vacheron Constantin’s

first directly operated store in

Japan plus Tocca Hartmann,

Samsonite Black Label and Din

Tai Fung. The three-storey

Ginza 6-chome Takiyama-cho

mall, featuring Versace and

Brunello Cucinelli, is due for

completion in autumn 2015.

Favourable investment

conditions push capital

value growth

Strong competition for

investment assets is expected

to continue amid historic low

interest rates that provide

favourable conditions for

fundraising. This is likely to

place further downward

pressure on yields and

accelerate the growth of

capital values.

1.8% n/a 69,195 JPY

4.3%

Note: Tokyo Retail refers to Tokyo’s Ginza and Omotesando Prime retail markets.

Source: JLL Research, 4Q14

FAST

FACTS

NEW RETAILERS

Cole Haan

Delvaux

Dior Fragrance &

Beauty

Givenchy

IWC

MCM

Vacheron Constantin

n/a

Current retail stock New supply forecast

(2015-2019)

Rental value

(per tsubo pm)

Rental growth

(y-o-y)

Retail sales growth

(December, y-o-y)

Month 00, 2014 13

Month 00, 2014 14

COPYRIGHT © JONES LANG LASALLE 2015

Thank you