revaluation of assets and reassessment of liabilities

TRANSCRIPT

REVALUATION OF ASSETS AND

REASSESSMENT OF LIABILITIES

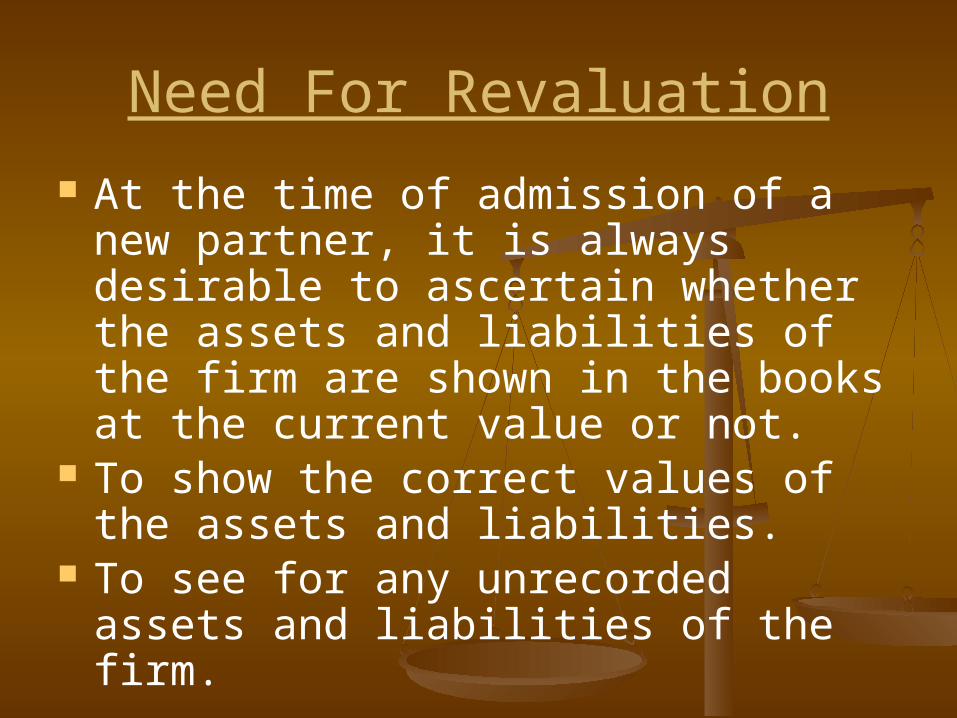

Need For Revaluation

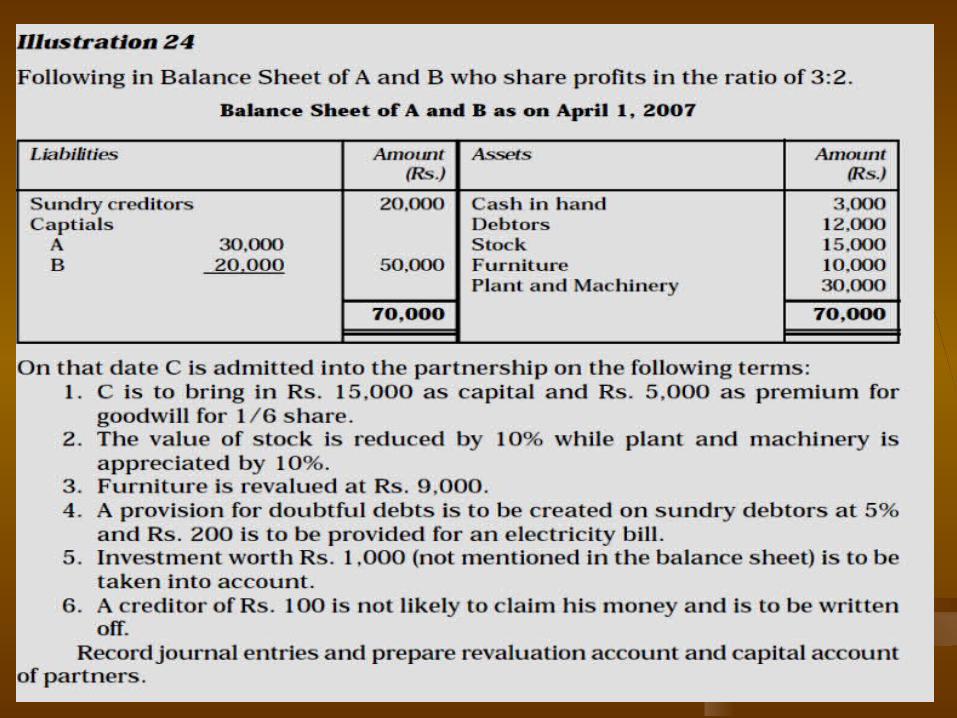

At the time of admission of a new partner, it is always desirable to ascertain whether the assets and liabilities of the firm are shown in the books at the current value or not.

To show the correct values of the assets and liabilities.

To see for any unrecorded assets and liabilities of the firm.

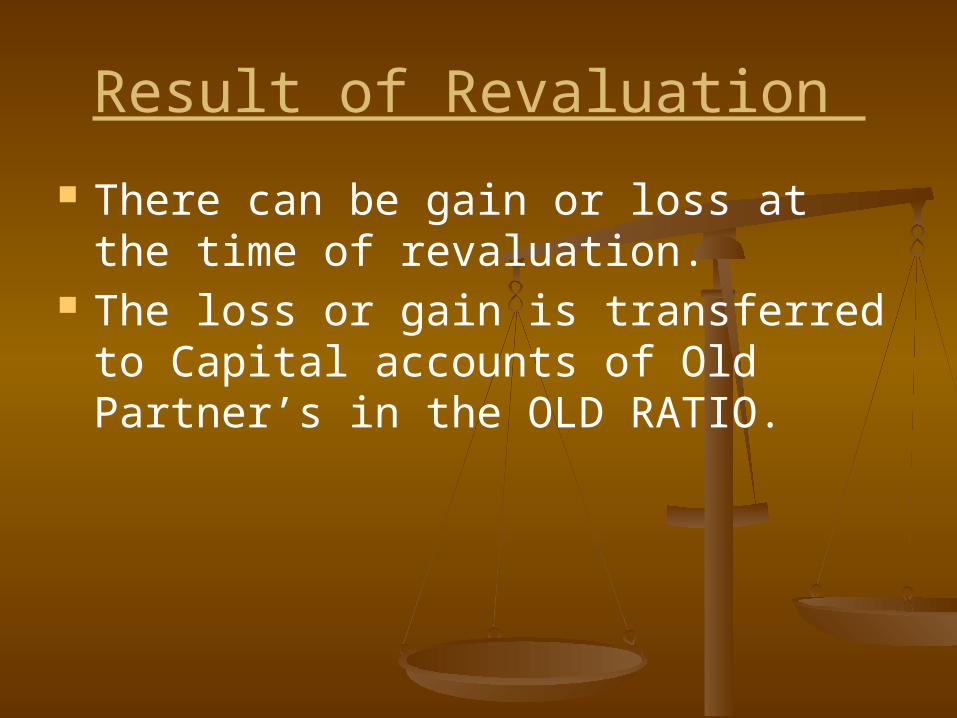

Result of Revaluation

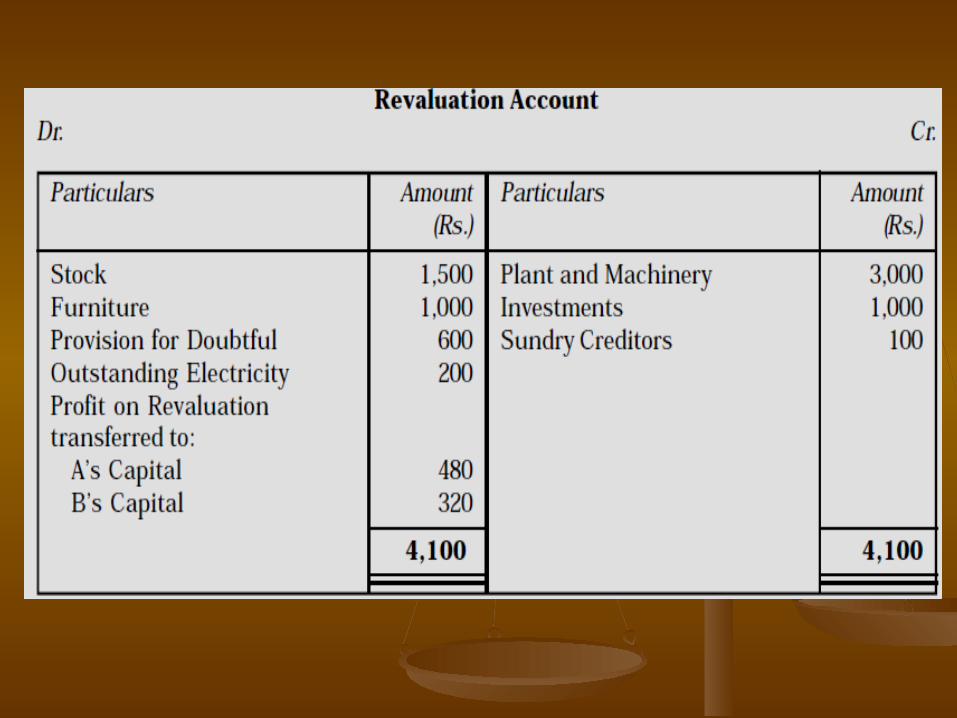

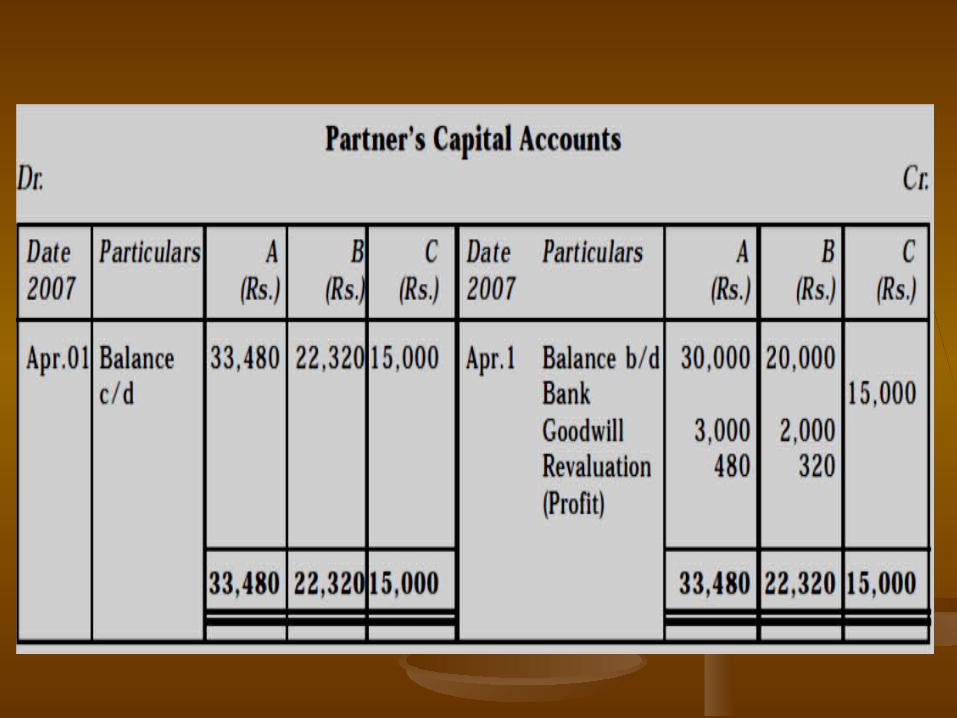

There can be gain or loss at the time of revaluation.

The loss or gain is transferred to Capital accounts of Old Partner’s in the OLD RATIO.

Accounting Treatment

1. For increase in the value of assets

Assets A/c (Individually) Dr. To Revaluation A/c (Increase in the value of

assets)2. For decrease in the value of

assets Revaluation A/c Dr. To Assets A/c’s

(Individually) (Decrease in the value of

assets)

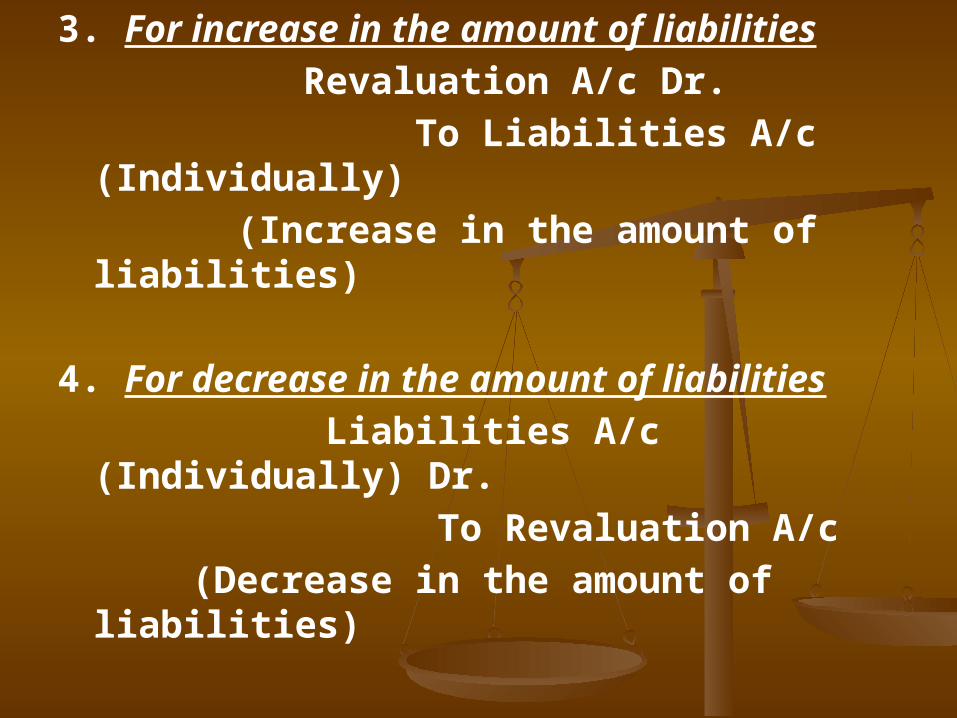

3. For increase in the amount of liabilities

Revaluation A/c Dr. To Liabilities A/c (Individually) (Increase in the amount of

liabilities)

4. For decrease in the amount of liabilities

Liabilities A/c (Individually) Dr. To Revaluation A/c (Decrease in the amount of

liabilities)

5. For an unrecorded asset Asset A/c Dr. To Revaluation A/c (Unrecorded asset brought into

book)

6. For an unrecorded liability Revaluation A/c Dr. To Liability A/c (Unrecorded liability brought

into books)

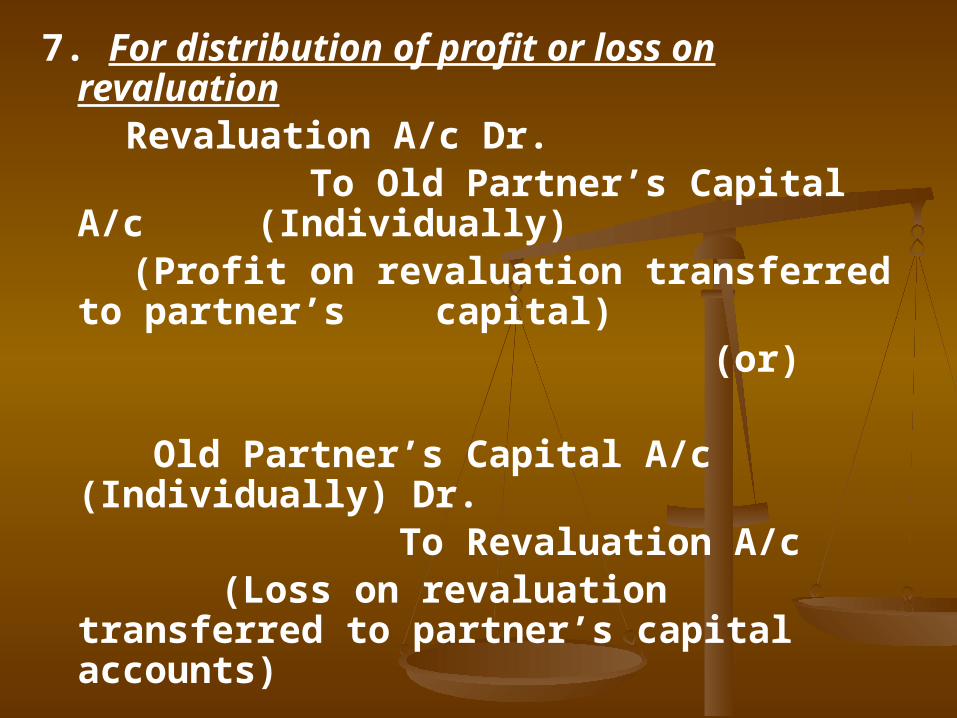

7. For distribution of profit or loss on revaluation

Revaluation A/c Dr. To Old Partner’s Capital A/c

(Individually) (Profit on revaluation transferred to

partner’s capital) (or)

Old Partner’s Capital A/c (Individually) Dr.

To Revaluation A/c (Loss on revaluation transferred to

partner’s capital accounts)